Embed Size (px)

Citation preview

Tax Considerations for

Farm Transitioning

Presented by Bill Wiebe, CPA, CA

Tax Partner(2017/01/25)

> Farm transitioning is the process of

transferring the farm business to either the

next generation or to unrelated parties.

> Today we will focus on:

• Three strategies available to minimize the

income tax on farm transitions,

• Some of the income tax tools available,

• Question and answers.

Farm Transitioning

> We will look at 3 strategies

• Using a corporation to own the farm land

(Landco).

• Selling the shares of a Landco

• Freezing the shares of a corporation

Farm Transitioning

> A number of our clients have kept farm land

outside of their corporation at the personal

level

• Received as an inheritance so no debt

• Bought a while ago and debt paid off

• Sometimes for estate planning purposes

Using a Landco

> Land values currently high

> The capital gain deduction (CGD) is at $1

million

> Operating company may have cash and be

offside the rollover rules

> Could sell the land to the operating company

(Opco)

> Consider a separate Landco

Using a Landco

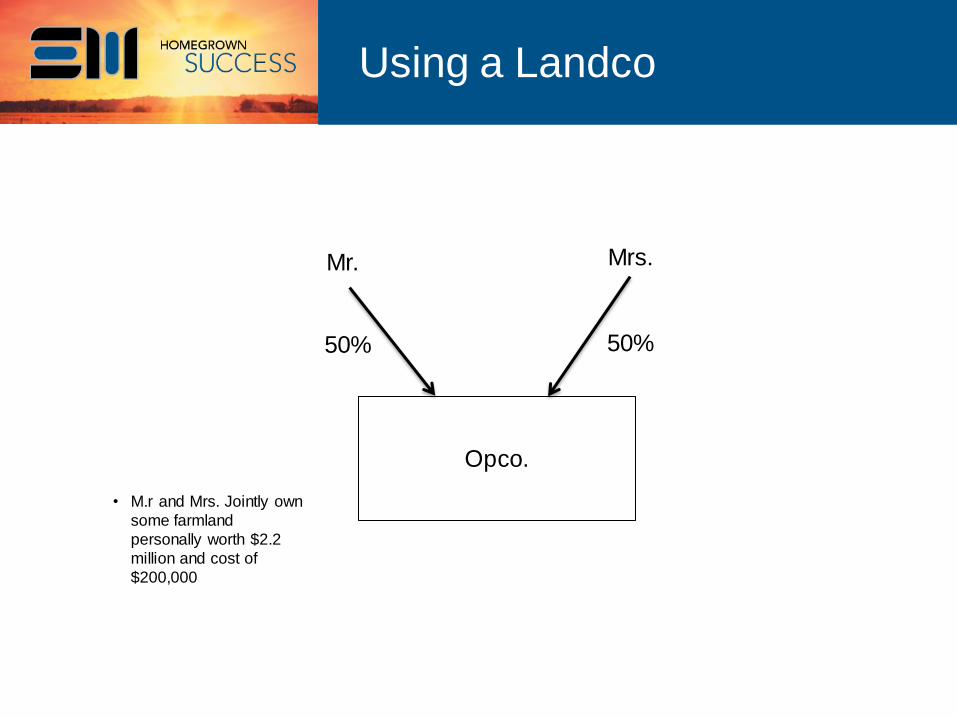

Using a Landco

Opco.

Mr. Mrs.

50% 50%

• M.r and Mrs. Jointly own

some farmland

personally worth $2.2

million and cost of

$200,000

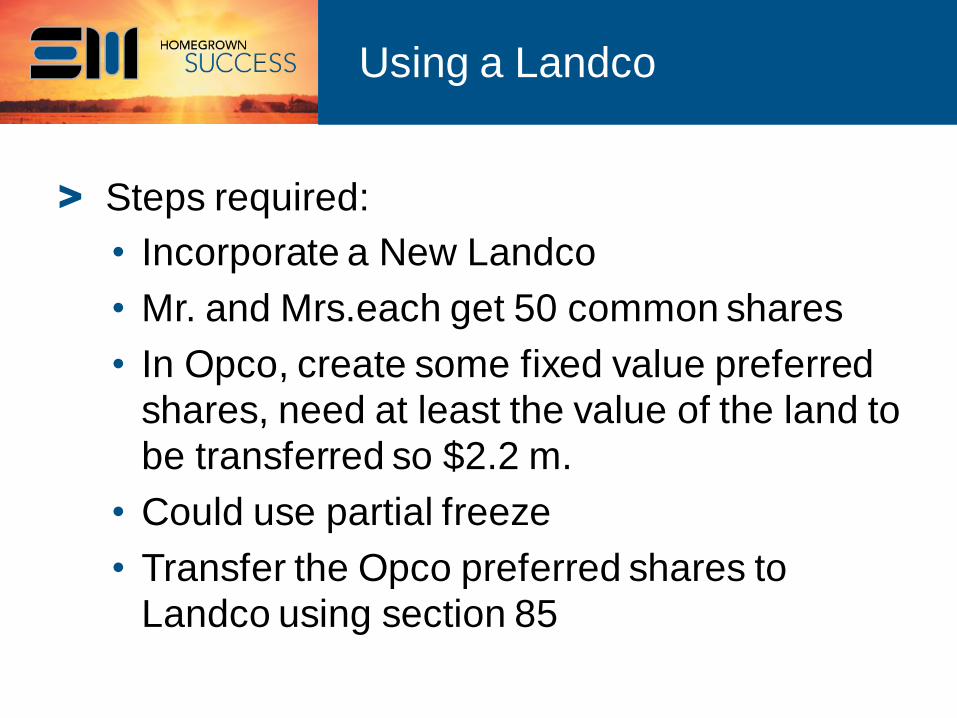

> Steps required:

• Incorporate a New Landco

• Mr. and Mrs.each get 50 common shares

• In Opco, create some fixed value preferred

shares, need at least the value of the land to

be transferred so $2.2 m.

• Could use partial freeze

• Transfer the Opco preferred shares to

Landco using section 85

Using a Landco

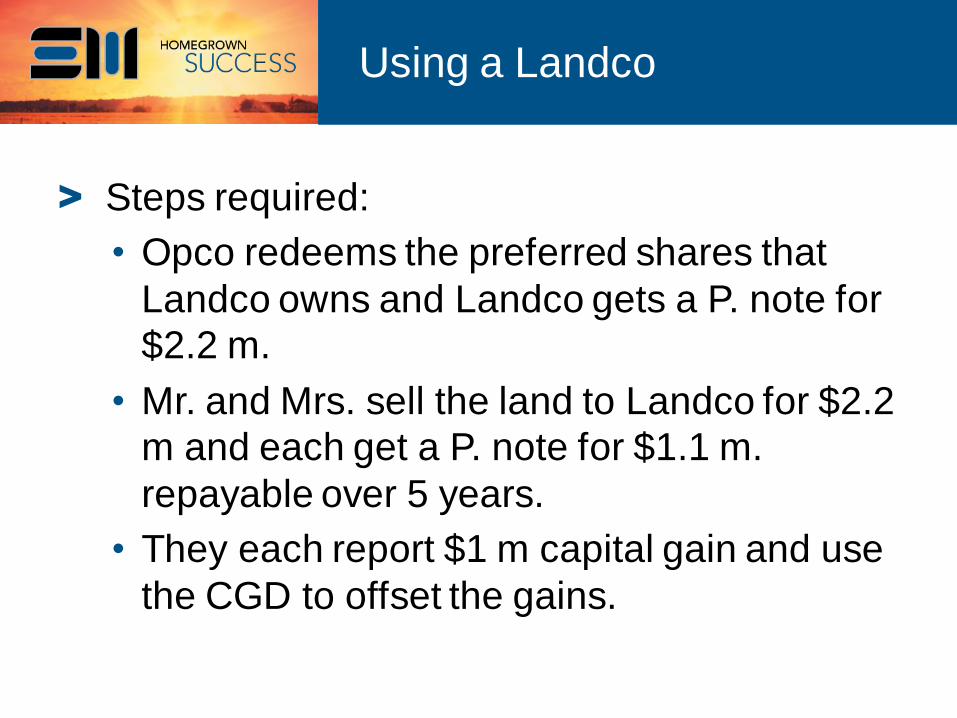

> Steps required:

• Opco redeems the preferred shares that

Landco owns and Landco gets a P. note for

$2.2 m.

• Mr. and Mrs. sell the land to Landco for $2.2

m and each get a P. note for $1.1 m.

repayable over 5 years.

• They each report $1 m capital gain and use

the CGD to offset the gains.

Using a Landco

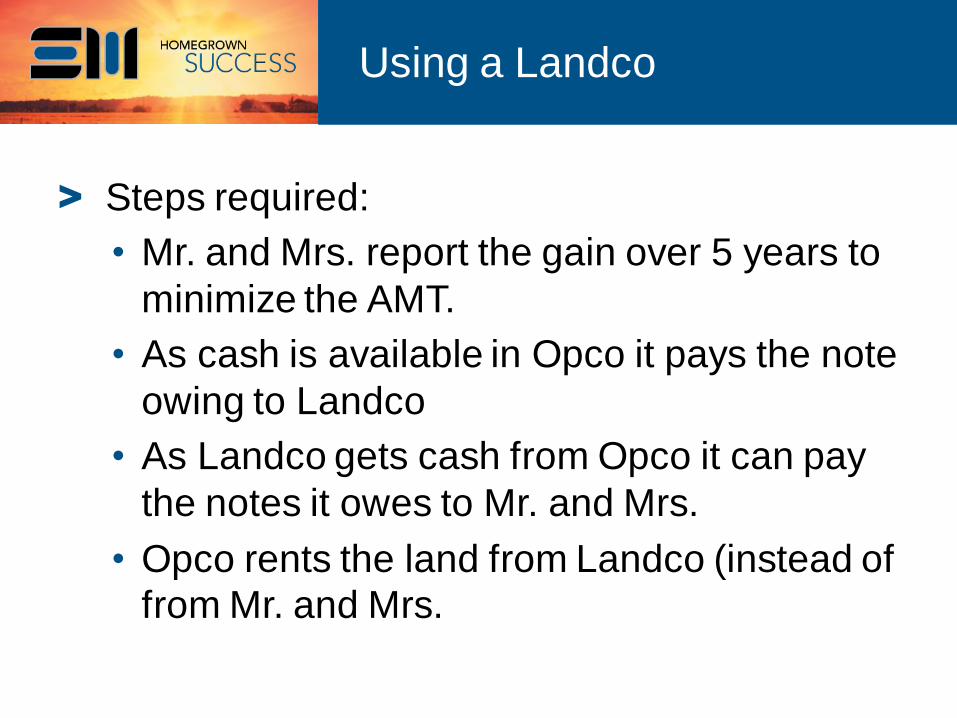

> Steps required:

• Mr. and Mrs. report the gain over 5 years to

minimize the AMT.

• As cash is available in Opco it pays the note

owing to Landco

• As Landco gets cash from Opco it can pay

the notes it owes to Mr. and Mrs.

• Opco rents the land from Landco (instead of

from Mr. and Mrs.

Using a Landco

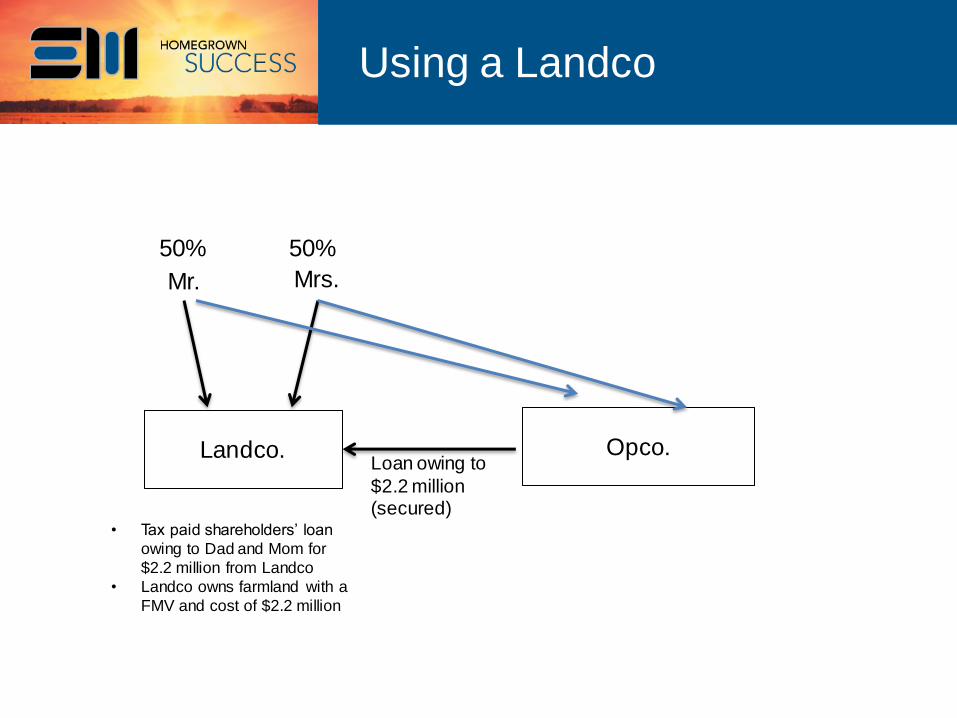

Using a Landco

Landco. Opco.

Mr. Mrs.

50% 50%

Loan owing to

$2.2 million (secured)

• Tax paid shareholders’ loan

owing to Dad and Mom for

$2.2 million from Landco

• Landco owns farmland with a

FMV and cost of $2.2 million

What have we achieved?

> Utilized the CGD for Mr. and Mrs. with the

result they can withdraw $2.2 million with no

personal income tax consequences

> Farm land owned by Landco has a cost equal

to the current fair market value (FMV) of $2.2

million

> Mr. and Mrs. can leave the shares of Landco

to farming and non-farming children. (could

put in a long-term lease with a farming sibling)

Using a Landco

What have we achieved?

> Purified Opco for the rollover rules

> Landco should also be qualified for rollovers

What else could be done?

> Opco shares could be transferred to a farming

child

> Landco could be transferred to the children, or

a trust could be used to own the Landco

shares; some protection against marital

claims.

Using a Landco

> Some Landco’s ( and Opco’s that convert to a

Landco) have farm land with FMV much

higher than cost.

> A corporation does not have a CGD.

> Consider selling the shares of Landco

> The gain on a sale of shares should be

eligible for the CGD.

> If CGD already utilized, CG tax rates still

better than dividend rates

Selling a Landco

> The purchaser of a Landco gets shares with a

high cost base but the land still has the low

cost base inside the old company

> Buyer could use an existing (or new)

corporation (Buyco) to buy the shares

> Wind up the Landco into the Buyco or

amalgamate with Buyco (no land title transfer

fees with an amalgamation)

Selling a Landco

> Buyco can elect to “bump up” the cost base on

the land up to the FMV when the shares were

bought

> Example: Landco has land with FMV of $1m

so Buyco purchased shares for $1 m, the land

cost can be bumped to the $1 m.

> Buyer could negotiate a reduction in price for

the costs of getting back to 1 corporation.

> Result – Buyer has land with full cost base.

Selling a Landco

> A share freeze is a common method to

transition the farming operation to the next

generation

> A sale of shares to the next generation and

utilizing the CGD does not work well in a

family situation – ITA 84.1 requires some one

to pay the tax

> With a share freeze the tax can be triggered

when the funds are taken.

Corporate Share Freeze

> Typically all of the value of the common

shares are frozen into fixed value preferred

shares

> Allows the next generation to obtain new

common shares at nominal value

> Future growth will accrue to the next

generation

> Mom and dad gradually redeem the preferred

shares in future years

Share Freeze

> Redemption of preferred shares create

taxable dividends for mom and dad

> Cash for the redemption comes from future

after tax income generated in the company

> Provides some protection for marital claims

with the next generation as long as mom and

dad continue to have significant value in their

preferred shares

Share Freeze

> Allows for future gifting of some or all of the

preferred shares to the next generation

> Mom and dad can keep control with a

separate class of voting shares if desired

> The preferred shares can go to non farming

children if there are not enough non farm

assets

Share Freeze

Choice of structure

Partnership

Corporation

Joint venture

Tax planning tools

Inter-generational rollovers – during life or on

death

• Farm land

• Farm equipment

• Farm corporation shares

• Farm partnership interests

Tax planning tools

Capital gain deduction (CGD)

• Farm land

• Farm corporation shares

• Farm partnership interests

Tax planning tools

Rollovers to partnerships and corporations

• Farm land

• Farm equipment

• Farm inventory; grain, livestock, etc.

• Quota’s and other intangibles

Tax planning tools

Corporate share freeze

Holding corporations (Holdco)

Land corporations (Landco)

Joint ownership of land with spouse

Family Trust

Life insurance

Rollover to spouse

Tax planning tools

> To request handouts:

• Call (306) 773-7285 and ask for Ashley

• Email [email protected]

• Will also be available on our website

http://www.starkmarsh.com/

Questions??