Embed Size (px)

Citation preview

2045

04标志、标准字组合

能源研究所Energy Research Institute

能源研究所Energy Research Institute

国家发展和改革委员会能源研究所Energy Research Institute National Deveiopment And Reform Commission

国家发展和改革委员会能源研究所Energy Research Institute National Deveiopment And Reform Commission

20452045

2035 2040

2050

SummaryOctober 2011

Technology RoadmapChina Wind Energy Development Roadmap 2050

ABOUT THE IEA

The IEA is an autonomous body, which was established in November 1974 within the framework of the Organisation for Economic Co-operation and Development (OECD) to implement an international energy programme.

The IEA carries out a comprehensive programme of energy co-operation among 28 of the 34 OECD countries. The basic aims of the IEA are:

zz To maintain and improve systems for coping with oil supply disruptions.

zz To promote rational energy policies in a global context through co-operative relations with non-member countries, industry and international organisations.

zz To operate a permanent information system on international oil markets.

zz To provide data on other aspects of international energy markets.

zz To improve the world’s energy supply and demand structure by developing alternative energy sources and increasing the efficiency of energy use.

zz To promote international collaboration on energy technology.

zz To assist in the integration of environmental and energy policies, including those relating to climate change.

ABOUT ENERGY RESEARCH INSTITUTE (ERI)

The Energy Research Institute (ERI) of the National Development and Reform Commission (NDRC) of P.R. China is a leading national think tank, focusing on energy policy research. ERI engages itself in broad range of research areas, including macro energy economic and energy planning, energy technology policy, energy demand and supply forecast, energy security, energy and environment, energy efficiency and conservation, and renewable energy. ERI provides strong support to the government of China regarding energy development strategies, planning, policy, laws and standards.

At the same time, ERI has established a broad and well functioning partnership and conducts joint research studies and consulting services with international agencies, organizations and academic entities, including the International Energy Agency (IEA), United Nation Development Programme (UNDP), World Bank (WB), Global Environmental Facility (GEF) as well with other institutes from USA, EU, Japan, Russia, and India.

Copyright © 2011

OECD/International Energy Agency

No reproduction or translation of this publication, or any portion thereof, may be made without prior written permission. Applications should be sent to: [email protected]

The China Wind Energy Development Roadmap was prepared by a team of China Experts under the lead of National Development and Reform Commission’s Energy Research Institute (NDRC ERI), with the close technical support of the International Energy Agency (IEA). This report provides a summary of the Chinese version of the roadmap. An English version of the full report will be released later this year.

Thanks are given to the British Embassy Beijing and the Sino-Danish Renewable Energy Development Programme for funding provided for this roadmap.

This paper reflects the views of the authors and does not necessarily reflect those of the IEA Secretariat, IEA Member countries or the funders. The roadmap does not constitute professional advice on any specific issue or situation. ERI and the IEA make no representation or warranty, express or implied, in respect of the roadmap’s contents (including its completeness or accuracy) and shall not be responsible for any use of, or reliance on, the roadmap. For further information, please contact: [email protected].

1Summary

Energy demand in China is growing to keep pace with rapid economic and social development. In 2020, it is expected to reach 4.5 to 5 billion tonnes of coal equivalent (tce) per annum, rising to 6.5 billion tce per annum in 2050. Electricity demand growth is likely to rise even more steeply, reaching 8 000 TWh in 2020, 10 000 TWh in 2030, and 13 000 TWh in 2050, up from 4 200 TWh in 2010.

The Chinese government has proposed a low-carbon development strategy, in which wind power will play a central role. Some 15 GW of wind power capacity will be installed each year up to 2020. Cumulative operational capacity in that year will be 200 GW, up from 31 GW at the end of 2010, meeting 5% of electricity production (400 TWh), up from 1.3% today.

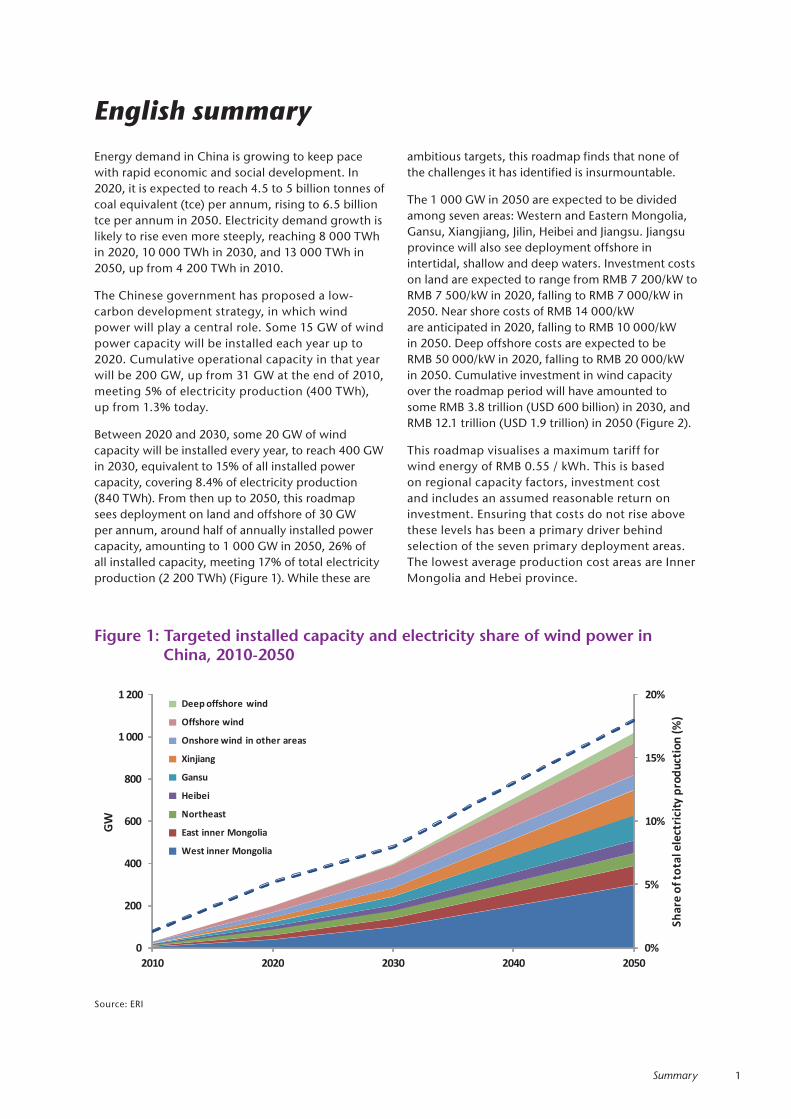

Between 2020 and 2030, some 20 GW of wind capacity will be installed every year, to reach 400 GW in 2030, equivalent to 15% of all installed power capacity, covering 8.4% of electricity production (840 TWh). From then up to 2050, this roadmap sees deployment on land and offshore of 30 GW per annum, around half of annually installed power capacity, amounting to 1 000 GW in 2050, 26% of all installed capacity, meeting 17% of total electricity production (2 200 TWh) (Figure 1). While these are

ambitious targets, this roadmap finds that none of the challenges it has identified is insurmountable.

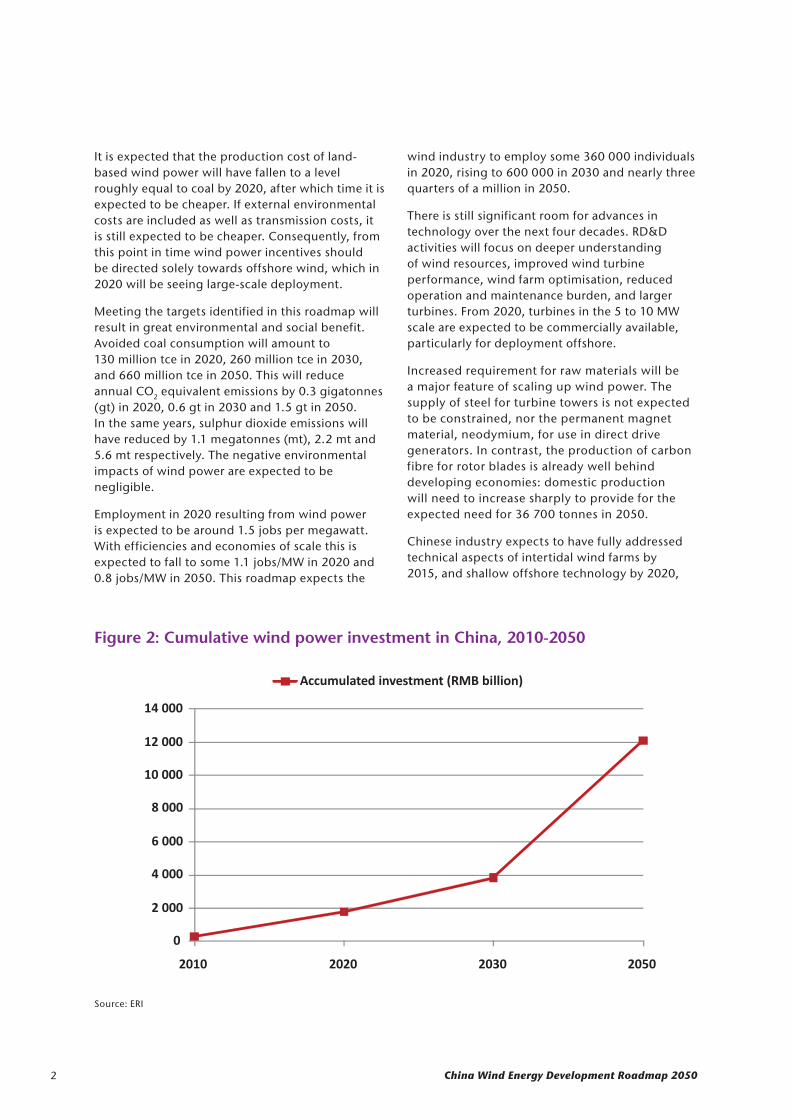

The 1 000 GW in 2050 are expected to be divided among seven areas: Western and Eastern Mongolia, Gansu, Xiangjiang, Jilin, Heibei and Jiangsu. Jiangsu province will also see deployment offshore in intertidal, shallow and deep waters. Investment costs on land are expected to range from RMB 7 200/kW to RMB 7 500/kW in 2020, falling to RMB 7 000/kW in 2050. Near shore costs of RMB 14 000/kW are anticipated in 2020, falling to RMB 10 000/kW in 2050. Deep offshore costs are expected to be RMB 50 000/kW in 2020, falling to RMB 20 000/kW in 2050. Cumulative investment in wind capacity over the roadmap period will have amounted to some RMB 3.8 trillion (USD 600 billion) in 2030, and RMB 12.1 trillion (USD 1.9 trillion) in 2050 (Figure 2).

This roadmap visualises a maximum tariff for wind energy of RMB 0.55 / kWh. This is based on regional capacity factors, investment cost and includes an assumed reasonable return on investment. Ensuring that costs do not rise above these levels has been a primary driver behind selection of the seven primary deployment areas. The lowest average production cost areas are Inner Mongolia and Hebei province.

English summary

1Summary

Energy demand in China is growing to keep pace with rapid economic and social development. In 2020, it is expected to reach 4.5 to 5 billion tonnes of coal equivalent (tce) per annum, rising to 6.5 billion tce per annum in 2050. Electricity demand growth is likely to rise even more steeply, reaching 8 000 TWh in 2020, 10 000 TWh in 2030, and 13 000 TWh in 2050, up from 4 200 TWh in 2010.

The Chinese government has proposed a low-carbon development strategy, in which wind power will play a central role. Some 15 GW of wind power capacity will be installed each year up to 2020. Cumulative operational capacity in that year will be 200 GW, up from 31 GW at the end of 2010, meeting 5% of electricity production (400 TWh), up from 1.3% today.

Between 2020 and 2030, some 20 GW of wind capacity will be installed every year, to reach 400 GW in 2030, equivalent to 15% of all installed power capacity, covering 8.4% of electricity production (840 TWh). From then up to 2050, this roadmap sees deployment on land and offshore of 30 GW per annum, around half of annually installed power capacity, amounting to 1 000 GW in 2050, 26% of all installed capacity, meeting 17% of total electricity production (2 200 TWh)

(Figure 1). While these are ambitious targets, this roadmap finds that none of the challenges it has identified is insurmountable.

The 1 000 GW in 2050 are expected to be divided among seven areas: Western and Eastern Mongolia, Gansu, Xiangjiang, Jilin, Heibei and Jiangsu. Jiangsu province will also see deployment offshore in intertidal, shallow and deep waters. Investment costs on land are expected to range from RMB 7 200/kW to RMB 7 500/kW in 2020, falling to RMB 7 000/kW in 2050. Near shore costs of RMB 14 000/kW are anticipated in 2020, falling to RMB 10 000/kW in 2050. Deep offshore costs are expected to be RMB 50 000/kW in 2020, falling to RMB 20 000/kW in 2050. Cumulative investment in wind capacity over the roadmap period will have amounted to some RMB 3.8 trillion (USD 600 billion) in 2030, and RMB 12.1 trillion (USD 1.9 trillion) in 2050 (Figure 2).

This roadmap visualises a maximum tariff for wind energy of RMB 0.55 / kWh. This is based on regional capacity factors, investment cost and includes an assumed reasonable return on investment. Ensuring that costs do not rise above these levels has been a primary driver behind selection of the seven primary deployment areas.

English summary

1

Chinese Wind Power Development Roadmap

English summary Energy demand in China is growing to keep pace with rapid economic and social development. In 2020, it is expected to reach 4.5 to 5 billion tonnes of coal equivalent (tce) per annum, rising to 6.5 billion tce per annum in 2050. Electricity demand growth is likely to rise even more steeply, reaching 8 000 TWh in 2020, 10 000 TWh in 2030, and 13 000 TWh in 2050, up from 4 200 TWh in 2010.

The Chinese government has proposed a low-carbon development strategy, in which wind power will play a central role. Some 15 GW of wind power capacity will be installed each year up to 2020. Cumulative operational capacity in that year will be 200 GW, up from 31 GW at the end of 2010, meeting 5% of electricity

production (400 TWh), up from 1.3% today.

Between 2020 and 2030, some 20 GW of wind capacity will be installed every year, to reach 400 GW in 2030, equivalent to 15% of all installed power capacity, covering 8.4% of electricity production (840 TWh). From then up to 2050, this roadmap sees deployment on land and offshore of 30 GW per annum, around half of annually installed power capacity, amounting to 1 000 GW in 2050, 26% of all installed capacity, meeting 17% of total electricity production (2 200 TWh) (Figure 1). While these are ambitious targets, this roadmap finds that none of the challenges it has identified is insurmountable.

Figure 1 Targeted installed capacity and electricity share of wind power in China, 2010 – 2050

0%

5%

10%

15%

20%

0

200

400

600

800

1 000

1 200

2010 2020 2030 2040 2050

Shar

e of

tota

l ele

ctri

city

pro

duct

ion

(%)

GW

Deep offshore wind

Offshore wind

Onshore wind in other areas

Xinjiang

Gansu

Heibei

Northeast

East inner Mongolia

West inner Mongolia

Source: ERI

Source: ERI

Figure 1: Targeted installed capacity and electricity share of wind power in China, 2010-2050

Source: ERI

Figure 1: Targeted installed capacity and electricity share of wind power in China, 2010-2050

2 China Wind Energy Development Roadmap 2050 Summary

It is expected that the production cost of land-based wind power will have fallen to a level roughly equal to coal by 2020, after which time it is expected to be cheaper. If external environmental costs are included as well as transmission costs, it is still expected to be cheaper. Consequently, from this point in time wind power incentives should be directed solely towards offshore wind, which in 2020 will be seeing large-scale deployment.

Meeting the targets identified in this roadmap will result in great environmental and social benefit. Avoided coal consumption will amount to 130 million tce in 2020, 260 million tce in 2030, and 660 million tce in 2050. This will reduce annual CO2 equivalent emissions by 0.3 gigatonnes (gt) in 2020, 0.6 gt in 2030 and 1.5 gt in 2050. In the same years, sulphur dioxide emissions will have reduced by 1.1 megatonnes (mt), 2.2 mt and 5.6 mt respectively. The negative environmental impacts of wind power are expected to be negligible.

Employment in 2020 resulting from wind power is expected to be around 1.5 jobs per megawatt. With efficiencies and economies of scale this is expected to fall to some 1.1 jobs/MW in 2020 and 0.8 jobs/MW in 2050. This roadmap expects the

wind industry to employ some 360 000 individuals in 2020, rising to 600 000 in 2030 and nearly three quarters of a million in 2050.

There is still significant room for advances in technology over the next four decades. RD&D activities will focus on deeper understanding of wind resources, improved wind turbine performance, wind farm optimisation, reduced operation and maintenance burden, and larger turbines. From 2020, turbines in the 5 to 10 MW scale are expected to be commercially available, particularly for deployment offshore.

Increased requirement for raw materials will be a major feature of scaling up wind power. The supply of steel for turbine towers is not expected to be constrained, nor the permanent magnet material, neodymium, for use in direct drive generators. In contrast, the production of carbon fibre for rotor blades is already well behind developing economies: domestic production will need to increase sharply to provide for the expected need for 36 700 tonnes in 2050.

Chinese industry expects to have fully addressed technical aspects of intertidal wind farms by 2015, and shallow offshore technology by 2020,

2

The 1 000 GW in 2050 are expected to be divided among seven areas: Western and Eastern Mongolia, Gansu, Xiangjiang, Jilin, Heibei and Jiangsu. Jiangsu province will also see deployment offshore in intertidal, shallow and deep waters. Investment costs on land are expected to range from RMB 7 200/kW to RMB 7 500/kW in 2020, falling to RMB 7 000/kW in 2050. Near shore costs of RMB 14 000/kW are anticipated in 2020, falling to RMB 10 000/kW in 2050. Deep offshore costs are expected to be RMB 50 000/kW in 2020, falling to RMB 20 000/kW in 2050. Cumulative investment in wind capacity

over the roadmap period will have amounted to some RMB 3.8 trillion (USD 600 billion) in 2030, and RMB 12.1 trillion (USD 1.9 trillion) in 2050 (Figure 2).

This roadmap visualises a maximum tariff for wind energy of RMB 0.55 / kWh. This is based on regional capacity factors, investment cost and includes an assumed reasonable return on investment. Ensuring that costs do not rise above these levels has been a primary driver behind selection of the seven primary deployment areas. The lowest average production cost areas are Inner Mongolia and Hebei province.

Figure 2 Cumulative wind power investment in China, 2010 ‐ 2050

Source: ERI

It is expected that the production cost of land‐based wind power will have fallen to a level roughly equal to coal by 2020, after which time it is expected to be cheaper. If external environmental costs are included as well as transmission costs, it is still expected to be cheaper. Consequently, from this point in time wind power

incentives should be directed solely towards offshore wind, which in 2020 will be seeing large‐scale deployment.

Meeting the targets identified in this roadmap will result in great environmental and social benefit. Avoided coal consumption will amount to 130 million

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

2010 2020 2030 2050

Accumulated investment (RMB billion)

Source: ERI

Figure 2: Cumulative wind power investment in China, 2010-2050

3Summary

after which deep offshore demonstration will commence (R&D in this area will commence before 2015). China’s offshore programme will require the transformation of existing ports and the development of new facilities, possibly located on islands to reduce weather related deployment uncertainties, as well as the development of specialised installation and transport vessels after 2016.

Wind power deployment can not be seen in isolation. Such large capacities of wind power will inevitably have influence on the wider power system. Up to 2020, R&D will focus on advanced, centralised forecasting techniques ranging from 72 hours ahead up to three ahead of the time of delivery. “Grid friendly” wind farms are anticipated by 2020, featuring active and reactive power control, fault ride through and frequency regulation capabilities. By 2030, with the deployment of system storage, grid reinforcement and advanced scheduling and dispatching techniques, inter alia, wind power across the country is expected to provide similar system support to conventional power plants.

Up to 2020 and beyond, the majority of wind power deployed will be in the north of China, far from load centres. Therefore efforts are needed to maximise the consumption of wind power locally, and minimise curtailment. Deployment of wind power plants must be co-ordinated with that of other plants types, particularly those which are technically more flexible, and transmission roll-out plans across the seven target regions.

Two pathways for development of the transmission system have been identified, one which retains the existing six regional power grids, strengthening integration among them, and one which sees the development of a new ultra-high voltage AC grid covering the main load centres in the centre and east, with DC connections to the north east, northwest and south.

Power sector reform will have enormous influence on the deployment of wind power. China is already making transition to more advanced power plant dispatch practices wherein cost and CO2 emissions of different plant types are taken into account. Wind power has first priority in dispatch, but in order for this to be the case in practice a more transparent power market is needed, and planned for 2020. Efforts are needed to increase the transparency of power prices, and to integrate the

external environmental costs of polluting types. Power prices should reflect the value of flexibility of power plants. In the mid-term, environmental and carbon tax approaches should be evaluated for use in China.

Unbundling vertically integrated players is an important task. Facilitating trade among provinces will help accommodate large fluctuations in wind output. In concert with advanced forecasting techniques, centralised operation of wind power plants will help smooth their aggregated output.

More of existing flexible resources must be made available through new ancillary service markets and smart grid technology for balancing fluctuations in output. Consumer response will be activated to some extent by new peak-and-valley pricing. And greater flexibility should be developed in the conventional generator fleet, including new hydropower deployment in the west, gas fired power plants for peaking and improved ramping capability of conventional thermal plants.

Key actions to 2020 z Reform power market to achieve market-

based power pricing, reflecting environmental externalities, the value of flexibility and integration costs.

z Strengthen priority grid access and dispatch of wind power; maximise the ability of northern provinces to accommodate locally produced wind power; facilitate inter-provincial transmission using smartest available technology.

z Accelerate deployment of flexible resources; deploy best available output forecasting techniques; activate consumer response to electricity scarcity.

z Establish a renewable R&D fund and common experimental platforms. Develop and deploy cost competitive 5 MW technology by 2015, and near offshore technology by 2020.

z Strengthen supply chains, especially offshore transport and installation infrastructure, and carbon fibre availability.

z Develop specialist wind power training courses and university curricula by 2015.

2020

2010

2015

International Energy Agency – IEA9 rue de la Fédération, 75015 Paris, FranceTel: +33 (0)1 40 57 65 00/01Email: [email protected], Web: www.iea.org

2025

2030

Tech

nol

ogy

Roa

dm

ap C

hina

Win

d En

ergy

Dev

elop

men

t Roa

dmap

205

0

Energy Research Institute – ERINational Development and Reform Commission (NDRC) of P. R. China Block B, Guohong Bldg., Muxidibeili-Jia 11, Xicheng District, Beijing, 100038, P. R. ChinaTel: +86 10 63908576/63Email: [email protected], Web: www.eri.org.cn