Embed Size (px)

Citation preview

The 4th International Conference

on Public Management in the 21st Century:

Opportunities and Challenges

第四屆 21 世紀的公共管理:機遇與挑戰 國際學術研討會

The United Nations Development Programme and Standard and Poor's Credit Rating Partnership: Outcomes and Challenges

Alexey Dorofeev

(Park University)

22/10 – 23/10/2010

Macau, China 中國 澳門

The United Nations Development Programme and Standard and Poor’s Credit

Rating Partnership: Outcomes and Challenges

Key-words: global governance, sovereign rating, capital market, Sub-Saharan Africa

Mr. Alexey Dorofeev

Park University/Development Gateway Foundation

9226 NW 60th St, Parkville, MO 64152 United States

Phone: +1 (917) 515 3754

Fax: + 1 (816) 505-5478

2

Abstract

The purpose of this paper is to provide analysis and evaluate the outcomes of the credit rating

partnership between the United Nations Development Programme (UNDP) and Standard and

Poor’s (S&P). The study attempts to assess the impact of economic and governance indicators on

selected S&P ratings. It also discusses the success of the program and estimates the extent to

which ratings contain country’s reliance on Official Development Assistance (ODA). Results

vary country by country. For most countries, external debt stocks and governance indicators

prove to be in strong correlation with the assigned S&P ratings. Conversely, the ratings have

only negligible effect on the share of ODA for all of the sampled countries. The paper concludes

with practical implications to policy makers.

3

Introduction

Most of the countries in Sub-Saharan Africa, with the exception of South Africa, suffer from

inability of central government and local private businesses to tap into global capital markets.

The difference in borrowing cost of credit for sovereigns in this region vis-à-vis most of the

emerging economies, is truly striking. It is estimated that the average SSA country would have

paid “about 3 percent more than the average emerging market borrower or 9.60 percent as of

end-2009” (Sy and Amadou 2010). A study of borrowing patterns by developing countries finds

that countries without stable access to global capital markets “suffer from greater political

instability and worse perceptions, and are more vulnerable to external shocks”(Gaston et al 2004,

p. 3). On the other hand, clearly, countries with serious political risks are more likely to have

lower ratings. In addition, Kaminsky and Schmukler provide evidence of contagion effect

spreading to neighboring countries in instance of investment rating downgrade (2009, p.19).

Financial markets in the poorest countries of the world, mostly in Sub-Saharan Africa, are either

absent or are in a nascent form. There is no mechanism for the funding, if it does become

available, to invest it within the local economy. Foreign direct investment is largely either short

term or goes to resource rich economies. Strikingly, local companies are virtually deprived of the

prospect to raise capital both locally and abroad. Creation of capital markets in African

economies would provide options for investing money in the local economy, and, hence, would

prevent the scarce financial resources from leaving the country. Another crucial benefit of local

capital markets is the increased role of local decision makers and the increased leverage of local

stakeholders (Applegarth 2004, p.6). Some of the other likely consequences of stronger financial

markets, according to Applegarth, include higher level of competition between local banks,

opportunities for locals to invest money received through remittances, and lastly, but very

4

importantly creates tools for African countries to conduct monetary policy. Since the cost of

sovereign borrowing is linked to economic conditions in the country, raising funds through

capital markets contrasts relying on ODA. Good economic policies implemented by central

government mean lower cost of borrowing in the capital market. Conversely, such economic

policies mean lesser availability of ODA funding, and hence gaps in budget that are difficult to

predict.

The UNDP has been in negotiations with S&P since early 1990s regarding an initiative that

would assist the sovereigns with acquiring ratings. Usually, the sovereign country would a pay a

fee to the rating agency for the rating assessment to take place. In the example of Sub-Saharan

Africa, many sovereigns lack the financial capacity to pursue the application. In addition, since

the country does not have a say with regards to the final rating, there is little incentive for the

government to approach the rating agency. Credit ratings are essential to the private sector’s role

in Africa’s economic development and the growth of capital markets at sovereign and regional

level. Ratha et al. vouch in favor of assisting poor countries obtain credit ratings not only for

sovereign borrowing, but for sub-sovereign entities' access to international capital markets (2007,

p.1).

Under the arrangement, the UNDP “plays a catalytic role in explaining the potential benefits of

ratings to interested governments” and in “providing Standard & Poor's with its own insights on

the key economic, financial, and political factors in the region” (Standard and Poors 2004). The

role of UNDP in determining the ratings remains unclear due to the lack of publicly available

5

relevant documentation. Most certainly, it has a very minimal impact on the actual ratings, if

any.

Up to this date, the following Sub-Saharan countries have acquired their sovereign ratings

through the UNDP initiative: Benin, Burkina Faso, Cameroon, Ghana, Kenya,

Madagascar (rating withdrawn) Mali (rating withdrawn), and Mozambique. This study looks at

all these countries, except for Cape Verde, which acquired its rating only in 2009, and thus

would not provide a sufficient amount of observations. Sub-Saharan Africa is of great

importance since many of the countries are clustered and are similar with respect to local capital

market deficiencies. Sovereigns from other regions, which have acquired their ratings through

the UNDP-S&P initiative are left aside, since political and economic environments in these

countries vary drastically from those in Sub-Saharan Africa. Nigeria, Senegal and South Africa,

also from Sub-Saharan Africa, are excluded from the study since their ratings were assigned

without the UNDP involvement.

All the assigned sovereign ratings are quite low and range between CCC assigned to Cameroon

on November 1, 2005 to B+ assigned to Ghana on March 19, 2009. With ratings being so low,

the question arises whether a junk status rating is better than no rating at all. Most of the

academic literature on the subject does confirm the following premise. Ratha et al. find unrated

countries to be perceived as riskier than they are, and, definitely, riskier than default risk

sovereigns (2007, p. 3). The same study also finds ratings to be sticky and to be unlikely to

change over time, unless precipitated by major events or drastic economic improvements (Ratha

et al. 2007, p.7). Hence there is very little deviation from original ratings for the majority of

6

countries. Standard and Poor’s does not disclose the methodology used to assign the ratings; in

public documents it only vaguely discusses some of the main factors considered.

External debt, domestic public debt, political risk and broad money as a share of GDP are found

to be the most important determinants of sovereign’s investment grade status for emerging

economies (Jaramillo 2004, p.3). Analysis was conducted based on the information provided by

all major rating agencies, and found inflation to be an additional statistically significant variable

for Standard and Poor’s. Cantor and Packer find per capita income, GDP growth, inflation, fiscal

balance, external balance, external debt, economic development are listed to have a strong

impact on sovereign ratings (1996, p.39). In another study, per capita income, government

income and changes in the real exchange rate are found to be the most important variables

(Mellios and Paget-Blanc 2006, p. 19). This study attempts to determine the most important

determinants of ratings for UNDP-S&P ratings in Sub-Saharan Africa.

The relevant data, on Sub-Saharan Africa, unfortunately, is very scarce. This study makes an

attempt to identify the most important determinants of sovereign ratings in the UNDP-S&P

Partnerships based on the information available, with a particular emphasis on governance

indicators. Gaston et al. do not find a significant relationship between the share of FDI as a

percentage of GDP and the likelihood of access to the capital market for the studied countries.

Since GDP per capita, appears to be one of the strongest determinants of a rating, many African

countries won’t be able to achieve a credit ranking beyond junk bond years to come.

7

Methodology

There are two models developed in this study: one to estimate the variables with the most

significant impact on sovereign ratings in Sub-Saharan Africa and another one to determine

whether ODA share in relation to GNI decreases as the country receives a sovereign rating. The

data was obtained from the World Bank Data and the World Bank Governance indicators and

covered the following years: 1996, 1998, 2000 and 2002-2008. 1997, 1999 and 2001 were

excluded since the governance indicators did not provide information for these years. Out of the

6 available governance indicators, political stability and government effectiveness were selected

to be included in this study, since both of these variables, in theory, are correlated with both

sovereign ratings and country’s reliance on ODA. Due to the scarcity of information on Sub-

Saharan Africa in comparison to most other regions of the world, the number of variables to pick

from for the study was extremely limited. The ratings are quantified as follows: No rating or

rating withdrawn = 0, CCC = 1, B - = 2, B = 3, B= = 4, BB - = -5. For years, when country’s

rating was changed, a mean of all the rating values for that specific year is calculated and

assigned as numeric value.

In the first model, rating is regressed over the share of external debt stocks (% to GNI), the

government effectiveness indicator, annual GDP Growth, inflation (GDP deflator) and the

political stability indicator. Regression is run by Ordinary Least Squares technique. Log function

is applied to external debt, GDP growth and inflation. With the exception of Gabon and Kenya,

models are quite robust.

8

The second model attempts to assess the impact of ratings on the country’s share of ODA in

GNI. The theory behind is that as the access of sovereigns to international capital markets

increases, they are less likely to rely on ODA. Other variables, such as financing via international

capital markets (gross inflows) would have been a better variable, but could not be included due

to virtual absence of capital market statistics for Sub-Saharan Africa. ODA (as a log function) is

regressed over GDP growth (as a log function), government effectiveness, inflation, political

stability and ratings. Inflation and government effectiveness are taken out for a number of

countries to have a better fit of the model. The model is not nearly as robust the first one, but to

some extent helps to understand the magnitude to which sovereign ratings affect country’s

dependency on foreign aid flows.

Findings

Below is the summary of statistically significant variables for each of the countries for the first

model (Annex II):

Benin – External Debt, Government Effectiveness, GDP Growth, Inflation, Political Stability

Burkina Faso – External Debt, Government Effectiveness

Cameroon – External Debt, Government Effectiveness, Inflation

Gabon – External Debt

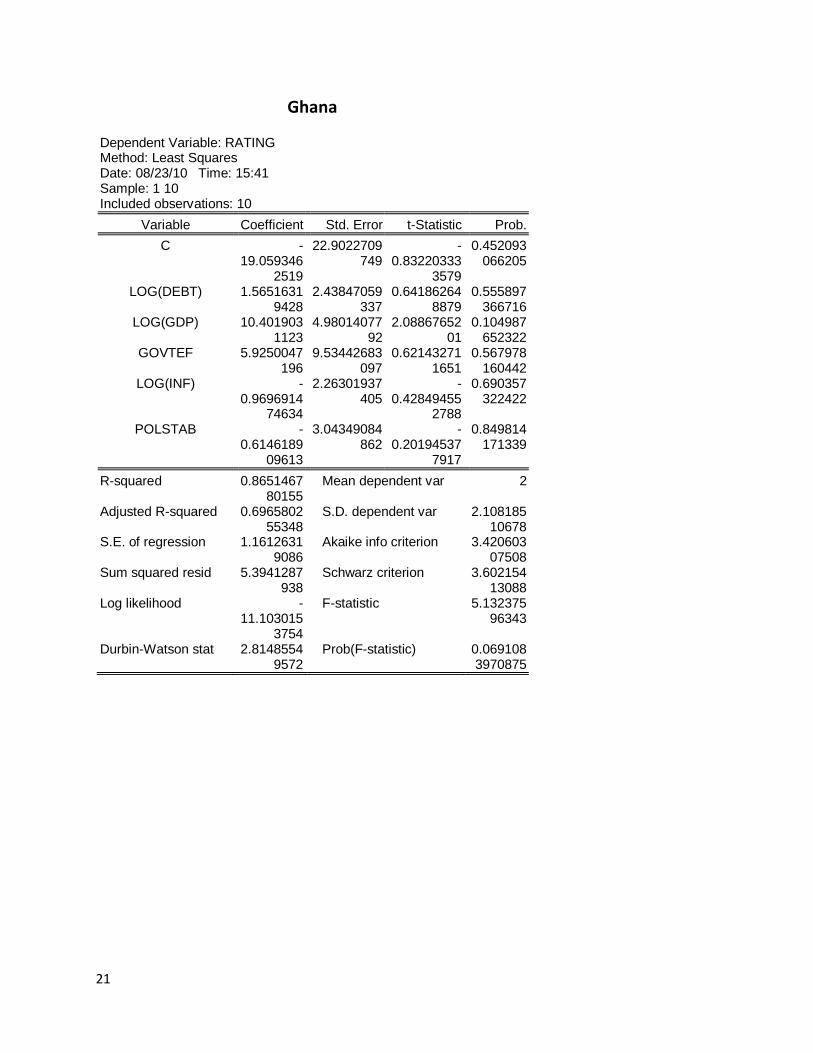

Ghana – GDP Growth

Kenya – External Debt, Inflation

Madagascar – External Debt, GDP Growth, Inflation

Mali – Inflation

Mozambique – External Debt, Government Effectiveness, Inflation, Political Stability

9

In the example of Benin, the sign for all of the independent variables, except for the GDP

growth, is consistent with the economic theory. In Cameroon, government effectiveness index is

negatively correlated with the sovereign rating. A similar finding for Mozambique could be

attributed to the past challenges in governances, which nevertheless did not seem to have a

strong negative impact on economic growth. This could be explained by significant number of

instances when its rating was revised. As it appears to be, improvements in the quality of

governance are not always translated into better economic indicators. In the examples of larger

economies, such as Ghana and Kenya, macroeconomic indicators, such as GDP and Inflation,

clearly become prevalent over the governance indicators. External debt stocks variable,

according to the model, has the greatest impact on sovereign ratings. These two variables are

inversely related. Out of the governance indicators, government effectiveness seems to be more

relevant than political stability, though its impact on ratings is not always consistent with the

economic theory.

The list of statistically significant variables for the second model (estimating the most significant

determinants of country’s dependence on ODA) is as follows (Annex III):

Benin – GDP Growth, Political Stability, Rating

Burkina Faso – Government Effectiveness, Political Stability, Rating

Cameroon – None

Gabon – Political Stability

Ghana – GDP Growth, Government Effectiveness, Political Stability

Kenya – GDP Growth, Government Effectiveness

Madagascar – Government Effectiveness, Political Stability

10

Mali – External Debt, GDP Growth, Government Effectiveness, Political Stability, Inflation

Mozambique – None

Mali is the only country with a good regression model where most of the independent variables

have a relationship with ODA share and consistent with economic theory. While both

government effectiveness and political stability are statistically significant, political stability in

Mali has a greater impact on country’s dependence on ODA. Rating is found not to be

statistically significant. Revealingly, political stability turns out to have the strongest positive

impact on ODA for Burkina Faso. This relationship contradicts economic theory. For Ghana,

government effectiveness is the most statistically significant variable and does have a strong

negative impact on ODA. The rating is statistically significant only for Burkina Faso and Benin,

but has only a negligible effect on ODA. Overall, the model proves that up to 2008 sovereign

ratings have had a minimal impact on country’s reliance on ODA. The second model, however,

is not as robust as the first one.

Policy Recommendations

The study of ratings in this paper does not mean that the sovereigns would get an actual access to

capital markets. According to statement by Standard and Poor’s, “many of the governments rated

under the new initiative will not use their ratings to international bond markets (Standard &

Poor’s 2006)”. Yet, acquisition of ratings is a good starting point and a serious incentive for

central governments to have well-designed economic policies and to consider tapping into the

capital markets in the future. Further, local private companies, in the long run, are better off due

to their increased prospects of raising capital abroad.

11

Quantitatively, based on this study, there is little evidence that the ratings are economically

beneficial to the sovereigns at present. Yet, in the long run, their potential positive impact should

not be neglected. On the other hand, credit ratings do serve as an important mechanism to

provide strong incentives for central governments to support better economic policies at home.

The publicly available evaluations by Standard & Poor’s offer a somewhat clear picture to

central governments on what needs to be improved for the rating to be upgraded. For example,

Standard and Poor’s states that the country’s “credit standing could benefit if tax and customs

administration was significantly strengthened (Standrad and Poor’s 2006)”. Some of the other

policy recommendations for Benin include faster reforms aimed at diversifying the economy and

promotion of industrial and agricultural development. Nothing that specific is found in donor’s

pledges or project documents of the World Bank. On the other hand, ratings are not always

conducive to long-term economic development. Elkhoury, for instance, contends that developing

countries adopt short-sighted policies in order to avoid rating downgrades, even when there is a

conflict with development needs (2008).

It is important for the UNDP to continue providing assistance to sovereigns seeking ratings.

Ratha et al. contend that countries without sovereign ratings are not necessarily at the bottom of the rating

scale (2007). They go further to predict that Equitaorial Guinea, Angola, Swaziland, Zambia and

Tanzania, if rated, would have above B+ ratings by Standards and Poor’s Scale in 2008. If these

countries receive sovereign ratings, their accessibility to capital markets would be boosted even

further. On the contrary, efforts to make capital markets more accessible to Sub-Saharan Africa

should not only be limited to the efforts of UNDP and S&P. There is a serious need to develop

the institutional framework that would allow sovereigns to borrow in the global capital markets.

This would be more beneficial to the sovereigns in the long run vis-à-vis relying heavily on

12

donors’ funding. The Global Emerging Markets Local Currency (GEMLOC) Bond Fund, a

partnership between the World Bank Group and the private sector, which aims to raise $5 billion

from international capital markets to invest in local-currency bond markets in developing

countries, is an example of such arrangement. A similar arrangement, but larger in scale and

targeting specifically Sub-Saharan Africa, would be another promising policy tool. Clearly,

countries in Sub-Saharan Africa would for a very long time be incapable of accessing capital

markets on par with other developing economies. A mechanism is needed that would create a

separate capital market for sub-Saharan Africa and allow sovereigns to borrow at rates

comparable to the cost of capital for most developing economies. A portion of donor’s money

could hypothetically provide liquidity to this capital market.

The UNDP-S&P partnership should be noted as an innovative form of public-private partnership

arrangement. As such, this arrangement is touted as a breakthrough in capacity development

efforts by an international organization (Muhlen-Schulte 2009). Historically, capacity

development efforts by international organizations were largely qualitative in nature. Thus, the

UNDP-S&P partnership is an example of how this could change in the future. This collaboration

serves as a precedent for other UN bodies, international organizations and development agencies.

For example, a multilateral development bank and one of the rating agencies could work together

to provide municipalities in a developing economy with ratings. This would allow sub-national

entities to access capital markets. This is a very far away prospect, but multilateral development

banks could partner with consulting companies when advising governments of middle- and high-

income developing countries on innovation driven growth.

13

Conclusion

UNDP-S&P sovereign ratings are greatly determined by countries’ external debt stocks and, in

many instances, by the quality of government effectiveness. The impact of sovereign ratings on

country’s reliance on ODA is very minimal. This however, by no means signifies that the

partnership arrangement was not successful. The initiative has set the ground for capital market

growth in countries and contributed to capacity building in selected countries. Remarkably, many

of the sovereigns would not applied for ratings had they not had the outside support. Looking

into the future, there is a great need for international organizations to foster government’s

capacity to tap into international capital markets and decrease their reliance on ODA. This would

give more leverage to the local stakeholders. This study would benefit from more robust

regression models, by accounting for a broader range of capital markets indicators for the studied

sovereigns and an estimate on whether ratings have had any effect on foreign capital outflows.

The UNDP-S&P arrangement itself is an example of innovative partnership between an

international organization and a private entity.

14

References

Applegarth, Paul V. 2004. “Capital Market and Financial Sector Development in Sub-

SaharanAfrica”, A Report of the Africa Policy Advisory Panel, Center for Strategic and

International Studies, Washington, DC

Cantor, R., and Packer, F. 1996. “Determinants and Impact of Sovereign Credit Ratings”.

Federal Reserve Bank of New York Economic Policy Review, October 1996, pp. 37-54.

Chimni, B., 2004. “International Institutions Today: An Imperial Global State in the Making”,

EJIL, Vole 15, No.1, pp. 1-37.

Credit FAQ: The Future of Sovereign Credit Ratings, 23 March, 2004. Standard & Poor’s

Elkhoury, Marwan 2008. “Credit rating Agencies and Their Potential Impact on Developing

Countries”, Report # 186, UNCTAD, January 2008

Gelos, Gaston, Ratna Sahay and Guido Sandleris, 2004. “Sovereign Borrowing by Developing

Countries: What Determines Market Access?. The International Monetary Fund, Working

Paper # 221.

Gueye, Cheick, Sy, Amadou, June 2010. “Beyond Aid: How much should African countries pay

to borrow?” IMF Working Paper

Jaramillo, Laura, 2010. “Determinants of Investment Grade Status in Emerging Markets”, IMF

Working Paper

Kaminsky, Graciela, Schmukler, Sergio. 2001. “Emerging Markets Instability: Do sovereign

Ratings Affect Country Risk and Stock Returns?”, February 28, 2001

Mellios, Constantin, Paget-Blanc, Eric, 2006. “Which Factors Determine Sovereign Ratings?”

The European Journal of Finance, Vol. 12, No.4 (June), pp. 361-377

Mohapatra, Sanket, Plaza, Sonia, Ratha, Dilip, April 2008. “New Sources and Innovative

Mechanisms for Financing Development in Sub-Saharan Africa”, Policy Research Working

Paper, The World Bank Development Prospects Group, Migration and Remittances Team

Muhlen-Schulte, Arthur, 2009. “Full Faith in Credit? The Power of Numbers in Rating Frontier

Sovereigns and the Global Governance Development by UNDP”, Working Paper, Center

for the Study of globalization and Regionalization, Department of Politics and International

Studies, University of Warwick

Ratha, Dilip, De, Prabal, Sanket, Mohaparta, , June 2007. “Shadow Sovereign Ratings for

Unrated Developing Countries”. Policy Research Paper, World Bank

Standard and Poor’s Commentary, September 5, 2006

15

Annex I

UNDP-S&P Partnership Ratings (Source: S&P)

Benin

Dec. 19, 2007 B/Positive/B B/Positive/B BBB

April 10, 2007 B/Stable/B B/Stable/B BBB

Sept.7, 2006 B/Negative/B B/Negative/B BBB

Nov. 1, 2005 B+/Stable/B B+/Stable/B BBB

Dec. 29, 2003 B+/Stable/B B+/Stable/B

Burkina Faso

Aug. 6, 2008 B/Stable/B B/Stable/B BBB

July 6, 2006 B/Positive/B B/Positive/B BBB

Nov. 1, 2005 B/Stable/B B/Stable/B BBBMarch 5, 2004 B/Stable/B B/Stable/BBB

Cameroon (Republic of)

Feb. 26, 2007 B/Stable/B B/Stable/B BBB

May 3, 2006 B-/Stable/C B-/Stable/C BBB

Nov.1, 2005 CCC/Stable/C CCC/Stable/C BBB

Dec. 3, 2004 CCC/Stable/C CCC/Stable/C

Nov. 26, 2003 B/Stable/B B/Stable/B

Gabonese Republic Nov. 8, 2007 BB-/Stable/B BB-/Stable/B

Ghana (Republic of)

March 16, 2009 B+/Negative/B B+/Negative/B 3 BB

Sept. 19, 2007 B+/Stable/B B+/Stable/B 3 BB

April 6, 2006 B+/Stable/B B+/Stable/B BB

Nov.1, 2005 B+/Stable/B B+/Stable/B B+ Sept. 4, 2003 B+/Stable/B B+/Stable/B

Kenya (Republic of)

Aug. 4, 2008 B/Positive/B B/Positive/B BB

March10, 2008 B/Stable/B B/Stable/B BB

Feb. 4, 2008 B/Negative/B B/Negative/B BB

Jan2, 2008 B+/Watch Neg/B B+/Watch Neg/B BB

Sept. 8, 2006 BB-/Stable/B B+/Stable/B

Madagascar (Republic of)

May 11, 2009 NR/NM/NR NR/NM/NR

March 18, 2009 B-/Negative/B B-/Negative/B B

Feb. 2, 2009 B/Negative/B B/Negative/B B

Nov. 1, 2005 B/Stable/B B/Stable/B B

May 25, 2004 B/Stable/B B/Stable/

16

Mali (Republic of)

July 3, 2008 NR/NM/NR NR/NM/NR

Nov. 1, 2005 B/Stable/B B/Stable/B BBB

May5, 2004 B/Stable/B B/Stable/B

Mozambique (Republic of)

Dec. 21, 2007 B+/Stable/B B+/Stable/B B+

April 6, 2006 B/Positive/B B/Positive/B B+

Nov. 1, 2005 B/Positive/B B/Positive/B B July 7, 2004 B/Positive/B B/Positive/B

17

Annex II

Determinants of Sovereign Ratings

Benin

Dependent Variable: RATING Method: Least Squares Date: 08/23/10 Time: 14:39 Sample: 1 10 Included observations: 9 Excluded observations: 1

Variable Coefficient Std. Error t-Statistic Prob.

C 22.69699 5.440866 4.171578 0.0251 LOG(EXTDEBT) -2.252400 0.791050 -2.847355 0.0653

GOVTEF 2.379962 2.352331 1.011746 0.3862 LOG(GDPGROWTH) -6.619433 2.124806 -3.115311 0.0527

LOG(INFLATION) -1.401813 0.752872 -1.861953 0.1595 POLSTAB 3.815900 3.469105 1.099967 0.3517

R-squared 0.951254 Mean dependent var 2.000000 Adjusted R-squared 0.870009 S.D. dependent var 1.936492 S.E. of regression 0.698187 Akaike info criterion 2.354061 Sum squared resid 1.462394 Schwarz criterion 2.485544 Log likelihood -4.593274 F-statistic 11.70858 Durbin-Watson stat 2.276750 Prob(F-statistic) 0.034953

18

Burkina Faso

Dependent Variable: RATING Method: Least Squares Date: 08/23/10 Time: 15:44 Sample: 1 10 Included observations: 10

Variable Coefficient Std. Error t-Statistic Prob.

C 17.7646802272

4.59266381907

3.86805586628

0.0117834319489

LOG(EXTDEBT) -3.4823940

6211

0.966370146685

-3.60358199

605

0.015484704493

LOG(GDP) -0.0670705

219556

0.814388060452

-0.08235695

63611

0.93755817828

GOVTEF 4.99683983965

3.64215003034

1.37194783247

0.228434760582

POLSTAB 1.23566902393

2.62838277688

0.470125217225

0.658056990703

R-squared 0.758750663484

Mean dependent var 1.5

Adjusted R-squared 0.565751194272

S.D. dependent var 1.58113883008

S.E. of regression 1.04193186645

Akaike info criterion 3.22688299366

Sum squared resid 5.4281100716

Schwarz criterion 3.37817554016

Log likelihood -11.134414

9683

F-statistic 3.93136140001

Durbin-Watson stat 2.13184823891

Prob(F-statistic) 0.0828123909159

19

Cameroon

Dependent Variable: RATING Method: Least Squares Date: 08/23/10 Time: 15:46 Sample: 1 10 Included observations: 9 Excluded observations: 1

Variable Coefficient Std. Error t-Statistic Prob.

C 6.09663241346

0.161664474637

37.7116396607

4.10153329495e-

05 LOG(DEBT) -

1.24216965493

0.0384762512521

-32.2840613

237

6.53142915569e-

05 LOG(GDP) 0.0940490

402596 0.12060861

7266 0.77978706

9875 0.492381

618098 GOVTEF -

0.270805567245

0.0518778823011

-5.22005824

512

0.0136725455679

LOG(INF) -0.5591177

98723

0.0999452815334

-5.59423906

907

0.011282787002

POLSTAB -0.0150207

942799

0.123368155367

-0.12175584

7246

0.910790192745

R-squared 0.998937146647

Mean dependent var 1.11111111111

Adjusted R-squared 0.997165724393

S.D. dependent var 1.26929551764

S.E. of regression 0.0675746470381

Akaike info criterion -2.316446

70912 Sum squared resid 0.0136989

98767 Schwarz criterion -

2.18496365756

Log likelihood 16.424010191

F-statistic 563.918142157

Durbin-Watson stat 1.59433531407

Prob(F-statistic) 0.00011753665286

7

20

Gabon

Dependent Variable: RATING Method: Least Squares Date: 08/23/10 Time: 15:50 Sample: 1 10 Included observations: 7 Excluded observations: 3

Variable Coefficient Std. Error t-Statistic Prob.

C 36.0463651394

22.9687088422

1.56936836924

0.257125439572

LOG(DEBT) -6.8008127

0865

4.86853552899

-1.39689084

493

0.297263927357

GOVTEF 2.67342841752

2.79574929372

0.956247551785

0.439861971816

LOG(INF) 1.06138595203

2.4027717944

0.44173398177

0.701852758736

POLSTAB -0.2417431

34202

4.1899417112

-0.05769606

13928

0.959236633273

R-squared 0.589880346918

Mean dependent var 1.42857142857

Adjusted R-squared -0.2303589

59246

S.D. dependent var 2.43975018237

S.E. of regression 2.70620864562

Akaike info criterion 5.00478278966

Sum squared resid 14.6471304672

Schwarz criterion 4.96614718184

Log likelihood -12.516739

7638

F-statistic 0.719156400437

Durbin-Watson stat 3.58808303361

Prob(F-statistic) 0.65204117632

21

Ghana

Dependent Variable: RATING Method: Least Squares Date: 08/23/10 Time: 15:41 Sample: 1 10 Included observations: 10

Variable Coefficient Std. Error t-Statistic Prob.

C -19.059346

2519

22.9022709749

-0.83220333

3579

0.452093066205

LOG(DEBT) 1.56516319428

2.43847059337

0.641862648879

0.555897366716

LOG(GDP) 10.4019031123

4.9801407792

2.0886765201

0.104987652322

GOVTEF 5.9250047196

9.53442683097

0.621432711651

0.567978160442

LOG(INF) -0.9696914

74634

2.26301937405

-0.42849455

2788

0.690357322422

POLSTAB -0.6146189

09613

3.04349084862

-0.20194537

7917

0.849814171339

R-squared 0.865146780155

Mean dependent var 2

Adjusted R-squared 0.696580255348

S.D. dependent var 2.10818510678

S.E. of regression 1.16126319086

Akaike info criterion 3.42060307508

Sum squared resid 5.3941287938

Schwarz criterion 3.60215413088

Log likelihood -11.103015

3754

F-statistic 5.13237596343

Durbin-Watson stat 2.81485549572

Prob(F-statistic) 0.0691083970875

22

Kenya

Dependent Variable: RATING Method: Least Squares Date: 08/23/10 Time: 15:56 Sample: 1 10 Included observations: 10

Variable Coefficient Std. Error t-Statistic Prob.

C 71.6202929635

50.9064675692

1.4068996806

0.232198826209

LOG(EXTDEBT) -9.9464685

1541

7.52303101923

-1.32213578

41

0.256659034026

LOG(GDP) 0.26207482947

1.53834018564

0.170362077202

0.872995173308

GOVTEF 4.49317540523

15.1874699498

0.29584752563

0.782069507912

LOG(INF) -1.5271275

2897

1.29833939374

-1.17621596

967

0.304730354242

POLSTAB 4.88600624191

13.0780591231

0.37360331498

0.727657755421

R-squared 0.67595408651

Mean dependent var 1.375

Adjusted R-squared 0.270896694648

S.D. dependent var 2.23994667595

S.E. of regression 1.91263550376

Akaike info criterion 4.41855060623

Sum squared resid 14.632698281

Schwarz criterion 4.60010166203

Log likelihood -16.092753

0312

F-statistic 1.668785955

Durbin-Watson stat 2.36006286454

Prob(F-statistic) 0.320015348122

23

Madagascar

Dependent Variable: RATING Method: Least Squares Date: 08/23/10 Time: 16:42 Sample: 1 10 Included observations: 9 Excluded observations: 1

Variable Coefficient Std. Error t-Statistic Prob.

C -5.1007494

9441

4.04158116234

-1.26206781

196

0.29611930723

LOG(EXTDEBT) -0.9298351

58783

0.294393487468

-3.15847733

855

0.0509309152721

LOG(GDP) 2.71081090505

0.95054354305

2.8518534736

0.0650100034299

GOVTEF 0.678796554447

1.17196013785

0.579197647192

0.603082013928

LOG(INF) 2.87616150822

0.635590382306

4.52518097863

0.0201852027977

POLSTAB 0.716506829223

0.951049620904

0.753385326564

0.505952346581

R-squared 0.975675471868

Mean dependent var 1.66666666667

Adjusted R-squared 0.935134591647

S.D. dependent var 1.58113883008

S.E. of regression 0.402695320164

Akaike info criterion 1.2534480464

Sum squared resid 0.486490562647

Schwarz criterion 1.38493109795

Log likelihood 0.359483791212

F-statistic 24.066459992

Durbin-Watson stat 3.80064098397

Prob(F-statistic) 0.0126001181971

24

Mali

Dependent Variable: RATING Method: Least Squares Date: 08/25/10 Time: 11:21 Sample: 1 10 Included observations: 8 Excluded observations: 2

Variable Coefficient Std. Error t-Statistic Prob.

C 23.3113770423

66.0216538928

0.353086838451

0.75776563556

LOG(DEBT) -5.3543126

1195

18.8905147193

-0.28343921

2298

0.803486222688

GOVTEF 3.40439602994

40.2421051803

0.0845978612371

0.940287021671

LOG(INF) -0.9633451

14155

0.894803384842

-1.07659976

535

0.3942758926

POLSTAB 14.0190357105

66.4046521126

0.211115264736

0.852355021543

LOG(GDP) 1.57444788939

21.614853673

0.0728410154059

0.948561809228

R-squared 0.654622326875

Mean dependent var 1.125

Adjusted R-squared -0.2088218

55937

S.D. dependent var 1.55264750852

S.E. of regression 1.70708058304

Akaike info criterion 4.02115200549

Sum squared resid 5.82824823398

Schwarz criterion 4.08073316175

Log likelihood -10.084608

022

F-statistic 0.758152454908

Durbin-Watson stat 0.883296325768

Prob(F-statistic) 0.653281485135

25

Mozambique

Dependent Variable: RATING Method: Least Squares Date: 08/23/10 Time: 17:22 Sample: 1 10 Included observations: 8 Excluded observations: 2

Variable Coefficient Std. Error t-Statistic Prob.

C 12.6618889691

2.78805135597

4.54148340634

0.0452212353545

LOG(DEBT) -3.3470746

4503

0.555136852293

-6.02927842

244

0.0264232178994

LOG(GDP) 0.262339902264

0.27339191853

0.959574458801

0.438526810922

GOVTEF -3.2677511

5442

2.37343988313

-1.37679963

063

0.302434759205

LOG(INF) 0.605241433481

0.601931949927

1.00549810249

0.420539320649

POLSTAB -1.6148681

3143

0.890394818222

-1.81365400

875

0.211405647657

R-squared 0.983018970671

Mean dependent var 1.75

Adjusted R-squared 0.94056639735

S.D. dependent var 1.90862703084

S.E. of regression 0.465304334752

Akaike info criterion 1.42145549701

Sum squared resid 0.433016247878

Schwarz criterion 1.48103665327

Log likelihood 0.314178011944

F-statistic 23.1556980829

Durbin-Watson stat 2.33920999661

Prob(F-statistic) 0.0419134404699

26

Annex III

Share of ODA to GNI

Benin Dependent Variable: LOG(ODA) Method: Least Squares Sample: 1 10 Included observations: 9

Excluded observations: 1

Variable Coefficient Std. Error t-Statistic Prob.

C 0.686352344648

0.754007558758

0.910272498831

0.429791872882

LOG(GDPGROWTH) 0.665831906688

0.3351094487

1.9869087824

0.141106828827

GOVTEF -0.1795754

27691

0.403038011605

-0.44555456

9346

0.686110016933

LOG(INFLATION) -0.0848062

158925

0.106059945552

-0.79960644

3801

0.482395500876

POLSTAB 0.615929570866

0.393037383875

1.56710174689

0.215080383307

RATING 0.0789770883463

0.0526221291627

1.50083414721

0.230383736673

R-squared 0.792532571999

Mean dependent var 2.23282534226

Adjusted R-squared 0.446753525331

S.D. dependent var 0.164621869938

S.E. of regression 0.122446635995

Akaike info criterion -1.127561

82581 Sum squared resid 0.0449795

359994 Schwarz criterion -

0.996078774249

Log likelihood 11.0740282161

F-statistic 2.29202023557

Durbin-Watson stat 2.35688376599

Prob(F-statistic) 0.263225063849

27

Burkina Faso

Dependent Variable: LOG(ODA) Method: Least Squares Sample: 1 10 Included observations: 10

Variable Coefficient Std. Error t-Statistic Prob.

C 2.97747682054

0.31153217063

9.55752599972

0.00021229505105

2 LOG(GDP) -

0.0600615800057

0.0878239023743

-0.68388648

6275

0.524447379676

GOVTEF 0.61530759151

0.382274391538

1.60959668011

0.168400230611

POLSTAB 0.907673192056

0.290559280145

3.12388298733

0.0261373186419

RATING -0.0587166

769251

0.0255308547996

-2.29983200

272

0.0697871038662

R-squared 0.712287907583

Mean dependent var 2.23980131733

Adjusted R-squared 0.482118233649

S.D. dependent var 0.156766869032

S.E. of regression 0.112815713633

Akaike info criterion -1.219269

40287 Sum squared resid 0.0636369

262129 Schwarz criterion -

1.06797685638

Log likelihood 11.0963470144

F-statistic 3.09462100462

Durbin-Watson stat 2.81221181171

Prob(F-statistic) 0.123467459801

28

Cameroon

Dependent Variable: LOG(ODA) Method: Least Squares Sample: 1 10 Included observations: 9 Excluded observations: 1

Variable Coefficient Std. Error t-Statistic Prob.

C -4.8739644

7566

10.0070213576

-0.48705446

9207

0.651705270704

LOG(INF) 1.31723150271

1.39858769583

0.941829752

0.39960655808

LOG(DEBT) 1.14870922776

1.9164923002

0.599381081595

0.581215458648

POLSTAB 0.598149292859

0.978096513633

0.611544243867

0.573888872287

RATING 0.935619496361

1.51416571811

0.617910896523

0.570078565383

R-squared 0.244764708032

Mean dependent var 1.56386590621

Adjusted R-squared -0.5104705

83936

S.D. dependent var 0.505051194171

S.E. of regression 0.620713996289

Akaike info criterion 2.18428824807

Sum squared resid 1.54114346076

Schwarz criterion 2.2938574577

Log likelihood -4.8292971

1632

F-statistic 0.324090665035

Durbin-Watson stat 2.48427582815

Prob(F-statistic) 0.84959830406

29

Gabon

Dependent Variable: LOG(ODA)

Method: Least Squares

Sample(adjusted): 1 10 Included observations: 5 Excluded observations: 4 after adjusting endpoints

Variable Coefficient Std. Error t-Statistic Prob.

C 0.195439420417

0.290567538092

0.672612714073

0.62305246158

LOG(GDP) -0.0940628

811246

0.323668158162

-0.29061518

3337

0.819948147521

POLSTAB -1.6637114

5486

0.587709534316

-2.83083965

414

0.216176373684

RATING 0.043057705592

0.0992647134006

0.433766482741

0.739449070241

R-squared 0.92563018843

Mean dependent var 0.219722457734

Adjusted R-squared 0.70252075372

S.D. dependent var 0.491314351676

S.E. of regression 0.26797099364

Akaike info criterion 0.194686079941

Sum squared resid 0.0718084534322

Schwarz criterion -0.117763

590112 Log likelihood 3.5132848

0015 F-statistic 4.148772

05724 Durbin-Watson stat 2.2246967

5791 Prob(F-statistic) 0.342869

826909

30

Ghana

Dependent Variable: LOG(ODA) Method: Least Squares

Sample: 1 10 Included observations: 10

Variable Coefficient Std. Error t-Statistic Prob.

C 3.03292739675

1.07215142391

2.82882373618

0.0367254704008

LOG(GDP) -0.6952139

90172

0.690849740609

-1.00631721

966

0.360450697194

GOVTEF -1.8858103

3959

0.661938359318

-2.84892137

319

0.0358690586316

POLSTAB 0.742453935767

0.306792397525

2.42005324042

0.06011346161

RATING 0.0272884037457

0.0552972972016

0.493485308083

0.642579379282

R-squared 0.674487983176

Mean dependent var 2.36972961574

Adjusted R-squared 0.414078369717

S.D. dependent var 0.202226078452

S.E. of regression 0.154794998978

Akaike info criterion -0.586577

363539 Sum squared resid 0.1198074

58542 Schwarz criterion -

0.435284817042

Log likelihood 7.9328868177

F-statistic 2.5901040066

Durbin-Watson stat 2.50366802728

Prob(F-statistic) 0.162389945575

31

Kenya

Dependent Variable: LOG(ODA) Method: Least Squares Sample: 1 10 Included observations: 10

Variable Coefficient Std. Error t-Statistic Prob.

C 1.78566458334

0.796460551047

2.24200003502

0.0884256135001

LOG(GDP) 0.116281377021

0.100127124277

1.1613374284

0.31008388076

GOVTEF 1.14222146965

1.03445682635

1.10417509997

0.331469936012

LOG(INF) -0.0223995

891704

0.119178595709

-0.18794976

5955

0.860065544046

RATING -0.0044421

1243957

0.0334490651527

-0.13280228

9669

0.900762559074

POLSTAB -0.2613255

55893

0.632495786769

-0.41316568

6413

0.70067379059

R-squared 0.642786828294

Mean dependent var 1.37338665689

Adjusted R-squared 0.196270363661

S.D. dependent var 0.171088654836

S.E. of regression 0.153382638062

Akaike info criterion -0.628052

820021 Sum squared resid 0.0941049

34635 Schwarz criterion -

0.446501764224

Log likelihood 9.1402641001

F-statistic 1.43955907387

Durbin-Watson stat 3.0270783831

Prob(F-statistic) 0.372916186739

32

Madagascar

Dependent Variable: LOG(ODA) Method: Least Squares Sample: 1 10 Included observations: 9 Excluded observations: 1

Variable Coefficient Std. Error t-Statistic Prob.

C 2.14833690655

3.91522636613

0.548713332424

0.621400731748

LOG(GDP) -0.0835333

409005

1.16526939533

-0.07168586

18577

0.947363435964

GOVTEF 1.08446480236

0.921474856775

1.176879428

0.32411901188

LOG(INF) 0.401723736092

0.940867310609

0.426971722328

0.698188968026

POLSTAB 0.849301275172

0.72100819013

1.17793568339

0.323755794552

RATING 0.0694512784299

0.225116048345

0.308513226581

0.777874243444

R-squared 0.758017199135

Mean dependent var 2.52478407934

Adjusted R-squared 0.354712531027

S.D. dependent var 0.406514922152

S.E. of regression 0.326552571348

Akaike info criterion 0.834269454317

Sum squared resid 0.319909745562

Schwarz criterion 0.965752505875

Log likelihood 2.24578745557

F-statistic 1.87951506411

Durbin-Watson stat 2.2875866026

Prob(F-statistic) 0.320074524338

33

Mali

Dependent Variable: LOG(ODA) Method: Least Squares Date: 08/25/10 Time: 12:06 Sample: 1 10 Included observations: 8 Excluded observations: 2

Variable Coefficient Std. Error t-Statistic Prob.

C 1.32473195043

0.694394054748

1.90775243735

0.307361063753

LOG(DEBT) 0.453873712384

0.196600464469

2.3086095631

0.260226523353

LOG(GDP) -0.8891516

02792

0.220859673309

-4.02586669

386

0.15499545968

GOVTEF -1.5464385

3471

0.411381882658

-3.75913135

679

0.165519572009

POLSTAB -1.0667486

409

0.685130466772

-1.55700073

582

0.363455878972

LOG(INF) -0.0736845

311225

0.0114757442159

-6.42089347

204

0.0983580005067

RATING 0.00246721166282

0.00721562275012

0.341926365646

0.790256547414

R-squared 0.998175659932

Mean dependent var 2.663693609

Adjusted R-squared 0.987229619526

S.D. dependent var 0.154149074378

S.E. of regression 0.0174197869671

Akaike info criterion -5.591861

54896 Sum squared resid 0.0003034

48977979 Schwarz criterion -

5.52235019999

Log likelihood 29.3674461958

F-statistic 91.1905696358

Durbin-Watson stat 1.64665730701

Prob(F-statistic) 0.0799882025695

34

Mozambique

Dependent Variable: LOG(ODA) Method: Least Squares Sample: 1 10 Included observations: 10

Variable Coefficient Std. Error t-Statistic Prob.

C 2.63467833502

1.30586271737

2.01757680956

0.0996779313785

LOG(GDP) 0.169662195759

0.219139466891

0.774220172046

0.473800424336

POLSTAB -0.3079774

34137

0.498411960423

-0.61791742

2919

0.563684842965

GOVTEF 0.602822655916

1.14579760126

0.526116179029

0.621300067819

RATING 0.0699997014446

0.107652867633

0.650235362826

0.544229784058

R-squared 0.387584615066

Mean dependent var 2.49202812914

Adjusted R-squared -0.1023476

92882

S.D. dependent var 0.397016758684

S.E. of regression 0.41683880111

Akaike info criterion 1.39461848585

Sum squared resid 0.868772930553

Schwarz criterion 1.54591103234

Log likelihood -1.9730924

2923

F-statistic 0.791098298231

Durbin-Watson stat 1.48734279836

Prob(F-statistic) 0.57789969273