Embed Size (px)

Citation preview

Current scenario of the

Indian sugar sector

Points to be covered today

Some important characteristics of Indian Sugar Industry

Current sugar scenario

The Government Controls & recent decisions of Govt.

Scenario after decontrol

Ethanol blending with petrol

2

The Indian Sugar Sector

2nd largest producer of sugar in the world

Around 5 million hectares of land

Producing about 350 million tons of sugarcane

50 million cane farmers and dependants

Cane payment of Rs.55,000 crore annually received directly to

farmers, without middlemen.

3

The Indian Sugar Industry

Annual estimated consumption of 23 million tons

Capacity to produce over 30 million tons of sugar

65% of sugar consumed by bulk consumers

Rs.80,000 crore industry

Potential to generate 7500 MW of green power

Producing 250 crore litres of alcohol

Located in rural heartland, directly contributes to rural

economic development & employment

4

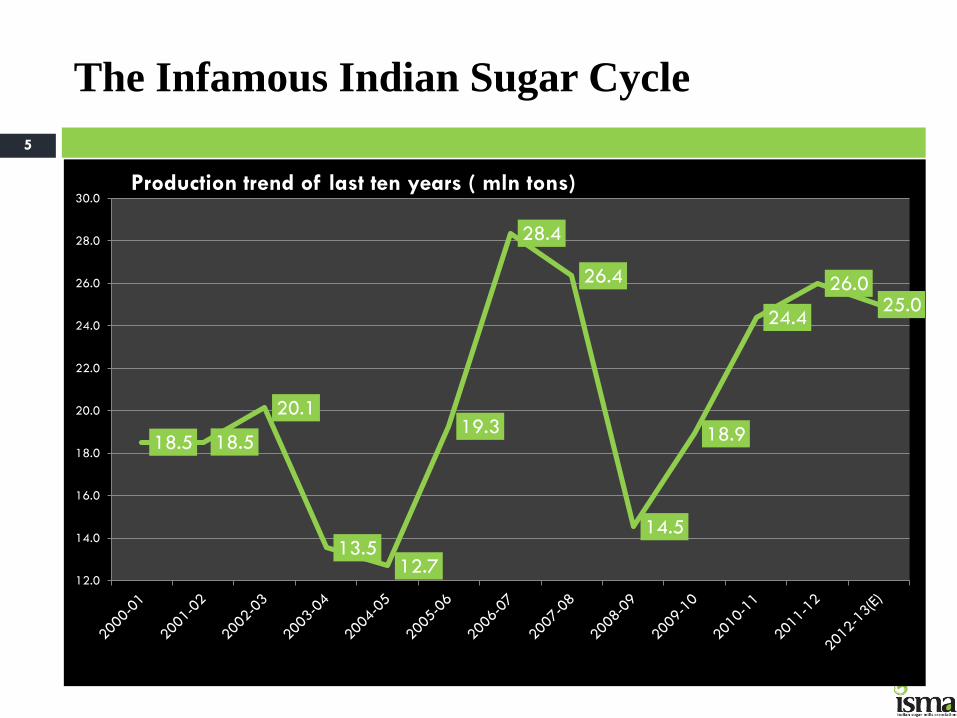

The Infamous Indian Sugar Cycle

5

18.5 18.5

20.1

13.5 12.7

19.3

28.4

26.4

14.5

18.9

24.4

26.0 25.0

12.0

14.0

16.0

18.0

20.0

22.0

24.0

26.0

28.0

30.0Production trend of last ten years ( mln tons)

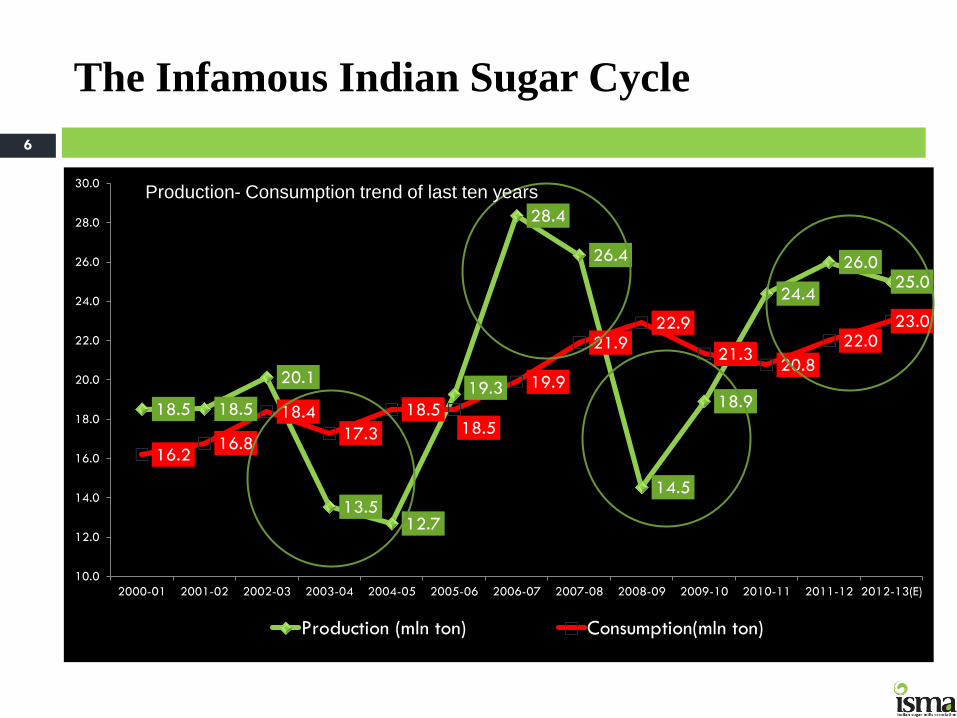

The Infamous Indian Sugar Cycle

6

18.5 18.5

20.1

13.5 12.7

19.3

28.4

26.4

14.5

18.9

24.4

26.0 25.0

16.2 16.8

18.4

17.3

18.5 18.5

19.9

21.9 22.9

21.3 20.8

22.0 23.0

10.0

12.0

14.0

16.0

18.0

20.0

22.0

24.0

26.0

28.0

30.0

2000-01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13(E)

Production (mln ton) Consumption(mln ton)

Production- Consumption trend of last ten years

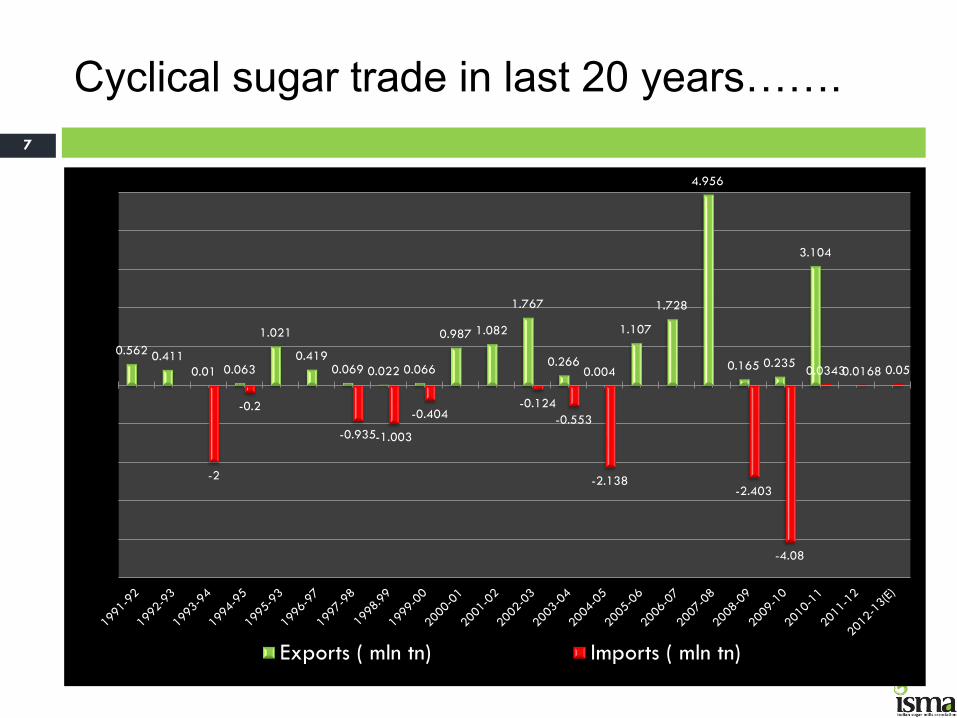

Cyclical sugar trade in last 20 years…….

7

0.562 0.411

0.01 0.063

1.021

0.419 0.069 0.022 0.066

0.987 1.082

1.767

0.266 0.004

1.107

1.728

4.956

0.165 0.235

3.104

-2

-0.2

-0.935 -1.003

-0.404 -0.124

-0.553

-2.138 -2.403

-4.08

0.0343 0.0168 0.05

Exports ( mln tn) Imports ( mln tn)

Current sugar scenario

Surplus domestic sugar produced 3 years in a row

Opening balance for 2013-14 expected to be over 80 lakh tons

More than 4 months’ consumption requirement

Estimated sugar production for next sugar season 2013-14 is

similarly expected to be more than domestic requirement

Ex-mill sugar prices significantly lower to cost of production

By around Rs.2-4 per kilo of sugar, losses to mills throughout season

8

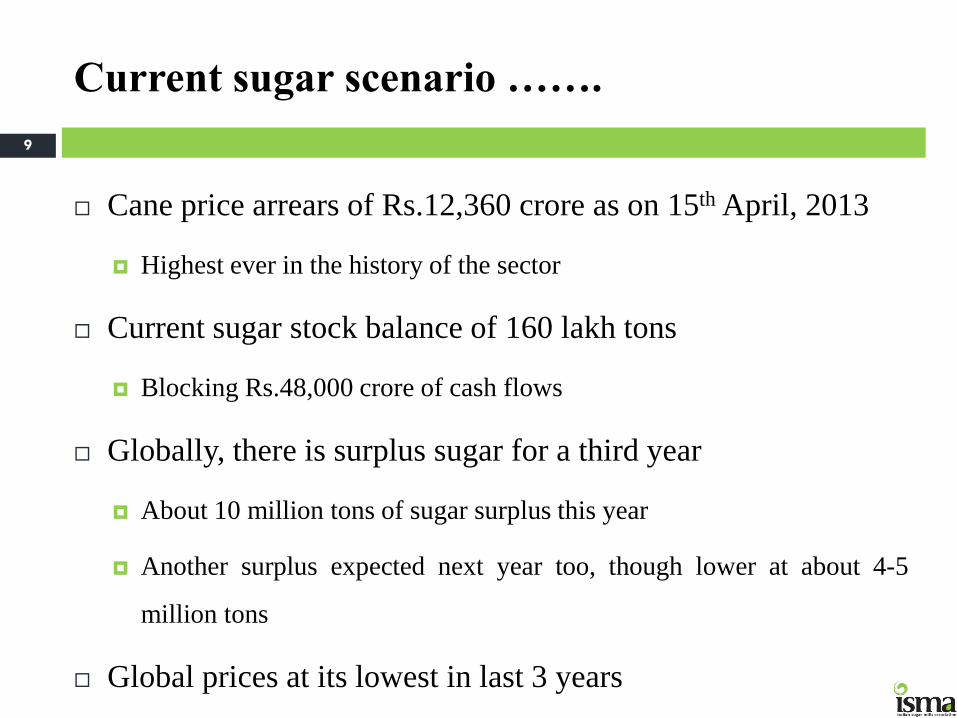

Current sugar scenario …….

Cane price arrears of Rs.12,360 crore as on 15th April, 2013

Highest ever in the history of the sector

Current sugar stock balance of 160 lakh tons

Blocking Rs.48,000 crore of cash flows

Globally, there is surplus sugar for a third year

About 10 million tons of sugar surplus this year

Another surplus expected next year too, though lower at about 4-5

million tons

Global prices at its lowest in last 3 years

9

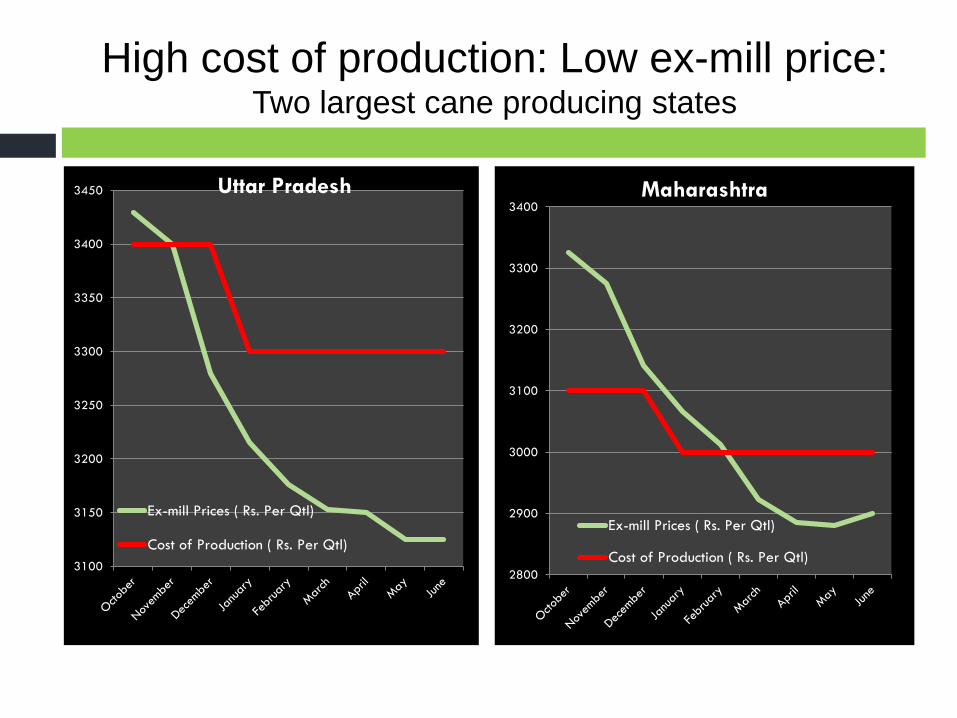

High cost of production: Low ex-mill price: Two largest cane producing states

(Rs/ qtl)

3100

3150

3200

3250

3300

3350

3400

3450 Uttar Pradesh

Ex-mill Prices ( Rs. Per Qtl)

Cost of Production ( Rs. Per Qtl)

2800

2900

3000

3100

3200

3300

3400Maharashtra

Ex-mill Prices ( Rs. Per Qtl)

Cost of Production ( Rs. Per Qtl)

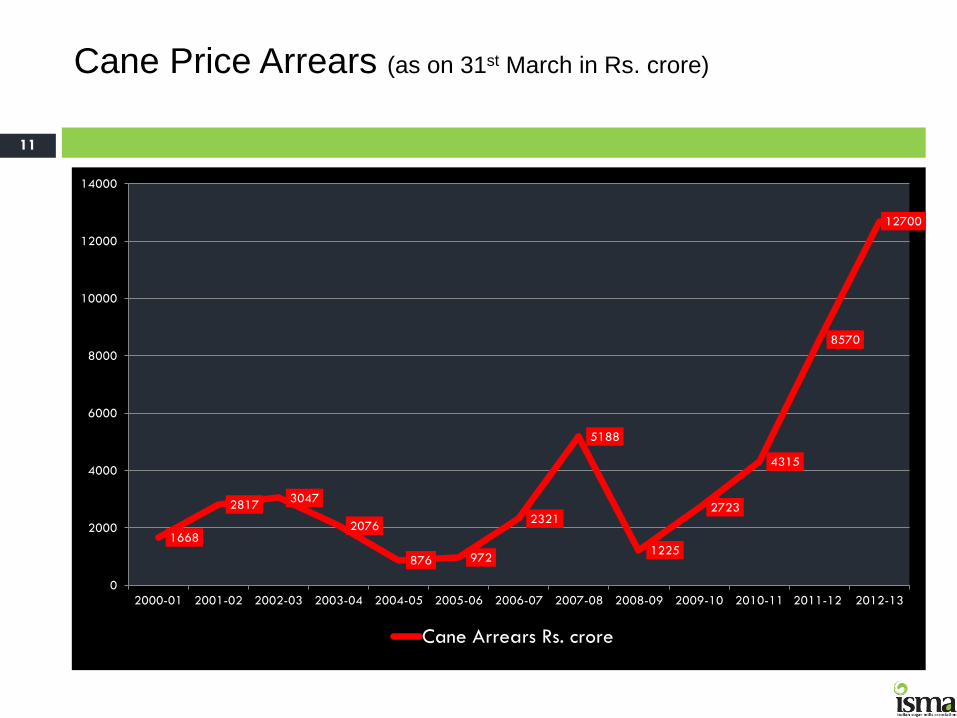

Cane Price Arrears (as on 31st March in Rs. crore)

11

1668

2817 3047

2076

876 972

2321

5188

1225

2723

4315

8570

12700

0

2000

4000

6000

8000

10000

12000

14000

2000-01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

Cane Arrears Rs. crore

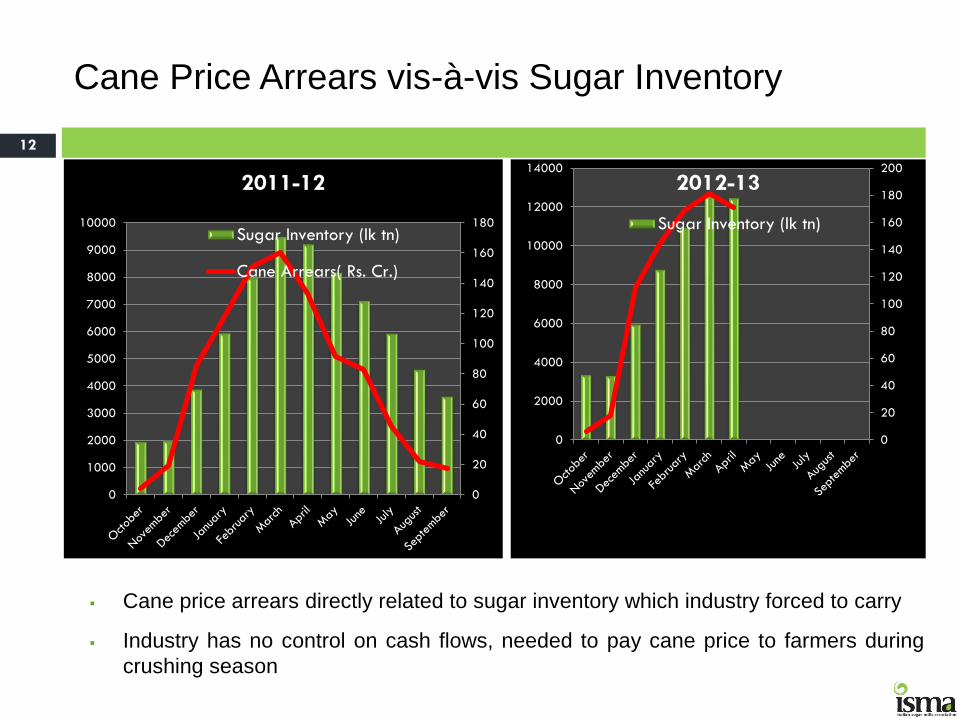

Cane Price Arrears vis-à-vis Sugar Inventory

12

Cane price arrears directly related to sugar inventory which industry forced to carry

Industry has no control on cash flows, needed to pay cane price to farmers during

crushing season

0

20

40

60

80

100

120

140

160

180

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

2011-12

Sugar Inventory (lk tn)

Cane Arrears( Rs. Cr.)

0

20

40

60

80

100

120

140

160

180

200

0

2000

4000

6000

8000

10000

12000

14000

2012-13

Sugar Inventory (lk tn)

Controls on Indian Sugar Sector

Minimum

Distance Criteria

between mills

Levy Sugar

Obligation on

mills

Import and

Export

Dual Cane

Pricing:

Centre/State

Regulated

Release

Mechanism

Cane Area

Reservation

GOVT. POLICIES

Compulsory

sugar packing

in jute only

Central Govt. controls State Govt. controls

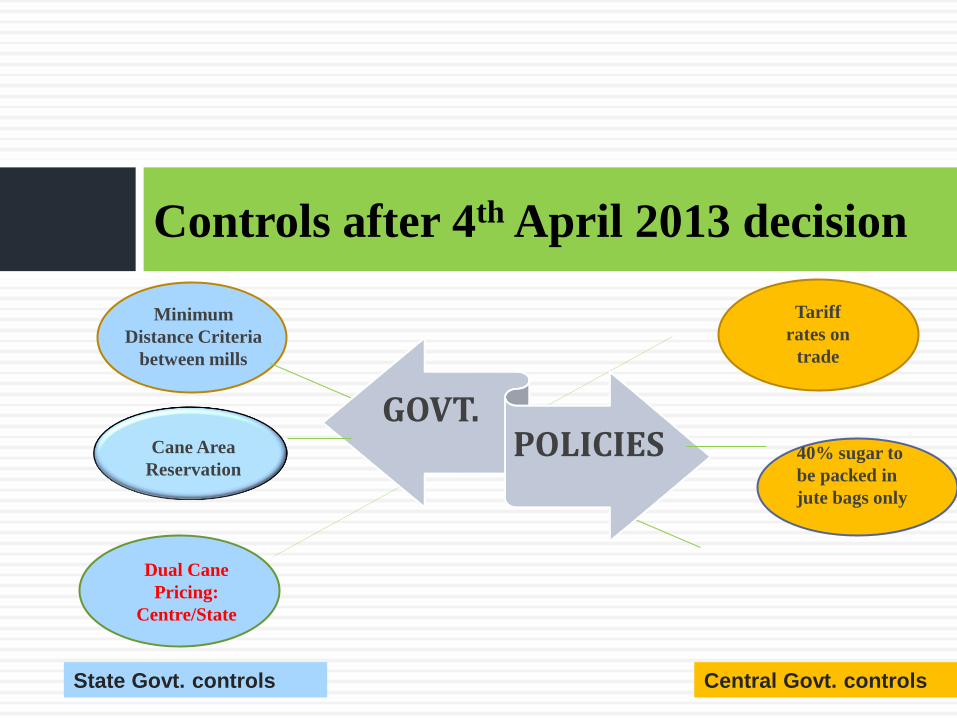

Controls after 4th April 2013 decision

Minimum

Distance Criteria

between mills

Tariff

rates on

trade

Dual Cane

Pricing:

Centre/State

Cane Area

Reservation

GOVT. POLICIES 40% sugar to

be packed in

jute bags only

Central Govt. controls State Govt. controls

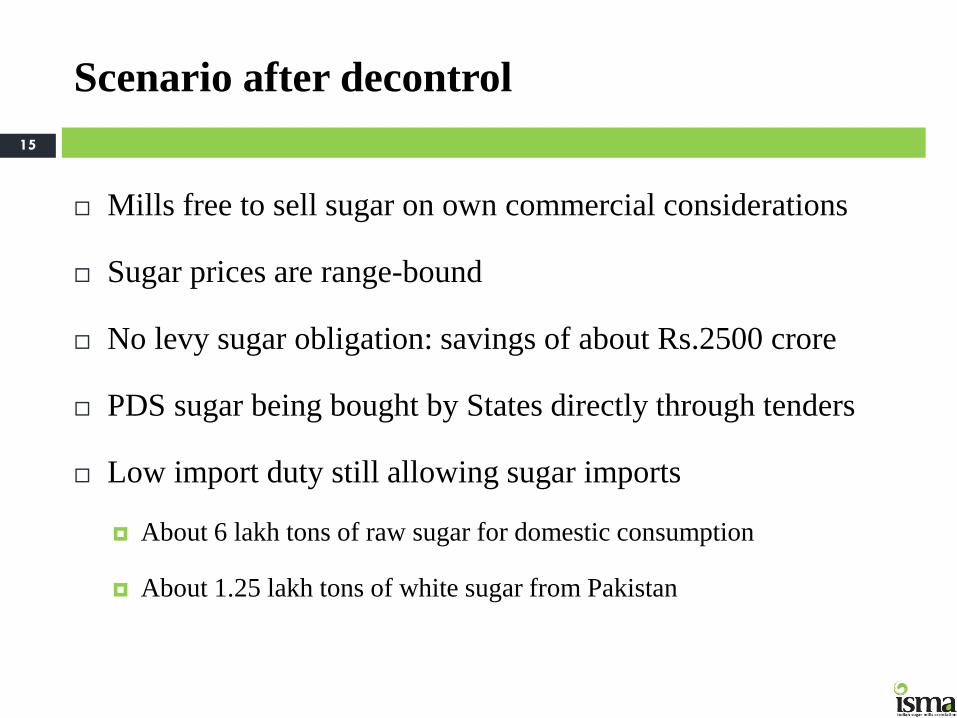

Scenario after decontrol

Mills free to sell sugar on own commercial considerations

Sugar prices are range-bound

No levy sugar obligation: savings of about Rs.2500 crore

PDS sugar being bought by States directly through tenders

Low import duty still allowing sugar imports

About 6 lakh tons of raw sugar for domestic consumption

About 1.25 lakh tons of white sugar from Pakistan

15

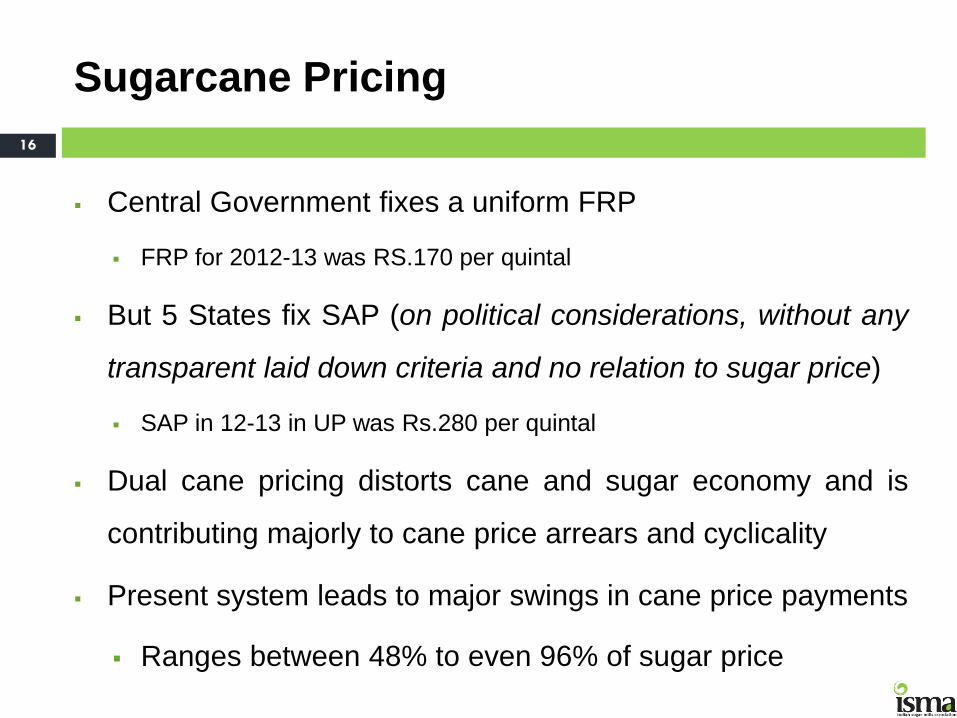

Sugarcane Pricing

Central Government fixes a uniform FRP

FRP for 2012-13 was RS.170 per quintal

But 5 States fix SAP (on political considerations, without any

transparent laid down criteria and no relation to sugar price)

SAP in 12-13 in UP was Rs.280 per quintal

Dual cane pricing distorts cane and sugar economy and is

contributing majorly to cane price arrears and cyclicality

Present system leads to major swings in cane price payments

Ranges between 48% to even 96% of sugar price

16

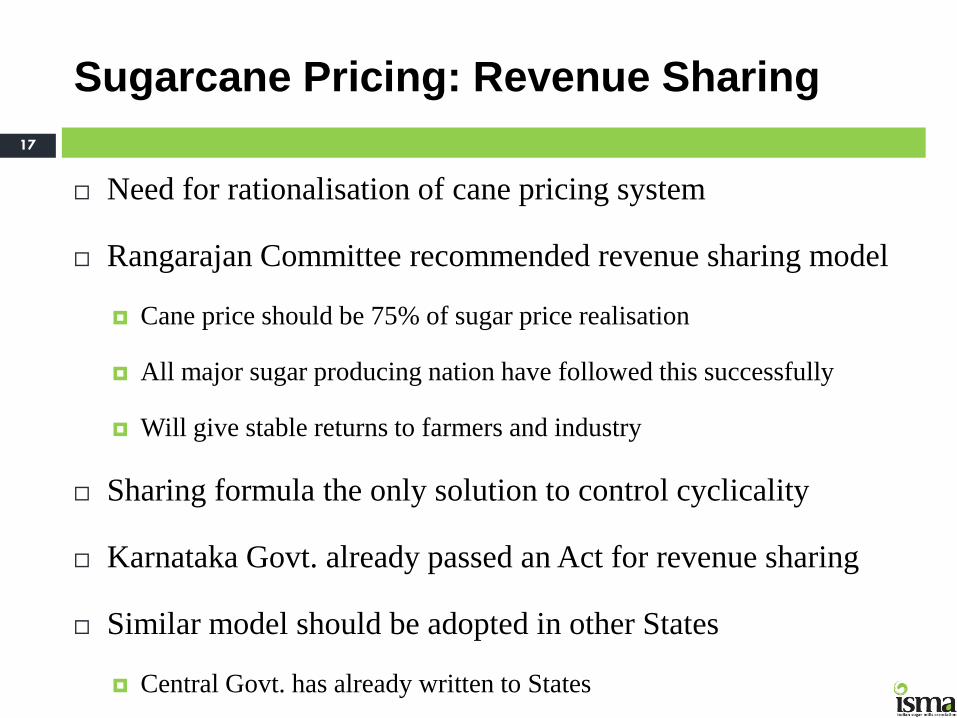

Sugarcane Pricing: Revenue Sharing

Need for rationalisation of cane pricing system

Rangarajan Committee recommended revenue sharing model

Cane price should be 75% of sugar price realisation

All major sugar producing nation have followed this successfully

Will give stable returns to farmers and industry

Sharing formula the only solution to control cyclicality

Karnataka Govt. already passed an Act for revenue sharing

Similar model should be adopted in other States

Central Govt. has already written to States

17

Investments required in the sector

Rangarajan Committee suggested that the sector has potential

to grow to Rs.160,000 crore from Rs.80,000 crore in 5 years

For this large investments required both at farm & mill level

Considering huge opportunities and potential in Indian sugra

sector, several investors, including foreign, watching……

Waiting for rationalisation in the cane pricing policy

So, reforms on cane side is urgently awaited

18

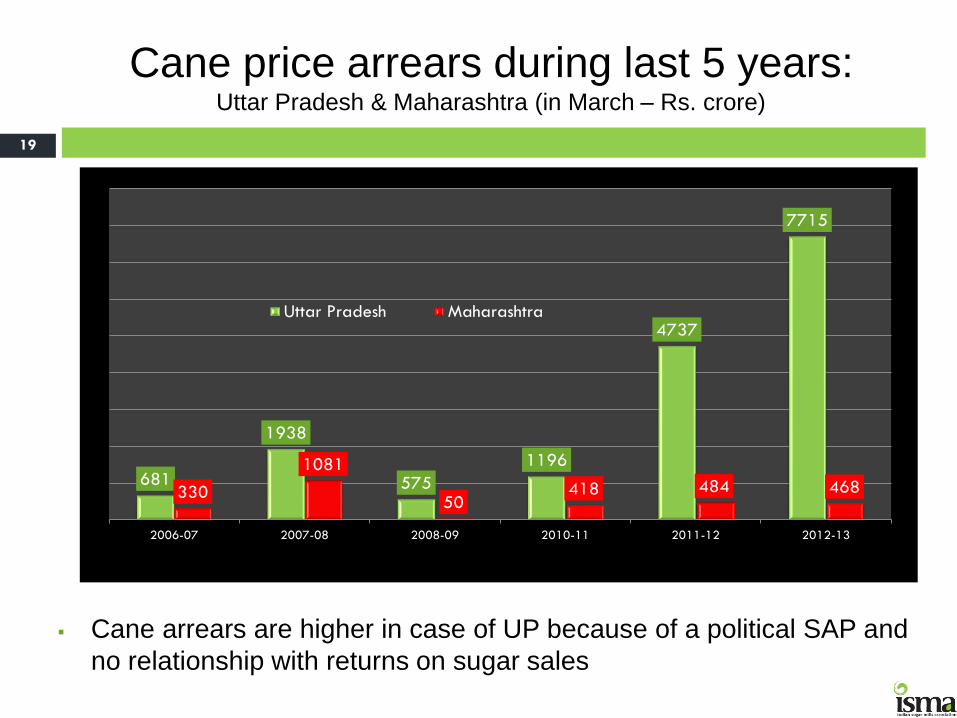

Cane price arrears during last 5 years: Uttar Pradesh & Maharashtra (in March – Rs. crore)

Cane arrears are higher in case of UP because of a political SAP and

no relationship with returns on sugar sales

19

681

1938

575

1196

4737

7715

330

1081

50 418 484 468

2006-07 2007-08 2008-09 2010-11 2011-12 2012-13

Uttar Pradesh Maharashtra

Ethanol blending with petrol

Mandatory 5% ethanol blending with petrol

To be achieved by 30 June, 2013

Requirement of 105 crore litres annually

Almost 35% of molasses production

55 crore litres offered currently for which POs are being issued

Supplementary tender being floated by OMCs for balance

Tendered price for imported ethanol very high

20

Thank You