Embed Size (px)

Citation preview

Sarah Hillyear, Operations Manager

the offshore decommissioning market in the North Sea

the decommissioning market – present & future

the industry role for Decom North Sea

North Sea decommissioning activity

• developing decommissioning market

• ~ 7% of facilities removed to date with varying conditions and complexity

• estimated £400-500m annual spend, and rising

• supply chain capability developing

Shell Indefatigable

just completed BP NW Hutton

removed

Shell Brent Delta

being prepared

“coming soon”BP Miller, ValhallMarathon BraeCNR Murchison,

Ninian NorthHess Fife, Flora,

Angus, FergusPerenco Lemanand others

many forthcoming projects will be “firsts” for their respective operators

decommissioning projects have largely been “one-offs”

limited opportunity for learning and knowledge transfer

decommissioning cost estimates continuing to increase

early contractual experiences not always happy - for operators or contractors

industry now genuinely seeking more co-operation and innovation

some new technologies needed

some market observations

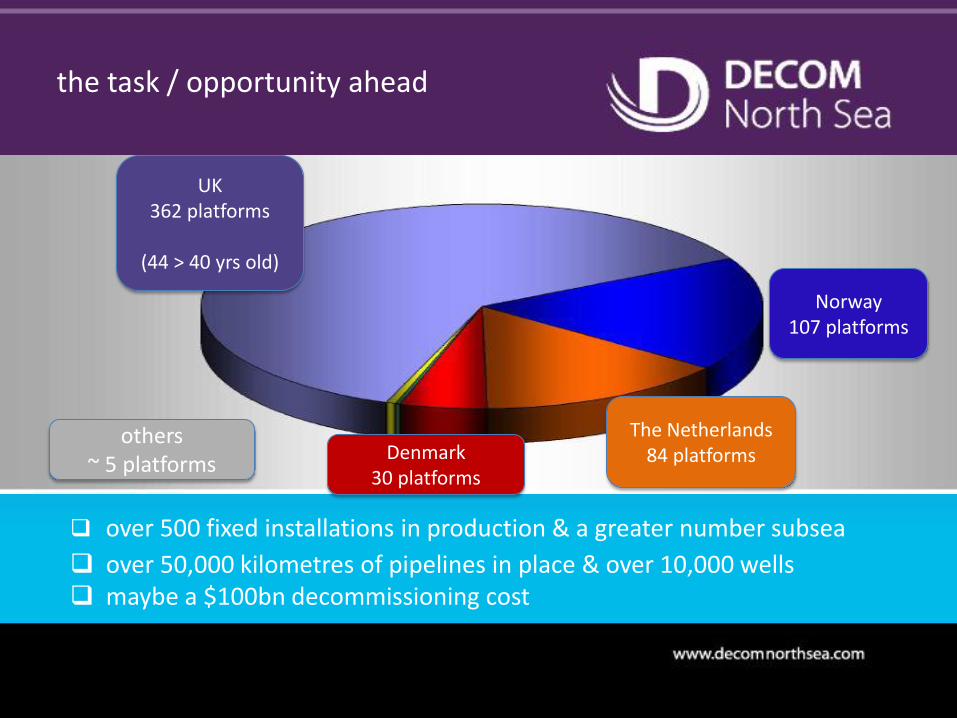

the task / opportunity ahead

over 500 fixed installations in production & a greater number subsea

over 50,000 kilometres of pipelines in place & over 10,000 wells maybe a $100bn decommissioning cost

UK 362 platforms

(44 > 40 yrs old)

Norway107 platforms

The Netherlands84 platformsDenmark

30 platforms

others ~ 5 platforms

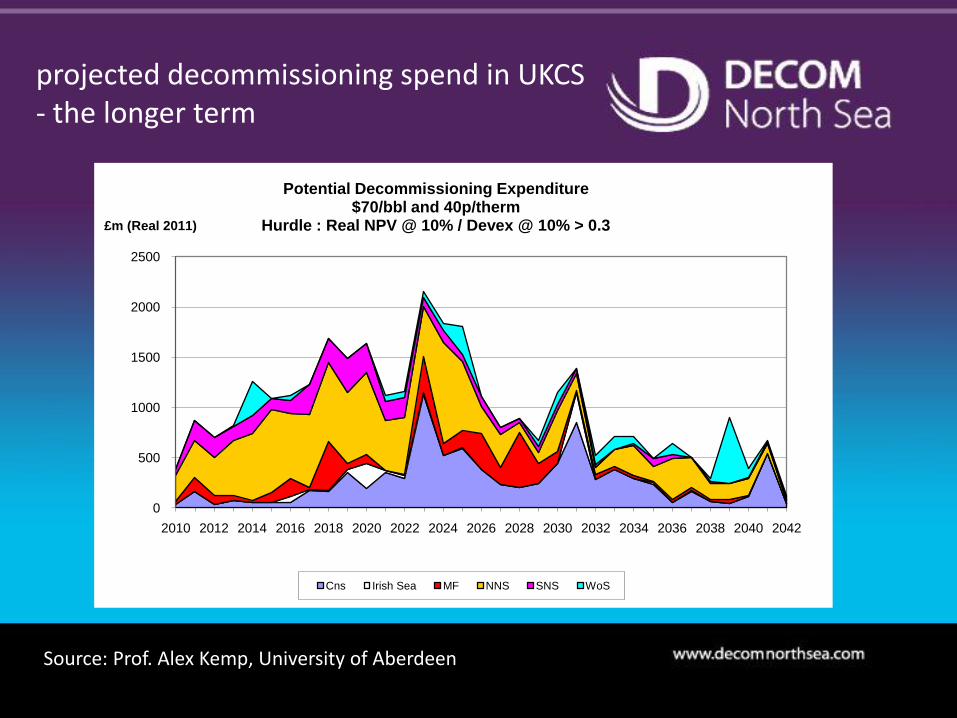

projected decommissioning spend in UKCS- the longer term

0

500

1000

1500

2000

2500

2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030 2032 2034 2036 2038 2040 2042

£m (Real 2011)

Potential Decommissioning Expenditure$70/bbl and 40p/therm

Hurdle : Real NPV @ 10% / Devex @ 10% > 0.3

Cns Irish Sea MF NNS SNS WoS

Source: Prof. Alex Kemp, University of Aberdeen

0

200

400

600

800

1000

1200

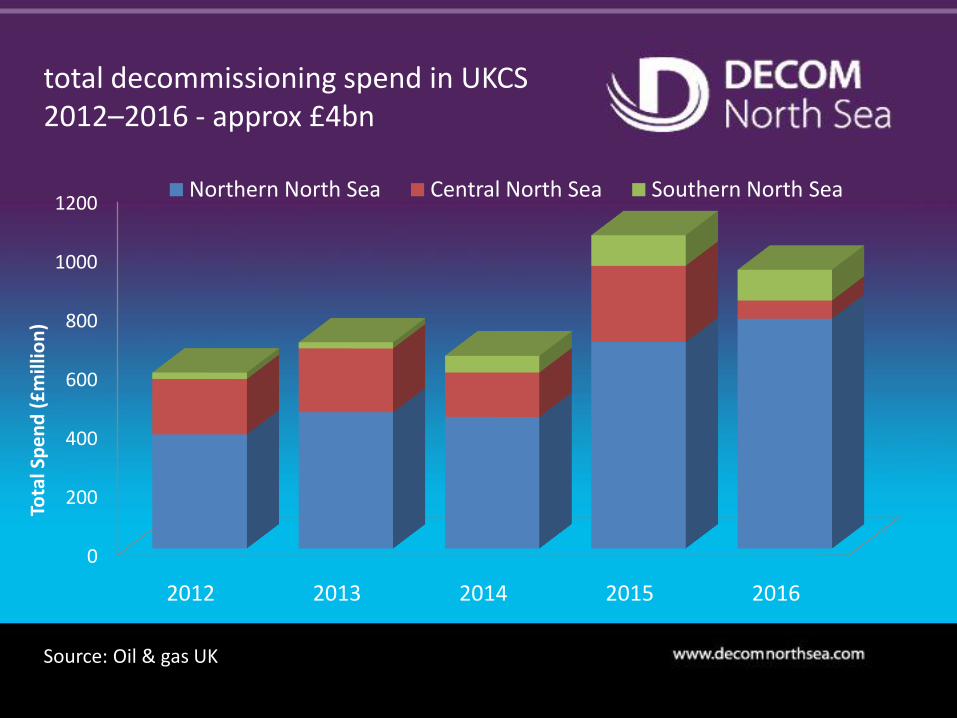

2012 2013 2014 2015 2016

Tota

l Sp

en

d (

£m

illio

n)

Northern North Sea Central North Sea Southern North Sea

Source: Oil & Gas UK Decommissioning Survey

total decommissioning spend in UKCS 2012–2016 - approx £4bn

Source: Oil & gas UK

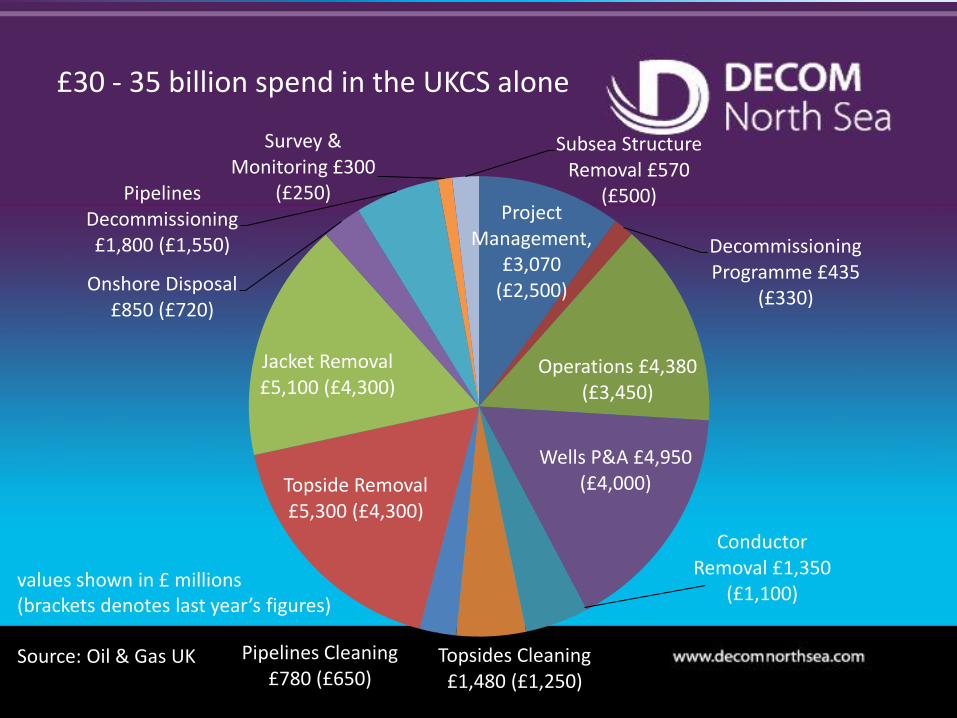

£30 - 35 billion spend in the UKCS alone

Project Management,

£3,070(£2,500)

Decommissioning Programme £435

(£330)

Operations £4,380 (£3,450)

Wells P&A £4,950 (£4,000)

Conductor Removal £1,350

(£1,100)

Topsides Cleaning £1,480 (£1,250)

Pipelines Cleaning £780 (£650)

Topside Removal £5,300 (£4,300)

Jacket Removal £5,100 (£4,300)

Onshore Disposal £850 (£720)

Pipelines Decommissioning £1,800 (£1,550)

Survey & Monitoring £300

(£250)

Subsea Structure Removal £570

(£500)

values shown in £ millions (brackets denotes last year’s figures)

Source: Oil & Gas UK

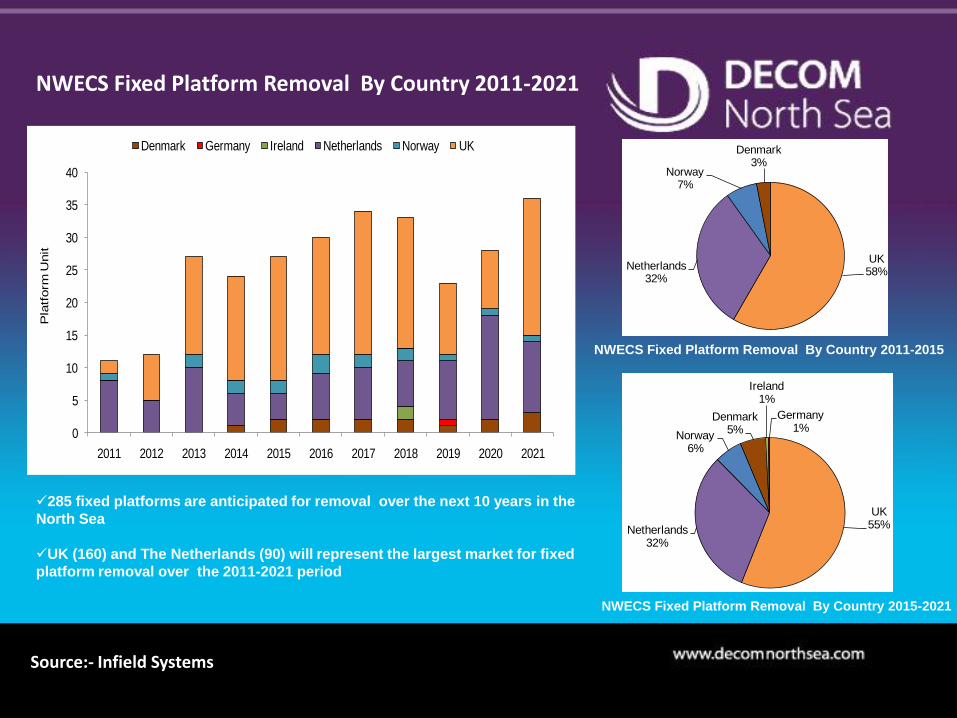

Source:- Infield Systems

NWECS Fixed Platform Removal By Country 2011-2015

NWECS Fixed Platform Removal By Country 2015-2021

NWECS Fixed Platform Removal By Country 2011-2021

285 fixed platforms are anticipated for removal over the next 10 years in the

North Sea

UK (160) and The Netherlands (90) will represent the largest market for fixed

platform removal over the 2011-2021 period

0

5

10

15

20

25

30

35

40

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Denmark Germany Ireland Netherlands Norway UK

Pla

tform

Unit

UK58%

Netherlands32%

Norway7%

Denmark3%

UK55%Netherlands

32%

Norway6%

Denmark5%

Ireland1%

Germany1%

Source:- Infield Systems

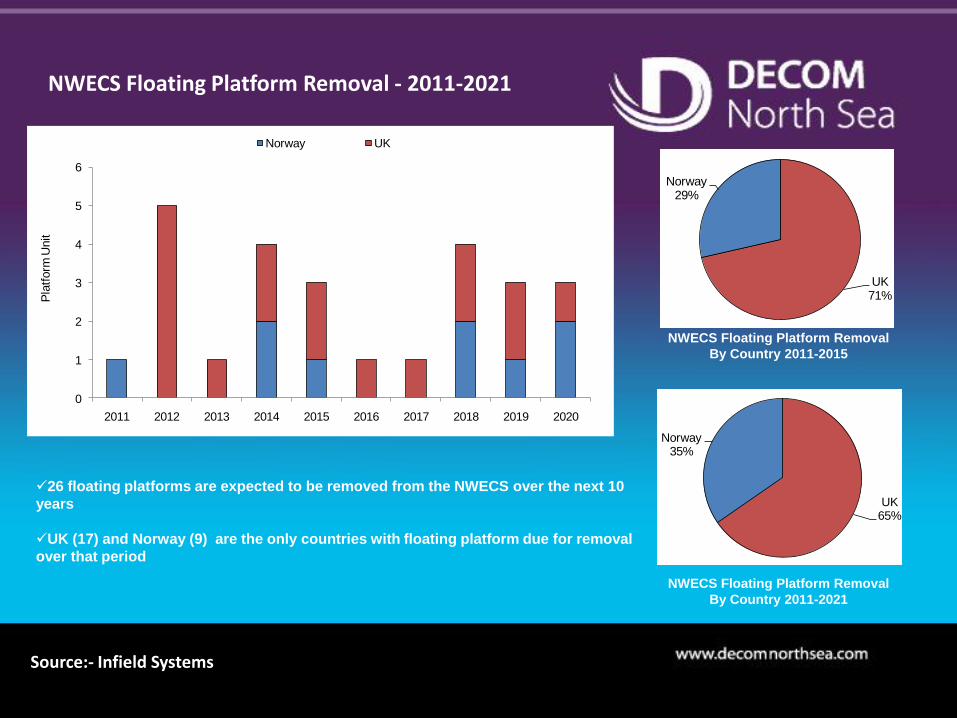

0

1

2

3

4

5

6

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Norway UK

Pla

tform

Unit

NWECS Floating Platform Removal

By Country 2011-2015

26 floating platforms are expected to be removed from the NWECS over the next 10

years

UK (17) and Norway (9) are the only countries with floating platform due for removal

over that period

NWECS Floating Platform Removal

By Country 2011-2021

NWECS Floating Platform Removal - 2011-2021

UK65%

Norway35%

UK71%

Norway29%

Source:- Infield Systems

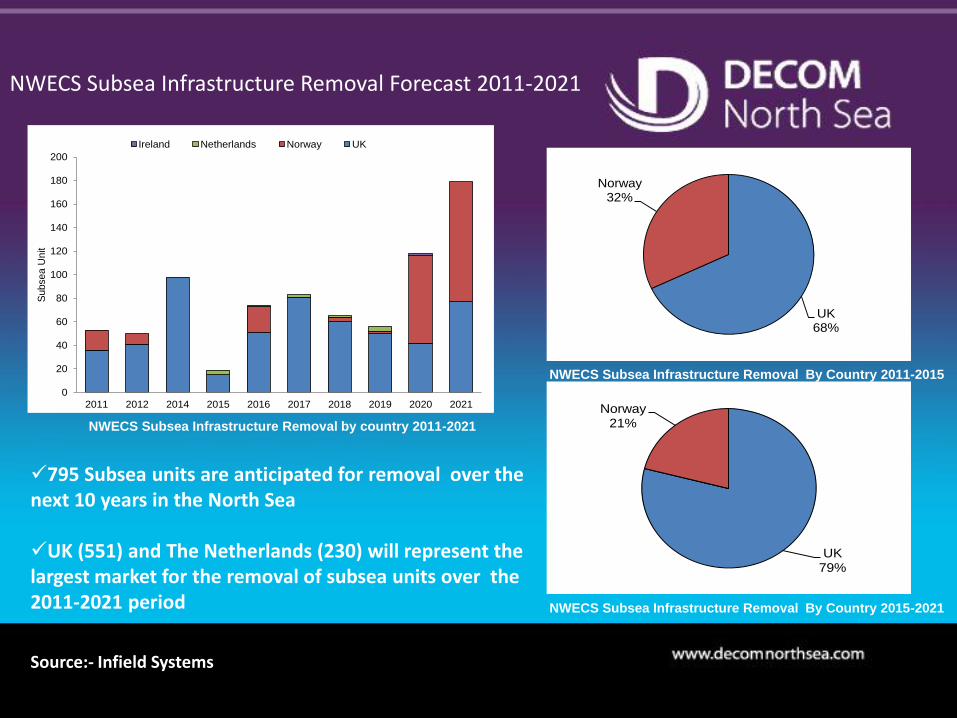

NWECS Subsea Infrastructure Removal Forecast 2011-2021

0

20

40

60

80

100

120

140

160

180

200

2011 2012 2014 2015 2016 2017 2018 2019 2020 2021

Subsea U

nit

Ireland Netherlands Norway UK

UK68%

Norway32%

NWECS Subsea Infrastructure Removal By Country 2011-2015

UK79%

Norway21%

NWECS Subsea Infrastructure Removal By Country 2015-2021

NWECS Subsea Infrastructure Removal by country 2011-2021

795 Subsea units are anticipated for removal over the next 10 years in the North Sea

UK (551) and The Netherlands (230) will represent the largest market for the removal of subsea units over the 2011-2021 period

Source:- Infield Systems

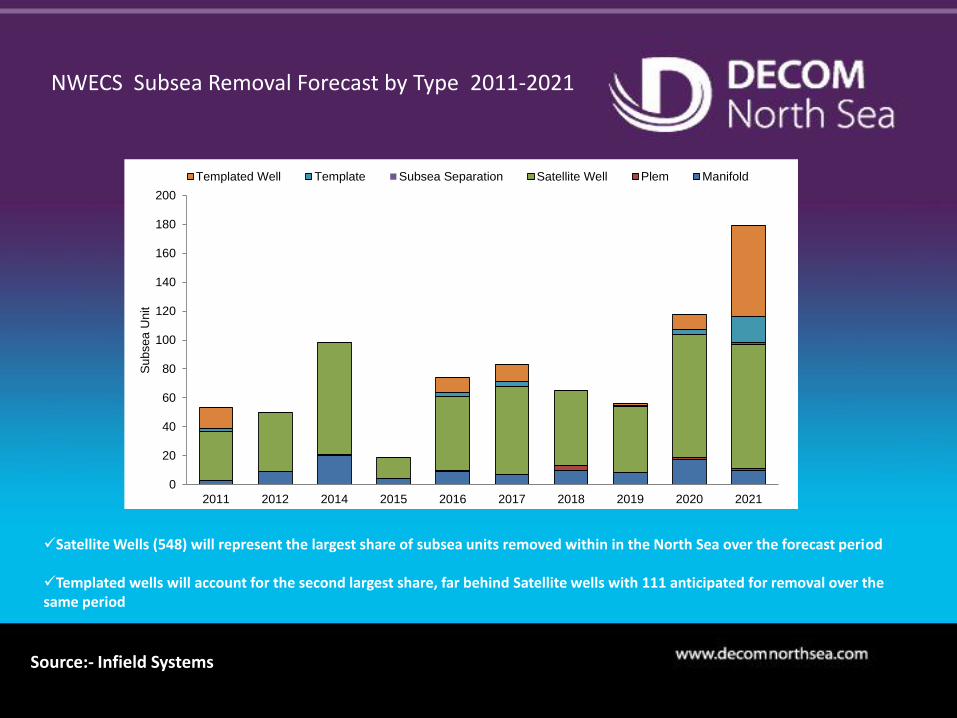

NWECS Subsea Removal Forecast by Type 2011-2021

0

20

40

60

80

100

120

140

160

180

200

2011 2012 2014 2015 2016 2017 2018 2019 2020 2021

Subsea U

nit

Templated Well Template Subsea Separation Satellite Well Plem Manifold

Satellite Wells (548) will represent the largest share of subsea units removed within in the North Sea over the forecast period

Templated wells will account for the second largest share, far behind Satellite wells with 111 anticipated for removal over the same period

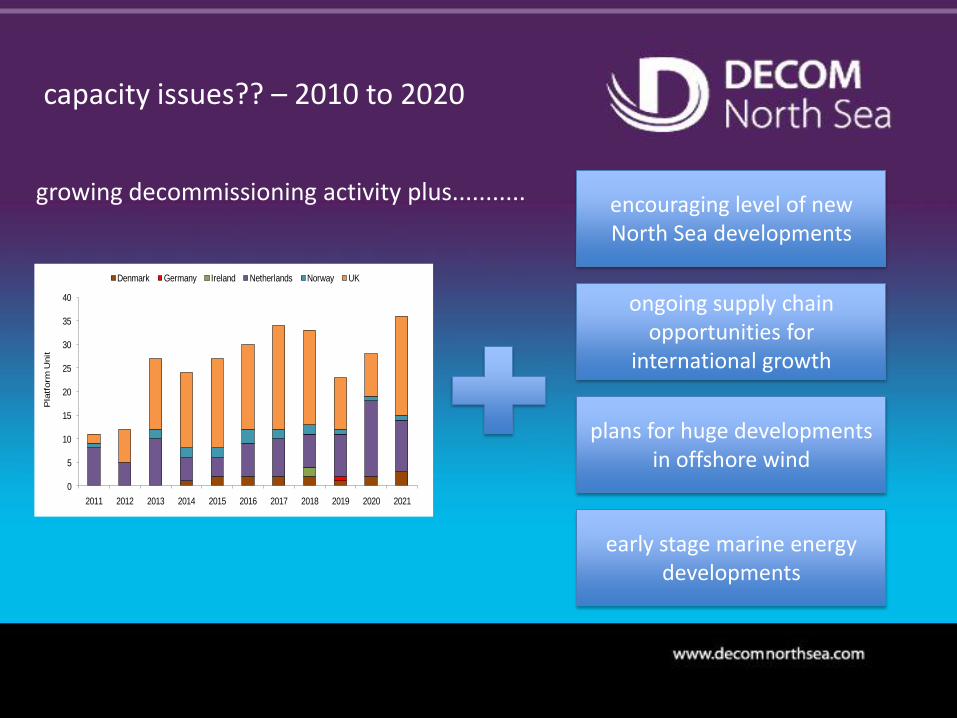

capacity issues?? – 2010 to 2020

encouraging level of new North Sea developments

ongoing supply chain opportunities for

international growth

plans for huge developments in offshore wind

early stage marine energy developments

growing decommissioning activity plus...........

0

5

10

15

20

25

30

35

40

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Denmark Germany Ireland Netherlands Norway UK

Pla

tform

Unit

opportunities for innovation

mapping of hazardous materials• identification and quantification• non-intrusive measuring techniques• continuous monitoring techniques• access and sampling techniques

well plugging and abandonment• alternatives to expensive rigs• cutting technologies – verification• barrier techniques – new materials

hydrocarbon free• improved flushing techniques• reception, storage and separation• industry standard for cleanliness

cleaning & waste management• mercury, asbestos, NORM• chemical & non-chemical techniques• qualification and verification

removal• alternative methods• jacket dismantling – near shore option• concrete mattresses• cutting technologies (incl. explosives)

legacy and monitoring• remote monitoring of remaining assets• long term leach rates of drill cuttings• accelerate degradation of footings

Brian Nixon , Chief ExecutiveSarah Hillyear, Marketing Executive

the UK decommissioning market – present & future

the role for Decom North Sea

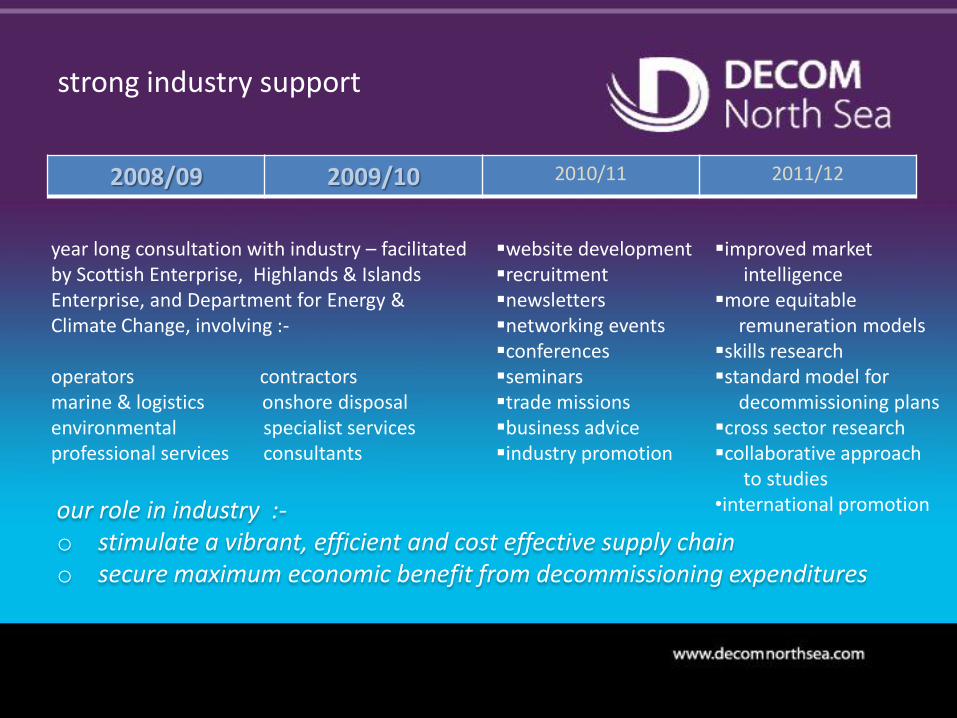

strong industry support

2008/09 2009/10 2010/11 2011/12

year long consultation with industry – facilitated by Scottish Enterprise, Highlands & Islands Enterprise, and Department for Energy & Climate Change, involving :-

operators contractorsmarine & logistics onshore disposalenvironmental specialist servicesprofessional services consultants

our role in industry :-o stimulate a vibrant, efficient and cost effective supply chaino secure maximum economic benefit from decommissioning expenditures

website developmentrecruitmentnewslettersnetworking eventsconferencesseminarstrade missionsbusiness adviceindustry promotion

improved marketintelligence

more equitable remuneration models

skills researchstandard model for

decommissioning planscross sector researchcollaborative approach

to studies•international promotion

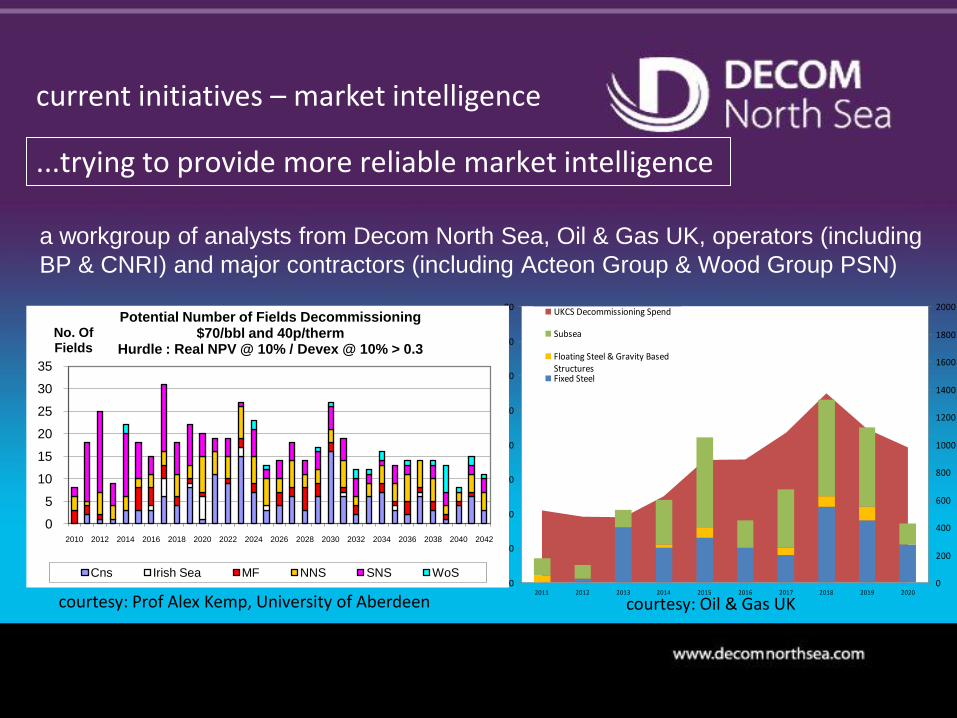

current initiatives – market intelligence

a workgroup of analysts from Decom North Sea, Oil & Gas UK, operators (including

BP & CNRI) and major contractors (including Acteon Group & Wood Group PSN)

0

10

20

30

40

50

60

70

80

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

No

. Of

Pla

tfo

rms/

Inst

alla

tio

ns

0

200

400

600

800

1000

1200

1400

1600

1800

2000

UK

CS

De

com

mis

sio

nin

g Sp

en

d (

£M

20

09

mo

ne

y)

UKCS Decommissioning Spend

Subsea

Floating Steel & Gravity BasedStructuresFixed Steel

courtesy: Prof Alex Kemp, University of Aberdeen courtesy: Oil & Gas UK

0

5

10

15

20

25

30

35

2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030 2032 2034 2036 2038 2040 2042

No. OfFields

Potential Number of Fields Decommissioning$70/bbl and 40p/therm

Hurdle : Real NPV @ 10% / Devex @ 10% > 0.3

Cns Irish Sea MF NNS SNS WoS

...trying to provide more reliable market intelligence

current initiatives – assessing skills & training needs

o industry steering group from Falck Nutec, Wood Group PSN, Tyco Fire

& Security, Mintra Training Portal and Petrofac Training

o 12-15 individual interviews with experienced professionals

o on-line survey of all Decom North Sea member companies

courtesy of Veolia / Peterson SBS

cross sector research - what can we learn ?

nuclear

first workshop in March 2011 - joint working with ITF and Scottish Enterprise

second workshop 16 November 2011 in Glasgow – joint working with Nuclear Industries Association

salvage

initial seminar in December 2010 -joint working with SUT

second seminar on 6th December 2011 in London – again with SUT

potential synergies being identified and progressed

promoting the benefits of :-o spreading investment costs over more than one projecto encouraging collaboration and joint venturingo achieving greater transfer of learning and best practiceo greater efficiency in the use of marine & lifting equipment, ports, yards etc

current initiatives - packaging of projects

Sarah Hillyear, Operations Manager

www.decomnorthsea.com