Embed Size (px)

Citation preview

INVESTOR PRESENTATION

JUNE 19, 2018

Important Disclosures

Forward-Looking Statements

This presentation contains projections and other forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities

Exchange Act of 1934. Words such as “estimate,” “project,” “will,” “may,” “anticipate,” “plan,” “intend,” “believe,” “expect,” “outlook,” “guidance,” “target,” “objective,” “forecast” or similar

expressions that convey the prospective nature of events or outcomes generally indicate forward-looking statements. These projections and statements reflect the Company’s current

views with respect to future events and financial performance as of this date. No assurances can be given, however, that these events will occur or that these projections will be

achieved, and actual results could differ materially from those projected as a result of certain factors. For a summary of events that may affect the accuracy of these projections and

forward-looking statements, see “Risk Factors” in our Form 10-K for the year ended December 31, 2017 filed with the Securities and Exchange Commission (the “SEC”). Unless legally

required, Callon does not undertake any obligation to update forward looking statements as a result of new information, future events or otherwise

SUPPLEMENTAL NON-GAAP FINANCIAL MEASURES

This presentation includes non-GAAP measures, such as Adjusted EBITDA, Adjusted Income, Adjusted Income per diluted share, Adjusted G&A and other measures identified as non-

GAAP.

Adjusted EBITDA is a supplemental non-GAAP financial measure that is used by management and external users of our financial statements, such as industry analysts, investors,

lenders and rating agencies. We define Adjusted EBITDA as net income (loss) before interest expense, income taxes, depreciation, depletion and amortization, exploration expense,

(gains) losses on derivative instruments excluding net cash receipts (payments) on settled derivative instruments and premiums paid for put options that settled during the period,

impairment of oil and natural gas properties, non-cash equity based compensation, asset retirement obligation accretion expense, other income, gains and losses from the sale of

assets and other non-cash operating items. Adjusted EBITDA is not a measure of net income as determined by United States generally accepted accounting principles (‘‘GAAP’’).

Management believes Adjusted EBITDA is useful because it allows it to more effectively evaluate our operating performance and compare the results of our operations from period to

period and against our peers without regard to our financing methods or capital structure. We exclude the items listed above from net income in arriving at Adjusted EBITDA because

these amounts can vary substantially from company to company within our industry depending upon accounting methods and book values of assets, capital structures and the method

by which the assets were acquired. Adjusted EBITDA should not be considered as an alternative to, or more meaningful than, net income as determined in accordance with GAAP or as

an indicator of our operating performance or liquidity. Certain items excluded from Adjusted EBITDA are significant components in understanding and assessing a company’s financial

performance, such as a company’s cost of capital and tax structure, as well as the historic costs of depreciable assets, none of which are components of Adjusted EBITDA. Our

presentation of Adjusted EBITDA should not be construed as an inference that our results will be unaffected by unusual or non-recurring items.

We believe that the non-GAAP measure of Adjusted income available to common shareholders (“Adjusted Income”) and Adjusted Income per diluted share are useful to investors

because they provide readers with a meaningful measure of our profitability before recording certain items whose timing or amount cannot be reasonably determined. These measures

exclude the net of tax effects of certain non-recurring items and non-cash valuation adjustments, which are detailed in the reconciliation provided below. Prior to being tax-effected and

excluded, the amounts reflected in the determination of Adjusted income and Adjusted income per diluted share below were computed in accordance with GAAP.

Adjusted general and administrative expense (“Adjusted G&A”) is a supplemental non-GAAP financial measure that excludes certain non-recurring expenses and non-cash valuation

adjustments related to incentive compensation plans. We believe that the non-GAAP measure of Adjusted G&A is useful to investors because it provides readers with a meaningful

measure of our recurring G&A expense and provides for greater comparability period-over-period. The Appendix table details all adjustments to G&A on a GAAP basis to arrive at

Adjusted G&A.

For a reconciliation of non-GAAP measures to their most directly comparable GAAP measure, please see schedules included in the Appendix.

Important Disclosures

3

METRIC CALCULATION METHODOLOGIES

$ / Net Acre (Adj.): This calculation aims to normalize transaction purchase prices for the value of the

production acquired to arrive at an implied adjusted valuation for the undeveloped acreage acquired. The

adjustment value for the acquired production is determined by applying what management believes is a

reasonable valuation multiple for the present value of a flowing equivalent barrel of production—based on

prevailing NYMEX strip pricing at the time of the acquisition—to reported sustained production rates at the

time of the acquisition. This adjusted undeveloped valuation is then divided by the net surface acreage

acquired to yield a best-efforts, “apples-to-apples” transaction metric to use as a rough guide for relative

valuation purposes.

$ / Net Delineated Hz Location (Adj.): This calculation aims to normalize transaction purchase prices for

the value of the production acquired to arrive at an implied adjusted valuation for the inventory of

undeveloped horizontal locations (net to the acquired interest), in zones, which management believes to

have been sufficiently delineated by operated and/or offsetting industry activity to date. The adjustment

value for the acquired production is determined by applying what management believes is a reasonable

valuation multiple for the present value of a flowing equivalent barrel of production—based on prevailing

NYMEX strip pricing at the time of the acquisition—to reported sustained production rates at the time of

the acquisition. It also adjusts for management’s estimates of value for midstream and water disposal

infrastructure and net acreage that does not currently carry delineated well locations. This adjusted

undeveloped valuation is then divided by the previously described net identified horizontal locations

acquired to yield a best-efforts, “apples-to-apples” transaction metric to use as a rough guide for relative

valuation purposes.

Callon Petroleum

CURRENT RIG ACTIVITY

4

1Q18 RESULTS

1. LOE figures are calculated on a two-stream basis2. Statistical measures for Market Capitalization and Enterprise Value are as of market close on June 14, 2018. Shares outstanding and net debt are represented pro forma for the recently announced Delaware Basin

acquisition and related senior notes and equity offerings3. LTM Adjusted EBITDA calculated as Callon LTM Adjusted EBITDA plus acquisition 1Q18 Adjusted EBITDA annualized. For a reconciliation of Callon’s Net Income (Loss) to Adjusted EBITDA see the Offering

Memorandum

OPERATIONAL HIGHLIGHTS

1Q18 production of 26.6 Mboe/d

Oil mix of 77%

YOY growth of 30%

Operating margin of $44.31 per Boe (~83%)

LOE per Boe $5.45 (1)

Adjusted EBITDA of $91.7MM

Successful early time results from WC A down-spacing test in Wildhorse

Strong initial production from first Spur two well pad (UWC A & LWC A)

25%+ improvement in Delaware Basin drilling efficiency

Drilling of 1st “mega-pad” at Monarch underway

85,000+ PRO FORMA NET ACRES

Pro-forma Key Statistics (2)

Shares Outstanding 227 MM

Market Capitalization $2.3 B

Net Debt $1.0 B

Enterprise Value $3.3 B

Net debt/1Q18 LQA Adj. EBITDA (3) 2.0x

Sustained, Leading Operating Margins

$28.90 $27.83 $30.34 $34.02 $32.32 $32.58

$40.51 $44.31

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

2Q 2016 3Q 2016 4Q 2016 1Q 2017 2Q 2017 3Q 2017 4Q 2017 1Q 2018

5

OPERATING MARGIN GROWTH ($/Boe)

Note: Peer set includes CDEV, CXO, EGN, FANG, LPI, MTDR, PE, PXD, REN

1Q 2018 OPERATING MARGIN PEER COMPARISON ($/Boe)

$44.31

$20

$30

$40

$50

CPE Peer #1 Peer #2 Peer #3 Peer #4 Peer #5 Peer #6 Peer #7 Peer #8 Peer #9

Peer Average $34.72 /Boe

$17/Boe$10/Boe

Midland Basin – Operational Updates

6

2nd QUARTER MIDLAND ACTIVITY SHIFT

Monarch recycling program yielding benefits

Recent wells have been able to source over 40% of

frac volumes from recycling

Model for expanded efforts across footprint

1st “mega-pad” underway at Monarch

Targeting two Lower Spraberry flow units

Completion operations recently commenced

WildHorse increasing activity during 2Q

Positive initial results from WC A down-spacing test

Remaining 2018 scheduled activity still set for 660’

spacing (monitoring down-spacing test results)

Intra-basin sand testing underway with positive early

results

Multi-well pads in Fairway area driving operational

efficiency

2Q18 primary

activity areas

7

Early results are very encouraging with ten well spacing test (Open wells) currently

exceeding cumulative oil plots for comparable two well pads (eight well spacing)

Wildhorse WC A Down-Spacing Test

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

Da

y 1

Da

y 1

1

Da

y 2

1

Da

y 3

1

Da

y 4

1

Da

y 5

1

Da

y 6

1

Da

y 7

1

Da

y 8

1

Da

y 9

1

Day 1

01

Day 1

11

Day 1

21

Day 1

31

Day 1

41

Day 1

51

Day 1

61

Day 1

71

Day 1

81

Day 1

91

Day 2

01

Day 2

11

Day 2

21

Cu

mu

lative

Oil

(Bb

l)

OPEN A2 #1AH OPEN A3 #3AH PLAYERS #1AH

PLAYERS #2AH WYNDHAM #1AH WYNDHAM #2AH

Delaware Basin – Ramping Activity

8

SPUR AREA IN PROGRAM DEVELOPMENT MODE

Strong initial results from Rendezvous twowell pad (Upper and Lower WC A)

Improved efficiency in drilling as activityincreases

Goodnight Midstream pipeline projectedonline in 3Q, recycling projects movingforward

Upcoming delineation of Wolfcamp C and2nd Bone Spring Shale

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Day 50Day 40Day 30Day 20Day 10

Cum

ula

tive O

il (B

bls

)

Rendezvous Avg Cum Oil Prior 4 Well Avg Cum Oil

Rendezvous Pad

Goodnight Midstream

water pipeline

Improved Delaware Drilling Efficiency

9

AVERAGE DRILLING FOOTAGE PER DAY

1st 2nd 3rd 4th 5th 6th OffsetOperatorAverage

CPEAverage

LatestCPE Well

18%

increase

8%

increase

Callon Operated Delaware Wells

Note: Offset Operator average is composed of 14 recent peer results in the southeast Delaware basin targeting the Wolfcamp

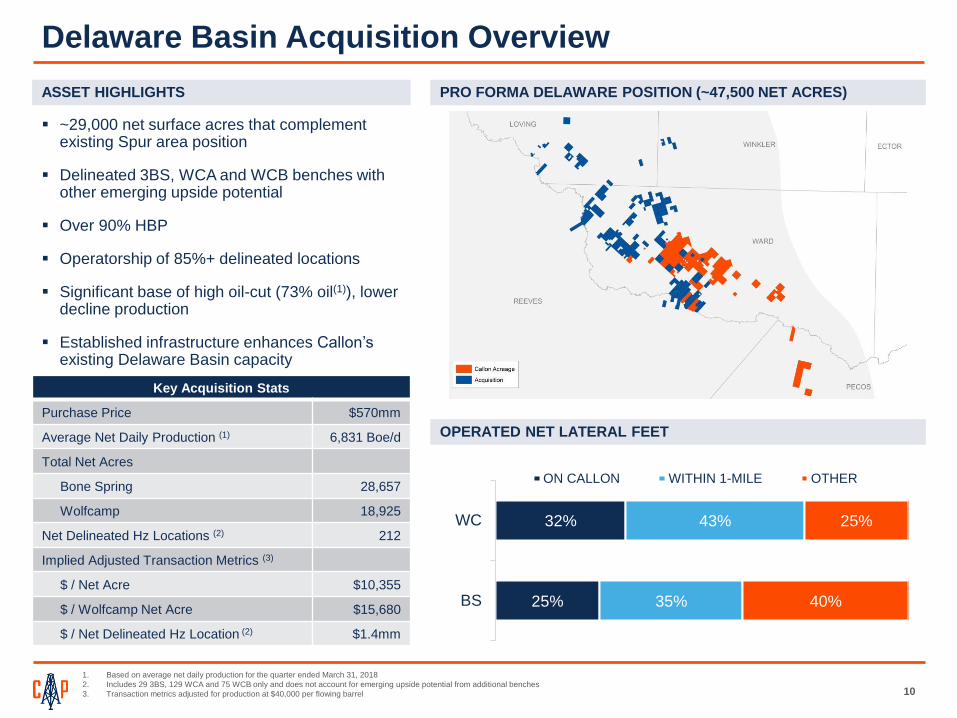

PRO FORMA DELAWARE POSITION (~47,500 NET ACRES)

Delaware Basin Acquisition Overview

~29,000 net surface acres that complement existing Spur area position

Delineated 3BS, WCA and WCB benches with other emerging upside potential

Over 90% HBP

Operatorship of 85%+ delineated locations

Significant base of high oil-cut (73% oil(1)), lower decline production

Established infrastructure enhances Callon’sexisting Delaware Basin capacity

Key Acquisition Stats

Purchase Price $570mm

Average Net Daily Production (1) 6,831 Boe/d

Total Net Acres

Bone Spring 28,657

Wolfcamp 18,925

Net Delineated Hz Locations (2) 212

Implied Adjusted Transaction Metrics (3)

$ / Net Acre $10,355

$ / Wolfcamp Net Acre $15,680

$ / Net Delineated Hz Location (2) $1.4mm

1. Based on average net daily production for the quarter ended March 31, 2018

2. Includes 29 3BS, 129 WCA and 75 WCB only and does not account for emerging upside potential from additional benches

3. Transaction metrics adjusted for production at $40,000 per flowing barrel

ASSET HIGHLIGHTS

10

25%

32%

35%

43%

40%

25%

BS

WC

ON CALLON WITHIN 1-MILE OTHER

OPERATED NET LATERAL FEET

December 2016 May 2018

Building Scale in the Core of the Delaware

11

Highly focused additions have enhanced our core operated position

Reeves

Ward

Pecos

Loving Winkler

Reeves

Ward

Pecos

Loving Winkler

Reeves

Ward

Pecos

Loving Winkler

December 2017

Bolt-On Acreage

Acquisitions

Acquired Assets from

Ameredev

~16,100 Total Net Acres

Pro Forma Delaware

Acreage Position

~47,500 Total Net Acres

Callon May 2018

Acquisition

Callon Dec 2016

2017 Bolt-OnsCallon Dec 2016

Strategic Acquisition Complements Our Strategy

Unique Bolt-On Opportunity

Contiguous

Acreage Benefits

1. Acquisition portion of pro forma 1Q18 Adjusted EBITDA is calculated as follows: midpoint of revenue range less midpoint of direct operating expenses range of seller for 1Q 2018 as disclosed in the Offering

Memorandum

Bolsters position in oil rich, over-pressured core of Delaware Basin

Land / ownership depth synergies unlock significant value

Benefits from existing geologic and technical data sets

Increased working interest and extended laterals drive near-term NAV benefits

Enhances optionality for multi-well pad development

Leverage of existing infrastructure on both footprints

1212

Compelling

Corporate Value

Proposition

Near-term corporate returns generated from established production base

Accretive to CF per DAS and ROCE

Additional organic upside from emerging target zones

13

Expansion in the Core of the Delaware Basin

Loving

Winkler

Reeves

Ward

Pecos

Loving Winkler

Reeves

Ward

Pecos

Expands operating

position in the core of the

Southern Delaware Basin

Primary Wolfcamp

horizons contain

attractive combination of

reservoir properties

High OOIP

High reservoir pressure

High % oil

Comprehensive 3D

seismic coverage across

pro forma acreage

Improves placement of

lateral in zone for more

effective completions

Advantage for delineation

of emerging zones

Core operating area

features structurally quiet

basin floor with minimal

faulting through position

WOLFCAMP TOTAL OOIP (MMBO/SEC)

3D SEISMIC COVERAGEWOLFCAMP A & B (% OIL)

WOLFCAMP RESERVOIR PRESSURECORE ACREAGE POSITION

High

Low

Wolfc

am

p

Tota

l OO

IP

(Mm

bo/s

ec)

200

0

Loving Winkler

Reeves

Ward

Pecos

Loving Winkler

Reeves

Ward

Pecos

High

Low

Wolfc

am

p

Perc

ent O

il

100%

0%

3D Seismic Coverage

High

Low

Wolfc

am

p

Reserv

oir

Pre

ssure

(psi)

10,000

2,000

Corbets 34 149 #02WA Prior operator “Kitchen Sink

Design” high proppant/fluid

loading and peak cluster/stage

density

Saratoga #07LA Testing lower cost limit 30%

lower proppant load, 15% less

fluid load, 40% lower

stage/cluster density

Sleeping Indian #01LA Cost / benefit optimization

lower proppant/fluid load offset

by 50% increase in cluster

density and use of frac tech

Rendezvous Pad Multi-well pad application

Upper A / Lower A co-

development

Seller WCA Hz PDPs

Wolfcamp A Design & Performance Optimization

1

1. All wells normalized to 7,500’ lateral length

2

3

0

20

40

60

80

100

120

140

160

180

0 30 60 90 120 150 180 210 240 270 300 330 360

Cum

ula

tive O

il P

roduction (

MB

O)

–N

orm

aliz

ed t

o 7

,500’

Days on Production

CORBETS 34 149 #02WA SARATOGA A1 #07LA

SLEEPING INDIAN A1 #01LA RENDEZVOUS A1 #01LA & #09UA

SELLER WCA AVG (9 wells)

4

1

2

3

4

S

Demonstrated performance improvement through optimized landing zone and completion design

S

COMPLETION DESIGN EVOLUTION

14

Benefits of Significant Existing Infrastructure

FACILITIES HIGHLIGHTS

Single Well Pad

INTEGRATED FACILITIES FOOTPRINT SUPPORTS EFFICIENT PAD DEVELOPMENT

Four operated SWD wells with 95 Mbbl/d of current injection capacity

Supporting water gathering lines

Full electrification across acquired asset base

Increased scale enhances recycling initiative benefiting capital and LOE

PAD DEVELOPMENT SAVINGS

Integration of acquired infrastructure into combined footprint provides

ample capacity to facilitate cost-efficient, multi-well pad development

15

Upside – 2nd Bone Spring Shale & Wolfcamp C

16

A

B

C

D

E

F

G

H

I

J

K

L

12

3

4

5

Reeves

Ward

Pecos

Loving Winkler

Callon plans to test upside horizons in 2018 (2nd Bone Spring and Wolfcamp C)

Industry delineation continues beyond primary horizons (Wolfcamp A, Wolfcamp B and 3rd Bone Spring)

State 5913A GGH 2H

Jagged Peak

IP24/1,000’: 177 Boe/d

Spud Date: 3/25/2017

UL Fourmile 1H

Felix Energy

IP24/1,000’: 160 Boe/d

Spud Date: 3/25/2017

UL Mayflower 42-18 3H

Felix Energy

IP24/1,000’: 194 Boe/d

Spud Date: 7/6/2017

County Line 18B-C2 1H

Jagged Peak

IP30/1,000’: 170 Boe/d

Spud Date: 9/15/2017

Whiskey River 7374B 1H

Jagged Peak

IP24/1,000’: 298 Boe/d

Spud Date: 9/17/2017

Link 1-32 Unit 4H

Anadarko

IP24/1,000’: 166 Boe/d

Spud Date: 3/25/2017

Elmer 33-67 801H

Energen

IP24/1,000’: 121 Boe/d

Spud Date: 3/25/2017

Whiskey River 7374A 1H

Jagged Peak

IP24/1,000’: 290 Boe/d

Spud Date: 9/15/2017

McIntyre State 40 1H

Diamondback

IP30/1,000’: 85 Boe/d

Spud Date: 3/15/2016

County Line 18A-C2 1H

Jagged Peak

IP30/1,000’: 180 Boe/d

Spud Date: 3/25/2017

Arno 78 121H

Matador

IP30/1,000’: 144 Boe/d

Spud Date: 1/15/2017

Dorothy White 82 124H

Matador

IP30/1,000’: 140 Boe/d

Spud Date: 3/8/2017

UL 20 Sugarloaf 1H

Forge/Oasis

IP24/1,000’: 112 Boe/d

Spud Date: 8/15/2017

Morrison H B 73H

Oxy

IP24/1,000’: 195 Boe/d

Spud Date: 10/17/2016

Shavano 38-28 1H

Felix Energy

IP30/1,000’: Pending

Spud Date: 12/14/2017

Collie A East N 63H

Oxy

IP30/1,000’: 93 Boe/d

Spud Date: 4/26/2017

Townsen 66 1

Carrizo

IP30/1,000’: 120 Boe/d

Spud Date: 2/11/2017

A

B

C

D

E

F

G

H

I

J

K

L

1 2 3 4 5

2nd Bone Spring

Wolfcamp C

Estimated 172 total net

upside locations targeting

the 2BS and WCC

Value Enhancing Financial Impact

Transaction is a measured approach to growth that is immediately accretive to debt-adjusted per

share metrics, including cash flow and production, and returns on capital employed

Material current cash flow contribution from significant PDP base

Provides meaningful optionality for planned capital allocation, but limited HBP requirements supports a measured

approach to development

Accelerates path to free cash flow generation

Completed acquisition financing preserves liquidity and maintains strong balance sheet and

leverage metrics

Pro forma net debt / 1Q’18 annualized Adjusted EBITDA of 2.0x (1)

Expected liquidity benefits from planned borrowing base redetermination

BENEFICIAL FINANCIAL IMPACTS

17

1. Acquisition portion of pro forma 1Q18 Adjusted EBITDA is calculated as follows: midpoint of revenue range less midpoint of direct operating expenses range and financing transactions

2. Based on average net daily production for the quarter ended March 31, 2018

3. This reflects underwriters exercising shoe in full for the equity issuance closed on May 30th, 2018

0%

20%

40%

60%

80%

SharesOutstanding

1Q'18Net Production

Net Acres Gross Hz Locations

% Incre

ase

+67%

+26%

ACQUISITION DRIVES SIGNIFICANT VALUE ENHANCEMENT

+13%

+51%

Current 26.6 Mboe/d ~56,900 net acres 1,545 gross Hz locations

Pro Forma 227.5 MM (3) 33.4 Mboe/d ~86,100 net acres 2,581 gross Hz locations

(2)

Financial Positioning

Long-term acquisition financing completed

$299MM equity offering

$400MM 8NC3 senior unsecured notes

Leverage statistics preserved and liquidity

position enhanced

Borrowing base redetermination to be

completed at closing of acquisition

18

PRO FORMA CAPITALIZATION ($MM)

1Q18 Adj. Pro Forma

Cash $18 37 $55

Credit facility 75 (75) 0

Senior notes due 2024 600 600

New senior notes 0 400 400

Total debt $675 $1,000

Preferred stock 73 73

Stockholders’ equity 1,838 289 2,127

Total capitalization $2,586 $3,200

Credit statistics

Net debt / LTM Adj. EBITDA(1) 2.2x 2.3x

Net debt / LQA Adj. EBITDA(2) 1.8x 2.0x

Liquidity

Commitment amount $650 $650

Less: drawn (75) 0

Plus: cash 18 55

Total liquidity $593 $705

1. LTM Adjusted EBITDA calculated as Callon LTM Adjusted EBITDA plus acquisition 1Q18 Adjusted EBITDA annualized. For a reconcil iation of Callon’s Net Income (Loss) to Adjusted EBITDA see the

Appendix

2. Acquisition portion of pro forma 1Q18 Adjusted EBITDA is calculated as follows: midpoint of revenue range less midpoint of di rect operating expenses range of seller for 1Q 2018

3. Based off current consensus production estimates per FACTSET as of June 14, 2018

RISK MANAGEMENT (3)

HIGHLIGHTS

70%

40%45%

30%

20%

2H18 2019 2020

% o

f C

onse

nsu

s O

il

NYMEX WTI Midland-Cushing

Physical Oil Flow Assurance

~ 90% on pipeline/gathering systems (pro-forma) with firm transport

Long-term firm sales agreements (NYMEX-based) with multiple counterparties with FT out of the Permian

Acquired acreage under long-term firm sales agreements

Enhanced marketing options with larger pro-forma production base

19

OFFTAKE

1. Hedge contracts as of June 14, 2018

2. Peers included in oil price realization chart : CDEV, CXO, EGN, FANG, JAG, LPI, PE, RSPP

OIL TRANSPORT EVOLUTION ($/Bbl) 1Q18 OIL PRICE REALIZATIONS2 ($/Bbl)

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$/B

bl

Trucking On Pipe

55% Current

Production

Pipe takeaway

Medallion Firm

Transport

Purchasers

Shell, BP,

Trafigura, Rio

Energy, Delek

Enterprise / Plains Firm Sales 45% Current

Production

Enterprise Firm Sales Acquired

Production

$62.28

$60.00

$60.50

$61.00

$61.50

$62.00

$62.50

CPE Peer 1 Peer 2 Peer 3 Peer 4 Peer 5 Peer 6 Peer 7 Peer 8

Peer Average: $61.57

Portfolio Approach Provides Broad Optionality

Firm sales volumes are covered by buyer held

FT agreements for transport out of the Permian

basin

Diversified purchaser portfolio (Plains,

Enterprise, Shell, BP, Trafigura, Delek, etc.)

with multi-year term agreements covering up

to 60KBopd

More than 90% of oil on pipe (pro-forma) with

additional tie-ins pending for Medallion system

Primary transport rights on Medallion

equivalent to other “preferred shippers”

Multi-year firm gathering commitments from

three primary providers (Enterprise, Plains,

Medallion) with ratable increases covered as

volumes grow

Sales are linked to NYMEX based pricing

mechanisms

20

Oil Marketing Arrangements

1) Projected oil volumes are annual exit rate figures for legacy CPE properties

Firm Transport on Medallion System Provides Broad Options for Delivery

Buyer 1 Buyer 2 Buyer 3 Buyer 4 Buyer 5 Buyer 6 Buyer 7

Up to

14 Mbopd

Up to

10 Mbopd

Up to

10 Mbopd

Up to

8 Mbopd

Up to

6.7 Mbopd

Up to

6 Mbopd

Up to

3 Mbopd

Flows on FT Flows on FT Flows on FT Flows on FT Flows on FT Flows on FTFT or local

refinery sale

Nymex

based pricing

Nymex

based pricing

Nymex

based pricing

Nymex

based pricing

Nymex

based pricing

Nymex

based pricing

Nymex

based pricing

Multi-year dedications with WTG, Enlink,

Targa, and Brazos across the basin

Delaware purchaser flows direct connect to El

Paso 1600 line with additional capacity

pending on Whitewater line

Gas Marketing Arrangements

• Longhorn

• Cactus II

(Pending)

• Grey Oak

(pending)

Centurion

• Centurion

• PE II

• WTG

• Bridgetex

Midland to

Sealy

• >60% of CPE(1) oil to flow on Medallion by YE 18

• Firm delivery to all market off-take points

• Capacity increasing with production growth

Basin

Medallion pipeline

Medallion offtake points

Callon Pure Play Peers <$10 Bn Market Cap

21

Source: Latest public investor presentations and 10-Q filing for the quarter ended March 31, 2018

Note: Operating Margin defined as unhedged sales revenue less lease operating expenses, gathering and transportation expenses and production taxes

Lea

Pecos

Terrell

Brewster

Gaines

Upton

Lynn

Crockett

Reeves

Terry

Andrews

Ector

Ward

Martin

ReaganCrane

MidlandWinkler

Dawson

Yoakum

Borden

Loving

Howard

Glasscock

Val Verde

Hockley LubbockCochran

NM TX

Lea

Pecos

Terrell

Brewster

Gaines

Upton

Lynn

Crockett

Reeves

Terry

Andrews

Ector

Ward

Martin

Reagan

Crane

MidlandWinkler

Dawson

Yoakum

Borden

Loving

Howard

Glasscock

Val Verde

Hockley LubbockCochran

NM TX

Callon has amassed a highly economic acreage position ripe for full-scale development

Callon 1Q’18 Pro Forma:

Net acres: ~86,100

Net Mbo/d: 25.6

Op. margin ($/boe): $43.92

Jagged Peak 1Q’18:

Net acres: ~77,700

Net Mbo/d: 21.9

Op. margin ($/boe): $44.90

Centennial 1Q’18:

Net acres: ~80,100

Net Mbo/d: 31.6

Op. margin ($/boe): $35.28

RSP Permian 1Q’18:

Net acres: ~91,900

Net Mbo/d: 45.3

Op. margin ($/boe): $40.34

Jagged Peak

Lea

Pecos

Terrell

Brewster

Gaines

Upton

Lynn

Crockett

Reeves

Terry

Andrews

Ector

Ward

Martin

ReaganCrane

MidlandWinkler

Dawson

Yoakum

Borden

Loving

Howard

Glasscock

Val Verde

Hockley LubbockCochran

NM TX

Centennial RSP Permian

Lea

Pecos

Terrell

Brewster

Gaines

Upton

Lynn

Crockett

Reeves

Terry

Andrews

Ector

Ward

Martin

ReaganCrane

MidlandWinkler

Dawson

Yoakum

Borden

Loving

Howard

Glasscock

Val Verde

Hockley LubbockCochran

NM TX

Callon May 2018

Acquisition

APPENDIX

23

Between company owned and third party committed volumes, Callon has in excess of 400,000 bbl/d of water disposal capacity (excluding pending Goodnight project of 80,000 bbl/d)

Average CPE water disposal during February was ~90K Bwpd across the entire Permian footprint (25% of controlled capacity)

Water Disposal as a Competitive Advantage

WATER MANAGEMENT INITIATIVES

Strategic Water Handling Agreements

• Gravity – water sourcing (Wildhorse

and Spur areas)

• Goodnight Midstream – Spur disposal

pipeline to the CBP

Recycling Efforts

• Underway at Monarch, utilized on

recently fracked wells +40% of

sourced volumes

• Spur build-out progressing, goal of

sourcing 50% of frac water volumes

from recycling by year end

Incremental Capacity in Key Areas

• New Deep Ellenburger wells projected

online at Ranger and Wildhorse

during Q2 supplying significant

incremental capacity

COMPANY OWNED AND OPERATED DISPOSAL CAPACITY BY AREA

~60,000 bwpd

~50,000 bwpd

~100,000 bwpd

~45,000 bwpd

Current Guidance Summary (Unadjusted for Acquistion)

24

1. Excludes stock-based compensation and corporate depreciation and amortization. See the Non-GAAP related disclosures in the Appendix

2. Excludes certain non-recurring expenses and non-cash valuation adjustments. See the non-GAAP related disclosures in the Appendix

3. All cash interest expense anticipated to be capitalized

4. Includes drilling, completions, facilities, seismic, land and other items. Excludes capitalized expenses. Net of infrastructure monetizations of $20 million

FY18

Guidance

Total production (MBoepd) 29.5 – 32.0

Oil production 77%

Income statement expenses (per BOE)

LOE, including workovers $5.25 - $6.25

Production taxes, including ad valorem

(% of unhedged revenues)6%

Adjusted G&A: cash component (1) $1.75 - $2.50

Adjusted G&A: non-cash component (2) $0.50 - $1.00

Cash interest expense (3) $0.00

Statutory income tax rate 22%

Capital expenditures ($MM, accrual basis)

Total operational capital (4) $500 - $540

Capitalized expenses $60 - $70

Net operated horizontal wells placed on production 43 – 46

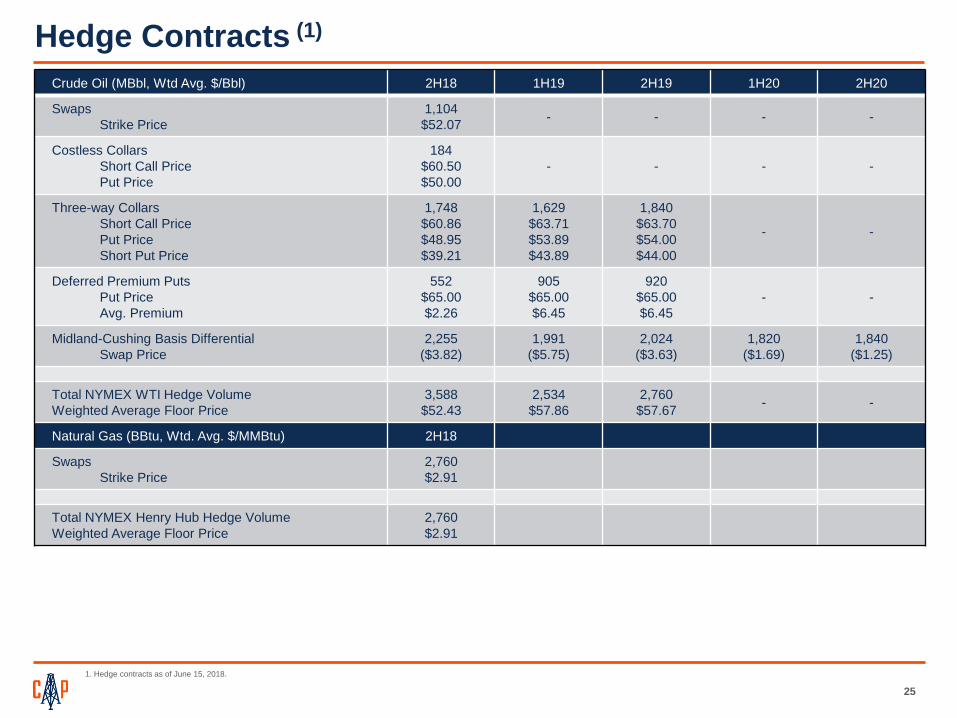

Hedge Contracts (1)

25

1. Hedge contracts as of June 15, 2018.

Crude Oil (MBbl, Wtd Avg. $/Bbl) 2H18 1H19 2H19 1H20 2H20

Swaps

Strike Price

1,104

$52.07- - - -

Costless Collars

Short Call Price

Put Price

184

$60.50

$50.00

- - - -

Three-way Collars

Short Call Price

Put Price

Short Put Price

1,748

$60.86

$48.95

$39.21

1,629

$63.71

$53.89

$43.89

1,840

$63.70

$54.00

$44.00

- -

Deferred Premium Puts

Put Price

Avg. Premium

552

$65.00

$2.26

905

$65.00

$6.45

920

$65.00

$6.45

- -

Midland-Cushing Basis Differential

Swap Price

2,255

($3.82)

1,991

($5.75)

2,024

($3.63)

1,820

($1.69)

1,840

($1.25)

Total NYMEX WTI Hedge Volume

Weighted Average Floor Price

3,588

$52.43

2,534

$57.86

2,760

$57.67- -

Natural Gas (BBtu, Wtd. Avg. $/MMBtu) 2H18

Swaps

Strike Price

2,760

$2.91

Total NYMEX Henry Hub Hedge Volume

Weighted Average Floor Price

2,760

$2.91

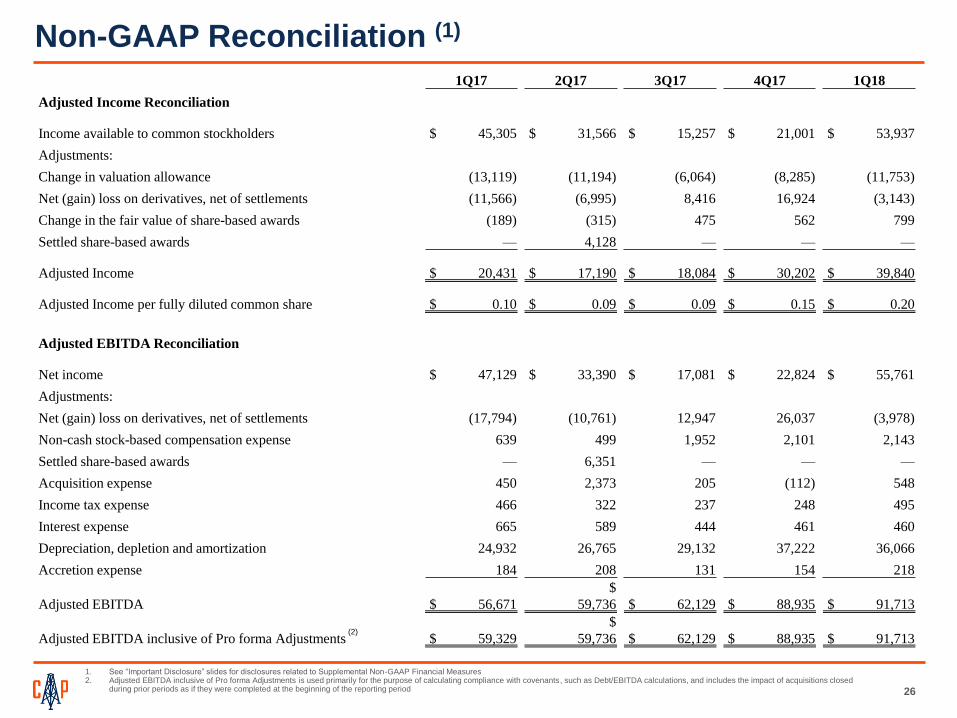

1Q17 2Q17 3Q17 4Q17 1Q18

Adjusted Income Reconciliation

Income available to common stockholders $ 45,305 $ 31,566 $ 15,257 $ 21,001 $ 53,937

Adjustments:

Change in valuation allowance (13,119) (11,194) (6,064) (8,285) (11,753)

Net (gain) loss on derivatives, net of settlements (11,566) (6,995) 8,416 16,924 (3,143)

Change in the fair value of share-based awards (189) (315) 475 562 799

Settled share-based awards — 4,128 — — —

Adjusted Income $ 20,431 $ 17,190 $ 18,084 $ 30,202 $ 39,840

Adjusted Income per fully diluted common share $ 0.10 $ 0.09 $ 0.09 $ 0.15 $ 0.20

Adjusted EBITDA Reconciliation

Net income $ 47,129 $ 33,390 $ 17,081 $ 22,824 $ 55,761

Adjustments:

Net (gain) loss on derivatives, net of settlements (17,794) (10,761) 12,947 26,037 (3,978)

Non-cash stock-based compensation expense 639 499 1,952 2,101 2,143

Settled share-based awards — 6,351 — — —

Acquisition expense 450 2,373 205 (112) 548

Income tax expense 466 322 237 248 495

Interest expense 665 589 444 461 460

Depreciation, depletion and amortization 24,932 26,765 29,132 37,222 36,066

Accretion expense 184 208 131 154 218

Adjusted EBITDA $ 56,671

$

59,736 $ 62,129 $ 88,935 $ 91,713

Adjusted EBITDA inclusive of Pro forma Adjustments $ 59,329

$

59,736 $ 62,129 $ 88,935 $ 91,713

Non-GAAP Reconciliation (1)

26

1. See “Important Disclosure” slides for disclosures related to Supplemental Non-GAAP Financial Measures2. Adjusted EBITDA inclusive of Pro forma Adjustments is used primarily for the purpose of calculating compliance with covenants, such as Debt/EBITDA calculations, and includes the impact of acquisitions closed

during prior periods as if they were completed at the beginning of the reporting period

(2)

1Q17 2Q17 3Q17 4Q17 1Q18

Adjusted G&A Reconciliation

Total G&A expense $ 5,206 $ 6,430 $ 7,259 $ 8,173 $ 8,769

Adjustments:

Less: Early retirement expenses — (444) — — —

Less: Early retirement expenses related to share-based compensation — (81) — — —

Less: Change in the fair value of liability share-based awards (non-cash) (307) 567 (731) (844) (991)

Adjusted G&A – total 5,513 6,472 6,528 7,329 7,778

Less: Restricted stock share-based compensation (non-cash) (921) (966) (1,198) (1,202) (1,105)

Less: Corporate depreciation & amortization (non-cash) (121) (114) (146) (125) (124)

Adjusted G&A – cash component $ 4,471 $ 5,392 $ 5,184 $ 6,002 $ 6,549

Adjusted Total Revenue Reconciliation

Oil revenue $ 72,008 $ 72,885 $ 73,349 $ 104,132 $ 115,286

Natural gas revenue 9,355 9,398 11,265 14,081 12,154

Total revenue 81,363 82,283 84,614 118,213 127,440

Impact of cash-settled derivatives (2,491) (267) (1,214) (4,501) (8,459)

Adjusted Total Revenue $ 78,872 $ 82,016 $ 83,400 $ 113,712 $ 118,981

Total Production (Mboe) 1,838 2,021 2,074 2,439 2,391

Adjusted Total Revenue per Boe $ 42.91 $ 40.58 $ 40.21 $ 46.62 $ 49.76

Discretionary Cash Flow Reconciliation

Net cash provided by operating activities $ 52,684 $ 43,128 $ 53,893 $ 80,186 $ 92,215

Changes in working capital (5,890) 8,968 7,777 8,642 (4,512)

Payments to settle asset retirement obligations 765 816 250 216 366

Payments to settle vested liability share-based awards 8,662 4,511 — — 3,089

Discretionary cash flow $ 56,221 $ 57,423 $ 61,920 $ 89,044 $ 91,158

Discretionary cash flow per diluted share $ 0.28 $ 0.28 $ 0.31 $ 0.44 $ 0.45

Non-GAAP Reconciliation (1)

27

1. See “Important Disclosure” slides for disclosures related to Supplemental Non-GAAP Financial Measures