Embed Size (px)

Citation preview

Trinidad y Tobago

Vikash Supersad Sao Paulo, Brazil, November 6, 2013

Gobernanza del transporte: Integración logística para un uso más sostenible de recursos naturales en América latina y el Caribe

Proyecto CEPAL / UNDA: Integración logística para una explotación más sostenible de los recursos naturales en América Latina y el Caribe

Bienvenido al Caribe!

Source: European Parliamentary

Research Service

• Comprises many countries, with various foreign territories with small populations

• There are multiple languages and great cultural diversity

• But most of all – the Caribbean is Logistically Complex!

0

10

20

30

40

50

60

US

cen

ts /

Kw

h

Electricity Tariff (¢/Kwh)

LAC

US

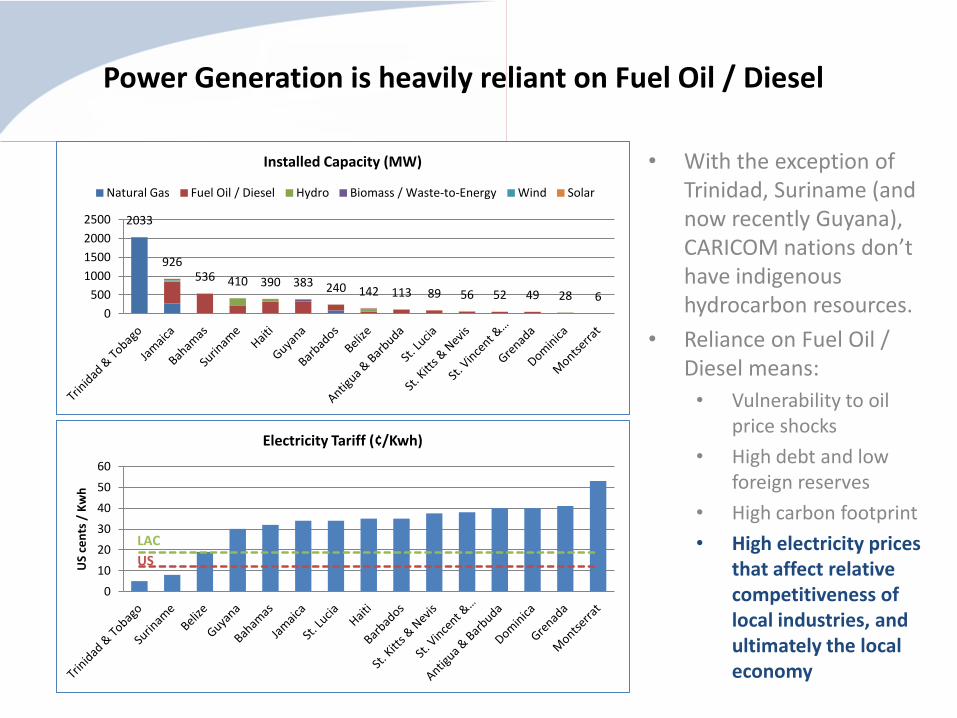

Power Generation is heavily reliant on Fuel Oil / Diesel

• With the exception of Trinidad, Suriname (and now recently Guyana), CARICOM nations don’t have indigenous hydrocarbon resources.

• Reliance on Fuel Oil / Diesel means:

• Vulnerability to oil price shocks

• High debt and low foreign reserves

• High carbon footprint

• High electricity prices that affect relative competitiveness of local industries, and ultimately the local economy

2033

926 536 410 390 383 240 142 113 89 56 52 49 28 6

0

500

1000

1500

2000

2500

Installed Capacity (MW)

Natural Gas Fuel Oil / Diesel Hydro Biomass / Waste-to-Energy Wind Solar

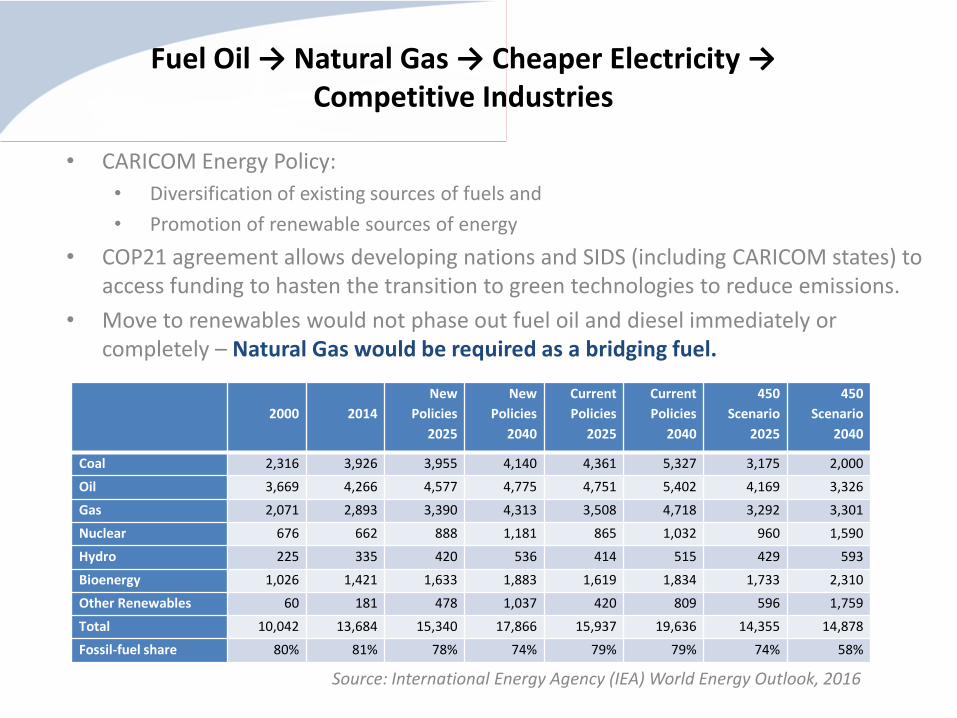

Fuel Oil → Natural Gas → Cheaper Electricity → Competitive Industries

• CARICOM Energy Policy:

• Diversification of existing sources of fuels and

• Promotion of renewable sources of energy

• COP21 agreement allows developing nations and SIDS (including CARICOM states) to access funding to hasten the transition to green technologies to reduce emissions.

• Move to renewables would not phase out fuel oil and diesel immediately or completely – Natural Gas would be required as a bridging fuel.

2000

2014

New

Policies

2025

New

Policies

2040

Current

Policies

2025

Current

Policies

2040

450

Scenario

2025

450

Scenario

2040

Coal 2,316 3,926 3,955 4,140 4,361 5,327 3,175 2,000

Oil 3,669 4,266 4,577 4,775 4,751 5,402 4,169 3,326

Gas 2,071 2,893 3,390 4,313 3,508 4,718 3,292 3,301

Nuclear 676 662 888 1,181 865 1,032 960 1,590

Hydro 225 335 420 536 414 515 429 593

Bioenergy 1,026 1,421 1,633 1,883 1,619 1,834 1,733 2,310

Other Renewables 60 181 478 1,037 420 809 596 1,759

Total 10,042 13,684 15,340 17,866 15,937 19,636 14,355 14,878

Fossil-fuel share 80% 81% 78% 74% 79% 79% 74% 58%

Source: International Energy Agency (IEA) World Energy Outlook, 2016

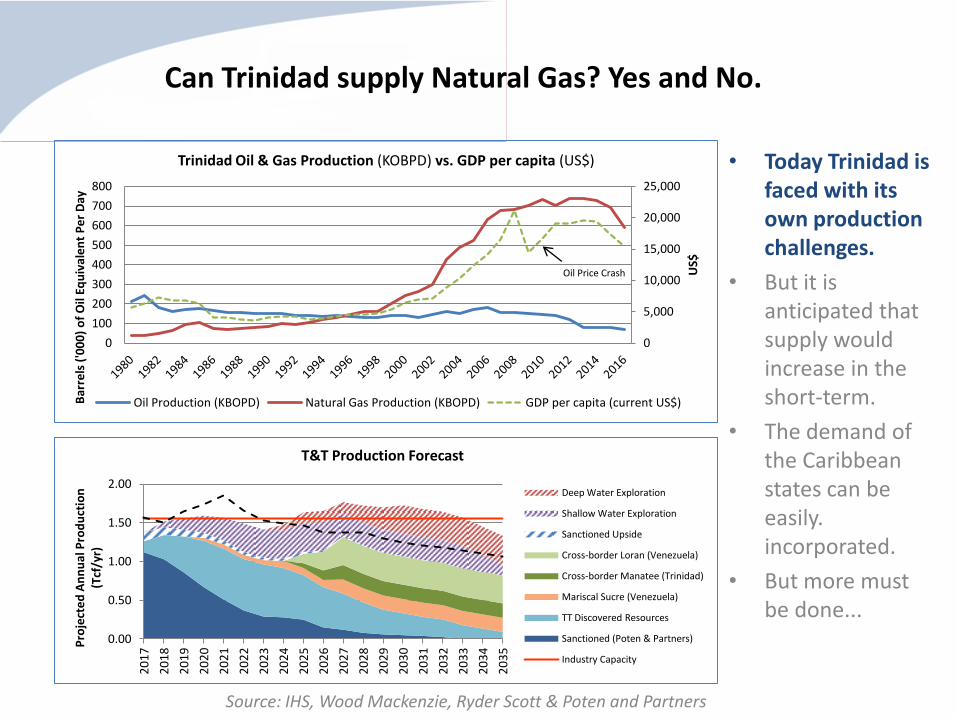

Can Trinidad supply Natural Gas? Yes and No.

• Today Trinidad is faced with its own production challenges.

• But it is anticipated that supply would increase in the short-term.

• The demand of the Caribbean states can be easily. incorporated.

• But more must be done...

0

5,000

10,000

15,000

20,000

25,000

0

100

200

300

400

500

600

700

800

US$

Bar

rels

('0

00

) o

f O

il Eq

uiv

ale

nt

Pe

r D

ay

Trinidad Oil & Gas Production (KOBPD) vs. GDP per capita (US$)

Oil Production (KBOPD) Natural Gas Production (KBOPD) GDP per capita (current US$)

Oil Price Crash

0.00

0.50

1.00

1.50

2.00

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

Pro

ject

ed

An

nu

al P

rod

uct

ion

(T

cf/y

r)

T&T Production Forecast

Deep Water Exploration

Shallow Water Exploration

Sanctioned Upside

Cross-border Loran (Venezuela)

Cross-border Manatee (Trinidad)

Mariscal Sucre (Venezuela)

TT Discovered Resources

Sanctioned (Poten & Partners)

Industry Capacity

Source: IHS, Wood Mackenzie, Ryder Scott & Poten and Partners

What is happening in some Caribbean islands?

• Jamaica began importing LNG via FSU with shuttle vessel in 2016.

• DR is fast becoming an established hub, and also plans to export LNG in ISOTANKs to the Bahamas. The AES Andres facility in DR imports conventional size LNG from Trinidad, as does Puerto Rico.

• Barbados imported ISOTANKS in 2016 from the USA, and have plans to import from Dominican Republic (DR).

• Other territories with smaller demand have been unable to implement LNG solutions.

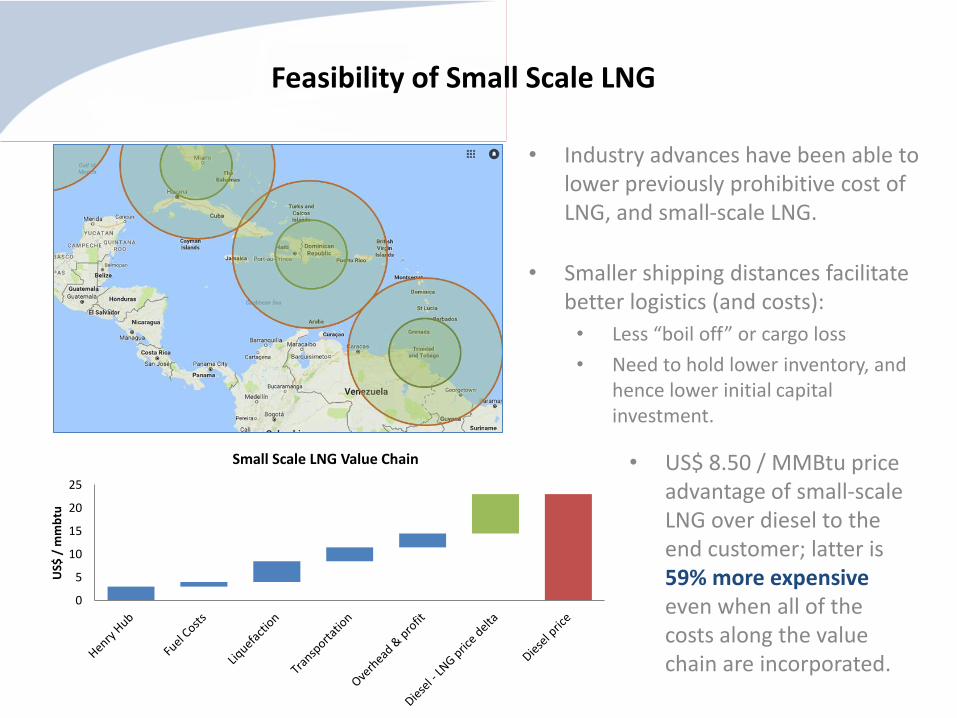

Feasibility of Small Scale LNG

• Smaller shipping distances facilitate better logistics (and costs):

• Less “boil off” or cargo loss

• Need to hold lower inventory, and hence lower initial capital investment.

0

5

10

15

20

25

US$

/ m

mb

tu

Small Scale LNG Value Chain

• Industry advances have been able to lower previously prohibitive cost of LNG, and small-scale LNG.

• US$ 8.50 / MMBtu price advantage of small-scale LNG over diesel to the end customer; latter is 59% more expensive even when all of the costs along the value chain are incorporated.

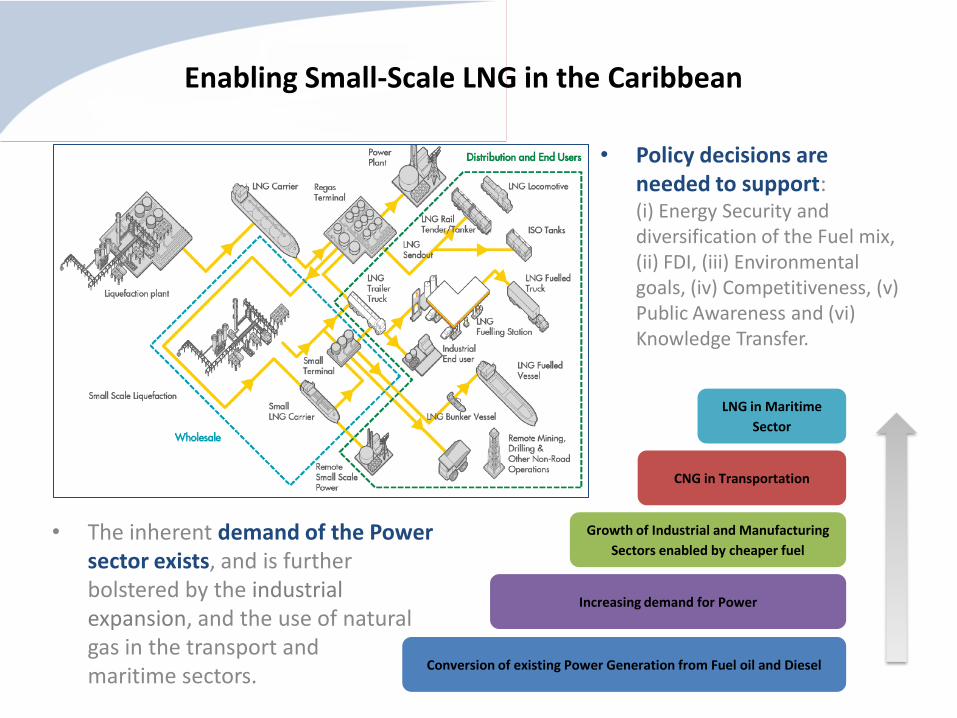

Enabling Small-Scale LNG in the Caribbean

• Policy decisions are needed to support: (i) Energy Security and diversification of the Fuel mix, (ii) FDI, (iii) Environmental goals, (iv) Competitiveness, (v) Public Awareness and (vi) Knowledge Transfer.

• The inherent demand of the Power sector exists, and is further bolstered by the industrial expansion, and the use of natural gas in the transport and maritime sectors.

Conversion of existing Power Generation from Fuel oil and Diesel

Increasing demand for Power

Growth of Industrial and Manufacturing

Sectors enabled by cheaper fuel

CNG in Transportation

LNG in Maritime

Sector

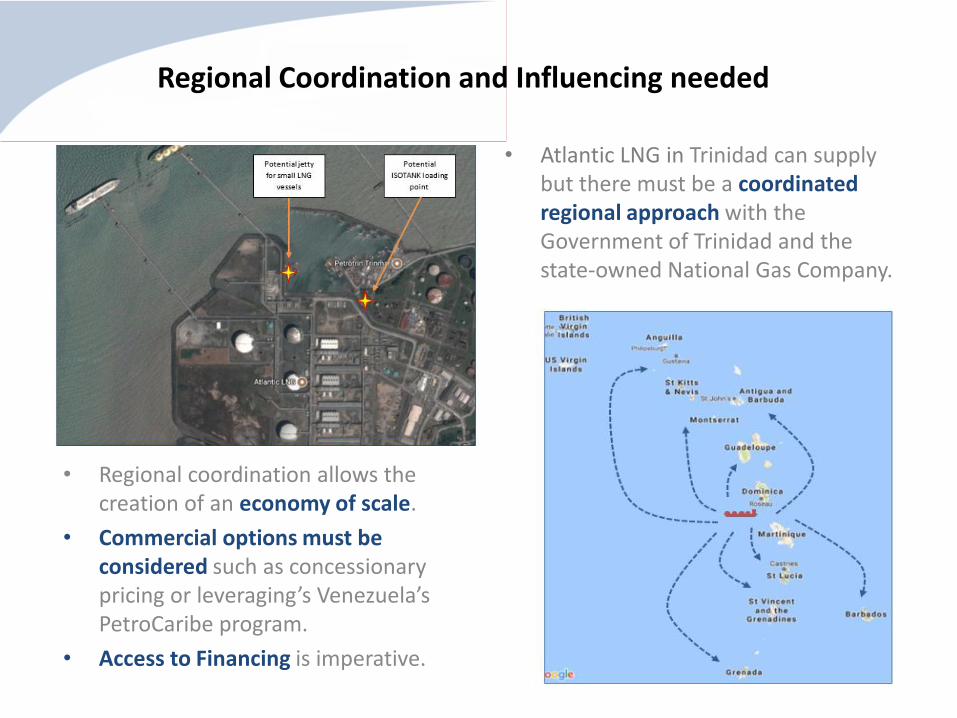

Regional Coordination and Influencing needed

• Atlantic LNG in Trinidad can supply but there must be a coordinated regional approach with the Government of Trinidad and the state-owned National Gas Company.

• Regional coordination allows the creation of an economy of scale.

• Commercial options must be considered such as concessionary pricing or leveraging’s Venezuela’s PetroCaribe program.

• Access to Financing is imperative.

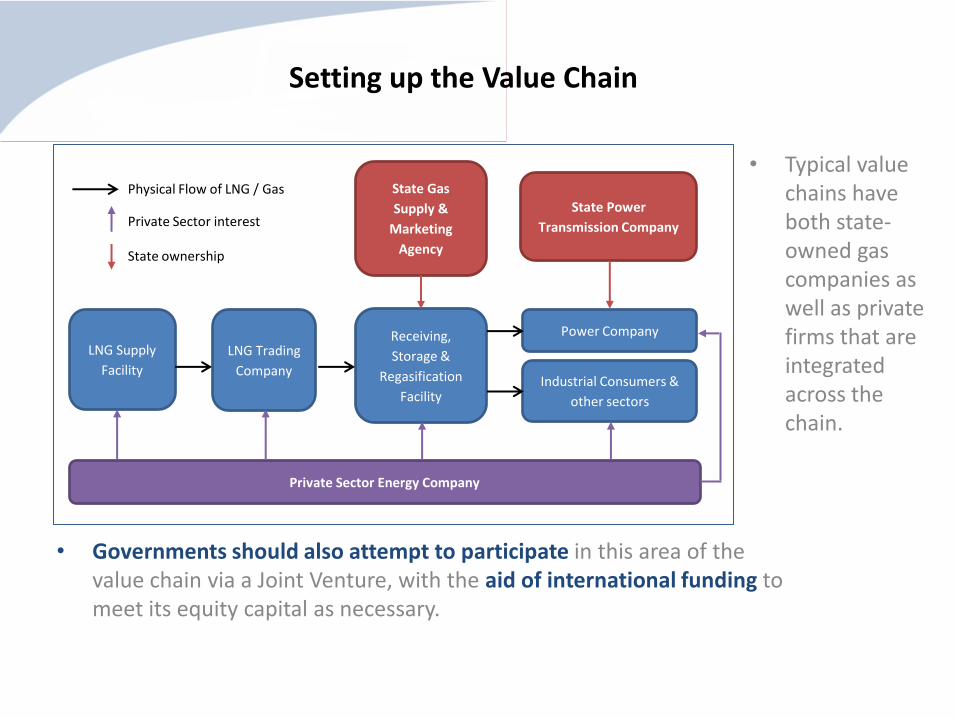

Setting up the Value Chain

• Typical value chains have both state-owned gas companies as well as private firms that are integrated across the chain.

LNG Supply

Facility

LNG Trading

Company

State Power

Transmission Company

Industrial Consumers &

other sectors

State Gas

Supply &

Marketing

Agency

Power Company Receiving,

Storage &

Regasification

Facility

Private Sector Energy Company

Physical Flow of LNG / Gas

Private Sector interest

State ownership

• Governments should also attempt to participate in this area of the value chain via a Joint Venture, with the aid of international funding to meet its equity capital as necessary.

Integrated LNG / small-scale logistics for greater economic prosperity and meeting environmental targets

“The Old Harbour Bay plant in Jamaica [running on natural gas via LNG] will generate electricity at a tariff less than US$ 0.13/Kwh (compared to the current estimated tariff of US$ 0.31/Kwh)…” - Kelly Tomblin, former President and CEO of the Jamaica Public Service, 2017

“With LNG, we will save 50% of our annual energy costs, or about US$336,000 per year, and also reduce 6,000 tons of green house gas emissions annually…” - Ricardo Nuncio, Managing Director of Red Stripe Beer, 2017

“The power plant will be more fuel efficient and will reduce Jamaica's imports of oil and use of fuel. Once operational, we estimate that will be about US$200 million in savings per annum…” - Dan Theoc, General Manager of SJPC, and CFO of Jamaica Public Service, 2017

Thank you!