Embed Size (px)

Citation preview

TRƯỜNG ĐẠI HỌC KINH TẾ TP.HCM

TRUNG TÂM DỮ LIỆU - PHÂN TÍCH KINH TẾ

BÁO CÁO DỮ LIỆU PHỤC VỤ NGHIÊN CỨU

CHỦ ĐỀ: DỮ LIỆU VÀ NGHIÊN CỨU VỀ NGÂN HÀNG TỪ

BANKSCOPE

TP.HCM, 11/2016

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

1

MỤC LỤC

1. DỮ LIỆU NGÂN HÀNG TỪ BANKSCOPE ............................................................................ 2

1.1 Giới thiệu .............................................................................................................................. 2

1.2 Download dữ liệu từ Bankscope ......................................................................................... 11

1.2.1 Download dữ liệu theo tên ngân hàng ......................................................................... 11

1.2.2 Download dữ liệu theo nước/khu vực địa lý ................................................................ 14

2. NGHIÊN CỨU SỬ DỤNG DỮ LIỆU BANKSCOPE ............................................................. 20

Tài liệu tham khảo ........................................................................................................................ 26

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

2

1. DỮ LIỆU NGÂN HÀNG TỪ BANKSCOPE

1.1 Giới thiệu

Bankscope cung cấp các báo cáo tài chính của khoảng 32,000 ngân hàng trên phạm vi toàn cầu:

Báo cáo tài chính chi tiết

Xếp hạng tín nhiệm ngân hàng (FitchRatings, Moody's, Standard & Poor's)

Thông tin cơ cấu sở hữu ngân hàng (Ownership data)

Thông tin về cổ phiếu (stock) của các ngân hàng niêm yết

Bankscope là nguồn dữ liệu quan trọng cho các nghiên cứu trong lĩnh vực ngân hàng và được sử

dụng bởi hơn 90% top 1000 ngân hàng lớn nhất thế giới.

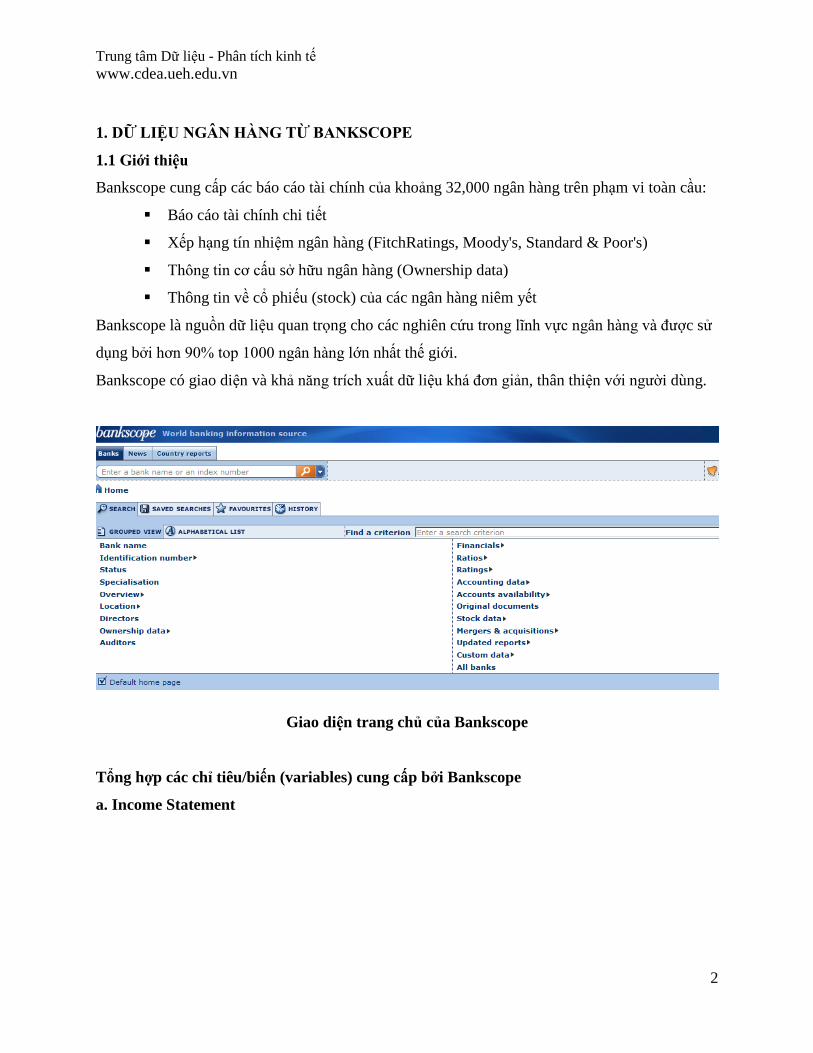

Bankscope có giao diện và khả năng trích xuất dữ liệu khá đơn giản, thân thiện với người dùng.

Giao diện trang chủ của Bankscope

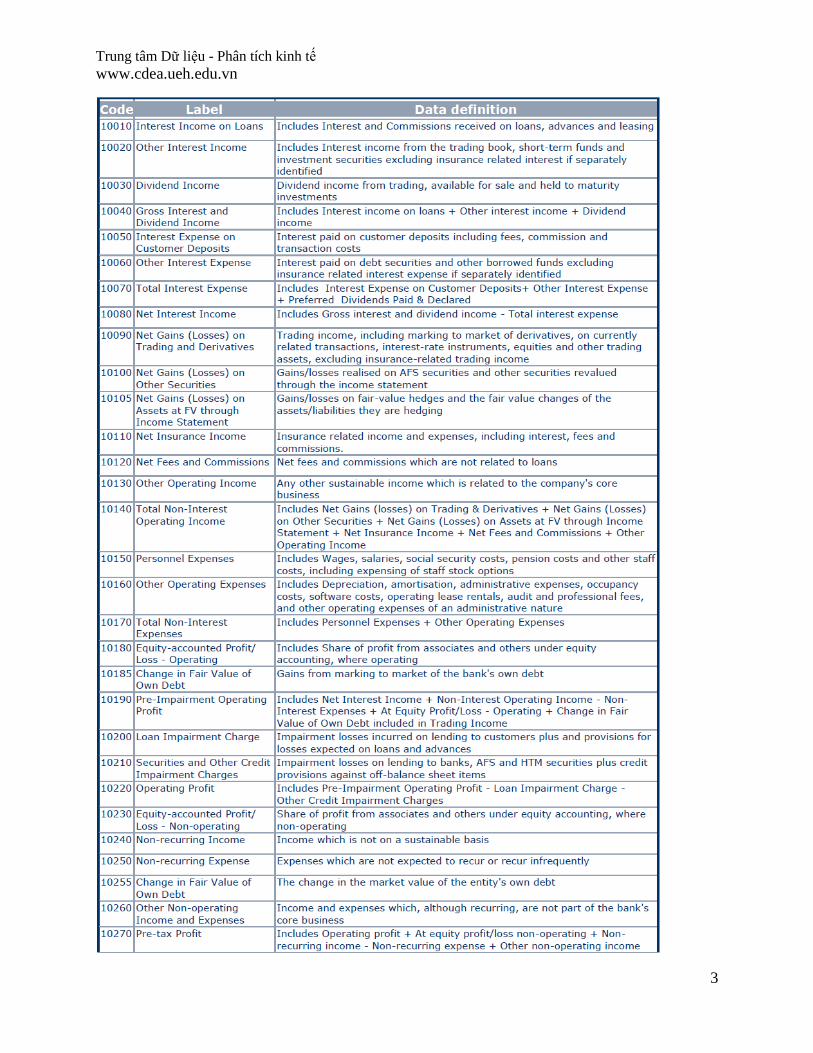

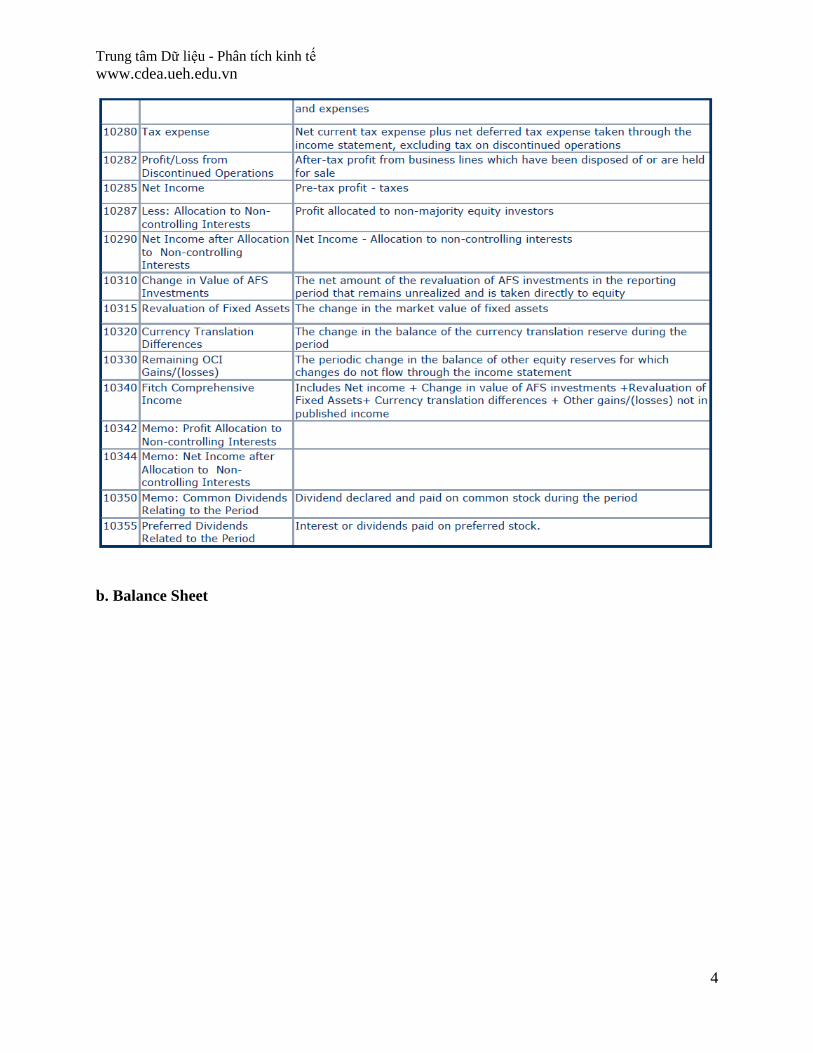

Tổng hợp các chỉ tiêu/biến (variables) cung cấp bởi Bankscope

a. Income Statement

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

3

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

4

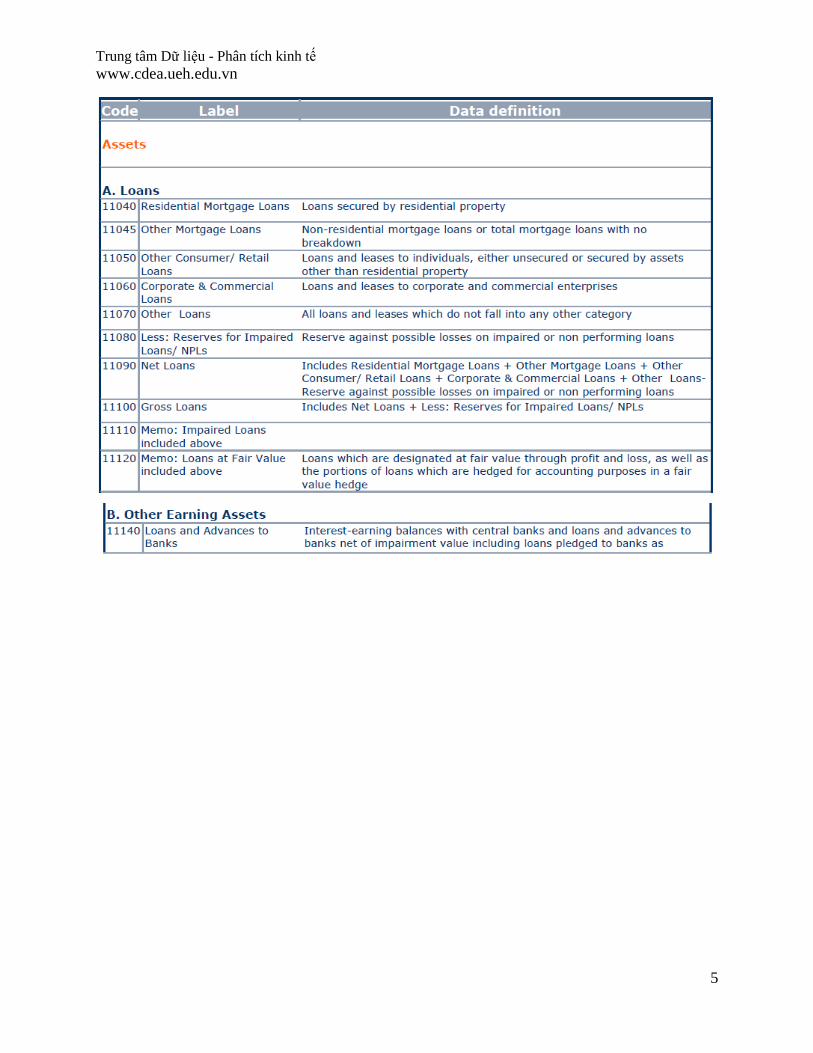

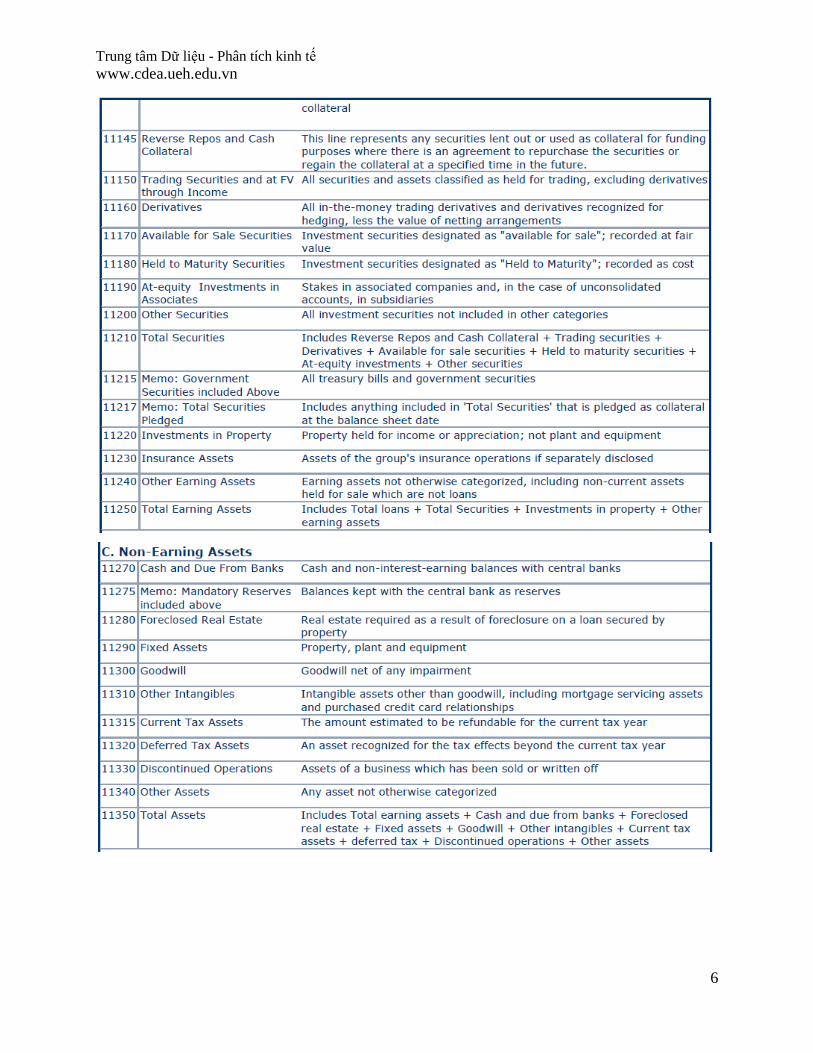

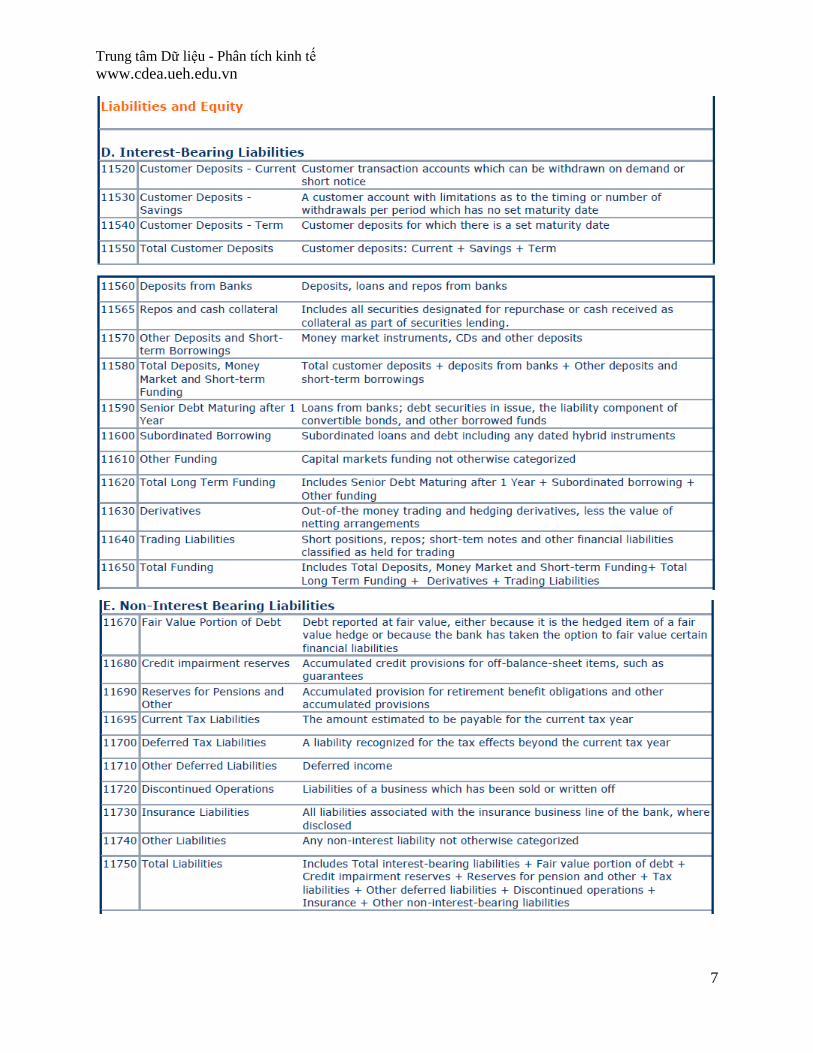

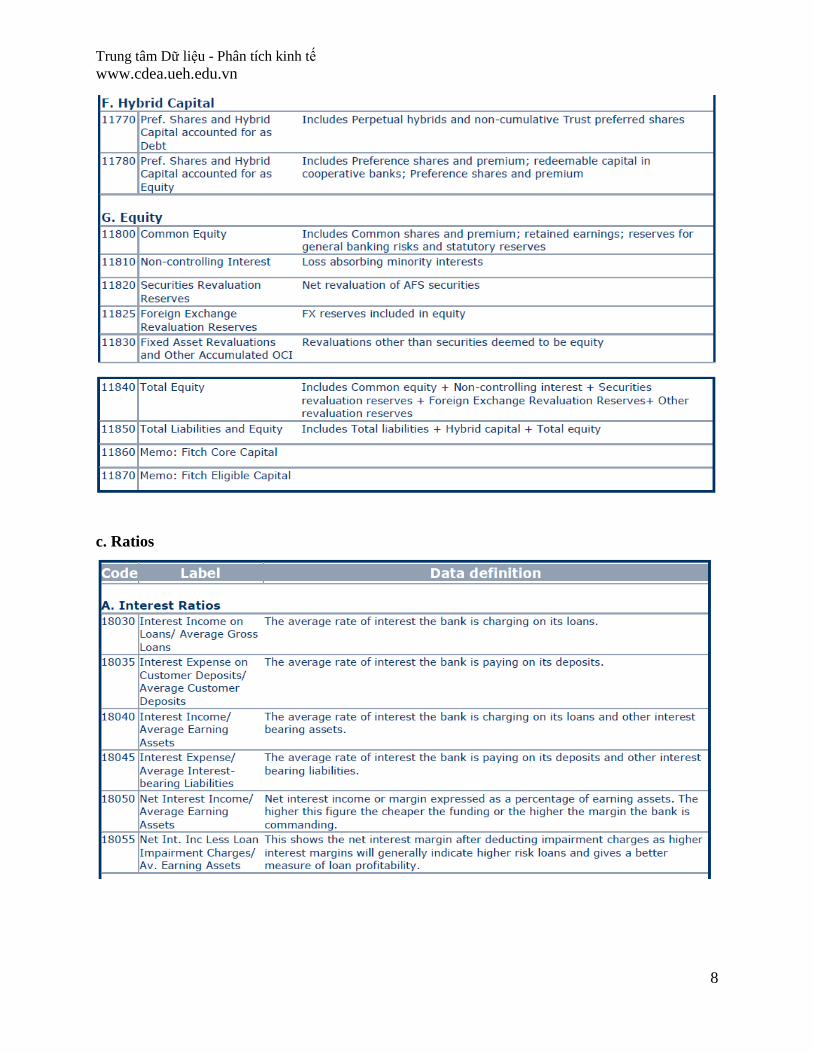

b. Balance Sheet

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

5

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

6

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

7

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

8

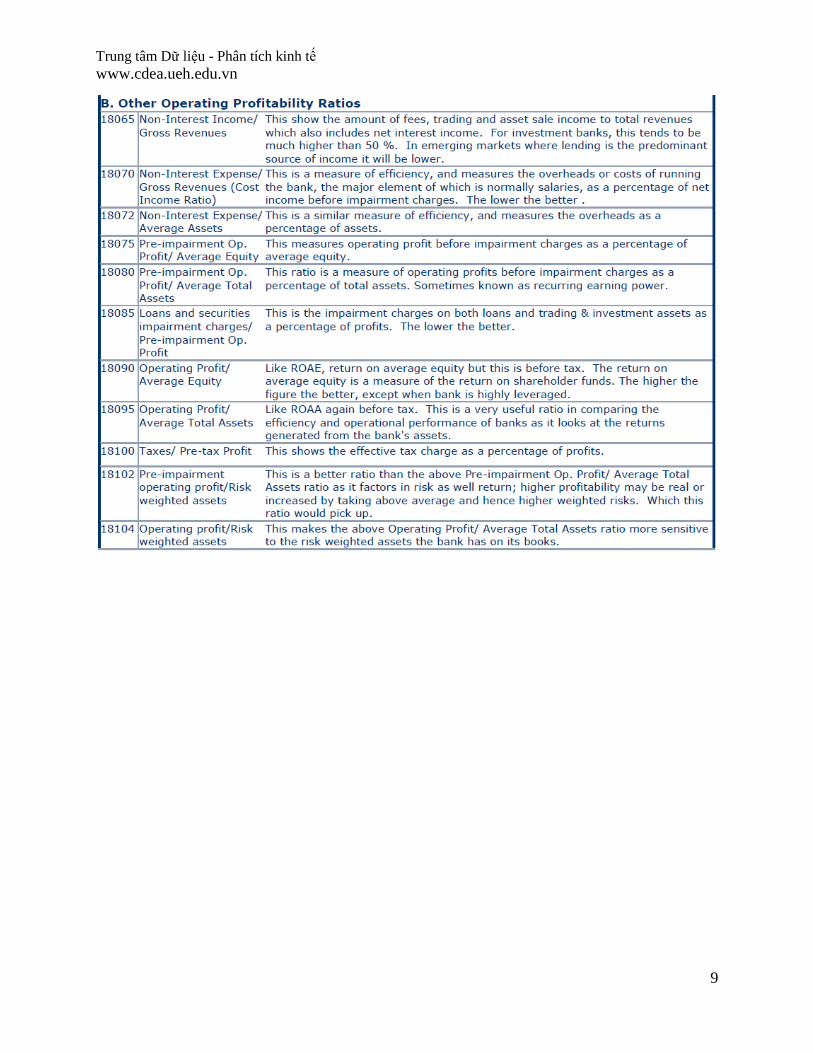

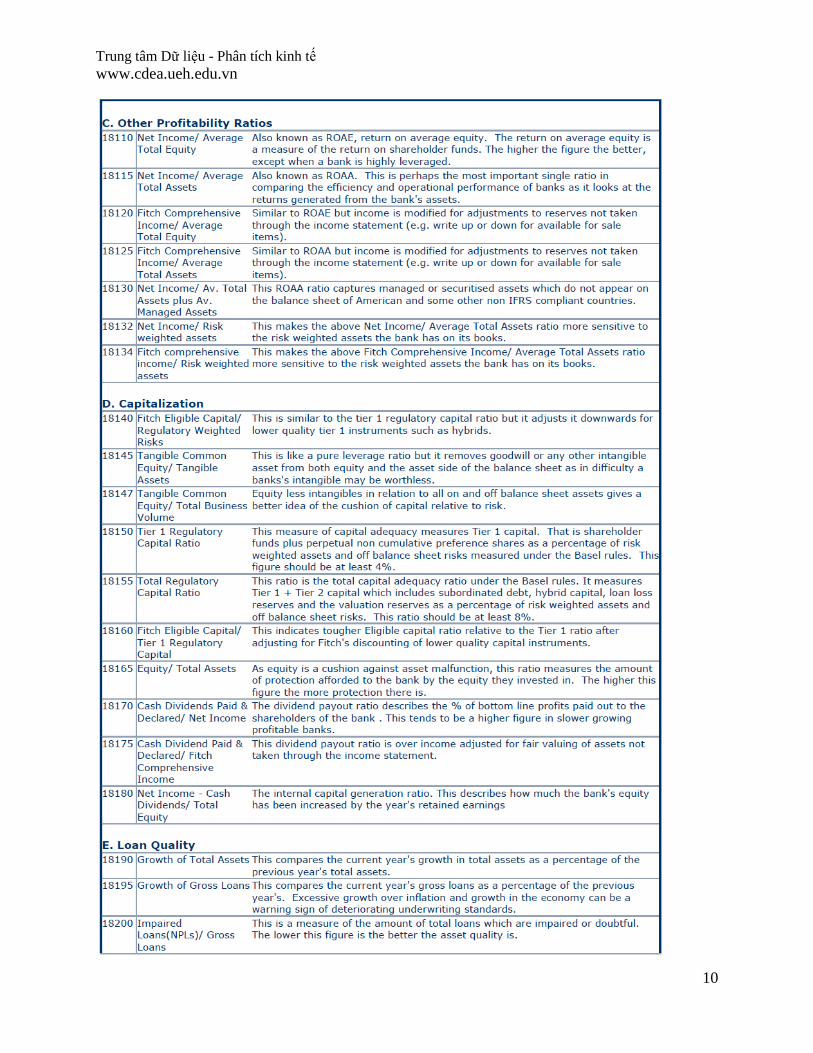

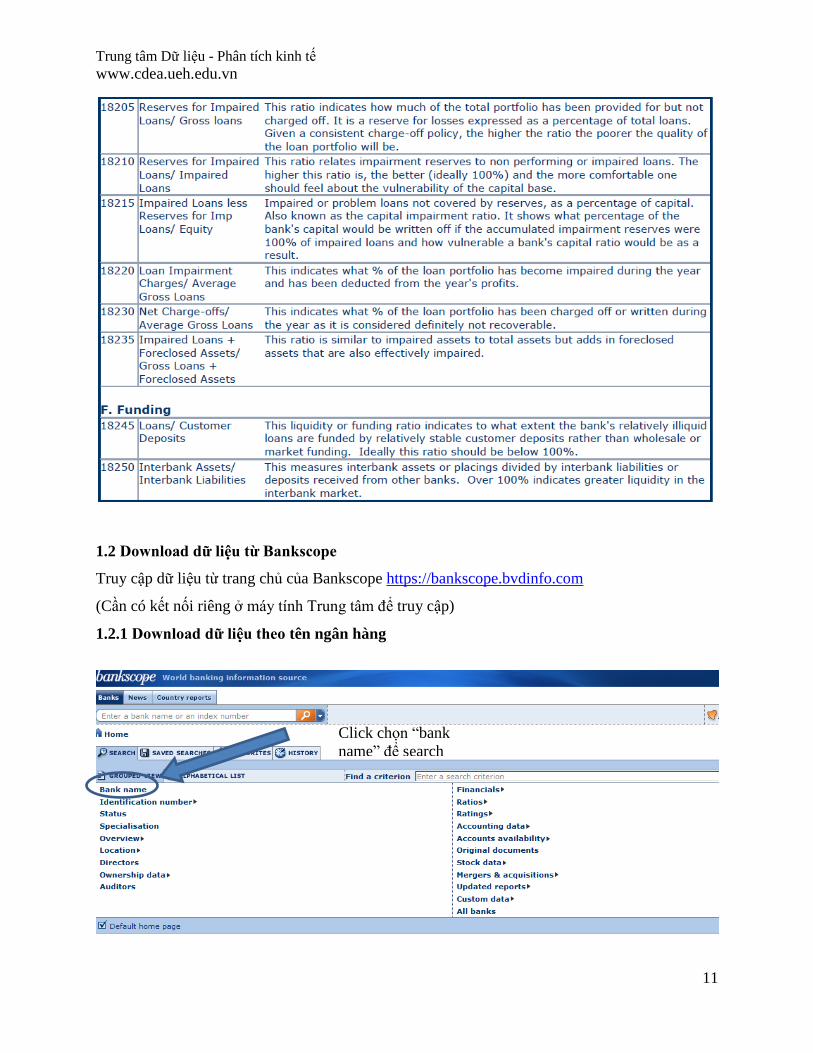

c. Ratios

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

9

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

10

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

11

1.2 Download dữ liệu từ Bankscope

Truy cập dữ liệu từ trang chủ của Bankscope https://bankscope.bvdinfo.com

(Cần có kết nối riêng ở máy tính Trung tâm để truy cập)

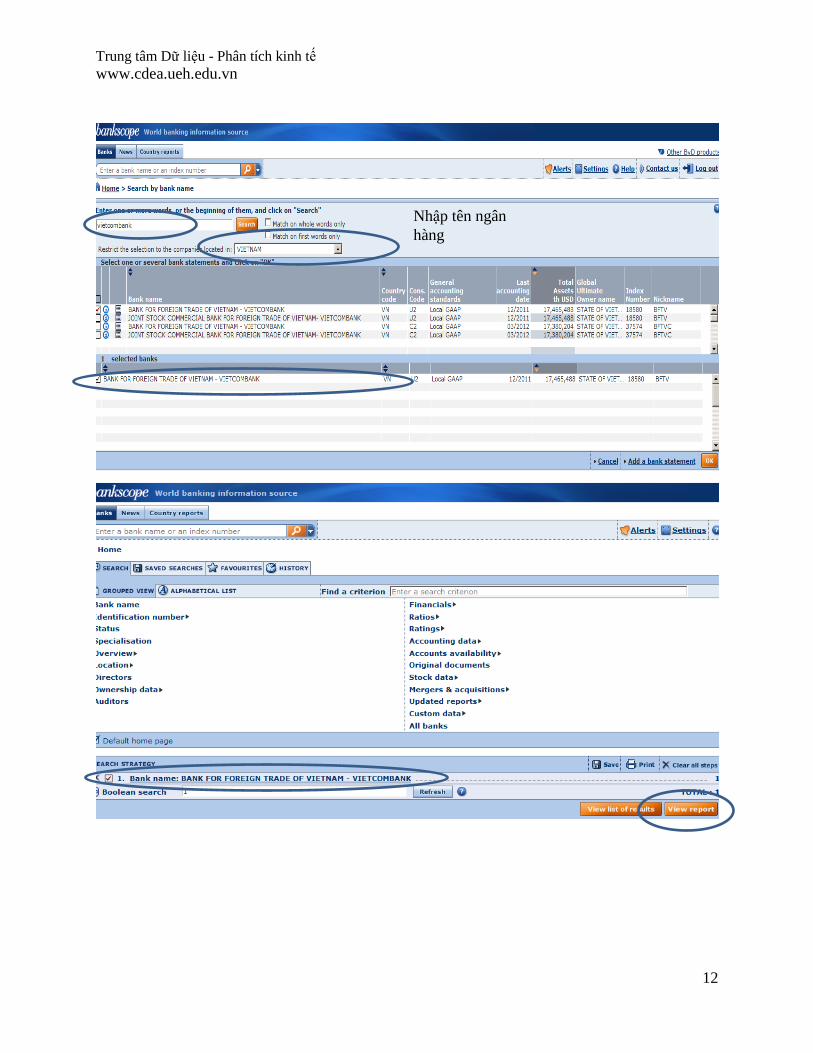

1.2.1 Download dữ liệu theo tên ngân hàng

Click chọn “bank

name” để search

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

12

Nhập tên ngân

hàng

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

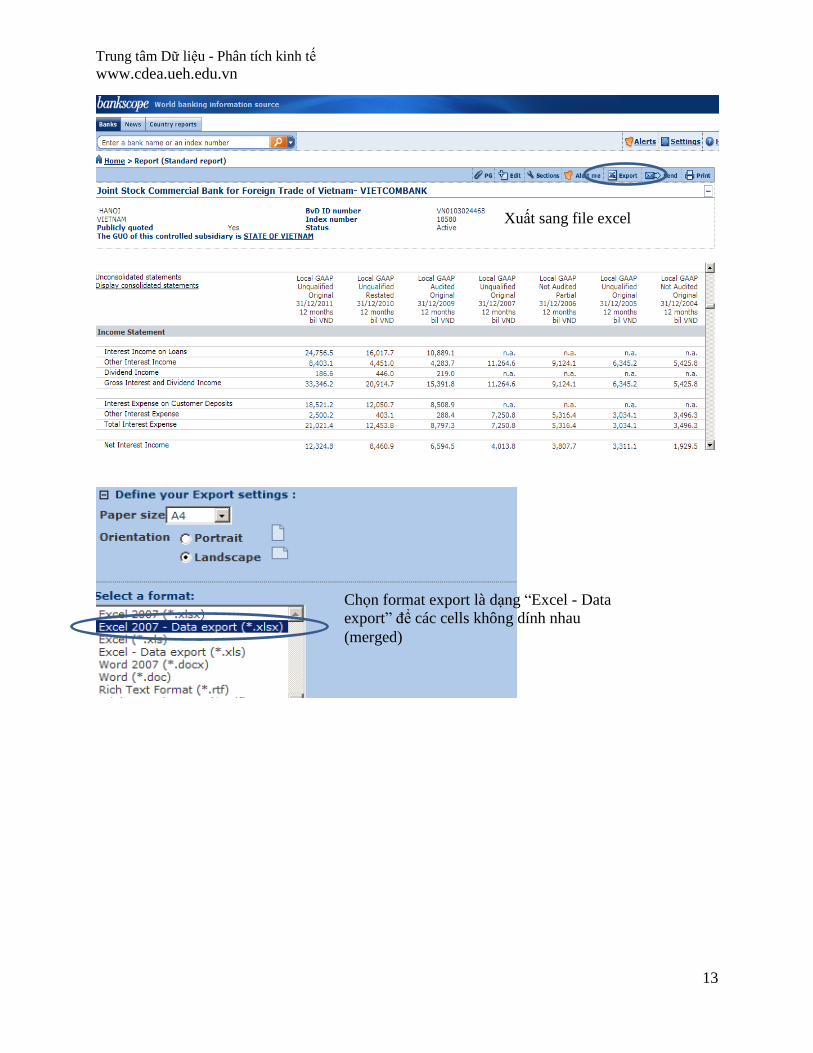

13

Xuất sang file excel

Chọn format export là dạng “Excel - Data

export” để các cells không dính nhau

(merged)

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

14

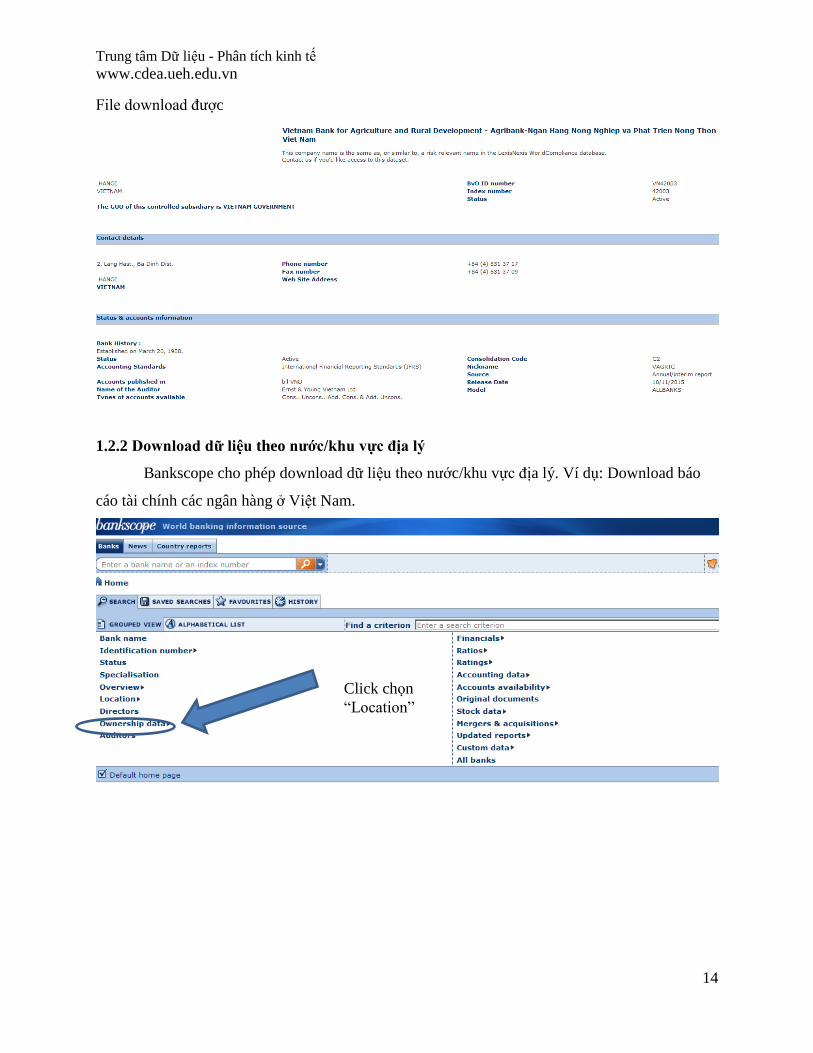

File download được

1.2.2 Download dữ liệu theo nước/khu vực địa lý

Bankscope cho phép download dữ liệu theo nước/khu vực địa lý. Ví dụ: Download báo

cáo tài chính các ngân hàng ở Việt Nam.

Click chọn

“Location”

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

15

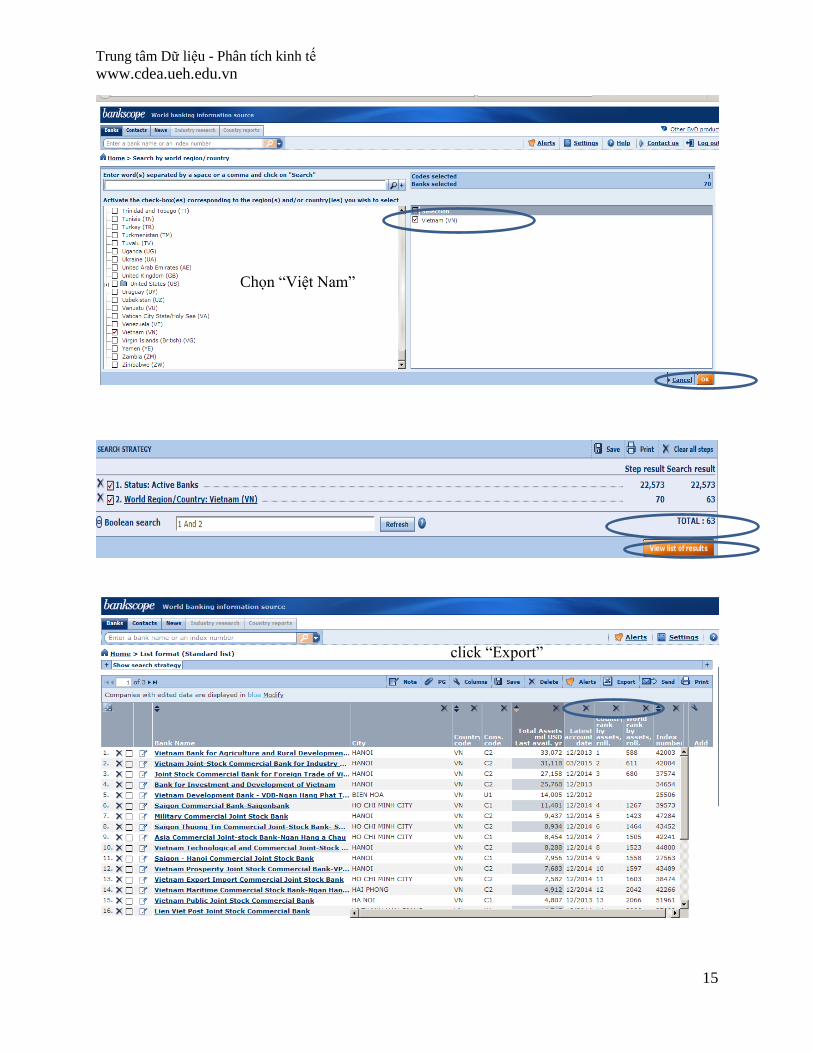

Chọn “Việt Nam”

click “Export”

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

16

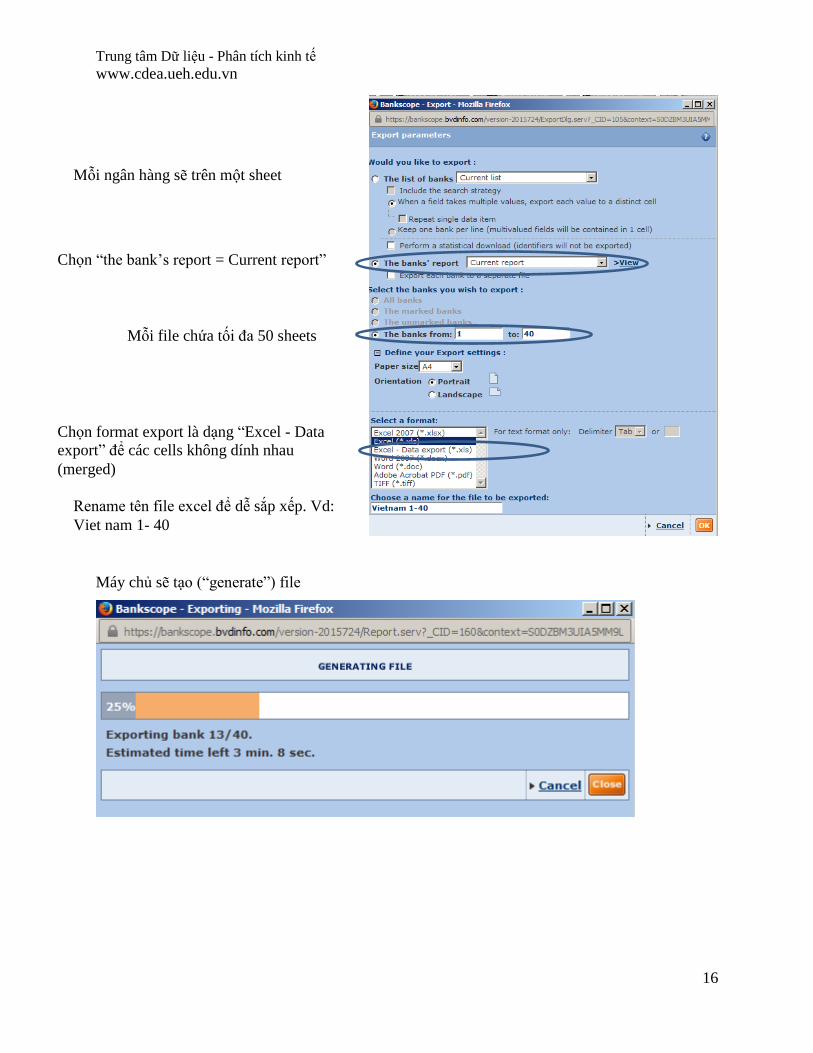

Máy chủ sẽ tạo (“generate”) file

Mỗi file chứa tối đa 50 sheets

Chọn “the bank’s report = Current report”

Mỗi ngân hàng sẽ trên một sheet

Chọn format export là dạng “Excel - Data

export” để các cells không dính nhau

(merged)

Rename tên file excel để dễ sắp xếp. Vd:

Viet nam 1- 40

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

17

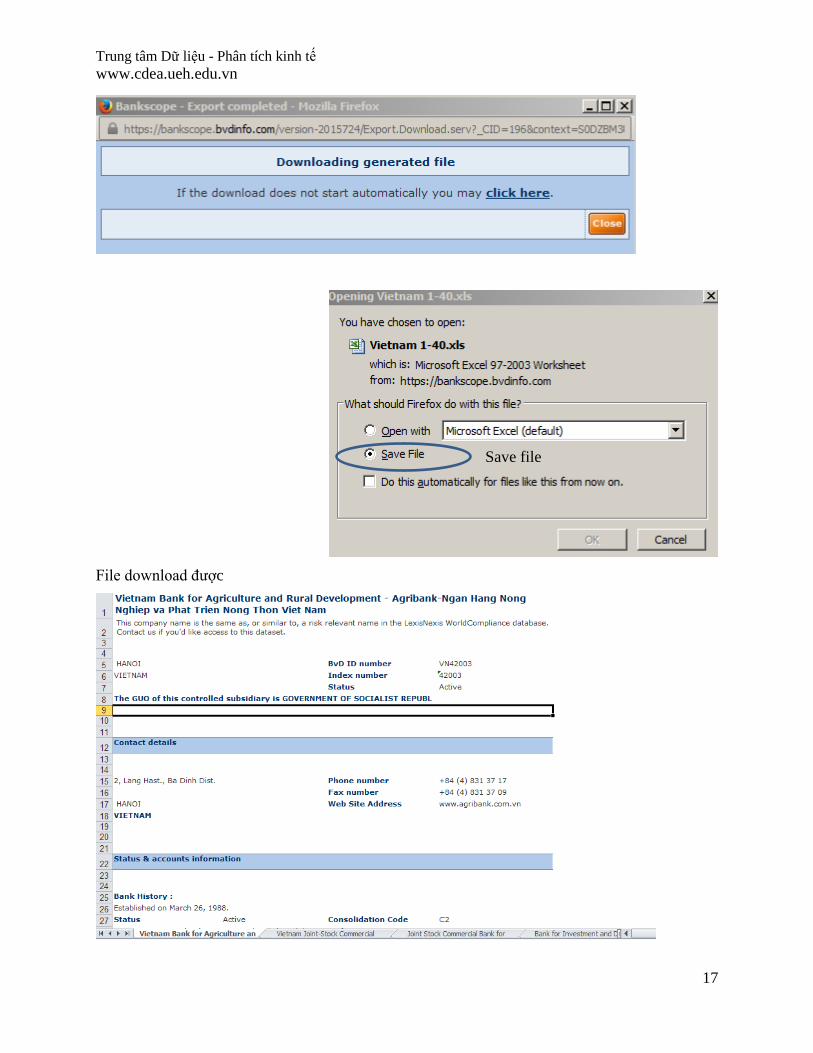

File download được

Save file

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

18

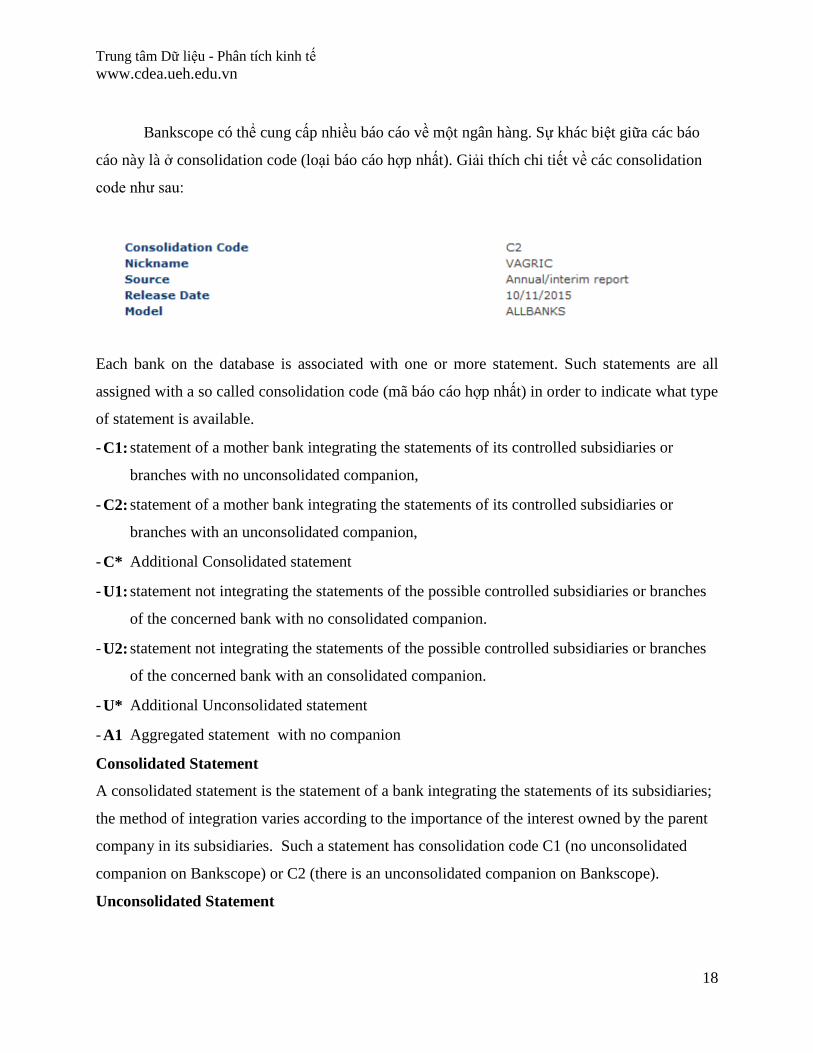

Bankscope có thể cung cấp nhiều báo cáo về một ngân hàng. Sự khác biệt giữa các báo

cáo này là ở consolidation code (loại báo cáo hợp nhất). Giải thích chi tiết về các consolidation

code như sau:

Each bank on the database is associated with one or more statement. Such statements are all

assigned with a so called consolidation code (mã báo cáo hợp nhất) in order to indicate what type

of statement is available.

- C1: statement of a mother bank integrating the statements of its controlled subsidiaries or

branches with no unconsolidated companion,

- C2: statement of a mother bank integrating the statements of its controlled subsidiaries or

branches with an unconsolidated companion,

- C* Additional Consolidated statement

- U1: statement not integrating the statements of the possible controlled subsidiaries or branches

of the concerned bank with no consolidated companion.

- U2: statement not integrating the statements of the possible controlled subsidiaries or branches

of the concerned bank with an consolidated companion.

- U* Additional Unconsolidated statement

- A1 Aggregated statement with no companion

Consolidated Statement

A consolidated statement is the statement of a bank integrating the statements of its subsidiaries;

the method of integration varies according to the importance of the interest owned by the parent

company in its subsidiaries. Such a statement has consolidation code C1 (no unconsolidated

companion on Bankscope) or C2 (there is an unconsolidated companion on Bankscope).

Unconsolidated Statement

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

19

A statement not integrating the possible subsidiaries of the concerned bank. Such a statement has

a consolidation code U1 (no consolidation companion on Bankscope) or U2 (there is a

consolidated companion on Bankscope).

Additional companion statements (C* or U*)

The additional statements might differ from the main statements according to one or more of the

following criteria:

The source used to spread the data is different (FDIC, SEC…)

The accounting standard (generally historical accounts in Local GAAP, more recent ones

in IFRS are in the main statements)

Inflation adjusted vs nominal values

Proforma accounts vs original accounts

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

20

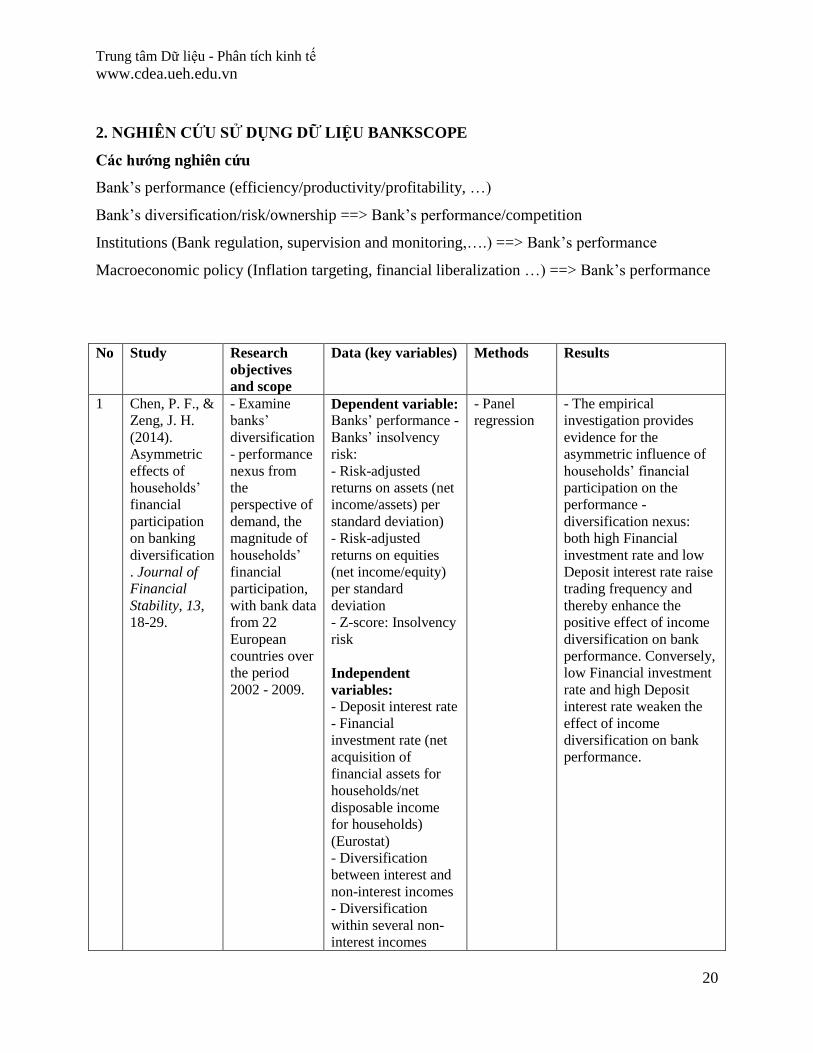

2. NGHIÊN CỨU SỬ DỤNG DỮ LIỆU BANKSCOPE

Các hướng nghiên cứu

Bank’s performance (efficiency/productivity/profitability, …)

Bank’s diversification/risk/ownership ==> Bank’s performance/competition

Institutions (Bank regulation, supervision and monitoring,….) ==> Bank’s performance

Macroeconomic policy (Inflation targeting, financial liberalization …) ==> Bank’s performance

No Study Research

objectives

and scope

Data (key variables) Methods Results

1 Chen, P. F., &

Zeng, J. H.

(2014).

Asymmetric

effects of

households’

financial

participation

on banking

diversification

. Journal of

Financial

Stability, 13,

18-29.

- Examine

banks’

diversification

- performance

nexus from

the

perspective of

demand, the

magnitude of

households’

financial

participation,

with bank data

from 22

European

countries over

the period

2002 - 2009.

Dependent variable: Banks’ performance -

Banks’ insolvency

risk:

- Risk-adjusted

returns on assets (net

income/assets) per

standard deviation)

- Risk-adjusted

returns on equities

(net income/equity)

per standard

deviation

- Z-score: Insolvency

risk

Independent

variables:

- Deposit interest rate

- Financial

investment rate (net

acquisition of

financial assets for

households/net

disposable income

for households)

(Eurostat)

- Diversification

between interest and

non-interest incomes

- Diversification

within several non-

interest incomes

- Panel

regression

- The empirical

investigation provides

evidence for the

asymmetric influence of

households’ financial

participation on the

performance -

diversification nexus:

both high Financial

investment rate and low

Deposit interest rate raise

trading frequency and

thereby enhance the

positive effect of income

diversification on bank

performance. Conversely,

low Financial investment

rate and high Deposit

interest rate weaken the

effect of income

diversification on bank

performance.

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

21

- Total assets

- Equity to total

assets

- GDP growth

- Inflation rate

…

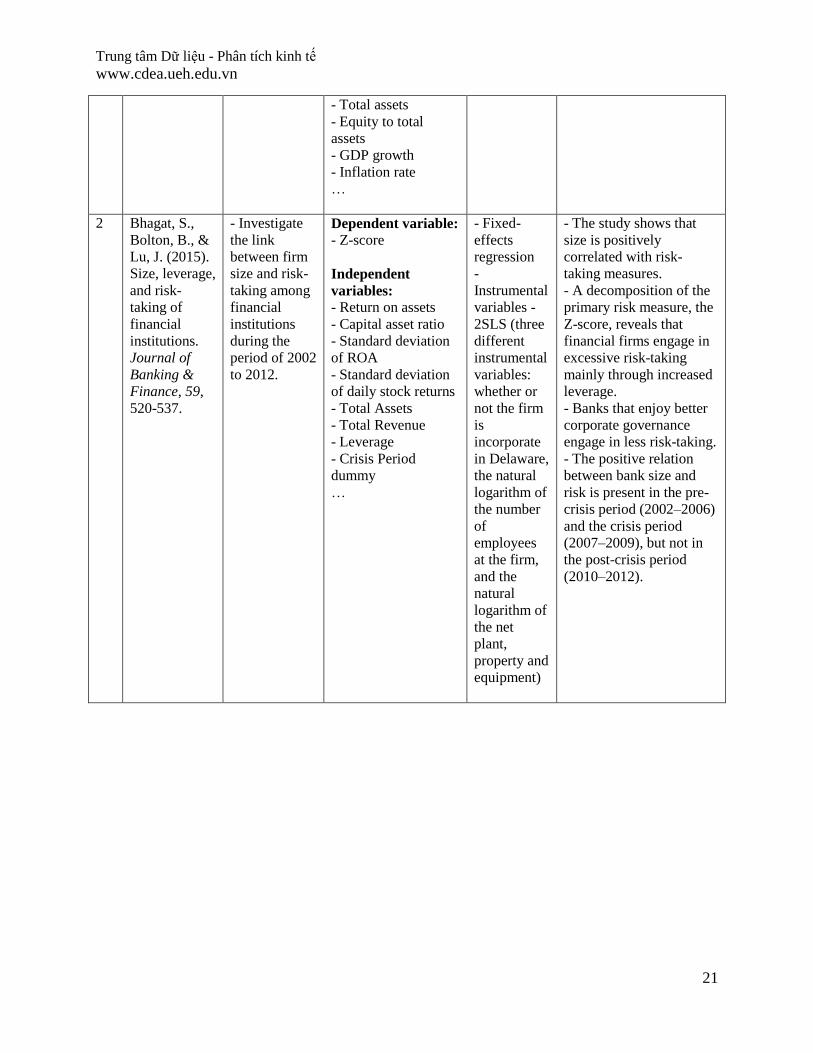

2 Bhagat, S.,

Bolton, B., &

Lu, J. (2015).

Size, leverage,

and risk-

taking of

financial

institutions.

Journal of

Banking &

Finance, 59,

520-537.

- Investigate

the link

between firm

size and risk-

taking among

financial

institutions

during the

period of 2002

to 2012.

Dependent variable: - Z-score

Independent

variables:

- Return on assets

- Capital asset ratio

- Standard deviation

of ROA

- Standard deviation

of daily stock returns

- Total Assets

- Total Revenue

- Leverage

- Crisis Period

dummy

…

- Fixed-

effects

regression

-

Instrumental

variables -

2SLS (three

different

instrumental

variables:

whether or

not the firm

is

incorporate

in Delaware,

the natural

logarithm of

the number

of

employees

at the firm,

and the

natural

logarithm of

the net

plant,

property and

equipment)

- The study shows that

size is positively

correlated with risk-

taking measures.

- A decomposition of the

primary risk measure, the

Z-score, reveals that

financial firms engage in

excessive risk-taking

mainly through increased

leverage.

- Banks that enjoy better

corporate governance

engage in less risk-taking.

- The positive relation

between bank size and

risk is present in the pre-

crisis period (2002–2006)

and the crisis period

(2007–2009), but not in

the post-crisis period

(2010–2012).

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

22

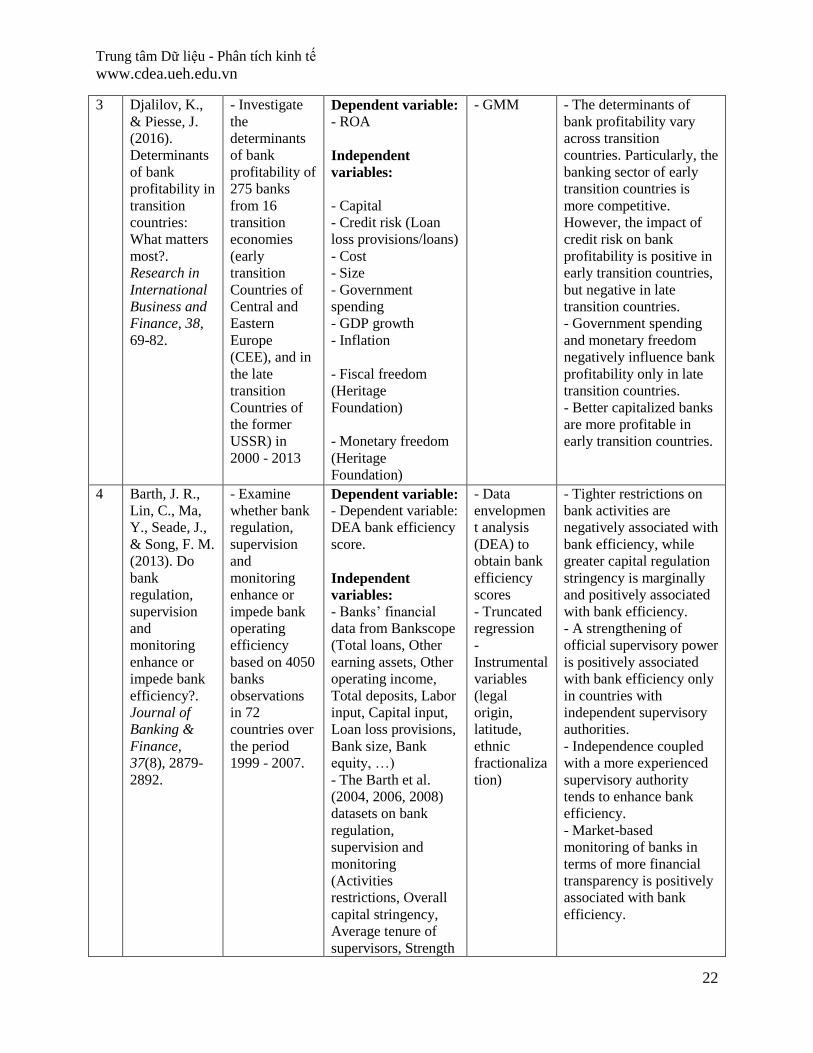

3 Djalilov, K.,

& Piesse, J.

(2016).

Determinants

of bank

profitability in

transition

countries:

What matters

most?.

Research in

International

Business and

Finance, 38,

69-82.

- Investigate

the

determinants

of bank

profitability of

275 banks

from 16

transition

economies

(early

transition

Countries of

Central and

Eastern

Europe

(CEE), and in

the late

transition

Countries of

the former

USSR) in

2000 - 2013

Dependent variable: - ROA

Independent

variables:

- Capital

- Credit risk (Loan

loss provisions/loans)

- Cost

- Size

- Government

spending

- GDP growth

- Inflation

- Fiscal freedom

(Heritage

Foundation)

- Monetary freedom

(Heritage

Foundation)

- GMM - The determinants of

bank profitability vary

across transition

countries. Particularly, the

banking sector of early

transition countries is

more competitive.

However, the impact of

credit risk on bank

profitability is positive in

early transition countries,

but negative in late

transition countries.

- Government spending

and monetary freedom

negatively influence bank

profitability only in late

transition countries.

- Better capitalized banks

are more profitable in

early transition countries.

4 Barth, J. R.,

Lin, C., Ma,

Y., Seade, J.,

& Song, F. M.

(2013). Do

bank

regulation,

supervision

and

monitoring

enhance or

impede bank

efficiency?.

Journal of

Banking &

Finance,

37(8), 2879-

2892.

- Examine

whether bank

regulation,

supervision

and

monitoring

enhance or

impede bank

operating

efficiency

based on 4050

banks

observations

in 72

countries over

the period

1999 - 2007.

Dependent variable: - Dependent variable:

DEA bank efficiency

score.

Independent

variables:

- Banks’ financial

data from Bankscope

(Total loans, Other

earning assets, Other

operating income,

Total deposits, Labor

input, Capital input,

Loan loss provisions,

Bank size, Bank

equity, …)

- The Barth et al.

(2004, 2006, 2008)

datasets on bank

regulation,

supervision and

monitoring

(Activities

restrictions, Overall

capital stringency,

Average tenure of

supervisors, Strength

- Data

envelopmen

t analysis

(DEA) to

obtain bank

efficiency

scores

- Truncated

regression

-

Instrumental

variables

(legal

origin,

latitude,

ethnic

fractionaliza

tion)

- Tighter restrictions on

bank activities are

negatively associated with

bank efficiency, while

greater capital regulation

stringency is marginally

and positively associated

with bank efficiency.

- A strengthening of

official supervisory power

is positively associated

with bank efficiency only

in countries with

independent supervisory

authorities.

- Independence coupled

with a more experienced

supervisory authority

tends to enhance bank

efficiency.

- Market-based

monitoring of banks in

terms of more financial

transparency is positively

associated with bank

efficiency.

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

23

of external audit,

Certified Audit

Required, Bank

accounting

informative, Official

Supervisory Power,

Supervisory

independence, …)

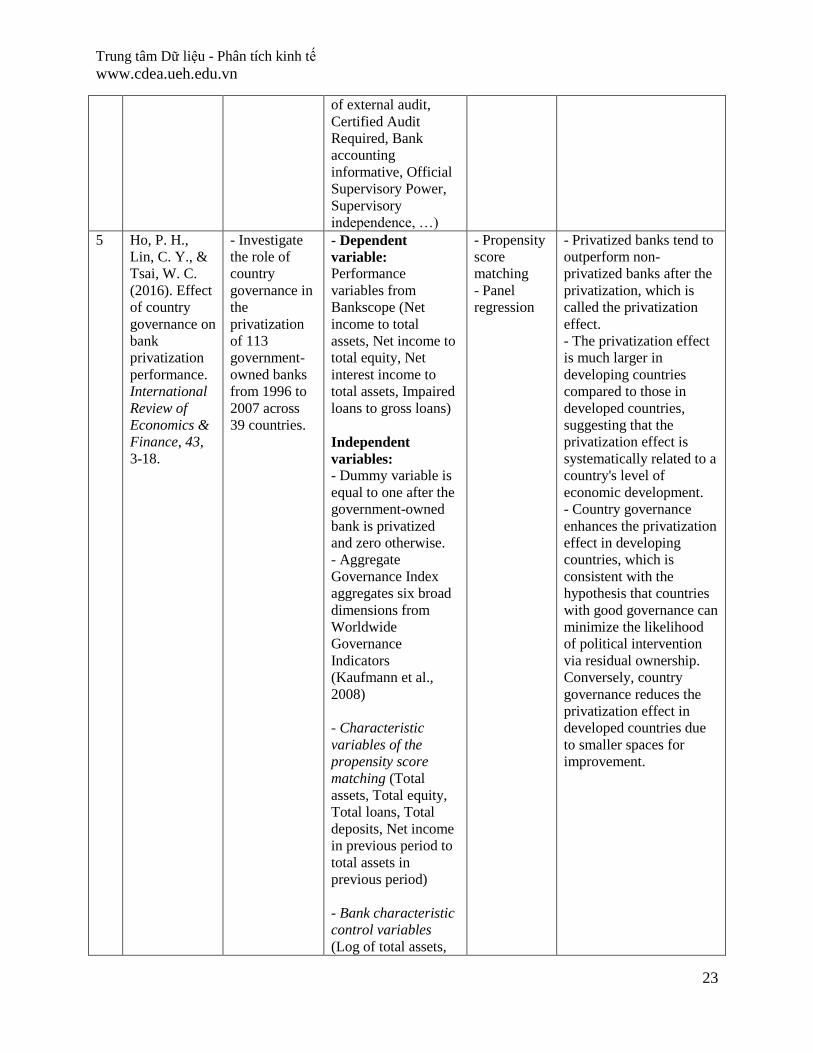

5 Ho, P. H.,

Lin, C. Y., &

Tsai, W. C.

(2016). Effect

of country

governance on

bank

privatization

performance.

International

Review of

Economics &

Finance, 43,

3-18.

- Investigate

the role of

country

governance in

the

privatization

of 113

government-

owned banks

from 1996 to

2007 across

39 countries.

- Dependent

variable:

Performance

variables from

Bankscope (Net

income to total

assets, Net income to

total equity, Net

interest income to

total assets, Impaired

loans to gross loans)

Independent

variables:

- Dummy variable is

equal to one after the

government-owned

bank is privatized

and zero otherwise.

- Aggregate

Governance Index

aggregates six broad

dimensions from

Worldwide

Governance

Indicators

(Kaufmann et al.,

2008)

- Characteristic

variables of the

propensity score

matching (Total

assets, Total equity,

Total loans, Total

deposits, Net income

in previous period to

total assets in

previous period)

- Bank characteristic

control variables

(Log of total assets,

- Propensity

score

matching

- Panel

regression

- Privatized banks tend to

outperform non-

privatized banks after the

privatization, which is

called the privatization

effect.

- The privatization effect

is much larger in

developing countries

compared to those in

developed countries,

suggesting that the

privatization effect is

systematically related to a

country's level of

economic development.

- Country governance

enhances the privatization

effect in developing

countries, which is

consistent with the

hypothesis that countries

with good governance can

minimize the likelihood

of political intervention

via residual ownership.

Conversely, country

governance reduces the

privatization effect in

developed countries due

to smaller spaces for

improvement.

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

24

Total debts to total

equities, Average

balance of loans to

average balance of

deposits, Inverse

Mills ratio)

- Macroeconomic

control variables

(GDP to population,

GDP growth rate,

Government budget

surplus as a

percentage of GDP,

Inflation, …)

6 Fazio, D. M.,

Tabak, B. M.,

& Cajueiro,

D. O. (2015).

Inflation

targeting: Is

IT to blame

for banking

system

instability?.

Journal of

Banking &

Finance, 59,

76-97.

- Examine the

relationship

between

inflation

targeting and

banking

system

stability of

nearly 5500

commercial

banks from 70

countries

(among

which, 22 are

inflation

targeting) for

the period

1998–2012.

Dependent

variables:

- Financial Stability

- Risk-Adj. Profits

- Equity Ratio

- ROA Volatility

Independent

variables:

- Inflation targeting:

a dummy equal to

one if country where

bank operates is an

inflation targeter.

(Source: IMF

website, Roger

(2010))

- Banks’ financial

variables (Liquidity

Ratio, Cost to Assets,

Total assets, …)

- Macroeconomic

control variables

(Economic Openess,

Financial Freedom

Index, Property

Rights Index, …)

- Fixed-

effects

regression

- Inflation targeting

national banking systems

(i) are more stable; (ii)

possess sounder

systemically important

banks; and (iii) are less

distressed than (or at least

as distressed as) other

banks during periods of

global liquidity shortages.

- Results are robust to a

series of tests, such as

when comparing

countries with the same

legal origins or

controlling for the

delegation of bank

supervision responsibility

to bodies other than the

central bank.

7 Lee, C.,

Hsieh, M., &

Yang, S.

(2016). The

effects of

foreign

ownership on

competition in

the banking

industry: The

key role of

- Analyze the

impacts of

foreign

ownership on

competition

- Investigate

the

relationship

between

foreign

ownership and

Dependent

variables:

- The share of the

loan market

controlled by the four

largest banks.

- A country-level

indicator of bank

concentration,

measured by the

Herfindahl-

- Dynamic

panel GMM

- A higher ratio of foreign

ownership in a bank can

enhance competition,

whereas a liberalization

policy on banking

supervision instead

mitigates this positive

relation between foreign

ownership and

competition. Conversely,

the liberalization on bank

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

25

financial

reforms.

Japan And

The World

Economy, 37-

38, 27-46.

competition

changes under

financial

reforms

implemented

in the host

country with

the sample of

50 countries

in 4 regions

(emerging

Asia, Latin

America,

Middle East

and North

Africa

(MENA), and

Sub-Saharan

Africa (SSA)

from 1995 to

2005

Hirschman Deposits

Index

- A country-level

indicator of bank

concentration,

measured by the

Herfindahl-

Hirschman Total

Assets Index

- A country-level

indicator of bank

concentration,

measured by the

Herfindahl-

Hirschman Gross

Loans Index

Independent

variables:

- Bank-level foreign

bank ownership

- Logarithm of total

bank assets

- Ratio of liquidity

assets to total assets

- Ratio of non-

interest expenses to

total assets

…

Conditional factors

Financial reforms

(financial

liberalizations)

CCON: Credit

controls; 0 to 3

means the higher the

value, the higher the

liberalization.

ICON: Interest

controls; 0 to 3

means the higher the

value, the higher the

liberalization

EBAR: Entry

barriers; 0 to 3 means

the higher the value,

the higher the

liberalization

privatization in Latin

America and Sub-Saharan

Africa (SSA) countries

significantly increases

competition. Thus,

financial reforms do

matter to the foreign

ownership-bank

competition nexus.

Trung tâm Dữ liệu - Phân tích kinh tế

www.cdea.ueh.edu.vn

26

Tài liệu tham khảo

Barth, J. R., Lin, C., Ma, Y., Seade, J., & Song, F. M. (2013). Do bank regulation, supervision

and monitoring enhance or impede bank efficiency?. Journal of Banking & Finance,

37(8), 2879-2892.

Bhagat, S., Bolton, B., & Lu, J. (2015). Size, leverage, and risk-taking of financial institutions.

Journal of Banking & Finance, 59, 520-537.

Chen, P. F., & Zeng, J. H. (2014). Asymmetric effects of households’ financial participation on

banking diversification. Journal of Financial Stability, 13, 18-29.

Djalilov, K., & Piesse, J. (2016). Determinants of bank profitability in transition countries: What

matters most?. Research in International Business and Finance, 38, 69-82.

Fazio, D. M., Tabak, B. M., & Cajueiro, D. O. (2015). Inflation targeting: Is IT to blame for

banking system instability?. Journal of Banking & Finance, 59, 76-97.

Ho, P. H., Lin, C. Y., & Tsai, W. C. (2016). Effect of country governance on bank privatization

performance. International Review of Economics & Finance, 43, 3-18.

Lee, C., Hsieh, M., & Yang, S. (2016). The effects of foreign ownership on competition in the

banking industry: The key role of financial reforms. Japan And The World Economy, 37-

38, 27-46.