Embed Size (px)

Citation preview

What Role for the ECB during the Great Recession?

Giuseppe De Arcangelis DiSSEc

Plan of the talk

• Organization of the ECB • The decision making mechanism • Monetary Policy in the Eurozone • Changes in monetary policy making during

the Great Recession • Some considerations on the current

monetary environment

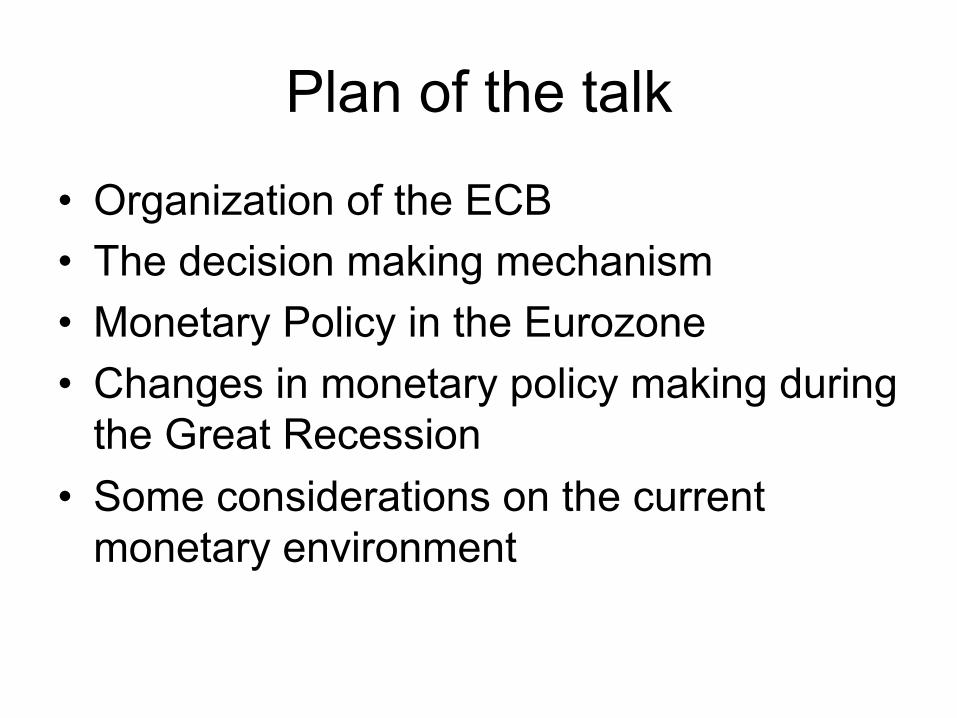

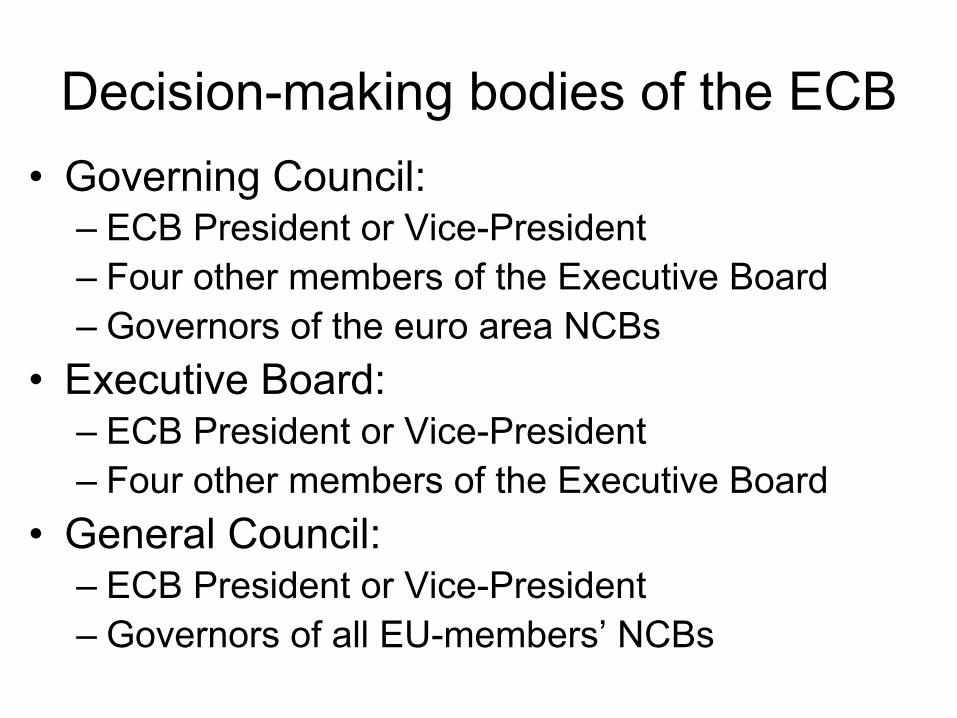

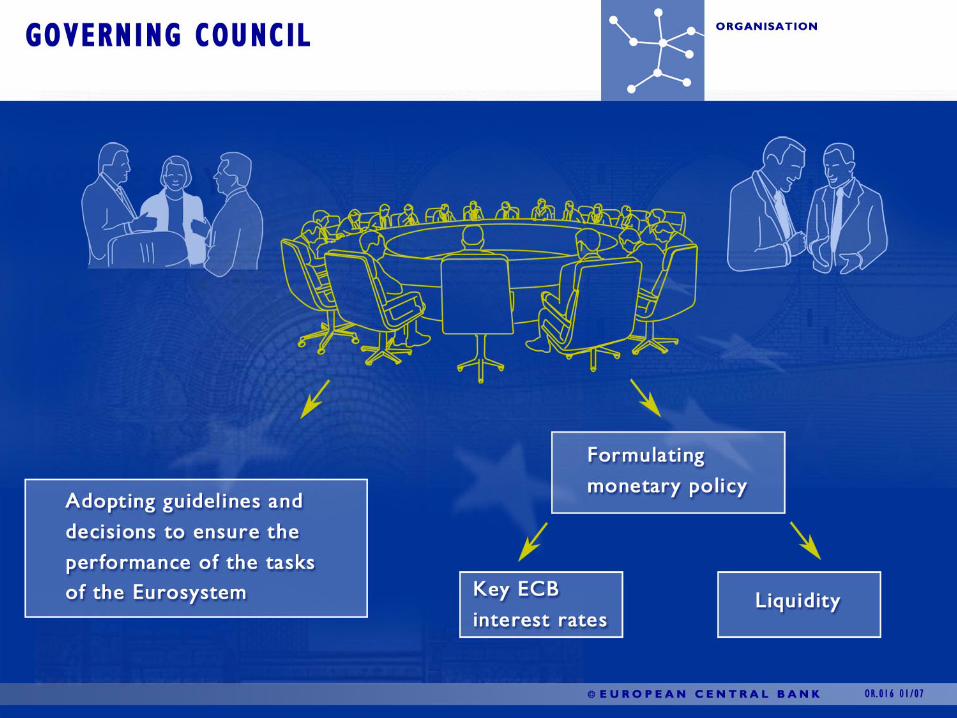

Decision-making bodies of the ECB • Governing Council:

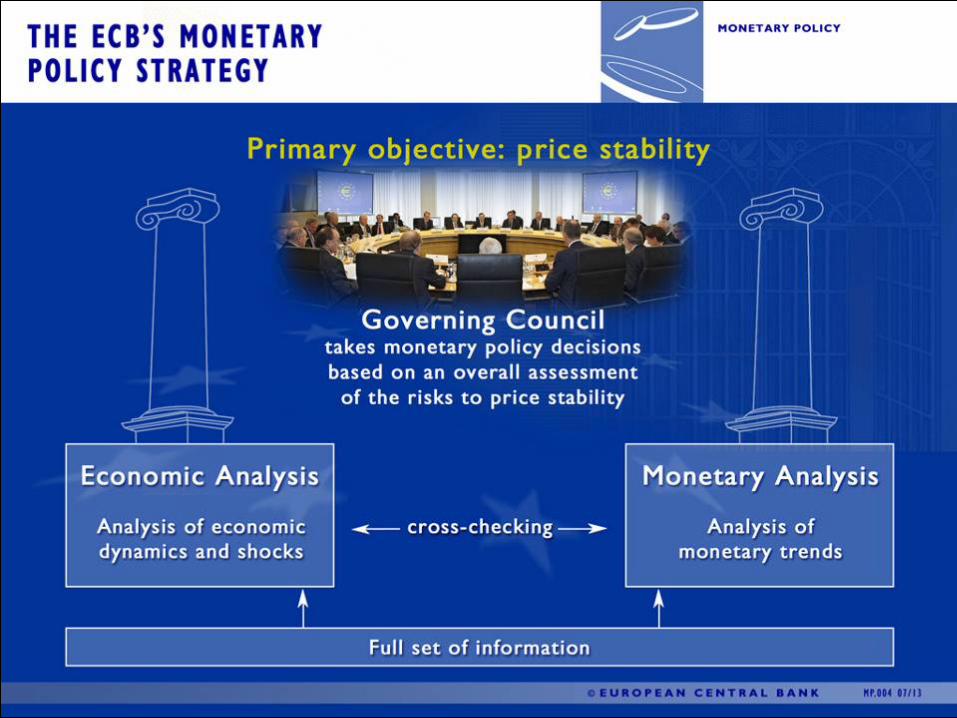

– ECB President or Vice-President – Four other members of the Executive Board – Governors of the euro area NCBs

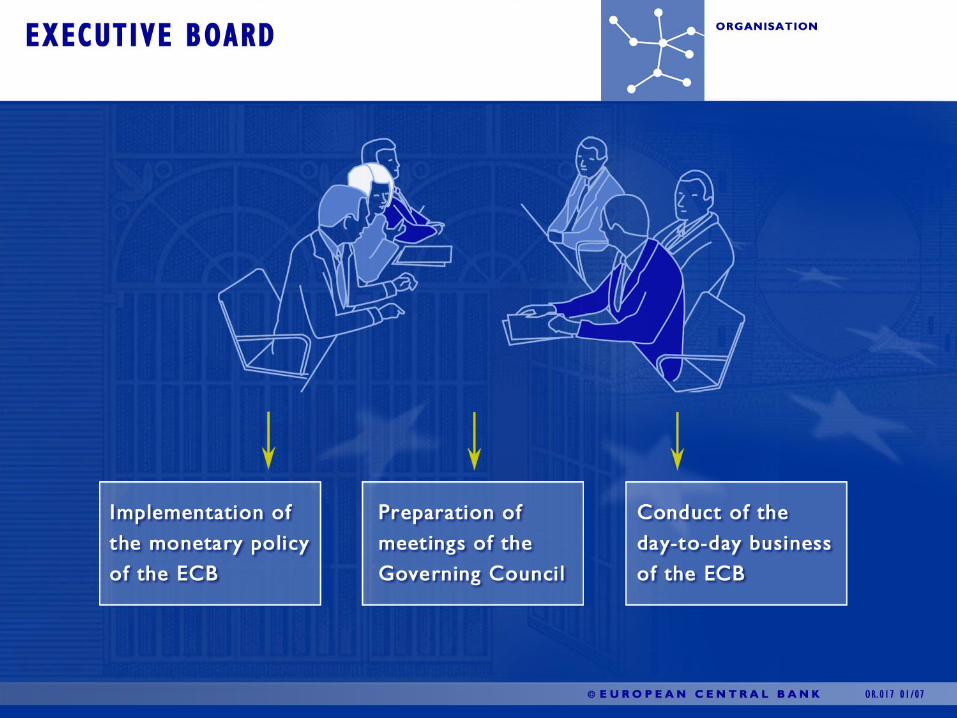

• Executive Board: – ECB President or Vice-President – Four other members of the Executive Board

• General Council: – ECB President or Vice-President – Governors of all EU-members’ NCBs

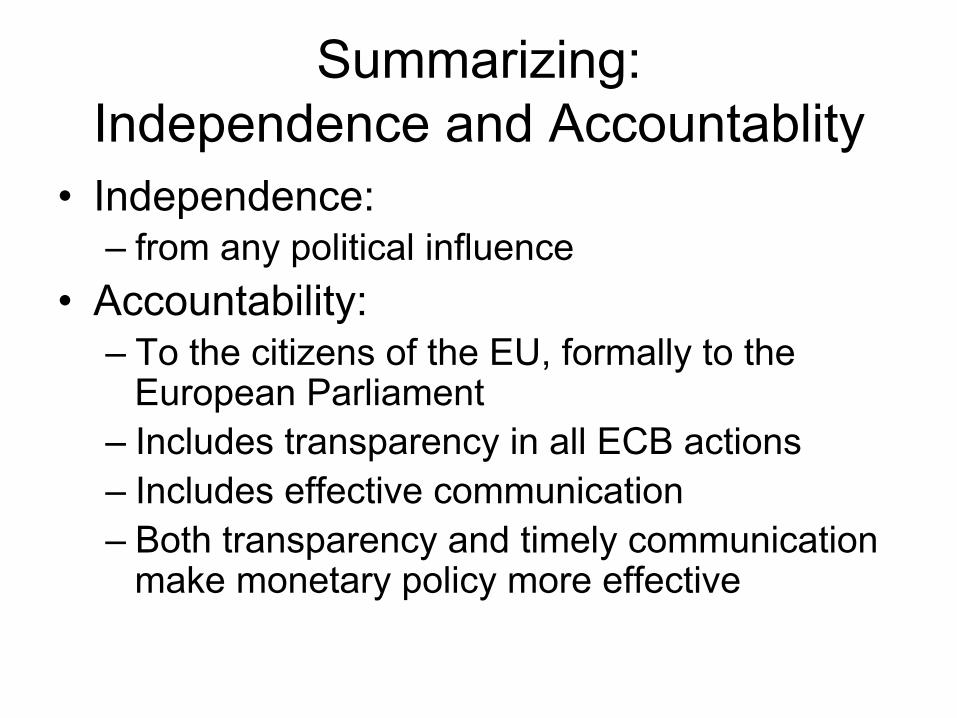

Summarizing: Independence and Accountablity

• Independence: – from any political influence

• Accountability: – To the citizens of the EU, formally to the

European Parliament – Includes transparency in all ECB actions – Includes effective communication – Both transparency and timely communication

make monetary policy more effective

Some considerations • The problem is the fragmentation of the

national money mkts: is this the right monetary policy?

• From competitive devaluations to competitive relaxed monetary policies?

• We are living in a world of low interest rates: what consequences?

• PS: The revenge of the Mundell-Fleming model and the Poole model

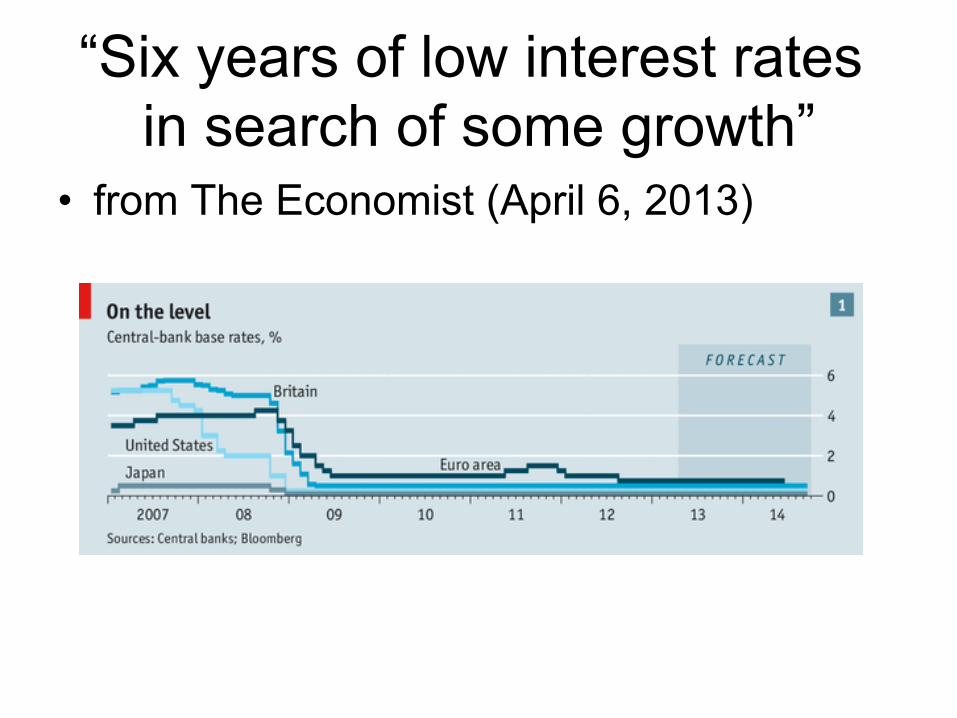

“Six years of low interest rates in search of some growth”

• from The Economist (April 6, 2013)

This is great! • Mortgages more affordable to more people à more «liquid» housing mkt à more people mobility

• Easier consumption credit, however positive signs only from the US (automobile mkt)

• Big bonanza for all debtors – including (some) sovereign debtors «instead of offering risk-free return they offer return-free risk» (Jim Grant)

Are we sure? • Cheap credit has consequences also on

other financial mkts • Savers dislike low rates of return (hate

negative real RoR) and new derivatives are (re)created and moving to more riskier investment

• Companies may engage in more riskier project and banks may be willing to lend

• Bubbles again

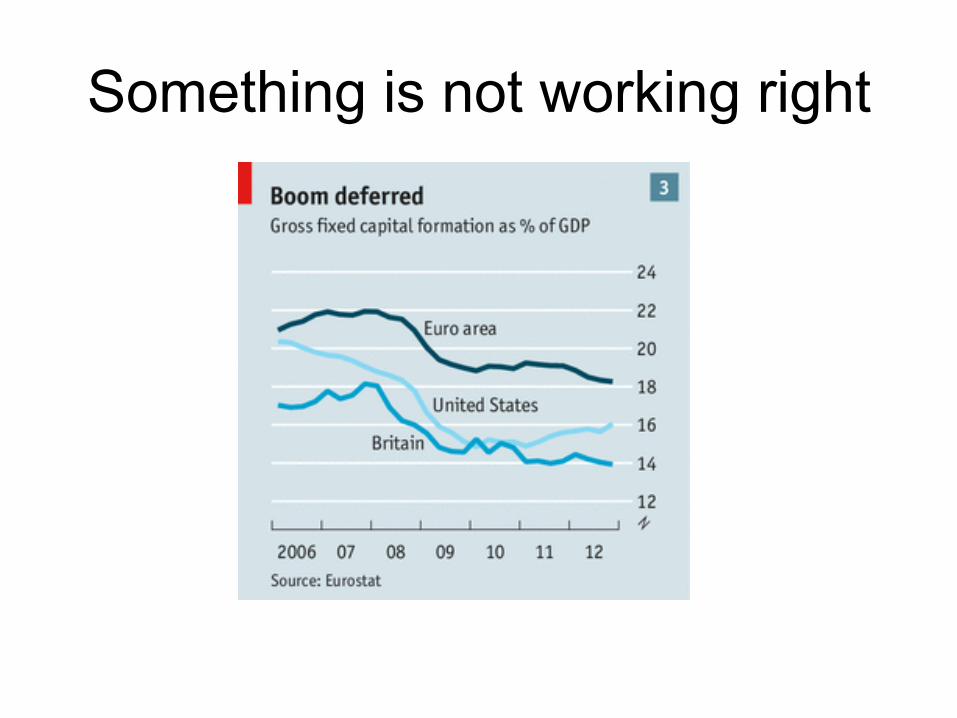

Something is not working right

Conclusions

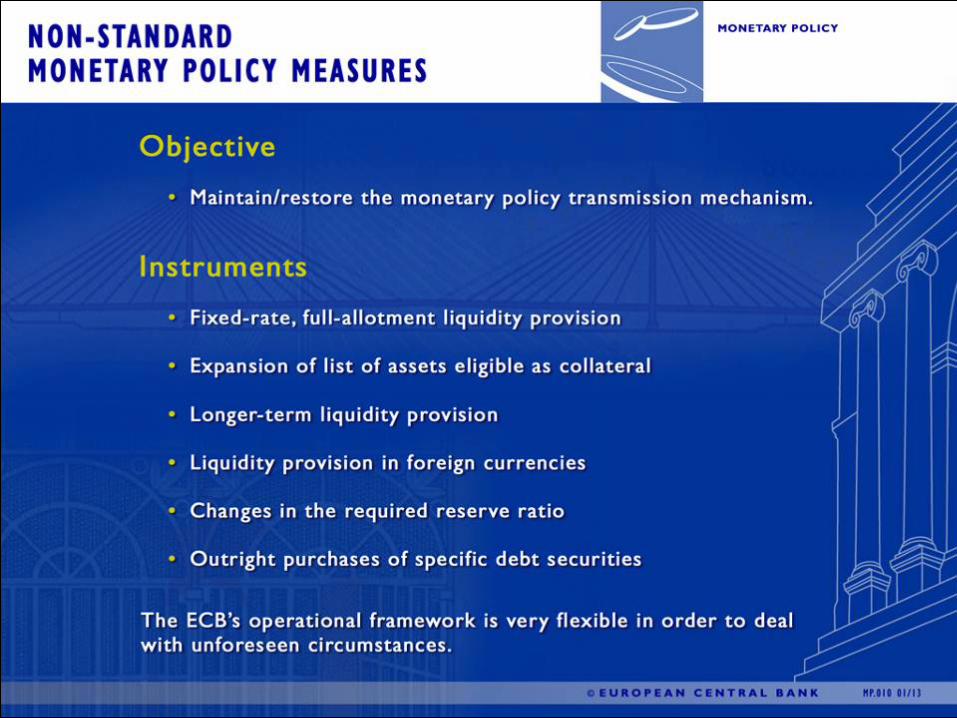

• Cheap credit from central banks may not help

• The transmission mechanism may be broken

• Large amounts of liquidity are not igniting growth

• Careful not to ignite a new bubble! • Back to the inital point?