Adaptive short term forecasting How to approach short term forecasting of multiple interdependent

time series and reduce forecasting error twice [spoiler]

A. AkimenkoMoscow’16

Contents

First glance on the data

Forecasting algorithm

Data preparation and new features

Modeling

Final results & summary

First glance on the data

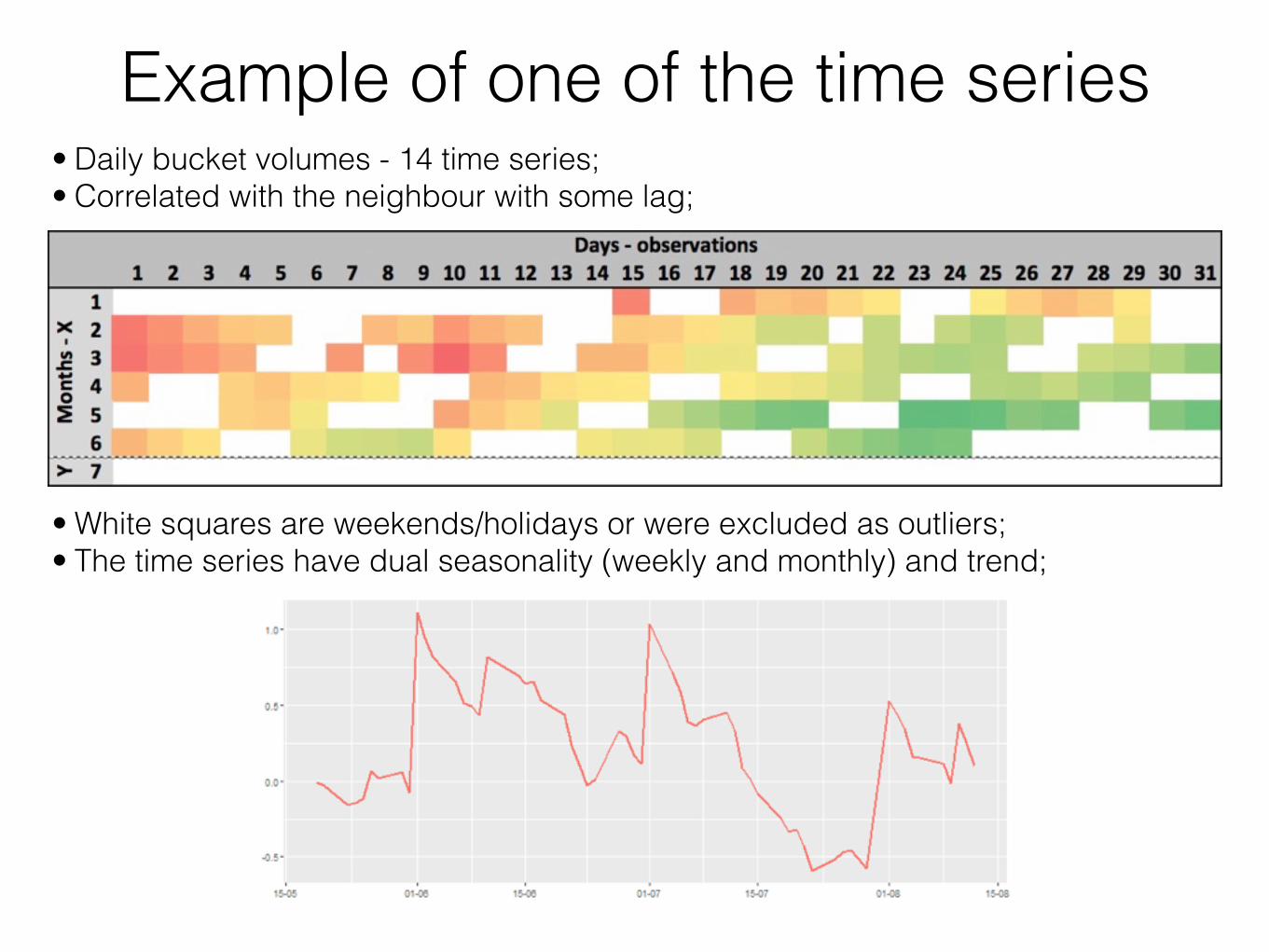

• Daily bucket volumes - 14 time series; • Correlated with the neighbour with some lag;

Example of one of the time series

• White squares are weekends/holidays or were excluded as outliers; • The time series have dual seasonality (weekly and monthly) and trend;

The task is to develop an algorithm which will predict Y for the next month for each time series with Mean

Absolute Percentage Error (MAPE) < 3%.

Forecasting algorithm

Auto-regression models and moving average (ARMA, ARIMA, GARCH)

SSA/Gusenitca

Neural networks (RNN)

Adaptive short term forecasting:• Exponential smoothing; • Seasonal and trend decomposition;• Adaptive auto-regression;

Adaptive model selection & composition

...

Auto-regression models and moving average (ARMA, ARIMA, GARCH)

SSA/Gusenitca

Neural networks (RNN)

Adaptive short term forecasting:• Exponential smoothing; • Seasonal and trend decomposition);• Adaptive auto-regression;

Adaptive model selection & composition

...

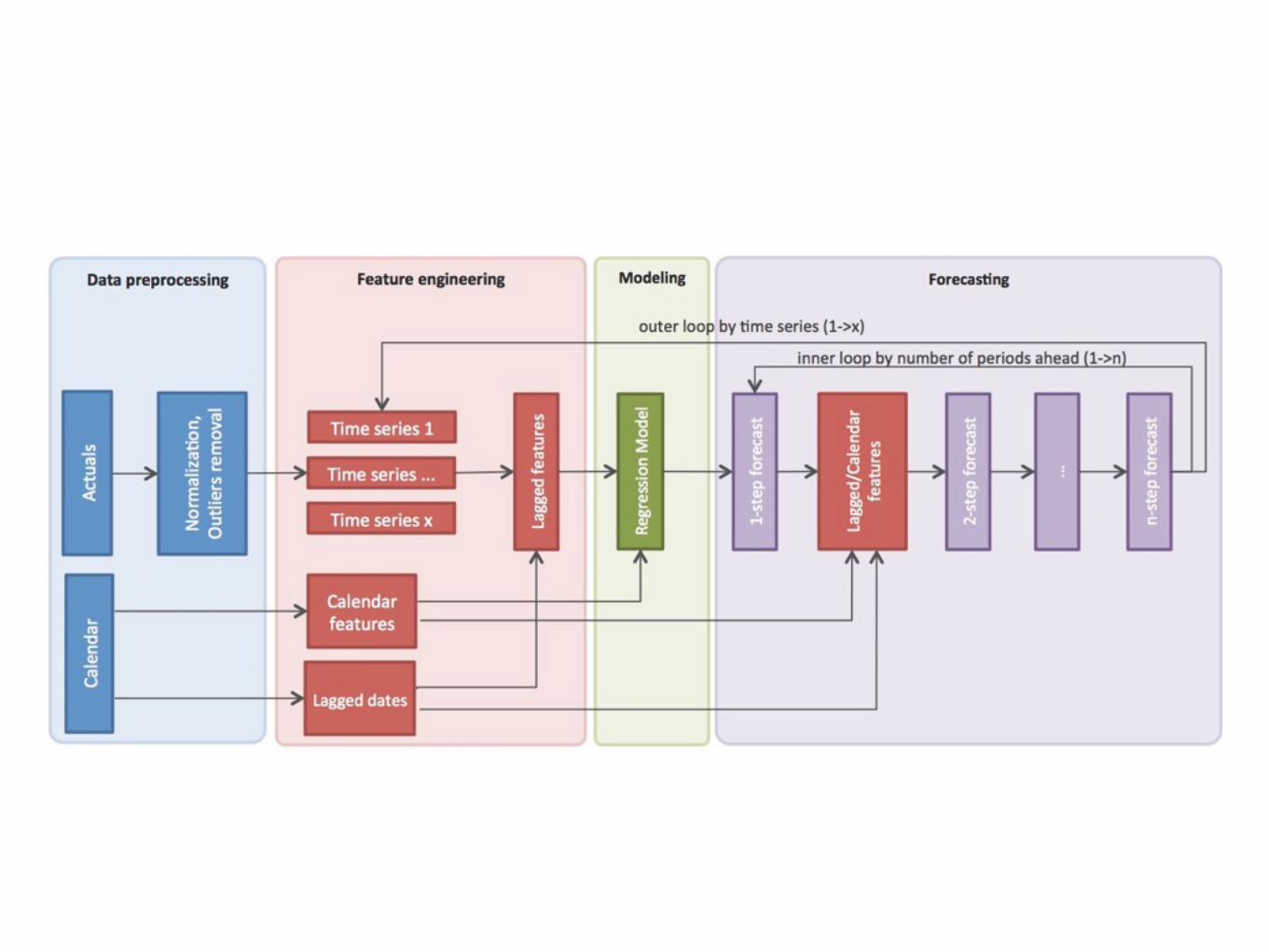

Data preparation and new features

Normalization

Outliers

Observation period

Lagged features

Calendar features

Weighing

Modeling

Regular Linear Model

Penalized Linear Model

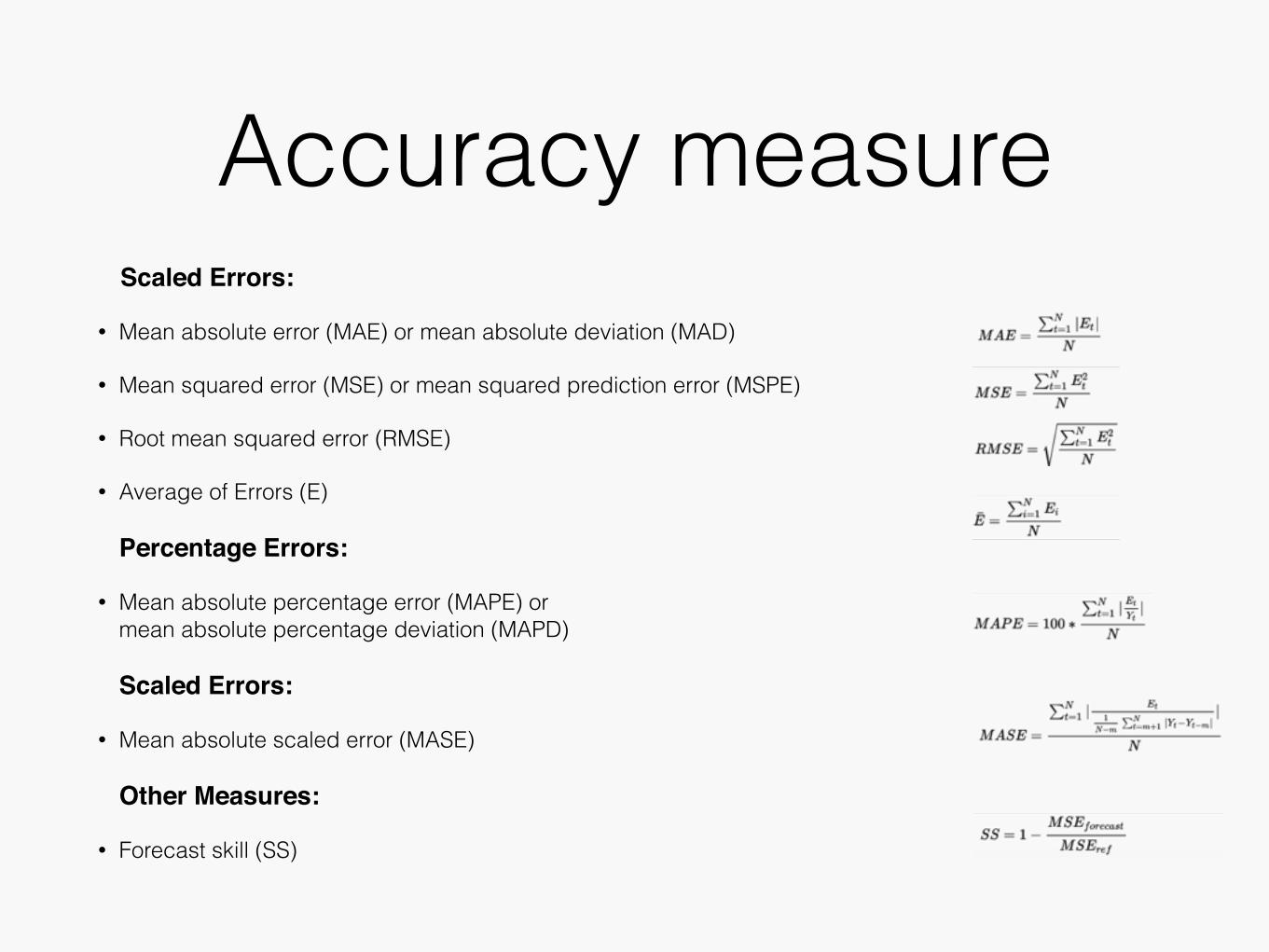

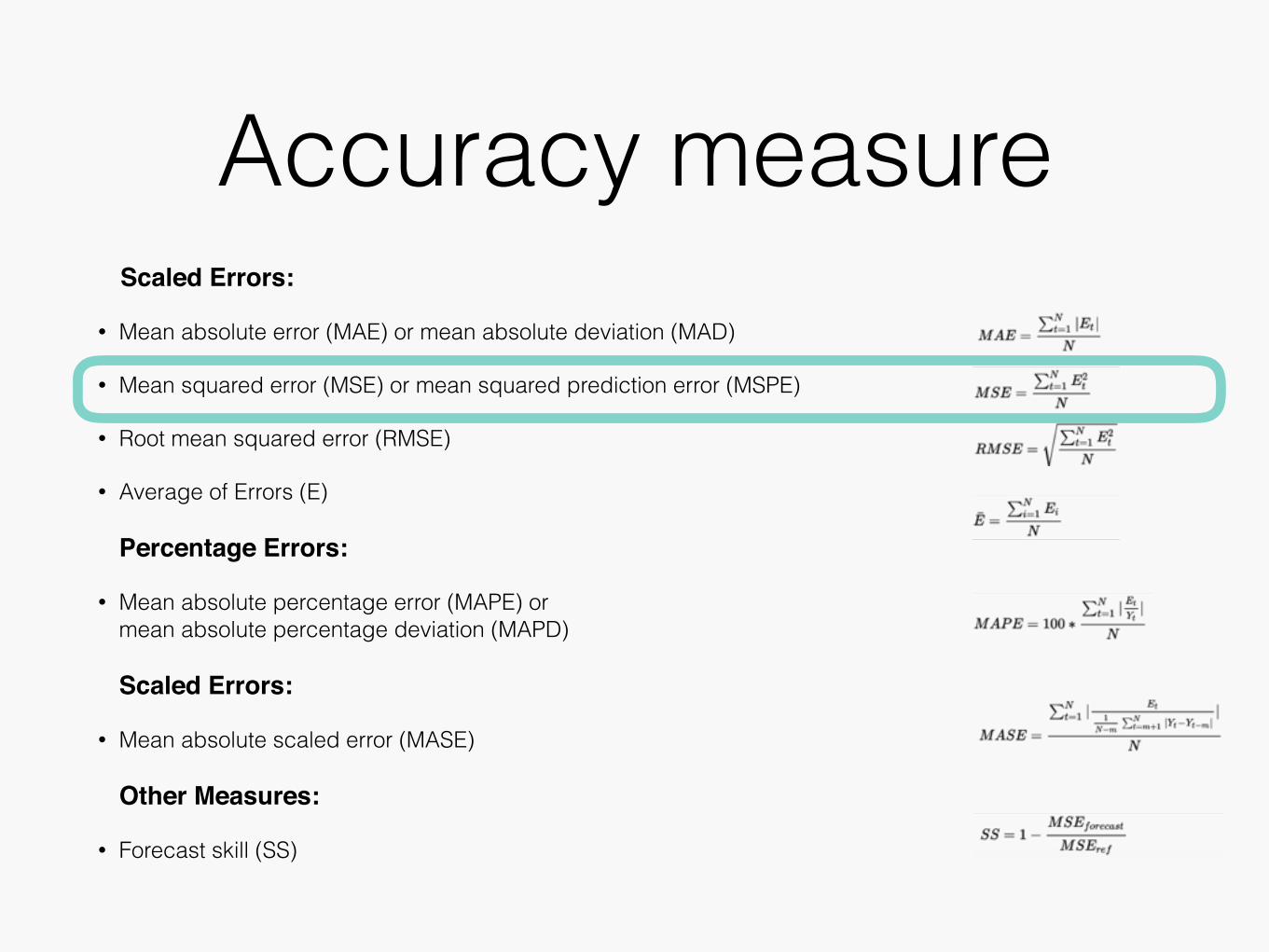

Accuracy measureScaled Errors:

• Mean absolute error (MAE) or mean absolute deviation (MAD)

• Mean squared error (MSE) or mean squared prediction error (MSPE)

• Root mean squared error (RMSE)

• Average of Errors (E)

Percentage Errors:

• Mean absolute percentage error (MAPE) or mean absolute percentage deviation (MAPD)

Scaled Errors:

• Mean absolute scaled error (MASE)

Other Measures:

• Forecast skill (SS)

Accuracy measureScaled Errors:

• Mean absolute error (MAE) or mean absolute deviation (MAD)

• Mean squared error (MSE) or mean squared prediction error (MSPE)

• Root mean squared error (RMSE)

• Average of Errors (E)

Percentage Errors:

• Mean absolute percentage error (MAPE) or mean absolute percentage deviation (MAPD)

Scaled Errors:

• Mean absolute scaled error (MASE)

Other Measures:

• Forecast skill (SS)

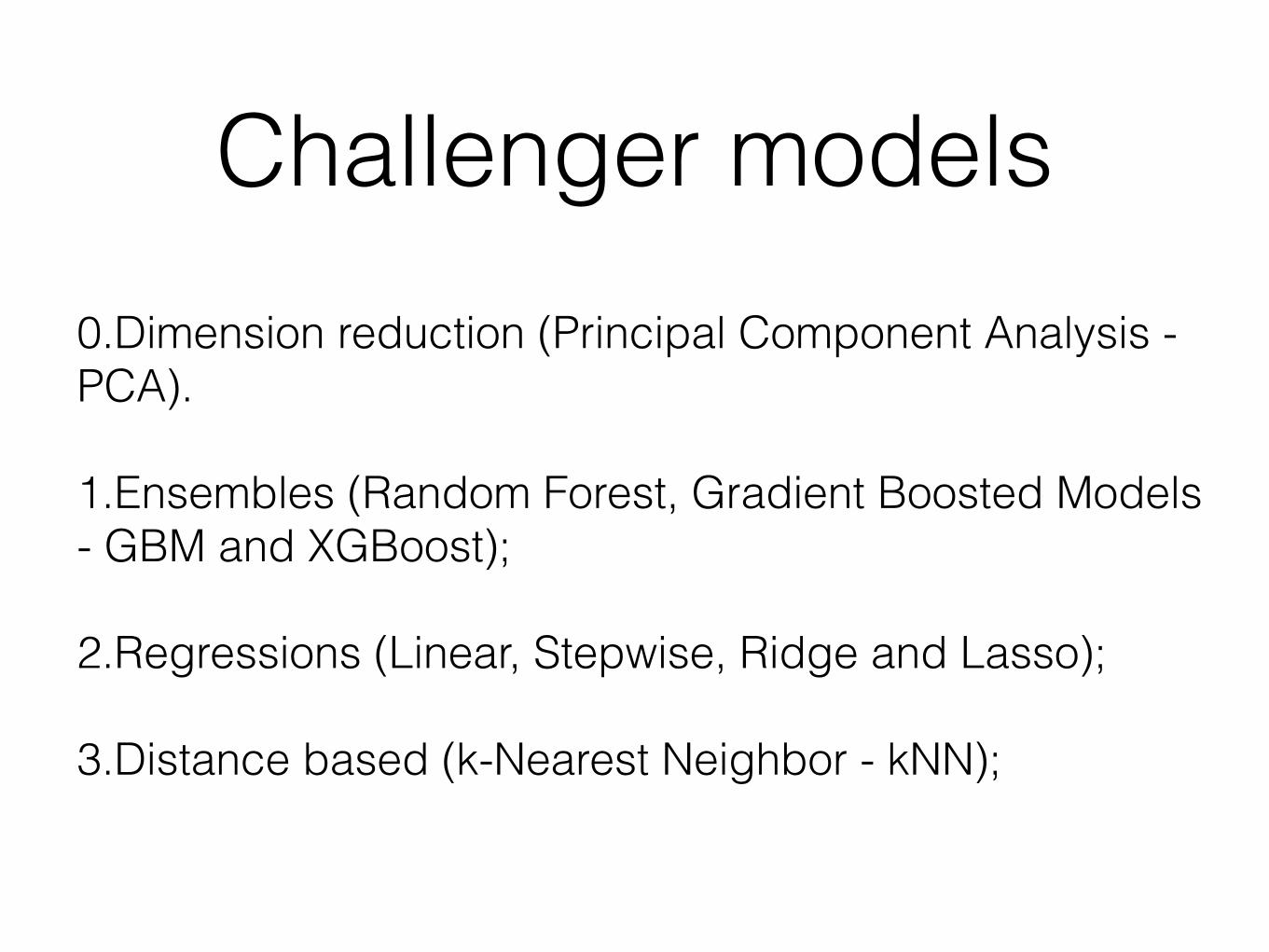

Challenger models0.Dimension reduction (Principal Component Analysis - PCA).

1.Ensembles (Random Forest, Gradient Boosted Models - GBM and XGBoost);

2.Regressions (Linear, Stepwise, Ridge and Lasso);

3.Distance based (k-Nearest Neighbor - kNN);

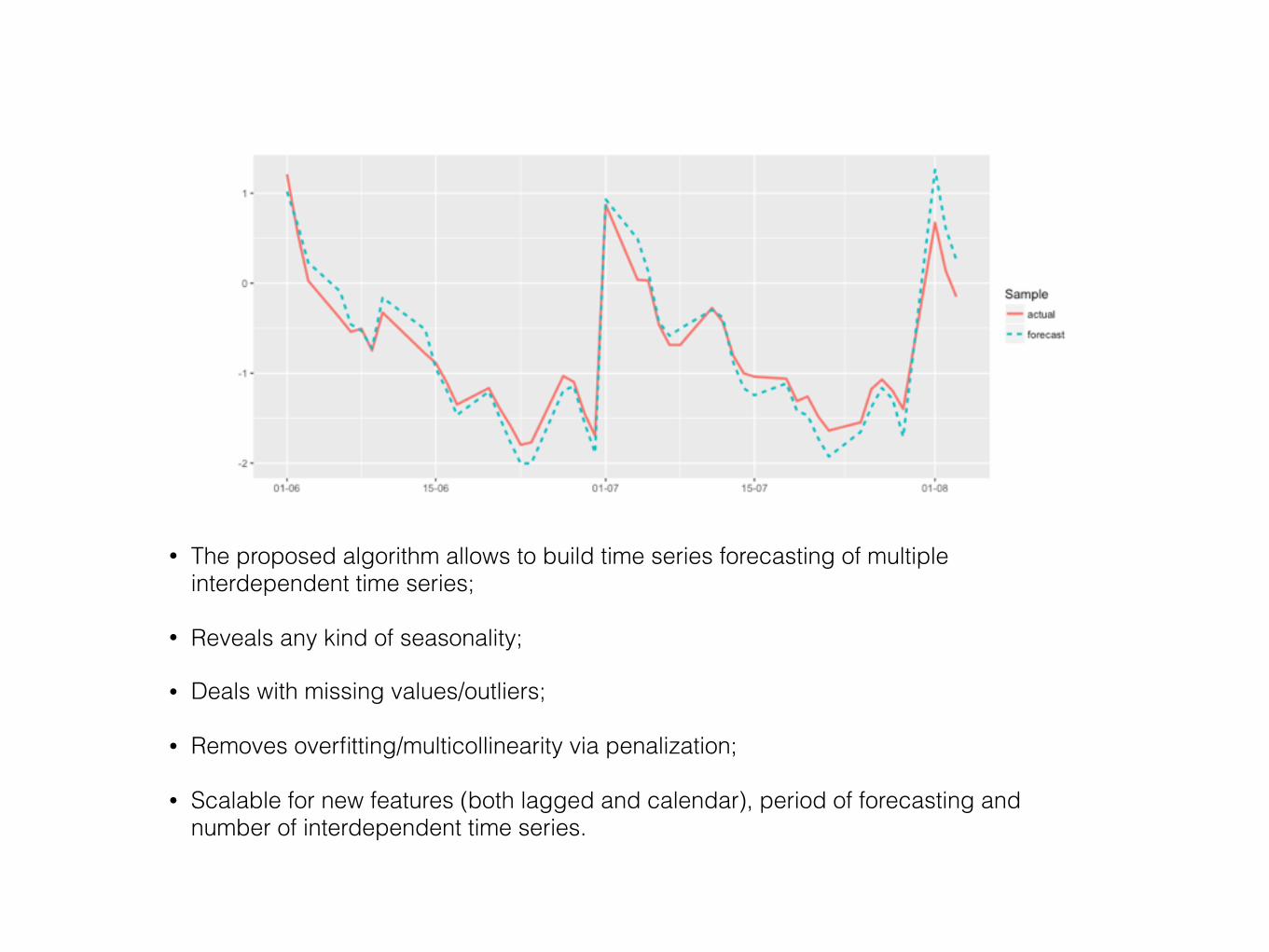

Final results & summary

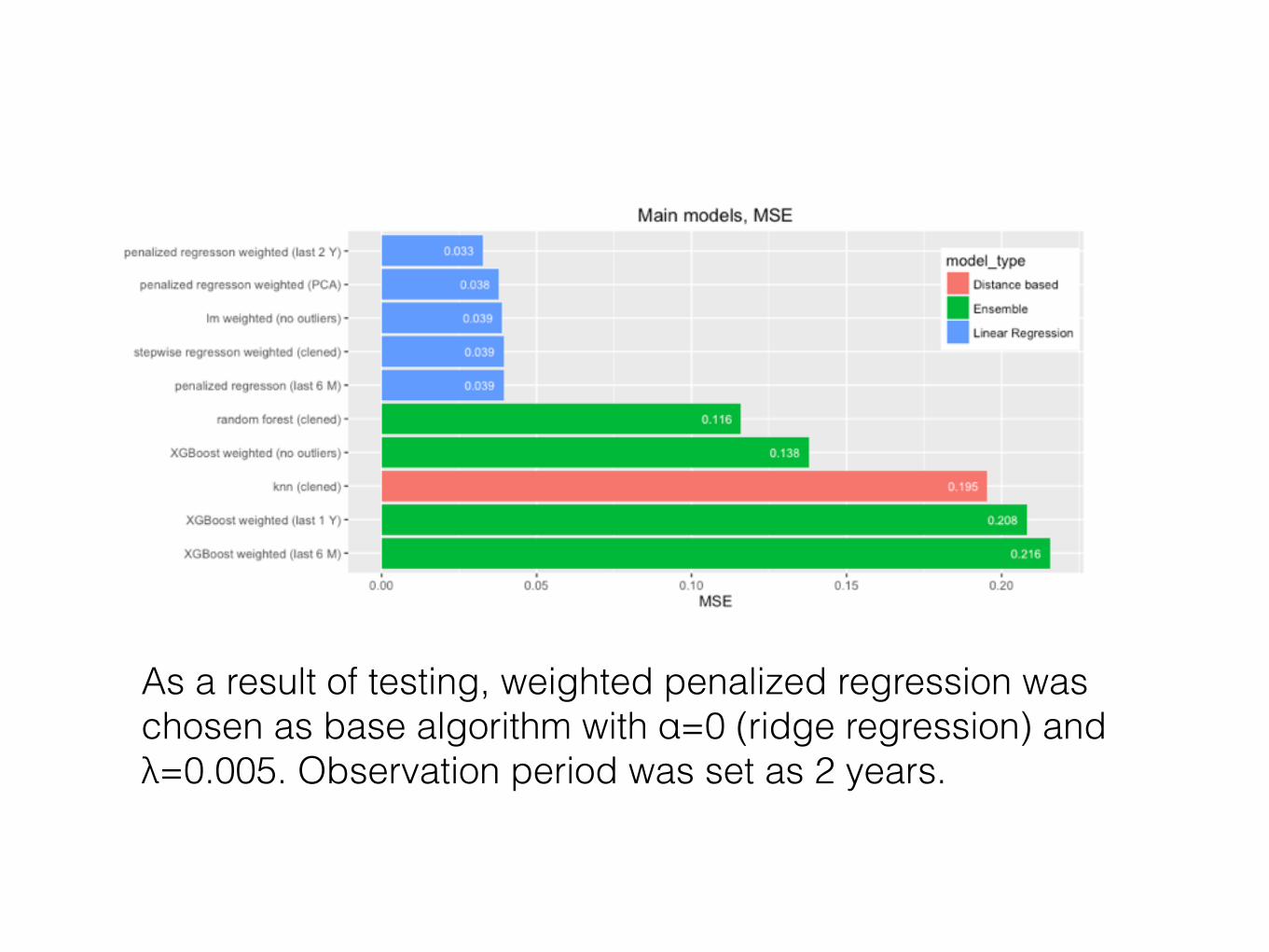

As a result of testing, weighted penalized regression was chosen as base algorithm with α=0 (ridge regression) and λ=0.005. Observation period was set as 2 years.

• The proposed algorithm allows to build time series forecasting of multiple interdependent time series;

• Reveals any kind of seasonality;

• Deals with missing values/outliers;

• Removes overfitting/multicollinearity via penalization;

• Scalable for new features (both lagged and calendar), period of forecasting and number of interdependent time series.

Thank you for your attention!

Full research is available here: https://alexakimenko.github.io/time_series/2016/09/18/adaptive-short-term-forecasting/

Recommended