Diversification and Portfolios

Economics 71a: Spring 2007

Mayo chapter 8Malkiel, Chap 9-10Lecture notes 3.2b

Goals

Portfolios and correlationsDiversifiable versus nondiversifiable riskCAPM and Beta

Capital asset pricing model Is the CAPM really useful?Asset allocation

Risk: Individual->Portfolio

Early models Risk is based on each individual stock

Modern approaches Consider how it effects “portfolio” of

holdings Markowitz Modern portfolio theory Diversification

Diversification and Portfolios

“Don’t put all your eggs in one basket”Buying a large set of securities can

reduce risk

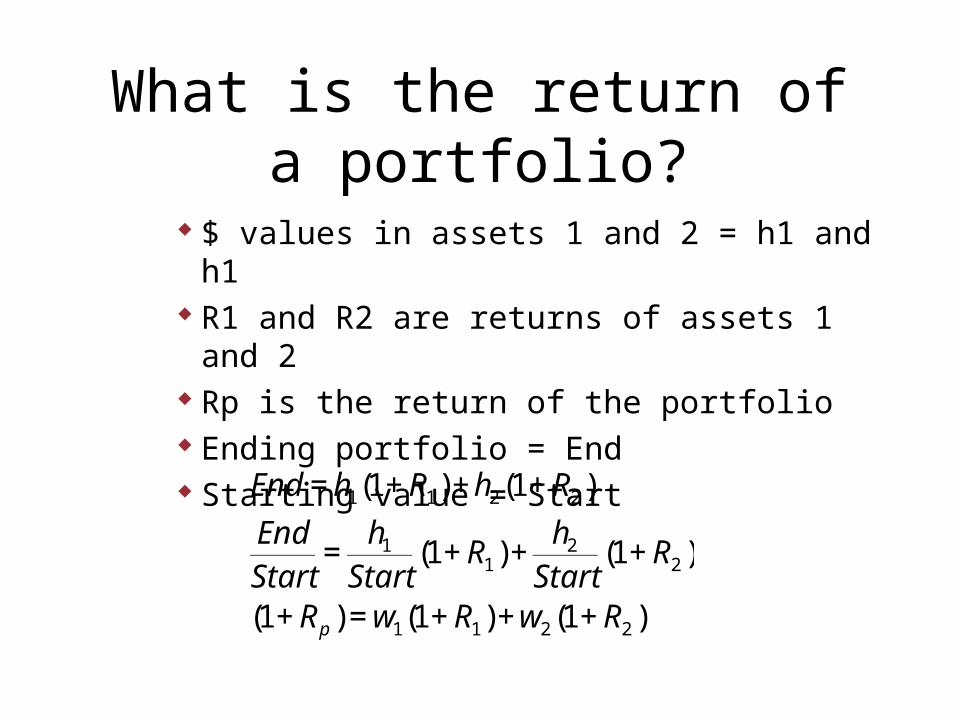

What is the return of a portfolio?

$ values in assets 1 and 2 = h1 and h1 R1 and R2 are returns of assets 1 and 2 Rp is the return of the portfolio Ending portfolio = End Starting value = Start

€

End = h1(1+ R1)+h2(1+ R2 )

EndStart

=h1

Start(1+ R1)+

h2

Start(1+ R2 )

(1+ Rp ) =w1(1+ R1)+w2(1+ R2 )

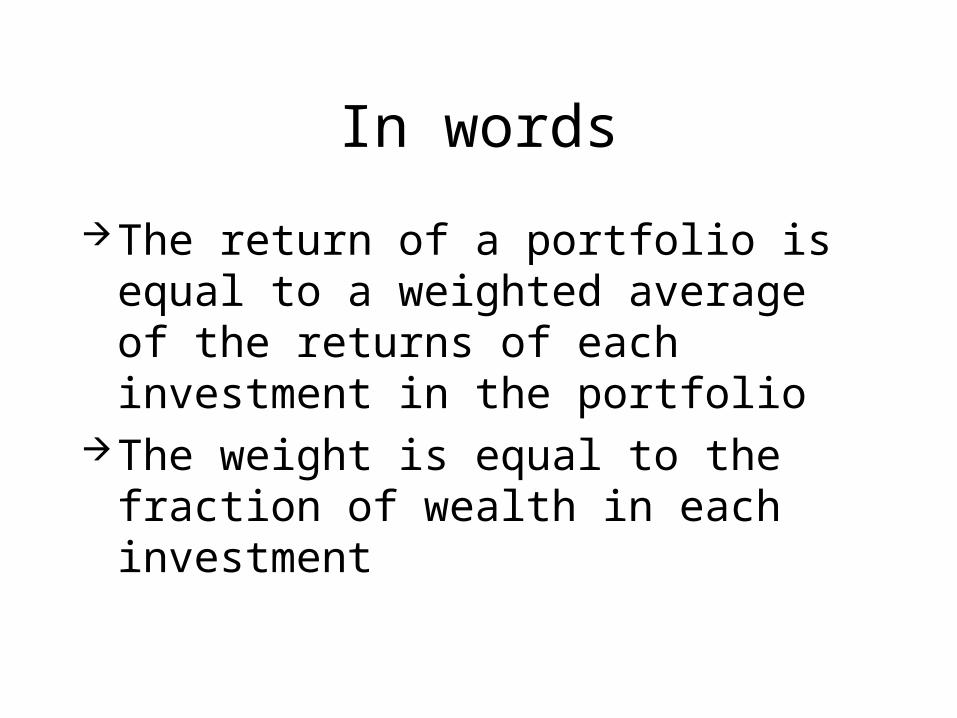

In words

The return of a portfolio is equal to a weighted average of the returns of each investment in the portfolio

The weight is equal to the fraction of wealth in each investment

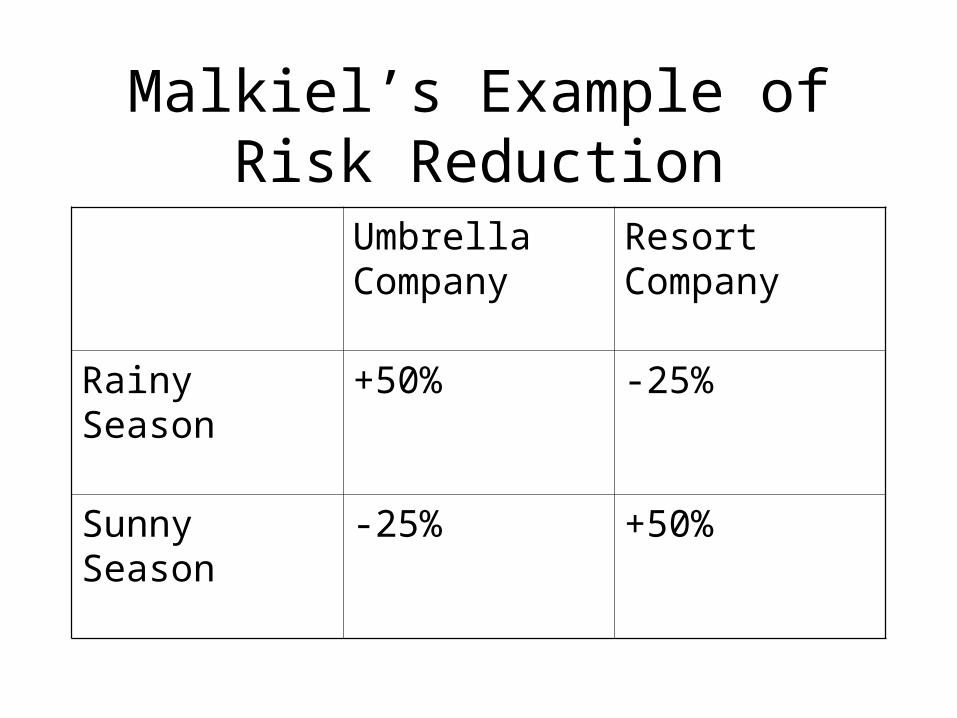

Malkiel’s Example of Risk ReductionUmbrella Company

Resort Company

Rainy Season +50% -25%

Sunny Season -25% +50%

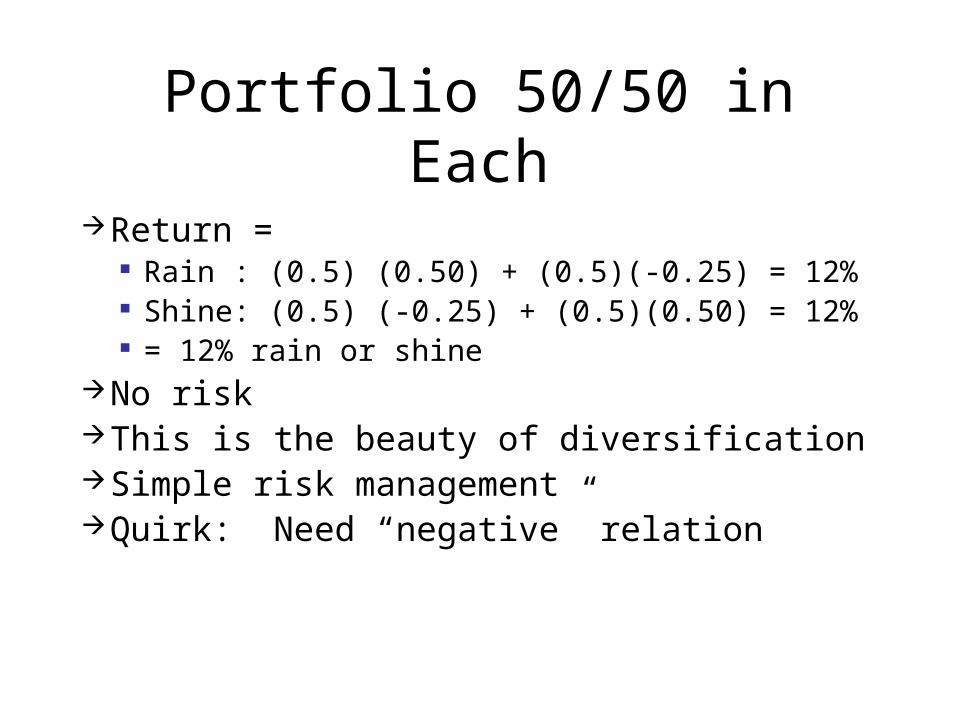

Portfolio 50/50 in Each

Return = Rain : (0.5) (0.50) + (0.5)(-0.25) = 12% Shine: (0.5) (-0.25) + (0.5)(0.50) = 12% = 12% rain or shine

No riskThis is the beauty of diversificationSimple risk managementQuirk: Need “negative” relation

What is going on?

Asset returns have perfect “negative correlation”

They move exactly opposite to each other

Is this always necessary? No

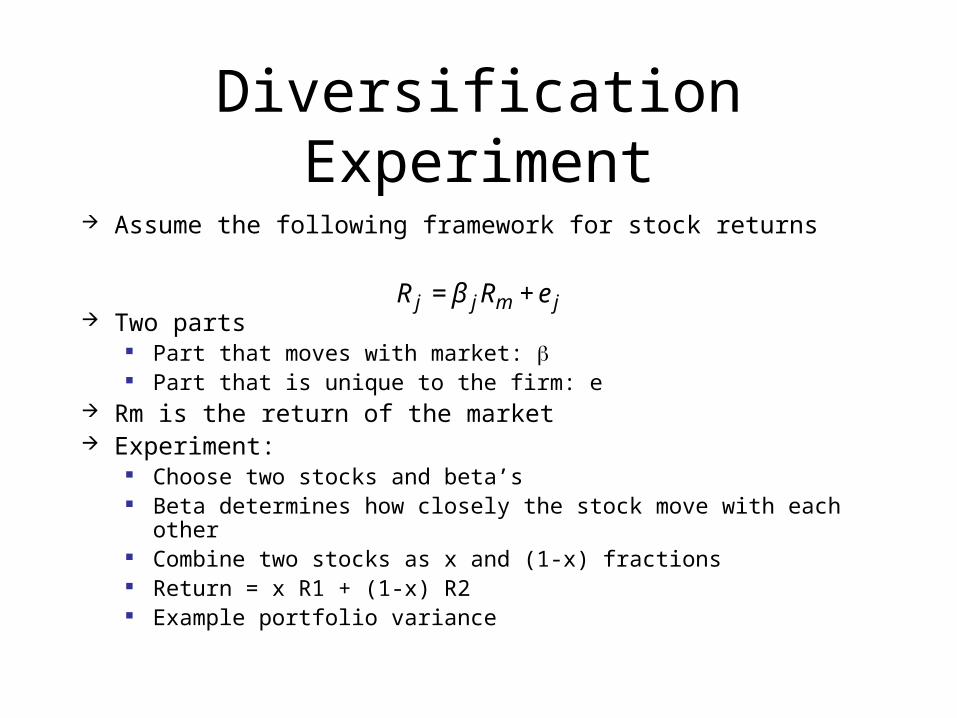

Diversification Experiment

Assume the following framework for stock returns

Two parts Part that moves with market: Part that is unique to the firm: e

Rm is the return of the market Experiment:

Choose two stocks and beta’s Beta determines how closely the stock move with each other Combine two stocks as x and (1-x) fractions Return = x R1 + (1-x) R2 Example portfolio variance

€

R j = β jRm + e j

Web Examples

See multi-Beta scatter plots Portfolio 2

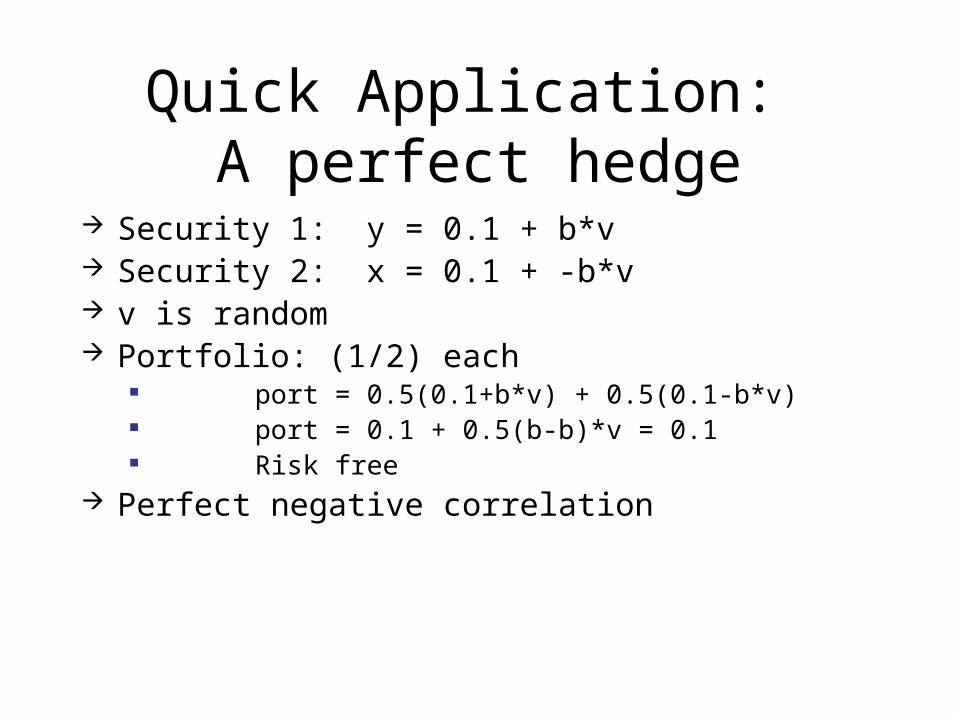

Quick Application: A perfect hedge

Security 1: y = 0.1 + b*v Security 2: x = 0.1 + -b*v v is random Portfolio: (1/2) each

port = 0.5(0.1+b*v) + 0.5(0.1-b*v) port = 0.1 + 0.5(b-b)*v = 0.1 Risk free

Perfect negative correlation

Summary: Portfolio Theory

A radically new approach to risk In the 1950’s

Two key points Diversification matters Worry about how an investment moves

with the rest of your portfolio Worry more about correlations than

standard deviations and variances

Goals

Portfolios and correlationsDiversifiable versus nondiversifiable riskCAPM and Beta

Capital asset pricing model Is the CAPM really useful?

Nondiversifiable Risk

Many equity returns are positively correlated

What does that mean to our new thoughts on risk?

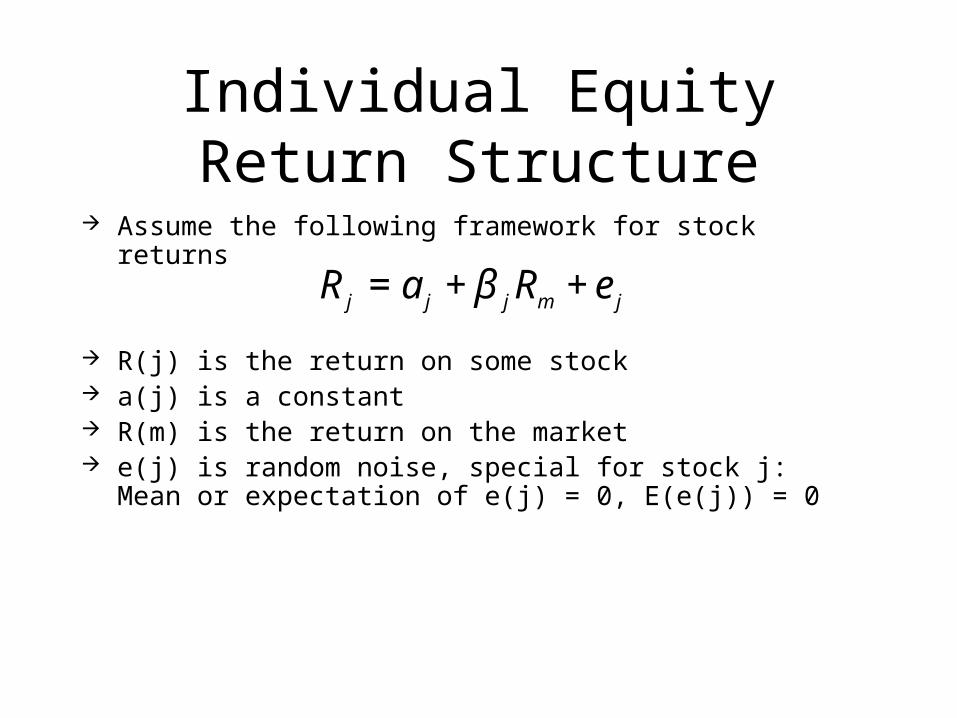

Individual Equity Return Structure

Assume the following framework for stock returns

R(j) is the return on some stock a(j) is a constant R(m) is the return on the market e(j) is random noise, special for stock j: Mean or expectation of

e(j) = 0, E(e(j)) = 0€

R j = a j + β jRm + e j

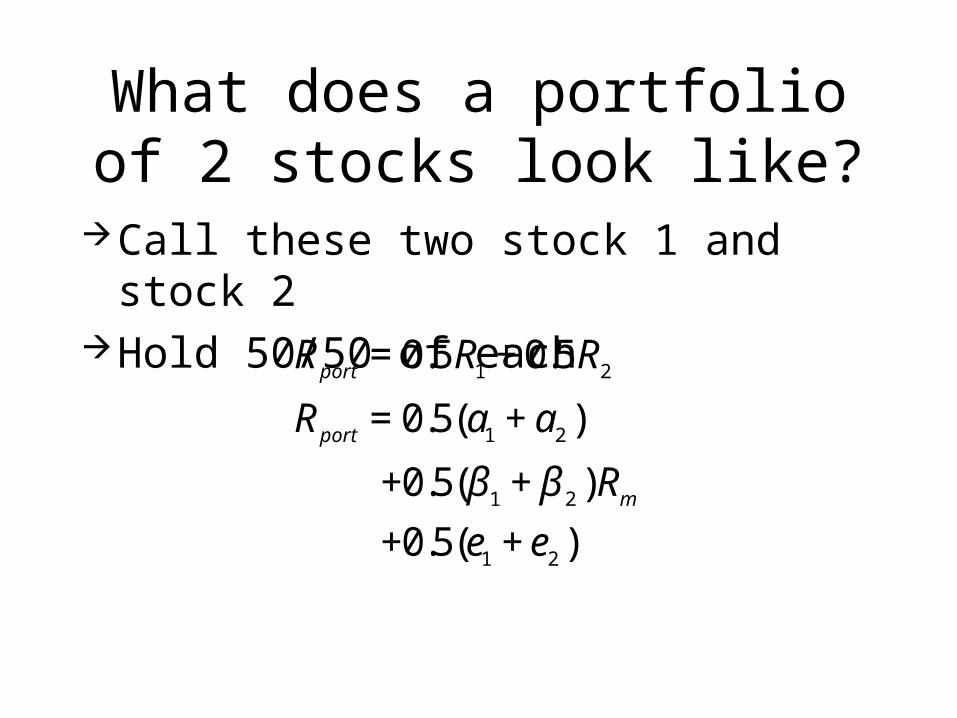

What does a portfolio of 2 stocks look like?

Call these two stock 1 and stock 2Hold 50/50 of each

€

Rport = 0.5R1 + 0.5R2

Rport = 0.5(a1 + a2 )

+0.5(β1 + β 2 )Rm+0.5(e1 + e2 )

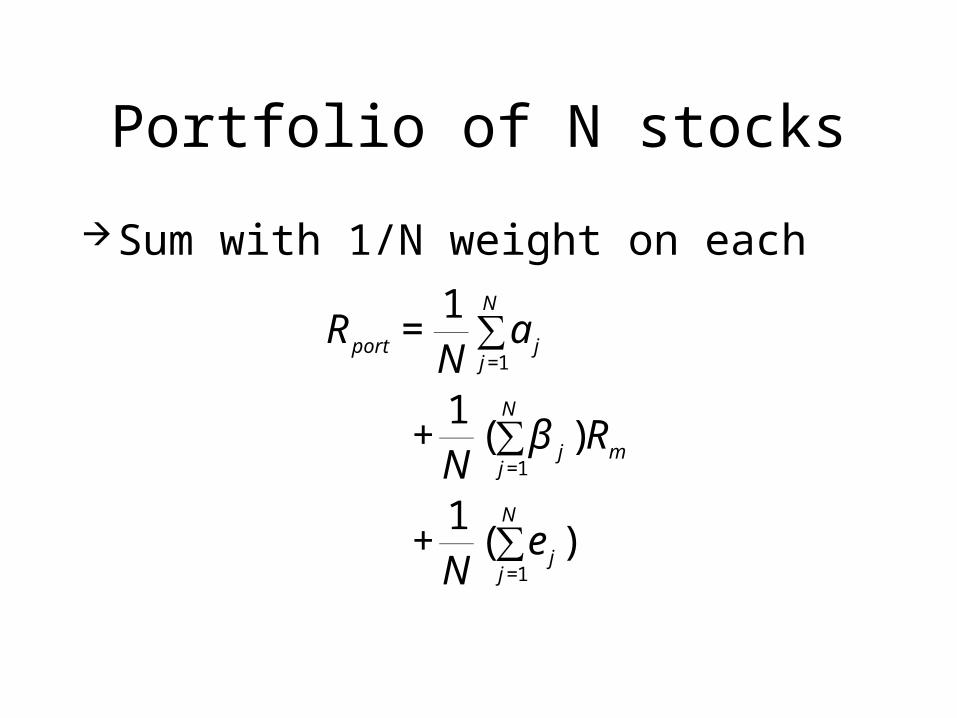

Portfolio of N stocks

Sum with 1/N weight on each

€

Rport =1N

a jj=1

N

∑

+1N

( β jj=1

N

∑ )Rm

+1N

( e jj=1

N

∑ )

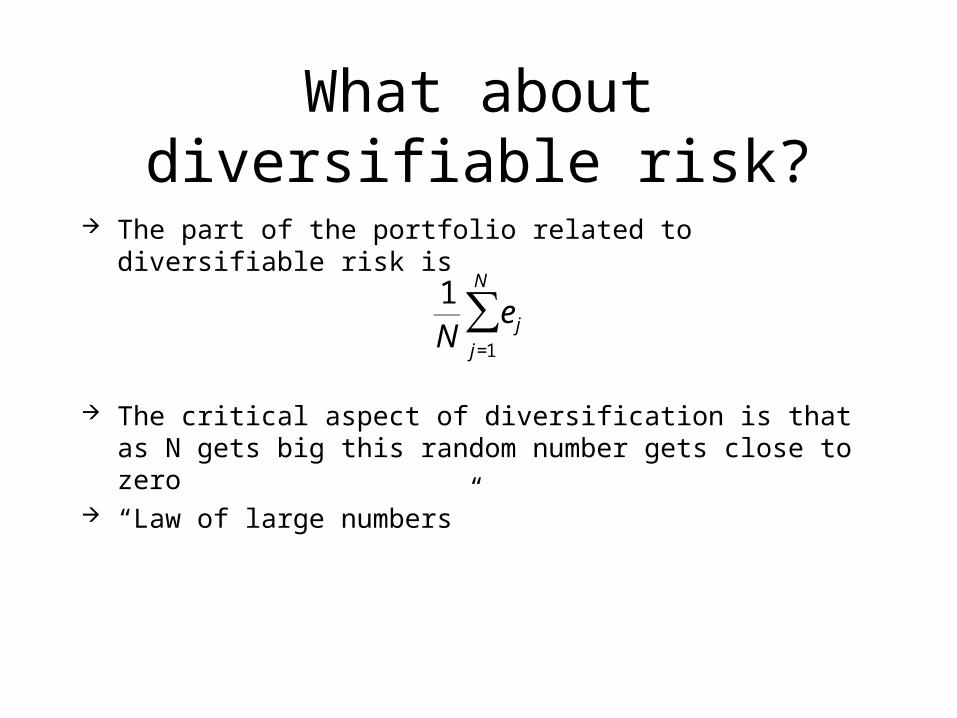

What about diversifiable risk?

The part of the portfolio related to diversifiable risk is

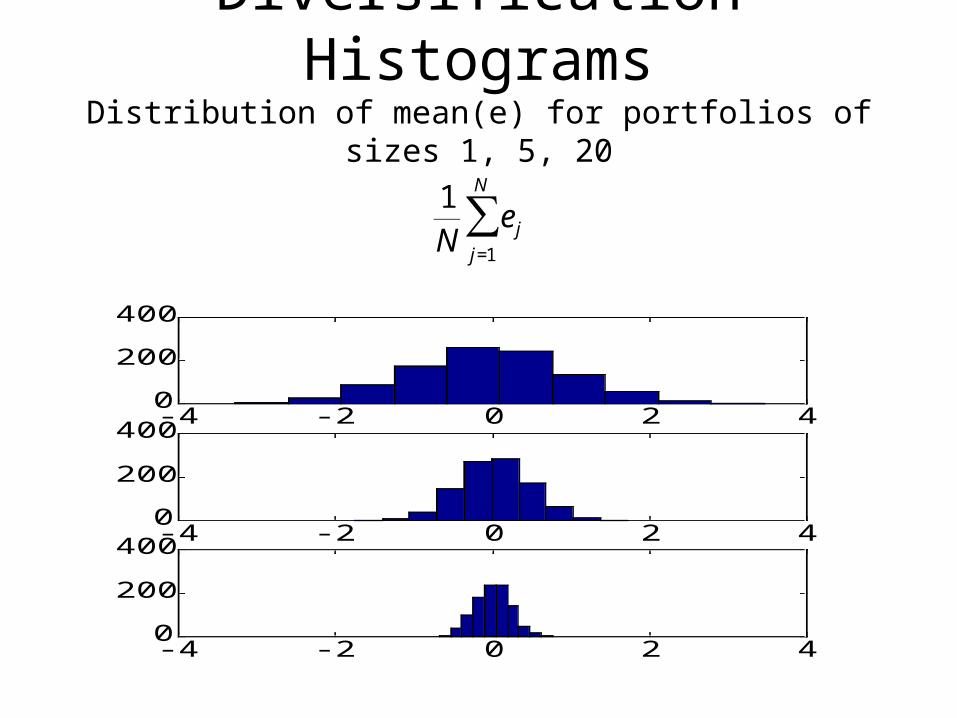

The critical aspect of diversification is that as N gets big this random number gets close to zero

“Law of large numbers”€

1N

ejj=1

N

∑

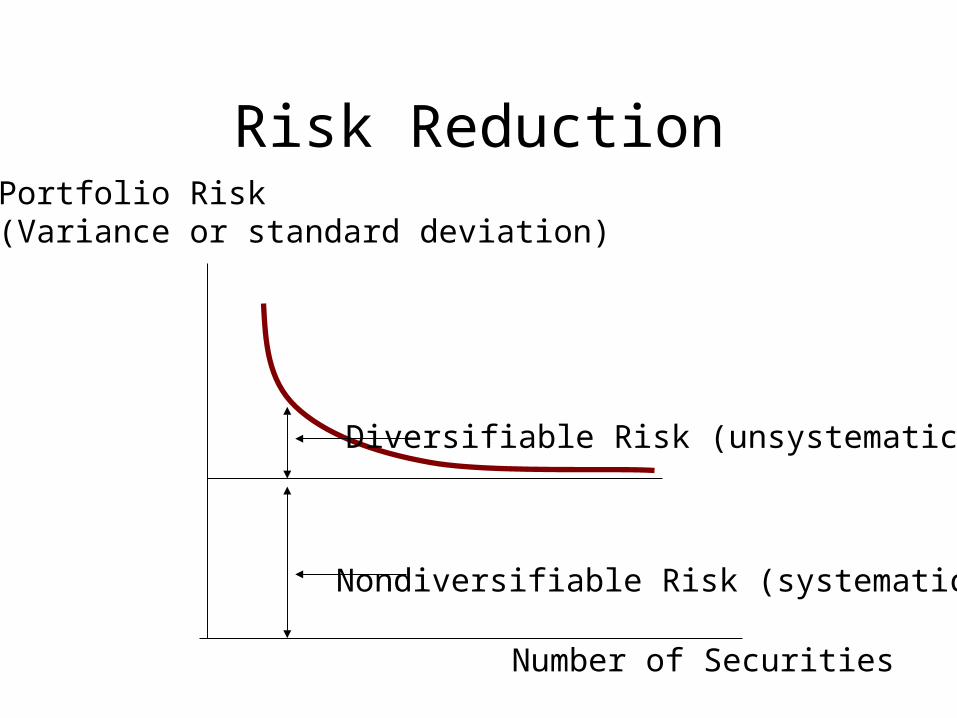

Risk Reduction

Number of Securities

Portfolio Risk(Variance or standard deviation)

Nondiversifiable Risk (systematic)

Diversifiable Risk (unsystematic)

Why?

This is a little like going to a casino, and playing roulette

You bet on red many, many timesKeep track of W/(W+L)As you play more and more this gets

very close to 0.5

Diversification HistogramsDistribution of mean(e) for portfolios of sizes 1, 5, 20

-4 -2 0 2 40

200

400

-4 -2 0 2 40

200

400

-4 -2 0 2 40

200

400

€

1N

ejj=1

N

∑

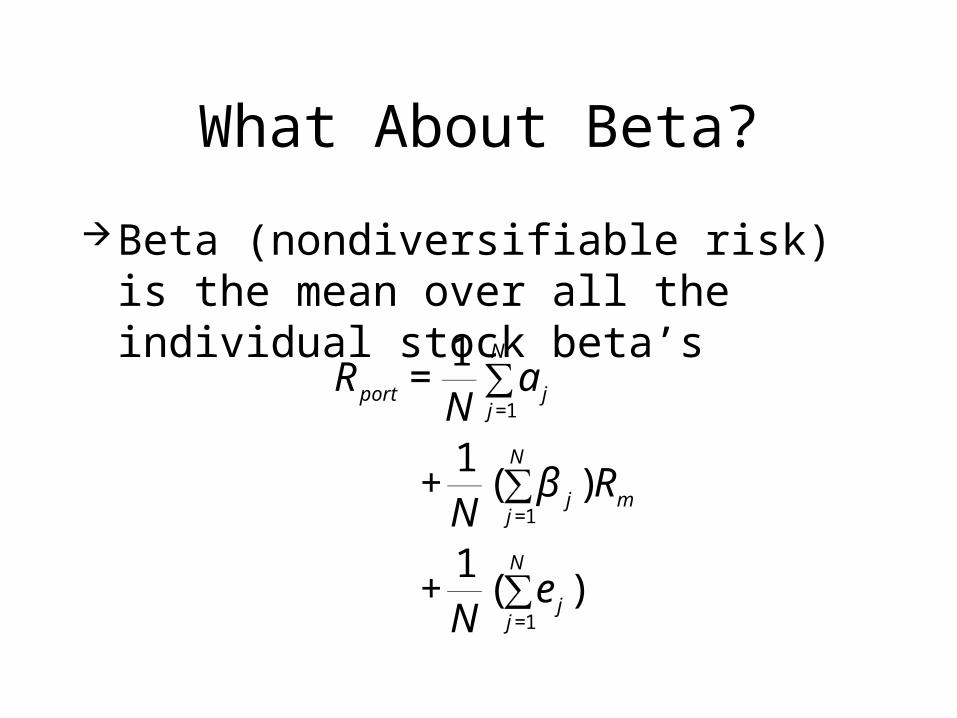

What About Beta?

Beta (nondiversifiable risk) is the mean over all the individual stock beta’s

€

Rport =1N

a jj=1

N

∑

+1N

( β jj=1

N

∑ )Rm

+1N

( e jj=1

N

∑ )

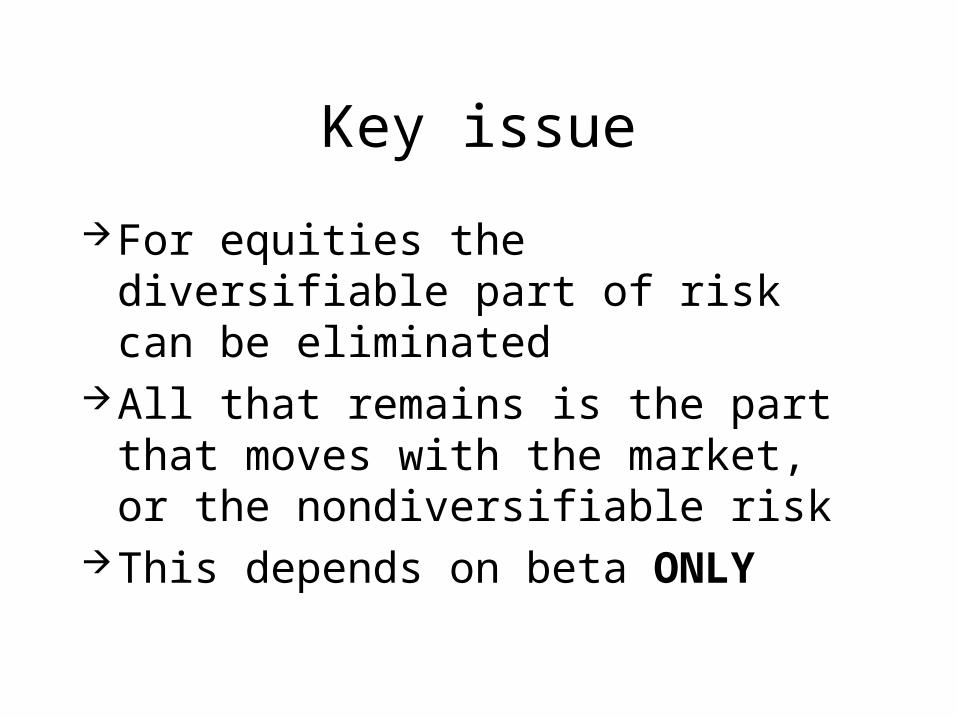

Key issue

For equities the diversifiable part of risk can be eliminated

All that remains is the part that moves with the market, or the nondiversifiable risk

This depends on beta ONLY

Java Example

See web example

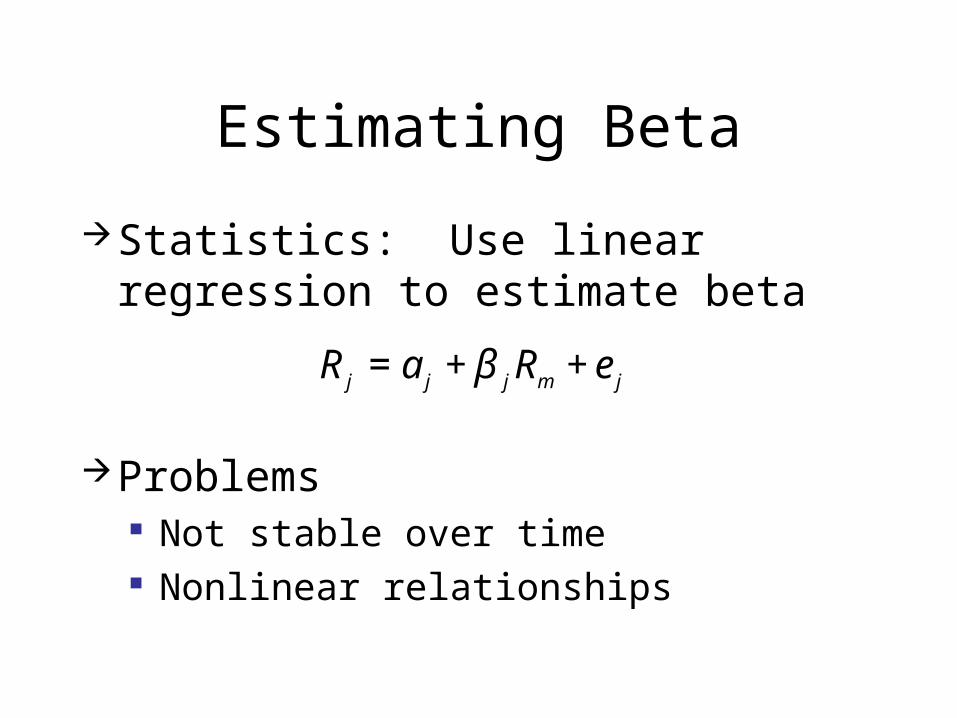

Estimating Beta

Statistics: Use linear regression to estimate beta

Problems Not stable over time Nonlinear relationships€

R j = a j + β jRm + e j

Goals

Portfolios and correlationsDiversifiable versus nondiversifiable riskCAPM and Beta

Capital asset pricing model Is the CAPM really useful?

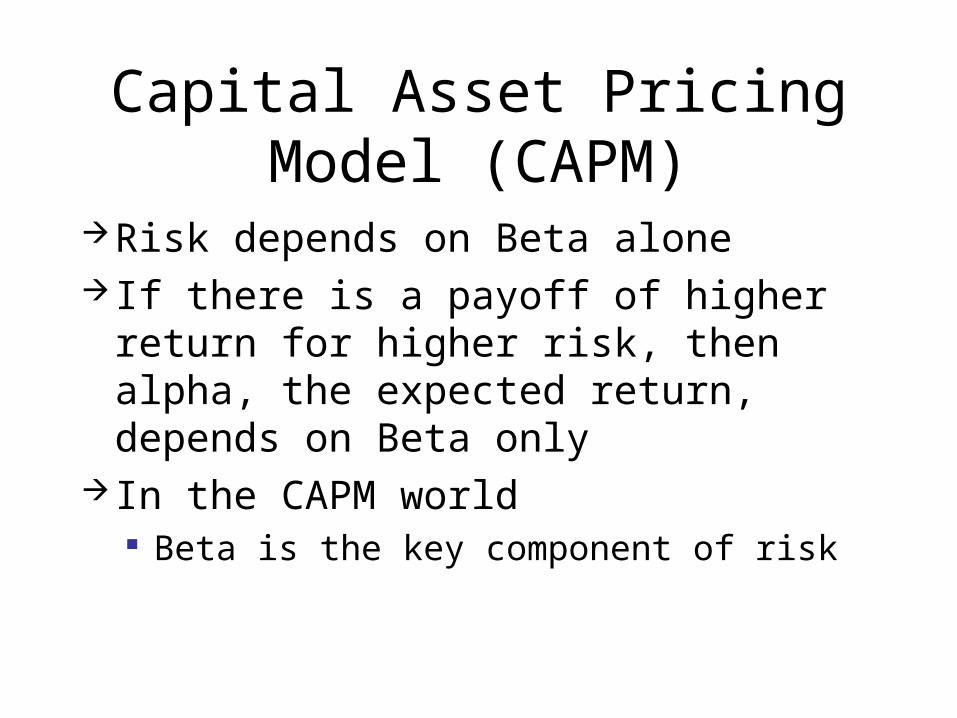

Capital Asset Pricing Model (CAPM)

Risk depends on Beta alone If there is a payoff of higher return for

higher risk, then alpha, the expected return, depends on Beta only

In the CAPM world Beta is the key component of risk

What would happen in a non CAPM world?Malkiel’s experiment

Assume the risk measure that people care about is related to the total (nondiversifiable+diversifiable) risk

Stocks with higher e(j) variance pay higher returns

Build two stock portfolios High e(j) variance, Beta = 1 Low e(j) variance, Beta = 1

More on Malkiel’s Experiment

Since this is a nonCAPM world The first portfolio earns a higher return

However, the risk of the two portfolios is the same They have the same beta e(j) risk is diversified away

Investors will load up on high e(j) risk stocks This drives the price up, and expected returns will

fall on these stocks until they are equal to the others

Beta is Key

In the CAPM world: No reward for holding stocks with lots of

diversifiable risk Only beta matters as a measure of risk

Adjusting Beta Using a Risk Free Asset

Market Portfolio Expected return = 10% Beta = 1

Risk free (bank account) Expected return = 4% Beta = 0

Combine these two

Combinations

All risk free Beta = 0, expected return = 4%

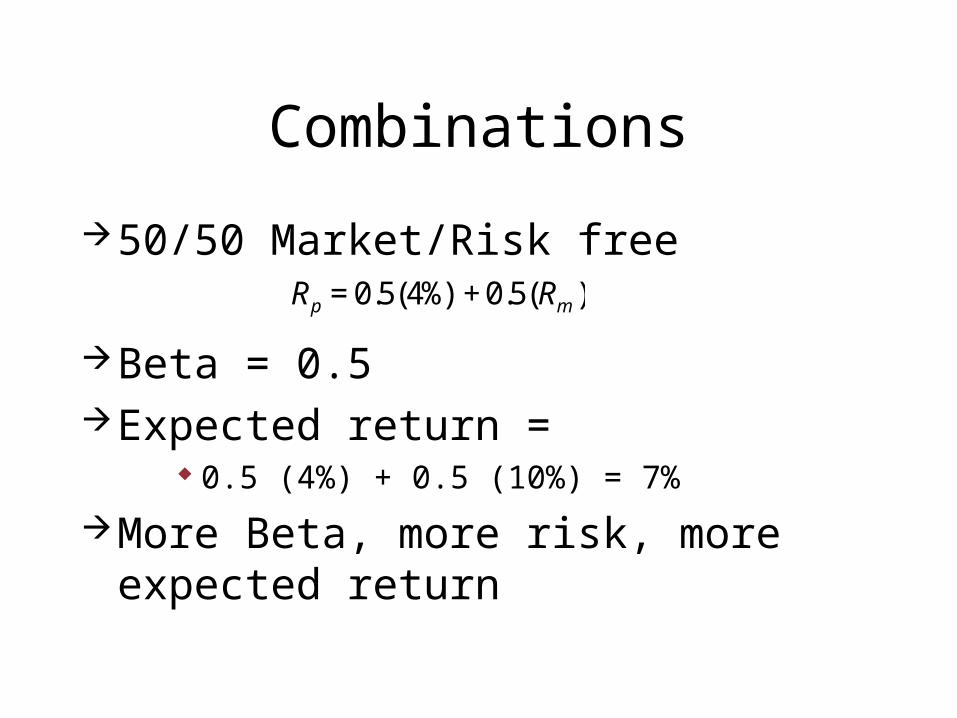

Combinations

50/50 Market/Risk free

Beta = 0.5Expected return =

0.5 (4%) + 0.5 (10%) = 7%

More Beta, more risk, more expected return

€

Rp = 0.5(4%)+ 0.5(Rm )

Fully Invested in Market

Easy Beta = 1 Expected return = 10%

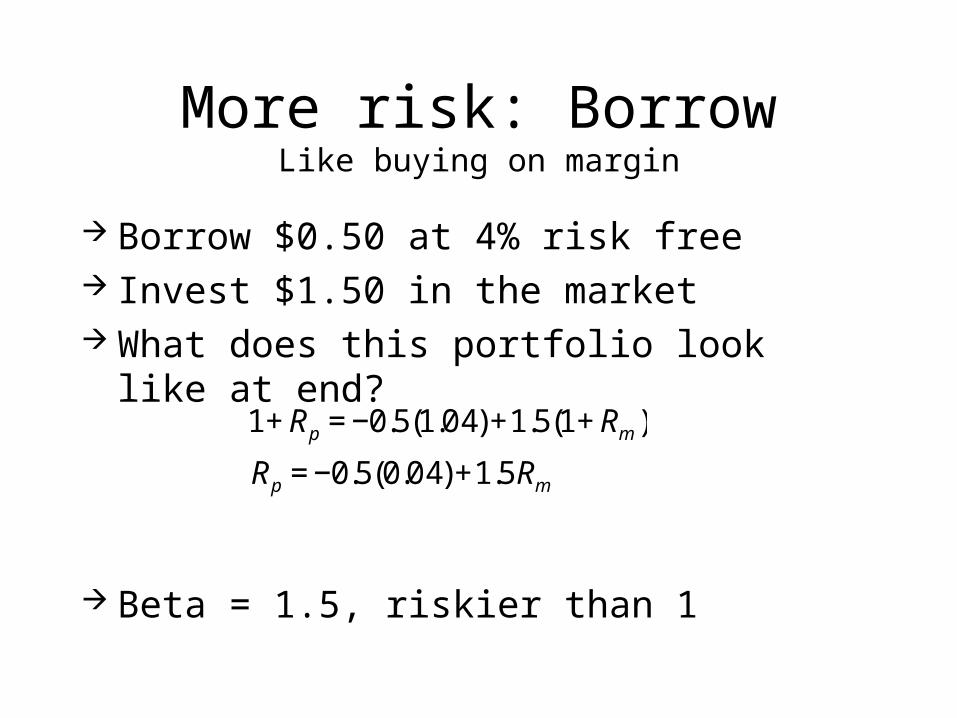

More risk: BorrowLike buying on margin

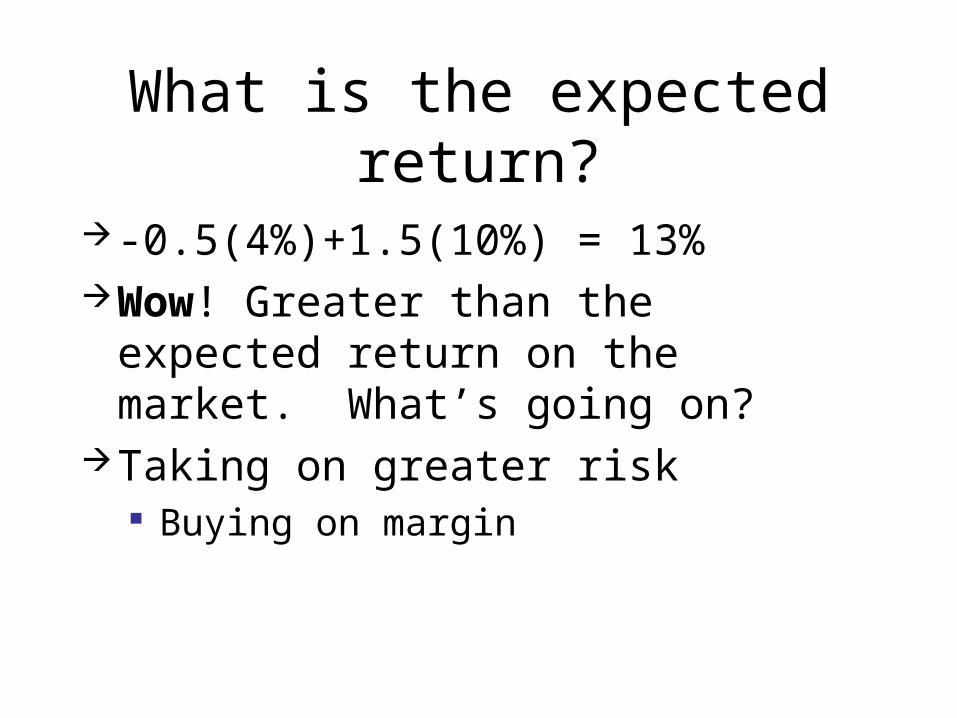

Borrow $0.50 at 4% risk free Invest $1.50 in the market What does this portfolio look like at end?

Beta = 1.5, riskier than 1

€

1+ Rp = −0.5(1.04)+1.5(1+ Rm )

Rp = −0.5(0.04)+1.5Rm

What is the expected return?

-0.5(4%)+1.5(10%) = 13%Wow! Greater than the expected return

on the market. What’s going on?Taking on greater risk

Buying on margin

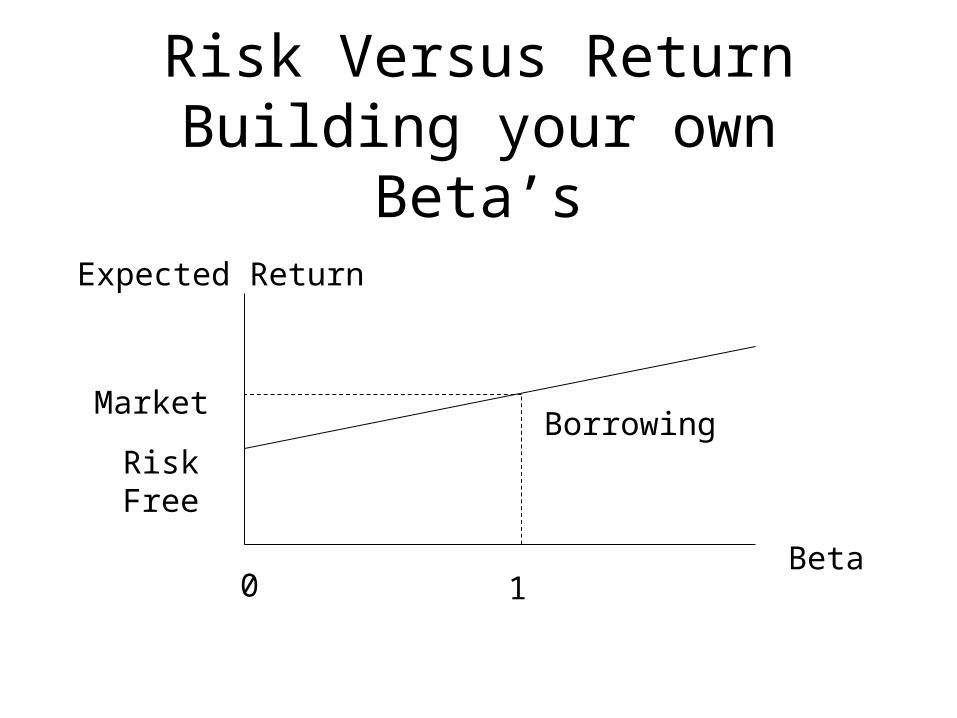

Risk Versus ReturnBuilding your own Beta’s

Beta

Expected Return

0

Risk Free

1

MarketBorrowing

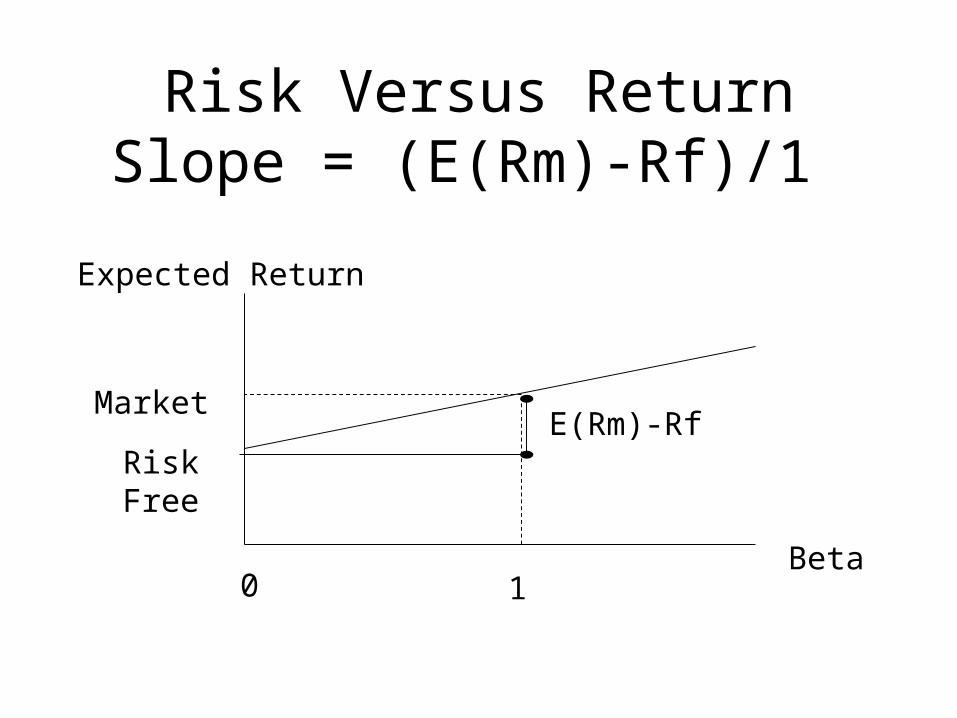

Risk Versus ReturnSlope = (E(Rm)-Rf)/1

Beta

Expected Return

0

Risk Free

1

MarketE(Rm)-Rf

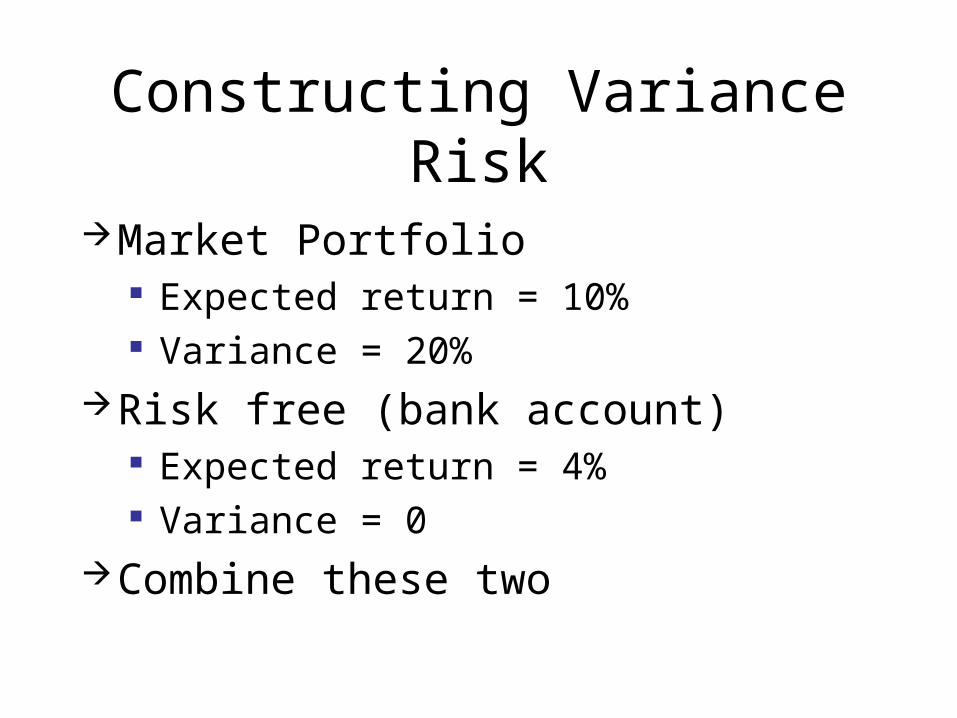

Constructing Variance Risk

Market Portfolio Expected return = 10% Variance = 20%

Risk free (bank account) Expected return = 4% Variance = 0

Combine these two

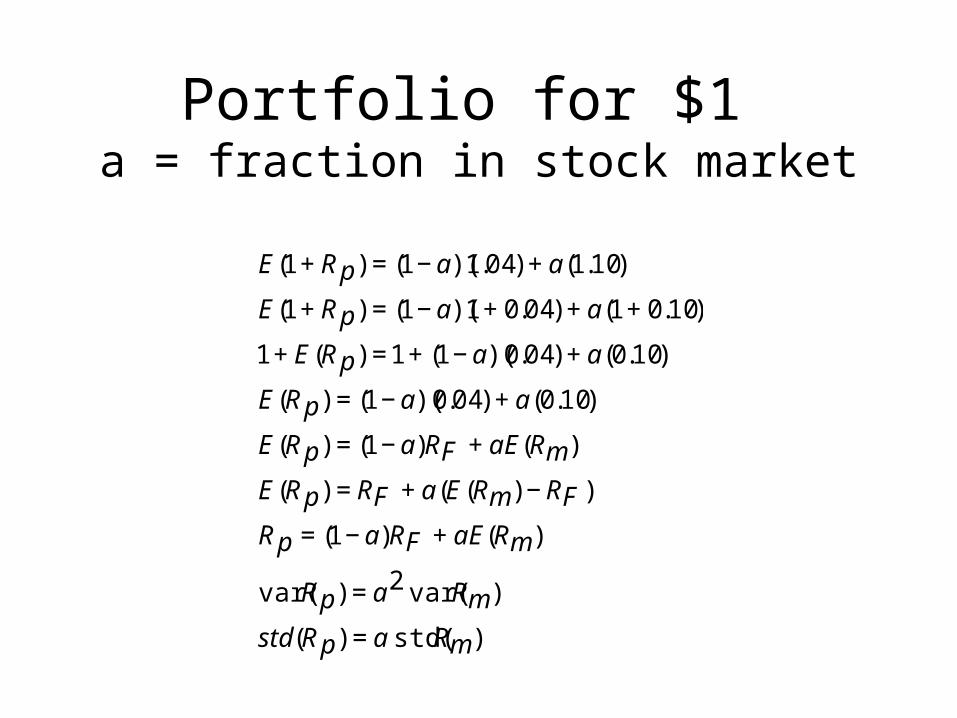

Portfolio for $1 a = fraction in stock market

€

E(1 + Rp) = (1 − a)(1.04) + a(1.10)

E(1 + Rp) = (1 − a)(1 + 0.04) + a(1 + 0.10)

1 + E(Rp) = 1 + (1 − a)(0.04) + a(0.10)

E(Rp) = (1 − a)(0.04) + a(0.10)

E(Rp) = (1 − a)RF + aE(Rm )

E(Rp) = RF + a(E(Rm ) − RF )

Rp = (1 − a)RF + aE(Rm )

var(Rp) = a2 var(Rm )

std (Rp) = a std(Rm )

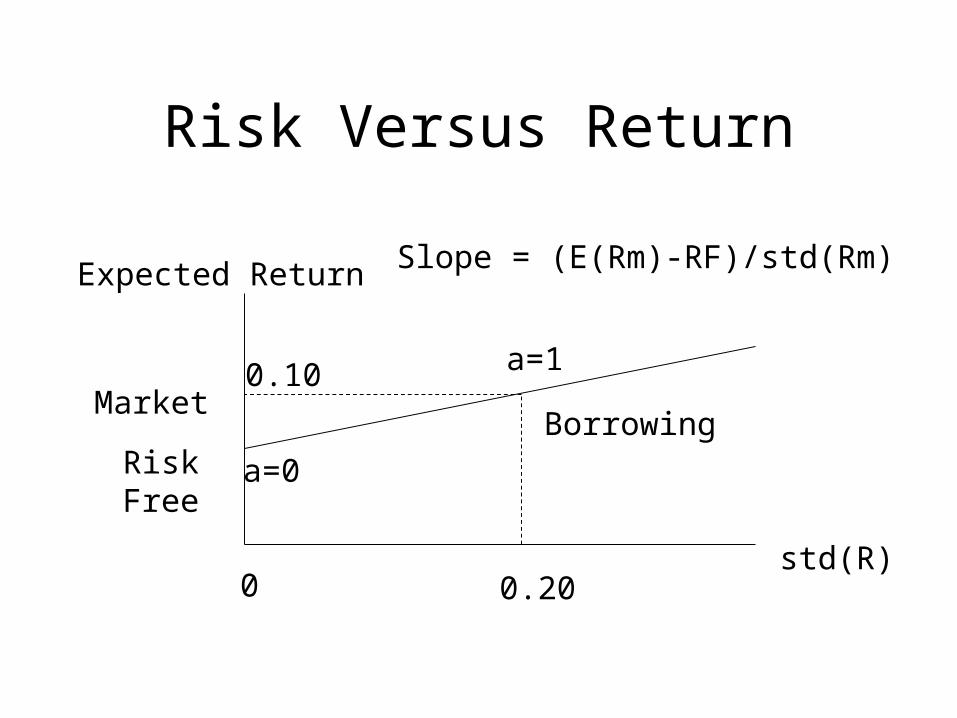

Risk Versus Return

std(R)

Expected Return

0

Risk Free

0.20

MarketBorrowing

a=1

a=0

0.10

Slope = (E(Rm)-RF)/std(Rm)

Returns and Borrowing

By borrowing more (leverage) can increase returns

Also, increase risk It is easy to be on the line (if you have

enough credit) Simply reporting returns alone is never

enough Would a return of 20% per year be amazing?

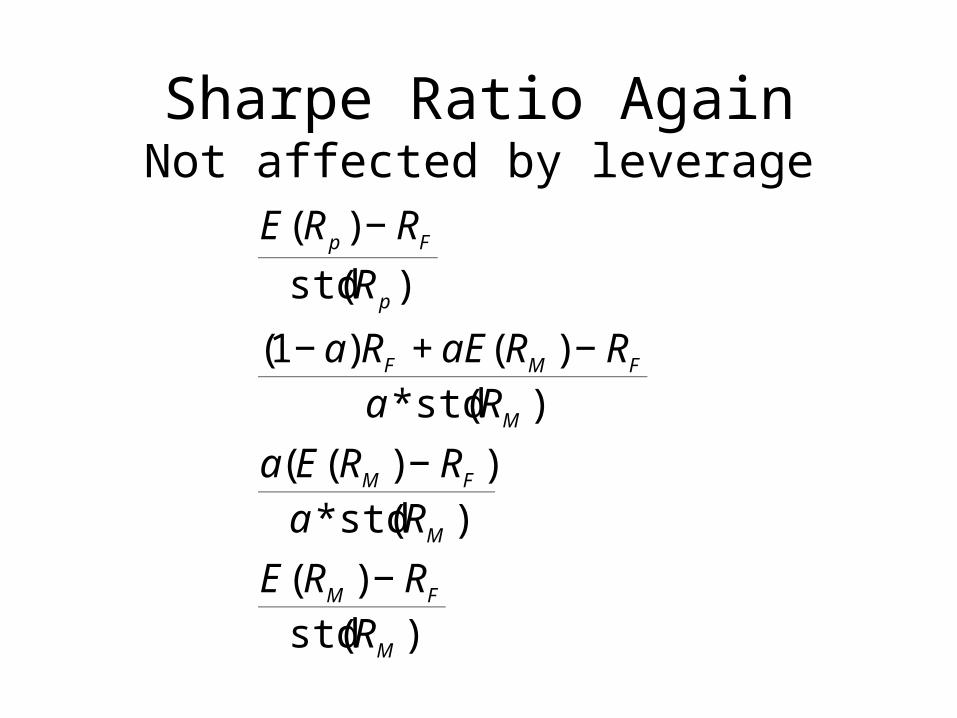

Sharpe Ratio AgainNot affected by leverage

€

E(Rp ) − RFstd(Rp )

(1− a)RF + aE(RM ) − RFa*std(RM )

a(E(RM ) − RF )a*std(RM )

E(RM ) − RFstd(RM )

CAPM: Two views

Simple risk measure, BetaPerfect CAPM world

Market equilibrium linking beta and expected returns

Perfect CAPM World

Beta (and Beta alone) is risk measureEveryone holds market portfolio and

some amount of risk free Individual stock returns and Beta are

linearly related

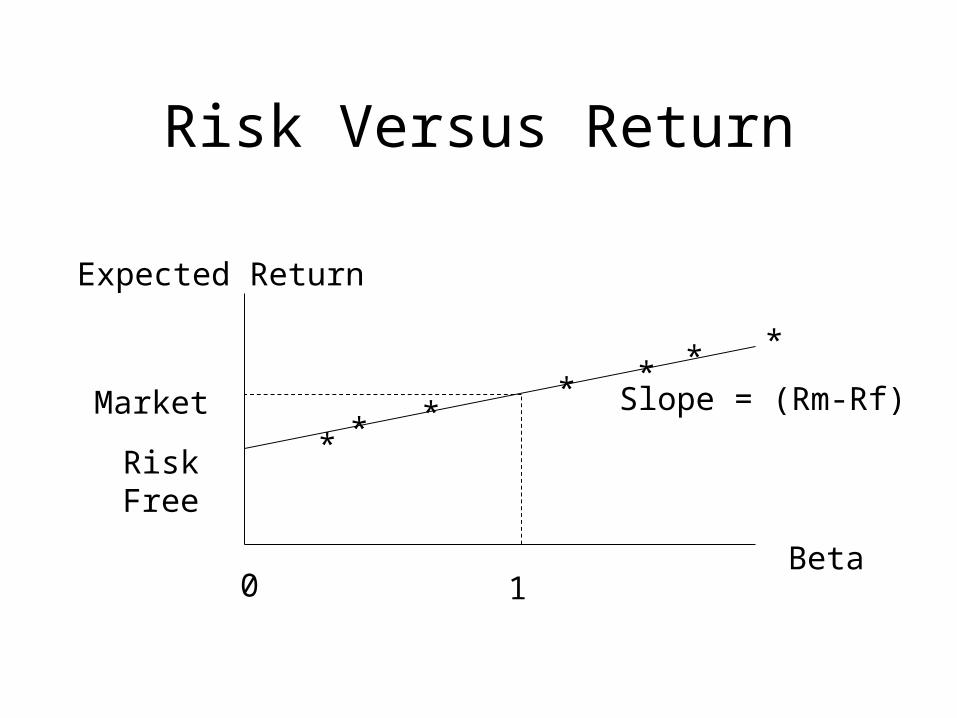

Risk Versus Return

Beta

Expected Return

0

Risk Free

1

Market*

***

*

**

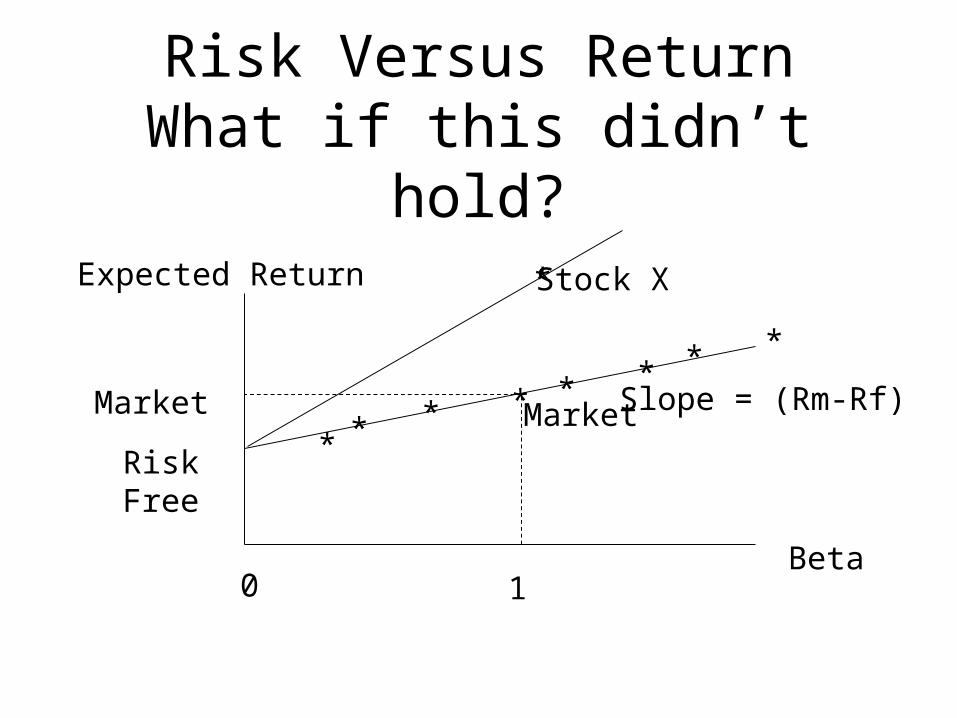

Slope = (Rm-Rf)

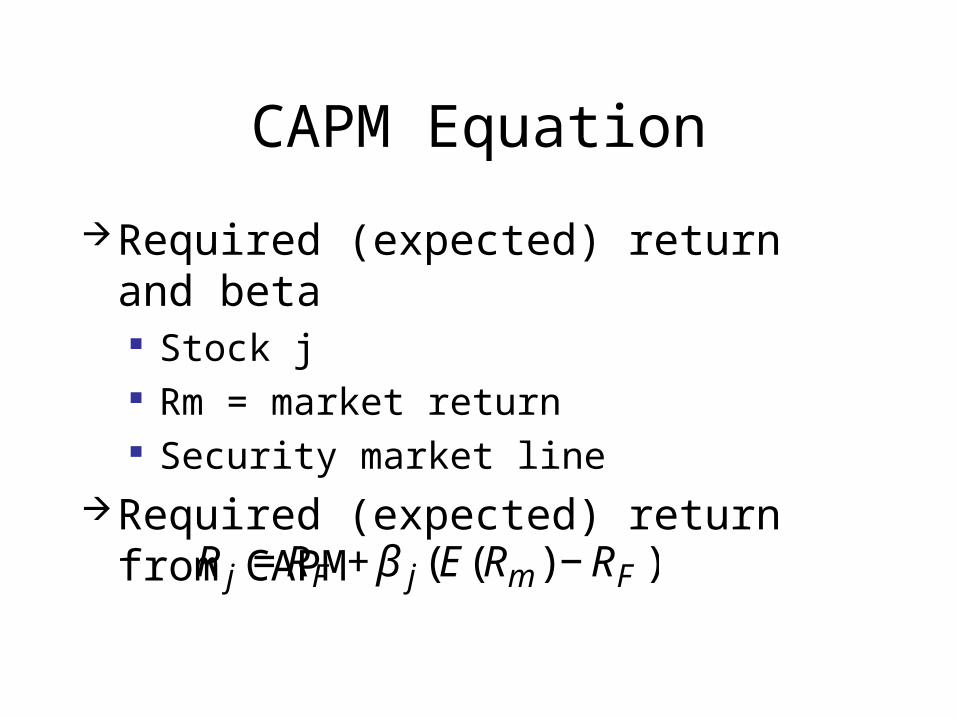

CAPM Equation

Required (expected) return and beta Stock j Rm = market return Security market line

Required (expected) return from CAPM

€

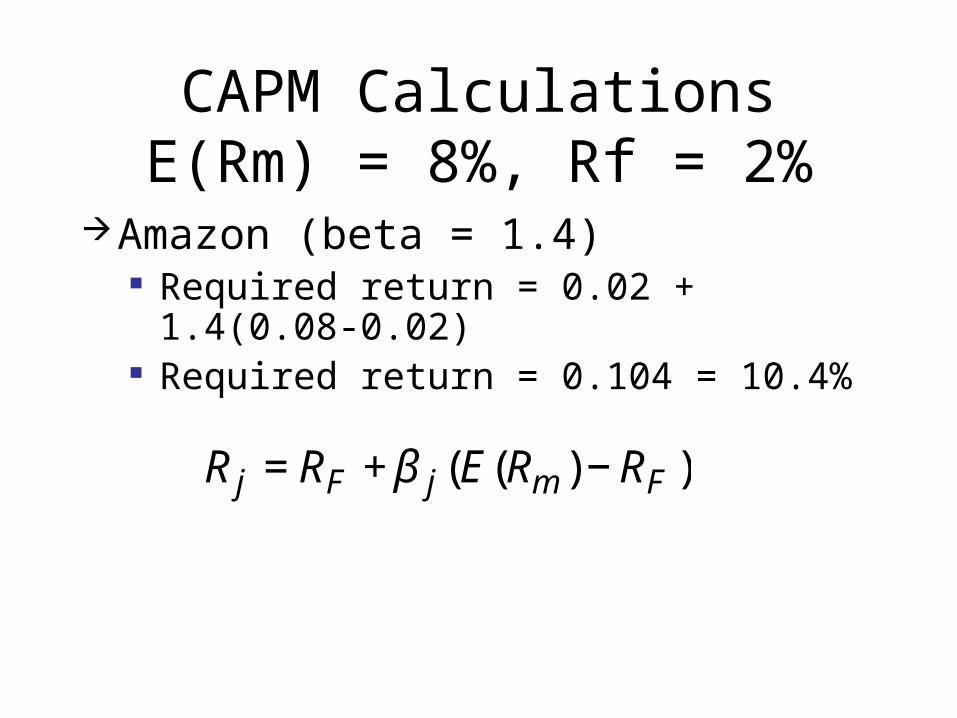

R j = RF + β j (E(Rm ) − RF )

Risk Versus ReturnWhat if this didn’t hold?

Beta

Expected Return

0

Risk Free

1

Market*

***

*

**

Slope = (Rm-Rf)

*

* Market

Stock X

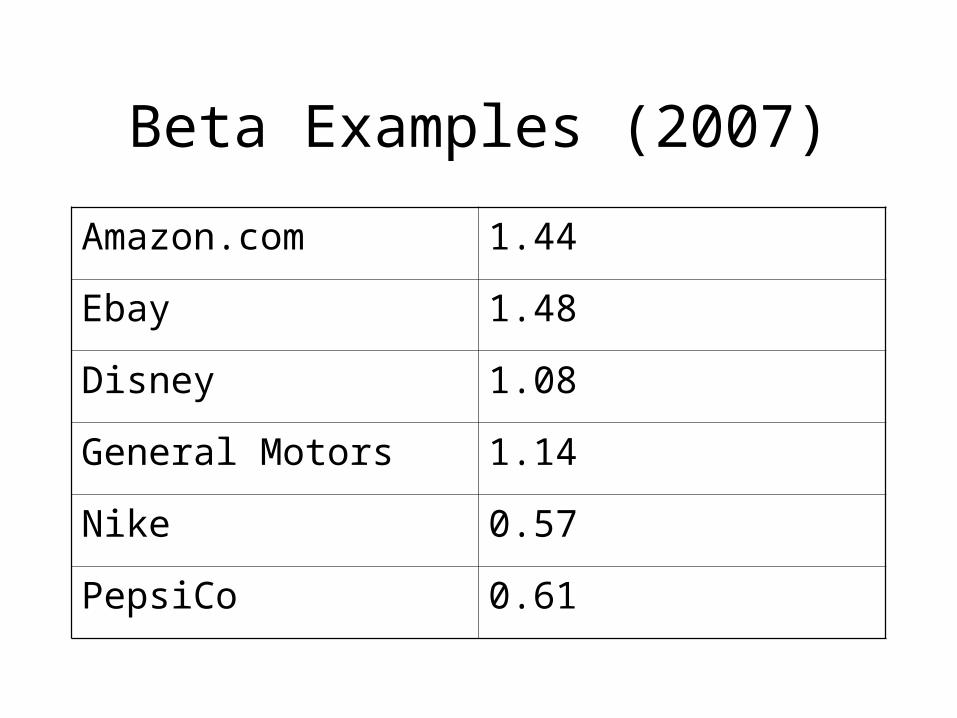

Beta Examples (2007)

Amazon.com 1.44

Ebay 1.48

Disney 1.08

General Motors 1.14

Nike 0.57

PepsiCo 0.61

CAPM CalculationsE(Rm) = 8%, Rf = 2%

Amazon (beta = 1.4) Required return = 0.02 + 1.4(0.08-0.02) Required return = 0.104 = 10.4%

€

R j = RF + β j (E(Rm ) − RF )

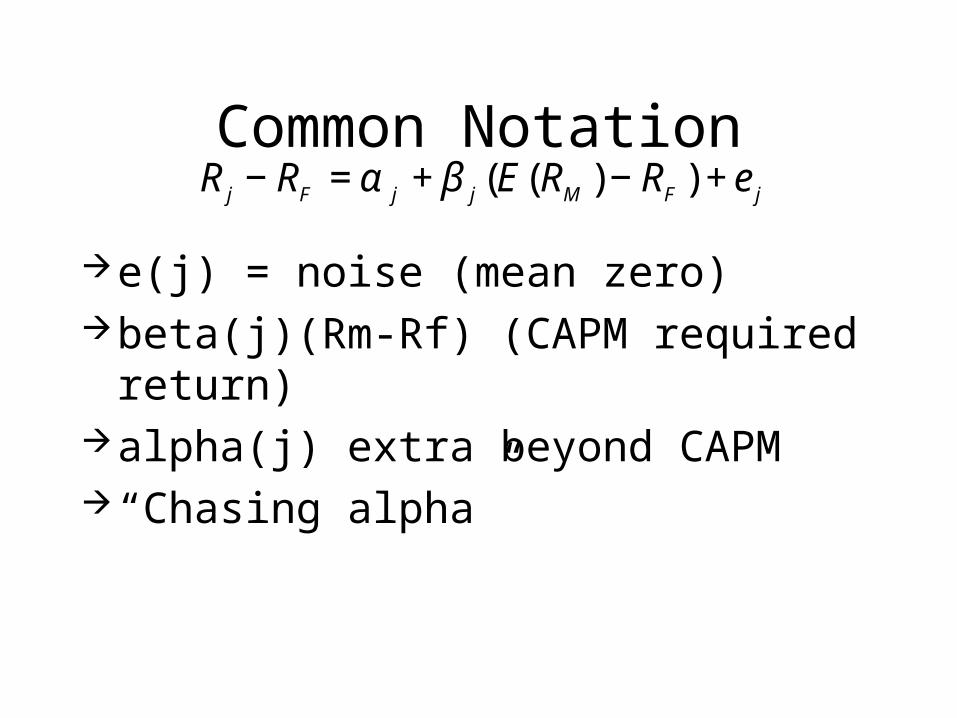

Common Notation

€

R j − RF = α j + β j (E(RM ) − RF ) + e j

e(j) = noise (mean zero)beta(j)(Rm-Rf) (CAPM required return)alpha(j) extra beyond CAPM “Chasing alpha”

Goals

Portfolios and correlationsDiversifiable versus nondiversifiable riskCAPM and Beta

Capital asset pricing model Is the CAPM really useful?

How well does the CAPM work?

Results: Fama and French Malkiel

Construct portfolios of stocksEstimate betasPlot beta versus expected returnNo relationship

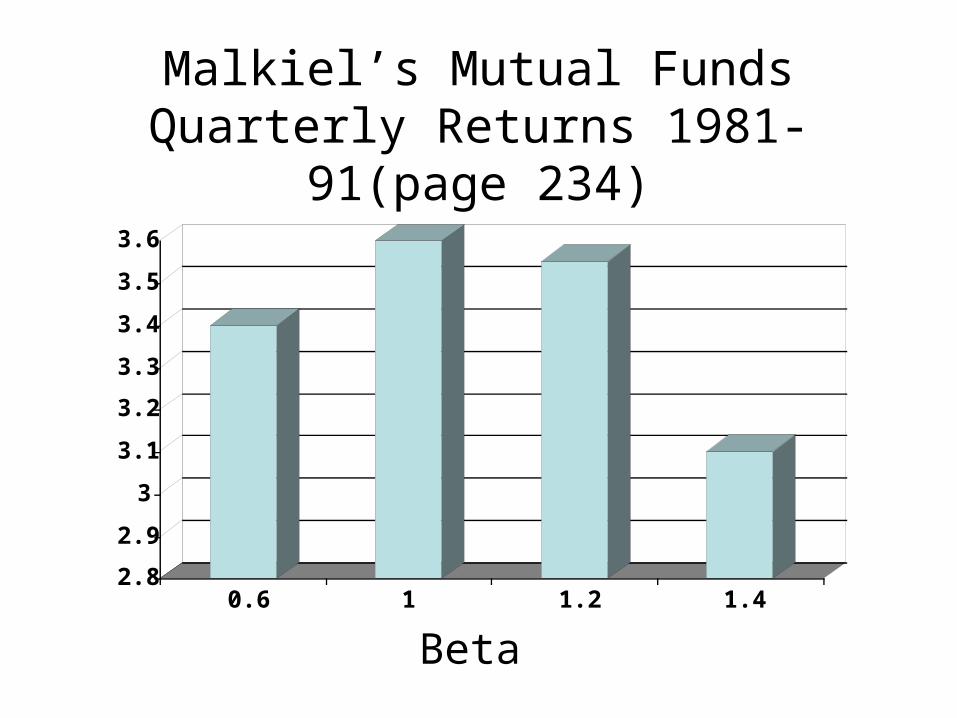

Malkiel’s Mutual FundsQuarterly Returns 1981-91(page

234)

2.8

2.9

3

3.1

3.2

3.3

3.4

3.5

3.6

0.6 1 1.2 1.4

Beta

Is Beta Dead?

Older research showed a weak relationship between beta and expected return

Recent evidence shows that there is probably no relationship

Premier model of asset pricingShould or do we still care?

Reasons to Still think about Beta

Diversification and portfolio theory is still important Beta is informative about how a security

moves with the market If the CAPM is not working, should try to

“beat it” Load up on low beta stocks Should be lower risk, and higher return

Problems with CAPM

Beta is very unstable over time Hard to estimate

Market inefficiencyDiversificationAttitudes toward risk Important side message

Look at other stuff

Goals

Portfolios and correlationsDiversifiable versus nondiversifiable riskCAPM and Beta

Capital asset pricing model Is the CAPM really useful?

Recommended