Gas Industry micro CHP workshop 2008 Paris, France May 29 – 30, 2008

Subsidizing mCHP. What is the situation? Impact of different models

A. H. Pedersen / DONG Energy A/S

Policies in selected countries

• Portugal

• Japan

• UK

• Germany

• Holland

• US

2

Huge investments needed to overcome the jump from niche – to mainstream market

Present mCHP technologies – without public Present mCHP technologies – without public support - are only available for:support - are only available for:

• "rich" technology interested consumers and"rich" technology interested consumers and

• energy companies with a strong believe in energy companies with a strong believe in future business in the mCHP market.future business in the mCHP market.

Market – and demonstration - are necessary to Market – and demonstration - are necessary to create a competetive product. For some mCHP create a competetive product. For some mCHP products the industry is facing reduction of products the industry is facing reduction of production cost to 1/5 of the present production production cost to 1/5 of the present production cost to create a competitive product.cost to create a competitive product.

3

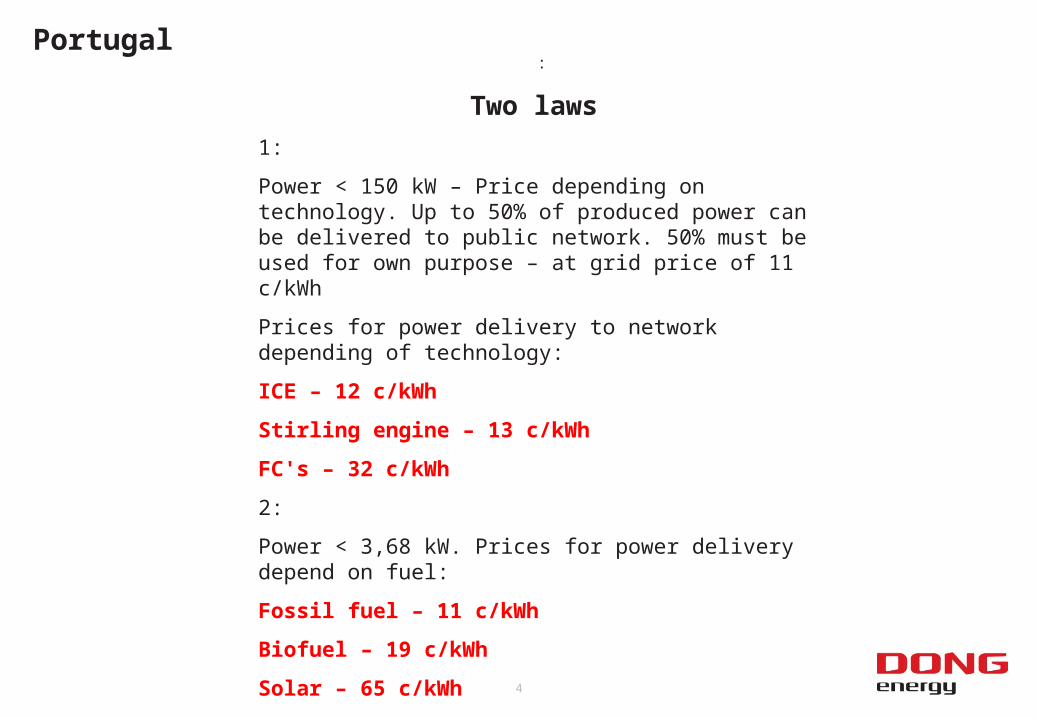

Portugal

4

:

Two laws

1:

Power < 150 kW – Price depending on technology. Up to 50% of produced power can be delivered to public network. 50% must be used for own purpose – at grid price of 11 c/kWh

Prices for power delivery to network depending of technology:

ICE – 12 c/kWh

Stirling engine – 13 c/kWh

FC's – 32 c/kWh

2:

Power < 3,68 kW. Prices for power delivery depend on fuel:

Fossil fuel – 11 c/kWh

Biofuel – 19 c/kWh

Solar – 65 c/kWh

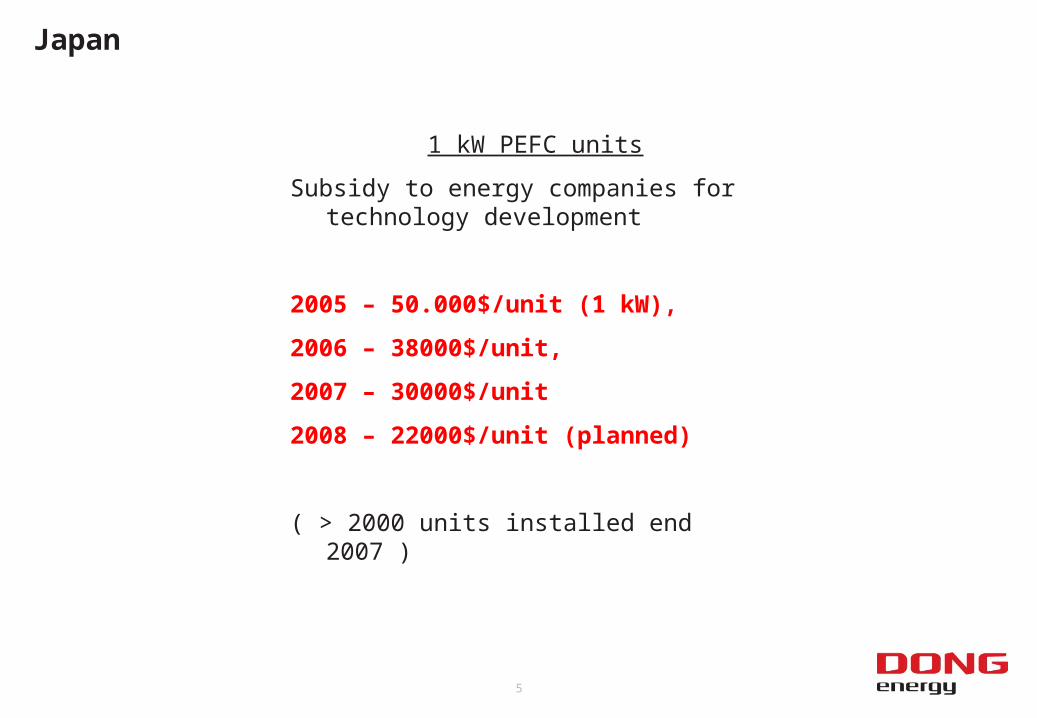

Japan

5

1 kW PEFC units

Subsidy to energy companies for technology development

2005 – 50.000$/unit (1 kW),

2006 – 38000$/unit,

2007 – 30000$/unit

2008 – 22000$/unit (planned)

( > 2000 units installed end 2007 )

Field test number of installed units

Fuel kind 2005 year

2006 year

2007 year Total

Tokyo Gas City gas 150 160 210 520

Osaka Gas City gas 63 160 81 224

Toho Gas City gas 12 40 38 90

Saibu Gas City gas 10 10 13 33

Hokkaido Gas City gas - 10 10 20

Nippon GasCity gas - 3 3 6

LP gas - 7 7 14

New Nippon OilLP gas 134 226 250 610

Kerosene - 75 146 221

Idemitsu Kosan LP gas 33 40 50 123

Japan Energy LP gas 30 40 34 104

Iwatani & Co., Ltd. LP gas 10 34 29 73

Cosmos oilLP gas 10 19 14 43

Kerosene - - 5 5

Taiyo Oil LP gas 8 13 18 39

Kyushu Oil LP gas 8 10 12 30

Showa Shell Oil LP gas 6 10 10 26

Lemon gas LP gas 6 - - 6

Total 480 777 930 2,187

1 k W PEFC Fuel Cell

2005 – 50.000$/unit (1 kW),

2006 – 38000$/unit,

2007 – 30000$/unit

2008 - 22000 $/unit planned

Natural gas 893 units

ICE engines installed – end 2007

about 65000 – 1 kW units

about 3500 units in the range from 1 to 10kW

100 JPY = 1 US$

1 kW

UK

8

•VAT reduction from 17,5% til 5%

•Beneficial description

•Easy access to ROC’s

•Partly funding from Energy companies

Germany

9

5,1 cent/kWh +

0,8 c/kWh (avoiding high and medium voltage grid) +

0,55 c/kWh gas used (discount on app. 5,5 c/m3 natural gas - or app. 1 c/kWh electricity produced)

In total: app. 7c/kWh sold to grid.

Feed-in tariffs for microCHP in Germany

Holland

11

No incentives for households to buy MicroCHP – only for industries (tax breaks)

Up to 3000 kWh/y delivered to net – can be subtracted from delivered power from public network

US

12

Subsidy: 1000 – 2000 $/unit

Depending on state

Impacts of models for public support to mCHP

13

Subsidy to energy companies has shown most remarkable results.

In Japan is now installed :

65000 – 1 kW gas engine units

2000 FC – 1 kW units

3500 mCHP units from 1 - 10kW

Other kinds of public support still have to prove markable effect

Global sale of mCHP Delta mCHP summit 2008

Recommended