Protecting Craft Against Pseudos

June 2014

2

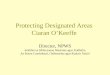

“Craft to the Consumer” is Broader than Industry Definition

Brewers Association (Est. 2005) Dictionary(1) “Craft to Consumer”(2)

Craft8%

Non-Craft92%

Craft2%

Non-Craft98%

Craft11%

Non-Craft89%

Merriam-Webster Dictionary:

– “A specialty beer produced in

limited quantities”

Oxford Dictionary:

– “A beer made in a traditional or

non-mechanized way by a small

brewery”

Collins Dictionary:

– “A specialized beer produced in

limited quantities; a microbrew”

Small:

– Annual production of less than 6

million barrels of beer

Independent:

– >25% of the Craft Brewery cannot

be owned or controlled by a

beverage alcohol industry

member that is not itself a Craft

Brewer

Traditional:

– Flavor derives from traditional or

innovative brewing ingredients

and their fermentation

Perception of Small Batch

Perception of Independence

Distinct / Innovative Flavor(s)

Regional

Historic

Premium

(1) Craft as defined as brewers with <1 million barrels produced annually. (2) Craft as defined as the Brewers Association definition + “Craft-positioned” brands excluded from the Brewers

Association definition because of corporate ownership. Note: In 2014, the Brewers Associated amended the Craft definition to include brewers utilizing certain adjuncts in the mash bill.

Note: Craft percentages based on volume.

24.2%25.4% 25.4% 25.4%

26.7%

39.2% 39.9%

ShockTop

Lagunitas Pyramid RedHook

SierraNevada

SamuelAdams

BlueMoon

3

Consumers Do Not Differentiate Craft and Craft-Positioned Pseudos (“Pseudos”)(1)

Consumer Survey(2) Defining Brands

Source: Demeter Group-commissioned Google Consumer Survey. (1) Demeter Group defines Pseudos as Craft-positioned beer owned by non-Craft brewers. (2) Survey conducted via Google Consumer Surveys to 650 Males 4/29/2014 through 5/1/2014. “None of the above” results removed from the survey.

Brewers

Association Craft?

Craft to

Consumer?

—

—

—

Dictionary

Craft?

—

—

—

—

—

“Which of the following do you consider to be a "Craft" beer?

(choose all that apply)”

Craft (BA Definition) Pseudos

Blue

Moon

Samuel

Adams

Sierra

Nevada

Red

Hook

Pyramid

Lagunitas

Shock Top

—

—

—

Average: 29.4%

4

Adding to the Confusion, Retailers Co-Mingle Craft and Pseudos

Pseudos Imports

Note: Craft vs. Pseudos as determined by Brewers Association definition.

$6.3 $6.6

$7.6

$8.7

$10.2

$1.6 $1.8

$1.9

$2.3

$2.5

$1.1 $1.2

$1.5

$1.7

$2.1

$0.2 $0.3

$0.3

$0.6

$0.9

$0.6 $0.6

$0.7

$0.8

$0.8

$9.9 $10.4

$11.9

$14.1

$16.6

9.8% 10.3% 11.8% 14.7% 16.5%

2008 2009 2010 2011 2012

Craft (BA Definition) New Craft (Adjunts)

Pseudos (MC) Pseudos (ABI)

Pseudos (Other Ownership) % of Beer Market (Craft + Pseudos)

Pseudos

38%

8.59.1

10.1

11.5

13.2

2.12.4

2.5

3.0

3.3

1.51.6

2.0

2.3

2.7

0.30.4

0.4

0.8

1.2

0.80.9

0.9

1.0

1.1

13.314.3

15.9

18.6

21.5

6.3% 7.0% 7.8% 9.3% 10.6%

2008 2009 2010 2011 2012

Craft (BA Definition) New Craft (Adjunts)

Pseudos (MC) Pseudos (ABI)

Pseudos (Other Ownership) % of Beer Market (Craft + Pseudos)

Craft’s Market Size Potential is Much Larger from a “Craft to Consumer” Lens

5

“Craft to Consumer” Volume “Craft to Consumer” Retail $ Share

(1) In 2014, the Brewers Associated amended the Craft definition to include brewers utilizing certain adjuncts in the mash bill.

Source: Brewers Association and Demeter Group industry research.

(Millions of Barrels) ($ in Billions)

BA

Craft

62%

(1) (1)

“Craft to Consumer” is 19% of Today’s Beer Market & Could Reach 33% (Retail $)

6

Barrel Volume

Retail $ Share

Craft Forecast Assumptions

Maintain 15% Craft and

“Craft to Consumer”

volume growth in 2014P

and 2015P

– Grow Craft and “Craft

to Consumer” volume

8% in 2016P – 2020P

Hold overall Beer category

flat with 2013E

Barrel Volume

Retail $ Share

Average retail price per

barrel average of 2008 –

2013 average retail price(1)

Retail $ share of the entire

beer market increases 2%

yearly

(1) 2013 average retail price of $918 is $168 larger than the 2008 – 2012 average retail price per barrel.

If 2013 retail price per Craft barrel maintains 2013 level, retail sales of Craft to the Consumer could reach 38%.

9.8% 10.3%11.8%

14.7%16.5%

19.3%21.9%

24.9%26.3%

27.9%29.5%

31.3%33.1%

7.8% 8.3% 9.4%11.5% 12.7%

14.9%16.8%

19.0% 20.1% 21.3% 22.6%23.9%

25.3%

2008 2009 2010 2011 2012 2013E 2014P 2015P 2016P 2017P 2018P 2019P 2020P

Craft to Consumer Craft (BA Definition)

6.3% 7.0% 7.8%9.3%

10.6%12.3%

14.2%16.4%

17.7%19.1%

20.7%22.3%

24.1%

5.0% 5.6% 6.2% 7.2% 8.2% 9.4%10.9%

12.5% 13.5% 14.6% 15.8% 17.1%18.4%

2008 2009 2010 2011 2012 2013E 2014P 2015P 2016P 2017P 2018P 2019P 2020P

Craft to Consumer Craft (BA Definition)

7

In Other Categories, Pseudos have Captured a Large Portion of the Opportunity

Personal

Care

Restaurants

Natural / Authentic Pseudo Original

Bread(1)

KFC’s

New Fast

Casual Concept

Taco Bell’s

New Fast

Casual Concept

Nashville’s

Authentic

Chicken

Restaurant

San Diego’s

Authentic

Taco

Restaurant

(1) Bread segmented based on wheat-positioned breads being made of whole wheat flour vs. combinations of other flours (“white bread in disguise”).

8

Craft is More Authentically Positioned, but Pseudos will Intrude on Craft’s Growth

Craft Pseudos

Select

Brands

Marketing

Distribution

Focus on Brew Pub as word of mouth and key

marketing tool

Packaging as cue to tell story and artisan

positioning

Utilize social media to broadcast production

process and engage with consumers

Appearance of artisan, small batch, and / or

historic beer

Leverage packaging to suggest artisan positioning

Large national marketing budgets to drive

mainstream advertising and social media

Broad national distribution networks

Piggybacking clout of parent company to rapidly

achieve full national distribution

Production /

Scalability

Evaluate a diversity of financing strategies to

fund expansion

Ability to scale to demand quickly via production

arbitrage

Focus on home markets with some developing a

national presence

16.5

19.4

22.0

25.427.5

29.7

32.0

34.6

37.4

25.9

29.831.8

34.235.6

37.038.5

40.041.6

3.9

2.0 2.4 1.4 1.4 1.5 1.5 1.6

2012 2013 2014P 2015P 2016P 2017P 2018P 2019P 2020P

Barrels Sold Potential Capacity Incremental Capacity

Rapid Craft Facility Expansion ($1B+ by 2020P) Needed to Guard Against Pseudos

9

Production Expansion (Barrels) Cost of Expansion

Assumptions:

Median Cost of Expansion

($ in Thousands) (Barrels in Millions)

$101

$134

$53 $57 $61 $65 $70

$201

$234

$153 $157 $161 $165 $170

2014P 2015P 2016P 2017P 2018P 2019P 2020P

$151

$184

$103$107

$111 $115$120

Production grows at half the rate of Craft volume growth

– 7% in 2014P, 8% in 2015P, and 4% in 2016P – 2020P

Sales volume reaches 90% of Craft beer production volume in 2020

On average, each additional barrel of production capacity will cost $75

Source: Brewers Association and Demeter Group industry research.

10

Access to Capital Needed to Quickly Expand Production

Brewery Stage Cash Flow Assumption Funding Implication(s)

Top 10 Craft

Brewery

Expansion Past

100,000 Barrels

Expansion Past

50,000 Barrels

Expansion Past

25,000 Barrels

Top 2 Brewery

$3

$20

$7

$35

EBITDA

Revenue

$1

$10

$3

$20

EBITDA

Revenue

$0

$2

$2

$10

EBITDA

Revenue

Note: EBITDA margins assumed at 15% - 20%. Brewpub Revenue assumed at $5 million for over 50,000 barrels and $2 million for <50,000 barrels.

$2,000

$8,000

$17,000

$45,000

EBITDA

Revenue

Limited Growth Equity options

Debt imposes growth covenants and

restrictions

Partial or full sale to a financial or

strategic buyer

Ample Cash Flow allows expansion

of existing facilities and / or new

geographies

Ability to arbitrage fading brand

capacity with Shock Top, Blue

Moon, etc.

Limited Growth Equity options

Debt imposes growth covenants and

restrictions

Partial or full sale to a financial or

strategic buyer

Limited Growth Equity options

Alignment with strategic partner

may be attractive, but difficult to

negotiate

Self-Fund

Growth Equity

Debt

Sale

Growth Equity

JV with Large Craft Brewers

Growth Equity

Debt

Sale

Self-Fund

$15

$100

$150

$800

EBITDA

Revenue

$ in Millions

11

Marc Levit Associate

Jeff Menashe Chief Executive Officer

www.demetergroup.net

Recommended