Agência Nacional do PetróleoAgência Nacional do Petróleo

Quarta Rodada de LicitaçõesQuarta Rodada de Licitações

Houston, LondonDecember 11-14, 2001

Giovanni ToniattiDirector

ANP:Challenges and

Achievements inBrazil’s

Upstream Sector

BrasilBrasil Round Round 4 4

Agência Nacional do Petróleo

Brazil’s Energy SectorBrazil’s Energy Sector

BrasilBrasil Round Round 4 4

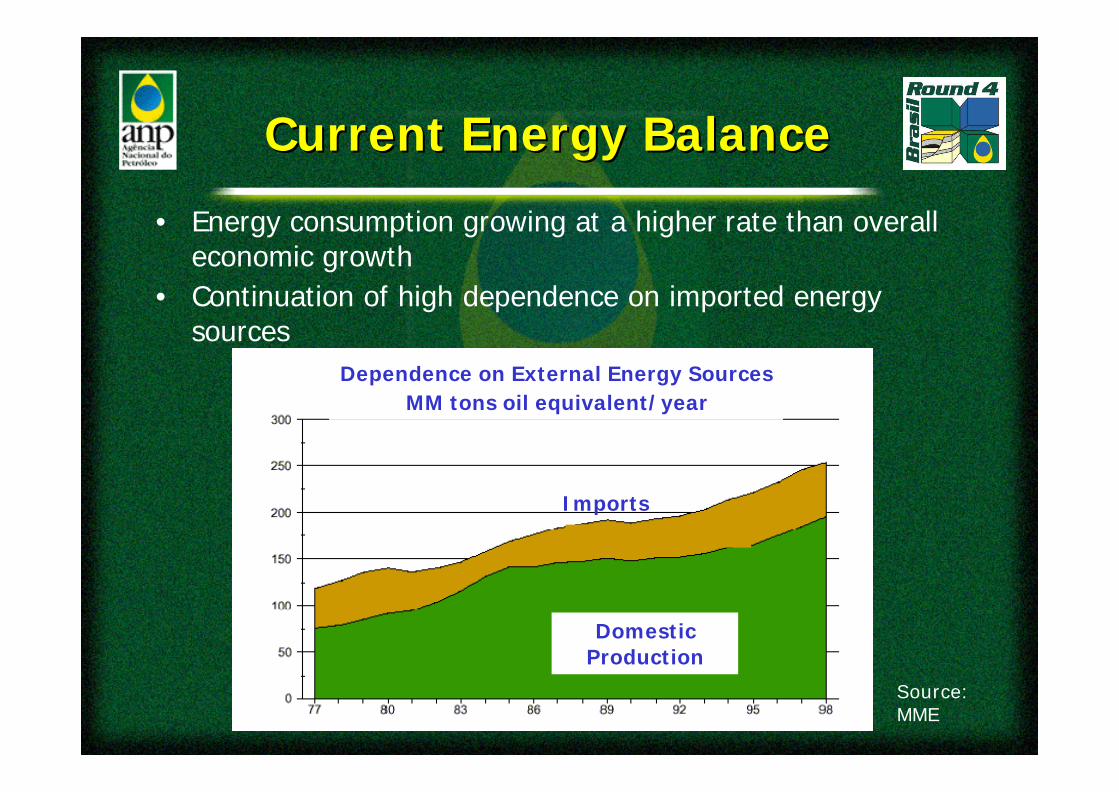

Source:MME

Current EnergyCurrent Energy Balance Balance

• Energy consumption growing at a higher rate than overalleconomic growth

• Continuation of high dependence on imported energysources

Dependence on External Energy SourcesMM tons oil equivalent/year

Imports

DomesticProduction

Brazil’s Market Potential

l World's 9th largest economyl 2000 GDP ~ US$553 Bn

l Greater than Argentina, Chile,Colombia, and Venezuelacombined

l 170 million peoplel Consumption - 1.8 MMBOPDl Production - 1.4 MMBOPDl Natural Gas - <3% of energy

demand mix

Current Energy Balance

• E&P Activities:Ø Important force for the advancement of the

economyØTechnology Development

• Exploration Activities:ØEssential for the maintenance of reserves and

assurance of future productionØFundamental element in the reduction of

dependency on foreign energy importsØSustained level of exploration activity achieved

through periodic licensing rounds

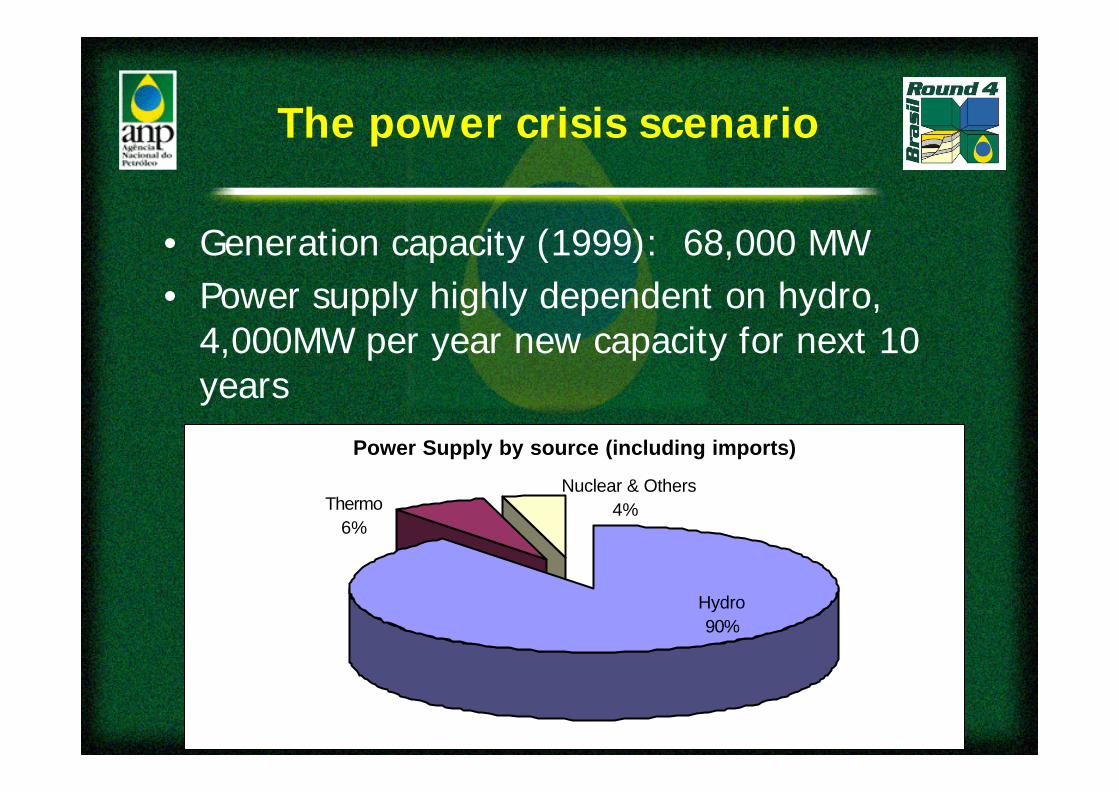

Power Supply by source (including imports)

Hydro90%

Thermo6%

Nuclear & Others4%

The power crisis scenario

• Generation capacity (1999): 68,000 MW• Power supply highly dependent on hydro,

4,000MW per year new capacity for next 10years

Government actions to assist thePriority Thermal Program

• Assume the exchange rate risk for the imported gasprovided to thermal plants for the next 15 years, forplants that start operation by end of June 2003 (newinter-ministerial ruling, issued June 4th 2001)

• Imported gas will have a fixed value ofUS$2.581/MMBTU during one year.

• Thermal plants gas price will be readjusted yearlybased on two factors (80% exch. rate variation; 20%Brazilian inflation.).

• Gas contracts can be rearranged every 3 years. Thismeans prices and/or supplier can be changed.

• Government has instructed IBAMA to speed up newplant permits

Major opportunity period for everyenergy related business, especially

along the gas chain….

• Gas thermal power plants• Local Gas Distribution Companies• Gas transporters• Gas traders• Gas producers

General Panorama of E&PGeneral Panorama of E&P

activities in Brazilactivities in Brazil

BrasilBrasil Round Round 4 4

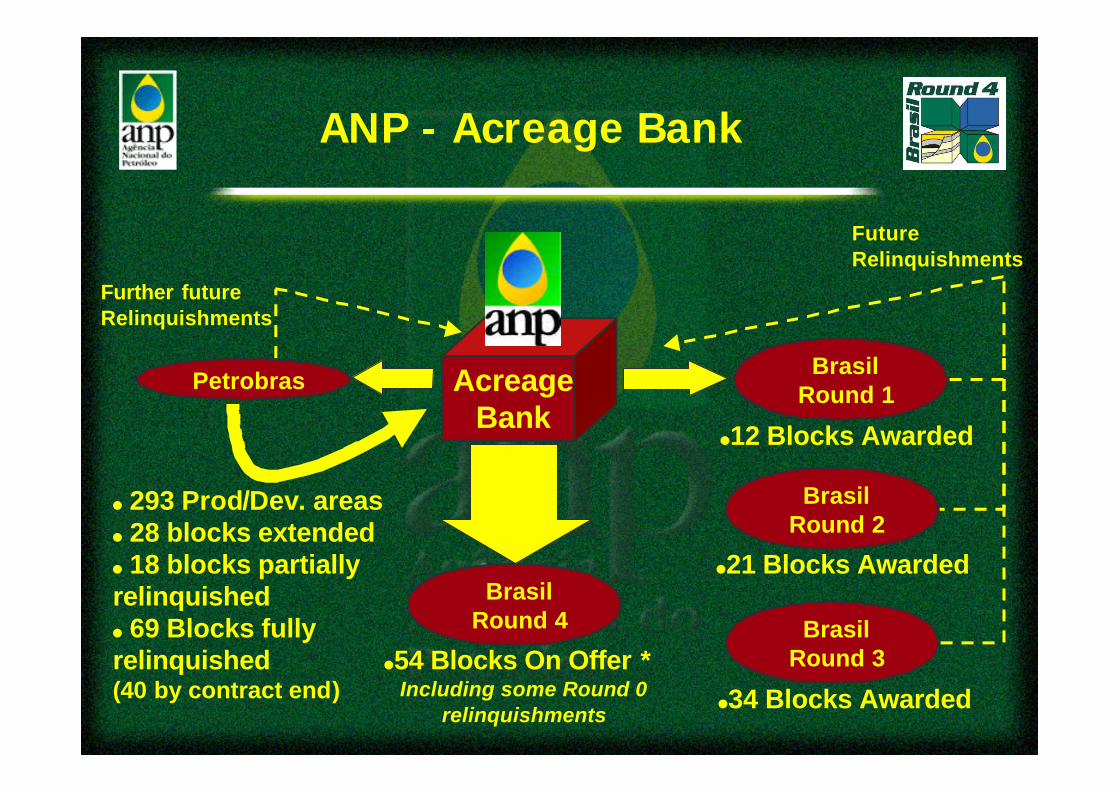

ANP - Acreage Bank

AcreageBank

PetrobrasBrasil

Round 1

l12 Blocks Awarded

BrasilRound 4

l 293 Prod/Dev. areasl 28 blocks extendedl 18 blocks partiallyrelinquishedl 69 Blocks fullyrelinquished(40 by contract end)

l54 Blocks On Offer *

Further futureRelinquishments

FutureRelinquishments

BrasilRound 2

l21 Blocks Awarded

BrasilRound 3

l34 Blocks AwardedIncluding some Round 0relinquishments

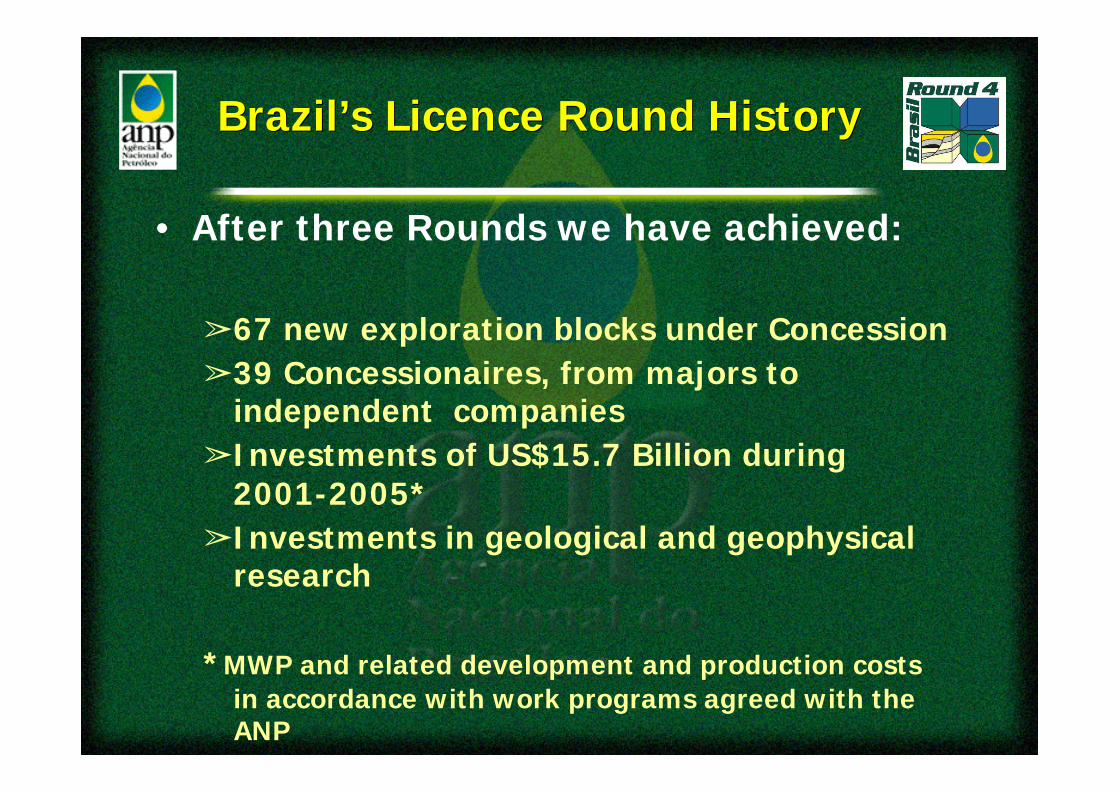

Brazil’s Brazil’s LicenLicencce Round Historye Round History

• After three Rounds we have achieved:

â67 new exploration blocks under Concessionâ39 Concessionaires, from majors to

independent companiesâInvestments of US$15.7 Billion during

2001-2005*âInvestments in geological and geophysical

research

*MWP and related development and production costsin accordance with work programs agreed with theANP

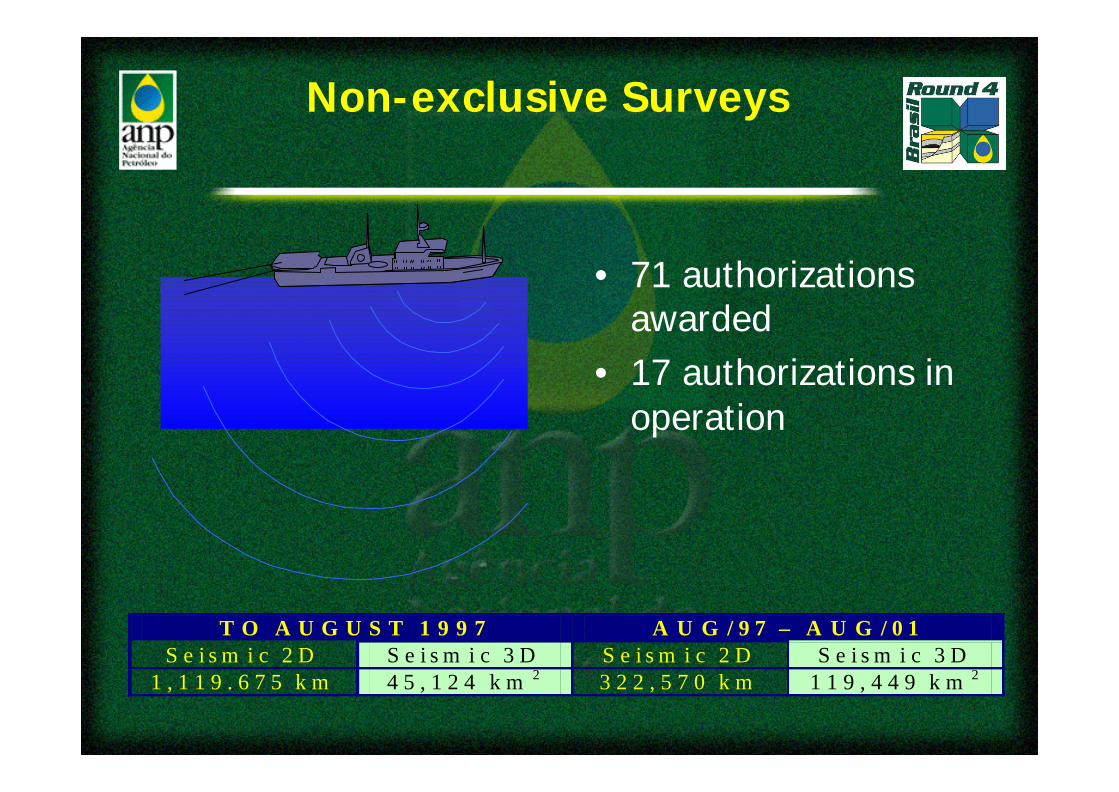

T O A U G U S T 1 9 9 7 A U G / 9 7 – A U G / 0 1 S e i s m i c 2 D S e i s m i c 3 D S e i s m i c 2 D S e i s m i c 3 D

1 , 1 1 9 . 6 7 5 k m 4 5 , 1 2 4 k m 2 3 2 2 , 5 7 0 k m 1 1 9 , 4 4 9 k m 2

Non-exclusive Surveys

• 71 authorizationsawarded

• 17 authorizations inoperation

E&PE&P Database Database (BDEP) (BDEP)

• 19 registered users• Rock and Fluids Center to be operating in the

second semester of 2003 (port area in Rio deJaneiro)

• Visualization Center will be installed near theSeismic and Wells Center of BDEP, providingconditions to better evaluate Brazil’spetroleum potential

ANP Concessionaire CompaniesANP Concessionaire Companies

• Contracts in the Exploration Phase: 33companies (24 operators)

• Contracts in Development or Production: 18companies (8 operators)

• Concessionaires Total: 39 companies, 26being operators

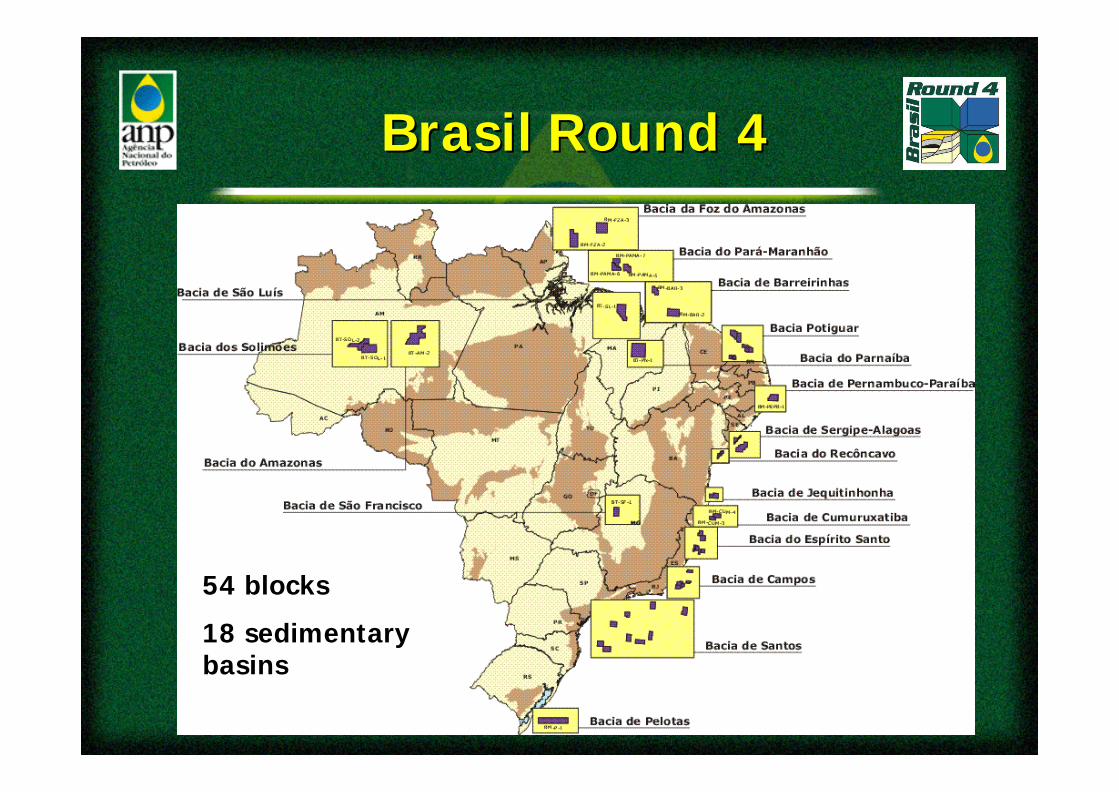

BrasilBrasil Round Round 4 4

54 blocks

18 sedimentarybasins

BrasilBrasil Round Round 4 4Objectives

• Opportunities for companies of differentprofiles

• Continuity of exploration activities alreadyconsolidated in the mature basinsØVery important for regional development

• Stimulate the entry of companies in areas ofless knowledge and greater risk - the newexploration frontiers

BrasilBrasil Round Round 4 4Commitments

• Maintain an open dialogue with the industry• Continue to conduct the process in a

transparent manner, per earlier rounds• Maintain rules and procedures• Information and Data Package of high quality• Keep strictly to the schedule

Recommended