Understanding Excessive

Risk Taking Seen in

Experiments on Financial

Markets

SYstemic Risk TOmography:

Signals, Measurements, Transmission Channels, and Policy Interventions

Jørgen Vitting Andersen, CNRS, Centre d’Economie de la Sorbonne, University of Paris 1. CSRA research meeting – December, 15 2014

Understanding Excessive Risk Taking Seen in

Experiments on Financial Markets

• Jørgen Vitting Andersen, CNRS,

Centre d’Economie de la Sorbonne,

University of Paris 1.

• Research in progress, collaborators:

Yifang Liu, Philippe de Peretti, Maxim

Frolov, Roberto Savona, Hayette Gatfaoui,

Rania Kaffel

Individual versus collective risk taking

• Individual risks: Men are known to be more risk loving

compared to women. For real market traders see e.g. :

“Endogenous steroids and financial risk on a London

trading floor”, J. M. Coates and J. Herbert, PNAS, V.105,

16, 6167-72 (2008); “A note on trader Sharpe Ratios”, J.

M. Coates and L. Page, PLoSONE, V.4, 11, e8036 (2009)

• Collective risks: how does a group of traders with

heterogeneous risk profiles influence the formation of

market risks?

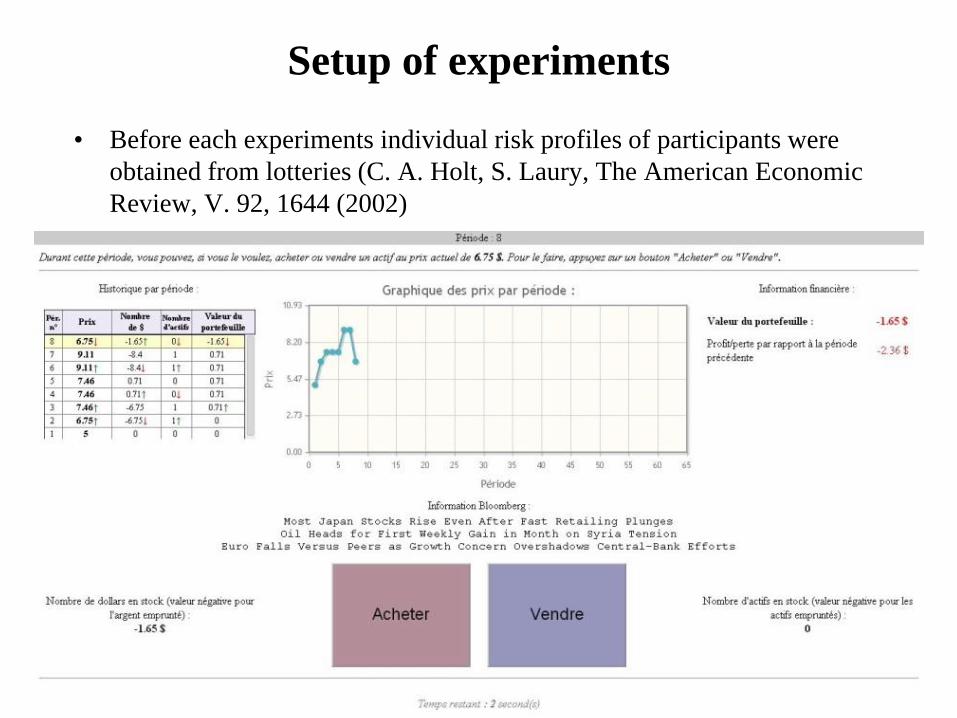

Setup of experiments

• Before each experiments individual risk profiles of participants were

obtained from lotteries (C. A. Holt, S. Laury, The American Economic

Review, V. 92, 1644 (2002)

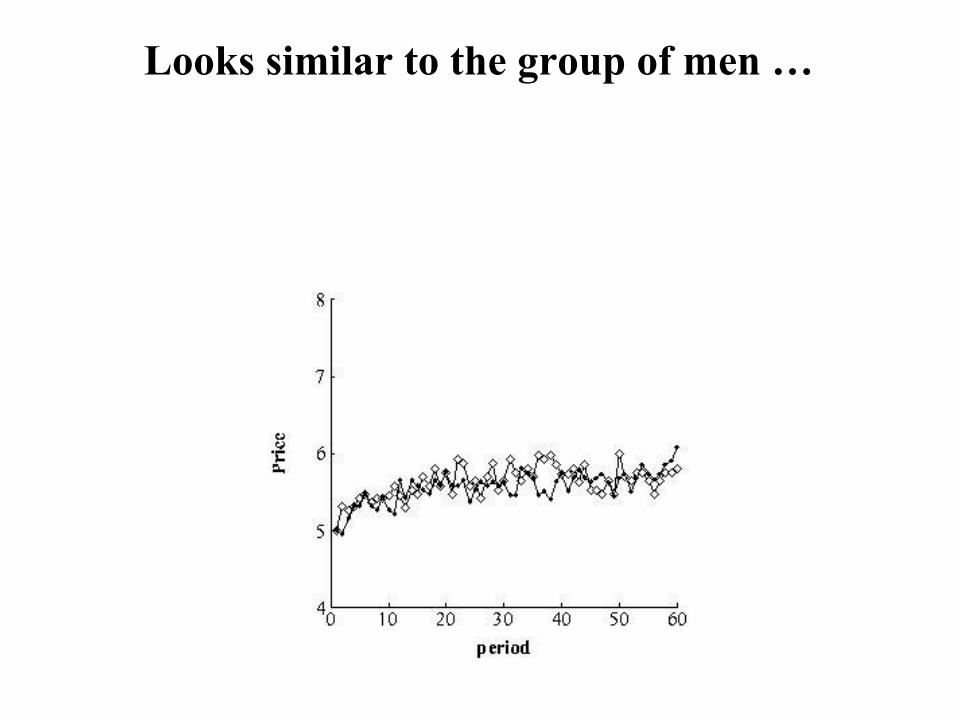

Here’s what happens when a group of men

trade …

Next we let a group of women trade …

Looks similar to the group of men …

Then another group of women … initially this

group of women seem to trade differently…

And indeed in this experiment the group of

women creates a speculative state…

Their speculation however was « dwarfed »

compared to state created by yet another

group of men…

Claim: we need a fluctuation based framework in

order to be able to understand behavior seen in

experiments.

The $-Game

The $-Game

Results: simulations of the $G

Important: Symmetry break

Taking the «temperature» of the market: predicting big

price «swings »

• Internal state of water? Insert a thermometer into the

liquid.

• Internal state of market? «slave » an agent based model to

the price evolution.

• Market in a “hot” or “cold” state.

ACTION

0000 0

0000

0001 0

0100 1

1010

0101 1

0101

0110 1

1011

0111 1

Christmas: for the person who has everything

here a suggestion of an « obvious » Christmas

gift ;)

All

Female

Male

This project has received funding from the European Union’s

Seventh Framework Programme for research, technological

development and demonstration under grant agreement n° 320270

www.syrtoproject.eu

This document reflects only the author’s views.

The European Union is not liable for any use that may be made of the information contained therein.

Recommended

![[1] Aagaard, Troels; Greenwood, Brian; Nielsen, Jorgen · [1] Aagaard, Troels; Greenwood, Brian; Nielsen, Jorgen: Cross-Shore Sediment Transport: A Field Test of the Bailard Energetics](https://img.pdfslide.tips/doc/110x75/5b59407d7f8b9a655d8d0c5d/1-aagaard-troels-greenwood-brian-nielsen-1-aagaard-troels-greenwood.jpg)