Embed Size (px)

Citation preview

Today, let’s s-art with

Solomon Asch’s Experiment

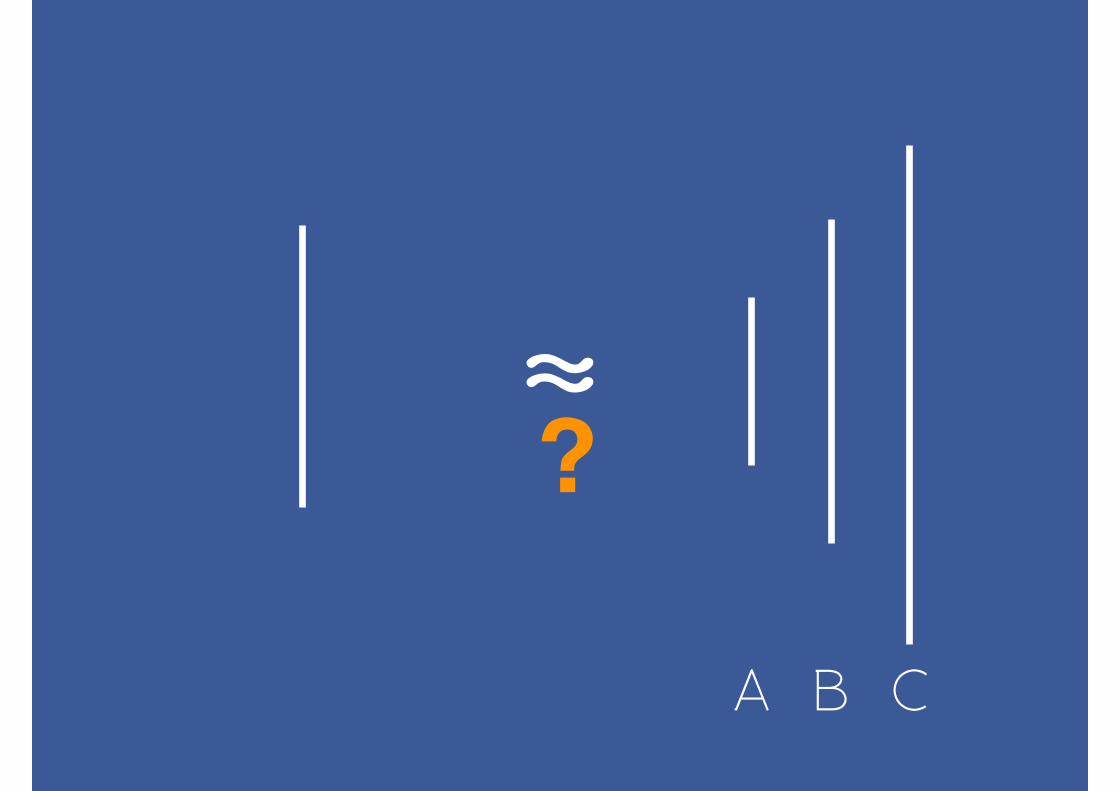

?

A B C

⼼心理OS: 天啊!智障嗎? 這是在污辱我智商嗎?! 當然是B啊!我智商157耶!

東尼史塔克:唉廢話! 當然是A啊!你是⽩白痴嗎,我智商157耶!

WTF! 真的是豬⼀一般的隊友,智商157是什麼⻤⿁鬼!連這種問題都回答錯

⿊黑寡婦:這是什麼⻤⿁鬼問題! 答案當然是A啊!這有什麼好疑問的!!!

…… $%@^&!$#!

隊⻑⾧長:不選A是要選什麼啊?

……

⼩小綠綠隊友:A !!!!!

……

獨眼⻯⿓龍:嘿神明隊友!你勒?

……

神明隊友:當然是A啊!

從 眾 行 為

Herding Behaviour

真正能夠⼀一個打⼗十個的⼈人很少!

挑對隊友變成很重要的事情

正 向 回 饋

Positive Feedback

處 份 效 應

Disposition Effect

資 訊 階 流

Information Cascades

7-11’s City Coffee!

想要Starbuck, … 算了還是City Coffee 好了!

City Coffee 感覺好像⽐比較好

City Coffee 應該沒⽐比較差!

就我觀察啦,City Coffee!

Someday, . . .

The influence of noise traders

Will become apparent

Fisher Black, 1986

Sys-ematic noise

# Speakers: 張博能 | Department of Money and Banking

Brad M. Barber, Terrance Odean, Ning Zhu

Course of Financial Economics @ National Chengchi University

[email protected] | @SCephan_Chang

2015/6/15

有⾜足夠多的⽂文獻、證據證明機構投資⼈人確實有”從眾⾏行為”

可否觀察到散⼾戶的從眾⾏行為?兩者從眾⾏行為的成因是否相同?

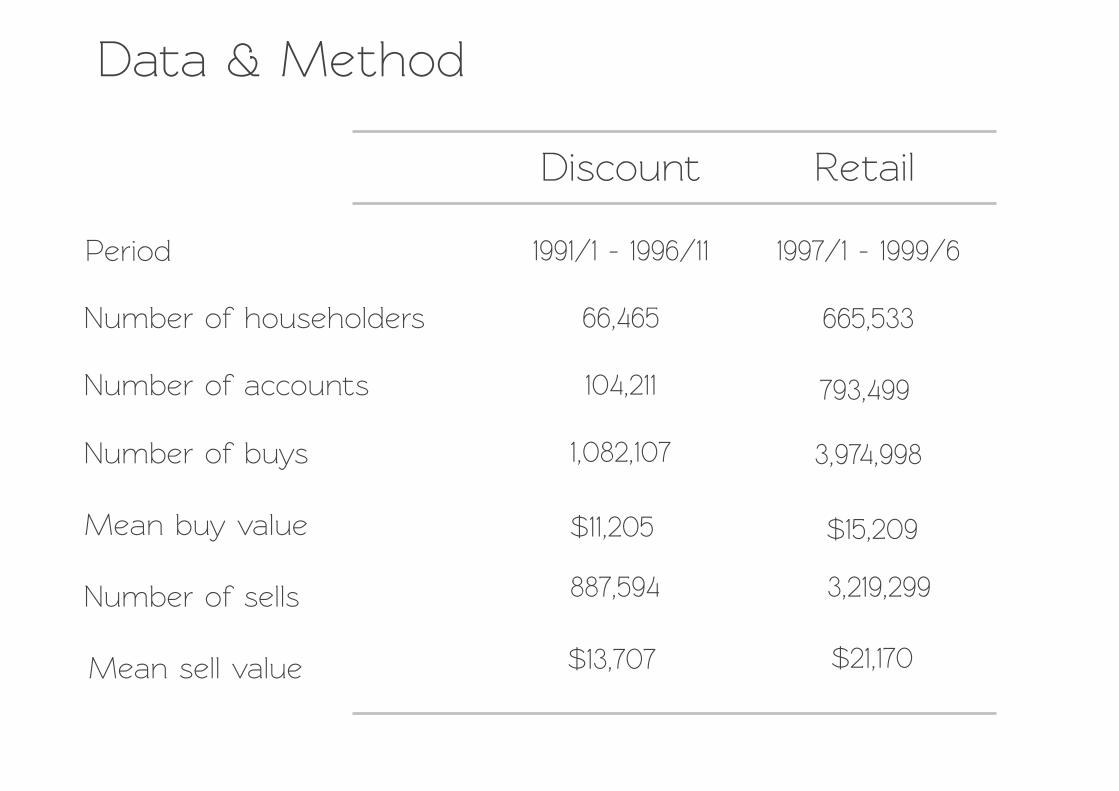

Discount Re+ail

Period

Number of householders

Number of accounts

Number of buys

Mean buy value

Number of sells

Mean sell value

Da+a & Method

1991/1 - 1996/11 1997/1 - 1999/6

66,465 665,533

104,211 793,499

1,082,107 3,974,998

$11,205 $15,209

887,594 3,219,299

$13,707 $21,170

How +o measure the Herding?

Da+a & Method

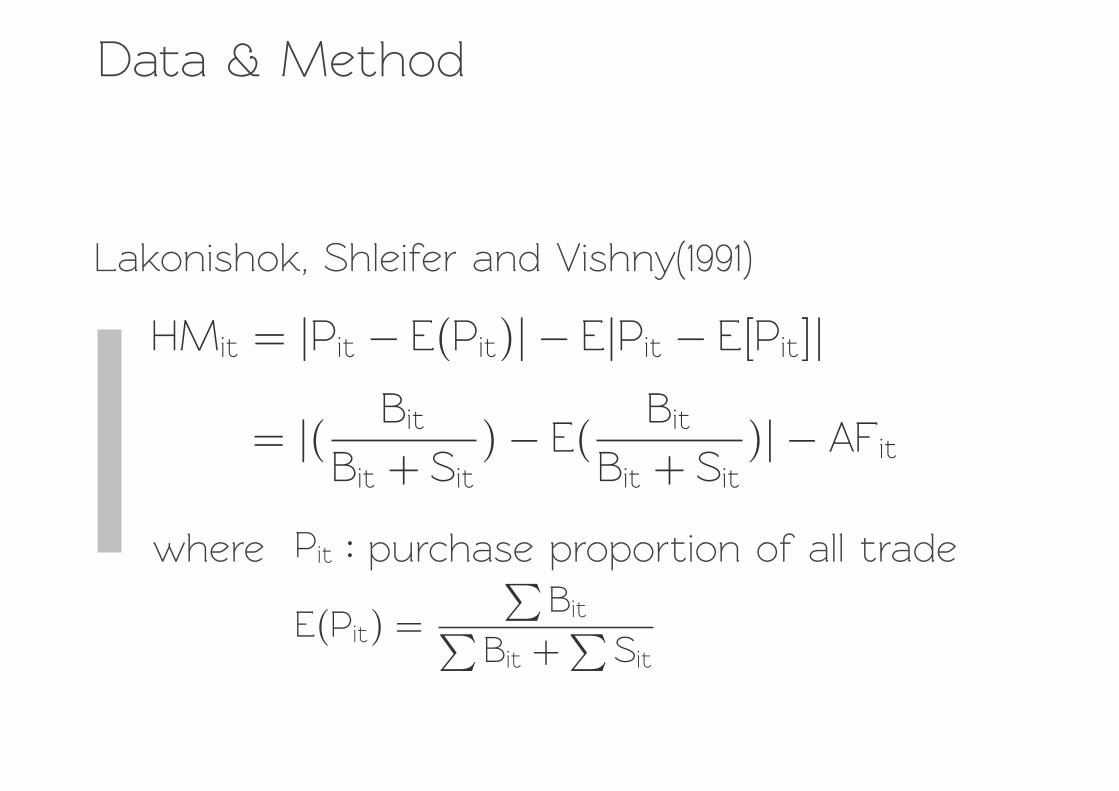

Lakonishok, Shleifer and Vishny(1991)

HMit = |Pit � E(Pit)| � E|Pit � E[Pit]|

= |( Bit

Bit + Sit) � E(

Bit

Bit + Sit)| � AFit

where Pit : purchase proportion of all trade

E(Pit) =

�Bit�

Bit +�

Sit

Da+a & Method

Discount Broker Re+ail Broker

All S+ocks

Large

Medium

Small

0.0681 (< 0.001) ***

0.0758 (< 0.001) ***

0.0659 (< 0.001) ***

0.0637 (< 0.001) ***

0.1279 (< 0.001) ***

0.1138 (< 0.001) ***

0.1313 (< 0.001) ***

0.1250 (< 0.001) ***

Common Shift in risk-aversion ?

Con+emporaneously ?

Over Time ?

Da+a & Method

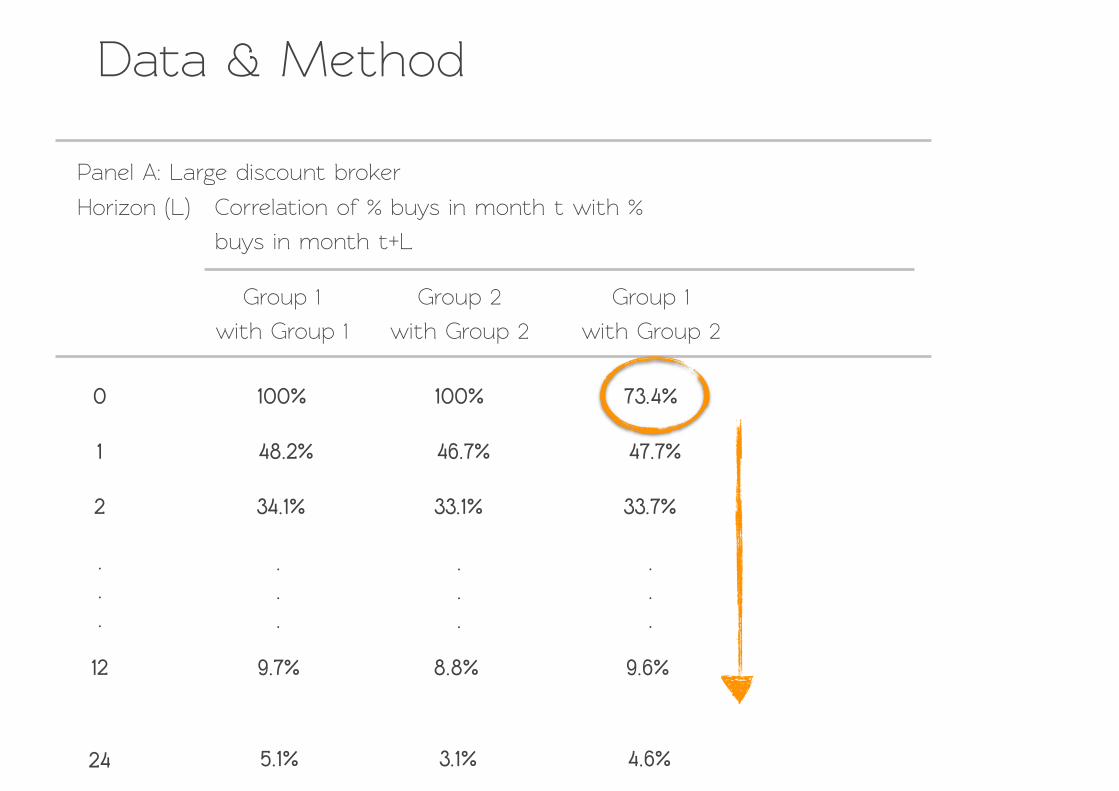

Panel A: Large discount broker

Group 1

with Group 1

Group 2

with Group 2

Horizon (L) Correlation of % buys in month t with %

buys in month t+L

Group 1

with Group 2

0

1

2

.

.

.

12

24

100% 100% 73.4%

48.2% 46.7% 47.7%

34.1% 33.1% 33.7%

9.7% 8.8% 9.6%

5.1% 3.1% 4.6%

.

.

.

.

.

.

.

.

.

Da+a & Method

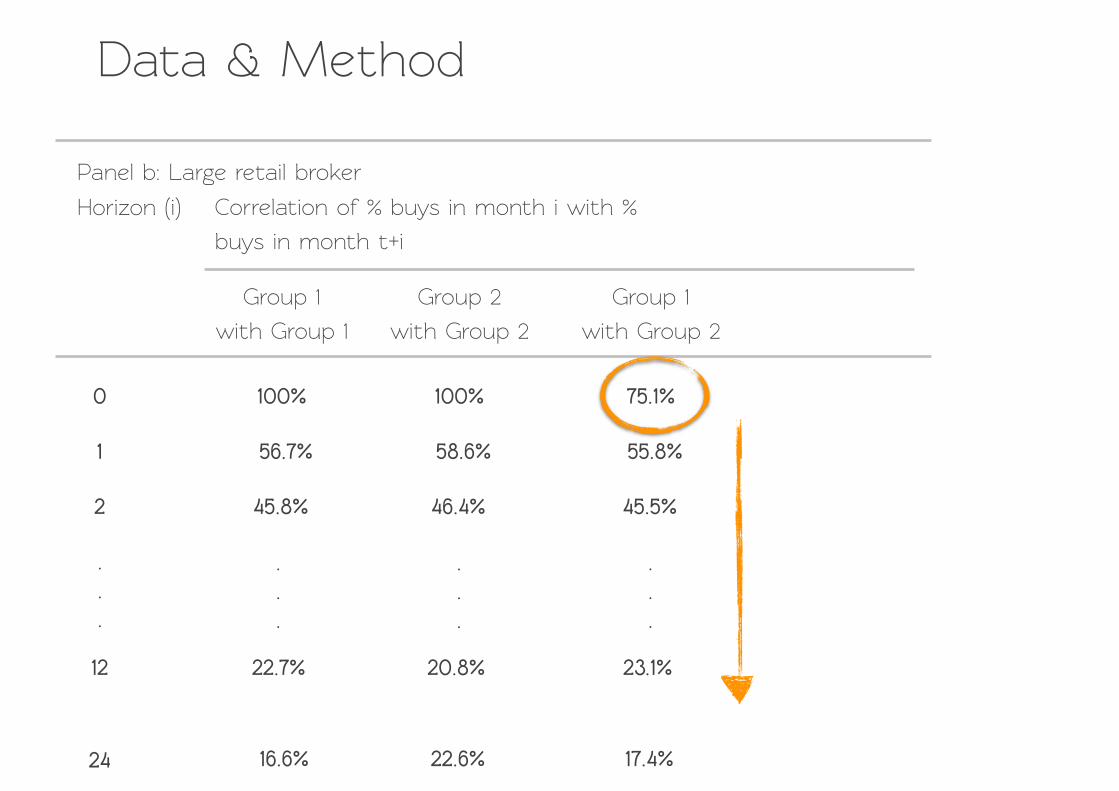

Panel b: Large re+ail broker

Group 1

with Group 1

Group 2

with Group 2

Horizon (i) Correlation of % buys in month i with %

buys in month t+i

Group 1

with Group 2

0

1

2

.

.

.

12

24

100% 100% 75.1%

56.7% 58.6% 55.8%

45.8% 46.4% 45.5%

22.7% 20.8% 23.1%

16.6% 22.6% 17.4%

.

.

.

.

.

.

.

.

.

Institutional Herding ?

1. Principal-agent concerns

2. Information Cascades

3. Rational response +o correla+ed

information

Individuals’ Herding

Unfil+ered da+a = Market orders

+ Limit Orders

1. Limit order driven?

Accounts = +axable accounts

+ +ax-deferred accounts

2. Avoid +ax losing

3. Risk-aversion ?

Use firms’ size as proxy for risk

(Berk, 1995)

Let’s have discussion about

Psychological biases

Represen+ativeness Heuristic

Overweight the impor+ance of past

return when forecasting future’s

Sell winners, hold on+o losing

Disposition Effect

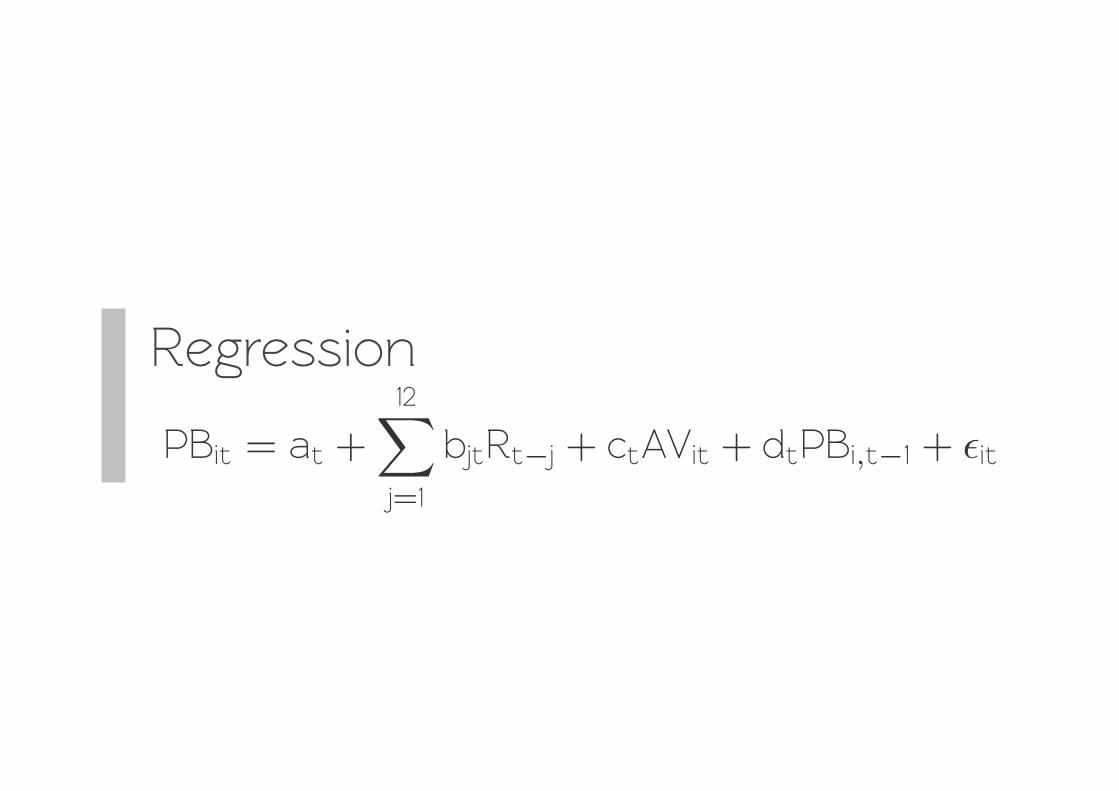

Regression

PBit = at +12�

j=1

bjtRt�j + ctAVit + dtPBi,t�1 + �it

自 我 因 循

Self-herding

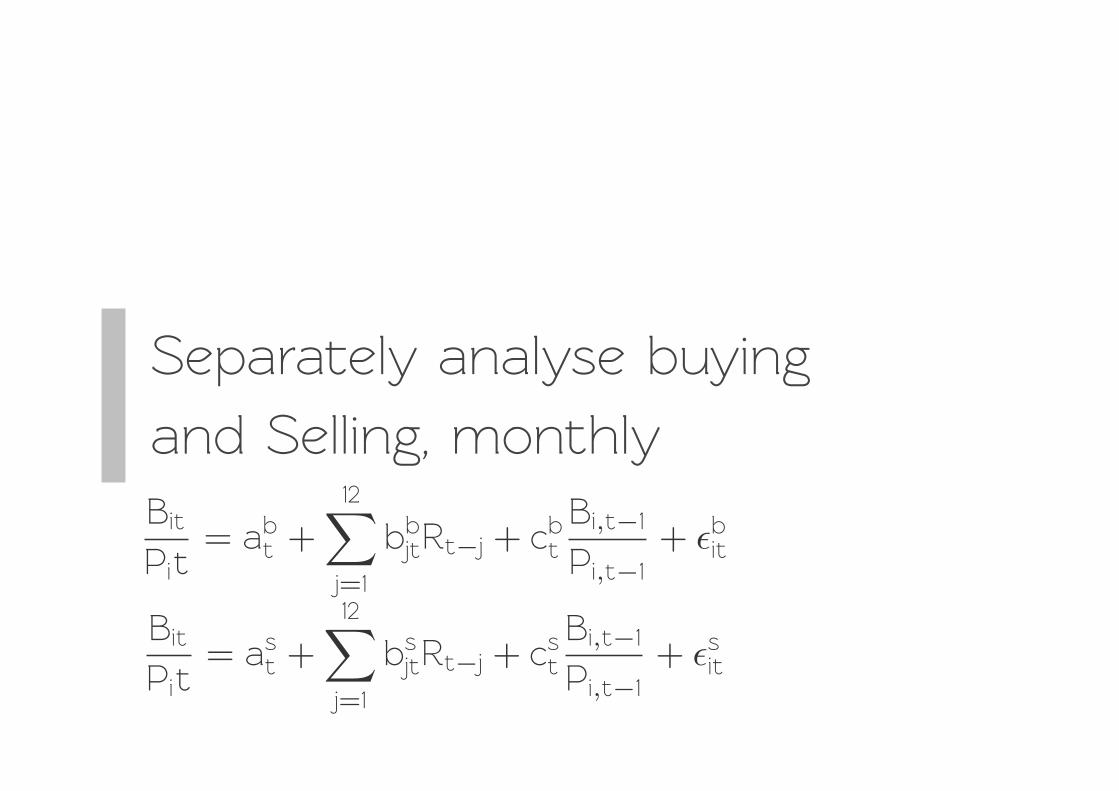

Separa+ely analyse buying

and Selling, monthlyBit

Pit= ab

t +12�

j=1

bbjtRt�j + cbt

Bi,t�1

Pi,t�1+ �bit

Bit

Pit= as

t +12�

j=1

bsjtRt�j + cst

Bi,t�1

Pi,t�1+ �sit

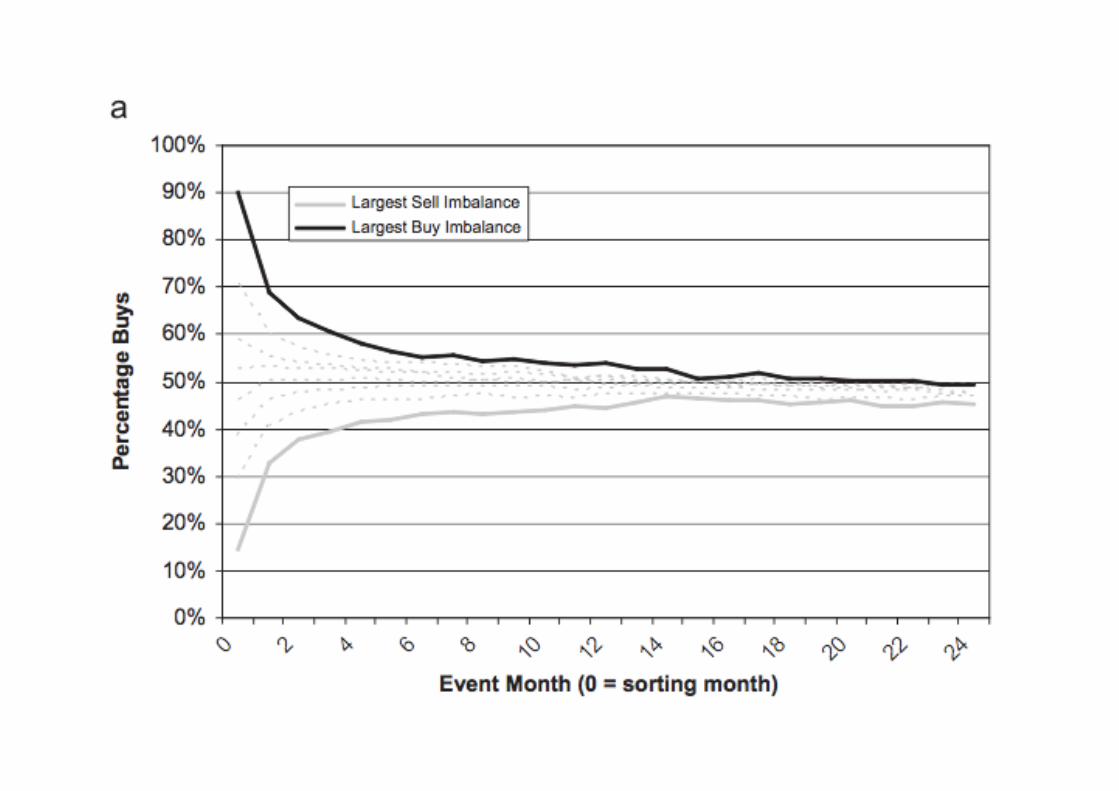

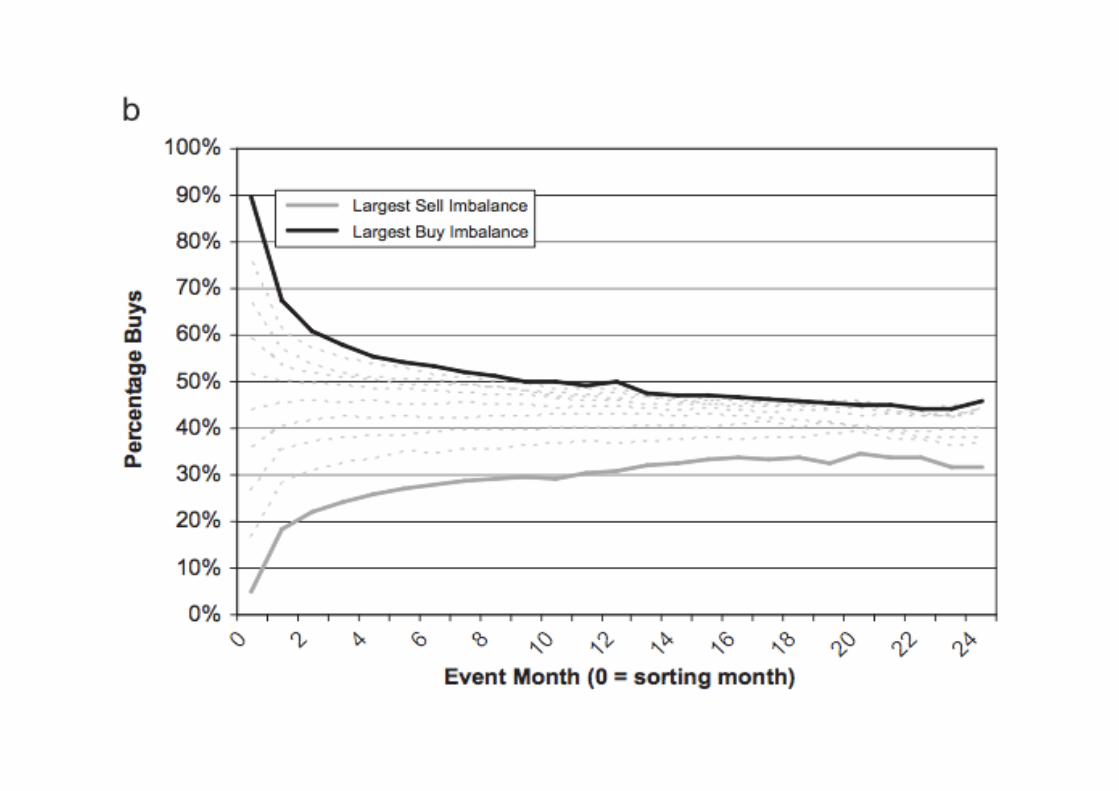

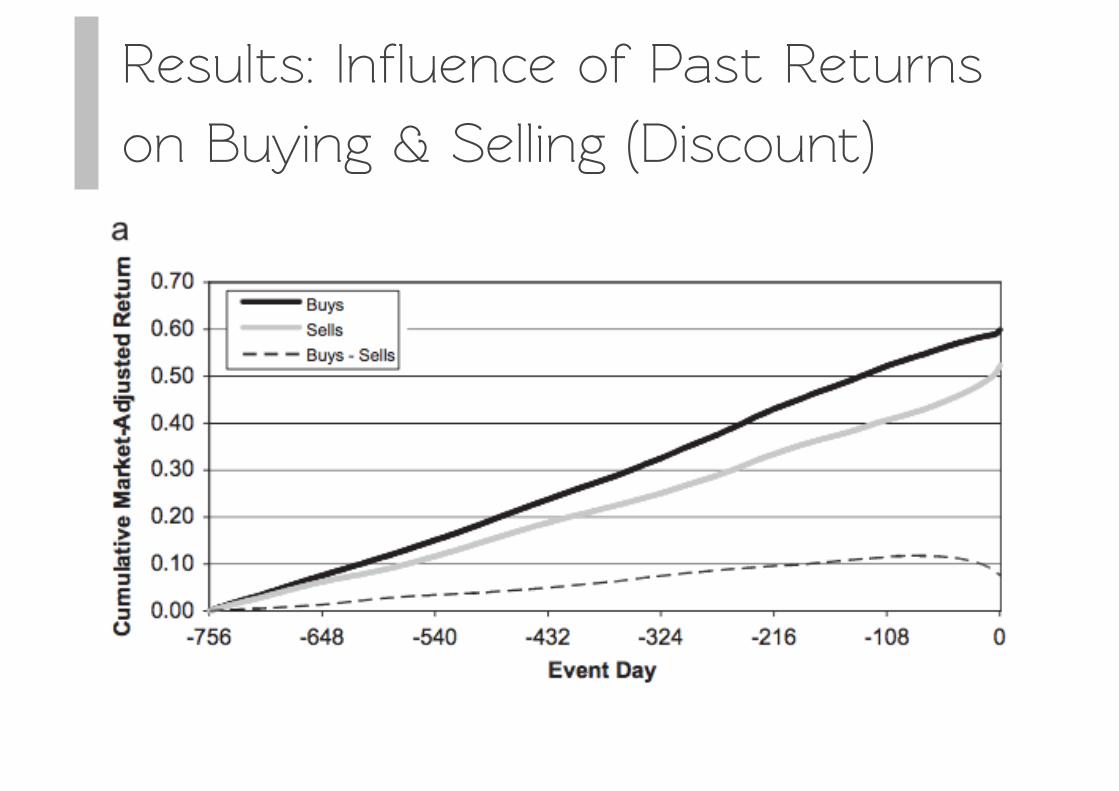

Results: Influence of Past Returns

on Buying & Selling (Discount)

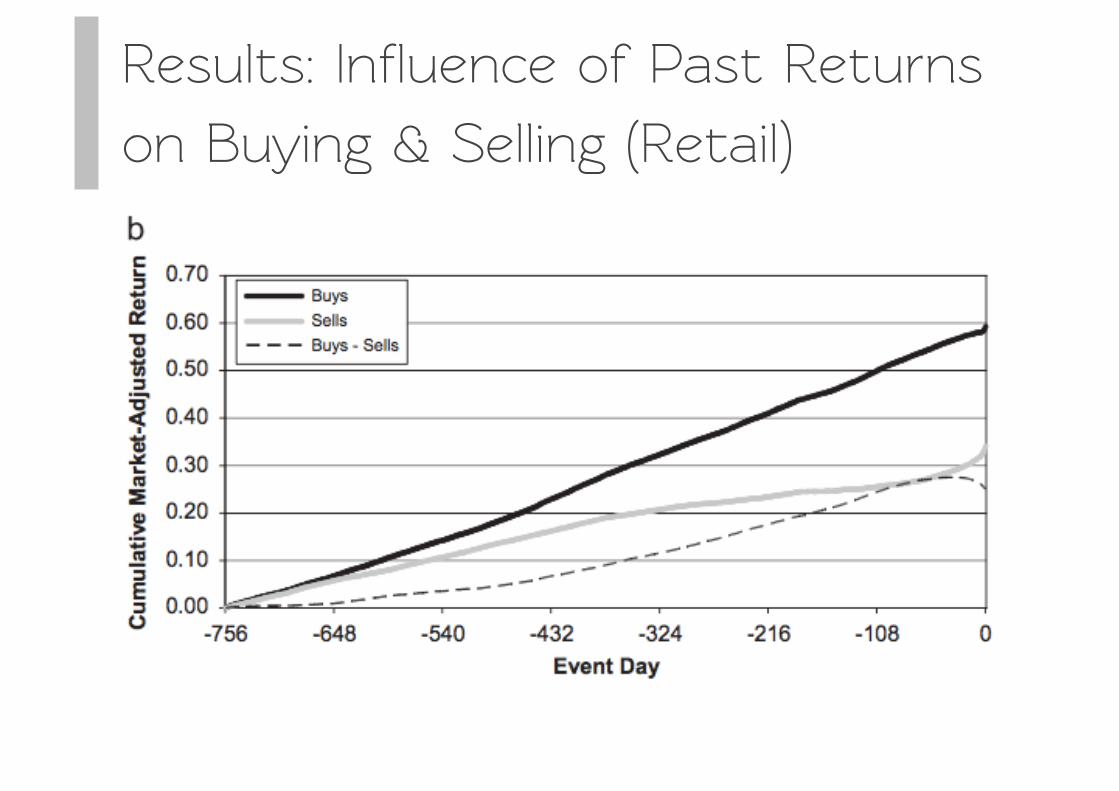

Results: Influence of Past Returns

on Buying & Selling (Re+ail)

The purchase and sale decisions of

individual inves+ors are highly correla+ed.

Summary

These are not primarily driven by:

Summary

> Passive response +o trades of institutional inves+ors

> Tax loss selling

> Risk preference

Inves+ors buy and sell s+ocks with

strong past returns.

Summary

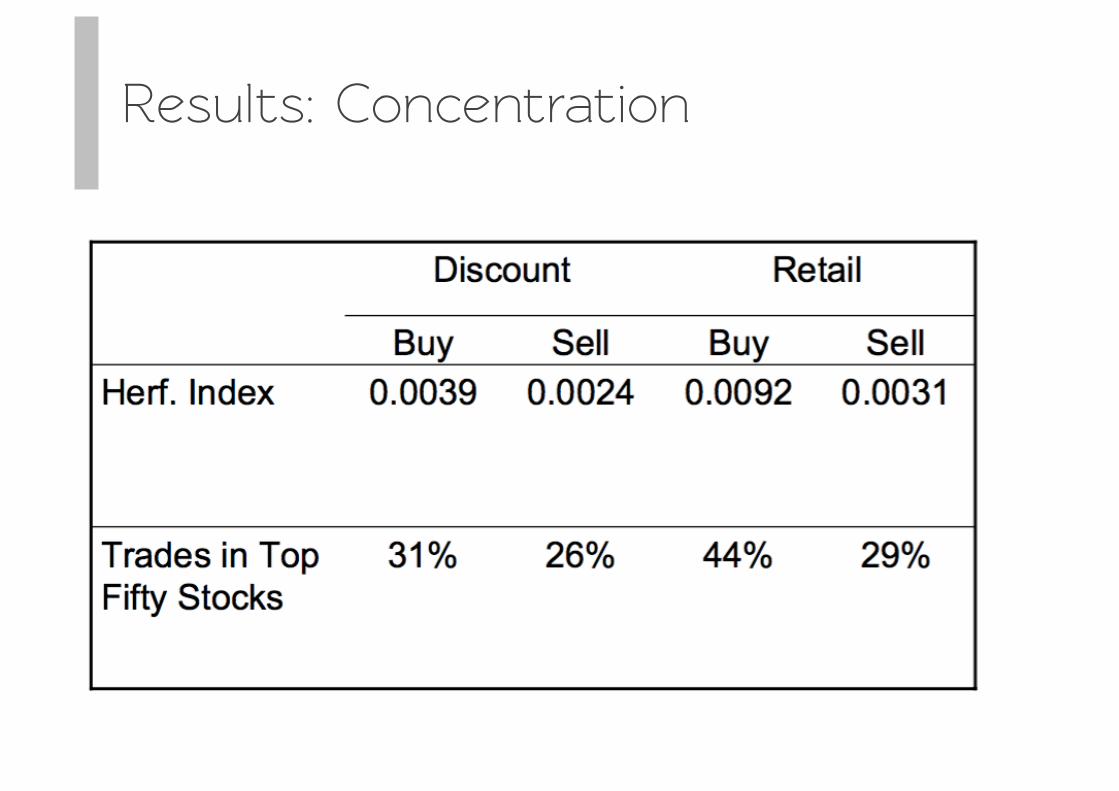

Results: Concentration

Buying is concentra+ed in fewer s+ocks

than selling

Summary

Inves+ors are net buyers of s+ocks with

unusually high trading volume.

Summary

Individual inves+ors, sometimes referred

+o as noise traders, have the po+ential

+o affect asset prices because their

noise is sys+ematic.

Conclusion

Thanks for your at+ention :)