Embed Size (px)

Citation preview

Chapter 13: Working Capital Management

Group 8:Phan Nguyễn Phương Anh_295918Đỗ Thị Phương Dung_295889Nguyễn Hải Phương Hạnh_295903Lê Thị Thanh Tâm_295897

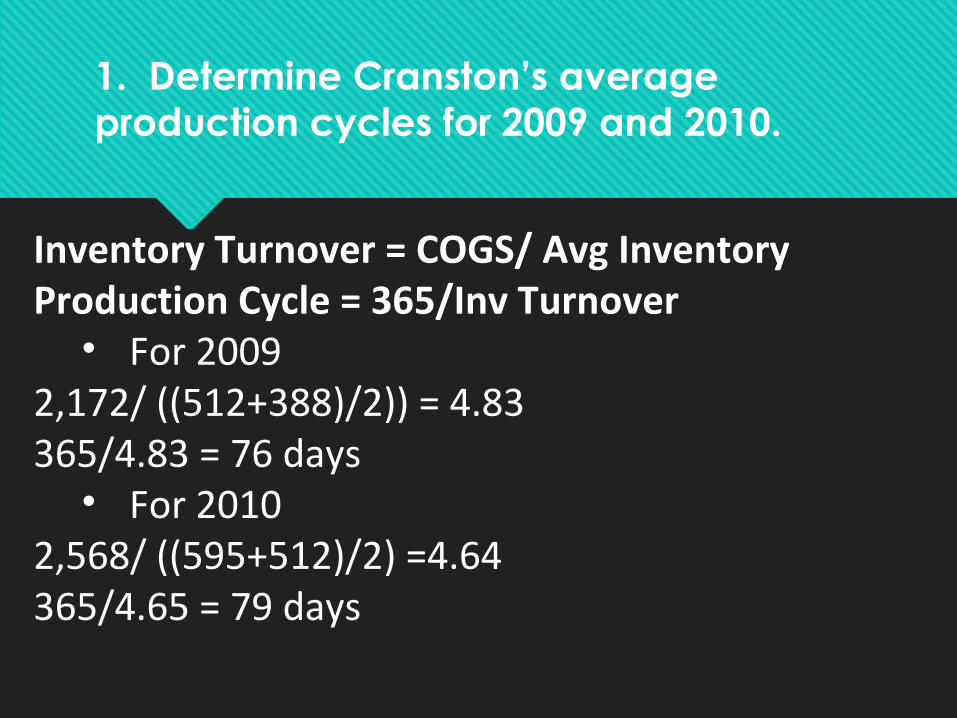

1. Determine Cranston’s average production cycles for 2009 and 2010.

Inventory Turnover = COGS/ Avg Inventory Production Cycle = 365/Inv Turnover

• For 2009 2,172/ ((512+388)/2)) = 4.83 365/4.83 = 76 days

• For 2010 2,568/ ((595+512)/2) =4.64 365/4.65 = 79 days

2. Determine Cranston’s average collection cycles for 2009 and 2010. Assume that all sales are credit sales.

Receivable Turnover = Credit Sales/ Avg Acc. Rec. Collection cycle = 365/Receivables Turnover

• For 2009 3,202/((642+320)/2) = 6.66 365/6.66=55 days

• For 2010 3,784/ ((722+642)/2) = 5.55 365/5.55 = 66 days

3. Determine Cranston’s average payment cycles for 2009 and 2010.

Payables turnover = COGS/Avg Acc Payable Payment cycle = 365/Payables Turnover • For 2009

2,172/ ((288+204)/2) = 8.83 365/8.83 = 41 • For 2010

2,568/ ((332+288)/2) = 8.28 365/8.28 = 44 days

4. Using your answers to Questions 1 through 3, determine Cranston’s cash conversion cycles for 2009 and 2010.

• For 2010 Business cycle = 79 + 66 = 145 days Cash conversion cycle = 145-44 = 101 days • For 2009

Business cycle = 76 + 55 = 131 days Cash conversion cycle = 131-41 = 90 days

5. Cranston now bills its customers on terms of net 45, meaning that payment is due on the forty-fifth day after the goods are shipped. Although most customers pay on time, some routinely stretch the payment period to sixty and even ninety day. What steps can Cranston take to encourage clients to pay on time? What is the potential risk of implementing penalties for late payment?

• Cranston has both carrot and stick approaches available_ a polite reminder call

• The company could impose penalties on late payments• The company could also offer a discount for early payment.• Penalties run the risk of alienating some customers who may choose to

take their business elsewhere. Cranston would need to be especially careful not to lose very large accounts that are an important part of their business.

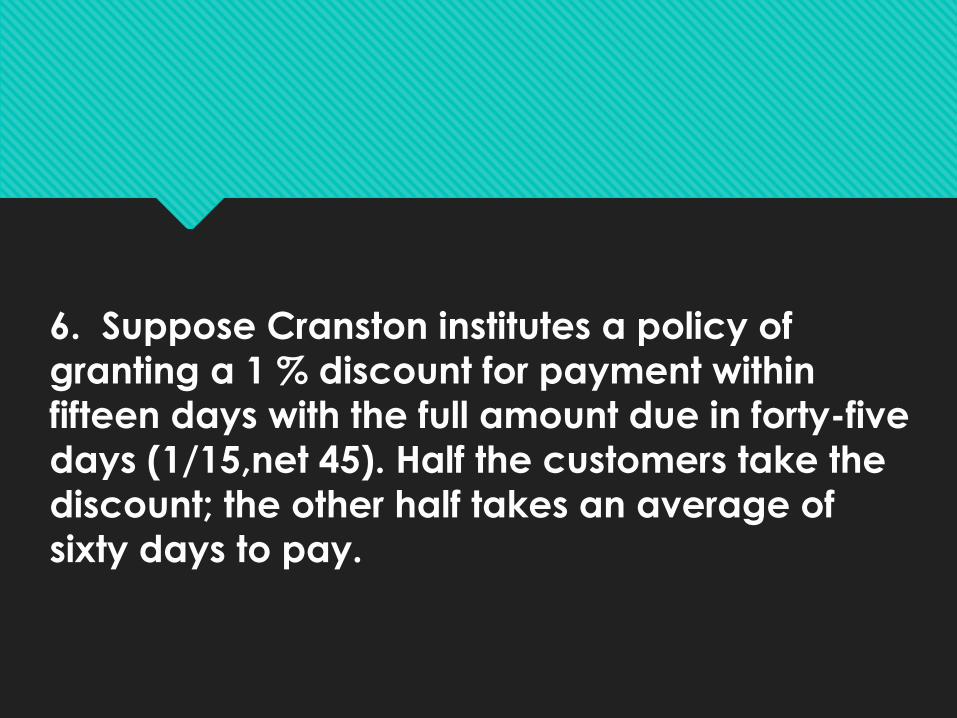

6. Suppose Cranston institutes a policy of granting a 1 % discount for payment within fifteen days with the full amount due in forty-five days (1/15,net 45). Half the customers take the discount; the other half takes an average of sixty days to pay.

a.) What would be the length of Cranston’s collection cycle under this new

policy? The new collection period will be 15/2 + 60/2 = 47.5 days. Customers who forego the discount will apparently take another 15 days beyond the due date.

b.) In dollars, how much would the policy have cost Cranston in 2010? Cranston would lose 1% on half of its sales, or $3,784/2 × .01 = $18.92 million

before taxes. Since this amount would not be taxed, we can estimate the after-tax

effect as $18.92 million × (1-119.55/398.50) = approximately $13.24 million.

c.) If this policy had been in effect during 2010, by how many days would the

cash conversion cycle have been shortened? In 2010, the collection cycle was 66 days. The new policy would shorten the

collection period, and the cash conversion cycle, by 66 – 47.5 = 18.5 days.

7. An image-based lockbox system could accelerate Cranston’s cash collections by three days. Cranston can earn an annual rate of 6% on the cash freed by accelerated collections. Using sales for 2010, what is the most Cranston should be willing to pay per year for the lockbox system?

The lockbox system would free up 3 days sales or $3,784/365 × 3 = $31.10 million dollars.

If Cranston can earn 6% on this money, the lockbox system would be advantageous at any cost less than $31.10 million × .06 =$1.866 million per year.

8. One of Cranston’s principal raw materials is plastic pellets, which it purchases in lots of 100 pounds at $0.35 per pound. Annual consumption is 8,000,000 pounds. Within a broad range of order sizes, ordering and shipping costs are $120 per order. Carrying costs are $1.50 per year per 100 pounds. Compute the Economic Order Quantity for plastic pellets. The pellets can only be ordered in whole lots of 100 pounds, so use 8,000,000/100 as S in Equation 13.17. If Cranston used the EOQ model, how often would it order pellets?

EOQ = (2 × 800,000 × 120/1.50)1/2 =11,314 lots per order.800,000/ 11,314 = 71, so Cranston would be placing orders every five days.

Thanks for attention.