Embed Size (px)

Citation preview

[March, 2015]

Islamic University of Gaza

Deanery of Graduate Studies

College of Engineering

Architecture Department By: Aliaa M. Shamallakh

Housing Policies Singapore

I

CONTENTS

1. INTRODUCTION :

1.1 Brief on country geography and history ………………………………………………………… 1

1.2 Demographics ………………………………………………………………………………………………. 2

1.3 The 2conomy…………………………………………………………………………………….…………… 2

1.4 Employment and Poverty…………………………………………………………………………….... 3

2. HOUSING HISTORY: 2.1 Overview ……………………………………………………………………………………………………….. 4

2.2 Phases of Housing policies in post-war period ……………………………………………….. 5

2.2.1 Phase I: Shortage of Housing ……………………………………………………………….… 5

2.2.2 Phase II (1979 – Early 1990s): Resale Market Deregulation …………………... 10

2.2.3 Phase III (Early 1990s – 1997): Financial Liberalization ……………………….…. 12

2.2.4 Phase IV (1998 – Present): Excess Housing Stock …………………………………… 14

3. GOALS & PRINCIPLES: 3.1 Developing Vibrant Towns …………………………………………………………………………….. 15

3.2 Providing Affordable Homes ………………………………………………………………………….. 16

3.3 Cohesive Communities …………………………………………………………………………………… 17

4. POLICIES’ OUT-COMES: 4.1 Under the Lee Kuan Yew Government, 1959 – 1990 ……………………………………… 19

4.2 Under the Goh Chok Tong Government, 1990 – 2004 ……………………………………. 21

4.3 Under the Lee Hsien Loong Government, 2004 – Present ……………………………… 21

5. PROBLEMS & CHALLENGES 24

6. CONCLUSION 28

7. REFERENCES 29

1

This part briefly introduces Singapore in order to set the context for subsequent parts. It focuses on country basics such as geography, history, demographics, the economy, and employment and poverty. It also includes a section on household incomes and poverty. Finally, there is a brief on urban development in Singapore.

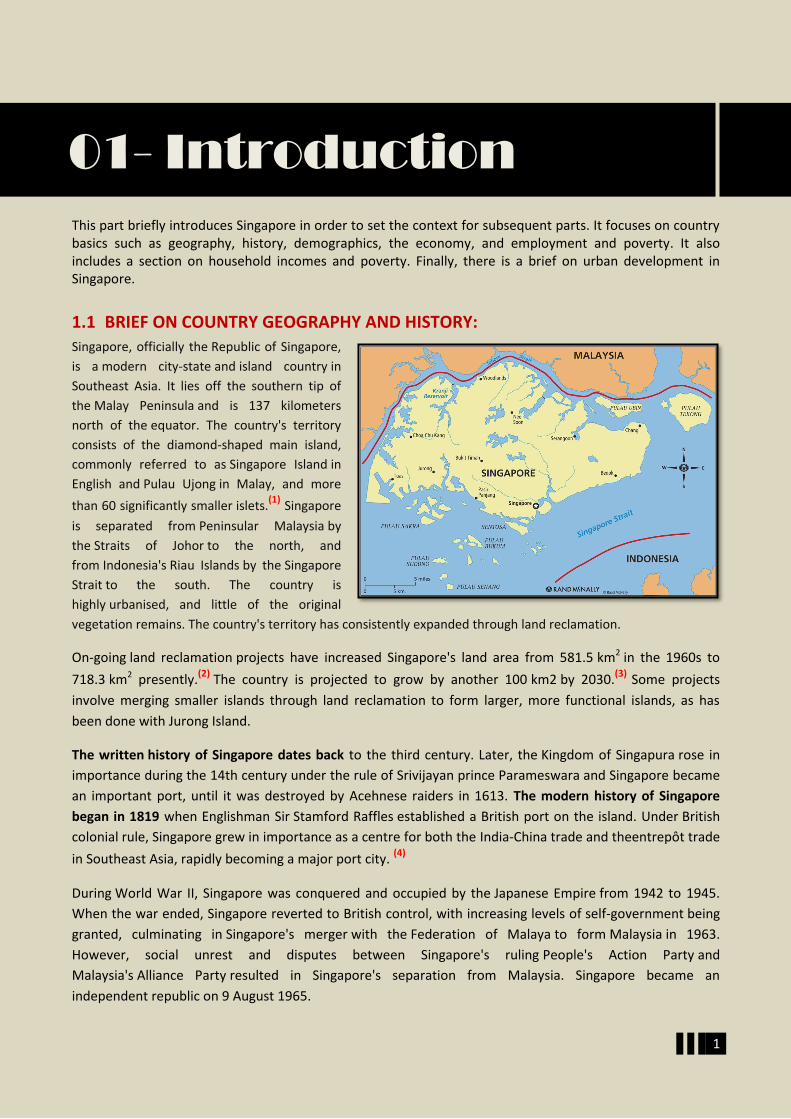

1.1 BRIEF ON COUNTRY GEOGRAPHY AND HISTORY: Singapore, officially the Republic of Singapore,

is a modern city-state and island country in

Southeast Asia. It lies off the southern tip of

the Malay Peninsula and is 137 kilometers

north of the equator. The country's territory

consists of the diamond-shaped main island,

commonly referred to as Singapore Island in

English and Pulau Ujong in Malay, and more

than 60 significantly smaller islets.(1)

Singapore

is separated from Peninsular Malaysia by

the Straits of Johor to the north, and

from Indonesia's Riau Islands by the Singapore

Strait to the south. The country is

highly urbanised, and little of the original

vegetation remains. The country's territory has consistently expanded through land reclamation.

On-going land reclamation projects have increased Singapore's land area from 581.5 km2 in the 1960s to

718.3 km2 presently.(2) The country is projected to grow by another 100 km2 by 2030.(3) Some projects

involve merging smaller islands through land reclamation to form larger, more functional islands, as has

been done with Jurong Island.

The written history of Singapore dates back to the third century. Later, the Kingdom of Singapura rose in

importance during the 14th century under the rule of Srivijayan prince Parameswara and Singapore became

an important port, until it was destroyed by Acehnese raiders in 1613. The modern history of Singapore

began in 1819 when Englishman Sir Stamford Raffles established a British port on the island. Under British

colonial rule, Singapore grew in importance as a centre for both the India-China trade and theentrepôt trade

in Southeast Asia, rapidly becoming a major port city. (4)

During World War II, Singapore was conquered and occupied by the Japanese Empire from 1942 to 1945.

When the war ended, Singapore reverted to British control, with increasing levels of self-government being

granted, culminating in Singapore's merger with the Federation of Malaya to form Malaysia in 1963.

However, social unrest and disputes between Singapore's ruling People's Action Party and

Malaysia's Alliance Party resulted in Singapore's separation from Malaysia. Singapore became an

independent republic on 9 August 1965.

01- Introduction

2

Facing severe unemployment and a housing crisis, Singapore embarked on a modernization programme

beginning in the late 1960s through the 1970s that focused on establishing a manufacturing industry,

developing large public housing estates and investing heavily on public education. Since independence,

Singapore's economy has grown by an average of 9% each year. By the 1990s, the country had become one

of the world's most prosperous nations, with a highly developed free market economy, strong international

trading links, and the highest per capita gross domestic product in Asia outside of Japan. (5)

1.2 DEMOGRAPHICS:

As of mid-2014, the estimated population of Singapore was 5,469,700 people, 3,343,000 (61.12%) of whom

were citizens, while the remaining 2,126,700 (38.88%) were permanent residents (527,700) or foreign

students/foreign workers/dependants (1,599,000). (6) According to the census in 2010 (the most recent

census), 23% of Singaporean residents (i.e. citizens and permanent residents) are foreign born. (7)

The average household size is 3.47 persons. Due to scarcity of land, 81.9% of resident households (i.e.

households headed by a Singapore citizen or permanent resident) live in subsidised, high-rise, public housing

apartments known as Housing and Development Board (HDB) flats, after the board responsible for public

housing in the country. (7) (8) Live-in foreign domestic workers are quite common in Singapore, with about

224,500 foreign domestic workers there, as of December 2013. (9)

In 2010, three quarters of Singaporean residents live in properties that are equal to or larger than a four-

room HDB flat or in private housing. The rate of home ownership is 87%. Mobile phone penetration rate is

extremely high at 156 mobile phone subscribers per 100 people. (10)

The median age of Singaporean residents is 39.3, and the total fertility rate is estimated to be 0.80 children

per woman in 2014, the lowest in the world and well below the 2.1 needed to replace the population. To

overcome this problem, the Singapore government has been encouraging foreigners to immigrate to

Singapore for the past few decades. The large number of immigrants has kept Singapore's population from

declining. (11) Singapore traditionally has one of the lowest unemployment rates among developed countries.

The Singaporean unemployment rate has not exceeded 4% in the past decade, hitting a high of 3% during

the 2009 global financial crisis and falling to 1.9% in 2011. (12)

1.3 THE ECONOMY:

Pre-independence economy

Before independence in 1965, Singapore was the capital of the British Straits Settlements, a Crown Colony. It

was also the main British naval base in East Asia. Because it was the main British naval base in the region and

held the Singapore Naval Base, the largest dry dock of its time, Singapore was commonly described in the

press as the 'Gibraltar of the East'.(13) The opening of the Suez Canal in 1869 caused a major increase in trade

between Europe and Asia, helping Singapore become a major world trade center, and turning the Port of

Singapore into one of the largest and busiest ports in the world.(14) Prior to 1965, Singapore had a GDP per

capita of $ 700, then the third-highest in East Asia.(15) After independence, the combination of foreign direct

investment and a state-led drive for industrialisation, based on plans by Goh Keng Swee and Albert

Winsemius, started the expansion of the country's economy.

3

Modern-day economy

Today, Singapore has a highly developed market economy, based historically on extended entrepôt trade.

The Singaporean economy is known as one of the freest,(16)

most innovative, most competitive, and most

business-friendly. The 2013 Index of Economic Freedom ranks Singapore as the second freest economy in

the world, behind Hong Kong. According to the Corruption Perceptions Index, Singapore is consistently

ranked as one of the least corrupt countries in the world, along with New Zealand and

the Scandinavian countries.

Singapore is the 14th largest exporter and the 15th largest importer in the world. The country has the

highest trade-to-GDP ratio in the world at 407.9 percent, signifying the importance of trade to its economy.

The country is currently the only Asian country to receive AAA credit ratings from all three major credit

rating agencies: Standard & Poor's, Moody's, Fitch.(17)(18)

Singapore attracts a large amount of foreign

investment as a result of its location, corruption-free environment, skilled workforce, low tax rates and

advanced infrastructure. There are more than 7,000 multinational corporations from the United States,

Japan, and Europe in Singapore. There are also approximately 1,500 companies from China and a similar

number from India. Foreign firms are found in almost all sectors of the country's economy. Singapore is also

the second-largest foreign investor in India.(19)

Roughly 44 percent of the Singaporean workforce is made up

of non-Singaporeans. Over ten free-trade agreements have been signed with other countries and

regions. Despite market freedom, Singapore's government operations have a significant stake in the

economy, contributing 22% of the GDP.

Singapore also possesses the world's eleventh largest foreign reserves, and has one of the highest net

international investment positions per capita. The currency of Singapore is the Singapore dollar, issued by

the Monetary Authority of Singapore. It is interchangeable with the Brunei dollar.

In recent years, the country has been identified as an increasingly popular tax haven for the wealthy due to

the low tax rate on personal income and tax exemptions on foreign-based income and capital gains.

Australian millionaire retailer Brett Blundy, with an estimated personal wealth worth AU$835 million, and

multi-billionaire Facebook co-founder Eduardo Saverin are two examples of wealthy individuals who have

settled in Singapore (Blundy in 2013 and Saverin in 2012).(20) Singapore ranked fifth on the Tax Justice

Network's 2013 Financial Secrecy Index of the world's top tax havens, scoring narrowly ahead of the United

States.

1.4 EMPLOYMENT AND POVERTY:

Singapore has the world's highest percentage of millionaires, with one out of every six households having at

least one million US dollars in disposable wealth. This excludes property, businesses, and luxury goods,

which if included would increase the number of millionaires, especially as property in Singapore is among

the world’s most expensive.(21) Singapore does not have a minimum wage, believing that it would lower its

competitiveness. It also has one of the highest income inequalities among developed countries, being below

Hong Kong and above the United States.(22)

Acute poverty is rare in Singapore. The government has rejected the idea of a generous welfare system, stating that each generation must earn and save enough for its entire life cycle. There are, however, numerous means-tested assistance programs provided by the Ministry of Social and Family Development. Some of the programs include providing between SGD 400 and SGD 1000 per month to needy households, free medical care at government hospitals, money for children's school fees, rental of studio apartments and

training grants for courses.(23)

4

This part focuses on the history, policy, schemes, and programs relating to housing sector and management. It first takes an historic approach, describing the efforts of government over the last five decades to regulate and plan for urban development, to develop programs, and policies to support affordable housing, and to combat poverty. Then descriptions of the main institutions in housing operating today and the programs they support are presented.

Before proceeding, it is worthwhile to summarize the results of the efforts by government and its institutions to develop and support the housing sector, mainly through enabling schemes and programs. It is undeniable that there has been impressive progress in advancing the accessibility and quality of shelter for a very large segment of the Singaporeans population. The banking sector has developed a sophisticated range of housing loan products to target a wide range of clients.

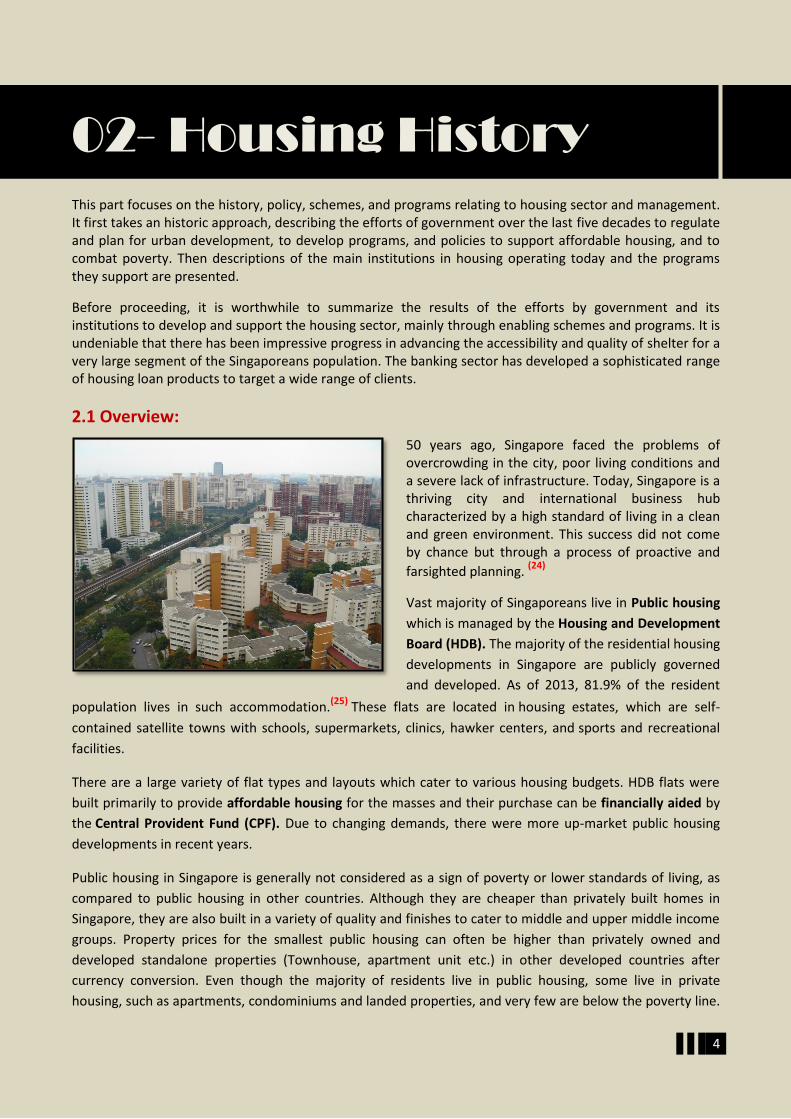

2.1 Overview:

50 years ago, Singapore faced the problems of overcrowding in the city, poor living conditions and a severe lack of infrastructure. Today, Singapore is a thriving city and international business hub characterized by a high standard of living in a clean and green environment. This success did not come by chance but through a process of proactive and

farsighted planning. (24)

Vast majority of Singaporeans live in Public housing

which is managed by the Housing and Development

Board (HDB). The majority of the residential housing

developments in Singapore are publicly governed

and developed. As of 2013, 81.9% of the resident

population lives in such accommodation.(25) These flats are located in housing estates, which are self-

contained satellite towns with schools, supermarkets, clinics, hawker centers, and sports and recreational

facilities.

There are a large variety of flat types and layouts which cater to various housing budgets. HDB flats were

built primarily to provide affordable housing for the masses and their purchase can be financially aided by

the Central Provident Fund (CPF). Due to changing demands, there were more up-market public housing

developments in recent years.

Public housing in Singapore is generally not considered as a sign of poverty or lower standards of living, as

compared to public housing in other countries. Although they are cheaper than privately built homes in

Singapore, they are also built in a variety of quality and finishes to cater to middle and upper middle income

groups. Property prices for the smallest public housing can often be higher than privately owned and

developed standalone properties (Townhouse, apartment unit etc.) in other developed countries after

currency conversion. Even though the majority of residents live in public housing, some live in private

housing, such as apartments, condominiums and landed properties, and very few are below the poverty line.

02- Housing History

5

2.2 PHASES OF HOUSING POLICIES IN POST-

WAR PERIOD IN SINGAPORE:

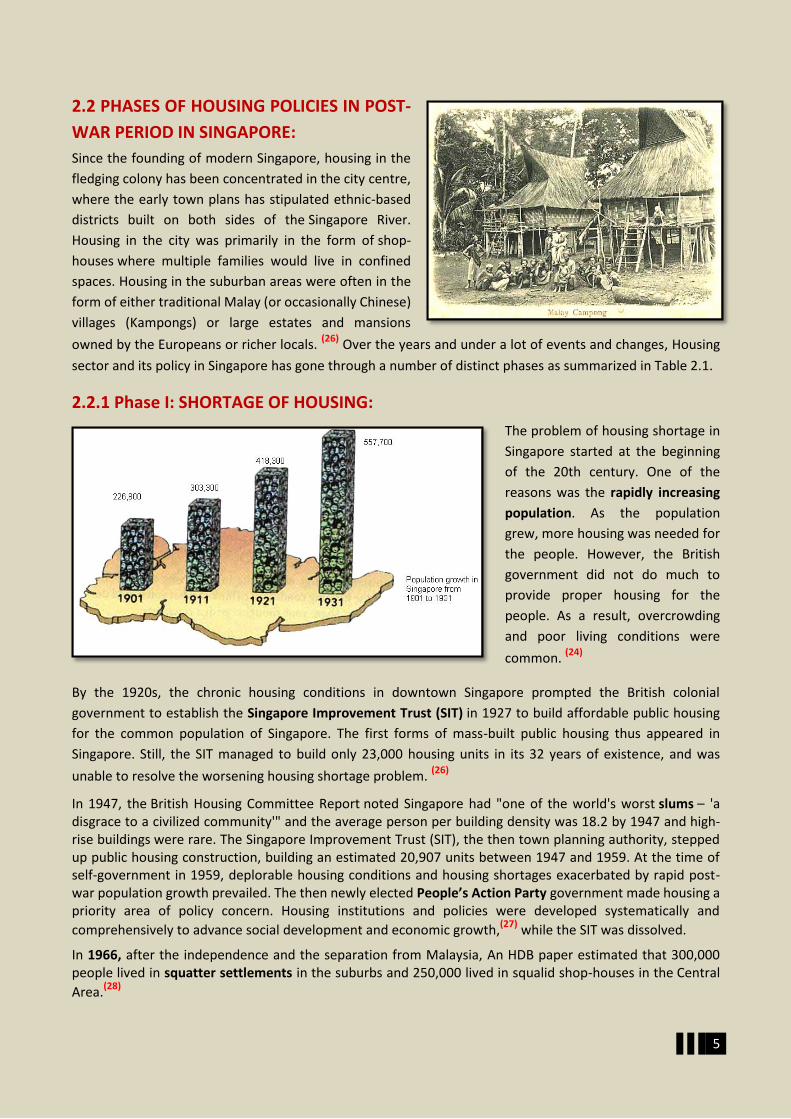

Since the founding of modern Singapore, housing in the

fledging colony has been concentrated in the city centre,

where the early town plans has stipulated ethnic-based

districts built on both sides of the Singapore River.

Housing in the city was primarily in the form of shop-

houses where multiple families would live in confined

spaces. Housing in the suburban areas were often in the

form of either traditional Malay (or occasionally Chinese)

villages (Kampongs) or large estates and mansions

owned by the Europeans or richer locals. (26)

Over the years and under a lot of events and changes, Housing

sector and its policy in Singapore has gone through a number of distinct phases as summarized in Table 2.1.

2.2.1 Phase I: SHORTAGE OF HOUSING:

The problem of housing shortage in

Singapore started at the beginning

of the 20th century. One of the

reasons was the rapidly increasing

population. As the population

grew, more housing was needed for

the people. However, the British

government did not do much to

provide proper housing for the

people. As a result, overcrowding

and poor living conditions were

common. (24)

By the 1920s, the chronic housing conditions in downtown Singapore prompted the British colonial

government to establish the Singapore Improvement Trust (SIT) in 1927 to build affordable public housing

for the common population of Singapore. The first forms of mass-built public housing thus appeared in

Singapore. Still, the SIT managed to build only 23,000 housing units in its 32 years of existence, and was

unable to resolve the worsening housing shortage problem. (26)

In 1947, the British Housing Committee Report noted Singapore had "one of the world's worst slums – 'a disgrace to a civilized community'" and the average person per building density was 18.2 by 1947 and high-rise buildings were rare. The Singapore Improvement Trust (SIT), the then town planning authority, stepped up public housing construction, building an estimated 20,907 units between 1947 and 1959. At the time of self-government in 1959, deplorable housing conditions and housing shortages exacerbated by rapid post-war population growth prevailed. The then newly elected People’s Action Party government made housing a priority area of policy concern. Housing institutions and policies were developed systematically and

comprehensively to advance social development and economic growth,(27) while the SIT was dissolved.

In 1966, after the independence and the separation from Malaysia, An HDB paper estimated that 300,000 people lived in squatter settlements in the suburbs and 250,000 lived in squalid shop-houses in the Central

Area.(28)

6

Table 2.1 Phases of housing policy in the post-war period (27)

Year Housing Development

Phase What happened? Why?

1947 Rent control at 1939 rents To protect tenants at a time of severe housing shortages

I. Developing housing

policies and institutions

to cope with building

shortages

1955 Central Provident Fund (CPF) To provide social security for the working population

1959 Self Governing Colony

1960 Housing & Development Board (HDB)

To provide housing for all those who needed them

1963 Merger with Malaysia

1964 HDB’s Home ownership Scheme (HOS)

To enable the lower income group to own their own homes

1965 Independence: Separation from Malaysia

1966 Land Acquisition Act To Facilitate land acquisition by the state

1968 CPF Approved Housing Scheme

To allow CPF savings to be used to support the HDB’s HOS

1971 Resale market for HOS To allow owners of HOS flats to exit the sector

1979 Easing of restrictions on resale of HOS flats

To facilitate upgrading to a second new HDB flat as well as residential mobility within the sector

II. Deregulation as shortage

eased

1981 CPF Approved Residential Properties Scheme

To allow CPF savings to be used for private housing mortgage payments

1985 First economic recession since independence

1988 Phasing out of rent control To facilitate private sector participation in the conservation of historical areas.

1989 Citizenship requirement and income ceilings for resale flats lifted.

To allow permanent residents access to resale HOS flats. To facilitate residential mobility.

1993 More housing loans for HDB resale flats

To bring HDB housing loans policy for resale flats closer to market practices

III. Financial Liberalization and housing

price inflation

1994 CPF housing grants To facilitate demand side housing subsidies for resale HOS flats

1995 Executive Condominiums To provide private housing at affordable prices to the upper-middle income group.

1996 Anti-speculation measures To curb speculative activities and rapid rise in housing prices.

1997 Asian financial crisis

IV. Excess housing

stock

2002 Caps of CPF withdrawals for housing

To reduce risk of over concentration of household assets in housing.

2003 HDB downsizes In view of fall in demand for new flats and 17500 unsold HDB flats in 2002.

7

2.2.1.1 THE HOUSING AND DEVELOPMENT BOARD (1960):

The Housing and Development Board (HDB) was established in February 1960, replacing the SIT, to provide

`decent homes equipped with modern amenities for all those who needed them’ and to develop public

housing and improve the quality of living environment for its residents. Led by Lim Kim San, its first priority

during formation was to build as many low-cost housing units as possible, and the Five-Year Building

Programme (from 1960 to 1965) was introduced. The housing that was initially built was mostly meant for

rental by the low income group. (26)

A target of 110,000 dwelling units was set for 1960 to 1970. From 1964, the HDB began offering housing

units for sale at below market prices, on 99-year leasehold basis, under its Home Ownership Scheme (HOS).

The HDB was able to price its units below market prices mainly because HDB flats are built on state owned

land, much of which had been compulsorily acquired from private landowners at below market prices. (29)

This was made possible by the Land Acquisition Act (LAA), enacted in 1966, which abolished eminent

domain provisions. (27)

The political and economic motivations for the HOS are perhaps best understood in the words of the then Prime Minister, Mr Lee Kuan Yew: My primary preoccupation was to give every citizen a stake in the country and its future. I wanted a home-owning society. I had seen the contrast between the blocks of low-cost rental flats, badly misused and poorly maintained, and those of house-proud owners, and was convinced that if every family owned its home, the country would be more stable. I had seen how voters in capital cities always tended to vote against the government of the day and was determined that our householders should become homeowners; otherwise we would not have political stability. My other important motive was to give all parents whose sons would have to do national service a stake in the Singapore their sons had to defend. If the soldier’s family did not own their home, he would soon conclude he would be fighting to protect the properties of the wealthy. I believed this sense of ownership was vital for our new society which

had no deep roots in a common historical experience. (30) Policies were introduced to achieve the goal of a home-owning society. There was a rapid increase in the HDB housing stock: from 120,138 units in 1970 to 846,649 units in 2000. The homeownership rate for the resident population increased from 29 % in 1970 to 92 % by 2000. Singapore’s large public housing sector is therefore in ownership terms, a largely privatized sector. However, ownership tenure of a HDB dwelling differs in many aspects from ownership of a private dwelling. Ownership rights are limited by numerous regulations concerning eligibility conditions for purchase, resale, subletting and housing loans.

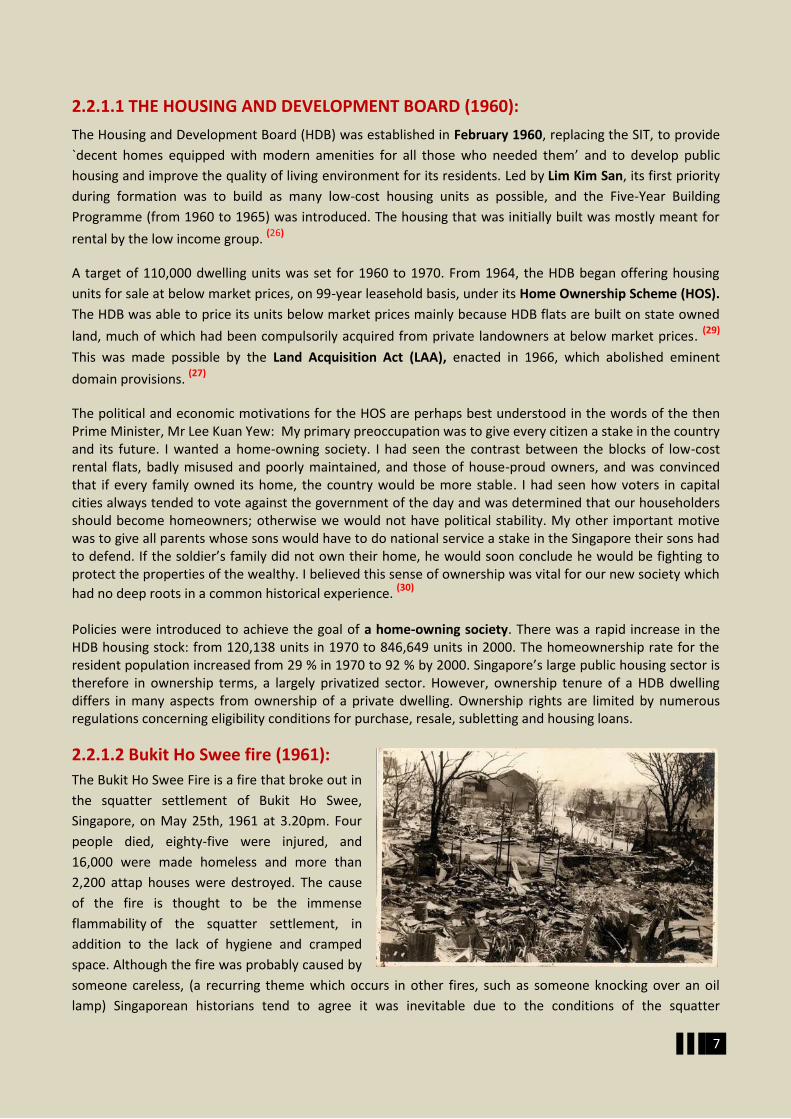

2.2.1.2 Bukit Ho Swee fire (1961):

The Bukit Ho Swee Fire is a fire that broke out in

the squatter settlement of Bukit Ho Swee,

Singapore, on May 25th, 1961 at 3.20pm. Four

people died, eighty-five were injured, and

16,000 were made homeless and more than

2,200 attap houses were destroyed. The cause

of the fire is thought to be the immense

flammability of the squatter settlement, in

addition to the lack of hygiene and cramped

space. Although the fire was probably caused by

someone careless, (a recurring theme which occurs in other fires, such as someone knocking over an oil

lamp) Singaporean historians tend to agree it was inevitable due to the conditions of the squatter

8

settlement. The fire itself tended to be part of the citation in many arguments afterwards by the People's

Action Party, who wished to relocate the squatters to more permanent, sanitary and humane housing, in

addition to reducing social unrest. The government acquired the razed land and began reconstruction

immediately after the fire to house the homeless. The Housing and Development Board (HDB) quickly

resettled the victims of the fire to newly built flats in Queenstown and St. Michael areas. In February 1962,

five blocks of flats were completed and many families moved back to Bukit Ho Swee. (24)

2.2.1.3 Government Land Acquisition (1966):

The most striking feature of the land system in Singapore is the prevalence of government landholding and

the leasehold as a method of landholding. (31) (29) More than 90% of the land in Singapore belongs to the state and much of real estate in Singapore is therefore built on the land leased from the state. Land scarcity in Singapore has been used to justify the extensive state land ownership and the need for judicious allocation of scarce land resource by the land use planner among various competing uses. In 1966, the government enacted the Land Acquisition Act (LAA) which permitted the state and its agencies to acquire land for any public purpose or for any work which is of public benefit, of public utility or of the public interest; or for any residential, commercial, or industrial purposes. Thus, the Government was and is still empowered to acquire sufficient land from private land owners to develop new public housing flats.

A 1973 amendment set payments independent of market conditions and the landowner’s purchase price. Between 1973 and 1987, the compensation for the acquired land was assessed at the market value as of Nov 30, 1973, or the date of gazette notification whichever was lower. The existence of rent control further depressed land values for affected properties. Government land acquisition at below market values in the 1970s greatly facilitated the industrialization and housing programs. State ownership of the land grew from 44% in 1960 to 76% by 1985. This dramatic increase was achieved through land acquisition, land reclamation and the transfer of the British military land.

Subsidiary legislation in the form of State Land Rules 1968 stated that titles for state-owned land should be

for terms not exceeding 99 years. Through the LAA, the government cleared low density housing, slums,

villages and squatter areas, and assembled land parcels. State land was leased to government agencies for

the development of ‘public’ housing which were sold on a 99 year leasehold basis to eligible households as

well as the development of industrial estates. Subsequent amendments to the Act from 1987 changed the

statutory date used for pegging compensation which is currently at market rates.

Public land leasing generally goes under the term Government Land Sales (GLS) in Singapore. Much urban

redevelopment in Singapore has been achieved through the GLS program administered mainly by the Urban

Redevelopment Authority with the HDB at a smaller extent. Under the program, the government

amalgamates land, inserts infrastructure, provides planning and urban design guidelines, and releases the

land for sale to private (including foreign) developers. Sites are usually sold on 99-year leases for

commercial, hotel and private residential development whereas leases for industrial sites are usually for 60

years or less. The lease tenure for other types of sites varies depending on the uses. The usual sale method is

through public tender. (32)

2.2.1.4 The Central Provident Fund (1968):

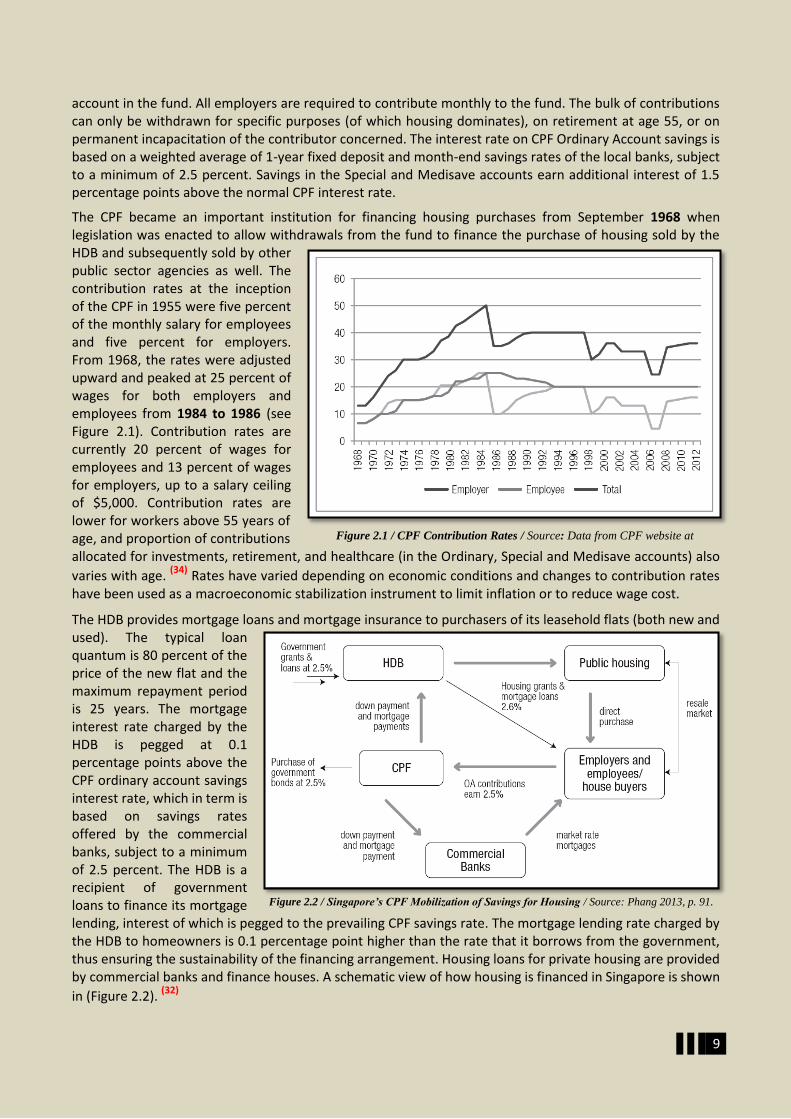

While HDB and related construction finance and land policy brought about a transformation of the housing supply side, demand for homeownership was `created’ by directing savings in the Central Provident Fund

(CPF) towards housing.(33) The CPF had been in existence before the HDB, having been established as a pension plan in 1955 by the colonial government to provide social security for the working population in Singapore. The scheme required contributions by both employers and employees, respectively, of a certain percentage of the individual employee’s monthly salary toward the employee’s personal and portable

9

account in the fund. All employers are required to contribute monthly to the fund. The bulk of contributions can only be withdrawn for specific purposes (of which housing dominates), on retirement at age 55, or on permanent incapacitation of the contributor concerned. The interest rate on CPF Ordinary Account savings is based on a weighted average of 1-year fixed deposit and month-end savings rates of the local banks, subject to a minimum of 2.5 percent. Savings in the Special and Medisave accounts earn additional interest of 1.5 percentage points above the normal CPF interest rate.

The CPF became an important institution for financing housing purchases from September 1968 when legislation was enacted to allow withdrawals from the fund to finance the purchase of housing sold by the HDB and subsequently sold by other public sector agencies as well. The contribution rates at the inception of the CPF in 1955 were five percent of the monthly salary for employees and five percent for employers. From 1968, the rates were adjusted upward and peaked at 25 percent of wages for both employers and employees from 1984 to 1986 (see Figure 2.1). Contribution rates are currently 20 percent of wages for employees and 13 percent of wages for employers, up to a salary ceiling of $5,000. Contribution rates are lower for workers above 55 years of age, and proportion of contributions allocated for investments, retirement, and healthcare (in the Ordinary, Special and Medisave accounts) also

varies with age. (34)

Rates have varied depending on economic conditions and changes to contribution rates have been used as a macroeconomic stabilization instrument to limit inflation or to reduce wage cost.

The HDB provides mortgage loans and mortgage insurance to purchasers of its leasehold flats (both new and used). The typical loan quantum is 80 percent of the price of the new flat and the maximum repayment period is 25 years. The mortgage interest rate charged by the HDB is pegged at 0.1 percentage points above the CPF ordinary account savings interest rate, which in term is based on savings rates offered by the commercial banks, subject to a minimum of 2.5 percent. The HDB is a recipient of government loans to finance its mortgage lending, interest of which is pegged to the prevailing CPF savings rate. The mortgage lending rate charged by the HDB to homeowners is 0.1 percentage point higher than the rate that it borrows from the government, thus ensuring the sustainability of the financing arrangement. Housing loans for private housing are provided by commercial banks and finance houses. A schematic view of how housing is financed in Singapore is shown

in (Figure 2.2). (32)

Figure 2.1 / CPF Contribution Rates / Source: Data from CPF website at

www.cpf.gov.sg.

Figure 2.2 / Singapore’s CPF Mobilization of Savings for Housing / Source: Phang 2013, p. 91.

10

2.2.2 PHASE II (1979 - EARLY 1990s): RESALE MARKET DEREGULATION:

The desirability of any asset is determined to a large extent by its liquidity. Ease of trade determines the efficiency of a market. The promotion of ownership of subsidized new HDB dwellings therefore had to be accompanied by policies concerning the secondary market for that housing. However, from the perspective of public policy, there was early concern that given the then general housing shortage, HDB dwellings should not become a vehicle for speculation by allowing the price subsidies to be capitalized on a secondary market. Resale regulations were therefore extremely onerous in the early days of the housing program. These regulations were eased as the housing stock increased over time and the housing market became more

mature. (31)

Prior to 1971, there was no resale market for owner-occupied HDB dwellings. HDB required owners who wished to sell their flats to return them to the HDB at the original purchase price plus the depreciated cost of improvements. In 1971, a resale market was created when the HDB allowed owners who had resided in their flats for a minimum of three years to sell their flats at market prices to buyers of their choice who satisfied the HDB eligibility requirements for homeownership. However, these households were debarred from applying for public housing for a year. The debarment period was increased to two and a half years in 1975. The minimum occupancy period before resale was increased to five years in 1973 and has remained in place since.

The debarment period, a great deterrent for any household considering sale of its dwelling, was abolished in 1979 thereby greatly facilitating exchanges within the public housing sector. This was replaced by a five percent levy on the transacted price of the dwelling to `reduce windfall profits’. A system of graded resale levy based on flat type was introduced in 1982, and rules regarding circumstances under which levies could

be waived were fine-tuned in the 1980s. (31) The resale levy system ensures that the subsidy on the second new flat purchased by the household from the HDB is smaller than that for the first flat.

Between 1968 and 1981, CPF savings could only be withdrawn for purposes of down payment, stamp duties, mortgage, and interest payments incurred for the purchase of public-sector-built housing. In 1981, the scheme was extended to allow for withdrawals for mortgage payments for the purchase of private housing. From 1984, rules governing the use of CPF savings have been gradually liberalized to allow for withdrawals

for medical and education expenses, insurance, and investments in various financial assets. (34)

Only citizens, non-owners of any other residential property, households with a minimum size of two persons with household incomes below the income ceiling set by the HDB were eligible to purchase new or resale HDB flats prior to 1989. In 1989, residential mobility was enhanced when the income ceiling restriction was removed for HDB resale flats; the resale market was opened to permanent residents as well as private property owners who had to owner-occupy their HDB flat. HDB flat-owners who could not own any other residential property before, could also invest in private sector built dwellings. From 1991, single citizens above the age of 35 have been allowed to purchase HDB resale flats for owner-occupancy.

2.2.2.1 HDB Upgrading and Selective En-bloc Redevelopment Schemes:

By the late 1980s, the age gradient for HDB estates became evident. Older estates had been built closer to the CBD and new towns were built at distances further away from the CBD. was Also, the trend was that younger families moved out of older HDB towns as they were allocated new flats in outlying new towns. In 1989, the government announced an ambitious long term HDB Upgrading Programme to upgrade existing HDB estates. The upgrading programs varied in their nature and scale (see Table 2.2) and were subsidized by

roughly between 53 to 93 percent by the government depending on the type of flat. (35) The Chok Tong government also launched the Selective En bloc Redevelopment Scheme (SERS) in 1995 under which older low density blocks of HDB flats had to be demolished and occupants had to be moved to brand new and high density developments within the same estate.

11

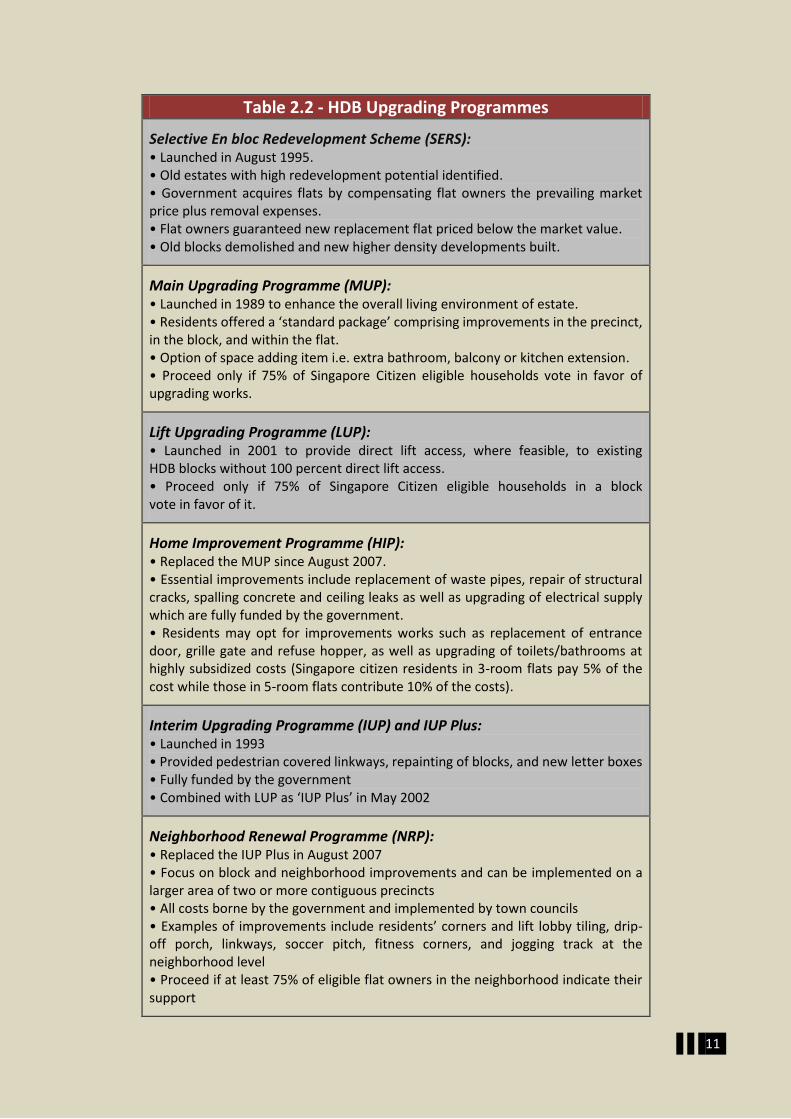

Table 2.2 - HDB Upgrading Programmes

Selective En bloc Redevelopment Scheme (SERS): • Launched in August 1995. • Old estates with high redevelopment potential identified. • Government acquires flats by compensating flat owners the prevailing market price plus removal expenses. • Flat owners guaranteed new replacement flat priced below the market value. • Old blocks demolished and new higher density developments built.

Main Upgrading Programme (MUP): • Launched in 1989 to enhance the overall living environment of estate. • Residents offered a ‘standard package’ comprising improvements in the precinct, in the block, and within the flat. • Option of space adding item i.e. extra bathroom, balcony or kitchen extension. • Proceed only if 75% of Singapore Citizen eligible households vote in favor of upgrading works.

Lift Upgrading Programme (LUP): • Launched in 2001 to provide direct lift access, where feasible, to existing HDB blocks without 100 percent direct lift access. • Proceed only if 75% of Singapore Citizen eligible households in a block vote in favor of it.

Home Improvement Programme (HIP): • Replaced the MUP since August 2007. • Essential improvements include replacement of waste pipes, repair of structural cracks, spalling concrete and ceiling leaks as well as upgrading of electrical supply which are fully funded by the government. • Residents may opt for improvements works such as replacement of entrance door, grille gate and refuse hopper, as well as upgrading of toilets/bathrooms at highly subsidized costs (Singapore citizen residents in 3-room flats pay 5% of the cost while those in 5-room flats contribute 10% of the costs).

Interim Upgrading Programme (IUP) and IUP Plus: • Launched in 1993 • Provided pedestrian covered linkways, repainting of blocks, and new letter boxes • Fully funded by the government • Combined with LUP as ‘IUP Plus’ in May 2002

Neighborhood Renewal Programme (NRP): • Replaced the IUP Plus in August 2007 • Focus on block and neighborhood improvements and can be implemented on a larger area of two or more contiguous precincts • All costs borne by the government and implemented by town councils • Examples of improvements include residents’ corners and lift lobby tiling, drip-off porch, linkways, soccer pitch, fitness corners, and jogging track at the neighborhood level • Proceed if at least 75% of eligible flat owners in the neighborhood indicate their support

12

2.2.3 PHASE III (EARLY 1990s – 1997): FINANCIAL LIBERALIZATION AND HOUSING PRICE INFLATION:

The HDB also provides loans to buyers of resale HDB flats. Loan financing prior to 1993 was based on 80 percent of 1984 HDB new flat (posted) prices. As both new and resale prices rose, households purchasing resale flats had to pay an increasing larger proportion of the price in cash. In 1993 HDB moved its mortgage financing terms closer to market practice by granting loan financing of up to 80 percent of current valuation or the declared resale price of the flat, whichever is lower. In 1993, the CPF Board also began to allow withdrawals of CPF savings to be used to meet interest payments on mortgage loans for resale HDB and private housing purchases. Before this, CPF members were allowed to withdraw only up to 100 percent of the value of these properties at the time of purchase.

Deregulation of the HDB resale market has been accompanied by an increase in the number of transactions. The transaction volume of resale HDB flats increased from fewer than 800 units in 1979, to 13000 units in 1987, 60000 units in 1999, and 31000 in 2004 (HDB Annual Reports). Resale transactions as a proportion of total (new and resale) owner occupied public housing transactions, were three percent, 37 percent, 64 percent and 68 percent in 1979, 1987, 1999, and 2004 respectively. The increase in the demand for resale

flats in the latter half of the 1990s is in part due to the introduction of demand side housing grants.(27)

2.2.3.1 CPD HOUSING GRANTS:

In 1994, demand-side subsidies in the form of CPF housing grants for the purchase of resale HDB flats were introduced. This represents a shift from total reliance on subsidies tied to new flats to a system of partial reliance on subsidies tied to resale flats. The subsidy is deposited into the CPF account of the eligible household when it applies to purchase a resale HDB flat. Under the scheme, the government provides the first time applicant household with a grant of $30000 to purchase a HDB resale flat close to either parents' or married child's residence. In 1995, the grant was increased to $50000. The government also introduced a more general grant of $40 000 for eligible households that purchase a resale flat which does not need to satisfy the criterion of being close to parents/married child's residence.

The shift towards constrained housing grants for the purchase of housing on the secondary market was necessary for the following reasons. In the first three decades of the HDB’s existence, annual supply of new public housing added substantially to the housing stock particularly in the early 1980s. It was a rapid rate that was consistent with high income and population growth combined with a situation of grave housing shortage. The supply policies of the HDB that were suitable under the above circumstances had to be

reviewed as population growth stabilized and as basic housing needs were generally met. (32)

In cities of developed countries, new construction of housing is a small percentage of existing stock and comprises mostly high quality housing. Even as the construction of the basic 1 to 3-room HDB flats have been phased out, the construction of 4-room HDB flats may eventually meet with the same fate. The housing board’s ongoing modernization of older estates and its selective en-bloc redevelopment scheme (under which old apartment blocks are repurchased, demolished, and new estates built) will be even more important then. Owner-occupier subsidies (which almost all new households and a large proportion of existing households have come to expect as a right of citizenship) will, as a matter of economic efficiency if not political efficacy, has to be increasingly in the form housing grants for the purchase of existing housing

rather than subsidized prices for the purchase of a new unit. (27)

2.2.3.2 HOUSING BUBBLE, THE EC SCHEME AND THE ASIAN FINANCIAL CRISIS:

Financial liberalization as well as positive macroeconomic factors resulted in rapidly rising housing prices in the early 1990s (see Figure 2.3). With the growing concern over the affordability of private housing, the government introduced the Executive Condominium (EC) scheme, a hybrid public-private house type in 1995. The EC scheme also facilitated the HDB’s withdrawal from the upper-middle-income housing market, allowing it to discontinue building Executive Flats. Its similarity with 99-year leasehold private condominium

13

house type enabled the government to affect private housing prices with another instrument on the supply side. The government auctioned the land off for the development of EC units to housing developers (private as well as government-linked companies) who are responsible for design, construction, pricing, arrangements for financing and estate management. Applicant households had to satisfy eligibility conditions and abided by regulations on these units.

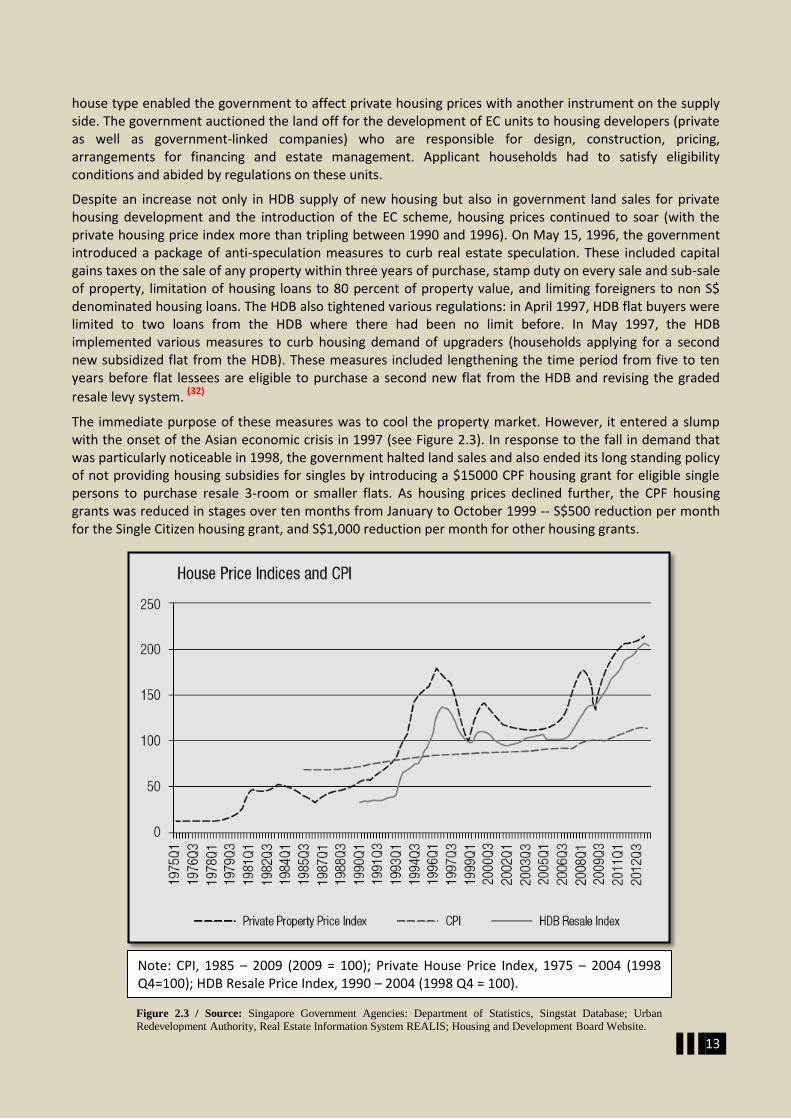

Despite an increase not only in HDB supply of new housing but also in government land sales for private housing development and the introduction of the EC scheme, housing prices continued to soar (with the private housing price index more than tripling between 1990 and 1996). On May 15, 1996, the government introduced a package of anti-speculation measures to curb real estate speculation. These included capital gains taxes on the sale of any property within three years of purchase, stamp duty on every sale and sub-sale of property, limitation of housing loans to 80 percent of property value, and limiting foreigners to non S$ denominated housing loans. The HDB also tightened various regulations: in April 1997, HDB flat buyers were limited to two loans from the HDB where there had been no limit before. In May 1997, the HDB implemented various measures to curb housing demand of upgraders (households applying for a second new subsidized flat from the HDB). These measures included lengthening the time period from five to ten years before flat lessees are eligible to purchase a second new flat from the HDB and revising the graded

resale levy system. (32)

The immediate purpose of these measures was to cool the property market. However, it entered a slump with the onset of the Asian economic crisis in 1997 (see Figure 2.3). In response to the fall in demand that was particularly noticeable in 1998, the government halted land sales and also ended its long standing policy of not providing housing subsidies for singles by introducing a $15000 CPF housing grant for eligible single persons to purchase resale 3-room or smaller flats. As housing prices declined further, the CPF housing grants was reduced in stages over ten months from January to October 1999 -- S$500 reduction per month for the Single Citizen housing grant, and S$1,000 reduction per month for other housing grants.

Note: CPI, 1985 – 2009 (2009 = 100); Private House Price Index, 1975 – 2004 (1998 Q4=100); HDB Resale Price Index, 1990 – 2004 (1998 Q4 = 100).

Figure 2.3 / Source: Singapore Government Agencies: Department of Statistics, Singstat Database; Urban

Redevelopment Authority, Real Estate Information System REALIS; Housing and Development Board Website.

14

2.2.4 PHASE IV (1998 - PRESENT): EXCESS HOUSING STOCK:

In response to the fall in demand for housing during the Asian crisis, that was particularly pronounced in 1998, the government halted land sales and also ended its long standing policy of not providing housing subsidies for singles by introducing a $15000 CPF housing grant for eligible single persons to purchase resale 3-room or smaller flats. As housing prices declined further, the CPF housing grants was reduced in stages over ten months from January to October 1999 -- $500 per month for the Single Citizen housing grant, and $1,000 per month for the other housing grants. (In FY 2003/2004, 7,260 households purchased a resale flat under the CPF housing grant scheme.)

Both the private and public housing sectors were faced with a situation of declining prices and unsold units. A study in 2001 estimated unsold housing stock of about 19,800 units for the private sector (Monetary Authority of Singapore, 2001). With more than 17,500 unsold new flats in early 2002, the HDB suspended its Registration for Flat or queuing system, diverting remaining and new applicants to its Built-To-Order programme under which flats are built only when there is sufficient demand for them. In July 2003, in a major restructuring exercise, the HDB’s 3000 strong Building and Development Division6 was re-organized and the HDB Corporation Private Limited (HDB Corp) set up as a fully-owned subsidiary of HDB. In November 2004, HDB divested its 100 percent shareholding in HDB Corp to the government’s investment holding company, Temasek Holdings. HDB Corp has been assigned responsibility for the design and development of all HDB projects until June 2006. The subsidiaries of HDB Corp now include the Surbana group of companies which have also ventured into housing development projects overseas.

The HDB provides loans to purchasers of both new and resale flats, with the CPF having first claim on a property if a borrower defaults on his loan, thus protecting the CPF savings of the purchaser. Interest rate is at the CPF savings rate plus 0.1 percentage points. The recent low interest rate environment has however given rise to the anomaly where interest rates for commercial bank housing loans have been lower than HDB’s `subsidized’ loans (as there is a 2.5 percent floor on the CPF ordinary account savings rate). From September 2002, commercial banks have been given the go-ahead to compete for a slice of the $63 billion HDB loans market pie. However, as is the case for private housing, banks instead of the CPF would be given

first claim for such housing loans. (27)

15

Despite its relatively small land and unpromising outlook as a nation, Singapore progressed from a third world status in the 1960s to one of the highest income countries in the world today. Singapore has achieved a great and remarkable success in the housing sector; its successful development has been thanks to far-sighted and careful management of the economy by the government as well as well established policies. Singapore’s housing policy is built on certain implied principles, and geared towards achieving well-defined social goals and stability. This section discusses these principles and efforts towards achieving them.

3.1 Developing Vibrant Towns:

(a) Comprehensive Town Planning: Through the decades, the physical planning of HDB towns has evolved in tandem with the changing socio-economic and demographics of Singaporeans. To ensure sustainability of HDB towns, they have developed the Comprehensive Town Planning Principles that help address the constraints they face, and fulfill their

vision. These principles are: (36)

- Planning for Self-Sufficiency Towns are planned and developed as a total living environment for people to work, live, play and learn. Facilities such as schools, shops and markets, polyclinics as well as recreational facilities such as sport complexes, and parks are planned for. To meet social needs, community centers, and places of worship are provided. Employment opportunities are found in commercial centers that are well-distributed in the town, as well as in industrial parks, which are located at the periphery of the town.

- Neighbourhood Concept From 1960s to mid 1990s, towns were planned with neighborhoods of around 4,000 to 6,000 dwelling units. Each Neighbourhood is served by a neighbourhood centre which is its commercial hub, and a whole range of facilities such as schools, community centers, social and institutional centers and recreational areas. Several neighborhoods would be located around the Town Centre which is usually in the geographical centre of the town. This is where the main transport hub is located together with key commercial, entertainment and social facilities.

- Concept of Hierarchy To provide a sense of structure and order within the town, HDB has adopted the concept of hierarchy in the planning of towns. Several neighborhoods make up a town, each neighbourhood in turn comprises of smaller precincts of around 400 to 800 dwelling units each, allowing for a better sense of identity with place and neighbours in order to foster sense of ownership and pride. The smaller precincts are more conducive for social interaction. Commercial facilities are also planned on a hierarchy system where the town centre is the main commercial, transport, activity hub for the town. On a smaller scale are the neighbourhood centers with neighbourhood shops and marketing facilities, while smaller clusters of precinct hops serve local needs.

- Planning for Connectivity The transportation network for the new town is a critical element in the town as it is planned from the outset together with land use. The network of roads and rail connects the town to the other parts of the country and ensures good circulation within the town. A hierarchical concept is also applied to road planning, where major roads that carry through-traffic do not cut through a town and interfere with its local traffic, but is located at the periphery of the town. Bus interchanges and mass rapid transit stations are located in the town centre which is the activity hub for the town. Every town is linked by an island-wide network of rapid transit lines.

03- Goals & Principles

16

- Checkerboard Concept To optimize land use because of the constraint of land scarcity, a high-rise, high density model has been adopted right from the beginning. To help reduce the sense of crowdedness, high-rise high density housing developments are interspersed with low-rise developments such as schools and parks to provide visual and spatial relief, in a checker-board pattern. With such a checkerboard concept, facilities are also brought closer to the residents.

(b) Rejuvenation/Upgrading:

HDB has existed for more than 50 years, and some of developments preceded HDB. Hence, it is necessary to continually ensure that old towns and developments do not lag behind newer towns. This is done with a regular review town development. Listening to feedback and upgrading towns and flats to meet the people’s rising aspirations. As new towns spring up, HDB ensure that the old towns do not lag behind. Rejuvenation is brought about in several ways. New facilities are added, existing ones being upgraded. Where there is an

opportunity, some areas would be re-planned and redeveloped to optimize land use. (36)

The Estate Renewal Strategy (ERS) was announced in Sep 1995 to systematically redevelop the older towns/estates and blend in new developments. It helps to bring the towns/estates to the latest standards and improve the living environment for residents. The objectives of ERS are:

- Bring Mature Estates to a standard comparable with Young Estates. - Upgrade living environment and facilities to meet rising expectations. - Retain family ties and community spirit. - Keep the town rejuvenated, vibrant and sustainable.

The current key programmes of ERS are presented in (Table 2.2) in last Section.

3.2 Providing Affordable Homes:

(a) Promoting Home Ownership in Singapore Public housing policy encourages home ownership rather than rental. Home ownership gives every citizen a stake in Singapore. Homeownership instills pride and ensures that the home and the environment is up kept and well maintained. Homeownership also fosters an industrious work force, where each person works and aspires to own his or her flat. To enable Singaporean to afford ownership of HDB flat, the Home Ownership Scheme was introduced in February 1964. In 1968, the use of compulsory savings from the Central Provident Fund (CPF) was allowed in the purchase of HDB flats. Since then, amongst 82 percent of the resident population in Singapore who live

in HDB flats, some 95% own their own flats. Some areas of assistance for people to own a HDB home are: (36)

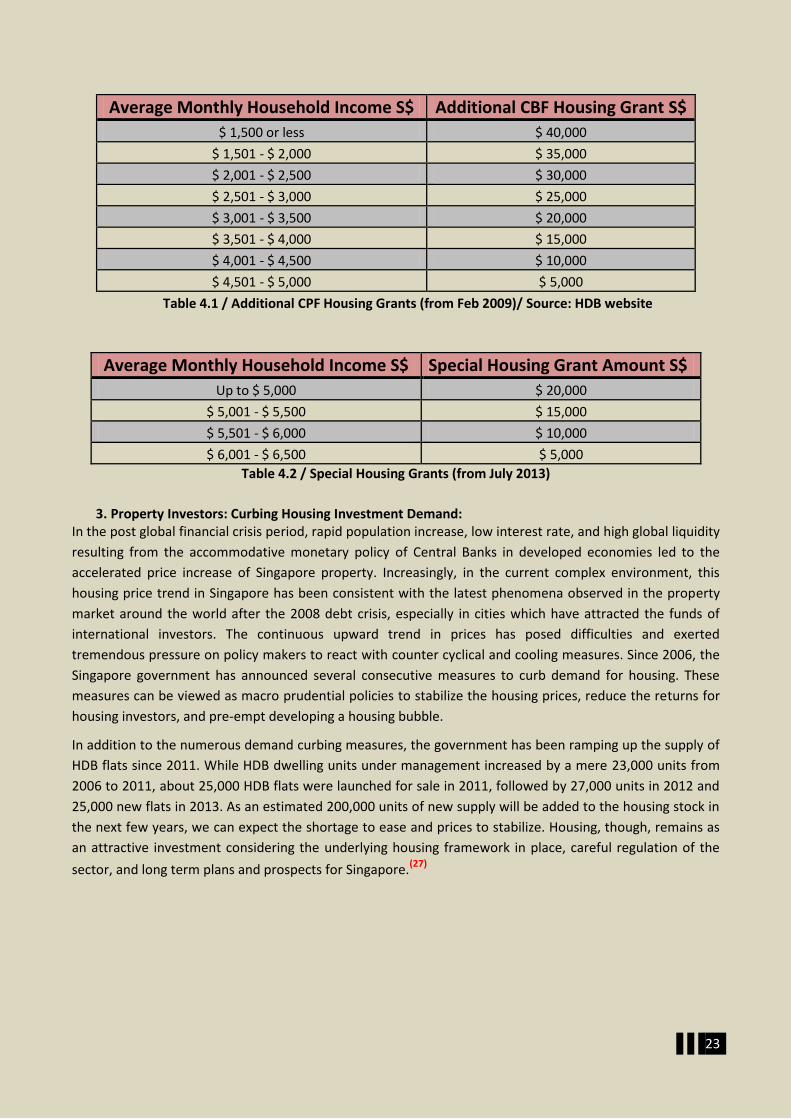

- Assisting Lower-Income Families Singapore citizen households with average gross monthly household incomes not exceeding $5,000 per month is entitled to Additional CPF Housing Grant on top of the existing housing subsidies.

- Promoting Family Ties A higher CPF Housing Grant of $40,000 is given to married eligible applicants who buy a resale flat with or near to their parents or married child. Married children will also be given additional chances in the ballot under the various HDB sales exercises if they apply for a flat to live near to together with their parents and vice versa.

- Giving Incentives to Singles Living with Parents To encourage singles to take care of their elderly parents, with effect from 1 Apr 2008, singles aged 35 years and above who buy an HDB resale flat to live together with their parents may apply for a higher CPF Housing Grant of $20,000.

17

- Providing more Options for the Elderly The Studio Apartment (SA) Scheme launched in 1998 provides another housing option for the elderly. SAs, which are sold on 30-year leases, are specially designed with elderly-friendly features and offer convenient access to amenities and facilities.

- Helping Singles Singles are able to purchase their own HDB home either on their own via the Single Singapore Citizen Scheme, or with other Singles under the Joint Singles Scheme.

(b) Wide Range of Housing Choices: Approximately 914,000 flats are spread across Singapore, with a variety of sizes to suit the income and lifestyle requirements of Singaporeans. One- and two-room rental flats cater to lower income families while four-room and bigger flats meet the needs of higher income households and extended families who want to stay together.

To meet rising aspirations, HDB has engaged private sector architects to introduce new ideas into public housing design. For instance, under the Design, Build and Sell Scheme that was launched in 2005, private sector developers bid for the land, design, construct and sell flats to eligible buyers directly. A total of 13

sites and 11 projects have since been launched in various locations across Singapore. (37)

Besides financing needs, HDB offers a wide range of options to meet the varied housing needs of

Singaporeans: (36)

- For All Pockets There are six different flat types to choose from, ranging from 1-room to 5-room flats and executive flats. Also there are offers of premium apartments, with more quality finishes that require minimum renovation. To encourage innovation in design and create better value for money for buyers, HDB invites private sector involvement to develop and sell its new housing projects under the Design, Built and Sell Scheme. To cater for the low-income families, they will receive an Additional Housing Grant to buy their first flats, over and above the existing housing subsidies. Some low-income families which cannot afford to own homes, HDB rental flats are offered to them at heavily subsidized rates.

- For Different Life Stages Recognizing the ageing population in Singapore, SAs are provided for the elderly where the homes are specially customized for older people. SAs also allow the elderly to move into smaller apartments while still remaining part of the community, close to families and friends. Alternatively, home buyers have the option of getting a flat from the secondary market, and with a housing grant if they are eligible.

- New Typologies Faced with challenges such as land scarcity in Singapore, a high-rise high density approach has been adopted for public housing in Singapore. With more housing sites being intensified, HDB is conscious of the built environment and has been putting in effort to help mitigate the sense of “crowdedness”. To keep HDB homes attractive to Singaporeans, HDB puts in effort to continuously introduce innovative ideas in tackling the land scarcity in Singapore. One such project is Central Horizon in Toa Payoh. It was the first HDB precinct that has a garden located at the mid level (12th storey) which spans across five blocks of flats over a total distance of 240m. Another such project is The Pinnacle@Duxton which HDB held its first international architectural competition for the design of public housing. Aimed at creating a housing design that is distinctive and liveable, the winning design of The Pinnacle@Duxton provided a variety of interesting communal spaces for interaction, such as skybridges and sky gardens at the 26th and 50th storeys. These communal spaces are also lookout points with panoramic views of the city.

3.3 Cohesive Communities: HDB does not just develop towns but integrated communities that people feel part of. Being a multi-cultural nation, must recognize the need for social harmony and racial integration. To ensure Singaporean communities remain cohesive, HDB consciously work towards building vibrant communities through the provision of “hardware”, “software” and “heartware”.

18

(a) Hardware Given the diverse nature of Singapore’s society, it is crucial to integrate these communities of different backgrounds. The planning and design of HDB towns, neighborhoods, precincts and blocks plays an important role in the shaping of cohesive communities, providing opportunities for social interaction within the total living environment. Our precincts are designed to incorporate varying types and sizes of flats so that households of different income and social profiles are given the opportunity to mingle and live together. A unique and defining feature of HDB flats is the void deck. The ground floor of high rise blocks of flats are intentionally kept open or “void” to allow residents to use the space for casual meeting or planned functions. Some of the space is also used for social community facilities such a child care centers, kindergartens, social welfare agencies or elderly day care centers. One such facility is the Residents’ Committees (RCs) Centre; RCs will help organize residents’ parties and other neighbourhood activities to establish good communal relations amongst the residents. Some void decks also have Senior Citizens Corners for the elderly to gather, rest and chat. These corners are equipped with facilities like toilets, wash basins, storeroom, pantry and even a television set. Flat in a precinct also share common spaces and facilities such as playgrounds, fitness corners and precinct pavilions, which help to facilitate interaction and enhance neighborliness in the community. A comprehensive range of commercial and recreational facilities such as neighbourhood markets, shops and parks are places that residents get to meet familiar faces on a daily basis. Town plazas and open spaces are located at high human traffic areas and near commercial facilities to encourage interaction among residents. Events are also held at such locations to bring the crowds together to participate in various community activities.

(b) Software HDB housing policies are also geared towards encouraging married children to live near their parents, promoting extended family living, upholding Asian family values. HDB has provided many incentives such as priority flat allocation or additional housing subsidies to multi-tier families and married children who are living together with or near to their parents for mutual care and support. Some of these policies are Joint Selection Scheme, Multi-Tier Family Housing Scheme, Married Child Priority Scheme, high income ceiling for extended and higher-tier Housing Grant. Policies like the Third Child Priority Scheme also help in encouraging Singaporeans towards family formation and having more children. As Singaporeans consist of a multi-racial community, HDB also implements the Government’s Ethnic Integration Policy (EIP) in maintaining racial harmony in public housing estates. The EIP was implemented in 1989 and is aimed to prevent the formation of racial enclaves in public housing by setting the maximum allowable proportion of each ethnic group living in each HDB neighbourhood and block. This creates a balanced mix of residents from various ethnic groups which helps to foster ties within the community, and hence promoting ethnic integration.

(c) Heartware To enhance the sense of belonging in HDB towns and instilling a stronger sense of ownership in residents, we encourage our residents to be actively involved in the management of HDB estates through Town Councils, Citizens’ Consultative Committees or Residents’ Committees. The primary role of Town councils is to maintain the common property within HDB estates. Getting the residents involved in Town Councils allows them to participate and contribute in the decision making process in the management of their estate. Residents are also encouraged to be involved in shaping the physical environment of their estate. Platforms like regular briefings to grassroots leaders, community forums and consultation exercises, and regular surveys allow residents to express their views and provide feedback on their preferences. Not only would this allow HDB standard of physical environment to meet the expectations of their residents, it helps to promote community bonding and a sense of identity as well. HDB also organizes welcome parties and key handover/completion ceremonies to welcome new residents into the community. These parties allow existing and new residents to get to know each other and also a good platform for residents to befriend each other, fostering a close-knitted community in HDB towns.

19

4.1. UNDER THE LEE KUAN YEW GOVERNMENT, 1959 - 1990:

Improvements in the urban environment and the standards of housing in Singapore during the three decades under Lee’s government showed the success of the economic development and housing strategy adopted by the Singapore government. This overwhelming success has been well documented. Land and properties in the cities and rural areas were acquired by the government. Also, squatter settlements were cleared and entire neighborhoods and villages were resettled in HDB new towns. HDB’s housing stock increased rapidly from 120,138 units in 1970 to 574,443 units in 1990, which was 87% of the resident population. The homeownership rate for the resident population increased from 29 percent in 1970 to 88 percent in 1990. Singapore’s large public housing sector is therefore in ownership terms, a largely privatized sector. However, the ownership tenure of a HDB dwelling differs from that of the private dwelling in many aspects. Ownership rights are limited by numerous regulations concerning eligibility conditions for purchase, resale, subletting and housing loans.

The housing market is highly segmented according to regulations on eligibility of households. Only citizen households are eligible for HDB rental and direct purchase (one unit per household) with current monthly gross household income caps at S$1,500 for rental and S$10,000 for direct purchase, respectively. The resale HDB sector is open to citizens and permanent residents with housing grants for purchaser households carefully calibrated according to citizenship, marital status and household income. The private housing sector caters largely to higher income Singapore citizens, permanent residents, expatriates, and foreign

investors. Foreign ownership of housing is confined to private flats and the condominium sector. (32)

That a large public housing program could deliver satisfactory housing for the majority in a relatively affluent city testifies Singapore government’s production efficiency and responsiveness to changes. This public provision of private goods on a large scale was accompanied by numerous regulations on eligibility, resale, and financing, which resulted in some consumption inefficiencies in the earlier decades. The public-private hybrid has, however, allowed the government to regulate, deregulate and re-regulate the sector with changes in socio-economic as well as market conditions.

Favorable socio-economic effects of Singapore’s housing welfare approach include the following: (38)

1. Increase in Savings Rate: At the inception of the CPF home ownership scheme in 1968, the Gross National Saving to GNP ratio was less than 20 percent, which was insufficient to fund the country’s investment needs (32 percent of GNP). The CPF contributed to a significant leap in the savings rate, 44 percent of GNP by 1990 – certainly one of the highest savings rates in the world, more than sufficient to meet the country’s investment needs.

2. Increase in Quantity and Quality of Housing Stock The housing welfare approach enabled Singapore to mobilize long term resources on the demand side. This was to finance the rapid supply of housing by the public sector with minimal involvement of government expenditure. Although it is critically described Singapore’s economic development as “a mobilization of

resources that would have done Stalin proud”,(39) in the housing sector, it was a mobilization of resources that visibly raised living standards of the entire population, transformed the housing environment of Singapore, and resulted in the creation of significant housing and real estate wealth.

3. Increase in Homeownership Rate The development of well functioning mortgage markets is often viewed as a means to achieving a higher

homeownership rate. Homeownership is promoted in many countries and various policies and institutional

arrangements provide incentives for homeownership by reducing its costs relative to renting. (40) In addition

04- Policies’ Out-Comes

20

to government provision of affordable subsidized HDB housing and HDB mortgage loans, the policy of

allowing high mandatory savings for home purchasing made homeownership the dominant option for most

Singaporean households. It is not surprising that homeownership rate for the resident population increased

from 29 percent in 1970 to 95 percent in 2011(37)

due to sustained income increases and low unemployment

rates.

4. Development of Mortgage Market Housing policies have contributed to the development of the mortgage sector in Singapore. In 1970, shortly

after the implementation of the CPF Approved Housing Scheme, outstanding housing loans were a mere

S$215 million. This constituted only 4% of the GNP. In 1990, housing loans to the GNP ratio increased to 29%

with the HDB share at 54%. (32)

5. Racial Integration The large HDB housing sector has played an extremely important role in shaping the Singapore society. Singapore is a multi-racial, multi-religious country; in 2012, the Chinese consisted of 74.2% of the resident population, the Malays 13.3%, Indians 9.2%, with other races comprising 3.3%. The physical plans of HDB new towns have been designed to integrate the various income and racial groups within the public housing program, and this has prevented the development of low-income and ethnic ghettos. The colonial administration had a policy of racial segregation in its early days of town planning. Along with the communist threat, controlling racial tensions (there were racial riots on a number of occasions) was major political challenges in the 1960s. Beginning in the 1970s, the HDB allocated new flats in a manner that would give a “good distribution of races” to different new towns. However, by 1988, a trend of ethnic regrouping through the resale market was highlighted as a housing problem which would lead to the re-emergence of ethnic enclaves. In 1989, the HDB implemented an Ethnic Integration Policy under which racial limits were set for HDB neighborhoods. When the set racial limits for a neighborhood was reached, those wishing to sell their HDB flats in the particular neighborhood had to sell it to another household of the same ethnic group. The government emphasized that “our multiracial policies must continue if we are to develop a more cohesive, better integrated society. Singapore’s racial harmony, long term stability, and even viability as a nation

depend on it”. (41)

6. Impact on Economic Distribution

The vast majority of households including low income households in Singapore have benefited from the government’s policy which gives access to ownership of affordable public housing. The active resale market allows mobility within and out of the market and the benefits of price discounts to be capitalized after a minimum occupancy period. Each household is allowed to apply for a “housing subsidy” that has been

described as “a ticket to an easier life for the HDB heartlander” twice. (42)

Due to the massive program, trade-offs were inevitable. The housing approach adopted in Singapore undoubtedly increased the savings and homeownership rates, mobilized resources for the housing sector and contributed to the increase in housing loans and the development of the primary mortgage market. However, the approach was not without its detractors. Singapore’s housing strategy was inherently policy-driven and centrally-controlled with major decisions on savings rates, savings allocation, land use, housing production, and housing prices being largely determined by the government. It was, in other words, a neo-classical economist’s nightmare. Pugh (1985), advocating Singapore’s strategy as a good model in the context of providing a set of guidelines for a good housing system, writes:

… do not be too perturbed if some orthodox (neo-classical) economists argue that housing is over-allocated

by subsidy. Show them that `subsidy’ is a concept which cannot be fitted easily to housing, and produce

counter arguments, which are respectable in economics, and which are readily available.

21

4.2 The Goh Chok Tong Government, 1990 – 2004: “Asset Enhancement”

When Mr Goh Chok Tong succeeded Mr Lee Kuan Yew as the Prime Minister in 1990, the housing shortage problem was solved. The homeownership rate increased steadily over the years and was 88% in 1990. 87% percent of the resident population was already housed by the HDB and the property-owning democracy became a reality. In the 1990s, the HDB shifted its focus on providing larger and better quality flats for existing HDB and upper-middle income households, redevelopment of old estates, and retrofitting existing flats. Upgrading households to larger flats within the HDB sector was facilitated by the development of an active secondary market and a system that allowed an eligible household to apply for a second (usually larger) subsidized flat after a minimum occupation period.

The land planning in the early 1990s shifted its focus to the one that was more visionary and that provided a larger market space for private sector developers to meet the aspirations of a growing segment of the population for more exclusive housing. This was the period when the government land sales program to private developers resulted in a marked increase in the supply of private housing. Revenue from the sale of state land leases constituted a significant proportion of government revenue, particularly during the `boom’ years of the property cycle.

Housing policies under Goh Chok Tong’s term as the Prime Minister were marked as market deregulation,

“asset enhancement” and “upgrading” policies. The Goh government viewed Singaporean homes as an

asset and potential source of security for their old age (43). Implemented policies included the deregulation

of the HDB resale market including housing loans for HDB resale flats which facilitated mobility, physical

upgrading of HDB flats and neighborhoods as well as the introduction of demand side subsidies in the form

of CPF housing grants. These policies partly contributed to the rapid escalation of housing prices in the early

half of the 1990s.

4.3 The Lee Hsien Loong Government, from 2004: “Management of Housing

Affordability in a Global City”: Mr Lee Hsien Loong became Singapore’s third Prime Minister in August 2004, having served as a Member of

Parliament since 1984 and a member of the cabinet since 1987. The housing market at the start of his term

appeared to be stabilizing at the trough of the property cycle. The HDB had been restructured and

downsized. The economy was recovering from the shock of the SARS crisis of 2003. The Asian economic crisis

of 1997 and the subsequent fall in property prices, however, had resulted in the risks of housing bubbles,

unemployment, and reliance on housing as an asset to finance retirement. A rapidly aging population and

the decline in total fertility rate over the years posed a major demographic challenge. Policy attention

shifted to elderly households that could monetize their housing asset, better targeting of housing grants to

benefit lower income households, and regulation of the housing market and housing loans.

In 2005, the government made a decision to proceed with the development of two casino based integrated

resorts –until then, casinos were not allowed in Singapore. This decision could be said to mark another

phase in the economic development of Singapore as a global city. On the population front, immigration and

foreign worker policies led to a rapid growth in the number of foreigners in Singapore. However, the global

financial crisis of 2008-2009 and the uncertainties it brought about made the government hold off

increasing housing supply which subsequently led to a housing shortage in 2010 – the year when the two

integrated resorts opened and the economy rebounded sharply (with real GDP growth of 14.8%).

Housing price increases in excess of median income growth, younger generation’s inability to afford housing, rising income inequality, and over-crowded public transportation and other facilities contributed to a decline in support for the People’s Action Party (PAP). The share of the PAP’s vote declined from 66.6% at the 2006

22

election to 60.1% at the 2011 election, with the opposition Workers’ Party winning 6 of the 87 seats for elected Members of Parliament (only 2 seats were won by opposition parties in the 2006 election).

This section considers the policies implemented by Lee Hsien Loong’s government to address the housing

problems of elderly and lower income households as well as to curb the investment demand for housing,

aimed at controlling housing price increases.

1. Elderly Households: Monetizing Housing Assets:

A typical household in Singapore has invested a large portion of its wealth in housing. (44)

showed through simulations that the average worker in Singapore is likely to be “asset-rich and cash-poor” with 75 percent of his retirement wealth in housing asset upon retirement, under the condition that housing values continue to rise in real terms. In contrast, an American elderly household would have only 20 percent of their retirement wealth in housing asset. This raises the problematic issue of over concentration of household assets in housing which results in a risky under-diversified portfolio at retirement.

Economic Review Committee appointed by the government in 2002 arrived at a similar conclusion that CPF

members were “asset rich and cash-poor” and made recommendations to limit CPF withdrawals for housing

in a report. It also suggested that the government should explore ways to monetize their property for

homeowners. Agreeing with the committee’s recommendations, the government moved to cap CPF

withdrawals for housing at 150 percent of the value of the property with the cap moving down gradually to

120 percent over five years for new private housing loans.

To address the problem of “asset rich and cash poor” faced by the old, the HDB introduced the Lease Buyback Scheme (LBS) in 2009 to allow the low income elderly (age 63 or older) living in 3-room or smaller flats to unlock the equity in their homes. The proceeds of the part sale will be used to top up their CPF Retirement Accounts and to purchase an annuity plan that will provide a monthly income for life. The amount of monthly income would be determined by the market value of the flat, the length of the remaining lease, the amount of outstanding loan on the flat, and the age and the gender of the elderly owner(s). Under this scheme, the HDB will buy back the tail lease of the flat with the elderly flat owner retaining a 30 year lease, and provide a bonus (up to S$20,000) with the unlocked housing equity. The LBS thus allows the elderly to continue to stay in their flat.