Embed Size (px)

Citation preview

US Liquid Handling Market Strategies to Drive Growth in an Increasingly Competitive Market

NE41-52

December 2014

2NE41-52

Section Slide Number

Methodology 6

Executive Summary 7

• Key Findings 8

• Scope and Segmentation 9

• Key Questions This Study Will Answer 10

• Market Engineering Measurements 11

• CEO’s Perspective 12

• Key Companies to Watch 13

• Executive Summary—3 Big Predictions 14

Market Overview and Segmentation 15

• Market Background 16

• Market Segmentation 17

• Market Overview 19

• Defining Healthcare Trends in the Future 20

Competitive Playbook 21

Contents

3NE41-52

Section Slide Number

• New Market Opportunities 22

• Merger and Acquisition Assessment 25

Drivers, Restraints, and Trends—Total Liquid Handling Market 26

• Market Drivers 27

• Market Restraints 28

• Market Impact of Top Trends 29

Forecasts and Trends—Total Liquid Handling Market 30

• Market Engineering Measurements 31

• Forecast Assumptions 32

• Revenue Forecast 33

• Revenue Forecast by Segment 34

• Percent Revenue Forecast by Segment 36

• Revenue Forecast Discussion 37

• Procurement Process 39

• Segment Lifecycle Analysis 40

Contents (continued)

4NE41-52

Section Slide Number

Competitive Environment 41

• Competitive Structure 42

• Recent Major Product Launches 43

• Top Competitors 45

• Competitive Assessment 47

Automated Robotic Workstations Market Analysis 48

• Automated Robotic Workstations Market Key Findings 49

• Market Engineering Measurements 50

• Revenue Forecast 51

• Revenue Forecast Discussion 52

• Competitive Tier Analysis 54

Low-to-Mid Throughput Automated Liquid Handling Tools Market Analysis 55

• Low-to-Mid Throughput Automated Liquid Handling Tools Market Key Findings 56

• Market Engineering Measurements 57

• Revenue Forecast 58

Contents (continued)

5NE41-52

Section Slide Number

• Revenue Forecast Discussion 59

• Competitive Tier Analysis 61

Manual Pipettes and Consumables Market Analysis 62

• Manual Pipettes and Consumables Market Key Findings 63

• Market Engineering Measurements 64

• Revenue Forecast 65

• Revenue Forecast Discussion 66

• Competitive Tier Analysis 67

The Last Word 68

• The Last Word—3 Big Predictions 69

• The Last Word—Discussion 70

• Legal Disclaimer 73

Appendix 74

• Drivers Explained 75

• Restraints Explained 77

• Competitor Profiles 79

Contents (continued)

6NE41-52

Source: Frost & Sullivan

The majority of the quantitative and qualitative information contained in this research service was

acquired through primary research conducted with liquid handling product providers. Most consultations

were conducted with vice presidents (VPs) of business units, VPs of marketing, product managers,

marketing managers, marketing directors, and business development directors from various competitors

in the liquid handling market.

Industry-specific information obtained include:

• Liquid handling revenue breakdowns by product segments and regions

• Company revenues, market share estimates, and projected growth rates of various competitors

• Top-level customer, regional, and technology market trend information

• Market drivers, restraints, and challenges

Supplementary research was conducted utilizing secondary sources including scientific journals, online

media, Frost & Sullivan databases and research services, and publicly available corporate filings.

Forecasts are based on the data and analyses regarding industry challenges, market drivers and

restraints, and market trends. If specific revenues or market sizes were unavailable, estimates were

derived through the consultations with industry experts, augmented by secondary research. Growth

trends specific to certain market participants are based on consultations, past growth rates, and

technology reviews.

Methodology

Return to contents

7NE41-52

Executive Summary

8NE41-52

Source: Frost & Sullivan

Scope and Segmentation

Geographic Coverage

United States

Market Segmentation

Automated Robotic Workstations

Low-to-Mid Throughput Automated Liquid Handling Tools

Manual Pipettes and Consumables

Study Period 2011–2021

Base Year 2014

Forecast Period 2014–2021

Monetary Unit US dollars

The total market, as defined by this study, includes automated robotic workstations, low-to-mid

throughput automated liquid handling tools, and manual pipettes and consumables. Excluded from this

analysis are liquid handling services.

9NE41-52

Source: Frost & Sullivan

How did the market respond to the difficult US economic climate over the past 3 years?

What application trends are driving adoption of liquid handlers?

What emerging companies are providing innovative products and challenging market leaders?

What unforeseen future factors may dramatically affect market forecasts?

What are the key differentiating competitive factors companies are using to be successful?

What larger life science research tools trends are making their way into the liquid handling market and affecting product, end-user, and economic dynamics?

Key Questions This Study Will Answer

10NE41-52

Source: Frost & Sullivan

CEO’s Perspective

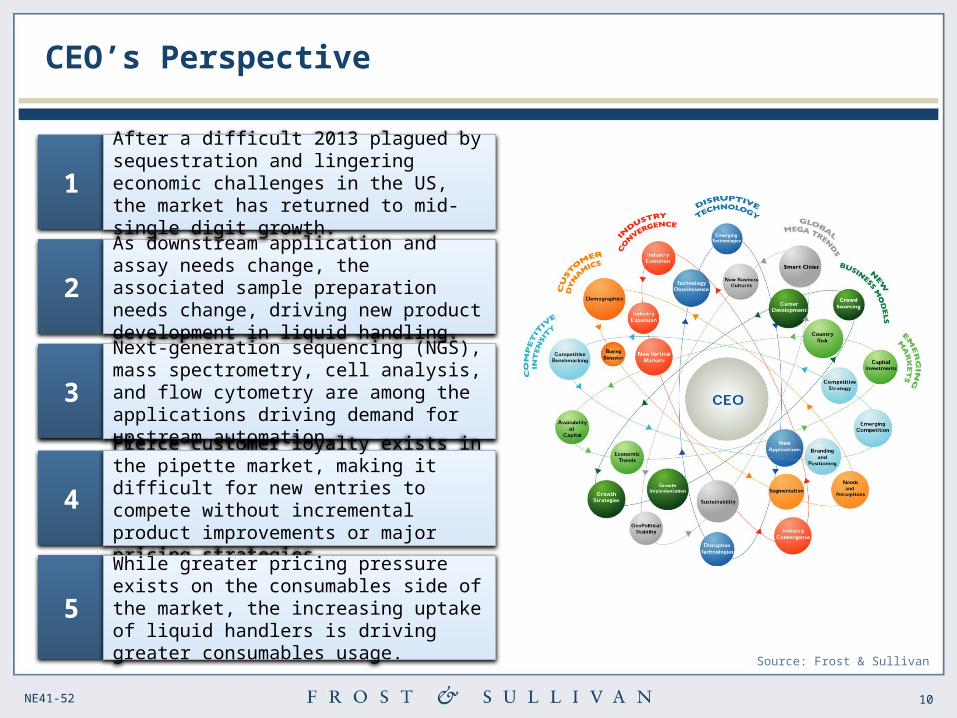

2As downstream application and assay needs change, the associated sample preparation needs change, driving new product development in liquid handling.

3Next-generation sequencing (NGS), mass spectrometry, cell analysis, and flow cytometry are among the applications driving demand for upstream automation.

4Fierce customer loyalty exists in the pipette market, making it difficult for new entries to compete without incremental product improvements or major pricing strategies.

5While greater pricing pressure exists on the consumables side of the market, the increasing uptake of liquid handlers is driving greater consumables usage.

1After a difficult 2013 plagued by sequestration and lingering economic challenges in the US, the market has returned to mid-single digit growth.

Return to contents

11NE41-52

Market Overview and Segmentation

12NE41-52

Source: Frost & Sullivan

The total market, as defined by this study, includes automated robotic workstations, low-to-mid

throughput automated liquid handling tools, and manual pipettes and consumables. Excluded from this

analysis are liquid handling services. For the purpose of this study, the market is divided into three

product segments.

• The Automated Robotic Workstations segment includes automated liquid handling robotic

workstations, pipetting workstations, fully integrated robotic workstations, and high-end high

throughput liquid handling instruments.

• The Low-to-Mid Throughput Automated Liquid Handling Tools segment includes benchtop small

and mid-sized automated pipette instruments, automated liquid/reagent dispensers, electronic

pipettes, and integrated automated microplate washers.

• The Manual Pipettes and Consumables segment includes manual pipettes, pipette tips (manual

and automated certified), vials, and storage tubes.

Market Background

13NE41-52

Source: Frost & Sullivan

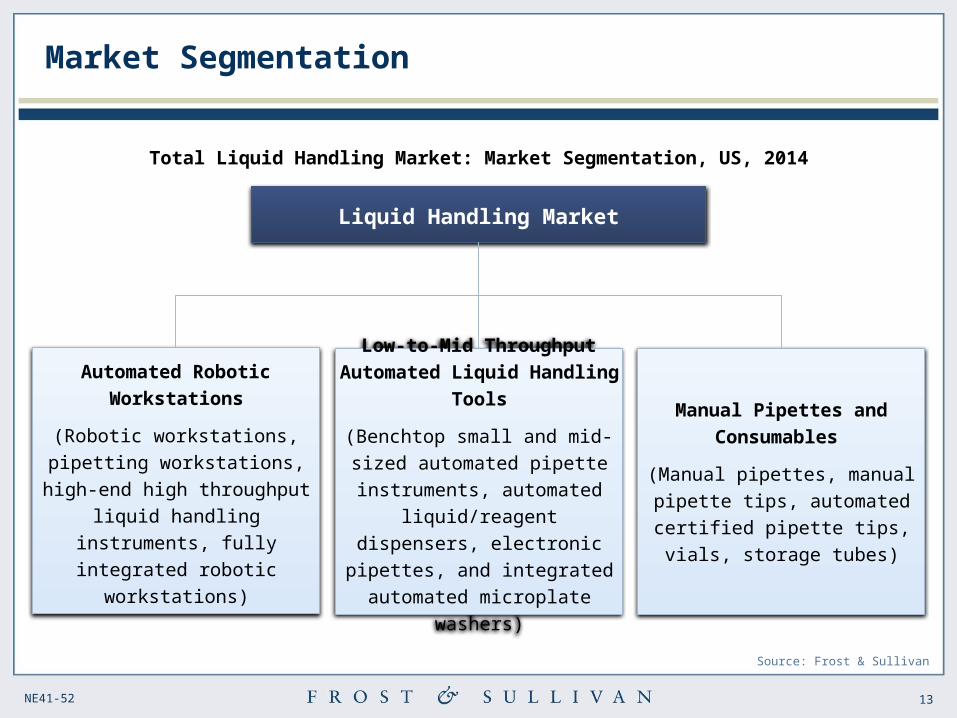

Total Liquid Handling Market: Market Segmentation, US, 2014

Market Segmentation

Low-to-Mid Throughput

Automated Liquid Handling

Tools

(Benchtop small and mid-sized

automated pipette instruments,

automated liquid/reagent

dispensers, electronic pipettes,

and integrated automated

microplate washers)

Liquid Handling Market

Manual Pipettes and

Consumables

(Manual pipettes, manual

pipette tips, automated certified

pipette tips, vials, storage

tubes)

Automated Robotic

Workstations

(Robotic workstations, pipetting

workstations, high-end high

throughput liquid handling

instruments, fully integrated

robotic workstations)

14NE41-52

Note: All figures are rounded. The base year is 2014. Source: Frost & Sullivan

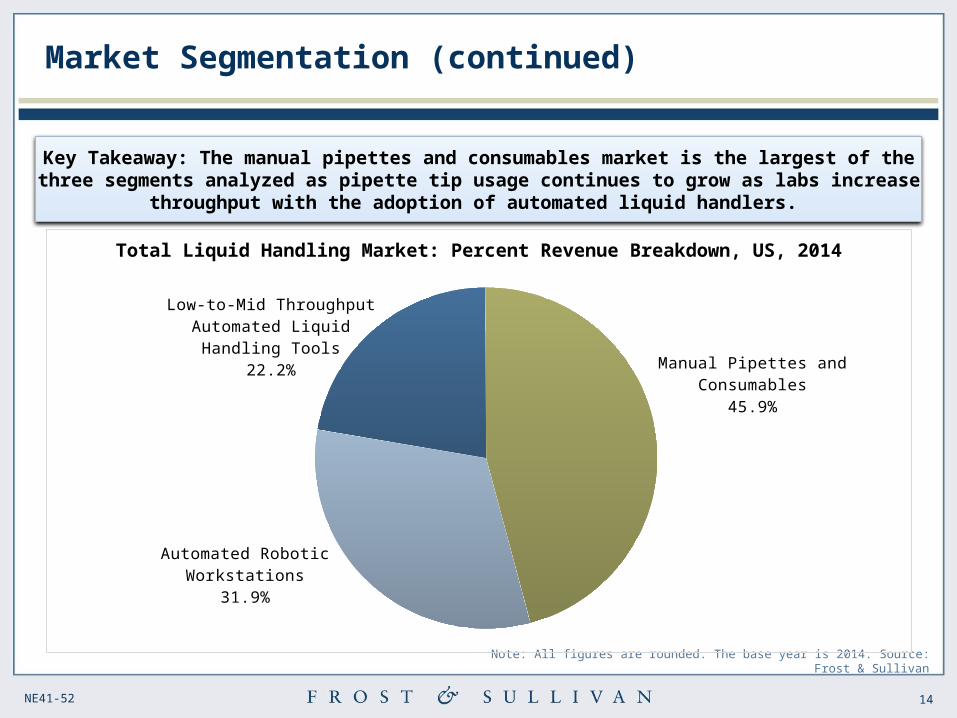

Automated Robotic Worksta-tions

31.9%

Low-to-Mid Throughput Au-tomated Liquid Handling

Tools22.2% Manual Pipettes and Con-

sumables45.9%

Key Takeaway: The manual pipettes and consumables market is the largest of the three segments analyzed as pipette tip usage continues to grow as labs increase throughput with the adoption of

automated liquid handlers.

Total Liquid Handling Market: Percent Revenue Breakdown, US, 2014

Market Segmentation (continued)

15NE41-52

Source: Frost & Sullivan

Market Overview

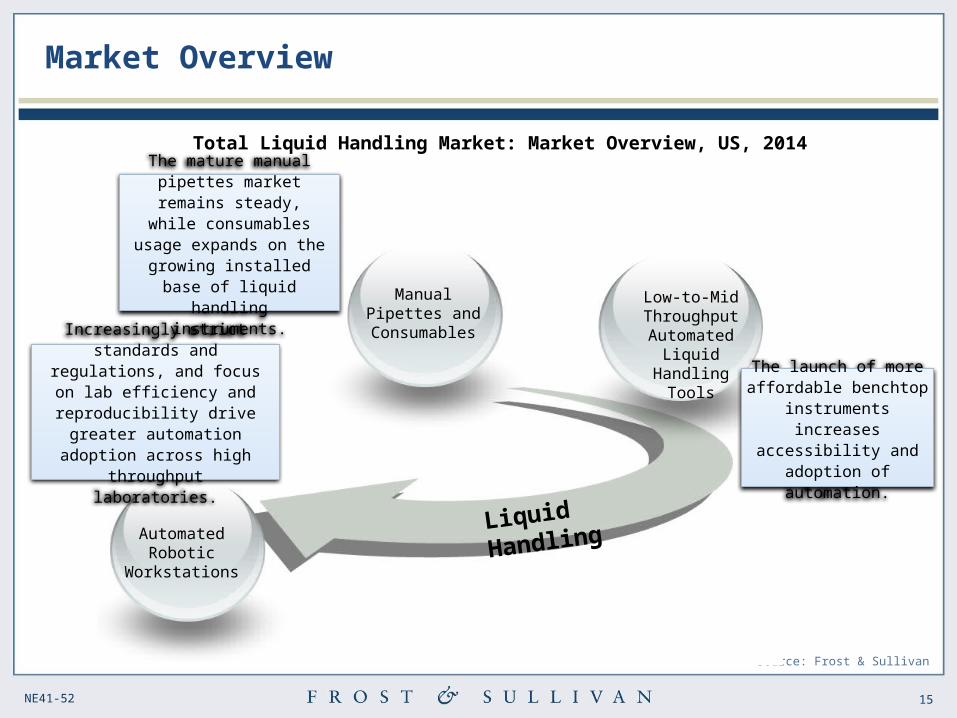

Total Liquid Handling Market: Market Overview, US, 2014

Manual Pipettes and

Consumables

Low-to-Mid Throughput

Automated Liquid Handling Tools

Automated Robotic

Workstations

Liquid Handling

Increasingly strict standards and regulations, and focus on

lab efficiency and reproducibility drive greater automation

adoption across high throughput laboratories.

The launch of more affordable benchtop

instruments increases accessibility and adoption

of automation.

The mature manual pipettes market remains steady,

while consumables usage expands on the growing installed base of liquid handling instruments.

16NE41-52

Exhibit Slide Number

Total Liquid Handling Market: Revenue Summary, US, 2014–2021 8

Total Liquid Handling Market: Market Engineering Measurements, US, 2014 11

Total Liquid Handling Market: Market Segmentation, US, 2014 17

Total Liquid Handling Market: Percent Revenue Breakdown, US, 2014 18

Total Liquid Handling Market: Market Overview, US, 2014 19

Total Liquid Handling Market: Market Outlook, US, 2014 and 2024 20

Total Liquid Handling Market: Game-changing Strategies, US, 2014 23

Total Liquid Handling Market: Mergers and Acquisitions, US, 2011–2014 25

Total Liquid Handling Market: Key Market Drivers, US, 2015–2021 27

Total Liquid Handling Market: Key Market Restraints, US, 2015–2021 28

Total Liquid Handling Market: Impact of Top Trends, US, 2014 29

Total Liquid Handling Market: Market Engineering Measurements, US, 2014 31

Total Liquid Handling Market: Revenue Forecast, US, 2011–2021 33

Total Liquid Handling Market: Revenue Forecast by Segment, US, 2011–2021 34

List of Exhibits

17NE41-52

Exhibit Slide Number

Total Liquid Handling Market: Percent Revenue Forecast by Segment, US, 2011–2021 36

Total Liquid Handling Market: Procurement Process, US, 2014 39

Total Liquid Handling Market: Segment Lifecycle Analysis, US, 2014 40

Total Liquid Handling Market: Competitive Structure, US, 2014 42

Total Liquid Handling Market: Recent Major Product Launches, US, 2013–2014 43

Total Liquid Handling Market: SWOT Analysis, US, 2014 45

Total Liquid Handling Market: Competitive Assessment, US, 2014 47

Automated Robotic Workstations Market: Percent Revenue Breakdown, US, 2014 49

Automated Robotic Workstations Market: Market Engineering Measurements, US, 2014 50

Automated Robotic Workstations Market: Revenue Forecast, US, 2011–2021 51

Automated Robotic Workstations Market: Competitor Tier Analysis, US, 2014 54

Low-to-Mid Throughput Automated Liquid Handling Tools Market: Percent Revenue Breakdown, US, 2014

56

List of Exhibits (continued)

18NE41-52

Exhibit Slide Number

Low-to-Mid Throughput Automated Liquid Handling Tools Market: Market Engineering Measurements, US, 2014

57

Los-to-Mid Throughput Automated Liquid Handling Tools Market: Revenue Forecast, US, 2011–2021

58

Low-to-mid Throughput Automated Liquid Handling Tools Market: Competitor Tier Analysis, US, 2014

61

Manual Pipettes and Consumables Market: Percent Revenue Breakdown, US, 2014 63

Manual Pipettes and Consumables Market: Market Engineering Measurements, US, 2014

64

Manual Pipettes and Consumables Market: Revenue Forecast, US, 2011–2021 65

Manual Pipettes and Consumables Market: Competitor Tier Analysis, US, 2014 67

Planned Lab Instrument Purchases, Global, 2014–2015 72

List of Exhibits (continued)