Embed Size (px)

Citation preview

1

Bar Talk

The away-from-home consumption phenomenon:

A fuzzy research study between induction

and deduction.

Febo Leondini and Matteo De Angelis

2

Contents

Foreword……………………………………………………………………………………………………..

3

Methodological Note…………………………………………………………………………………. 6

The HoReCa consumption phenomenon: An inductive research

study study

study for a new analytical methodology ……………………………………………… 8

SECTION ONE

Drivers influencing the Ho.Re.Ca. consumption phenomena ……….… 14

SECTION TWO

Demand targeting and supply segmentation.................................. 31

SECTION THREE

Conclusions.................................................................................... 35

SECTION FOUR

A methodological proposal for analysing the Ho.Re.Ca market ……. 40

SECTION FIVE

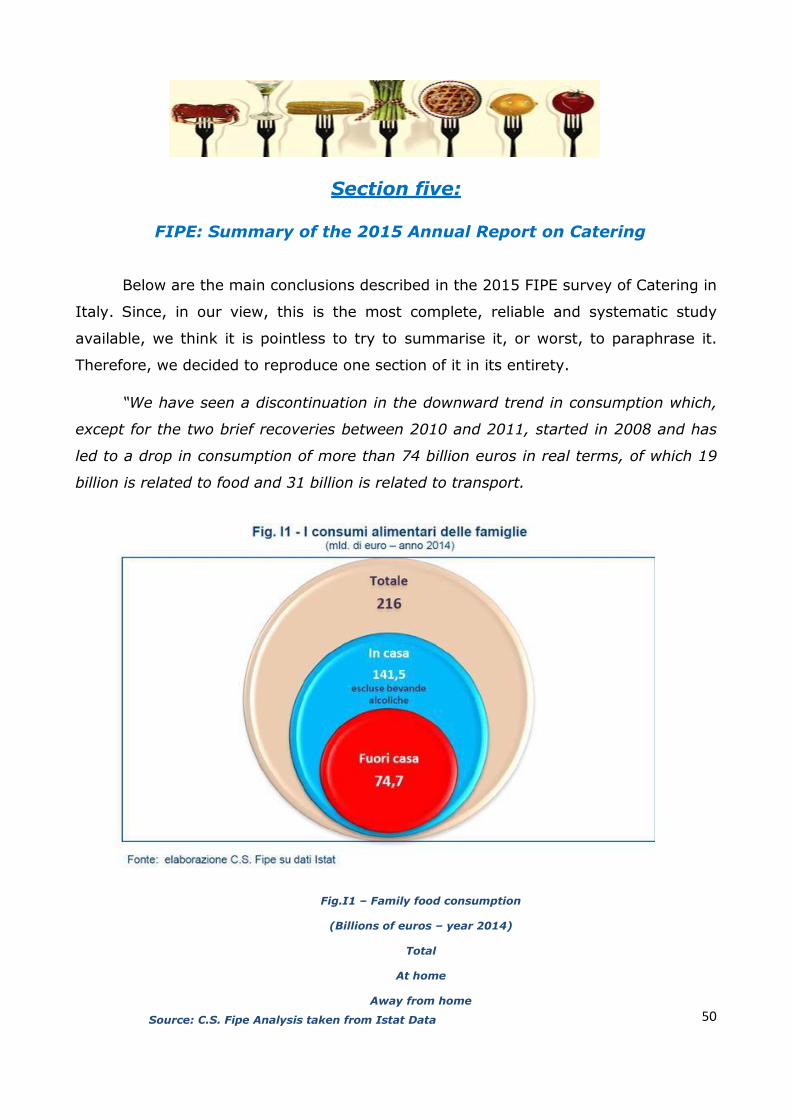

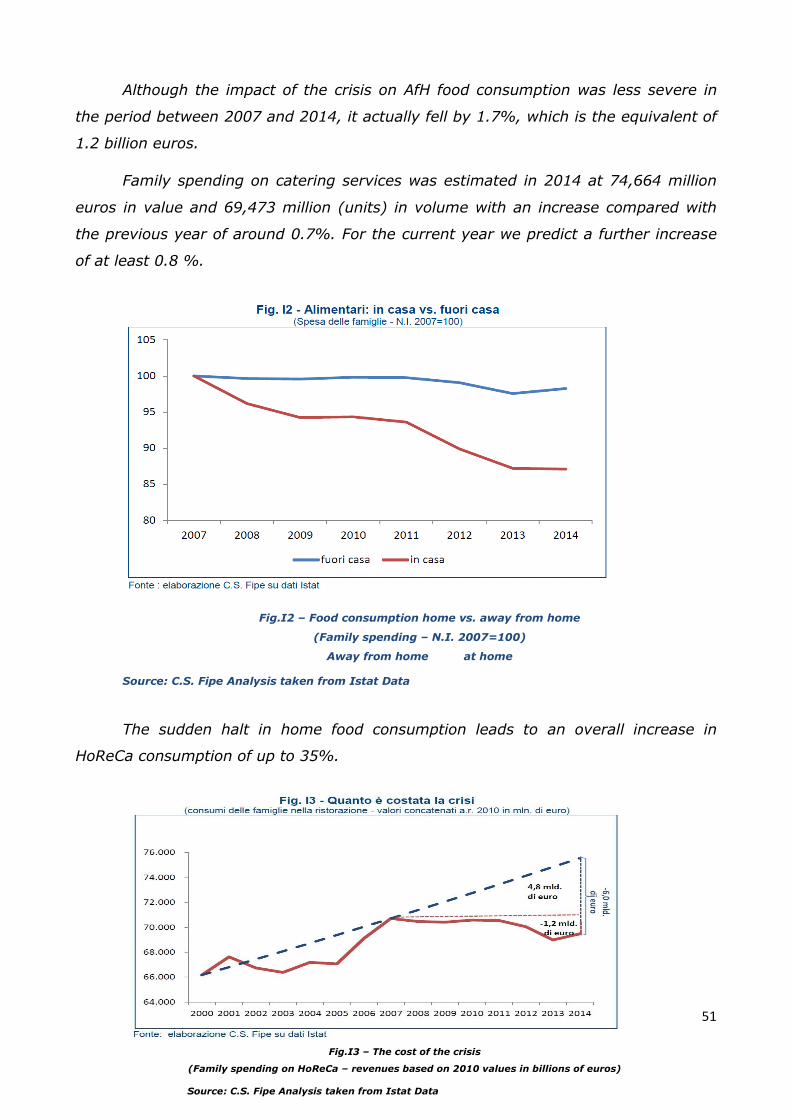

FIPE: Ho.Re.Ca. Annual Report 2015…………………………………..…............ 50

SECTION SIX

Bibliography .....................…………………………..…………………………………..….. 58

3

Foreword

Despite the existence of a substantial number of analytical studies on the

Consumption phenomenon, there are still only a few documents that deal specifically

with what happens in HoReCa (Hotel, Restaurants, and Cafés). This omission, mainly

due to the difficulty of collecting and processing data of any type, has prompted the

industry to adapt business strategies developed for other sectors to those of HoReCa,

rather than develop its own strategy. This document attempts to discourage the

tendency to consider the HoReCa as a sort of “child of a lesser god” of which,

essentially, we know almost nothing.

Let’s take Oldenburg’s definition as our starting point, according to which

HoReCa is the third place, after the home and the workplace, where a person

discovers their sense of community and interacts socially. We have decided to

examine the process of Consumption both from a social and cultural perspective. This,

however, has not stopped us from identifying a quantitative, in other words objective

and repeatable method, which enables us to measure the drivers influencing the

process, in order to give us the tools to understand the hidden potential of the sector.

The search for a “process”, in this case that of AfH Consumption (Away from

Home, in a bar for instance) in HoReCa, does not enable us to identify specific

parameters that can immediately be fed into operational processes which have a

direct effect on costs and revenues. The analysis of a process can, and should, show

trends and significant events that enable the organisation to understand as early as

possible if someone is trying to take it by surprise, overtaking it on the inside. To put

it another way and to take an example from another industry, analysing the way in

which mobile devices are used would certainly not have identified a specific future

product but would have avoided wasting time improving physical keyboards, coming

up instead with the idea of the touch screen. Taking this into account, in this paper we

do not explore the processes of creating the Brand image and of giving personality to

the future product. These are specific to the marketing strategies of the individual

company and it would be unrealistic to try to address them in a general paper like this

one.

In terms of structure, this paper is divided into 6 separate sections.

4

The first section, which is necessarily theoretical, aims to define the drivers

affecting the HoReCa phenomena of consumption. What is innovative about what we

are proposing is that we have sought to support our theoretical conclusions, which are

based on accredited studies around the world, with a series of empirical observations,

which are based on objective data. By doing this we have created a bridge between

deductive rational models and the genuine empiricism of concrete field testing. Our

aim, which we hope we have achieved, was to confirm, by means of a series of

repeatable studies, the validity of the theoretical models presented.

The second section outlines the implications of the studies we carried out both

for the targeting of Demand as well as for the segmentation of Supply. The

conclusions we reached, which were often counter-intuitive, will, it is hoped,

encourage further research studies and engender further discussion.

In the third section we have presented and summarised the conclusions that we

have reached as a result of this study and which, at least in part, can form the basis

for more in-depth analysis in the future.

The fourth section, which is more technical and serves as a kind of appendix to

this paper, proposes a way of carrying out research into the Ho.Re.Ca sector enabling

the various stakeholders to take advantage of a tool, which can certainly be improved

over time, that can be used both to analyse a little-understood Segment and to

attempt to measure the effects of consumer behaviour on the profit-and-loss account.

The fifth section reproduces an extract from the publication “Considerazioni

Generali dell’Indagine FIPE 2015 sulla ristorazione in Italia: il documento più completo

sull’HoReCa” (which translates approximately into "General Considerations resulting

from the FIPE 2015 investingation on the Italian catering industry: the most

comprehensive document on Ho.Re.Ca).

The sixth section provides a basic bibliography for a more in-depth study of the

topics covered by this paper.

Finally, two more points.

As previously mentioned, we have carried out a study of the HoReCa

phenomenon of consumption, which, based on our research, is determined by both

social and cultural factors. This means that we have separated it from the product

process. In other words, we have tried to show that the function of the product is to

5

be an “experiential facilitator” and not, as happens in the purchasing function, an

experience driver. This perspective may seem infuriatingly subtle but it is of

fundamental importance because it enables us to clearly separate the two analytical

functions: that of Consumption and that of institutional Marketing Strategies.

This study finally asks how it might be possible to improve, through a better

understanding, the cash performance of a sector that, whether viewed objectively or

subjectively, represents a very important commercial opportunity. This paper suggests

that people working in this sector should try to use new research tools to develop a

commercial strategy that suits the inherent characteristics of the Market, but in any

case it will also have achieved its objective if it succeeds in stimulating a debate

among managers working in the sector.

***

6

Methodological Note

The aim of the research study, hereinafter referred to as R1, being the first

of its kind as far as we are aware, was to verify a series of theoretical insights that,

although considered to be true according to the logic of consumer theory, needed

to be proven empirically.

R1, we should emphasise, was conducted in a non-cooperative context, and

therefore the consumers were anonymous and were unaware of the research study

taking place. Therefore, the data presented was all objective data, deduced from

the cash-register sales receipts. For example, the number of consumers involved in

the study was determined by the number of covers recorded in the cash register,

which are therefore objectively verifiable.

With regard to the choice of the POS sample we were faced with two options: a

large number of POSs and relatively few sales receipts or a single POS with a large

number of receipts for us to analyse. The second alternative was chosen because

the consumption phenomenon, as demonstrated later, does not depend on the

type of POS and therefore a longitudinal study was preferable to a horizontal

study. The POS chosen is situated at the mid-point between the Milan–Piacenza

road and the Brescia-Mantova road. Customers are served either at the tables or at

the bar and the establishment offers a full food and beverages menu.

The parameters of R1 are as follows:

- Period: from week 19 to week 30 of 2016 subdivided into:

o T1 for weeks 22 to 30;

o T2 for weeks 19 to 22.

- Consumption situations analysed: 2

o Dinner, identified by the sales receipts issued between 20.00 and

21.59;

o After dinner, identified by the sales receipts issued between 22.00 and

23.59.

- Product category consumed:

o Mineral water;

o Bottled or canned soft drinks;

o Fruit juices;

o Bottled or canned beers;

7

o Bottled wines;

o Spirits and cordials;

o Non-packaged drinks;

o Cocktails;

o Sandwiches and pizzas;

o Traditional dishes, or portions;

o Hot drinks.

- Number of sales receipts analysed: 4,643;

- No. of sales receipt lines processed: 37,120;

- No. of consumers participating: 12,555 of which

o Dinner: 5,320;

o After dinner: 7,235;

- Type of consumption analysed: 3, specifically:

o Consumption at the bar;

o Consumption of food and beverages at the table;

o Consumption of beverages only at the table;

- Clusters used by week: 3, specifically:

o From Monday to Thursday inclusive;

o From Friday to Saturday inclusive;

o Sunday.

***

8

The HoReCa Consumption phenomenon: an inductive research study

for a new analytical methodology

Febo Leondini1, Matteo De Angelis2

This study aims to explore the demand-supply dynamics which characterise the

HoReCa sector (that is the consumption of food and beverages “away from home”). In

particular, through a transactional analysis of a sample of over 12,000 consumers in a

selected POS, our study fills the obvious gap in our scientific knowledge about the key

drivers influencing consumer behaviour in this significant sector, with major

implications both in terms of demand targeting and of supply segmentation. In our

study we have used an inductive approach, which is based on empirical observations

and data relating to the behaviour of the consumers of HoReCa goods and services in

various consumption situations, for different product categories and at different times

of the week. The most important point of this study is that the empirical research

carried out prepares the ground for a proposed new study method based on three

variables which are: servitisation, time and space. These, in turn, are divided into a

number of useful indicators that provide applicable and comparable measures for

assessing the demand–supply dynamics within the HoReCa sector.

Key terms: HoReCa, consumption, services, experience, time, space.

1. Research objectives and context

Despite the existence of a substantial number of analytical studies on the

Consumption processes in various contexts and markets, there are still only a few

research studies that deal specifically with what happens in HoReCa, which is in the

“away-from-home” food and beverage consumption sector. This lack, mainly due to

the difficulty in collecting and processing systematic data, prompted the industry to

adapt commercial strategies that had been developed for other sectors to those of

HoReCa, rather than develop its own strategy. The lack of in-depth knowledge of the

HoReCa sector is even more surprising given its significant economic value, which is

equal to 74.7 billion euros (2014 data), compared with approx. 66 billion euros in

2008, which is the equivalent to 35% of what Italians spend on food (FIPE 2015

1 Contact author, Consigliere Delegato di Noumeno 2 Assistant Professor di Marketing, Università LUISS Guido Carli

9

Report). This document attempts to discourage the tendency to consider the HoReCa

as a sort of “child of a lesser god” about which, essentially, we know almost nothing.

Let’s take Oldenburg’s definition as our starting point, according to which HoReCa is

the third place, after the home and the workplace, where a person discovers their

sense of community and interacts socially. We have decided to examine the process of

Consumption both from a social and cultural perspective. This, however, has not

stopped us from identifying a quantitative, in other words objective and repeatable

method, which enables us to measure the key drivers of the process, in order to give

us the tools to understand the hidden potential of the sector.

Starting with the basic assumption that HoReCa consumption has social and

cultural drivers, this study maintains that the main purpose of the HoReCa product is

to be “an experiential facilitator” and not to be a direct driver of the consumption

experience. On the basis of these arguments the study aims to provide professionals

in this industry with an inductive approach for assessing consumption processes that

is based on the observations of consumer behaviours at POSs, aimed at creating an

analysis model for use by both academics and managers in future. This inductive

approach goes against, to a certain extent, the deductive approach based on the

application of pre-prepared analysis schemes which are therefore less and less

capable of grasping the complex, varied and multi-dimensional aspects of HoReCa

consumption. The empirical research study presented in this document is based on

data relating to transactions carried out by a sample of over 12,000 consumers at a

POS located in Northern Italy, and leads to a methodological proposal for assessing

consumption within the HoReCa sector.

2. Customer experience in the HoReCa consumption

These days HoReCa consumption is strongly characterised by experience. According to

Miao and Mattila (2013), "food consumption needs to be examined from a broader

sociological perspective beyond product acquisition". According to Gentile et al. (2007,

p. 397), "the customer experience originates from a set of interactions between a

customer and a product, a company, or part of its organisation, which provoke a

reaction. This experience is strictly personal and implies the customer’s involvement

at different levels (rational, emotional, sensorial, physical, and spiritual)”. In other

words, the term customer experience (CE) identifies a descriptive model of what the

10

consumer experiences during the process of buying and consuming goods. A

noteworthy study that identified the parameters and people’s previous consumer

experience was written by Verhoef et al. (2009) in which the authors present a model

where the key drivers of the CE are the social environment, the service interface

(which includes the use of technology for the provision of services and the possibility

to co-create and personalise the service itself), the POS environment and the range

and price of products and services.

HoReCa consumption can be considered as having three fundamental dimensions:

servitisation, defined as the combination of the physical product and the intangibles of

experience, time and space. In other words, servitisation refers to the idea that the

physical product is one of the components of the consumption experience, not the

driver of the experience itself. This is due to the fact that the HoReCa consumption

dynamic often has a tendency to make the product seem anonymous. As far as time is

concerned, this is defined as when the consumption takes place, and this differs

between breakfast, lunch, an aperitif and dinner and depends on the importance of

the social occasion. Finally, space indicates the place where consumption takes place

and is determined by the various POSs (from vending machines and take-away kiosks

to POSs with service). These 3 dimensions can be interpreted using the Verhoef at al

model (2009), which stresses the importance of associating the social environment

with the time dimension (when the consumption takes place), the service interface

and the POS environment with the space dimension, and, finally, the range and price

of products and services with the servitisation dimension.

Setting the definition of CE in the context of HoReCa consumption, we can

conclude that CE is triggered by the occasion, determined by the context and defined

by the attitude of the consumer. CE is therefore strongly influenced by qualitative

factors that have an unpredictable impact, since they are in a bi-univocal relationship

with the experience of the consumer. To incorporate this assumption into the current

social dynamic, however, means to undermine the classical theories of demand

segmentation. The post-modern tribalism context (Maffesoli, 2004) in which the

consumer operates and exists prevents the attribution of pre-conceived meaning to

his or her own experience and consequently goes against the idea of a segmentation

based on a classification that, despite being multi-varied, excludes experience. In this

framework, with its socio-economic connotations, we retrieve the difference between

HoReCa consumption and other forms of consumption: while in the latter, the same

experience can be derived from the same quantitative data, in the former this does

11

not happen. HoReCa consumption adheres to a new formulation of the principle of

uncertainty that goes more or less like this: it is impossible for us to understand the

quantitative data of the act of consumption or the experiences of the consumer at that

very moment; the same quantitative data can describe different experiences and,

conversely, identical experiences can be described by different quantitative data.

When you become aware of this particular feature of HoReCa consumption, you have

to recognise the impossibility of coming to a descriptive conclusion which does not

take account of experience and, consequently, to accept the need to move from a

metaphysic of the consumer to an anthropology of consumption.

3. Empirical research

Empirical research into HoReCa consumption was conducted in a non-cooperative

context, and therefore the consumers were anonymous and were unaware of the

research study taking place. Consequently, the data presented was all objective data,

deduced from cash-register sales receipts. We decided to go to a single POS, which is

situated at the mid-point between the Milan–Piacenza road and the Brescia-Mantova

road. Customers are served either at the tables or at the bar and the establishment

offers a full food and beverage menu. The research study was conducted between

weeks 19 and 30 in 2016 and we analysed dinner and after dinner as our consumption

situations. We analysed the following product categories: mineral water, pre-packed

drinks, juices, beers, wines, liquors, non-packaged drinks, cocktails, sandwiches,

pizzas, traditional dishes, and coffees. We analysed 12,555 consumers and 4,643 sales

receipts. The analysis was divided into three consumption methods (at the bar, food

and beverages at the table or just beverages at the table) and three clusters during

the week (from Monday to Thursday, from Friday to Saturday and Sunday).

4. A methodological proposal for the analysis of HoReCa consumption

The methodological proposal presented in this study is based, on the one hand, on the

definition of the parameters of supply and, on the other hand, on the definition of the

parameters of demand. With regard to the supply aspect, the aim is to identify

objective data definable in quantitative terms, which enable us to analyse the value

drivers of the HoReCa consumption phenomena. Specifically, in line with what we

presented in the theoretical part, the methodological proposal is based on the three

12

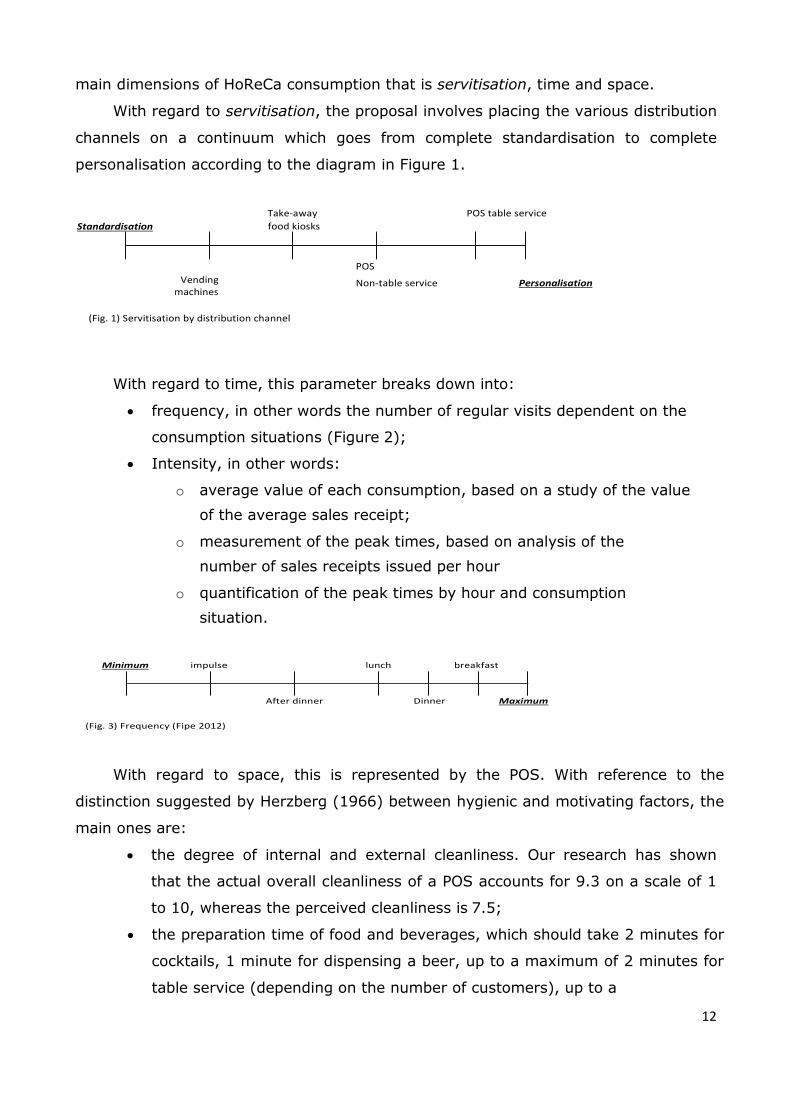

main dimensions of HoReCa consumption that is servitisation, time and space.

With regard to servitisation, the proposal involves placing the various distribution

channels on a continuum which goes from complete standardisation to complete

personalisation according to the diagram in Figure 1.

Standardisation

Take-away

food kiosks

POS table service

Vending machines

POS

Non-table service Personalisation

(Fig. 1) Servitisation by distribution channel

With regard to time, this parameter breaks down into:

frequency, in other words the number of regular visits dependent on the

consumption situations (Figure 2);

Intensity, in other words:

o average value of each consumption, based on a study of the value

of the average sales receipt;

o measurement of the peak times, based on analysis of the

number of sales receipts issued per hour

o quantification of the peak times by hour and consumption

situation.

Minimum impulse lunch breakfast

After dinner Dinner Maximum

With regard to space, this is represented by the POS. With reference to the

distinction suggested by Herzberg (1966) between hygienic and motivating factors, the

main ones are:

the degree of internal and external cleanliness. Our research has shown

that the actual overall cleanliness of a POS accounts for 9.3 on a scale of 1

to 10, whereas the perceived cleanliness is 7.5;

the preparation time of food and beverages, which should take 2 minutes for

cocktails, 1 minute for dispensing a beer, up to a maximum of 2 minutes for

table service (depending on the number of customers), up to a

(Fig. 3) Frequency (Fipe 2012)

13

maximum of 2 minutes for taking the order, and a maximum of 6 minutes

for the preparation and cooking of pizzas and hot dishes.

Among the motivating factors, on the other hand, we include the friendliness of

the staff, how pleasant the environment is, the sensory experience, the retail-

tainment and special events.

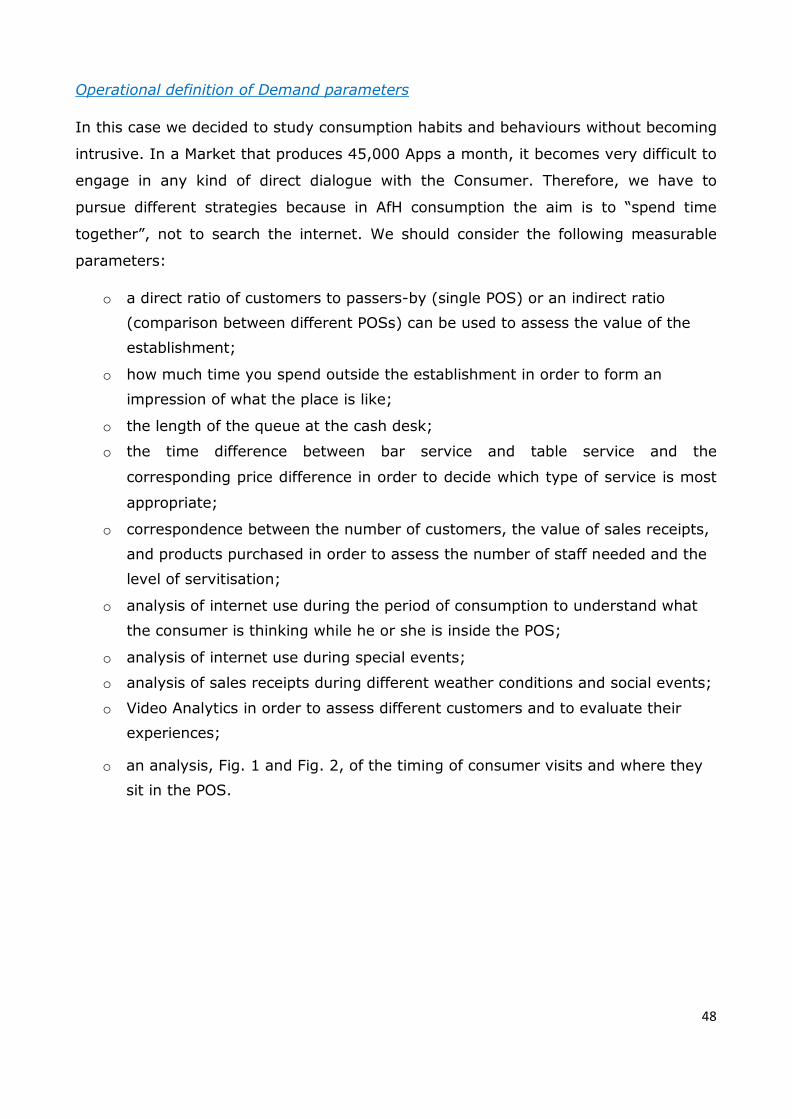

With regard to demand, it was a case of examining consumption habits and

behaviour without being too intrusive. Quantitative data to take into account includes:

the ratio of customers to passers-by, both direct (individual POS) and indirect

(comparison between different POSs), to measure the value of the location;

the time spent looking in to define the in-store communication policies of the

establishment;

the time spent in the queue for the till;

the time differential between consumption at the bar or at the table;

the correlation between customer flow, value of the sales receipt and products

purchased in order to modify either the staffing levels required or the

servitisation;

the analysis of internet traffic during consumption to understand what the

consumer thinks while he or she is inside the POS;

the integration of the analysis of sales receipts with climatic and social variables;

video analytics to assess the participants and to define the various types of

experience.

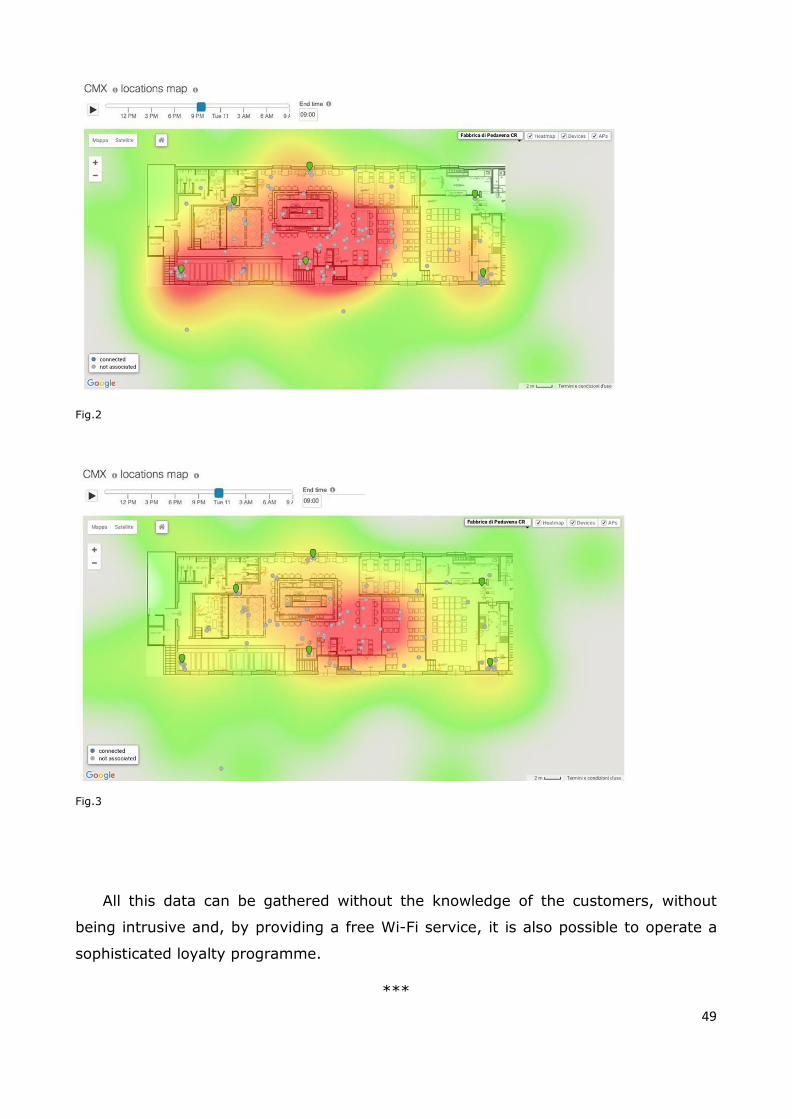

All of the above data can be collected in non-collaborative contexts, without being

intrusive, and by mere provision of a free Wi-Fi service.

***

14

Section One:

Drivers influencing the Ho.Re.Ca. consumption phenomena

AfH consumption: essential components

The social driver: Consumption between impulse and relationship

The need to identify more precisely the potential users of a service or potential

consumers of goods has been increasing with the increase of the productive potential

of a Supply system in constant expansion. The response to such need is complex and

intricate. In the interests of providing a general summary only, we can identify three

different approaches to resolving the problem which were adopted in three phases

following the Second World War:

- a “company centric” vision which, in an unspecified Market that is driven by

needs and experiences continuous, fast expansion, was motivated by the need

to fill the void of Supply. Essentially, we were faced with a proportion of

Demand left unsatisfied and the response was simply to produce more and

faster. This phase, which started in the period after the second world war, came

to an end in the mid-70s;

- a “market centric” vision in which, with a Consumption dynamic increasingly

liberated from Need, the principles of Market segmentation are confirmed. The

market is no longer regarded as a kind of quintessential ether, but as an

aggregate of different components. Consumers can be precisely classified

according to demographic and social indicators. This phase will last for ten

years and will come to an end towards the middle of the 80s. It is a period in

which powerful emotions and shifting values are causing tensions within

society. Society tended to give hierarchical responses, which in the end were

the drivers of the Consumption phenomena approach;

15

- a “consumer centric” vision which lasted until the end of the 20th Century. In

this phase it was realised that, when describing the behaviour of buyers and

consumers, demographic and social variables are inadequate. Although society

was still influenced by the patterns and values of previous decades, it began to

be affected by millennial phenomena and to have hedonistic tendencies. The

development of sophisticated psychographic techniques, the explosion of the

sociology of consumption and the study of youth dynamics originate in this

period.

Towards the end of the last century these behavioural dynamics and ethics, which had

affected society in this final decade, ceased to be considered the framework of

reference, which could be precisely describable and identifiable, and became instead

the main drivers, if not the instruments, of change. A new social model began to be

developed, no longer describable in terms of stratified differentiation (Luhman, 1990),

and therefore subjected to a hierarchical order. It was instead based on functional

differentiation, in which hierarchical boundaries fade until they lose their

representative capacity. The birth and the development of social networks, the

pervasiveness of interconnected networks and the spread of low-cost flights, following

an initial shock in a neo-oblative way, increased the flow of information and group

dynamics, and mankind became again the measure of all things: of the things that are

as they are, and of the things that are not as they are not. From now on we begin to

refer to Customer Experience (CE) as a dialectical synthesis of the three periods

described above. Starting from CE, seen not as a new descriptive model but as an

interactive process of mutual engagement between the consumer and third parties on

a pseudo-contractual basis, we can define the limits of the traditional theory of

Demand segmentation in AfH consumption: “The results from this study further affirm

the notion that food consumption needs to be examined from a broader sociological

perspective beyond product acquisition” (Miao, Mattila 2013).

16

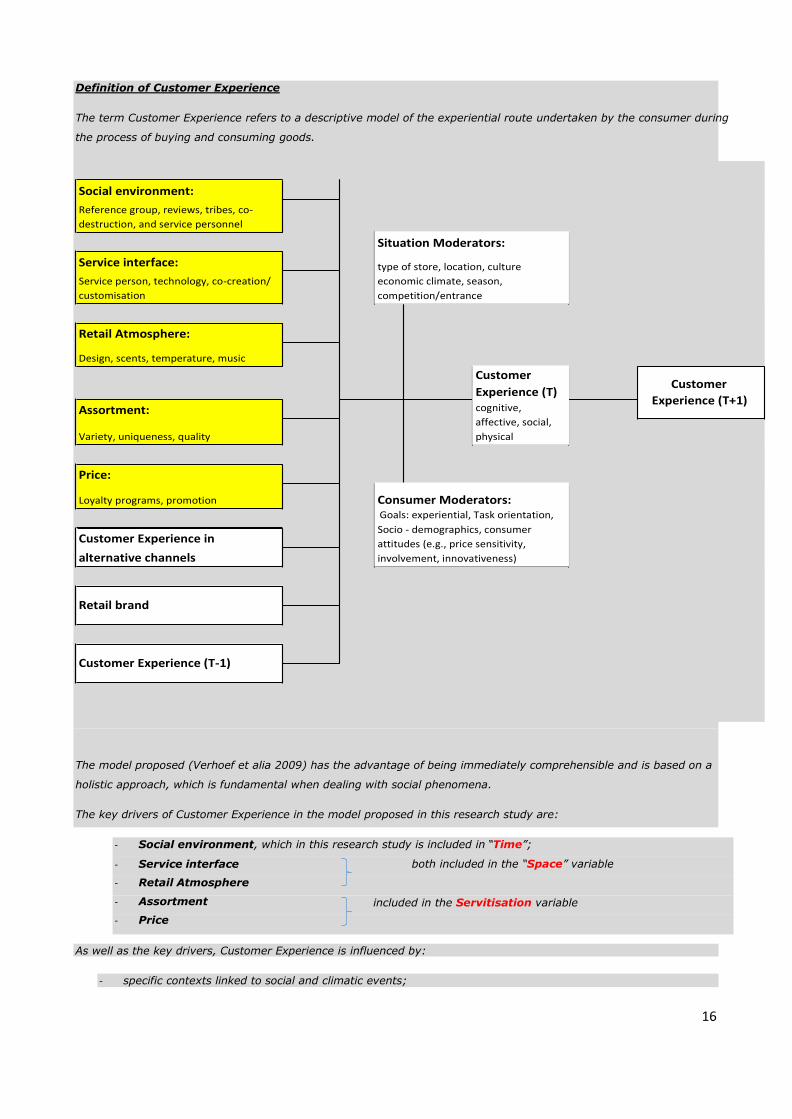

Definition of Customer Experience

The term Customer Experience refers to a descriptive model of the experiential route undertaken by the consumer during

the process of buying and consuming goods.

Social environment:

Reference group, reviews, tribes, co-

destruction, and service personnel

Service interface:

Service person, technology, co-creation/

customisation

Retail Atmosphere:

Design, scents, temperature, music

Assortment:

Customer

Experience (T+1)

Variety, uniqueness, quality

Price:

Loyalty programs, promotion

Customer Experience in

alternative channels

Retail brand

Customer Experience (T-1)

The model proposed (Verhoef et alia 2009) has the advantage of being immediately comprehensible and is based on a

holistic approach, which is fundamental when dealing with social phenomena.

The key drivers of Customer Experience in the model proposed in this research study are:

As well as the key drivers, Customer Experience is influenced by:

- specific contexts linked to social and climatic events;

- Social environment, which in this research study is included in “Time”;

- Service interface

- Retail Atmosphere

- Assortment

- Price

both included in the “Space” variable

included in the Servitisation variable

Situation Moderators:

type of store, location, culture

economic climate, season,

competition/entrance

Customer

Experience (T) cognitive,

affective, social,

physical

Consumer Moderators: Goals: experiential, Task orientation,

Socio - demographics, consumer

attitudes (e.g., price sensitivity,

involvement, innovativeness)

17

The driver of the supply system: "Where are we going tonight?"

Consumption, separated from need, is a social action which is determined

culturally and gives meaning to the goods in question. More specifically, it is possible

to condense the act of consumption into three main drivers:

- Servitisation;

- Time;

- Space.

1) Servitisation

The term servitisation does not simply define an entity consisting of

physical goods and additional services, but identifies a genuine new product in

which the physical and the intangible form an indivisible union. In fact, while

this holistic vision has the importance of a descriptive synthesis, it brings with

it some problems from the point of view of the analysis of the consumption

phenomenon. We will break down the measurable drivers in a different section

of this document but for the time being we will only focus on physical goods in

the social context of AfH consumption.

Physical goods are what makes the act of consumption possible; they

turn it into a concrete entity as part of a quantitative choice which can be

described objectively. In the context of AfH consumption, however, it is

important to distinguish between generic goods, as we have defined them, and

goods identified by a brand. If, in fact, the aim of the product is to turn a

cultural action into a physical entity, the comforting function of the brand in the

context of F&B (food and beverage) goods has the tendency to fade until it no

longer makes sense. The dynamic of AfH consumption as social action which is

- the opinions of friends and relatives;

- previous experiences;

- value of the POS brand.

In this document we have considered and developed all the above aspects except for the last one. This was an almost

obligatory choice given that our research study is contextualised within the Italian situation where there is not a brand

such as Starbucks, which is strong enough to influence the choice of POS.

Finally, we completed the model by adding a further time variable, T+1, in order to underline that Customer

Experience continues even once you leave the POS, and is associated with memories that go beyond the

simple act of consumption itself. This aspect should be stressed because it highlights the interactivity of the

cognitive processes of Customer Experience which make it, on the one hand, a phenomenon that cannot

be attributed to a specific category of consumers and, on the other hand, an experience influenced by

social contexts and not necessarily by professional ones.

18

inadvertently stimulated by the physical goods, makes the product anonymous.

This phenomenon, which is self-evident in draught-dispensed products (so-

called draught beverages), is even more evident when you think of the act of

transforming demand into something material, which, at best, identifies an

undefined category of product or situation (a beer or an aperitif) and hardly

ever applies to a specific brand.

In order to conduct a more complete research study, we should cite a few

examples in which the brand has become synonymous with an entire product category

or a consumption situation (e.g. Crodino for a non-alcoholic aperitif, Spritz for an

alcoholic aperitif, or Coca Cola for a soft drink), turning a non-specific intention into a

specific request. However, due to its pervasiveness, the contextualisation of the brand

has lost its intrinsic brand identity and, therefore, could be interpreted more as a loss

of brand value, which is, however, an issue for the manufacturer who thus sees the

unwitting dispersal of the money spent on promotion, rather than as a way of

branding the consumption situation.

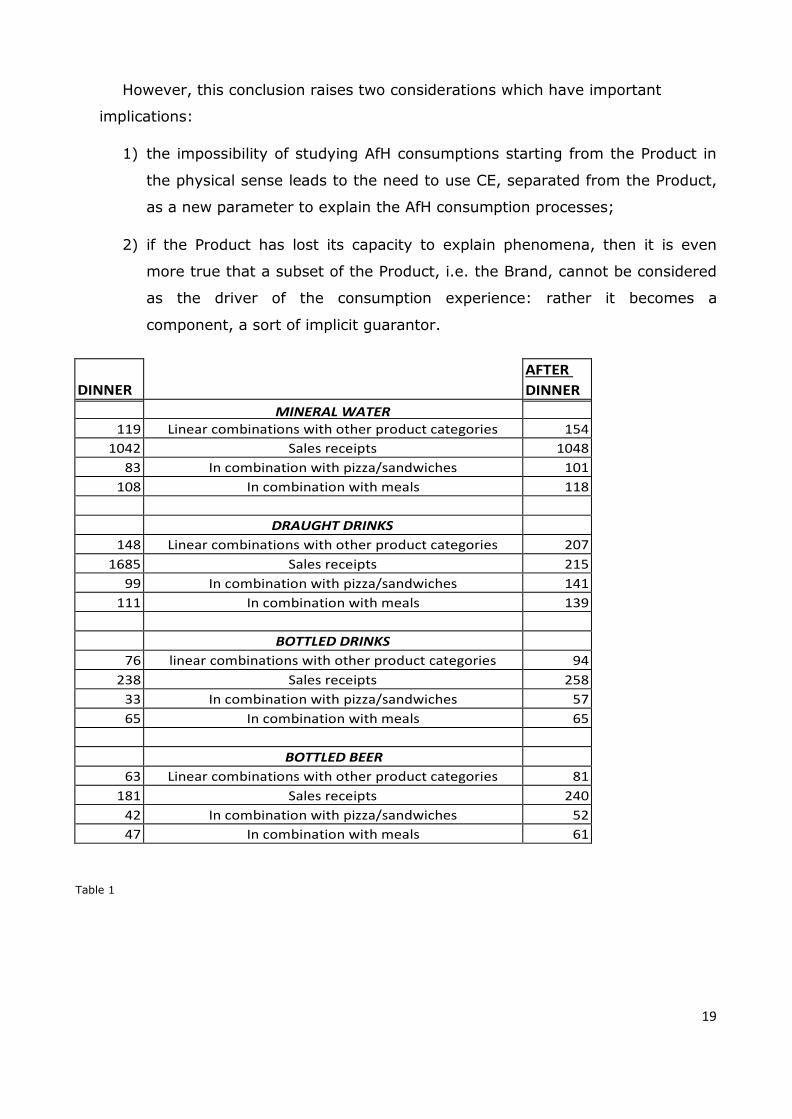

The above is shown in the data featured in table 1). Assuming that at

least one type of drink should always appear at least once on a sales receipt, for the

obvious reason that you do not eat without drinking, while you can drink without

eating, we analysed the Food/Beverage linear combinations. The analysis showed

that:

1) a preferred combination does NOT exist. On the contrary, food and beverages

are totally unrelated;

2) the Food/Beverage combination, in the Italian situation, is a genuine “food

diphthong”, subject to personal rules and dependent on the fleeting moment of

the experiential context.

The conclusions resulting from the above data suggest that in AfH F&B

consumption there are no rules allowing us to determine that the consumer's

choice of a drink is linked to a specific food in a given context; a context that, it

should be emphasised, apart from the excessive number of linear combinations,

easily exceeds the number of the consumption situations analysed.

19

However, this conclusion raises two considerations which have important

implications:

1) the impossibility of studying AfH consumptions starting from the Product in

the physical sense leads to the need to use CE, separated from the Product,

as a new parameter to explain the AfH consumption processes;

2) if the Product has lost its capacity to explain phenomena, then it is even

more true that a subset of the Product, i.e. the Brand, cannot be considered

as the driver of the consumption experience: rather it becomes a

component, a sort of implicit guarantor.

DINNER

AFTER

DINNER

MINERAL WATER 119 Linear combinations with other product categories

erceologiche 154

1042 Sales receipts 1048

83 In combination with pizza/sandwiches 101

108 In combination with meals 118

DRAUGHT DRINKS

148 Linear combinations with other product categories merceologiche

207

1685 Sales receipts 215

99 In combination with pizza/sandwiches 141

111 In combination with meals 139

BOTTLED DRINKS

76 linear combinations with other product categories 94

238 Sales receipts 258

33 In combination with pizza/sandwiches 57

65 In combination with meals 65

BOTTLED BEER

63 Linear combinations with other product categories 81

181 Sales receipts 240

42 In combination with pizza/sandwiches 52

47 In combination with meals 61

Table 1

20

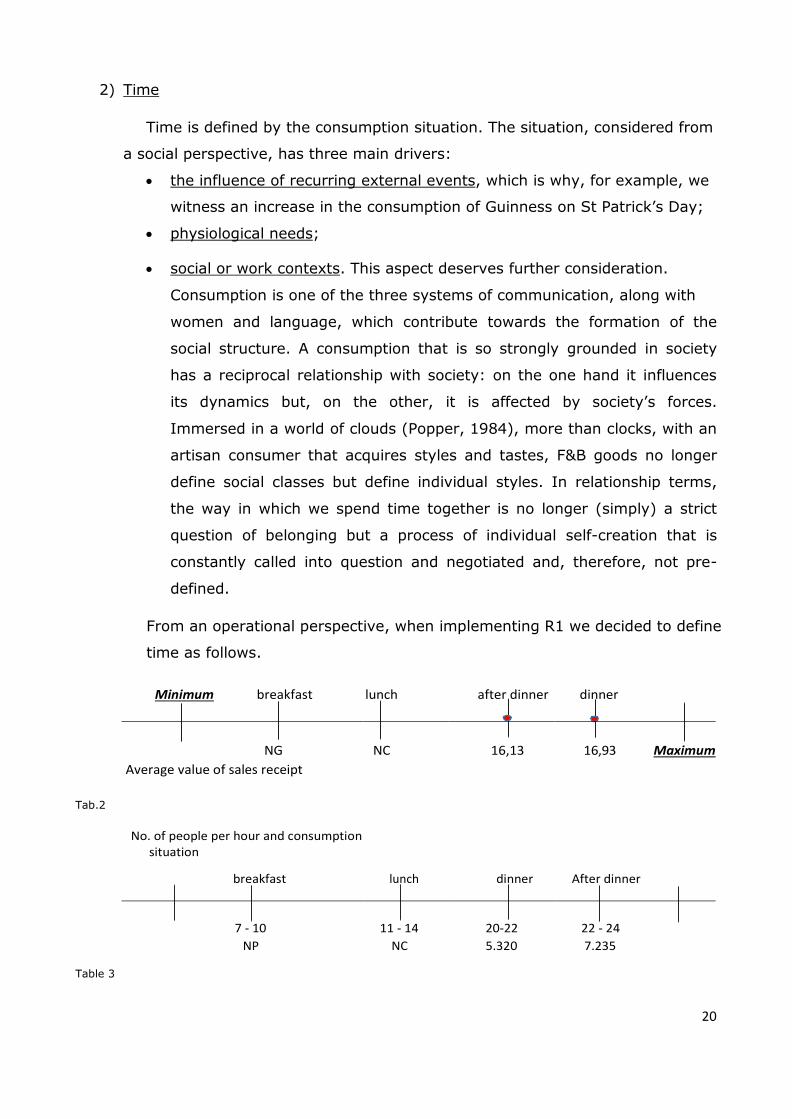

2) Time

Time is defined by the consumption situation. The situation, considered from

a social perspective, has three main drivers:

the influence of recurring external events, which is why, for example, we

witness an increase in the consumption of Guinness on St Patrick’s Day;

physiological needs;

social or work contexts. This aspect deserves further consideration.

Consumption is one of the three systems of communication, along with

women and language, which contribute towards the formation of the

social structure. A consumption that is so strongly grounded in society

has a reciprocal relationship with society: on the one hand it influences

its dynamics but, on the other, it is affected by society’s forces.

Immersed in a world of clouds (Popper, 1984), more than clocks, with an

artisan consumer that acquires styles and tastes, F&B goods no longer

define social classes but define individual styles. In relationship terms,

the way in which we spend time together is no longer (simply) a strict

question of belonging but a process of individual self-creation that is

constantly called into question and negotiated and, therefore, not pre-

defined.

From an operational perspective, when implementing R1 we decided to define

time as follows.

Minimum breakfast lunch after dinner dinner

NG

NC

16,13

16,93 Maximum

Average value of sales receipt

Tab.2

No. of people per hour and consumption situation

breakfast lunch dinner After dinner

7 - 10

11 - 14

20-22

22 - 24

NP NC 5.320 7.235

Table 3

21

3) Space

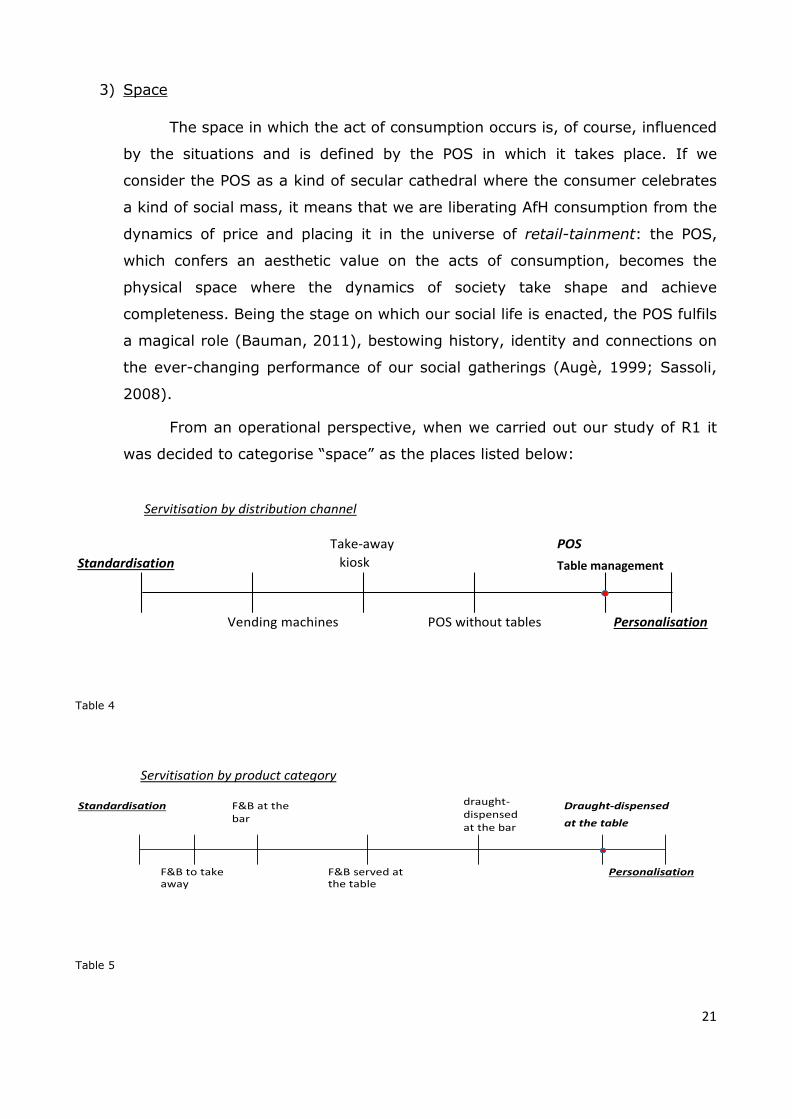

The space in which the act of consumption occurs is, of course, influenced

by the situations and is defined by the POS in which it takes place. If we

consider the POS as a kind of secular cathedral where the consumer celebrates

a kind of social mass, it means that we are liberating AfH consumption from the

dynamics of price and placing it in the universe of retail-tainment: the POS,

which confers an aesthetic value on the acts of consumption, becomes the

physical space where the dynamics of society take shape and achieve

completeness. Being the stage on which our social life is enacted, the POS fulfils

a magical role (Bauman, 2011), bestowing history, identity and connections on

the ever-changing performance of our social gatherings (Augè, 1999; Sassoli,

2008).

From an operational perspective, when we carried out our study of R1 it

was decided to categorise “space” as the places listed below:

Servitisation by distribution channel

Standardisation

Take-away

kiosk

POS

Table management

Vending machines POS without tables Personalisation

Table 4

Servitisation by product category

Standardisation F&B at the bar

draught-dispensed at the bar

Draught-dispensed

at the table

F&B to take away

F&B served at the table

Personalisation

Table 5

22

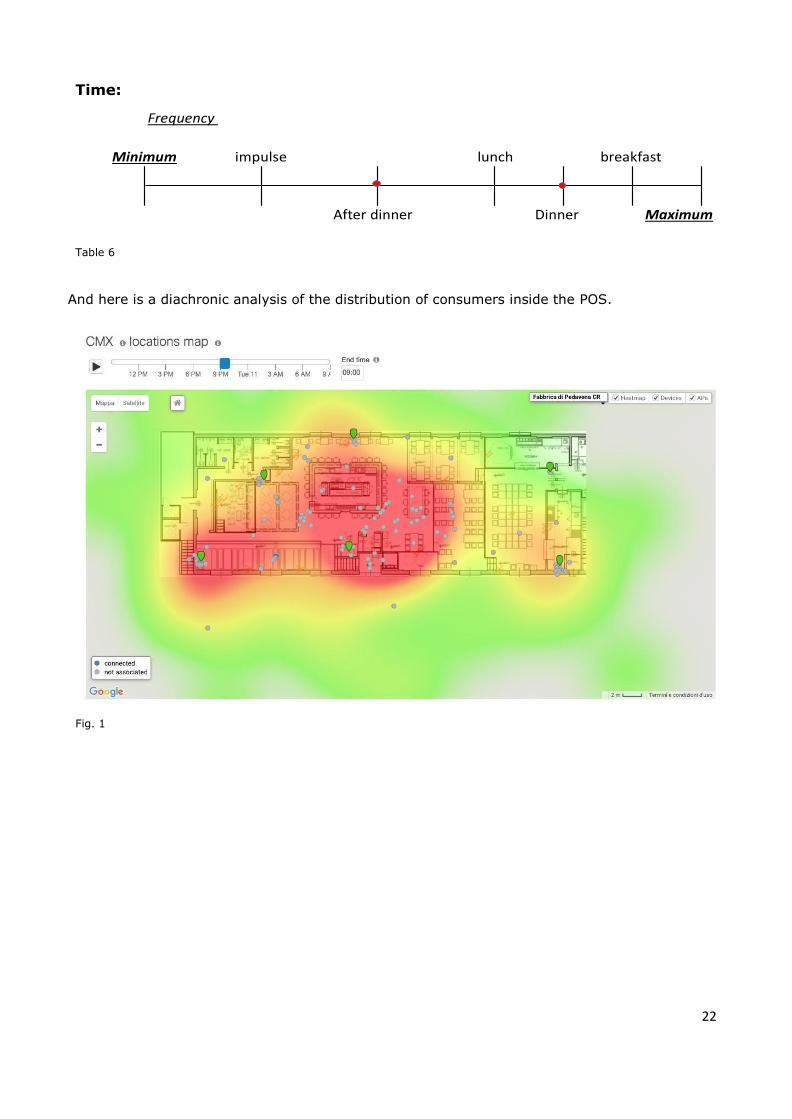

Time:

Frequency

Minimum impulse lunch breakfast

After dinner Dinner Maximum

Table 6

And here is a diachronic analysis of the distribution of consumers inside the POS.

Fig. 1

23

The driver of demand: "Who will I spend the evening with?"

If, at this stage, we refer to the definition given at the beginning and we put it in

the context of AfH consumption, we can conclude that CE is activated by the Situation,

emerges in the Context and is defined by the attitude of the Consumer. CE, therefore,

is strongly influenced by qualitative phenomena which have a pre-defined impact,

because they are in a reciprocal relationship with the experience of the Consumer. To

include this assumption in current social dynamics, however, means to undermine the

classical theories of demand segmentation. The post-modern tribalism context

(Maffesoli, 2004), in which the consumer operates and exists, prevents the attribution

of pre-conceived meaning to his or her own experience and consequently goes against

the idea of a segmentation based on a classification that, despite being multi-varied,

excludes experience. In this framework, with its socio-economic connotations, we

retrieve the difference between AfH consumption and Ah consumption: while in the

latter the same experience derives from the same quantitative data, in the former this

does not happen. AfH consumptions adhere to a new formulation of the principle of

uncertainty that goes more or less like this: it is impossible for us to understand the

quantitative data of the act of consumption or the experiences of the consumer at that

very moment; the same quantitative groups can describe different experiences and,

conversely, identical experiences can be described by different quantitative groups.

When you become aware of this particular feature of AfH consumption, you have to

recognise the impossibility of coming to a descriptive conclusion which does not take

account of experience and, consequently, to accept the need to move from a

metaphysic of the consumer to an anthropology of consumption.

The parameters used in R1 to define the variables of demand from an

operational perspective are based on the manner of consumption and the frequency of

demand. It seemed appropriate to subdivide the study into two large periods taking

into account POS location:

- T1 corresponds to the beginning of the holiday period / end of school year and

hot weather

- T2 corresponds to May, with temperatures on the rise and characterised by

regular consumers.

To facilitate the study, we decided to create a separate table for each period

24

of the week, comparing the data directly with the average of the observations. The

data is expressed in complementary index numbers to 100.

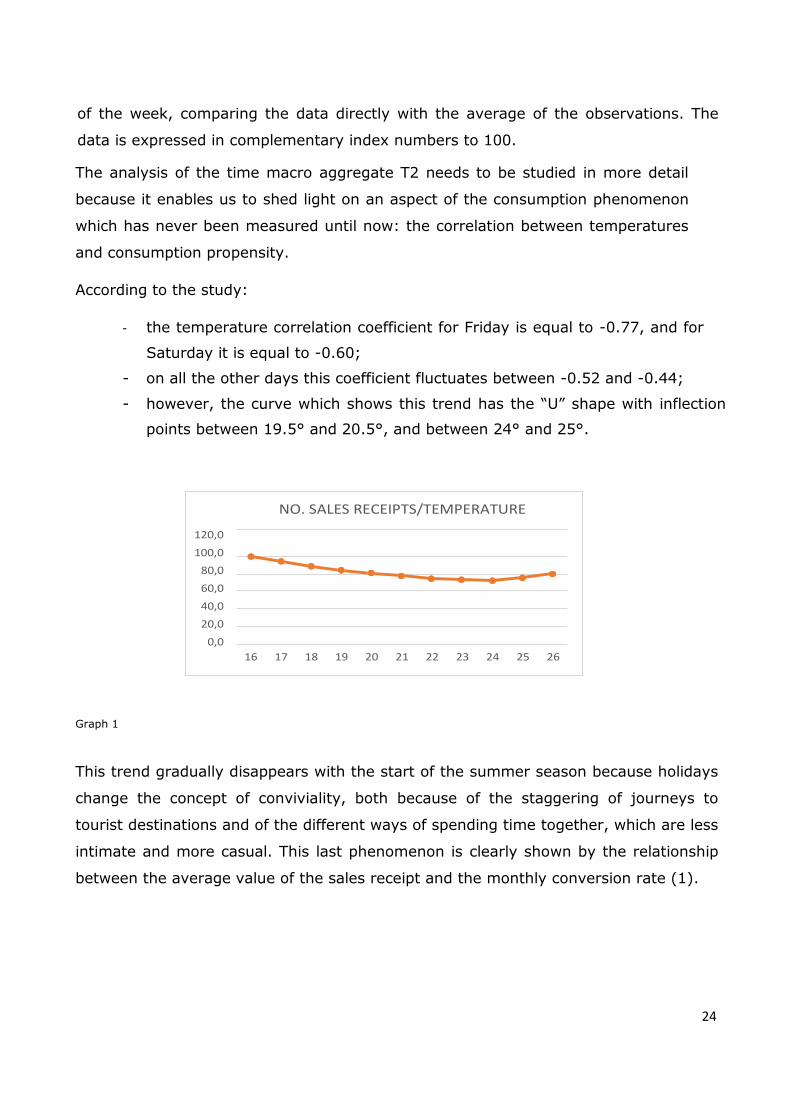

The analysis of the time macro aggregate T2 needs to be studied in more detail

because it enables us to shed light on an aspect of the consumption phenomenon

which has never been measured until now: the correlation between temperatures

and consumption propensity.

According to the study:

- the temperature correlation coefficient for Friday is equal to -0.77, and for

Saturday it is equal to -0.60;

- on all the other days this coefficient fluctuates between -0.52 and -0.44;

- however, the curve which shows this trend has the “U” shape with inflection

points between 19.5° and 20.5°, and between 24° and 25°.

Graph 1

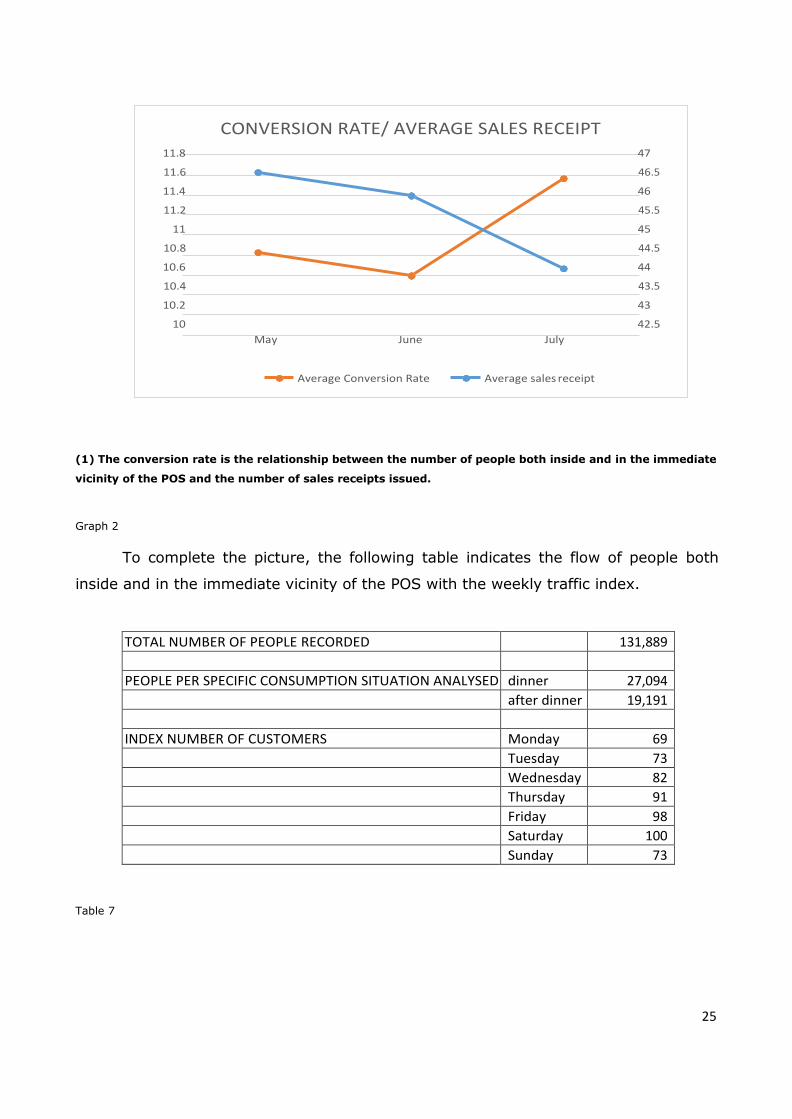

This trend gradually disappears with the start of the summer season because holidays

change the concept of conviviality, both because of the staggering of journeys to

tourist destinations and of the different ways of spending time together, which are less

intimate and more casual. This last phenomenon is clearly shown by the relationship

between the average value of the sales receipt and the monthly conversion rate (1).

NO. SALES RECEIPTS/TEMPERATURE

120,0

100,0

80,0

60,0

40,0

20,0

0,0

16 17 18 19 20 21 22 23 24 25 26

25

(1) The conversion rate is the relationship between the number of people both inside and in the immediate

vicinity of the POS and the number of sales receipts issued.

Graph 2

To complete the picture, the following table indicates the flow of people both

inside and in the immediate vicinity of the POS with the weekly traffic index.

TOTAL NUMBER OF PEOPLE RECORDED 131,889

PEOPLE PER SPECIFIC CONSUMPTION SITUATION ANALYSED dinner 27,094

after dinner 19,191

INDEX NUMBER OF CUSTOMERS Monday 69

Tuesday 73

Wednesday 82

Thursday 91

Friday 98

Saturday 100

Sunday 73

Table 7

CONVERSION RATE/ AVERAGE SALES RECEIPT 11.8 47

11.6 46.5

11.4 46

11.2 45.5

11 45

10.8 44.5

10.6 44

10.4 43.5

10.2 43

10 42.5

May June July

Average Conversion Rate Average sales receipt

26

Before presenting the T2 data here are some key points.

The first point is intended to explain the different coefficient values found

between the weekend and week days. The most plausible interpretation is related to

disposable income. In other words, if going out at weekends is a social ritual which is

almost compulsory, it is different to have to carry out a reality check on one’s

finances, which would often suggest it would be a bad idea to incur extra expenditure

despite the presence of fine weather.

Another interesting aspect is the “U” trend of the curve in Figure A. In this case

the theory suggested is that there is a late-spring temperature (of 19°-20°) which

entices you to go out into the open air rather than spend time inside a POS, except for

when it becomes too hot and unbearable and you wish to get together with other

people in an air-conditioned establishment.

The comments accompanying the following tables are based on the results from

period T2, especially for the majority of the data collected, bearing in mind what we

said earlier, and are equally valid for the month of May.

Finally, an explanatory note:

- by “at-the-bar” we mean having food or drinks without table service;

- by “table beverage” we mean having drinks only with table service;

- by “table food & beverage” we mean having food and beverages with table

service.

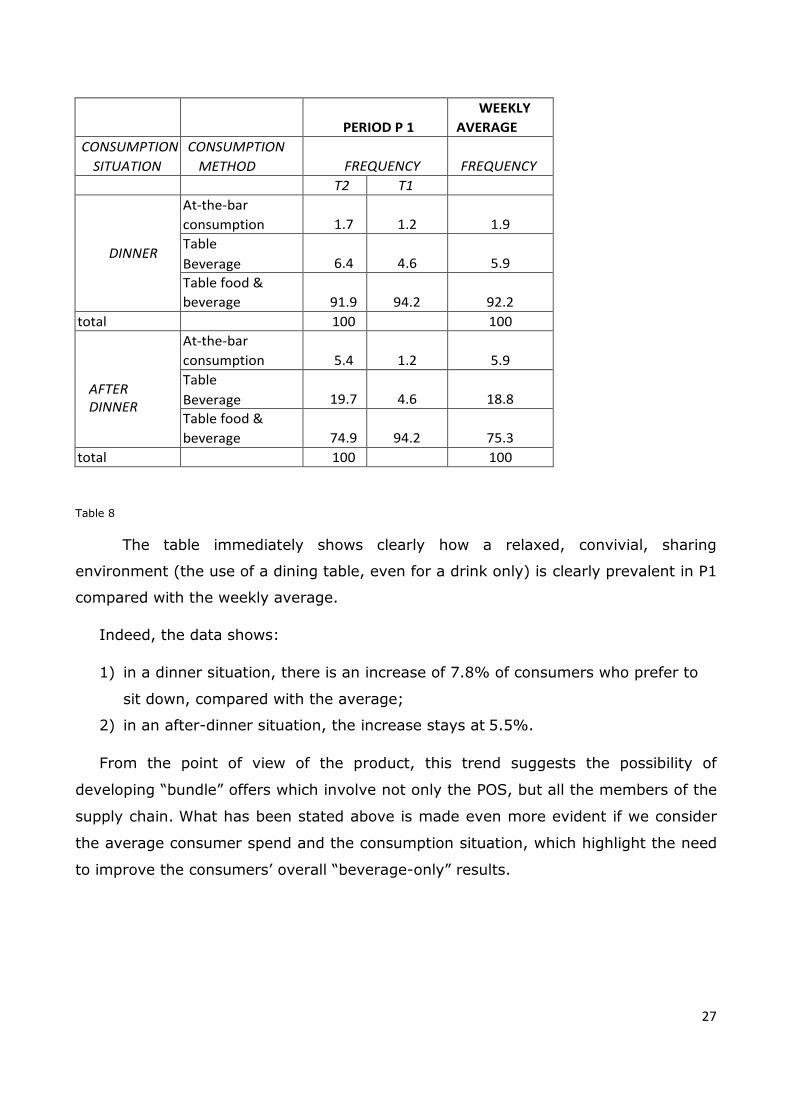

27

PERIOD P 1

WEEKLY

AVERAGE

CONSUMPTION

SITUATION

CONSUMPTION

METHOD

FREQUENCY

FREQUENCY

T2 T1

DINNER

At-the-bar

consumption

1.7

1.2

1.9

Table

Beverage

6.4

4.6

5.9

Table food &

beverage

91.9

94.2

92.2

total 100 100

AFTER DINNER

At-the-bar

consumption

5.4

1.2

5.9

Table

Beverage

19.7

4.6

18.8

Table food &

beverage

74.9

94.2

75.3

total 100 100

Table 8

The table immediately shows clearly how a relaxed, convivial, sharing

environment (the use of a dining table, even for a drink only) is clearly prevalent in P1

compared with the weekly average.

Indeed, the data shows:

1) in a dinner situation, there is an increase of 7.8% of consumers who prefer to

sit down, compared with the average;

2) in an after-dinner situation, the increase stays at 5.5%.

From the point of view of the product, this trend suggests the possibility of

developing “bundle” offers which involve not only the POS, but all the members of the

supply chain. What has been stated above is made even more evident if we consider

the average consumer spend and the consumption situation, which highlight the need

to improve the consumers’ overall “beverage-only” results.

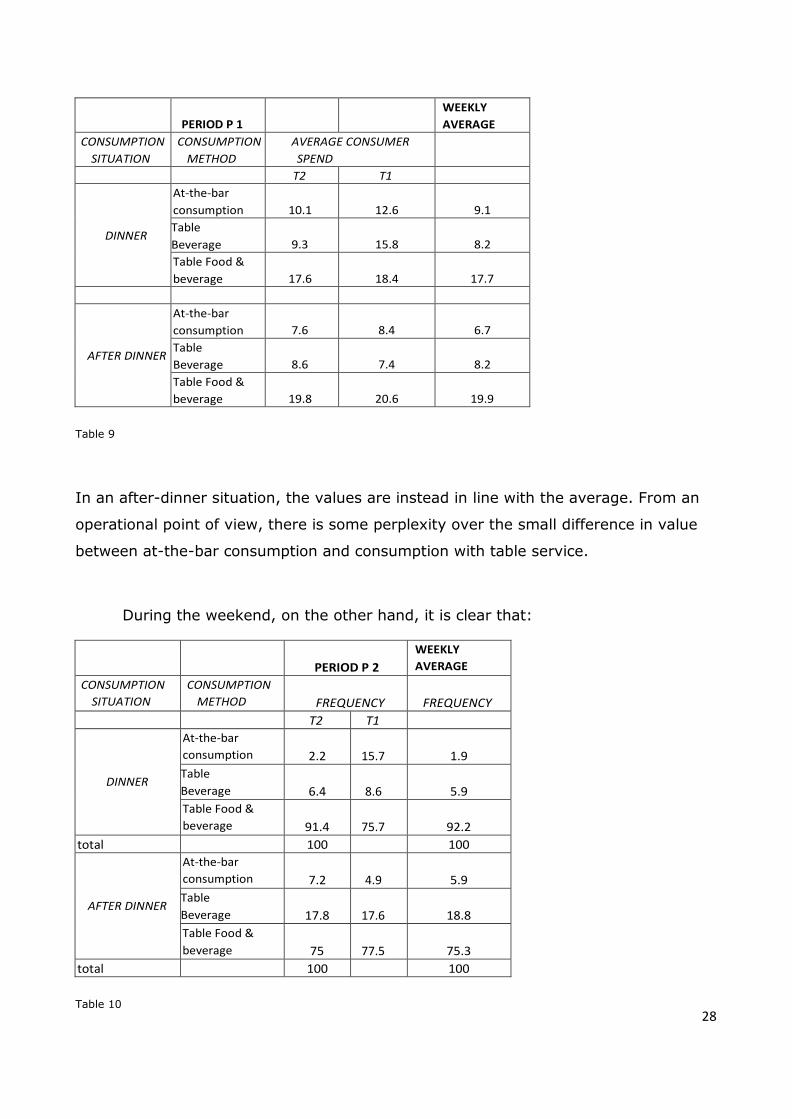

28

PERIOD P 1

WEEKLY

AVERAGE

CONSUMPTION

SITUATION

CONSUMPTION

METHOD

AVERAGE CONSUMER

SPEND

T2 T1

DINNER

At-the-bar

consumption

10.1

12.6

9.1

Table

Beverage

over

9.3

15.8

8.2

Table Food &

beverage

17.6

18.4

17.7

AFTER DINNER

At-the-bar

consumption

7.6

8.4

6.7

Table

Beverage

cover

8.6

7.4

8.2

Table Food &

beverage

19.8

20.6

19.9

Table 9

In an after-dinner situation, the values are instead in line with the average. From an

operational point of view, there is some perplexity over the small difference in value

between at-the-bar consumption and consumption with table service.

During the weekend, on the other hand, it is clear that:

PERIOD P 2

WEEKLY

AVERAGE

CONSUMPTION

SITUATION

CONSUMPTION

METHOD

FREQUENCY

FREQUENCY

T2 T1

DINNER

At-the-bar

consumption

2.2

15.7

1.9

Table

Beverage

6.4

8.6

5.9

Table Food &

beverage

91.4

75.7

92.2

total 100 100

AFTER DINNER

At-the-bar

consumption

7.2

4.9

5.9

Table

Beverage

17.8

17.6

18.8

Table Food &

beverage

75

77.5

75.3

total 100 100

Table 10

29

The weekend is still the key time for informal conviviality with significant

increases in at-the-bar consumption in both contexts. The creation of offer “bundles”

for this type of consumption is also extremely important in this case.

Particular attention should be paid to an unusual finding: at-the-bar

consumption at dinner time in Period T1. In this case it should be noted that at 21.05,

and therefore in T2, a live concert was held at the POS, which began at 20:45 and

ended at 23:00 and clearly affected the linearity of our observations.

With regard to the average consumer spend and the consumption method, data

shows the following:

PERIOD P 2

WEEKLY

AVERAGE

CONSUMPTION

SITUATION CONSUMPTION

METHOD AVERAGE CONSUMER

SPEND

T2 T1

DINNER

At-the-bar

consumption

7.5

9

9.1

Table

Beverage

7

10.2

8.2

Table food &

beverage

17.9

17.9

17.7

AFTER DINNER

At-the-bar

consumption

5.9

13.5

6.7

Table

Beverage

7.9

6.8

8.2

Table food &

beverage

20.2

17.9

19.9

Table 11

e

a low average level of expenditure by consumer on 2 out of 3 situations in T2

a separate analysis had to be carried out for Sundays, atypical days, that

fluctuate like Wendy, between the wish to have fun and the need to be.

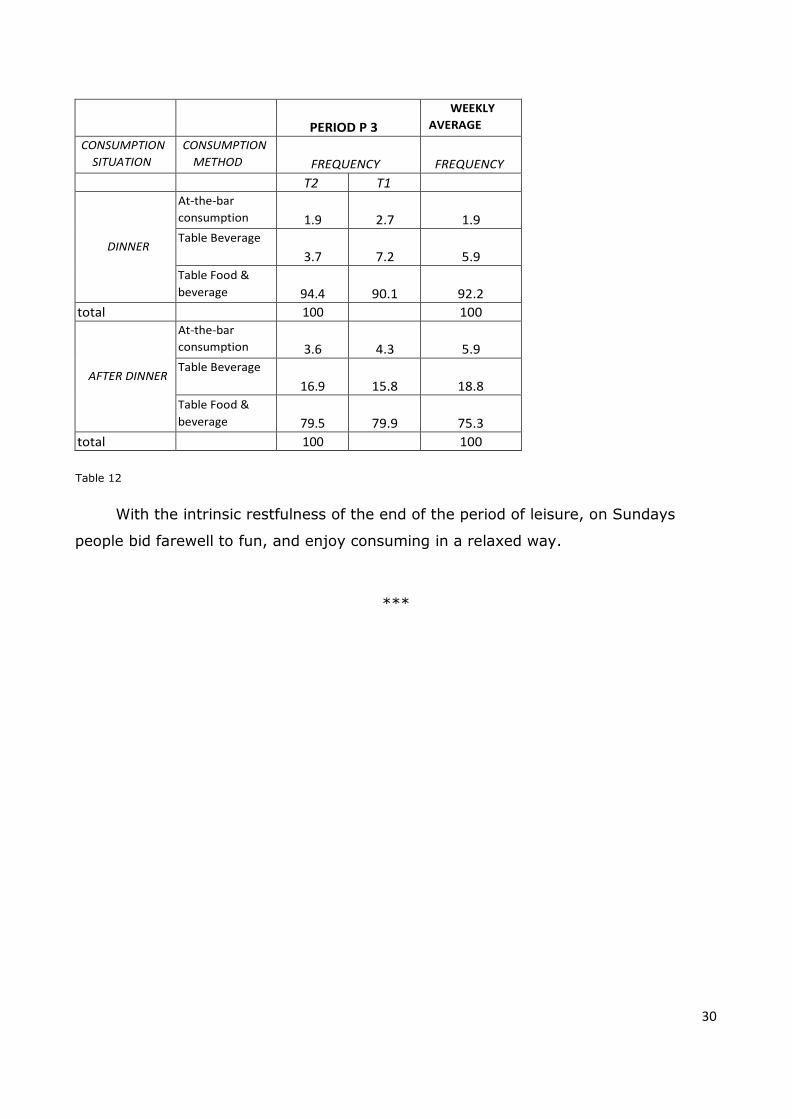

30

PERIOD P 3

WEEKLY

AVERAGE

CONSUMPTION

SITUATION CONSUMPTION

METHOD

FREQUENCY

FREQUENCY

T2 T1

DINNER

At-the-bar

consumption

1.9

2.7

1.9 Table Beverage

3.7

7.2

5.9

Table Food &

beverage

94.4

90.1

92.2

total 100 100

AFTER DINNER

At-the-bar

consumption

3.6

4.3

5.9 Table Beverage

16.9

15.8

18.8

Table Food &

beverage

79.5

79.9

75.3

total 100 100

Table 12

With the intrinsic restfulness of the end of the period of leisure, on Sundays

people bid farewell to fun, and enjoy consuming in a relaxed way.

***

31

Section Two:

Demand targeting and supply segmentation

Demand targeting: from the metaphysics of the Consumer to the anthropology

of consumption

The shift from the study of the Consumer to the study of CE

The study of the parameters that define consumer behaviour has a long and

difficult history involving constant field testing. Then again, the entire social structure

lent itself to being grouped into phenotypes and to being described using subordinate

syntactic models. Consider that when we think of the last 40 years of the 20th Century

we associate each decade with Hippies, factory workers (operai), “Travoltini” (1970s

disco goers), “Paninari” (middle-class youngsters who embraced consumerism in the

1980s), Yuppies, Hedonists and Beatniks, to mention but a few. With the development

of communication networks and the rapid rise of phonations at the expense of

metaconstructions, society also broke down and became more conformist. However,

on the research front, rather than calling into question the main principles, we

preferred to adapt our methods instead. If the creation of phenotypes was initially an

inductive process, the last decade has seen a preference towards a deductive analysis

using the previous model as our starting point. If it is true that by using an inductive

approach we run the risk of ending up like the famous turkey, it is also true that a

deductive process has an intrinsic pre-determined synthetic root. In other words, the

real danger is of making genotypes created with DNA laboratory, unless we ask

ourselves why reality does not conform to the model that has been developed. This is

the metaphysics of the Consumer; the logical consequence of an analysis of social

dynamics, which, due to constantly simplifying its complexity, has over-structured its

modelling and has ended up losing its descriptive capacity. Faced with this aberration

the suggestion is that we should go back, in the AfH consumption analysis, to an

anthropology of consumption. It is only a question of accepting the new principle of

32

uncertainty mentioned above, by defining a method of empirical research, of inductive

inspiration, which allows us to infer consumer behaviour starting from the situations

related to the contexts. It is worth remembering that these contexts do not end with

the “bill”, but “what happens to customers after they leave the restaurant is also part

of their overall experience with the restaurant” (Miao, Mattila ibid.).

In this research endeavour it is important to observe how the new technological

platforms have contributed to redeveloping the way we interact with others and with

ourselves. In fact, the Web 3.0 does not mean “Surfing the internet with a smart

phone” all over the world, but it represents the new social and syntactic connection

between people. In this sense, the digital divide is an important factor in social

discrimination; it is not the recreational implications that are the focus of our studies,

but the marginalising effects of the inability to access information. If information

constitutes the new basis of social relationships, the consumption phenomenon, as a

social act, is obviously strongly affected by this. It is in this new context that we

should focus on the need to review the ways in which we analyse consumption

phenomena.

By adopting the scenarios of the Game Theory we can address the problem as

follows. Talking about “Consumer satisfaction” means to accept both the existence of

an information deficit to the detriment of the Consumer, and almost complete

information in favour of the strongest player, in this case the industry. Clearly, in this

situation, the game needs to be defined in dynamic terms, with sequential moves by

the players, and not in a cooperative way, because it is far more advantageous for

one side. However, the increase in information and the ability to access it immediately

have changed the rules. These days we need to accept a game that favours perfect

information, because the Consumer is more informed about the Environment and the

Industry, as well as a game, that, thanks to information being available

instantaneously, is leaning towards a stable description, because the players will aim

to synchronise their moves. In this situation the most convenient way to play is to

collaborate. In fact, in the presence of reduced information asymmetries and, to an

extent, organisational asymmetries, getting along well is a far more satisfying

strategy. Then again, incorrectly, the paradigm on which the sharing economy is based

is an example: injecting trust, which is the logical requirement of collaboration, into a

supply system, means to make goods, which would otherwise be underused,

accessible.

33

In light of the above, all we can do is conclude, and this takes courage, that there

is no specific Consumer for each type of product; there is no “Type of consumer for

xxxxx”, because we can all be that type in different contexts.

The innovative significance of this conclusion, which overturns our consolidated

vision of society and its related relationships, should be investigated with the tools at

our disposal today.

And, to conclude, we should remember that all of the above is valid for analysing

the Consumption process, but not, on the other hand, for determining corporate

Communication strategies that incorporate the purchase function that, as we know

only too well, follows different rules.

Supply segmentation: between flatus vocis and commercial necessity

And then we will be like the stars drinking whiskey at Roxy Bar

If Demand segmentation has lost its meaning, we need to review the

parameters of the analysis of Supply. In other words, skipping the Consumer-Product

link, we need to understand whether a Consumer-POS Type link can exist. In this case

too, we should use empirical analysis to find the answer.

The first phenomenon is the expansion of the supply system that has

characterised every POS in the last twenty years. If, indeed, until the end of the

1990s, it was still possible to differentiate, for example, POSs where you could have

lunch from others where you could not, since the beginning of the 21st century these

distinctions have started to fade. Nowadays, most HoReCa POSs offer breakfast,

lunch, dinner and often stay open “late into the evening”. This extension of potential

consumption situations has, on the one hand, weakened the horizontal differentiation

based on the Product and, on the other hand, forced POSs to extend the range of

services they offer because “…restaurants should not be entirely driven by revenue-

maximisation and should approach impulse buying from a broader social responsibility

perspective” (Miao, Mattila ibid.).

A second aspect concerns the separation of the Product from CE. It is a typical

HoReCa phenomenon, defined as “anonymisation of the product”, which has important

consequences:

- the first one relates to the Brand which, in HoReCa, is not the driver of the

34

experience, but, at the most, is its guarantor. This implies that the Product

takes on the role of experiential facilitator rather than consumption marketer;

- the second one is that the term “Product”, in this context, indicates a

manufactured item produced by the organisational structure of the POS,

commonly referred to as “manager”;

- the third one is that if we separate the experience from the product, the latter

ends up taking on a secondary role in the dynamic of consumption. Consider

that, for example, 51% of the pizzas we eat, despite the huge number of

combinations available to us, are reduced to two: margherita and spicy salami

(Doxa, 2014). Do not believe that the solution is found in improvised, health-

related options because “…Our results show that primary food motives are a

strong predictor of impulse buying of restaurant food. However, when affect-

regulation motive is activated in a particular consumption situation, primary

food motives are overridden by affect-regulation motive and individuals’

impulse buying behaviour is predominantly driven by the powerful motivation

to feel better” (Miao, Mattila ibid.).

One should not be surprised, at this point, that the POS is chosen in a

completely unplanned way (Donlon, 1998): once again the supply system is not the

main driver of the experience. Similarly, one should not be surprised that the word of

mouth between friends, not as influencer, is the basis of advice on which POS to

patronise (Oliver, 2012).

The conclusion, just as with the analysis of Demand, is that supply

segmentation has almost entirely lost its cognitive characteristics because of the

different types of POS.

It should be stressed that, also in this case, the conclusion refers exclusively to

the study of the Consumption process and it would not be appropriate to arbitrarily

broaden its sphere. In other words, if it is true that the CE of a top model or Billionaire

is identical to that of a group of friends meeting up after dinner in a bar of a provincial

town, we cannot deny that the products they consume will be completely different.

And the fact that these products are not the drivers of the process does not mean that

we can ignore them. Consequently, if it is true that segmentation by POS type does

not help us to understand the consumption process, it is also true that it plays a

fundamental role in determining commercial operations in the field.

35

Section Three:

Conclusions

The research study presented is different from all previous similar analyses

under three crucial aspects:

1) the database analysed consists of certified documents within an objective

framework;

2) the research study was conducted in a non-collaborative context;

3) the empirical analysis was used to support a theory which, based on the most

important studies on the topic of AfH consumption, reached counter-intuitive

and, at times, original conclusions.

At this stage, we are now in a position to draw some conclusions.

From the analysis of consumption processes emerged the need to identify the

new descriptive reference parameter in CE. However, having Customer Experience

as our starting point can bring unforeseen consequences:

a) Customer Experience is detached from the product, suppressed in

Servitisation, and deeply embedded in society as a shared experience and

belongs more to the relational aspect rather than to the economic aspect.

This shift has three main consequences:

traditional Demand segmentation has suddenly lost its voice,

unable to explain consumption phenomena;

Supply segmentation no longer serves any informative purpose, as

it has been rendered worthless by the social contextualisation of

Customer Experience;

the product has become an experiential layer, giving up its role of

driver of the experience.

36

The first set of considerations, and perhaps the most important one, refers to

Demand targeting. If, on the one hand, we demonstrated the loss of cognitive value in

traditional Consumer segmentation we cannot, on the other hand, accept losing the

possibility to develop an information system capable of offering some generalisations

regarding the data collected. What we call into question, in fact, is not the principle

which is submitted to segmentation, but the parameter which is the subject of our

analysis, the Consumer, and the method applied, which is extremely deductive. That

Consumption is a social process is certainly not new. The obvious consequence is that,

as Pierce says, the Consumer-Signal is ‘something which equals someone times

something divided by certain aspects or capacities'. As long as Society was described

in terms of stratified differentiation, therefore attributable to a series of approximate

hierarchical relationships, abstraction worked, but since the end of the 1990s society

has changed. As soon as the ways of spending time together started to favour

functional criteria as opposed to hierarchical criteria, the Consumer as synecdoche of

Consumption ceased to be representative, hence the need for a new knowledge

driver: Customer Experience, to be precise. For this reason, we must now ask

ourselves how we can define a research study method of CE which is both rigorous

and operationally applicable and that delivers useful results from a corporate point of

view. The proposal, detailed in part four below, is to view the AfH F&B consumption

expressed in various “consumption situations” in turn as “experiential connections”. To

simplify the above, the situation could be as follows:

Consumption situation:

o Dinner

Experiential connection:

Stag/Hen party

Work-related

Hanging out with friends

Women’s Day.

This framework has various important implications:

a. it shifts the emphasis away from functional characteristics, the dinner, to

experiential ones, for instance “with friends”. The important difference is

that the former have a price, while the latter have a value;

37

b. the servitisation proposal is aimed at satisfying experience and, therefore,

it is necessary to define some preliminary experiential paths. In this

process the Industry’s marketing departments should be engaged in a

series of innovative, fundamentally important BTL operations (e.g. the

creation of a brand hot spot, of guided experiential paths…);

c. the development of an experiential path is NOT the preserve of a single

member of the supply chain. Therefore, it is possible to develop a home-

grown commercial and marketing policy which is dedicated to HoReCa;

d. at this point, the Consumer, whoever he or she may be, only has to

specify the experience he or she wants to have, because that will

determine his or her levels of satisfaction.

The second set of considerations refers to Supply segmentation. Although

Supply segmentation has lost its capacity to inform consumption processes, it still

retains a strong position in purely commercial operations. In other words, if it is true

that the understanding of consumption phenomena no longer uses the subdivision of

POSs by type of supply system (Day, Night, Evening Bars et alia), mainly due to the

inherent expansion of supply offered by various Commercial Concerns, it is also true

that there are entire product categories whose ideal commercial outlet is identifiable

by means of specific types of key Supply. Therefore, our proposal is to improve Supply

segmentation but restricting its use to the sphere of commercial operations where

having “boots on the ground” is fundamental.

The third set of considerations refers to the Product and, consequently, to the

Brand. From the standpoint of the product, if it is true that it loses its role as driver of

consumption experience, because it cannot be separated from a combination of

tangible and intangible services, it retains this role in the act of purchasing. Otherwise

known as Brand vulgarisation, which we explained at the beginning, although almost

inconsequential as far as Customer Experience is concerned, it plays a vitally

important role from the point of view of sales. This means that the traditional

functions of ATL Marketing play the role of “external involvement in consumption

processes”, while the sales function becomes a key factor in the management of the

SKUs.

38

The fourth consideration, instead, refers to engagement processes. If the driver

of the Consumption process, in F&B AfH contexts, is the experience, then loyalty and

Customer engagement processes are a consequence of this. This conclusion, however,

forces us to review the function of Branded Apps and intangible processes of

Consumer engagement. For this reason, we should stress that 60% of Consumers

prefer to visit (35%), or to have direct telephone communication (25%) with the

retailers themselves, relegating the other forms of communication and relationships to

insignificant levels (15% SMS, 14% e-mail and only 8% in-app messages) (MEF,

2016). This data explains the difficulty of popularising and implementing Branded

Apps and other hi-tech ways of retaining customer loyalty. In other words, we can

argue that the role of Branded Apps, and similar things, is secondary to, and not

determined by, previous personal experience. Inverting this sequence has given the

practises of Consumer engagement a role which does not suit their purpose, which is

to consolidate an experience that a person has already had, and not to try to persuade

them to try something out, as happens all too often.

The last consideration is strictly operational: using a consumption situation, rather

than the individual POSs, as reference, and Customer Experience, rather than the

single SKUs, as the focus of our study, enables us to increase both the quantity of

data to be processed and the population sample, all of which favours transparency

and reduces costs. In the Italian context, generally speaking, a sample of 300 POSs

would be sufficient to describe and draw conclusions from the results of the Customer

Experience analysis for the various consumption situations.

The methodological approach proposed below which, in the context of this study,

represents an innovation, and expands the scope of the functional analysis to all the

stages of the supply chain. It improves and reshapes the relationship between, on the

one hand, Industry and Distribution, giving the latter the role of the supply hub and

the management of futures relating to consumption (brand voucher) and information

(consortium management of virtual market places) and, on the other hand, between

Distributor and POS, giving the former the task of listening to its customers’ pulses,

freeing itself from its obsession with cardboard boxes, and acknowledging the role of

the latter as Market nerve ending.

Finally, we need to determine who should be responsible for implementing this new

form of Market research; and who should facilitate these new information services.

Once again, the key player should be the Distributor, directly or through Category

39

aggregations. And once again, the challenge is not to finish in second place: either

you win, in which case all the Sector dynamics become the property of Distribution, or

you lose, and Distribution will continue “to exist because there is Industry”, to

paraphrase the definition of Beverage Distributor given by a Distribution business

woman.

***

40

Section Four:

A methodological approach to analysing the HoReCa Market

Leaving behind the negative side of the case, it is essential that we try to

propose some solutions. If, indeed, the Industry is intended to start developing an

original, authentic Distribution Channel policy for HoReCa, it should be provided with

the necessary cognitive tools.

The study model we propose is intended to be used by all the members of the

supply chain. Therefore, the total number of parameters to be analysed is modular

and depends on the phenomenon that is the subject of our analysis, on who carries

out the analysis, and on the purposes of the analysis. The research process consists of

a two-track analysis:

1) contextualised measurement of CE, which as such is useful to all the members

of the supply chain;

2) detailed economic, or simply cognitive analyses, that are relevant to one or

more specific commercial bodies. In other words, the total number of

parameters proposed and the methods employed to describe them can be used

by the manager of the POS to manage his/her supply system, by the Beverage

Distributor to assess its own market and by the Industry to draw attention to

new consumer trends.

Having written off both the efficacy of Demand segmentation, and the cognitive

capability of Supply subdivision means starting again from CE. At this stage we can

only determine the parameters that, by implication, allow us to measure consumption

experience as much as possible from a quantitative perspective.

Analysing Consumption by type of experience, from a methodological

perspective, means:

41

1) to identify precise consumption situations, for example:

a. Breakfast

b. Aperitif

c. Lunch

d. Impulse

e. Pre-dinner drink

f. Dinner after dinner

2) to segment consumption situations by type of experience, for example:

a. Work-related event,

b. Being with friends,

c. Stag/Hen party,

d. Free burp.

e. ………….

In this research study we did not attempt to identify the type of experience but

limited ourselves to analysing consumption situations. This was mainly due to the

need to verify the new research methods and the parameters that were becoming

apparent.

From an operational perspective, on the other hand, this means working with

significantly smaller data samples compared with traditional quantitative statistical

analysis. In the Italian context, for example, the sample could be limited to no more

than 300 POSs across the country, which has cost benefits.

By defining the boundaries of our study in this way, the advantages of involving

all the members of the HoReCa supply chain become obvious:

1) the Industry can intervene in Consumer experience through BTL marketing

initiatives in which the Brand is implicitly chosen according to the

servitisation;

2) the Distributor becomes a facilitating platform of information services;

3) the Manager “modifies” the appearance of his/her own business according to

experiential considerations, cheaply and in a way that can be easily

changed, rather than making logistical or architectural changes at an

unacceptable cost.

42

Operational definition of Supply parameters

The aim of this section of the document is to identify the objective parameters,

defined in quantitative terms, in order to enable us to analyse the drivers of the value

of AfH Consumption phenomena. The parameters we will deal with are:

- Supply parameters:

o Servitisation;

o Time;

o Space;

- Demand parameters:

o Consumption situation;

o Experiential methods.

Servitisation:

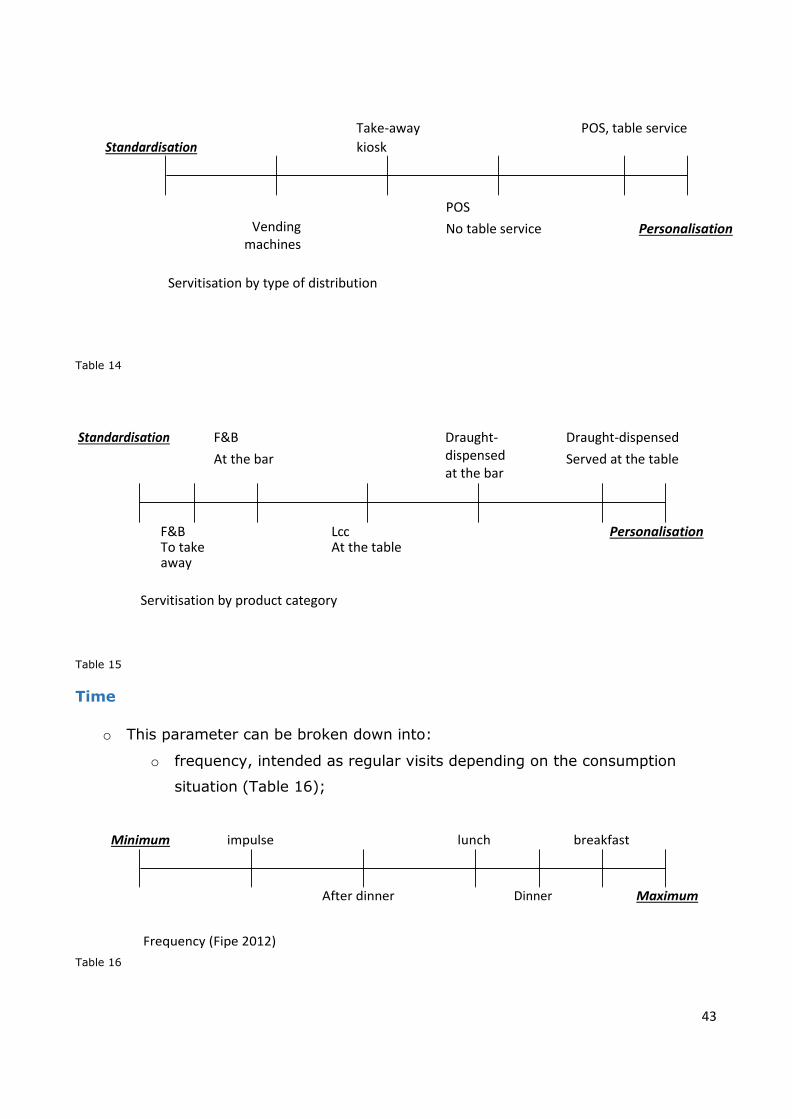

o In AfH Consumption, more than in any other sphere, the product must be

redefined in terms of “servitisation”, where the term indicates the inseparable

aggregate of goods and all of their related services. This relationship is as

strong as it is susceptible to a separate analysis. It is strong because imagining

AfH consumption broken down into its physical and intangible components is,

from the standpoint of understanding the phenomenon, little more than an

intellectual abstraction; susceptible to a separate analysis because it is possible

to identify the components and use them as proxy for the measurement of

value. Identifying these proxies is the first step towards objectifying the drivers

of the value of AfH Consumption. To illustrate this, the data within which we

place the different distributive forms (Tab.14) and the product categories

(Fig.2) can be defined in terms of “standardisation” and “personalisation”. The

driver that moves the parameter along the axis is the organisational structure

of the supply system. Such distinctions account for the different service

contents in relation to the type of distribution and the product category under

consideration.

43

Standardisation

Take-away

kiosk

POS, table service

Vending

machines

POS

No table service Personalisation

Servitisation by type of distribution

Table 14

Standardisation F&B

At the bar

Draught-dispensed at the bar

Draught-dispensed

Served at the table

F&B To take away

Lcc At the table

Personalisation

Servitisation by product category

Table 15

Time

o This parameter can be broken down into:

o frequency, intended as regular visits depending on the consumption

situation (Table 16);

Minimum impulse lunch breakfast

After dinner

Frequency (Fipe 2012)

Table 16

Dinner Maximum

44

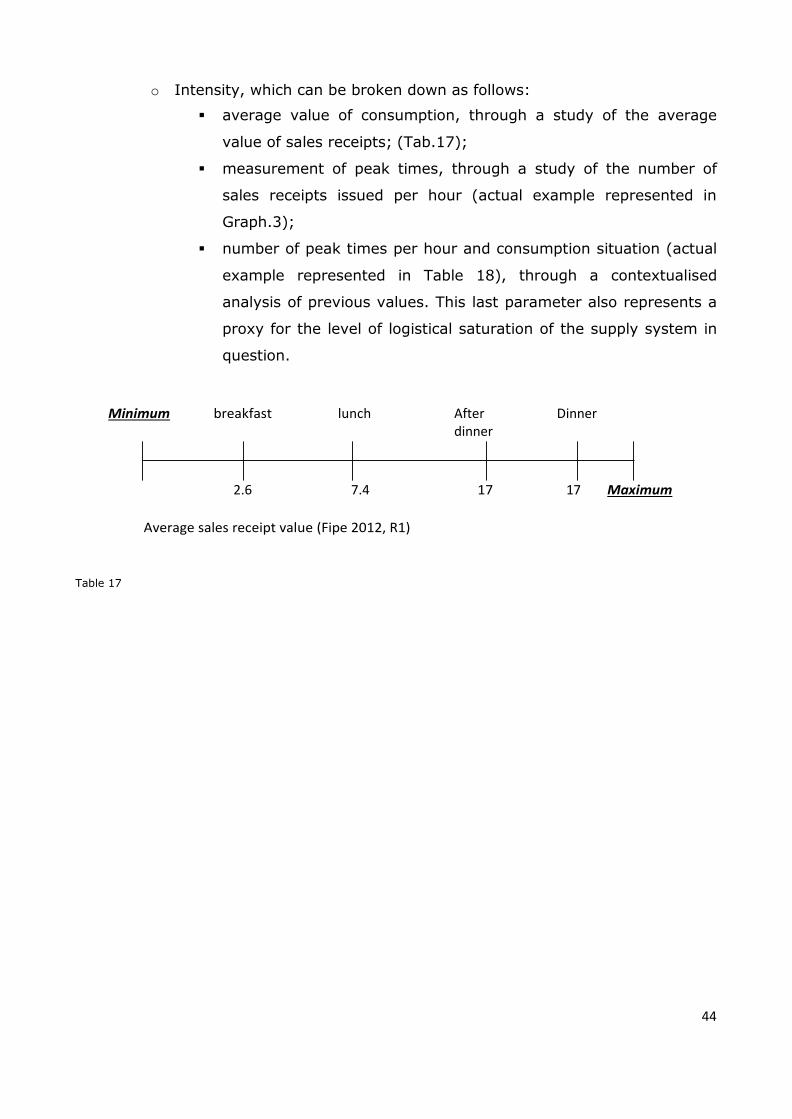

o Intensity, which can be broken down as follows:

average value of consumption, through a study of the average

value of sales receipts; (Tab.17);

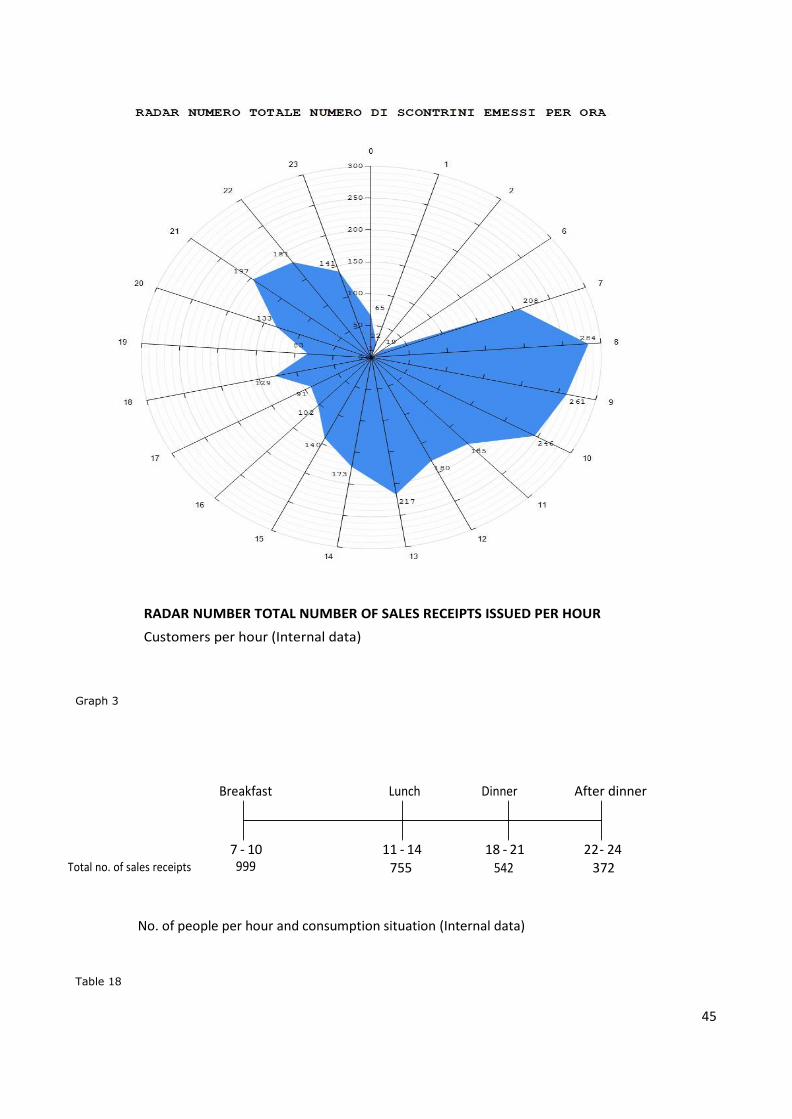

measurement of peak times, through a study of the number of

sales receipts issued per hour (actual example represented in

Graph.3);

number of peak times per hour and consumption situation (actual

example represented in Table 18), through a contextualised

analysis of previous values. This last parameter also represents a

proxy for the level of logistical saturation of the supply system in

question.

Minimum breakfast lunch

After dinner

Dinner

2.6 7.4 17 17 Maximum

Average sales receipt value (Fipe 2012, R1)

Table 17

45

RADAR NUMBER TOTAL NUMBER OF SALES RECEIPTS ISSUED PER HOUR

Customers per hour (Internal data)

Graph 3

Breakfast Lunch Dinner After dinner

7 - 10 11 - 14 18 - 21 22 - 24

Total no. of sales receipts 999 755 542 372

No. of people per hour and consumption situation (Internal data)

Table 18

46

This analysis allows us:

to objectify some proxies for evaluating the importance of the

consumption contexts;

to measure and define concrete opportunities to manage the peak times

and visits to the POSs. Indeed, considering the products and the

techniques used to deliver the service deduced from sales receipts, and

the analysis of standard delivery peak times, it is possible to determine

the workload that is effectively achievable by the organisation in any

given period of time.

Space

o The final driver of the supply system generally corresponds to the POS. In