Embed Size (px)

Citation preview

China Li-ion Battery E-News: instant news updates and analysis of the

latest policy, market dynamics, technology, company moves, and more.

Market Data: comprehensive data on a

target product - prices, producers, consumption, etc.

Company Profile Full Report

China and the global Li-ion battery market

Rise of the alternative energy vehicle market and China’s L-ion battery market

Li-ion battery materials industry

A three-horse race between China, Japan and South Korea

In 2013, China, Japan and South Korea

accounted for about 93% of total global

output of Li-ion batteries.

From 2003–2013, global Li-ion battery

industry revenues increased from

USD5.31 billion to USD27.55 billion, with

a CAGR of 17.89%.

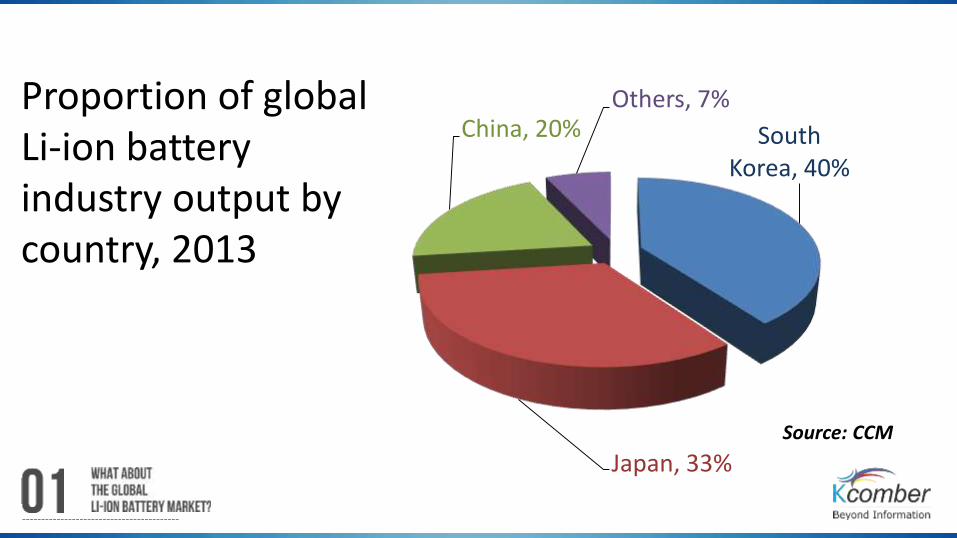

Proportion of globalLi-ion battery industry output by country, 2013

South Korea, 40%

Japan, 33%

China, 20%Others, 7%

Source: CCM

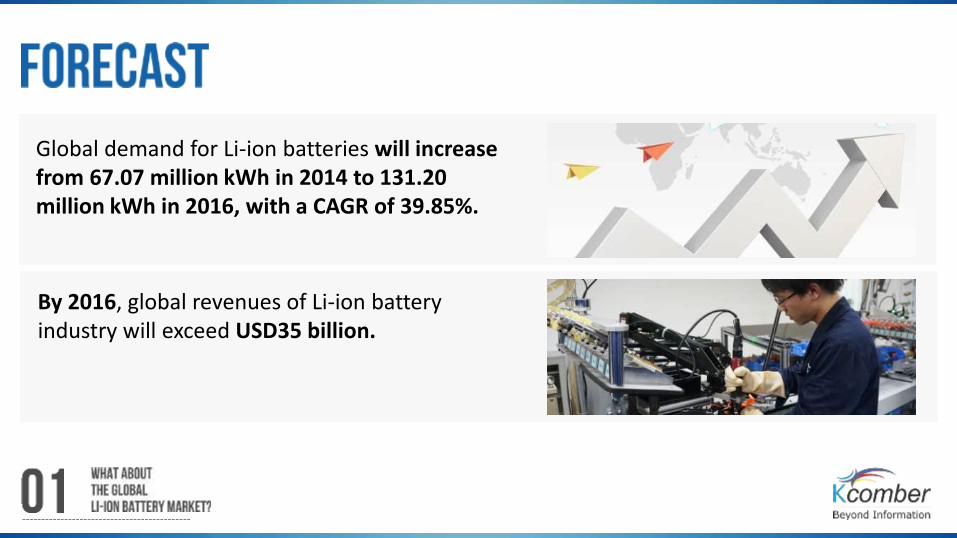

Global demand for Li-ion batteries will increase from 67.07 million kWh in 2014 to 131.20 million kWh in 2016, with a CAGR of 39.85%.

By 2016, global revenues of Li-ion battery industry will exceed USD35 billion.

Japan’s market share is decreasing; South Korea has surpassed Japan to become the largest Li-ion battery manufacturer in the world;

China is quickening the development of its Li-ion battery industry, claiming an ever greater market share, and is expected to close the gap with Japan over the next few years.

Stronger upturn

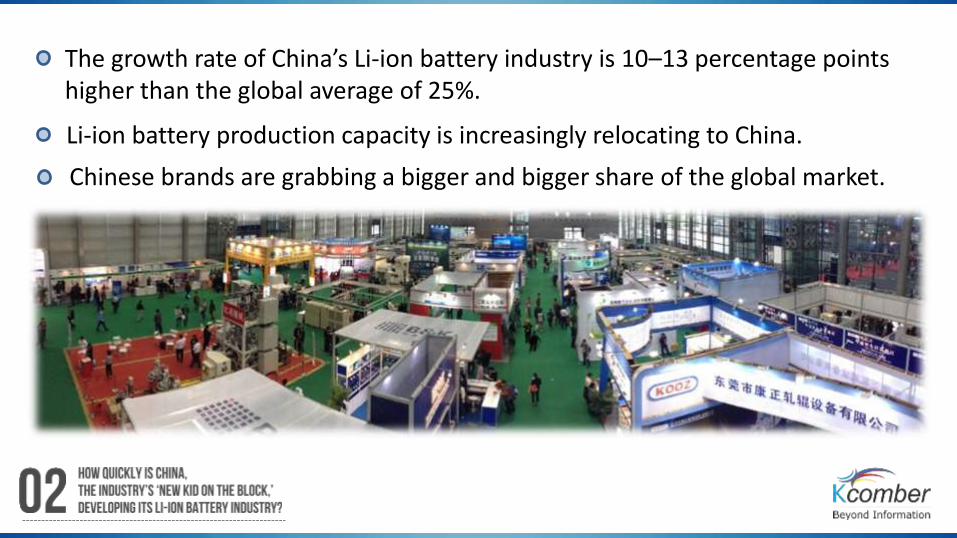

The growth rate of China’s Li-ion battery industry is 10–13 percentage points higher than the global average of 25%.

Li-ion battery production capacity is increasingly relocating to China.

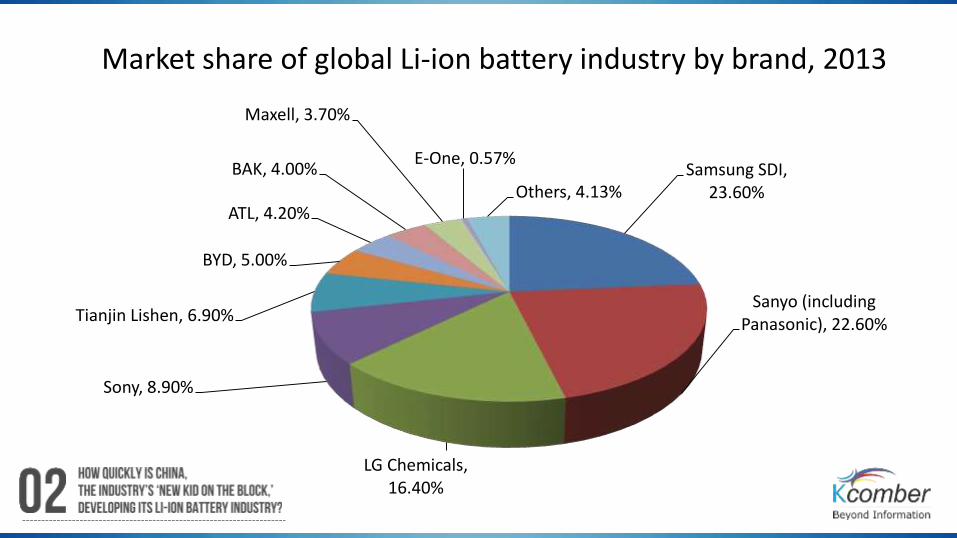

Chinese brands are grabbing a bigger and bigger share of the global market.

Market share of global Li-ion battery industry by brand, 2013

Samsung SDI, 23.60%

Sanyo (including Panasonic), 22.60%

LG Chemicals, 16.40%

Sony, 8.90%

Tianjin Lishen, 6.90%

BYD, 5.00%

ATL, 4.20%

BAK, 4.00%

Maxell, 3.70%

E-One, 0.57%

Others, 4.13%

Promising alternative energy vehicle industry

Each alternative energy vehicle requires 50 kg of cathode materials, 50 kg of electrolyte and 40 kg of anode materials

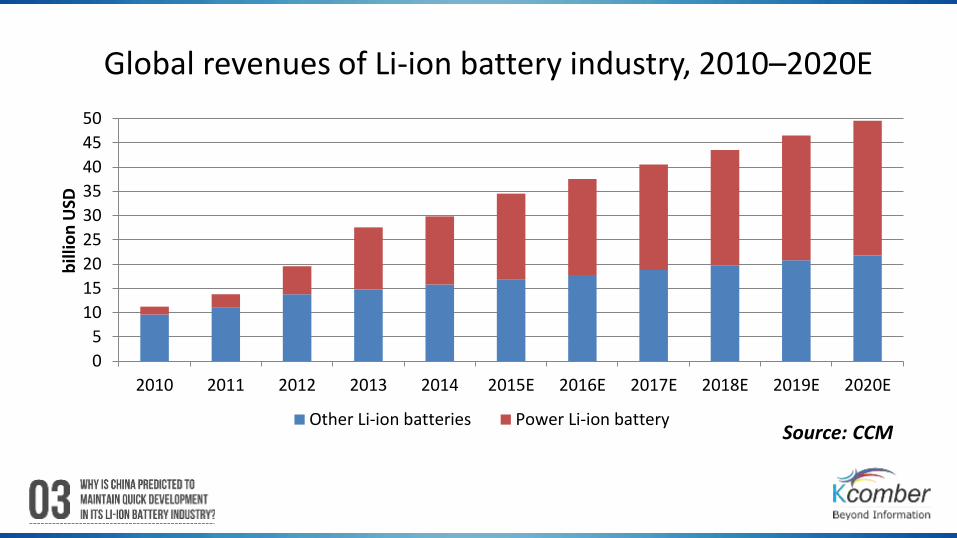

Global revenues of Li-ion battery industry, 2010–2020E

0

5

10

15

20

25

30

35

40

45

50

2010 2011 2012 2013 2014 2015E 2016E 2017E 2018E 2019E 2020E

bill

ion

USD

Other Li-ion batteries Power Li-ion batterySource: CCM

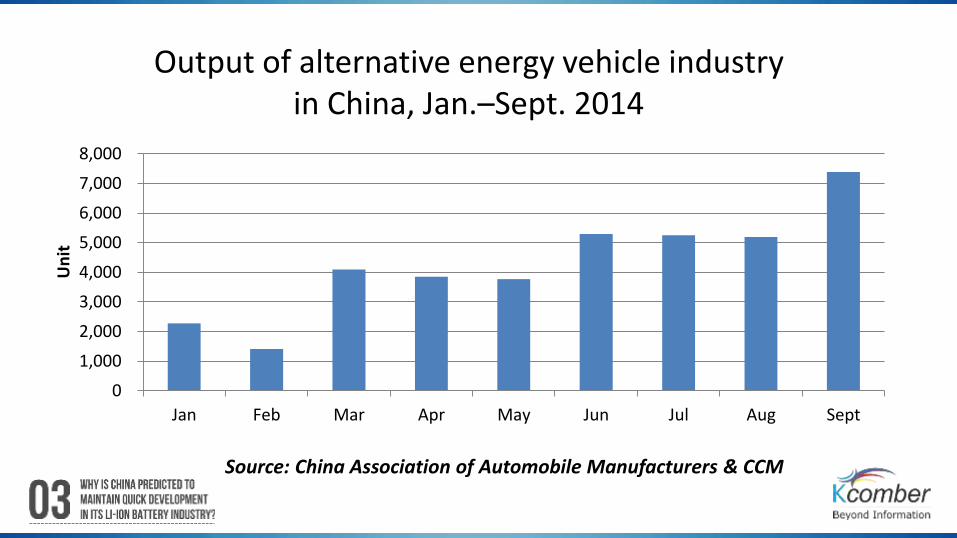

Output of alternative energy vehicle industry in China, Jan.–Sept. 2014

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Jan Feb Mar Apr May Jun Jul Aug Sept

Un

it

Source: China Association of Automobile Manufacturers & CCM

The quick development of China’s alternative energy vehicle industry cannot go forward without government support.

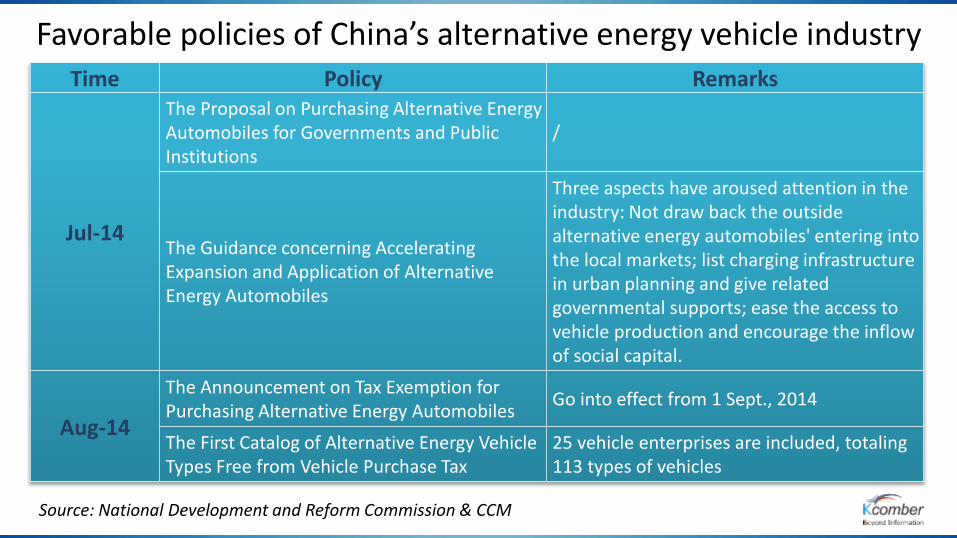

Favorable policies of China’s alternative energy vehicle industryTime Policy Remarks

Jul-14

The Proposal on Purchasing Alternative Energy Automobiles for Governments and Public Institutions

/

The Guidance concerning Accelerating Expansion and Application of Alternative Energy Automobiles

Three aspects have aroused attention in the industry: Not draw back the outside alternative energy automobiles' entering into the local markets; list charging infrastructure in urban planning and give related governmental supports; ease the access to vehicle production and encourage the inflow of social capital.

Aug-14

The Announcement on Tax Exemption for Purchasing Alternative Energy Automobiles

Go into effect from 1 Sept., 2014

The First Catalog of Alternative Energy Vehicle Types Free from Vehicle Purchase Tax

25 vehicle enterprises are included, totaling 113 types of vehicles

Source: National Development and Reform Commission & CCM

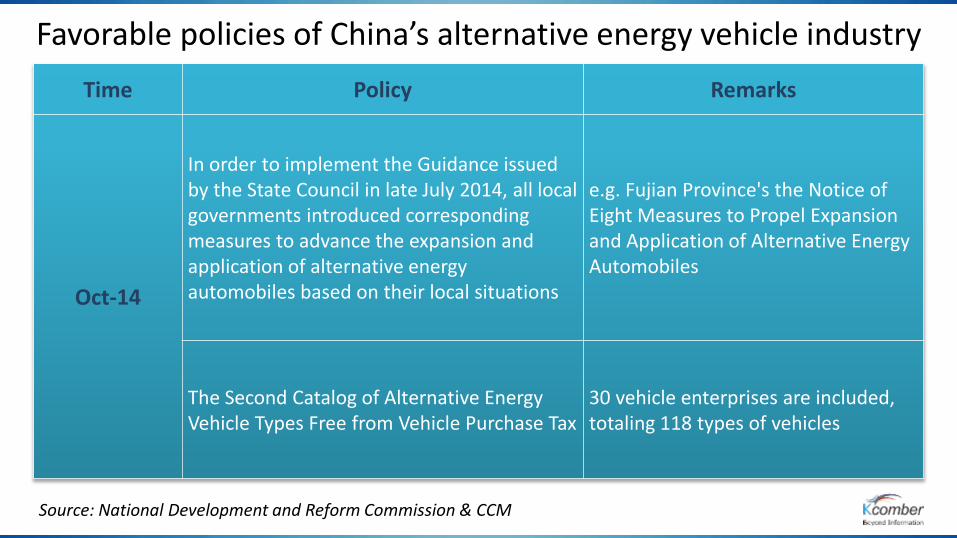

Time Policy Remarks

Oct-14

In order to implement the Guidance issued by the State Council in late July 2014, all local governments introduced corresponding measures to advance the expansion and application of alternative energy automobiles based on their local situations

e.g. Fujian Province's the Notice of Eight Measures to Propel Expansion and Application of Alternative Energy Automobiles

The Second Catalog of Alternative Energy Vehicle Types Free from Vehicle Purchase Tax

30 vehicle enterprises are included, totaling 118 types of vehicles

Favorable policies of China’s alternative energy vehicle industry

Source: National Development and Reform Commission & CCM

CCM predicts that during the Thirteenth Five-year Plan (2016–2020), China will issue more supportive policies. This indicates that China is determined to develop the alternative energy vehicle industry.

Though China’s Li-ion battery industry is driven by strong demand from downstream markets, CCM believes that the industry still lags behind Japan in many aspects, especially regarding high-end applications such as power Li-ion batteries.

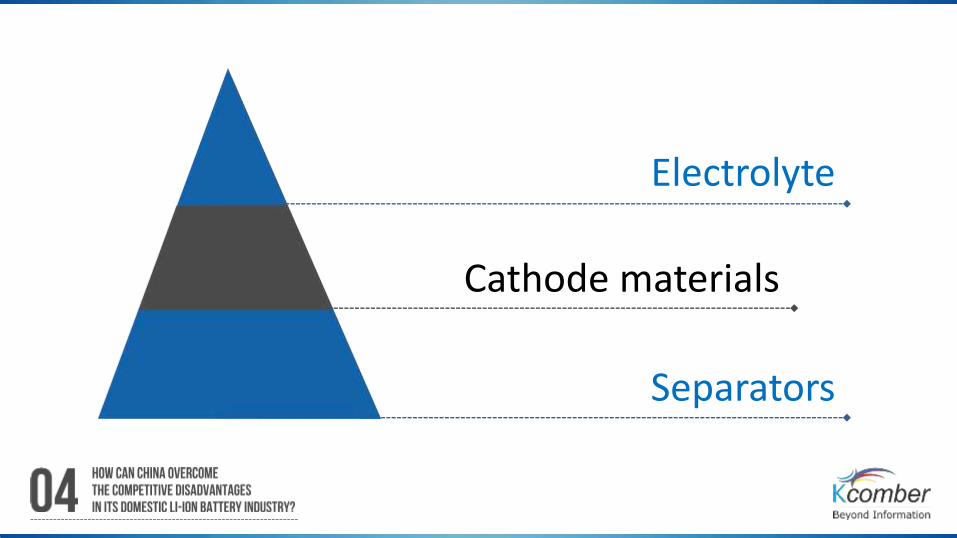

Increasing input inkey materials

Electrolyte

Cathode materials

Separators

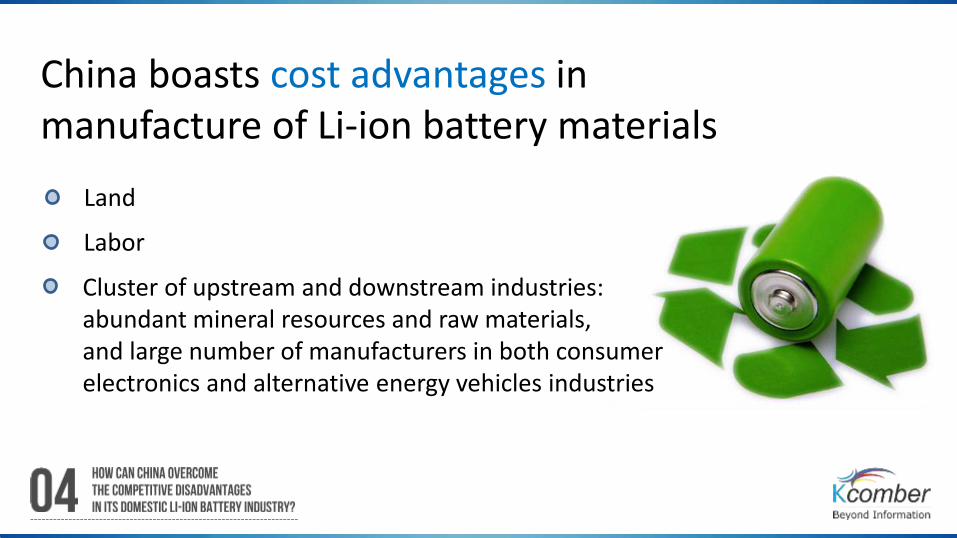

China boasts cost advantages in manufacture of Li-ion battery materials

Land

Labor

Cluster of upstream and downstream industries: abundant mineral resources and raw materials, and large number of manufacturers in both consumer electronics and alternative energy vehicles industries

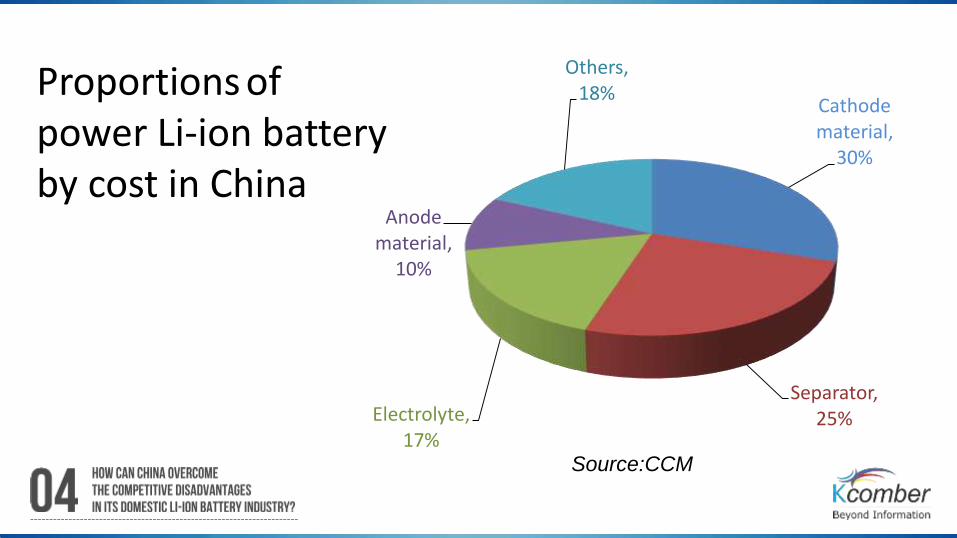

Proportions of power Li-ion battery by cost in China

Cathode material,

30%

Separator, 25%Electrolyte,

17%

Anode material,

10%

Others, 18%

Source:CCM

CCM:

As China invests more in key materials, technological obstacles will be overcome.

Based on cost advantages, the prices of related products will decline to become the cheapest on the global market.

Electrolyte: LiPF6, core raw material, sees fine industrialization.

Cathode & anode materials: Related mineral resources, like lithium, manganese, ferrum, phosphate and graphite are abundant.

Separator: The domestication is quickened.

Electrolyte

China continues its fast increase in market share, thanks to cost advantages.

In 2013, global market capacity was about 60,000 tonnes. Of this, the sales volume of Chinese enterprises reached about 31,000 tonnes. China took the first time to occupy over 50% of market shares.

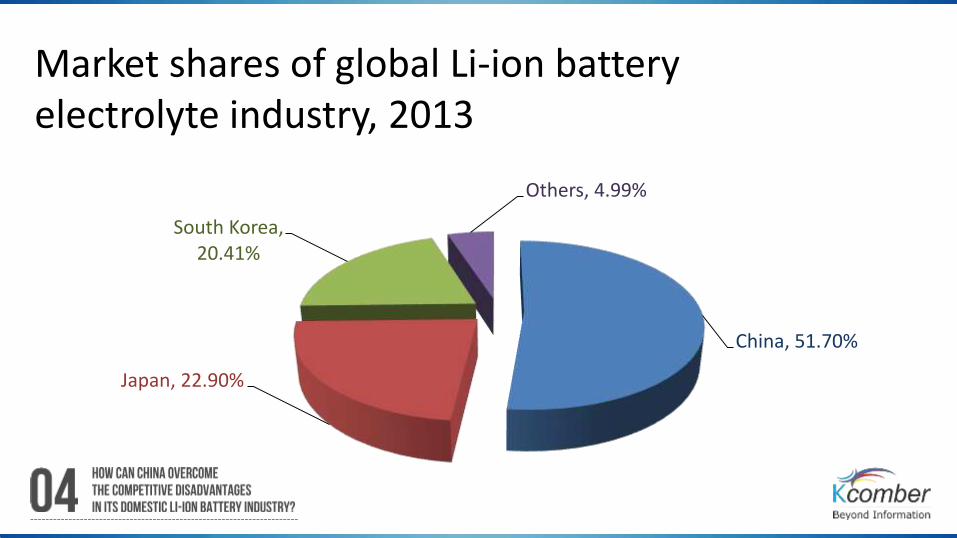

Market shares of global Li-ion battery electrolyte industry, 2013

China, 51.70%

Japan, 22.90%

South Korea, 20.41%

Others, 4.99%

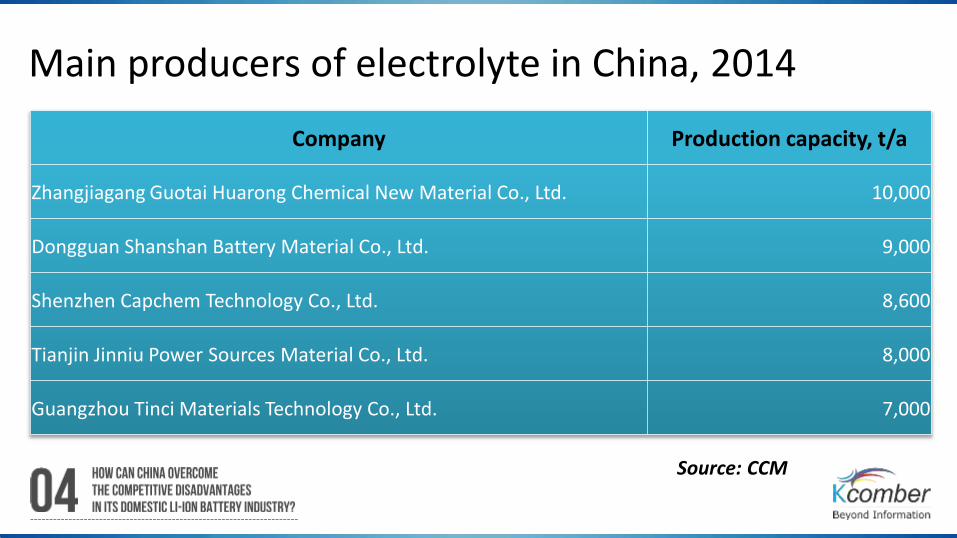

Main producers of electrolyte in China, 2014

Company Production capacity, t/a

Zhangjiagang Guotai Huarong Chemical New Material Co., Ltd. 10,000

Dongguan Shanshan Battery Material Co., Ltd. 9,000

Shenzhen Capchem Technology Co., Ltd. 8,600

Tianjin Jinniu Power Sources Material Co., Ltd. 8,000

Guangzhou Tinci Materials Technology Co., Ltd. 7,000

Source: CCM

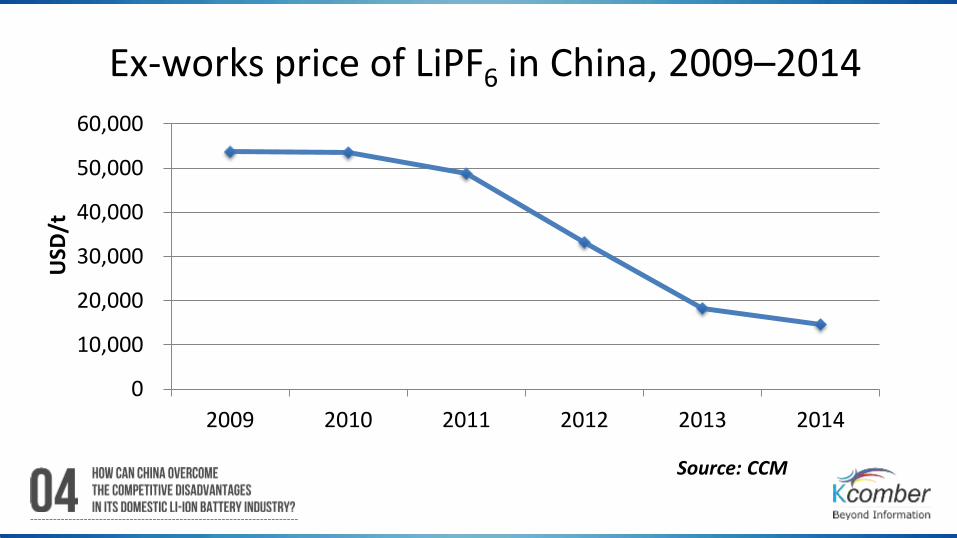

Lithium hexafluorophosphate (LiPF6 )

The global production capacity of LiPF6 reaches 12,000 t/a.

China realizes commercial production and breaks Japan’s monopoly.

Now LiPF6 prices are declining due to overcapacity.

Some small-scale Japanese factories have stopped production.

Ex-works price of LiPF6 in China, 2009–2014

0

10,000

20,000

30,000

40,000

50,000

60,000

2009 2010 2011 2012 2013 2014

USD

/t

Source: CCM

As the technology matures,China quickens LiPF6 industrialization.

In the light of cost advantages from fluorochemical raw materials, some Chinese LiPF6. enterprises make noticeable profits.

China is expected to become the world’s dominant supply base for LiPF6.

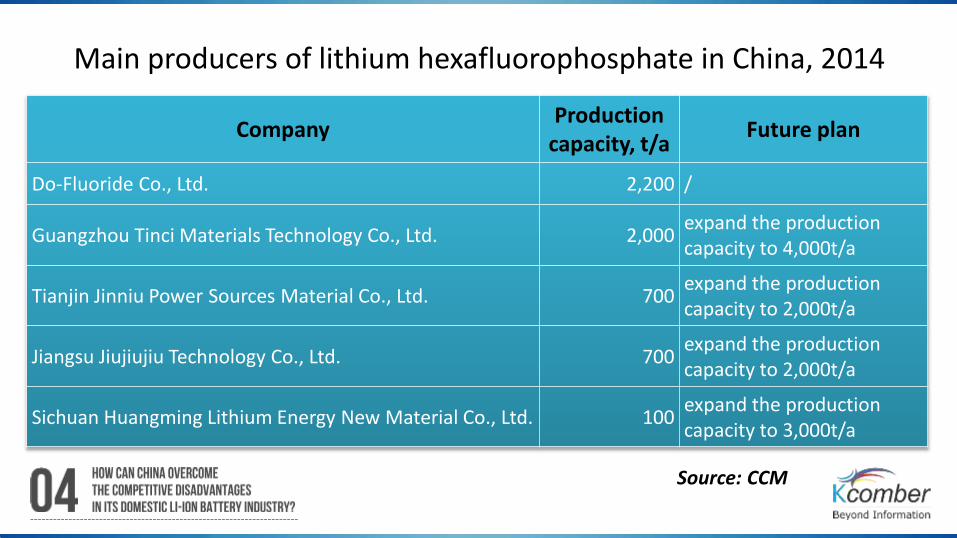

Main producers of lithium hexafluorophosphate in China, 2014

CompanyProduction

capacity, t/aFuture plan

Do-Fluoride Co., Ltd. 2,200 /

Guangzhou Tinci Materials Technology Co., Ltd. 2,000expand the production capacity to 4,000t/a

Tianjin Jinniu Power Sources Material Co., Ltd. 700expand the production capacity to 2,000t/a

Jiangsu Jiujiujiu Technology Co., Ltd. 700expand the production capacity to 2,000t/a

Sichuan Huangming Lithium Energy New Material Co., Ltd. 100expand the production capacity to 3,000t/a

Source: CCM

Cathode materials

In 2013, China’s total output of cathode materials amounted to 48,000 tonnes.

Regarding power Li-ion battery, ternary materials such as lithium nickel cobalt manganate (NCM) are expected to dominate the field.

Cathode materials

Global production capacity is increasingly relocating to China.

In 2013, China produced 49.83% of the total market share of cathode materials.

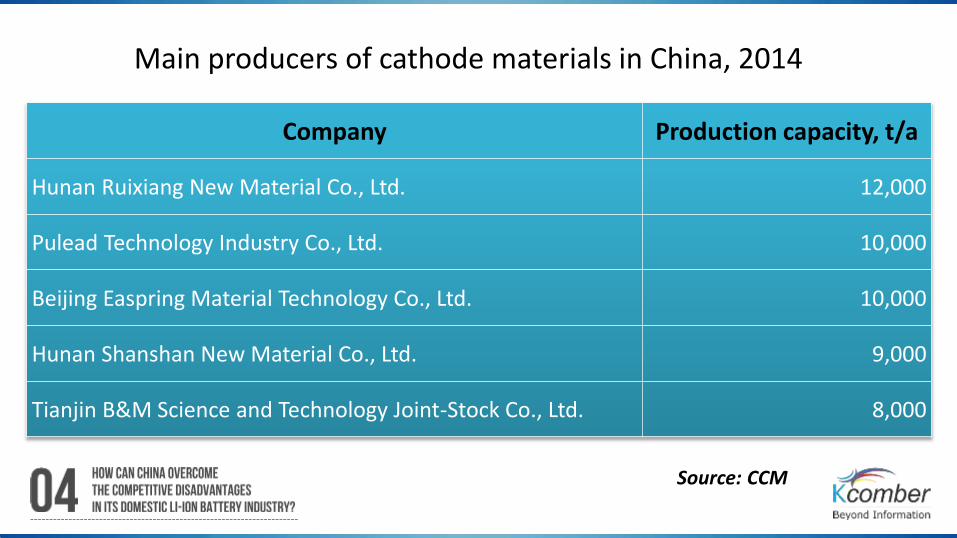

Main producers of cathode materials in China, 2014

Company Production capacity, t/a

Hunan Ruixiang New Material Co., Ltd. 12,000

Pulead Technology Industry Co., Ltd. 10,000

Beijing Easpring Material Technology Co., Ltd. 10,000

Hunan Shanshan New Material Co., Ltd. 9,000

Tianjin B&M Science and Technology Joint-Stock Co., Ltd. 8,000

Source: CCM

Separators

In 2013, China’s total output of separators reached 220 million m2.

It is expected that China will rely on a high performance to price ratio to further move up the international supply chain.

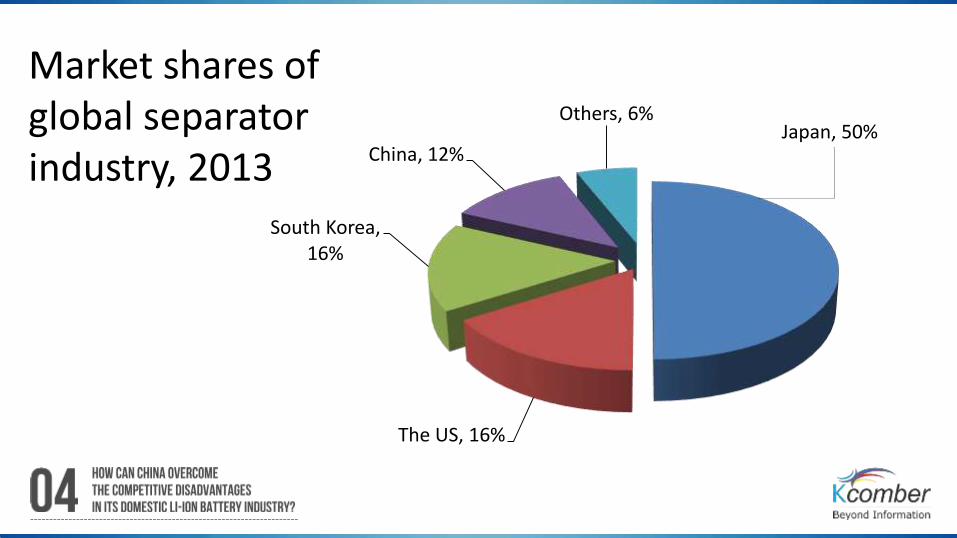

Market shares of global separator industry, 2013

Japan, 50%

The US, 16%

South Korea, 16%

China, 12%

Others, 6%

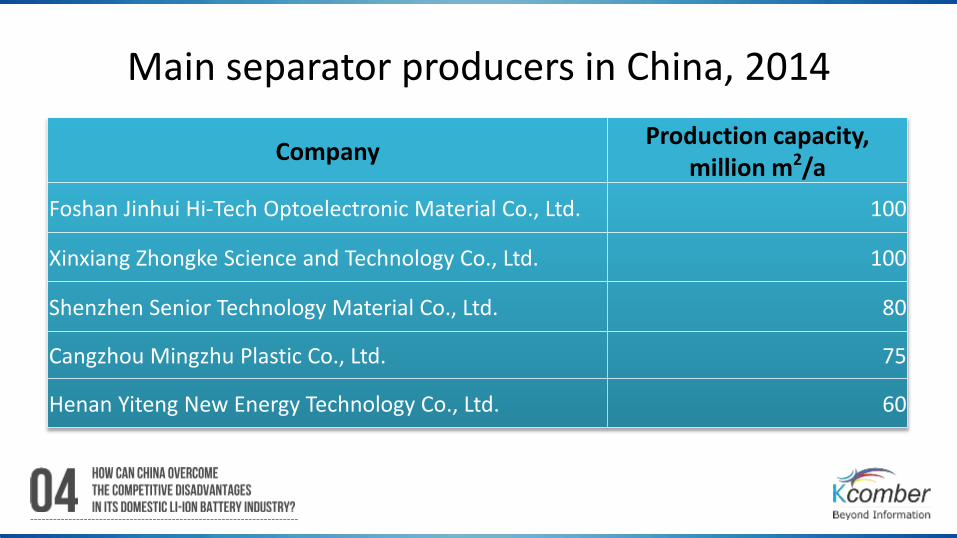

Main separator producers in China, 2014

CompanyProduction capacity,

million m2/a

Foshan Jinhui Hi-Tech Optoelectronic Material Co., Ltd. 100

Xinxiang Zhongke Science and Technology Co., Ltd. 100

Shenzhen Senior Technology Material Co., Ltd. 80

Cangzhou Mingzhu Plastic Co., Ltd. 75

Henan Yiteng New Energy Technology Co., Ltd. 60

Stimulated by active downstream markets, more and more Chinese Li-ion battery enterprises will devote themselves to developing key materials.

This will facilitate China to distinguish itself by its cost competitiveness.

All the information contained in this webinar comes from CCM’s China Li-ion Battery E-News

Much more than a typical e-news service, CCM’s E-Journal articles are the result of original research using only the most reliable data sources, which we then verify thoroughly.

Not only ‘what’, but ‘why’: at CCM, ourmission is to provide you with genuineinsight on the forces shaping the market.

Grasp the latest information

Dig up the hottest issues

Find remarkable insight

Offer support to your key strategic decisions, including material acquisitions, business development, and more

If you would like to get free sample of China Li-ion Battery E-News, please email [email protected]

![China's amazingbridges 2003v[1]](https://img.pdfslide.tips/doc/110x75/555b6bf3d8b42aae678b45df/chinas-amazingbridges-2003v1.jpg)

![China's amazing bridges 2003v[1]](https://img.pdfslide.tips/doc/110x75/555b6bf7d8b42aae678b45e1/chinas-amazing-bridges-2003v1-55849d6d9cc1c.jpg)

![China's amazing bridges_-_2003v[1]](https://img.pdfslide.tips/doc/110x75/555b6bfbd8b42aae678b45e3/chinas-amazing-bridges-2003v1-55849d6d91890.jpg)