Embed Size (px)

Citation preview

Green Giant and the Introduction of Veggie Smiles in the Market: Made to Make Life Simpler

Melanie Calabrese

Pierre-Clement Lihou

Andrew Sponable

Kristin Walsh

Professor Buff

Marketing 324, Consumer Behavior

November 31, 2016

Calabrese, Lihou, Sponable, Walsh

Table of Contents

1. Target Audience......................................................................................................................4

2. The Product.............................................................................................................................4a. Provide a brief description of the product you envision…essentially the product’s elevator pitch..............................................................................................................................................4b. Identify in detail the target audience, including demographic, psychographic, lifestyle, and geodemographic information as relevant.....................................................................................4c. What are the utilitarian and hedonistic needs that your product satisfies?..........................7d. Articulate why the target market will be attracted to your product......................................7e. Product Positioning...............................................................................................................8

a) Please indicate how your product will be positioned........................................................8b) Create a perceptual map to show how your product is perceived relative to competing products in the market...............................................................................................................9

f. What products, if any, represent direct competition or are viable substitute products to your new product?......................................................................................................................10i. Describe your product strategy...........................................................................................10

1. What are the product characteristics/features/benefits provided/need(s) satisfied?........102. As part of this step, develop a product/product package.................................................13

ii. Clearly describe your pricing strategy................................................................................151. How will you price the product? Why?...........................................................................15

iii. Clearly describe your promotion strategy for this new product......................................161. Please create one communications piece for the product (print ad, online ad, video, etc.) that reflects your message strategy.........................................................................................19

iv. Clearly describe your distribution strategy.....................................................................211. Where will you distribute the product? What distribution channels will be used? Why?

21v. How must marketing ethics and social responsibility be factored into strategic decision making for the product you are recommending?........................................................................21vi. How would you measure or determine the overall success of your marketing strategy?22

3. Conclusion..............................................................................................................................23

4. Works Cited...........................................................................................................................25

5. Summary of Responsabilities...............................................................................................27

6. Appendices.............................................................................................................................28i. Part 1...................................................................................................................................28ii. The Ad Evaluated................................................................................................................57iii. The Product Prototype.....................................................................................................59

2

Calabrese, Lihou, Sponable, Walsh

iv. The Ad Created................................................................................................................60v. The Power Point Slides.......................................................................................................61

`

3

Calabrese, Lihou, Sponable, Walsh

1. Target Audience

Our target audience is: « Families with children under 10. »

2. The Produc t

a. Provide a brief description of the product you envision…essentially the product’s elevator pitch.

Veggie Smiles are 100% vegetables made products in shape of smiley faces that your kids

will love. Available in several flavors like broccoli or carrot, and sold at several food markets

without putting a hole in your pocket. Our products will stimulate your children’s needs for

entertainment while providing them a positive experience of vegetables consumption. Our

products are aimed to change your consumption behavior toward vegetables, for both your

children and you. Veggies Smiles are not only loved by your kids, you will want to sneak a few

too!

b. Identify in detail the target audience, including demographic, psychographic, lifestyle,

and geodemographic information as relevant.

Our target audience is “Families with children under 10”. Under this denomination, we

can assume that families are made of at least two members. To find relevant and up to date

information about these families, we went on the Bureau of Labor Statistic and look for tables

corresponding to this category. The table 3413 provided us relevant demographics,

psychographics and lifestyle information.

First, the demographics. According to the consumer expenditure survey of the year 2014-

2015, there was 90,042 thousand US families with two or more people. Most of them were

earning $70,000 or more. The minimum number concerning the income is for the income

between $5,000 and $9,999: only 1,841 thousand families were in this situation. It can be

4

Calabrese, Lihou, Sponable, Walsh

explained by the fact that it is barely impossible to provide a family of two or more people with

so few resources, if we consider all the expenditures: education, transportation, food, health

insurance...From the total amount of families of 2 or more people, the children under 18 represent

an average consumer unit of 0.8. Of these families, 47% of the reference person are men, 53% are

women. Out of these gender percentages, 12% are Black or African-American, 88% are White,

Asian or of other races. 64% of the reference person got a college degree, only 3% have an

elementary degree, 33% have an high-school degree. 93% of the families own or lease at least

one car.

Second, the lifestyles and psychographics characteristics. Overall, families with two or

more people spend $63,852 on annual expenditures. These expenditures are to be divided in

different categories. The first category that interest our company the most are the expenditures on

food, and more specifically on fruits and vegetables. Overall, families spend $904 annually for

this category: the families which spend the most are the one which earn the most: those with an

income of $70,000 and more spend $1,121; the families who spend the less are still the families

who earn between $5,000 and $9,999: they spend $588 on this category annually. The fruits and

vegetables category is divided in four subcategories. The first one is Fresh Fruits: the overall

expenditure is of $330, the income range that spends the most is the one who earns $70,000 or

more ($423), the one that spends the less is the one which earns between $5,000 and $9,999

($185). The second subcategory is Fresh Vegetables: the overall expenditure is of $290, the

income range that spends the most is the one who earns $70,000 or more ($361), the one that

spends the less is the one which earns between $5,000 and $9,999 ($196). The third category is

Processed Fruits: the overall expenditure is of $127, the income range that spends the most is the

one who earns $70,000 or more ($154), the one that spends the less is the one which earns

between $10,000 and $14,999 ($81). The fourth subcategory is Processed vegetables: the overall

5

Calabrese, Lihou, Sponable, Walsh

expenditure is of $157, the income range that spends the most is the one which earns $70,000 or

more ($183), the one that spends the less is the one which earns between $5,000 and $9,999

($117). To conclude for this category, we can say that the families which earn the most are those

who consume the more fruits and vegetables, whether they are processed or not. However, it is

strange to see that families with less than $5,000 of income spend and consume more of those

products than families who earns between $5,000 and $9,999. This should be the reverse. The

second category to analyze is how those families spend their leisure time. Overall, the families

with two or more people spend $132 on reading, the income range that spends the most is the one

which earns $70,000 or more ($188), the one that spends the less is the one which earns between

$5,000 and $9,999 ($29). Also, they like to spend time entertaining: overall, the families with two

or more people spend $33 on toys, games, arts and crafts, and tricycles; the income range that

spends the most is the one which earns $70,000 or more ($47), the one that spends the less is the

one which earns between $5,000 and $9,999, because no data were reported for this category. On

other entertainments, overall, the families with two or more people spend $69, the income range

that spends the most is the one which earns $70,000 or more ($113), the one that spends the less

is the one which earns less than $5,000 ($10).

With this overview of different demographics and psychographics, we can get a closer

and more relevant look at our target audience. Our audience is well-educated, earns enough to

provide the families a decent lifestyle and consumer vegetables and fruits. Since there is no data

about the consumption of frozen vegetables, we can assume our products will help market

researchers to get some (if not count under processed found).

6

Calabrese, Lihou, Sponable, Walsh

c. What are the utilitarian and hedonistic needs that your product satisfies?

Our new product, Veggie Smiles, not only satisfies the need for hunger, but also satisfies

the need for nutrition. Veggie Smiles is a newer and healthier way to sneak vegetables into a kids

diet without them knowing, which parents will be thankful for! Instead of snacking on junk food,

Veggie Smiles are a healthier alternative that replaces the consumption of unhealthy foods that

will affect children's diets across the country. After one bite, kids will realize the not all

vegetables taste bad and find themselves not missing junk food they once loved. Our smiley face

design is a fun way to introduce vegetables to children, without giving an intimidation factor that

come from a plate full of vegetables. This non intimidating approach allows parents to feed their

children vegetables without feeling like they are forcing their kids to eat their vegetables.

d. Articulate why the target market will be attracted to your product

As stated in the first part of our project, and more specifically in the complete analysis of the

demographics, children who are aged 12 or younger consume less vegetables as they use to do

five years ago. However, we found out that children between 13 and 17 years old eat more

vegetables. This trend shows a difference in consumption of vegetables among age. This could be

because young children’s palate is not mature, but also to the fact that vegetables are not targeted

enough toward the youngest consumers. Children represent an important market: they do not

have purchasing power, but have the pester power: they push their parents to buy products they

would not buy in general. This works for toys, but also for food. Children need to be entertained,

because among utilitarian needs, playing and having fun satisfy a hedonic need. By selling

vegetables in the shape of smiley faces, children will forget about the negative network they

usually make with vegetables, and the funny feeling will get the upper hand. This is the first

7

Calabrese, Lihou, Sponable, Walsh

reason why the first part of our market (children under 10) will be attracted to our product. Once

successfully targeted and convinced, children will influence their parents’ decision making

process. At this stage, our job is to convince them too. In the first part of our project, we

presented you five different consumer attitudes toward the consumption of vegetables, that

segmented our market. Whatever the segment parents are part of, we can target them accordingly.

However, we think that Family Pleasers’ consumptions and lifestyles characteristics better fit

with our products. Finally, and according to the website About Kids Health, over $11 billion are

spent on marketing food and beverages, and most of the time, it is not to promote healthy food: it

is processed food, rich in saturated fat and sugar (aboutkidshealth.ca 3). By promoting and selling

our Veggie Smiles, we could be able to differentiate on this aspect: because it is not common to

advertise healthy food, parents would remember them more easily. Also, other aspects that you

will discover in the product strategy could be differential elements that would stick on parents’

mind.

e. Product Positioning

a) Please indicate how your product will be positioned.It is important for companies that are introducing new products, such as B&G Foods, to

reach out to the consumers to the extent that the product is in the consumer’s consideration set.

This is important for new products because it is often so that consumers do not give new products

a chance due to the fact that they already have all the products/brands of the product that they

want or need. Therefore, by being in the consideration set, B&G Foods’ product will be in the

consumer’s mind along with several competing products. Ultimately, the goal is for the consumer

to choose our product instead of our competitor’s products.

8

Calabrese, Lihou, Sponable, Walsh

b) Create a perceptual map to show how your product is perceived relative to competing

products in the market

After looking at several different frozen vegetable companies, we’ve created a perceptual

map comparing these brands with Green Giant. When comparing these brands, we’ve based it off

of the quality of the products as well as the price they are being sold at. Competitors such as

Trader Joe’s and Cascadian Farm offer organic produce which costs more than other frozen food

companies, causing them to fall in the upper righthand corner of the perceptual map. This is

because the quality of their products are much higher than a typical frozen food brands. Like the

two brands that were previously mentioned, companies like Stouffer’s and Ore-Ida have products

that tend to be on the pricey side, but do not share the same quality as Trader Joe’s and Cascadian

Farm. Out of all the companies we looked at, we found that Birds Eye had cheap product and

lacked in quality. After looking at all of these brands, we feel that Green Giant sells products that

are good in quality and sells a decent price.

9

Calabrese, Lihou, Sponable, Walsh

f. What products, if any, represent direct competition or are viable substitute products to

your new product?

Right now our direction competition with our new product, Veggie Smiles, is McCain’s

Smiles potato fries. Like our new product, Smiles are directed towards young children and are

being used as a snack food product or as a side dish at a meals. Unlike our product, McCain’s

Smiles are made out of “100% real potatoes” and are trans fat-free, cholesterol-free, and low in

saturated fat. Another product of McCain’s that we would also compete with is their Tasti Taters.

Like Smiles, they are also a potato product that is trans fat-free, cholesterol-free, and low in

saturated fat. The difference between McCain’s products and our product is that our new product

is a combination of both Smiles and Tasti Tots, but instead of potatoes we are using other

vegetables such as broccoli and carrots. We created a product that is fairly familiar among all

audiences, especially young children, that provides nutritious value to their meal.

1. Marketing strategy and influencing consumer behavior

i. Describe your product strategy.

1. What are the product characteristics/features/benefits provided/need(s) satisfied?

The product we decided to create is targeted toward families with children under 10.

When we think about this target audience, we think about the parents and their children. With our

product, we want to make their life easier, and especially when it comes to family times around

the table. Nowadays, the society puts a lot of pressure over families to make them understand the

10

Calabrese, Lihou, Sponable, Walsh

importance of eating healthy, especially when it comes to children’s diet. However, we all know

that eating healthy is most of the time associated with eating vegetables, and children rarely enjoy

them. Lunch times can easily turn into a fiasco if parents have to force their children to eat

vegetables, or even to punish them for not eating them. And we do not think it should be a matter

for parents. That is why we decided to create “Veggie Smiles”, the first line of frozen vegetables

products in shapes of smiley faces that will bring back smiles on children’s faces. With our

products, we want parents and children to spend great lunch times together. Parents will not be

stressed and rushed by time anymore, nor by the issue of going to the supermarket to cook fresh

products to the family: frozen vegetables are easy to conserve and only one part of the product

can be consumed, depending on the quantity needed. Over time, the quality will not decrease.

Also, they are quick and easy to cook, enabling parents to allocate more of their free time to

leisure activities with their children, without feeling guilty about the food they will serve for

dinner. We also want children to enjoy eating vegetables, for them to stop associating vegetables

with cries and tantrums, but to associate them with pleasure and relishment. Based on our

findings about our target audience characteristics, our product will mostly answer mothers’

needs, whom society’s pressure is heavier on their shoulders when it comes to healthy food and

diets. For our product’s package to have the right features for both the parents and the children,

they both must convey trust and fun.

The trust part is conveyed by several features. First, the omnipresent green color: this

color conveys wealth and fresh growth feelings. These characteristics are important for our

product, because they will make buyers aware that they buy fresh vegetables-made products that

have been growth in respect of the nature but also of the ingredients used. The green color also

conveys vitality. When seeing this product, buyers will feel the vitality in the moment, but also

the vitality that the vegetables will bring to their bodies and to their children’s bodies. Second,

11

Calabrese, Lihou, Sponable, Walsh

the words used on the package also convey trust. We first start by saying how our product will

change parents’ everyday life by offering them an alternative to potatoes or fries, that tend to be

considered as vegetables when they are not. We inform them that a full serving of the product,

either it is the carrot or broccoli flavor, meets the requirements in term of nutrients intake. Also,

we reassure them on the fact that the Veggie Smiles are 100% made of vegetables, that they

haven’t been filed with potatoes to make them more heavy or consistent in density. Finally, the

design of the product is pure and simple, it allows the buyers to quickly see the information they

are looking for. The picture, poised in the middle of the package, is clear: the client knows what

he/she is going to buy and eat. Added to the feelings the colors used convey, they can make a

quick and rational buying decision.

We also focused on the fun part, the most important one. Indeed, selling the product is a

good thing, but getting customers’ feedbacks about their product experience is better, mostly if

they liked the product. The fun part is visible on the package first, thanks to the picture: the

smiley faces are obvious, and children can easily guess the flavor of it. Indeed, under the

conditional learning theory, children have learnt to associate colors with ingredients, and

ingredients with flavors. But first seeing the color of the Veggie Smiles, children can guess what

we’ll be the flavor of it. The smiley shape of the vegetables works as a distraction: the element of

surprise, conveyed by the uncommon shapes of the vegetables will make them forget the

association they make between an ingredient and the bad moment they experienced with it. The

more the children will eat vegetables under these shapes, the more they will replace the negative

conditioned stimulus with the positive one: the fun smiley faces. And if they are too young for

being able to associate colors with ingredients and ingredients with tastes, our products will have

even more important benefits, because they will be their primary base of learning, their primary

conditioning example.

12

Calabrese, Lihou, Sponable, Walsh

Overall, our products will be made of recyclable materials, respectful of the environment.

The opening of the packages will be intentionally difficult to avoid choking risks due to the

ingestion of frozen or not-frozen Veggie Smiles by children.

2. As part of this step, develop a product/product package.

13

Calabrese, Lihou, Sponable, Walsh 14

Calabrese, Lihou, Sponable, Walsh

ii. Clearly describe your pricing strategy.

1. How will you price the product? Why?

While various factors can affect a company’s revenue potential, one of the most important

factors to take into consideration is the pricing strategy that is utilized by the company to price its

products. A good pricing strategy can help determine the price point at which the company can

maximize profits on the sales of its products, in this case being Veggie Smiles. The process of

setting prices is complex due to the fact that the company needs to consider a wide range of

factors including production and distribution costs, competitor offerings, positioning strategies,

and the company’s target market. It is important to take into account that customers will not

purchase over priced goods and that the company will not succeed if the prices are too low.

There are four different pricing strategies that could potentially be used for the Veggie

Smiles. The first strategy would be premium pricing. Premium pricing occurs when businesses

set costs higher than their competitors. It is often most effective in the early days of product’s life

cycle. However, since customers need to perceive the product as being worthy of the higher

price, a company must work hard to create a value perception. For instance, the company needs

to ensure that the product’s packaging and the store’s décor combine to support the premium

price.

The second strategy that could potentially be used would be penetration strategy pricing.

This strategy aims to attract buyers by offering a lower price on goods such as our Veggie

Smiles. Although many companies use this technique to draw attention away from competitors,

penetration pricing does tend to result in an initial loss for the company. Over time the increase in

awareness of the product can increase profits, however companies tend to raise their prices

anyway to reflect the state of their position in the market.

15

Calabrese, Lihou, Sponable, Walsh

Economy pricing is used by a wide range of companies, including generic food suppliers,

and is the third option that could be used to price our Veggie Smiles products. Economy pricing

aims to attract the most price-conscious consumers by minimizing the costs associated with

marketing and production in order to keep product prices down. This strategy is particularly the

most effective for large companies such as B&G Foods.

Price skimming is the fourth and final strategy that could be used to price our Veggie

Smiles. Price skimming is designed to help companies maximize their sales on new products due

to the fact that it involves setting rates high during the introductory phase and then lowering them

gradually, as competitor goods appear on the market. This allows the company to maximize

profits before dropping prices to attract more price-sensitive consumers. Not only does price

skimming allow the company to quickly make up for its costs, but it also creates an illusion of

quality when the product is first introduced to the market.

Out of the four possible pricing strategies, economy pricing would be the most beneficial

strategy for pricing our Veggie Smiles. This is large in part because our target market is families

with children under the age of ten. It is likely that when these families are shopping for grocery

products like ours, they will be very price conscious and will purchase lower priced goods. Also,

due to the size of our company, we can minimize the production costs of the Veggie Smiles to

create lower prices without hurting the welfare of the company. By selling our products for a

lower price point, $3.99, our target market will be more likely to purchase our products, therefore

driving out our competition.

iii. Clearly describe your promotion strategy for this new product.

The promotion strategy for this new product will be based on different platforms. In fact, it will

be promoted via Magazine with the simple one page ad presented below, but it will mainly be

16

Calabrese, Lihou, Sponable, Walsh

done via online promotional strategy (email marketing, target ad marketing and social media

promotion).

First via magazine, we will post on food magazine to increase consumer interest and at

the same time reduce our cost by not posting on many different magazines. We will select the top

5 most popular food magazine, so according to statistics from Cision’s website, Taste of Home,

Cooking Light, Every Day with Rachael Ray, Food Network Magazine and bon appetit.

However, according to Statista, the magazine retail sales are constantly dropping and dropped

from 103 million at the end of 2014 to about 85 million in the second quarter of 2016. Moreover,

people spend less and less time reading a magazine, on a daily basis, American spend on average

24.7 minutes reading in 2010 compared to an estimated 16.5 minutes in 2017.

However, even if these numbers decrease over the time, Magazine advertising shouldn’t be out of

our promotion strategy.

The other media, we will focus on to promote our product will be via online strategy

based on four elements, email marketing, use of target marketing ad with the help of cookies,

Social media, and online promotion via the use of cooking YouTube channel.

The first one, email marketing, thanks to the large number of data available gathered by not only

Green Giant but also B&G, we will send an email campaign to most of them which seem to be

the most appropriate. The title of the email will be “Make a Giant difference!”. This specific title

is a link to a previous campaign launched in 2013 which was “Eat more. Make a Giant

difference”, showing a comparison between 100 calories, portion of vegetables and 100 calorie

portion of chips. This for some trigger an interest because of the words used but also for other

because it will make them remember of something, of a previous ad. Moreover, email marketing

provides a really high Return On Investment.

17

Calabrese, Lihou, Sponable, Walsh

The second one, target advertising, will track consumers visiting food, supermarket

websites etc. thanks to the use of cookies and target them with our ad on social platform or other

website for example. The ad will be a simple one with a call to action to the Green Giant website

to the specific Veggie Smiles page.

Then, social media, with a specific focus on Facebook. In fact, according to the Pew

Research Institute, 68% of all U.S. adults use Facebook, and older adults are joining in increasing

numbers. Moreover, 84% of online adults ages between 30 to 49 years old use Facebook, which

indicate a high chance to reach our targeted population of families with a child of ten or lower.

The Facebook strategy will consist in using the GreenGiant page and promote the new product

via pictures, but also call to action, with the use of hashtags and interaction with consumers in the

comment section.

18

Calabrese, Lihou, Sponable, Walsh

1. Please create one communications piece for the product (print ad, online ad, video, etc.)

that reflects your message strategy.

This advertising has been designed in a way to directly target family with kids below 10

years old. In fact, we decided to create a simple ad, easy to read and understand the signification

of it by picturing a situation. We decided to use the memory process of the consumer by

triggering them memories of actions that might have happened before. Many parents have

19

Calabrese, Lihou, Sponable, Walsh

difficulties to make their child eat vegetables and the child most of the time finish by doing the

same face than the top section of the ad and decide to not eat his/her vegetables. By looking at

this image and using memory process, the parent will directly understand the situation, and will

be intrigued with the changing emotion of the child. The sentence “put a smile on their face” not

only serve as a delimitation between the two images, but as a reminder of the ideal state search by

many parents. In fact, this sentence is a delimitation between the actual and the ideal state, which

trigger a want of reaching this ideal state and the product displayed on the side is the element that

will help the consumer reach that state.

We decided to use a white background in order to really focus on the child and the changing

emotion perceived through the body language.

The advertising is organized in a linear way and can be read from top to bottom. We

organize the ad in order to have first, the reaction of the child, then where the problem came

from, then an incentive text separating the ideal and actual state, then the second reaction, with

the reason why. This disposition emphasizes our product and put it as a problem solver, and the

solution to put smiles on their child as the child is only happy after we change the vegetables into

our Veggie Smiles.

We use green color for the text to give this sensation of nature and healthy products. In

fact, the use of wood, white and green color give this sensation of natural and healthy.

We designed this communication piece in a simple way, helping consumers to understand the

meaning rapidly due to our online promotion strategy. In fact, people don’t spend that much time

looking at advertises coming from email or target advertising.

Moreover, we used a child as a spokes character as we are targeting families with kids

below 10 years old, which perfectly fit our target population as they can identify themselves into

this advertising.

20

Calabrese, Lihou, Sponable, Walsh

iv. Clearly describe your distribution strategy.

1. Where will you distribute the product? What distribution channels will be used? Why?

We will base our distribution strategy on two different distribution channels, in the

grocery store/supermarket and online. We decided to sell through a dealer network like WalMart,

for example (via brick-and-mortar supermarkets, but also via their online website), but also direct

sell to end users directly from our website. We plan to adopt this strategy not only to increase our

revenue and market share, but also due to the evolution.

In fact, according to a research done in April 2015 by Nielsen about the Future of

Grocery, 57% think grocery shopping in a retail store is a fun day out for the family. Also,

according to Statista, in 2014, 86.4% of American prefer to purchase most OF their food in

Grocery store and supermarket.

However, there is a constantly growing market for online grocery shopping. According to

Nielsen, one quarter of online respondents say they order grocery products online, and 55% are

willing to do the same in the future. The numbers are still low in America. Only 9% of American

are using virtual supermarket, however, 51% more are willing to use it, which indicate a market

that shouldn’t be avoided.

v. How must marketing ethics and social responsibility be factored into strategic decision

making for the product you are recommending?

Besides coming up with a product that is fun for kids, we also wanted to give them

something healthy to snack on instead of settling for junk food. For several years, the United

States has had a bad wrap for having high levels of obesity because of poor diets. Because of this,

we are seeing a change in American diets by improving their diets and consuming healthier

21

Calabrese, Lihou, Sponable, Walsh

foods. According to IBISWorld, “the healthiness of Americans’ diets has increased slowly but

steadily since the 1980s” (IBISWorld). This trend is expected to continue in years to come.

To keep up with this trend, we want Americans to think about our product when it come

to consuming healthier foods, in this case vegetables. We understand that people becoming more

aware of what they are eating and are trying to rule of unhealthy foods in their diets. That’s where

our product comes into play. We are offering healthier alternative to junk food, that not only is

delicious, but also a fun twist on vegetables (which is why kids love it). Our new product

encourages kids and adults to incorporate vegetables into their diets. With that being said, Green

Giant will provide truthful information to the public about this new product so people know what

they are consuming. Our new product will consist of the purest ingredients, without containing

GMOs and other hormones that are in the used when growing the vegetables. By providing our

consumers with this kind of information, this will allow our customers to gain trust in our

company and convince others to choose our product among our competitors. We also want to

make it know that we are incorporating eco-friendly packaging for our product by using recycled

materials.

vi. How would you measure or determine the overall success of your marketing strategy?

In order to determine the overall success of our market strategy, our company will look at

individual, firm, and social outcomes. By looking at each category, we can get a better

understanding about how our product is performing in the market. Since Green Giant is already a

well-known frozen food company, they already have loyal followers. With that being said, we

assumed that these loyal followers will be willing to try our new product and spread the word

about it to others. Then, we will would look at what people are saying about Veggie Smiles. This

includes their first impressions, what they think of the flavors, their overall experience, etc. With

22

Calabrese, Lihou, Sponable, Walsh

that being said, we can look at who is purchasing our product more than once. This is a good

indicator if people are enjoying our product. Today, our society is becoming more green friendly

and finding better ways to make use of existing materials. Our company choose to use packaging

made out of recycled materials to help promote a greener planet while selling our product. After

looking at these types of factors, it is important to look at the amount of sales, as well as revenue

from Veggie Smiles. We are aware that the consumption of fresh vegetables across the

population is slightly increasing, yet the consumption of frozen foods is remaining fairly the same

over the past ten years. According to data, when fresh vegetable consumption were down in 2012

and 2013, the level of frozen food consumption were at its highest in 2012 and 2013

(pbhfoundation.org, 11). But when the consumption of fresh vegetables increased in the year of

2014, the consumption of frozen vegetables decreased (pbhfoundation.org, 11). By looking at this

type of information, we can get an idea of what our possible sales would be like.

3. Conclusion

Our new product that we came up with for Green Giant is Veggie Smiles. This new

product is made from 100% all natural vegetables that are in the shape of a smiley face and are

directly targeted towards families with children who 10 years old or younger. Veggie Smiles are

great way to incorporate vegetables into a kids’ diet. Their fun shape and flavorful options are

bound to be loved by young kids, and parents too! We feel that this can lead to more children

across the nation to consume more vegetable than they once did. Veggie Smiles will catch the

attention of children and convince their parents to purchase this new product. Parents will realize

that Veggie Smiles will not only satisfy the hedonic needs (entertainment aspects) of their child,

but also their utilitarian needs (practical and functional aspects) too. When it comes to pricing, we

are well aware that our target market is sensitive to pricing. With that being said, we priced

23

Calabrese, Lihou, Sponable, Walsh

Veggie Smiles at $3.99. Our new product is set at a low price so our target market is more likely

to purchase or product. To promote Veggie Smiles, we came up with several ways to bring

awareness to our product based on different platforms. We are using more traditional strategy,

like placing ads in food magazines, along with more non traditional medias, such as social media,

emails, and online promotions. When it came to the design of our advertisement, we wanted to

show how difficult it is feeding children vegetables. But, when you introduce children Veggie

Smiles, kids are more than willing to eat and enjoy their vegetables. Veggie Smiles will be

available in grocery stores and online supermarkets. As a company it is important to have good

marketing ethics and social responsibility when it comes to making decisions about our new

product. We came up with decisions such as having environmentally friendly packaging,

providing truthful information to our customers, along with choosing the purest ingredients for

our product.

24

Calabrese, Lihou, Sponable, Walsh

4. Works Cited

About Cision StaffCision's Research Staff Makes over 20,000 Media Updates to Cision's Media Database Each Day! For More Updates and Other Thought Leadership in the Industry, Follow @Media_Moves. "Top 10 Food Magazines in the U.S. | Cision." Cision. N.p., 01 May 2013. Web. Nov. 2016.

Copyright © 2015 The Nielsen Company, Nielsen. "E-COMMERCE, DIGITAL TECHNOLOGY AND CHANGING SHOPPING PREFERENCES AROUND THE WORLD." THE FUTURE OF GROCERY (n.d.): n. pag. Apr. 2015. Web. Nov. 2016.

"Distribution Channels in Marketing | Marketing MO." Marketing MO. N.p., 03 Apr. 2016. Web. Nov. 2016.

Greenwood, Shannon, Andrew Perrin, and Maeve Duggan. "Social Media Update 2016." Pew Research Center: Internet, Science & Tech. N.p., 11 Nov. 2016. Web. Nov. 2016.

"Healthy Eating Index." IBISWorld. IBISWorld US, Nov. 2016. Web.

Lacy, Lisa. "Green Giant to Dieters: Go Ahead, Cheat with Vegetables." ClickZ Green Giant to Dieters Go Ahead Cheat with Vegetables Comments. N.p., 26 Sept. 2013. Web. Nov. 2016.

Marvick, Bin. "Target Market: Children as Consumers." AboutKidsHealth. AboutKidsHealth, 30 Oct. 2010. Web. 18 Nov. 2016.

President, BCG Senior Vice. "U.S. Consumers' Primary Food Shopping Locations by Type, 2014 | Statistic." Statista. N.p., 2014. Web. Nov. 2016.

Research, Market. on INFLUENCE OF CHILDREN (n.d.): n. pag. ICMAB. Feb. 2016. Web. Nov. 2016.

"Table 3413. Consumer Units of Two or More People by Income before Taxes: Average Annual Expenditures and Characteristics, Consumer Expenditure Survey, 2014-2015." The Bureau of Labor Statistics. The Bureau of Labor Statistics, n.d. Web. 27 Nov. 2016.

Wilson, Jamar. "Topic: U.S. Consumers: Online Grocery Shopping."

25

Calabrese, Lihou, Sponable, Walsh

Www.statista.com. N.p., n.d. Web. Nov. 2016.

Wohl, Jessica, and Michelle Dopp. "As Green Giant Heads to B&G Foods, a Look at His Career." Advertising Age CMO Strategy RSS. N.p., 03 Sept. 2015. Web. Nov. 2016.

"70 Email Marketing Stats You Need to Know ." 70 Email Marketing Stats You Need to Know | Campaign Monitor. N.p., n.d. Web. Nov. 2016.

26

Calabrese, Lihou, Sponable, Walsh

5. Summary of Responsibilities

Media review: Pierre-Clément Lihou

Existing product research: Pierre-Clément Lihou

Library Research: Kristin Walsh

New product concept: Melanie Calabrese, Pierre-Clément Lihou, Andrew Sponable, Kristin

Walsh

Locating the advertisements: Pierre-Clément Lihou

New product marketing strategy: Melanie Calabrese, Pierre-Clément Lihou

Artistic Design: Melanie Calabrese, Pierre-Clément Lihou

Ad development: Pierre-Clément Lihou

Summary of responsibilities: Melanie Calabrese

Paper compilation: Melanie Calabrese

Theoretical evaluation – new product: Melanie Calabrese

Editing: Melanie Calabrese, Andrew sponable, Kristin Walsh

Theoretical Evaluation – advertising : Pierre-Clément Lihou

Presentation: Melanie Calabrese, Pierre-Clément Lihou, Andrew Sponable

References cited: Melanie Calabrese, Pierre-Clément Lihou, Kristin Walsh

Handouts/PowerPoint: Melanie Calabrese

Executive Summary: Melanie Calabrese

Letter of Transmittal: Melanie Calabrese, Kristin Walsh

Part 1 Revision: Andrew Sponable

27

Calabrese, Lihou, Sponable, Walsh

6. Appendices

i. Part 1

B&G Foods Inc. and Green Giant: An Analysis of the Frozen Food and Manufacturing Food

Industry

Melanie Calabrese

Pierre-Clement Lihou

Andrew Sponable

Kristin Walsh

Dr. Buff

Marketing 324, Consumer Behavior

October 13, 2016

28

Calabrese, Lihou, Sponable, Walsh

Part 1: Market Analysis - REVISED

1. Company Analysis

Green Giant is previously held by a group called B&G Foods Inc. According to the

database IBIS, and based on its SIC code (311999), B&G Foods Inc. operates in the “All Other

Miscellaneous Food Manufacturing”(IBISWORLD). The group operates in the U.S. and in

Canada, with its headquarters located in Parsippany, NJ. It manufactures, sells and distributes a

broad range of shelf-stable and frozen food going from maple syrup to frozen vegetables: Green

Giant is specialized in the manufacture and sell of frozen and canned products. According to the

NAICS, it is referenced under the 31141 SIC code, and its competitors are Nestle Prepared

Foods, Kraft Pizza Co Inc or ConAgra Foods Inc (NAICS).

According to B&G Foods Inc.’s SWOT Analysis, the first major strength of this group is

the diverse portfolio of products it owns, supported by strong brands (B&G Foods). Indeed, B&G

Foods owns The Maple Grove Farms of Vermont, Ac’cent, Baker Joe’s, Canoleo, Cream of Rice

etc... These brands have important local and national market shares across the U.S., Canada and

Puerto Rico and are day-to-day consumer packaged goods brands. Owning all those brands

assure B&G Foods Inc. a competitive advantage over its competitors, which are, according to

NAICS, ConAgra Foods Inc., Cargill Inc, Solae LLC etc (NAICS).

The second major strength of B&G Foods Inc. is the way it manages and allocates its

manufacturing processes. According to its SEC Filings, the group owns nine manufacturing

facilities, of which seven are owned and two are leased. The facilities are most of the time located

near major customer markets and raw materials. The group sources a big portion of its products

under co-packing arrangements from third parties. According to Wikinvest, co-packing

arrangements can be described as the outsourcing of manufacturing processes to other companies

(Wikinvest). B&G Foods Inc.’s third party manufacturers are located both in the U.S. and in

29

Calabrese, Lihou, Sponable, Walsh

foreign countries; they also manufacture Regina, Underwood, Las Palmas and Joan of Arc’s

products. This method of manufacturing shows several advantages. Firstly, it is a cost-effective

and time-effective method. The time that is not spent on manufacturing processes can be

allocated for selling and distributing goods. According to the UC Food Safety Publication, it does

not require specific capital requirements nor up-front money: no facilities have to be built, no

equipment or permits have to be purchased, and the company does not have to pay huge deposits

for facilities (Blan-Byford). According to FoodBusinessNews, B&G Foods Inc. acquired Green

Giant brand from General Mills Inc. in November 2015 (Nunes). B&G Foods Inc. signed a two-

years transition co-packing agreement with General Mills Inc. that will expire in November 2017.

This agreement allocated 30% of Green Giant’s products manufacturing to B&G Goods Inc. in a

previously owned General Mills’ manufacturing facility based in Irapuato, Mexico, and 60% of

Green Giant’s products manufacturing to General Mills Inc. at a General Mills Inc.

manufacturing facility based in Belvidere, Illinois (B&G Foods, Inc. SWOT Analysis 5).

The third strength of B&G Foods. Inc. rests on its strong financial performance. The

FY2015 statement states revenues of $966.4 million, which is an increase of 14% compared to

2014. This increase can be explained by different acquisitions made during the year 2015. But

Green Giant brand is definitely the brand which contributed to the revenues’ increase. Acquired

in November 2015, it contributed $106.2 million for the FY 2015. Mama Mary’s, which was also

acquired during the FY2015, contributed $18.4 million to the net sales. Overall, the group’s

profitability significantly increased, with an increase of 48.5% in operating, and 68.7% in net

profits. Benefiting from strong financial performances will allow B&G Goods Inc. to more

rapidly find new shareholders and financial investors who will help it investing for future

growing opportunities (B&G Foods, Inc. SWOT Analysis 5-6).

30

Calabrese, Lihou, Sponable, Walsh

But B&G Foods Inc. also has weaknesses. The first one would be the use of local

marketing strategies, mainly focusing on the U.S. Indeed, 95.9% of the FY2015 revenues were

generated in the U.S while Canada only recorded 4.1% of the revenues. This strategy makes the

group dependent to environmental, political, economic factors that may negatively affect the U.S

market and its customers. Moreover, it also limits the group’s extension and growth capabilities,

since only targeting a small portion of the world population (B&G Foods, Inc. SWOT Analysis

6). The second weakness would be the dependence on local customers for generating all the

revenues of the group. Indeed, all the brands owned by the group are mainly American and

Canadian brands. So it only relies on these two regions to make most of the sales.

2. Competitor Analysis

a) Overall size and characteristics of market (reference NAICS information

As explained above, focusing on their NAICS reference information, B&G Foods Inc.

focuses their industry in the meat, beef and poultry processing industry. However, we will focus

on Green Giant Frozen food industry with their product Veggie Tots. The NAICS reference for

Frozen Food Manufacturing is 31141, and according to the US Census Bureau, this industry

comprises, frozen fruit, frozen juices, frozen vegetables (our target market), and frozen specialty

foods (except seafood), such as frozen dinners, entrees, and side dishes (Sadowski).

The Frozen Food Production industry has seen its industry annual growth, reducing over

the years, going from an annual growth of 1.6% of the past 5 years to an expected annual growth

of 0.6% from 2016 to 2021. This reduction can be explained by the increase of household income

over the years (5.2% growth in the U.S in 2015). This rise in income push consumers to purchase

fresh food over frozen ones and also goes eat out more frequently.

31

Calabrese, Lihou, Sponable, Walsh

Another big reason for the decline in growth is the rise of health concern and the research of

more healthy, organic and nutritious food. According to a study made by the Nielsen’s Global

Health and Wellness in 2015 on 30,000 consumers in 60 countries, 41% of the Generation Z

(consumer under age 20) would willingly pay a premium for “healthier” products compare to

32% of the 21 to 34 and 21% of the Baby-Boomers (50 to mid 60s).

However, the competition is important and frozen market is not the only one that wants to

go to a more healthier food, fast food too. That’s why, despite all the efforts made, the revenue

increased by 1.6% over the past five years (2011 to 2016) with a revenue of $32.5billion in 2016,

but this growth is expected to decline to an annual growth of 0.6% over the next 5 years (2016 to

2021). As you can see on the graph below, of the Products and services segmentation in 2016, the

frozen vegetables represent 29.5% of the market (IBIS).

As explained above, consumers search for more healthier products, and that’s why frozen

vegetables are a prolific market, which is expected to grow over the year. First, the increase in

household disposable income is in part due to the increase of the number of working hours so a

32

Calabrese, Lihou, Sponable, Walsh

decrease in leisure time, indirectly, cooking time. That’s why frozen vegetable is a good

alternative as it is easier to prepare than fresh or refrigerated products. Another benefit is that it

lasts longer than fresh products. That’s why, according to studies made by the Frozen food

Foundation state that 90 percent of Americans fail to consume the daily recommended amounts

of vegetables. Moreover, another study made by the Frozen Food Foundation partnered with the

University of California-Davis with the aim of evaluating the nutrient content of commonly-

purchased frozen fruit and vegetables revealed that frozen fruit and vegetables are generally equal

and in some cases better than fresh ones.

b) Competitors’ brands and market share

The Major competitors are listed as follow:

There are three main leaders and competitors, Nestle SA with 16.3% of the market share,

ConAgra Foods Inc. with 15.9% of the market share and The Schwan Food Company with 7.6%

of the market share.

The first main competitor and leader of the market is Nestle SA with 16.3% of the market

share. Nestle was created in 1866, which mean they have 150 years of experience, explaining

why they are the leading in Nutrition, Health and Wellness and the world’s largest food and

beverage producer. Their Headquarter is based in Vevey, Switzerland, and they operate in 194

countries with around 339,000 employees.

33

Calabrese, Lihou, Sponable, Walsh

Despite operating in more than 190 countries, one fourth of Nestle $92.1 billion net sales in 2015

came from the United States. Nestle is part of the Frozen industry market through different iconic

frozen food companies such as DiGiorno, Kraft Foods’ (acquired in 2010), Hot Pockets frozen

snacks, Tombstone frozen pizza etc.

Nestle wants to expand their market through the acquisition of different companies and

have in mind to improve their products in link to the increase of consumer health concern.

In 2014, Nestle even launch a series of campaign such as “Freshly Made. Simply Frozen”, or

“Balance your Plate with Nestle” in order to demonstrate the good impact of frozen food in

consumer minds.

As you can see in Nestle’s S.W.O.T. analysis below, their main threats are the expansion

by competitors which might be a good opportunity for us.

34

Calabrese, Lihou, Sponable, Walsh

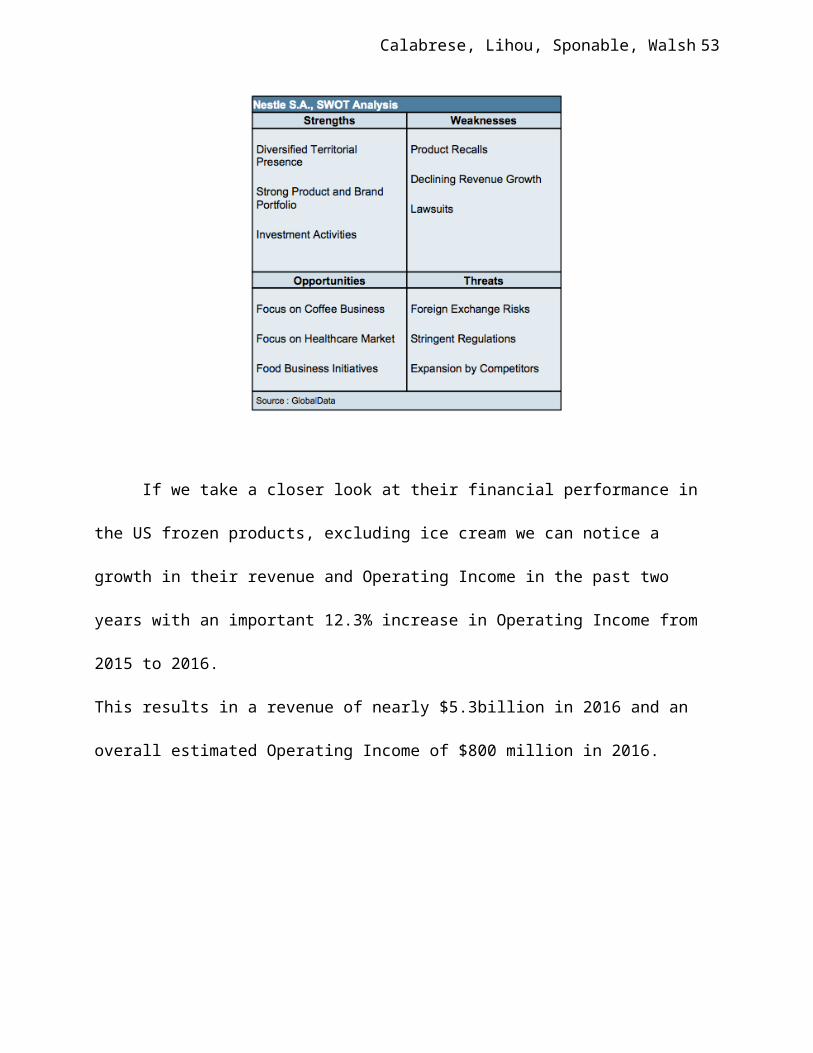

If we take a closer look at their financial performance in the US frozen products,

excluding ice cream we can notice a growth in their revenue and Operating Income in the past

two years with an important 12.3% increase in Operating Income from 2015 to 2016.

This results in a revenue of nearly $5.3billion in 2016 and an overall estimated Operating Income

of $800 million in 2016.

The second main competitor is ConAgra Foods Inc., with 15.9% of the market share.

ConAgra Foods was founded in 1919, their nearly 100 years of experience make them an

important competitor. They are one of North America’s largest food companies with more than

33,000 employees, that they use to call “family” on their website. One of the industry’s most

relevant segment market is their frozen section which includes popular brands such as Healthy

Choice which in April 2009, ConAgra reintroduced their line of frozen meals with new products,

with a new line of All Natural Entrees. And also brand like, Marie Callender’s and Banquet.

They also expanded their product portfolio in order to introduce healthier products with Marie

Callender’s Fresh Flavor steamer entrees for example. ConAgra did a series of acquisition in

order to boost their revenue and expand their market, like the purchase of Unilever’s North

35

Calabrese, Lihou, Sponable, Walsh

American frozen meal business for $265million in 2012, which give them a broad product and

brand portfolio as you can see in the Strengths section of their S.W.O.T. analysis below.

If we now take a closer look to their financial performance, we can notice that compared

to Nestle for example, they have nearly the same revenue for the year 2016-2017, however, they

have an operating income that was lower, this means that their operating expenses and cost of

good sold (COGS) are a lot higher than Nestle which can be a result of the higher number of

brand acquisition over the past 5 years.

36

Calabrese, Lihou, Sponable, Walsh

The third major competitor is the Schwan Food Company with a market share of 7.6%.

Schwan Food Company, founded in 1952, by one man name Marvin Schwan. This company

really shows the expansion of a brand growing from a “one-man-and-a-truck” as they call it on

their website, to a “multibillion-dollar private company with 12,000 team members nationwide.”

Their main market is based on a home delivery system of frozen food to more than

3.5million consumers across the US. Moreover, the Schwan Food Company has a portfolio of

more than 350 different food products such as, entrees or frozen pizza or frozen vegetables.

37

Calabrese, Lihou, Sponable, Walsh

Source: SWOT Analysis24.com

On a financial point of view, The Schwan Food Company as its competitors are aware of

the growing importance consumer give to healthier products. That’s why they plan to remove,

over the next few years, artificial flavors, colors, and high-fructose corn syrup from most of its

frozen products and focus on healthier products.

38

Calabrese, Lihou, Sponable, Walsh

3. Conditions Analysis

To maintain a successful business organization it is important to keep in mind the external

conditions and their impacts, both favorable and unfavorable, that they have on the company. The

five main external conditions that impact business organizations are the economy, government

regulations, technology, sociocultural environment, and physical environment. By analyzing the

current conditions of the organization, it is easy to view what external conditions have either a

favorable or unfavorable effect on the company. Once the company has a better understanding of

its strengths, weaknesses, threats, and opportunities, they can assess them how they see fit by

potentially rearranging their marketing strategy. For example if the company intended a certain

product to be for people of high income and the current economic conditions make it so that the

majority of the population has low to middle income then the company much adjust accordingly

to accommodate their customers.

In August of 2016, the U.S Bureau of Economic Analysis reported that disposable income

in the United States has reached an all time high of 14075.70 Billion USD. Since the economy

has been on the rise and families are earning a larger salary, more money can be allocated

towards wants rather than needs. In relation to this, according to IBIS World’s Industry Outlook,

“[the] Frozen Food Production Industry is expected to grow only marginally over the next five

years as rising disposable income levels enable consumers to dine out more often and choose

fresh produce over frozen foods” (Yucel, 1). In this situation, the external economic condition,

the rise of disposable income, has an unfavorable effect on the industry due to the fact that it is

preventing companies such as B&G Foods Inc. from growing to reach its full potential. Families

who now have more income than they previously have had in the past are looking to buy fresher

foods and products rather than frozen foods. This desire for fresh foods derives from the false

belief that the fresher the food is, the healthier this is. As stated above, frozen foods and

39

Calabrese, Lihou, Sponable, Walsh

vegetables can be just as healthy as fresh foods. For those consumers who understand this

concept, the increase in disposable income can have a favorable impact on B&G Foods Inc.

because they will not shy away from purchasing frozen foods. Although, the dining out option is

still a threat.

Much like the economy, the government plays a large role in how successful a business

organization can be. The food industry in particular is subjected to many government regulations

and inspections to ensure that products are safe for consumers to consume. For example, the Food

and Drug Administration inspects most of the foods that cross State lines or foods that have been

imported from foreign countries. It is not uncommon for situations to occur where fruits and

vegetables are blocked from entering the marketplace because of organisms such as E. coli that

cause foodborne illnesses. These inspections can be timely and costly for organizations. It is like

so that they can be viewed as having an unfavorable impact on the company. However, by

passing inspections consumers will have faith in the company and will believe that the product

they will be consuming is safe and healthy.

One set of regulations in particular that B&G Foods Inc. has to pay attention to regards

frozen foods handling and storage. Since the products that B&G Foods Inc. produces are frozen

foods, they must abide by these regulations in order to sell their products commercially. The

generally accepted temperature that foods are frozen at is zero degrees Fahrenheit. It is also noted

that frozen foods should be stored in a relative humid environment to prevent freezer burn and

the drying out of food (Frozen Foods Handling and Storage). If kept in these conditions, most

frozen fruits and vegetables can be stored for 10-12 months without any significant quality loss.

These regulations are relatively easy for companies to meet. The main problem lies in the

handling of these frozen products. Exposure to heat for short periods of time is not serious unless

it is repeated often. It is prolonged exposure to heat that causes the most damage to the goods. It

40

Calabrese, Lihou, Sponable, Walsh

is imperative that companies use refrigeration equipment to ship frozen foods to prevent spoiling

of product. These regulations that B&G Foods Inc. must follow and abide by are crucial to their

survival in the market. These regulations that are enforced by the government take time and

money, which hurt the company financially. However, every consumer loves the peace of mind

they receive knowing that the food that they purchase is healthy and safe due to these inspections

and regulations.

Frozen food companies such as B&G Foods Inc. are highly influenced by modern science

and technology. Scientific and technologic advances are responsible for making the frozen food

market one of the largest and most dynamic sectors of the food industry. In IBIS World’s

Industry Outlook it is stated that, “technological advances in freezing, packaging and sorting,

combined with aggressive marketing for new products, will be imperative for industry

participants to maintain market share” (Yucel, 1). In other words, the moment a company stops

developing and inventing new methods to better their product, they will lose their place in the

market. The most common method of freezing vegetables among frozen food companies is

industrial freezing. This process involves the cooling down of the product to the temperature at

which nucleation starts. Nucleation is the process by which a nucleus, or seed is produced and

allows ice crystals to begin forming. Once crystals begin appear, a phase change occurs in which

the product turns from liquid to solid. This method is proven to be just as cost effective as any

other method of food preservation. However, third parties such as Linde Food have begun to

create new and quicker ways to freeze products at a lower cost while improving quality and

reducing product loss. They accomplish this by using state-of-the-art cryogenic freezers. Linde

Food reports that, “many high-volume processors are saving $2-3 million and more per year with

Linde solutions” (Linde). If B&G Foods Inc. were to invest in this new advancement in

41

Calabrese, Lihou, Sponable, Walsh

technology, it could be considered as a favorable impact because they would have the advantage

of providing customers with higher quality products at a lower cost.

The sociocultural environment, or cultural norms and demographics, is a key aspect to look at

when observing the external conditions and their impacts on business organizations. Currently in

the United States there is an increased popularity in fitness and health trends. In IBIS World’s

Industry Outlook, it was noted that, “consumers’ growing demand for nutritious food and

convenience is expected to drive product innovation” (Yucel, 1). This is great news for

companies such as B&G Foods Inc. who are looking to introduce new products into the frozen

food market that are healthy, nutritious, convenient, and fun. That’s why in 2015 they acquired

Green Giant for $765 millions to expand their market with a new product line that include our

product Veggie Tots. This product will not only impact sociocultural environment but also

answer the question of “growing demand for nutritious food”.

On the other hand, the same great things cannot be said with the physical environment.

Global warming in particular has proven to be a problem for many companies that produce

agricultural related products. Global warming refers to the gradual heating of the Earth’s surface,

oceans, and atmosphere. Scientists have stated that Earth’s average temperature has increased by

1.4 degrees Fahrenheit over the past century. It is popular belief that greenhouse gases produced

by humans around the world are to blame for the rise of Earth’s temperature. According to

Amanda MacMillan, “[in] the United States, the burning of fossil fuels to make electricity is the

largest source of heat-trapping pollution, producing about two billion tons of CO2 every year”

(MacMillan, 1). These emissions are responsible for not only raising the temperature of the

Earth’s surface, oceans, and atmosphere, but also the extreme weather that is caused as a result of

the increase of global temperatures. Later in MacMillan’s article she mentioned that, “[in] 2015,

for example, scientists said that an ongoing drought in California – the state’s worst water

42

Calabrese, Lihou, Sponable, Walsh

shortage in 1,200 years – had been intensified by 15 percent to 20 percent by global warming”

(MacMillan, 1). Droughts such as these make it very difficult for farmers to grow the crops that

companies such as B&G Food Inc. rely on to produce products such as Vegetots.

As of 2016, since this is a new product, it is not available in stores yet. However, it is

expected that Veggie Tot will be sold at all of the main supermarkets such as Hannaford, Price

Chopper, and Wal-Mart. It can be found now online at Green Giant’s website for pre-order and if

you pre-order and if you subscribe to the newsletter about the product, you will receive a

discount.

Three common brands that might be in the buyer’s consideration set are Great Value,

Birds Eye, and Cascadian Farm. These three brands offer very similar products at very

competitive prices. Cascadian Farm in particular is known for its nutritious and healthy frozen

vegetables and meals. On Wal-Mart’s website they are the highest rated frozen vegetable on a

scale based on their impact on the society, environment, and consumer’s health. Another

important product competitor is Alexia, with their organic range product. In fact, most of their

products have the word “organic” in their name. This really is an incentive for the consumer as

they are more likely to search for healthier products. Moreover, on different food websites, they

rank as one of the best frozen vegetable brands, along with Cascadian farm. That’s why these two

brand and product line might be our biggest competitors for our product Veggie Tots.

4. Consumer Analysis

a) How is the market segmented?

For this kind of company, this market is segmented based off of the different attitudes

towards the consumption of vegetables. According to the National Purchase Diary (NPD), this

43

Calabrese, Lihou, Sponable, Walsh

market is segmented into five different groups. The first segment is Traditional Health Followers.

Under this segment, people are more health conscious and are looking for food with nutritional

value. These people are older (females 55 + or males 65 +), which means that they are mostly

likely to have health problems such as, “heart disease, high blood pressure, high cholesterol,

diabetes or osteoporosis” (pbhfoundation.org, 52). They are also more educated and tend to have

incomes that are high. Traditional Health Followers are more likely to try new foods and less

likely to eat things that they usually eat. The second market segment is Natural Health

Embracers. Under this segment, Natural Health Embracers are adults who are motivated by

nutrition and health. This segment consists of female adults, whose ages range from 35-44 to 55-

64 year olds, and tend to have low income levels. In this segment, people prefer organic foods

over other options. With that being said, this segment is into natural remedies and are least to

have issues with their health. The third segment is called Health Strugglers. Health Strugglers

consist of adults who are 45 years old or older, who do not have children, and have low incomes.

Under this segment, people, “say their food choices are also strongly driven by convenience,” and

are likely, “to eat the same things over and over again,” which means that they are are least likely

to be food adventurous (pbhfoundation.org, 52). The fourth market segment is Family Pleasers.

This market segment consists of females between the ages of 18 and 34, who are also influenced

by children. These people are all about pleasing their family and feel that they have a hectic

lifestyle. Unlike Health Strugglers, Family Pleasers choose food that are not driven by

convenience. Last but not least, the fifth market segment is called Short Cut Fuelers. This

segment is made up of adults, who are mostly males, that claim that their lives are rushed and

hectic, just like Family Pleasers. Similar to Health Strugglers, Short Cut Fuelers are also likely to

pick certain foods depending on how convenient they are. They are also less likely to be

interested in the value of nutrition in food, along with not caring about a healthy lifestyle.

44

Calabrese, Lihou, Sponable, Walsh

Although the males in this market segment may have children of their own, they do not care in

making food choices that will please their children.

b) A complete analysis of the target market demographics

When analyzing our target market, one demographic we looked at was age. Children who

are 12 or young have been reported to be not consuming as many vegetables as they did five

years ago. According to data about the consumption of vegetables, children between the ages of

6-12 in 2009 had an annual eatings per capita of 386 pounds and an annual eating per capita of

375 pounds in 2014, thus showing there is a downward trend of this age group eating vegetables

(pbhfoundation.org, 22). The data also shows a decrease of the consumption of vegetables in

children who are 6 years old or less from 2009 to 2014 too. During this five year period, as the

consumption of vegetable decreased, the consumption of fruits increased. Children between the

ages of 6-12 increased their annual eatings per capita of fruits from 201 pounds to 227 pounds.

The annual eatings per capita of fruits for children who are 6 or younger went from 272 pounds

to 305 pounds. In contrast, children between the age group of 13-17 are eating more vegetables.

Although the eatings per capita went from 375 to 376 during those five years, it shows a slight

increase of the consumption of vegetables in this age group. People between the ages of 18-44

showed similar results to the children who were 12 years old or less. From 2009 to 2014, there

was a 5% decrease in the annual eatings per capita in vegetables, yet their consumption of fruits

remained the same (pbhfoundation.org, 24). The last age group that we analyzed was adults who

are 45 years old or older. This age group experienced a 12% decrease in the annual eatings per

capita, along with a decrease of 11% in the annual eatings per capita for fruit. According to the

2015 Study on America’s Consumption of Fruits & Vegetables, reason behind the lack of

vegetables that are being consumed is because of the type of meals people are eating. Today,

people are shifting from having meals ‘center of the plate’ protein meals, which often consists a

45

Calabrese, Lihou, Sponable, Walsh

vegetable as a side, to faster alternatives, like pizza, sandwiches, or soups (pbhfoundation.org,

24) Unlike the ‘center of the plate’ protein meals, these faster alternatives do not have side

dishes, thus contributing to the lack of vegetables being eaten.

Another demographic our group looked at was gender. By analyzing both males and

females, we can get a better understanding of who we should target our product to. First, we

looked at the male demographic. Males who are 45 or older have been reported to have a large

decline in the consumption of vegetables from 2009 to 2014, and the consumption of fruits too.

Looking at the younger demographic of males, ages 18 through 34, they are consuming more

fruits and vegetables. In the 2015 Study on America’s Consumption of Fruits & Vegetables, chart

32 shows that the annual eatings per capita for vegetable for this particular male demographic has

raised from 349 pounds to 351 pounds. The same happened for the annual eatings per capita for

fruits, resulting in an increase from 122 pounds to 128 pounds. Like the males who are 45 or

older, females in the same age group also are not eating as much of vegetables as they once did.

In five years, females have also had a significantly large decrease in annual eatings per capita for

both vegetables and fruit. Unlike the younger male demographic, the younger females not

consuming as much of vegetables (6% decrease), but are consuming more fruits (2% increase)

(pbhfoundation.org, 27).

The last demographic we analyzed was regions in the United States. There are nine

regions that are located in the United States, they include: New England, Middle Atlantic, South

Atlantic, West South Central, East South Central, West North Central, East North Central,

Mountain, and Pacific. According to data from 2014, regions such as the Pacific, New England,

and the West North Central, are consuming the most amount of fruits and vegetables in the

United States. With that being said, our group should target these specific regions in order for our

product to have the proper exposure. In contrast, regions such as the East South Central and West

46

Calabrese, Lihou, Sponable, Walsh

South Central reported to have a decrease in the consumption of vegetables, along the significant

decline of fruits consumed in the the East South Central and the West South Central regions.

With that information, our group know not to target those regions when we market our product.

c) Evolving customer needs

Although we may be concerned with our customers now, we need to think about our current

and potential customers needs in the future. To pay attention to our customers needs, we need to

be up to date with the ongoing trends that are in our market. For example, from the data that we

observed, from 2009 to 2014 both children and adults are not consuming enough vegetables. This

can be tied to the shifting of the types of meals people are eating. Initially, people were having

meals that consisted of a piece of protein, such as chicken, fish or pork, along with a side of

vegetables. Today, Americans are gravitating away from these kinds of meals and finding

something that is more convenient, like pizza, soups, frozen dishes, etc. Thus, resulting in this

downward shift of vegetable consumption among people. With that in mind, we need to make our

product convenient for people to obtain. If our product is convenient to get your hands on, people

will continue to buy the product, resulting to an increase of vegetables being consumed by

people. We should also keep in mind the poor health diet that is associated with Americans. Our

product is a healthier alternative compared to other frozen food options, which in a way will

promote a healthier lifestyle. Because people are consuming less vegetables, our company needs

to bring attention back to vegetables and incorporate them back into people's lifestyles.

According this particular study, it is predicted that there will be a 4% increase in the consumption

of vegetables and fruits within the next five years (pbhfoundation.org, 7).

5. What opportunities or threats exist in this particular market?

The frozen food industry has a promising future. It is growing due to consumers’ changing ways

47

Calabrese, Lihou, Sponable, Walsh

of consumption towards frozen food. But because the industry is prosperous, a lot of companies

are bidding on it, which increases a lot the competition.

The frozen food industry market has a lot of opportunities. Firstly, the industry is benefiting from

an increasing consumption: according to the Frozen Food Market in the U.S analysis conducted