Embed Size (px)

Citation preview

1

2

2Q10 Earnings

Results Presentation

08/12/2010

3

This release contains forward-looking statements relating to the prospects of the business,

estimates for operating and financial results, and those related to growth prospects of TPI –

Triunfo Participações e Investimentos S.A.. These are merely projections and, as such, are

based exclusively on the expectations of the Company’s management concerning the future of

the business. Such forward-looking statements depend substantially on changes in market

conditions, the performance of the Brazilian economy, the sector and the international markets,

and are, therefore, subject to changes without previous notice.

Forward-Looking Statements

4

Digite aqui o Título

da Palestra

Digite aqui o Nome do Palestrante e a Data

I - Highlights

5

I - Highlights

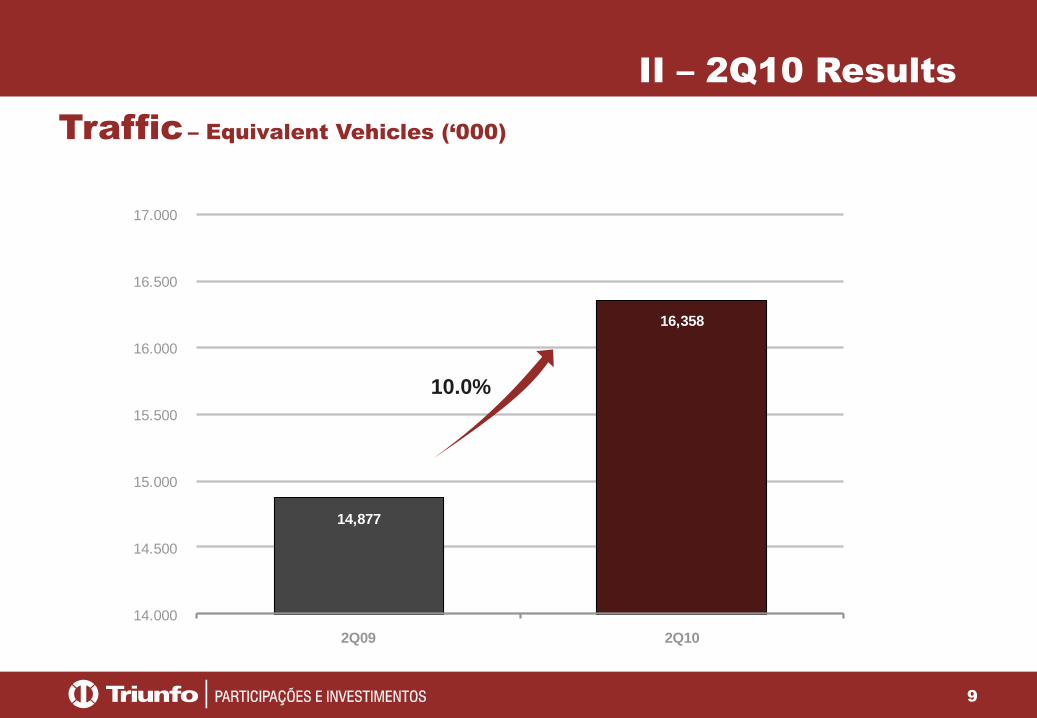

Total traffic volume on our toll road concessions grew 10.0% year-on-year to 16,358,000

equivalent vehicles.

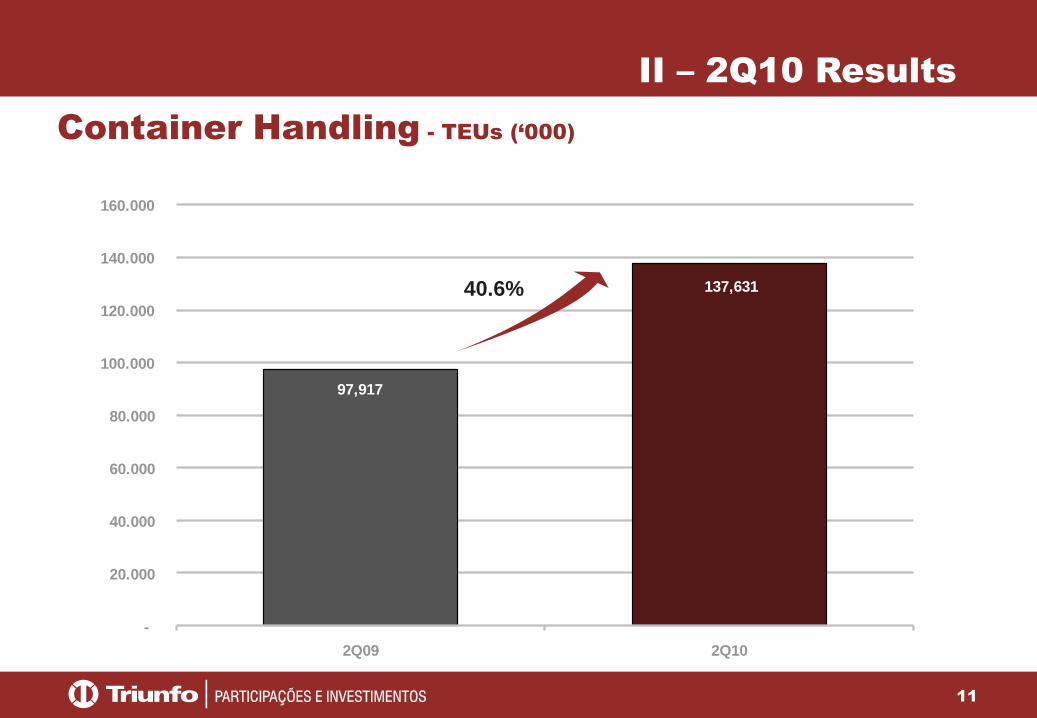

Handled container volume climbed by 40.6% over 2Q09 to 137,631 TEUs.

Electricity output totaled 47,188 MW in 2Q10, generation revenue of R$6.388 million.

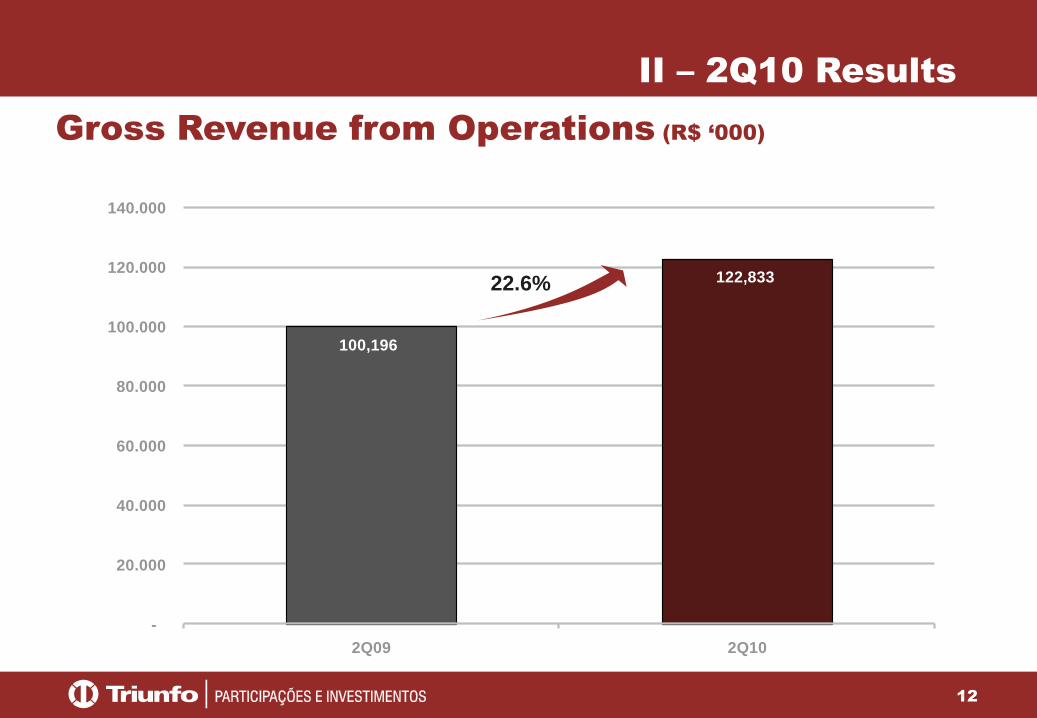

Gross Revenue increased by 22.6% in 2Q10 over the same period last year, reaching

R$122.833 million.

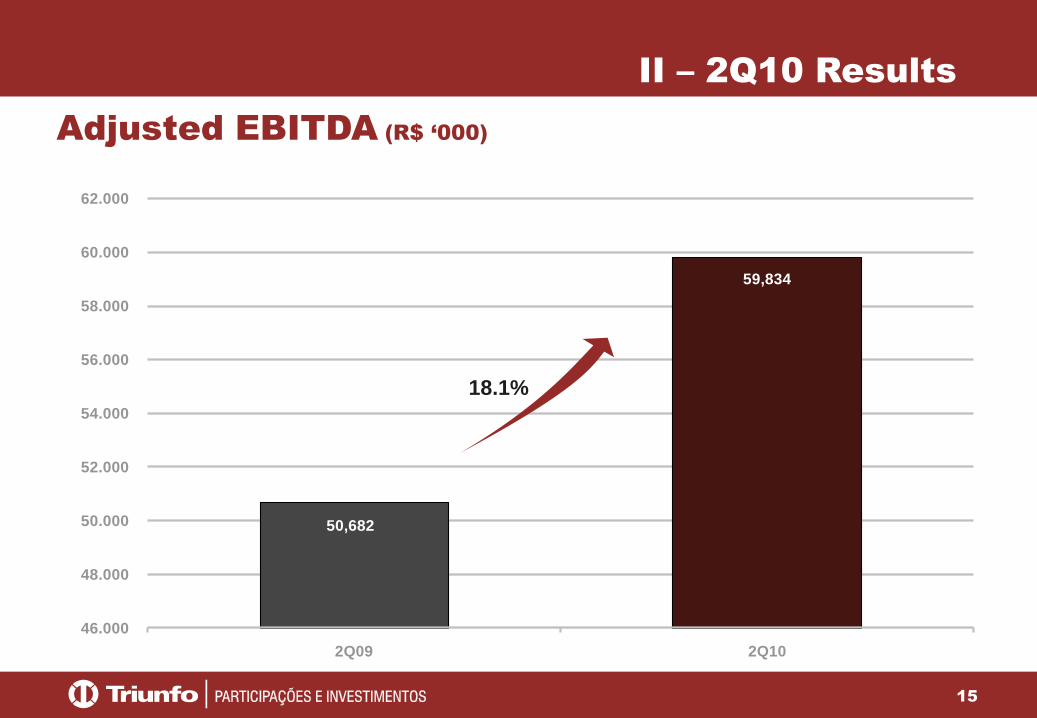

EBITDA grew by 18.10% to R$59.834 million.

6

I - Highlights

On April 29, Triunfo disclosed the reconciliation between BR GAAP and IFRS, pursuant to the

Novo Mercado listing rules.

On May 25, Rio Verde Energia announced the commercial start-up of the Salto hydroelectric

plant’s first turbine.

On June 25, an Extraordinary General Meeting approved the Company’s 2nd Public Issue of

Simple Debentures, elected the Audit and Finance Committee and incorporated the

subsidiary Esparta.

7

I – Subsequent Events

On July 20, Portonave signed an agreement with the unions representing the Santa Catarina

port employees (OGMO).

On July 30, Triunfo presented the lowest tariff at the auction of the Garibaldi hydroelectric

plant, on the Canoas River. The concession is for 35 years and 70% of the plant’s assured

energy has already been sold.

8

Digite aqui o Título

da Palestra

Digite aqui o Nome do Palestrante e a Data

II – 2Q10 Results

9

14,877

16,358

14.000

14.500

15.000

15.500

16.000

16.500

17.000

2Q09 2Q10

Traffic – Equivalent Vehicles (‘000)

II – 2Q10 Results

10.0%

10

3,028 3,359

5,925 6,395

5,924

6,604

-

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

9.000

10.000

2Q09 2Q10 2Q09 2Q10 2Q09 2Q10

Traffic – Equivalent vehicles in the concessionaries (‘000)

II – 2Q10 Results

ECONORTE CONCER CONCEPA

10.9%

7.9%11.5%

11

97,917

137,631

-

20.000

40.000

60.000

80.000

100.000

120.000

140.000

160.000

2Q09 2Q10

Container Handling - TEUs (‘000)

II – 2Q10 Results

40.6%

12

100,196

122,833

-

20.000

40.000

60.000

80.000

100.000

120.000

140.000

2Q09 2Q10

Gross Revenue from Operations (R$ ‘000)

II – 2Q10 Results

22.6%

13

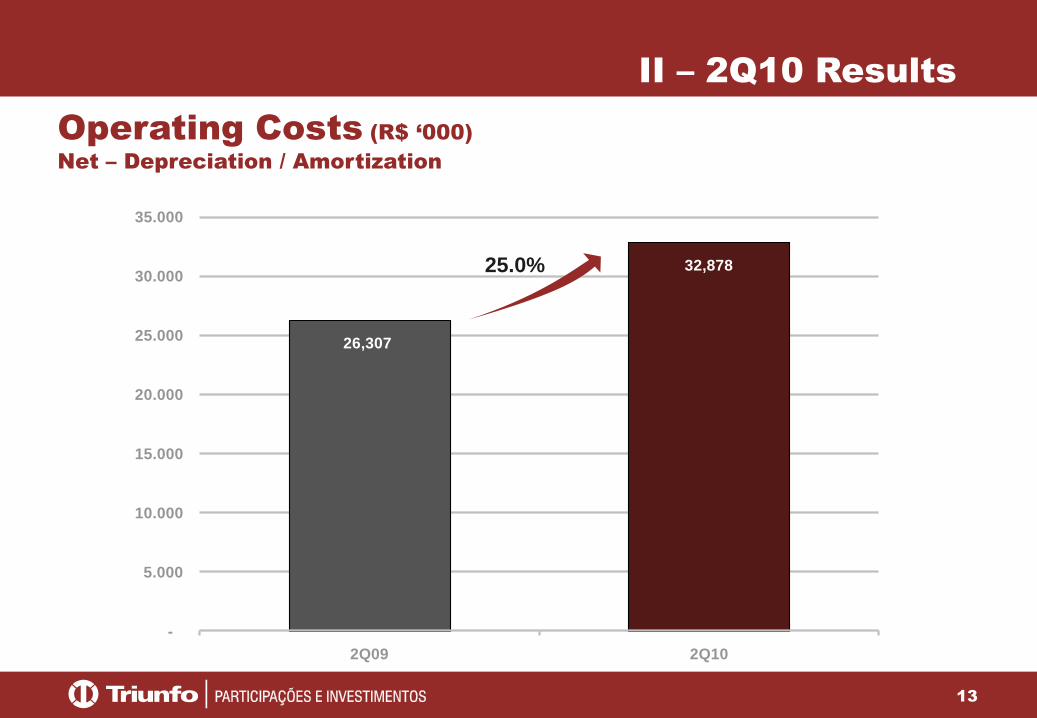

26,307

32,878

-

5.000

10.000

15.000

20.000

25.000

30.000

35.000

2Q09 2Q10

Operating Costs (R$ ‘000)

Net – Depreciation / Amortization

II – 2Q10 Results

25.0%

14

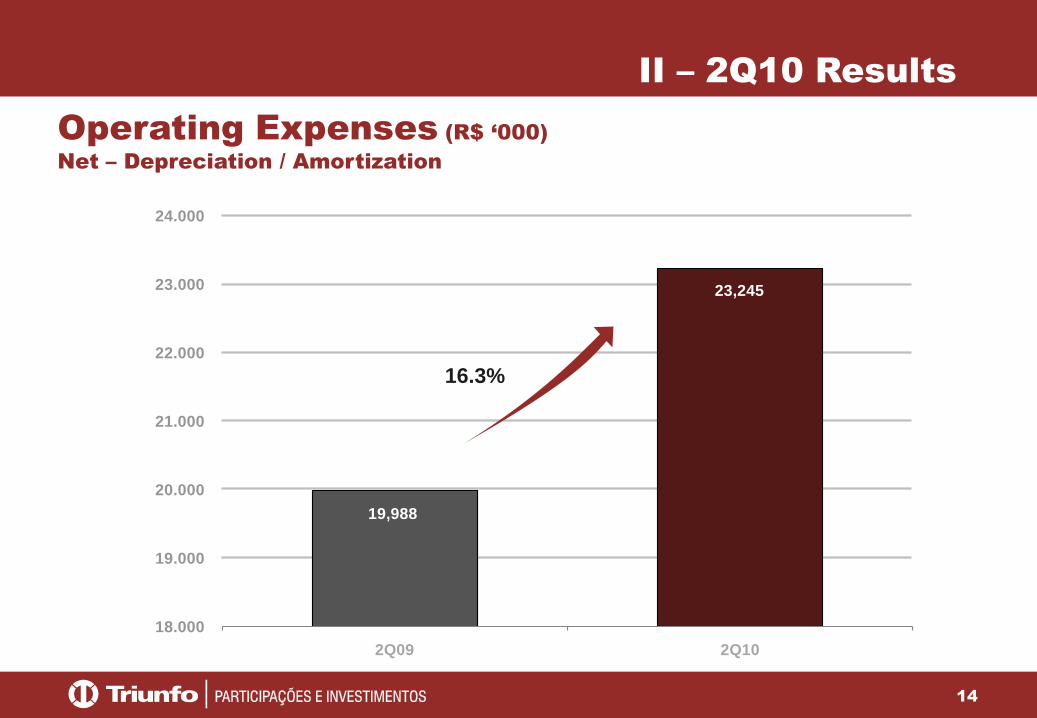

19,988

23,245

18.000

19.000

20.000

21.000

22.000

23.000

24.000

2Q09 2Q10

Operating Expenses (R$ ‘000)

Net – Depreciation / Amortization

II – 2Q10 Results

16.3%

15

50,682

59,834

46.000

48.000

50.000

52.000

54.000

56.000

58.000

60.000

62.000

2Q09 2Q10

Adjusted EBITDA (R$ ‘000)

II – 2Q10 Results

18.1%

16

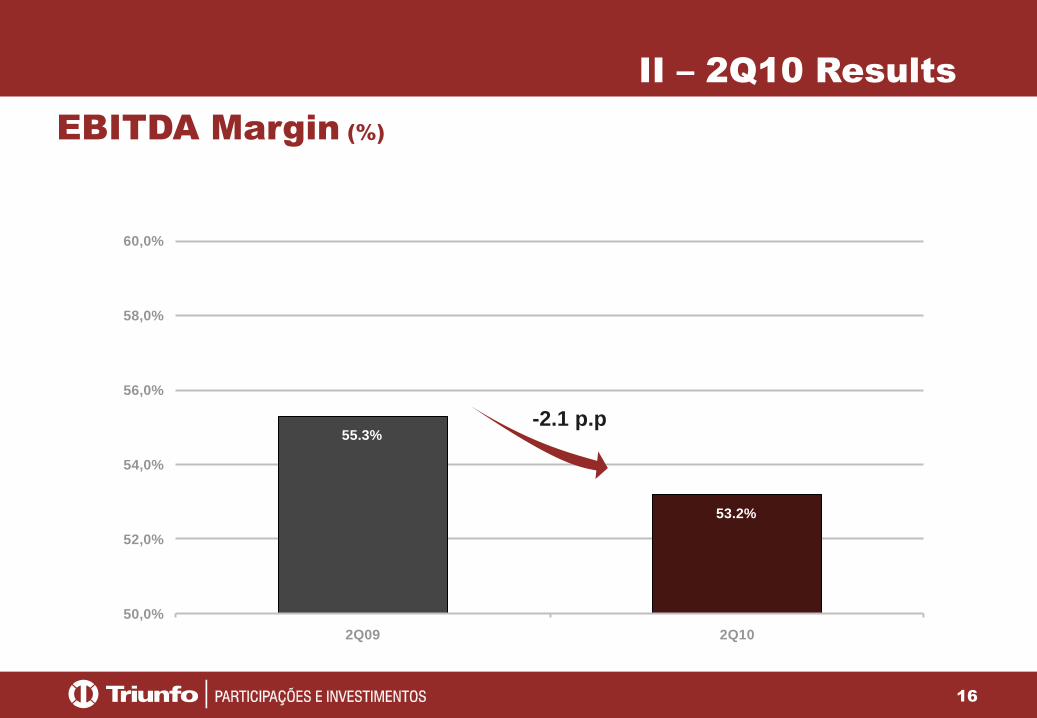

55.3%

53.2%

50,0%

52,0%

54,0%

56,0%

58,0%

60,0%

2Q09 2Q10

EBITDA Margin (%)

II – 2Q10 Results

-2.1 p.p

17

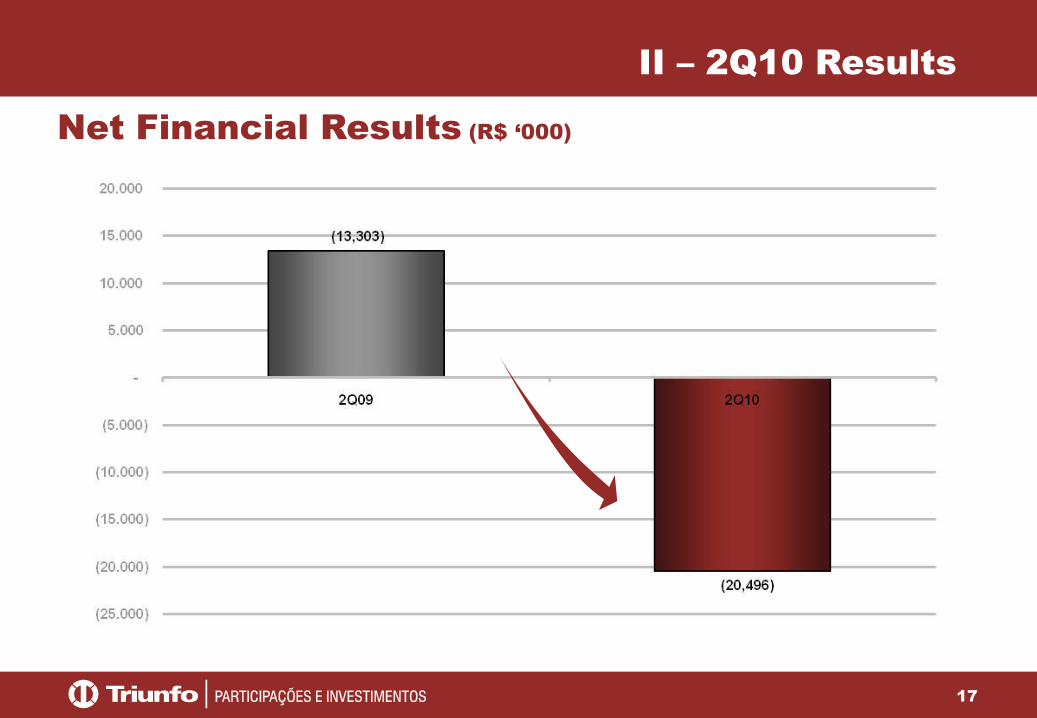

Net Financial Results (R$ ‘000)

II – 2Q10 Results

18

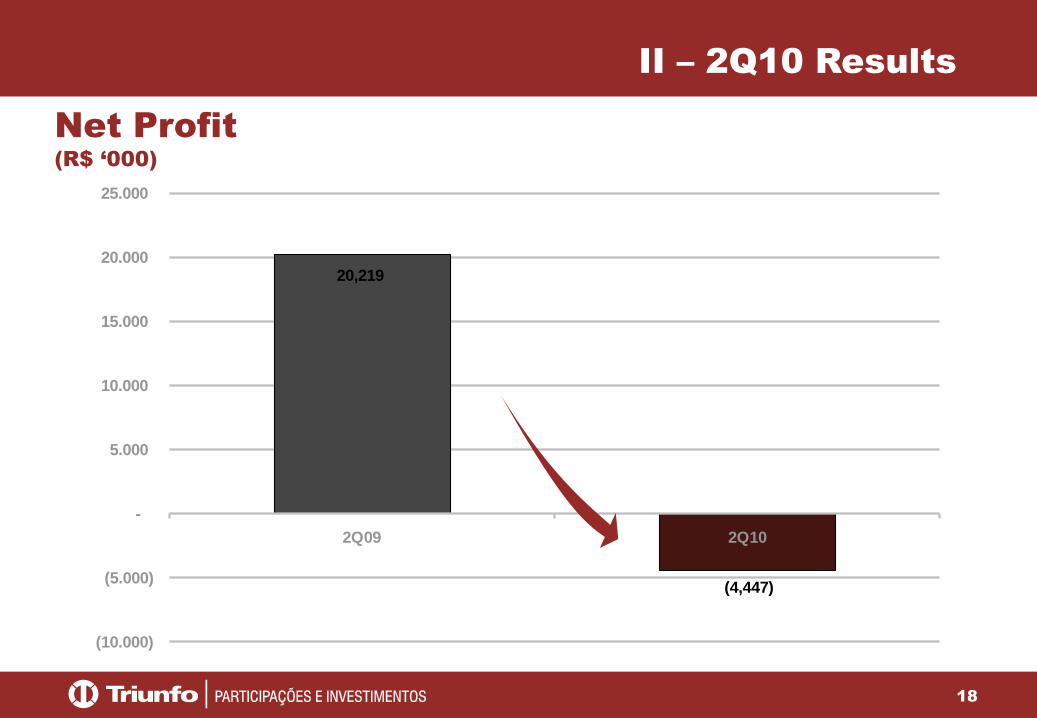

20,219

(4,447)

(10.000)

(5.000)

-

5.000

10.000

15.000

20.000

25.000

2Q09 2Q10

Net Profit

(R$ ‘000)

II – 2Q10 Results

19

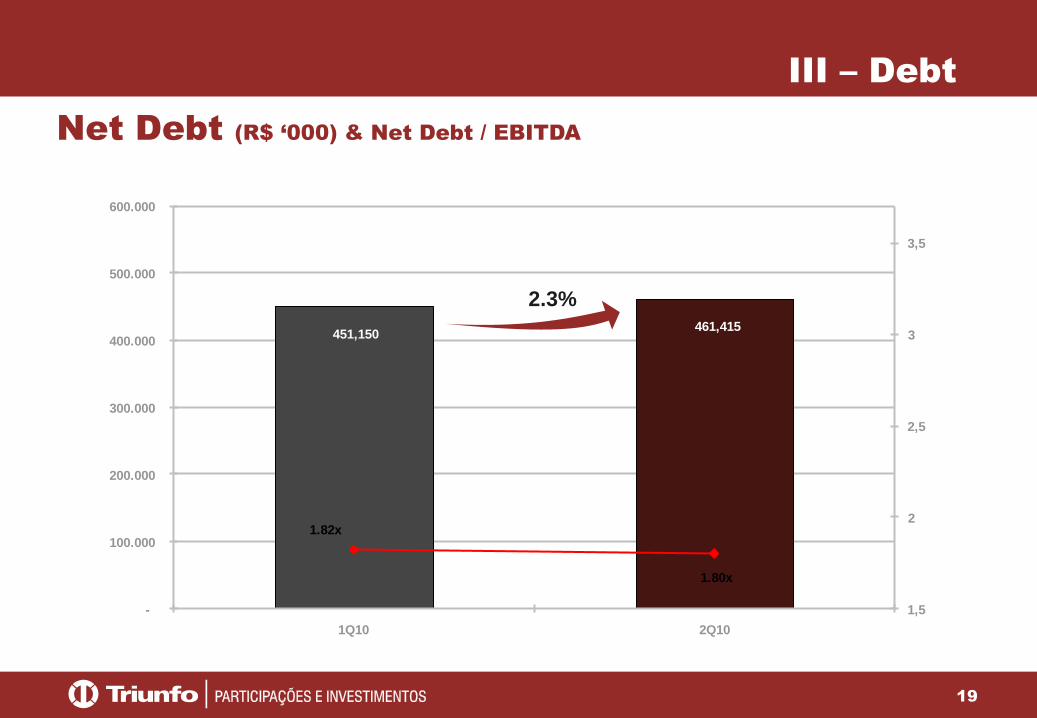

451,150 461,415

1.82x

1.80x

1,5

2

2,5

3

3,5

-

100.000

200.000

300.000

400.000

500.000

600.000

1Q10 2Q10

Net Debt (R$ ‘000) & Net Debt / EBITDA

III – Debt

2.3%

20

IV – Capex

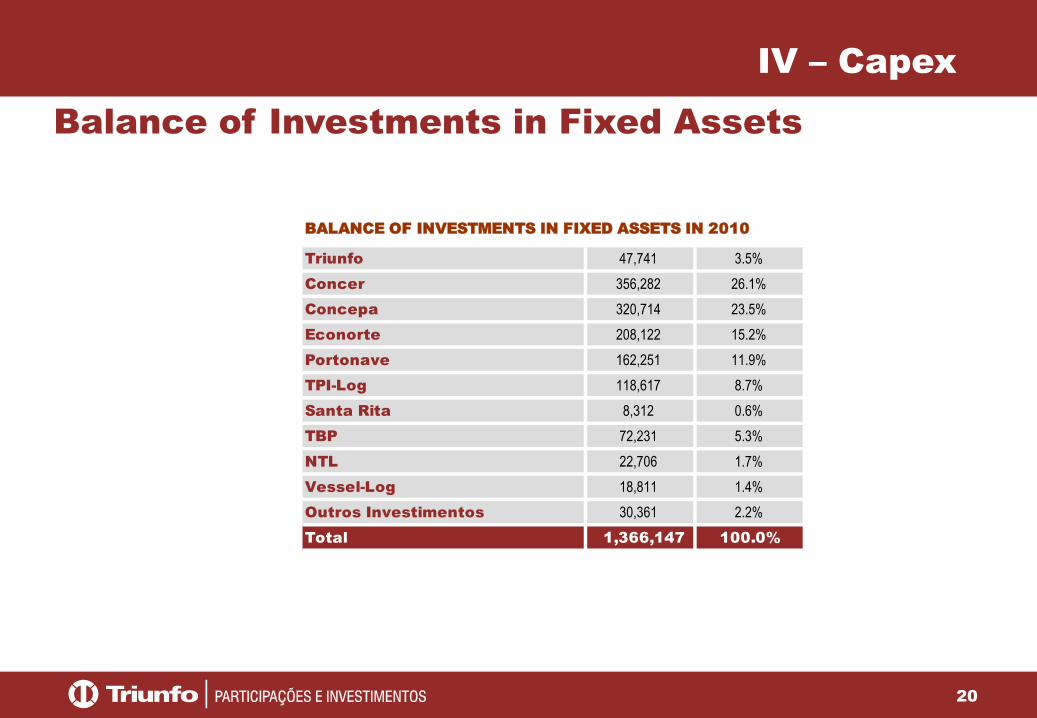

Balance of Investments in Fixed Assets

Triunfo 47,741 3.5%

Concer 356,282 26.1%

Concepa 320,714 23.5%

Econorte 208,122 15.2%

Portonave 162,251 11.9%

TPI-Log 118,617 8.7%

Santa Rita 8,312 0.6%

TBP 72,231 5.3%

NTL 22,706 1.7%

Vessel-Log 18,811 1.4%

Outros Investimentos 30,361 2.2%

Total 1,366,147 100.0%

BALANCE OF INVESTMENTS IN FIXED ASSETS IN 2010

21

IV – Capex

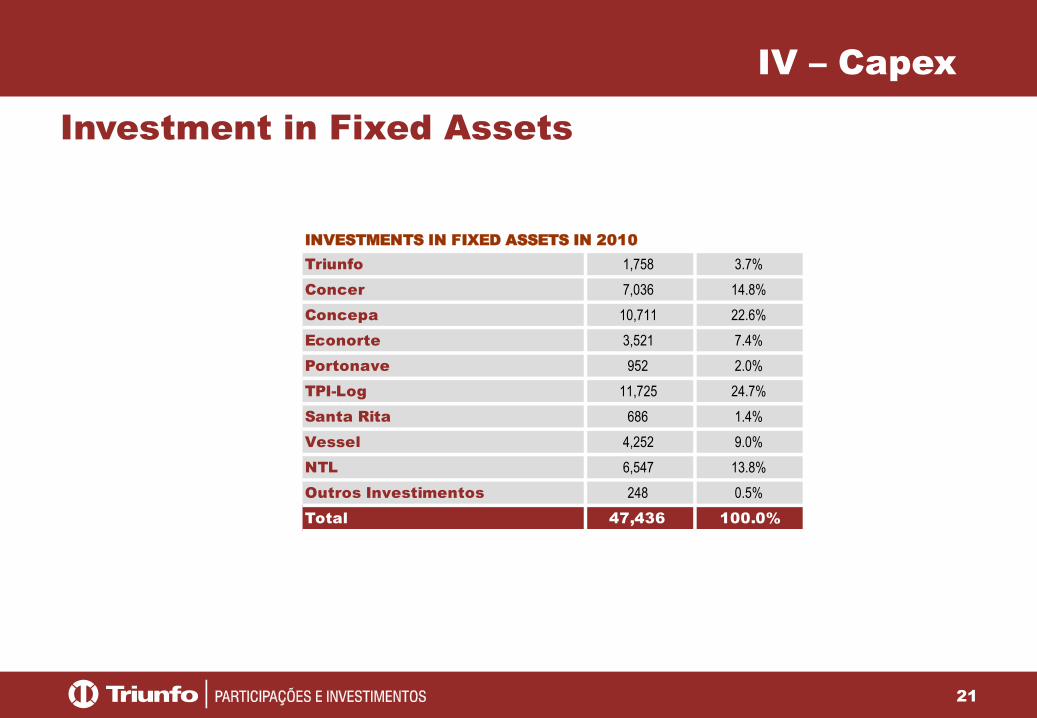

Investment in Fixed Assets

Triunfo 1,758 3.7%

Concer 7,036 14.8%

Concepa 10,711 22.6%

Econorte 3,521 7.4%

Portonave 952 2.0%

TPI-Log 11,725 24.7%

Santa Rita 686 1.4%

Vessel 4,252 9.0%

NTL 6,547 13.8%

Outros Investimentos 248 0.5%

Total 47,436 100.0%

INVESTMENTS IN FIXED ASSETS IN 2010

22

Digite aqui o Título

da Palestra

Digite aqui o Nome do Palestrante e a Data

UHE Garibaldi

23

Strategy

Mitigated geological risk

Known technical solution

Small reservoir

Relocation – Itá, Machadinho, Barra Grande, Campos Novos

Construction and operational logistics

Existing relations with the State of Santa Catarina (Portonave)

24

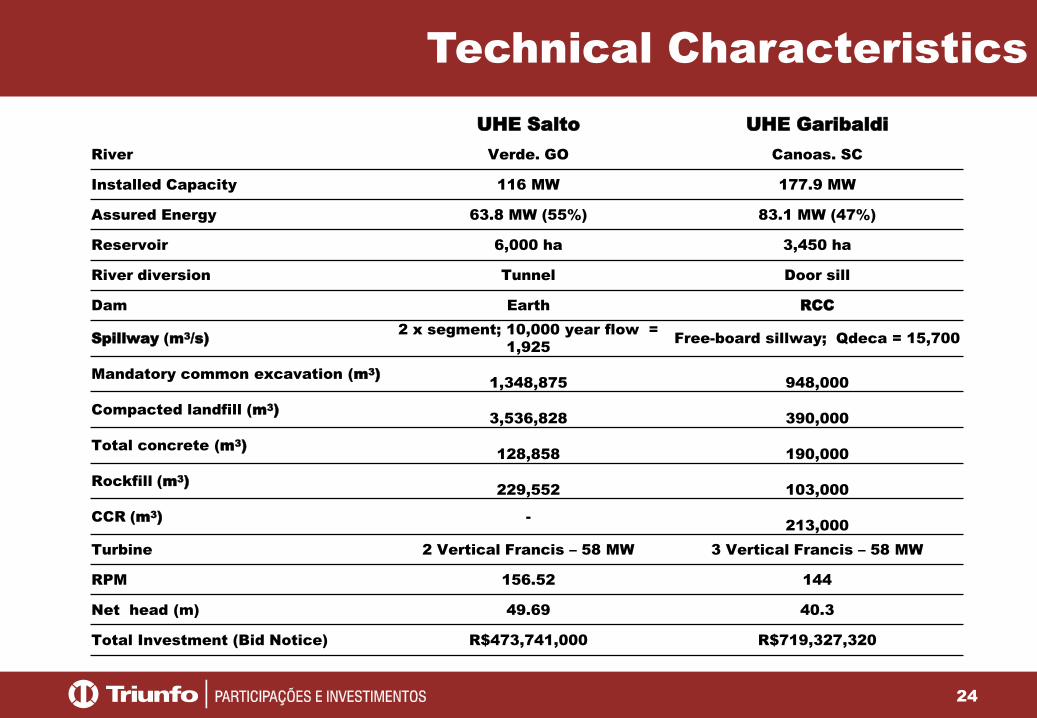

Technical Characteristics

UHE Salto UHE Garibaldi

River Verde. GO Canoas. SC

Installed Capacity 116 MW 177.9 MW

Assured Energy 63.8 MW (55%) 83.1 MW (47%)

Reservoir 6,000 ha 3,450 ha

River diversion Tunnel Door sill

Dam Earth RCC

Spillway (m3/s)2 x segment; 10,000 year flow =

1,925 Free-board sillway; Qdeca = 15,700

Mandatory common excavation (m3)1,348,875 948,000

Compacted landfill (m3)3,536,828 390,000

Total concrete (m3)128,858 190,000

Rockfill (m3)229,552 103,000

CCR (m3) -213,000

Turbine 2 Vertical Francis – 58 MW 3 Vertical Francis – 58 MW

RPM 156.52 144

Net head (m) 49.69 40.3

Total Investment (Bid Notice) R$473,741,000 R$719,327,320

25

Location

26

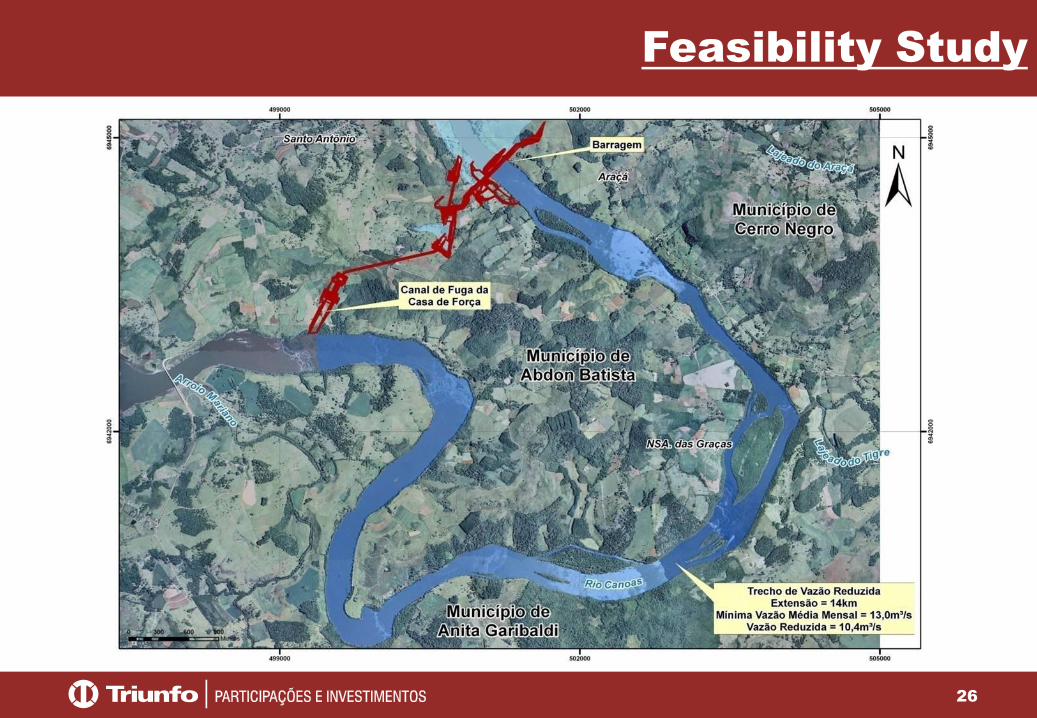

Feasibility Study

27

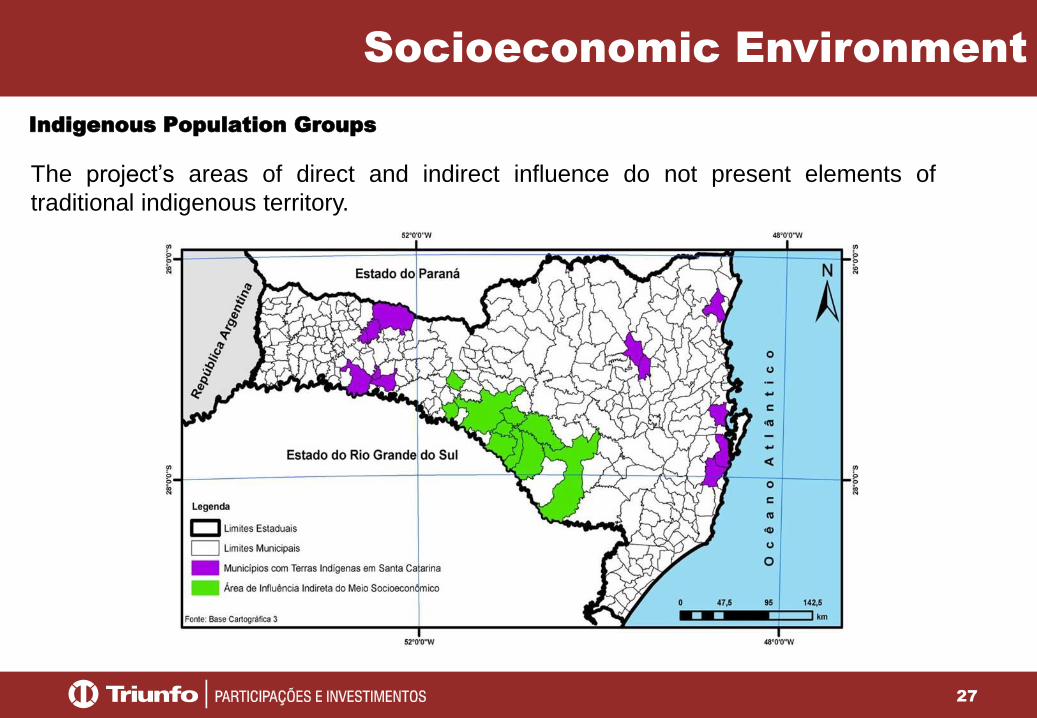

Indigenous Population Groups

The project’s areas of direct and indirect influence do not present elements of

traditional indigenous territory.

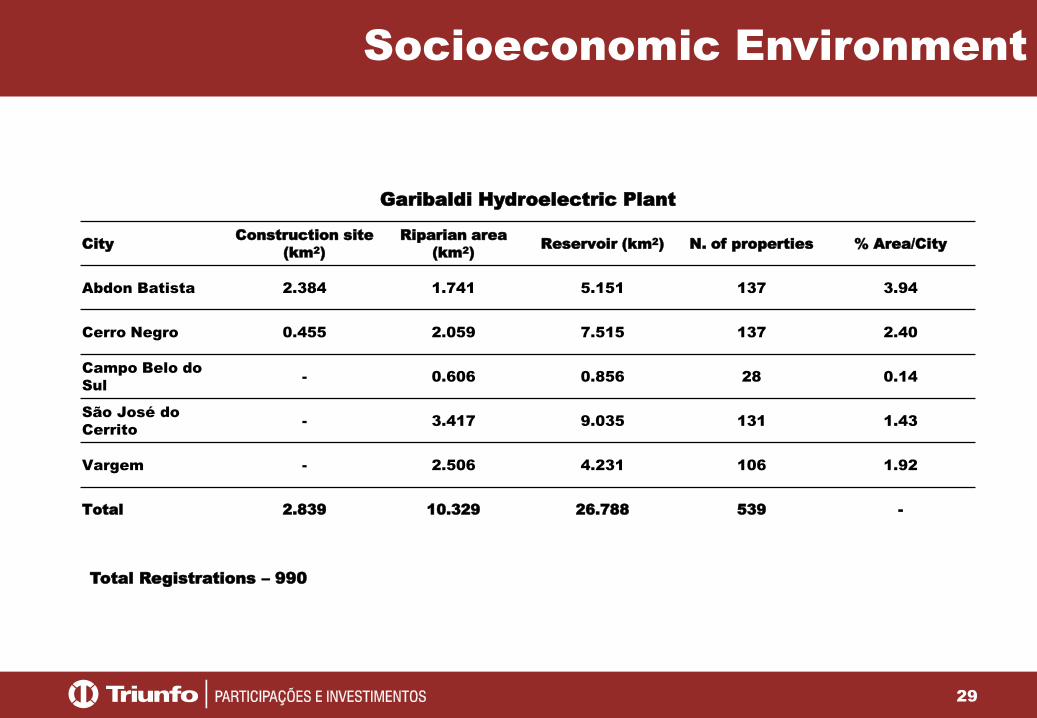

Socioeconomic Environment

28

Socioeconomic Environment

29

Total Registrations – 990

Garibaldi Hydroelectric Plant

CityConstruction site

(km2)

Riparian area

(km2)Reservoir (km2) N. of properties % Area/City

Abdon Batista 2.384 1.741 5.151 137 3.94

Cerro Negro 0.455 2.059 7.515 137 2.40

Campo Belo do

Sul- 0.606 0.856 28 0.14

São José do

Cerrito- 3.417 9.035 131 1.43

Vargem - 2.506 4.231 106 1.92

Total 2.839 10.329 26.788 539 -

Socioeconomic Environment

30

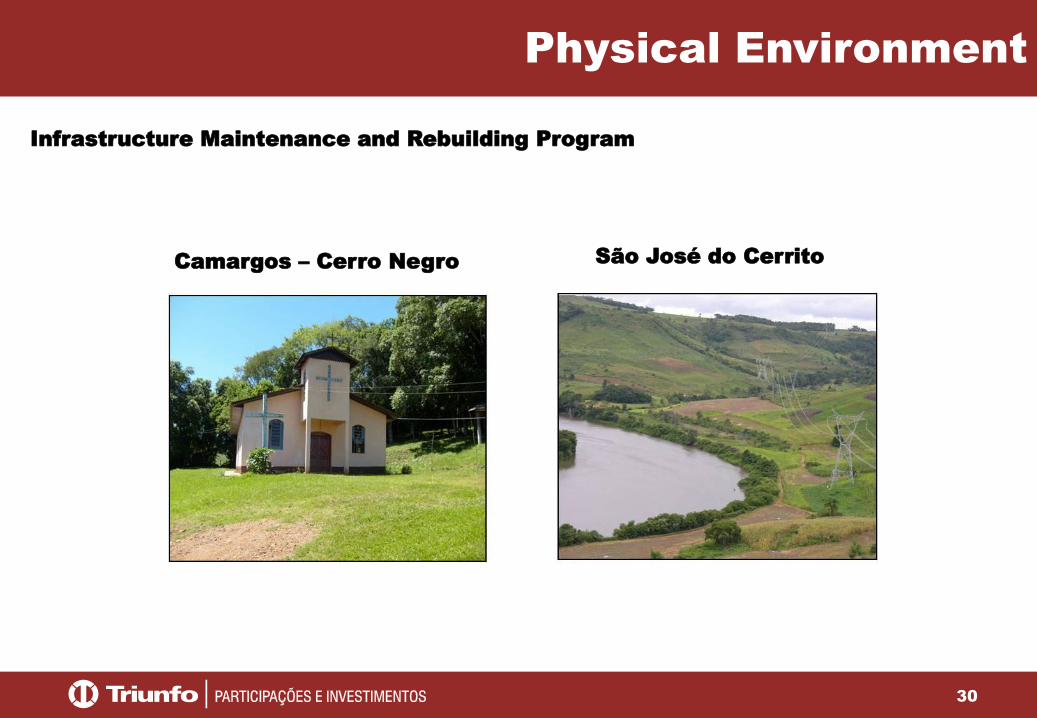

Camargos – Cerro Negro São José do Cerrito

Infrastructure Maintenance and Rebuilding Program

Physical Environment

31

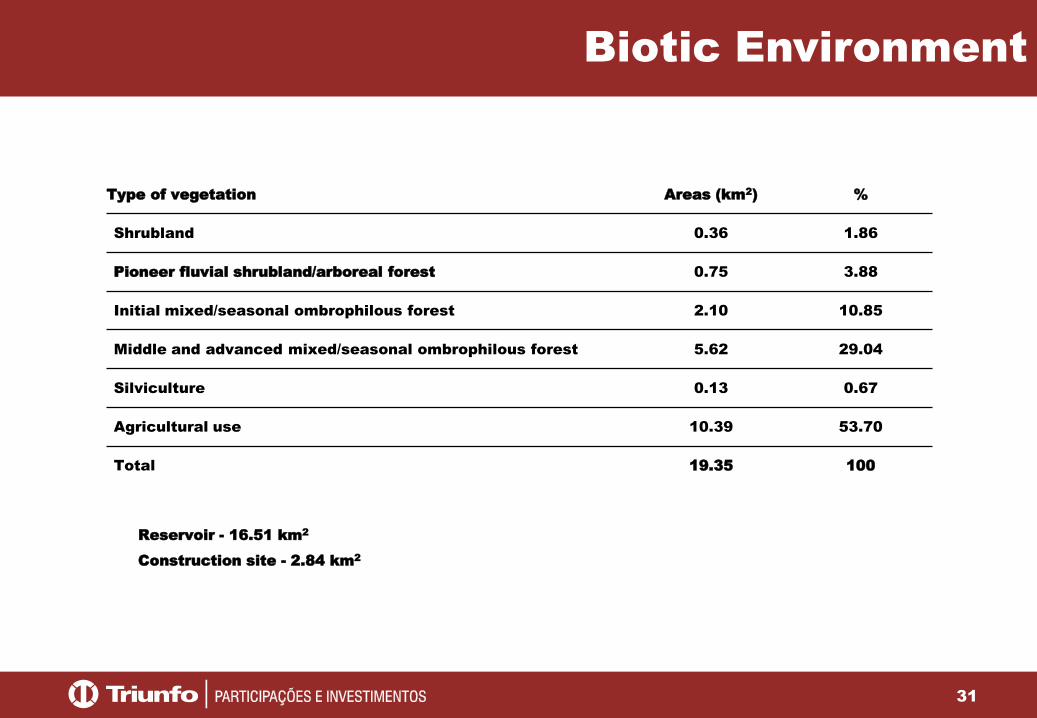

Reservoir - 16.51 km2

Construction site - 2.84 km2

Type of vegetation Areas (km2) %

Shrubland 0.36 1.86

Pioneer fluvial shrubland/arboreal forest 0.75 3.88

Initial mixed/seasonal ombrophilous forest 2.10 10.85

Middle and advanced mixed/seasonal ombrophilous forest 5.62 29.04

Silviculture 0.13 0.67

Agricultural use 10.39 53.70

Total 19.35 100

Biotic Environment

32

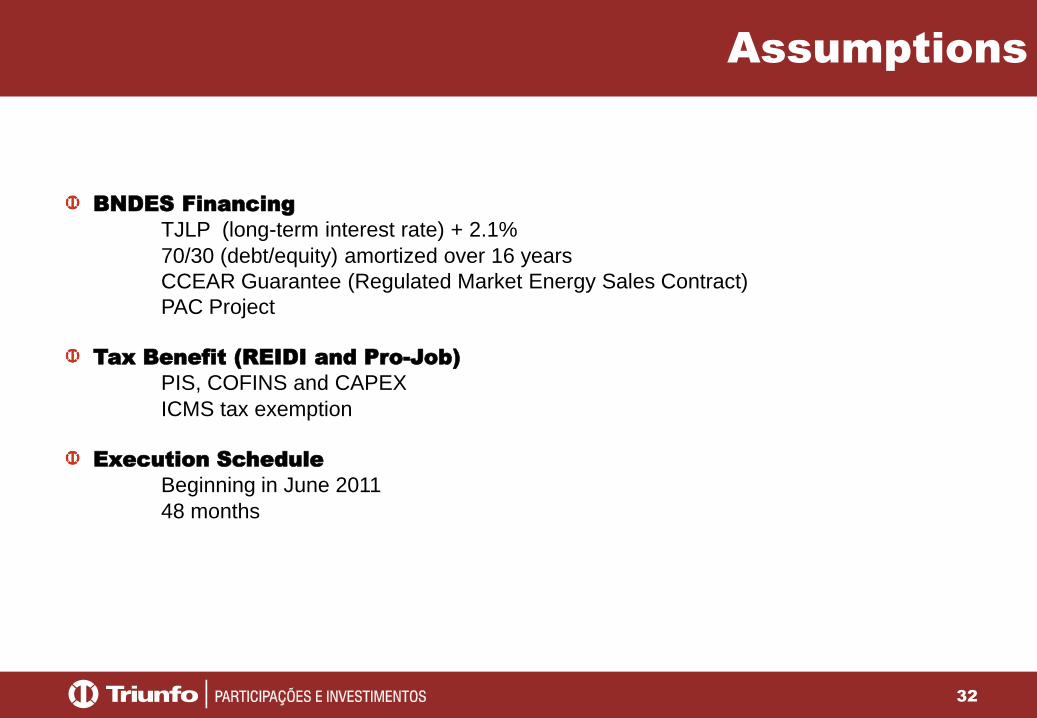

BNDES Financing

TJLP (long-term interest rate) + 2.1%

70/30 (debt/equity) amortized over 16 years

CCEAR Guarantee (Regulated Market Energy Sales Contract)

PAC Project

Tax Benefit (REIDI and Pro-Job)

PIS, COFINS and CAPEX

ICMS tax exemption

Execution Schedule

Beginning in June 2011

48 months

Assumptions

33

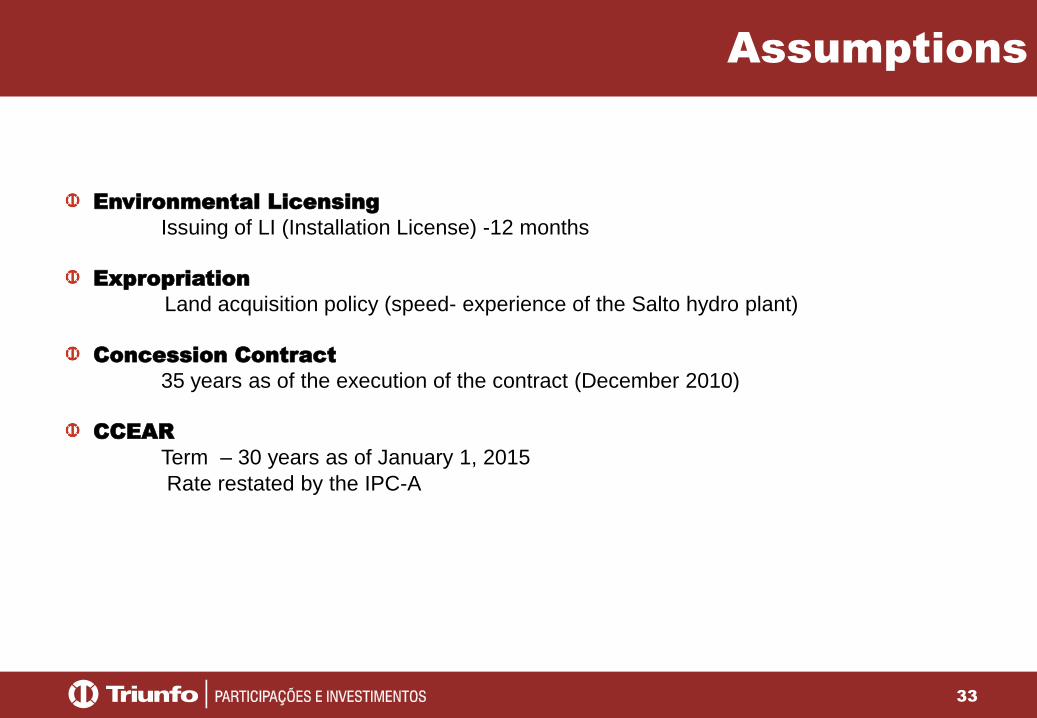

Assumptions

Environmental Licensing

Issuing of LI (Installation License) -12 months

Expropriation

Land acquisition policy (speed- experience of the Salto hydro plant)

Concession Contract

35 years as of the execution of the contract (December 2010)

CCEAR

Term – 30 years as of January 1, 2015

Rate restated by the IPC-A

34

Assumptions

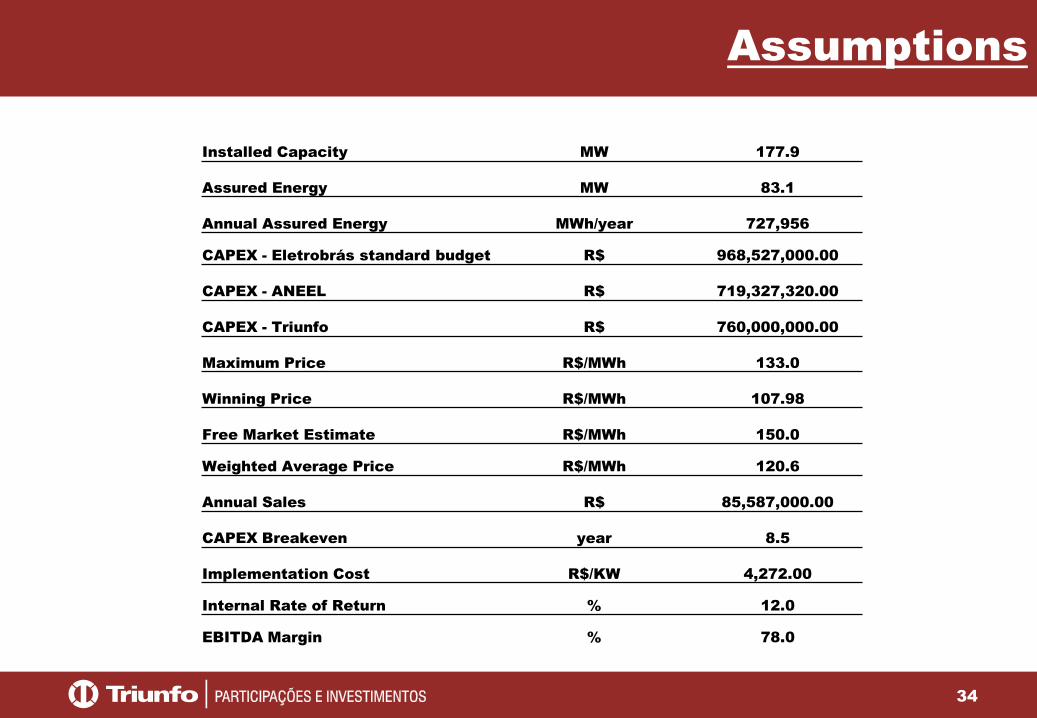

Installed Capacity MW 177.9

Assured Energy MW 83.1

Annual Assured Energy MWh/year 727,956

CAPEX - Eletrobrás standard budget R$ 968,527,000.00

CAPEX - ANEEL R$ 719,327,320.00

CAPEX - Triunfo R$ 760,000,000.00

Maximum Price R$/MWh 133.0

Winning Price R$/MWh 107.98

Free Market Estimate R$/MWh 150.0

Weighted Average Price R$/MWh 120.6

Annual Sales R$ 85,587,000.00

CAPEX Breakeven year 8.5

Implementation Cost R$/KW 4,272.00

Internal Rate of Return % 12.0

EBITDA Margin % 78.0

35

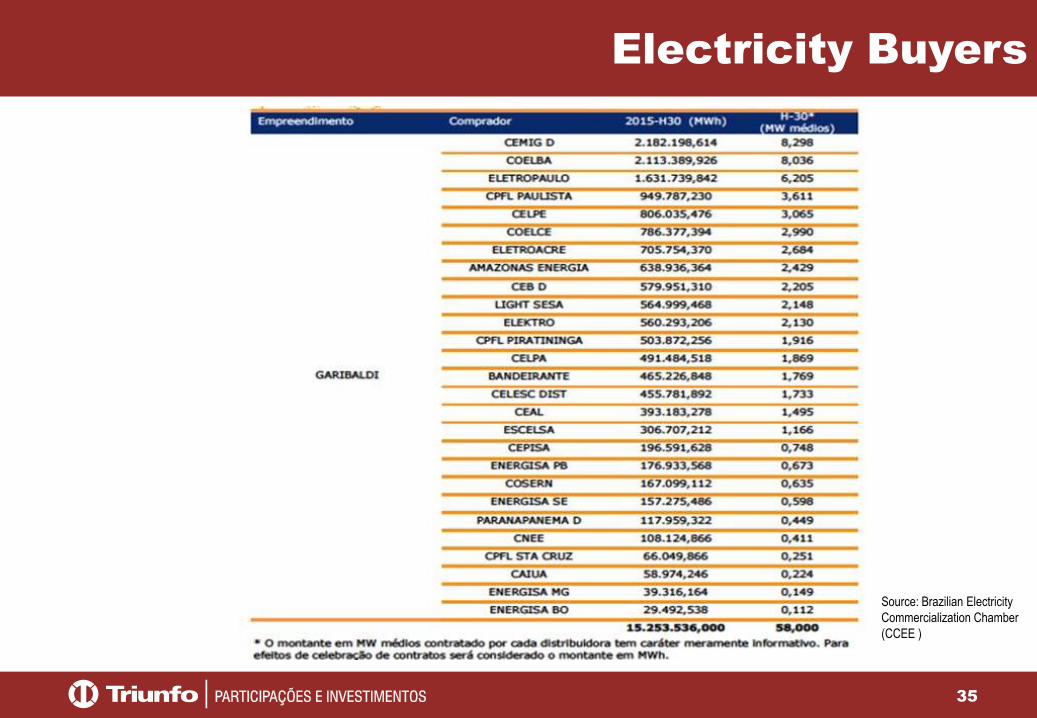

Electricity Buyers

Source: Brazilian Electricity

Commercialization Chamber

(CCEE )

36

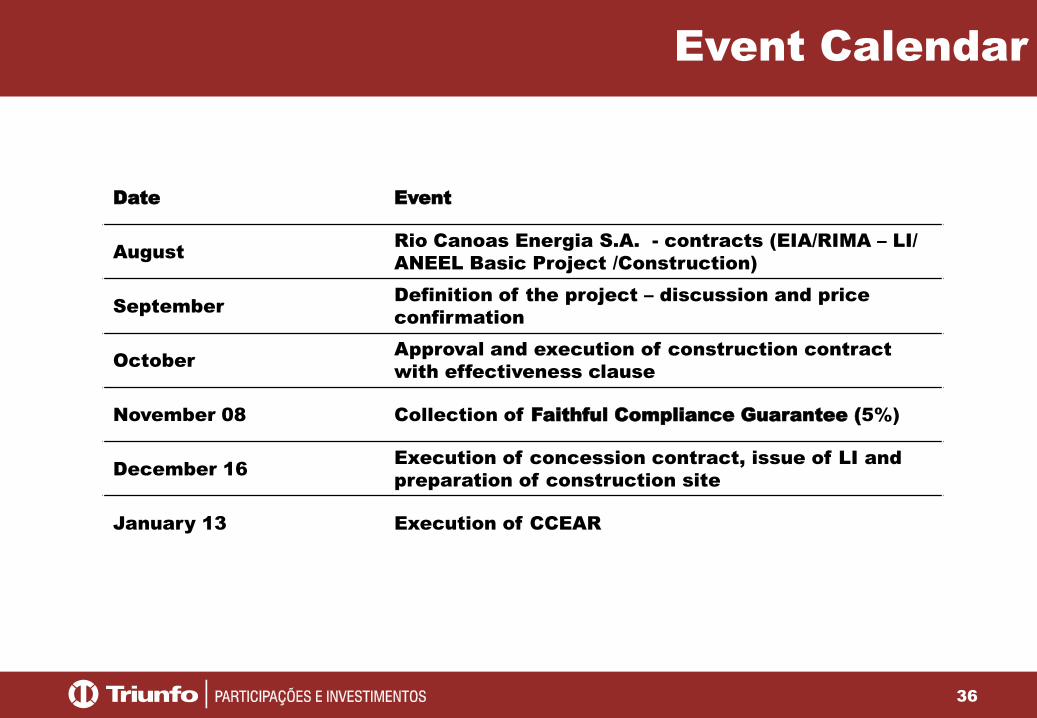

Event Calendar

Date Event

AugustRio Canoas Energia S.A. - contracts (EIA/RIMA – LI/

ANEEL Basic Project /Construction)

SeptemberDefinition of the project – discussion and price

confirmation

OctoberApproval and execution of construction contract

with effectiveness clause

November 08 Collection of Faithful Compliance Guarantee (5%)

December 16Execution of concession contract, issue of LI and

preparation of construction site

January 13 Execution of CCEAR

37

www.tpisa.com.br

Tr iunf o São Paulo

Rua Olimpíadas 205 14º andar cj. 1402

CEP 04551-000 São Paulo SP BRFone 55 11 2169 3999

Fax 55 11 2169 3969

Rua Olimpíadas 205 14º andar cj. 1402 CEP 04551-000 São Paulo SP BR

Fone 55 11 2169 3999 Fax 55 11 2169 3939

www.triunfo.com