Embed Size (px)

Citation preview

23 April 2009

José Gijon Spalla Head, Africa Desk

OECD Development Centre

Africa and the global crisis: Impact and way forward

Africa Forum, Paris5 June, 2009

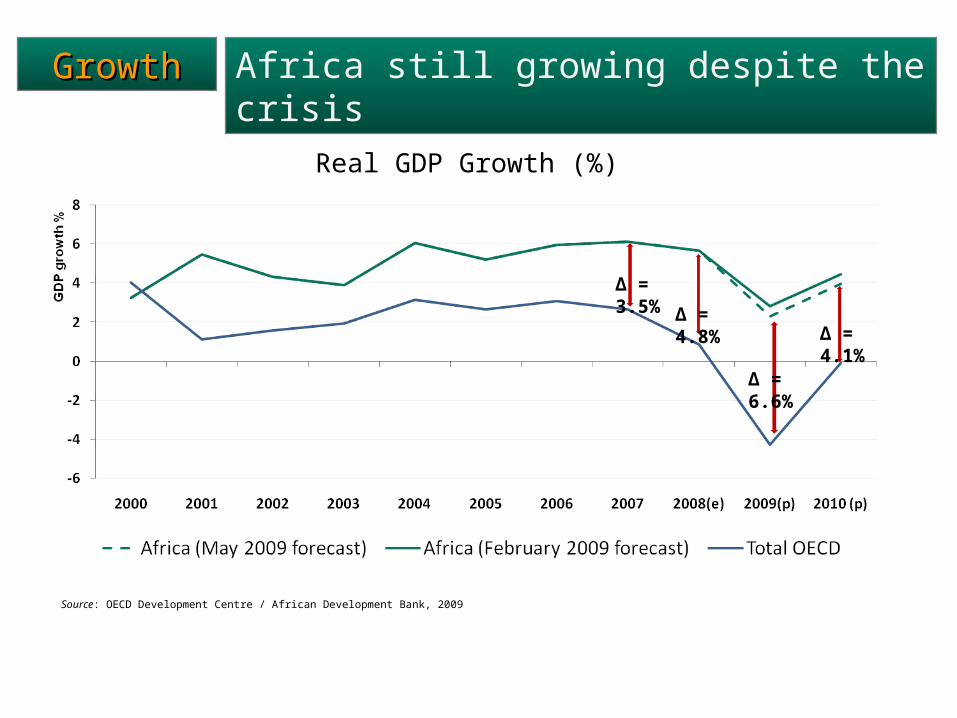

GrowthGrowth Africa still growing despite the crisis

Source: OECD Development Centre / African Development Bank, 2009

Δ = 6.6%

Δ = 4.1%

Δ = 3.5%

Δ = 4.8%

Real GDP Growth (%)

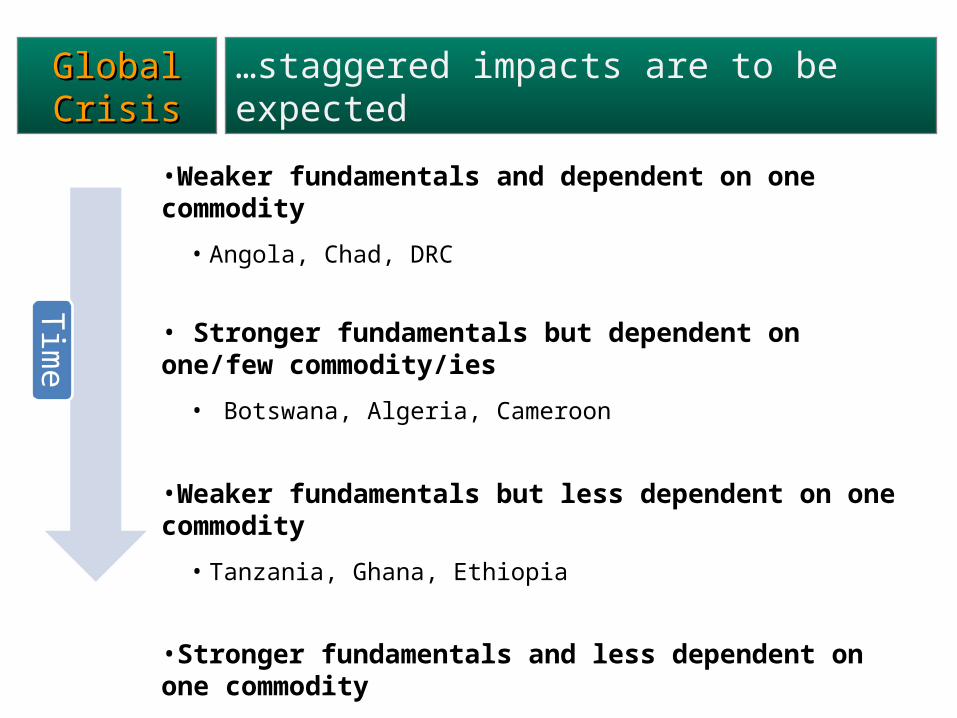

Global CrisisGlobal Crisis …staggered impacts are to be expected

•Weaker fundamentals and dependent on one commodity

• Angola, Chad, DRC

• Stronger fundamentals but dependent on one/few commodity/ies

• Botswana, Algeria, Cameroon

•Weaker fundamentals but less dependent on one commodity

• Tanzania, Ghana, Ethiopia

•Stronger fundamentals and less dependent on one commodity

• Tunisia, Uganda, Kenya

Time

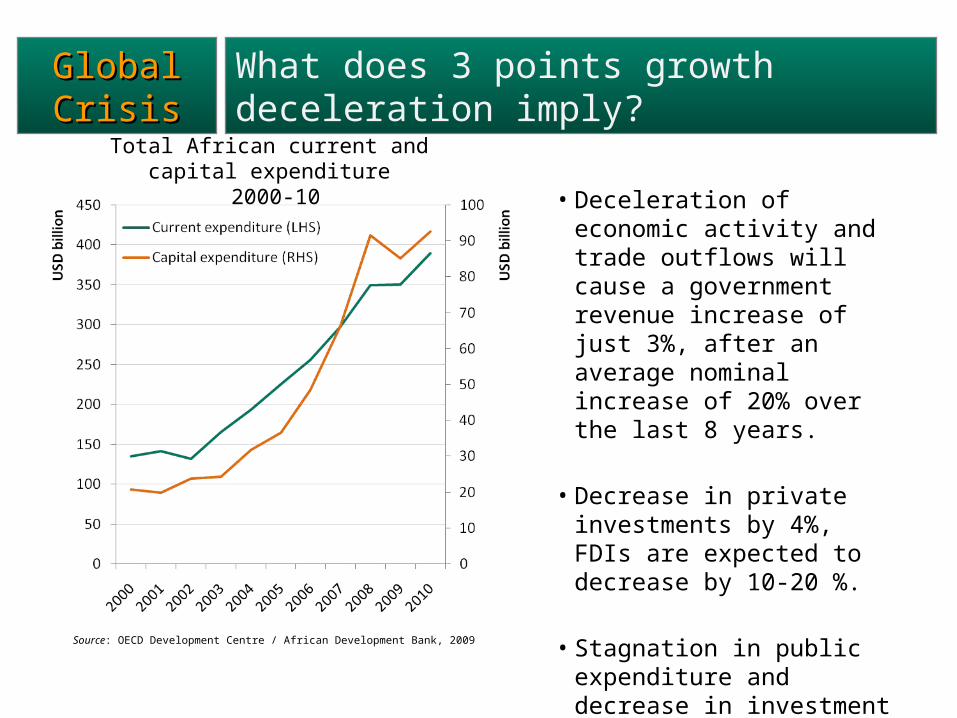

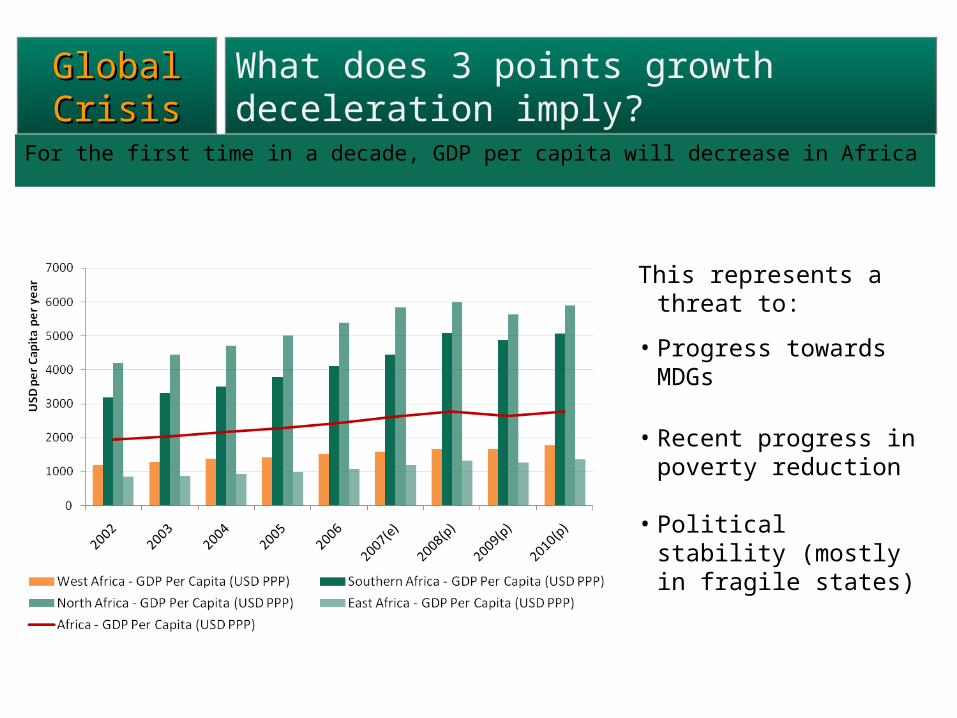

Global CrisisGlobal Crisis What does 3 points growth deceleration imply?

• Deceleration of economic activity and trade outflows will cause a government revenue increase of just 3%, after an average nominal increase of 20% over the last 8 years.

• Decrease in private investments by 4%, FDIs are expected to decrease by 10-20 %.

• Stagnation in public expenditure and decrease in investment (7%) in 2009

Total African current and capital expenditure 2000-10

Source: OECD Development Centre / African Development Bank, 2009

For the first time in a decade, GDP per capita will decrease in Africa

Global CrisisGlobal Crisis What does 3 points growth deceleration imply?

This represents a threat to:

• Progress towards MDGs

• Recent progress in poverty reduction

• Political stability (mostly in fragile states)

Global CrisisGlobal Crisis Fiscal balances will deteriorate significantly

* Including grants** Excluding Zimbabwe, Estimations for 20078and predictions for 2009/10

Source: OECD Development Centre / African Development Bank, 2008

Inflation

Current Account

Fiscal balance

0

10

20

2000-05 2006 2007 2008(e) 2009(p) 2010(p)

infla

tion

%

Central East NorthSouth West AFRICA

Source: OECD Development Centre, African Economic Outlook, 2009

2008 (e) 2009 (p) February

2009 (p)May

External Current Account* (% GDP) 3.3 -4.4 -5.3

2008 (e) 2009 (p) February

2009 (p)May

Overall fiscal balance* (% GDP) 2.8 -5.4 -5.8

2008 (e) 2009 (p) February

2009 (p)May

Consumer prices 11.6 8.1 8.4

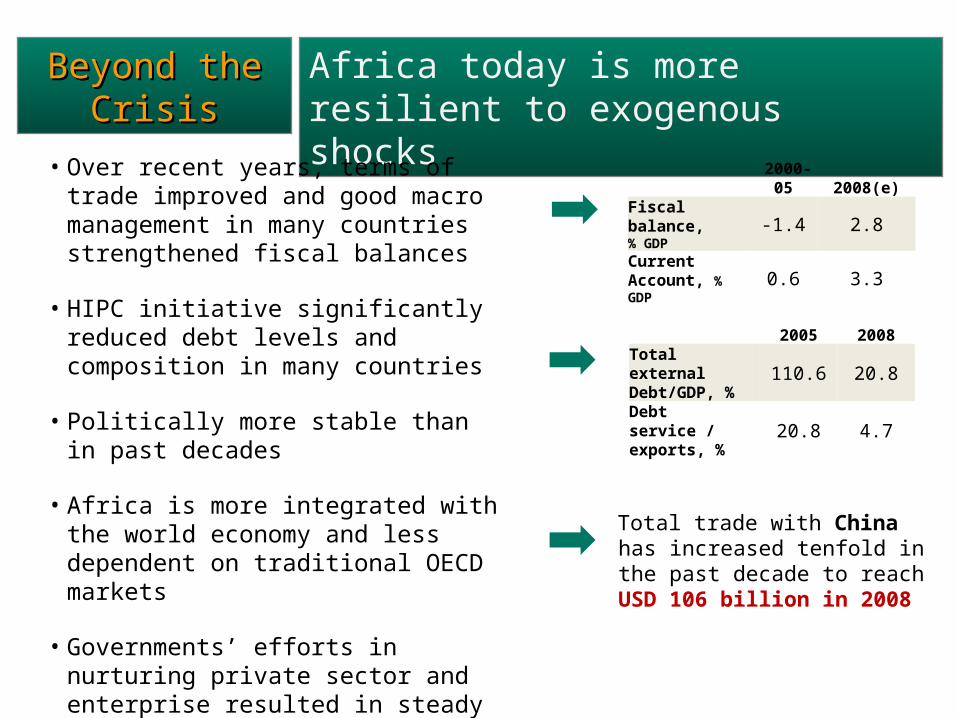

Beyond the CrisisBeyond the Crisis Africa today is more resilient to exogenous shocks

• Over recent years, terms of trade improved and good macro management in many countries strengthened fiscal balances

• HIPC initiative significantly reduced debt levels and composition in many countries

• Politically more stable than in past decades

• Africa is more integrated with the world economy and less dependent on traditional OECD markets

• Governments’ efforts in nurturing private sector and enterprise resulted in steady improvements in business climate indicators

2000-05 2008(e)Fiscal balance, % GDP -1.4 2.8

Current Account, % GDP 0.6 3.3

Total trade with China has increased tenfold in the past decade to reach USD 106 billion in 2008

2005 2008Total external Debt/GDP, % 110.6 20.8

Debt service / exports, % 20.8 4.7

It’s time for Africa to tap its unexploited potential

Beyond the CrisisBeyond the Crisis

AEO 09: Innovation and ICT• ICTs are an engine of endogenous growth : they contribute to improve

the local business environment by fostering markets development, overcoming infrastructural bottlenecks and reducing production costs

• ICTs foster human development allowing a better acces to basic services

• ICTs in Africa represent a new innovation fronteer , combining existing technologies with innovative applications, suited to the local environment and constraints.

•Domestic Markets: More attention should be given to fostering domestic investment and domestic demand

• Regional Markets: Only 9.5% of total African trade is regional

• Structural reforms are necessary to increase domestic resource mobilisation, overcome infrastructural hurdles and improve the business climate

23 April 2009

José Gijon Spalla Head, Africa Desk

OECD Development Centre

Africa and the global crisis: Impact and way forward

Africa Forum, Paris5 June, 2009