Embed Size (px)

Citation preview

Financial Crime Hot Topics -Singapore

Correspondent Banking and DPAs

March 2016

David Brain & Colin Darby

2

Agenda

• Correspondent Banking

o Correspondent relationship money laundering risks

o MAS requirements and guidance

o Correspondent banking compliance challenges

o Wholesale ‘de-risking’

o Changing EU requirements

o Effective correspondent banking operating models

• DPAs

o Evolution of UK DPAs

o Pros and cons of self-reporting

o Pros and cons of entering into a DPA

o The UK’s first DPA

o Monitors

Correspondent BankingThe Good, The Bad and The Challenging

4

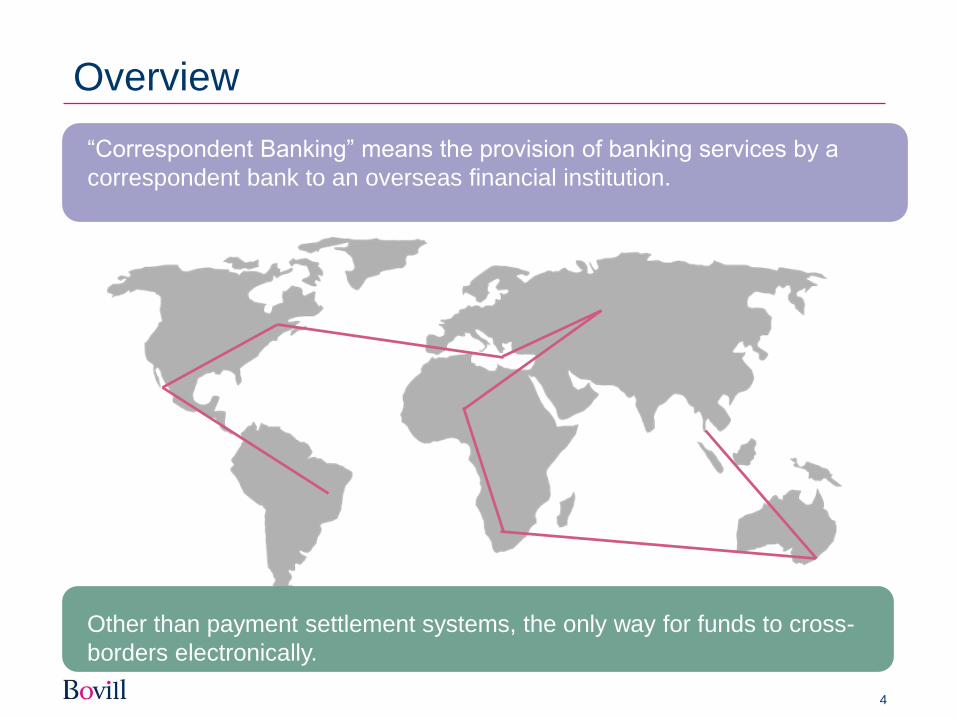

Overview

“Correspondent Banking” means the provision of banking services by a

correspondent bank to an overseas financial institution.

Other than payment settlement systems, the only way for funds to cross-

borders electronically.

5

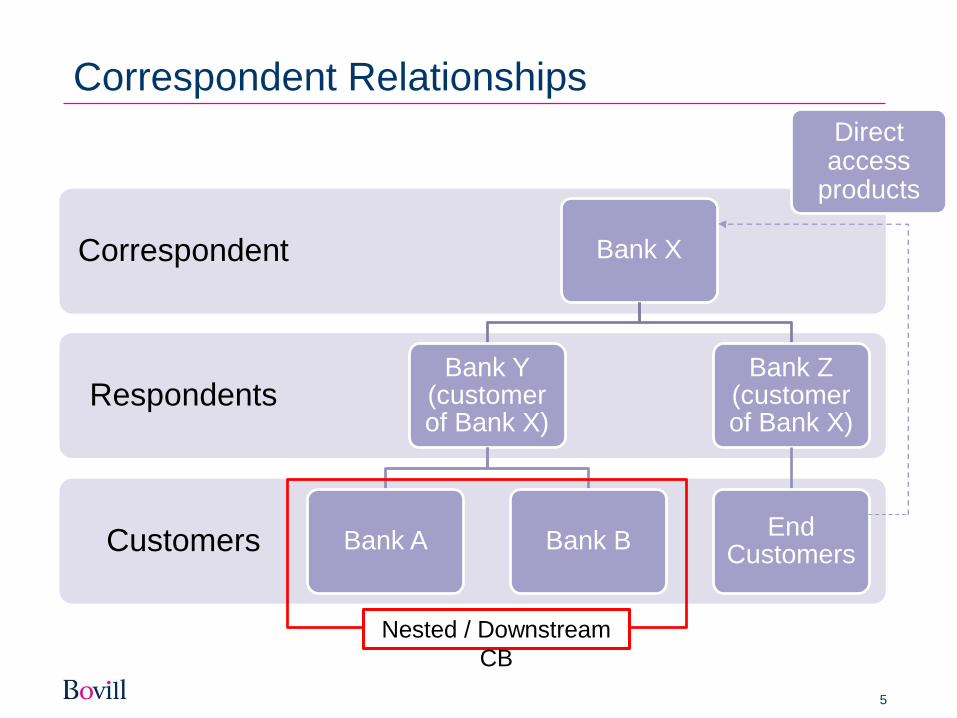

Correspondent Relationships

Customers

Respondents

Correspondent Bank X

Bank Y (customer of Bank X)

Bank A Bank B

Bank Z (customer of Bank X)

End Customers

Direct access

products

Nested / Downstream

CB

6

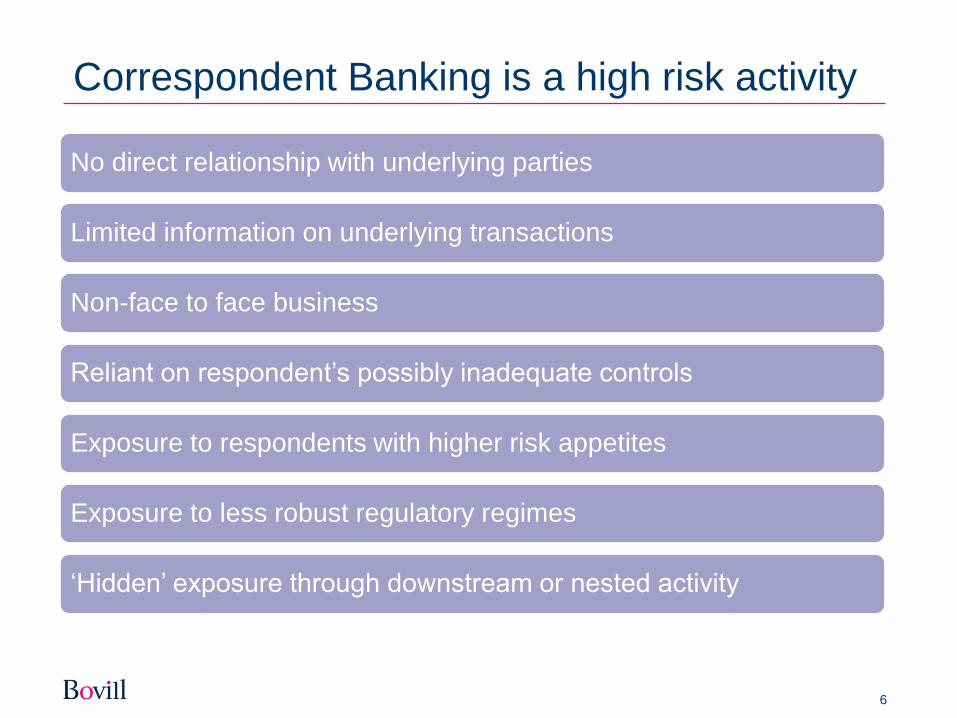

Correspondent Banking is a high risk activity

No direct relationship with underlying parties

Limited information on underlying transactions

Non-face to face business

Reliant on respondent’s possibly inadequate controls

Exposure to respondents with higher risk appetites

Exposure to less robust regulatory regimes

‘Hidden’ exposure through downstream or nested activity

7

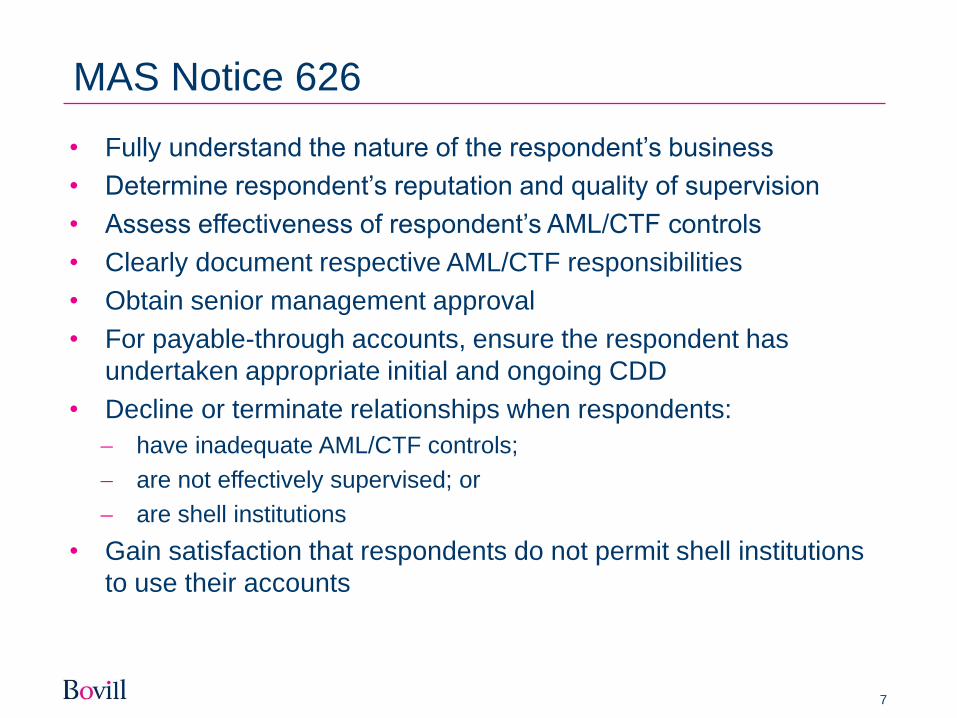

MAS Notice 626

• Fully understand the nature of the respondent’s business

• Determine respondent’s reputation and quality of supervision

• Assess effectiveness of respondent’s AML/CTF controls

• Clearly document respective AML/CTF responsibilities

• Obtain senior management approval

• For payable-through accounts, ensure the respondent has

undertaken appropriate initial and ongoing CDD

• Decline or terminate relationships when respondents:

have inadequate AML/CTF controls;

are not effectively supervised; or

are shell institutions

• Gain satisfaction that respondents do not permit shell institutions

to use their accounts

8

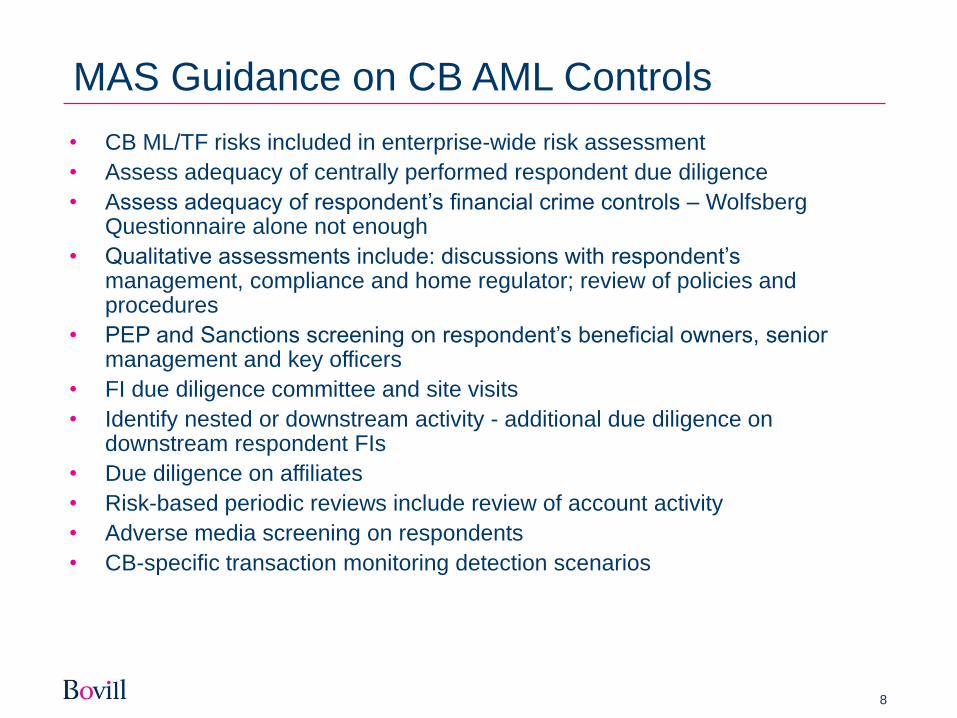

MAS Guidance on CB AML Controls

• CB ML/TF risks included in enterprise-wide risk assessment

• Assess adequacy of centrally performed respondent due diligence

• Assess adequacy of respondent’s financial crime controls – Wolfsberg Questionnaire alone not enough

• Qualitative assessments include: discussions with respondent’s management, compliance and home regulator; review of policies and procedures

• PEP and Sanctions screening on respondent’s beneficial owners, senior management and key officers

• FI due diligence committee and site visits

• Identify nested or downstream activity - additional due diligence on downstream respondent FIs

• Due diligence on affiliates

• Risk-based periodic reviews include review of account activity

• Adverse media screening on respondents

• CB-specific transaction monitoring detection scenarios

9

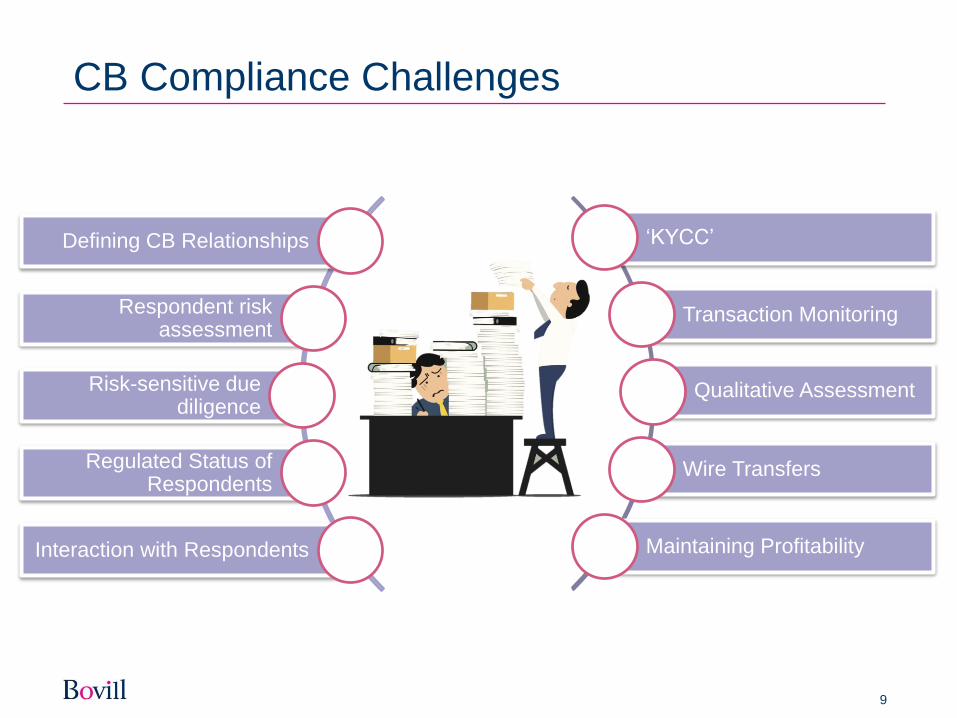

CB Compliance Challenges

Defining CB Relationships

Respondent risk assessment

Risk-sensitive due diligence

Regulated Status of Respondents

Interaction with Respondents

‘KYCC’

Transaction Monitoring

Qualitative Assessment

Wire Transfers

Maintaining Profitability

10

Wholesale De-risking

Benefits Impacts

11

Changing European Landscape

4MLD definition of ‘correspondent relationship’ – broad and may capture

relationships between NBFIs.

Removal of ‘equivalent jurisdictions’ in favour of identification of high risk

third countries – Singapore was considered to be equivalent

Less prescriptive, more risk-based approach to SDD – CB due diligence

likely to become less polarised, more risk sensitive.

12

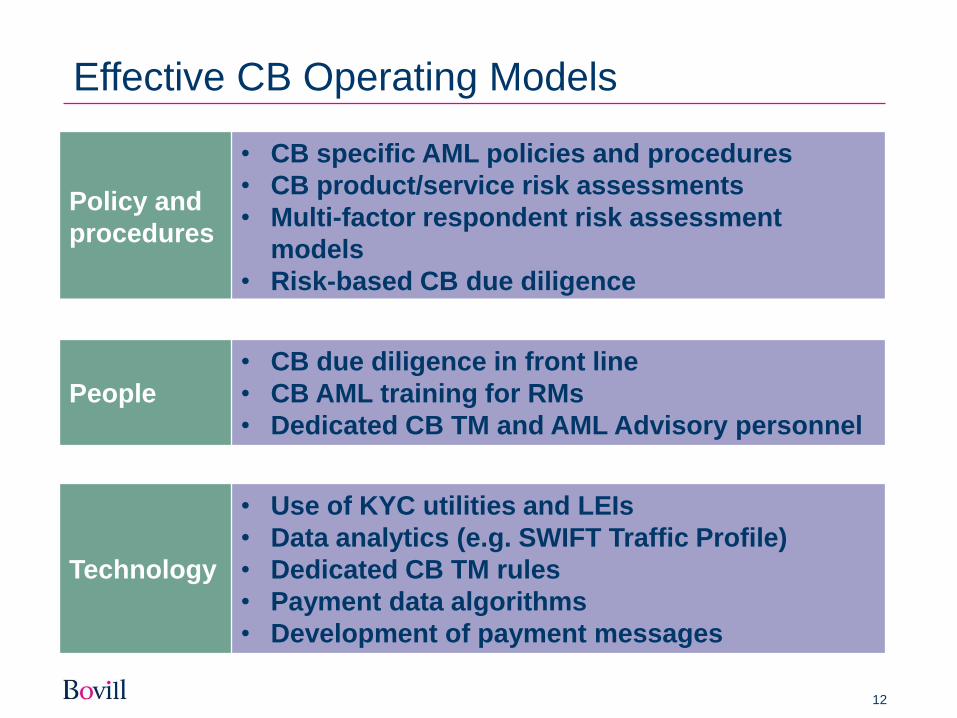

Effective CB Operating Models

Policy and

procedures

• CB specific AML policies and procedures

• CB product/service risk assessments

• Multi-factor respondent risk assessment

models

• Risk-based CB due diligence

People

• CB due diligence in front line

• CB AML training for RMs

• Dedicated CB TM and AML Advisory personnel

Technology

• Use of KYC utilities and LEIs

• Data analytics (e.g. SWIFT Traffic Profile)

• Dedicated CB TM rules

• Payment data algorithms

• Development of payment messages

13

Key messages

CB remains vital

Sustainability through

collaboration

Risk-Based Approach

Authorities remain

interested

More technology

Financial Crime Hot Topics

Deferred Prosecution Agreements (DPAs)

March 2016

David Brain

15

What is a deferred prosecution agreement (DPA)?

• Official Wording:

A DPA is an agreement between a designated prosecutor

and an organisation which could be prosecuted, under the

supervision of a judge. (SFO)

• Practical Terms:

DPAs are designed to encourage companies to self-report

wrongdoing in the hope of more lenient treatment.

16

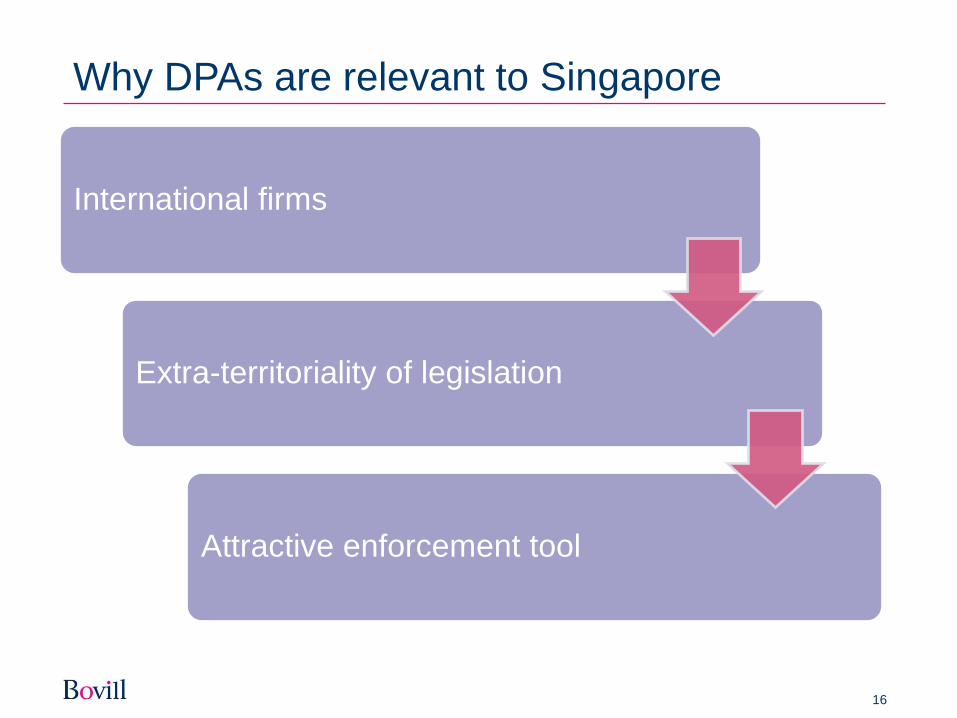

Why DPAs are relevant to Singapore

International firms

Extra-territoriality of legislation

Attractive enforcement tool

17

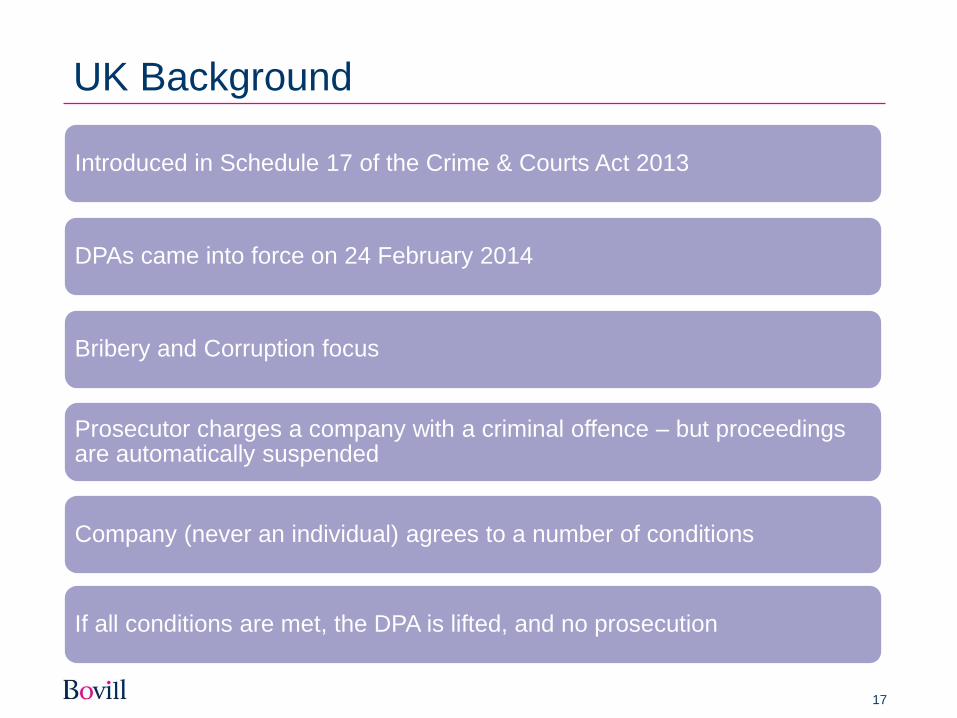

UK Background

Introduced in Schedule 17 of the Crime & Courts Act 2013

DPAs came into force on 24 February 2014

Bribery and Corruption focus

Prosecutor charges a company with a criminal offence – but proceedings are automatically suspended

Company (never an individual) agrees to a number of conditions

If all conditions are met, the DPA is lifted, and no prosecution

18

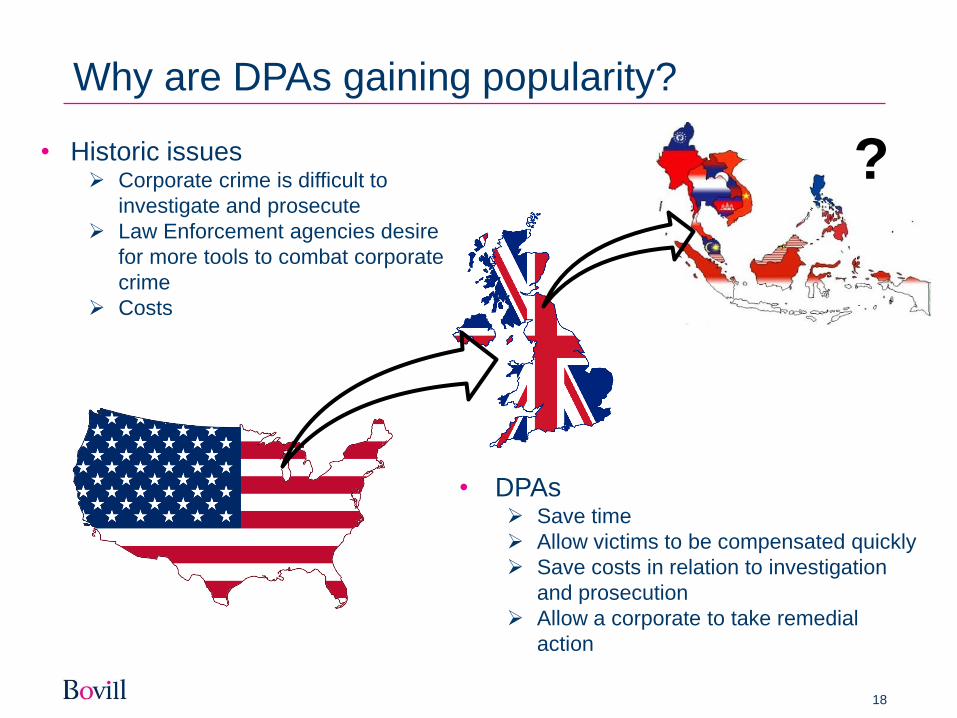

Why are DPAs gaining popularity?

• Historic issues Corporate crime is difficult to

investigate and prosecute

Law Enforcement agencies desire

for more tools to combat corporate

crime

Costs

• DPAs Save time

Allow victims to be compensated quickly

Save costs in relation to investigation

and prosecution

Allow a corporate to take remedial

action

?

19

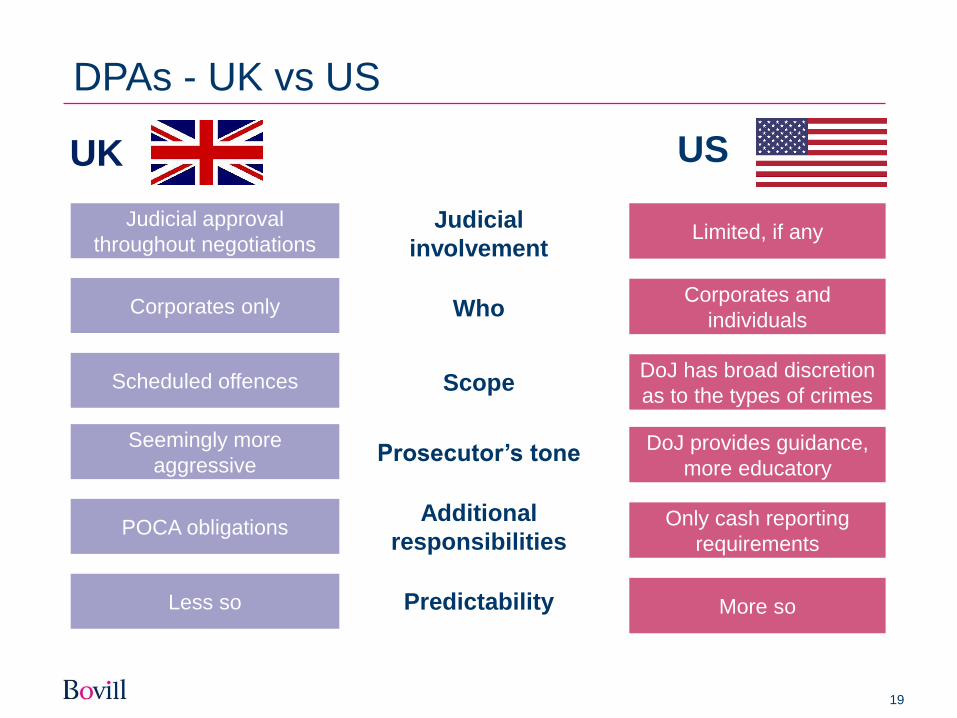

DPAs - UK vs US

Judicial

involvement

Predictability

Who

Scope

Prosecutor’s tone

Additional

responsibilities

Limited, if any

Corporates and

individuals

DoJ has broad discretion

as to the types of crimes

DoJ provides guidance,

more educatory

Only cash reporting

requirements

More so

Judicial approval

throughout negotiations

Corporates only

Scheduled offences

Seemingly more

aggressive

POCA obligations

Less so

USUK

20

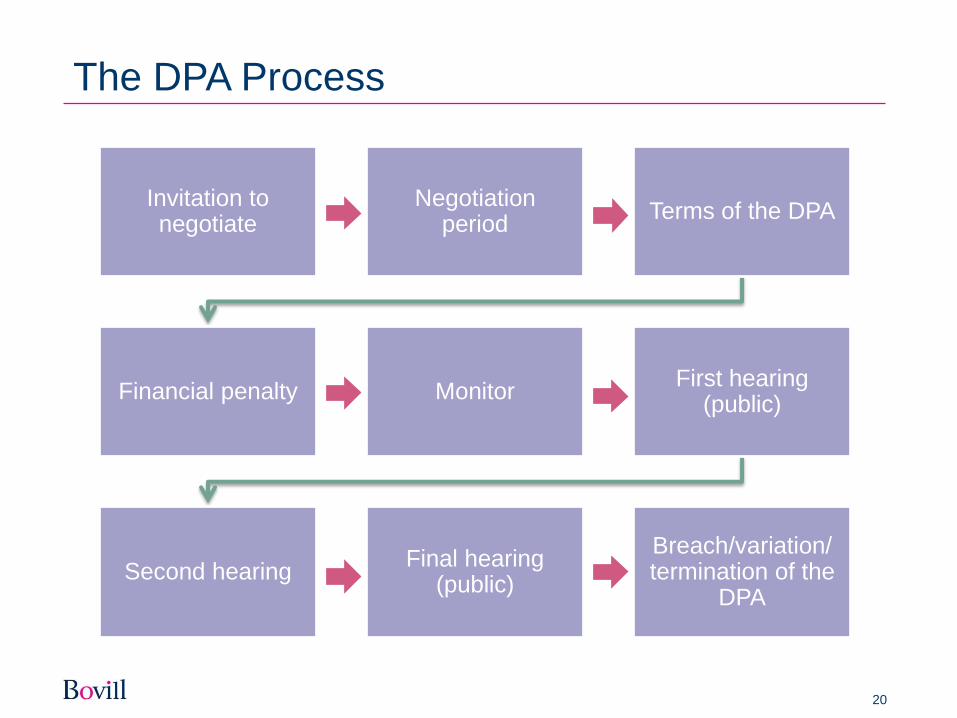

The DPA Process

Invitation to negotiate

Negotiation period

Terms of the DPA

Financial penalty MonitorFirst hearing

(public)

Second hearingFinal hearing

(public)

Breach/variation/ termination of the

DPA

21

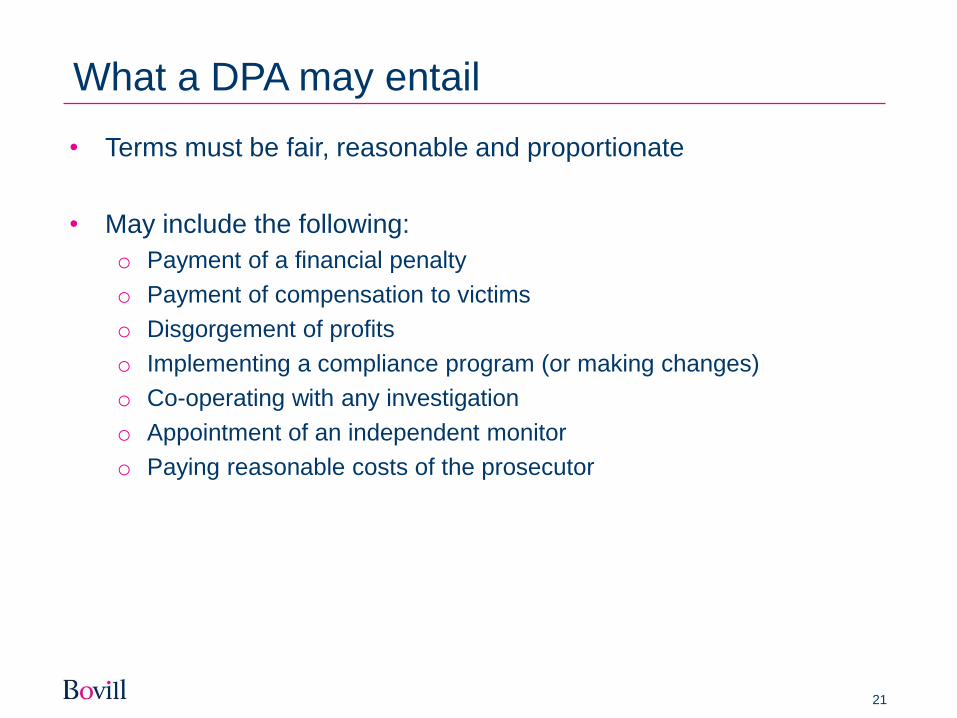

What a DPA may entail

• Terms must be fair, reasonable and proportionate

• May include the following:

o Payment of a financial penalty

o Payment of compensation to victims

o Disgorgement of profits

o Implementing a compliance program (or making changes)

o Co-operating with any investigation

o Appointment of an independent monitor

o Paying reasonable costs of the prosecutor

22

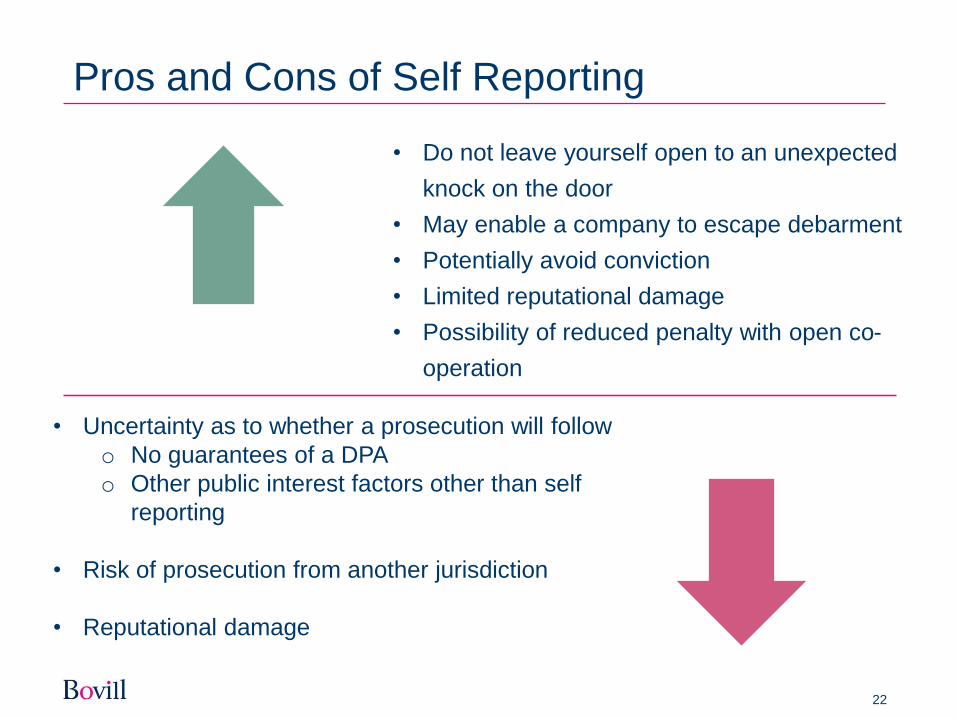

Pros and Cons of Self Reporting

• Uncertainty as to whether a prosecution will follow

o No guarantees of a DPA

o Other public interest factors other than self

reporting

• Risk of prosecution from another jurisdiction

• Reputational damage

• Do not leave yourself open to an unexpected

knock on the door

• May enable a company to escape debarment

• Potentially avoid conviction

• Limited reputational damage

• Possibility of reduced penalty with open co-

operation

23

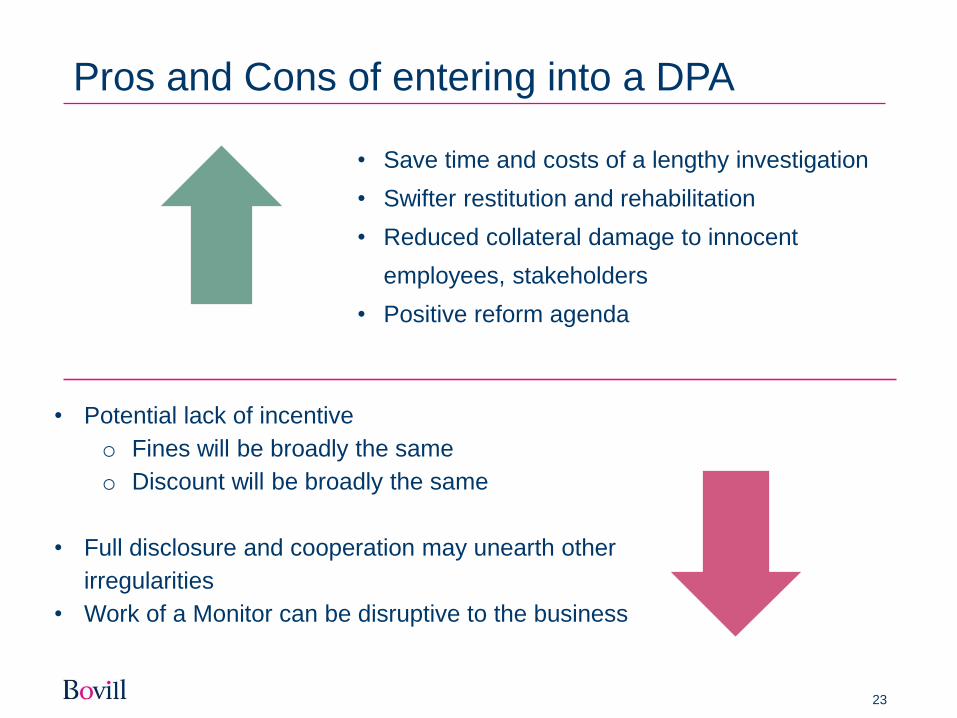

Pros and Cons of entering into a DPA

• Potential lack of incentive

o Fines will be broadly the same

o Discount will be broadly the same

• Full disclosure and cooperation may unearth other

irregularities

• Work of a Monitor can be disruptive to the business

• Save time and costs of a lengthy investigation

• Swifter restitution and rehabilitation

• Reduced collateral damage to innocent

employees, stakeholders

• Positive reform agenda

24

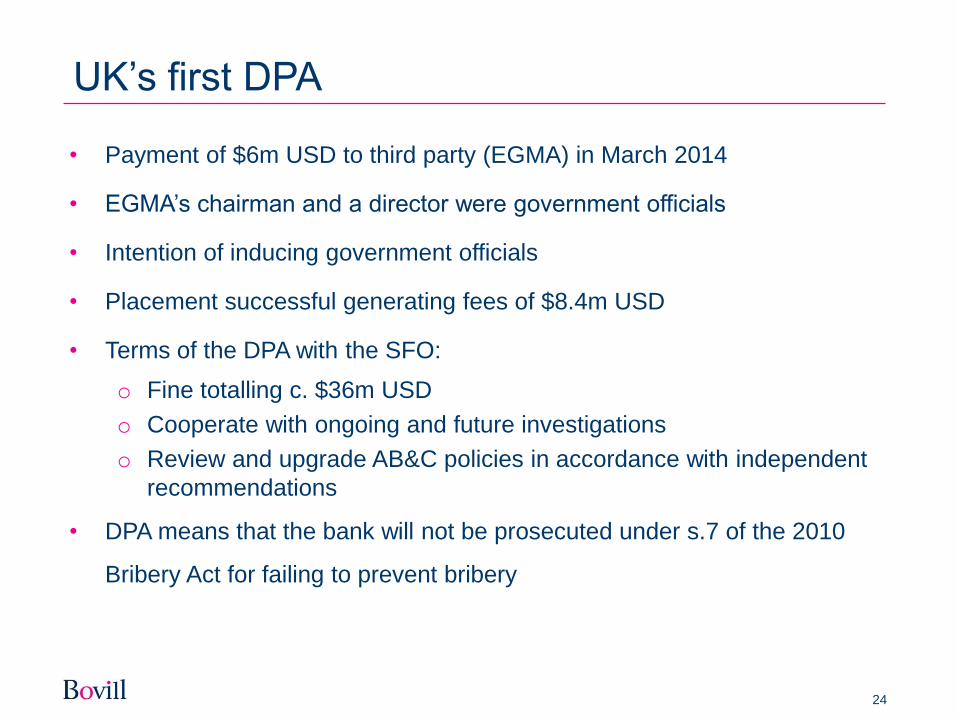

UK’s first DPA

• Payment of $6m USD to third party (EGMA) in March 2014

• EGMA’s chairman and a director were government officials

• Intention of inducing government officials

• Placement successful generating fees of $8.4m USD

• Terms of the DPA with the SFO:

o Fine totalling c. $36m USD

o Cooperate with ongoing and future investigations

o Review and upgrade AB&C policies in accordance with independent

recommendations

• DPA means that the bank will not be prosecuted under s.7 of the 2010

Bribery Act for failing to prevent bribery

25

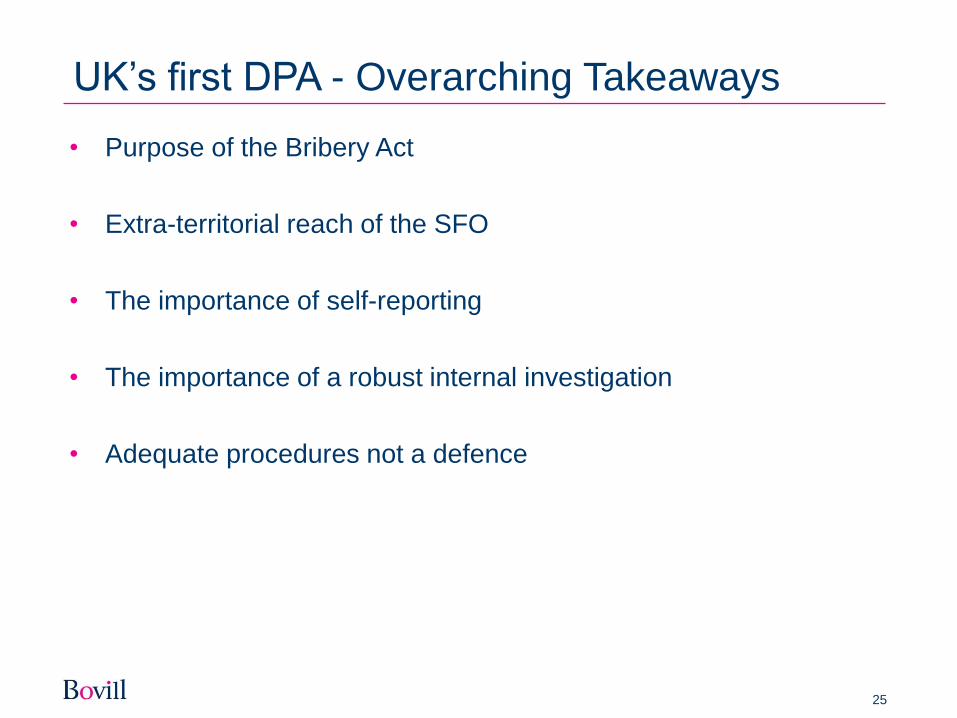

UK’s first DPA - Overarching Takeaways

• Purpose of the Bribery Act

• Extra-territorial reach of the SFO

• The importance of self-reporting

• The importance of a robust internal investigation

• Adequate procedures not a defence

26

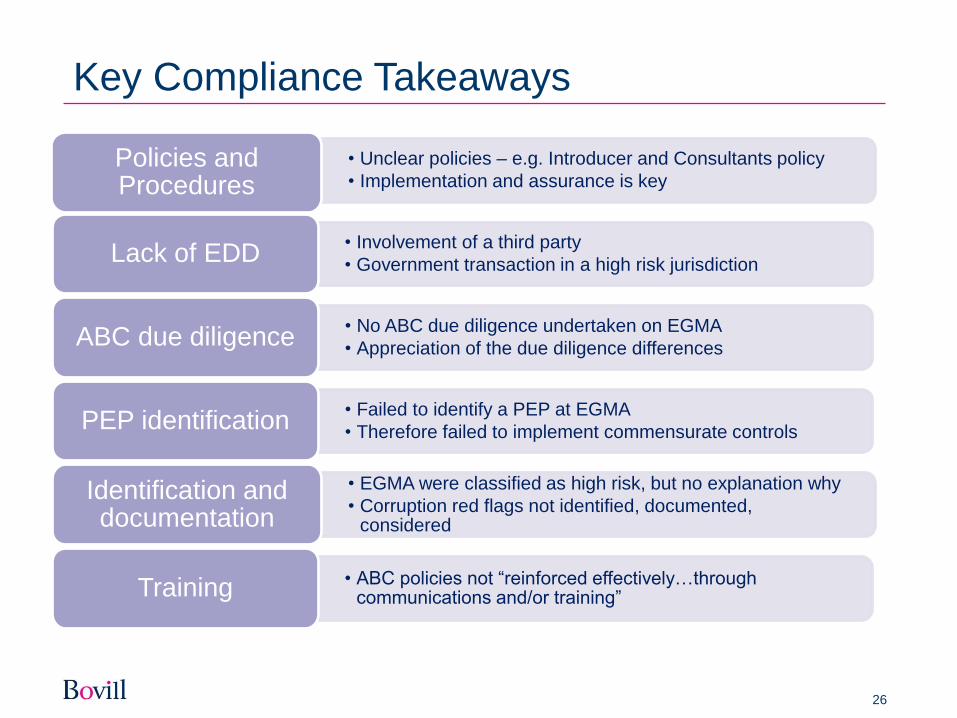

Key Compliance Takeaways

• Unclear policies – e.g. Introducer and Consultants policy

• Implementation and assurance is keyPolicies and Procedures

• Involvement of a third party

• Government transaction in a high risk jurisdiction Lack of EDD

• No ABC due diligence undertaken on EGMA

• Appreciation of the due diligence differencesABC due diligence

• Failed to identify a PEP at EGMA

• Therefore failed to implement commensurate controlsPEP identification

• EGMA were classified as high risk, but no explanation why

• Corruption red flags not identified, documented, considered

Identification and documentation

• ABC policies not “reinforced effectively…through communications and/or training”Training

27

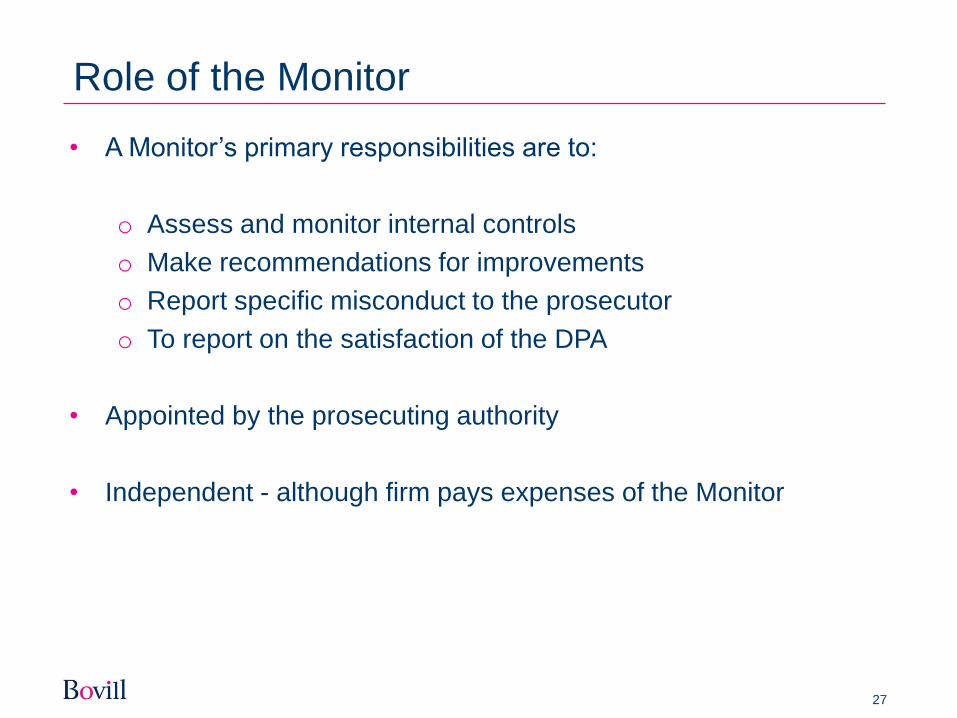

Role of the Monitor

• A Monitor’s primary responsibilities are to:

o Assess and monitor internal controls

o Make recommendations for improvements

o Report specific misconduct to the prosecutor

o To report on the satisfaction of the DPA

• Appointed by the prosecuting authority

• Independent - although firm pays expenses of the Monitor

28

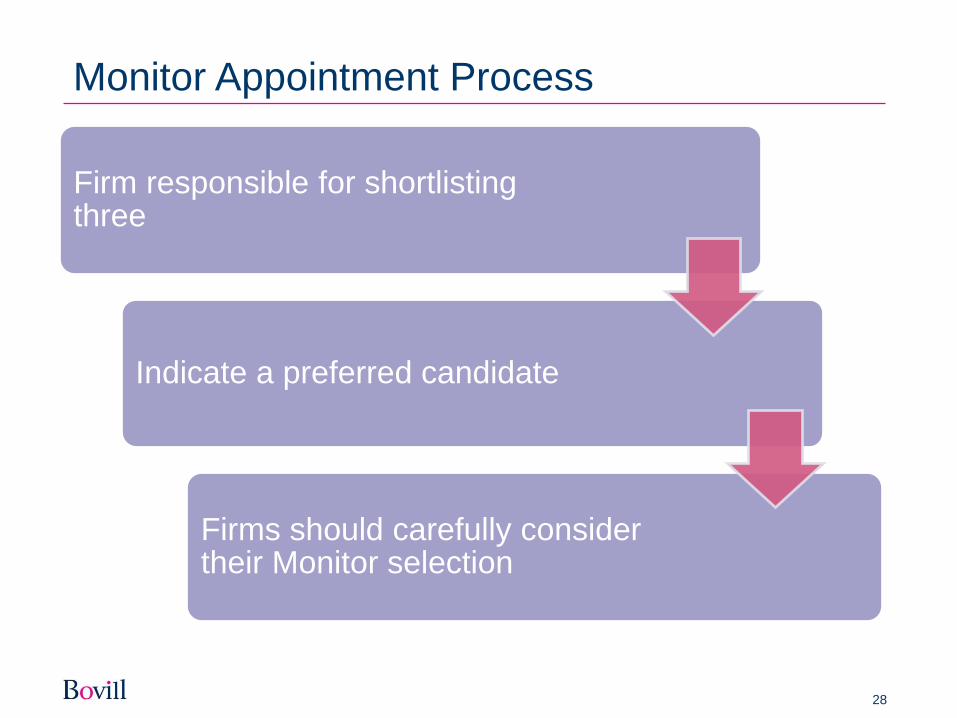

Monitor Appointment Process

Firm responsible for shortlisting three

Indicate a preferred candidate

Firms should carefully consider their Monitor selection

29

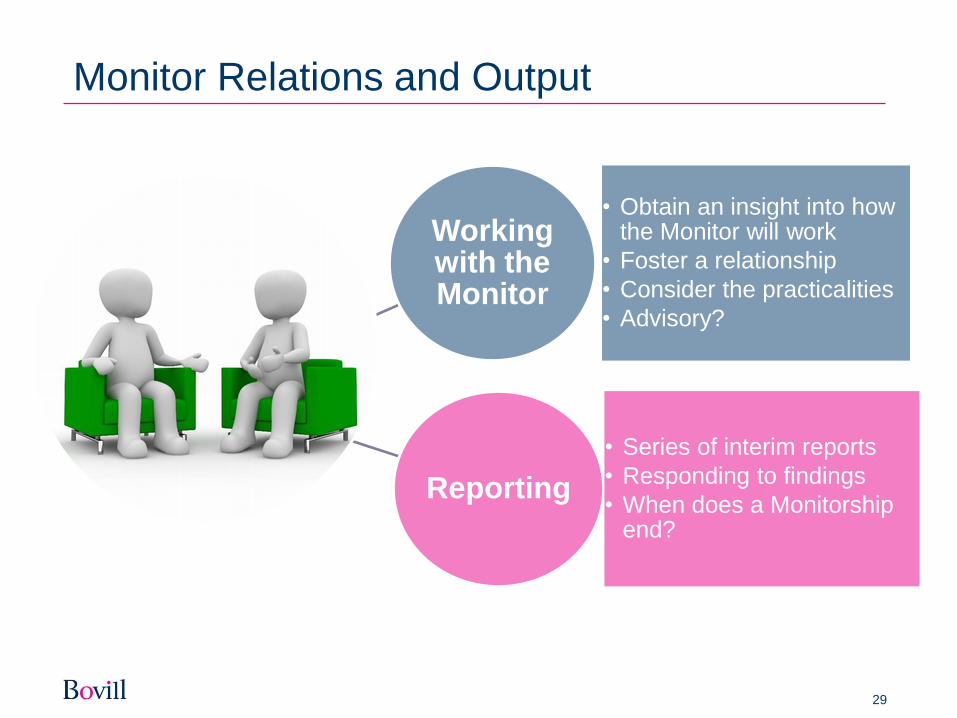

Monitor Relations and Output

Working with the Monitor

• Obtain an insight into how the Monitor will work

• Foster a relationship

• Consider the practicalities

• Advisory?

Reporting

• Series of interim reports

• Responding to findings

• When does a Monitorship end?

30

Conclusion

• DPAs are here to stay

• Moved into an enforcement era regarding ABC

• The importance of an effective compliance programme

• Joined up financial crime controls

31

Questions

?