Embed Size (px)

Citation preview

FİNANSAL MATEMATİK

Hedging, Arbitraging, Pricing

Eğitim Program Taslağı

Mart 2015

Doç. Dr. Kutlu MERİH

Bu sunum Finansal Matematik Analiz için gerekli ve temel olan konuları içeriyor.

Bunlara ek yapılabilir veya daraltılabilir.Her konu wikipedia ile bağlantılı hale

getirilmiştir.Böylece içerik ve kapsam hakkında fikir

edinilebilir.

Temel Matematik

Calculus Power / Taylor SeriesDifferential Equations Real AnalysisMathematical models

Olasılık ve Dağılımlar

Probability Probability Distributions Quantile FunctionsValue At Risk Expected Value İntegral Dönüşümler

Moment Üreten Fonksiyon Laplace Transformation Karakteristik Fonksiyon

Stokastik Prosesler

Binomial Distribution/ProcessNormal Distribution/ProcessLog-normal Distribution/ProcessPoisson Distribution/Process

Korelasyon - Kointegrasyon

KorelasyonKointegrasyonCopulasGaussian CopulasDiğer Copulas

Volatilite/Heteroscedasticity

Volatility ARCH model GARCH model

Stochastic volatility SABR Volatility Model Markov Switching Multifractal

Stokastik Analiz

Risk-neutral Measure Stochastic IntegralsChapman-Kolmogorov KDDPartial Differential Equations

Heat Equation

Stochastic Differential Equations Itô's LemmaStochastic Calculus

Brownian Motion Lévy Process

Bu kısma ben talibim: K. M.

Türev Ürün Fiyatlama

The Brownian Motion Model of Financial Markets

Rational pricing assumptions Risk neutral valuation Arbitrage-free pricing

Futures Futures contract pricing

Options Put–call parity (Arbitrage relationships for options) Intrinsic value, Time value Moneyness

Black-Scholes Fiyatlama Black–scholes Model Black Model Binomial Options Model Monte Carlo Option Model Implied Volatility, Volatility Smile Optimal Stopping (Pricing Of American Options

)

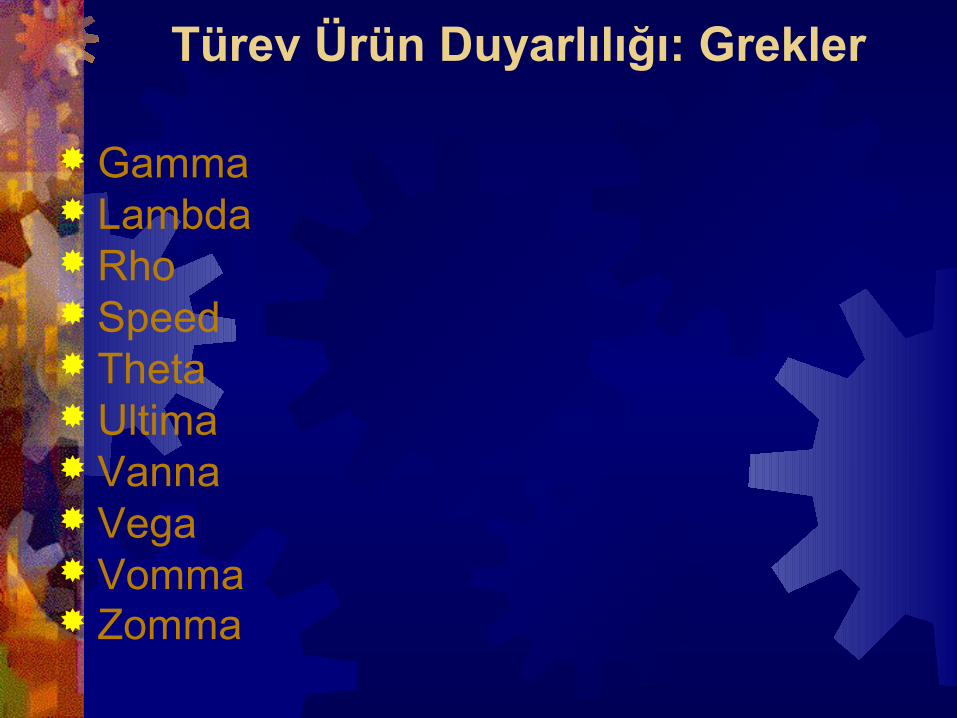

Türev Ürün Duyarlılığı: Grekler

Gamma Lambda Rho Speed Theta Ultima Vanna Vega Vomma Zomma

The table shows the relationship of the more common sensitivities to the four primary inputs into the Black-Scholes model (spot price of the underlying security, time remaining until option expiration, volatility and the rate of return of a risk-free investment)

and to the option's value, delta, gamma, vega and vomma. Greeks which are a

first-order derivative are in blue, second-order derivatives are in green, and third-order derivatives are in yellow.

Note that vanna is used, intentionally, in two places as the two sensitivities are mathematically equivalent.

SpotPrice (S)

Volatility(σ)

Time toExpiry

(τ)

Risk-FreeRate

(r)

Value (V) Δ Delta ν Vega Θ Theta ρ Rho

Delta (Δ) Γ Gamma Vanna Charm

Gamma (Γ) Speed Zomma Color

Vega (ν) Vanna VommaDvegaDtime

Vomma Ultima

speed

zomma

color

Olasılık Metrik Değişimleri

Girsanov's Theorem Radon–Nikodym Derivative Martingale Representation Theorem

Feynman–Kac Formula Statistical Finance

Alternatif Teknikler

Asymptotic AnalysisErgodic TheorySaddlepoint Approximation

Nümerik Teknikler

Numerical AnalysisMonte Carlo Method Numerical Methods

Laplace TransformsFourier Transforms

Numerical Partial Differential Equations Crank–Nicolson Method Finite Difference Method Finite Elements Method

Faiz Türevleri

Interest rate derivatives Short rate model

Hull-White model Cox-Ingersoll-Ross model Chen model

LIBOR Market Model Heath-Jarrow-Morton framework

Diğer Destek Konular

Chaos Theory and FractalsComputational Finance Quantitative Behavioral Finance Derivative (Finance), List Of Derivatives

Topics Modeling And Analysis Of Financial

Markets International Swaps And Derivatives

Association Fundamental Financial Concepts - Topics Model (Economics) List Of Finance Topics