Embed Size (px)

Citation preview

© South-Western Educational Publishing

Chapter 11

Investing for Your Future

Investing FundamentalsExploring Investment Options

© South-Western Educational Publishing

Chapter 11

Investing for Your Future

Understand some investment options

© South-Western Educational Publishing

Savings Accounts

Pros access any time risk – little to none minimum balance - $10-$50

Cons yield – low taxable - yes

© South-Western Educational Publishing

Certificates of Deposit (CDs)

What are they? Bank pays a fixed amount of interest for a fixed amount of money during a fixed amount of time i.e. 4.5% interest over 6 months

© South-Western Educational Publishing

Certificates of Deposit (CDs)

Pros risk – little to none simple no fees higher interest rate than savings

Consrestricted access to moneypenalty for early withdrawal

© South-Western Educational Publishing

Bonds

What are they? An “IOU” certifying that you loaned money to

a corporation municipal government federal government

terms of repayment are outlined

© South-Western Educational Publishing

Bonds – cont.

Corporate Bonds - risky Sold by private companies to raise money If company goes bankrupt, bondholders have first claim to assets, before stockholders

© South-Western Educational Publishing

Bonds – cont.

Municipal Bonds - less risky issued by any non-federal government Interest paid comes from taxes or revenues from special projects Earned interest is exempt from federal income tax

© South-Western Educational Publishing

Bonds – cont.

Federal Government Bonds – safest even if U.S. Government goes bankrupt, it is obligated to repay

© South-Western Educational Publishing

Mutual Funds

What are they? professionally managed portfolios made up of stocks, bonds, and other investments

How they work individuals buy shares, and fund uses money to purchase stocks, bonds, etc. profits returned monthly, quarterly, or semi-annually in the form of dividends

© South-Western Educational Publishing

Mutual Funds

Advantage allows small investors to take advantage of professional account management and diversification normally only available to large investors

© South-Western Educational Publishing

Types of Mutual Funds

Balanced – variety of stocks & bonds Global Bond Fund – has corporate bonds of companies from around the world Global Stock Fund – has stocks from companies in many parts of the world

© South-Western Educational Publishing

Types of Mutual Funds

Growth Fund – companies expected to increase in value – higher riskIncome Fund – stocks and bonds with high dividends & interestIndustry Fund – stocks of companies in a single industry (technology, health care, banking)

© South-Western Educational Publishing

Types of Mutual Funds

Municipal Bond Fund – features debt instruments of state and local governmentsRegional Stock Fund – stocks of companies from one geographic region of the world (i.e. Asia or Latin America)

© South-Western Educational Publishing

Stocks

What is stock? stock represents ownership in a companyStockholders own a share of the company & are entitled to a share of the profits as well as a vote in how the company is run

© South-Western Educational Publishing

Stocks

How earnings are madeCompany profits may be divided among shareholders in the form of dividendsLarger profits can be made through an increase in the value of the stock on the open market

© South-Western Educational Publishing

Stocks

Pros If the market value goes up, the gain can be considerableMoney is easily accessible

Cons If market value goes down, the loss can be considerable Selecting and managing stock often requires study and time

© South-Western Educational Publishing

Retirement Plans

Plans help individuals set aside money to be used after they retireFederal income tax not immediately due on money put into a retirement account, or on the interest it makesIncome tax paid when money is withdrawn

© South-Western Educational Publishing

Retirement Plans

Penalty charges apply is money is withdrawn before retirement age, except under certain circumstances Income after retirement is usually lower, so tax rate is lower

© South-Western Educational Publishing

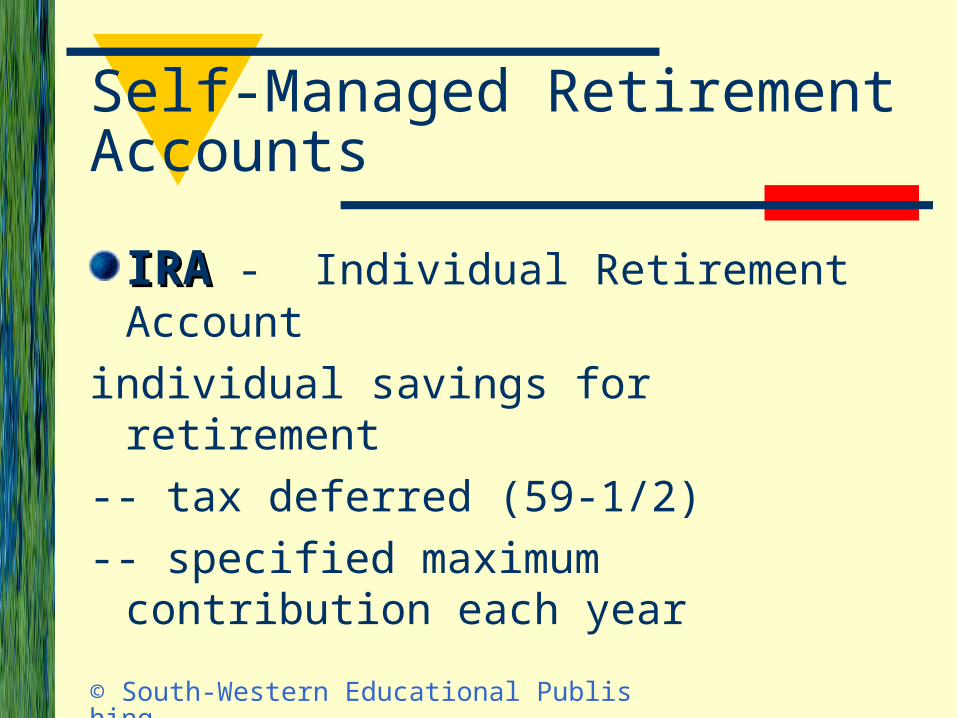

Self-Managed Retirement Accounts

IRAIRA - Individual Retirement Account

individual savings for retirement-- tax deferred (59-1/2)-- specified maximum contribution

each year

© South-Western Educational Publishing

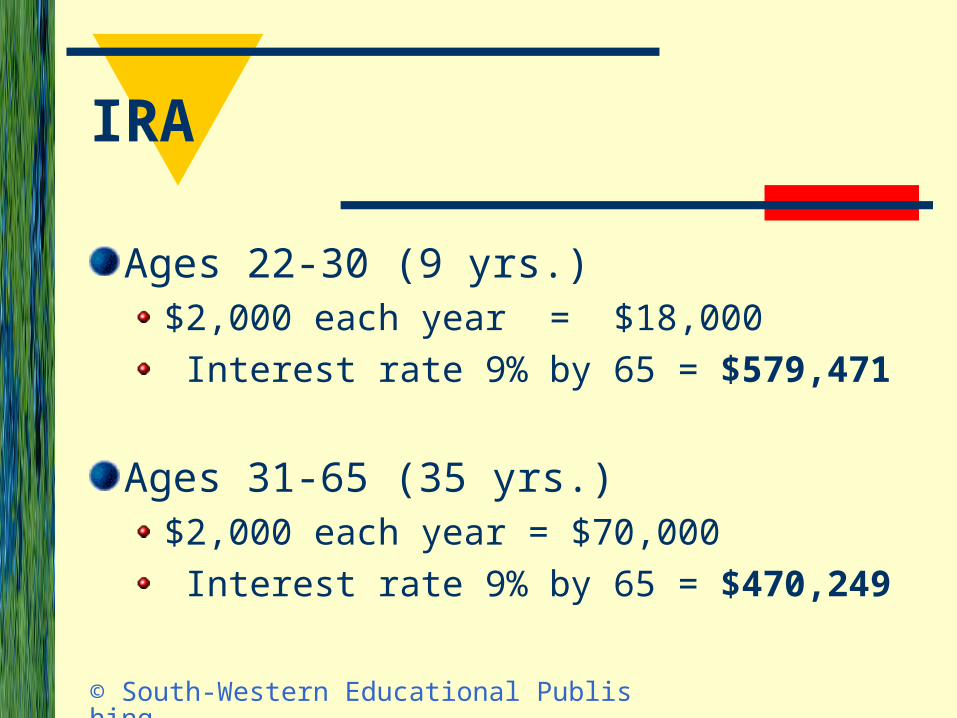

IRA

Ages 22-30 (9 yrs.)$2,000 each year = $18,000 Interest rate 9% by 65 = $579,471

Ages 31-65 (35 yrs.)$2,000 each year = $70,000 Interest rate 9% by 65 = $470,249

© South-Western Educational Publishing

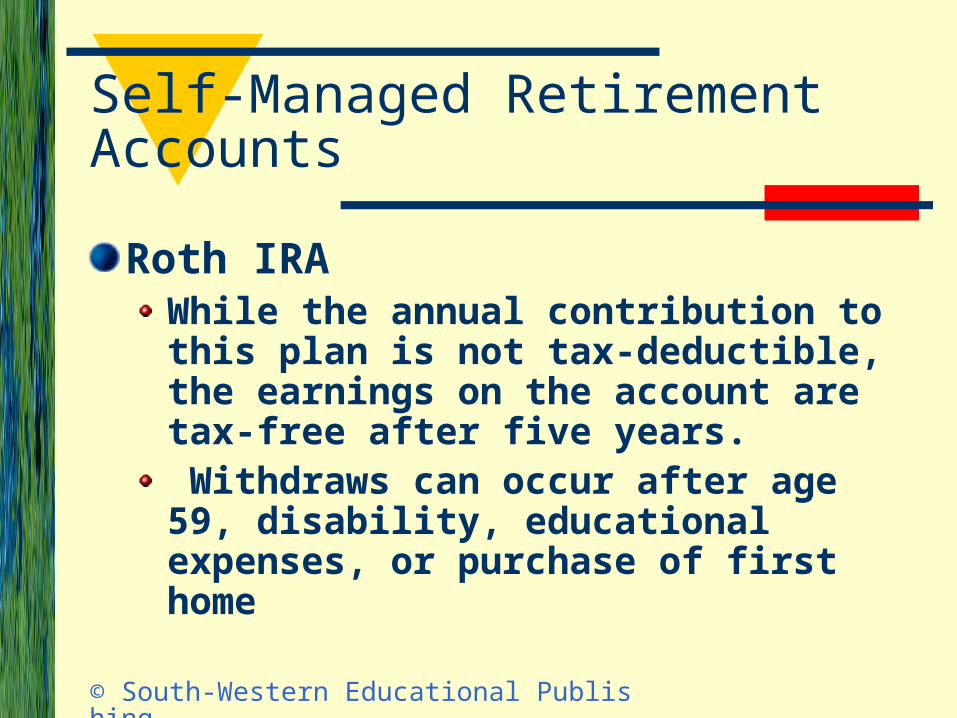

Self-Managed Retirement Accounts

Roth IRA While the annual contribution to this plan is not tax-deductible, the earnings on the account are tax-free after five years. Withdraws can occur after age 59, disability, educational expenses, or purchase of first home

© South-Western Educational Publishing

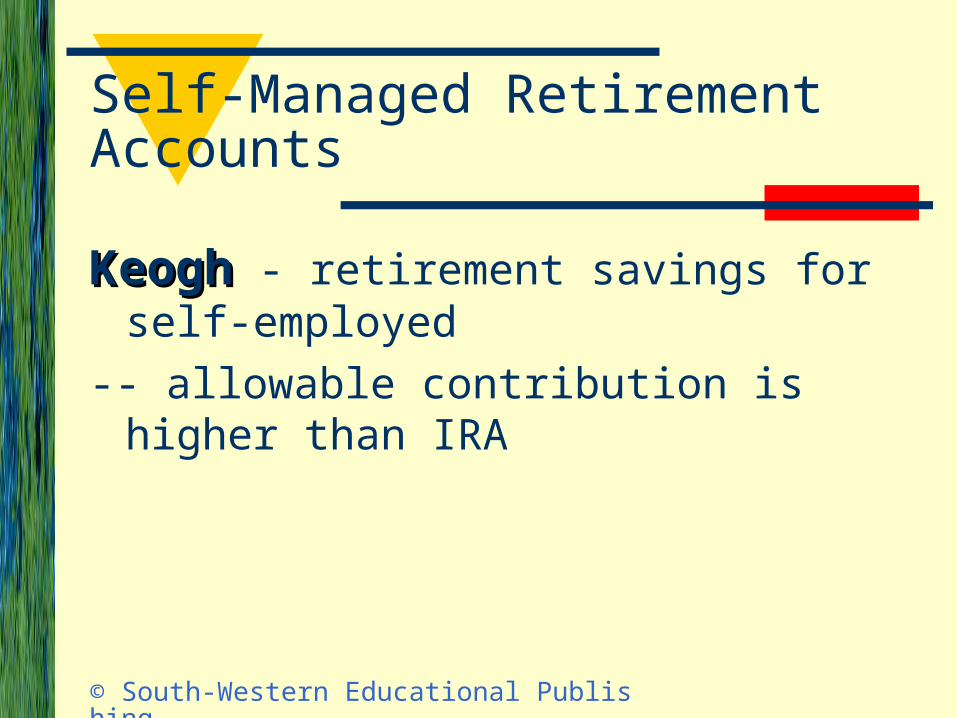

Self-Managed Retirement Accounts

KeoghKeogh - retirement savings for self-employed

-- allowable contribution is higher than IRA

© South-Western Educational Publishing

Self-Managed Retirement Accounts

401K401K - employer sponsored account

-- deferred taxes

403(b)403(b) - not-for-profit / government

-- equivalent of 401Kemployee may choose how

contributions will be invested

© South-Western Educational Publishing

Real Estate

Large and often non-liquid investmentmust find buyer (time factor)proven protection against inflation in most parts of the USREITs - Real Estate Investment Trust

corporation pooling individual investments

© South-Western Educational Publishing

Real Estate

Large and often non-liquid investmentmust find buyer (time factor)proven protection against inflation in most parts of the USREITs - Real Estate Investment Trust

corporation pooling individual investments

© South-Western Educational Publishing

Annuities

Contract sold by an insurance company Provides investor with a series of regular

payments (usually after retirement)Generally receive monthly payments as

long as you continue to liveBuy from life insurance companyTax deferredOpposite of life insurance

© South-Western Educational Publishing

Comparing Retirement Options

Refer to your handout -- “Saving for Retirement”

© South-Western Educational Publishing

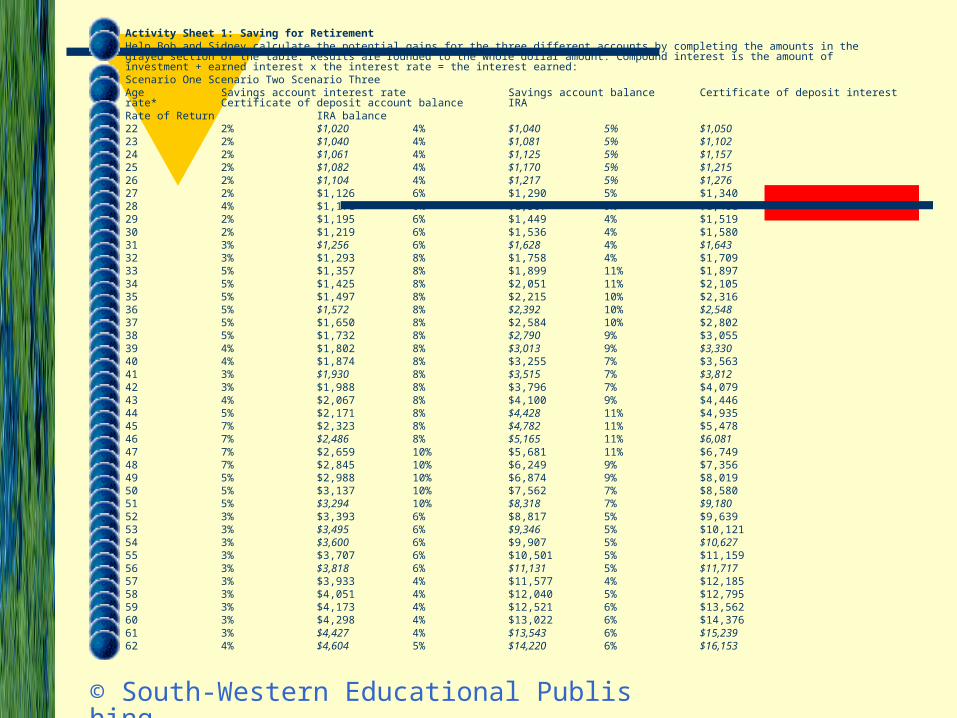

Activity Sheet 1: Saving for Retirement Help Bob and Sidney calculate the potential gains for the three different accounts by completing the amounts in the grayed section of the table. Results are rounded to the whole dollar amount. Compound interest is the amount of investment + earned interest x the interest rate = the interest earned: Scenario One Scenario Two Scenario Three Age Savings account interest rate Savings account balance Certificate of deposit interest rate* Certificate of deposit account balance IRA Rate of Return IRA balance 22 2% $1,020 4% $1,040 5% $1,050 23 2% $1,040 4% $1,081 5% $1,102 24 2% $1,061 4% $1,125 5% $1,157 25 2% $1,082 4% $1,170 5% $1,215 26 2% $1,104 4% $1,217 5% $1,276 27 2% $1,126 6% $1,290 5% $1,340 28 4% $1,171 6% $1,367 9% $1,461 29 2% $1,195 6% $1,449 4% $1,519 30 2% $1,219 6% $1,536 4% $1,580 31 3% $1,256 6% $1,628 4% $1,643 32 3% $1,293 8% $1,758 4% $1,709 33 5% $1,357 8% $1,899 11% $1,897 34 5% $1,425 8% $2,051 11% $2,105 35 5% $1,497 8% $2,215 10% $2,316 36 5% $1,572 8% $2,392 10% $2,548 37 5% $1,650 8% $2,584 10% $2,802 38 5% $1,732 8% $2,790 9% $3,055 39 4% $1,802 8% $3,013 9% $3,330 40 4% $1,874 8% $3,255 7% $3,563 41 3% $1,930 8% $3,515 7% $3,812 42 3% $1,988 8% $3,796 7% $4,079 43 4% $2,067 8% $4,100 9% $4,446 44 5% $2,171 8% $4,428 11% $4,935 45 7% $2,323 8% $4,782 11% $5,478 46 7% $2,486 8% $5,165 11% $6,081 47 7% $2,659 10% $5,681 11% $6,749 48 7% $2,845 10% $6,249 9% $7,356 49 5% $2,988 10% $6,874 9% $8,019 50 5% $3,137 10% $7,562 7% $8,580 51 5% $3,294 10% $8,318 7% $9,180 52 3% $3,393 6% $8,817 5% $9,639 53 3% $3,495 6% $9,346 5% $10,121 54 3% $3,600 6% $9,907 5% $10,627 55 3% $3,707 6% $10,501 5% $11,159 56 3% $3,818 6% $11,131 5% $11,717 57 3% $3,933 4% $11,577 4% $12,185 58 3% $4,051 4% $12,040 5% $12,795 59 3% $4,173 4% $12,521 6% $13,562 60 3% $4,298 4% $13,022 6% $14,376 61 3% $4,427 4% $13,543 6% $15,239 62 4% $4,604 5% $14,220 6% $16,153

© South-Western Educational Publishing

Saving for Retirement

Based on the results above, which savings vehicle yields the best results for retirement? Why? The best results would have to be the IRA, Scenario 3 because from the ages of 22-62, its balance is the highest.

© South-Western Educational Publishing

The story of Bob and Sidney includes changes in interest rates throughout the years. Which type of savings account is the most stable? Which the most volatile? CD is the most stable because its interest rates do not change over the deposit period. The interest rates don’t differ much. On the other hand, the IRA interest rates are unstable. They usually change every couple of years with very major interest rate differences.

© South-Western Educational Publishing

The Individual Retirement Account seems to have risks and rewards. Based upon the chart, is the IRA a sound investment over the 40 years? What could happen to have you change your advice? The IRA sounds like a really nice investment over 40 years, but if the interest is unstable and decides to drop low for most of the 40 years, then I would change my advice.

© South-Western Educational Publishing

GOALSGOALS

Lesson 11.1

Investing Fundamentals

Describe the stages of investing and the relationship between risk and potential return.Explain effective investment strategies, criteria for choosing an investment, and steps for investing wisely.

© South-Western Educational Publishing

Stages of Investing

Stage 1. Put-and-take accountStage 2. Beginning investingStage 3. Systematic investingStage 4. Strategic investingStage 5. Speculative investing

© South-Western Educational Publishing

1) Put and Take Account

PUT your paycheck into an account and TAKE money as needed to pay bills

Investment begins with budgetingINCOMEEXPENSESSAVINGS PUT & TAKE excess BEGINNING INVESTMENTS

© South-Western Educational Publishing

Put & Take - continued

Financial advisers recommend3 to 6 months set aside for unexpected expenses

avoids having to tap into permanent investments

© South-Western Educational Publishing

2) Beginning Investing

InvestingInvesting – use of savings to earn a financial returnbegins when savings are “permanent” rather than “put and take”

First investments should be:conservativelow risk (can’t afford to risk losing)

(20s to 30s)

© South-Western Educational Publishing

3) Systematic Investing

Systematic InvestingSystematic Investing – investing on a regular and planned basisEach month – set aside $ for investing; increasing $ as your income growsGoals: long-range (middle age)

© South-Western Educational Publishing

4) Strategic Investing

Strategic InvestingStrategic Investing - careful management of investment alternatives to maximize portfolio growth over next 5-10 years

Manage Portfolio – transfer $ to various types of investments to take advantage of opportunities (maximize returns)

© South-Western Educational Publishing

5) Speculative Investing

Speculation – final stage of investing where you have $ to assume larger risks and can continue to invest regularly in a diversified account can lose or gain large sums in a short time periodBe aware of risks & prepared to deal with consequences

© South-Western Educational Publishing

Reasons for Investing

Investing helps beat inflation.Investing increases wealth.Investing is fun and challenging.

© South-Western Educational Publishing

Inflation

InflationInflation - rise in the general level of prices

The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid

by urban consumers for a market basket of consumer goods and services.

Greatest impact on people living on fixed-income

© South-Western Educational Publishing

Risk and Return

DiversificationTypes of risk

Interest-rate riskPolitical riskMarket riskCompany or industry risk

© South-Western Educational Publishing

Diversification

Diversification: An investment strategy in which you spread your investment dollars among industry sectors. It is a widely used and highly successful way to reduce risk.

© South-Western Educational Publishing

Diversification

Most financial planners agree with the admonition “don’t put all your eggs in one basket.

© South-Western Educational Publishing

Types of Risk

© South-Western Educational Publishing

Types of Investment Risk

Company Risk / Financial RiskCompany Risk / Financial Riskbusiness or government may not be able

to return your money

Market RiskMarket Riskif demand for certain investments

decrease, so does the price of the investment (national/world events, business decline)

© South-Western Educational Publishing

Types of Investment Risk

Political RiskPolitical Riskgovernment actions affect business

decisions

Liquidity RiskLiquidity Riskability to turn your money into cash or

spendable funds

Fraud RiskFraud Riskinvestments that are misrepresented

© South-Western Educational Publishing

Types of Investment Risk

Inflation RiskInflation Riskreturn on investment will not keep up with

inflationReal Rate of Return v. Nominal Rate

of Return

Nominal Rate minus (-) inflation rateEX: CD @ 8% return = If inflation rate is 3%, your

real rate of return is 5%

© South-Western Educational Publishing

GOALSGOALS

Lesson 11.2

Exploring Investment Options

List and describe sources of financial information useful for making investment decisions.List and define basic investment options, rated by risk.

© South-Western Educational Publishing

Investment Options

RISK - The chance of losing all or part of the value of an investment. Risk can be divided into three categories;

Conservative—fixed income and preferred stocks are considered conservative.

Moderate—include growth stocks—particularly young companies with great potential.

Speculative—stocks that are highly unpredictable. For example, many dot/com stocks are highly speculative, with incredible highs and devastating lows.

© South-Western Educational Publishing

Investment Options

Risk Tolerance: An investor’s ability to accept loss of some or all of the money he or she has invested, based on a number of factors including

-- age, financial stability, amount of time before the invested funds are needed for other purposes, etc.

© South-Western Educational Publishing

Risk Tolerance Quiz

Go to MHS Website K. Cohen / Personal Finance Student Activities Chapter 11 – Risk Tolerance

Test

© South-Western Educational Publishing

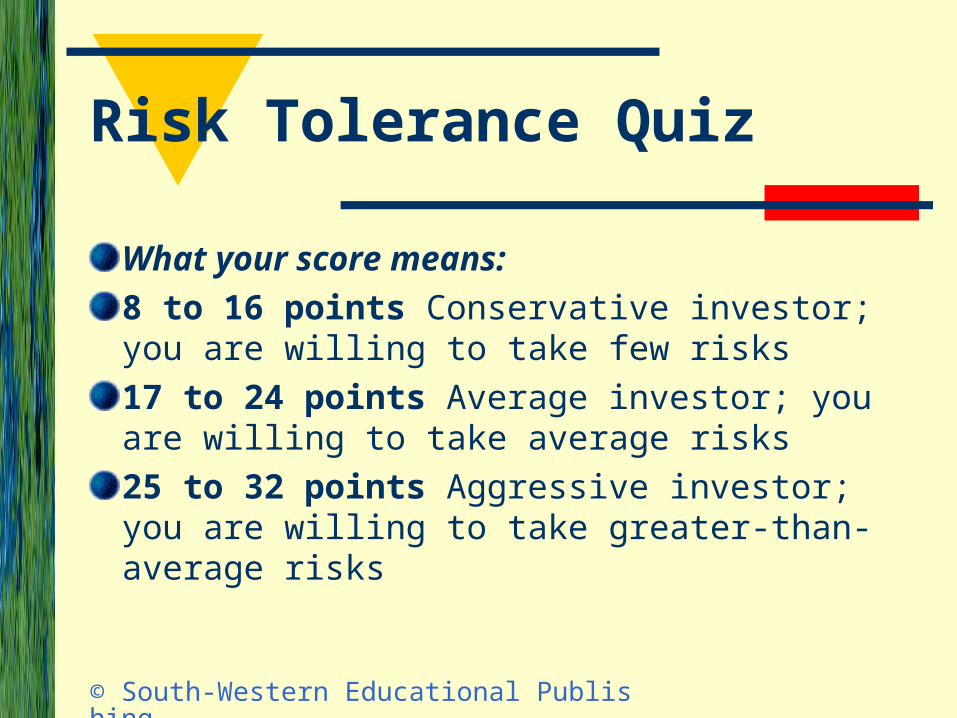

Risk Tolerance Quiz

What your score means:8 to 16 points Conservative investor; you are willing to take few risks17 to 24 points Average investor; you are willing to take average risks25 to 32 points Aggressive investor; you are willing to take greater-than-average risks

© South-Western Educational Publishing

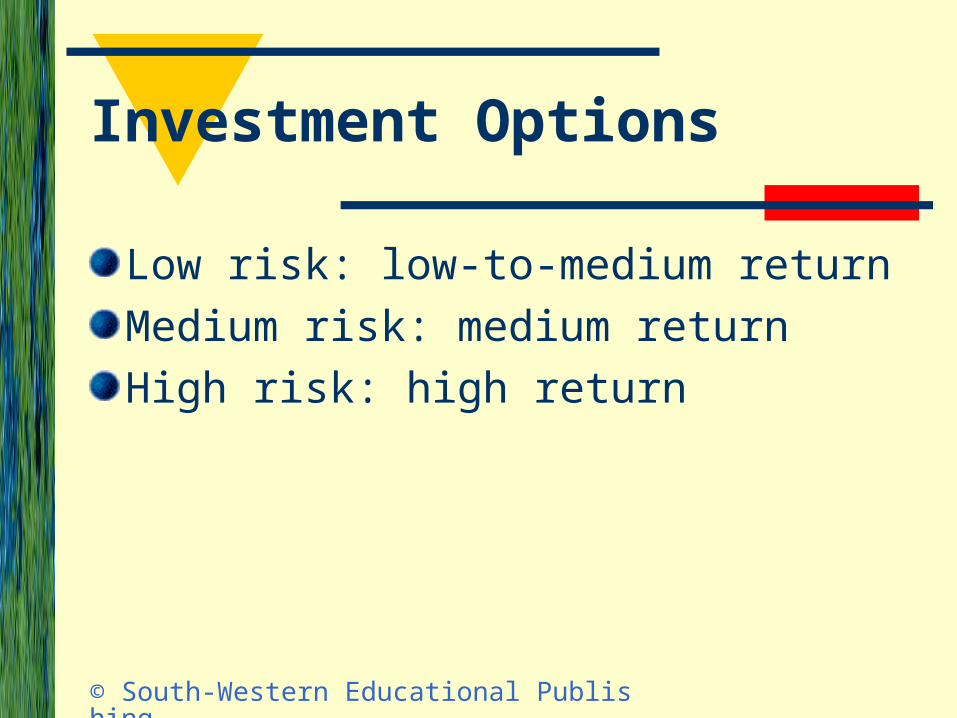

Investment Options

Low risk: low-to-medium returnMedium risk: medium returnHigh risk: high return

© South-Western Educational Publishing

Low Risk:Low-to-Medium Return

Corporate and municipal bondsU.S. government savings bondsTreasury securities

© South-Western Educational Publishing

Medium Risk:Medium Return

Mutual fundsAnnuitiesSelf-managed retirement accountsReal estate

© South-Western Educational Publishing

High Risk:High Return

Stocks and trading instrumentsFuturesOptionsPenny stocksCollectibles

© South-Western Educational Publishing

Investment Options

Go to Quia Personal Finance Chapter 11 - RISK

© South-Western Educational Publishing

Criteria for Choosing an Investment

SafetyHigh liquidityHigh dividends or interestGrowth in value that exceeds the inflation rateReasonable purchase priceTax benefits

© South-Western Educational Publishing

Wise Investment Practices

Define your financial goals.Go slowly.Follow through.Keep good records.Seek good investment advice.Keep investment knowledge current.Know your limits.

© South-Western Educational Publishing

Sources of Financial Information

NewspapersInvestor services and newslettersFinancial magazinesBrokersFinancial advisersAnnual reports and financial statementsOnline investor education

© South-Western Educational Publishing

Types of Brokers

Brokers are required to pass an exam and register with the National Association of Securities Dealers (NASD).

© South-Western Educational Publishing

Types of Brokers

Full-service brokers Helping clients develop investment goals,

researching and recommending investment opportunities for individual clients, as well as executing purchases and sales of bonds for a client’s portfolio

Higher costs involved for providing service

© South-Western Educational Publishing

Types of Brokers

Discount/Online brokers execute buy and sell orders for clients, but they generally do not make investment recommendations and they often provide very little adviceCommissions are lower

© South-Western Educational Publishing

Considerations for Evaluating a Potential Financial Professional

T R U S T You need to feel confident about this

person’s knowledge of the market as well as his or her ability to maintain and manage a professional relationship with you.

© South-Western Educational Publishing

Considerations for Evaluating a Potential Financial Professional

C O M P E T E N C E Make sure he or she has the

education, experience, and credentials necessary, as well as proven success in the field.

© South-Western Educational Publishing

Considerations for Evaluating a Potential Financial Professional

C O M P L I A N C E Ask whether or not he or she has a history

of regulatory disciplinary problems. You can check on a brokers’ background through the National Association of Securities Dealers’ NASD Broker Check online service or through the U.S. Securities and Exchange Commission Investment Adviser Public Disclosure service.

© South-Western Educational Publishing

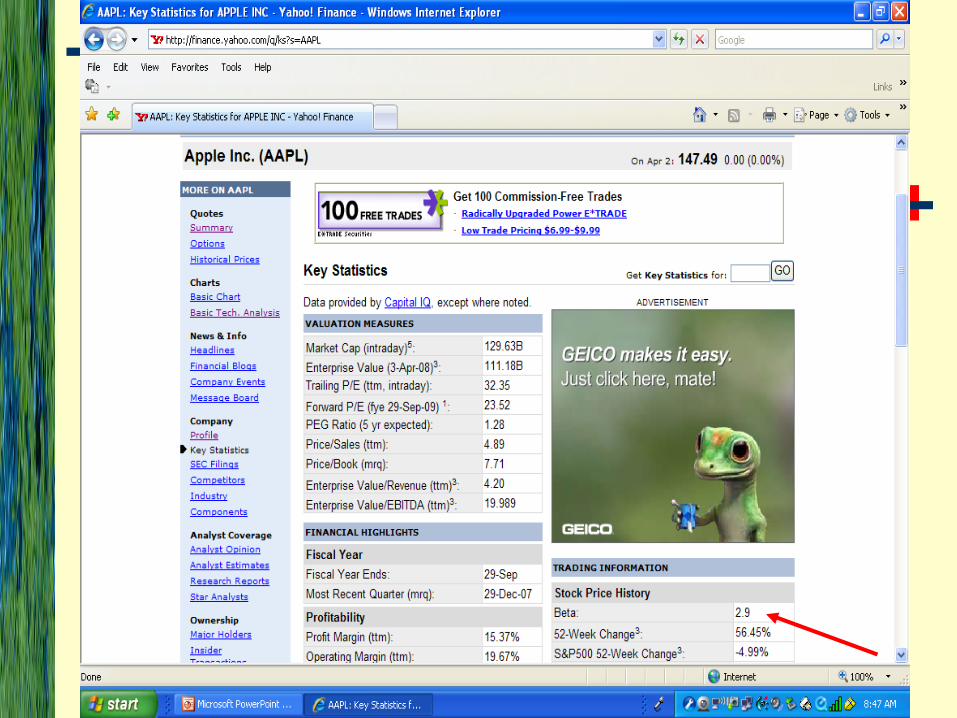

BETA

A stock’s beta number is one way investors can estimate the level of a stock’s risk. However, no measure of risk or volatility is fool-proof or consistently accurate. The beta—a measure of a stock’s volatility—shows of how a particular stock's price moves in relation to the market as a whole.

© South-Western Educational Publishing

BETA

There are betas for individual stock and for industries. A beta number greater than 1 is considered high risk.

© South-Western Educational Publishing

BETA

A beta of 1 indicates that the stock price should move with the overall market. For example, if a stock’s beta is 1 and the market goes up 20%, the stock’s price can be expected to go up 20%. If the market is down 10%, the stock may be down 10%. The beta reflects the stock’s performance over months, not days.

© South-Western Educational Publishing

© South-Western Educational Publishing

© South-Western Educational Publishing

© South-Western Educational Publishing

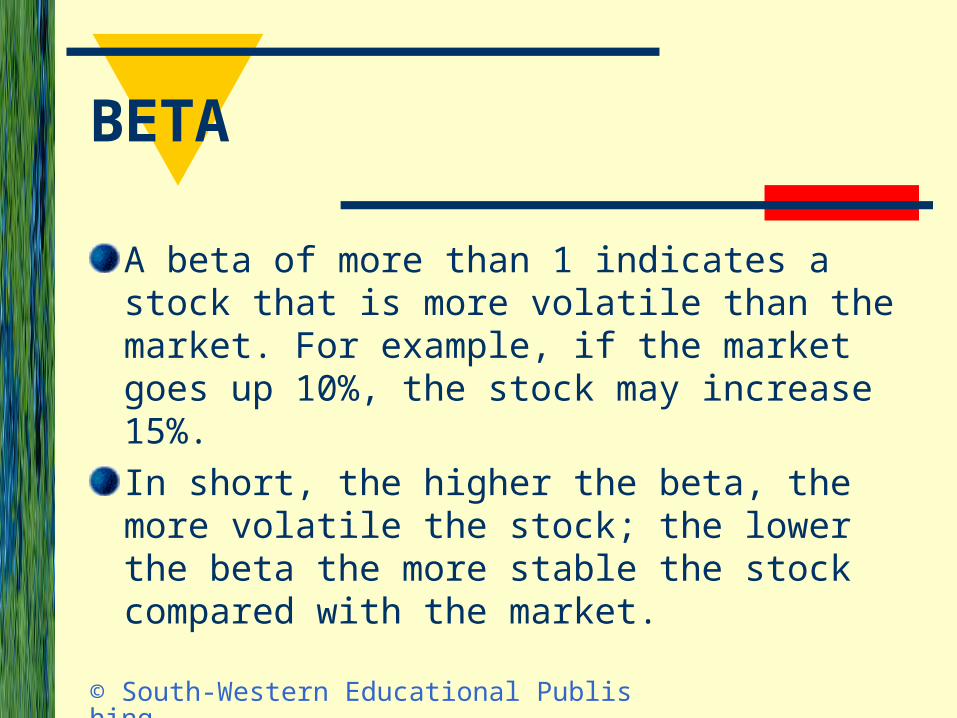

BETA

A beta of more than 1 indicates a stock that is more volatile than the market. For example, if the market goes up 10%, the stock may increase 15%. In short, the higher the beta, the more volatile the stock; the lower the beta the more stable the stock compared with the market.

© South-Western Educational Publishing

© South-Western Educational Publishing

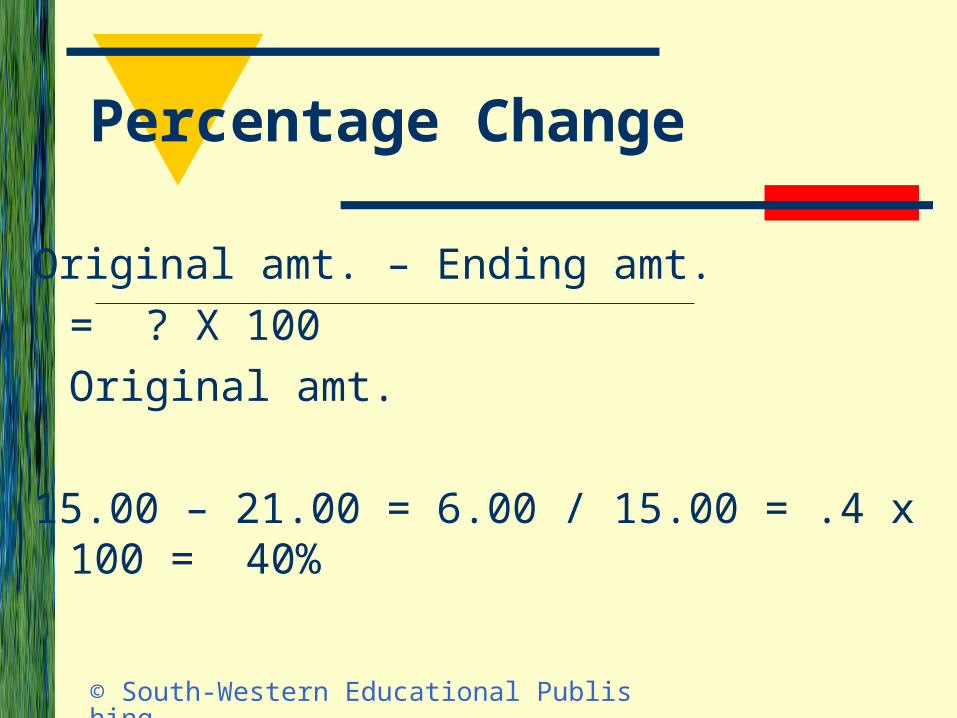

Percentage Change

Original amt. – Ending amt.= ? X

100Original amt.

15.00 – 21.00 = 6.00 / 15.00 = .4 x 100 = 40%

© South-Western Educational Publishing

Beta

(S&P x Beta) x Cost of Share

© South-Western Educational Publishing

Annual Report

An SEC (Securities and Exchange Commission) -required summary of a corporation’s financial results for the year and prospects for the future.

© South-Western Educational Publishing