Embed Size (px)

Citation preview

Minnesota Mosquitos…and other things that bite!

Accounting + Taxes … and morePam Lesch & Rick Krolak have worked together for 20+ years specializingin taxes & accounting for individuals and small to mid-sized businesses.

This booklet previews their Recipes for Financial Success. It will help youto be more creative with your money and to make dealing with the IRSless taxing … without getting stung!

Compare different business models, their advantages & disadvantages,and determine which is the right one for you. Learn about depreciation,gains & losses, and the importance of separating personal expenses frombusiness expenses.

Gain insight on these topics, all served up without cookin’ the books.

P.A.M. LeschTaxes + Accounting Services

3538 Stinson Blvd. NE • Minneapolis, MN 55418612.378.3070 • Fax: 612.378.2559

www.taxpam.com • [email protected]

The Clarion Group, Inc.Accounting & Tax Services

Rick Krolak, EA10201 Wayzata Blvd., #100 • Minnetonka, MN 55305

612.825.5700 • Fax: 888.201.8539www.clariongroup.net • [email protected]

BookKeepMeBookkeeping Service for Busy People

3538 Stinson Blvd. NE • Minneapolis, MN 55418612.816.3505 • Fax: 612.378.2559

Take the sting out of Accounting & Taxes

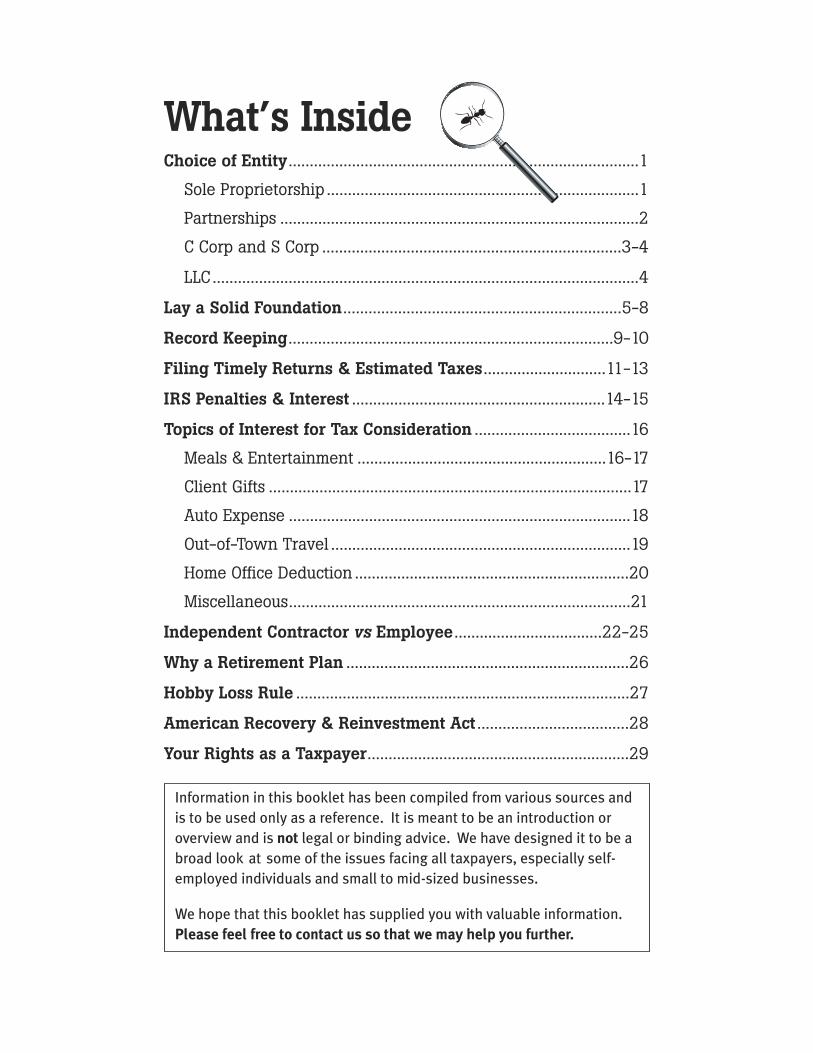

What’s InsideChoice of Entity...................................................................................1

Sole Proprietorship ..........................................................................1

Partnerships .....................................................................................2

C Corp and S Corp .......................................................................3-4

LLC.....................................................................................................4

Lay a Solid Foundation..................................................................5-8

Record Keeping.............................................................................9-10

Filing Timely Returns & Estimated Taxes.............................11-13

IRS Penalties & Interest ............................................................14-15

Topics of Interest for Tax Consideration .....................................16

Meals & Entertainment ...........................................................16-17

Client Gifts ......................................................................................17

Auto Expense .................................................................................18

Out-of-Town Travel .......................................................................19

Home Office Deduction .................................................................20

Miscellaneous.................................................................................21

Independent Contractor vs Employee ...................................22-25

Why a Retirement Plan ...................................................................26

Hobby Loss Rule ...............................................................................27

American Recovery & Reinvestment Act ....................................28

Your Rights as a Taxpayer..............................................................29

Information in this booklet has been compiled from various sources andis to be used only as a reference. It is meant to be an introduction oroverview and is not legal or binding advice. We have designed it to be abroad look at some of the issues facing all taxpayers, especially self-employed individuals and small to mid-sized businesses.

We hope that this booklet has supplied you with valuable information.Please feel free to contact us so that we may help you further.

Choice of EntityThe choice of entity decision is one of the most important decisionsfacing those who own and operate businesses. There are severalforms to choose from, each of which generates different legal andtax consequences. Further, there is no single form of entity that isappropriate for every type of business owner or entity.

Choosing the appropriate form of entity in which to operate abusiness is a complex decision. It is always best to sit down withan attorney and/or an accountant to discuss the best corporatestructure for your specific business.

Sole ProprietorshipGeneral - A sole proprietorship is an unincorporated form ofbusiness with one owner. For tax purposes, the income andexpenses of the business are reported on the personal tax returnof the owner (Schedule C, Form 1040 ). In addition to income taxes,the Sole Proprietor is also subject to self-employment (socialsecurity & medicare) taxes at a current rate of up to 15.3%.

Liability protection - A legal Single Person is not a separate legalentity from its owner. However, a single-member LLC or LLP isseparate from its owner, even though, for tax purposes, it is nottreated as a separate entity.

Taxation - For tax purposes only, a Sole Proprietor includes a single-member entity, such as a limited liability company ("LLC")or limited liability partnership ("LLP"), which has not elected to betaxed as a corporation. The default tax classification of a single-member entity is SP, if the owner is an individual, or a branch ordivision of a business entity.

1

PartnershipsGeneral Partnership

General - A general partnership is an unincorporated entity(either U.S. or non-U.S.), with at least two owners, which isorganized to carry on a trade or business. A general partnershipis not registered in a specific state, since there is no formalregistration required to form a general partnership. Instead, ageneral partnership comes into being as soon as two or morepersons join together to own and operate a business. Ownershipof a general partnership is in the form of partnership units, shares,or percentages. A general partnership must have at least twoowners, but there is no upper limit on the number of owners.In addition, there are no restrictions on the kinds of owners thatcan be partners.

Liability protection - A general partnership ordinarily owns itsassets, although not always. Sometimes property is held in thename of individual partners, and is used in the partnership.A general partnership is nominally responsible for its own debts;that is, money may be borrowed in the name of the partnership.However, general partners are also personally responsible for allpartnership recourse debt.

Transfer of income to partners - A general partnership can hireemployees who are not partners.

Employees of a general partnership are eligible to receive a varietyof tax-free fringe benefits, such as health care. However, partnerscannot receive these benefits tax-free. Both partners andemployees, however, can participate in company-sponsoredretirement plans.

2

Taxation of a general partnership - A general partnership doesnot pay tax.

Taxation of partners - Partners of a general partnership are taxeddirectly on partnership-level income.

Partners can deduct losses equal only to their investmentsin the company.

C CorporationGeneral - A C corp is a corporate entity (either U.S. or non-U.S.).A U.S. corporation is organized in a single state, although thecorporation may do business in many states. Ownership of acorporation is in the form of stock. There is no limit to the numberof shareholders that can own a single C corporation. A corporationcomes into being when its organizers file articles of incorporationwith a state (or country, in the case of a foreign corporation).

Liability protection - A corporation owns its assets and is liable forits debts. Shareholders are not liable for corporate debt. The factthat the shareholders are not liable for corporation debt is one ofthe primary advantages of the corporation as a form of business.

Taxation - A C corporation is taxable on the income it earns.Shareholders of a C corporation are not directly taxable on thisincome. A C corporation is the only business form where this isthe case.

3

S CorporationGeneral - An S corporation is a U.S. corporation that elects to betaxed as an S corporation. A U.S. corporation is organized in asingle state, although the corporation may do business in manystates. Ownership of a corporation is in the form of stock.An S corporation can have no more than 100 shareholders, andcan have only one class of stock. In addition, eligible shareholdersinclude only individuals, certain estates, certain trusts, andcertain other S corporations.

Liability protection - Same as C corporation as outlined above.

Taxation of an S corporation - With some exceptions,an S corporation is not taxable on the income it earns as it passesto the shareholders on their respective K-1s.

Limited Liability Company (LLC)A limited liability company ("LLC") is a hybrid entity that istreated like a corporation for limited liability purposes, but,for tax purposes can choose to be taxed either as a corporation,partnership, or disregarded entity (single-member LLC). An LLC iscreated under state law by registering under a state LLC statute.Like corporate shareholders, LLC members are not personallyliable for the obligations of the LLC; instead, their liability is limitedto their financial investment in the enterprise. Unlike a limitedpartnership, where general partners remain liable for partnershipdebt, all members of an LLC have limited liability.

For an LLC that chooses to be taxed as a partnership, the tax rulesare the same as those of general partnerships, except for minordifferences. Similarly, an LLC that elects to be taxed as acorporation will be taxed in the same way as a corporation.

4

Lay A Solid FoundationFor Your Young BusinessTalking points pulled from the article by Andrew Tellijohn “In theBeginning: How to lay a solid foundation for your young business”appearing in Upsize magazine, November 2007.

1. Corporate structure matters, to you and investors,so get advice

• A business lawyer and/or accountant will know what thebest entity is. It is important for entrepreneurs to find theseexperts for these and other decisions.

2. Conduct market research

• Identify your top 20 potential customers.

• Talk to people in your industry. They have a vested interestin seeing your industry succeed.

• Be ready to make a concise case to potential investors,and include your own investment as they like to seeentrepreneurs put their own money on the line.

3. Writing a business plan

• Key question to address is how will you be different?

• Inexperienced entrepreneurs often rely on instinct and thinkthey can have a plan but not write it down, but investors aregoing to want to get a sense for the homework you’ve done.

• One frequently overlooked portion of a business plan is thecompetition analysis.

5

4. Drafting business documents

• Some documents are a must at the outset, others can wait.

• There’s no need to put together an employment agreementuntil you are planning to hire employees.

• The articles of incorporation (or articles of organization forLLC’s), which state a corporation’s name, principal place ofbusiness, corporate purpose, a registered agent authorizedto accept delivery of certain legal documents, and stockinformation, are required in most states.

• Several other documents should be considered.

• Noncompete agreements are good to have, though courtsare making them harder to enforce.

• If you are starting a business with a partner, it’s a good ideato put in writing a partnership agreement spelling out whathappens if things go bad. It is best to include a businessattorney in the process.

5. Implementing technology systems

• Choose tech systems to grow along with company. Choosewisely. Replacing the wrong system is much more expensivethan taking the time to do it right the first time.

6. Managing and insuring risk

• How much insurance? Weigh risks against cost to decide.

• Assuming your small business is renting property, has somebank debt, and has or is planning for employees, there is achecklist of insurance coverages it will be required topurchase right out of the gate.

6

7. Handling daily finances

• Pay attention to all-important cash flow to avoid downfall.

• Making sales calls, monitoring productivity, it can be easy tofall behind on day-to-day accounting activities like enteringtransactions or filing payroll taxes. It’s also one of the mostoverwhelming mistakes a start-up company can make.While it depends on the initial size of the company it oftenmakes sense to outsource accounting functions initially soentrepreneurs can focus on their business, while knowingthe daily cash flow statements, monthly financial reportsand quarterly tax filings will be up to date. If you choose tokeep the accounting functions in house you need toimmediately establish procedures so you know where youstand.

8. Hiring employees

• Adding staff means knowing laws, offering benefits.

• Entrepreneurs often think they can handle each and everypart of their business. They can’t. Live with it. And bringpeople in who can help.

• Create an employee handbook. It doesn’t need to becomplex and it should be reviewed so it doesn’t create anactual contract with employees.

• Train, train, train. Human resources rules and policieschange frequently and whoever is in charge of knowingthem at your company must constantly be getting updated.

• The need for noncompete contracts depends on thetype of company.

• On a benefits front, the basic starting points are amedical plan, a retirement plan, a dental plan, perhaps lifeinsurance, long-term disability, and short-term disability.

7

9. Finding people to help

• Advisors who’ve seen it all can help owners throughadversity.

• Seek mentorship.

• Maintain regular communication with your attorney, youraccountant and your banker.

• Keep employees informed about the status of the companybut don’t make them a part of the inner advisory circle as itmay create anxiety and insecurity.

• Don’t feel like you have to go through adversity alone.

8

9

Record KeepingRecord keeping & compiling is critical to running aresponsible business.

If you as the individual business owner, have a preferred wayof organizing & compiling records, income & expenses thatis wonderful.

Most all accountants & tax preparers can work withestablished reporting.

Some of the preferred forms that we have seen are Xceland/or general worksheets, QuickBooks, Quicken, & MYOB.

Our clients have used both in-house bookkeeping (themselvesor an employee) & outsourced services as well.

Accuracy & consistency are critical hallmarks in this area.

The IRS reacts more favorably to good records than shoeboxes, rubber banded receipts & post-it notes.

Saving RecordsIt is necessary to keep all receipts & complication records as theyapply to your tax return for three years in order to substantiatethe information on the tax return.

The Statute of Limitations for most federal tax returns isthree years.

For prior year tax returns seven or more years is necessary.

If in the course of your business you buy buildings or have othersubstantial assets, loans, capital losses, etc., it is advisable tohang onto them for the life of the business.

Personal Tax ReturnsThe same holds true plus additional record holdings, e.g. marriage,death & birth certificates, etc. are a few.

It is important to know what your state's statutes are as well.

Tax payers bear the burden of proving entitlement to anyclaimed deductions. As part of their burden,tax payers must substantiate the amount oftheir claimed deductions.

A tax payer is required to maintain records sufficientto establish the amount of any deduction claimed.

10

BUGOFF

Filing Timely Returns& Making EstimatedPayments

It is important that timely returns be filed.

APRIL 15TH is the filing date for all personal returns, includingSole Proprietors & single member LLC. It is also the date for filingannual Partnership Returns. Fiscal returns are due three & one-half months after the close of the fiscal year end.

S Corp & Corporate Annual Returns are due MARCH 15TH unlessyou have a fiscal year-end. In that case they are due two & one-half months after the close of your fiscal year end.

You are entitled to file an extension for all of these returns.

There is a three year statute of limitationson refunds for UNFILED tax returns.

11

Estimated Taxes The federal income tax system is a pay as you go system. Ingeneral you're required to pay tax over the course of the yearrather than waiting until April 15. Most people meet thisrequirement without really thinking about it because of tax that'swithheld from their wages. But if you have significant amounts ofinvestment income (or other types of income that aren't subject towithholding) you may incur a penalty if you don't make quarterlypayments of estimated tax. If you don't pay enough estimated tax,or don't pay on time, you'll have to pay a penalty. It's best to avoidthis penalty.

What we recommend as a good thumbnail for your startup year isto put aside 36% of your net bottom line (income less expenses)for estimate tax payments. You will need 15% for social security,10-15% for federal income tax, and 6% for Minnesota income tax.

Prior year safe harborMost people can avoid paying estimated tax if their withholdingand credits equal 100% of the tax shown on the prior year's return.We call this the prior year safe harbor.

Voluntary paymentsSome people choose to make estimated tax payments even whenthe payments aren't required. This approach deprives you of theopportunity to earn interest on the amount you prepaid, butassures that you won't have a crushing tax bill on April 15.

12

When to send paymentsFor nearly all taxpayers, the due date for the first estimated taxpayment of each year is April 15 … the same day the return is duefor the previous year. Subsequent payments are due June 15,September 15, and January 15 of the following year. You'll want tonote the following points:

If you owe money with your tax return, and have to make anestimated tax payment, you have two checks to write onApril 15. Be prepared!

Although the payments are "quarterly," they aren't threemonths apart. The second payment is due just two monthsafter the first one.

What to fileForm 1040-ES, Estimated Tax

Keep recordsBe sure to keep an accurate record of your estimated tax paymentsso you can claim credit for them when you file your return.

13

IRS Tax Penalties & InterestFiling & Owing is Better ThanNot Filing & OwingIf you owe taxes, the Internal Revenue Service will calculatepenalties and interest on the amount owed. If you have a refund,the IRS may pay you interest on the delayed refund. (Note thedifference between "will" and "may"; the IRS generally paysinterest on refunds that have been delayed because of slowprocessing by the IRS. Since most late tax returns take longer toprocess, the IRS may pay you interest based on the extra amountof time it takes them to process your return.) If you have a refund,there is no penalty for filing late. Penalties are calculated on theamount due. Since there is no amount due, there is no penalty.

If you have a balance due on a late tax return, the IRS will calculateadditional penalties and interest. There are three separatepenalties. Each is calculated differently.

• Failure to File Penalty

• Failure to Pay Penalty

• Interest

Failure to File PenaltyThe failure-to-file penalty is calculated based on the time from thedeadline of your tax return (including extensions) to the date youactually filed your tax return. The penalty is 5% for each month thetax return is late, up to a total maximum penalty of 25%. Thepercentage is of the tax due as shown on the tax return. If your taxreturn is more than five months late, simply multiply your balancedue by 25% to calculate your failure to file penalty.

14

Failure to Pay PenaltyThe failure-to-pay penalty is calculated based on theamount of tax you owe. The penalty is 0.5% for eachmonth the tax is not paid in full. There is no maximumlimit to the failure-to-pay penalty. The penalty iscalculated from the original payment deadline(the original April 15th filing deadline) until thebalance due is paid in full.

InterestInterest is calculated based on how much tax you owe. Interestrates change every three months. Currently, the IRS interest ratefor underpayment of tax is 5% per year. The interest is calculatedfor each day your balance due is not paid in full. IRS interest ratesare variable and are set quarterly.

Action Plan ItemsThere's a lesson to be learned by looking at thepenalties. If you owe, it is better to file soonerrather than later. Also, if it looks like you are goingto be a few months late on your next tax return,file an extension. By filing an extension youmay reduce or eliminate the Failure to File Penalty.

15

BUGOFF

Topics of Interest for TaxConsiderationMeals & Entertainment50% deduction when allowed

Must be present to take the deduction. Example: tickets forentertainment or sporting events given to clients that you don’tattend are considered client gifts.

Substantiation required:

Amount of expenses

Time and place

Business relationship with client

An expense less than $75 does not need a receipt

Per diem rate can be used as a standard deductionwhile traveling

Per diem rates can be used for travel – high of $64 and low of $45

No deduction allowed for entertaining in clubs, bars, sportingevents or entertainment venues unless directly before or afterbusiness discussions/activity.

No deduction for use of an entertainment facility includingexpenses for depreciation and operating costs such as rent,utilities, maintenance, and protection.

16

An entertainment facility is any property that you won,rent, or use for entertainment such as a yacht,hunting lodge, fishing camp, swimming pool, tennis court,bowling alley, car, airplane, apartment, hotel suite,or home in a vacation resort.

No deduction for club dues or membership fees.

Take a full deduction for meals/beverages in connection with itemsprovided to the general public or in connection with meeting.

Client Gifts

Limit to $25 per client per year

Items of small value, such as giving away pens imprinted withbusiness name costing $4 or less, are not included in the limit.

17

Standard or Actual Auto ExpenseMethodsYou may know that because the IRS provides a standard mileagerate for the deduction of vehicle expenses used in your business,you are allowed to choose between this rate and the actualexpenses you incur in calculating this deduction. Because themileage rate includes nearly all of the expenses you incur it istypically much easier to apply. All you need are mileage logs andthe current rate allowed by the IRS. Actual expenses includedepreciation, licenses, gas, oil, tolls, lease payments, insurance,garage rental, parking, registration fees, repairs, maintenance, tirecosts, etc. Expenses for personal property taxes and parking aredeductible even if you do take the standard mileage deduction.

As of January 2009, the current standard mileage rate is .55 centsper mile. It is still a good idea to runboth calculations to be sureyou’re deducting as much as youcan. If you will ever use thestandard mileage deduction,you are required to use it in thefirst year your vehicle is in servicefor business purposes.

18

Out of Town TravelMust have a business purpose

Must separate out expenses from hotels that are for meals orbeverages – lodging is 100% deductible, the meal/beverageportion is 50% deductible.

Can use per diem rate rather than keep receipts for meals andincidentals.

Transportation costs to/from location are deductible unlessthe trip is deemed to be personal/vacation in nature. Nodeduction allowed for transportation to or from location butdirect business expense while on the trip are deductible.

Can’t deduct expenses for extended stays on business tripunless proof of travel savings. For example, if staying over aFriday night would reduce airfare substantially to justify theextra night.

There are substantial limitations on travel outside of U.S. andtravel on cruise ships.

Laundry and dry cleaning are deductible while traveling.

19

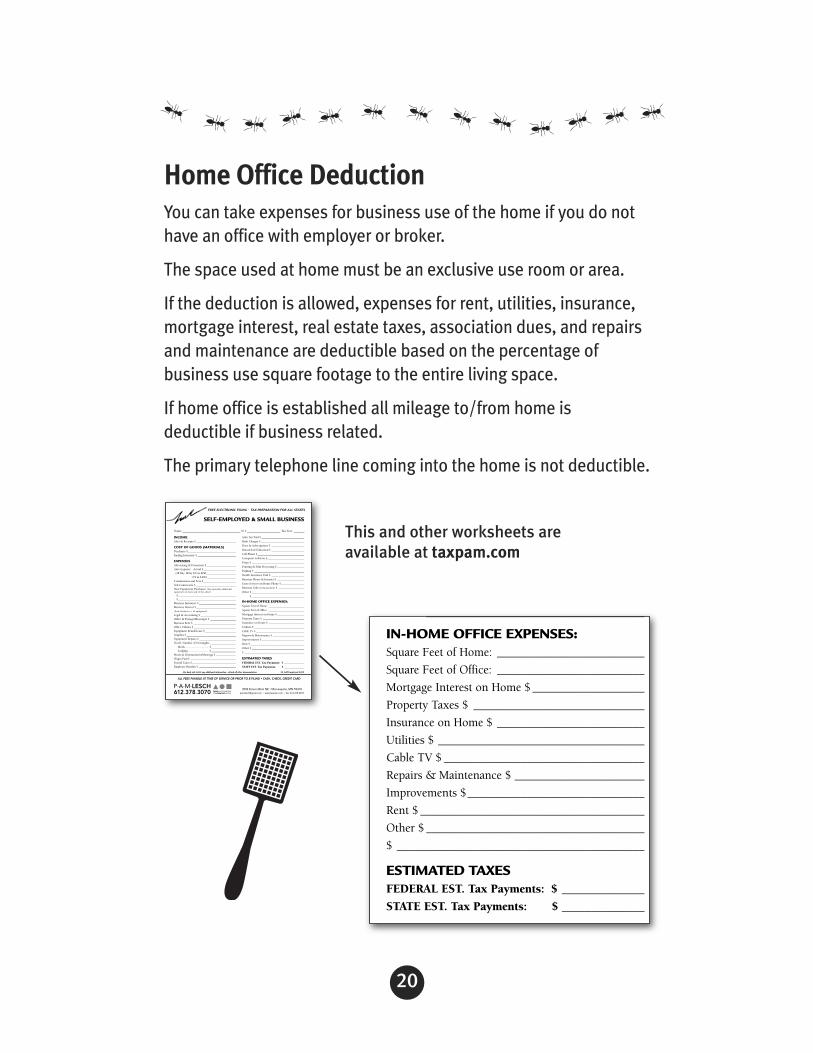

Home Office DeductionYou can take expenses for business use of the home if you do nothave an office with employer or broker.

The space used at home must be an exclusive use room or area.

If the deduction is allowed, expenses for rent, utilities, insurance,mortgage interest, real estate taxes, association dues, and repairsand maintenance are deductible based on the percentage ofbusiness use square footage to the entire living space.

If home office is established all mileage to/from home isdeductible if business related.

The primary telephone line coming into the home is not deductible.

20

SELF-EMPLOYED & SMALL BUSINESS

FREE ELECTRONIC FILING • TAX PREPARATION FOR ALL STATES

INCOMESales & Receipts $ ____________________________

COST OF GOODS (MATERIALS)Purchases $__________________________________Ending Inventory $ ___________________________

EXPENSESAdvertising & Promotion $_____________________Auto Expense: Actual $_______________________

OR Bus. Miles 1/1 to 6/30_____________________7/1 to 12/31 ____________________

Commissions and Fees $_______________________Sub-Contractors $ ____________________________New Equipment Purchases: (list separately additionalequipment on back side of this sheet)

$_________________________________________$_________________________________________

Business Insurance $ __________________________Business Interest $ ____________________________(loan, business c.c. & equipment)

Legal & Accounting $ _________________________Office & Postage/Messenger $ __________________Business Rent $ ______________________________Office Utilities $______________________________Equipment Rental/Lease $______________________Supplies $___________________________________Equipment Repairs $ __________________________Travel: Number of Overnights __________________

Meals ..................................$_________________Lodging ..............................$_________________

Meals & Entertainment/Meetings $ ______________Wages Paid $ ________________________________Payroll Taxes $_______________________________Employee Benefits $ __________________________

Sales Tax Paid $ ______________________________

Bank Charges $ ______________________________

Dues & Subscriptions $ _______________________

Research & Education $ _______________________

Cell Phone $_________________________________

Computer Software $__________________________

Props $ _____________________________________

Printing & Film Processing $ ___________________

Parking $ ___________________________________

Health Insurance Paid $ _______________________

Business Phone & Internet $ ___________________

Extra Services on Home Phone $ ________________

Business Gifts ($25max/client) $ __________________

Other $ _____________________________________

Other $ _____________________________________

IN-HOME OFFICE EXPENSES:Square Feet of Home: _________________________

Square Feet of Office: _________________________

Mortgage Interest on Home $ ___________________

Property Taxes $ _____________________________

Insurance on Home $ _________________________

Utilities $ ___________________________________

Cable TV $ __________________________________

Repairs & Maintenance $ ______________________

Improvements $______________________________

Rent $ ______________________________________

Other $ _____________________________________

$ __________________________________________

ESTIMATED TAXESFEDERAL EST. Tax Payments: $ ______________

STATE EST. Tax Payments: $ ______________

Use back side to list any additional information - attach all other documentation.

Name:______________________________________ SS # ______________________ Tax Year: _______

TAXES+ACCOUNTINGFORCREATIVEPEOPLE

P·A·M·LESCH612.378.3070

3538 Stinson Blvd. NE • Minneapolis, MN [email protected] • www.taxpam.com • fax: 612.378.2559

ALL FEES PAYABLE AT TIME OF SERVICE OR PRIOR TO E-FILING • CASH, CHECK, CREDIT CARD

02 Self Employed 2009

This and other worksheets areavailable at taxpam.com

_____________________________________

IN-HOME OFFICE EXPENSES:Square Feet of Home: _________________________

Square Feet of Office: _________________________

Mortgage Interest on Home $ ___________________

Property Taxes $ _____________________________

Insurance on Home $ _________________________

Utilities $ ___________________________________

Cable TV $ __________________________________

Repairs & Maintenance $ ______________________

Improvements $______________________________

Rent $ ______________________________________

Other $ _____________________________________

$ __________________________________________

ESTIMATED TAXESFEDERAL EST. Tax Payments: $ ______________

STATE EST. Tax Payments: $ ______________

Other Miscellaneous HOT ItemsFor Audit Review100% deductions for cell phone, internet and other expenses thatmay have a portion allocated to personal use.

What If You Have Incomplete Records?

If you do not have complete records to prove an element of anexpense, then you must prove the element with:

your own written or oral statement containing specificinformation about the element, and

other supporting evidence that is sufficient to establish theelement. You can use a sampling method. You can keep anadequate record for parts of a tax year and use that to provethe amount of business or investment use for the entire year.You must demonstrate by other evidence that the periods forwhich an adequate record is kept are representative of the usethroughout the tax year.

21

Independent Contractor vs.Employee StatusTwenty Factor Checklist to Determine1. Instructions. A worker who is required to comply with other

persons' instructions about when, where, and how he or she isto work is ordinarily an employee.

2. Training. Training a worker indicates that the person orpersons for whom the services are performed want theservices performed in a particular method or manner.

3. Integration. Integration of the worker's services into thebusiness operation generally shows that the worker is subjectto direction and control.

4. Services Rendered Personally. If the services must berendered personally presumably the person or persons forwhom the services are performed are interested in themethods used to accomplish the work as well as in the result.

5. Hiring, Supervising, and Paying Assistants. If the person orpersons for whom the services are performed hire, supervise,and pay assistants, that factor generally shows control overthe workers on the job. However, if one worker hiredsupervises, and pays the other assistant pursuant to a contractunder which the worker agrees to provide materials and laborand under which the worker is responsible only for theattainment of a result, this factor indicates an independentcontractor status.

22

6. Continuing Relationship. A continuing relationship betweenthe worker and the person or persons for whom the servicesare performed indicates that an employer-employeerelationship exists.

7. Set Hours of Work. The establishment of set hours of work bythe person for whom the services are performed is a factorindicating control.

8. Full Time Required. If the worker must devote substantiallyfull time to the business and impliedly restrict the worker fromdoing other gainful work. An independent contractor, on theother hand, is free to work when and for whom he or shechooses.

9. Doing Work on Employer's Premises. If the work is performedon the premises of the person or persons for whom theservices are performed, that factor suggests control over theworker, especially if the work could be done elsewhere.

10. Order or Sequence Set. If a worker must perform services inthe order or sequence set by the person or persons for whomthe services are performed, that factor shows that the workeris not free to follow the worker's own pattern of work but mustfollow the established routines and schedules of the person orpersons for whom the services are performed. Often, becauseof the nature of an occupation, the person or persons forwhom the services are being performed do not set the order ofthe services or set the order infrequently. It is sufficient toshow control, however, if such person or persons retain theright to do so. See Rev. Rule 56-694.

23

11. Oral or Written Reports. A requirement that the worker submitregular or written reports to the person or persons for whomthe services are performed indicates a degree of control.

12. Payment by Hour, Week, Month. Payment by the hour, week,or month generally points to an employer-employeerelationship. Payment made by the job or on a straightcommission generally indicates that the worker is anindependent contractor.

13. Payment of Business and/or Traveling Expenses. If theperson or persons for whom the services are performedordinarily pay the worker's business and/or travelingexpenses, the worker is ordinarily an employee.

14. Furnishing of Tools and Materials. The fact that the person orpersons for whom the services are performed furnishsignificant tools, materials, and other equipment tends toshow the existence of an employer-employee relationship.

15. Significant Investment. If the worker invests in facilities thatare used by the worker in performing services and are nottypically maintained by employees (such as the maintenanceof an office rented at fair value from an unrelated party), thatfactor tends to indicate that the worker is an independentcontractor.

16. Realization of Profit or Loss. A worker who can realize a profitor suffer a loss as a result of the worker's services is generallyan independent contractor, but the worker who cannot is anemployee.

24

17. Working for More Than One Firm at a Time. If a workerperforms more than de minimis services for a multiple ofunrelated persons or firms at the same time, that factorgenerally indicates that the worker is an independentcontractor.

18. Making Service Available to General Public. The fact that aworker makes his or her services available to the generalpublic on a regular and consistent basis indicates anindependent contractor relationship.

19. Right to Discharge. The right to discharge a worker is a factorindicating that the worker is an employee, and the personpossessing the right is an employer.

20. Right to Terminate. If the worker has the right to end his or herrelationship with the person for whom the services areperformed at any time he or she wishes without incurringliability, that factor indicates an employer-employeerelationship.

Once you have concluded that the person you are hiringis either a contractor or an employee there is oneimportant form that needs to be put into place beforeyou have made a payment to your new hire.

If the person is an employee (W-2) hire they will need to fillout a W-4 giving their Social Security Number, stating theirpermanent address, recording the number of deductions theyare claiming & whether they are filing single or married.

On the other hand if the individual is a contract hire they needto complete the W-9 to record their Social Security Number, orFederal Identification Number & their address.

25

26

Why a Retirement Plan?A retirement plan is a great idea because you are taking theresponsibility of taking care of yourself and/or your employees.Setting up a Retirement plan will reduce your taxable income andwill promote employee retention and employee motivation.

Retirement Plan TypesThere is a maze of retirement plans. We are not experts in thisfield, but we encourage our clients to set up a relationship with afinancial advisor & begin saving.

Hobby Loss RuleIRS reminds taxpayers aboutHobby Loss Rule(FS-2008-23)

The IRS has released a fact sheet to help taxpayers determinewhether an activity is engaged in for profit or merely as a hobby.The fact sheet discusses the hobby loss rules and lists several non-inclusive factors to be considered when making this determination,including:

Does the time and effort put into the activity indicate anintention to make profit?

Do you depend on income from the activity?

If there are losses, are they due to circumstances beyond yourcontrol or did they occur in the start-up phase of the business?

Have you changed methods of operation to improveprofitability?

Have you made a profit in similar activities in the past?

Does the activity make a profit in some years?

Do you expect to make a profit in the future from theappreciation of assets used in the activity?

Critical: Is/was substantial record keeping in place?

27

American Recovery andReinvestment ActSome ARRA Provisions that could affect2009 tax returns:

Deductions for taxes paid on new vehicle purchase

Credit for higher education expenses ($500 more than theprevious maximum credit)

Some unemployment benefits tax exempt in 2009

Health insurance continuation (COBRA) subsidy

Reduce income tax withholding

• Additional child tax credit

• Earned income tax credit

• Economic Recovery Payment (a one-time payment of$250) will be made to retirees, disabled veterans,and railroad retirees

Affecting Individuals:First-time homebuyer credit expands

Money back for new vehicle purchases

Energy efficiency and renewable energy incentives

Affecting BusinessesMaking work pay tax credit

Work opportunity tax credit

COBRA

28

Your Rights as a TaxpayerIf you have issues that come up with the IRS, you are allowed tohave representation if you decide not to represent yourself.

Your representative must be a person qualified to practicebefore the IRS, such as an attorney, CPA,or an EA (Enrolled Agent).

They will communicate with the IRS for the taxpayerregarding the taxpayer's rights, privileges or liabilities.

They can represent a taxpayer at conference, hearing ormeeting with the IRS. He/she may do that alone or in thecompany of the taxpayer.

They can prepare & file all documents with the IRS forthe taxpayer.

In order to represent you, the individual must be designated asthe the taxpayer's power of attorney and file a written declarationwith the IRS stating the he/she is authorized & qualified torepresent a particular taxpayer.

Form 2848 must be used, filed and accepted for this purpose.

29

Notes

Notes

![PDF-1.3 %âãÏÓ 5958 0 obj /Linearized 1 /O 5961 /H [ 1622 1117 ] /L 1102521 /E 94814 /N 78 /T 983241 >> endobj xref 5958 39 0000000016 00000 n 0000001135 00000 n 0000001478 00000](https://img.pdfslide.tips/doc/110x75/5b07fcad7f8b9a5f6d8bb967/pdf-13-5958-0-obj-linearized-1-o-5961-h-1622-1117-l-1102521-e-94814.jpg)