Embed Size (px)

Citation preview

8/21/2019 408-2012-Lec03 DCF2

http://slidepdf.com/reader/full/408-2012-lec03-dcf2 1/1003

• Interest – Real and Nominal

• Project Evaluation Methods

– Discounted Cash Flow

MIN E 408: Mining Enterprise Economics

Review of Economic Indicators

Resources: Any economics book

A class ic: Runge, 1998. Mining Economics and Strategy. 295 p.

Slides modified from Dr. Oy Leuangthong

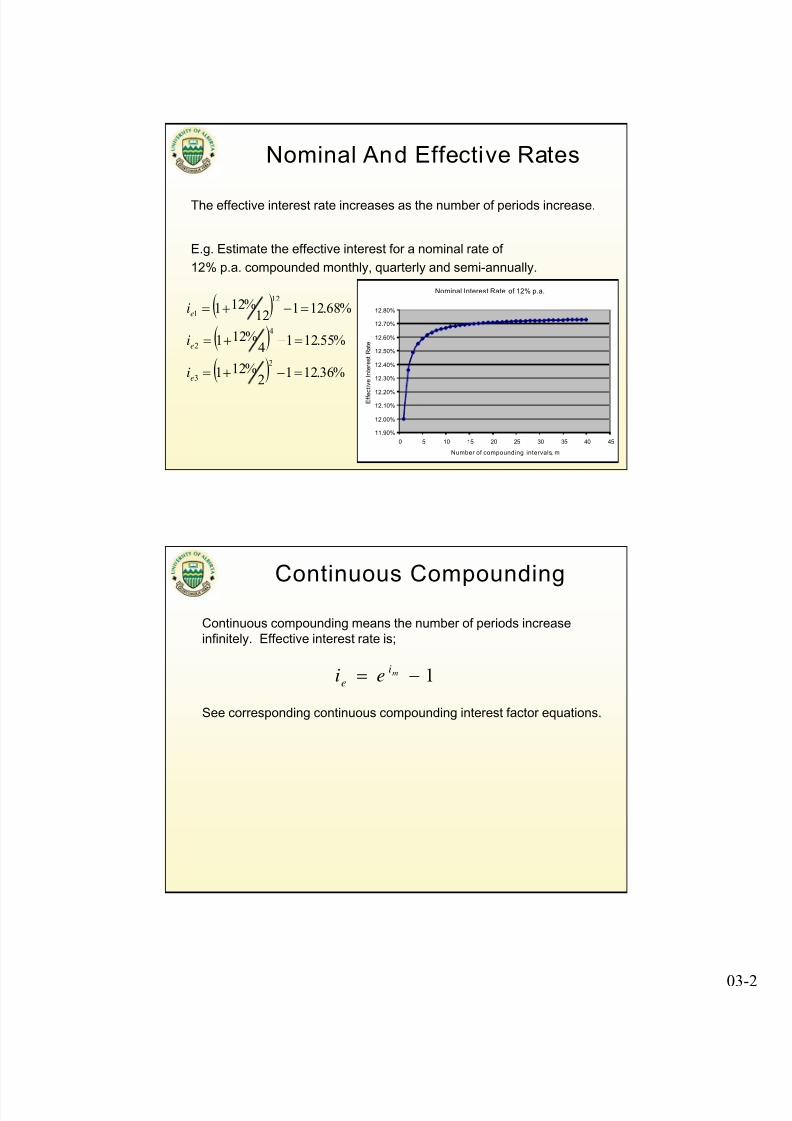

Nominal And Effective Rates

• If m = # of compounding periods per year and m > 1, thenthe effective interest rate, ie > i, the interest rate percompounding period;

• the nominal interest im is given as i*m; and

• the effective interest rate ie is given by

(1 ) 1

m

e

i i

8/21/2019 408-2012-Lec03 DCF2

http://slidepdf.com/reader/full/408-2012-lec03-dcf2 2/1003

The effective interest rate increases as the number of periods increase.

E.g. Estimate the effective interest for a nominal rate of

12% p.a. compounded monthly, quarterly and semi-annually.

Nominal And Effective Rates

%36.1212

%121

%55.1214

%121

%68.12112

%121

2

3

4

2

12

1

e

e

e

i

i

i

Nominal Interest Rate of 12% p.a.

11.90%

12.00%

12.10%

12.20%

12.30%

12.40%

12.50%

12.60%

12.70%

12.80%

0 5 10 15 20 25 30 35 40 45

Number of compounding intervals, m

E f f e c t i v e I n t e r e s t R a t e

Continuous Compounding

Continuous compounding means the number of periods increaseinfinitely. Effective interest rate is;

See corresponding continuous compounding interest factor equations.

1mi

ei e

8/21/2019 408-2012-Lec03 DCF2

http://slidepdf.com/reader/full/408-2012-lec03-dcf2 3/1003

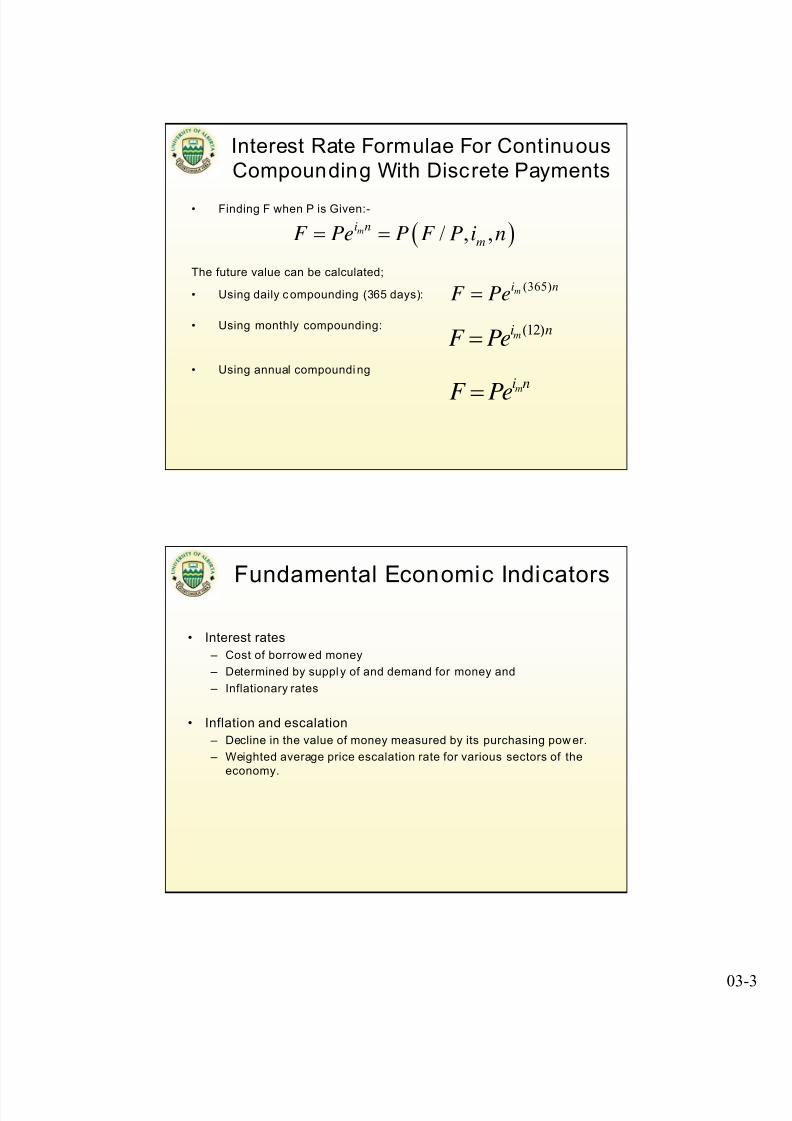

Interest Rate Formulae For ContinuousCompounding With Discrete Payments

• Finding F when P is Given:-

The future value can be calculated;

• Using daily compounding (365 days):

• Using monthly compounding:

• Using annual compoundi ng

/ , ,mi n

mF Pe P F P i n

(365)m

i nF Pe

(12)m

i nF Pe

mi n

F Pe

Fundamental Economic Indicators

• Interest rates

– Cost of borrow ed money

– Determined by suppl y of and demand for money and

– Inflationary rates

• Inflation and escalation

– Decline in the value of money measured by its purchasing pow er.

– Weighted average price escalation rate for various sectors of theeconomy.

8/21/2019 408-2012-Lec03 DCF2

http://slidepdf.com/reader/full/408-2012-lec03-dcf2 4/1003

• Real interest rates

– Nominal interest rate adjusted for inf lation.

If a bank pays 10% (nominal) on deposits

$1000 deposited wil l yield $1100 in a year

If liter of gas cost $1 → $1000 will purchase 1000 liters today

Suppose inflati on rate is 6% after a year

Liter of gas will cost $1.06

The purchasing power of $1100 is in a year 1100/1.06=1,038 liters

Real return on $1000 = 3.8%

Fundamental Economic Indicators

• Real Interest rate

1 Nominal interest rateReal interest rate 1

1 Inflation rate

approximated byReal interest rate Nominal rate - inflation

Fundamental Economic Indicators

8/21/2019 408-2012-Lec03 DCF2

http://slidepdf.com/reader/full/408-2012-lec03-dcf2 5/1003

• Cash flow and Inflation

Like interest rates cash flows can be expressed in either real or nominalterms.

Nominal if actual/current dollars to be received is used.

Real if cash flows are deflated –expressed in terms of current dollar.

Example

Gas price is 50¢ per liter today. Expect prices to appreciate by 4% p.a. forthe next five years. If inflation is 6% p.a. Calculate the nominal and realfuel cost per year if your annual demand is 2 million liters. Determine the

PV of your costs if nominal discount rate is 12%.

Fundamental Economic Indicators

Cash flow and Inflation

Year Nominalcost/liter

Realcost/liter

Nominal cost(m$)

Real cost(m$)

0 0.50 0.50 1.00 1.00

1 0.52 0.49 1.04 0.98

2 0.54 0.48 1.08 0.96

3 0.56 0.47 1.12 0.94

4 0.58 0.46 1.17 0.93

5 0.61 0.45 1.22 0.91

Fundamental Economic Indicators

8/21/2019 408-2012-Lec03 DCF2

http://slidepdf.com/reader/full/408-2012-lec03-dcf2 6/1003

• Real discount rate = 1.12/1.06 – 1= 5.66%

Year Nominalcost (m$)

Realcost(m$)

PV ofNominalCost(m$)

PV of RealCost(m$)

0 1.00 1.00 1 1

1 1.04 0.98 0.93 0.93

2 1.08 0.96 0.86 0.86

3 1.12 0.94 0.80 0.80

4 1.17 0.93 0.74 0.74

5 1.22 0.91 0.69 0.69

PV 5.03 5.03

Nominal cash

flows are

discounted with

nominal discount

rate and real

cash flows are

discounted with

real rates.

Discounting- Real or Nominal interest rate?

Project Evaluation Methods

8/21/2019 408-2012-Lec03 DCF2

http://slidepdf.com/reader/full/408-2012-lec03-dcf2 7/1003

1. Discounted Cash Flow (DCF):Cash flow discounted at an investor arbitrarily selected discount rate

– Net Present Value (NPV).

– Internal Rate Of Return (IRR).

– Profitability Index Or Benefit Cost Ratio.

– Payback And Discounted Payback Period.

2. Capital Asset Pricing Method (CAPM):

Discount rate quantitatively modeled using the beta of a security or project withcomparable risk as project.

3. Option Pricing Method:

Uses Portfolio replication to duplicate the project as consisting of certain basicassets that are risk free. The resulting portfolio of assets must have a returnequal to the risk f ree rate.

Project Evaluation Methods

NET PRESENT VALUE (NPV)

• Decision Criteria - Take project if NPV>0

Example

• XYZ Resources is considering an expansion project; immediate cost is$120,000

• Project would increase cash flows by $15,000 per year for 10 years(starting next year)

• Residual salvage value: $48,000

• Should XYZ take project if discount rate = 10%?

returnof rate-

11

0

RRR

RRR

CF I NPV

T

t

t

t

Investment Decision Criteria

8/21/2019 408-2012-Lec03 DCF2

http://slidepdf.com/reader/full/408-2012-lec03-dcf2 8/1003

Investment Decision Criteria: NPV

• Take project if PI > 1.

0

0

0

1

0

PV

I

PV I

PV I

0

(Cash inflow)

(Cash Outflow)

PV PI

I

Investment Decision Criteria:

PROFITABILTY INDEX (Benefit Cost ratio)

0 NPV

IRR – internal rate of return, NPV = 0• Solve for simple eqn’s• Guess and test• Goal seek in Excel

8/21/2019 408-2012-Lec03 DCF2

http://slidepdf.com/reader/full/408-2012-lec03-dcf2 9/1003

• For any given project the NPV method and the PI will provide thesame accept/ reject decision

• Mutually exclusive projects ??

• Scale issue

50200NPV

50300PV of cash outflow (m$)

100500PV of Cash Inflow (m$)

Project BProject A

PI 1.67 2.0

Investment Decision Criteria:PROFITABILTY INDEX (Benefit Cost ratio)

• What happens to the remaining $400m if p roject B i s accepted?

• If there is a project C , PI of A compared with the composite PI ofB and C

• Capital rationing – firm has capital constraints

– There is ranking of projects

• PI may be used for ranking - Requires smaller projects to exactlyuse up budget else

• Consider NPV of all feasible combinations of projects with in thebudget.

Investment Decision Criteria:

PROFITABILTY INDEX (Benefit Cost ratio)

8/21/2019 408-2012-Lec03 DCF2

http://slidepdf.com/reader/full/408-2012-lec03-dcf2 10/1003-

Review Of Main Points

• Discounted Cash Flow (DCF) is one of the mostcommon approaches to project evaluation

• Various measures that are used for decision making: – Net Present Value (NPV)

• If NPV > 0, then project will provide benefit

– Profitability Index (PI) or Benefit Cost Ratio

• If PI > 1.0, then NPV > 0

• Can be used to rank projects

• Higher PI, higher the return per dollar on investment

![Lec03-1 : Classification Abstraction...nattapong songneam] การพัฒนาระบบ • เมื่อได รับมอบหมาย จาก หน วยงาน](https://img.pdfslide.tips/doc/110x75/5fbbf829d93b85003a107bfa/lec03-1-classification-abstraction-nattapong-songneam-aaaaaaaaaaaa.jpg)