Embed Size (px)

Citation preview

AOZORA BANK, LTD.Annual Report 2001 Year ended March 31, 2001

AO

ZO

RA

BA

NK

, LTD. A

nnual Report 2001

あおぞらBK AR E Cover 01.8.22, 4:01 PMPage 3 Adobe PageMaker 6.5J/PPC

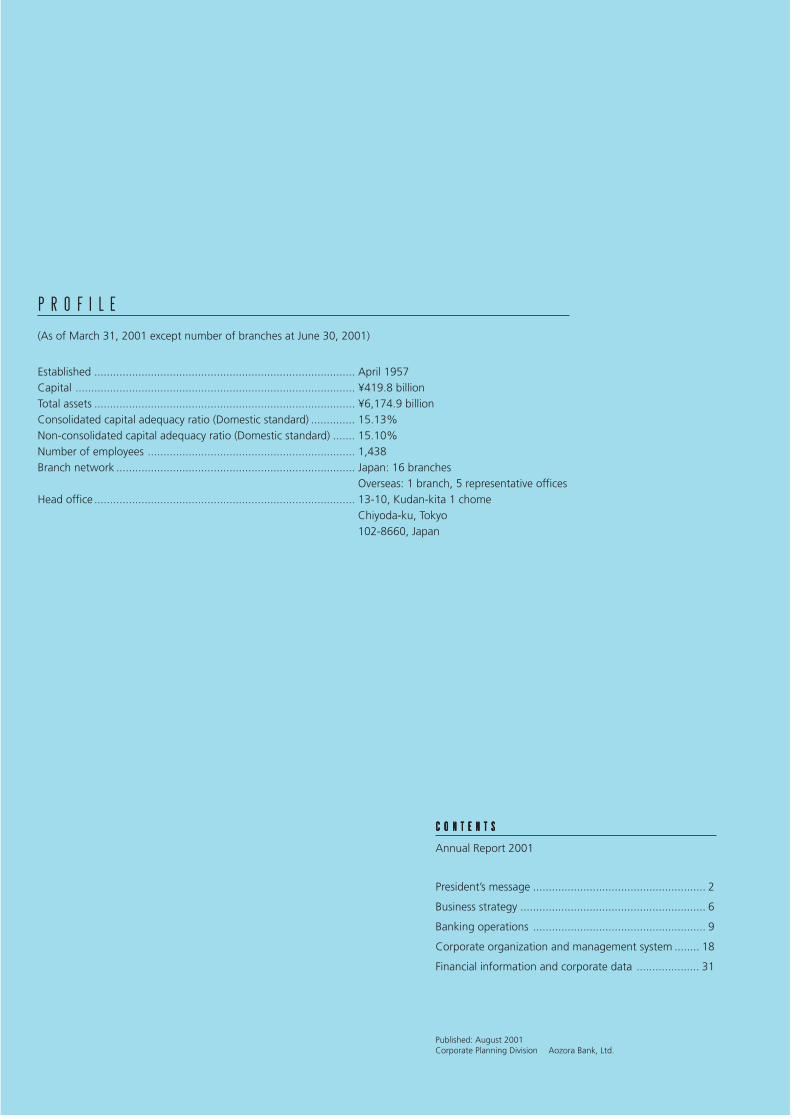

P R O F I L E

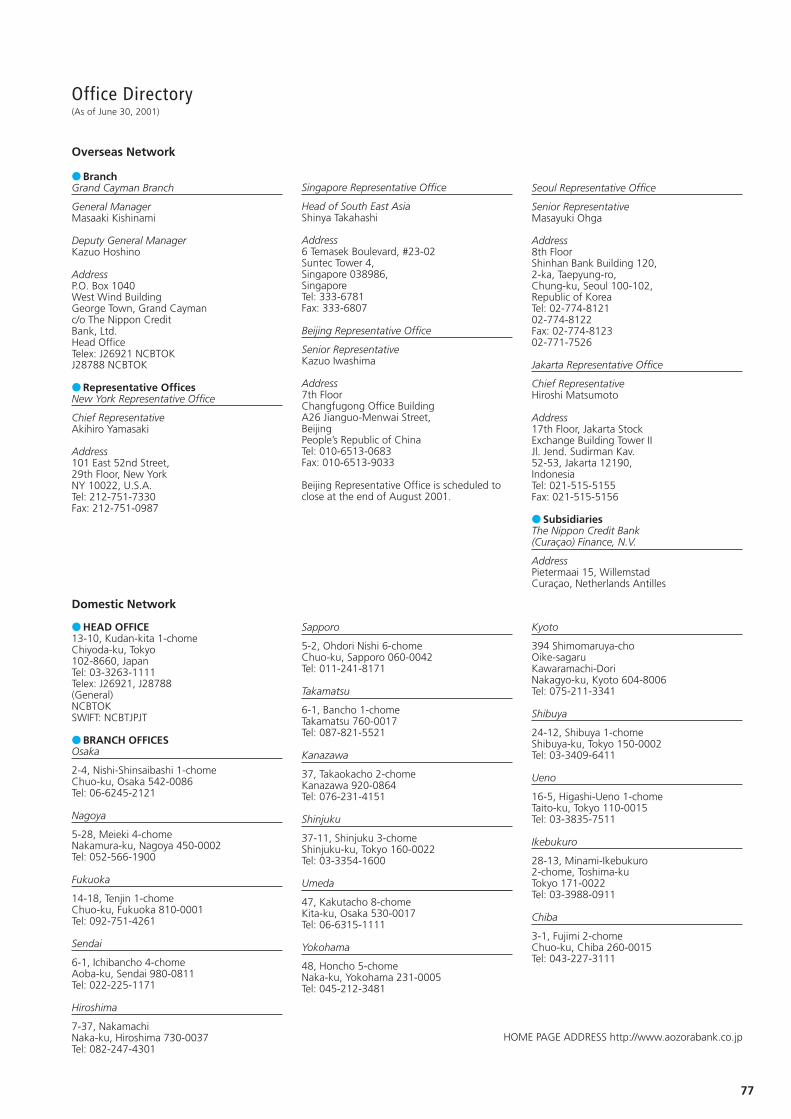

(As of March 31, 2001 except number of branches at June 30, 2001)

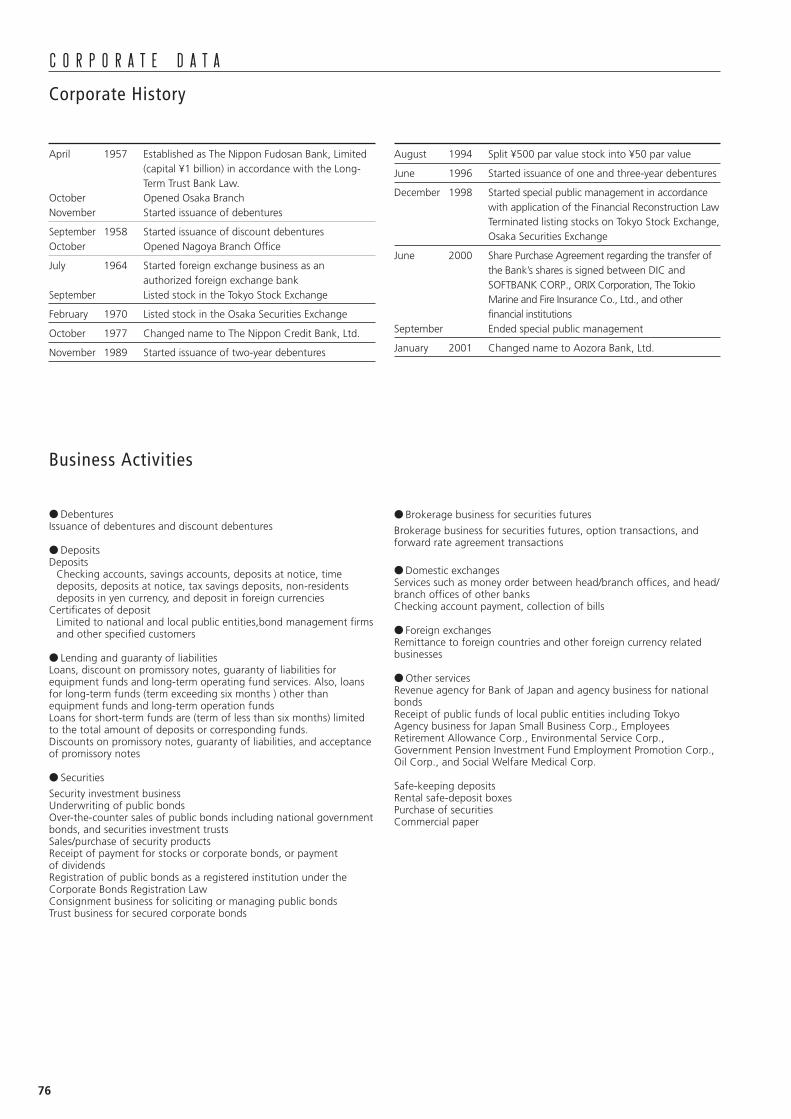

Established ................................................................................... April 1957Capital ......................................................................................... ¥419.8 billionTotal assets ................................................................................... ¥6,174.9 billionConsolidated capital adequacy ratio (Domestic standard) .............. 15.13%Non-consolidated capital adequacy ratio (Domestic standard) ....... 15.10%Number of employees .................................................................. 1,438Branch network ............................................................................ Japan: 16 branches

Overseas: 1 branch, 5 representative officesHead office ................................................................................... 13-10, Kudan-kita 1 chome

Chiyoda-ku, Tokyo102-8660, Japan

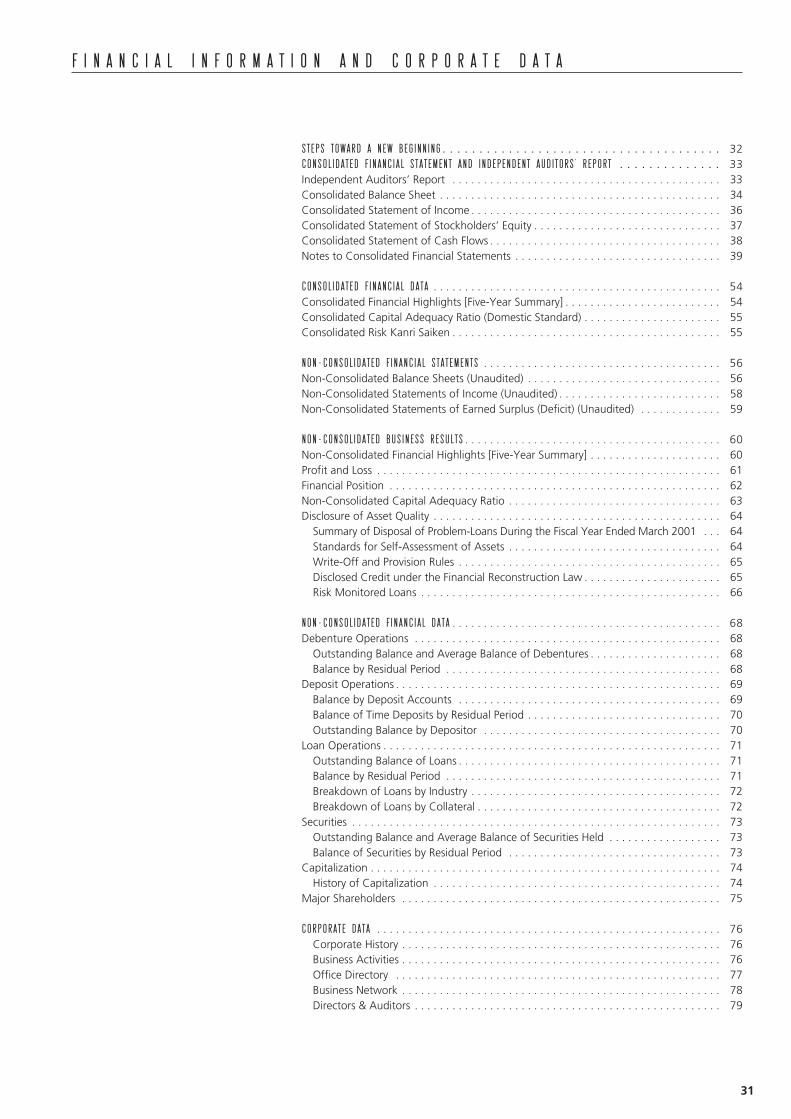

C O N T E N T SC O N T E N T SC O N T E N T SC O N T E N T SC O N T E N T S

Annual Report 2001

President’s message ....................................................... 2

Business strategy ........................................................... 6

Banking operations ....................................................... 9

Corporate organization and management system ........ 18

Financial information and corporate data .................... 31

Published: August 2001Corporate Planning Division Aozora Bank, Ltd.

T

Y

T

J

T

あおぞらBK AR E Cover 01.8.22, 4:01 PMPage 4 Adobe PageMaker 6.5J/PPC

1

Aozora, the Japanese word for clear sky,embodies our aspirations to attain the highest standards of compliance,

transparency and fairness.As such, we decided to adopt Aozora Bank as our new name.

The bank’s logo represents a powerful stream rising into the sky,flowing into the future.

The blue diamond of our logo symbolizes intelligenceand trustworthiness and the central

white stream represents the driving force of hope for a better future.

Our logo symbolizes our firm commitment to enriching societyby addressing new challenges and possibilities in the finance industry.

We will do so by applying novel ideasand creativity that traditional banks cannot match.

The best is yet to come for Aozora Bank of the 21st century.

The Nippon Credit Bank, Ltd. was renamed Aozora Bank, Ltd. on January 4, 2001.

2

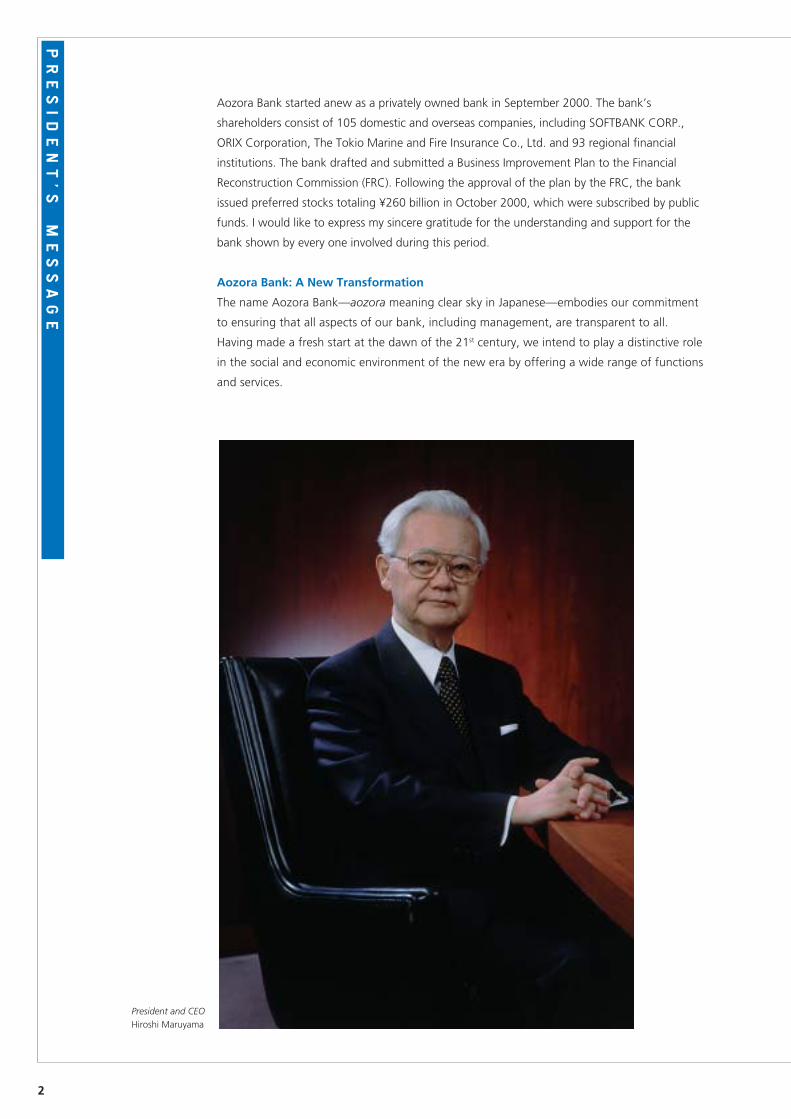

Aozora Bank started anew as a privately owned bank in September 2000. The bank’s

shareholders consist of 105 domestic and overseas companies, including SOFTBANK CORP.,

ORIX Corporation, The Tokio Marine and Fire Insurance Co., Ltd. and 93 regional financial

institutions. The bank drafted and submitted a Business Improvement Plan to the Financial

Reconstruction Commission (FRC). Following the approval of the plan by the FRC, the bank

issued preferred stocks totaling ¥260 billion in October 2000, which were subscribed by public

funds. I would like to express my sincere gratitude for the understanding and support for the

bank shown by every one involved during this period.

Aozora Bank: A New Transformation

The name Aozora Bank—aozora meaning clear sky in Japanese—embodies our commitment

to ensuring that all aspects of our bank, including management, are transparent to all.

Having made a fresh start at the dawn of the 21st century, we intend to play a distinctive role

in the social and economic environment of the new era by offering a wide range of functions

and services.

President and CEOHiroshi Maruyama

PRESIDENT’ S

M

ESSAGE

3

At present, in such a severe economic environment, competition is intensifying among

financial institutions the world over. With their very survival at stake, financial institutions are

clarifying core competences and other traits, such as proprietary know-how and other

competitive advantages, and are thus expected to become even more specialized. Moreover,

the rapid pace of change today underscores the importance of swift decision-making and

taking prompt action. We must squarely face the reality that without proactive self-

transformation, we may not stay competitive.

Even as society and the economy undergo remarkable changes, I believe that there are

still plenty of roles for the bank to fulfill and many opportunities for growth. Why? From now

on the quality of financial services will take precedence over business scale. And for this cause,

we must be prepared to undertake substantial reforms. Distinctive competitive advantages

and resources must be aggressively channeled into business areas with high growth potential.

As such, foresight and courage are of paramount importance. While thoroughly

implementing risk management, I am committed to realigning our operations to maximize

profitability and to building a competitive business structure.

To this end, Aozora Bank will provide financial services that leverage its distinctive expertise

and maximize synergies with its shareholders. Our primary customers will be small and medium-

sized enterprises engaged in the creation of new industries and those realigning their

businesses so as to focus on high growth areas. For instance, we will introduce new methods of

risk assessment, incorporating analysis of cash flows and business models, as well as novel

financing methods for which our overseas business partners have successful precedents. In this

way, we will work to propose creative solutions to a variety of issues faced by our customers.

Another key focus is retail banking. We will continue to extend systems, products and

services in this area. So far, we launched the sale of investment trusts in 1998, formed an online

partnership with the postal savings system in 2000 and rolled out telephone banking services

the same year. In April 2001, we launched “Aozora Super”—discounted debentures covered by

Japan’s deposit insurance system.

“Without being tied to the past, how will we achieve a change in our mindset and

behavior in the conduct of new businesses?” This question is the essence of the bank’s reforms.

My responsibility is to set forth a clear approach to this issue. Furthermore, I want to clarify two

concepts that are important, in my view, in dealing effectively with clients: “In pursuit of

specialization” and “In close touch with customer needs.”

In Pursuit of Specialization

In regard to specialization, we must find answers to two questions. First, how can we most

effectively and efficiently apply our core competencies and competitive advantages to the

execution of operations? Second, to what extent can we enhance the abilities of our officers,

and thus raise our ability to provide solutions that meet customer needs?

The ability to provide quality solutions requires that each officer realize his or her full

potential and achieve a higher degree of specialization. In particular, we must hone our

techniques and expertise in fields that are attracting the interest of our customers, such as real

estate financing, syndicated loans, structured finance, loan servicer operations and venture

business support. To this end, the bank is introducing compensation systems grounded in basic

policies that emphasize skills and ability as well as hiring people with specialized skills from

outside the bank.

4

To achieve a transformation from within, it is essential to flexibly incorporate a wide range

of new ideas and methodologies from outside the bank and enhance specialization in line with

current market demands. Aozora Bank has built up long-standing relationships with financial

institutions nationwide through the placement of debentures. At the same time, most of the

financial institutions we serve are also our shareholders. Another characteristic of Aozora Bank

is its network of shareholders from outside the financial services sector.

As we move to enhance specialization, strengthening relationships with shareholders and

creating synergies together is also paramount. A prime example of this is our support for Blue

Planet Corporation, which provides a portal for financial matters using information technology.

This project aims to provide a forum for an exchange of views among users, including regional

financial institutions and their customers, and also to serve as a channel to provide financial

services in cooperation with regional financial institutions. We will continue to concentrate a

substantial amount of resources on regional financial institutions, and providing financial

services that promote the development of local economies in cooperation with regional

financial institutions.

In Close Touch with Customer Needs

In order to support our clients with effective solutions, we must foster awareness and improve

the ability of all employees in two respects. One is the importance of a precise understanding of

customer needs, from their viewpoints. The other is meeting those needs directly by remaining

in close touch with our customers.

To accomplish this goal, we must become an organization capable of listening, thinking

and taking action at the frontlines of our business, where we interact with customers and are

closest to their needs. I am working to foster a strong awareness of this principle in all

employees. In more specific terms, human resources from peripheral and highly specialized

operations will be transferred to customer business divisions. We will seek to build a problem-

solving, proposal-oriented organizations comprising employees from frontline business, head

office operations, and specialized divisions. Moreover, we are set to upgrade our information

systems in order to optimize the efficiency of in-house collaboration.

Launched in April 2001, Aozora Club embodies these new principles guiding our activities.

The goal of this club is to provide a forum for an exchange of information that can help

companies grow. Targeted companies include not only existing customers, but also prospective

customers, particularly small and medium-sized customers and new enterprises. Aozora Club

project represents the very foundation for our own growth: a commitment to building lasting

relationships with customers that support mutual growth and prosperity.

Strong Management, a Sound Asset Portfolio, and Further Rationalization

Aozora Bank has instituted a new corporate governance system in which supervision and actual

execution of business are clearly separated, to establish a sound management base and faster

decision-making. External directors, including scholars and professionals independent from

shareholders, compose more than half of the Board of Directors, which is responsible for

supervising the execution of business strategies. The Internal Audit Committee, comprising

independent directors and auditors, was established to provide a check on management

practices that is completely autonomous of all shareholders. We have taken all possible

measures to ensure that we do not become a captive bank for any single company—the

Internal Audit Committee conducts strict audits of the bank’s transactions with parent

companies, the Credit Committee, which I chair, sets rigorous credit limits, and transparent

disclosure is maintained at all times.

5

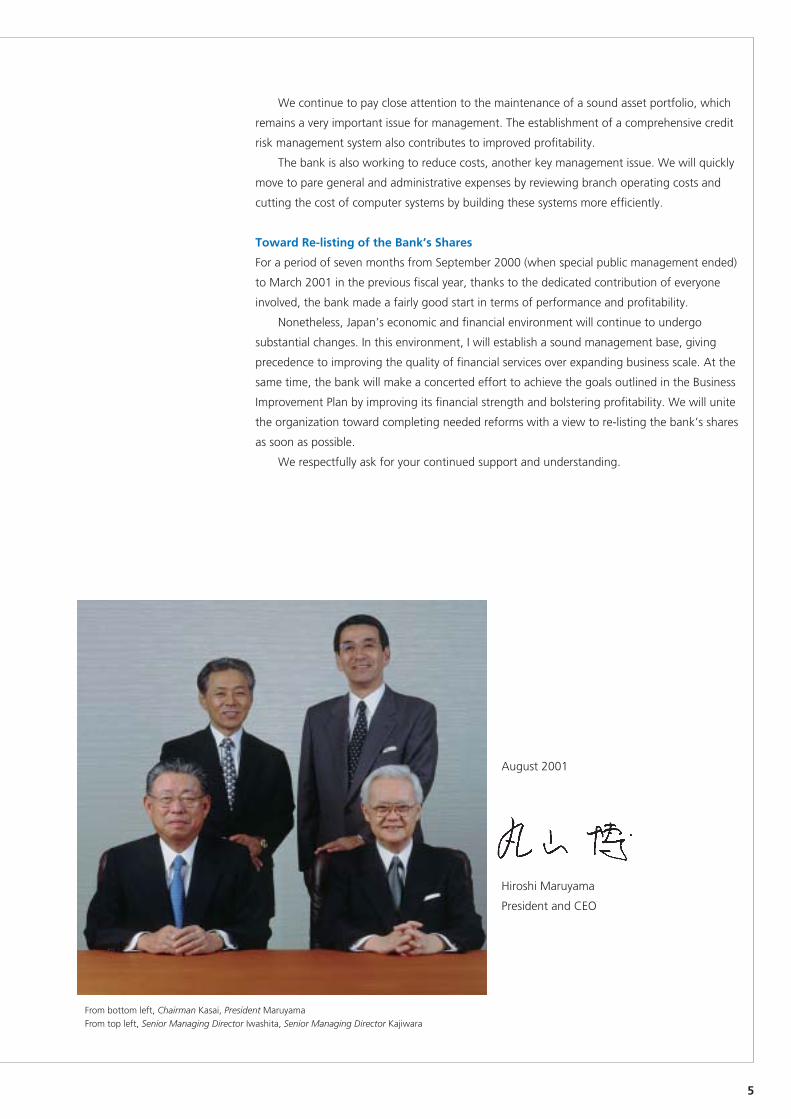

From bottom left, Chairman Kasai, President MaruyamaFrom top left, Senior Managing Director Iwashita, Senior Managing Director Kajiwara

We continue to pay close attention to the maintenance of a sound asset portfolio, which

remains a very important issue for management. The establishment of a comprehensive credit

risk management system also contributes to improved profitability.

The bank is also working to reduce costs, another key management issue. We will quickly

move to pare general and administrative expenses by reviewing branch operating costs and

cutting the cost of computer systems by building these systems more efficiently.

Toward Re-listing of the Bank’s Shares

For a period of seven months from September 2000 (when special public management ended)

to March 2001 in the previous fiscal year, thanks to the dedicated contribution of everyone

involved, the bank made a fairly good start in terms of performance and profitability.

Nonetheless, Japan’s economic and financial environment will continue to undergo

substantial changes. In this environment, I will establish a sound management base, giving

precedence to improving the quality of financial services over expanding business scale. At the

same time, the bank will make a concerted effort to achieve the goals outlined in the Business

Improvement Plan by improving its financial strength and bolstering profitability. We will unite

the organization toward completing needed reforms with a view to re-listing the bank’s shares

as soon as possible.

We respectfully ask for your continued support and understanding.

August 2001

Hiroshi Maruyama

President and CEO

6

In the years ahead, the quality of financial services will take precedence over scale, as banks

compete for customers. As such, there are still plenty of roles for the bank to fulfill and many

opportunities for growth. Aozora Bank aims to deliver quality financial services through the

single-minded pursuit of excellence in all banking operations and by narrowing down busi-

nesses to areas where client needs are greatest.

Quality Financial Services:

Corporate Clients

Aozora Bank aims to satisfy the needs of corporate clients seeking for business strategies that

enable them to enhance competency in the market. The bank offers financial services as well as

solutions on issues for both non-financial corporations and financial institutions.

The bank not only provides corporate finance services to meet financing needs of corporate

clients but is ready to hold a business relationships with new clients in sound financial conditions.

The Bank offers a wide range of financial instruments and services, including solutions on

investment and management strategy to clients from small-to-medium-sized enterprises, the

engine of Japan’s economy, high-growth enterprises like start-ups and high-tech venture

companies, to large corporations at the vanguard of Japan’s economy.

The Bank is also prepared with a broad array of financial products and services for financial

institutions, including tools for asset management, servicing, advisory on how to provide

solutions for the their own customers, as well as Internet-related services.

Individual Clients

The Bank maximizes customers satisfaction through enhancement of quality of asset manage-

ment service lineups to match customers’ needs at various stages in life. Professional advisors

are placed in every local branches to advise clients in person. The Bank has introduced new

access channels including ATM alliances and telephone banking as a step for service quality

improvement. One of the Bank’s current initiative is development of a new types of lending.

The Competitive Edge

One of the Aozora Bank’s most distinguished business strength in providing customers its

sophisticated financial services lies in the extensive network it has built over the years. The bank

has formed a wide variety of business relationships in the course of its history—indeed, it is one

of the core competitive edge.

Firstly, Aozora Bank has built strong relationships with regional financial institutions

through debenture issuance and offering of various financial services as a long-term credit

bank. The strong relationship is an invaluable asset that plays an crucial role in achieving our

strategic goals.

Now, the new shareholders of the Bank, have now joined as new members of the Bank’s

network and have become our business partners. We will collaborate with our shareholders in

different business fields in developing our competency as a solutions provider, and create new

business models.

The accomplishment of strategic goals in retail banking hinges on targeted customers—

most of Aozora Bank’s individual clients are comparatively wealthy individuals.

BUSINESS STRATEGY

7

The financial environment surrounding individual clients is undergoing substantial changes,

as exemplified by persistently low interest rates, commencement of the over-the-counter sale of

investment trusts and insurance at banks, the introduction of Japan’s own 401k plan, and the

government’s plan to limit deposit guarantees to ¥10 million per individual. In response, Aozora

Bank offers not only bonds and deposits, but also provides new financial services and operations

that foster long-term client relationships.

Strategies in Key Banking Operations

Aozora Bank will focus on highly specialized business areas, where client needs are

high, such as investment banking and market operations and further strive to improve

service quality.

At Aozora Bank, divisions for customer relationships and divisions on specialized operations work

in close collaborations in offering exceptional business solutions to clients tackling on issues

such as corporate restructuring, concentration of management resources and asset improvement.

The Bank offers a broad range of service lineups, in the areas of financial management, M&A,

spin-off, overseas business operations, taking good advantages of alliances with our major

shareholders. The Bank has a strong competence in problem loan disposals and real estate

financing where it holds notable achievements, and M&As and loan syndications in which our

network with regional financial institutions plays a pivotal role. Aozora Bank also assists

customers on risk management by providing customized products for risk-hedging.

Aozora Bank will expand investment and lending to venture businesses, a promising

growth area, under strict assessment on technological propriety and marketability of

emerging companies’ business plans.

Lending and investments are not only targeted to venture companies but also to early-stage

companies newly established through spin-offs, downsizing and outsourcing of large corpora-

tions. Aozora Bank works to bring our client’s visions to life, by providing exceptional business

solutions to the truly important issues clients must resolve, which will be identified by the

Bank’s feasibility studies on clients’ business plans and technological competency in fields of

growth potential.

Internet businesses provide new opportunities to develop innovative financial services

and greatly enhance our network of business relationships.

Internet is offered as an unprecedented types of new financial services. Aozora Club (p.8)

provides a virtual forum to exchange views and information among member corporations. It is

by no means a vehicle for one-way communication from the bank to clients. We begin by

asking the corporate members of this service about their financing needs. This stimulates

dialogue, which we value above all else. We aim to create innovative virtual forums and

systems that enable dialogue even among customers.

Retail banking services will be expanded by creating new marketing channels and

introducing innovative financial instruments.

8

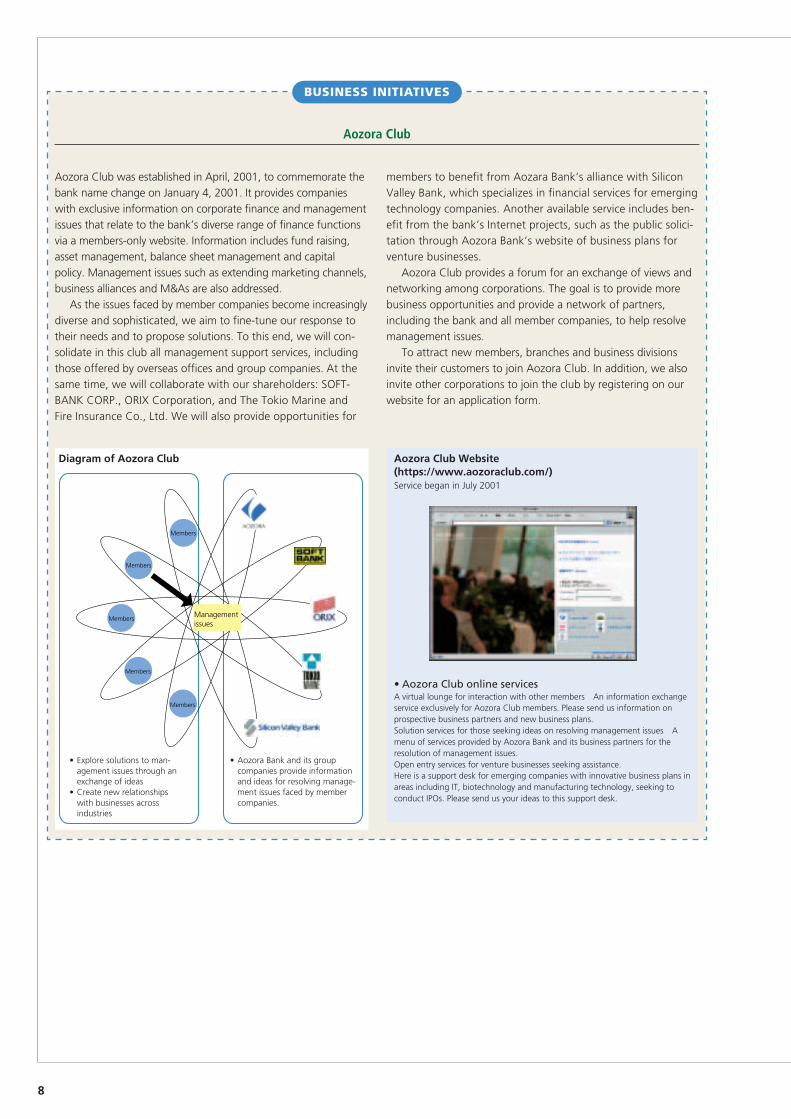

Aozora Club was established in April, 2001, to commemorate thebank name change on January 4, 2001. It provides companieswith exclusive information on corporate finance and managementissues that relate to the bank’s diverse range of finance functionsvia a members-only website. Information includes fund raising,asset management, balance sheet management and capitalpolicy. Management issues such as extending marketing channels,business alliances and M&As are also addressed.

As the issues faced by member companies become increasinglydiverse and sophisticated, we aim to fine-tune our response totheir needs and to propose solutions. To this end, we will con-solidate in this club all management support services, includingthose offered by overseas offices and group companies. At thesame time, we will collaborate with our shareholders: SOFT-BANK CORP., ORIX Corporation, and The Tokio Marine andFire Insurance Co., Ltd. We will also provide opportunities for

members to benefit from Aozara Bank’s alliance with SiliconValley Bank, which specializes in financial services for emergingtechnology companies. Another available service includes ben-efit from the bank’s Internet projects, such as the public solici-tation through Aozora Bank’s website of business plans forventure businesses.

Aozora Club provides a forum for an exchange of views andnetworking among corporations. The goal is to provide morebusiness opportunities and provide a network of partners,including the bank and all member companies, to help resolvemanagement issues.

To attract new members, branches and business divisionsinvite their customers to join Aozora Club. In addition, we alsoinvite other corporations to join the club by registering on ourwebsite for an application form.

BUSINESS INITIATIVES

Aozora Club

• Aozora Club online servicesA virtual lounge for interaction with other members An information exchangeservice exclusively for Aozora Club members. Please send us information onprospective business partners and new business plans.Solution services for those seeking ideas on resolving management issues Amenu of services provided by Aozora Bank and its business partners for theresolution of management issues.Open entry services for venture businesses seeking assistance.Here is a support desk for emerging companies with innovative business plans inareas including IT, biotechnology and manufacturing technology, seeking toconduct IPOs. Please send us your ideas to this support desk.

Aozora Club Website(https://www.aozoraclub.com/)Service began in July 2001

Diagram of Aozora Club

• Explore solutions to man-agement issues through anexchange of ideas

• Create new relationshipswith businesses acrossindustries

• Aozora Bank and its groupcompanies provide informationand ideas for resolving manage-ment issues faced by membercompanies.

Management issues

Members

Members

Members

Members

Members

9

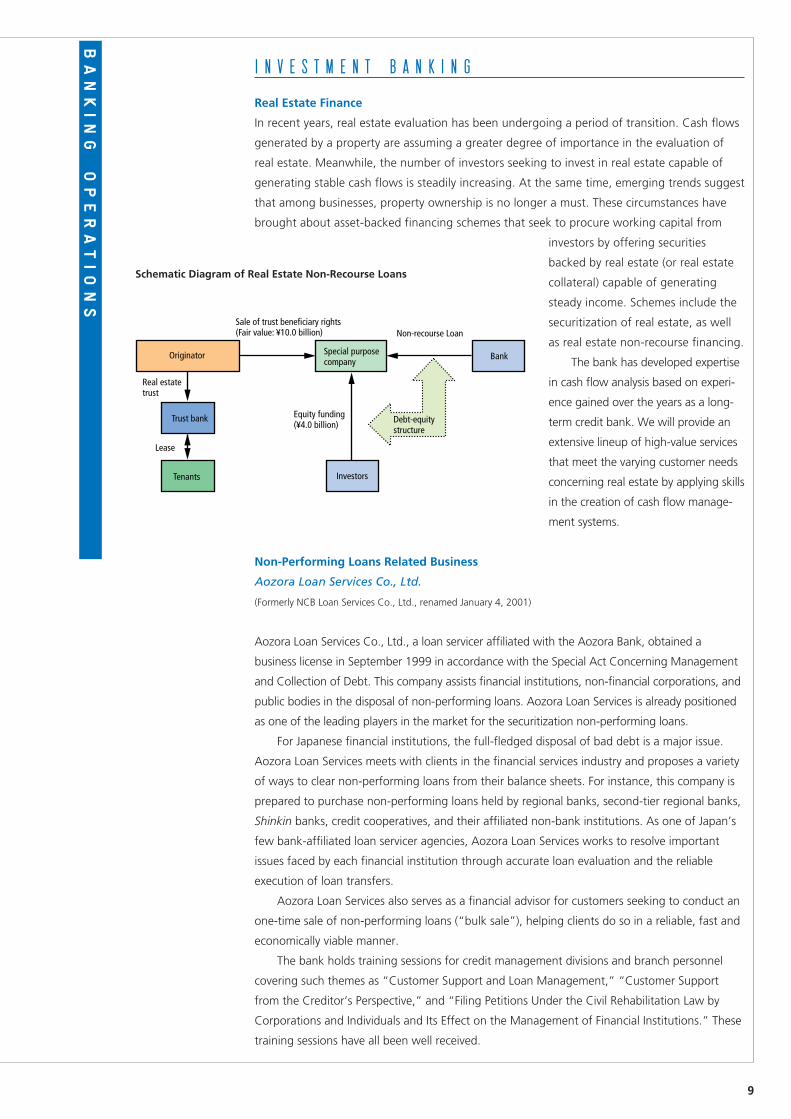

Sale of trust beneficiary rights(Fair value: ¥10.0 billion) Non-recourse Loan

Real estate trust

Equity funding(¥4.0 billion)

Lease

Tenants

Originator

Trust bank

Special purpose company

Bank

Investors

Debt-equity structure

Real Estate Finance

In recent years, real estate evaluation has been undergoing a period of transition. Cash flows

generated by a property are assuming a greater degree of importance in the evaluation of

real estate. Meanwhile, the number of investors seeking to invest in real estate capable of

generating stable cash flows is steadily increasing. At the same time, emerging trends suggest

that among businesses, property ownership is no longer a must. These circumstances have

brought about asset-backed financing schemes that seek to procure working capital from

investors by offering securities

backed by real estate (or real estate

collateral) capable of generating

steady income. Schemes include the

securitization of real estate, as well

as real estate non-recourse financing.

The bank has developed expertise

in cash flow analysis based on experi-

ence gained over the years as a long-

term credit bank. We will provide an

extensive lineup of high-value services

that meet the varying customer needs

concerning real estate by applying skills

in the creation of cash flow manage-

ment systems.

Non-Performing Loans Related Business

Aozora Loan Services Co., Ltd.

(Formerly NCB Loan Services Co., Ltd., renamed January 4, 2001)

Aozora Loan Services Co., Ltd., a loan servicer affiliated with the Aozora Bank, obtained a

business license in September 1999 in accordance with the Special Act Concerning Management

and Collection of Debt. This company assists financial institutions, non-financial corporations, and

public bodies in the disposal of non-performing loans. Aozora Loan Services is already positioned

as one of the leading players in the market for the securitization non-performing loans.

For Japanese financial institutions, the full-fledged disposal of bad debt is a major issue.

Aozora Loan Services meets with clients in the financial services industry and proposes a variety

of ways to clear non-performing loans from their balance sheets. For instance, this company is

prepared to purchase non-performing loans held by regional banks, second-tier regional banks,

Shinkin banks, credit cooperatives, and their affiliated non-bank institutions. As one of Japan’s

few bank-affiliated loan servicer agencies, Aozora Loan Services works to resolve important

issues faced by each financial institution through accurate loan evaluation and the reliable

execution of loan transfers.

Aozora Loan Services also serves as a financial advisor for customers seeking to conduct an

one-time sale of non-performing loans (“bulk sale”), helping clients do so in a reliable, fast and

economically viable manner.

The bank holds training sessions for credit management divisions and branch personnel

covering such themes as “Customer Support and Loan Management,” “Customer Support

from the Creditor’s Perspective,” and “Filing Petitions Under the Civil Rehabilitation Law by

Corporations and Individuals and Its Effect on the Management of Financial Institutions.” These

training sessions have all been well received.

I N V E S T M E N T B A N K I N G

Schematic Diagram of Real Estate Non-Recourse Loans

BANKING OPERATIONS

10

Japanese law prohibits Aozora Loan Services from assuming and collecting non-performing

assets held by non-financial corporations. However, the company can meet a wide variety of

asset securitization needs, including the accurate evaluation of non-performing loans, brokering

a sale of loans and advising on strategic planning related to the disposal of non-performing

loans. In response to the needs of public and nonpublic corporations, a number of training

sessions on themes such as “Initial Procedure for Indications of Bankruptcy and Payment

Default” are held, and have been well received.

Structured Finance

Aozora Bank arranges a wide range of financing schemes designed to meet ever diversifying

funding needs of its clients. These include the arrangement of syndicated loans, and the

securitization of assets including customers’ monetary claims.

Syndicated loans constitute a lending method where multiple financial institutions agree to

the same loan conditions and contract. As a relatively new means of funding in Japan, it has

rapidly gained popularity in recent years. Syndicated loans allow customers to procure funds in

an efficient manner, since negotiations and loan administration are centralized. Other merits

include allowing customers to extend their funding base and benefit from favorable public

relations. The bank conducts the arrangement of syndicated loans (“arranger”) and the

subsequent administrative operations of these loans (“agent”). In this way, the bank links its

business relationships with regional financial institutions to the funding needs of its customers.

The securitization of monetary claims such as notes and accounts receivable, lease assets, and

installment credit claims have grown to become just as common as bank loans and the issuance

of corporate bonds as a means of funding. Securitization provides several key merits for custom-

ers, including the diversification of funding sources, lower interest rates in funding achieved by

leveraging the credit of the monetary claims, and the streamlining of balance sheets. The bank

will endeavor to offer a broad range of securitization schemes so as to address these types of

customer needs.

Aozora Trust Bank, Ltd.

(Formerly The Nippon Credit Trust Bank, Ltd., renamed January 4, 2001)

Aozora Trust Bank, formerly The Nippon Credit Trust Bank, Ltd., was established in February

1994 to offer innovative financial products through the effective use of trust banking functions.

Ever since its establishment, the trust company has been a source of distinctive financial services

centered on the securitization of monetary claims.

The trust company provides beneficial rights to a variety of assets placed in trust accounts:

notes and accounts receivable, loans, lease assets and a variety of claims that arise in the course

of conducting business. Examples include claims to residential security deposits, remuneration

claims and accounts receivable related to the sale of condominiums. While providing innovative

fund-raising channels to corporations, these methods will also serve to streamline clients’

balance sheets and thus improve their overall financial position. Moreover, trust beneficiary

rights are widely favored as investment products by institutional investors, principally regional

financial institutions.

Of the various types of assets held in trust, we are especially focusing on the

securitization of aggregated receivables. Thus far, the securitization of small quantities of

notes receivable, medical fee claims and loans has been considered difficult. We aim to

amalgamate small-quantity receivables into a single trust. There is a significant need for this

type of service, since it can substantially reduce each customer’s transaction costs. In addi-

tion, we offer customer-segregated and general purpose money trusts.

11

We are committed to leveraging the agility that comes with being a trust bank that is a

subsidiary of a bank, and the manifold possibilities of trust functions, so as to meet diverse

customer needs. We will continue to provide innovative financial services unrestricted by any

traditional business practice.

M&As

The progress of globalization and deregulation has intensified competition, while selection and

focus on core businesses and high growth fields has spurred even more corporate restructuring.

Amid these developments, M&As have gained widespread acceptance as an effective way to

optimize the allocation of corporate resources.

Ever since the launch of M&A operations in 1988, Aozora Bank has handled a hundred and

several tens of these deals. By maximizing its wealth of experience and expertise in this area,

the bank offers advisory services on corporate mergers and the drafting of policies related to

business alliances, and transaction assessment including pricing. In this way, the bank has

assisted in expanding its customers’ business and improving their operating efficiency.

To offer customers highly specialized services in an expeditious manner, the bank has

established and maintains close ties with expert attorneys and accountants as well as external

institutions such as regional financial institutions and local chambers of commerce and industry.

The bank will apply its expertise to initiatives such as MBOs and business related to com-

pany reconstruction, which have attracted wide interest as effective means to promote the

revitalization of Japan’s economy.

Cross Border Operations

The bank provides advisory services tailored to the overseas business of small and medium-size

corporations, in areas including (1) establishing or withdrawing from overseas operations; (2)

minimizing operational risk of existing or new businesses and conducting effective financial

management. The bank also provides information required to resolve issues that emerge when

expanding overseas operations, including information on foreign exchange, economic trends, and

taxation and accounting systems of foreign countries, centered on the Asian region. This informa-

tion is published in the monthly newsletter “Aozora

Asia Business” and in various other reports.

PFI (Private Financial Initiative)

The bank provides financial advisory services on PFI

utilizing its extensive expertise in overseas project

finance. While being consulted by various non-

financial corporations interested in PFIs, the bank

also supports regional financial institutions seeking

to become financial advisors on local PFI projects in

a variety of ways.

The bank is also actively engaged in project

finance for those newly involved in the indepen-

dent power generation business, a field that has

emerged in the wake of Japan’s liberalization of

the electric power market.

Advisory Services on Market Risk Management

Changes in bank management techniques brought about by the advance of

financial technology and the disclosure of financial inspection manuals have

underscored the importance of maintaining sound risk management systems at

financial institutions. Accordingly, Aozora Bank and several regional financial

institutions have entered into an “Advisory Contract Related to Market Risk

Management.” Under this arrangement, Aozora Bank’s Risk Management

Division helps customers improve market risk management systems.

Aozora Bank’s involvement in risk management dates back to 1988. The

bank began market risk management by assessing maximum estimated losses,

using these figures to set limits on market exposure for the entire bank and

other risk controls. In particular, the early development of a value-at-risk

management system utilizing proprietary PC software developed by the bank

(patent pending) has been highly acclaimed.

Aozora Bank has thus far entered into market risk management advisory contracts

with approximately 30 customers including regional banks, second-tier regional banks

and Shinkin banks.

12

Risk Hedging Tools That Utilize Derivatives

In line with each customer’s stance toward market risks, Aozora Bank provides detailed and

fine-spun advice about risk-hedging methods from medium and long-term perspectives.

Financial instruments offered by the bank are intended to minimize and control the influence of

fluctuations in foreign exchange rates, interest rates and other risk factors. Customers can thus

shield operating results from market volatility or reduce their funding costs. New instruments

are being added to cover more uncertainties. One is weather derivatives, which allow compa-

nies to cover losses caused by unfavorable weather movements. Another being credit deriva-

tives, which allow companies to cover losses caused by a default of reference entity in the

investment portfolio.

Bank divisions involved in market-related activities have two groups. One group supports

business divisions and branches, and the other group develops new products that tap the latest

advances in financial engineering. By working together, the two groups create a base for

supplying customers with order-made financial products in a timely and effective way. The bank

provides after-deal services such as market price information, information on outsorcing of

backoffice operations for derivative transactions.

Sophisticated Financial Engineering Techniques and Market Information

Aozora Bank provides customers with various market-linked products while using its sophisti-

cated global dealer type risk management system to participate actively in the interbank

market. The bank deals with interest rate derivatives, bonds, foreign exchange contracts and

other products globally. This yields opportunities to develop new products, analyze various risks

and seek gains through arbitrage trading. For customers, this breadth makes Aozora Bank a

reliable source of advice on investments, hedging strategies and other critical subjects.

Our analysts with each area of specialization supply customers with a wide scope of

information required to make their savvy investment decisions. Reports extend from fundamen-

tal analyses to outlooks for foreign exchange rates, interest rates, etc. Comments of analysts are

made public through various media, earning the bank’s analysts a widespread reputation for

their excellent work quality.

Aozora Bank has now developed several system trading models utilizing artificial intelli-

gence (AI). These models have already been applied to Japanese government bond futures and

foreign exchange transactions. Results have been particularly strong in the JGB futures market.

And efforts will continue to be made to upgrade these systems for the service of our customers.

Investment Trusts Distributed Through Private Offerings

Aozora Bank has started offering quality and high value-added investment trusts mainly to

financial institutions. The first trust was formed in January 2001: Aozora Japanese Stock

Active Open (“Hit & Run”) a product of Aozora Asset Management Co.,Ltd. Next came in

May 2001: Tokio Marine and Fire AM Long-Short Fund, a product of Tokio Marine and Fire

Asset Management.

M A R K E T A C T I V I T I E S

13

Full-fledged Financing for New Enterprises

What is vital for young venture businesses—newly established or in an early stage of their

growth—is to draw up proper business plans and to secure needed funds based on those

drafted business plans. Aozora Bank complies with their specific fund needs in the form of

extending loans to them. In addition, Aozora Investment Co., Ltd., our venture capital sub-

sidiary, assists their fund-raising activities in the form of investing in them.

Two elements are essential to loan and investment schemes for new enterprises: First, the

bank must conduct an accurate evaluation of the technical aspects of those companies and

marketability of their planned products. Second, we must provide appropriate management

advice to them to enhance their corporate value. By forming a wide range of

alliances with venture capital companies, business incubators, universities,

non-financial corporations, and auditors, the bank is well prepared to resolve

any issues faced by them.

For instance, recent advances in the field of biotechnology are expected

to widely impact industry as a whole—from medicine/pharmaceuticals, to

foods, environment, chemicals, machinery and bioinformatics, a new disci-

pline combining IT and life sciences. Focusing on this dynamic discipline, the

bank will aggressively support venture businesses specializing in biotechnology,

as we harness a network of experts in academia and business consultants as

a source of expertise. The growth of biotechnology ventures depends even

more so than other industries on strategic business alliances. As such, the

bank will actively provide advisory services on business alliance-making.

Aozora Bank has formed an alliance with U.S.-based Silicon Valley Bank

(SVB) in a move to introduce SVB’s proven high technology finance methods

to Japan and the bank aims to support Japanese venture businesses to

establish an alliance with U.S. counterparts. The bank provides a contact point

on its website that enables venture businesses to present their business plans

over the Internet (pictured to the left). We are planning various new initiatives

to support venture businesses. For instance, we arrange business presentations

on venture businesses to our marketing staff so that they can support

marketing efforts of venture businesses that the bank financed.

F I N A N C I N G F O R N E W E N T E R P R I S E S

Online form for presenting business plans(Aozora Bank’s website)(http://www.aozorabank.co.jp/)

Aozora Asset Management Co., Ltd.

(Formerly Nippon Credit Asset Management Co., Ltd., renamed January 4, 2001)

This company was formed in August 1986 as Nippon Credit Asset Management Co., Ltd.,

which specializes in asset management. Primary activities are the investment management of

entrusted securities for financial institutions and pension funds, and the establishment and

management of investment trusts distributed through private offerings. In June 2001, Softbank

Investment Group purchased a 70% stake in this company from Aozora Bank. Before this, this

company was a wholly owned subsidiary of Aozora Bank. The purpose of this move is to

strengthen its customer base by serving more investment needs through the development of

new products, and to build up a closer connection to enhance the scope and quality of its asset

management services, such as by taking on new investment assets to be managed.

14

New Funding Schemes

One example of the bank’s distinguished fund-raising initiatives for new enterprises is a finance

scheme for companies engaged in franchising operations. In the first project, the bank and QB

NET CO., LTD., a new-type hair salon chain operator (offering hair cut services at lower prices),

created a joint investment fund to open and develop new “QB house” outlets.

Under this scheme, funds required to open new franchised stores are provided from the

investment fund, while the store operator is charged with staff recruiting, staff training, etc.

Aozora Investment Co., Ltd. assesses growth potential of prospective new franchisees and

authorizes funding.

Besides investment funds for chain store operators, the bank has a proven record in

investment funds arrangement for home video game software development. Our finance

schemes are by no means limited to conventional forms of loans and investments. The bank

will continue to offer a diverse range of financing arrangements for venture businesses.

Aozora Investment Co., Ltd.

(Formerly NCB Private Equity Co., Ltd., renamed January 4, 2001)

Aozora Investment Co., Ltd., a wholly owned subsidiary of Aozora Bank, Ltd, has enhanced its

IPO support operations—its mainstay business for more than 10 years—and started anew in

July 1999 a venture capital business in order to offer comprehensive support services for

venture businesses.

The Aozora Bank Group applies its expertise and business network to meet various

needs of entrepreneurs planning for initial public offerings (IPOs). With a view to maximizing

potential of emerging companies, Aozora Investment Co., Ltd. provides

consultation services on drafting business plans that address issues faced by

each customer and on venture capital fund-raising schemes. In addition,

Aozora Investment Co., Ltd. is involved in equity finance such as underwrit-

ing equities, warrant bonds and convertible bonds. In this way, we offer

comprehensive supporting services to venture businesses.

The company is deeply involved in the development of new schemes such

as investments in specific projects, and providing support to business develop-

ment through arranging funds. And, this is one of the Aozora Investment’s

unique features as a venture capital. The company has been highly successful

in arranging investment funds for companies expanding their franchised

stores’ network and in arranging investment funds for home video game

software companies.

By harnessing the entire Aozora Bank Group’s expertise and its business

network, Aozora Investment will continue to meet various needs of entrepre-

neurs, to support the development of prospective venture businesses and help

them make IPOs.

Aozora Investment’s Website(http://www.aozora-invest.co.jp/)

15

BUSINESS INITIATIVES

Alliance with Silicon Valley Bank

Silicon Valley Bank (SVB) of the United States has a clout infinancing high-technology startup companies. In April 2001,Aozora Bank and SVB agreed to collaborate in areas such asfinancing high-tech venture companies.

Through this alliance, Aozora Bank aims to serve as abridge between Japanese customers and Silicon Valley compa-nies, providing an interface leading to new value creation. Tothis end, the two banks will be in full cooperation in providingservices both in Japan and in the U.S. Specific steps includesetting up of a “Japan Desk” at SVB to connect U.S. com-panies with Japanese companies. In addition, SVB’s websitecontents will be available in Japanese on Aozora Bank’shomepage. The two banks will hold joint conferences andseminars, that provide not only lectures on the latest themes,but also serve as forums for interaction with local businessesand venture capitalists.

Aozora Bank will attempt to absorb SVB’s excellent busi-ness expertise in specialized fields of finance focusing onSilicon Valley companies, the epicenter of IT and life sciencesindustries. To this end, we will dispatch our employees to SVB.

Silicon Valley BankSilicon Valley Bank is a regional financial institution based inthe Silicon Valley region of the United States. SVB focuses onhigh-tech venture companies. The bank enjoys a nationalreputation as number 1 bank in the U.S. for its excellence inthe field of financing start-up and early-stage companies.

Established: 1983Capital: US$684 million (As of December

2000)Total assets: US$5,627 million

(As of December 2000)Branches in the U.S.: 25Number of employees: Approximately 900Number of customers: More than 9,000 companies,

centered on technologyStock listing: Nasdaq (SIVB)

(http://www.svb.com/)

Features of Our Internet Business

By using the Internet, the bank aims to create some new value added such as an improvement

in customer convenience, new customer development, etc. In this day and age when the

Internet is causing a cataclysmic change to Japan’s industrial structure, linking our principal

shareholders’ expertise to the bank’s business resources in the area of the Internet, will provide

the bank with countless opportunities to develop highly distinctive Internet businesses.

Aozora Bank has received funds from 93 regional financial institutions, and they have

strongly sought support from Aozora Bank in developing their respective Internet businesses on

neutral ground. The bank will endeavor to meet their expectations and respond to their needs

to the best of its ability.

Internet businesses are vital to the bank’s business strategy. The bank aims to create new

business models by realizing its full potential by the use of the Internet. The bank has invested

in Blue Planet Corporation a venture established in April 2001 to support the design and

operation of portal sites for regional financial institutions. This is an example of the direction in

which the bank’s Internet business is headed.

Furthermore, we are exploring Internet banking—offering various banking services online—

from many angles, focusing on customer convenience and cost effectiveness and synergy effect

with our shareholders.

I N T E R N E T — R E L A T E D B U S I N E S S E S

16

Small and medium-sized companies

Customer

Customer

Customer

Customer

Customer

Customer

Use of servicesSupport services for small and medium-sized companies Shinkin Bank B

SOFTBANK EC HOLDINGS

F&M

Aozora Bank

Others

Bank A

Community services

Area newsletters

Services for corporations

Advisory services on subsidies

Administrative contents

Various Information

Accounting Payroll calculationManagement, accounting, tax

Legal consultingMarketing support

Purchase of indirect materials

E-commerce shops

Support services for small and medium-sized companies

Blue Planet

Outsourcing services

Shopping mallCorporate informationBusiness networking

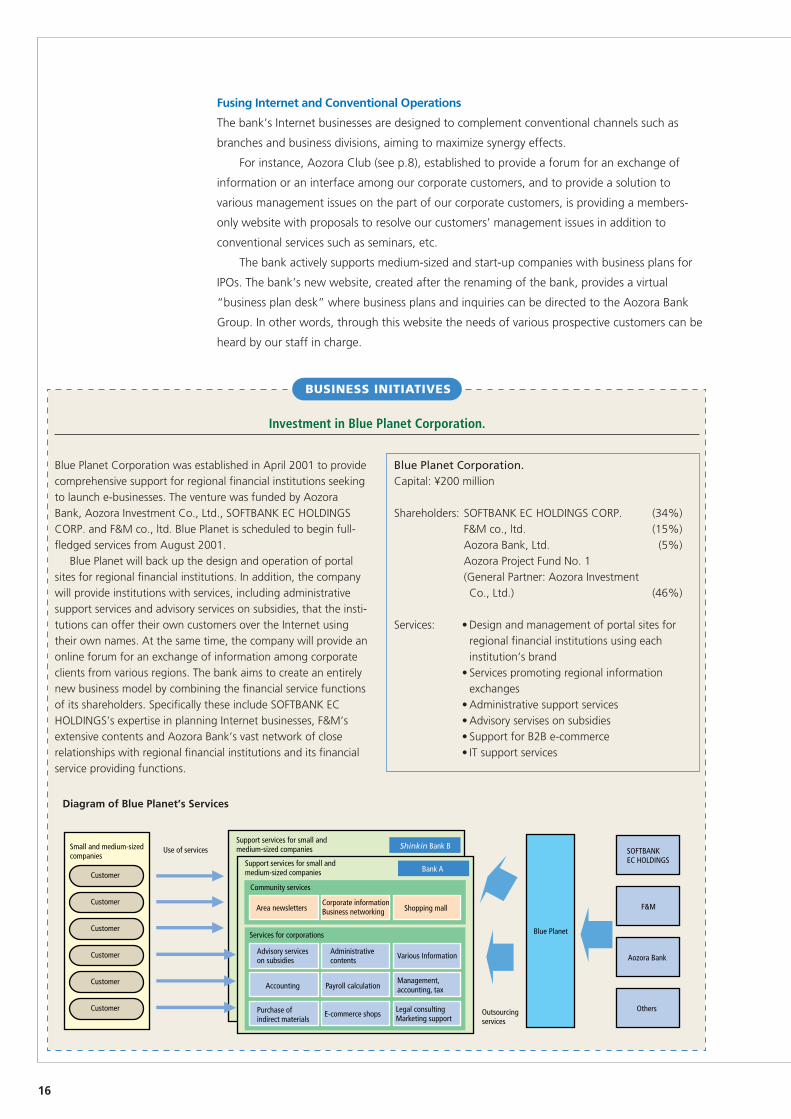

Blue Planet Corporation was established in April 2001 to providecomprehensive support for regional financial institutions seekingto launch e-businesses. The venture was funded by AozoraBank, Aozora Investment Co., Ltd., SOFTBANK EC HOLDINGSCORP. and F&M co., ltd. Blue Planet is scheduled to begin full-fledged services from August 2001.

Blue Planet will back up the design and operation of portalsites for regional financial institutions. In addition, the companywill provide institutions with services, including administrativesupport services and advisory services on subsidies, that the insti-tutions can offer their own customers over the Internet usingtheir own names. At the same time, the company will provide anonline forum for an exchange of information among corporateclients from various regions. The bank aims to create an entirelynew business model by combining the financial service functionsof its shareholders. Specifically these include SOFTBANK ECHOLDINGS’s expertise in planning Internet businesses, F&M’sextensive contents and Aozora Bank’s vast network of closerelationships with regional financial institutions and its financialservice providing functions.

Blue Planet Corporation.Capital: ¥200 million

Shareholders: SOFTBANK EC HOLDINGS CORP. (34%)F&M co., ltd. (15%)Aozora Bank, Ltd. (5%)Aozora Project Fund No. 1(General Partner: Aozora InvestmentCo., Ltd.) (46%)

Services: • Design and management of portal sites forregional financial institutions using eachinstitution’s brand

• Services promoting regional informationexchanges

• Administrative support services• Advisory servises on subsidies• Support for B2B e-commerce• IT support services

BUSINESS INITIATIVES

Investment in Blue Planet Corporation.

Diagram of Blue Planet’s Services

Fusing Internet and Conventional Operations

The bank’s Internet businesses are designed to complement conventional channels such as

branches and business divisions, aiming to maximize synergy effects.

For instance, Aozora Club (see p.8), established to provide a forum for an exchange of

information or an interface among our corporate customers, and to provide a solution to

various management issues on the part of our corporate customers, is providing a members-

only website with proposals to resolve our customers’ management issues in addition to

conventional services such as seminars, etc.

The bank actively supports medium-sized and start-up companies with business plans for

IPOs. The bank’s new website, created after the renaming of the bank, provides a virtual

“business plan desk” where business plans and inquiries can be directed to the Aozora Bank

Group. In other words, through this website the needs of various prospective customers can be

heard by our staff in charge.

17

R E T A I L B A N K I N G

To serve individual clients’ various needs, Aozora Bank offers financial instruments such as time

deposits, savings plans, and investment trusts which banks started dealing in December 1998.

The bank is currently planning to provide new types of loans, such as innovative housing loans

and credit card loans.

The bank is putting stronger fucus on financial advisory services. For instance, licensed

financial planners, tax accountants and attorneys are stationed at branches to offer consulting

services free of charge on selected days. Internationally accredited, certified financial planners

are at the disposal of customers seeking even more comprehensive and detailed financial

advice. Meanwhile, the bank is aggressively moving ahead with the expansion of service

channels and financial instruments. To bolster its branch network, Aozora Bank has entered

into an ATM alliance with various financial institutions, including city and trust banks. Tele-

phone banking was initiated in November 2000, and was followed by the successive launch of

new services. For instance, “Aozora Direct Time Deposit,” a time deposit exclusively offered

through telephone banking, was rolled out in April 2001. In this way, we will continue to

enhance our menu of services so as to combine both benefit and convenience for customers

and develop a rich variety of new financial instruments.

Addressing New Businesses Created by the Internet

Thanks to the prevalence and development of the Internet, a wide variety of unprecedented

businesses have recently been created. Addressing the needs of these new businesses is one of

our critical tasks.

C2C (consumer-to-consumer) Internet auction, which has grown rapidly over the last 1–2

years, is a case in point. A number of

problems have emerged relating to ship-

ments of goods and payments. The bank, in

collaboration with Nippon Express Co., Ltd.,

established Netrust, Ltd. Which provides

delivery and settlement services for online

auction called “Net-Daibiki,” servicing as a

reliable intermediary. Aozora Investment

Co., Ltd. is the principal shareholder and

Aozora Bank provides relevant settlement

function.

B2B (business-to-business) e-commerce

has drawn wide interest in recent times. The

bank is taking the Lead in B2B e-commerce

research and plans to add research service

to its e-business service lineups for client

companies. And, at the same time, we

expect to develop the fruits of these efforts

into other new services as well.

The findings of our research have been

widely acclaimed, and were published in

“The Frontlines of B2B E-Commerce” in

April 2001.

Site of “Net-Daibiki,” delivery andsettlement services for online auction,operated by Netrust, Ltd.(http://www.net-daibiki.com/)

18

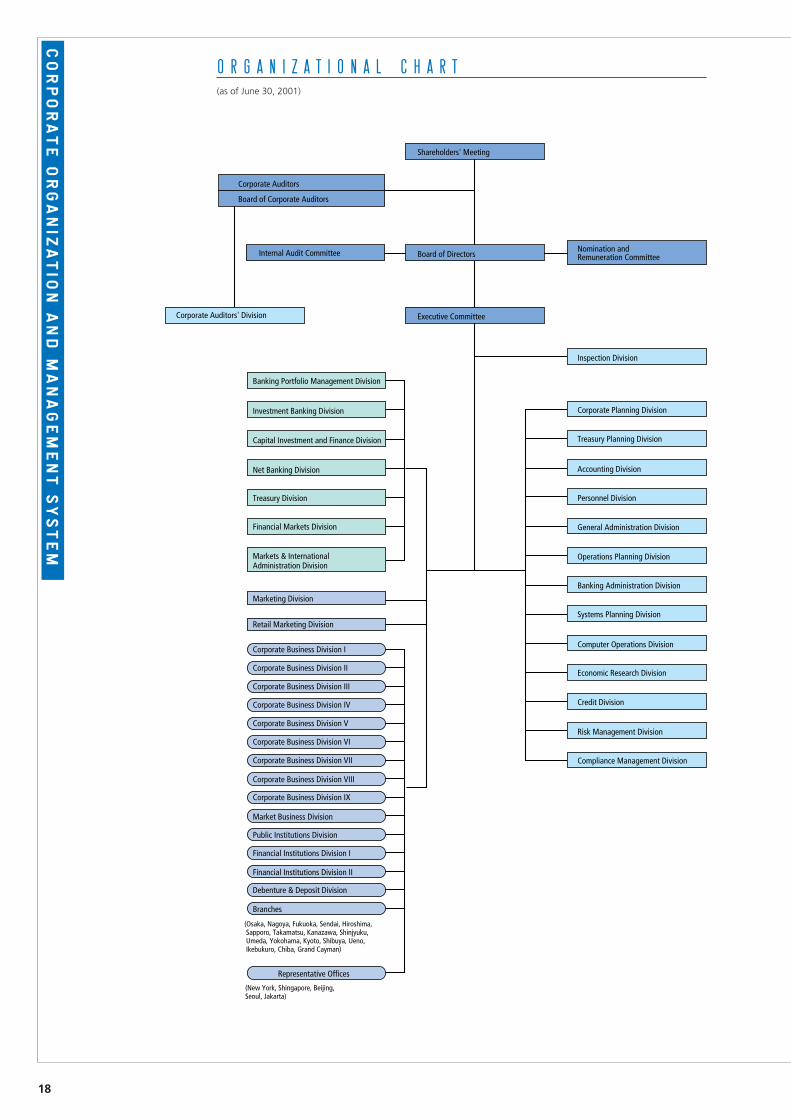

Nomination and Remuneration Committee

Inspection Division

Banking Portfolio Management Division

Investment Banking Division

Capital Investment and Finance Division

Net Banking Division

Corporate Planning Division

Treasury Division

Treasury Planning Division

Financial Markets Division

Accounting Division

Markets & International Administration Division

Personnel Division

Marketing Division

General Administration Division

Retail Marketing Division

Corporate Business Division I

Operations Planning Division

Corporate Business Division II

Corporate Business Division III

Banking Administration Division

Corporate Business Division IV

Corporate Business Division V

Systems Planning Division

Corporate Business Division VI

Corporate Business Division VII

Computer Operations Division

Corporate Business Division VIII

Corporate Business Division IX

Economic Research Division

Market Business Division

Public Institutions Division

Credit Division

Financial Institutions Division I

Financial Institutions Division II

Risk Management Division

Debenture & Deposit Division

Compliance Management Division

Branches

(Osaka, Nagoya, Fukuoka, Sendai, Hiroshima, Sapporo, Takamatsu, Kanazawa, Shinjyuku, Umeda, Yokohama, Kyoto, Shibuya, Ueno, Ikebukuro, Chiba, Grand Cayman)

Representative Offices

(New York, Shingapore, Beijing, Seoul, Jakarta)

Shareholders' Meeting

Board of Corporate Auditors

Internal Audit Committee Board of Directors

Corporate Auditors' Division Executive Committee

Corporate Auditors

O R G A N I Z A T I O N A L C H A R T(as of June 30, 2001)

CORPORATE O

RGANI Z

ATIO

N A

ND M

ANAGEMENT S

YSTEM

19

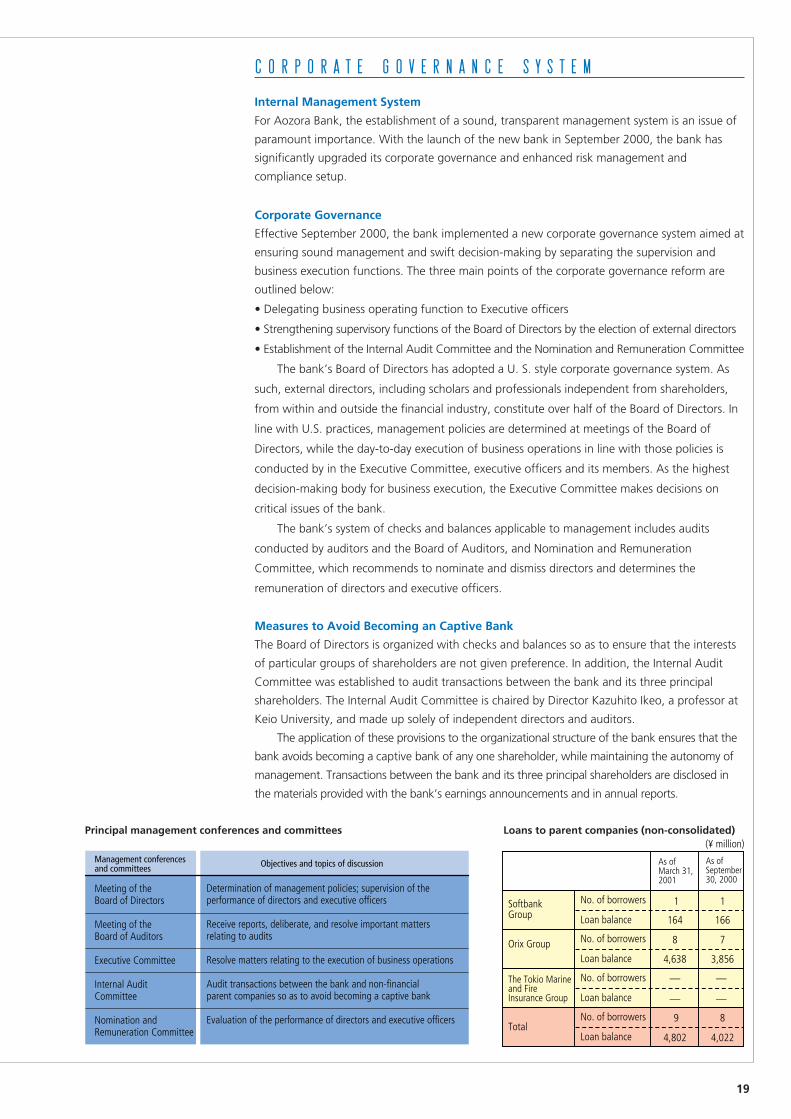

Management conferences and committees

Meeting of the Board of Directors

Meeting of the Board of Auditors

Executive Committee

Internal Audit Committee

Nomination and Remuneration Committee

Determination of management policies; supervision of the performance of directors and executive officers

Receive reports, deliberate, and resolve important matters relating to audits

Resolve matters relating to the execution of business operations

Audit transactions between the bank and non-financial parent companies so as to avoid becoming a captive bank

Evaluation of the performance of directors and executive officers

Objectives and topics of discussion

(¥ million)

As of March 31, 2001

As of September 30, 2000

Softbank Group

No. of borrowers 1 1

Loan balance 164 166

Orix Group 8 7

4,638 3,856

The Tokio Marine and Fire Insurance Group

― ―

― ―

Total 9 8

4,802 4,022

No. of borrowers

Loan balance

No. of borrowers

Loan balance

No. of borrowers

Loan balance

Internal Management System

For Aozora Bank, the establishment of a sound, transparent management system is an issue of

paramount importance. With the launch of the new bank in September 2000, the bank has

significantly upgraded its corporate governance and enhanced risk management and

compliance setup.

Corporate Governance

Effective September 2000, the bank implemented a new corporate governance system aimed at

ensuring sound management and swift decision-making by separating the supervision and

business execution functions. The three main points of the corporate governance reform are

outlined below:

• Delegating business operating function to Executive officers

• Strengthening supervisory functions of the Board of Directors by the election of external directors

• Establishment of the Internal Audit Committee and the Nomination and Remuneration Committee

The bank’s Board of Directors has adopted a U. S. style corporate governance system. As

such, external directors, including scholars and professionals independent from shareholders,

from within and outside the financial industry, constitute over half of the Board of Directors. In

line with U.S. practices, management policies are determined at meetings of the Board of

Directors, while the day-to-day execution of business operations in line with those policies is

conducted by in the Executive Committee, executive officers and its members. As the highest

decision-making body for business execution, the Executive Committee makes decisions on

critical issues of the bank.

The bank’s system of checks and balances applicable to management includes audits

conducted by auditors and the Board of Auditors, and Nomination and Remuneration

Committee, which recommends to nominate and dismiss directors and determines the

remuneration of directors and executive officers.

Measures to Avoid Becoming an Captive Bank

The Board of Directors is organized with checks and balances so as to ensure that the interests

of particular groups of shareholders are not given preference. In addition, the Internal Audit

Committee was established to audit transactions between the bank and its three principal

shareholders. The Internal Audit Committee is chaired by Director Kazuhito Ikeo, a professor at

Keio University, and made up solely of independent directors and auditors.

The application of these provisions to the organizational structure of the bank ensures that the

bank avoids becoming a captive bank of any one shareholder, while maintaining the autonomy of

management. Transactions between the bank and its three principal shareholders are disclosed in

the materials provided with the bank’s earnings announcements and in annual reports.

C O R P O R A T E G O V E R N A N C E S Y S T E M

Principal management conferences and committees Loans to parent companies (non-consolidated)

20

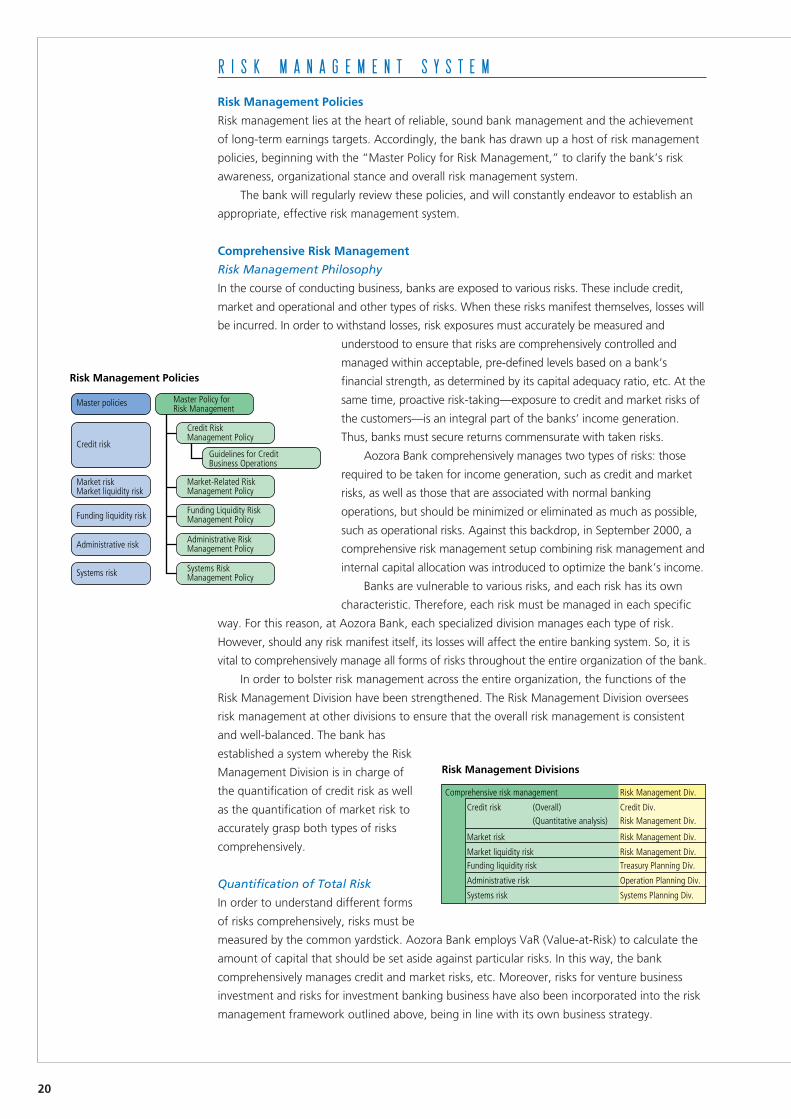

Risk Management Policies

Master policies

Credit risk

Market riskMarket liquidity risk

Funding liquidity risk

Administrative risk

Systems risk

Master Policy for Risk Management

Credit Risk Management Policy

Market-Related Risk Management Policy

Funding Liquidity Risk Management Policy

Administrative Risk Management Policy

Systems Risk Management Policy

Guidelines for Credit Business Operations

Risk Management Divisions

Comprehensive risk management Risk Management Div.

Credit risk (Overall) Credit Div.

(Quantitative analysis) Risk Management Div.

Market risk Risk Management Div.

Market liquidity risk Risk Management Div.

Funding liquidity risk Treasury Planning Div.

Administrative risk Operation Planning Div.

Systems risk Systems Planning Div.

R I S K M A N A G E M E N T S Y S T E M

Risk Management Policies

Risk management lies at the heart of reliable, sound bank management and the achievement

of long-term earnings targets. Accordingly, the bank has drawn up a host of risk management

policies, beginning with the “Master Policy for Risk Management,” to clarify the bank’s risk

awareness, organizational stance and overall risk management system.

The bank will regularly review these policies, and will constantly endeavor to establish an

appropriate, effective risk management system.

Comprehensive Risk Management

Risk Management Philosophy

In the course of conducting business, banks are exposed to various risks. These include credit,

market and operational and other types of risks. When these risks manifest themselves, losses will

be incurred. In order to withstand losses, risk exposures must accurately be measured and

understood to ensure that risks are comprehensively controlled and

managed within acceptable, pre-defined levels based on a bank’s

financial strength, as determined by its capital adequacy ratio, etc. At the

same time, proactive risk-taking—exposure to credit and market risks of

the customers—is an integral part of the banks’ income generation.

Thus, banks must secure returns commensurate with taken risks.

Aozora Bank comprehensively manages two types of risks: those

required to be taken for income generation, such as credit and market

risks, as well as those that are associated with normal banking

operations, but should be minimized or eliminated as much as possible,

such as operational risks. Against this backdrop, in September 2000, a

comprehensive risk management setup combining risk management and

internal capital allocation was introduced to optimize the bank’s income.

Banks are vulnerable to various risks, and each risk has its own

characteristic. Therefore, each risk must be managed in each specific

way. For this reason, at Aozora Bank, each specialized division manages each type of risk.

However, should any risk manifest itself, its losses will affect the entire banking system. So, it is

vital to comprehensively manage all forms of risks throughout the entire organization of the bank.

In order to bolster risk management across the entire organization, the functions of the

Risk Management Division have been strengthened. The Risk Management Division oversees

risk management at other divisions to ensure that the overall risk management is consistent

and well-balanced. The bank has

established a system whereby the Risk

Management Division is in charge of

the quantification of credit risk as well

as the quantification of market risk to

accurately grasp both types of risks

comprehensively.

Quantification of Total Risk

In order to understand different forms

of risks comprehensively, risks must be

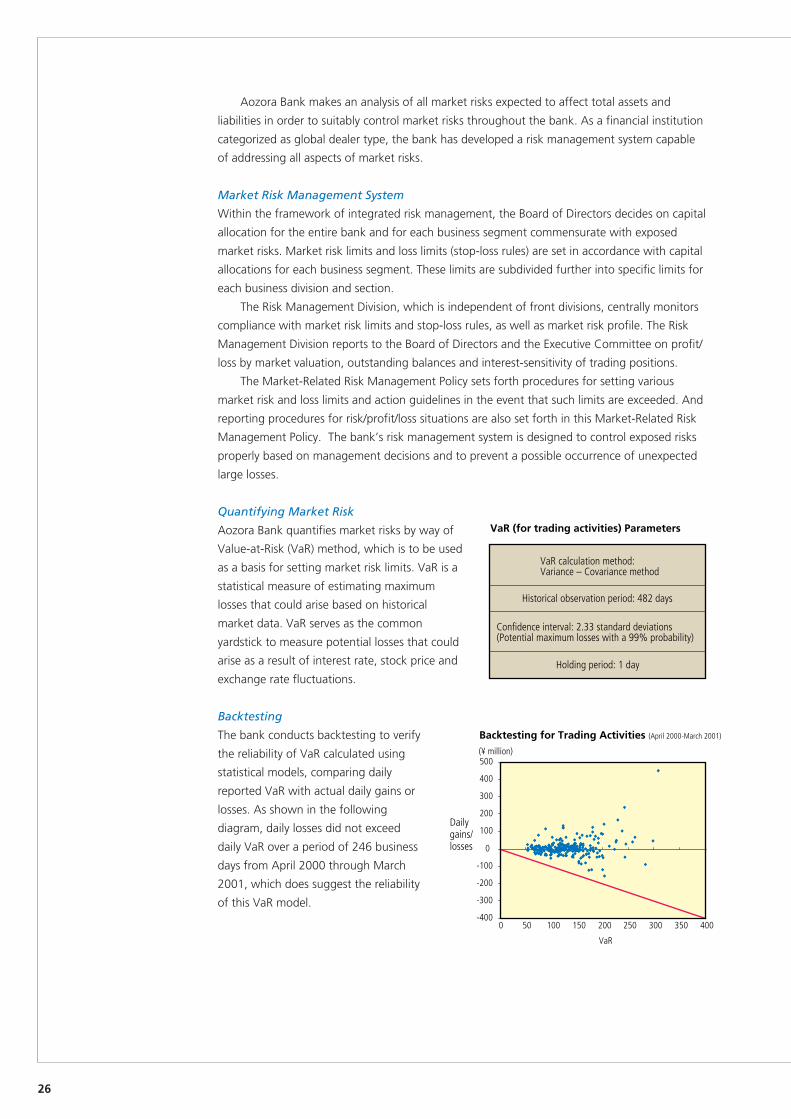

measured by the common yardstick. Aozora Bank employs VaR (Value-at-Risk) to calculate the

amount of capital that should be set aside against particular risks. In this way, the bank

comprehensively manages credit and market risks, etc. Moreover, risks for venture business

investment and risks for investment banking business have also been incorporated into the risk

management framework outlined above, being in line with its own business strategy.

21

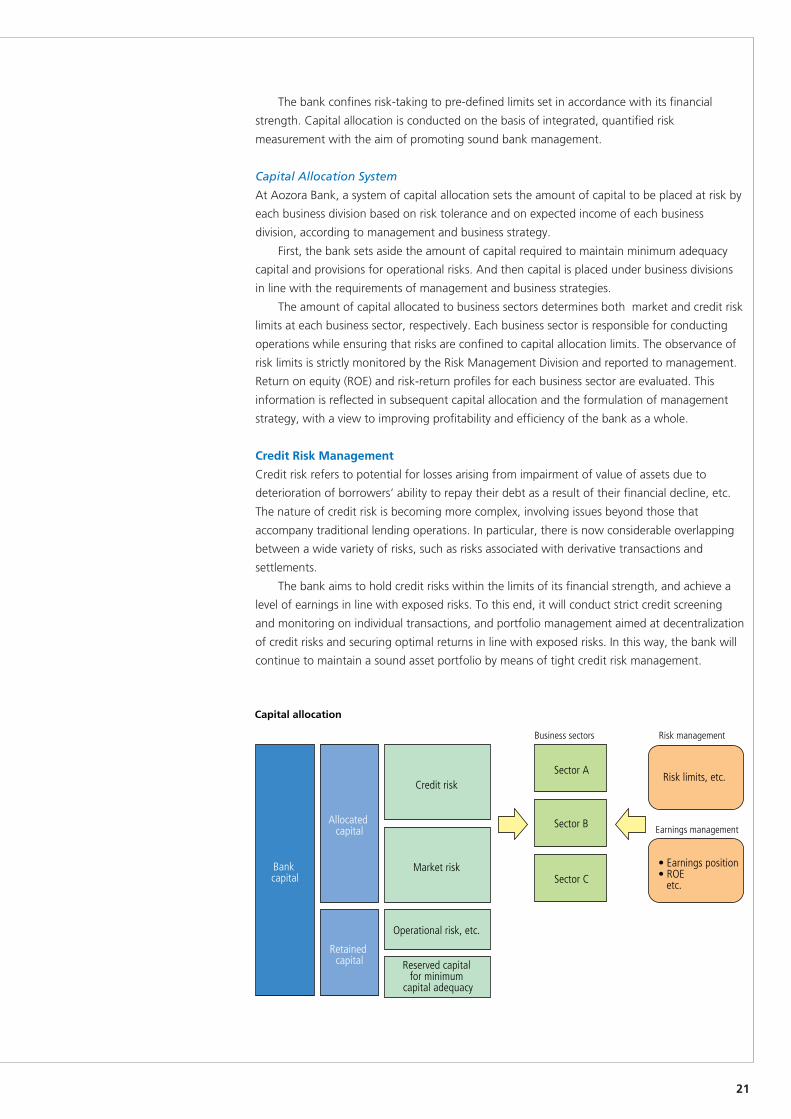

Capital allocation

Bank capital

Allocated capital

Credit risk

Market risk

Operational risk, etc.

Retained capital Reserved capital

for minimum capital adequacy

Business sectors

Sector A

Sector B

Sector C

Risk management

Risk limits, etc.

Earnings management

• Earnings position• ROE etc.

The bank confines risk-taking to pre-defined limits set in accordance with its financial

strength. Capital allocation is conducted on the basis of integrated, quantified risk

measurement with the aim of promoting sound bank management.

Capital Allocation System

At Aozora Bank, a system of capital allocation sets the amount of capital to be placed at risk by

each business division based on risk tolerance and on expected income of each business

division, according to management and business strategy.

First, the bank sets aside the amount of capital required to maintain minimum adequacy

capital and provisions for operational risks. And then capital is placed under business divisions

in line with the requirements of management and business strategies.

The amount of capital allocated to business sectors determines both market and credit risk

limits at each business sector, respectively. Each business sector is responsible for conducting

operations while ensuring that risks are confined to capital allocation limits. The observance of

risk limits is strictly monitored by the Risk Management Division and reported to management.

Return on equity (ROE) and risk-return profiles for each business sector are evaluated. This

information is reflected in subsequent capital allocation and the formulation of management

strategy, with a view to improving profitability and efficiency of the bank as a whole.

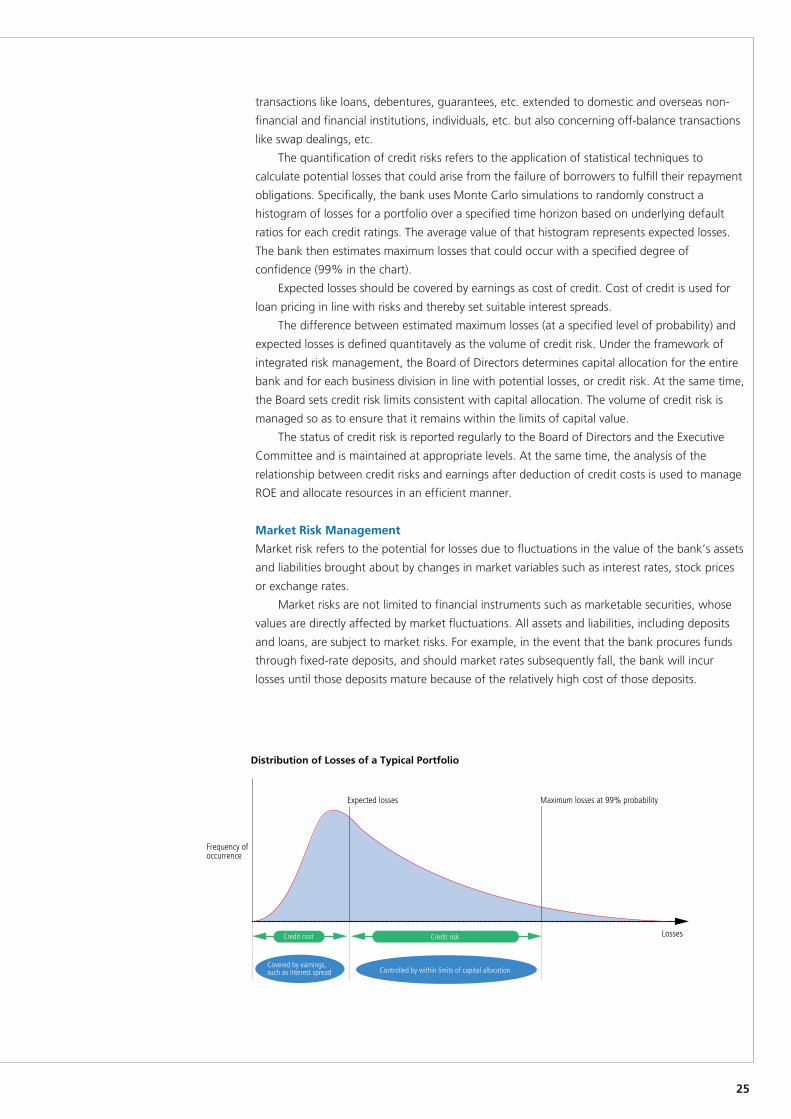

Credit Risk Management

Credit risk refers to potential for losses arising from impairment of value of assets due to

deterioration of borrowers’ ability to repay their debt as a result of their financial decline, etc.

The nature of credit risk is becoming more complex, involving issues beyond those that

accompany traditional lending operations. In particular, there is now considerable overlapping

between a wide variety of risks, such as risks associated with derivative transactions and

settlements.

The bank aims to hold credit risks within the limits of its financial strength, and achieve a

level of earnings in line with exposed risks. To this end, it will conduct strict credit screening

and monitoring on individual transactions, and portfolio management aimed at decentralization

of credit risks and securing optimal returns in line with exposed risks. In this way, the bank will

continue to maintain a sound asset portfolio by means of tight credit risk management.

22

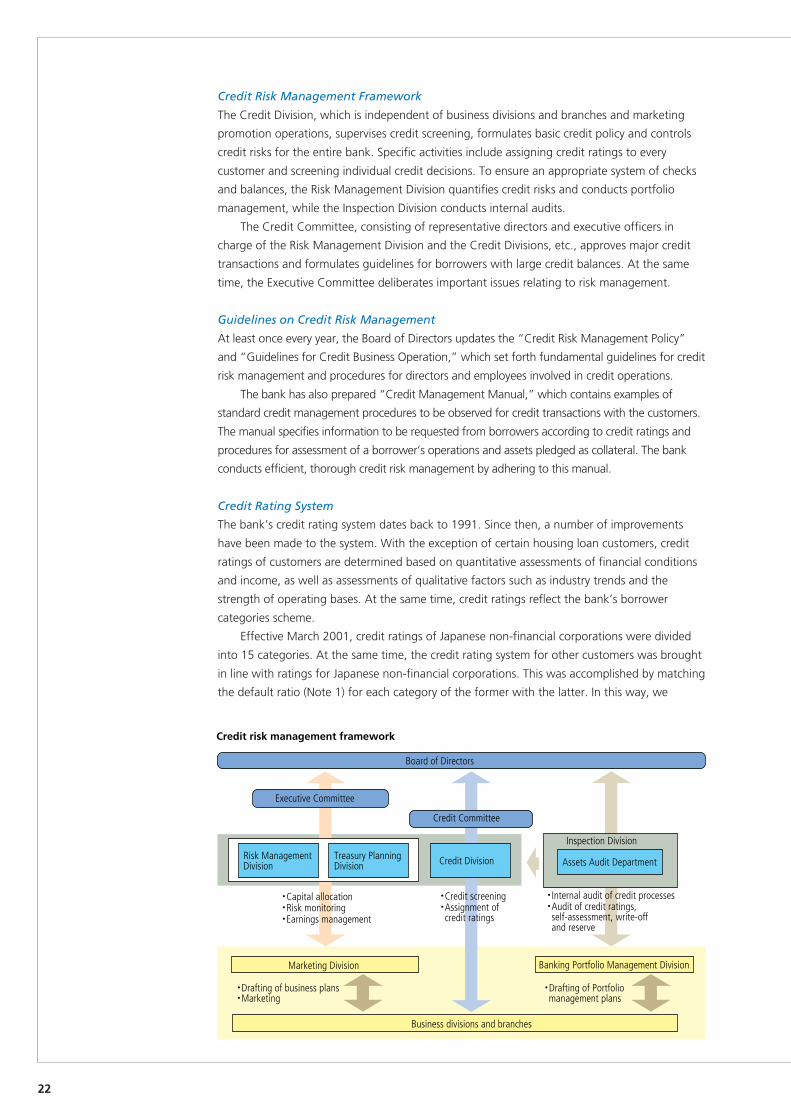

・Capital allocation・Risk monitoring・Earnings management

・Credit screening・Assignment of credit ratings

・Internal audit of credit processes・Audit of credit ratings, self-assessment, write-off and reserve

・Drafting of business plans・Marketing

・Drafting of Portfolio management plans

Banking Portfolio Management DivisionMarketing Division

Business divisions and branches

Credit risk management framework

Executive Committee

Inspection Division

Assets Audit Department

Credit Committee

Credit Division

Board of Directors

Treasury Planning Division

Risk Management Division

Credit Risk Management Framework

The Credit Division, which is independent of business divisions and branches and marketing

promotion operations, supervises credit screening, formulates basic credit policy and controls

credit risks for the entire bank. Specific activities include assigning credit ratings to every

customer and screening individual credit decisions. To ensure an appropriate system of checks

and balances, the Risk Management Division quantifies credit risks and conducts portfolio

management, while the Inspection Division conducts internal audits.

The Credit Committee, consisting of representative directors and executive officers in

charge of the Risk Management Division and the Credit Divisions, etc., approves major credit

transactions and formulates guidelines for borrowers with large credit balances. At the same

time, the Executive Committee deliberates important issues relating to risk management.

Guidelines on Credit Risk Management

At least once every year, the Board of Directors updates the “Credit Risk Management Policy”

and “Guidelines for Credit Business Operation,” which set forth fundamental guidelines for credit

risk management and procedures for directors and employees involved in credit operations.

The bank has also prepared “Credit Management Manual,” which contains examples of

standard credit management procedures to be observed for credit transactions with the customers.

The manual specifies information to be requested from borrowers according to credit ratings and

procedures for assessment of a borrower’s operations and assets pledged as collateral. The bank

conducts efficient, thorough credit risk management by adhering to this manual.

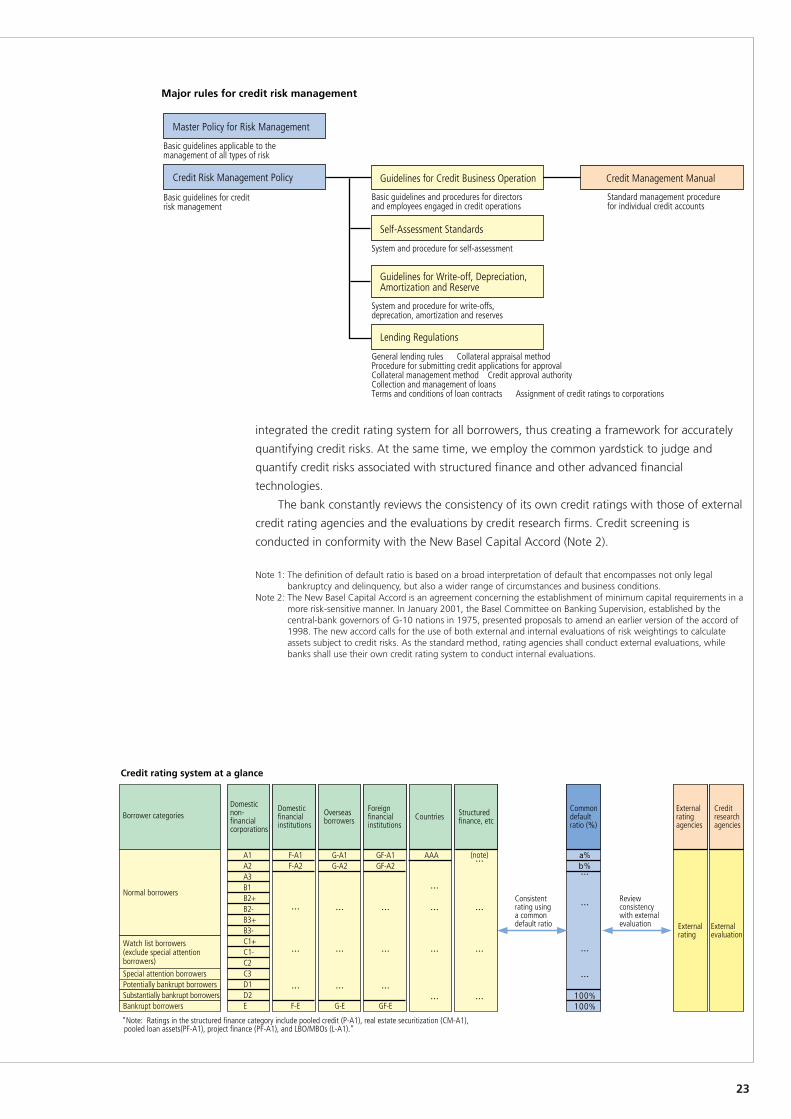

Credit Rating System

The bank’s credit rating system dates back to 1991. Since then, a number of improvements

have been made to the system. With the exception of certain housing loan customers, credit

ratings of customers are determined based on quantitative assessments of financial conditions

and income, as well as assessments of qualitative factors such as industry trends and the

strength of operating bases. At the same time, credit ratings reflect the bank’s borrower

categories scheme.

Effective March 2001, credit ratings of Japanese non-financial corporations were divided

into 15 categories. At the same time, the credit rating system for other customers was brought

in line with ratings for Japanese non-financial corporations. This was accomplished by matching

the default ratio (Note 1) for each category of the former with the latter. In this way, we

23

Major rules for credit risk management

Master Policy for Risk Management

Basic guidelines applicable to the management of all types of risk

Credit Risk Management Policy

Basic guidelines for credit risk management

Guidelines for Credit Business Operation Credit Management Manual

Standard management procedurefor individual credit accounts

Self-Assessment Standards

System and procedure for self-assessment

Guidelines for Write-off, Depreciation, Amortization and Reserve

System and procedure for write-offs, deprecation, amortization and reserves

Lending Regulations

General lending rules Collateral appraisal methodProcedure for submitting credit applications for approval Collateral management method Credit approval authority Collection and management of loansTerms and conditions of loan contracts Assignment of credit ratings to corporations

Basic guidelines and procedures for directors and employees engaged in credit operations

Borrower categoriesDomestic non-financial corporations

Domestic financial institutions

Overseas borrowers

Foreign financial institutions

Countries Structured finance, etc

Common default ratio (%)

External rating agencies

External rating

Credit research agencies

Review consistency with external evaluation

Consistent rating using a common default ratio

Credit rating system at a glance

A1 F-A1 G-A1 GF-A1 AAA (note) a%A2 F-A2 G-A2 GF-A2 b%A3B1B2+B2-B3+B3-C1+C1-C2

Special attention borrowers C3Potentially bankrupt borrowers D1Substantially bankrupt borrowers D2 100%Bankrupt borrowers E F-E G-E GF-E 100%

“Note: Ratings in the structured finance category include pooled credit (P-A1), real estate securitization (CM-A1), pooled loan assets(PF-A1), project finance (PF-A1), and LBO/MBOs (L-A1).”

Normal borrowers

Watch list borrowers(exclude special attention borrowers)

…

…

…

… …

… …

… …

… … … …

…

…

…

… … …

… …

…

…

External evaluation

integrated the credit rating system for all borrowers, thus creating a framework for accurately

quantifying credit risks. At the same time, we employ the common yardstick to judge and

quantify credit risks associated with structured finance and other advanced financial

technologies.

The bank constantly reviews the consistency of its own credit ratings with those of external

credit rating agencies and the evaluations by credit research firms. Credit screening is

conducted in conformity with the New Basel Capital Accord (Note 2).

Note 1: The definition of default ratio is based on a broad interpretation of default that encompasses not only legalbankruptcy and delinquency, but also a wider range of circumstances and business conditions.

Note 2: The New Basel Capital Accord is an agreement concerning the establishment of minimum capital requirements in amore risk-sensitive manner. In January 2001, the Basel Committee on Banking Supervision, established by thecentral-bank governors of G-10 nations in 1975, presented proposals to amend an earlier version of the accord of1998. The new accord calls for the use of both external and internal evaluations of risk weightings to calculateassets subject to credit risks. As the standard method, rating agencies shall conduct external evaluations, whilebanks shall use their own credit rating system to conduct internal evaluations.

24

Credit Management Centered on Ratings

At Aozora Bank, credit ratings are integral to credit management. Credit ratings affect credit

screening procedures, and constitute one of many important criteria for credit approval,

including criteria for interest spread and credit limits. Credit ratings are also used to conduct

self-assessments and are employed as benchmarks to quantify credit risks. The following

procedures are followed in assigning credit ratings.

• Business divisions and branches conduct preliminary evaluations of borrowers. Subsequently,

the Credit Division, which is independent of the former, is responsible for making the final

decision, and to ensure sufficient checks and balances, the final assignment of a credit rating

is reviewed by the Assets Audit Department and an auditor.

• Decision-making authority is delegated based on a combination of two factors: credit ratings

and credit exposure.

• Credit limits for each rating are determined based on bank capital and credit costs for each

rating. As such, ratings are a key indicator used to hold credit risks within appropriate limits.

• In April 2001, the bank adopted credit ratings linked to certain financing schemes, such as

structured finance, where collection is independent of a borrower’s ability to repay a debt.

We will continue to refine credit rating systems. For instance, we will develop initiatives such

as credit ratings for venture businesses based on evaluation of business models.

Credit Screening on Individual Transactions

Credit ratings are nothing more than indicators for borrowers’ creditworthiness, based on

default ratios. As such, actual credit screening must be conducted in such a way to evaluate

borrowers and their credit requirements on individual transactions.

Business divisions and branches are responsible for preliminary screenings. Subsequently,

experienced analysts in the Credit Division conduct secondary screenings, which involves, in

particular, a careful review of the business plans, the appropriateness of fund usage and its

financial soundness. Analysts also give consideration to the future availability of funds for

repayment, repayment methods, and the duration of the loan.

Credit monitoring is conducted in accordance with guidelines stipulated in Lending

Regulations and the Credit Management Manual. The bank carefully monitors the

creditworthiness of borrowers and the value of collateral. In this way, the bank works to

uncover problems at an early stage, with a view to preventing a possible occurrence of non-

performing loans.

Portfolio Management

To maintain the soundness of assets vulnerable to credit risks, the bank evaluates and manages

risks associated with each borrower and loan application along with estimated earnings from the

loan. At the same time, the bank analyzes and manages aggregate risks in the entire loan

portfolio. In August 2000, the Risk Management Division was strengthened and improved. The