Embed Size (px)

DESCRIPTION

Citation preview

© 2012 McGladrey LLP. All Rights Reserved. © 2012 McGladrey LLP. All Rights Reserved.

James Beal, Partner, Tax Services

Ron Copher, CFO/EVP, Glacier Bancorp, Inc.

Douglas P. Koch, MAI, AICP Director

Tax Credits – Beyond the Basics

© 2012 McGladrey LLP. All Rights Reserved.

Agenda

Low Income Housing Tax Credit (LIHTC)

New Markets Tax Credit (NMTC)

Historic Rehabilitation Tax Credit (HTC)

Review mechanics of each credit

Discuss the market for each credit

Investor returns

Risks and rewards

Commentary on the current developments and the

future

1

© 2012 McGladrey LLP. All Rights Reserved.

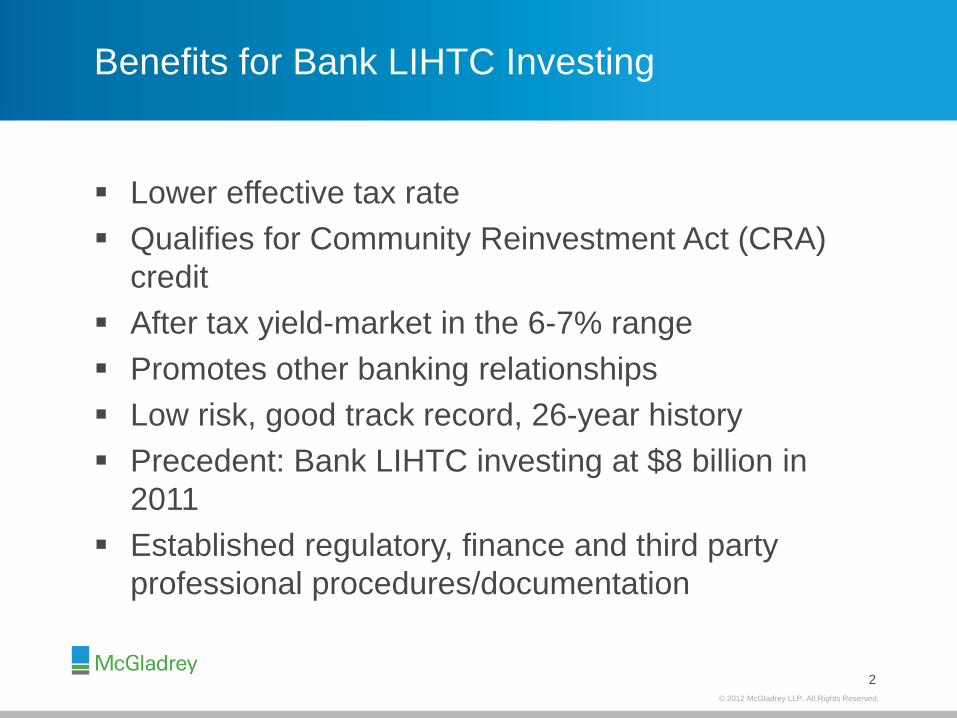

Benefits for Bank LIHTC Investing

Lower effective tax rate

Qualifies for Community Reinvestment Act (CRA)

credit

After tax yield-market in the 6-7% range

Promotes other banking relationships

Low risk, good track record, 26-year history

Precedent: Bank LIHTC investing at $8 billion in

2011

Established regulatory, finance and third party

professional procedures/documentation

2

© 2012 McGladrey LLP. All Rights Reserved.

Program Overview

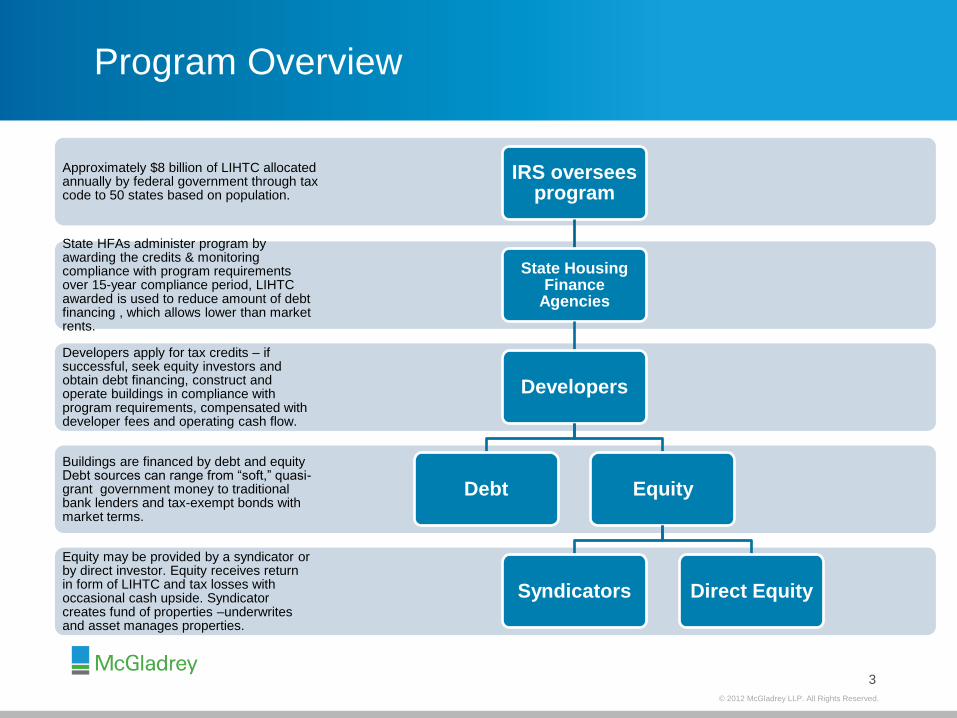

Equity may be provided by a syndicator or by direct investor. Equity receives return in form of LIHTC and tax losses with occasional cash upside. Syndicator creates fund of properties –underwrites and asset manages properties.

Buildings are financed by debt and equity Debt sources can range from “soft,” quasi-grant government money to traditional bank lenders and tax-exempt bonds with market terms.

Developers apply for tax credits – if successful, seek equity investors and obtain debt financing, construct and operate buildings in compliance with program requirements, compensated with developer fees and operating cash flow.

State HFAs administer program by awarding the credits & monitoring compliance with program requirements over 15-year compliance period, LIHTC awarded is used to reduce amount of debt financing , which allows lower than market rents.

Approximately $8 billion of LIHTC allocated annually by federal government through tax code to 50 states based on population.

IRS oversees program

State Housing Finance

Agencies

Developers

Debt Equity

Syndicators Direct Equity

3

© 2012 McGladrey LLP. All Rights Reserved.

How the Credit Works

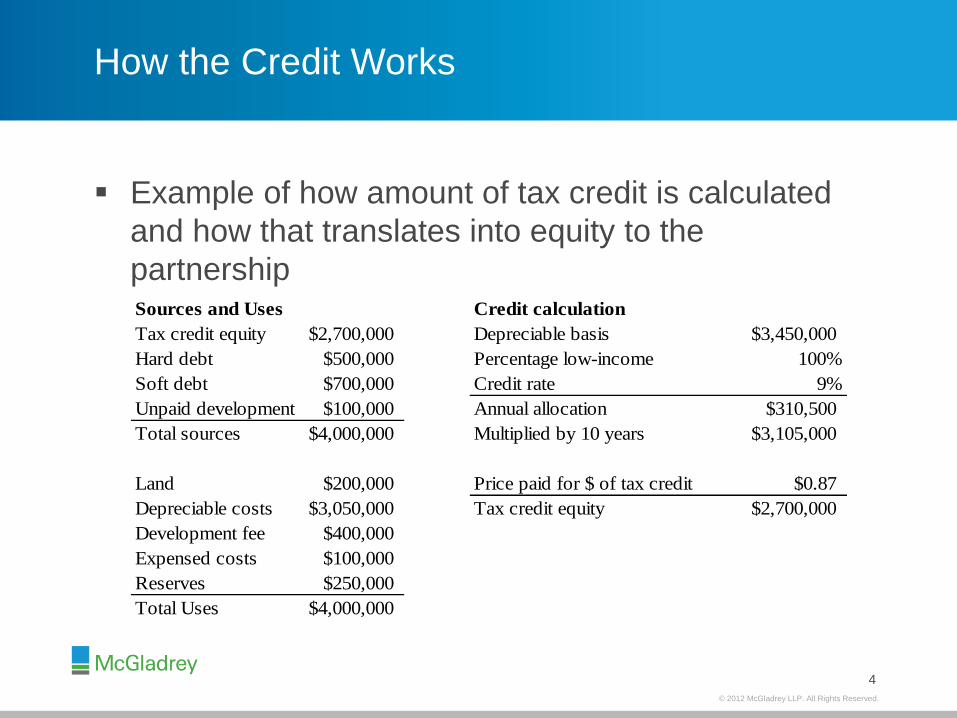

Example of how amount of tax credit is calculated

and how that translates into equity to the

partnership Sources and Uses Credit calculation

Tax credit equity $2,700,000 Depreciable basis $3,450,000

Hard debt $500,000 Percentage low-income 100%

Soft debt $700,000 Credit rate 9%

Unpaid development fee$100,000 Annual allocation $310,500

Total sources $4,000,000 Multiplied by 10 years $3,105,000

Land $200,000 Price paid for $ of tax credit $0.87

Depreciable costs $3,050,000 Tax credit equity $2,700,000

Development fee $400,000

Expensed costs $100,000

Reserves $250,000

Total Uses $4,000,000

4

© 2012 McGladrey LLP. All Rights Reserved.

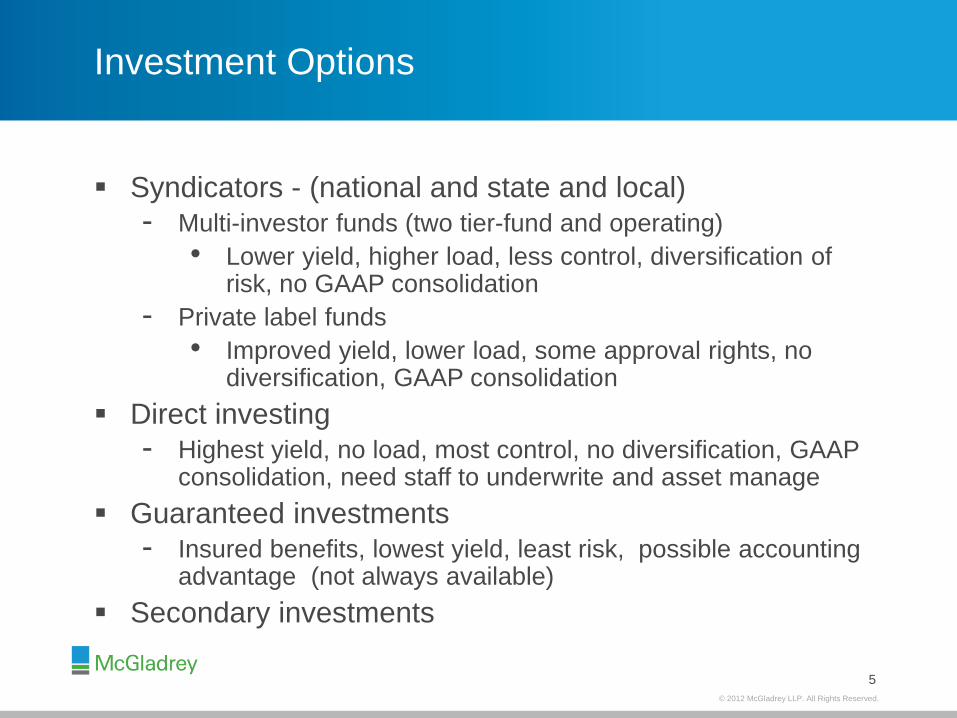

Investment Options

Syndicators - (national and state and local)

- Multi-investor funds (two tier-fund and operating)

• Lower yield, higher load, less control, diversification of risk, no GAAP consolidation

- Private label funds

• Improved yield, lower load, some approval rights, no diversification, GAAP consolidation

Direct investing

- Highest yield, no load, most control, no diversification, GAAP consolidation, need staff to underwrite and asset manage

Guaranteed investments

- Insured benefits, lowest yield, least risk, possible accounting advantage (not always available)

Secondary investments

5

© 2012 McGladrey LLP. All Rights Reserved.

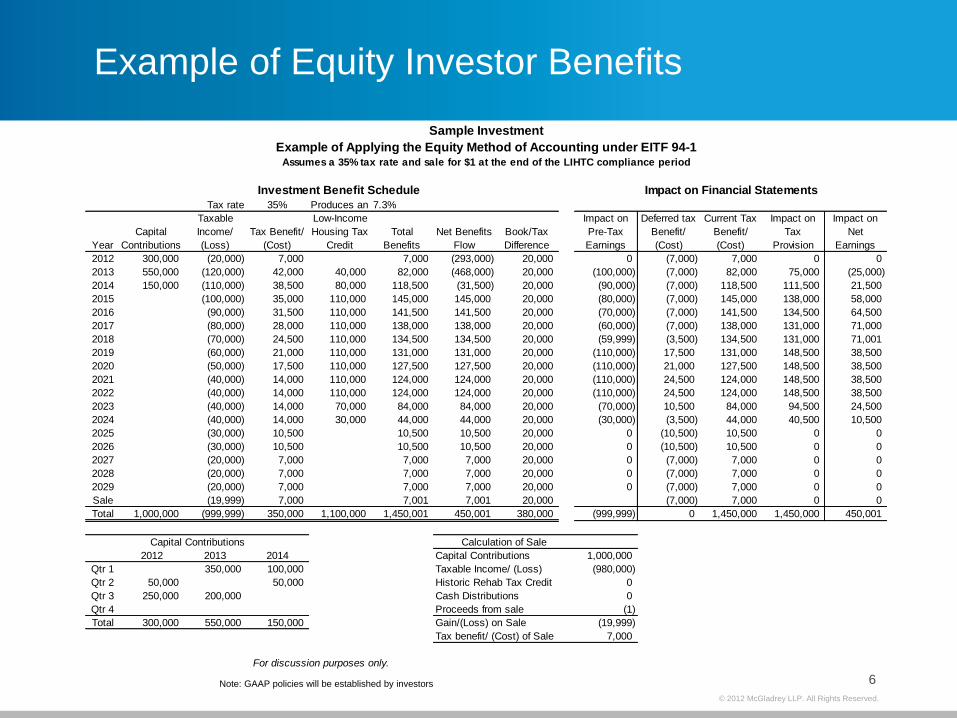

Example of Equity Investor Benefits

6

Tax rate 35% Produces an IRR of approximately -7.3%

Year

Capital

Contributions

Taxable

Income/

(Loss)

Tax Benefit/

(Cost)

Low-Income

Housing Tax

Credit

Total

Benefits

Net Benefits

Flow

Book/Tax

Difference

Impact on

Pre-Tax

Earnings

Deferred tax

Benefit/

(Cost)

Current Tax

Benefit/

(Cost)

Impact on

Tax

Provision

Impact on

Net

Earnings

2012 300,000 (20,000) 7,000 7,000 (293,000) 20,000 0 (7,000) 7,000 0 0

2013 550,000 (120,000) 42,000 40,000 82,000 (468,000) 20,000 (100,000) (7,000) 82,000 75,000 (25,000)

2014 150,000 (110,000) 38,500 80,000 118,500 (31,500) 20,000 (90,000) (7,000) 118,500 111,500 21,500

2015 (100,000) 35,000 110,000 145,000 145,000 20,000 (80,000) (7,000) 145,000 138,000 58,000

2016 (90,000) 31,500 110,000 141,500 141,500 20,000 (70,000) (7,000) 141,500 134,500 64,500

2017 (80,000) 28,000 110,000 138,000 138,000 20,000 (60,000) (7,000) 138,000 131,000 71,000

2018 (70,000) 24,500 110,000 134,500 134,500 20,000 (59,999) (3,500) 134,500 131,000 71,001

2019 (60,000) 21,000 110,000 131,000 131,000 20,000 (110,000) 17,500 131,000 148,500 38,500

2020 (50,000) 17,500 110,000 127,500 127,500 20,000 (110,000) 21,000 127,500 148,500 38,500

2021 (40,000) 14,000 110,000 124,000 124,000 20,000 (110,000) 24,500 124,000 148,500 38,500

2022 (40,000) 14,000 110,000 124,000 124,000 20,000 (110,000) 24,500 124,000 148,500 38,500

2023 (40,000) 14,000 70,000 84,000 84,000 20,000 (70,000) 10,500 84,000 94,500 24,500

2024 (40,000) 14,000 30,000 44,000 44,000 20,000 (30,000) (3,500) 44,000 40,500 10,500

2025 (30,000) 10,500 10,500 10,500 20,000 0 (10,500) 10,500 0 0

2026 (30,000) 10,500 10,500 10,500 20,000 0 (10,500) 10,500 0 0

2027 (20,000) 7,000 7,000 7,000 20,000 0 (7,000) 7,000 0 0

2028 (20,000) 7,000 7,000 7,000 20,000 0 (7,000) 7,000 0 0

2029 (20,000) 7,000 7,000 7,000 20,000 0 (7,000) 7,000 0 0

Sale (19,999) 7,000 7,001 7,001 20,000 (7,000) 7,000 0 0

Total 1,000,000 (999,999) 350,000 1,100,000 1,450,001 450,001 380,000 (999,999) 0 1,450,000 1,450,000 450,001

2012 2013 2014 Capital Contributions 1,000,000

Qtr 1 350,000 100,000 Taxable Income/ (Loss) (980,000)

Qtr 2 50,000 50,000 Historic Rehab Tax Credit 0

Qtr 3 250,000 200,000 Cash Distributions 0

Qtr 4 Proceeds from sale (1)

Total 300,000 550,000 150,000 Gain/(Loss) on Sale (19,999)

Tax benefit/ (Cost) of Sale 7,000

Impact on Financial Statements

Capital Contributions Calculation of Sale

For discussion purposes only.

Sample Investment

Example of Applying the Equity Method of Accounting under EITF 94-1Assumes a 35% tax rate and sale for $1 at the end of the LIHTC compliance period

Investment Benefit Schedule

Note: GAAP policies will be established by investors

© 2012 McGladrey LLP. All Rights Reserved.

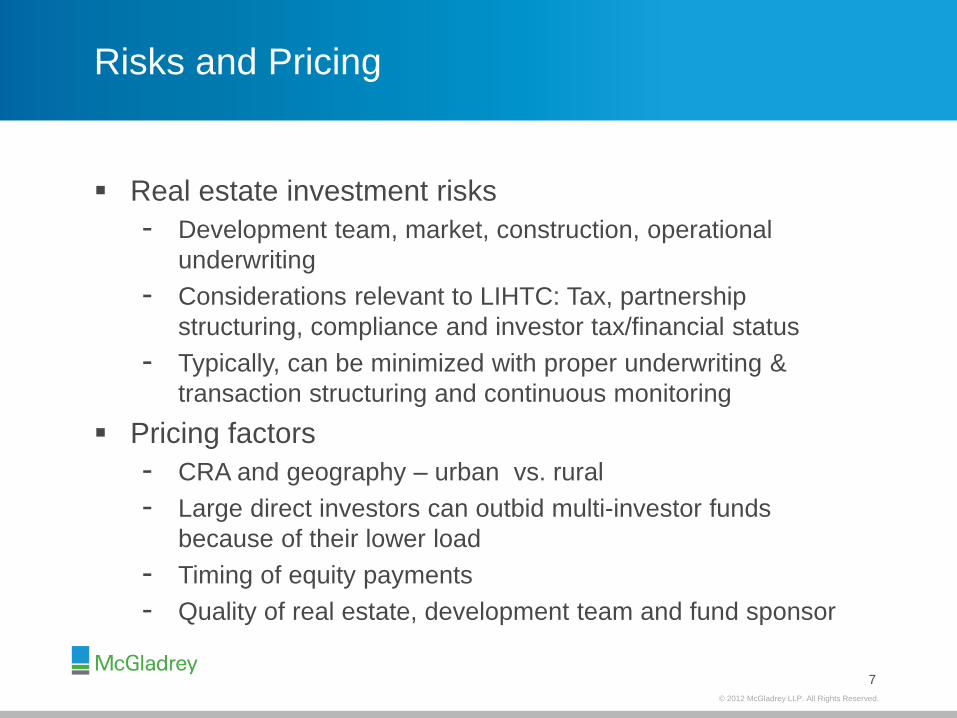

Risks and Pricing

Real estate investment risks

- Development team, market, construction, operational

underwriting

- Considerations relevant to LIHTC: Tax, partnership

structuring, compliance and investor tax/financial status

- Typically, can be minimized with proper underwriting &

transaction structuring and continuous monitoring

Pricing factors

- CRA and geography – urban vs. rural

- Large direct investors can outbid multi-investor funds

because of their lower load

- Timing of equity payments

- Quality of real estate, development team and fund sponsor

7

© 2012 McGladrey LLP. All Rights Reserved.

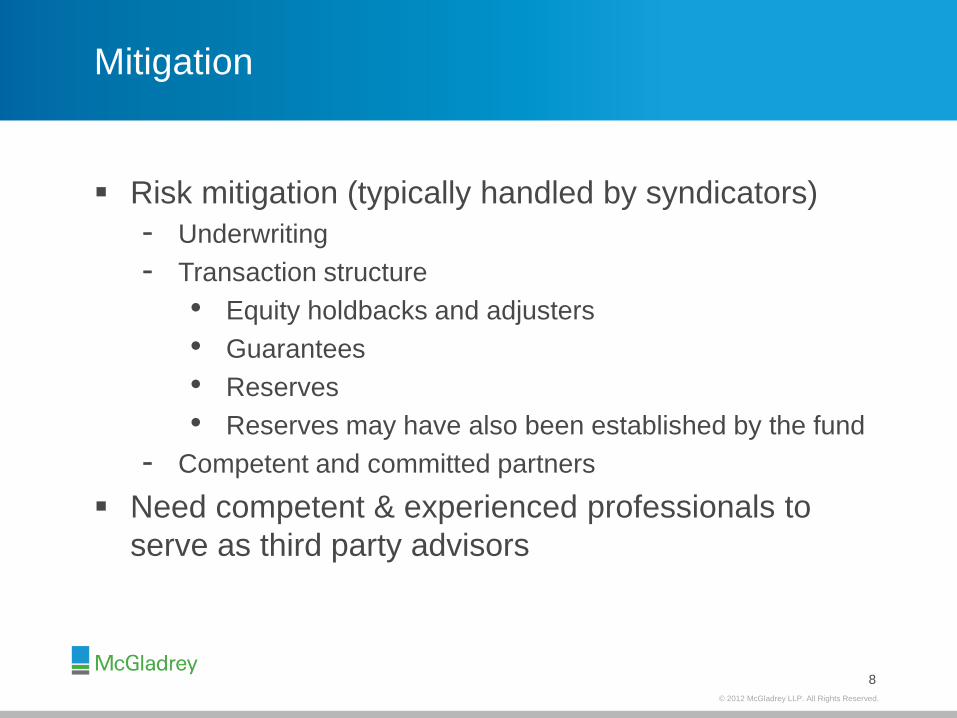

Mitigation

Risk mitigation (typically handled by syndicators)

- Underwriting

- Transaction structure

• Equity holdbacks and adjusters

• Guarantees

• Reserves

• Reserves may have also been established by the fund

- Competent and committed partners

Need competent & experienced professionals to

serve as third party advisors

8

© 2012 McGladrey LLP. All Rights Reserved.

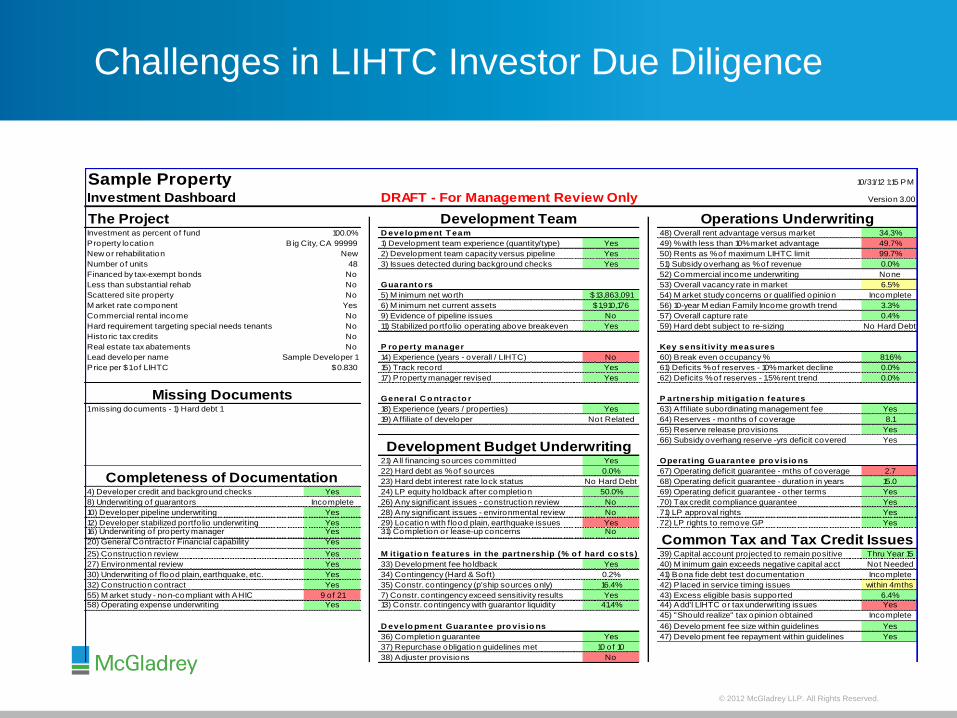

Challenges in LIHTC Investor Due Diligence

Sample PropertyInvestment Dashboard DRAFT - For Management Review Only Version 3.00

Investment as percent of fund 100.0% D evelo pment T eam 48) Overall rent advantage versus market 34.3%

Property location Big City, CA 99999 1) Development team experience (quantity/type) Yes 49) % with less than 10% market advantage 49.7%

New or rehabilitation New 2) Development team capacity versus pipeline Yes 50) Rents as % of maximum LIHTC limit 99.7%

Number of units 48 3) Issues detected during background checks Yes 51) Subsidy overhang as % of revenue 0.0%

Financed by tax-exempt bonds No 52) Commercial income underwriting None

Less than substantial rehab No Guaranto rs 53) Overall vacancy rate in market 6.5%

Scattered site property No 5) M inimum net worth $13,863,091 54) M arket study concerns or qualified opinion Incomplete

M arket rate component Yes 6) M inimum net current assets $1,910,176 56) 10-year M edian Family Income growth trend 3.3%

Commercial rental income No 9) Evidence of pipeline issues No 57) Overall capture rate 0.4%

Hard requirement targeting special needs tenants No 11) Stabilized portfo lio operating above breakeven Yes 59) Hard debt subject to re-sizing No Hard Debt

Historic tax credits No

Real estate tax abatements No P ro perty manager Key sensit ivity measures

Lead developer name Sample Developer 1 14) Experience (years - overall / LIHTC) No 60) Break even occupancy % 81.6%

Price per $1 of LIHTC $0.830 15) Track record Yes 61) Deficits % of reserves - 10% market decline 0.0%

17) Property manager revised Yes 62) Deficits % of reserves - 1.5% rent trend 0.0%

General C o ntracto r P artnership mit igat io n features

18) Experience (years / properties) Yes 63) Affiliate subordinating management fee Yes

19) Affiliate of developer Not Related 64) Reserves - months of coverage 8.1

65) Reserve release provisions Yes

66) Subsidy overhang reserve -yrs deficit covered Yes

21) All financing sources committed Yes Operat ing Guarantee pro visio ns

22) Hard debt as % of sources 0.0% 67) Operating deficit guarantee - mths of coverage 2.7

23) Hard debt interest rate lock status No Hard Debt 68) Operating deficit guarantee - duration in years 15.0

4) Developer credit and background checks Yes 24) LP equity holdback after completion 50.0% 69) Operating deficit guarantee - other terms Yes

8) Underwriting of guarantors Incomplete 26) Any significant issues - construction review No 70) Tax credit compliance guarantee Yes

10) Developer pipeline underwriting Yes 28) Any significant issues - environmental review No 71) LP approval rights Yes

12) Developer stabilized portfo lio underwriting Yes 29) Location with flood plain, earthquake issues Yes 72) LP rights to remove GP Yes16) Underwriting of property manager Yes 31) Completion or lease-up concerns No

20) General Contractor Financial capability Yes

25) Construction review Yes M it igat io n features in the partnership (% o f hard co sts) 39) Capital account pro jected to remain positive Thru Year 15

27) Environmental review Yes 33) Development fee holdback Yes 40) M inimum gain exceeds negative capital acct Not Needed

30) Underwriting of flood plain, earthquake, etc. Yes 34) Contingency (Hard & Soft) 0.2% 41) Bona fide debt test documentation Incomplete

32) Construction contract Yes 35) Constr. contingency (p'ship sources only) 16.4% 42) Placed in service timing issues within 4mths

55) M arket study - non-compliant with AHIC 9 of 21 7) Constr. contingency exceed sensitivity results Yes 43) Excess eligible basis supported 6.4%

58) Operating expense underwriting Yes 13) Constr. contingency with guarantor liquidity 41.4% 44) Add'l LIHTC or tax underwriting issues Yes

45) "Should realize" tax opinion obtained Incomplete

D evelo pment Guarantee pro visio ns 46) Development fee size within guidelines Yes

36) Completion guarantee Yes 47) Development fee repayment within guidelines Yes

37) Repurchase obligation guidelines met 10 of 10

38) Adjuster provisions No

Missing Documents

10/31/12 1:15 PM

The Project Operations UnderwritingDevelopment Team

Completeness of Documentation

Common Tax and Tax Credit Issues

Development Budget Underwriting

1 missing documents - 1) Hard debt 1

© 2012 McGladrey LLP. All Rights Reserved.

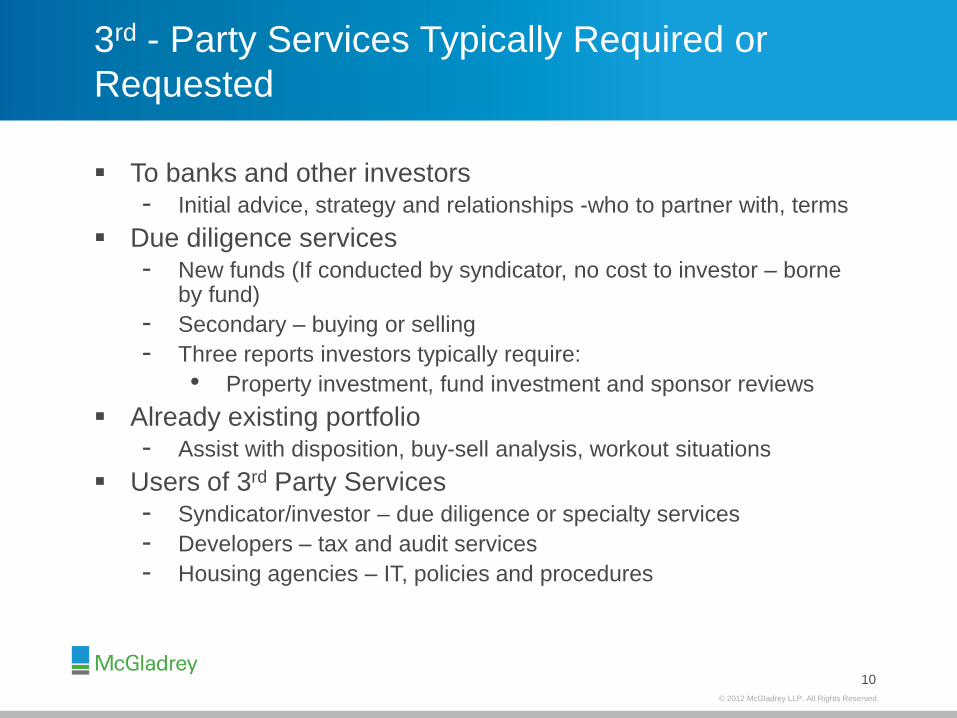

3rd - Party Services Typically Required or

Requested

To banks and other investors - Initial advice, strategy and relationships -who to partner with, terms

Due diligence services - New funds (If conducted by syndicator, no cost to investor – borne

by fund)

- Secondary – buying or selling

- Three reports investors typically require:

• Property investment, fund investment and sponsor reviews

Already existing portfolio - Assist with disposition, buy-sell analysis, workout situations

Users of 3rd Party Services - Syndicator/investor – due diligence or specialty services

- Developers – tax and audit services

- Housing agencies – IT, policies and procedures

10

© 2012 McGladrey LLP. All Rights Reserved.

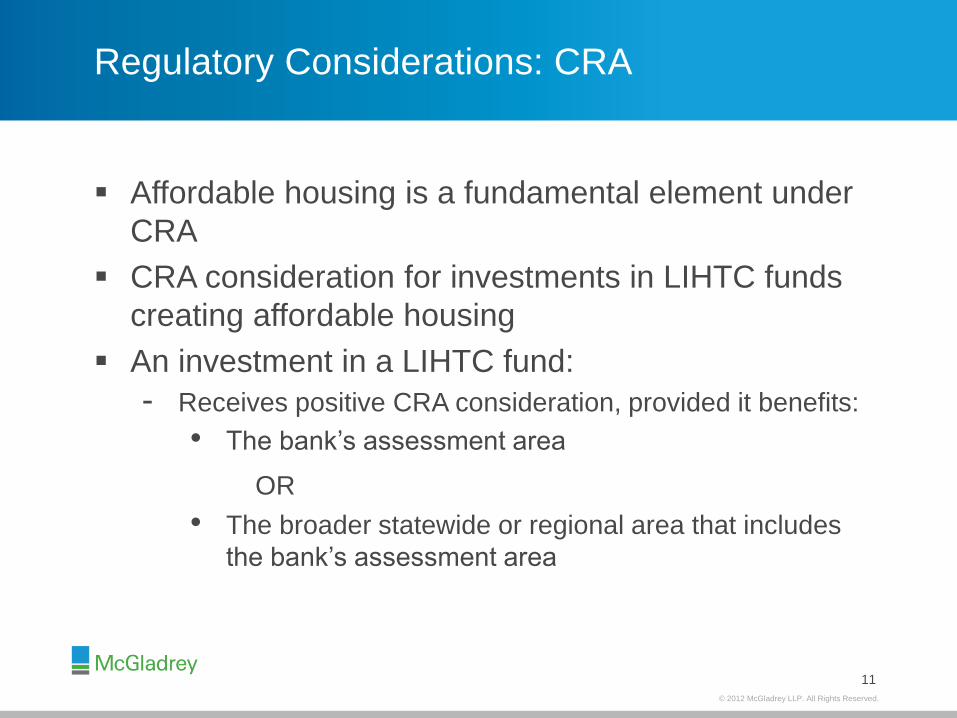

Regulatory Considerations: CRA

Affordable housing is a fundamental element under

CRA

CRA consideration for investments in LIHTC funds

creating affordable housing

An investment in a LIHTC fund:

- Receives positive CRA consideration, provided it benefits:

• The bank’s assessment area

OR

• The broader statewide or regional area that includes

the bank’s assessment area

11

© 2012 McGladrey LLP. All Rights Reserved.

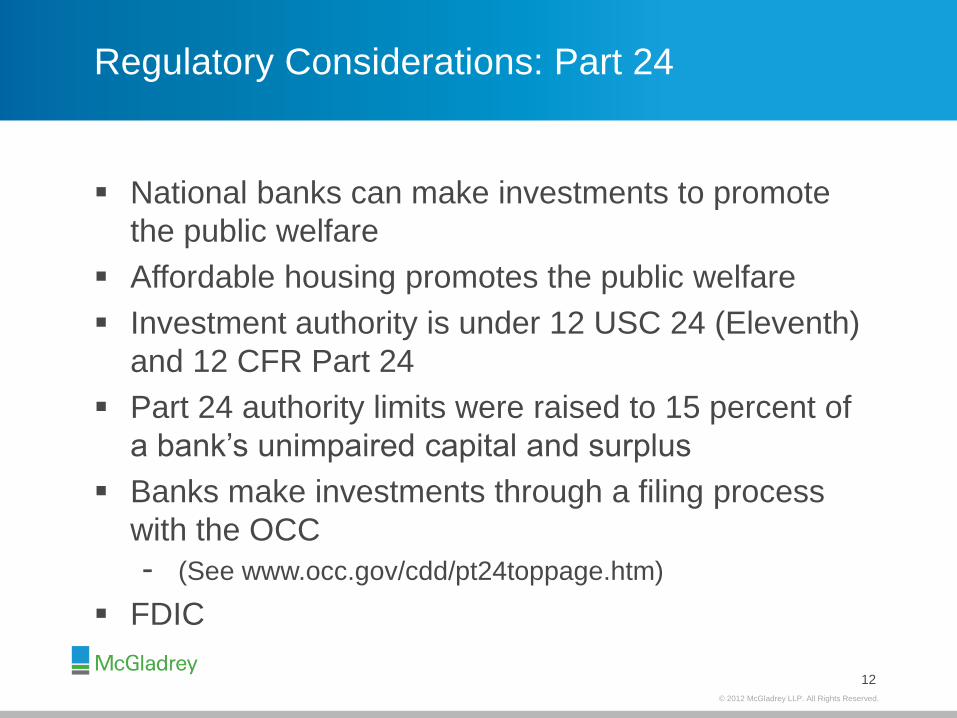

Regulatory Considerations: Part 24

National banks can make investments to promote

the public welfare

Affordable housing promotes the public welfare

Investment authority is under 12 USC 24 (Eleventh)

and 12 CFR Part 24

Part 24 authority limits were raised to 15 percent of

a bank’s unimpaired capital and surplus

Banks make investments through a filing process

with the OCC

- (See www.occ.gov/cdd/pt24toppage.htm)

FDIC

12

© 2012 McGladrey LLP. All Rights Reserved.

OCC Key Risks and Regulatory Issues

Associated with Tax Credit Investments

Liquidity risk

Underwriting and credit risk

- Management

- Real estate underwriting

Collateral risk

Operational and reputation risk

Part 24

Accounting considerations

13

© 2012 McGladrey LLP. All Rights Reserved.

New Markets Tax Credits

Overview

- Background of the NMTC program

- NMTCs: How do they work and what are the benefits?

- How can you utilize NMTCs?

- What are the obstacles in utilizing NMTCs?

- Challenges of troubled Qualified Low Income Community

Investments (QLICI)

- Tax issues with insolvent or bankrupt Qualified Active Low

Income Community Businesses (QALICB)

- Options to simplify the NMTC Program

- Regulatory considerations (CRA and Part 24 limits) and

OCC key risks

14

© 2012 McGladrey LLP. All Rights Reserved.

Background of the NMTC Program

The NMTC program was enacted in December 21, 2000

as a part of the Community Renewal Tax Relief Act of

2000 and provides for a 39% tax credit over a 7 year

period (5% yrs 1-3 and 6% yrs 4-7) based on the

investment (7 year compliance period)

The purpose of the program is to infuse investment dollars

in low income communities where access to capital is

generally more difficult to obtain

15

© 2012 McGladrey LLP. All Rights Reserved.

Background of the NMTC Program

The NMTC program has a highly competitive allocation

process where Community Development Entities (CDEs)

apply for allocation through the CDFI Fund, which is a

division of the US Department of the Treasury

The CDEs must use substantially all (85% or more) of the

proceeds from Qualified Equity Investments (QEIs) to

make QLICIs in QALICBs located in Low Income

Communities (LICs)

16

© 2012 McGladrey LLP. All Rights Reserved.

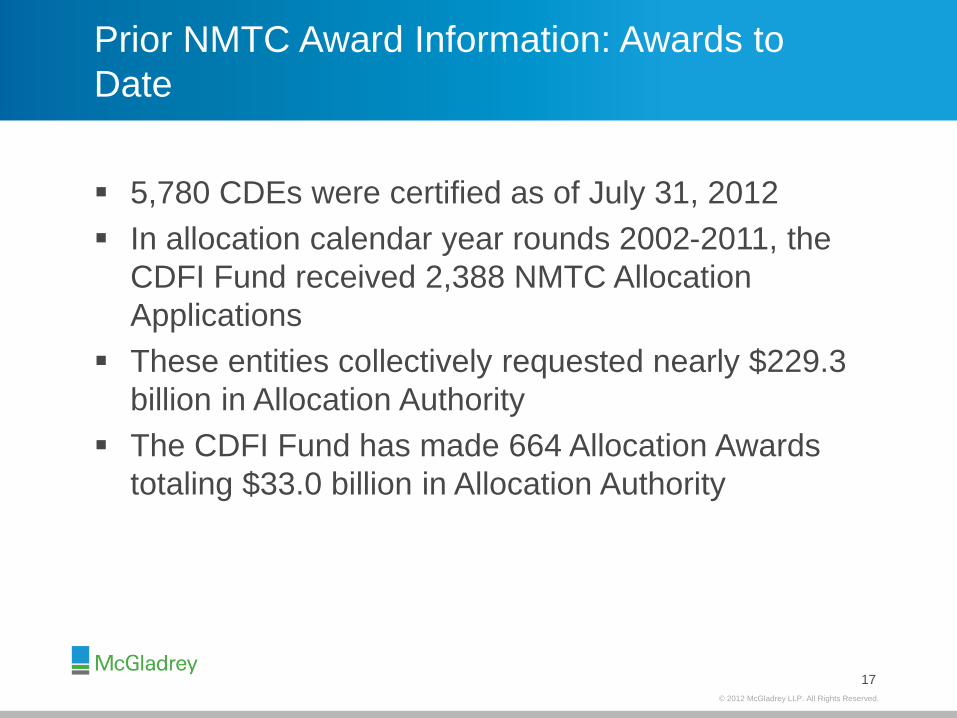

Prior NMTC Award Information: Awards to

Date

5,780 CDEs were certified as of July 31, 2012

In allocation calendar year rounds 2002-2011, the

CDFI Fund received 2,388 NMTC Allocation

Applications

These entities collectively requested nearly $229.3

billion in Allocation Authority

The CDFI Fund has made 664 Allocation Awards

totaling $33.0 billion in Allocation Authority

17

© 2012 McGladrey LLP. All Rights Reserved.

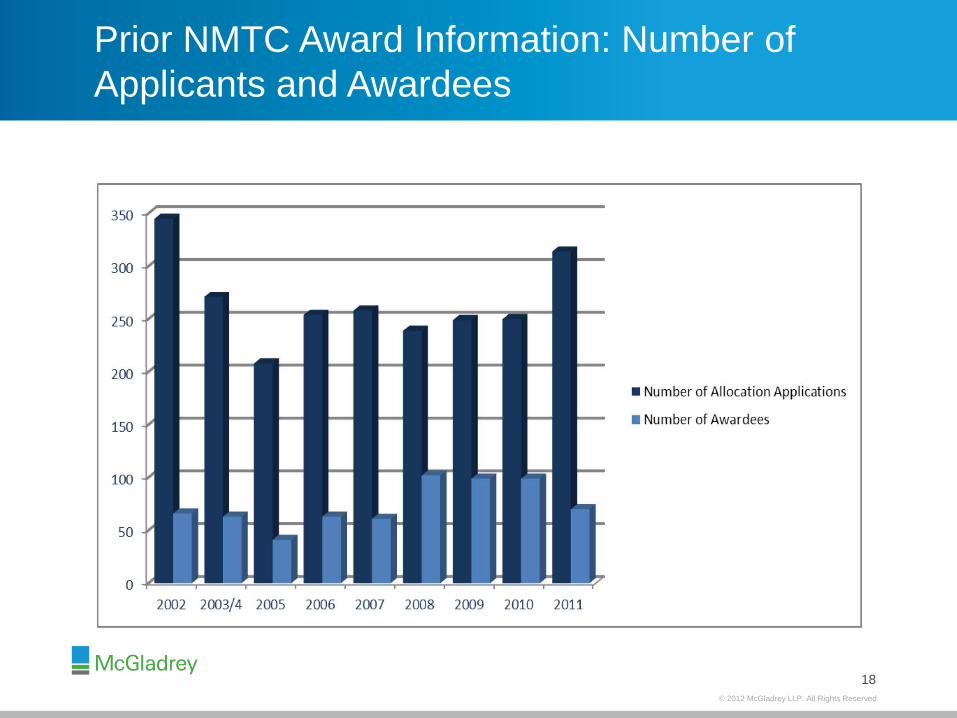

Prior NMTC Award Information: Number of

Applicants and Awardees

18

© 2012 McGladrey LLP. All Rights Reserved.

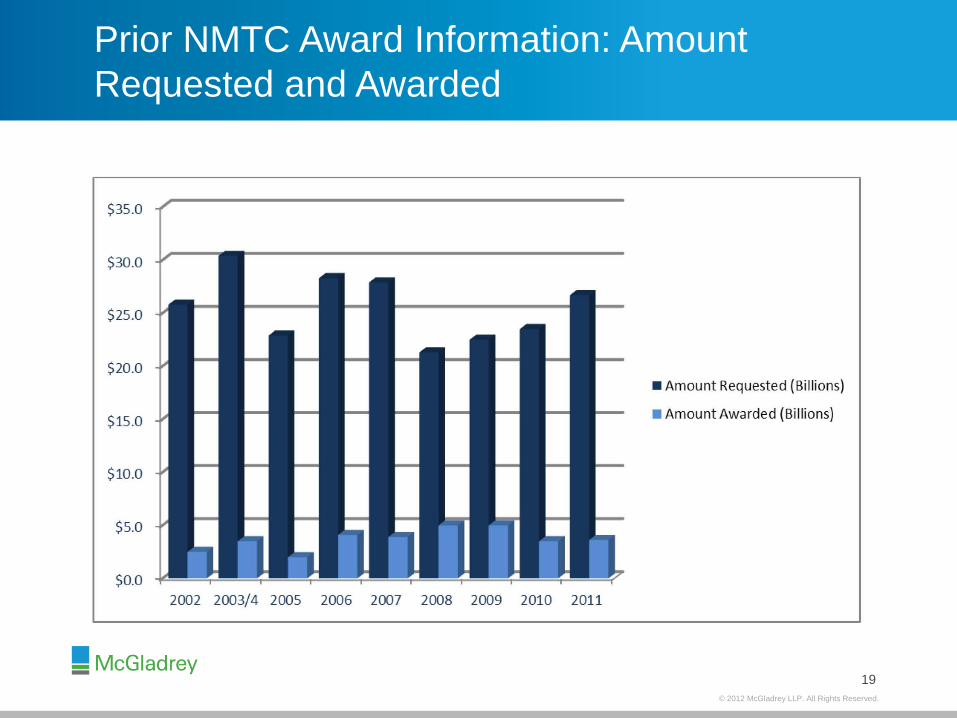

Prior NMTC Award Information: Amount

Requested and Awarded

19

© 2012 McGladrey LLP. All Rights Reserved.

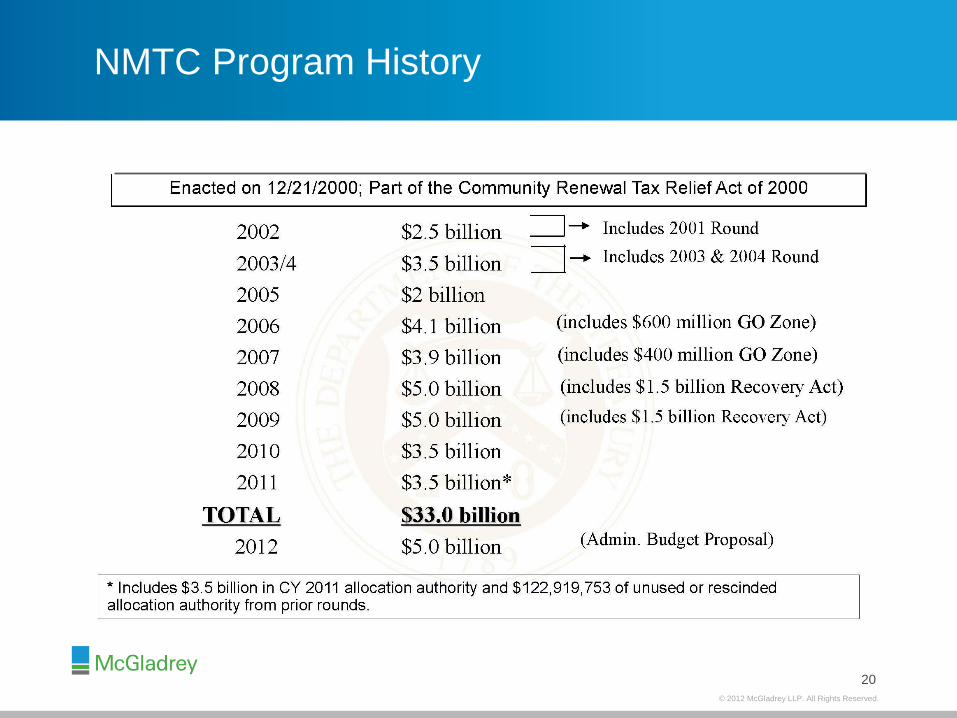

NMTC Program History

20

© 2012 McGladrey LLP. All Rights Reserved.

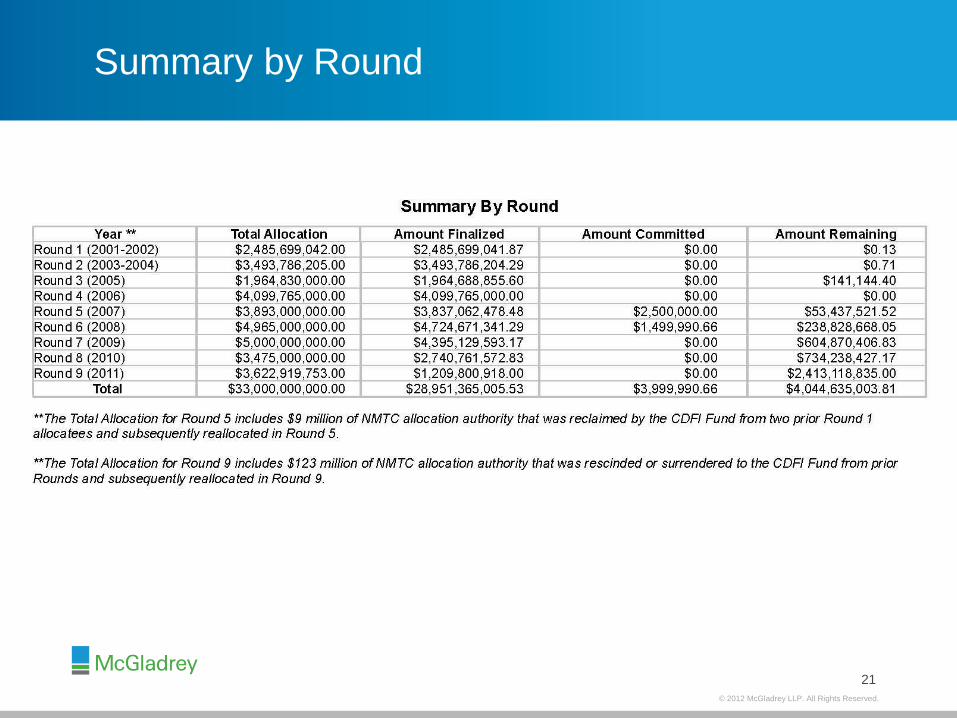

Summary by Round

21

© 2012 McGladrey LLP. All Rights Reserved.

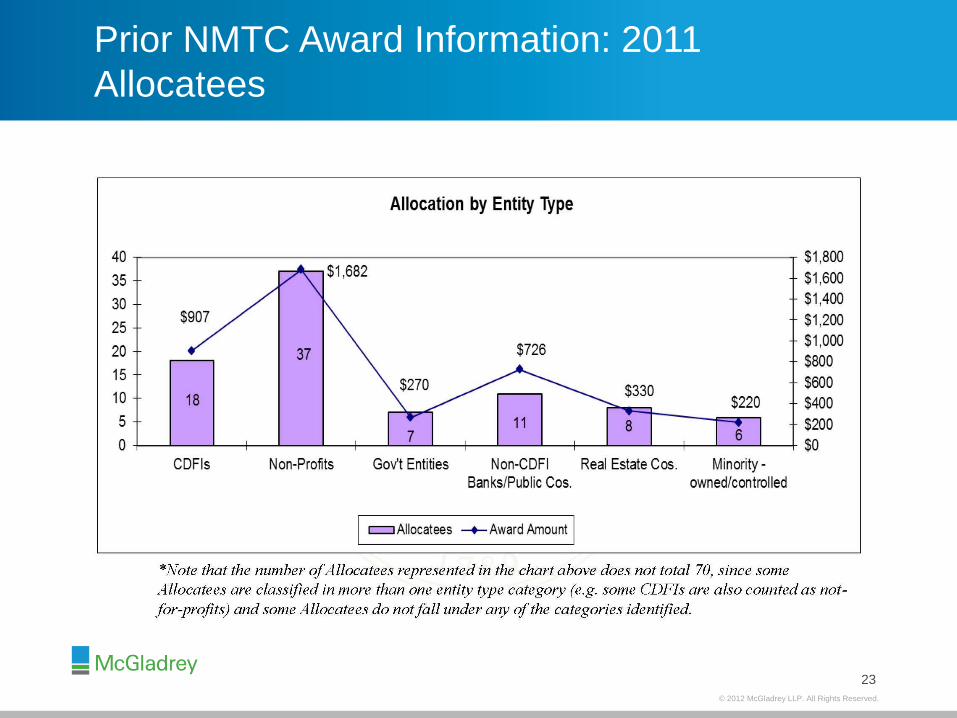

Prior NMTC Award Information: 2011

Allocatees

All 70 of the Allocatees committed to offering preferential rates and terms

All 70 of the Allocatees indicated that 100 percent of their investment dollars would be made either in the form of equity, equity-equivalent or debt financing that is at least 50 percent below market and/or is characterized by at least five concessionary features

All 70 of the Allocatees committed to providing at least 75 percent of their investments in areas characterized by: 1) multiple indicia of distress; 2) significantly greater indicia of distress than required by NMTC Program rules; or 3) high unemployment rates

All 70 Allocatees indicated that they would invest at least 95 percent of QEI proceeds in QLICIs - In real dollars, this means at least $466 million above and beyond

what is minimally required by the NMTC Program will be invested in LICs

22

© 2012 McGladrey LLP. All Rights Reserved.

Prior NMTC Award Information: 2011

Allocatees

23

© 2012 McGladrey LLP. All Rights Reserved.

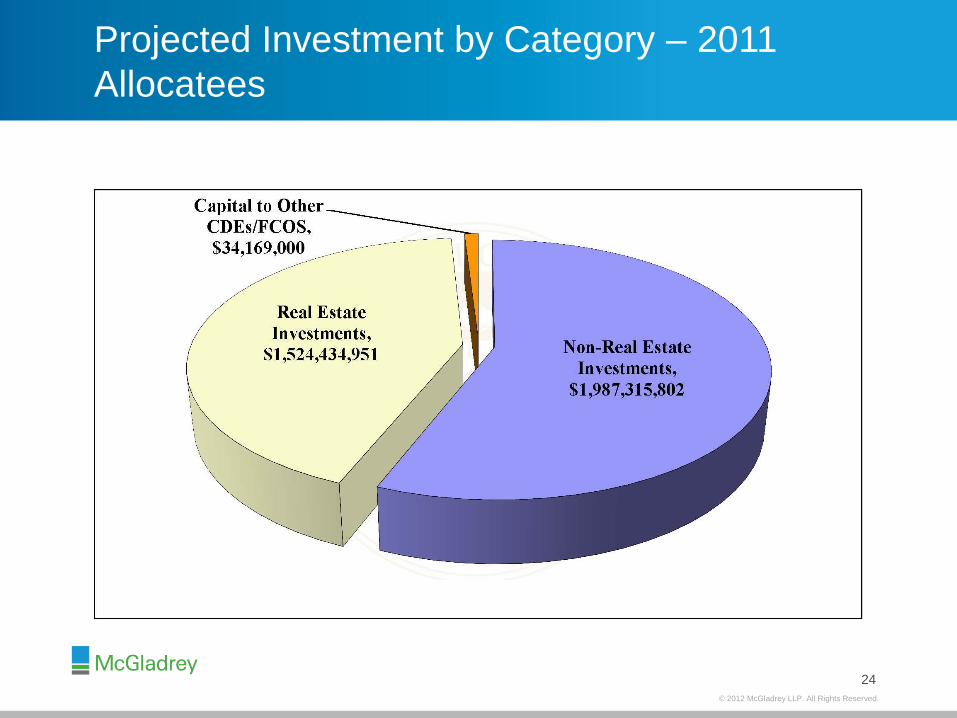

Projected Investment by Category – 2011

Allocatees

24

© 2012 McGladrey LLP. All Rights Reserved.

NMTCs: How Do They Work and What are the

Benefits?

Credit allowance period of 7 years

- The NMTCs are claimed on the date of the investor(s)

qualifying equity investment and the following six

anniversary dates

Basis reduction

- The investor is required to reduce its tax basis in its

qualifying equity investment by the amount of the NMTCs

claimed on each credit allowance date

NMTC can only be used to offset regular tax liability

(unlike LIHTC and HTC)

Unused NMTCs can be carried back 1 year and

forward 20 years

25

© 2012 McGladrey LLP. All Rights Reserved.

NMTCs: How Do They Work and What are the

Benefits?

Definitions of NMTC terms

- Community Development Entity

• Entity certified by the CDFI Fund which has a PRIMARY mission of community development serving low income communities

• Is a domestic corporation or partnership that is a required intermediary vehicle in NMTC structures

• CDEs apply for NMTC allocations through an annual competitive application process

• Maintains accountability to residents of the low income communities it serves

• Certification does not constitute an opinion by the CDFI Fund as to the effectiveness or financial viability of the CDE

26

© 2012 McGladrey LLP. All Rights Reserved.

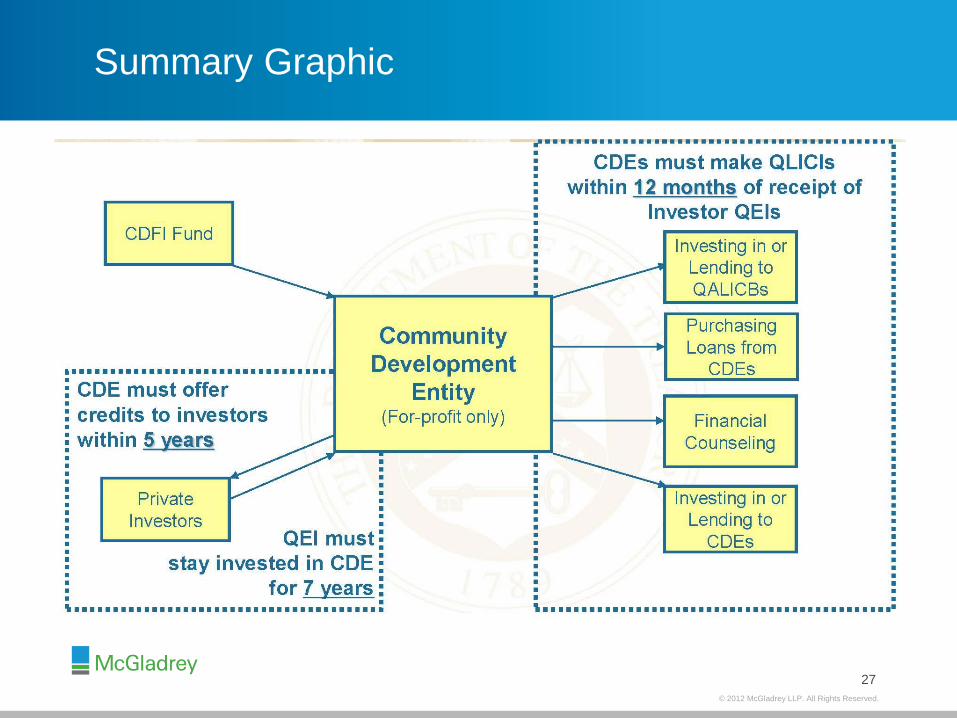

Summary Graphic

27

© 2012 McGladrey LLP. All Rights Reserved.

NMTCs: How Do They Work and What are the

Benefits?

Definitions of NMTC terms (cont.)

- Qualified Low Income Community Investment

• Any capital or equity investment in, or loan to, any

QALICB in a Low Income Community;

• The purchase from another CDE of any loan made by

such entity, if the loan is a QLICI;

• Financial counseling and other services (i.e., advice

regarding organization and operation) to businesses

located in, and residents of, low income communities;

• Any equity investment in, or loan to, any CDE

28

© 2012 McGladrey LLP. All Rights Reserved.

NMTCs: How Do They Work and What are the

Benefits?

Definitions of NMTC terms (cont.)

- Low Income Communities are census tracts where:

• Poverty rate exceeds 20% or

• Median income is below 80% of the greater of:

- Statewide median income, or

- Metropolitan area median income

• www.cdfifund.gov

29

© 2012 McGladrey LLP. All Rights Reserved.

NMTCs: How Do They Work and What are the

Benefits?

- Qualified Active Low Income Community Business

• Can be rental real estate, but cannot be 80% or more

residential and generally lessees cannot be involved

in a Precluded Business

• Excluded businesses:

- A business which develops or holds intangibles

for sale or license

- A business which operates a country club, golf

course, massage parlor, hot tub facility, suntan

facility, racetrack or other gambling facility or

liquor store (“Precluded Businesses”)

- Certain farming businesses

30

© 2012 McGladrey LLP. All Rights Reserved.

NMTCs: How Do They Work and What are the

Benefits?

- Qualified Active Low Income Community Business

(Continued)

• Compliance tests to be met:

- Must earn 50% of its gross income within a LIC;

- Must have 40% of its tangible assets within a LIC;

- Must have 40% of its employees providing service

within a LIC (or have 85% of its tangible assets

within a LIC if the entity does not have

employees);

- Exception: Gross income test is deemed satisfied

if the business meets either of tangible property

test or services test, applying 50% instead of 40%

31

© 2012 McGladrey LLP. All Rights Reserved.

NMTCs: How Do They Work and What are the

Benefits?

Less than 5% of the average of the aggregate

unadjusted basis of the property is attributable to

collectibles (e.g., art and antiques), other than those

held for sale in the ordinary course of business

(e.g., inventory); and

Less than 5% of the average of the aggregate

unadjusted bases of the property is attributable to

non-qualified financial property (e.g., debt

instruments with a term in excess of 18 months)

32

© 2012 McGladrey LLP. All Rights Reserved.

QALICB Examples

An operating business located in a LIC

A business that develops or rehabilitates

commercial, industrial, retail and mixed-use real

estate projects in a LIC

A business that develops or rehabilitates

community facilities, such as charter schools or

health care centers, in a LIC

A business that develops or rehabilitates for-sale

housing units located in LICs

33

© 2012 McGladrey LLP. All Rights Reserved.

Examples of NMTC Utilization

Real estate developers to close the funding gap in real estate projects (commercial, mixed-use, or community facilities)

Operating businesses for the purpose of the acquisition or the rehabilitation (including expansion) of facilities - Owner-occupied retail facilities

- Industrial or manufacturing facilities

- Warehouses and storage facilities

- Community facilities

Operating businesses for the purpose of expanding operations - Equity investments

- Fixed asset loans (equipment, furniture, machinery)

- Working capital loans to cover operating expenses

Additional ways to boost the benefit - Can be “twinned” with certain other tax credit equity (i.e. HTCs)

- Certain states have comparable NMTCs and HTCs creating additional equity for projects

34

© 2012 McGladrey LLP. All Rights Reserved.

NMTCs: How Do They Work and What are the

Benefits?

NMTC Structures

- Leveraged and non-leveraged structures

• Non-leveraged structure typically provides a low

interest rate loan that is required to be repaid after the

7 year compliance period.

• Leveraged structure is much more complex but

generates more bang for the buck. The leveraged

structure typically results in a forgivable loan and

equity through a put/call at the end of the compliance

period to buy out the tax credit investor.

• For both structures, interest only payments on QLICI

loans are typical to mitigate tax credit recapture risk.

35

© 2012 McGladrey LLP. All Rights Reserved.

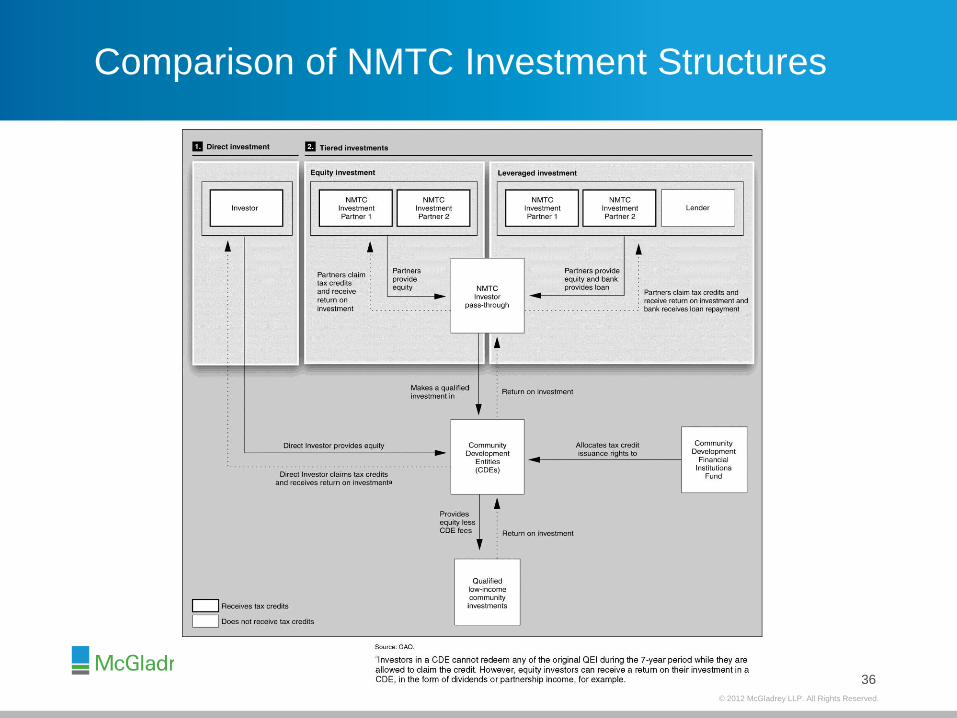

Comparison of NMTC Investment Structures

36

© 2012 McGladrey LLP. All Rights Reserved.

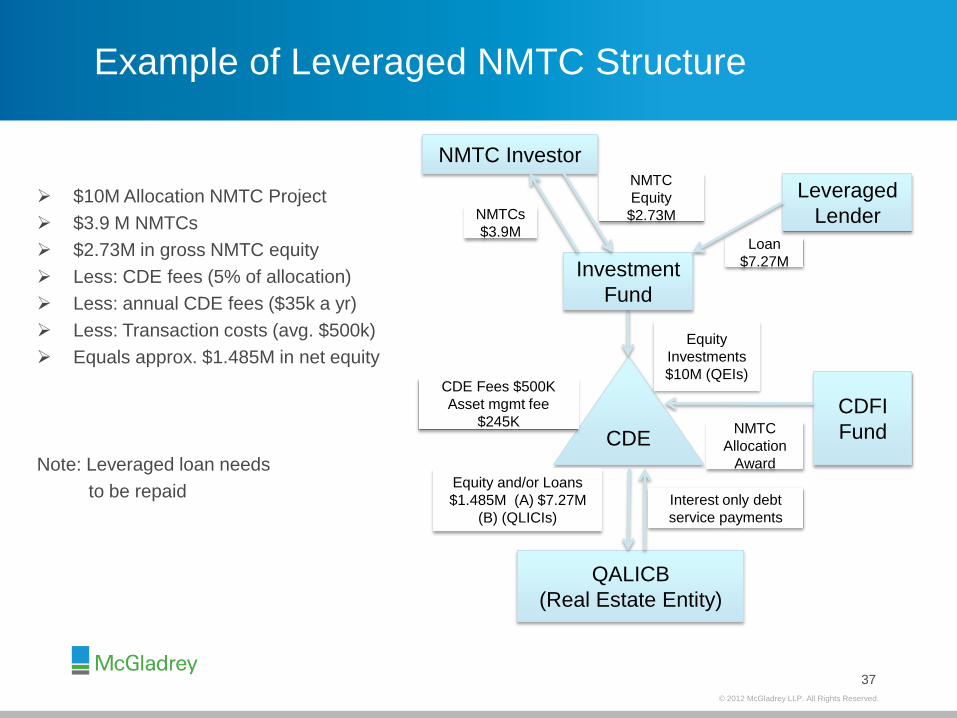

Example of Leveraged NMTC Structure

$10M Allocation NMTC Project

$3.9 M NMTCs

$2.73M in gross NMTC equity

Less: CDE fees (5% of allocation)

Less: annual CDE fees ($35k a yr)

Less: Transaction costs (avg. $500k)

Equals approx. $1.485M in net equity

Note: Leveraged loan needs

to be repaid

37

NMTC Investor

CDE

QALICB

(Real Estate Entity)

CDFI

Fund

Leveraged

Lender

Equity

Investments

$10M (QEIs)

NMTCs

$3.9M

NMTC

Allocation

Award

Equity and/or Loans

$1.485M (A) $7.27M

(B) (QLICIs)

Investment

Fund

NMTC

Equity

$2.73M

Loan

$7.27M

CDE Fees $500K

Asset mgmt fee

$245K

Interest only debt

service payments

© 2012 McGladrey LLP. All Rights Reserved.

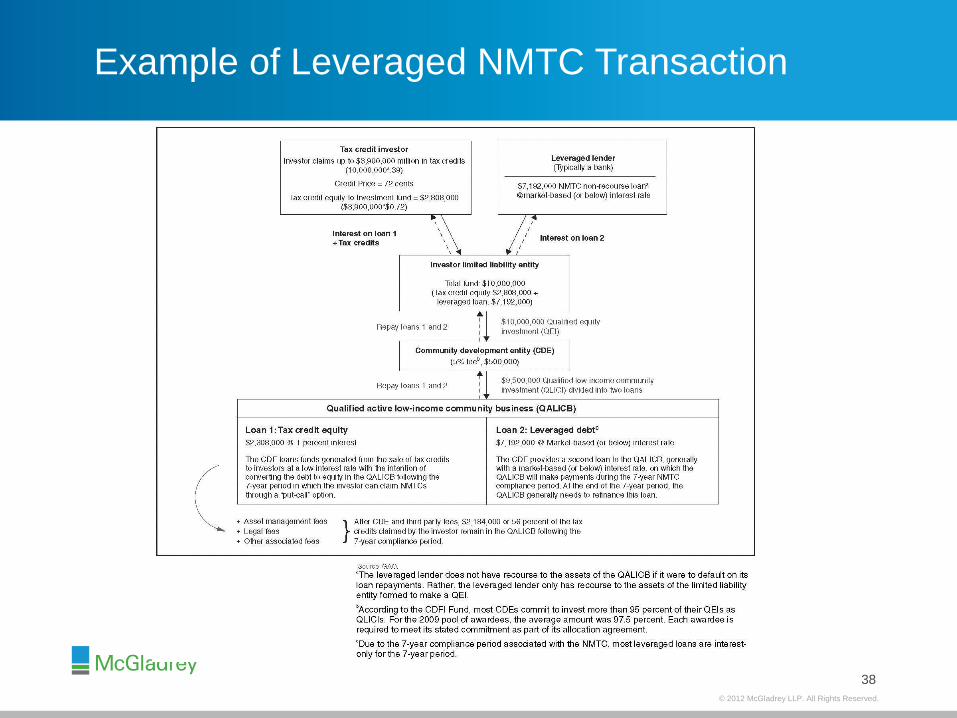

Example of Leveraged NMTC Transaction

38

© 2012 McGladrey LLP. All Rights Reserved.

Example of Leveraged NMTC Transaction

Exiting the Structure Through Put-Call Mechanism

- QALICB “or it’s designee” tax liability

- Cancellation of Debt (COD) income

39

© 2012 McGladrey LLP. All Rights Reserved.

What are the Obstacles in Utilizing NMTCs?

Finding a leveraged lender

Getting a CDE to commit a NMTC allocation

(chicken before the egg concept)

Costly and lengthy timeframe to close a transaction

Having to maintain the NMTC structure for the 7

year compliance period

40

© 2012 McGladrey LLP. All Rights Reserved.

NMTCs: How Do They Work and What are the

Benefits?

Recapture

- Subject to 100% recapture for 7 years for each QEI is

made in CDE (7 year compliance period)

- 3 ways to trigger recapture:

• CDE ceases to be a certified CDE; or

• CDE fails to continuously invest substantially all (85%)

of its QEIs in QLICIs; or

• CDE redeems investor’s equity investment (though a

CDE is allowed to distribute operating income)

* It is not an event of recapture if a CDE files for bankruptcy.

An investor may continue to claim NMTCs

41

© 2012 McGladrey LLP. All Rights Reserved.

NMTCs: How Do They Work and What are the

Benefits?

“Substantially all” of the QEI proceeds must be

invested in QLICIs within 12 months

- Years 1-6: Substantially All = 85% of amount paid by

investor at original issue. Generally, returns of equity,

capital or principal must be reinvested within 12 months.

- Year 7: Substantially All = 75%. Reinvestment is not

required in the final year of the 7-year credit period.

* At all times, 5% of the original QEI issue amount may be used

for certain reserves by the CDE and count towards meeting

the substantially-all requirement

42

© 2012 McGladrey LLP. All Rights Reserved.

NMTCs: How Do They Work and What are the

Benefits?

Recapture cure period (6 months) for failing to

satisfy the sub-all test

- 6 months AFTER the date the CDE becomes aware (or

reasonably should have became aware) of the failure

- Only ONE correction is permitted for each QEI during the

7 year credit period

43

© 2012 McGladrey LLP. All Rights Reserved.

Challenges of Troubled QLICI Loans

Restructuring vs. foreclosure

Taking title to collateral

Re-investment of QLICI proceeds

44

© 2012 McGladrey LLP. All Rights Reserved.

Tax Issues with Insolvent or Bankrupt

QALICBs

OID and CDE distributions

Basis reduction for worthless QLICI

Constructive liquidation

45

© 2012 McGladrey LLP. All Rights Reserved.

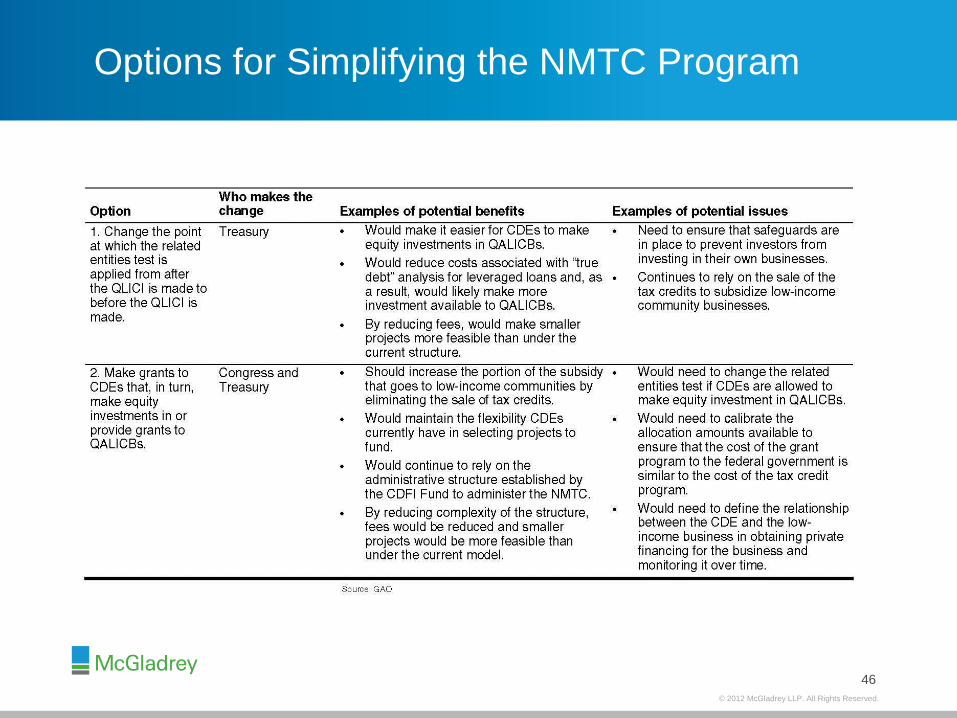

Options for Simplifying the NMTC Program

46

© 2012 McGladrey LLP. All Rights Reserved.

Federal Rehabilitation Tax Credit

Overview

- How the credit works

- What the credit is worth

- Other considerations

47

© 2012 McGladrey LLP. All Rights Reserved.

Federal Rehabilitation Tax Credit

How the Credit Works

Types

- Rehab of nonresidential structure placed in service before

1936 - 10%

- Rehab of certified historic structures regardless of use and

age - 20%

• Structure listed individually or in historic district

• Rehab certified by Secretary of Interior

48

© 2012 McGladrey LLP. All Rights Reserved.

Federal Rehabilitation Tax Credit

How the Credit Works

Tax implications

- Property must be a building

- Property cannot be a personal residence

- Depreciable base reduced by credit

- Recapture for early disposal (compliance period)

• Five-year holding period

• 20% of credit earned for every full 12 months held

past date taken

49

© 2012 McGladrey LLP. All Rights Reserved.

Federal Rehabilitation Tax Credit

How the Credit Works

Tax implications (cont.)

- At risk rules

• Do not apply if widely held C corp. investor

• Property cannot be financed by person related to

buyer of property

• Non-recourse financing cannot exceed 80% of credit

base

- Alternative minimum tax limits amount of credit allowed to

be used for credits incurred prior to 2008

- Unused credits can be carried back 1 year and forward for

20 years

- Credits are allocated based on profit percentage

50

© 2012 McGladrey LLP. All Rights Reserved.

Federal Rehabilitation Tax Credit

How the Credit Works

Credit base

- Substantial rehabilitation required

• At least $5,000 and exceed adjusted basis of property

• Adjusted basis is acquisition cost or book value

excluding land

- Measurement period

• Generally 2-year period commencing in year of rehab

start and ending at end of tax year of 2-year period

(period can be more than 24 months)

• Optional 5-year period if project divisible and written

plan and specifications prepared

51

© 2012 McGladrey LLP. All Rights Reserved.

Federal Rehabilitation Tax Credit

How the Credit Works

Credit base (cont.) - Qualified rehab expenditures (QRE)

• Most are costs related to direct construction (plumbing, electrical, HVAC, tenant finishes paid by landlord, etc.)

• Cost of enlarging, parking and site improvements excluded, with some limited exception

• Many soft costs included

- Regulatory - construction period interest and real estate taxes

- Related to construction (architect, engineering, legal, accounting, etc.)

52

© 2012 McGladrey LLP. All Rights Reserved.

Federal Rehabilitation Tax Credit

How the Credit Works

Tenant rehab expenditures

- Lease term at time of completion must exceed applicable

recovery period

• 27 ½ years for residential

• 39 years for nonresidential

- Excludes renewal options

Landlord rehab expenditure pass thru to tenant

- Lease must exceed 80% of applicable recovery period

- Tenant records credit as income proportionately over

recovery period

53

© 2012 McGladrey LLP. All Rights Reserved.

Federal Rehabilitation Tax Credit

What the Credit is Worth

Ownership structure

- Limited partnership

• Developer/owner/contractor/non-profit as general

partner, usually in corporate form

• Investor(s) as limited partner(s)

• Control to general partner with minimal ownership

- Limited liability company

• Similar structure as limited partnership except

partners are called members

• No need for corporate member due to liability shield

• Employment tax issue

54

© 2012 McGladrey LLP. All Rights Reserved.

Federal Rehabilitation Tax Credit

What the Credit is Worth

Valuation dependent on structure, pay-in, limited

partner holding period and expected rate of return

- Direct Investment - .85 to .92

- Lease pass thru - .95 to 1.40

55

© 2012 McGladrey LLP. All Rights Reserved.

Federal Rehabilitation Tax Credit

What the Credit is Worth

Investor candidates

- Investment funds/syndicators

- Local financial institutions with unfulfilled community

reinvestment requirements

- Profitable locally-based national company

- Most local companies are not profitable enough to

overcome alternate minimum tax limitations

- Large national companies

56

© 2012 McGladrey LLP. All Rights Reserved.

Federal Rehabilitation Tax Credit

Other Considerations

Tax exempt tenants

- Cannot participate in financing

- Cannot have purchase option for a fixed sum

- Cannot have used property prior to this lease

- Lease cannot exceed 20 year

57

© 2012 McGladrey LLP. All Rights Reserved.

Federal Rehabilitation Tax Credit

Other Considerations

New Market Tax Credit

- Leverage historic equity with NMTC

- CDE credit allocation

Financing

- First mortgage

- Bridge loans

58

© 2012 McGladrey LLP. All Rights Reserved.

Questions

© 2012 McGladrey LLP. All Rights Reserved.

Contact Us

James Beal

- Phone – 515.282-9287

- E-mail – [email protected]

Ron Copher

- Phone – 406.751.7706

- E-mail – [email protected]

Douglas P. Koch

- Phone – 617.241.1173

- E-mail – [email protected]

60

© 2012 McGladrey LLP. All Rights Reserved.

Disclaimer

The information contained herein is general in nature and based on

authorities that are subject to change. McGladrey LLP guarantees neither the

accuracy nor completeness of any information and is not responsible for any

errors or omissions, or for results obtained by others as a result of reliance

upon such information. McGladrey LLP assumes no obligation to inform the

reader of any changes in tax laws or other factors that could affect information

contained herein. This publication does not, and is not intended to, provide

legal, tax or accounting advice, and readers should consult their tax advisors

concerning the application of tax laws to their particular situations.

Circular 230 Disclosure

This analysis is not tax advice and is not intended or written to be used, and

cannot be used, for purposes of avoiding tax penalties that may be imposed

on any taxpayer.

McGladrey LLP is the U.S. member of the RSM International (“RSMI”)

network of independent accounting, tax and consulting firms. The member

firms of RSMI collaborate to provide services to global clients, but are

separate and distinct legal entities which cannot obligate each other. Each

member firm is responsible only for its own acts and omissions, and not those

of any other party.

McGladrey, the McGladrey signature, The McGladrey Classic logo, The

power of being understood, Power comes from being understood and

Experience the power of being understood are trademarks of McGladrey LLP.

© 2012 McGladrey LLP. All Rights Reserved.

McGladrey LLP

www.mcgladrey.com