Embed Size (px)

Citation preview

Columbia University Department of Industrial Engineering & Operations Research

Certified Portfolio Manager (CPM®) Program

1

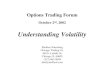

Day I: Monday June 2, 2014

Time Activity Presenter(s) Location

8:00 – 8:25AM Breakfast & Check-in Davis

Auditorium

8:25 – 8:40AM Welcome Address

S. Kachani, G.

Iyengar, E.

Derman, J. Mak,

M. Ross

Davis

Auditorium

8:40 – 9:00AM Overview of Program and Logistics S. Kachani, G.

Iyengar, M.

Haugh

Davis

Auditorium

9:15 – 10:45AM

I.1 Option Theory & Practice, Part I David DeRosa 501 NWC

10:45 – 11:00AM Break

11:00 – 12:30PM

I.2 Option Theory & Practice, Part II

Tim Leung 501 NWC

12:30 – 2:00PM

I.3

Lunch & Key Note Speaker:

My Life as a Quant

Emanuel Derman Carleton Lounge

2:00 – 2:15PM Break

2:15 – 3:45PM

I.4 Risk Management, Part I

Martin Haugh 501 NWC

3:45 – 4:00PM Break

4:00 – 5:30PM

I.5 Risk Management, Part II

Martin Haugh 501 NWC

5:45 – 6:45PM Cocktail Reception Bistro Ten 18

6:45PM Dinner Bistro Ten 18

Bistro Ten 18

1018 Amsterdam Avenue (Corner of 110th

Street)

New York, NY 10025

212-662-7600

Columbia University Department of Industrial Engineering & Operations Research

Certified Portfolio Manager (CPM®) Program

2

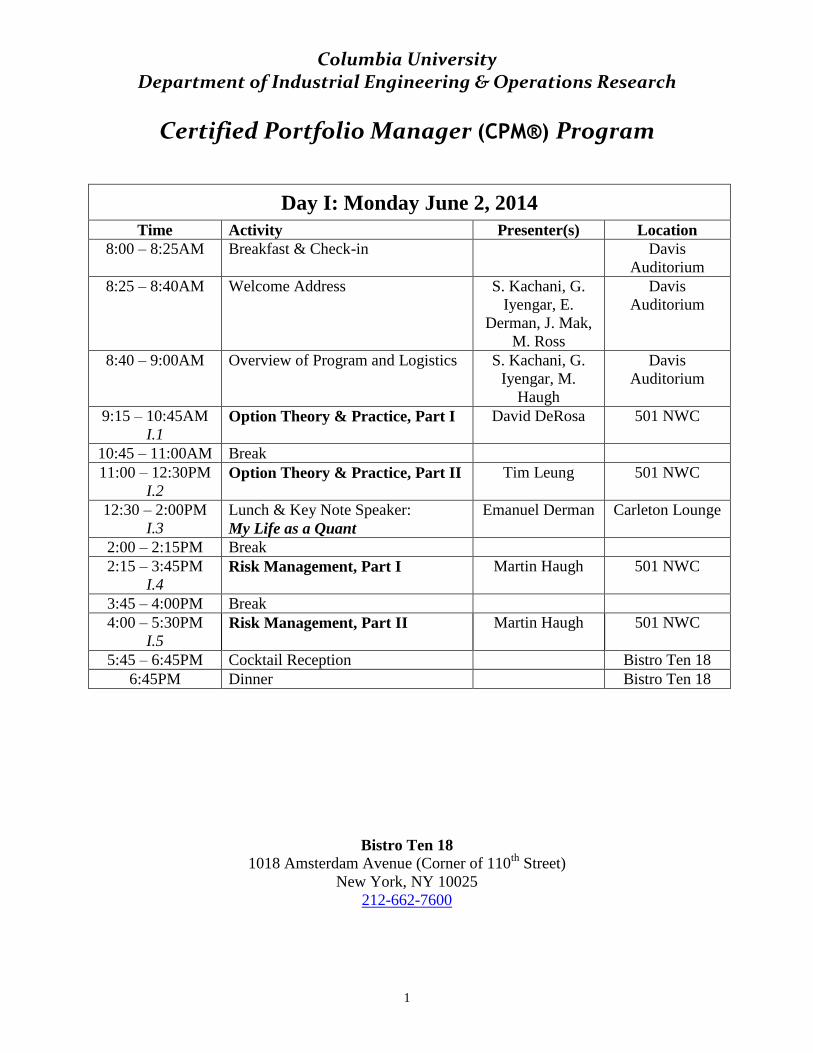

Day II: Tuesday June 3, 2014

Time Activity Presenter(s) Location

8:30 – 9:05AM Breakfast & Check-in Carleton Lounge

9:15 – 10:45AM

II.1 Asset Allocation, Part I

Garud Iyengar 501 NWC

10:45 – 11:00AM Break

11:00 – 12:30PM

II.2 Asset Allocation, Part II

Garud Iyengar

501 NWC

12:30 – 2:00PM

II.3

Lunch & Key Note Speaker:

Bringing back the Gold Standard

James Grant

Carleton Lounge

2:00 – 2:15PM Break

2:15 – 3:45PM

II.4 Fixed Income, Part I: Fixed-

Income Analysis & Derivatives

Martin Haugh 501 NWC

3:45 – 4:00PM Break

4:00 – 5:30PM

II.5 Equity Valuation in Today’s

Economy

Sid Dastidar 501 NWC

5:30 – 6:15PM Wine and Cheese Reception Carleton Lounge

6:15 – 7:00PM Columbia Campus Tour Soulaymane

Kachani, Darbi

Roberts

7:15PM Dinner LeMonde

Le Monde Restaurant

2885 Broadway (Between 112th

and 113th

Streets)

New York, NY 10027

(212) 531-3939

Columbia University Department of Industrial Engineering & Operations Research

Certified Portfolio Manager (CPM®) Program

3

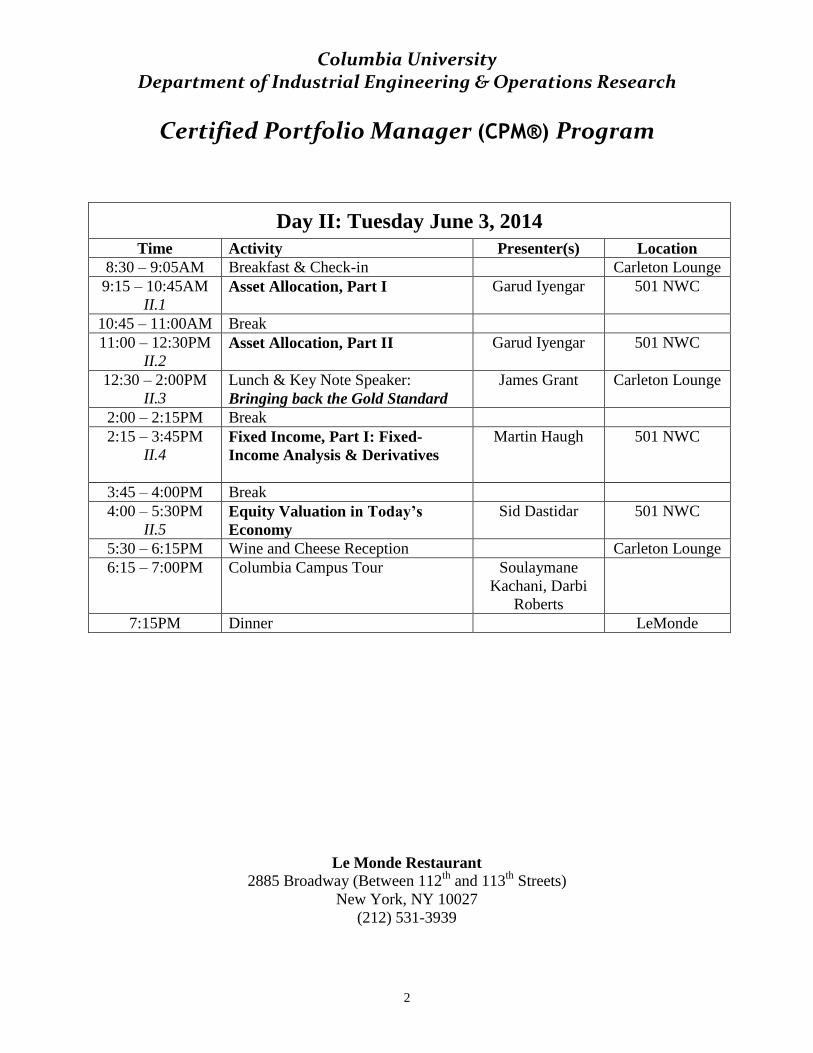

Day III: Wednesday June 4, 2014

Time Activity Presenter(s) Location

8:30 – 9:05AM Breakfast & Check-in Carleton Lounge

9:15 – 10:45AM

III.1 Fixed Income, Part II: Credit

Derivatives, Theory & Practice

Leon Tatevossian

501 NWC

10:45 – 11:00AM Break

11:00 – 12:30PM

III.2 Using Morningstar Tools to

Measure Risk in Mutual Fund

Portfolios

Shannon

Zimmerman

501 NWC

12:30 – 2:00PM

III.3

Lunch & Key Note Speaker:

Technical Analysis

Fred Meissner Carleton Lounge

2:00 – 2:15PM Break

2:15 – 3:45PM

III.4 Value Investing, Part I Tano Santos 501 NWC

3:45 – 4:00PM Break

4:00 – 5:30PM

III.5 Value Investing, Part II Tano Santos 501 NWC

5:30 – 6:30PM

III.6

Wine and Cheese Reception

Exam Review Session

Martin Haugh,

Garud Iyengar

Carleton Lounge

6:30PM Dinner Carleton Lounge

Dinner is catered by Kefi

Carleton Lounge

Columbia University

Columbia University Department of Industrial Engineering & Operations Research

Certified Portfolio Manager (CPM®) Program

4

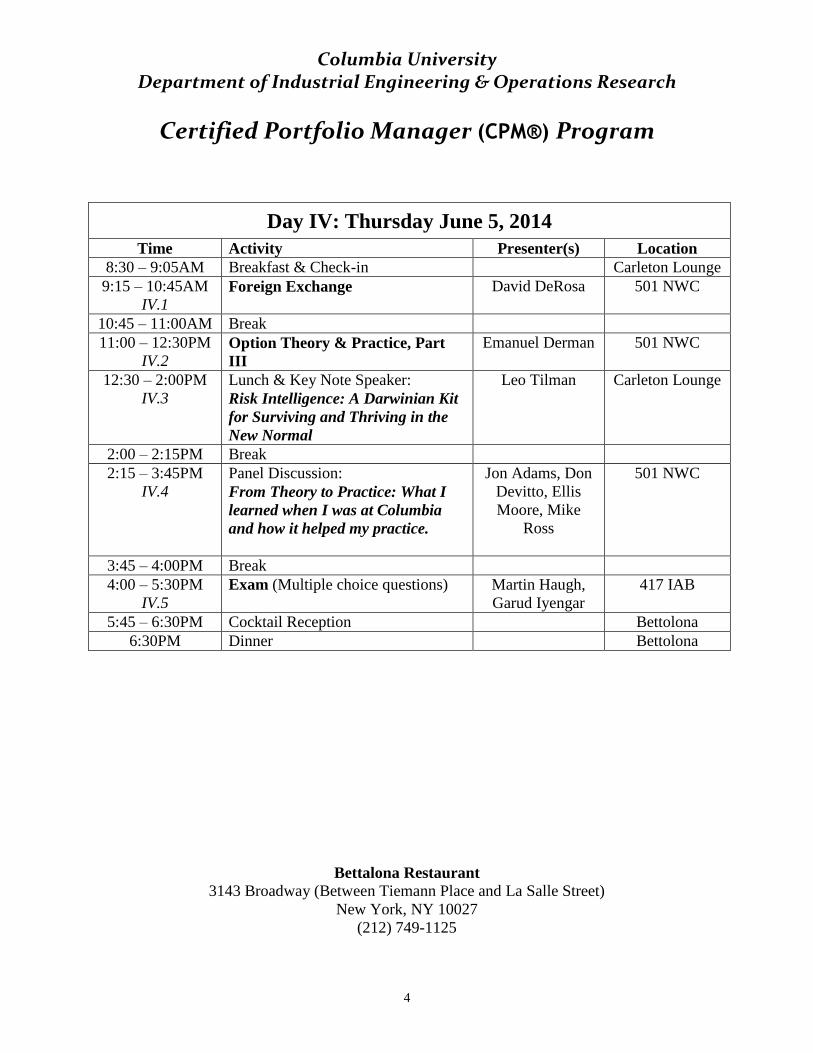

Day IV: Thursday June 5, 2014

Time Activity Presenter(s) Location

8:30 – 9:05AM Breakfast & Check-in Carleton Lounge

9:15 – 10:45AM

IV.1 Foreign Exchange

David DeRosa

501 NWC

10:45 – 11:00AM Break

11:00 – 12:30PM

IV.2 Option Theory & Practice, Part

III

Emanuel Derman 501 NWC

12:30 – 2:00PM

IV.3

Lunch & Key Note Speaker:

Risk Intelligence: A Darwinian Kit

for Surviving and Thriving in the

New Normal

Leo Tilman Carleton Lounge

2:00 – 2:15PM Break

2:15 – 3:45PM

IV.4

Panel Discussion:

From Theory to Practice: What I

learned when I was at Columbia

and how it helped my practice.

Jon Adams, Don

Devitto, Ellis

Moore, Mike

Ross

501 NWC

3:45 – 4:00PM Break

4:00 – 5:30PM

IV.5

Exam (Multiple choice questions) Martin Haugh,

Garud Iyengar

417 IAB

5:45 – 6:30PM Cocktail Reception Bettolona

6:30PM Dinner Bettolona

Bettalona Restaurant

3143 Broadway (Between Tiemann Place and La Salle Street)

New York, NY 10027

(212) 749-1125

Columbia University Department of Industrial Engineering & Operations Research

Certified Portfolio Manager (CPM®) Program

5

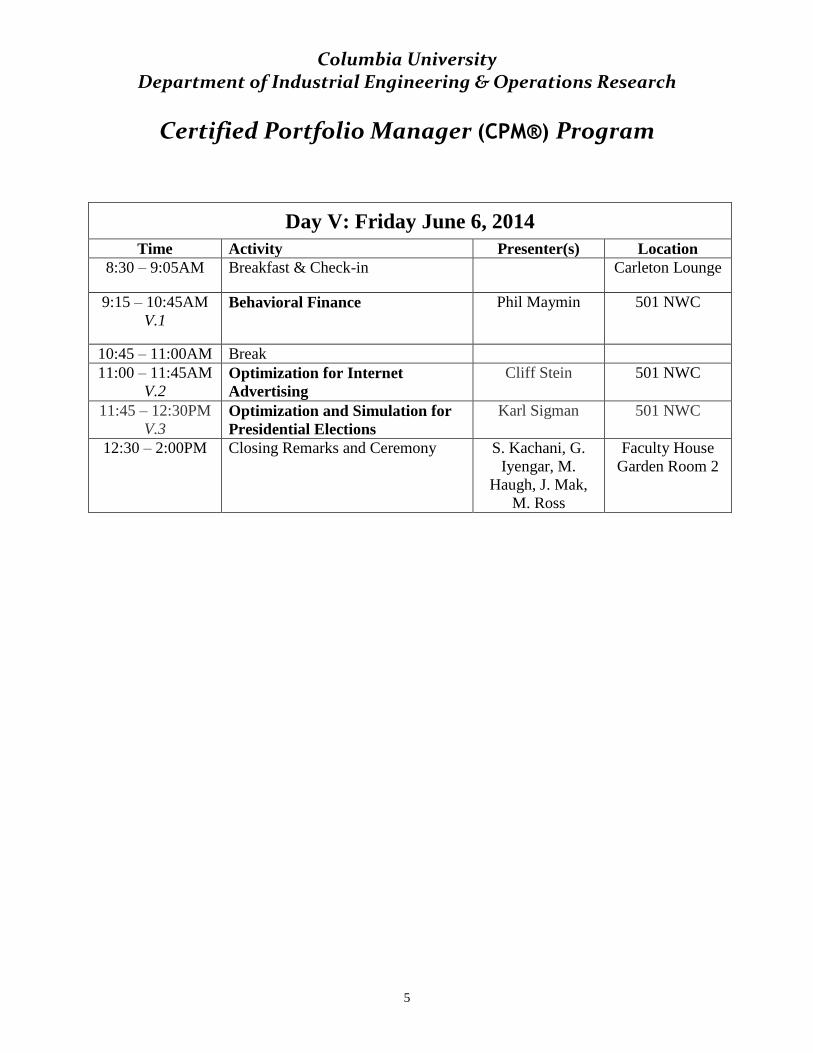

Day V: Friday June 6, 2014

Time Activity Presenter(s) Location

8:30 – 9:05AM Breakfast & Check-in Carleton Lounge

9:15 – 10:45AM

V.1 Behavioral Finance

Phil Maymin

501 NWC

10:45 – 11:00AM Break

11:00 – 11:45AM

V.2 Optimization for Internet

Advertising

Cliff Stein 501 NWC

11:45 – 12:30PM

V.3 Optimization and Simulation for

Presidential Elections

Karl Sigman 501 NWC

12:30 – 2:00PM

Closing Remarks and Ceremony S. Kachani, G.

Iyengar, M.

Haugh, J. Mak,

M. Ross

Faculty House

Garden Room 2

Columbia University Department of Industrial Engineering & Operations Research

Certified Portfolio Manager (CPM®) Program

6

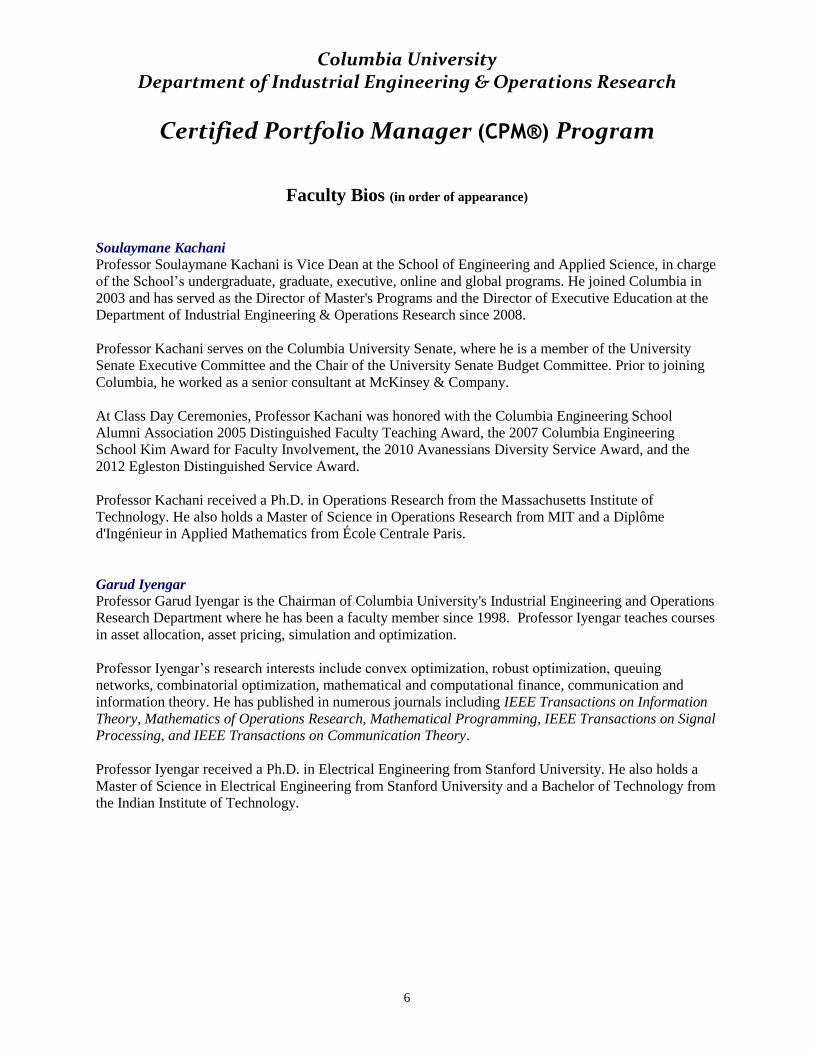

Faculty Bios (in order of appearance)

Soulaymane Kachani Professor Soulaymane Kachani is Vice Dean at the School of Engineering and Applied Science, in charge

of the School’s undergraduate, graduate, executive, online and global programs. He joined Columbia in

2003 and has served as the Director of Master's Programs and the Director of Executive Education at the

Department of Industrial Engineering & Operations Research since 2008.

Professor Kachani serves on the Columbia University Senate, where he is a member of the University

Senate Executive Committee and the Chair of the University Senate Budget Committee. Prior to joining

Columbia, he worked as a senior consultant at McKinsey & Company.

At Class Day Ceremonies, Professor Kachani was honored with the Columbia Engineering School

Alumni Association 2005 Distinguished Faculty Teaching Award, the 2007 Columbia Engineering

School Kim Award for Faculty Involvement, the 2010 Avanessians Diversity Service Award, and the

2012 Egleston Distinguished Service Award.

Professor Kachani received a Ph.D. in Operations Research from the Massachusetts Institute of

Technology. He also holds a Master of Science in Operations Research from MIT and a Diplôme

d'Ingénieur in Applied Mathematics from École Centrale Paris.

Garud Iyengar Professor Garud Iyengar is the Chairman of Columbia University's Industrial Engineering and Operations

Research Department where he has been a faculty member since 1998. Professor Iyengar teaches courses

in asset allocation, asset pricing, simulation and optimization.

Professor Iyengar’s research interests include convex optimization, robust optimization, queuing

networks, combinatorial optimization, mathematical and computational finance, communication and

information theory. He has published in numerous journals including IEEE Transactions on Information

Theory, Mathematics of Operations Research, Mathematical Programming, IEEE Transactions on Signal

Processing, and IEEE Transactions on Communication Theory.

Professor Iyengar received a Ph.D. in Electrical Engineering from Stanford University. He also holds a

Master of Science in Electrical Engineering from Stanford University and a Bachelor of Technology from

the Indian Institute of Technology.

Columbia University Department of Industrial Engineering & Operations Research

Certified Portfolio Manager (CPM®) Program

7

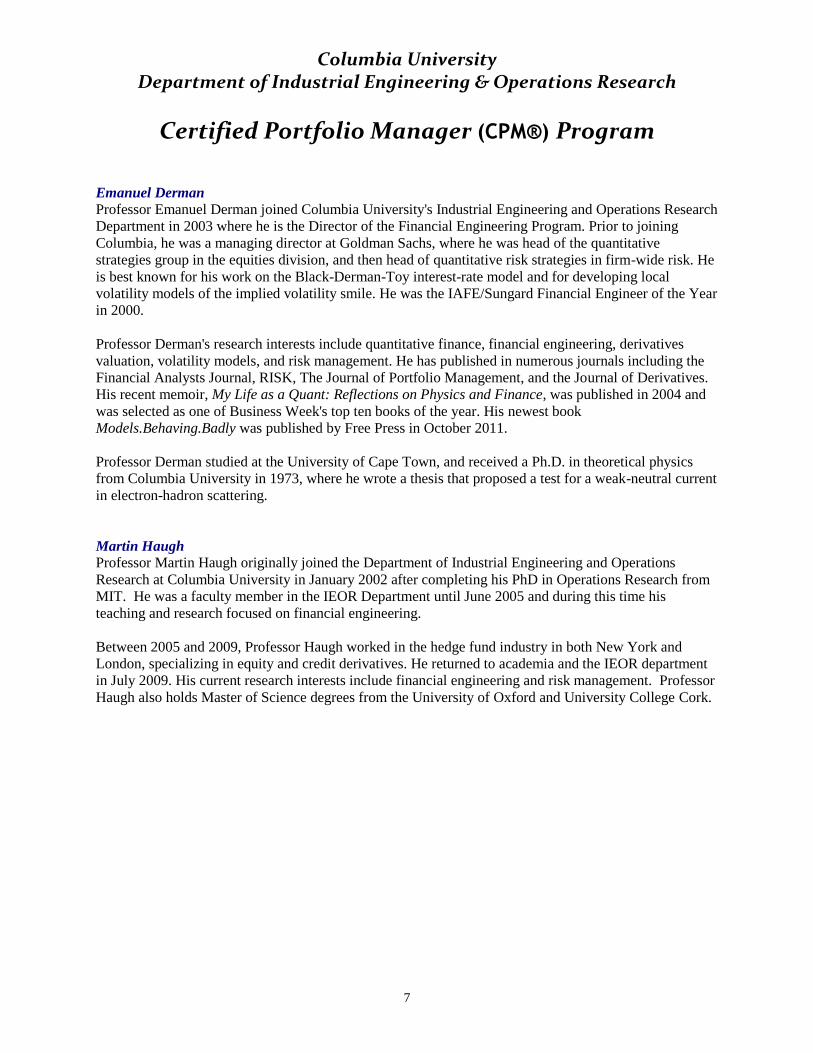

Emanuel Derman Professor Emanuel Derman joined Columbia University's Industrial Engineering and Operations Research

Department in 2003 where he is the Director of the Financial Engineering Program. Prior to joining

Columbia, he was a managing director at Goldman Sachs, where he was head of the quantitative

strategies group in the equities division, and then head of quantitative risk strategies in firm-wide risk. He

is best known for his work on the Black-Derman-Toy interest-rate model and for developing local

volatility models of the implied volatility smile. He was the IAFE/Sungard Financial Engineer of the Year

in 2000.

Professor Derman's research interests include quantitative finance, financial engineering, derivatives

valuation, volatility models, and risk management. He has published in numerous journals including the

Financial Analysts Journal, RISK, The Journal of Portfolio Management, and the Journal of Derivatives.

His recent memoir, My Life as a Quant: Reflections on Physics and Finance, was published in 2004 and

was selected as one of Business Week's top ten books of the year. His newest book

Models.Behaving.Badly was published by Free Press in October 2011.

Professor Derman studied at the University of Cape Town, and received a Ph.D. in theoretical physics

from Columbia University in 1973, where he wrote a thesis that proposed a test for a weak-neutral current

in electron-hadron scattering.

Martin Haugh Professor Martin Haugh originally joined the Department of Industrial Engineering and Operations

Research at Columbia University in January 2002 after completing his PhD in Operations Research from

MIT. He was a faculty member in the IEOR Department until June 2005 and during this time his

teaching and research focused on financial engineering.

Between 2005 and 2009, Professor Haugh worked in the hedge fund industry in both New York and

London, specializing in equity and credit derivatives. He returned to academia and the IEOR department

in July 2009. His current research interests include financial engineering and risk management. Professor

Haugh also holds Master of Science degrees from the University of Oxford and University College Cork.

Columbia University Department of Industrial Engineering & Operations Research

Certified Portfolio Manager (CPM®) Program

8

Jenny Mak Dr. Jenny Mak joined Columbia IEOR in 2003, providing leadership to the Department, specifically in

the areas of academic and faculty affairs, financial planning, alumni and employer relations, professional

development, executive education, and human resources. She teaches the IEOR professional development

courses and related workshops for Columbia Engineering.

Dr. Mak is a four time graduate of Columbia University. She received a Doctor of Education in adult

learning and leadership from Teachers College, Columbia University. She also holds a Master of Arts in

Higher and Postsecondary Education, Master of International Affairs, and Bachelor of Science in

Industrial Engineering from Columbia University. Her research interests include intellectual and ethical

development of college students, Asian student development, and adult learning. She conducts research in

and wrote her doctoral thesis investigating the intellectual and ethical development of graduate students

from mainland China.

Prior to joining Columbia, Dr. Mak served as a senior consultant in Deloitte Consulting. She also worked

at D. E. Shaw & Co. as a technology consultant.

Mike Ross A former captain in the U.S. Air Force and California native, Michael Ross takes a disciplined approach

to investing and managing client relationships. In his 25 years at Morgan Stanley Wealth Management

and its predecessors, he has worked with both individuals and institutions and garnered an array of

distinctions for his service to the industry.

Michael joined Smith Barney’s Portfolio Management Program in 1997 and earned his Certified

Investment Management Analyst® designation from the Wharton School of Business in 1999. Two years

later Citigroup Trust Company tapped him for the role of Fiduciary Portfolio Manager. His passion to

create custom portfolios, select securities and monitor performance spurred him to co-found the Portfolio

Management Institute (PMI), of which he is a past president. He is also co-founder of the Academy of

Certified Portfolio Managers and current President. He works extensively on portfolio management

topics with Columbia University. Michael’s outstanding performance has earned him a seat on the

Morgan Stanley Wealth Management President’s Council and the 2009 Bill Eager Award as Portfolio

Manager of the Year from the Portfolio Management Institute based on his dedication and commitment to

the client and passion for the markets. He is also a member of the Chartered Financial Analysts Institute

and the Investment Management Consultant Association.

While his distinctions are impressive, Michael’s clients report that it’s his personal attention and

determination to meet their financial goals that sets him apart. He traces his winning attitude back to his

high school football career, after which he was recruited to play for the U.S. Air Force Academy Falcons.

Michael holds a Bachelor of Science Degree from the U.S. Air Force Academy, Colorado Springs,

Colorado, and a Master of Arts Degree from State University of New York.

Columbia University Department of Industrial Engineering & Operations Research

Certified Portfolio Manager (CPM®) Program

9

David DeRosa David DeRosa is president of DeRosa Research and Trading, Inc. He is an Adjunct Associate Professor

of Finance at Columbia University’s Fu Foundation School of Engineering and Applied Science where he

teaches courses in financial modeling and derivatives. He has also served as an Adjunct Professor of

Finance and Fellow of the International Center for Finance at the Yale School of Management (1996-

2010). He received his Ph.D from the Graduate School of Business of the University of Chicago in

finance and economics and his A.B. in economics from the College of the University of Chicago.

David is the author of Options on Foreign Exchange, 3rd

edition (Wiley 2011), Central Banking and

Monetary Policy in Emerging Markets Nations (2009), In Defense of Free Capital Markets / The Case

Against A New International Financial Architecture (Bloomberg Press 2001), Managing Foreign

Exchange Risk (Irwin 1996), and is the editor of Currency Derivatives (Wiley 1998). He serves on the

boards of directors of Rubicon Fund Management, BlueCrest Capital International, the Children’s

Investment Fund, Pendragon Event Driven Fund, and GSA Capital Management.

Tim Leung Tim Leung joined Columbia University's IEOR Department in July 2011. He's also an affiliated faculty

member of The Center for Financial Engineering and Institute for Data Sciences & Engineering.

Previously, he had been an Assistant Professor of Applied Mathematics & Statistics at Johns Hopkins

University since September 2008. His research area is Financial Engineering, with focus on the valuation

and hedging of complex financial derivatives, such as employee stock options and exchange-traded fund

(ETF) options.

Professor Leung's research has been funded by the National Science Foundation (NSF), and published in

journals, such as Finance & Stochastics, Mathematical Finance, Quantitative Finance, and SIAM Journal

on Financial Mathematics. He has also given talks at numerous universities, conferences, investment

banks and hedge funds.

At Columbia University, Professor Leung teaches the core courses for the M.S. program in Financial

Engineering (MSFE), including IEOR E4706: Foundations of Financial Engineering and IEOR E4703:

Monte Carlo Simulation. He also teaches the MSFE elective IEOR E4710: Term Structure Models.

He received a B.S. in Operations Research & Industrial Engineering from Cornell University and a Ph.D.

in Operations Research & Financial Engineering from Princeton University, where he was awarded the

Charlotte Procter Honorific Fellowship. During 2003-2004, he was a consultant associate at Novantas, a

Manhattan-based management consulting firm.

James Grant James Grant, financial journalist and historian, is the founder and editor of Grant’s Interest Rate

Observer, a twice-monthly journal of the investment markets. Among his books is the newly published

Mr. Speaker! The Life and Times of Thomas B. Reed, the Man Who Broke the Filibuster (Simon &

Schuster). He is, in addition, the author of five books on finance and financial history: Bernard M.

Baruch: The Adventures of a Wall Street Legend (Simon & Schuster, 1983), Money of the Mind (Farrar,

Straus & Giroux, 1992), Minding Mr. Market (Farrar, Straus & Giroux, 1993) and The Trouble with

Prosperity (Times Books, 1996), and Mr. Market Miscalculates (Axios Press, 2008). His John Adams:

Columbia University Department of Industrial Engineering & Operations Research

Certified Portfolio Manager (CPM®) Program

10

Party of One, a biography of the second president of the United States was published in March 2005 by

Farrar, Straus & Giroux.

Mr. Grant’s television appearances include “60 Minutes,” “The Charley Rose Show,” “CBS Evening

News,” and a 10-year stint on Wall Street Week. His journalism has appeared in a variety of periodicals,

including the Financial Times, The Wall Street Journal and Foreign Affairs, and he contributed an essay

to the Sixth Edition of Graham and Dodd’s Security Analysis (McGraw-Hill, 2009). Mr. Grant, a former

Navy gunner’s mate, is a Phi Beta Kappa alumnus of Indiana University. He earned a master’s degree in

international relations from Columbia University and began his career in journalism in 1972, at the

Baltimore Sun. He joined the staff of Barron’s in 1975 where he originated the Current Yield column. He

and his wife, Patricia Kavanagh M.D., live in Brooklyn. They are the parents of four grown children.

Siddhartha Dastidar

Dr. Siddhartha Dastidar is an Adjunct Professor at the Department of Industrial Engineering & Operations

Research at Columbia University. He teaches courses on capital markets and investments and equity

valuation.

Dr. Dastidar has fifteen years of experience in the financial services industry, both buy-side and sell-side,

across asset classes and regions. As part of the Quantitative Portfolio Strategies team at Lehman and

Barclays, he has advised large institutional clients on portfolio construction, management and risk

budgeting issues. He was also the chief equity derivatives strategist at Newedge, owned by Societe

Generale. At present, he belongs to Brigade Capital, a USD 16 billion credit hedge fund, where he has

been responsible for coming up with portfolio construction, risk and quantitative frameworks. After his

MBA, he has also worked in emerging market private equity for 3 years.

Dr. Dastidar received a PhD in finance from Columbia Business School and holds the CFA charter. He

has published in top journals such as the Journal of Financial Economics and the Journal of Portfolio

Management, and has presented at the National Bureau of Economic Research.

Leon Tatevossian Leon Tatevossian is a senior risk manager at RBC Capital Markets, LLC, where he covers asset-backed

and commercial mortgage-backed securities. Leon is an associate in the Financial Engineering

Program at Columbia's IEOR Department and a fellow/adjunct instructor in the Mathematics in Finance

Program at NYU’s Courant Institute of Mathematical Sciences.

He has twenty-four years of experience in the fixed-income capital markets, including positions as a

trader, quantitative strategist, derivatives modeler, and market-risk analyst. Leon’s previous position was

as a principal/senior trader in an MBS/ABS proprietary-trading group at Banc of America Securities. His

product background also includes US Treasury securities, US agency securities, interest-rate derivatives,

and credit derivatives. Leon received an S.B. degree (mathematics) from MIT and was a graduate student

in mathematics (algebraic number theory) at Brown University.

Columbia University Department of Industrial Engineering & Operations Research

Certified Portfolio Manager (CPM®) Program

11

Shannon Zimmerman

Mr. Shannon Zimmerman is Associate Director of Active Funds Research for Morningstar. He covers the

Oakmark funds, John Hancock, and Legg Mason’s ClearBridge offerings, among others. He also serves

as director of training for fund research, responsible for overseeing the fund analyst training program and

coordinating efforts among Morningstar's U.S. and international analysts.

Fred Meissner

Fred Meissner, CMT is the founder and President of The FRED Report. His professional career spans 27

years in the investment business. He has a multifaceted background encompassing market analysis,

trading strategies/portfolio management and business development/relationship management in diverse

environments. He is known as a creative and intuitive thinker who leverages extensive knowledge of

financial markets and economic trends to consistently generate significant profits. A team builder and

leader who has a track record of successfully guiding groups towards organizational goals, Fred has high

multicultural awareness and knowledge of international business practices acquired through extensive

travel and education abroad.

Fred’s working career includes senior market analysis positions at The Robinson –Humphrey Company

(at the time, the largest regional brokerage in the United States), Merrill Lynch and Co., Inc. (at the time,

the largest national brokerage in the United States), and four years as President of the Market Technicians

Association (the largest association of professional technical analysts in the world). While President of

the MTA, that organization moved to a new structure encompassing the hiring of professional managers,

and successfully changed Sarbanes-Oxley to include the CMT (Chartered Market Technician) designation

as an exemption to the Series 86 requirement for financial analysts. This effectively placed the CMT on

par with the CFA (Chartered Financial Analyst), thus making Technical Market Analysis and traditional

Fundamental Analysis equal in the eyes of FINRA and in the securities laws of the United States of

America.

Fred holds a BS degree in Business Administration (with a minor in Economics) from Trinity University

in San Antonio, Texas, and an MA degree from The University of California, Los Angeles (UCLA) in

Latin American Studies encompassing an interdisciplinary curriculum of International Business, History,

and Sociology. Currently Fred publishes The FRED Report, a consulting service for financial advisors, as

well as speaking extensively on markets and market analysis around the world.

Tano Santos

Professor Tano Santos is the David L. and Elsie M. Dodd Professor of Finance at the Columbia Business

School, which he joined in 2003. He is the co-director, with Bruce Greenwald, of the Heilbrunn Center

for Graham and Dodd Investing. From 1996 to 2003 he was at the finance group of the Graduate School

of Business of the University of Chicago (now the University Of Chicago Booth School Of Business). He

is member of the National Bureau of Economic Research (NBER) and the Centre for Economic Policy

Research (CEPR) as well as of all the major professional organizations. Professor Santos obtained his

Ph.D. from the Department of Economics of the University of Chicago. His thesis was concerned with the

economic determinants of financial innovations as well as the effect that these have on the credit quality

of market participants and of pre-existing financial markets.

Columbia University Department of Industrial Engineering & Operations Research

Certified Portfolio Manager (CPM®) Program

12

Professor Santos’s research is divided in three areas. A first area of interest is concerned with the role of

financial intermediaries in markets. Specifically Professor Santos has studied whether intermediaries,

such as derivatives exchanges, competing for volume June drive the credit quality of market participants

below or above optimal levels and thus whether regulatory intervention is required to restore efficiency.

His recent work in this area focuses on the role of the private provision of liquidity in financial crisis and

the role and efficiency of the public provision of liquidity.

Professor Santos’s research extends also to the fields of asset pricing and organizational economics. His

work on asset pricing focuses on understanding the determinants of the value premium and its relation to

fundamental economic forces. Organizational economics is a recent addition to Professor Santos’s

research portfolio. Here the emphasis has been on the understanding of the determinants of specialization

in the organization of production when firms face standard trade-offs between adaptation and

coordination.

Leo Tilman

Leo M. Tilman is President of Tilman & Company, a strategic advisory firm that serves corporations,

financial institutions, governments, and institutional investors worldwide. Through thought leadership and

actionable solutions, Tilman & Company helps its clients create lasting value for the benefit of all

stakeholders. Prior to founding the firm, he held senior positions with BlackRock and Bear Stearns, where

he was Chief Institutional Strategist and Senior Managing Director.

Mr. Tilman teaches finance at Columbia University and is the author of three books translated into

foreign languages: Financial Darwinism (2009), Asset/Liability Management (2003), and Risk

Management (2000). In 2010, in collaboration with the Nobel economist Edmund Phelps, he co-authored

a Harvard Business Review proposal to create the First National Bank of Innovation – a novel financial

institution dedicated to financing innovative entrepreneurial projects and fostering economic dynamism.

In a 2012 European Financial Review article, he redefined risk intelligence and designated it a new

essential competence for companies and investors who aspire to contribute to economies and societies.

Mr. Tilman has been profiled as a Business Visionary by Forbes, a distinction given to “influential

authors, decision makers, and thought leaders in the field of business.” He is a contributing editor of The

Journal of Risk Finance and a Fellow of the Foreign Policy Association. Mr. Tilman serves on the board

of directors of Atlantic Partnership and advisory boards of the Center on Capitalism and Society at

Columbia University and British American Business. He was honored by the World Economic Forum

among a select group of executives, public figures and intellectuals recognized for “their professional

accomplishments, commitment to society and potential to contribute to shaping the future of the world.”

Mr. Tilman received B.A. and M.A. degrees in mathematics from Columbia University and executive

education in leadership and public policy from the Kennedy School of Government at Harvard

University.

Columbia University Department of Industrial Engineering & Operations Research

Certified Portfolio Manager (CPM®) Program

13

Jon Adams

A former business owner and a 28-year veteran of the financial services industry, Jon enjoys taking a

hands-on approach to meeting clients’ complex financial needs and long-term objectives. In serving high-

net-worth and ultra-high-net-worth clients, as a Certified Private Wealth Advisor® (awarded by the

Investment Management Consultants Association (IMCA®)), Jon is especially skilled at developing

disciplined and enduring strategies for asset accumulation, preservation and wealth transfer. He also

works closely with private foundations, trusts and endowments.

Jon came to Merrill Lynch in 1984 and has been recognized as a leader within the firm and the

community. His designations as a Certified Portfolio Manager and PIA Portfolio Manager enable him to

use his discretion in making timely investment decisions and adjustments for clients. Jon graduated from

Millersville University with a Bachelor of Science degree in Business Administration. He's a longtime

resident of the Linglestown area where Jon and his wife, Kelly, have three children and one grandchild.

Besides spending time with his family and being involved with his church, Jon stays quite active – with

martial arts, other fitness routines and riding his motorcycle.

Don DeVitto

Don DeVitto has been in the investment business since 1983. In 1996, he began managing equity

accounts on a discretionary basis and currently a Senior Portfolio Manager in the Portfolio Management

Program at UBS. During his career, he has witnessed many bull and bear markets in stocks and bonds.

More than anything else it is that experience which guides his day to day decision making. He

understands the importance of risk management and his goal is to preserve clients' hard earned money and

grow those assets in a prudent, disciplined manner.

Ellis Moore

Ellis is a founding member of The Westchester Group at Morgan Stanley Smith Barney. He is primarily

responsible for discretionary portfolio management and overall investment policy planning and research.

Ellis began his career in financial services in 1970 on the institutional corporate bond desk of Smith

Barney, a predecessor firm of Morgan Stanley Smith Barney’s. Prior to his 1981 decision to focus

exclusively on individual investors, Ellis served as an institutional corporate bond salesman and sales

coordinator and as head corporate bond trader at both Smith Barney and Shearson Hayden Stone,

predecessor firms of Morgan Stanley Smith Barney. He was the founder and first manager of Smith

Barney’s Corporate Bond Research Department and authored its weekly “Corporate Bond Comments” for

several years.

In 1990, Ellis joined the Portfolio Management Group and as of September 2010 managed or helped to

advise some $200 million of client assets for the Westchester Group. Ellis integrates financial planning

into his investment process to assist in setting risk tolerance and return targets for clients. He continues

his written client communications through a publication called “One Moore View.” Ellis was a founding

member of the board of the Portfolio Management Institute, a not-for profit association of Morgan

Stanley Smith Barney portfolio managers and served as its first secretary/treasurer from 2004-2010. He

was also a member of Morgan Stanley Smith Barney’s proxy voting committee for managed accounts.

During the 1970’s and 1980’s, Ellis became quite active in community service, first as a member of the

Board of Appeals and later its Chairman, and thereafter as a member of the Board of Trustees of the

Columbia University Department of Industrial Engineering & Operations Research

Certified Portfolio Manager (CPM®) Program

14

Village of Pelham Manor, NY, his home town. He was also President and a member of the Board of

Governors of the Shenorock Shore Club of Rye, NY. A Rotarian, Ellis was named a Paul Harris Fellow

and has served as President and on the Board of Directors of the Rotary Club of the Pelhams. He has been

an active member of the service organization since 1981 and currently chairs the club’s scholarship

committee.

A 1970 graduate of Princeton University, Ellis played varsity football for three years and captained the

university’s 1969 Ivy League Championship team. He is on the Board of Directors of the Ivy Football

Association and currently serves as an advisor to the Princeton Football Association. Ellis earned a

Bachelor of Arts degree in history. Ellis resides in Yorktown Heights, NY, and Raymond, ME, with his

wife, Marilyn. They have four children: Jon, also a member of the Westchester Group, Carrie, Michael

and Nikki; and three grandchildren, Leo, Maxwell and Nathan. In their leisure time, the Moore’s enjoy

reading, travel, and exercise.

Philip Maymin

Professor Philip Maymin is Assistant Professor of Finance and Risk Engineering at the NYU School of

Engineering. He is also the founding managing editor of Algorithmic Finance. He holds a Ph.D. in

Finance from the University of Chicago, a Master's in Applied Mathematics from Harvard University,

and a Bachelor's in Computer Science from Harvard University. He also holds a J.D. and is an attorney-

at-law admitted to practice in California.

Professor Maymin has been a portfolio manager at Long-Term Capital Management, Ellington

Management Group, and his own hedge fund, Maymin Capital Management. He has also been an award-

winning journalist, a policy scholar for a free market think tank, a Justice of the Peace, a Congressional

candidate, a columnist, and the author of several books. He was a finalist for the 2010 Bastiat Prize for

Online Journalism. He has also been a consultant for several NBA teams and is the co-founder and co-

editor-in-chief of the Journal of Sports Analytics. Professor Maymin’s popular writings have been published in dozens of media outlets ranging from

Bloomberg to Forbes to the New York Post to American Banker to regional newspapers, and his research

has been profiled in dozens more, including The New York Times, Wall Street Journal, USA

Today, Financial Times, Boston Globe, NPR, BBC, Guardian (UK), CNBC, Newsweek Poland, and

others. His research on behavioral and algorithmic finance has appeared in Quantitative Finance, Journal

of Wealth Management, Journal of Applied Finance, and Risk and Decision Analysis, among others, and

his textbook Financial Hacking was recently published by World Scientific.

Columbia University Department of Industrial Engineering & Operations Research

Certified Portfolio Manager (CPM®) Program

15

Cliff Stein Professor Clifford Stein he has been a faculty member since 2001 in the Department of Industrial

Engineering and Operations Research. He also holds an appointment as Professor of Computer Science at

Columbia. His research interests include the design and analysis of algorithms, combinatorial

optimization, operations research, network algorithms, scheduling, algorithm engineering and internet

algorithms. Prior to joining Columbia, he spent nine years as a professor in the Dartmouth College

Department of Computer Science.

Professor Stein has published over 60 scientific papers and occupied a variety of editorial positions

including the journals ACM Transactions on Algorithms, Mathematical Programming, Journal of

Algorithms, SIAM Journal on Discrete Mathematics and Operations Research Letters. He has been the

recipient of an NSF Career Award, an Alfred Sloan Research Fellowship and the Karen Wetterhahn

Award for Distinguished Creative or Scholarly Achievement. He is also the co-author of two textbooks,

Introduction to Algorithms, with T. Cormen, C. Leiserson and R. Rivest and Discrete Math for Computer

Science, with Ken Bogart and Scot Drysdale. Introduction to Algorithms is currently the best-selling

textbook in algorithms and has been translated into eight languages.

Professor Stein earned his B.S.E. from Princeton University in 1987, a Master of Science from The

Massachusetts Institute of Technology in 1989, and a PhD also from the Massachusetts Institute of

Technology in 1992.

Karl Sigman Professor Karl Sigman joined Columbia University’s Industrial Engineering and Operations Research

Department in 1987. Professor Sigman was the recipient of the Distinguished Faculty Teaching Award

both in 1998 and in 2002. He teaches courses in stochastic models, financial engineering, and queueing

theory. Before joining Columbia, Professor Sigman was a postdoctoral associate at the Mathematical

Sciences Institute at Cornell University. As of July 2011, Professor Sigman is currently the Director of

Undergraduate Programs.

Professor Karl Sigman’s research interests include queueing theory, stochastic networks, point processes,

insurance risk, and economics. He has published in numerous journals including Stochastic Processes and

Their Applications, Queueing Systems, Journal of Applied Probability, and Mathematics of Operations

Research.