Embed Size (px)

Citation preview

Chapter 8

Internal Control and Cash

Excel Application Exercise

Solution

1. Additional issues: The starter list is included on the instructor’s solution spreadsheet, but be sure to let students discuss any additional considerations they have included.

2. The sample instructor’s solution spreadsheet indicates that the “do nothing” alternative is the best choice. Students may have different answers, depending on how they scored each of their issues. You may wish to ask students if truly “doing nothing” is a viable option, even though we always include it in such an analysis.

3. Students will have different answers for Van Allen’s (and the board’s) response, depending both on (a) their spreadsheet solutions and (b) novice “gut feel” for such ethics-based decisions. Be sure to encourage all viewpoints so students can appreciate the ethical positions held by class members.

Chapter 8 Internal Control and Cash 535

Quick Check

Answers:

1. d 3. b 5. b 7. c 9. a2. a 4. d 6. d 8. c 10. c

Explanations:

8. c. Adjusted cash balance is $680 ($800 – Service charge$20 – NSF check $100)

Accounting 6/e Solutions Manual536

Starters

(5 min.) S 8-1

Safeguarding assets is most important because all organizations need assets to survive.

(5-10 min.) S 8-2

Separation of duties is essential for safeguarding assets. The person who has custody of an asset should not also account for the asset. With both duties, the person can steal the asset and hide the theft by making a false entry in the accounting records.

Chapter 8 Internal Control and Cash 537

(5 min.) S 8-3

Differences:

1. External auditors are entirely independent of the business.Internal auditors are employees of the business.

2. External audits are designed to determine whether the company’s financial statements are prepared in accordance with generally accepted accounting principles.

Internal audits are designed to ensure that employees follow company policies and that operations run efficiently.

Similarities:

1. Both types of auditors are independent of the operations they examine.

2. Both types of auditors suggest improvements that help the business run more efficiently.

Accounting 6/e Solutions Manual538

(5 min.) S 8-4

Merrill Lynch could have:

1. Kept all accounting duties away from the cashier. This would have kept the cashier from covering her theft with entries in the accounting records.

2. Required employees to take vacations and rotated employees from job to job. These measures would have placed another person in the cashier’s job and probably would have brought the theft to light earlier.

3. Used an internal auditor. Darlyne Lopez would be less likely to steal and manipulate customer accounts if she knew her work would be audited.

Only two measures are required.

Chapter 8 Internal Control and Cash 539

(5 min.) S 8-5

1. A bank statement is the document the bank uses to report what it did with the depositor’s cash. The statement shows the bank account’s beginning and ending cash balances and lists the month’s cash transactions conducted through the bank.

A bank reconciliation is a document prepared by the company (not by the bank) to explain all differences between the company’s cash records and the bank statement figures. The bank reconciliation ensures that all cash transactions have been accounted for and that the bank and book records of cash are correct.

2. A bank reconciliation is neither a journal, a ledger, an account, nor a financial statement. Instead, it is an accountant’s tool, separate from the company’s books, that explains all differences between the firm’s cash records and the bank statement figures.

Accounting 6/e Solutions Manual540

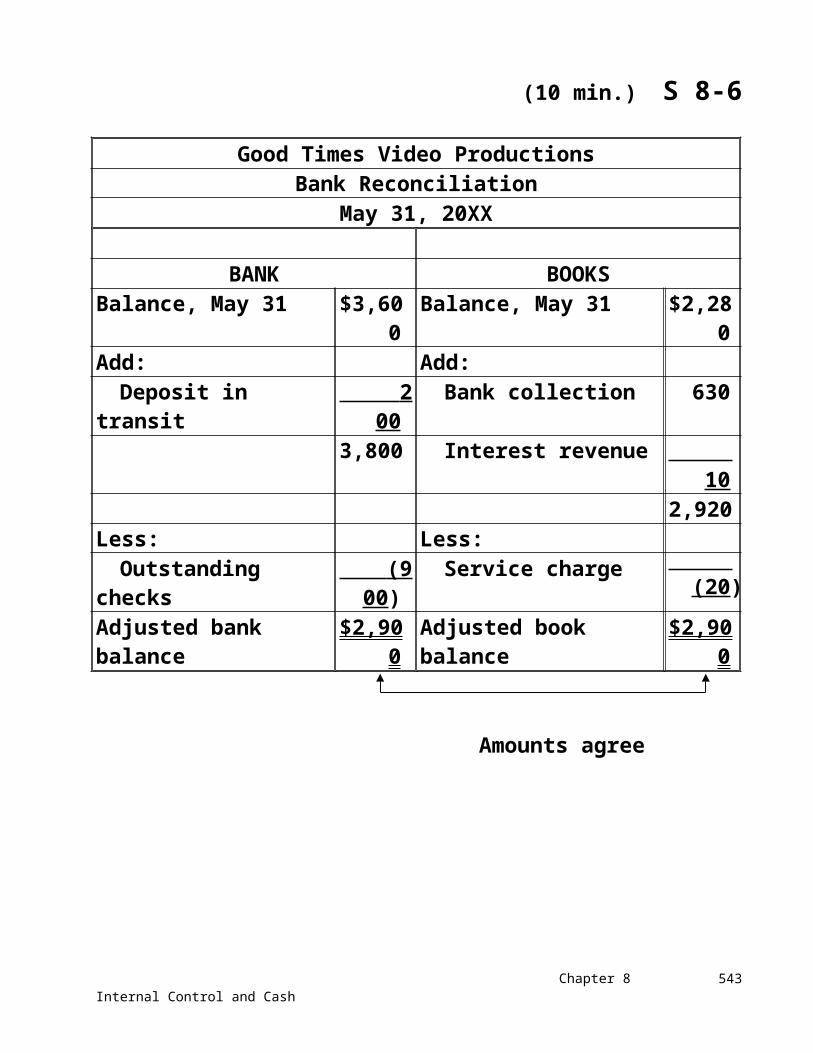

(10 min.) S 8-6

Good Times Video ProductionsBank Reconciliation

May 31, 20XX

BANK BOOKSBalance, May 31 $3,600 Balance, May 31 $2,280Add: Add:

Deposit in transit 200 Bank collection 6303,800 Interest revenue 10

2,920Less: Less:

Outstanding checks (900 ) Service charge (20 )Adjusted bank balance $2,900 Adjusted book balance $2,900

Amounts agree

Chapter 8 Internal Control and Cash 541

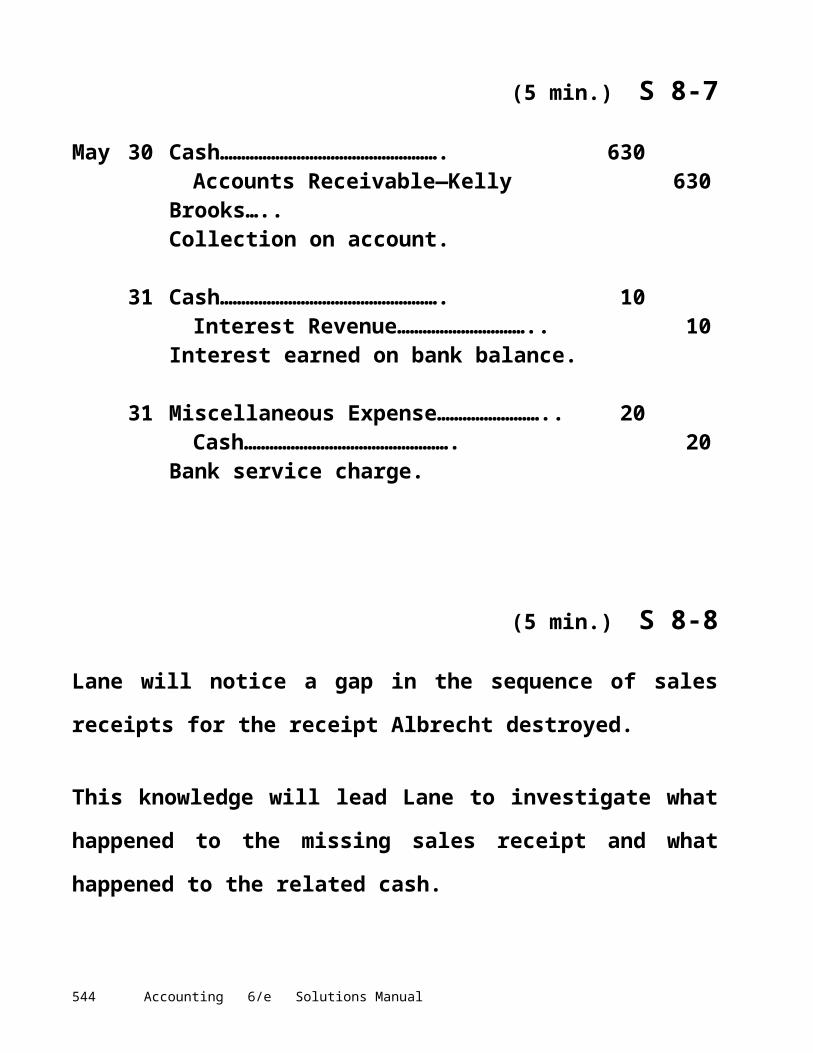

(5 min.) S 8-7

May 30 Cash……………………………………………. 630Accounts Receivable—Kelly Brooks….. 630

Collection on account.

31 Cash……………………………………………. 10Interest Revenue………………………….. 10

Interest earned on bank balance.

31 Miscellaneous Expense…………………….. 20Cash…………………………………………. 20

Bank service charge.

(5 min.) S 8-8

Lane will notice a gap in the sequence of sales receipts for the receipt Albrecht destroyed.

This knowledge will lead Lane to investigate what happened to the missing sales receipt and what happened to the related cash.

Accounting 6/e Solutions Manual542

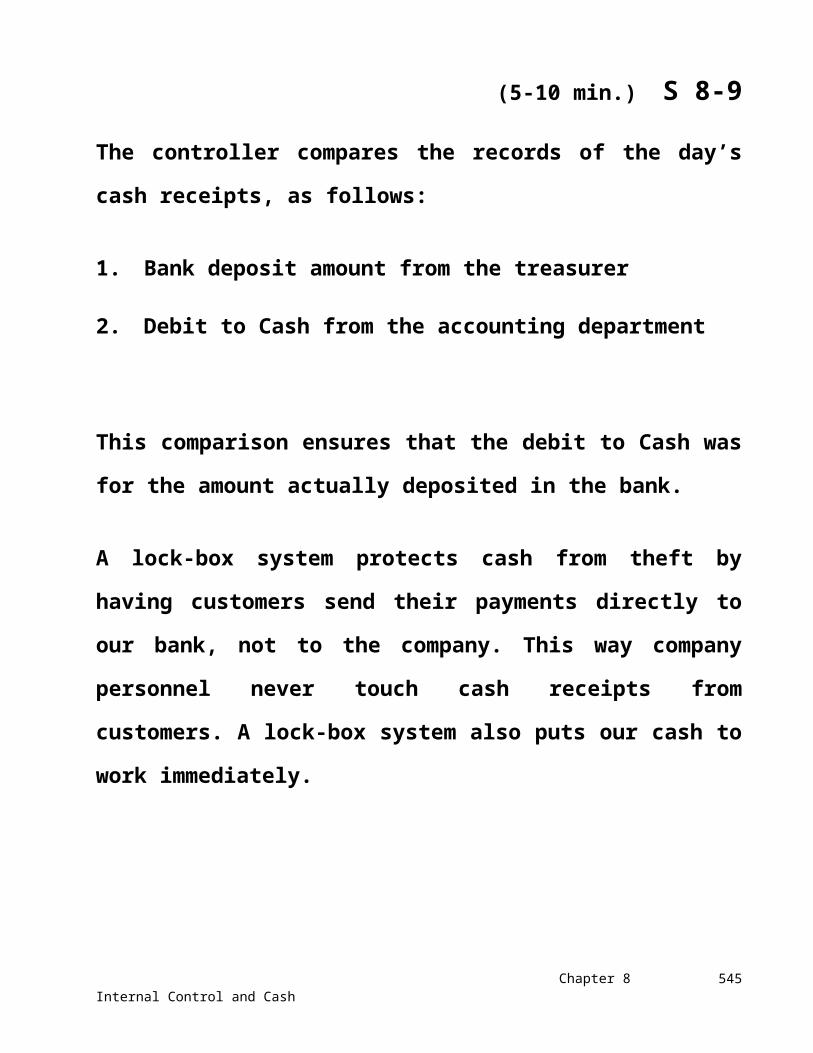

(5-10 min.) S 8-9

The controller compares the records of the day’s cash receipts, as follows:

1. Bank deposit amount from the treasurer

2. Debit to Cash from the accounting department

This comparison ensures that the debit to Cash was for the amount actually deposited in the bank.

A lock-box system protects cash from theft by having customers send their payments directly to our bank, not to the company. This way company personnel never touch cash receipts from customers. A lock-box system also puts our cash to work immediately.

Chapter 8 Internal Control and Cash 543

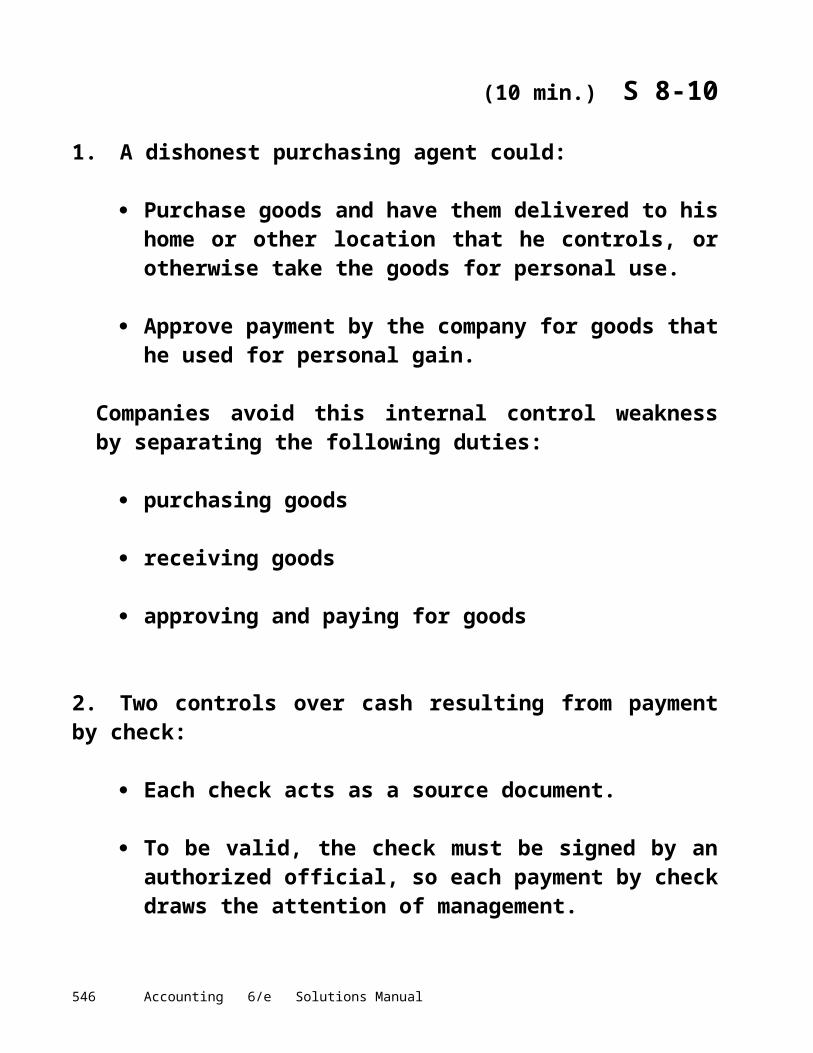

(10 min.) S 8-10

1. A dishonest purchasing agent could:

Purchase goods and have them delivered to his home or other location that he controls, or otherwise take the goods for personal use.

Approve payment by the company for goods that he used for personal gain.

Companies avoid this internal control weakness by separating the following duties:

purchasing goods

receiving goods

approving and paying for goods

2. Two controls over cash resulting from payment by check:

Each check acts as a source document.

To be valid, the check must be signed by an authorized official, so each payment by check draws the attention of management.

Accounting 6/e Solutions Manual544

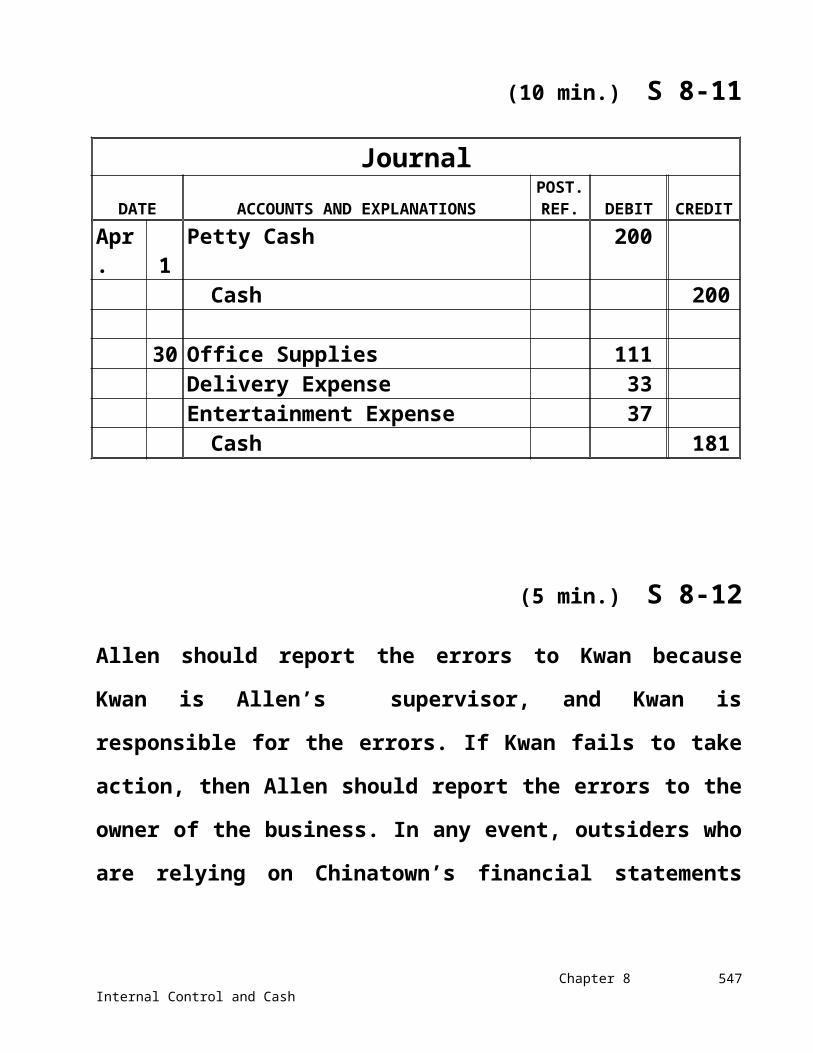

(10 min.) S 8-11

JournalDATE ACCOUNTS AND EXPLANATIONS

POST.REF. DEBIT CREDIT

Apr. 1 Petty Cash 200Cash 200

30 Office Supplies 111Delivery Expense 33Entertainment Expense 37

Cash 181

(5 min.) S 8-12

Allen should report the errors to Kwan because Kwan is Allen’s supervisor, and Kwan is responsible for the errors. If Kwan fails to take action, then Allen should report the errors to the owner of the business. In any event, outsiders who are relying on Chinatown’s financial statements must be made aware of the need to correct the reported net income figure.

Chapter 8 Internal Control and Cash 545

Exercises

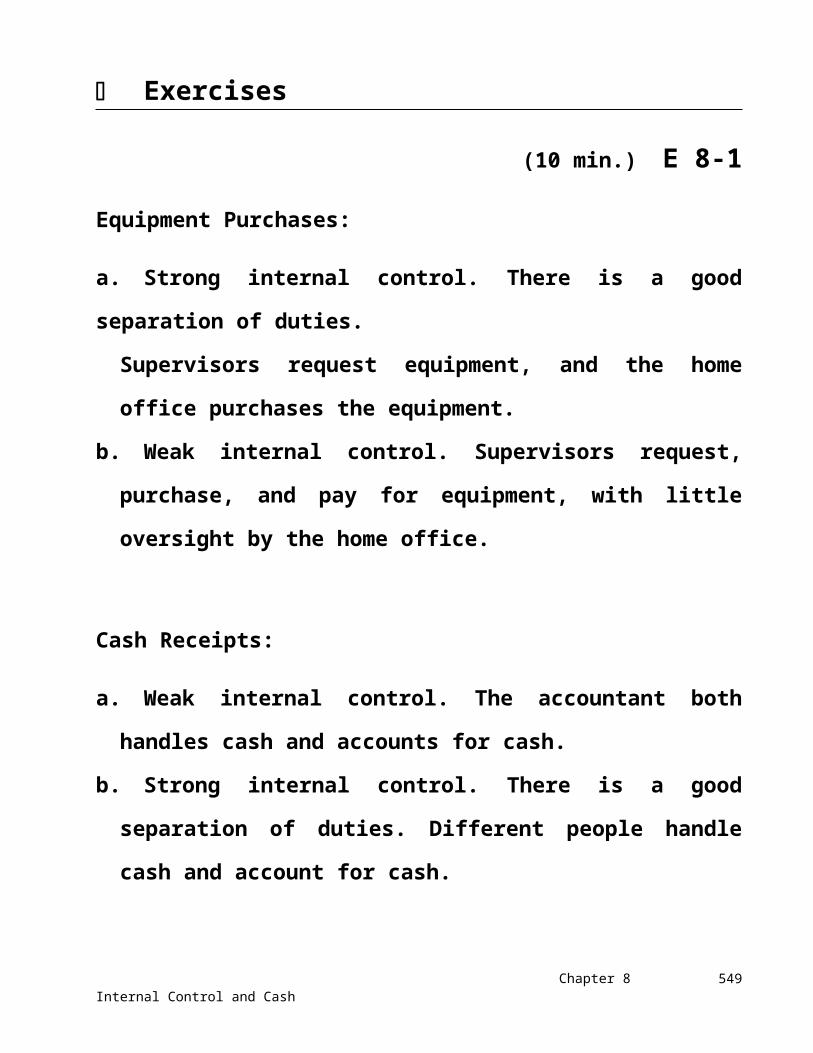

(10 min.) E 8-1

Equipment Purchases:

a. Strong internal control. There is a good separation of duties. Supervisors request equipment, and the home office purchases the equipment.

b. Weak internal control. Supervisors request, purchase, and pay for equipment, with little oversight by the home office.

Cash Receipts:

a. Weak internal control. The accountant both handles cash and accounts for cash.

b. Strong internal control. There is a good separation of duties. Different people handle cash and account for cash.

Accounting 6/e Solutions Manual546

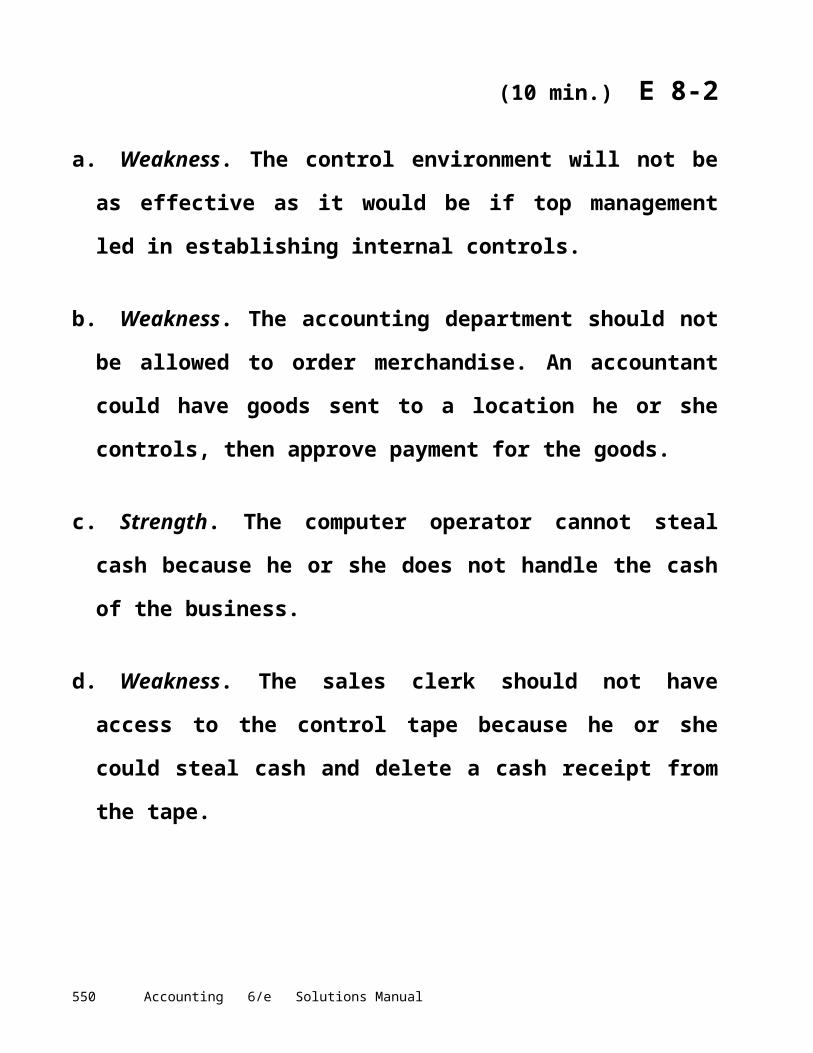

(10 min.) E 8-2

a. Weakness. The control environment will not be as effective as it would be if top management led in establishing internal controls.

b. Weakness. The accounting department should not be allowed to order merchandise. An accountant could have goods sent to a location he or she controls, then approve payment for the goods.

c. Strength. The computer operator cannot steal cash because he or she does not handle the cash of the business.

d. Weakness. The sales clerk should not have access to the control tape because he or she could steal cash and delete a cash receipt from the tape.

e. Weakness. The officer should examine the payment packet to ensure that the payment is for the correct amount.

Chapter 8 Internal Control and Cash 547

(10 min.) E 8-3

The missing internal control characteristic in each situation is:

a. Other controls (no job rotation).

b. Other controls (documents and records—no receiving report).

c. Other controls (not depositing cash frequently enough for adequate security).

d. Separation of duties (same person ordering merchandise and approving payment).

e. Separation of duties (same person selling tickets and taking tickets).

(5 min.) E 8-4

a. 2 e. 1

b. 3 f. 2

c. 2 g. 4

d. 1 h. 3

Accounting 6/e Solutions Manual548

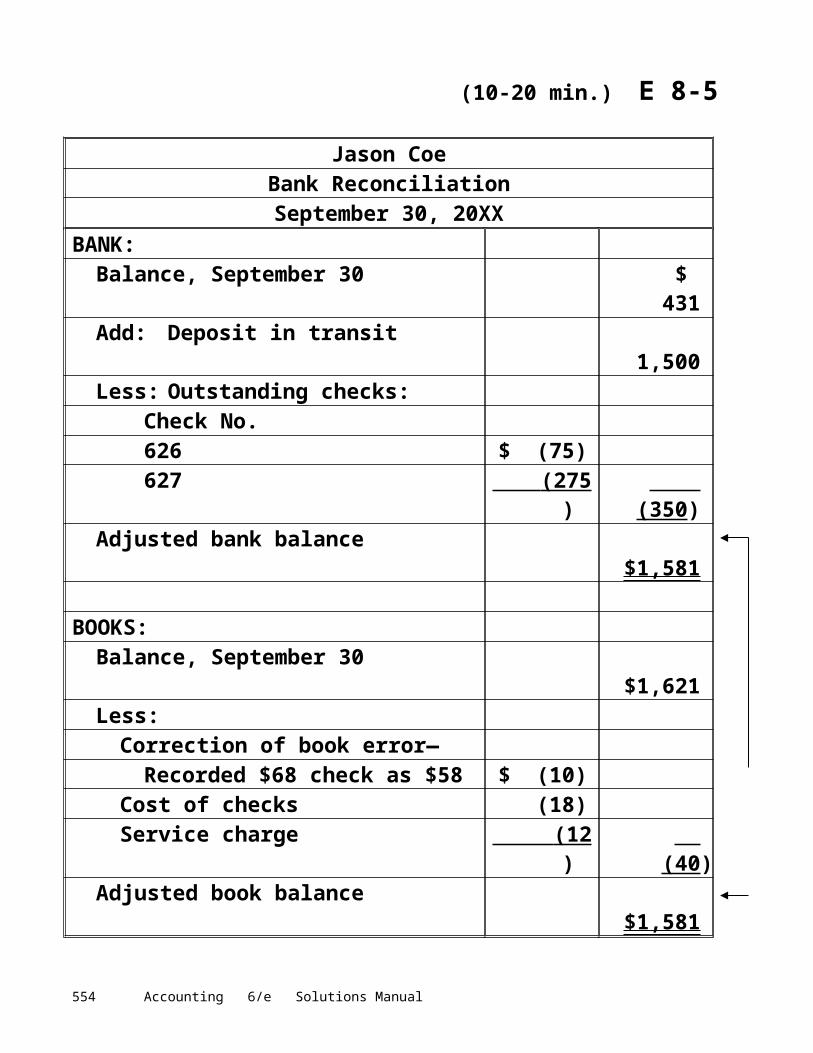

(10-20 min.) E 8-5

Jason CoeBank ReconciliationSeptember 30, 20XX

BANK:Balance, September 30 $ 431Add: Deposit in transit 1,500Less: Outstanding checks:

Check No.626 $ (75)627 (275 ) (350 )

Adjusted bank balance $1,581

BOOKS:Balance, September 30 $1,621Less:

Correction of book error—Recorded $68 check as $58 $ (10)

Cost of checks (18)Service charge (12 ) (40 )

Adjusted book balance $1,581

Coe has cash of $1,581 on September 30.

Chapter 8 Internal Control and Cash 549

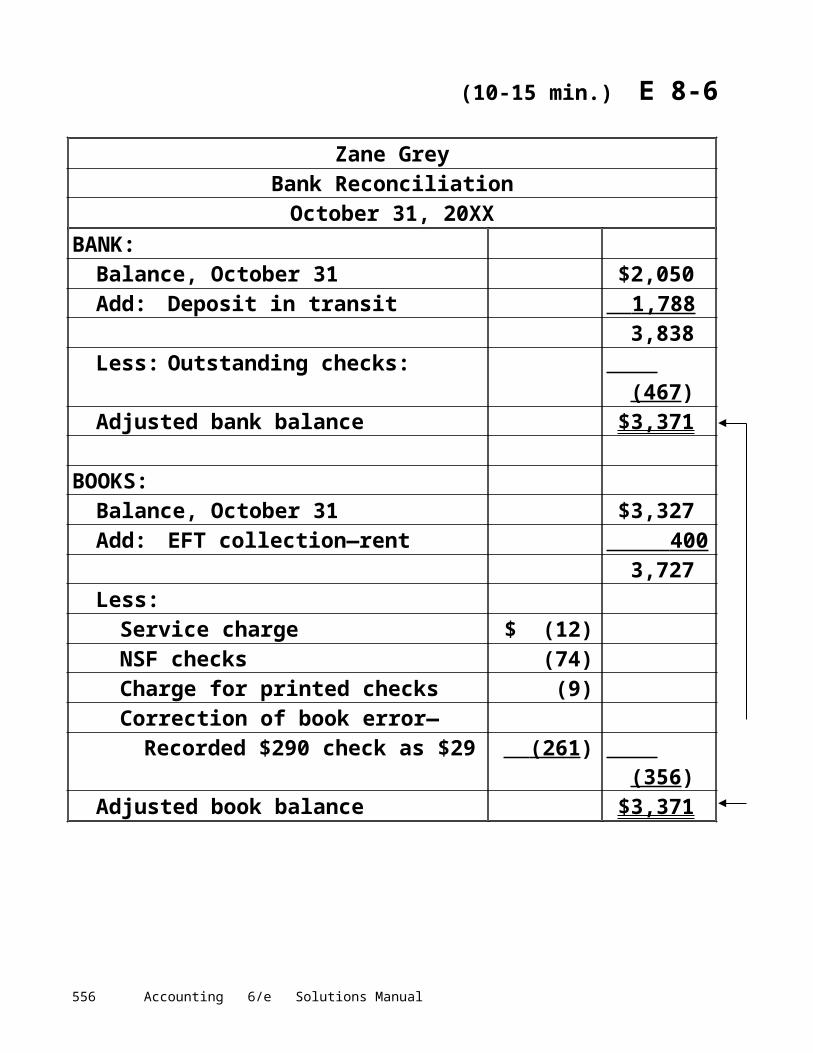

(10-15 min.) E 8-6

Zane GreyBank Reconciliation

October 31, 20XXBANK:

Balance, October 31 $2,050Add: Deposit in transit 1,788

3,838Less: Outstanding checks: (467 )Adjusted bank balance $3,371

BOOKS:Balance, October 31 $3,327Add: EFT collection—rent 400

3,727Less:

Service charge $ (12)NSF checks (74)Charge for printed checks (9)Correction of book error—

Recorded $290 check as $29 (261 ) (356 )Adjusted book balance $3,371

Accounting 6/e Solutions Manual550

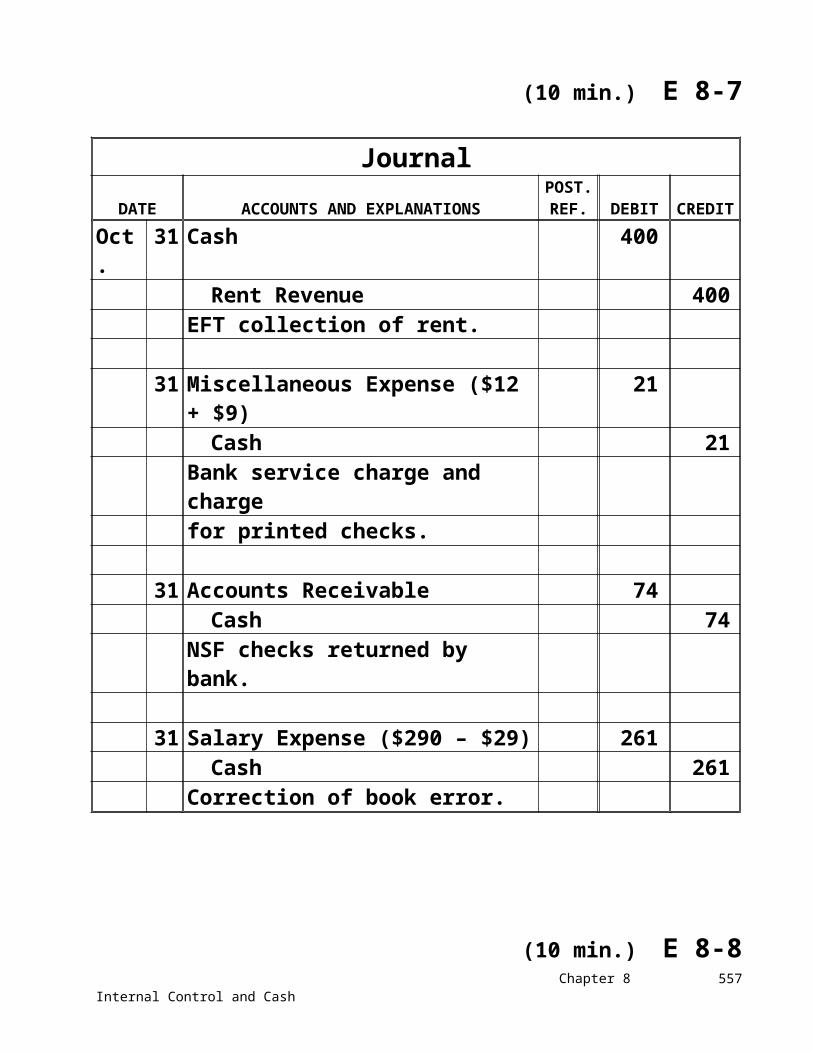

(10 min.) E 8-7

JournalDATE ACCOUNTS AND EXPLANATIONS

POST.REF. DEBIT CREDIT

Oct. 31 Cash 400Rent Revenue 400

EFT collection of rent.

31 Miscellaneous Expense ($12 + $9) 21Cash 21

Bank service charge and charge for printed checks.

31 Accounts Receivable 74Cash 74

NSF checks returned by bank.

31 Salary Expense ($290 – $29) 261Cash 261

Correction of book error.

(10 min.) E 8-8

The adjusted bank balance shows the company’s true cash balance, which is $2,300.

It appears that the employee has stolen $1,000 ($3,300 on the books – $2,300 in the bank).

Chapter 8 Internal Control and Cash 551

(10 min.) E 8-9

TO: Store Manager

There is a weakness in internal control over cash receipts. The cash registers do not keep an internal record of sales. With no record of sales, there is no way to determine how much cash should be in the cash drawer. This makes it easy for the cashier to steal cash and not get caught.

To improve internal control over cash, the company should use cash registers that record each sale inside the machine. The manager can prove the amount of cash in the cash drawer against this recorded amount.

Accounting 6/e Solutions Manual552

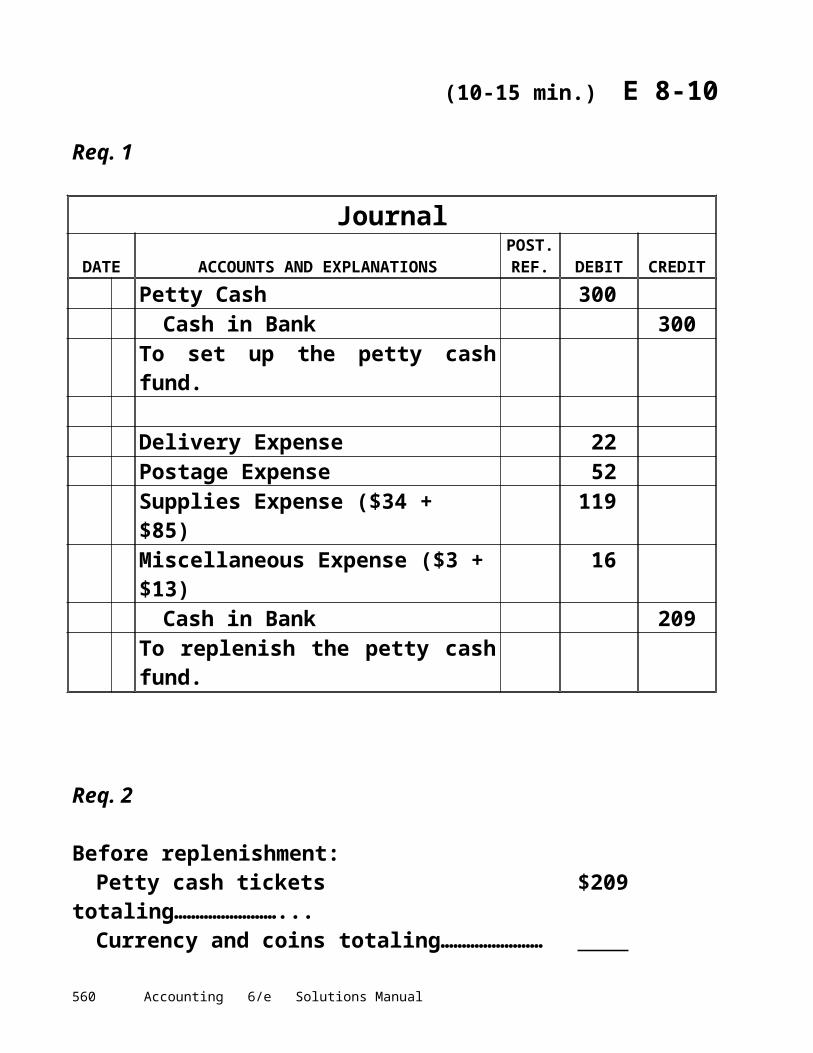

(10-15 min.) E 8-10

Req. 1

JournalDATE ACCOUNTS AND EXPLANATIONS

POST.REF. DEBIT CREDIT

Petty Cash 300Cash in Bank 300

To set up the petty cash fund.

Delivery Expense 22Postage Expense 52Supplies Expense ($34 + $85) 119Miscellaneous Expense ($3 + $13) 16

Cash in Bank 209To replenish the petty cash fund.

Req. 2

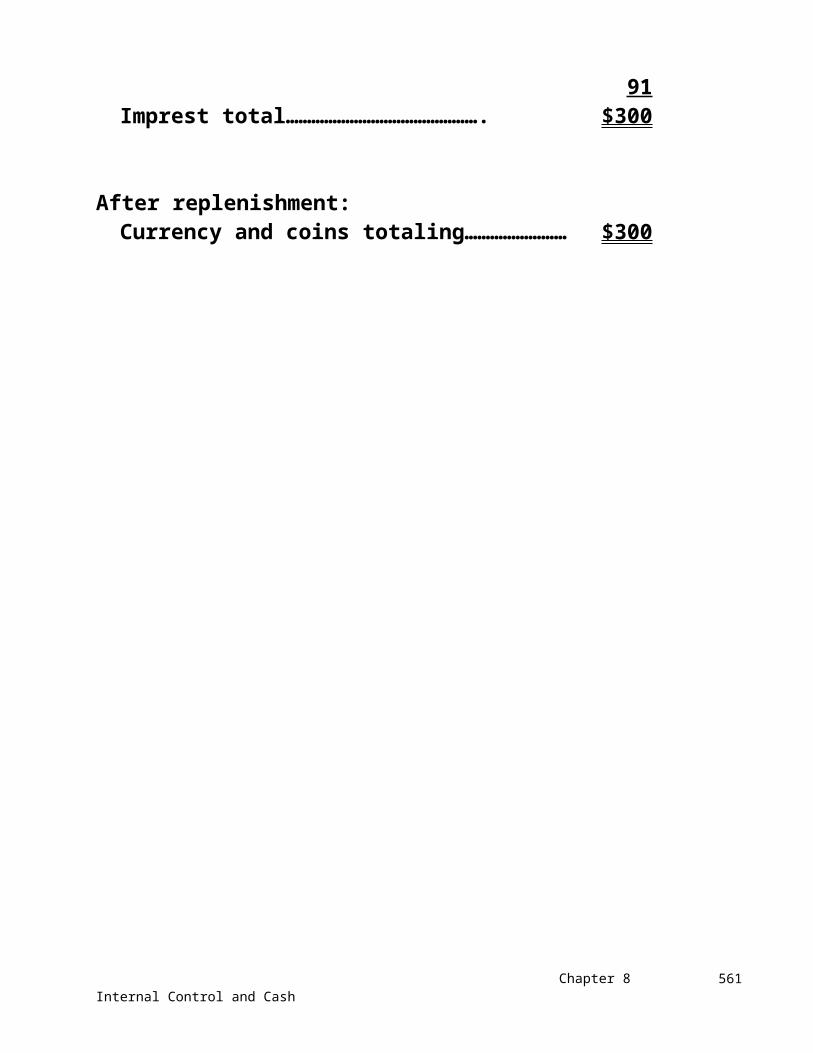

Before replenishment:Petty cash tickets totaling……………………... $209Currency and coins totaling…………………… 91 Imprest total………………………………………. $300

After replenishment:Currency and coins totaling…………………… $300

Chapter 8 Internal Control and Cash 553

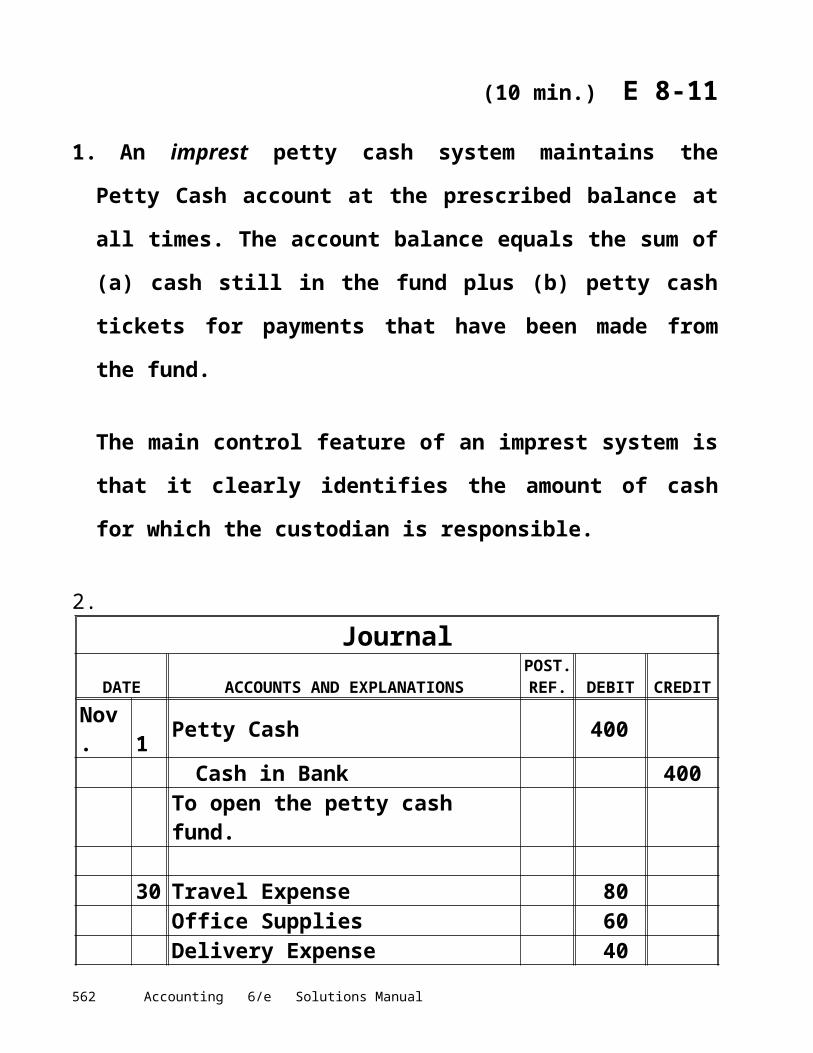

(10 min.) E 8-11

1. An imprest petty cash system maintains the Petty Cash account at the prescribed balance at all times. The account balance equals the sum of (a) cash still in the fund plus (b) petty cash tickets for payments that have been made from the fund.

The main control feature of an imprest system is that it clearly identifies the amount of cash for which the custodian is responsible.

2.Journal

DATE ACCOUNTS AND EXPLANATIONSPOST.REF. DEBIT CREDIT

Nov. 1 Petty Cash 400Cash in Bank 400

To open the petty cash fund.

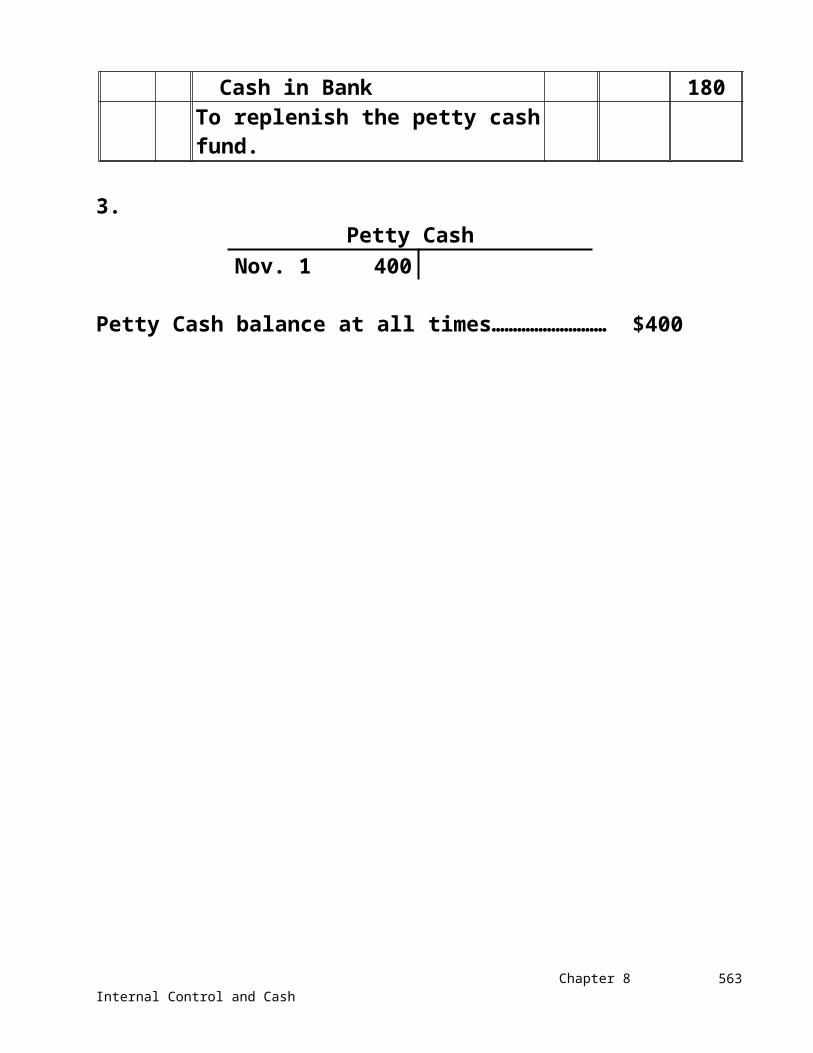

30 Travel Expense 80Office Supplies 60Delivery Expense 40

Cash in Bank 180To replenish the petty cash fund.

3.Petty Cash

Nov. 1 400

Petty Cash balance at all times……………………… $400

Accounting 6/e Solutions Manual554

(15-20 min.) E 8-12

1. Identify the ethical issue. You must decide whether it is ethical—good or bad, moral or immoral—for a member of the Congress to write NSF checks on a regular basis.

2. Specify the alternatives. Deliberately write the NSF checks or not.

3. Assess the possible consequences. If you write the NSF checks, you may anger your people back home because they do not enjoy this privilege and view the practice as dishonest. They may vote you out of office (this actually occurred). You may also be encouraging the public to be lax in their own money management.

4. Make the decision. It would be ethical and wise to avoid the practice. The high road is always best. Was it unethical for the legislators to write the NSF checks? Each person must decide for himself or herself. The class discussion should be lively.

It is interesting to contrast the House bank situation with private citizens’ writing NSF checks by prior arrangement with their bank and paying interest and other charges on the borrowed money. Because of the prior arrangement with the bank, this is simply another way to borrow money.

Chapter 8 Internal Control and Cash 555

Problems

Group A

(15-20 min.) P 8-1A

TO: Mike Key

FROM: Consultant

RE: Internal Control

Every business needs a system of internal controls. Internal control is the organizational plan and all the related measures adopted by an entity to (1) safeguard assets, (2) encourage employees to follow company policies, (3) promote operational efficiency, and (4) ensure accurate and reliable accounting records.

A company with an effective system of internal control needs competent and reliable personnel. The business may have to increase employee pay in order to attract and retain high-quality employees.

It is necessary to assign responsibilities to employees so that everyone in the organization knows his or her duties. This avoids confusion and helps ensure that all jobs are performed.

Accounting 6/e Solutions Manual556

(continued) P 8-1A

Certain duties should be separated between two or more employees to limit the opportunity for fraud. For example, the custody of cash should be separated from the accounting for cash.

The business may need to have an audit by an independent CPA. Auditors can evaluate the system of internal control and suggest ways to improve efficiency. Auditors also gauge the reliability of accounting records, which provide the information for business decisions.

Documents and records are needed to keep track of sales and cash receipts, expenses, payments, and other transactions. These records will help manage the business better and save money.

Electronic and other controls can safeguard assets. For example, the company needs burglar alarms to protect buildings, and should store real estate contracts and property titles in fireproof vaults.

Student responses may vary.

Chapter 8 Internal Control and Cash 557

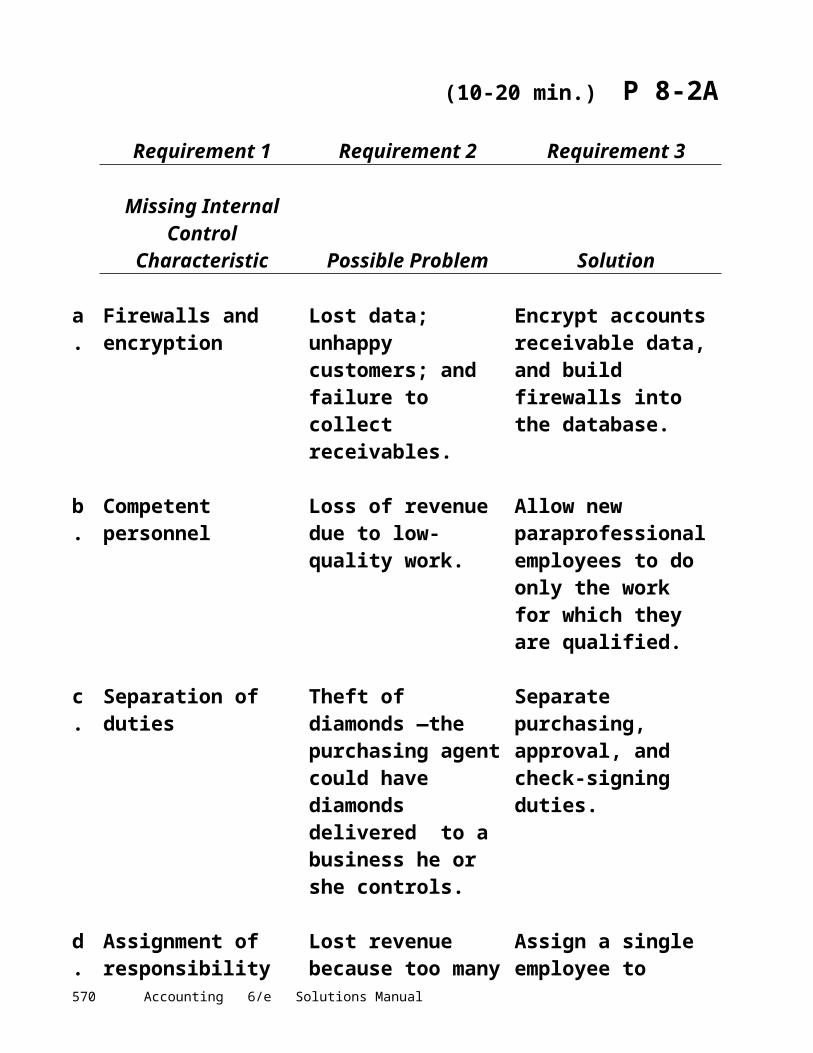

(10-20 min.) P 8-2A

Requirement 1 Requirement 2 Requirement 3

Missing InternalControl

Characteristic Possible Problem Solution

a. Firewalls and encryption

Lost data; unhappy customers; and failure to collect receivables.

Encrypt accounts receivable data, and build firewalls into the database.

b. Competent personnel

Loss of revenue due to low-quality work.

Allow new paraprofessional employees to do only the work for which they are qualified.

c. Separation of duties Theft of diamonds —the purchasing agent could have diamonds delivered to a business he or she controls.

Separate purchasing, approval, and check-signing duties.

d. Assignment of responsibility

Lost revenue because too many employees are managing the office and neglecting their duties.

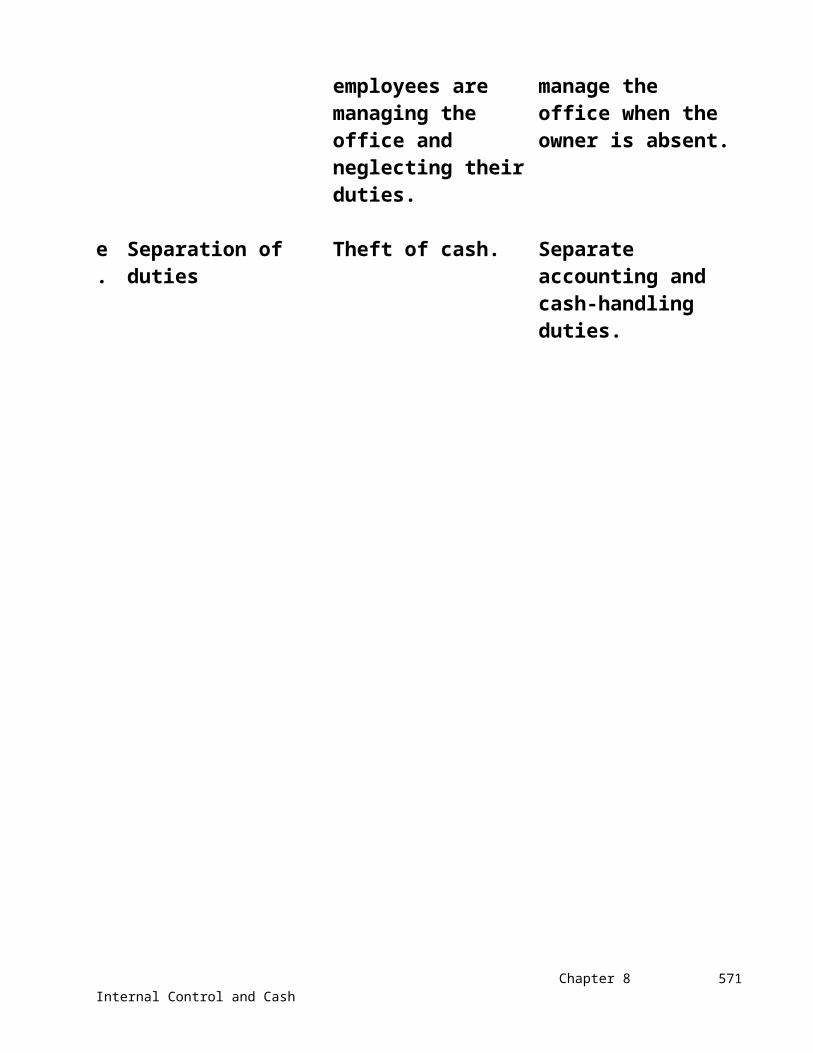

Assign a single employee to manage the office when the owner is absent.

e. Separation of duties Theft of cash. Separate accounting and cash-handling duties.

Accounting 6/e Solutions Manual558

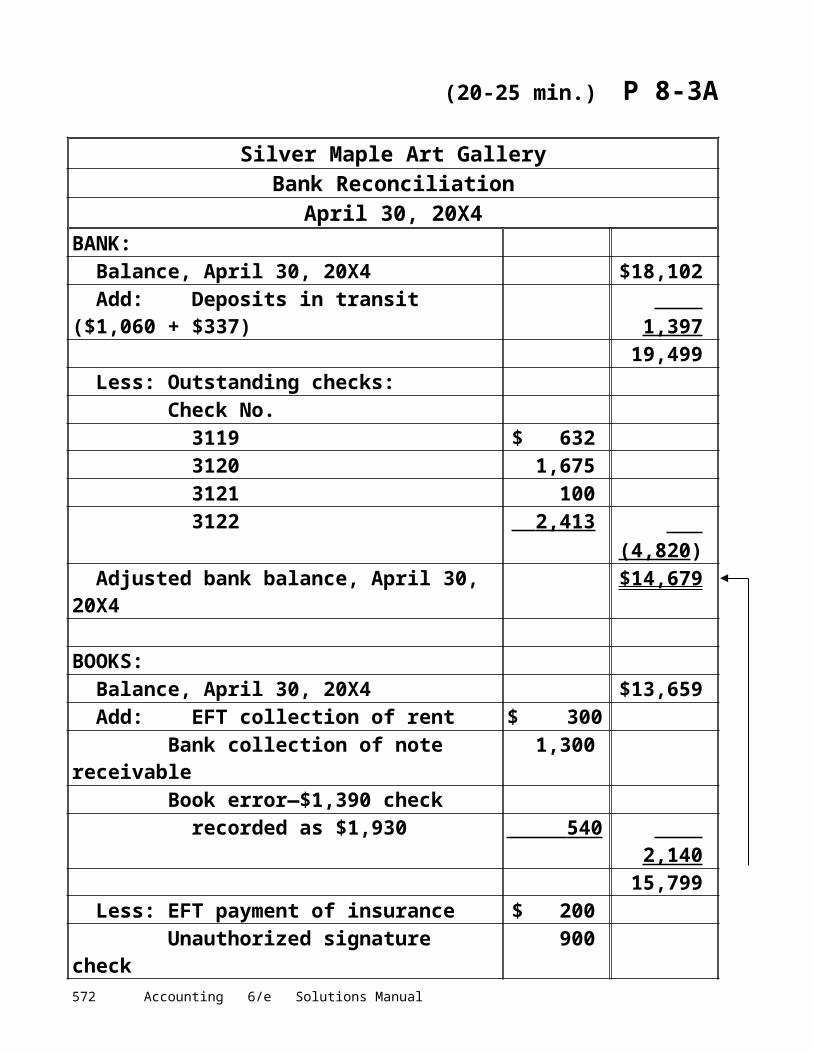

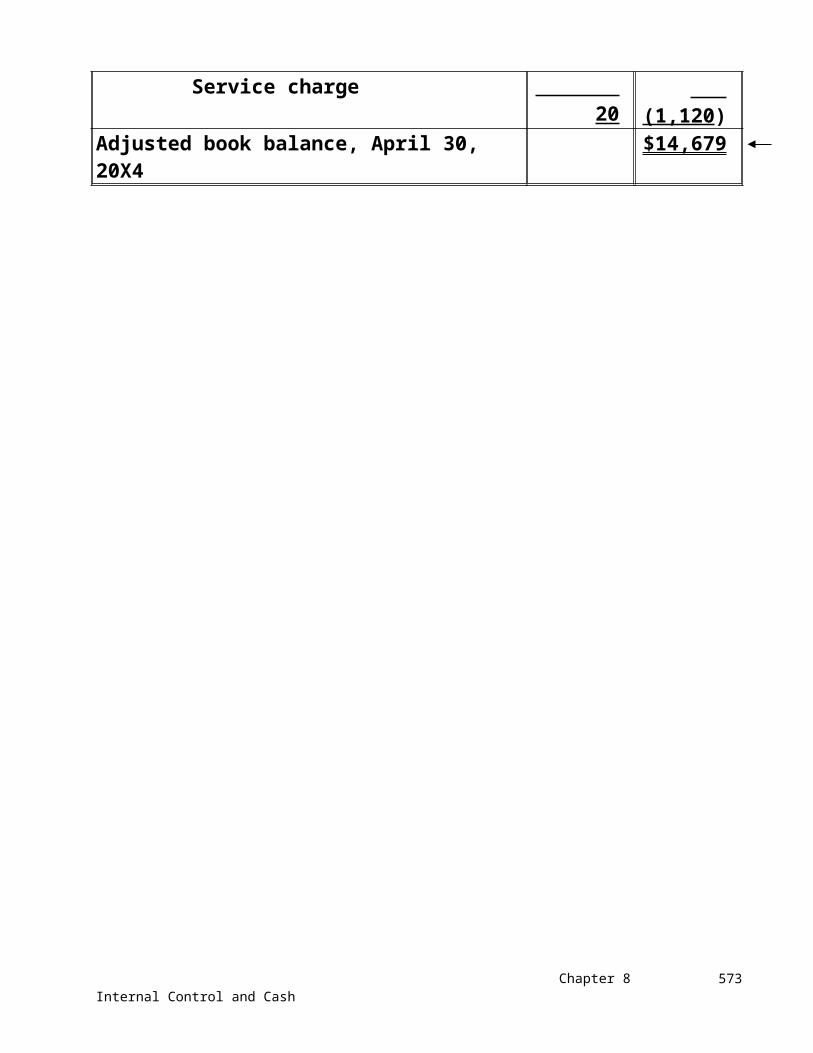

(20-25 min.) P 8-3A

Silver Maple Art GalleryBank Reconciliation

April 30, 20X4BANK:

Balance, April 30, 20X4 $18,102Add: Deposits in transit ($1,060 + $337) 1,397

19,499Less: Outstanding checks:

Check No.3119 $ 6323120 1,6753121 1003122 2,413 (4,820 )

Adjusted bank balance, April 30, 20X4 $14,679

BOOKS:Balance, April 30, 20X4 $13,659Add: EFT collection of rent $ 300

Bank collection of note receivable 1,300Book error—$1,390 check

recorded as $1,930 540 2,140 15,799

Less: EFT payment of insurance $ 200Unauthorized signature check 900Service charge 20 (1,120 )

Adjusted book balance, April 30, 20X4 $14,679

Chapter 8 Internal Control and Cash 559

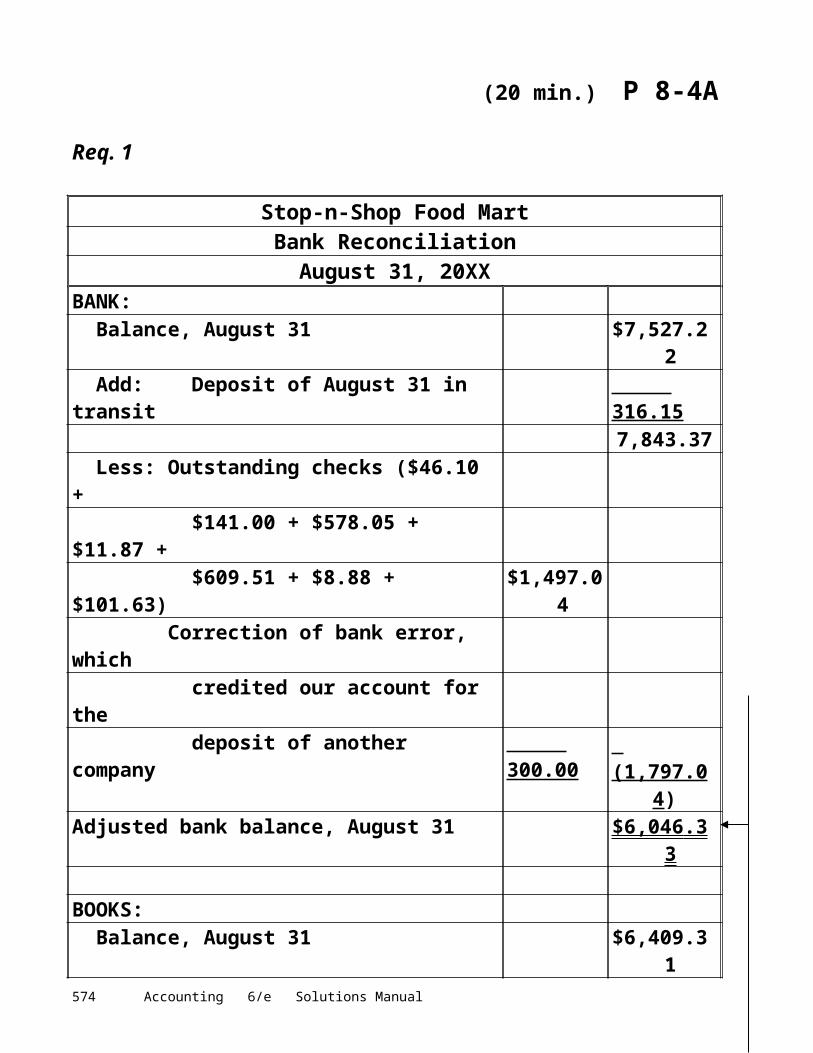

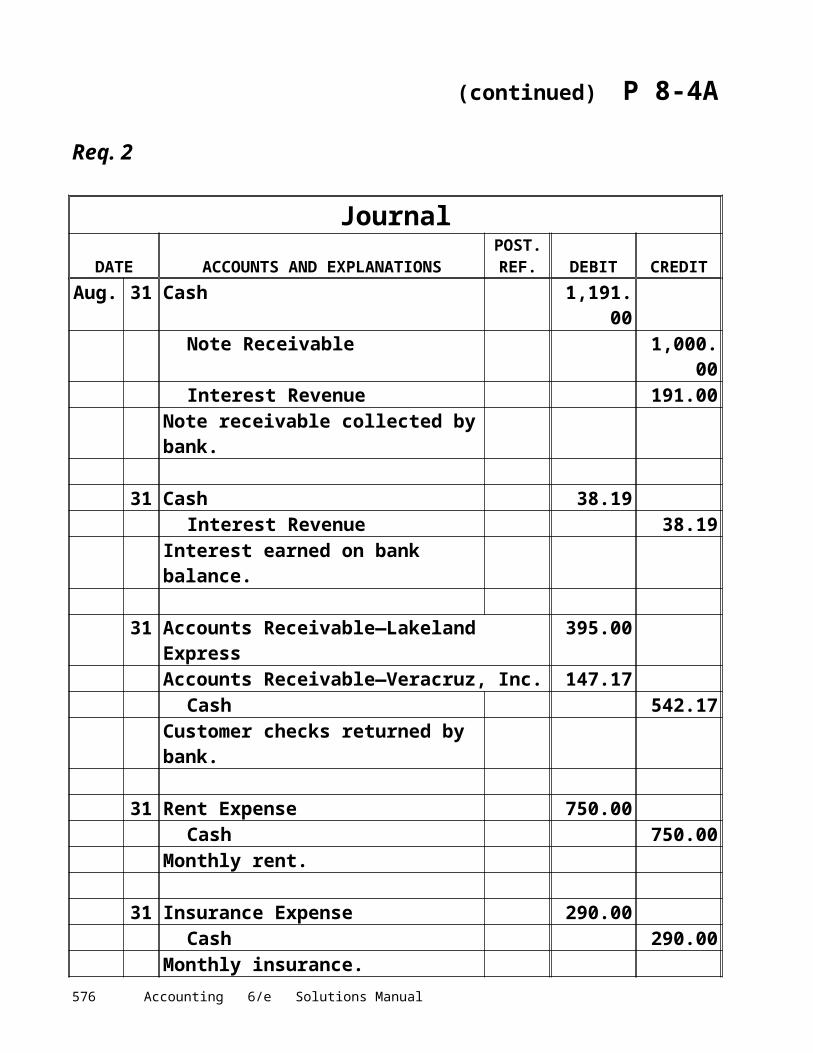

(20 min.) P 8-4A

Req. 1

Stop-n-Shop Food MartBank Reconciliation

August 31, 20XXBANK:

Balance, August 31 $7,527.22Add: Deposit of August 31 in transit 316 .15

7,843.37Less: Outstanding checks ($46.10 +

$141.00 + $578.05 + $11.87 +$609.51 + $8.88 + $101.63) $1,497.04

Correction of bank error, whichcredited our account for thedeposit of another company 300 .00 (1,797 .04 )

Adjusted bank balance, August 31 $6,046 .33

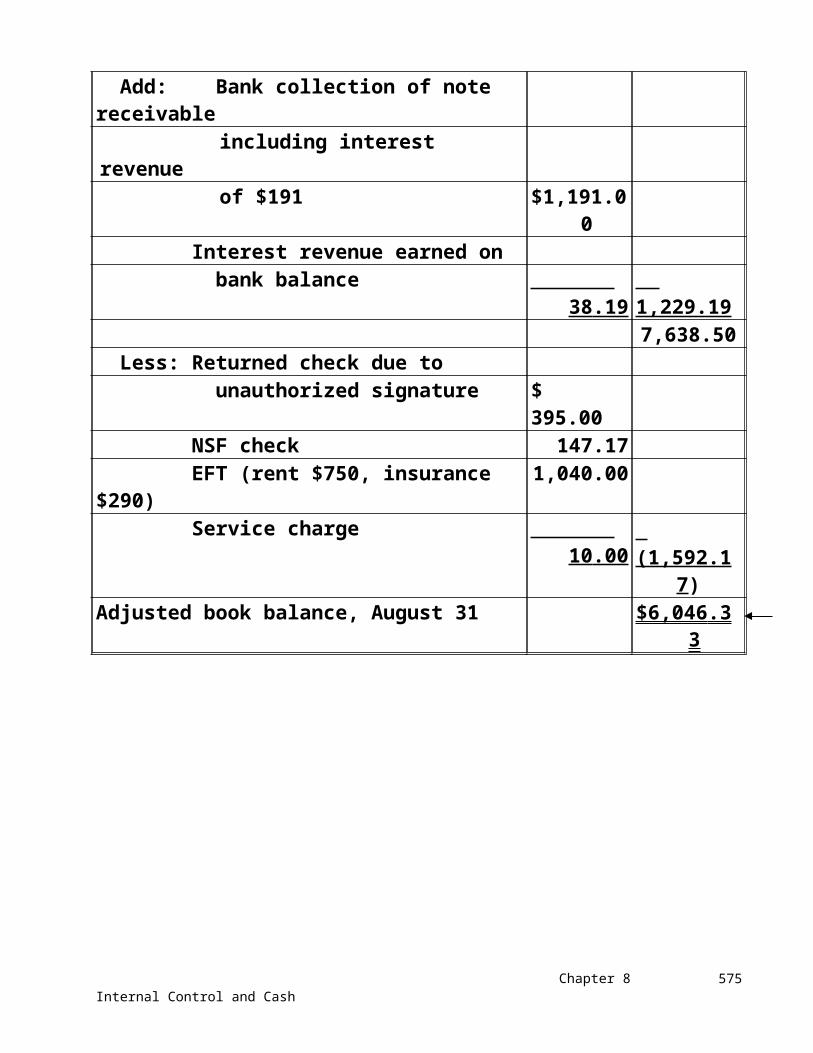

BOOKS:Balance, August 31 $6,409.31Add: Bank collection of note receivable

including interest revenueof $191 $1,191.00

Interest revenue earned on bank balance 38 .19 1,229 .19

7,638.50Less: Returned check due to

unauthorized signature $ 395.00NSF check 147.17EFT (rent $750, insurance $290) 1,040.00Service charge 10 .00 (1,592 .17 )

Adjusted book balance, August 31 $6,046 .33

Accounting 6/e Solutions Manual560

(continued) P 8-4A

Req. 2

JournalDATE ACCOUNTS AND EXPLANATIONS

POST.REF. DEBIT CREDIT

Aug. 31 Cash 1,191.00Note Receivable 1,000.00Interest Revenue 191.00

Note receivable collected by bank.

31 Cash 38.19Interest Revenue 38.19

Interest earned on bank balance.

31 Accounts Receivable—Lakeland Express 395.00Accounts Receivable—Veracruz, Inc. 147.17

Cash 542.17Customer checks returned by bank.

31 Rent Expense 750.00Cash 750.00

Monthly rent.

31 Insurance Expense 290.00Cash 290.00

Monthly insurance.

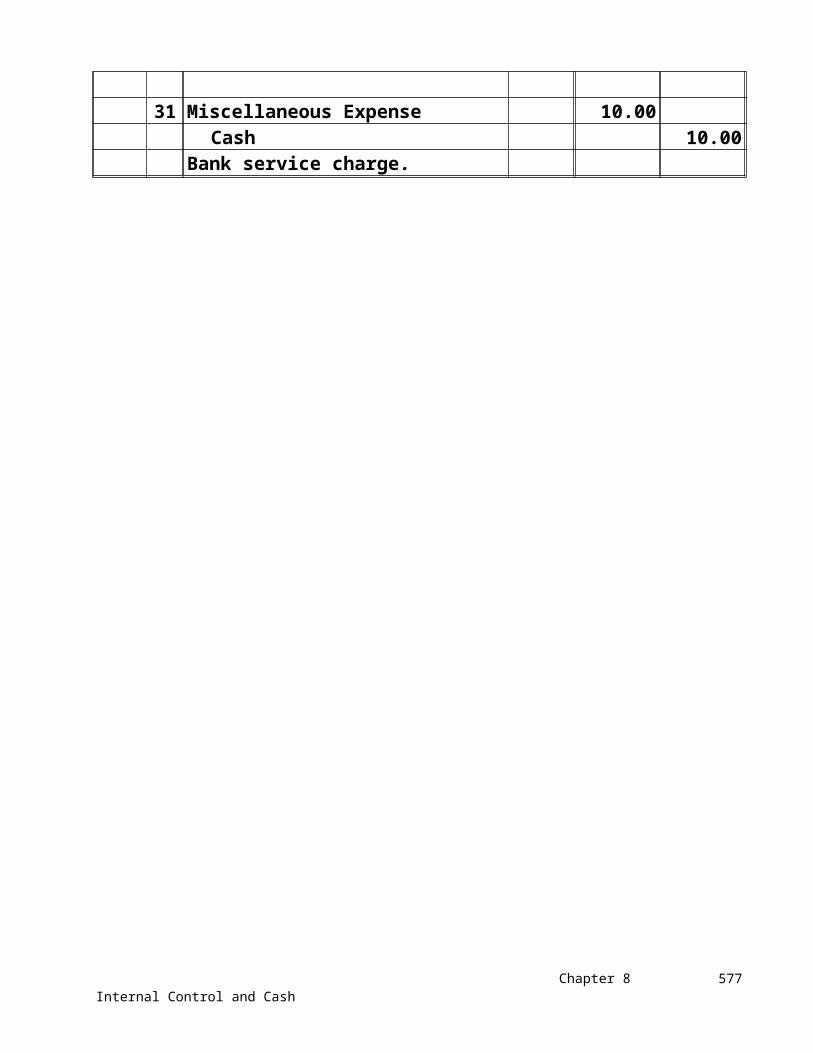

31 Miscellaneous Expense 10.00Cash 10.00

Bank service charge.

Chapter 8 Internal Control and Cash 561

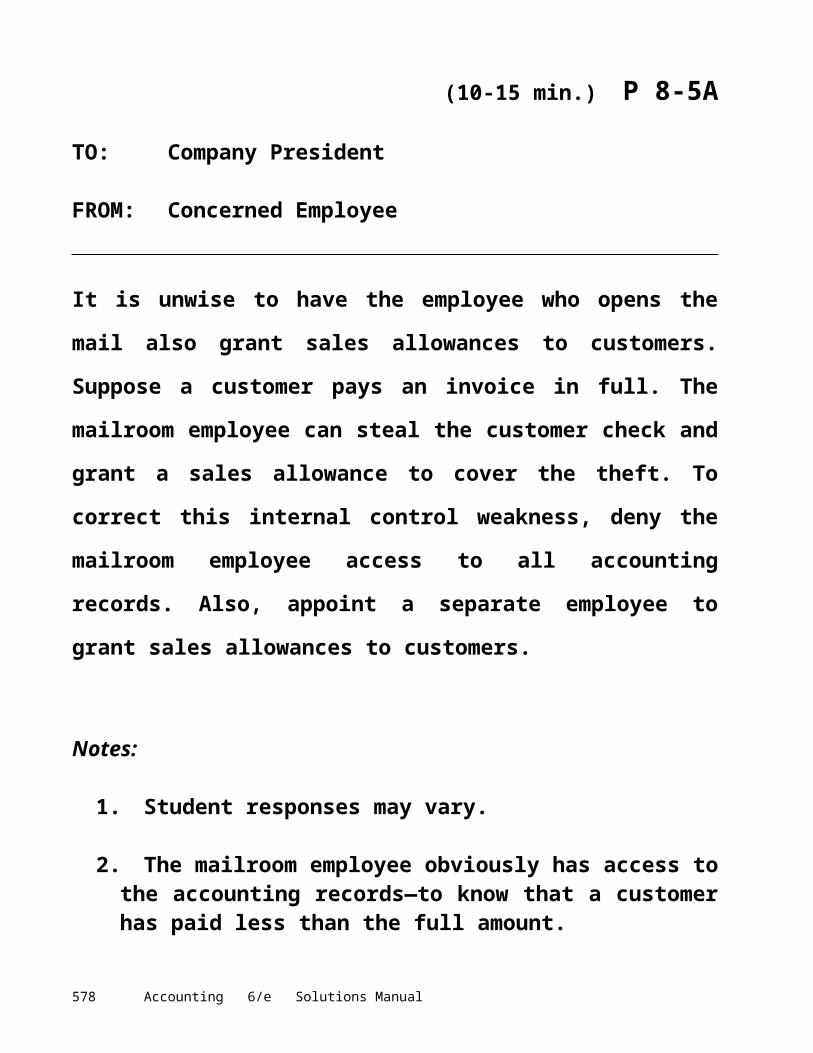

(10-15 min.) P 8-5A

TO: Company President

FROM: Concerned Employee

It is unwise to have the employee who opens the mail also grant sales allowances to customers. Suppose a customer pays an invoice in full. The mailroom employee can steal the customer check and grant a sales allowance to cover the theft. To correct this internal control weakness, deny the mailroom employee access to all accounting records. Also, appoint a separate employee to grant sales allowances to customers.

Notes:

1. Student responses may vary.

2. The mailroom employee obviously has access to the accounting records—to know that a customer has paid less than the full amount.

3. It may be necessary to explain to students that the mailroom employee must forge the company endorsement on stolen customer checks. This person must also open—and control—a bank account in the company’s name. Opening such an account may be quite easy.

Accounting 6/e Solutions Manual562

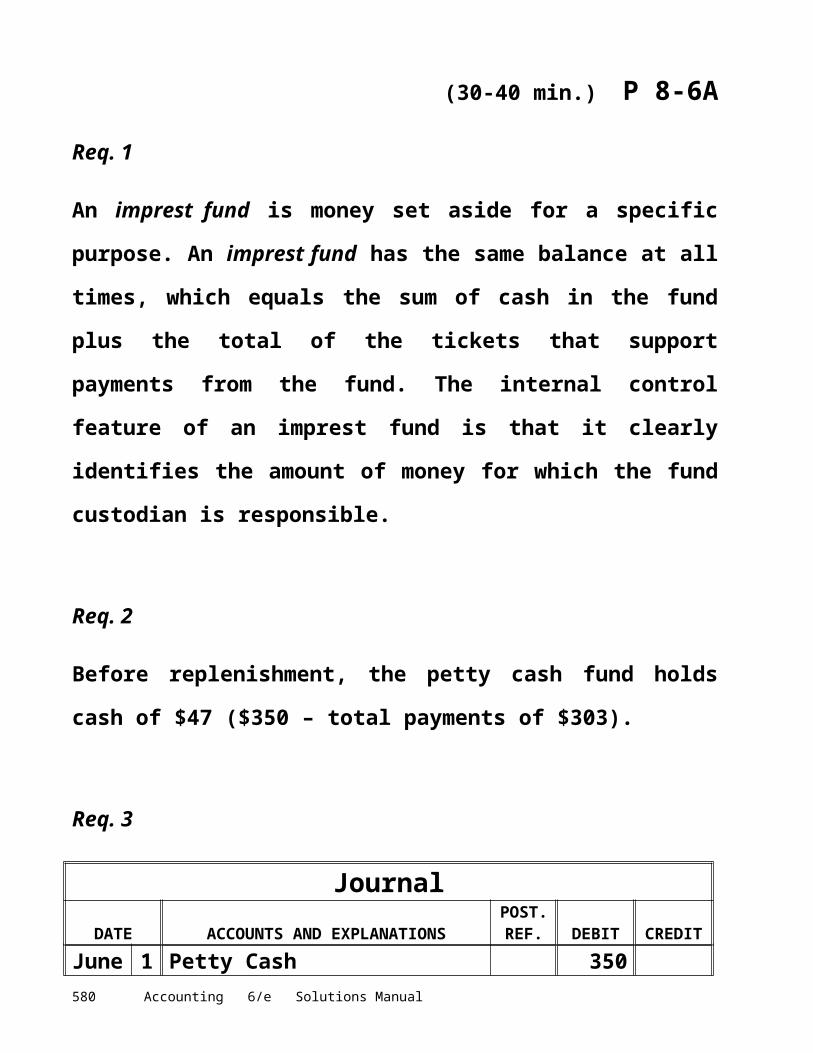

(30-40 min.) P 8-6A

Req. 1

An imprest fund is money set aside for a specific purpose. An imprest fund has the same balance at all times, which equals the sum of cash in the fund plus the total of the tickets that support payments from the fund. The internal control feature of an imprest fund is that it clearly identifies the amount of money for which the fund custodian is responsible.

Req. 2

Before replenishment, the petty cash fund holds cash of $47 ($350 – total payments of $303).

Req. 3

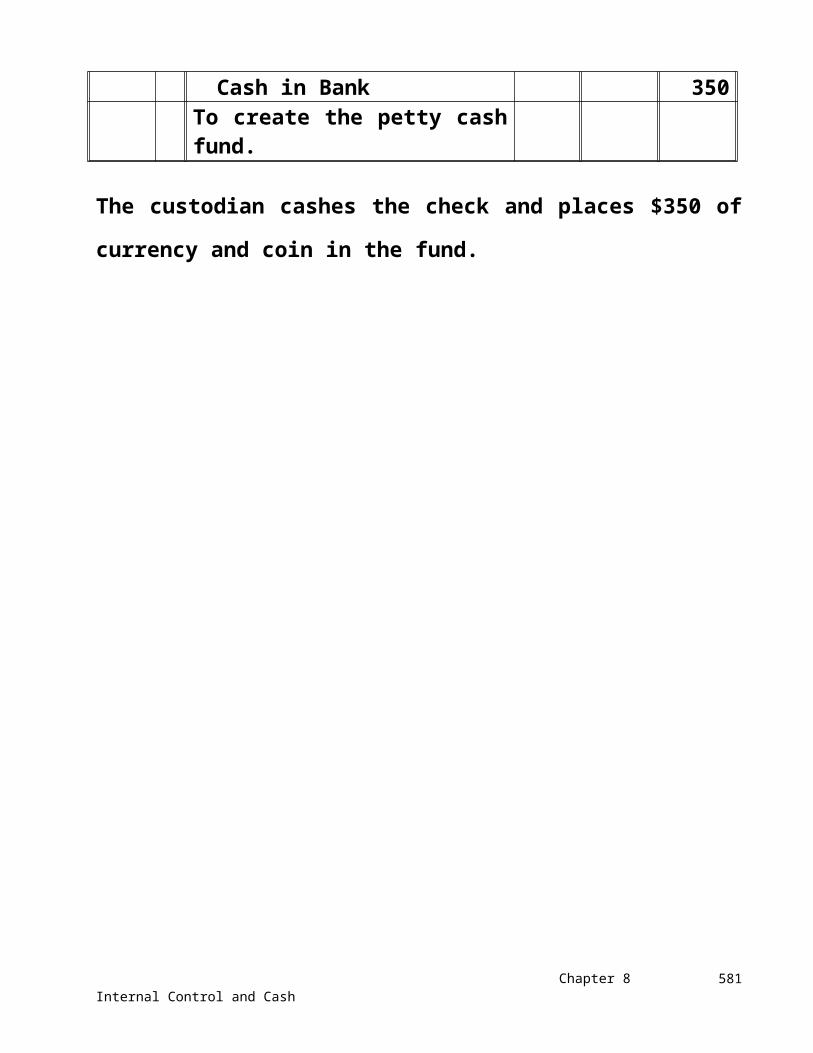

JournalDATE ACCOUNTS AND EXPLANATIONS

POST.REF. DEBIT CREDIT

June 1 Petty Cash 350Cash in Bank 350

To create the petty cash fund.

The custodian cashes the check and places $350 of currency and coin in the fund.

Chapter 8 Internal Control and Cash 563

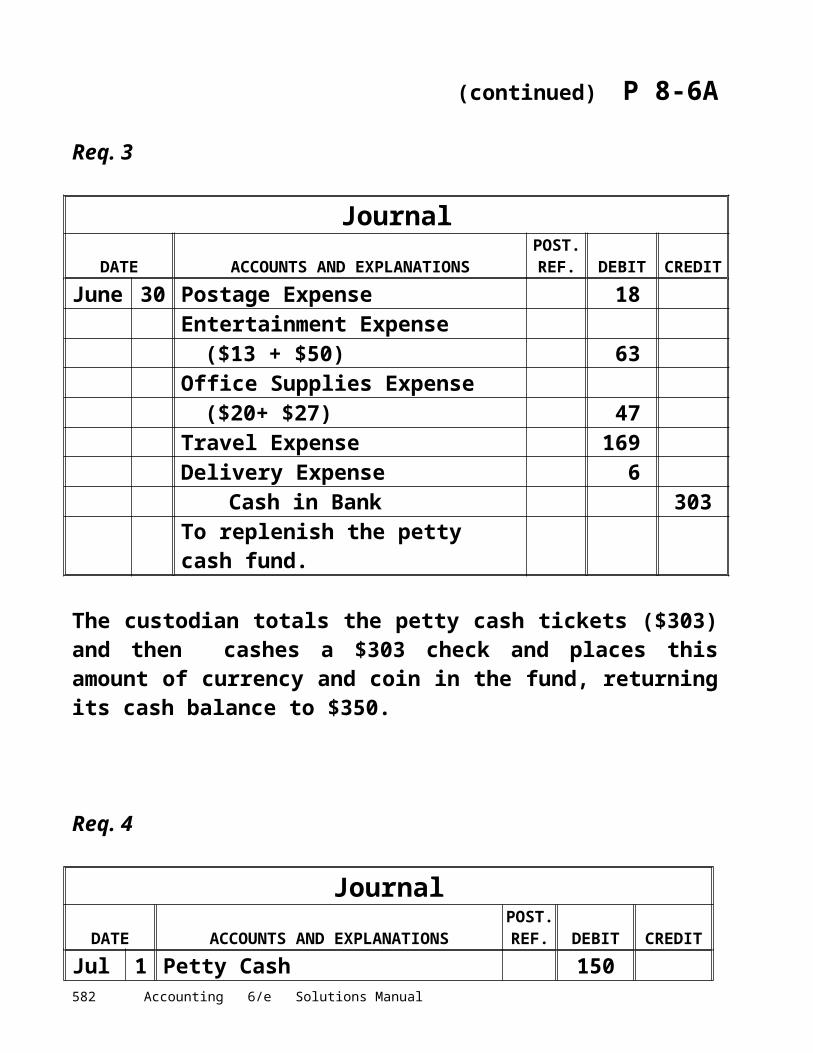

(continued) P 8-6A

Req. 3

JournalDATE ACCOUNTS AND EXPLANATIONS

POST.REF. DEBIT CREDIT

June 30 Postage Expense 18Entertainment Expense

($13 + $50) 63Office Supplies Expense

($20+ $27) 47Travel Expense 169Delivery Expense 6

Cash in Bank 303To replenish the petty cash fund.

The custodian totals the petty cash tickets ($303) and then cashes a $303 check and places this amount of currency and coin in the fund, returning its cash balance to $350.

Req. 4

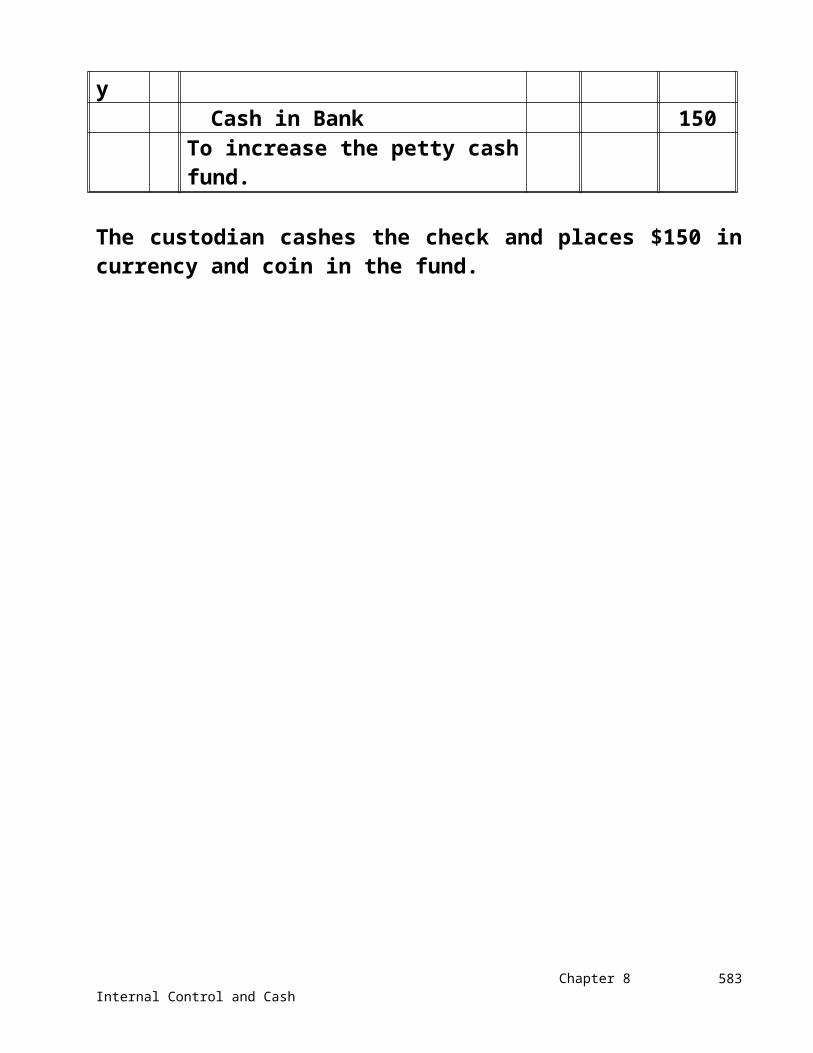

JournalDATE ACCOUNTS AND EXPLANATIONS

POST.REF. DEBIT CREDIT

July 1 Petty Cash 150Cash in Bank 150

To increase the petty cash fund.

The custodian cashes the check and places $150 in currency and coin in the fund.

Accounting 6/e Solutions Manual564

(15-30 min.) P 8-7A

1. Identify the ethical issue. Van Allen’s ethical issue is whether to use his knowledge of Baker’s plans and of Fletcher’s situation to either party’s advantage (or disadvantage). Should Van Allen help Baker buy the land at the lowest price? Should he help Fletcher sell the land at the highest price? Van Allen’s position presents him with a conflict of interest.

2. Specify the alternatives. There are several. Here are a few: (1) Let other members of the Baker board of directors know of Fletcher’s situation in the interest of helping Baker buy the land at a bargain price. (2) Disclose Fletcher’s situation to other board members and insist that Baker pay market price ($5 million) for the land. (3) Reveal nothing to the Baker board and take no part in the negotiation between the two parties. (4) Take a temporary leave of absence from the Baker board for unspecified “personal reasons.”

3. Assess the possible consequences. Disclosing Fletcher’s weakened condition to the Baker board may help Baker buy the land at a low price, depending on the ethical bearing of other board members. This would help Baker and hurt

Chapter 8 Internal Control and Cash 565

(continued) P 8-7A

Fletcher, relative to Fletcher’s ability to sell the land at market value of $5 million. Insisting that Baker offer market price for the land would seem fair to both parties, but that would betray the trust of Fletcher. And it may or may not sway the board to go along with a $5 million offer for the land.

Remaining silent would preserve Van Allen’s integrity. However, if either Baker or Fletcher ever learned of Van Allen’s relationship with the other party, they would wonder whether he used the information against them.

Taking a temporary leave of absence would preserve Van Allen’s integrity and remove him from the conflict of interest. It would also preserve his reputation for fairness and the reputation of Tri-Cities Bank for keeping customer information confidential.

4. Make the decision. The authors would take the leave of absence and hope other Baker board members do not probe Van Allen’s “personal reasons.” This way neither Baker nor Fletcher can accuse Van Allen of using privileged information to the advantage of the other party.

Accounting 6/e Solutions Manual566

Problems

Group B

(15-20 min.) P 8-1B

TO: Company President

FROM: Consultant

RE: Internal controls safeguard assets

Operations should be separated from accounting. Otherwise, operating personnel can manipulate the accounting records to make their performance look better than it really is. This can waste company assets.

Custody of assets should be separated from accounting. Otherwise, an employee can steal an asset and cover the theft by making a false entry on the books.

Internal and external audits validate accounting records, which keep track of assets and protect them from loss.

Chapter 8 Internal Control and Cash 567

(continued) P 8-1B

Electronic sensors attached to merchandise reduce shoplifting.

Job rotation and mandatory vacations keep employees moving from job to job. That way, employees check up on each other’s work.

Student responses may vary.

Accounting 6/e Solutions Manual568

(10-20 min.) P 8-2B

Requirement 1 Requirement 2 Requirement 3

Missing InternalControl

Characteristic Possible Problem Solution

a. Internal and external audits

Unreliable financial statements, lost credibility among investors and lenders.

Have an audit. Auditors should be able to prevent false financial statements.

b. Other controls (fidelity bonds for cashiers)

Theft of cash. Purchase fidelity bonds on all cashiers.

c. Documents (prenumbered invoices)

Theft of cash and inefficiency.

Have receipts prenumbered.

d. Assignment of responsibilities

Lost sales due to delay of product development.

Assign programmers to product development only. Assign company accountants to redesign the accounting system.

e. Separation of duties

Theft of cash. Keep accounting and cash handling duties separate.

Chapter 8 Internal Control and Cash 569

(20-25 min.) P 8-3B

Mailboxes Etc.Bank Reconciliation

March 31, 20X5BANK:

Balance, March 31, 20X5 $17,069Add: Deposit of March 31 in transit 2,038

19,107Less: Outstanding checks:

Check No.1420 $ 9701421 2001422 2,267 (3,437 )

Adjusted bank balance, March 31, 20X5 $15,670

BOOKS:Balance, March 31, 20X5 $14,941Add: EFT collection of rent $ 625

Bank collection of note receivable 1,000 1,625 16,566

Less: NSF check $ 441EFT payment of insurance 340Service charge 25Book error—$216 check

recorded as $126 90 (896 )Adjusted book balance, March 31, 20X5 $15,670

Accounting 6/e Solutions Manual570

(20 min.) P 8-4B

Req. 1

Marlow Furniture Co.Bank Reconciliation

May 31, 20XXBANK:

Balance, May 31 $19,209.82Add:

Deposit of May 31 in transit $381.14Correction of bank error—

charged our account for the check of another company 410 .00 791 .14

20,000.96Less: Outstanding checks ($403.00 +

$74.25 + $36.60 + $161.38 +$229.05 + $48.91) (953 .19 )

Adjusted bank balance, May 31 $19,047 .77

BOOKS:Balance, May 31 $18,200.55Add: EFT—collection on account $200.00

Bank collection of dividend

Chapter 8 Internal Control and Cash 571

revenue 899.14Interest revenue on bank balance 16 .86 1,116 .00

19,316.55Less: NSF check $ 67.50

Returned check due tounauthorized signature 195.03

Service charge 6 .25 (268 .78 )Adjusted book balance, May 31 $19,047 .77

Accounting 6/e Solutions Manual572

(continued) P 8-4B

Req. 2

JournalDATE ACCOUNTS AND EXPLANATIONS

POST.REF. DEBIT CREDIT

May 31 Cash 200.00Accounts Receivable—Jack Oates 200.00

Collection on account.

31 Cash 899.14Dividend Revenue 899.14

Dividend revenue collected by bank.

31 Cash 16.86Interest Revenue 16.86

Interest earned on bank balance.

31 Accounts Receivable—Sarah Batten 67.50Accounts Receivable—Lena Masters 195.03

Cash 262.53Customer checks returned by bank.

31 Miscellaneous Expense 6.25Cash 6.25

Bank service charge.

Chapter 8 Internal Control and Cash 573

(10-15 min.) P 8-5B

TO: Company President

FROM: Concerned Employee

It is unwise to have the employee who opens the mail also grant sales allowances to customers. Suppose a customer pays an invoice in full. The mailroom employee can steal the customer check and grant a sales allowance to cover the theft. To correct this internal control weakness, deny the mailroom employee access to all accounting records. Also, appoint a separate employee to grant sales allowances to customers.

Notes:

1. Student responses may vary.

2. The mailroom employee obviously has access to the accounting records—to know that a customer has paid less than the full amount.

3. It may be necessary to explain to students that the mailroom employee must forge the company endorsement on stolen customer checks. This person must also open—and control—a bank account in the company’s name. Opening such an account may be quite easy.

Accounting 6/e Solutions Manual574

(20-30 min.) P 8-6B

Req. 1

An imprest fund is money set aside for a specific purpose. An imprest fund has the same balance at all times, which equals the sum of cash in the fund plus the total of the tickets that support payments from the fund. The internal control feature of an imprest fund is that it clearly identifies the amount of money for which the fund custodian is responsible.

Req. 2

Before replenishment, the petty cash fund holds cash of $24 ($400 – total payments of $376).

Req. 3

JournalDATE ACCOUNTS AND EXPLANATIONS

POST.REF. DEBIT CREDIT

April 1 Petty Cash 400Cash in Bank 400

To create the petty cash fund.

The custodian cashes the check and places $400 of currency and coin in the fund.

Chapter 8 Internal Control and Cash 575

(continued) P 8-6B

Req. 3

JournalDATE ACCOUNTS AND EXPLANATIONS

POST.REF. DEBIT CREDIT

April 30 Office Supplies Expense($86 + $44) 130

Travel Expense 25Delivery Expense 37Entertainment Expense

($80 + $19) 99Inventory 85

Cash in Bank 376To replenish the petty cash fund.

The custodian totals the petty cash tickets ($376) and then cashes a $376 check and places this amount of currency and coin in the fund. Replenishment brings the fund’s cash balance to $400.

Req. 4

JournalDATE ACCOUNTS AND EXPLANATIONS

POST.REF. DEBIT CREDIT

May 1 Petty Cash 100Cash in Bank 100

To increase the petty cash fund.

The custodian cashes the check and places $100 in currency and coin in the fund.

Accounting 6/e Solutions Manual576

(15-30 min.) P 8-7B

1. Identify the ethical issue. Reed’s ethical issue is whether to tell Cortez personnel about Peters & Sons’ possible bankruptcy.

2. Specify the alternatives. (1) Keep quiet and let nature take its course, or (2) Tell Cortez’s top managers of Peters’ possible bankruptcy.

3. Assess the possible consequences. Telling Cortez about Peters & Sons’ possible bankruptcy may help Cortez avoid wasted effort on Peters & Sons. This may enable Cortez to seek more profitable ventures and aid Cortez’s recovery. In turn, this may help Cortez repay its loan to Tri State.

Revealing this information to Cortez would probably harm Peters & Sons (others may learn also). It may interfere with Peters’ plans. After all, Peters is not bankrupt yet. If others learned that a Tri State Bank officer was the source of this sensitive inside information, the bank’s reputation would suffer.

(continued)

Chapter 8 Internal Control and Cash 577

(continued) P 8-7B

The owners, employees, creditors, depositors, and communities of these organizations would feel the effects of a bankruptcy or other disruption of Peters’, Cortez’s, or the bank's business.

4. Make the decision. Reed should keep quiet. It would be unwise and unethical for him to convey speculative inside information about one client to another client. Peters and Cortez should be free to conduct their affairs without interference caused by any revelations by Reed. Any gain to Cortez (and Tri State Bank) from being able to protect themselves against Peters’ bankruptcy is more than offset by the potential damage to Peters’ viability and to the bank’s reputation.

Accounting 6/e Solutions Manual578

Decision Cases

(15-30 min.) Decision Case 1

a. The main internal control weakness in this case is a lack of separation of duties. The foreman performs too many duties.1. The foreman hires the workers.2. The foreman has workers complete their employment

documents.3. The foreman fills out workers’ time sheets and transmits

all documents to the home office.4. The foreman passes out paychecks to workers.5. The workers never go to the home office, so home-office

personnel do not even know that all workers exist.

The foreman could steal from the company as follows:1. The foreman could enter a fictitious worker into the payroll

system and fill out time sheets for the fictitious employee. Then the foreman could pocket the paycheck written to the employee.

2. The foreman could enter more time than actually worked by an employee and collude with the employee to split the extra pay received by the worker.

3. The foreman could pad his own hours to receive pay for time that he did not work.

Chapter 8 Internal Control and Cash 579

(continued) Decision Case 1

b. The following actions will correct the internal control weakness:1. The home office could have workers come to the office for

processing their employee documents. Then home office would at least know that all workers exist.

2. Use a time clock and have employees sign their own time sheets.

3. Have a home-office employee compare signatures on the workers’ time sheets to their signatures on file and, occasionally, to their endorsements on the backs of their paychecks.

4. Occasionally—or always—have a home-office employee go to the construction site to pass out paychecks.

5. Have a home-office employee go to the construction site occasionally to “take attendance” of workers on duty that day. Then match the names of workers on duty to the time sheets turned in at the end of the week.

Accounting 6/e Solutions Manual580

(20-30 min.) Decision Case 2

Diamondback’s RestaurantBank ReconciliationSeptember 30, 20XX

BANK:Balance, September 30 $3,124Add: Deposit of September 30 in transit 3,794

6,918Less: Outstanding checks ($116 + $150

+ $353 + $190 + $206 + $245) (1,260 )Adjusted bank balance, September 30 $5,658

BOOKS:Balance, September 30 $6,502Add: Bank collection 200

6,702Less: Service charge $ 8

NSF check 36 (44 )Adjusted book balance, September 30 $6,658

Based on the above reconciliation, it appears the cashier has stolen $1,000, the difference between the adjusted book and bank amounts ($6,658 – $5,658). He understated the total of outstanding checks by $1,000 to cover his theft.

Gilbreath should assign another employee with no cash-handling duties to prepare the bank reconciliation. The cashier should not perform this duty because a person who handles cash and also prepares the reconciliation can steal cash and manipulate the reconciliation to cover the theft. Perhaps Gilbreath should prepare the reconciliation herself.

Chapter 8 Internal Control and Cash 581

Ethical Issue

Req. 1

Dilley’s lenders and the potential buyers of the Lansing property can be harmed by this theft. Anyone who relies on Dilley’s financial statements can be harmed by the overstated amounts of cash. Dilley simply does not have as much cash as the balance sheet reports.

Req. 2

Accounting plays the critical role of providing information to persons who do business with Dilley. A common way for a business to represent itself to outsiders is through its financial statements. People commit their resources based on the information reported in these statements. To serve their intended purpose, financial statements must be complete and accurate.

Accounting 6/e Solutions Manual582

Financial Statement Case

(15-20 min.) Financial Statement Case

Req. 1

Ernst & Young LLP in Seattle, Washington, signed the audit opinion on January 17, 2003, which was 17 days after Amazon.com’s year ended on December 31, 2002.

Req. 2

Amazon’s management—not the outside auditors—bears primary responsibility for the financial statements. The audit report mentions management’s responsibility for the statements.

Req. 3

Amazon’s internal controls must have been adequate. Otherwise, Ernst & Young would have referred to any serious control weakness in the audit report.

Req. 4

The auditors used “generally accepted auditing standards” in the examination of the Amazon statements. (That is the norm.) The Amazon statements were evaluated by reference to “generally accepted accounting principles.” (That, too, is the norm.)

Req. 5

Cash increased by $197,972,000 during the year—from $540,282,000 to $738,254,000.

Chapter 8 Internal Control and Cash 583

Team Project

Suggested Answer

1. The team must decide how it will make decisions. Three possibilities are:a. Team decision making. This may be difficult because not

every member of the team will be present all the time.b. One person can be elected as the team leader, or

president, and be given the authority and the responsibility to make decisions.

c. A committee of the team can be given decision-making authority. If so, the team will need to agree how often and when to meet and how decisions will be reached.

The team must decide how it will share and distribute resources to the members, including pay for work performed on a day-to-day basis.

2. One team member should be responsible for arranging the band.

One team member should be responsible for arranging the venue for staging the concert.

One team member should be responsible for arranging for concessions to be sold at the concert.

Accounting 6/e Solutions Manual584

(continued) Team Project

One team member should be responsible for arranging security for the concert.

One team member should be responsible for handling the cash.

One group member should be responsible for arranging corporate sponsorships for the concert.

It may be best to hire an outside accountant in order to separate accounting from the (a) operational aspects of the business and (b) handling of business assets.

3. A different person may perform each duty, or one person may perform more than one duty. The important points are that Each major duty should be assigned to someone in order

to ensure that all important duties get done well and on a timely basis.

The accountant should have no other major responsibility.

Chapter 8 Internal Control and Cash 585