Embed Size (px)

Citation preview

Claims Predictive Modeling

Debashish BanerjeeAbhimanyu Dasgupta

Redefining the Claim Process

26th M 201126th May 2011

1

Table of Content

Introduction to Predictive Modeling

Background and Objectives

▪ Introduction to Predictive Modeling▪ Introduction to Predictive Modeling

g j

Claim Segmentation

Claim Business Applications

• Surveyor Assignment and Medical Case Management

• Soft and Hard Fraud

• Reserving• Reserving

• Business Competitive Advantage

Indian General Insurance Industry

Questions and Answers

2

Introduction to Predictive Modeling

HighPredictive modeling is not a new concept. Companies

(27)

Analytics &

ModelingForesight

p pacross various industries across the globe are using predictive modeling to increase organi ational

(38)

(444)

Modeling

Performancemanagement

Foresightincrease organizational effectiveness to capture immediate economic benefits.

(444)

(413)

management

Business

Insight•Harrah’s is using it to customize customer promotions to maximize client response and subsequent gaming revenues.

Hindsight

Intelligence

Data Low

•Capital one is using it to identify financial transactions with a high fraudulent potential to shut down credit as quickly

3

Management as possible.

Introduction to Predictive Modeling

Predictive modeling is a process for transforming data insights into an estimation of future outcomes upon which actionable decisions can be made.

Th d li i li h d b l i d d li b th t diti l• The modeling process is accomplished by analyzing and modeling both traditional and non-traditional data sources namely historical operational data supplemented by relevant public external data.

• The model quantifies the impact a variable has on the item being modeled• The model quantifies the impact a variable has on the item being modeled. • Models provide the reasons behind a certain outcome and enable us to proactively

predict what will happen. • Models allow for a more objective and meaningful way to manage and handle• Models allow for a more objective and meaningful way to manage and handle

claims.

Predictive Modeling is a well established technology with specific application toPredictive Modeling is a well established technology with specific application to insurance. Leading global carriers including Chubb, Liberty, Progressive have effectively used predictive models for underwriting and predictive models for claims are quickly emerging

4

claims are quickly emerging.

Table of Content

Introduction to Predictive Modeling

Background and Objectiv▪ Background and Objectives▪ Background and Objectivesg j

Claim Segmentation

Claim Business Applications

Background and ObjectivesBackground and Objectives

• Surveyor Assignment and Medical Case Management

• Soft and Hard Fraud

• Reserving• Reserving

• Business Competitive Advantage

Indian General Insurance Industry

Questions and Answers

5

Introduction to Predictive Modeling for Claims

Claim predictive modeling uses a sophisticated algorithm to effectively predict claim outcomes by level of exposure (claim segmentation)

(27)

As part of model development, several variables are analyzed to measure their correlation to claim outcomes

The model utilizes multiple risk characteristics

(38)

(444)

from both internal and external (public) data sources

At claim intake, the predictive model immediately produces ascore of 1–100 that indicates future severity as well as reason Below

Average claim outcomes

Claims projected to have high exposure

Below

Average claim outcomes

( )

(413)

ycodes that describe the factors driving the score

Scoring of claims continues on an ongoing basis as updated data is received and claim developments occur

average claim exposureaverage claim exposure

developments occur

Models are unique by line of business as the requirements, variables and algorithms vary for each. In this presentation, we will look at a Motor and Health Insurance example to observe

6

the application of Claims predictive modeling

Claims Model – Business Applications

Multiple business applications are enhanced by Claim Predictive Modeling, including optimal assignment of claims to the right claim resource, soft and hard fraud detection, and reserving guidance.

Soft & HardSurveyor Medical Case

ese g gu da ce

Soft & Hard Fraud Detection

Surveyor Assignment

Medical Case Management

B iBusiness Competitive Advantage

Set / AdjustReserves

RIGHT CLAIM RIGHT RESOURCE

7

Loss Cost Reduction Expense Reduction Improved Customer Service

Table of Content

Introduction to Predictive Modeling

Background and Objectivesg j

Claim Segmentation

Claim Business Applications

▪ Claim Segmentation▪ Claim Segmentation

• Surveyor Assignment and Medical Case Management

• Soft and Hard Fraud

• Reserving• Reserving

• Business Competitive Advantage

Indian General Insurance Industry

Questions and Answers

8

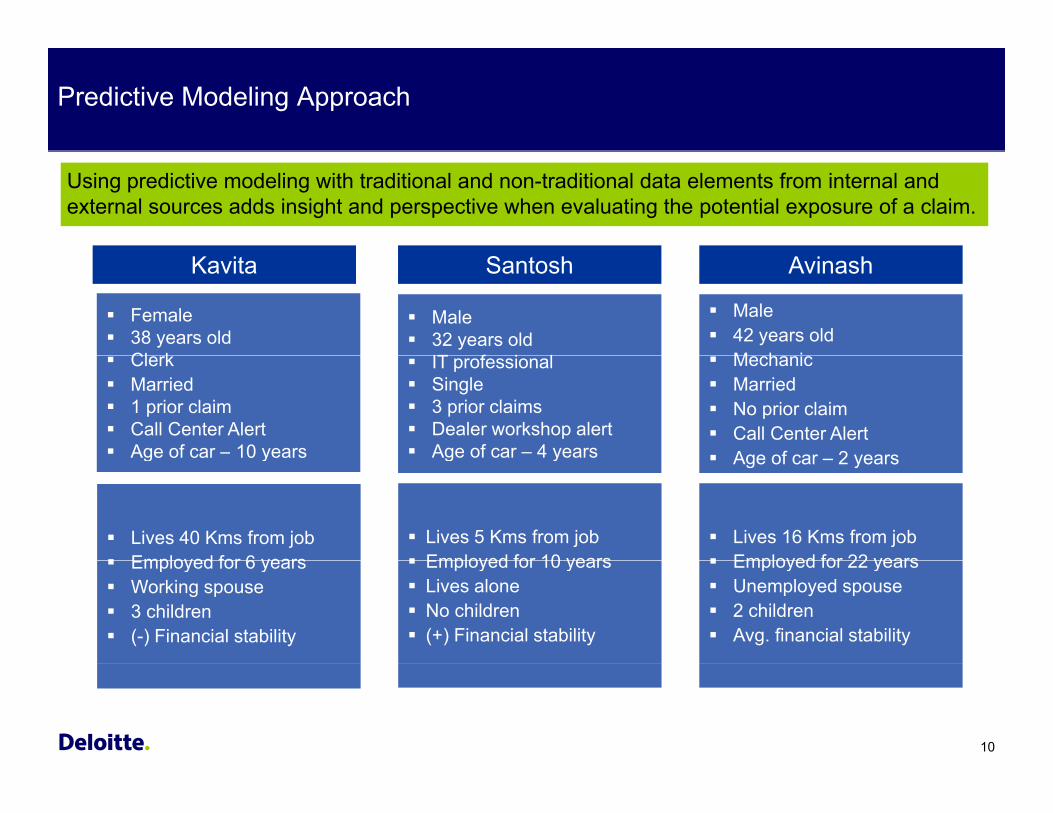

Traditional Approach – Motor Insurance

An example follows that demonstrates the value of predictive modeling in Motor insurance

First Notice of Loss information is evaluated by a Claim surveyor when assessing claim exposure and assigning the claim. Below are three soft-tissue back claims. Which claim is likely to be most costly?

Kavita AvinashSantosh

Female Male42 ld

Male38 years oldClerk2 prior claimEmployed 6 yearsCall Center Alert

42 years oldMechanicNo prior claims Employed 3 yearsDealer workshop alert

32 years oldIT profesional3 prior claimsEmployed 2 yearsDealer workshop alertCall Center Alert

Age of car – 10 yearsDealer workshop alertAge of car – 2 years

Dealer workshop alertAge of car – 4 years

9

Predictive Modeling Approach

Using predictive modeling with traditional and non-traditional data elements from internal and external sources adds insight and perspective when evaluating the potential exposure of a claim.

Kavita AvinashSantosh

Female38 years oldCl k

Male42 years oldM h i

Male32 years oldIT f i lClerk

Married 1 prior claimCall Center AlertAge of car – 10 years

MechanicMarriedNo prior claimCall Center AlertAge of car 2 years

IT professionalSingle3 prior claimsDealer workshop alertAge of car – 4 years

Lives 40 Kms from jobEmployed for 6 years

Lives 16 Kms from jobEmployed for 22 years

Lives 5 Kms from job Employed for 10 years

g y Age of car – 2 yearsg y

Employed for 6 yearsWorking spouse3 children(-) Financial stability

Employed for 22 yearsUnemployed spouse2 childrenAvg. financial stability

Employed for 10 yearsLives aloneNo children(+) Financial stability

10

Identifying High Exposure Claims

With predictive modeling, a more complete set of data can be automatically assimilated to accurately segment claims at the point of intake. In this example Kavita’s claim, which may represents the greatest exposure to an insurance company, can be assigned and managed

ff ti l

KAVITA

more effectively.

SANTOSH

AVINASHutco

me

AVINASH

Cla

im O

u

11

LOW HIGHEXPOSURE

Integrating Data Sources

By combining Data sources available at various levels, enhanced segmentation can be achieved.

Claimant DataClaimant Data

Claimant Specific Information

Line of Business DataLine of Business Data

Product Coverage & OptionsClaimant Specific InformationEmployment & Personnel InfoDriving & License records

Product, Coverage & OptionsExperience DataPolicy Data

Claims DataClaims Data

LossesF

NonNon--Traditional DataTraditional Data

Geographic / DemographicE l t R dFrequency

Timing/PatternsSettlement Data

Employment RecordsIndustry Claims

12

The Mechanics of Modeling - Motor

Upon claim intake, the model instantly produces a score of 1 to 100 that indicates the future severity relative to an injury type. Reason codes are generated that explain each score.

w1(Prior Claims) + w2(Distance to work) +w3(CC/Dealer Alert)+ w4(HH Income) + w5(Marital Status) + w6(Claimant Age)…

Sample Model Equation~35-50 Variables

Examples:Claimant ageMarital statusMarital statusDriving historyAccident date / timeVehicle claims historyDealer workshop data

Score

92

Sample Reason CodesFinancial InstabilityVehicle Claims HistoryClaimant Agep

Call Center/Dealer AlertFinancial stabilityYears of employmentVehicle make/type Average claim Claims

Claimant Age

Belowaverage claim exposure

goutcomes projected to

have high exposure

13

Table of Content

Introduction to Predictive Modeling

Background and Objectivesg j

Claim Segmentation

Claim Business Applications▪ Claim Business Applications▪ Claim Business Applications• Adjuster Assignment and Medical Case Management

• Soft and Hard Fraud

• Reserving

▪ Adjuster Assignment and Medical Case Management▪ Adjuster Assignment and Medical Case Management

• Reserving

• Business Competitive Advantage

Indian General Insurance Industry

Questions and Answers

14

Assigning Claims: Today’s Approach

Basic data elements combined with the experience and instincts of the claim supervisor typically determine claim assignment. Supervisors are challenged to accurately match claim complexity to adjuster skill level at initial assignment.

Accident Claim Report

ClaimIntake

Supervisors evaluate available data Supervisors evaluate available data points to assess claim and determine the points to assess claim and determine the appropriate assignment and action stepsappropriate assignment and action steps

AgeGenderInjury

Treating Dr. Occupation

Claims History

Claimant:Chitra

32 AmeerpetHyderabad, AP

Surveyor Assignment

15

Assignment of the wrong surveyor results in longer claim processing, supervisory involvement and higher loss costs.

Assigning Claims: Predictive Modeling Approach

Model score and reason codes combined with the experience and instincts of the claim supervisor determine claim assignment. Supervisors are more effective at accurately matching claim complexity to adjuster skill level at the outset of the claim.

InstantlyScored

Accident Claim Report

ClaimIntake

Supervisors evaluate model output to Supervisors evaluate model output to assess claim and determine the assess claim and determine the

appropriate assignment and action stepsappropriate assignment and action steps

Score

87

Sample Reason CodesFinancial InstabilityEmployment HistoryDr. treatment patterns

Claimant:

Chitra32 Ameerpet

Hyderabad, AP

Surveyor Assignment

16

Initial assignment of appropriately skilled surveyors reduces processing duration, less supervisory involvement and lower loss costs.

Optimal Resource Deployment

Matching technical competency to claim complexity optimizes resource deployment, decreasing loss costs and controlling loss adjustment expense. Predictive Modeling enhances insight at claim intake, promoting claim assignment consistent with exposure.

Current

HIGH(ex : category A)OVERQUALIFIED

resources on LOW exposure claims

Resource Deployment

With PredictiveModeling

RESOURCERESOURCE COMPETENCY

LOW(ex : category C)

UNDERQUALIFIED resources on HIGH

exposure claims

17

CLAIMS COMPLEXITY

LOW HIGH

Table of Content

Introduction to Predictive Modeling

Background and Objectivesg j

Claim Segmentation

Claim Business Applications▪ Claim Business Applications▪ Claim Business Applications• Surveyor Assignment and Medical Case Management

• Soft and Hard Fraud

• Reserving

• Soft and Hard Fraud• Soft and Hard Fraud

• Reserving

• Business Competitive Advantage

Indian General Insurance Industry

Questions and Answers

18

Soft and Hard Fraud

With Predictive Modeling we will identify fraud and refer the claim to Fraud experts in less time. Under normal circumstances, fraud identification could take 3 times longer. Addressing suspicious claims from the start will allow us to decrease malingering behavior, reducing claim duration.

PreventedActivity

High

Additional reduced loss and expense costs

Activity

ut /

evel

Mod

el O

utp

uspi

cion

le

Fraud First Fraud First

First Investigation

M Su

Low

Identified with model

Identified in normal scenario

19

DurationNormal CloseDate

Model CloseDate

Table of Content

Introduction to Predictive Modeling

Background and Objectivesg j

Claim Segmentation

Claim Business Applications▪ Claim Business Applications▪ Claim Business Applications• Surveyor Assignment and Medical Case Management

• Soft and Hard Fraud

• Reserving• Reserving• Reserving• Reserving

• Business Competitive Advantage

Indian General Insurance Industry

• Reserving• Reserving

Questions and Answers

20

Predictive Modeling versus Manual reserves(Source – a US WC Insurance Industry Analysis)

The manual reserves display a wide i i f d d i

ManualPaid

Reserves at 180 days from receipt of loss relative to ultimate paid

INR 1 00 000 variation of over- and under-reserving$100,000

High severityunder-reserved

claims

INR 1,00,000

1/11/101/1001/1000 10/1 100/1 1000/1$100

Low severityover-reserved

claims

INR 1,000

Predictive model predictions are closer to the actual final cost of each claim

1/11/101/1001/1000 10/1 100/1 1000/1

Predictive Model$100,000INR 1,00,000

21

$1001/11/101/1001/1000 10/1 100/1 1000/1

INR 1,000

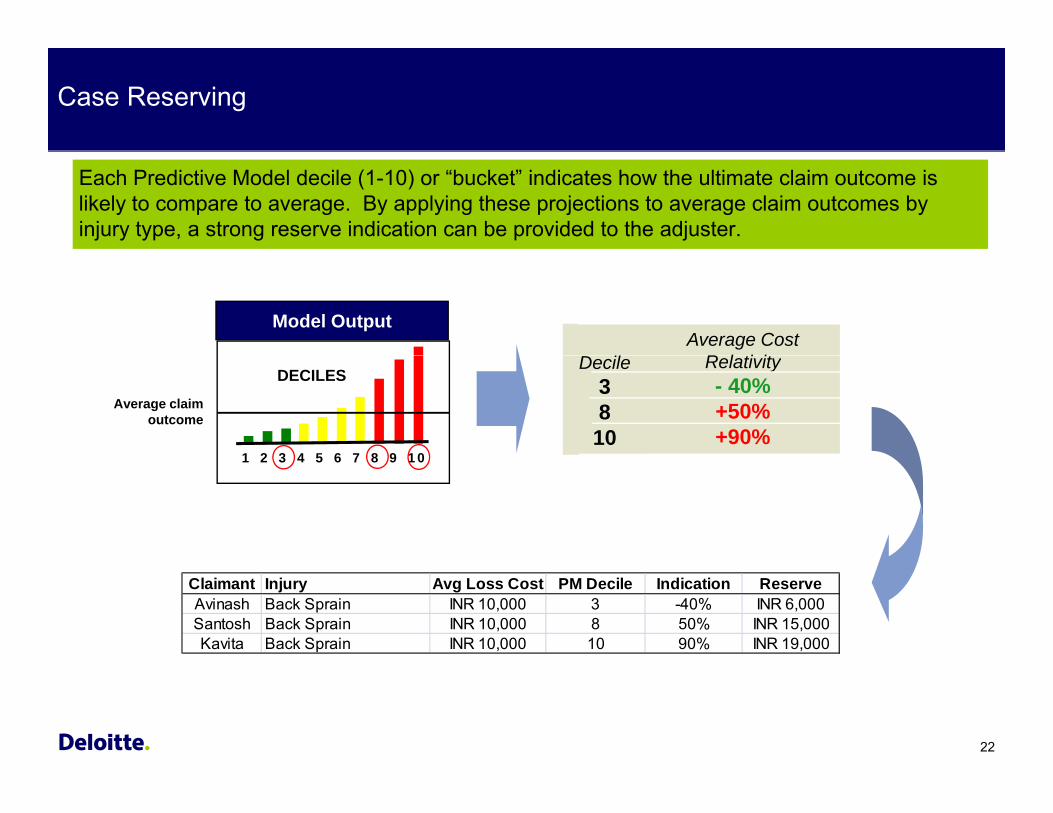

Case Reserving

Each Predictive Model decile (1-10) or “bucket” indicates how the ultimate claim outcome is likely to compare to average. By applying these projections to average claim outcomes by injury type, a strong reserve indication can be provided to the adjuster.

Model OutputAverage Cost

R l ti it

1 2 3 4 5 6 7 8 9 10

DECILESDecile

3810

Relativity- 40%+50%+90%

Average claim outcome

1 2 3 4 5 6 7 8 9 10

Claimant Injury Avg Loss Cost PM Decile Indication ReserveAvinash Back Sprain INR 10,000 3 -40% INR 6,000Santosh Back Sprain INR 10,000 8 50% INR 15,000Kavita Back Sprain INR 10,000 10 90% INR 19,000

22

Table of Content

Introduction to Predictive Modeling

Background and Objectivesg j

Claim Segmentation

Claim Business Applications▪ Claim Business Applications▪ Claim Business Applications

• Surveyor Assignment and Medical Case Management

• Soft and Hard Fraud

• Reserving• Reserving

• Business Competitive Advantage

Indian General Insurance Industry

• Business Competitive Advantage• Business Competitive Advantage

Questions and Answers

23

Business Competitive Advantage

Leveraging predictive model output and ensuing business process data provides powerful new insight to our business.

Management Information Customer Benefits

Claim Portfolio Management (prospective trend analysis by model score)

Insured benefits from reduced claimant loss costs

model score)

Performance Management (comparing actual claim outcomes to averages for the model score)

Differentiation of your offering for clients with loss sensitive programs (by identifying claim cost drivers and improving g )

Business Intelligence for Underwriting and Actuarial

reserve timeliness and accuracy)

Reduced Turn Around Time

24

Table of Content

Introduction to Predictive Modeling

Background and Objectivesg j

Claim Segmentation

Claim Business Applications

• Surveyor Assignment and Medical Case Management

• Soft and Hard Fraud

• Reserving• Reserving

• Business Competitive Advantage

Indian General Insurance Industry▪ Indian General Insurance Industry▪ Indian General Insurance Industry

Questions and Answers

yy

25

Indian General Insurance Industry

There are several areas that could to be focused on in the Indian General Insurance market in order to enable more efficient Claims Handling through Segmentation and Analytics. A few key strategies that could potentially help reach such a position are -

Apply Advanced Data

Management T h i

Apply Advanced Segmentation &

Analytics

Identify non-traditional Data

Sources

g p y p p

Develop Scoring System & Reason Code ProcessesTechniques AnalyticsSources

Use advanced IT resources to build a database that

-CIBIL Data sources for credit history

Use segmentation techniques to differentiate between

Code Processes

Design a scoring engine that-Is in sync with the

-is more efficiently managed-Easier to access data from-Cleaner

history-Statistics from other paid vendors-Pool and combine industry data

differentiate between handling bigger and smaller claims – thus reducing costs

Is in sync with the comprehensive database-Outputs a score instantly for any claim entered

“ f

-Outputs reason messages about why a score is high or low

26

Predictive modeling implementation is “an evolution, not a revolution” although the pace of change should reflect the significant business impact that exists.

Table of Content

Introduction to Predictive Modeling

Background and Objectivesg j

Claim Segmentation

Claim Business Applications

• Adjuster Assignment and Medical Case Management

• Soft and Hard Fraud

• Reserving• Reserving

• Business Competitive Advantage

Next Steps – Indian GI Market

▪ Questions and Answers▪ Questions and Answers

27

Questions

28