Embed Size (px)

Citation preview

Copyright © 2008 Pearson Education Canada12-1

Chapter 12

Home Mortgages

Copyright © 2008 Pearson Education Canada 12-2

To Rent or Buy a Home? No easy answer Depends on the individual

Financial circumstances Social circumstances

Copyright © 2008 Pearson Education Canada 12-3

Costs of Renting a Home Rental payment Tennant’s insurance Security deposit Opportunity cost of security

deposit

Copyright © 2008 Pearson Education Canada 12-4

Advantages of Renting a Home Mobility Fewer responsibilities Little or no maintenance Lower initial and ongoing costs Income-tax implications

Capital gain on principal residence not taxable

Copyright © 2008 Pearson Education Canada 12-5

Disadvantages of Renting a Home Limitations on remodeling Smaller space Restrictions on

Noise, pets, etc. Not building equity

Copyright © 2008 Pearson Education Canada 12-6

Costs of Buying a Home Down payment Mortgage payment Opportunity cost of down payment Home insurance Property tax Closing costs Maintenance and upkeep

Copyright © 2008 Pearson Education Canada 12-7

Advantages of Buying a Home Pride of ownership Possible capital gains from sale Payments going to equity No limitation to remodeling

Copyright © 2008 Pearson Education Canada 12-8

Disadvantages of Buying a Home Major commitment

Financial and time Large opportunity costs Limited mobility Responsible for maintenance and

repairs Higher insurance and property taxes Higher living costs

Copyright © 2008 Pearson Education Canada 12-9

The Price of Home You Can Afford Depend on Size of down payment The interest rate on the loan The amortization period The mortgage features

Copyright © 2008 Pearson Education Canada

12-10

Financing a Home Home is used as security of the loan Borrower signs a contract

Mortgage Borrower

Mortgagor Lender

Mortgagee

Copyright © 2008 Pearson Education Canada

12-11

Mortgage Contract Mortgagee (financial institution)

Retains ownership of property May sell mortgage Mortgagor’s permission not required

Mortgagor (homeowner) Retains possession Has equity of redemption

Copyright © 2008 Pearson Education Canada

12-12

Equity of Redemption Mortgagor’s right to redeem the

property Ownership transferred back

To mortgagor When mortgage is discharged

Copyright © 2008 Pearson Education Canada

12-13

Mortgage Repayment Amortization period

Time to completely pay off the mortgage

Mortgage term Time before lender can demand

Repayment of all the principal Payments

Equal blended payments Principal + interest

Copyright © 2008 Pearson Education Canada

12-14

Renewing the Mortgage At end of mortgage term

Balance has to be paid off, or Mortgage has to be renewed

Can transfer to another financial institution

Pay off part of the principal

Copyright © 2008 Pearson Education Canada

12-15

Mortgage Claims First mortgage

Offered by major financial institutions This claim has top priority

Second & later mortgages When down payment & first mortgage loan

Are not enough to buy house Rates are much higher Terms are always shorter Second mortgagee receives equity of

redemption

Copyright © 2008 Pearson Education Canada

12-16

Mortgage Options Open mortgages Closed mortgages

Copyright © 2008 Pearson Education Canada

12-17

Open Mortgages Prepay some or all of the balance

Prior to maturity Without penalty Wide range of terms

Copyright © 2008 Pearson Education Canada

12-18

Closed Mortgages Cannot prepay in full prior to

maturity Prepayments subject to interest

penalty Although certain prepayments can be

made Under prepayment options Without penalty

Copyright © 2008 Pearson Education Canada

12-19

Basic Types of Residential First Mortgages Conventional mortgages Insured mortgages

Copyright © 2008 Pearson Education Canada

12-20

Conventional Mortgages 25% or more down payment Loans up to 75 % of the smaller of

Appraised value of property Purchase price of property

Mortgage insurance not required

Copyright © 2008 Pearson Education Canada

12-21

Insured Mortgages 5% down payment Loans up to 95 % of property’s value Compulsory mortgage insurance

Protection for financial institution In event borrower defaults on loan

Provided by CMHC Genworth Financial Canada

Copyright © 2008 Pearson Education Canada

12-22

Mortgage Life Insurance Differs from mortgage insurance Protection for survivor

In event mortgagor dies Insurer pays off balance of mortgage Insured age requirement

Less than 65 years of age to qualify Premiums based on

Age and mortgage balance

Copyright © 2008 Pearson Education Canada

12-23

Assumption of an Existing Mortgage Take over the existing mortgage When buying a “used” house Assume the mortgage on the house

Involves a formal agreement Pick up payments where vendor left

off Vendor still responsible for payments

Unless specifically released by financial institution

Copyright © 2008 Pearson Education Canada

12-24

Closing Costs Purchase price Appraisal fees Survey fees Legal fees

Title search Document registration

Copyright © 2008 Pearson Education Canada

12-25

More Closing Costs 6% GST

On new houses Adjustments

Pro-rated items Property taxes Fuel Electricity Cable

Copyright © 2008 Pearson Education Canada

12-26

Mortgage Life Insurance Decreasing term Life insurance policy Discharge mortgage Same amount as the balance

Copyright © 2008 Pearson Education Canada

12-27

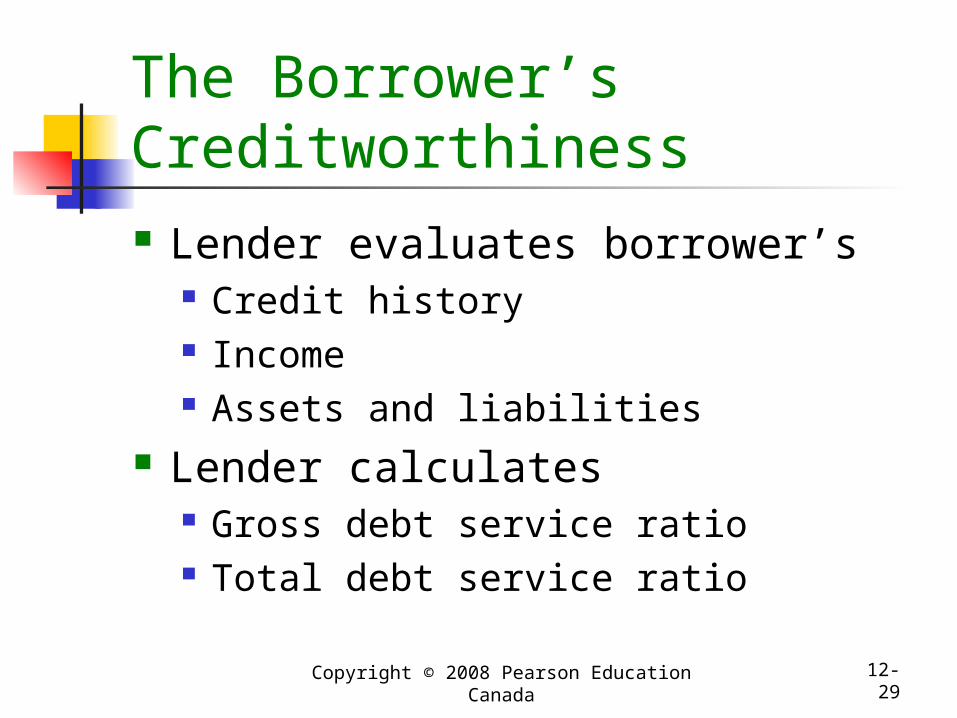

Qualifying for a Mortgage Depends Upon Two Criteria The quality of the property The borrower’s creditworthiness

Copyright © 2008 Pearson Education Canada

12-28

The Quality of the Property Lender appraises the property

Determines the lending value May differ from selling price

Mortgage loan based on The appraised value

Copyright © 2008 Pearson Education Canada

12-29

The Borrower’s Creditworthiness Lender evaluates borrower’s

Credit history Income Assets and liabilities

Lender calculates Gross debt service ratio Total debt service ratio

Copyright © 2008 Pearson Education Canada

12-30

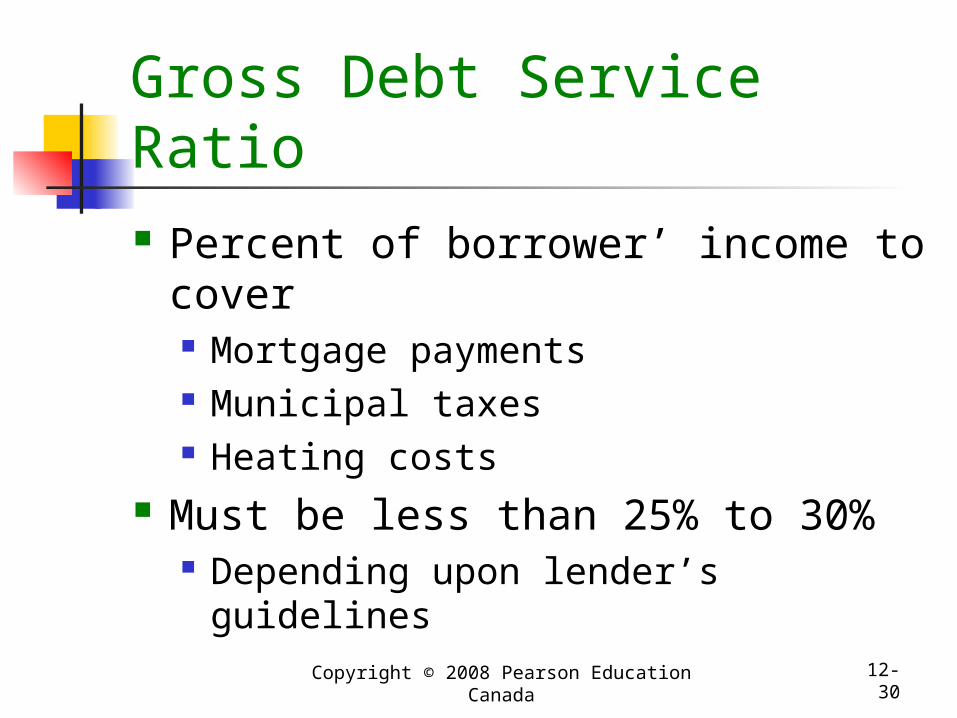

Gross Debt Service Ratio Percent of borrower’ income to

cover Mortgage payments Municipal taxes Heating costs

Must be less than 25% to 30% Depending upon lender’s guidelines

Copyright © 2008 Pearson Education Canada

12-31

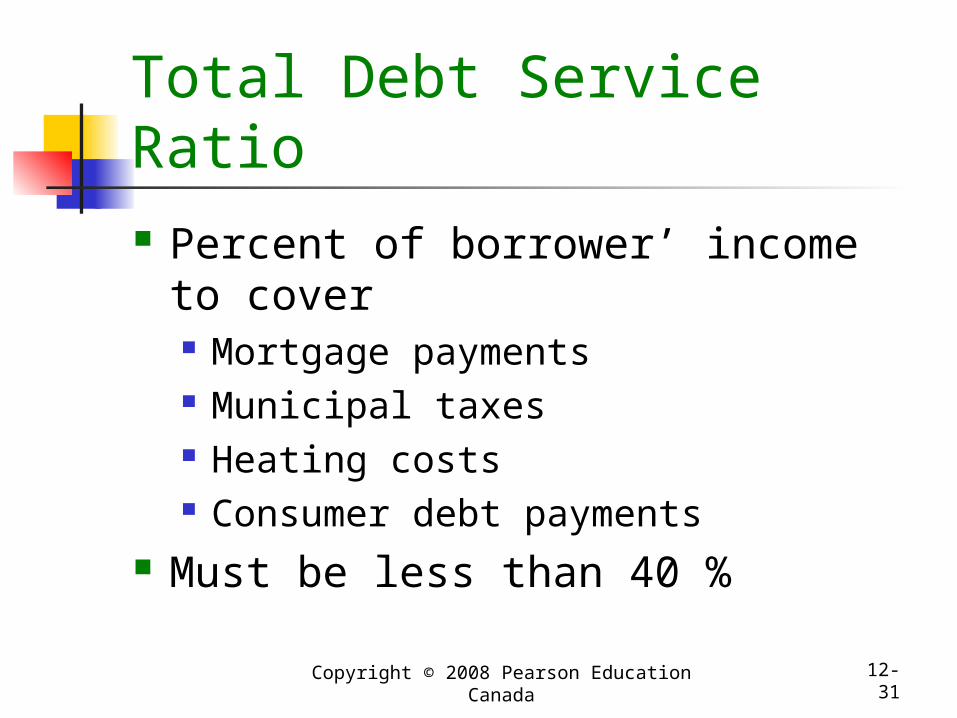

Total Debt Service Ratio Percent of borrower’ income to

cover Mortgage payments Municipal taxes Heating costs Consumer debt payments

Must be less than 40 %

Copyright © 2008 Pearson Education Canada

12-32

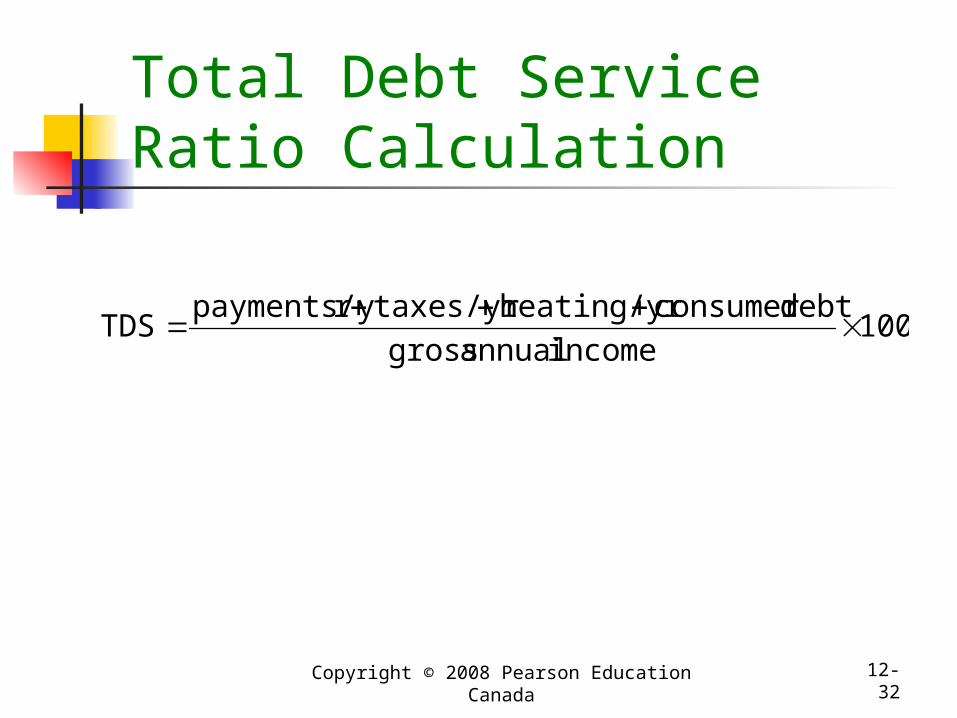

Total Debt Service Ratio Calculation

100income annual gross

debtconsumer heating/yrtaxes/yrrpayments/yTDS

Copyright © 2008 Pearson Education Canada

12-33

Reverse Mortgages Canadian Home Income Plan (CHIP

) Home equity

Used as collateral for a loan Eligibility

Homeowners At least aged 60

Specified geographical area

Copyright © 2008 Pearson Education Canada

12-34

Copyright © 2008 Pearson Education Canada

12-35

Copyright © 2008 Pearson Education Canada

12-36

Copyright © 2008 Pearson Education Canada

12-37