Embed Size (px)

Citation preview

Corporate finance

• SEC1. 宋泰青 summarize the theoretical arguments.

• SEC 2. 王宗正 discribe the data.

• SEC3. 林冠甫 empirical findings.

• SEC4. 楊政彥 conclusions.

Agency problems and dividend policies around the world

• compare two agency models:

1.outcome model:divd are paid by the minority outsiders pressure insider to disgorge cash.

2.substitute model:divd are paid for estabilsh reputation

Divd puzzle

• depend on MM theory,the divd policy is no relation to firm value,so in perfect world,no divd puzzle.

• In real world,we face a divd puzzle:how firm choose their divd policy?

explanations of divd puzzle

• predict firm’s growth: firm can convey the future profitability by paying divd, initially , empirically successful,because if the divd increases(decreases),the stock price will go up(down).But recent result,the divd can not help predict firm’s growth.

• agency problems :divd policy addresses agency problems between insiders and outsiders.the insiders may divert the cash to hurt outsiders.So the outsiders prefer for divd

eliminate two assumptions of MM

• the investment policy is dependent on divd policy

• The allocation of all profits of the firm to the shareholders on a pro rata basis can not be taken for granted.

address agency problem

• mainly use the law to explain the divd policy and agency problems.

• common law have better protection for investors,so the outsiders can get higher divd than civil law’s which has weaker protection.

• disscuss the relation between different growth opportunities and the divd policy.

Theoretical Issue

A. Agency problems and Legal RegimeBerle and Means(1932),Jensen&Meckling(1976):conflicts of interest between corporate insiders and outside investors.

Detriment:Divert corporate asset to insider.Dilution of outsider inverstor through share issue to insider.Asset sales to themselves or other corporations insider con

trol.Transfer pricing with other entities insider control.

Definition of Insider:

1.U.S. U.K. Canada Australia:Ownership in large corporation is relative dispersed.=>Manager control.2.Other countries:=>Founding families control.

Victims:Victims of insider control are minority shareholders.

Remedies:=>Law

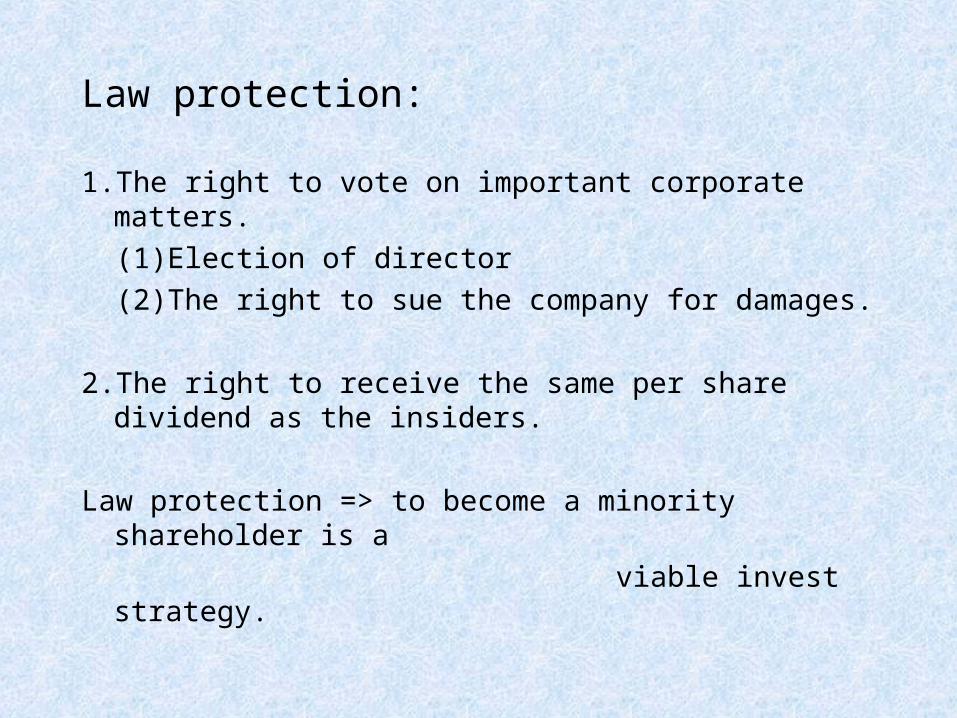

Law protection:

1.The right to vote on important corporate matters.

(1)Election of director

(2)The right to sue the company for damages.

2.The right to receive the same per share dividend as the insiders.

Law protection => to become a minority shareholder is a

viable invest strategy.

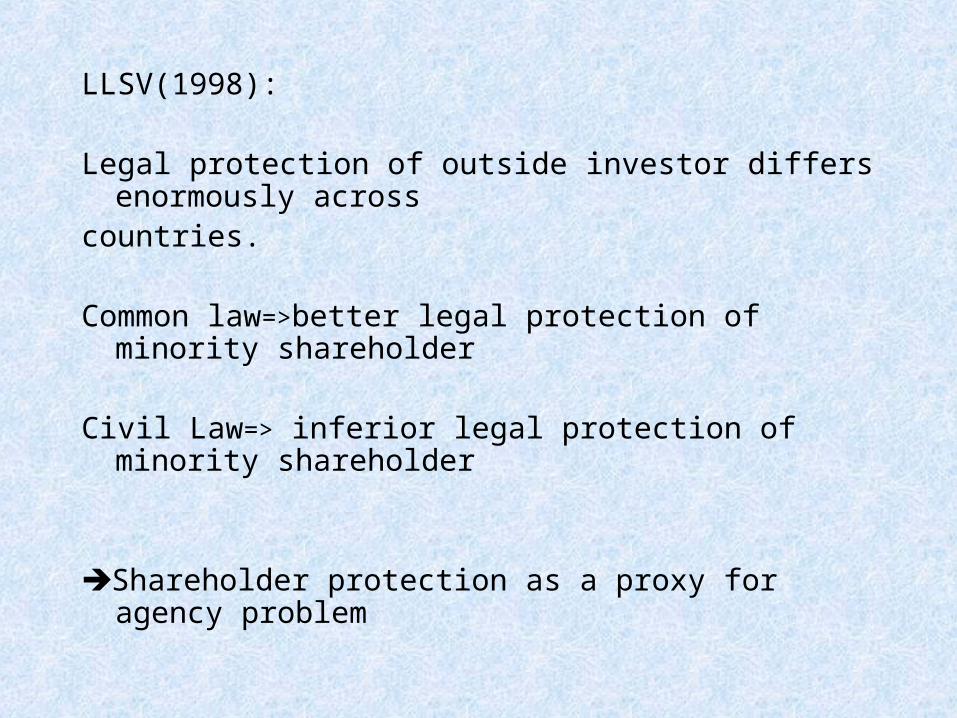

LLSV(1998):

Legal protection of outside investor differs enormously across

countries.

Common law=>better legal protection of minority shareholder

Civil Law=> inferior legal protection of minority shareholder

Shareholder protection as a proxy for agency problem

B. Agency and Dividends: Two Views

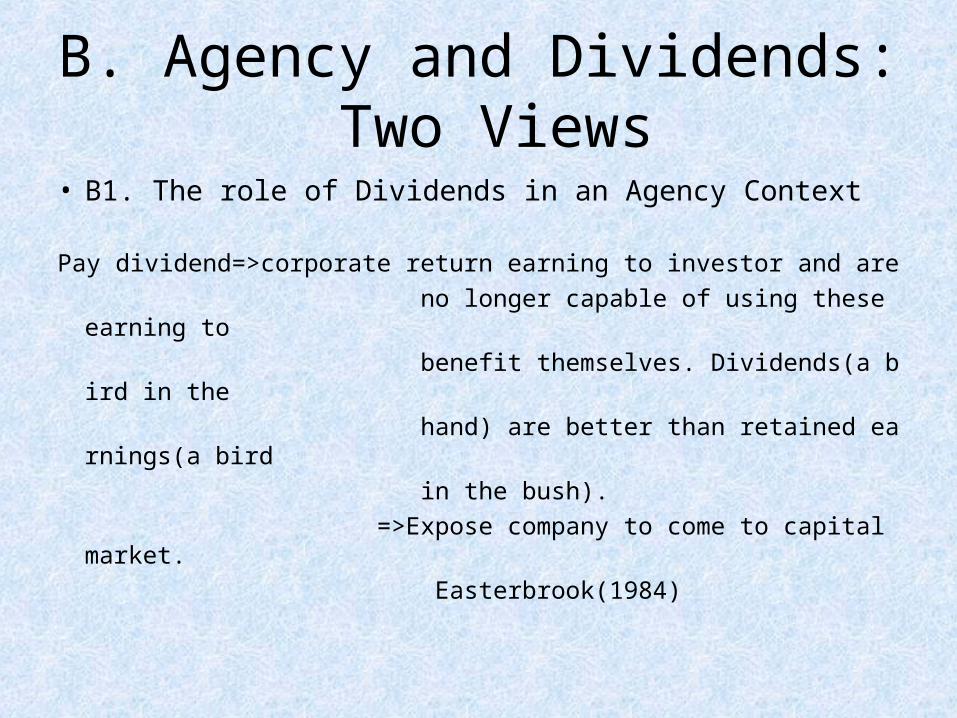

• B1. The role of Dividends in an Agency Context

Pay dividend=>corporate return earning to investor and are

no longer capable of using these earning to

benefit themselves. Dividends(a bird in the

hand) are better than retained earnings(a bird

in the bush).

=>Expose company to come to capital market.

Easterbrook(1984)

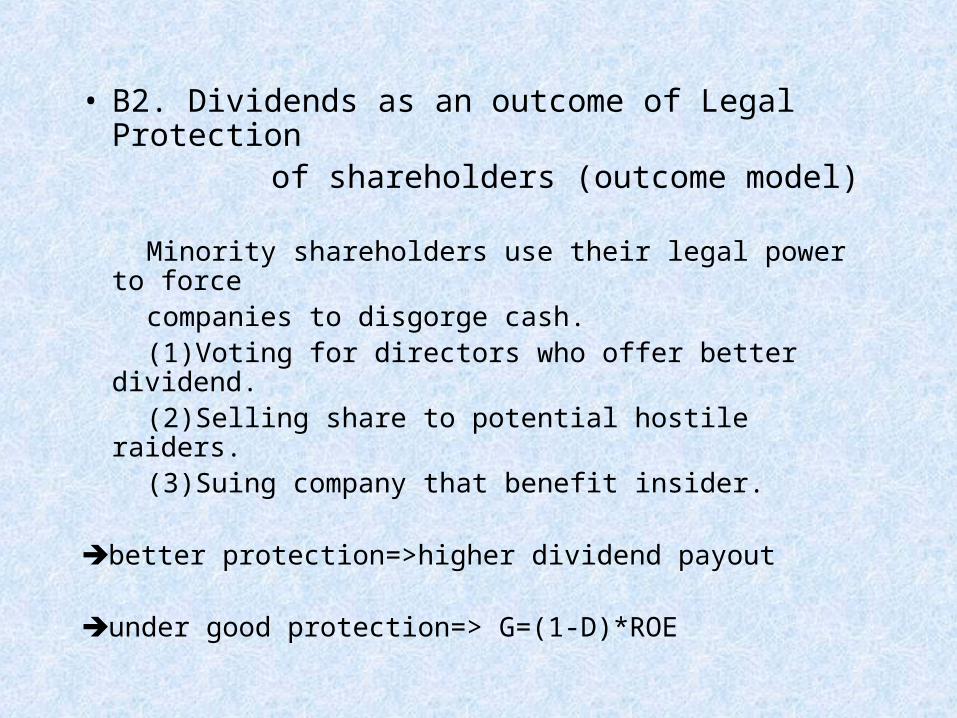

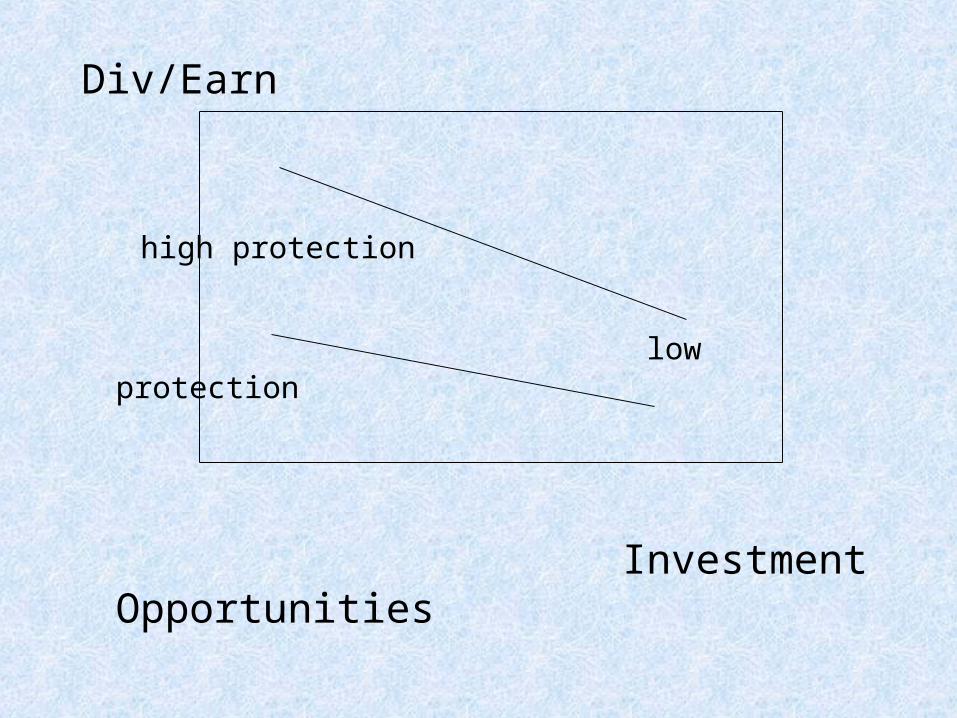

• B2. Dividends as an outcome of Legal Protection

of shareholders (outcome model) Minority shareholders use their legal power to force companies to disgorge cash. (1)Voting for directors who offer better dividend. (2)Selling share to potential hostile raiders. (3)Suing company that benefit insider.

better protection=>higher dividend payout

under good protection=> G=(1-D)*ROE

Div/Earn

high protection

low protection

Investment Opportunities

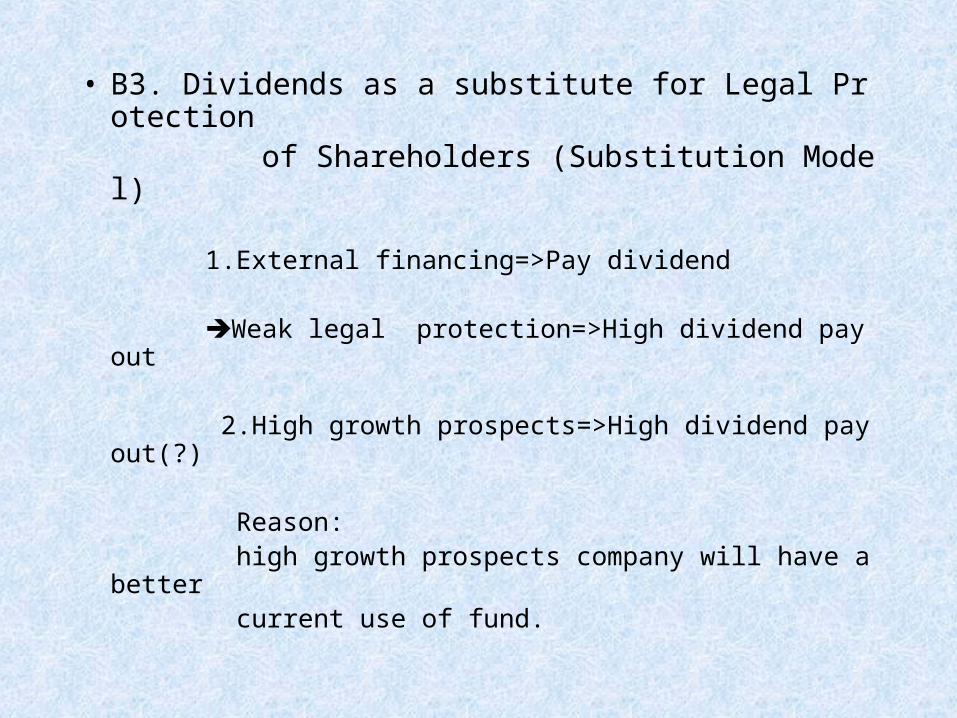

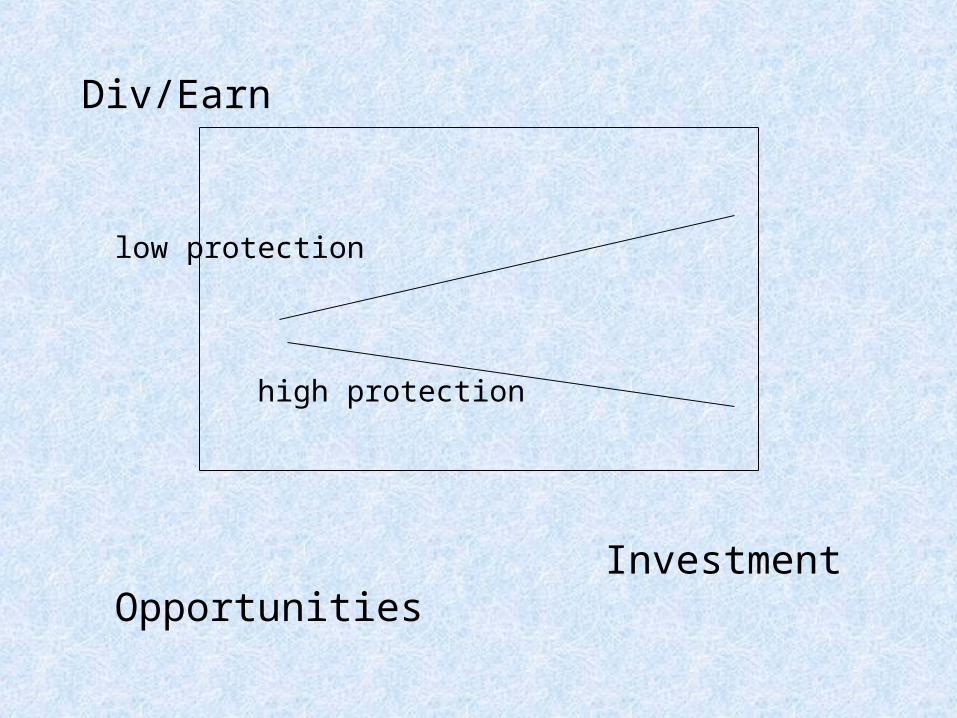

• B3. Dividends as a substitute for Legal Protection

of Shareholders (Substitution Model)

1.External financing=>Pay dividend Weak legal protection=>High dividend payout

2.High growth prospects=>High dividend payout(?) Reason: high growth prospects company will have a better current use of fund.

Div/Earn

low protection

high protection

Investment Opportunities

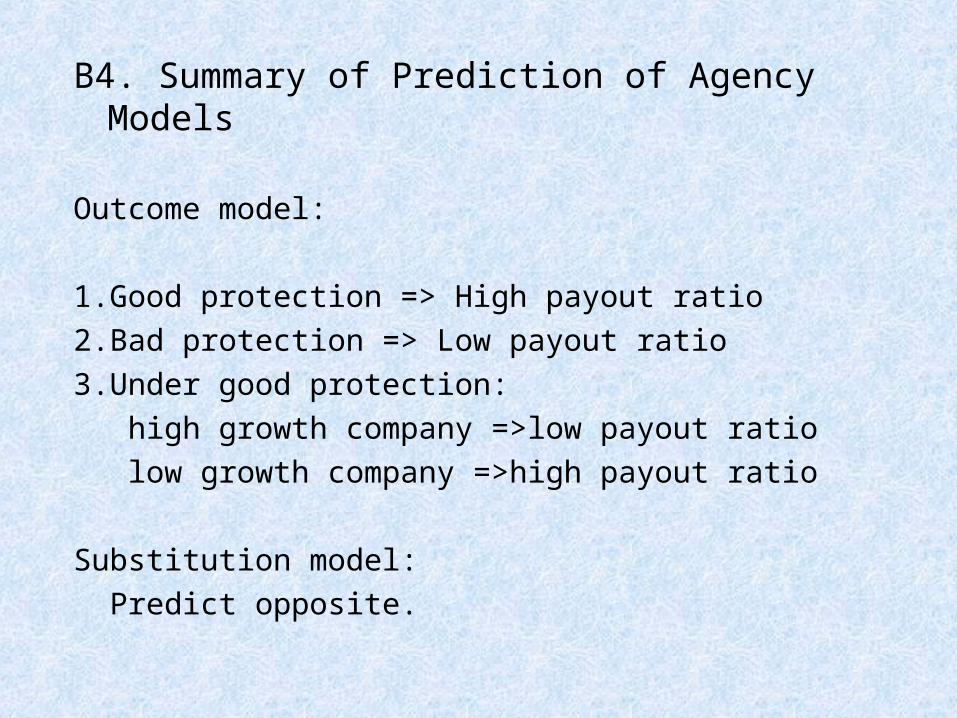

B4. Summary of Prediction of Agency Models

Outcome model:

1.Good protection => High payout ratio

2.Bad protection => Low payout ratio

3.Under good protection:

high growth company =>low payout ratio

low growth company =>high payout ratio

Substitution model:

Predict opposite.

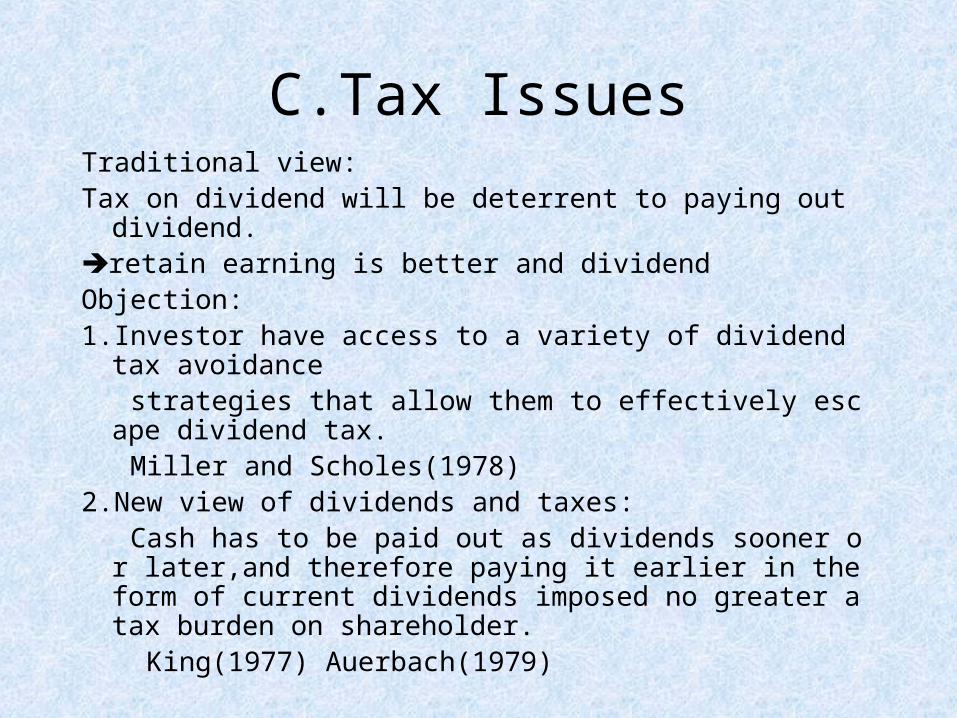

C.Tax IssuesTraditional view:Tax on dividend will be deterrent to paying out dividend.retain earning is better and dividendObjection:1.Investor have access to a variety of dividend tax avoidan

ce strategies that allow them to effectively escape dividend

tax. Miller and Scholes(1978)2.New view of dividends and taxes: Cash has to be paid out as dividends sooner or later,and

therefore paying it earlier in the form of current dividends imposed no greater a tax burden on shareholder.

King(1977) Auerbach(1979)

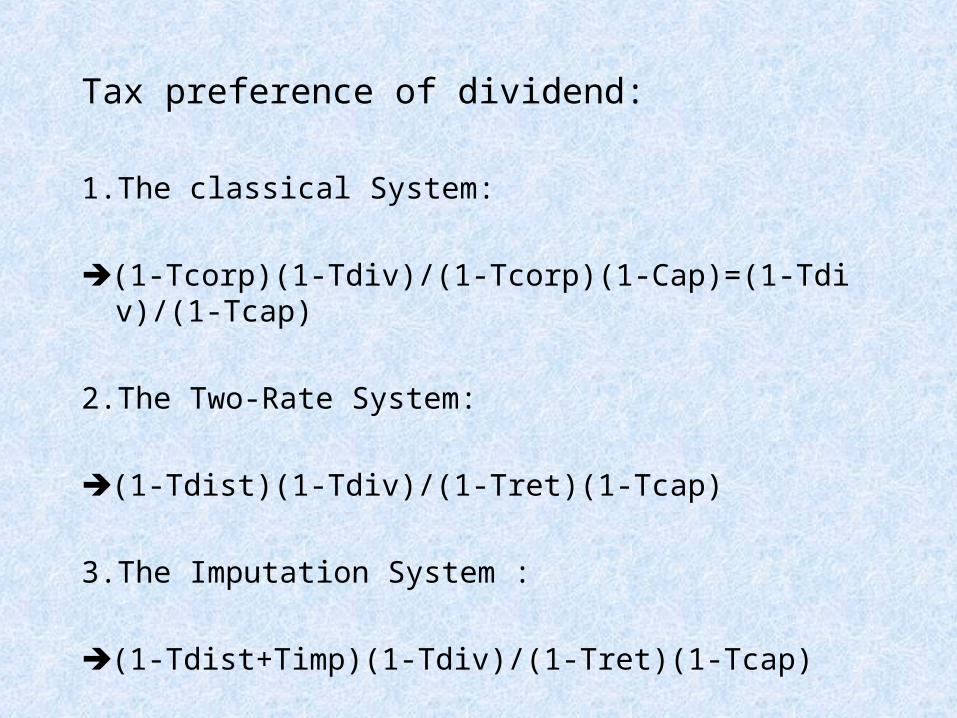

Tax preference of dividend:

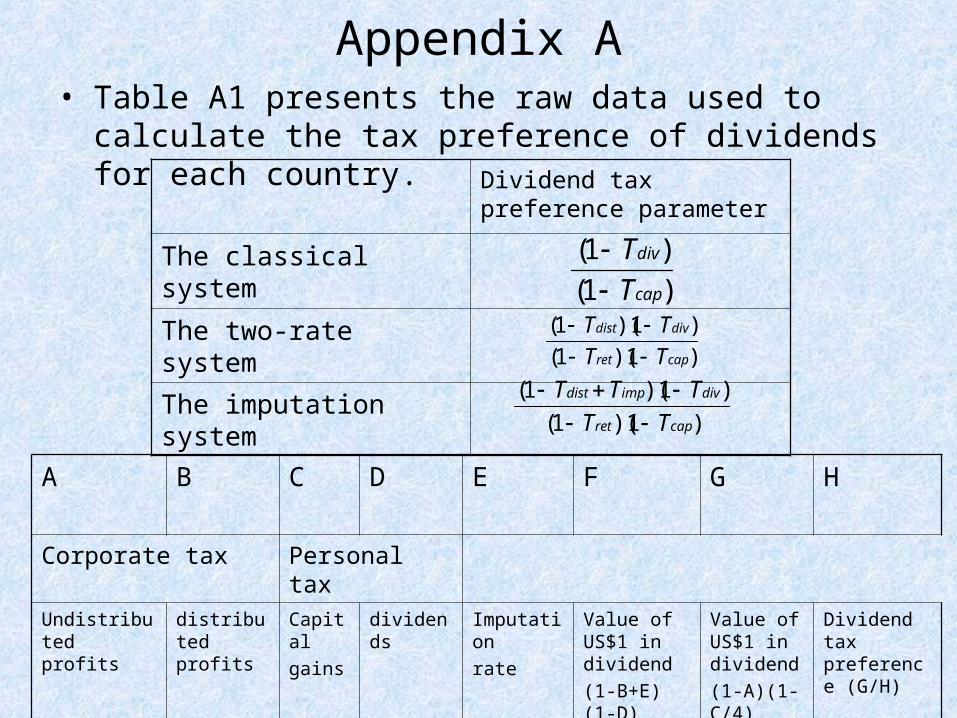

1.The classical System:

(1-Tcorp)(1-Tdiv)/(1-Tcorp)(1-Cap)=(1-Tdiv)/(1-Tcap)

2.The Two-Rate System:

(1-Tdist)(1-Tdiv)/(1-Tret)(1-Tcap)

3.The Imputation System :

(1-Tdist+Timp)(1-Tdiv)/(1-Tret)(1-Tcap)

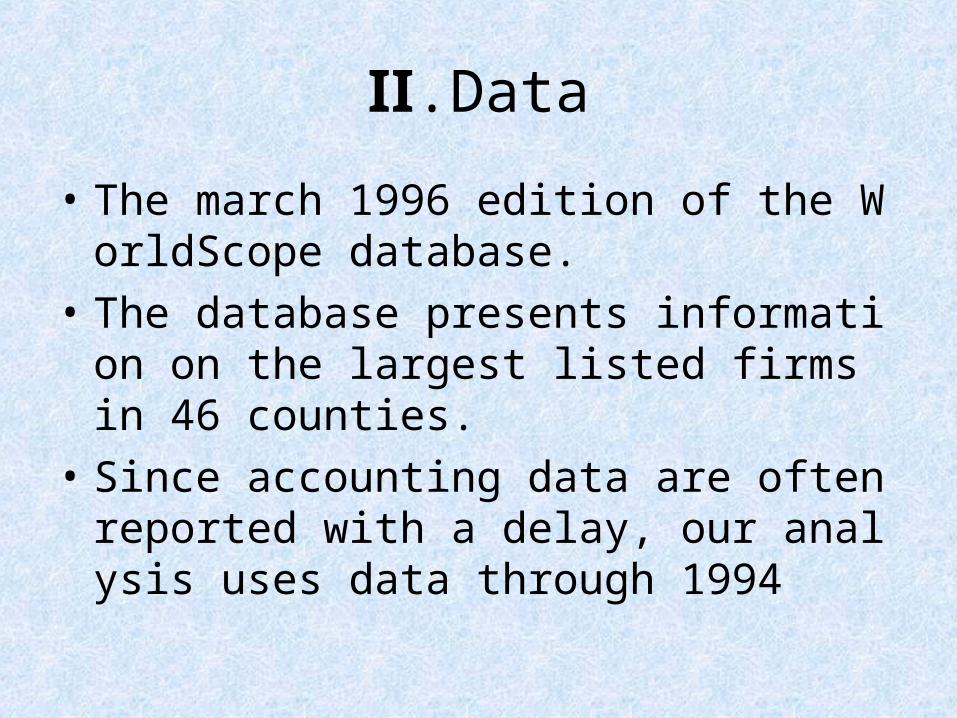

Ⅱ.Data

• The march 1996 edition of the WorldScope database.

• The database presents information on the largest listed firms in 46 counties.

• Since accounting data are often reported with a delay, our analysis uses data through 1994

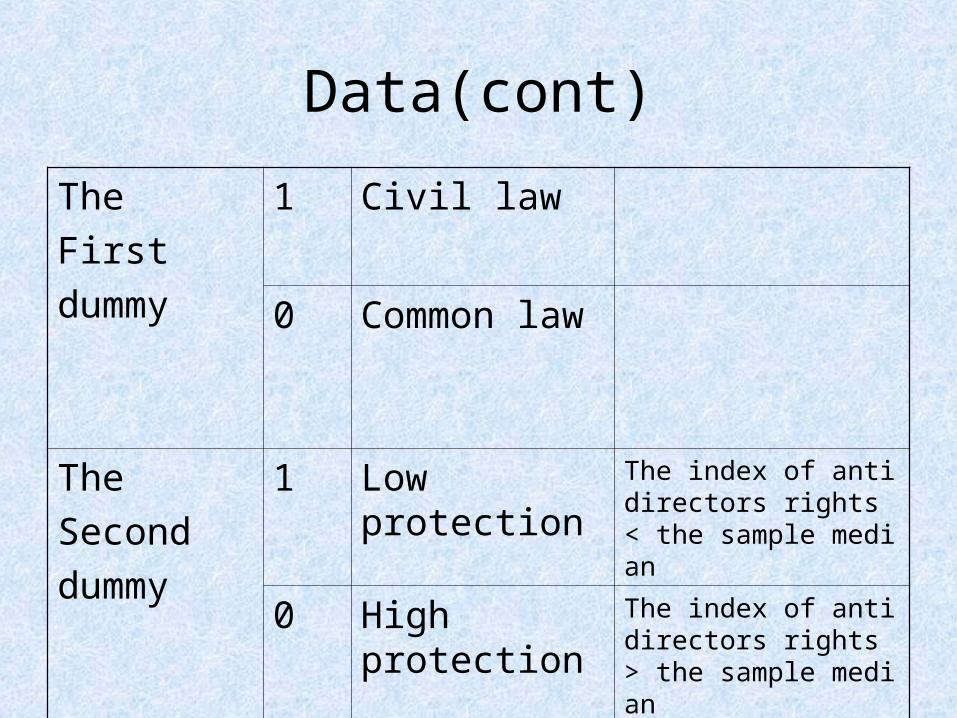

Data(cont)

The

First

dummy

1 Civil law

0 Common law

The

Second

dummy

1 Low protection The index of antidirectors rights < the sample median

0 High protection

The index of antidirectors rights > the sample median

Data(cont)

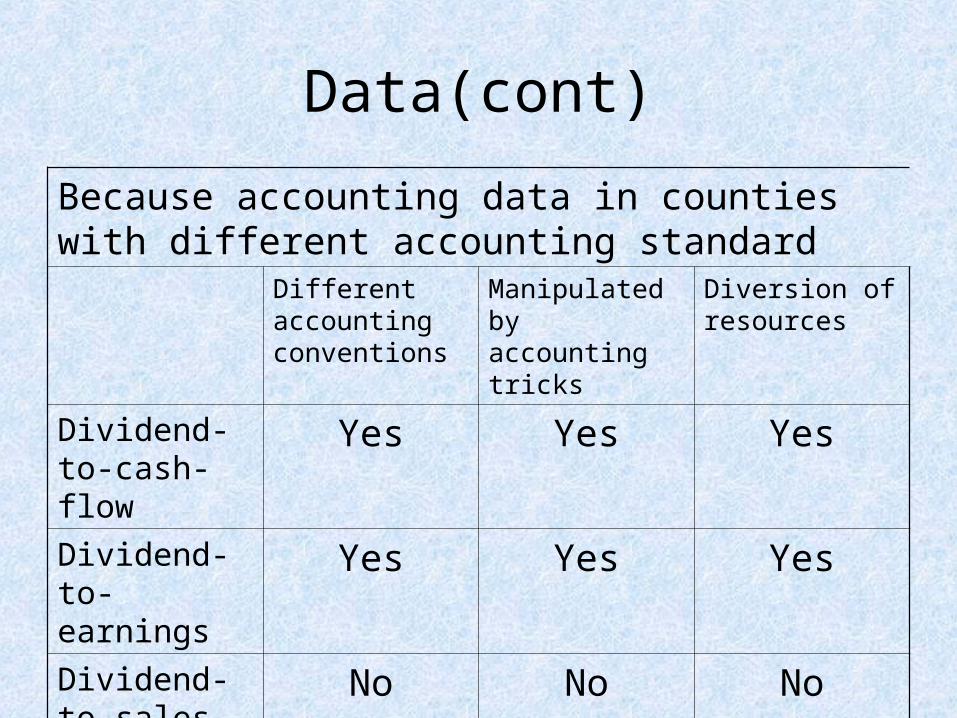

Because accounting data in counties with different accounting standard

Different accounting conventions

Manipulated by accounting tricks

Diversion of resources

Dividend-to-cash-flow

Yes Yes Yes

Dividend-to-earnings

Yes Yes Yes

Dividend-to-sales

No No No

Data(cont)

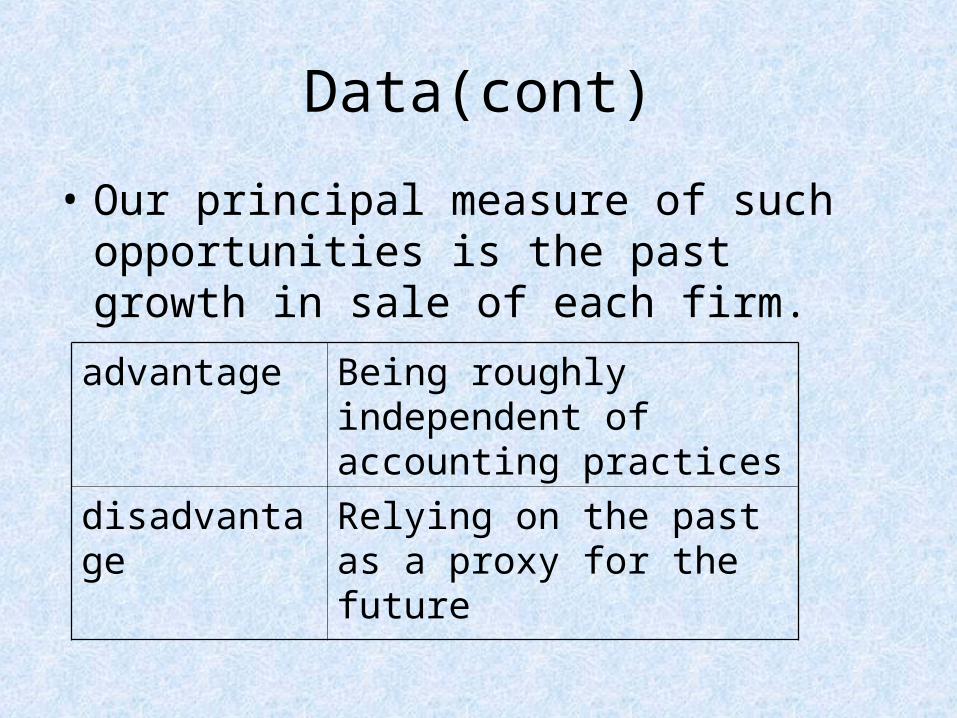

• Our principal measure of such opportunities is the past growth in sale of each firm.

advantage Being roughly independent of accounting practices

disadvantage Relying on the past as a proxy for the future

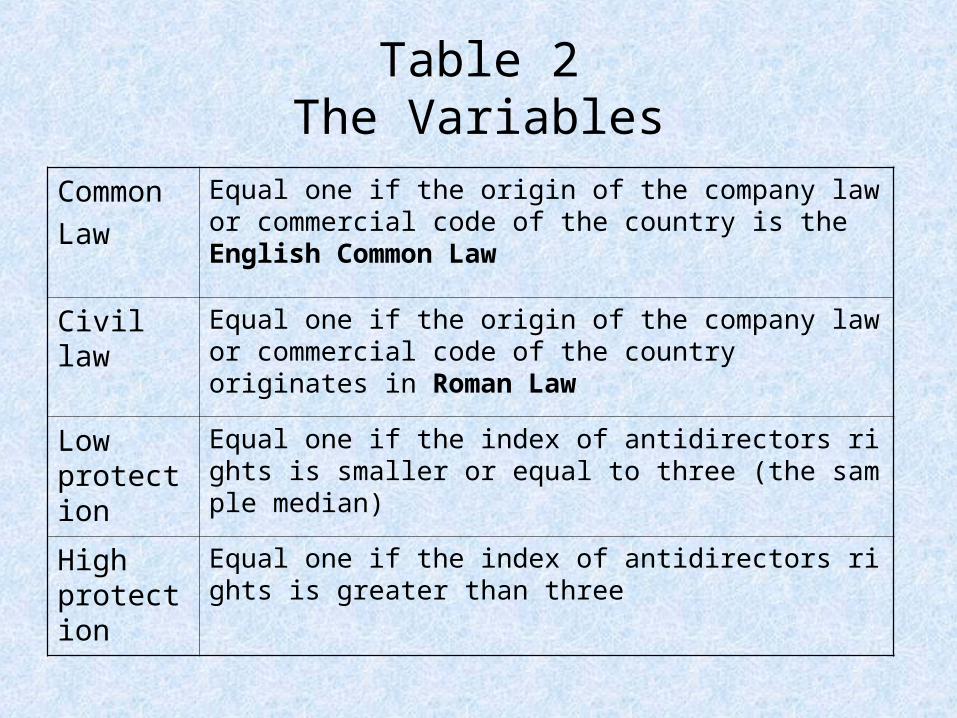

Table 2The Variables

Common

Law

Equal one if the origin of the company law or commercial code of the country is the English Common Law

Civil law Equal one if the origin of the company law or commercial code of the country originates in Roman Law

Low protection

Equal one if the index of antidirectors rights is smaller or equal to three (the sample median)

High protection

Equal one if the index of antidirectors rights is greater than three

Table 2The Variables(cont)

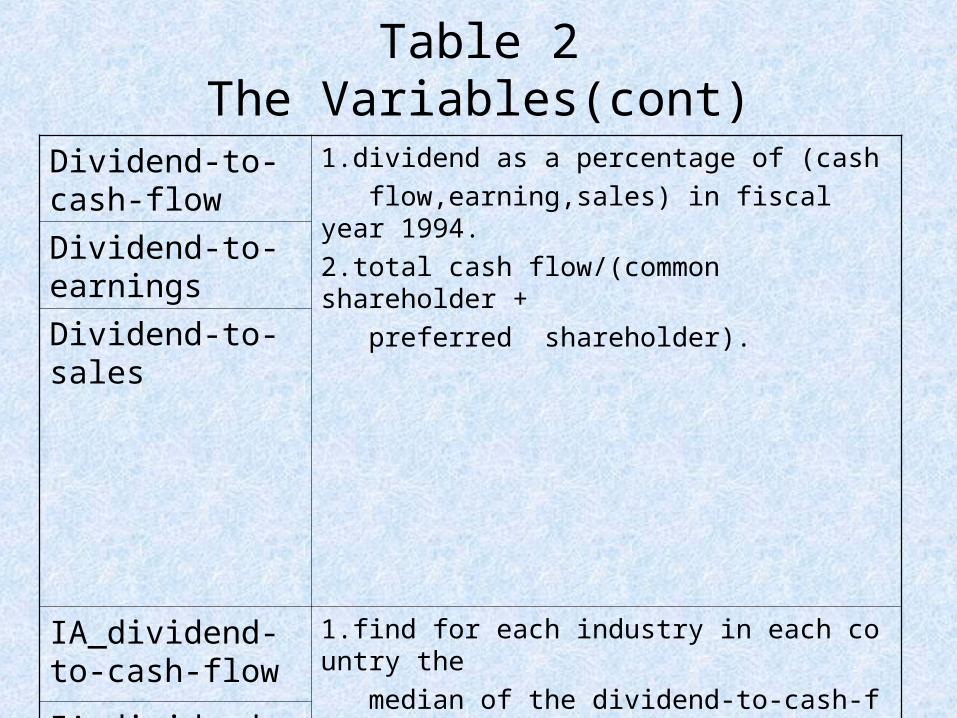

Dividend-to-cash-flow

1.dividend as a percentage of (cash

flow,earning,sales) in fiscal year 1994.

2.total cash flow/(common shareholder +

preferred shareholder).Dividend-to-earnings

Dividend-to-sales

IA_dividend-to-cash-flow

1.find for each industry in each country the

median of the dividend-to-cash-flow

ratio(C_D/CF)

2.define the world median as the median of

(C_D/CF) across countries

3.calculate the difference between firm dividend-

to-cash-flow and the world median

IA_dividend-to-earnings

IA_dividend-to-sales

Table 2The Variables(cont)

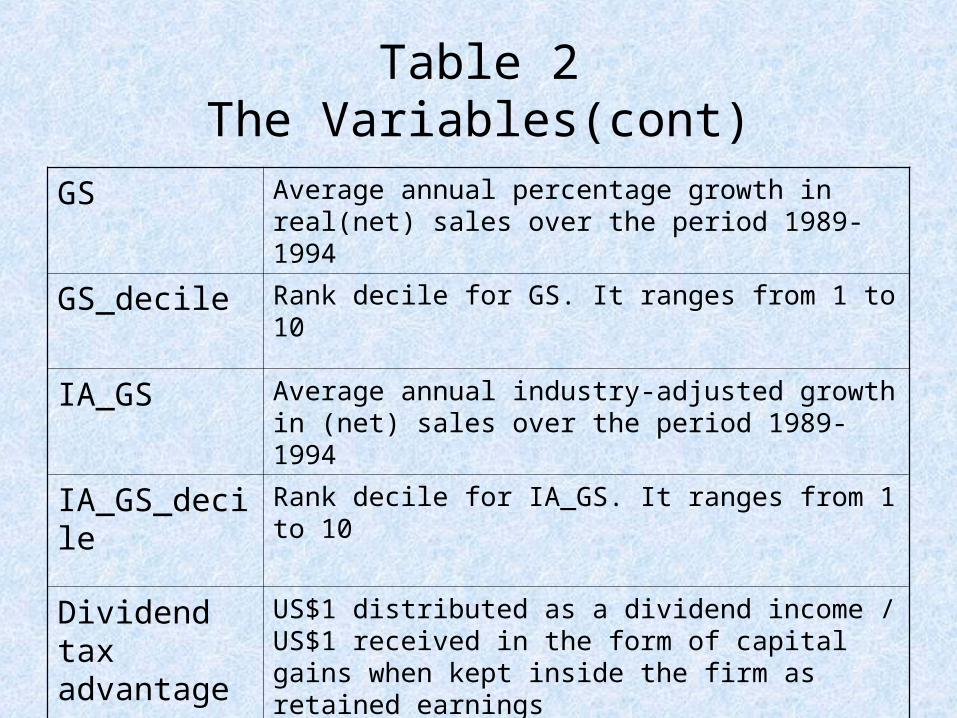

GS Average annual percentage growth in real(net) sales over the period 1989-1994

GS_decile Rank decile for GS. It ranges from 1 to 10

IA_GS Average annual industry-adjusted growth in (net) sales over the period 1989-1994

IA_GS_decile Rank decile for IA_GS. It ranges from 1 to 10

Dividend tax advantage

US$1 distributed as a dividend income / US$1 received in the form of capital gains when kept inside the firm as retained earnings

Appendix A• Table A1 presents the raw data used to calculate the tax

preference of dividends for each country.Dividend tax preference parameter

The classical system

The two-rate system

The imputation system

)1(

)1(

cap

div

T

T

)1)(1(

)1)(1(

capret

divdist

TT

TT

)1)(1(

)1)(1(

capret

divimpdist

TT

TTT

A B C D E F G H

Corporate tax Personal tax

Undistributed profits

distributed profits

Capital

gains

dividends Imputation

rate

Value of US$1 in dividend

(1-B+E)(1-D)

Value of US$1 in dividend

(1-A)(1-C/4)

Dividend tax preference (G/H)

The data

• More than half of the firms in the sample come from the USA and UK.

• WorldScope coverage and the equity of the data of data are also better for richer countries.

• The difference between the tax treatment of dividends and retained earnings is small.

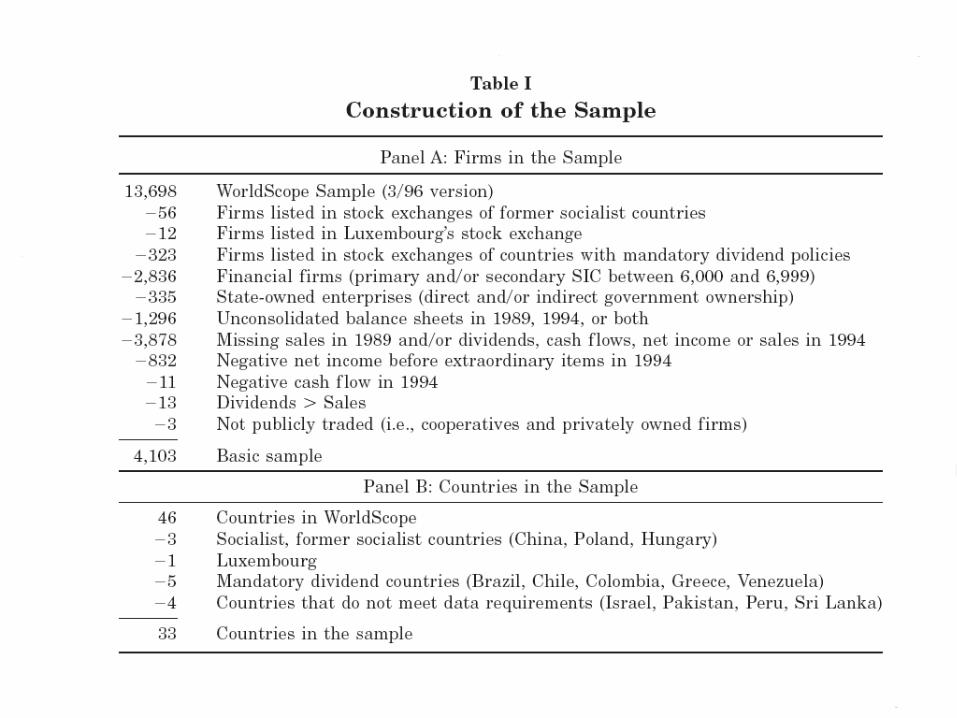

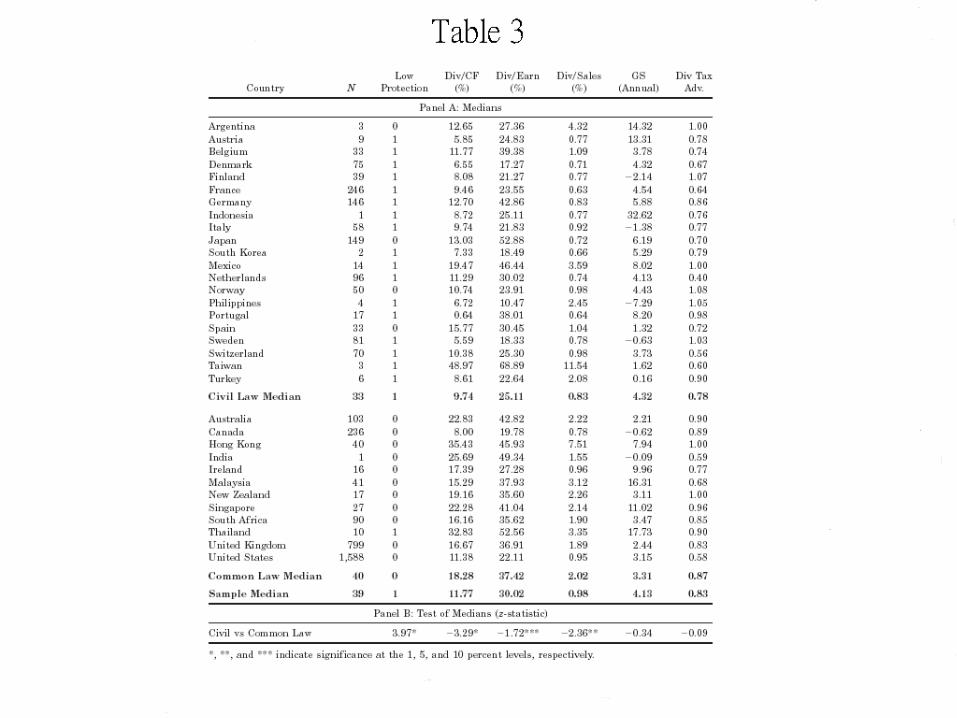

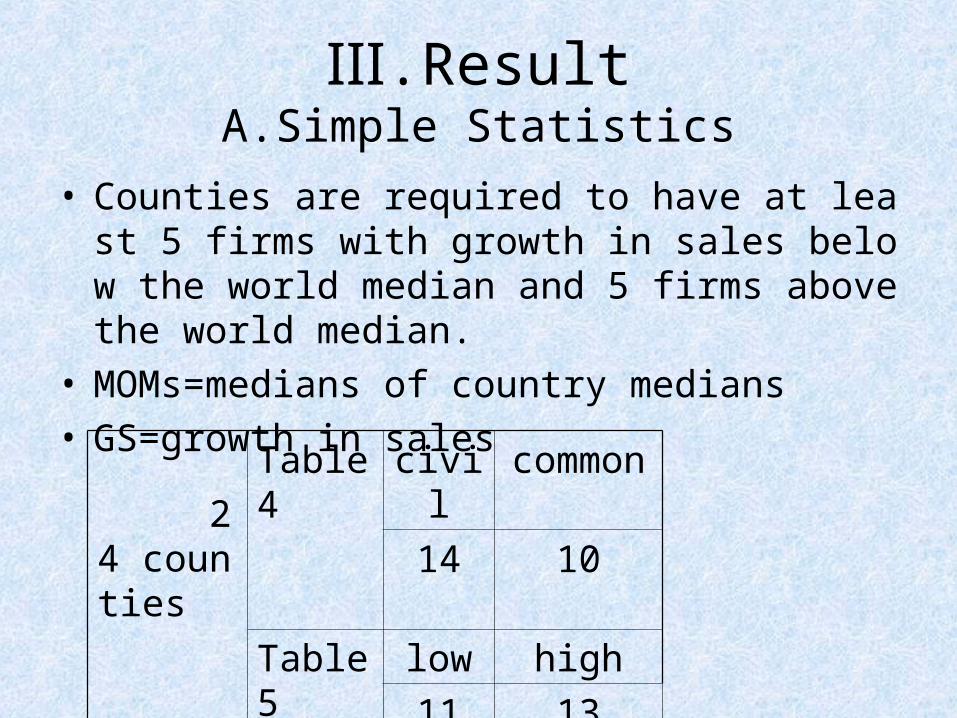

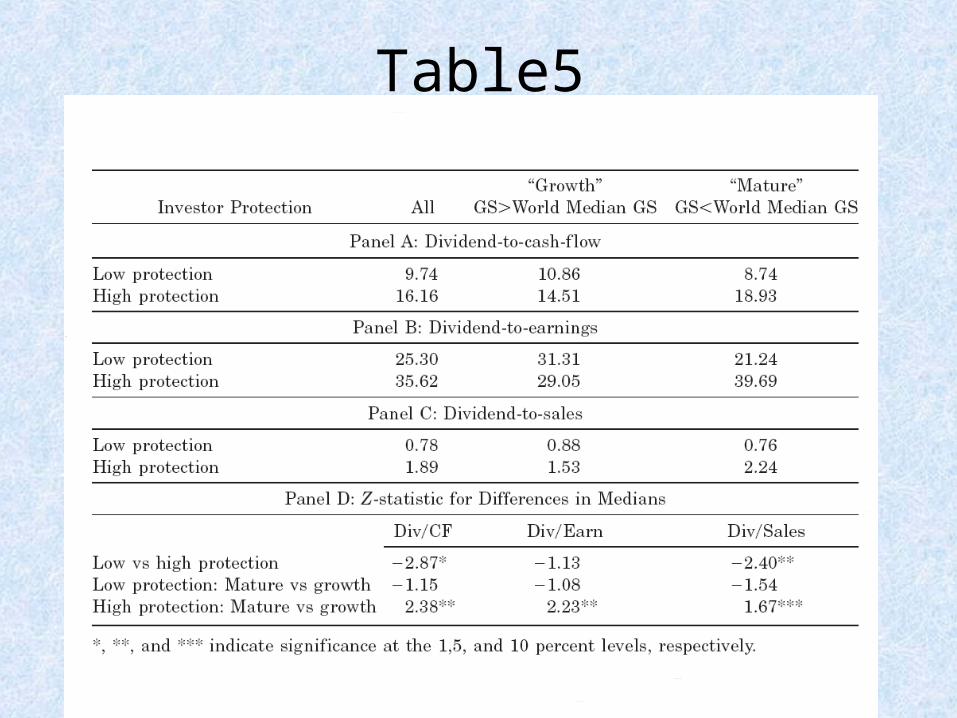

Ⅲ.ResultA.Simple Statistics

• Counties are required to have at least 5 firms with growth in sales below the world median and 5 firms above the world median.

• MOMs=medians of country medians • GS=growth in sales

24 counties

Table4 civil common

14 10

Table5 low high

11 13

Table 4

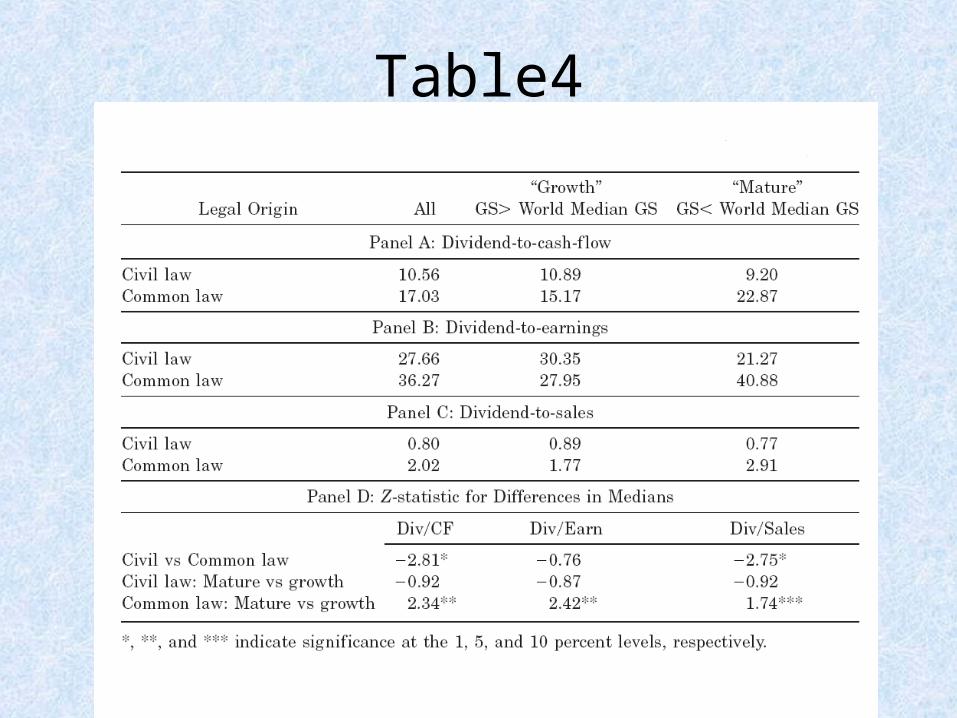

• We examine whether firms in civil and common law countries have different dividend payout policies.

• For all three ratios, common law countries have a higher dividend payout ratio than civil law countries do.

• For all three variables, these estimates are very close to those for the broader sample in table 3.

Table4

Table 4

• The additional results in table 4 address the relationship between dividend payout rates and sale growth rates across legal regimes

• These results are consistent with the predictions of the outcome agency model.

• Well-protected minority shareholders are willing to delay dividends in firms with good growth prospects.

Table5

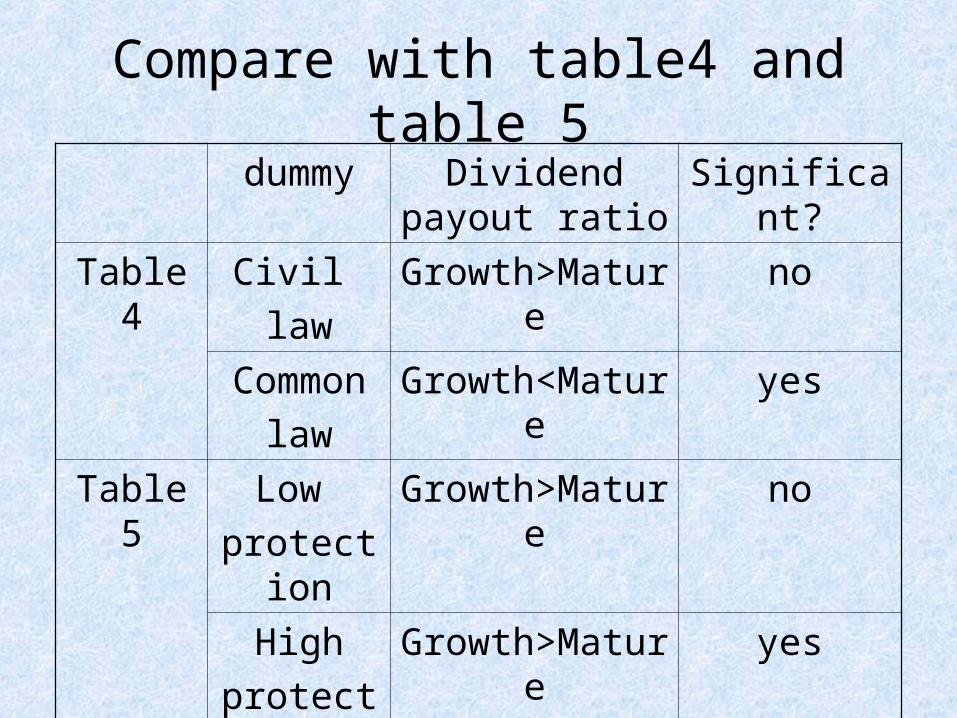

Compare with table4 and table 5

dummy Dividend payout ratio

Significant?

Table 4 Civil

law

Growth>Mature no

Common

law

Growth<Mature yes

Table 5 Low

protection

Growth>Mature no

High

protection

Growth>Mature yes

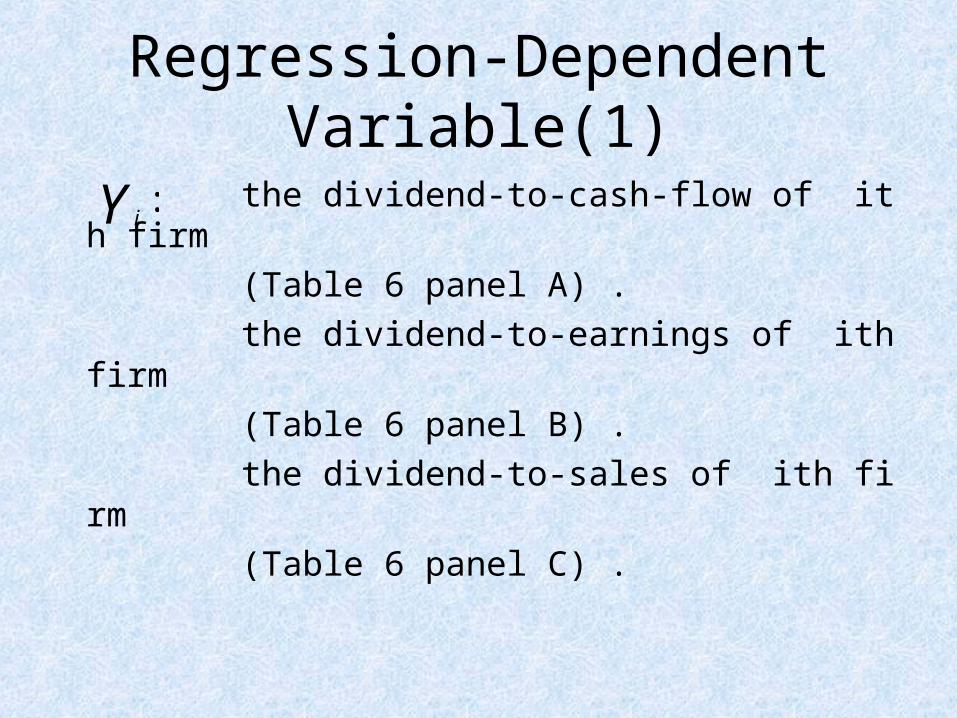

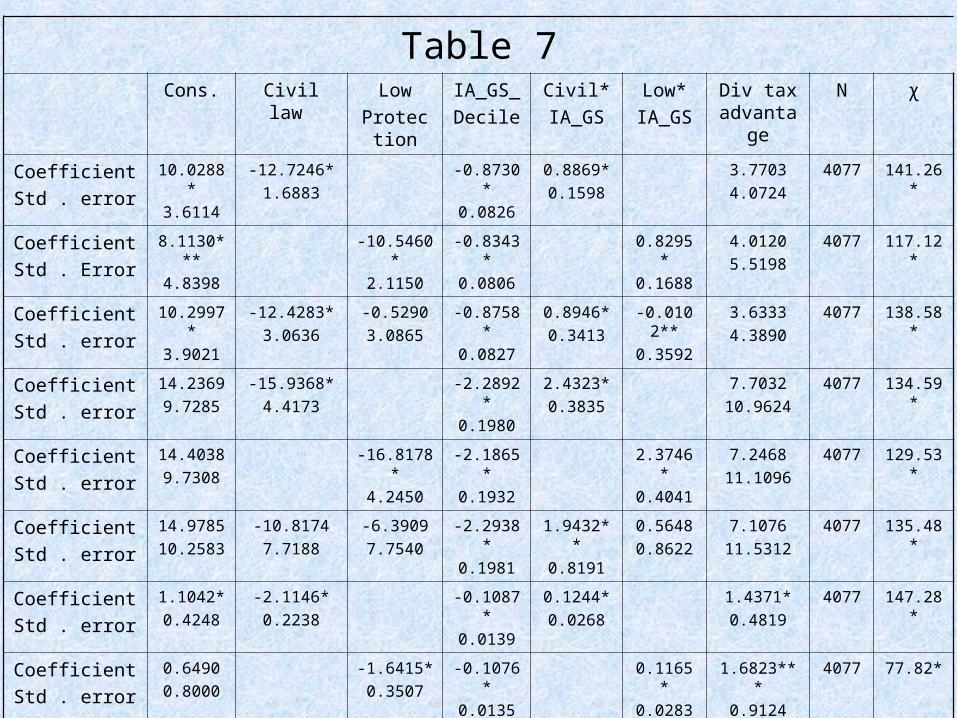

Regression-Dependent Variable(1)

the dividend-to-cash-flow of ith firm

(Table 6 panel A) .

the dividend-to-earnings of ith firm

(Table 6 panel B) .

the dividend-to-sales of ith firm

(Table 6 panel C) .

:Y i

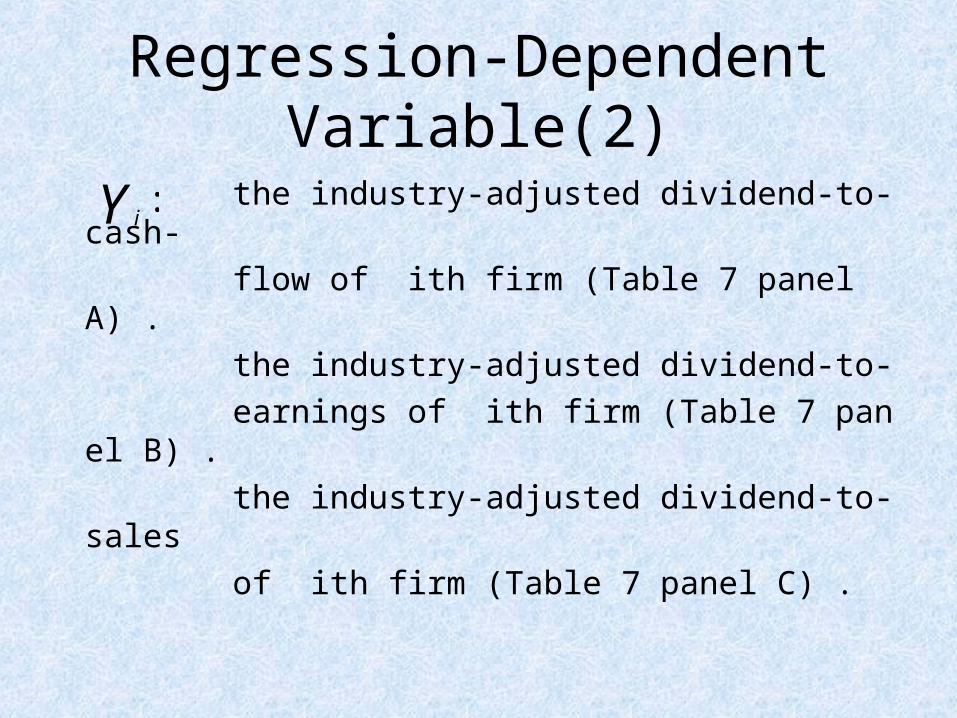

Regression-Dependent Variable(2)

the industry-adjusted dividend-to-cash-

flow of ith firm (Table 7 panel A) .

the industry-adjusted dividend-to-

earnings of ith firm (Table 7 panel B) .

the industry-adjusted dividend-to-sales

of ith firm (Table 7 panel C) .

:Y i

Regression-Independent Variable

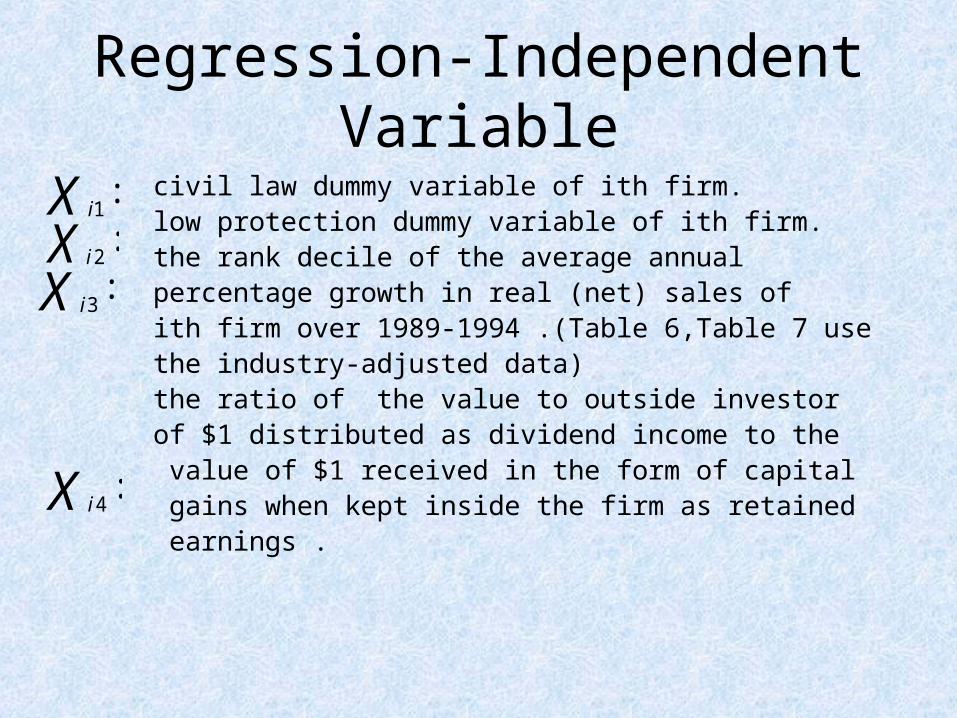

civil law dummy variable of ith firm. low protection dummy variable of ith firm. the rank decile of the average annual percentage growth in real (net) sales of ith firm over 1989-1994 .(Table 6,Table 7 use the industry-adjusted data) the ratio of the value to outside investor of $1 distributed as dividend income to the value of $1 received in the form of capital gains when kept inside the firm as retained earnings .

:1X i

:2X i

:3X i

:4X i

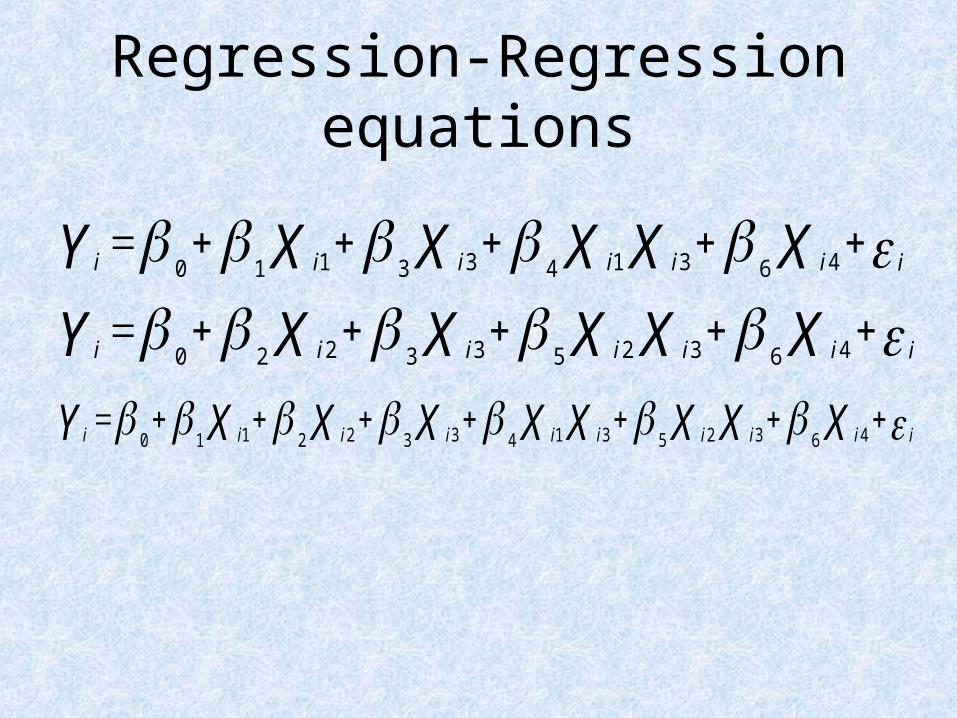

Regression-Regression equations

iiiiiii XXXXXY 4631433110

iiiiiii XXXXXY 4632533220

iiiiiiiiii XXXXXXXXY 463253143322110

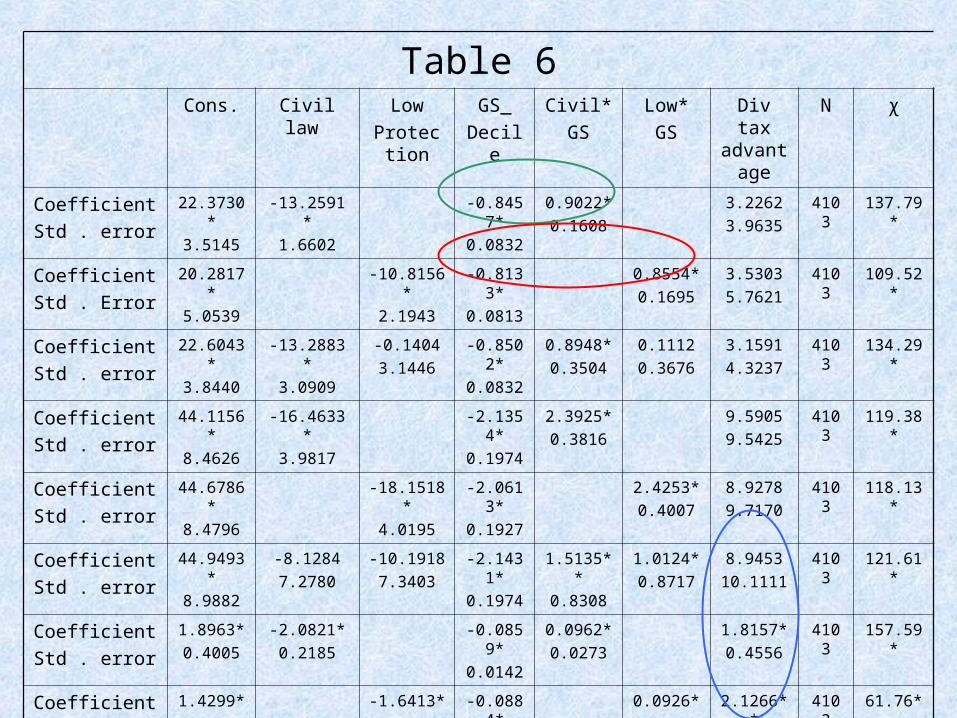

Table 6Cons. Civil law Low

Protection

GS_

Decile

Civil*

GS

Low*

GS

Div tax advanta

ge

N χ

Coefficient

Std . error

22.3730*

3.5145

-13.2591*

1.6602

-0.8457*

0.0832

0.9022*

0.1608

3.2262

3.9635

4103 137.79*

Coefficient

Std . Error

20.2817*

5.0539

-10.8156*

2.1943

-0.8133*

0.0813

0.8554*

0.1695

3.5303

5.7621

4103 109.52*

Coefficient

Std . error

22.6043*

3.8440

-13.2883*

3.0909

-0.1404

3.1446

-0.8502*

0.0832

0.8948*

0.3504

0.1112

0.3676

3.1591

4.3237

4103 134.29*

Coefficient

Std . error

44.1156*

8.4626

-16.4633*

3.9817

-2.1354*

0.1974

2.3925*

0.3816

9.5905

9.5425

4103 119.38*

Coefficient

Std . error

44.6786*

8.4796

-18.1518*

4.0195

-2.0613*

0.1927

2.4253*

0.4007

8.9278

9.7170

4103 118.13*

Coefficient

Std . error

44.9493*

8.9882

-8.1284

7.2780

-10.1918

7.3403

-2.1431*

0.1974

1.5135**

0.8308

1.0124*

0.8717

8.9453

10.1111

4103 121.61*

Coefficient

Std . error

1.8963*

0.4005

-2.0821*

0.2185

-0.0859*

0.0142

0.0962*

0.0273

1.8157*

0.4556

4103 157.59*

Coefficient

Std . error

1.4299*

0.7812

-1.6413*

0.3461

-0.0884*

0.0139

0.0926*

0.0288

2.1266**

0.8911

4103 61.76*

Coefficient

Std . error

1.8907*

0.4146

-2.3471*

0.4378

0.2979

0.4476

-0.0865*

0.0142

0.1189**

0.0595

-0.0248

0.0623

1.8457*

0.4708

4103 153.45*

Table 7Cons. Civil law Low

Protection

IA_GS_

Decile

Civil*

IA_GS

Low*

IA_GS

Div tax advantag

e

N χ

Coefficient

Std . error

10.0288*

3.6114

-12.7246*

1.6883

-0.8730*

0.0826

0.8869*

0.1598

3.7703

4.0724

4077 141.26*

Coefficient

Std . Error

8.1130***

4.8398

-10.5460*

2.1150

-0.8343*

0.0806

0.8295*

0.1688

4.0120

5.5198

4077 117.12*

Coefficient

Std . error

10.2997*

3.9021

-12.4283*

3.0636

-0.5290

3.0865

-0.8758*

0.0827

0.8946*

0.3413

-0.0102**

0.3592

3.6333

4.3890

4077 138.58*

Coefficient

Std . error

14.2369

9.7285

-15.9368*

4.4173

-2.2892*

0.1980

2.4323*

0.3835

7.7032

10.9624

4077 134.59*

Coefficient

Std . error

14.4038

9.7308

-16.8178*

4.2450

-2.1865*

0.1932

2.3746*

0.4041

7.2468

11.1096

4077 129.53*

Coefficient

Std . error

14.9785

10.2583

-10.8174

7.7188

-6.3909

7.7540

-2.2938*

0.1981

1.9432**

0.8191

0.5648

0.8622

7.1076

11.5312

4077 135.48*

Coefficient

Std . error

1.1042*

0.4248

-2.1146*

0.2238

-0.1087*

0.0139

0.1244*

0.0268

1.4371*

0.4819

4077 147.28*

Coefficient

Std . error

0.6490

0.8000

-1.6415*

0.3507

-0.1076*

0.0135

0.1165*

0.0283

1.6823***

0.9124

4077 77.82*

Coefficient

Std . error

1.1116*

0.4715

-2.5125*

0.4439

0.4255

0.4520

-0.1106*

0.0139

0.1557*

0.0571

-0.0332

0.0600

1.4931*

0.5329

4077 138.28*

Robustness-result

• From figure 3 , we find that there is a negative relationship between sales growth and dividend-to-earnings ratio in common law countries.

• From figure 4 , we find that the relationship between sales growth and dividend-to-earnings ratio is negative for 11of the 20 civil law countries , and positive relationship for 9 of 20 civil law countries.

• The relationship between sales growth and dividend-to-cash flow and the relationship between sales growth and dividend-to-sales are same as above .

Robustness-interpretation(high protection countries)

• One possible interpretation is that the measures of the investor protection is simply reflect the degree of the capital markets development.

• But it’s determined by legal origin and the quality of investor protection (LLSV(1997)) , and it does not to explain the relationship between investment opportunities and payouts .

Robustness-possibly important objection

• The lower payouts in civil law countries simply reflects greater reliance on debt finance in those countries.

• But according to the empirical ,even if firms in civil law countries rely on debt to a greater extent , they should not necessarily pay out less of their net-of-interest income .

Conclusion

• The result of this article is support the outcome agency model of dividends.

• Poorly protected shareholders seem to take whatever dividends they can get.

• The result of this article doesn’t find the effect of taxes on dividend policies.

![Ce Sec3 No. 18105-10 Privación Injusta de La Libertad Acarrea Falla Del Servicio[1]](https://img.pdfslide.tips/doc/110x75/55cf94c4550346f57ba43f24/ce-sec3-no-18105-10-privacion-injusta-de-la-libertad-acarrea-falla-del-servicio1.jpg)