Embed Size (px)

Citation preview

Open Banking:L’evoluzione dei pagamenti no-cash e il nuovo ruolo della banca

Monia Ferrari

Financial Services Director

November 2019

2© Capgemini 2019. All rights reserved |Open Banking: L’evoluzione dei pagamenti no-cash e il nuovo ruolo della banca | November 2019

Capgemini

GLOBAL ITALY

*

NorthAmerica

+40k

Latin America

+9k

Europe

+70k

Middle-East & Africa

+2kAsia-Pacific

+90k

20182008

3.800

1.550

20182008

350

150

Revenues

€13,197 million

People+210 thousand

Location+40 countries

Revenues (MI€)

Headcount

Consumer Products, Retail & Distribution

ManufacturingEnergy & Utilities

Telecom, High-Tech, Media &

Entertainment

Financial Services

PublicSector

10 locations bringing group and local knowledge, skills, and

expertise to our client premises

3© Capgemini 2019. All rights reserved |Open Banking: L’evoluzione dei pagamenti no-cash e il nuovo ruolo della banca | November 2019

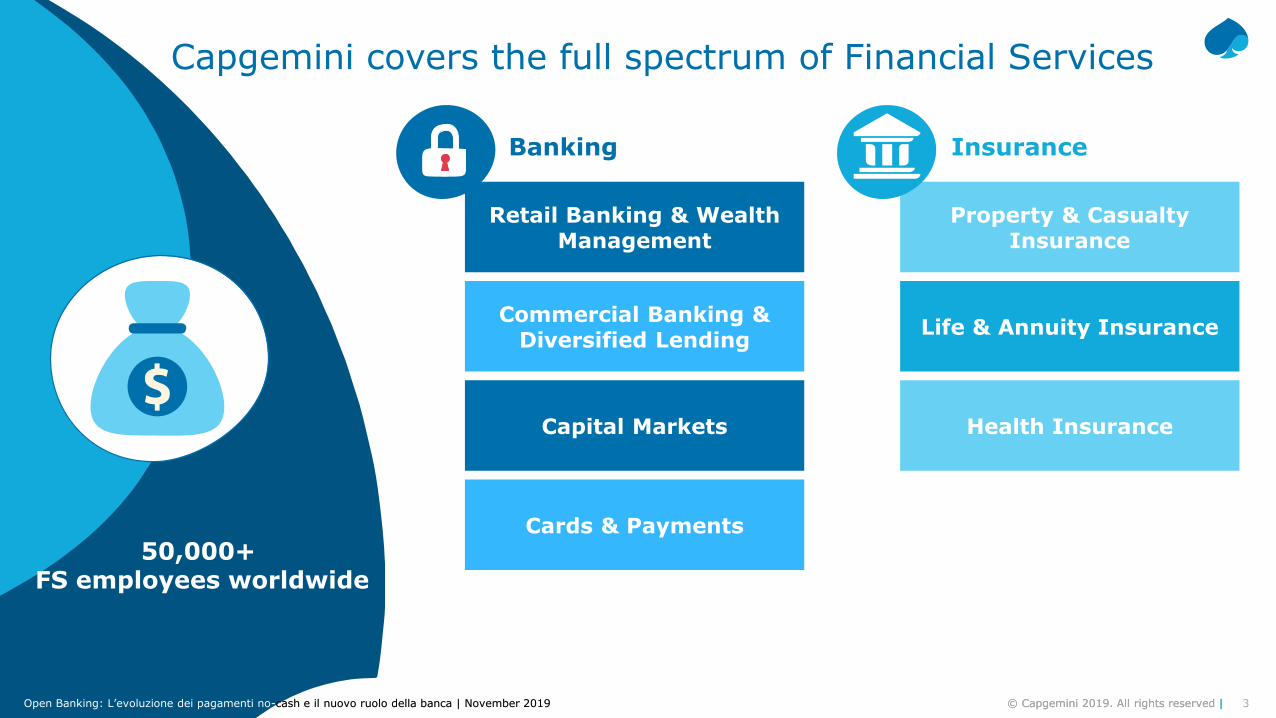

Capgemini covers the full spectrum of Financial Services

© Capgemini 2019. All rights reserved |Open Banking: L’evoluzione dei pagamenti no-cash e il nuovo ruolo della banca | November 2019

Property & CasualtyInsurance

Life & Annuity Insurance

Health Insurance

Retail Banking & Wealth Management

Commercial Banking & Diversified Lending

Capital Markets

Cards & Payments

50,000+ FS employees worldwide

Banking Insurance

4© Capgemini 2019. All rights reserved |Open Banking: L’evoluzione dei pagamenti no-cash e il nuovo ruolo della banca | November 2019

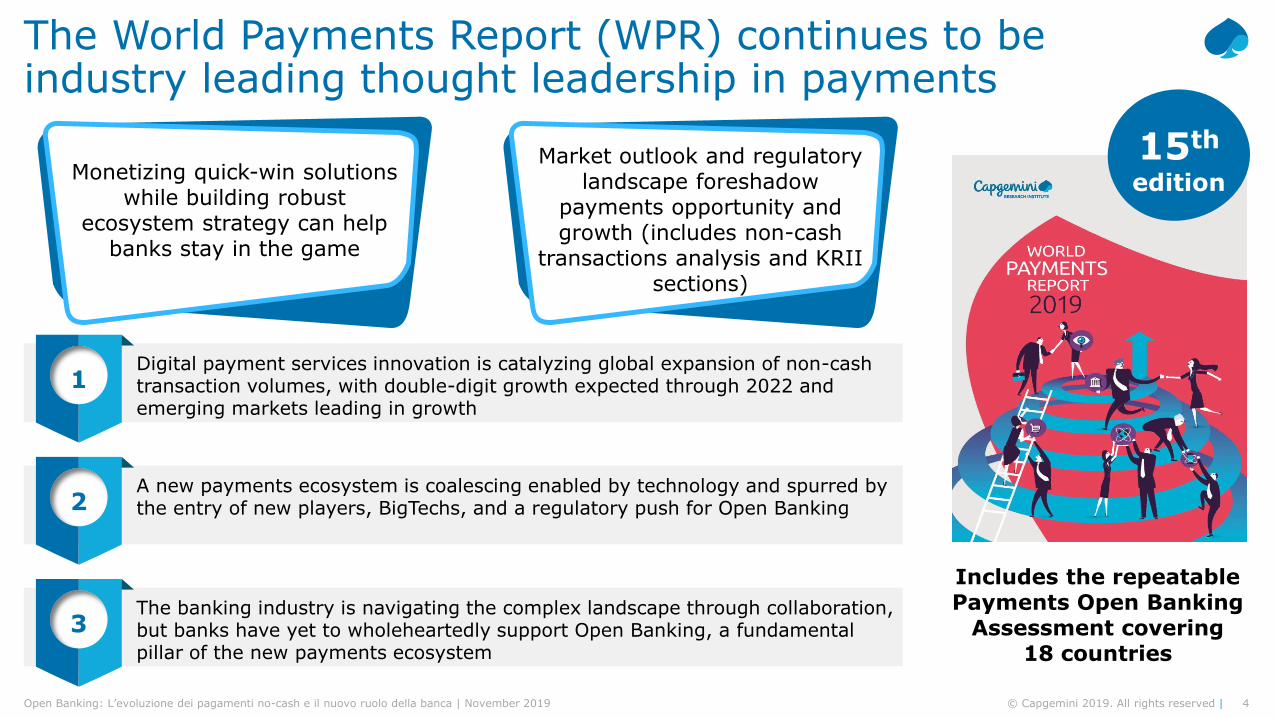

The World Payments Report (WPR) continues to be industry leading thought leadership in payments

Includes the repeatable Payments Open Banking

Assessment covering 18 countries

15th

editionMonetizing quick-win solutions while building robust

ecosystem strategy can help banks stay in the game

Market outlook and regulatory landscape foreshadow

payments opportunity and growth (includes non-cash

transactions analysis and KRII sections)

Digital payment services innovation is catalyzing global expansion of non-cash transaction volumes, with double-digit growth expected through 2022 and emerging markets leading in growth

A new payments ecosystem is coalescing enabled by technology and spurred by the entry of new players, BigTechs, and a regulatory push for Open Banking

The banking industry is navigating the complex landscape through collaboration, but banks have yet to wholeheartedly support Open Banking, a fundamental pillar of the new payments ecosystem

1

2

3

5© Capgemini 2019. All rights reserved |Open Banking: L’evoluzione dei pagamenti no-cash e il nuovo ruolo della banca | November 2019

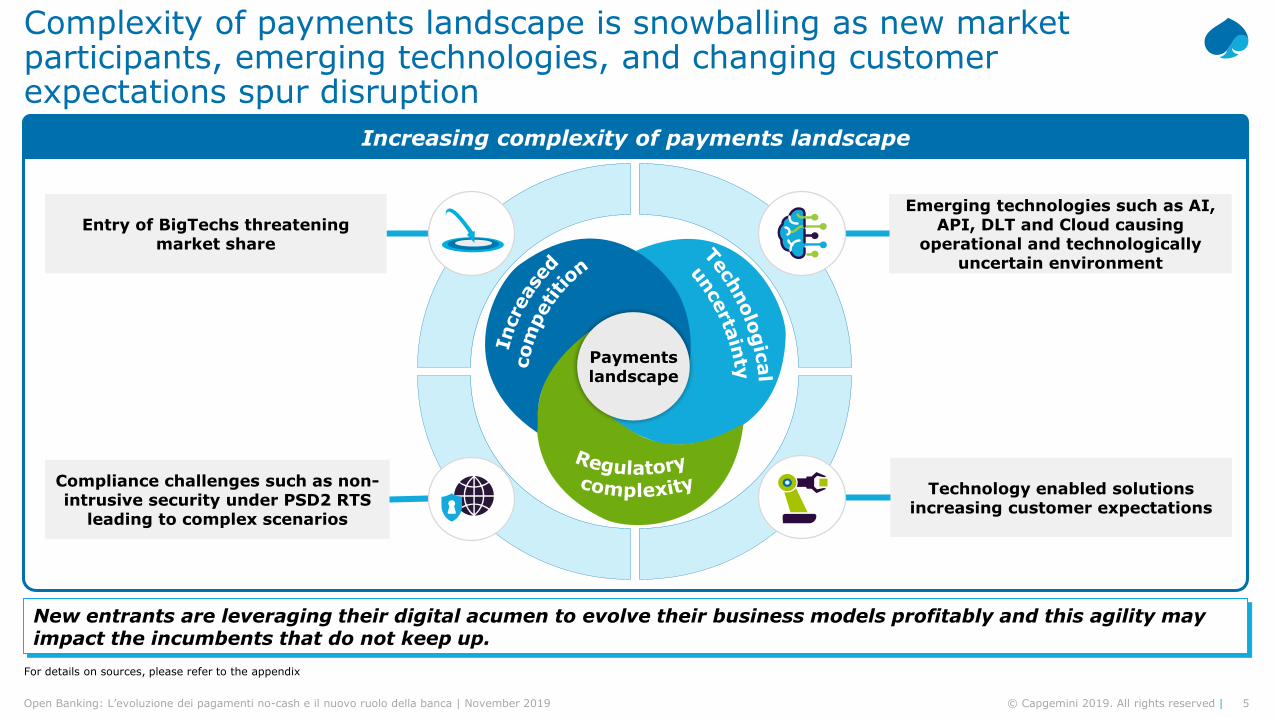

Complexity of payments landscape is snowballing as new market participants, emerging technologies, and changing customer expectations spur disruption

For details on sources, please refer to the appendix

Emerging technologies such as AI, API, DLT and Cloud causing

operational and technologically uncertain environment

Entry of BigTechs threatening market share

Compliance challenges such as non-intrusive security under PSD2 RTS

leading to complex scenarios

Technology enabled solutions increasing customer expectations

New entrants are leveraging their digital acumen to evolve their business models profitably and this agility may impact the incumbents that do not keep up.

Payments landscape

Increasing complexity of payments landscape

6© Capgemini 2019. All rights reserved |Open Banking: L’evoluzione dei pagamenti no-cash e il nuovo ruolo della banca | November 2019

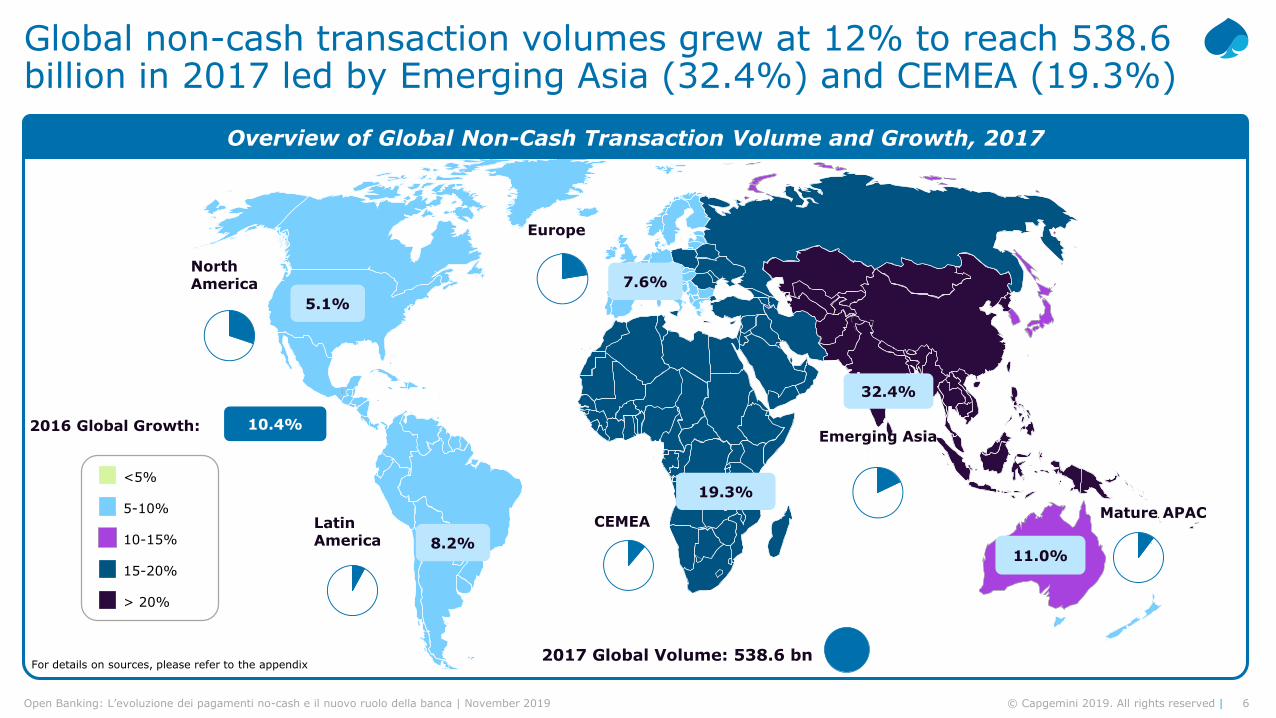

Global non-cash transaction volumes grew at 12% to reach 538.6 billion in 2017 led by Emerging Asia (32.4%) and CEMEA (19.3%)

For details on sources, please refer to the appendix2017 Global Volume: 538.6 bn

<5%

> 20%

15-20%

10-15%

5-10%

11.0%

5.1%

8.2%

North America

Latin America

Europe

Emerging Asia

Mature APAC

32.4%

2016 Global Growth: 10.4%

7.6%

19.3%

CEMEA

Overview of Global Non-Cash Transaction Volume and Growth, 2017

7© Capgemini 2019. All rights reserved |Open Banking: L’evoluzione dei pagamenti no-cash e il nuovo ruolo della banca | November 2019

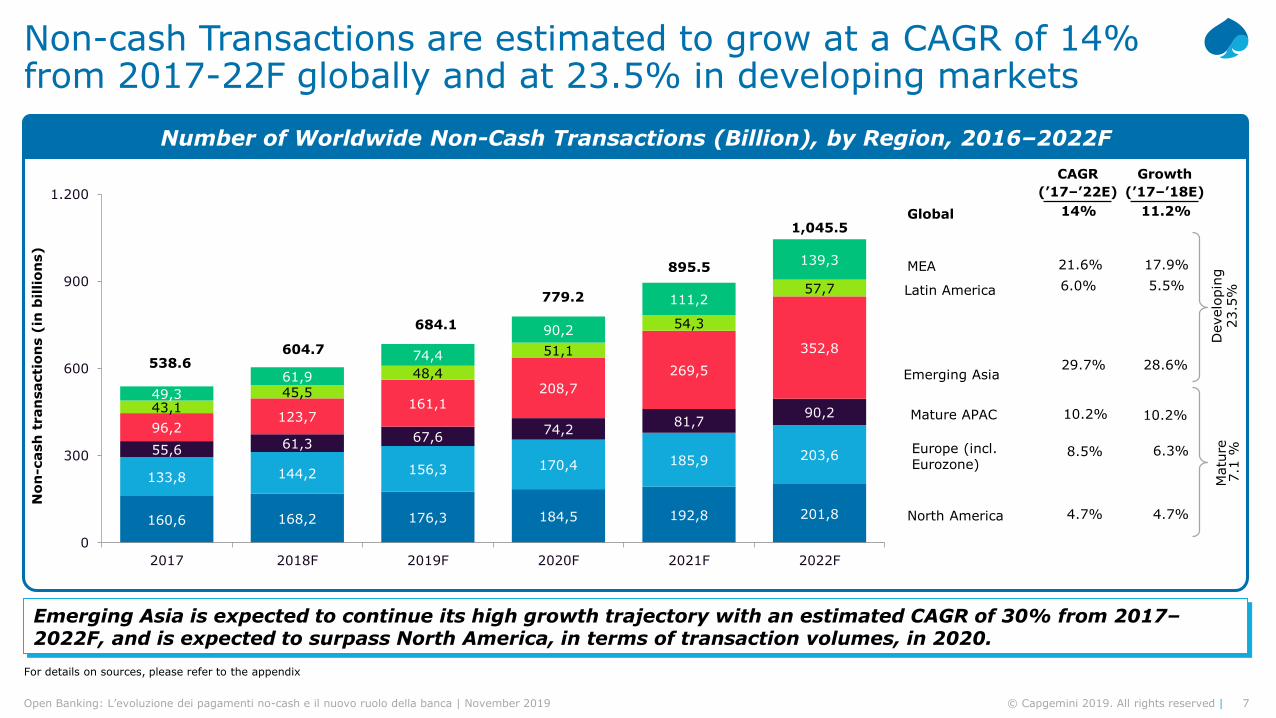

Non-cash Transactions are estimated to grow at a CAGR of 14% from 2017-22F globally and at 23.5% in developing markets

Emerging Asia is expected to continue its high growth trajectory with an estimated CAGR of 30% from 2017–2022F, and is expected to surpass North America, in terms of transaction volumes, in 2020.

For details on sources, please refer to the appendix

160,6 168,2 176,3 184,5 192,8 201,8

133,8 144,2 156,3 170,4 185,9 203,655,6 61,367,6

74,281,7

90,296,2

123,7161,1

208,7

269,5

352,8

43,145,5

48,4

51,1

54,3

57,7

49,3

61,9

74,4

90,2

111,2

139,3

0

300

600

900

1.200

2017 2018F 2019F 2020F 2021F 2022F

538.6604.7

684.1

779.2

895.5

1,045.5

No

n-c

ash

tran

sacti

on

s (

in b

illio

ns)

Matu

re

Develo

pin

g

Europe (incl. Eurozone)

6.3%8.5%

28.6%Emerging Asia

29.7%

Mature APAC 10.2%10.2%

Latin America 5.5%6.0%

Global 14%

(’17–’22E)

CAGR

11.2%

(’17–’18E)

Growth

23.5

%7.1

%

17.9%MEA 21.6%

North America 4.7%4.7%

Number of Worldwide Non-Cash Transactions (Billion), by Region, 2016–2022F

8© Capgemini 2019. All rights reserved |Open Banking: L’evoluzione dei pagamenti no-cash e il nuovo ruolo della banca | November 2019

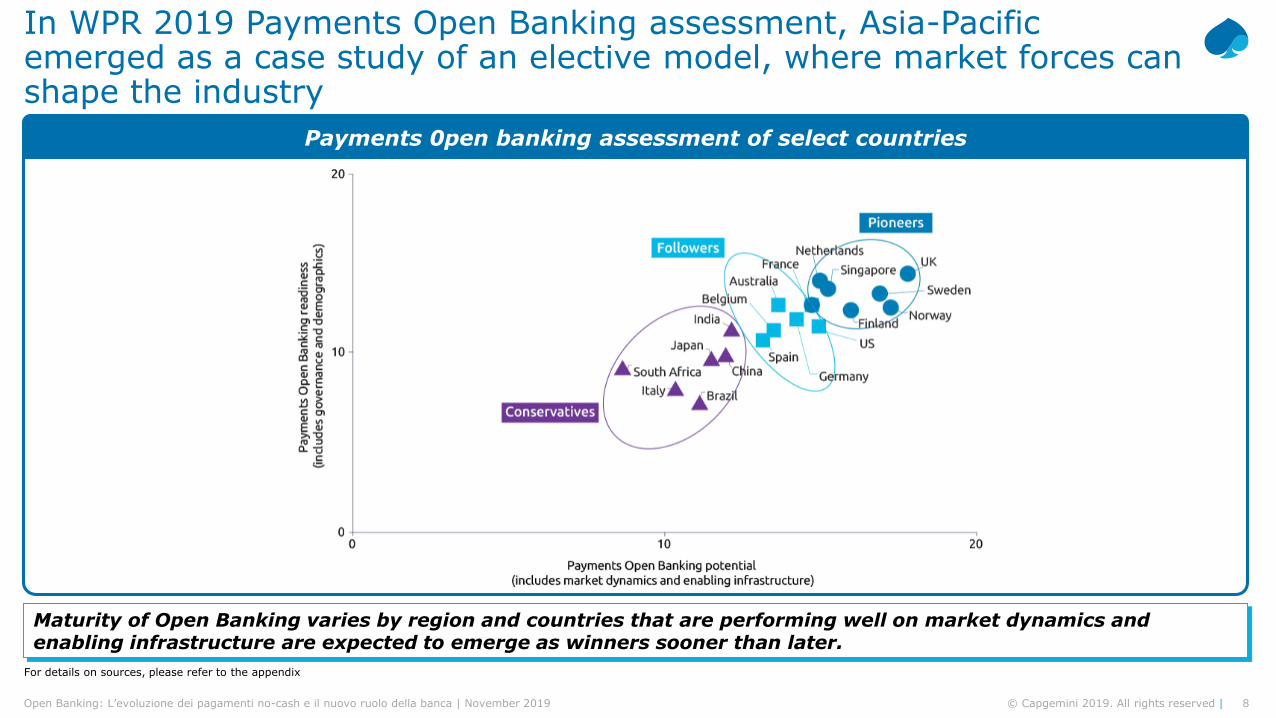

In WPR 2019 Payments Open Banking assessment, Asia-Pacific emerged as a case study of an elective model, where market forces can shape the industry

For details on sources, please refer to the appendix

Payments 0pen banking assessment of select countries

Maturity of Open Banking varies by region and countries that are performing well on market dynamics and enabling infrastructure are expected to emerge as winners sooner than later.

9© Capgemini 2019. All rights reserved |Open Banking: L’evoluzione dei pagamenti no-cash e il nuovo ruolo della banca | November 2019

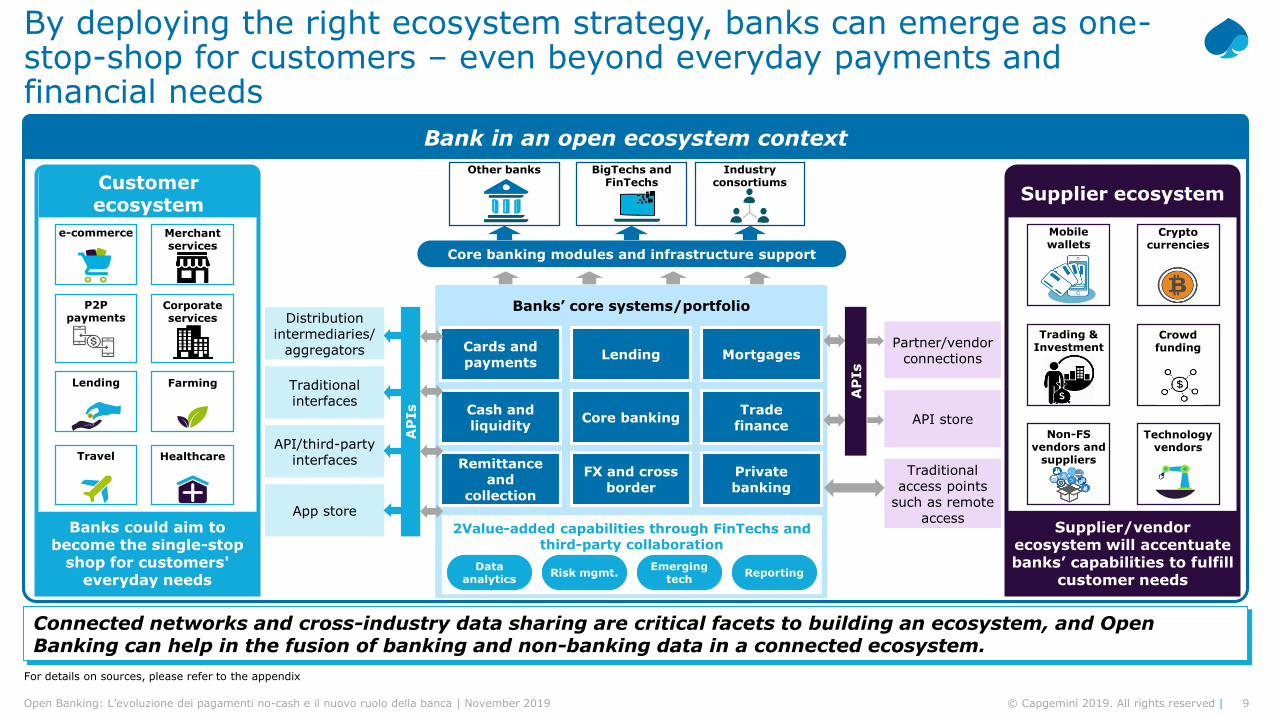

Connected networks and cross-industry data sharing are critical facets to building an ecosystem, and Open Banking can help in the fusion of banking and non-banking data in a connected ecosystem.

By deploying the right ecosystem strategy, banks can emerge as one-stop-shop for customers – even beyond everyday payments and financial needs

For details on sources, please refer to the appendix

Partner/vendor connections

API store

Traditional access points

such as remote access

Banks’ core systems/portfolio

Core banking

Cards and payments

Lending Mortgages

Trade finance

Cash and liquidity

Remittance and

collection

FX and cross border

Private banking

2Value-added capabilities through FinTechs and third-party collaboration

Data analytics

Risk mgmt. ReportingEmerging

tech

Distribution intermediaries/

aggregators

Traditional interfaces

API/third-party interfaces

App store

AP

Is

AP

Is

Customer ecosystem

Banks could aim to become the single-stop

shop for customers' everyday needs

Supplier ecosystem

Supplier/vendor ecosystem will accentuate banks’ capabilities to fulfill

customer needs

Core banking modules and infrastructure support

e-commerce

P2P payments

Lending

Merchant services

Corporate services

Farming

HealthcareTravel

Cryptocurrencies

Mobile wallets

Crowd funding

Trading & Investment

Technology vendors

Non-FS vendors and

suppliers

BigTechs and FinTechs

Other banks Industry consortiums

Bank in an open ecosystem context

10© Capgemini 2019. All rights reserved |Open Banking: L’evoluzione dei pagamenti no-cash e il nuovo ruolo della banca | November 2019

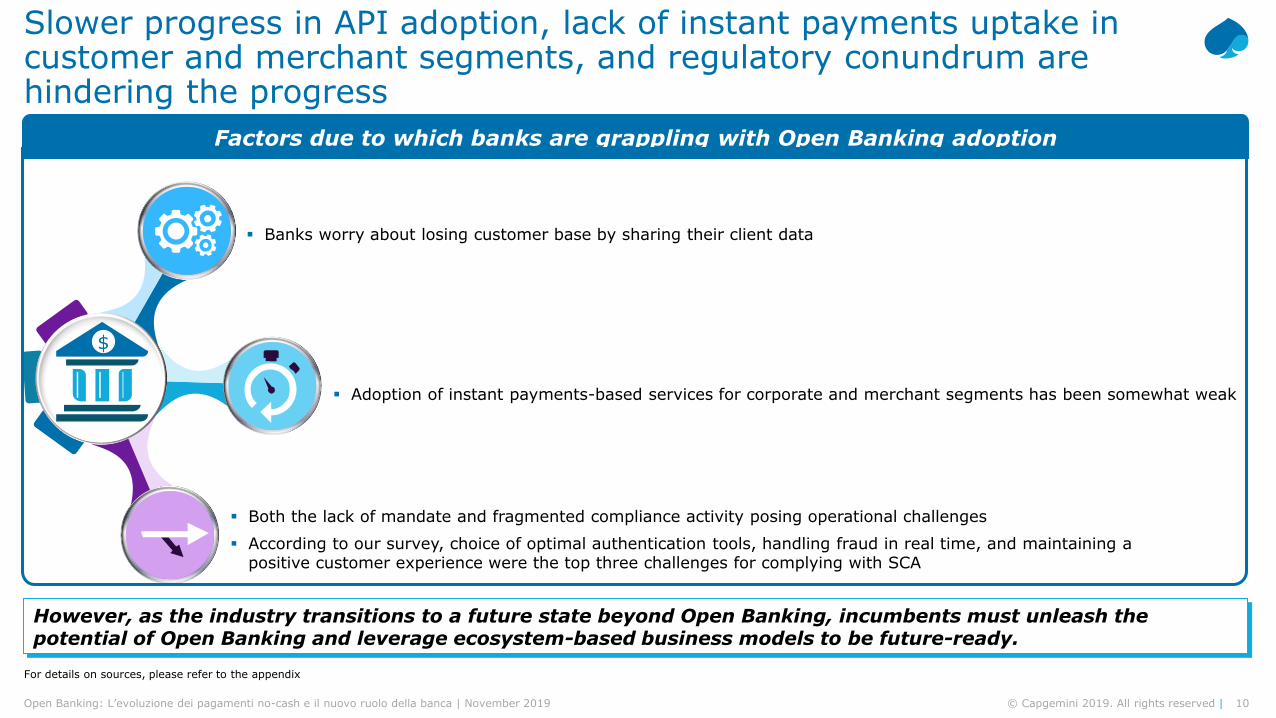

Slower progress in API adoption, lack of instant payments uptake in customer and merchant segments, and regulatory conundrum are hindering the progress

For details on sources, please refer to the appendix

However, as the industry transitions to a future state beyond Open Banking, incumbents must unleash the potential of Open Banking and leverage ecosystem-based business models to be future-ready.

▪ Banks worry about losing customer base by sharing their client data

▪ Adoption of instant payments-based services for corporate and merchant segments has been somewhat weak

▪ Both the lack of mandate and fragmented compliance activity posing operational challenges

▪ According to our survey, choice of optimal authentication tools, handling fraud in real time, and maintaining a positive customer experience were the top three challenges for complying with SCA

$

Factors due to which banks are grappling with Open Banking adoption

11© Capgemini 2019. All rights reserved |Open Banking: L’evoluzione dei pagamenti no-cash e il nuovo ruolo della banca | November 2019

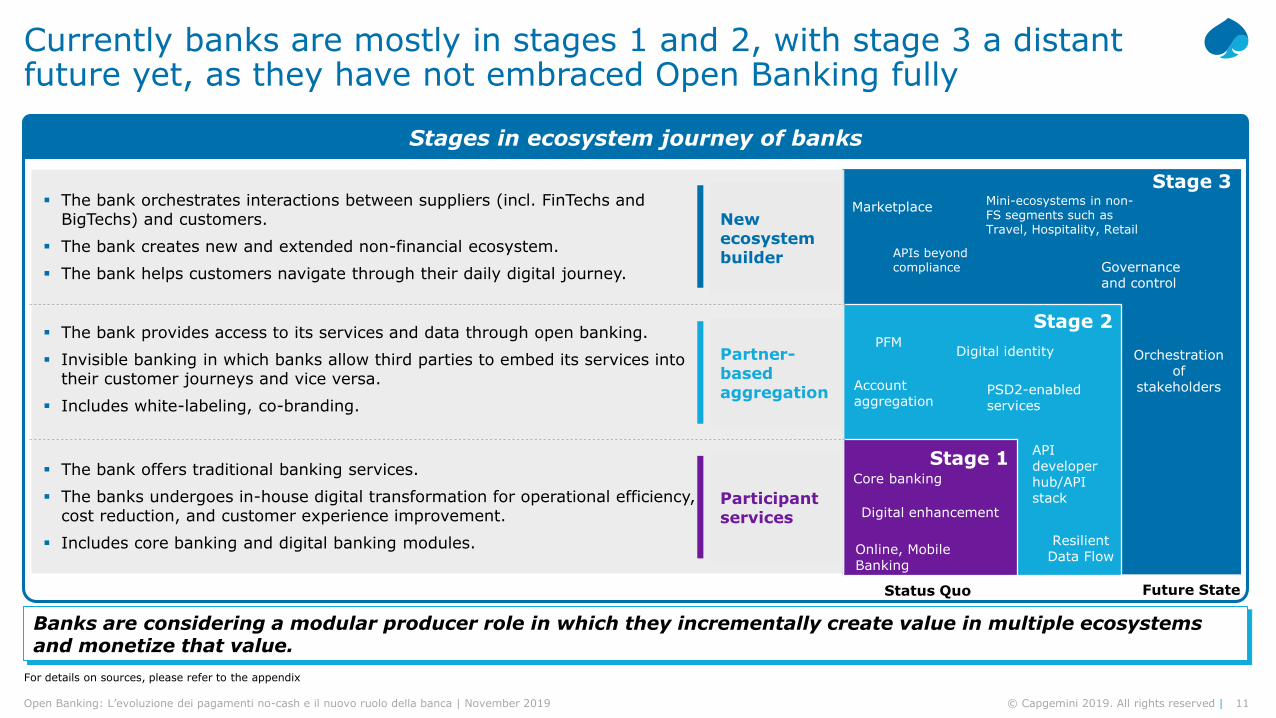

Currently banks are mostly in stages 1 and 2, with stage 3 a distant future yet, as they have not embraced Open Banking fully

For details on sources, please refer to the appendix

Stage 3

Core banking

Online, Mobile Banking

Digital enhancement

PFMDigital identity

Account aggregation

PSD2-enabled services

API developer hub/API stack

Marketplace

Orchestration of

stakeholders

Governance and control

Stage 2

Stage 1

Mini-ecosystems in non-FS segments such as Travel, Hospitality, Retail

APIs beyond compliance

Status Quo Future State

Resilient Data Flow

▪ The bank orchestrates interactions between suppliers (incl. FinTechs and BigTechs) and customers.

▪ The bank creates new and extended non-financial ecosystem.

▪ The bank helps customers navigate through their daily digital journey.

▪ The bank provides access to its services and data through open banking.

▪ Invisible banking in which banks allow third parties to embed its services into their customer journeys and vice versa.

▪ Includes white-labeling, co-branding.

▪ The bank offers traditional banking services.

▪ The banks undergoes in-house digital transformation for operational efficiency, cost reduction, and customer experience improvement.

▪ Includes core banking and digital banking modules.

Newecosystem builder

Partner-based aggregation

Participant services

Banks are considering a modular producer role in which they incrementally create value in multiple ecosystems and monetize that value.

Stages in ecosystem journey of banks

12© Capgemini 2019. All rights reserved |Open Banking: L’evoluzione dei pagamenti no-cash e il nuovo ruolo della banca | November 2019

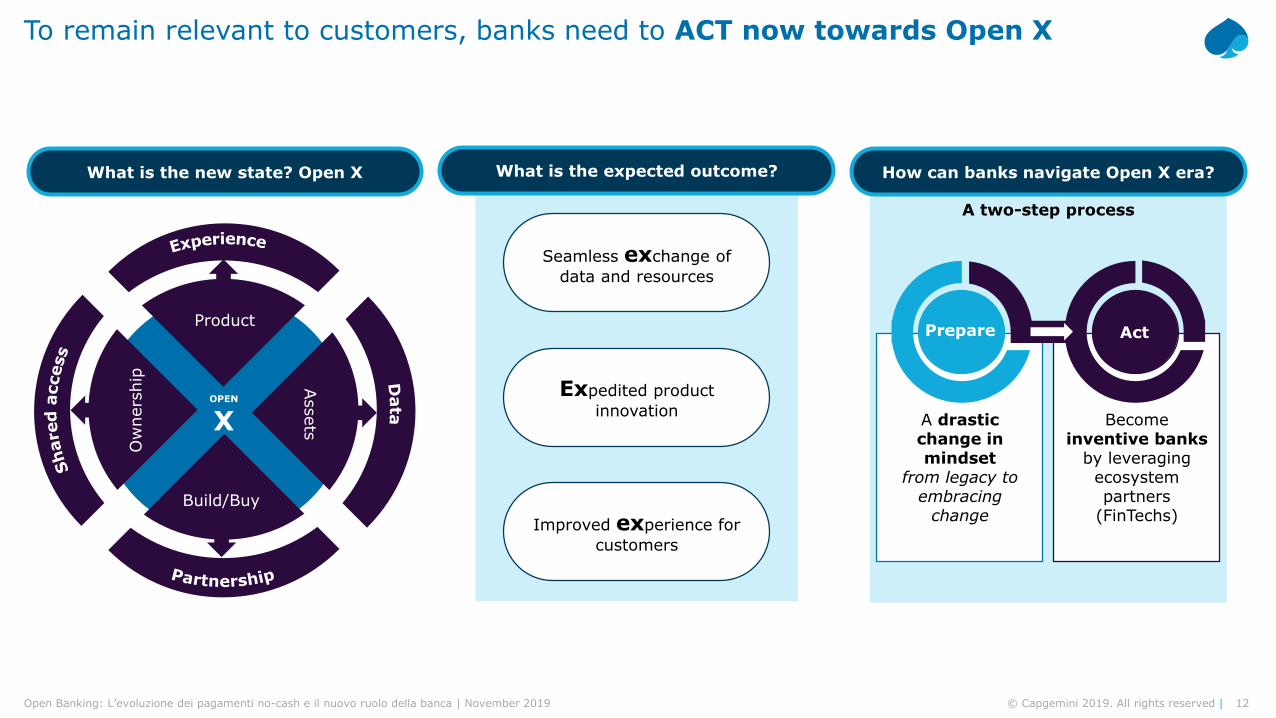

To remain relevant to customers, banks need to ACT now towards Open X

What is the new state? Open X

OPEN

X

Build/Buy

Assets

Product

Ow

ners

hip

Seamless exchange of

data and resources

Expedited product

innovation

Improved experience for

customers

What is the expected outcome?

A two-step process

How can banks navigate Open X era?

Become inventive banks

by leveraging ecosystem partners

(FinTechs)

A drastic change in mindset

from legacy to embracing

change

Prepare Act

13© Capgemini 2019. All rights reserved |

Contact

Monia Ferrari

Executive Vice President | Financial Services Director

E-mail: [email protected]

Open Banking: L’evoluzione dei pagamenti no-cash e il nuovo ruolo della banca | November 2019

A global leader in consulting, technology services and digital transformation,Capgemini is at the forefront of innovation to address the entire breadth of clients’opportunities in the evolving world of cloud, digital and platforms. Building on itsstrong 50-year heritage and deep industry-specific expertise, Capgemini enablesorganizations to realize their business ambitions through an array of services fromstrategy to operations. Capgemini is driven by the conviction that the businessvalue of technology comes from and through people. It is a multicultural companyof over 200,000 team members in more than 40 countries. The Group reported2018 global revenues of EUR 13.2 billion.

About Capgemini

Learn more about us at

www.capgemini.com

This presentation contains information that may be privileged or confidential and is the property of the Capgemini Group.

Copyright © 2019 Capgemini. All rights reserved.