Embed Size (px)

Citation preview

Enhancing Supply Chain Connectivity and Competitive ness of Malaysian Agriculture Products:

Identifying Chokepoints and Opportunities for Impro vement

Final Report submitted to

Economic Research Institute for ASEAN and East Asia (ERIA)

Fatimah Mohamed Arshad

Kusairi Mohd Noh Normaz Wana Ismail

Tai Shzee Yew Amna Awad Abdel Hameed

Ahmad Hanis Izani Abdul Hadi Ng Xin Khai

Mohd Khairul Rafiz Ramli Ng Keng Yap

Sahra Mohammadi

31st July 2013

Institute of Agricultural and Food Policy Studies (Institut Kajian Dasar Pertanian dan Makanan) Putra Infoport Universiti Putra Malaysia 43400 UPM Serdang Selangor, Malaysia Tel: (+6)03-8947 1076 Fax: (+6)03-8947 1077 Website: www.ikdpm.upm.edu.my Email: [email protected]

Enhancing Supply Chain Connectivity and Competitive ness of Malaysian Agriculture Products:

Identifying Chokepoints and Opportunities for Impro vement

Final Report submitted to

Economic Research Institute for ASEAN and East Asia (ERIA)

Fatimah Mohamed Arshad Kusairi Mohd Noh

Normaz Wana Ismail Tai Shzee Yew

Amna Awad Abdel Hameed Ahmad Hanis Izani Abdul Hadi

Ng Xin Khai Mohd Khairul Rafiz Ramli

Ng Keng Yap Sahra Mohammadi

31st July 2013

Institute of Agricultural and Food Policy Studies (Institut Kajian Dasar Pertanian dan Makanan) Putra Infoport Universiti Putra Malaysia 43400 UPM Serdang Selangor, Malaysia Tel: (+6)03-8947 1076 Fax: (+6)03-8947 1077 Website: www.ikdpm.upm.edu.my Email: [email protected]

iii

Acknowledgements

We would like to record our utmost appreciation to the Economic Research Institute for ASEAN and East Asia Economic (ERIA) for giving us the opportunity to conduct this research titled “Enhancing Supply Chain Connectivity and Competitiveness of Malaysian Agriculture Products: Identifying Chokepoints and Opportunities for Improvement”. In particular, we would like to thank the Executive Director of ERIA, Prof. Hidetoshi Nishimura, and Dr. Ponciano S. Intal, Jr, Leader and Coordinator of the Project for their trust in us. Our sincere thanks to Universiti Putra Malaysia for their support and facilities which enables us to conduct the project smoothly. We also are highly indebted to line agencies for providing insights, suggestions, comments and ideas in order to identify the chokepoints along the supply chain of palm oil and fish products as well as opportunities for improvement. The agencies involved are:

i. Ministry of Plantation Industries and Commodities (MPIC), ii. Malaysian Palm Oil Board (MPOB), iii. The Palm Oil Refiners Association of Malaysia (PORAM), iv. Royal Malaysian Customs Departments (Selangor, Kedah, Penang and Johor), v. Fisheries Development Authority of Malaysia (LKIM) (HQ, Penang and Kedah), vi. Department of Fisheries Malaysia (DoF) (Penang, Kedah, Putrajaya), vii. Northport (Malaysia) Bhd, viii. Johor Port Sdn. Bhd, ix. Asa Niaga Pelabuhan Barter Trade Sdn. Bhd., x. Sidhu Brothers Transport Sdn. Bhd, xi. Pasir Gudang Edible Oils Sdn. Bhd., xii. Felda Bulkers Sdn. Bhd., xiii. Syarikat Doyan Shipping & Forwarding (M) Sdn. Bhd., xiv. Seasons Forwarding and Distribution Agency Sdd. Bhd., xv. Orchid Shipping Forwarding & Contract Services Sdn. Bhd., and xvi. Malaysia Airlines Cargo Sdn. Bhd. A special thanks is due to Mr. Abdul Wahab Hassan, Senior Manager, Productivity and Quality Management at Northport (Malaysia) Bhd for his kindness in providing supports and insights into the study.

iv

We owe greatly to Dato’ Azis Bin Yacob, Director of Malaysian Royal Customs Department, Selangor for his warmth and kindness in receiving us at his office and his support to this study. We would like to express our gratitute towards our colleagues and members of the Institut Kajian Dasar Pertanian dan Makanan, Universiti Putra Malaysia for their tireless support which contributed to the successful completion of the project. Last but not least, we thank all the institutions and individuals who had lent their supports in providing inputs to the study. Fatimah Mohamed Arshad Kusairi Mohd Noh Normaz Wana Ismail Tai Shzee Yew Amna Awad Abdel Hameed Ahmad Hanis Izani Abdul Hadi Ng Xin Khai Mohd Khairul Rafiz Ramli Ng Keng Yap Sahra Mohammadi Institut Kajian Dasar Pertanian dan Makanan (Institute of Agricultural and Food Policy Studies) Putra Infoport, Universiti Putra Malaysia 43400 UPM Serdang Selangor, Malaysia 31st July 2013

v

Abstract This study aims to identify the chokepoints along the supply chain of palm oil and fish products in Malaysia as well as opportunities for improvement. Palm oil is categorised as “animal/vegetable fats and oils” (HS15) and fish products is categorised as “fish and crustaceans molluscs, and other aquatic invertebrates” (HS03). Both products play an important role in the country’s economy. In 2012, palm oil accounted for 49% of the agricultural GDP while fish (11%). Malaysia is the world’s second largest exporter of palm oil contributing RM 60 bn worth of foreign earning to the country. Very few references are available on the supply chain of agricultural produce and hence their competitiveness in the trade arena. In view of the growing importance of food trade in ASEAN, there is a need to review the supply chain of these two commodities particularly in terms of serious delays along the supply chain that is from the production point to the export/import sector. This study utilises a Key Informant Survey method to obtain relevant data and insights on the supply chains of the said commodities. This involved an in-depth interview with relevant stakeholders which include government agencies (such as Malaysian Palm Oil Board (MPOB), Fisheries Development Authority of Malaysia (LKIM), Department of Fisheries Malaysia (DoF) and Malaysian Royal Customs Department), port authorities, transporters and traders. A field survey using questionnaires prepared by Economic Research Institute for ASEAN and East Asia Economic (ERIA) (available at http://wbc.upm.edu.my/eria/) has been carried out from February to May 2013. A total of 111 questionnaires have been distributed to various agencies and stakeholders. However, only 87 responded and out of this total only 52 questionnaires are useable for analysis because of some of the respondents come from the same department hence they provide more or less similar answers. A case study approach is used in analysing the data or responses which are largely qualitative in nature. The study shows that a number of chokepoints exist in the supply chain of both commodities. In terms of the quality of infrastructure, the chokepoints identified are; limited capacities of most authorised laboratories, unstrategic location of these laboratories, limited number of refinery mills and bulking installations for palm oil in selected production areas such as in East Malaysia, congestion at the ports during peak period, lack of maintenance of port’s facilities and in the case of fish; insufficient import gates for land border crossing. In terms of internal transport and logistics, the chokepoints traced are: poor road condition (particularly around the port areas); traffic congestion at the port; high transportation cost; and pilferage of oil during transit. Pilferage of oil may not directly cause “choke”, but it has serious implication on food safety and the need for stringent testing. As for import and export clearance, the chokepoints observed are; firstly, different requirement of certificates demanded by importing countries which are strecthing the limited resources and facilities at the ports particularly the laboratories. Secondly, it was detected that some health certificates were written in foreign languanges by the importing countries. The chokepoints for certification and permit processes include; the requirement for halal certificate; non-standardised documentation requirements from importing countries; glitches in information system, threats to palm oil credibility due to Lynas rare earth processing project, preference on manual submission of documents, and lengthy period for import and export licenses issuance.

vi

There is lack of transparency and awareness of regulations. For instance, traders are not aware of International Air Transport Association (IATA) regulations on packaging and labelling requirements for transportation of fish through air cargo. Poor dissemination of rules and regulations has resulted in inconsistent intepretations among the officers at the port facilities. There are evidences to show that the industry is unable to handle strict hygienic standards required by the importing countries. It is clear that these chokepoints may hinder further progress of both sectors. The study has proposed some policies to rectify these problematic areas. These include; extensive infrastructural development and maintenance (such as roads, ports, bulking installations and laboratories), capacity building of staffs, total quality management of processes and procedures, monitoring of physical flow of products, effective maintenance of computer systems and effective regional collaboration and coordination.

vii

Contents Page

Acknowledgements ...................................................................................................... iii Abstract ......................................................................................................................... v

List of Abbreviations ................................................................................................... viii List of Tables ................................................................................................................ xi List of Figures .............................................................................................................. xii 1. Introduction .............................................................................................................. 1

2. Supply Chain of Palm Oil and Fish ........................................................................... 5

2.1 Palm Oil .............................................................................................................. 5

2.1.1 The Importance of Palm Oil to the Economy ................................................ 5

2.1.2 Product Description .....................................................................................10

2.1.3 Supply Chain of Palm Oil .............................................................................12

2.2 Fish Products .....................................................................................................30

2.2.1 Importance of Fish to the Economy .............................................................30

2.2.2 Product Description .....................................................................................32

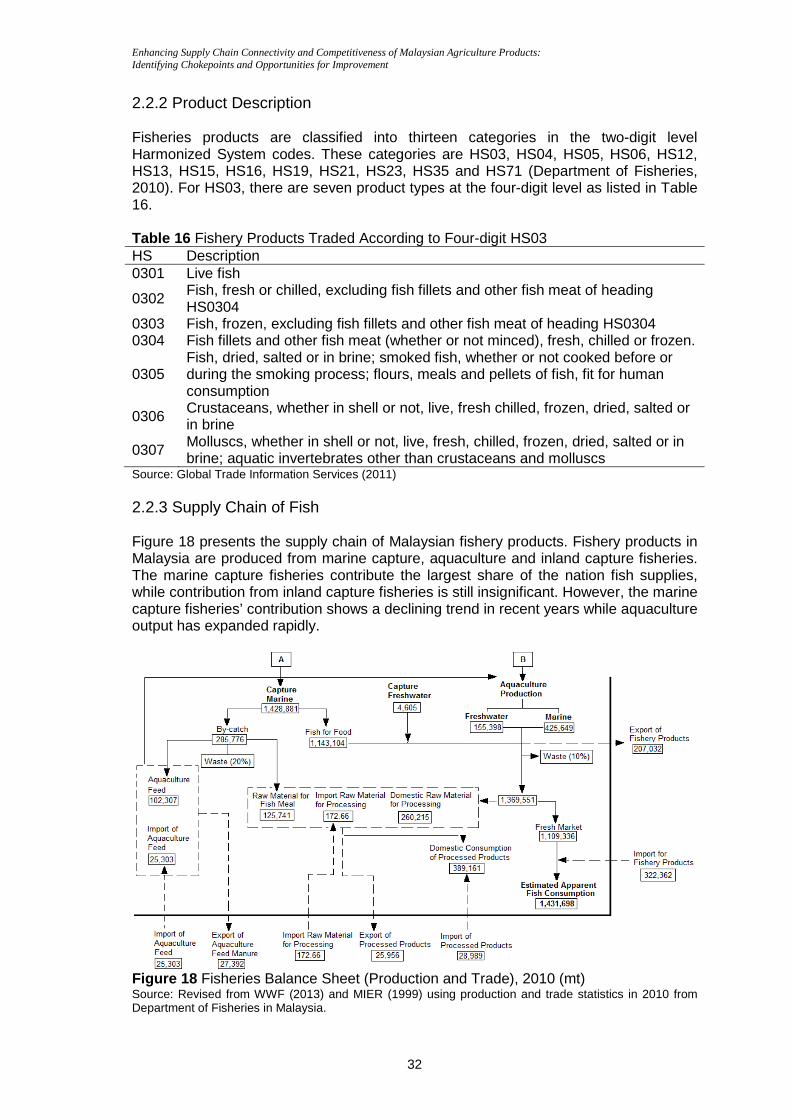

2.2.3 Supply Chain of Fish ...................................................................................32

3. Chokepoints in the Supply Chain .............................................................................40

3.1 Palm Oil .............................................................................................................40

3.1.1 The Quality of Infrastructure ........................................................................40

3.1.2 Internal Transport and Logistics ..................................................................42

3.1.3 Import and Export Clearance .......................................................................43

3.1.4 Certification and Permit Processes ..............................................................44

3.1.5 Transparency and Awareness of Regulations .............................................45

3.2 Fish Products .....................................................................................................46

3.2.1 The Quality of Infrastructure and Cold Chain ...............................................46

3.2.2 Internal Transport and Logistics ..................................................................46

3.2.3 Import and Export Clearance .......................................................................47

3.2.4 Certification and Permit Processes ..............................................................48

3.2.5 Transparency and Awareness of Regulations .............................................48

3.2.6 Non-tariff Measures .....................................................................................49

4. Policy, Regulatory and Institutional Issues...............................................................50

4.1 Palm Oil .............................................................................................................50

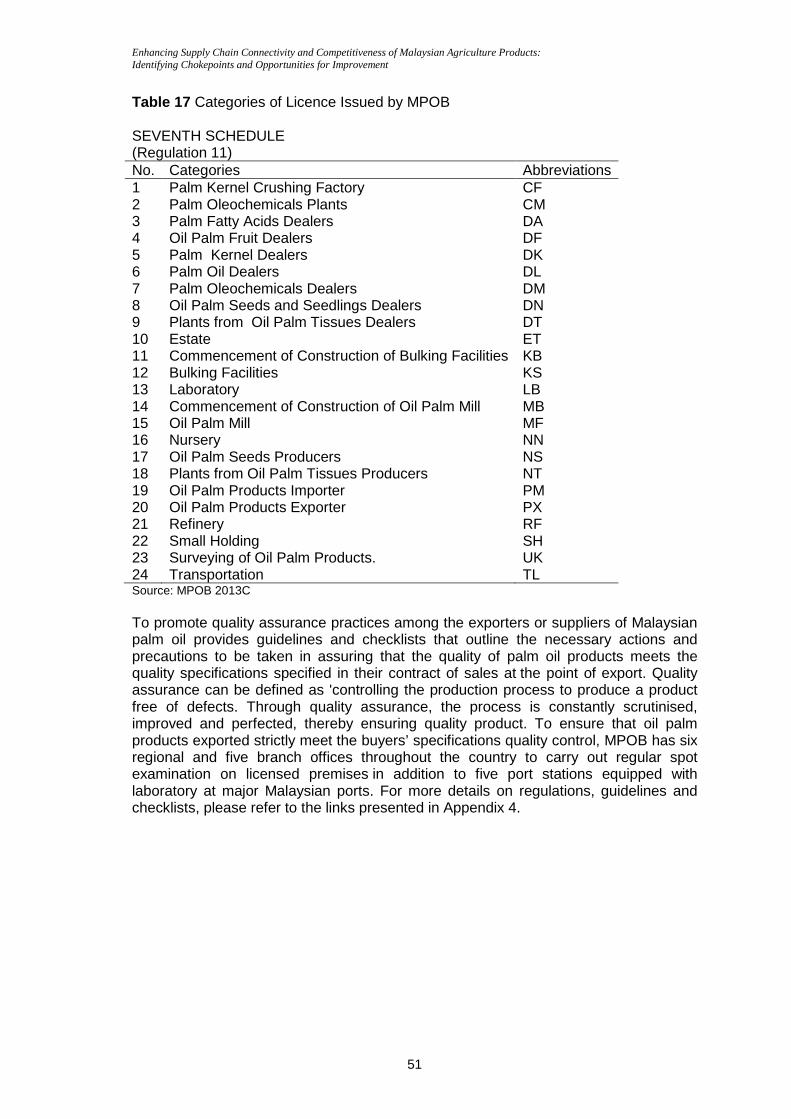

4.1.1 Acts, Regulations and Institutions Ruling the Palm Oil Industry ...................50

4.2 Fish Products .....................................................................................................55

4.2.1 Public Institutions Involved in Fishery Trade ................................................55

4.2.2 Acts, Regulations and Institutions Ruling the Fish Trade .............................55

4.2.3 Rules and Regulations for the Malaysian Fish Products in International Market ..................................................................................................................56

5. Conclusions and Recommendations .......................................................................58

5.1 Conclusions .......................................................................................................58

5.2 Recommendations .............................................................................................60

5.2.1 The Quality of Infrastructure ........................................................................60

5.2.2 Internal Transport and Logistics ..................................................................60

5.2.3 Import and Export Clearance .......................................................................61

5.2.4 Certification and Permit Processes ..............................................................61

5.2.5 Transparency and Awareness of Regulations .............................................62

5.2.6 Non-tariff Measures .....................................................................................62

References ..................................................................................................................63

Appendices .................................................................................................................67

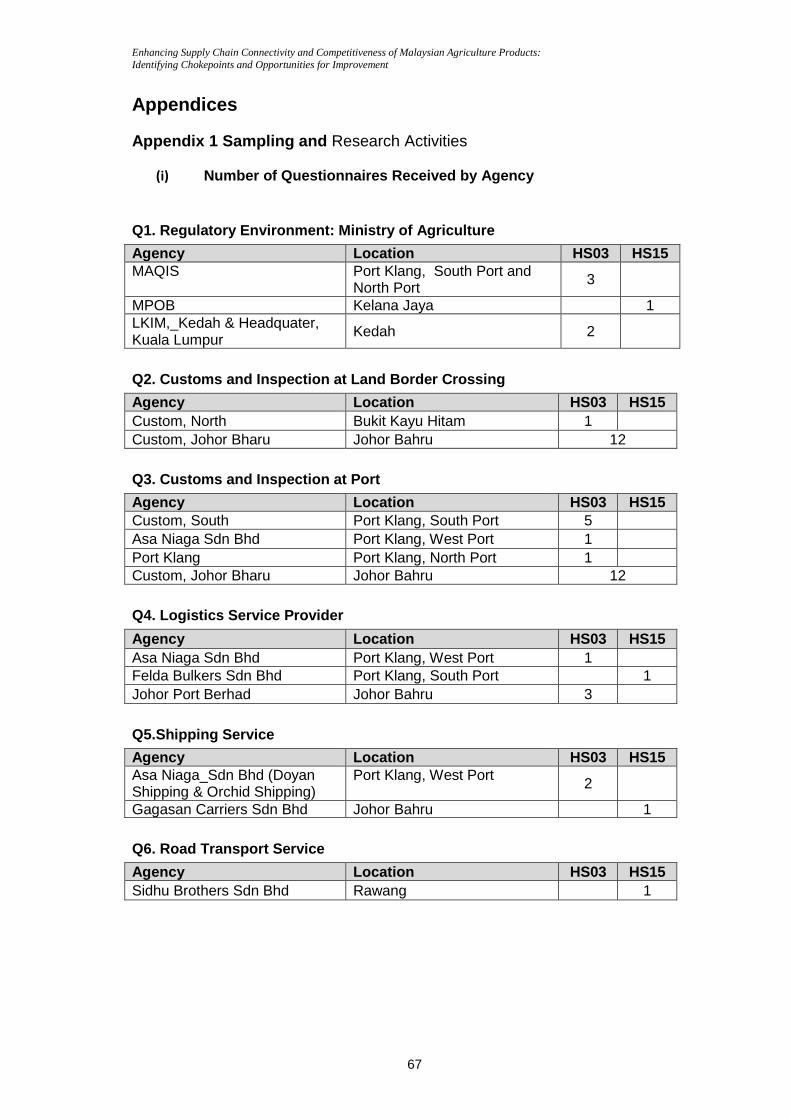

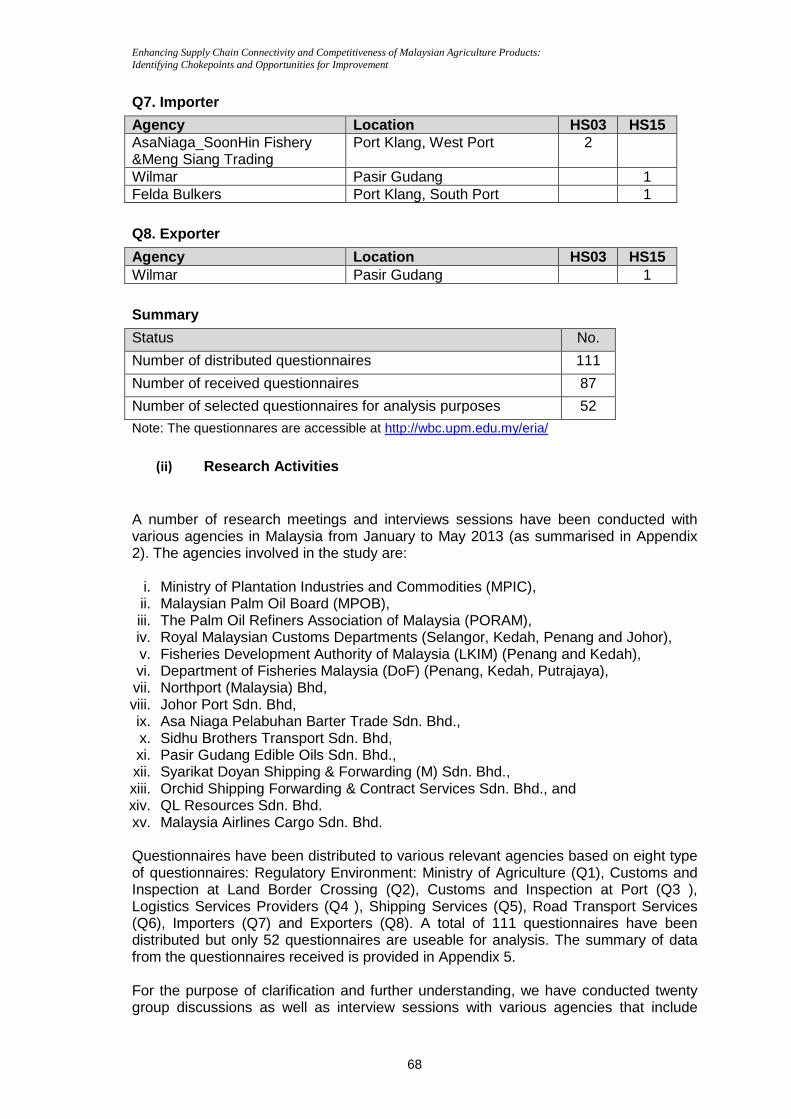

Appendix 1 Sampling and Research Activities .........................................................67

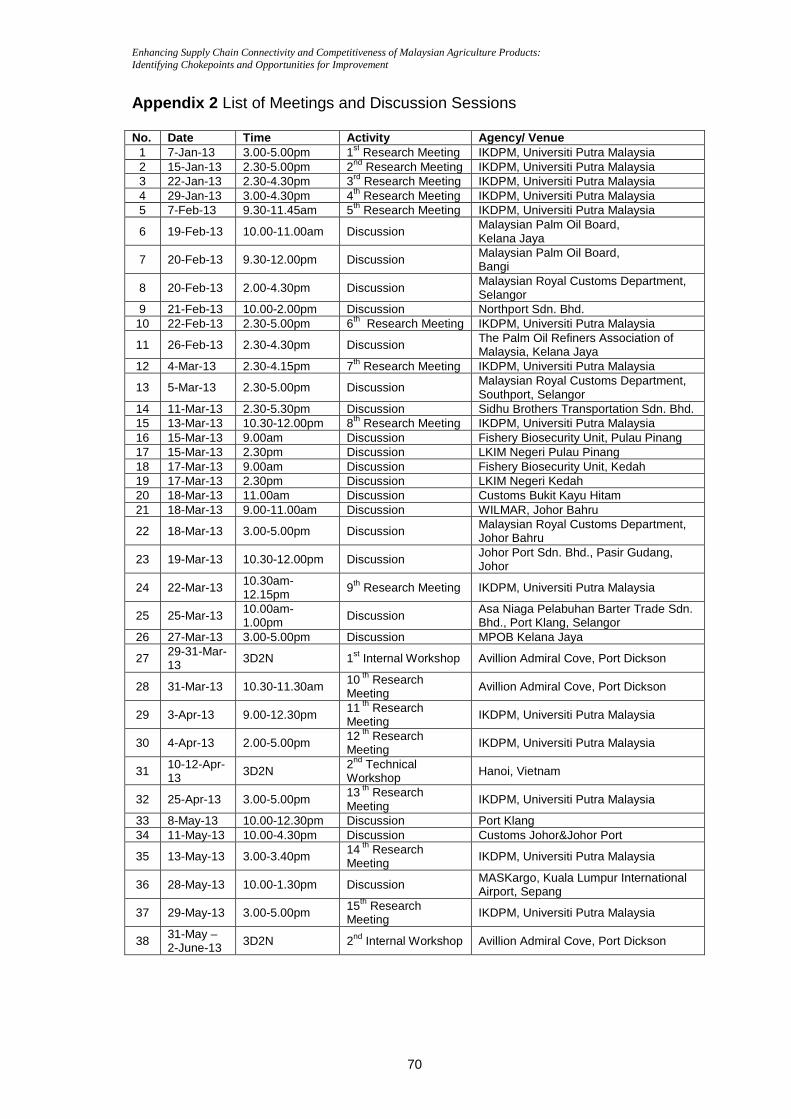

Appendix 2 List of Meetings and Discussion Sessions .............................................70

Appendix 3 List of Contacts .....................................................................................71

Appendix 4 List of Acts and Regulations ..................................................................74

Appendix 5 Summary of Questionnaires ..................................................................83

viii

List of Abbreviations AFTA ASEAN Free Trade Area AEC ASEAN Economic Community AFTA ASEAN Free Trade Area APEC Asia-Pacific Economic Cooperation ASEAN Association of Southeast Asia Nations ATIGA ASEAN Trade in Goods Agreement Bhd Berhad (Limited) BL Bill of Lading BOD Biochemical Oxygen Demand BPR Business Process Reengineering CAs Competent Authorities CEPT Common Effective Preferential Tariff

CITES Convention on International Trade in Endangered Species of Wild Fauna and Flora

COPs Codes of Practices COR Customs Official Receipt CPKO Crude Palm Kernel Oil CPO Crude Palm Oil CUSDEC Customs Declaration Message DB Doing Business DG Dangerous Goods DO Delivery Order DOA Department of Agriculture DOF Department of Fisheries EFB Empty Fruit Bunches EIA Environmental Impact Assessment EPCIS Electronic Product Code Information System EPF Employees Provident Fund EPP Entry Point Project ETI Enabling Trade Index EU European Union EQA Environmental Quality Act FAO Food and Agriculture Organization FBD Fisheries Biosecurity Division FDPM Forestry Department Peninsular Malaysia FELDA Federal Land Development Authority FFA Free Fatty Acids FFB Fresh Fruit Bunches FoSIM Food Safety Information System of Malaysia FQC First Quality Certificate FSQD Food Safety and Quality Division GAPs Good Agricultural Practices GDP Gross Domestic Product GHP Good Hygiene Practices GMP Good Manufacturing Practices HACCP Hazard Analysis Critical Control Point HS Harmonized System Codes IAS Invasive Alien Species IATA International Air Transport Association ICT Information and Communication Technology IED Integrated Export Document IID Integrated Import Document IPM Integrated Pest Management

ix

ISO International Organization for Standardization

JAKIM Jabatan Kemajuan Islam Malaysia (Malaysian Department of Islamic Development)

JKDM Jabatan Kastam DiRaja Malaysia (Royal Malaysian Customs Department)

JMEPA Japan-Malaysia Economic Partnership Agreement K1 Customs Declaration Form for Import K2 Customs Declaration Form for Export K9 Requisition/ Permit to Remove Dutiable Goods KIB Kotak Ikan Berinsulasi (Insulated Fish Boxes) LKIM Fisheries Development Authority of Malaysia LPI Logistic Performance Index MAMPU Malaysian Administrative Modernization and Management Planning Unit MAQIS Malaysian Quarantine and Inspection Services MCB Malaysian Cocoa Board MIER Malaysian Institute of Economic Research MITI Ministry of International Trade and Industry MOA Ministry of Agriculture and Agro-based Industry MOH Ministry of Health MOPGC Malaysian Oil Palm Growers Council MOT Ministry of Transport MPIC Ministry of Plantation Industries and Commodities MPOB Malaysian Palm Oil Board MPOPC Malaysian Palm Oil Promotion Council MRB Malaysian Rubber Board NBDPO Neutralised, Bleached and Deodorised Palm Oil NEKAD Fisher's Association Kedah NKEA National Key Economic Area NTB Non-Tariff Barriers OIE Office International Des Epizooties OPTEC Oil Palm Technology Centre OPGAP Oil Palm Good Agriculture Practice P.R. People's Republic PIA Permit Issuing Authorities PK Palm Kernel PKO Palm Kernel Oil PME Palm Oil Methyl Esters PNB Permodalan Nasional Berhad (National Equity Corporation) PORAM Palm Oil Refiners Association of Malaysia PORDB Palm Oil Research and Development Board PORIM Palm Oil Research Institute of Malaysia PORLA Palm Oil Registration and licensing Authority PPO Processed Palm Oil PSD Pharmaceutical Services Division RBD Refined Bleached Deodorized RBDPO Refined, Bleached and Deodorised Palm Oil RGA Rubber Growers’ Association RISDA Rubber Industry Smallholders Development Authority RM Ringgit Malaysia RPA Research in Priority Area RSPO Roundtable on Sustainable Palm Oil SAAB Sijil Amalan Akuakultur Baik (Good Aquaculture Practices Certificate) Sdn Bhd Sendirian Berhad (Private Limited) SMK Sistem Maklumat Kastam (Customs Information System) SOA Service Oriented Architecture

x

SPLAM Skim Pensijilan Ladang Akuakultur Malaysia (Malaysian Aquaculture Farm Certification Scheme )

SPS Sanitary and Phytosanitary SSOP Sanitation Standard Operating Procedures TREC Tamper Resistant Embedded Controller UN The United Nations UPAM United Planting Association of Malaysia UR Uruguay Round USA United State of America USD United States Dollar WTO World Trade Organization WWF World Wide Fund for Nature

xi

List of Tables Table 1 Malaysia’s Position in the World Ranking, 2012 .............................................. 2

Table 2 Value Added of Palm Oil and Percentage Contribution to the Malaysian GDP and Agriculture Sector, Value Added (at current price) (2005-2011) ............................. 5

Table 3 Contribution of Palm Oil to Total Malaysian Exports, (1960-2011) ................... 6

Table 4 Malaysia’s Export Volume (’000 mt) and Value (RM mn) of Primary Commodities and Commodity-based Products ............................................................. 6

Table 5 Malaysia’s Total Labour Force, Employment in Agriculture Sector and Palm Oil Estates (Number '000) during 1985-2011 ..................................................................... 7

Table 6 Malaysia’s Employment in the Primary Commodity Sector, 1990-2011 ........... 7

Table 7 Major Oil Palm Products of Malaysia and Their HS Codes .............................12

Table 8 Status of Port Bulking Installations, Malaysia, 2011 ........................................16

Table 9 Exports of Palm Products by Major Ports* (‘000 mt) in 2010 ...........................17

Table 10 Export Value and Quantities of Palm and Palm Kernel Oil Products from Malaysia in 2011 .........................................................................................................22

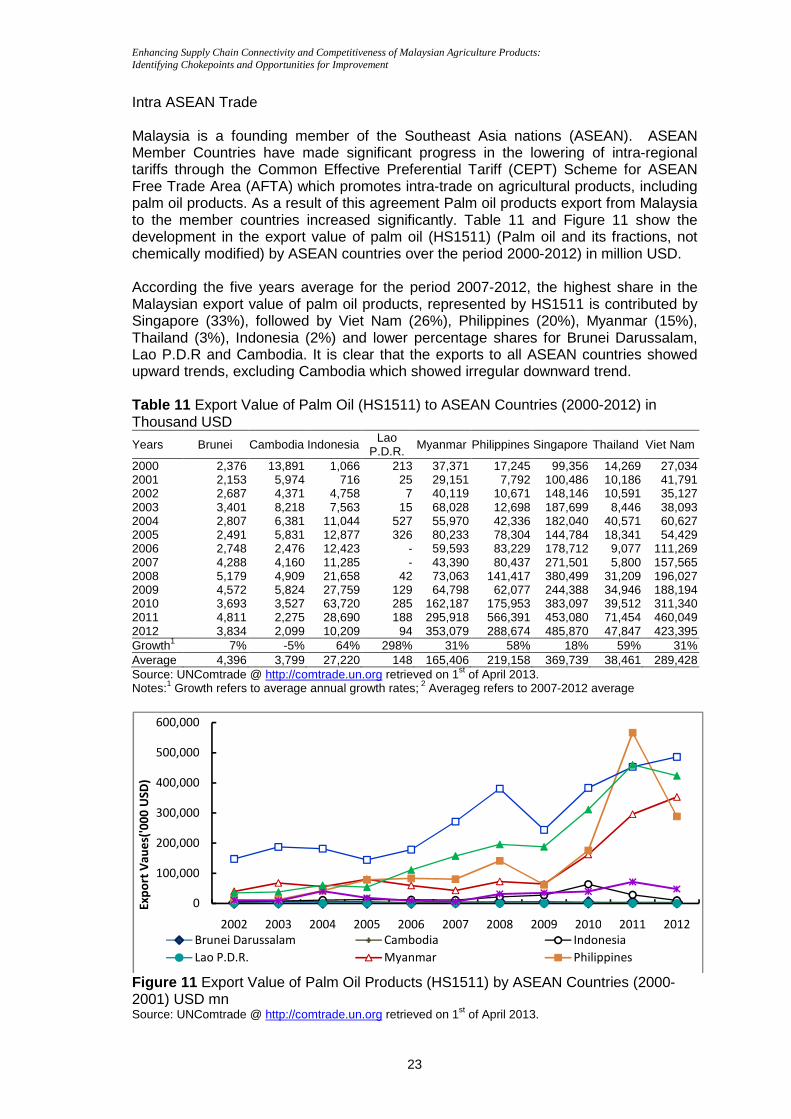

Table 11 Export Value of Palm Oil (HS1511) to ASEAN Countries (2000-2012) in Thousand USD ............................................................................................................23

Table 12 Intra-ASEAN Trade in Palm Oil Product: Malaysia Import from ASEAN (‘000 USD) ...........................................................................................................................24

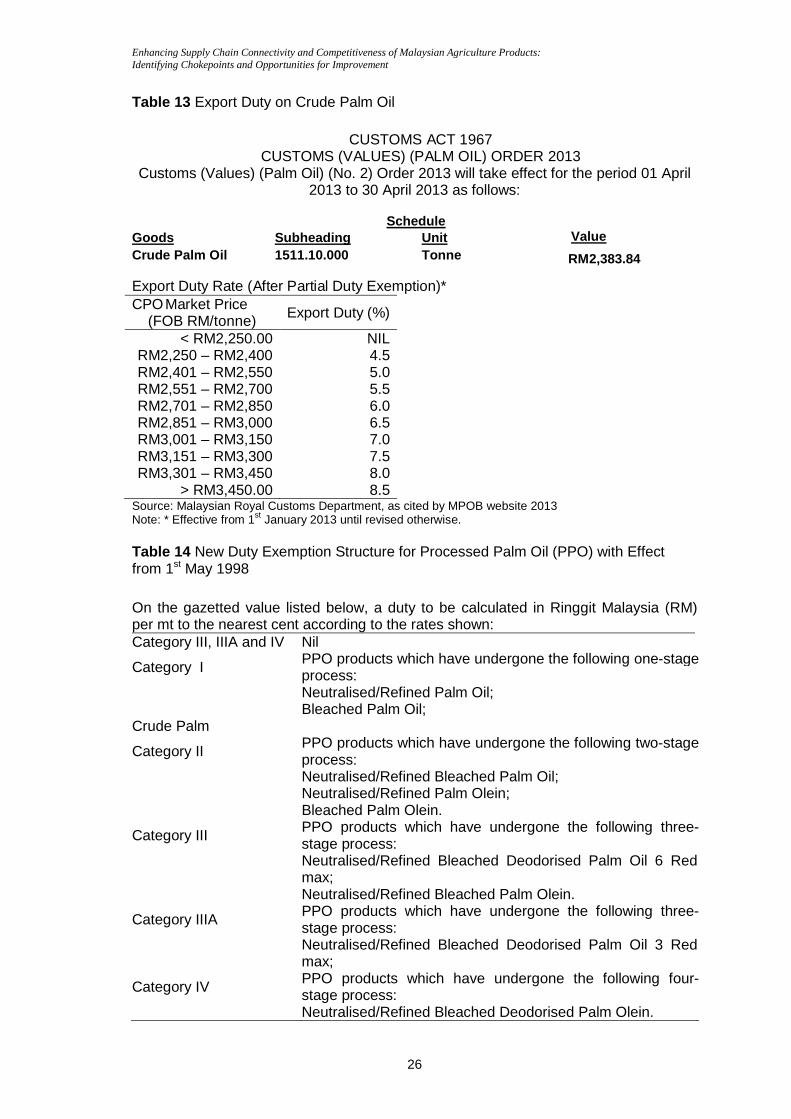

Table 13 Export Duty on Crude Palm Oil .....................................................................26

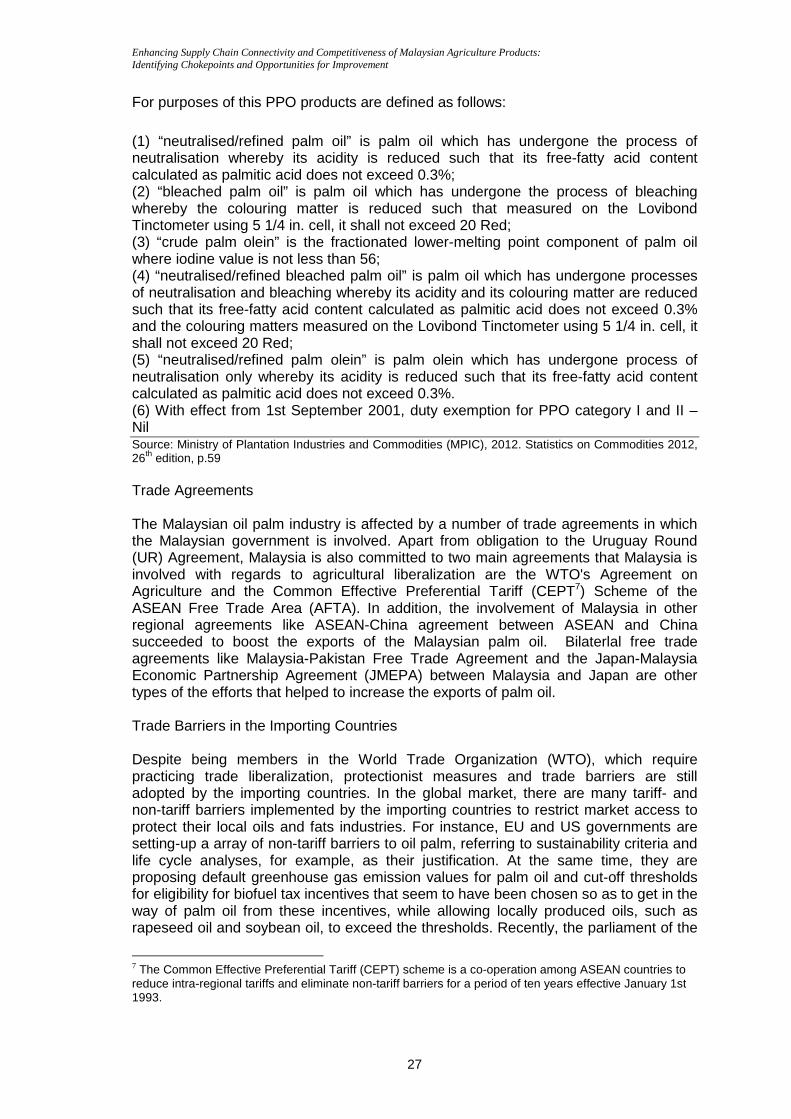

Table 14 New Duty Exemption Structure for Processed Palm Oil (PPO) with Effect from 1st May 1998 ................................................................................................................26

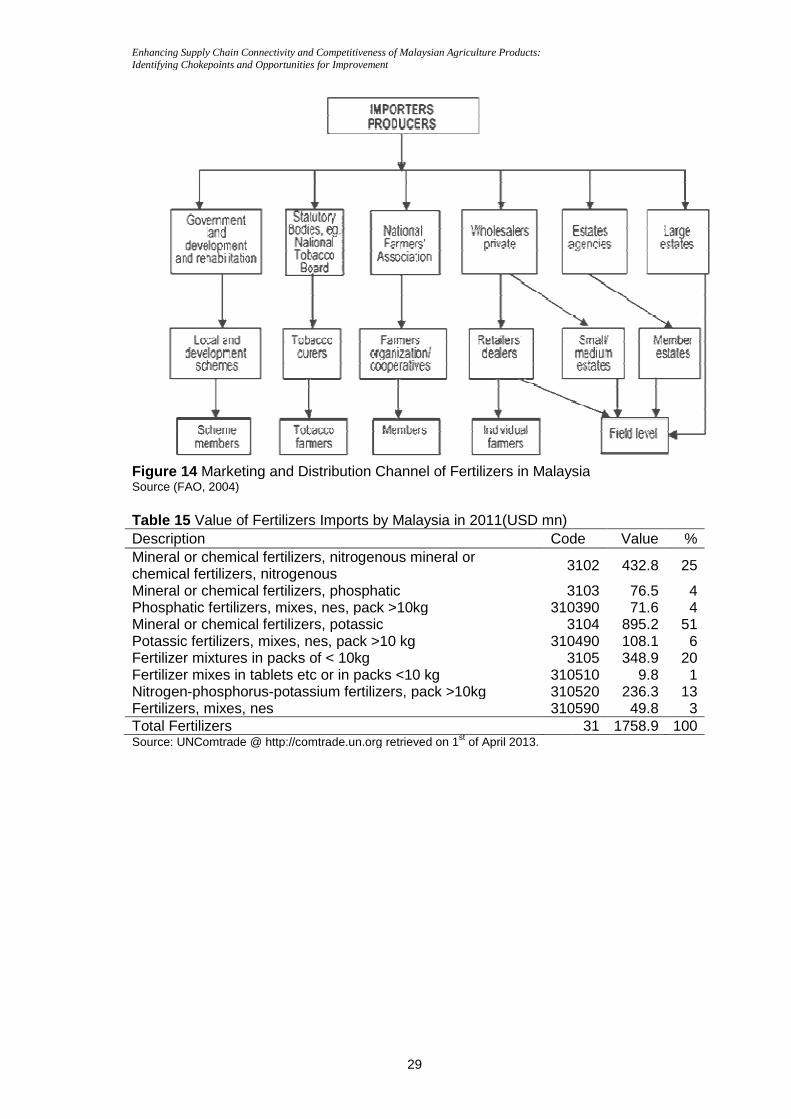

Table 15 Value of Fertilizers Imports by Malaysia in 2011(USD mn) ...........................29

Table 16 Fishery Products Traded According to Four-digit HS03 ................................32

Table 17 Categories of Licence Issued by MPOB .......................................................51

xii

List of Figures Figure 1 Major Players in the Palm Oil Supply Chain in Malaysia ..................................10

Figure 2 Palm Oil Processing Chart ............................................................................11

Figure 3 Supply Chain for Palm Oil in Malaysia ...........................................................13

Figure 4 Industry Players and Logistic Activities in the Supply Chain of Palm Oil in Malaysia ......................................................................................................................14

Figure 5 Export Flow: Liquid Bulk ................................................................................18

Figure 6 Import Flow: Liquid Bulk ................................................................................19

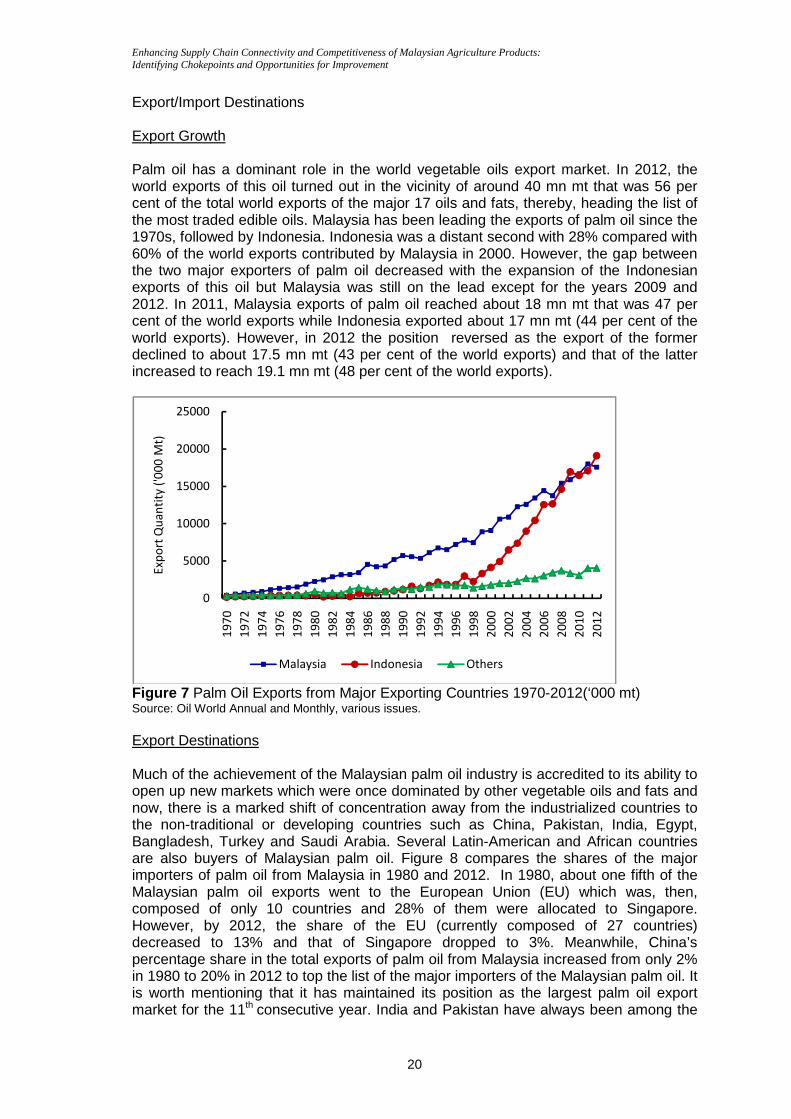

Figure 7 Palm Oil Exports from Major Exporting Countries 1970-2012(‘000 mt) ..........20

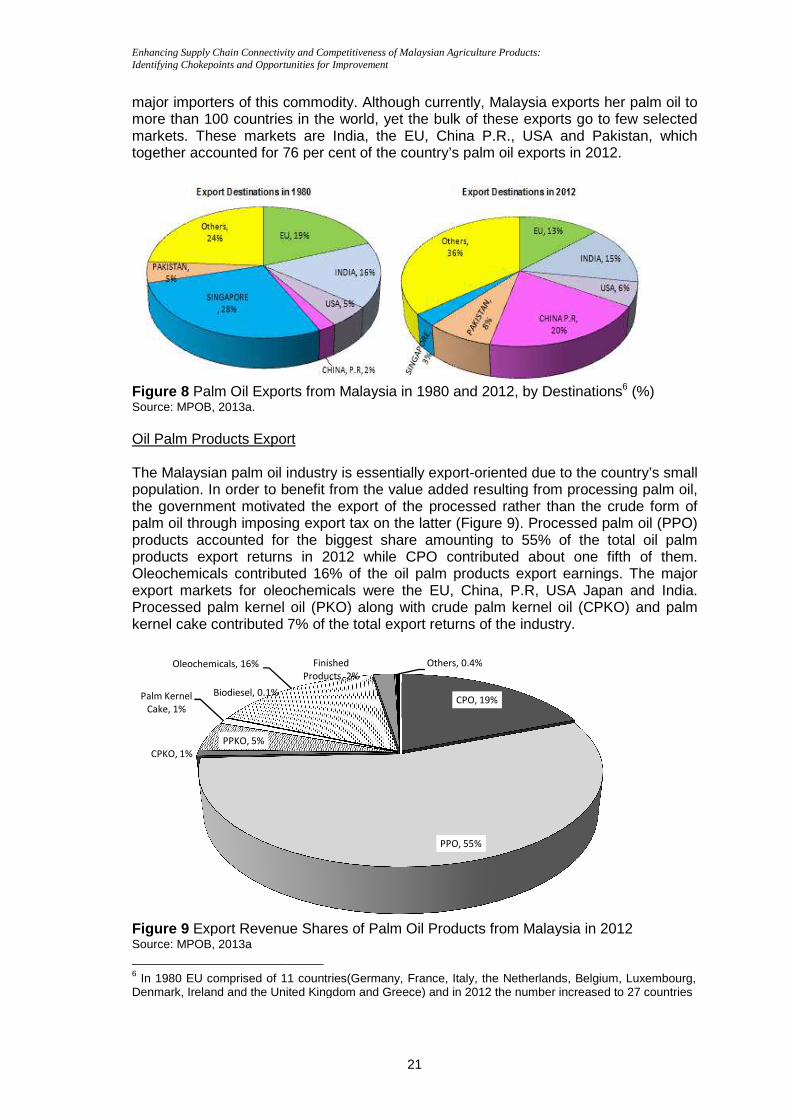

Figure 8 Palm Oil Exports from Malaysia in 1980 and 2012, by Destinations (%) ........21

Figure 9 Export Revenue Shares of Palm Oil Products from Malaysia in 2012 ............21

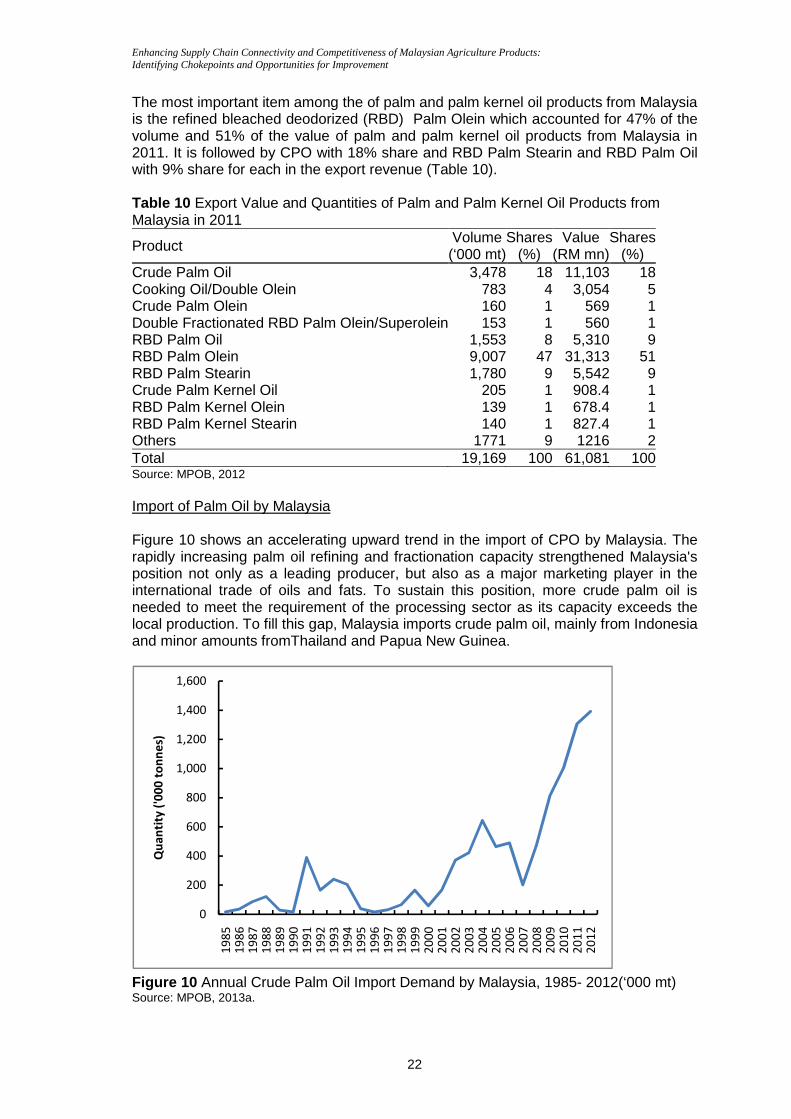

Figure 10 Annual Crude Palm Oil Import Demand by Malaysia, 1985- 2012(‘000 mt) .22

Figure 11 Export Value of Palm Oil Products (HS1511) by ASEAN Countries (2000-2001) USD mn ............................................................................................................23

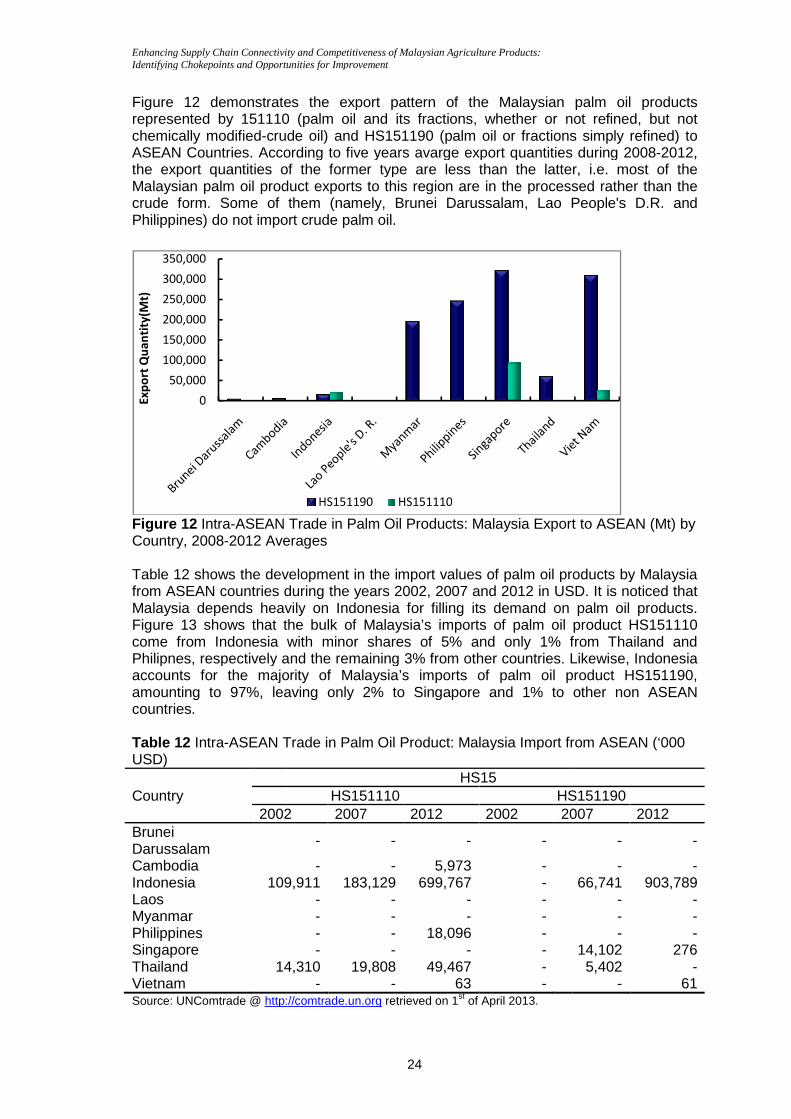

Figure 12 Intra-ASEAN Trade in Palm Oil Products: Malaysia Export to ASEAN (Mt) by Country, 2008-2012 Averages .....................................................................................24

Figure 13 Intra-ASEAN Trade in Palm Oil Products: Malaysia Import from ASEAN (Percentage Shares), 2010-2012 Averages ................................................................25

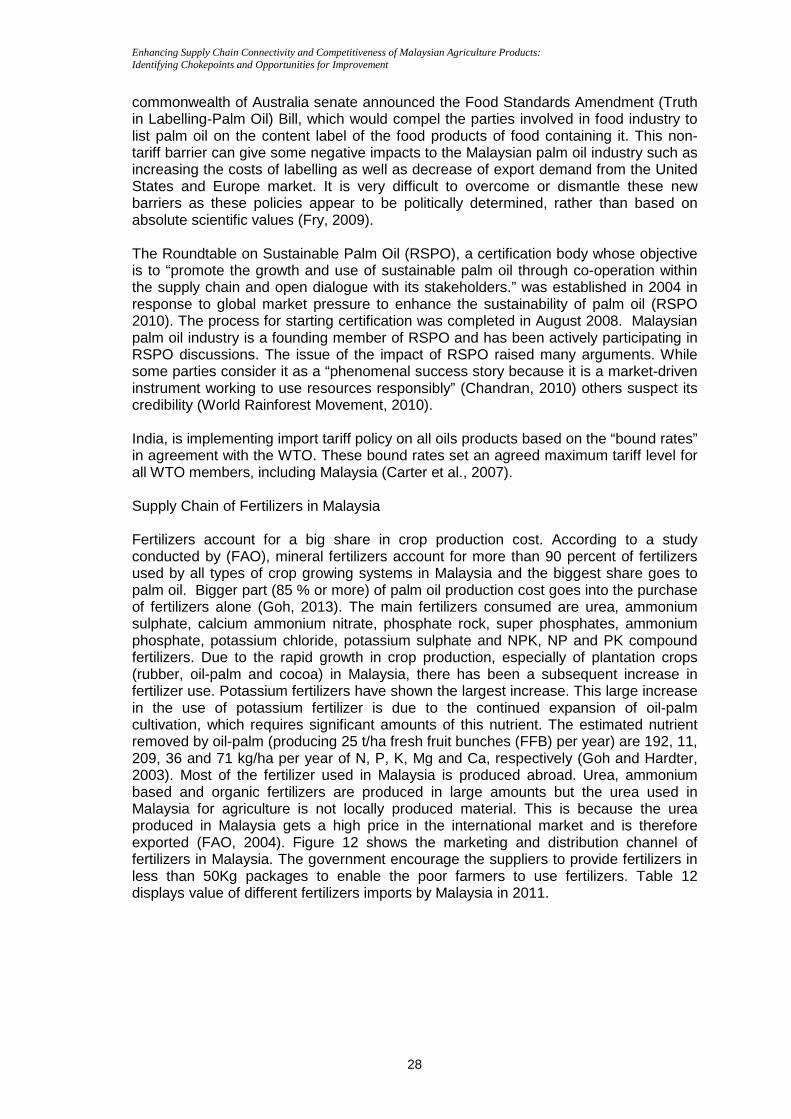

Figure 14 Marketing and Distribution Channel of Fertilizers in Malaysia ......................29

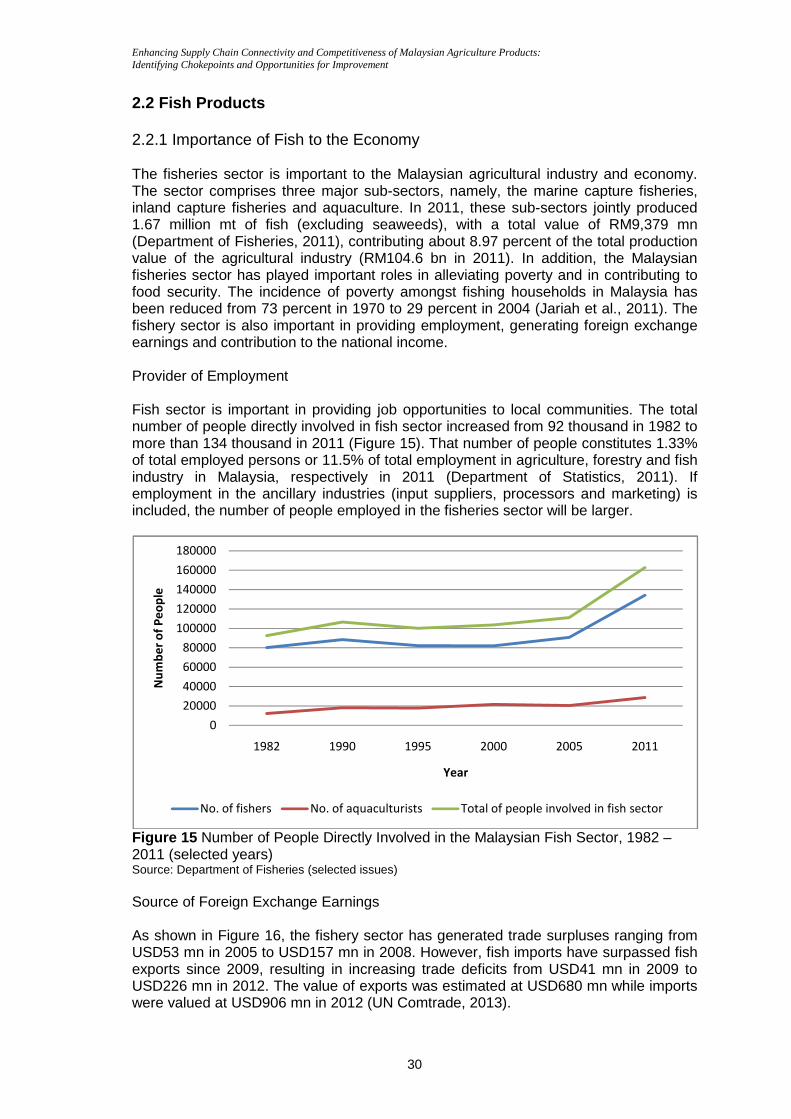

Figure 15 Number of People Directly Involved in the Malaysian Fish Sector, 1982 – 2011 (selected years) ..................................................................................................30

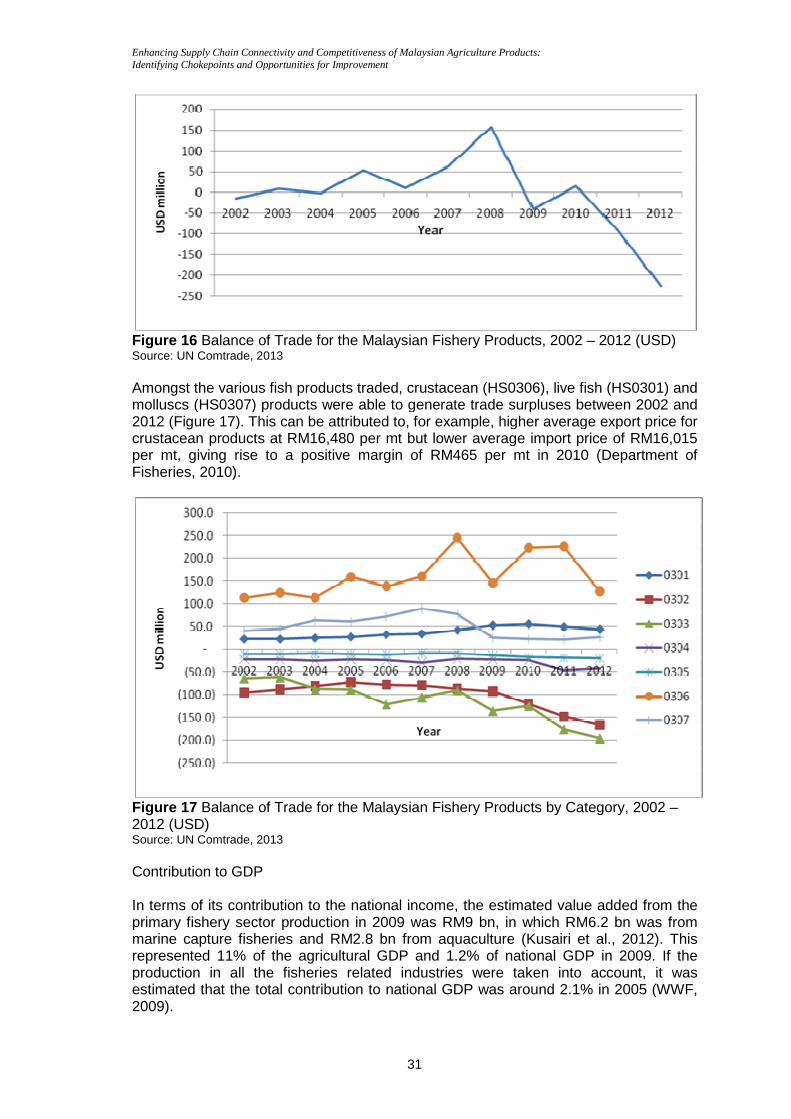

Figure 16 Balance of Trade for the Malaysian Fishery Products, 2002 – 2012 (USD) .31

Figure 17 Balance of Trade for the Malaysian Fishery Products by Category, 2002 – 2012 (USD) .................................................................................................................31

Figure 18 Fisheries Balance Sheet (Production and Trade), 2010 (mt) .......................32

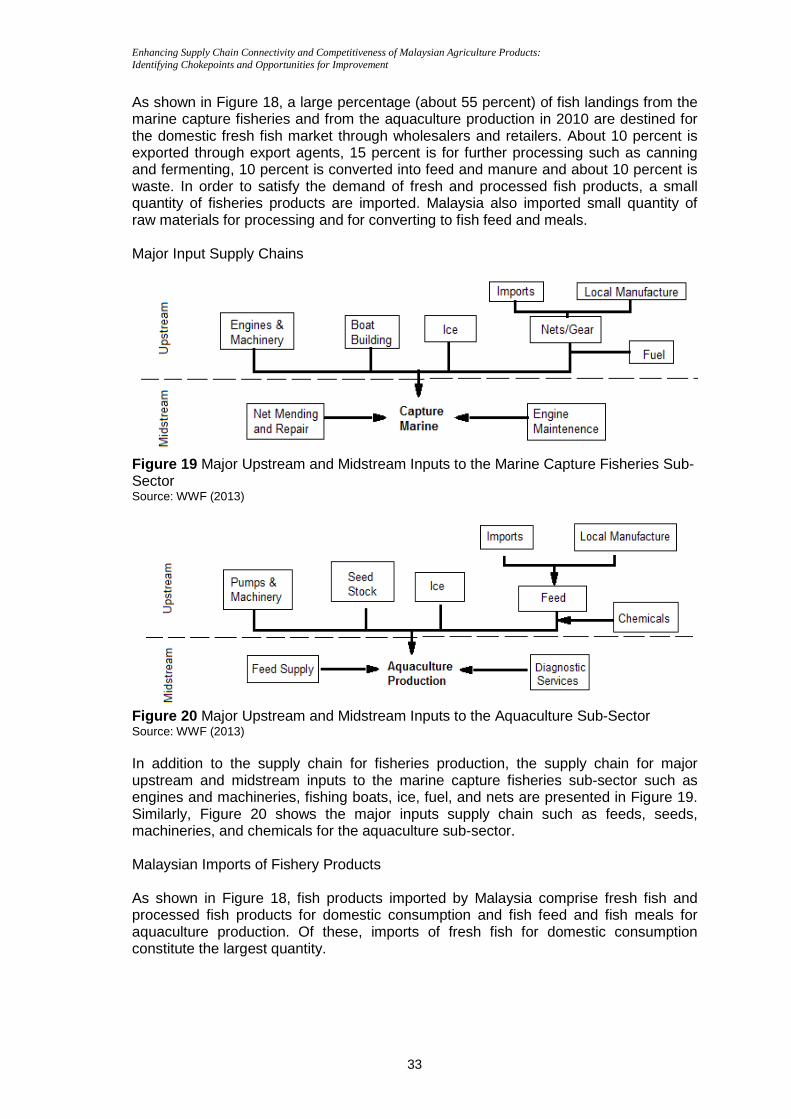

Figure 19 Major Upstream and Midstream Inputs to the Marine Capture Fisheries Sub-Sector..........................................................................................................................33

Figure 20 Major Upstream and Midstream Inputs to the Aquaculture Sub-Sector ........33

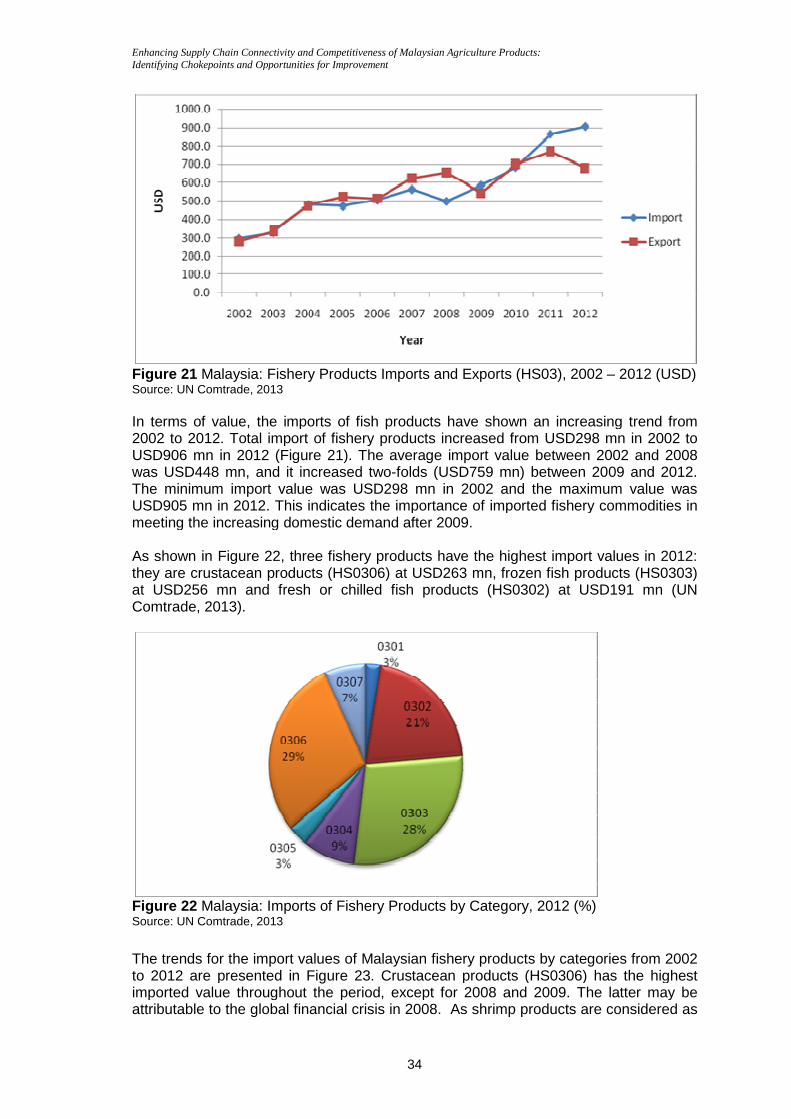

Figure 21 Malaysia: Fishery Products Imports and Exports (HS03), 2002 – 2012 (USD) ....................................................................................................................................34

Figure 22 Malaysia: Imports of Fishery Products by Category, 2012 (%) .....................34

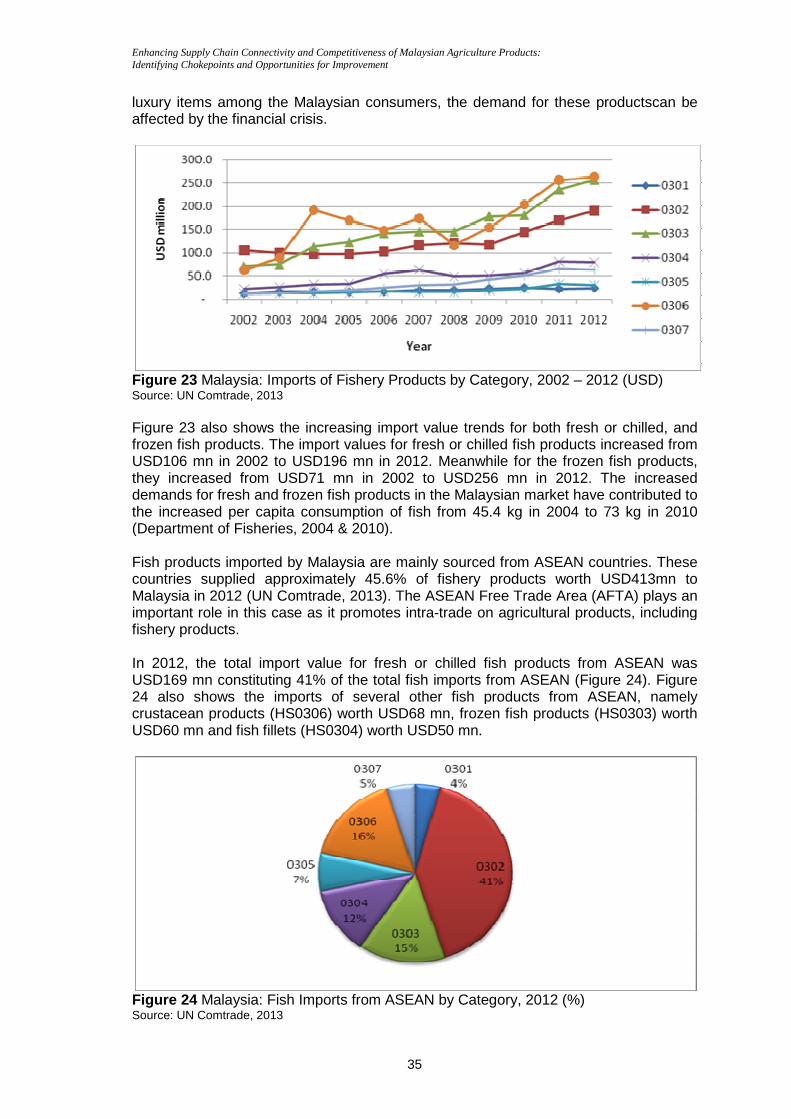

Figure 23 Malaysia: Imports of Fishery Products by Category, 2002 – 2012 (USD) .....35

Figure 24 Malaysia: Fish Imports from ASEAN by Category, 2012 (%) .......................35

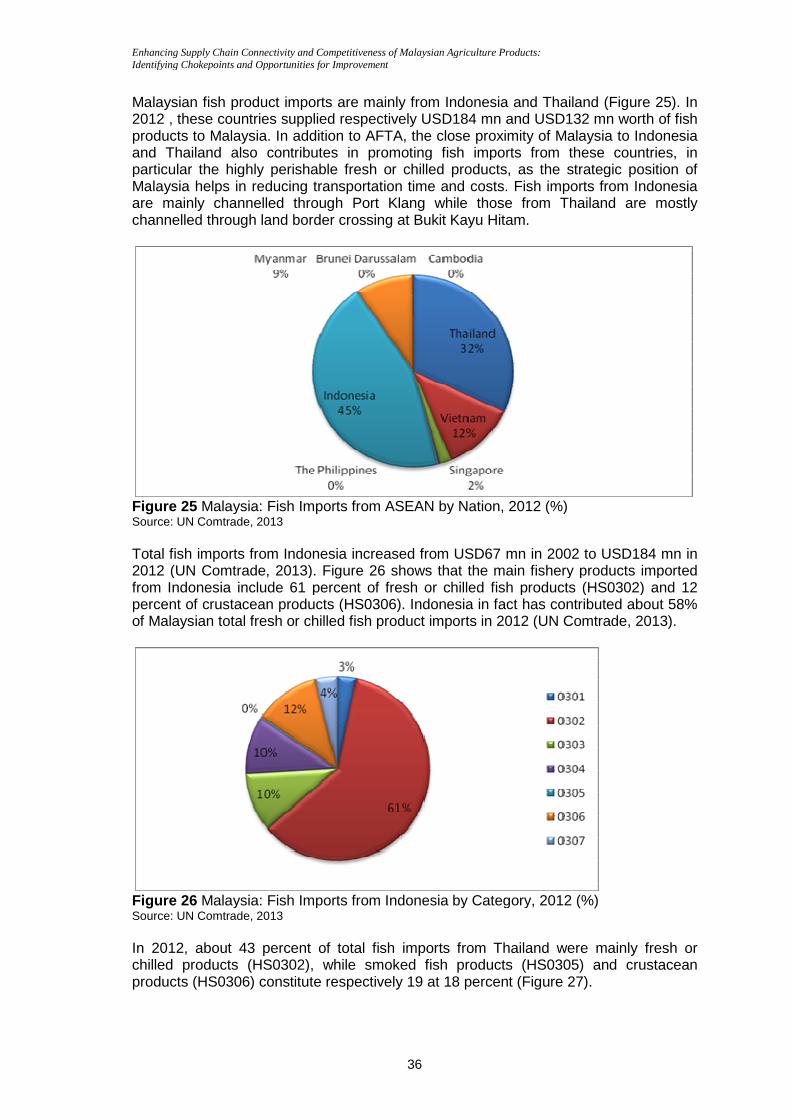

Figure 25 Malaysia: Fish Imports from ASEAN by Nation, 2012 (%) ...........................36

Figure 26 Malaysia: Fish Imports from Indonesia by Category, 2012 (%) ....................36

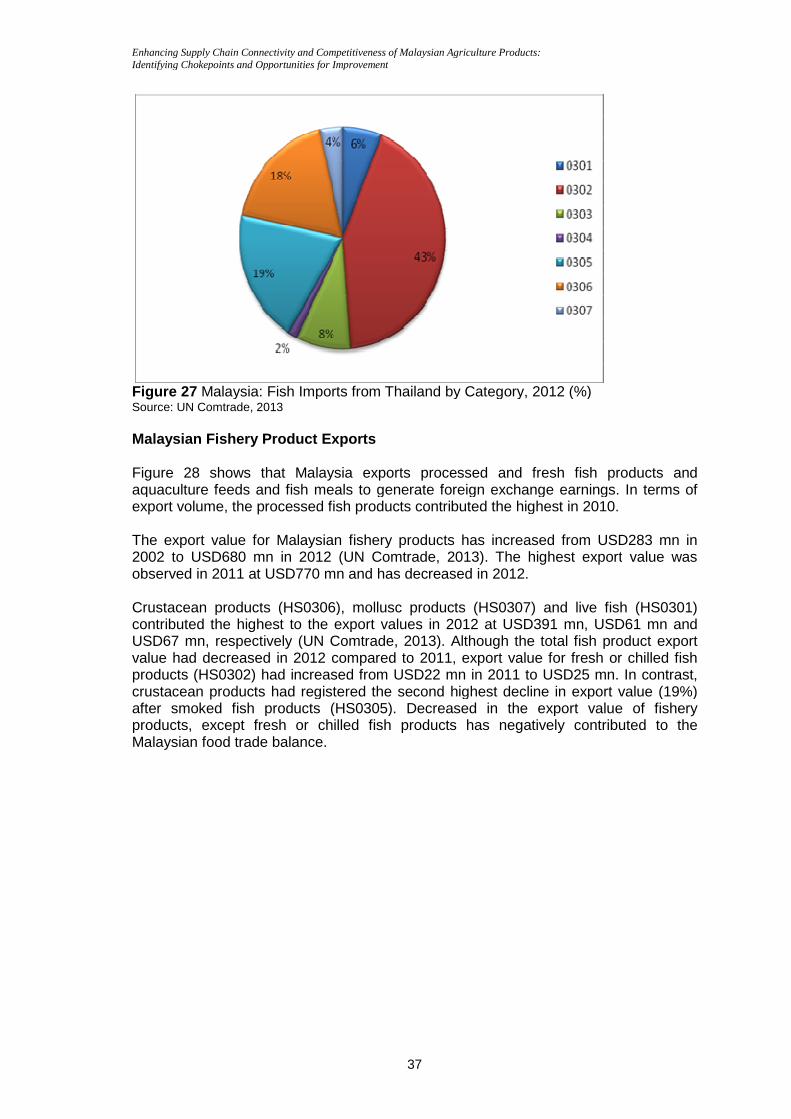

Figure 27 Malaysia: Fish Imports from Thailand by Category, 2012 (%) ......................37

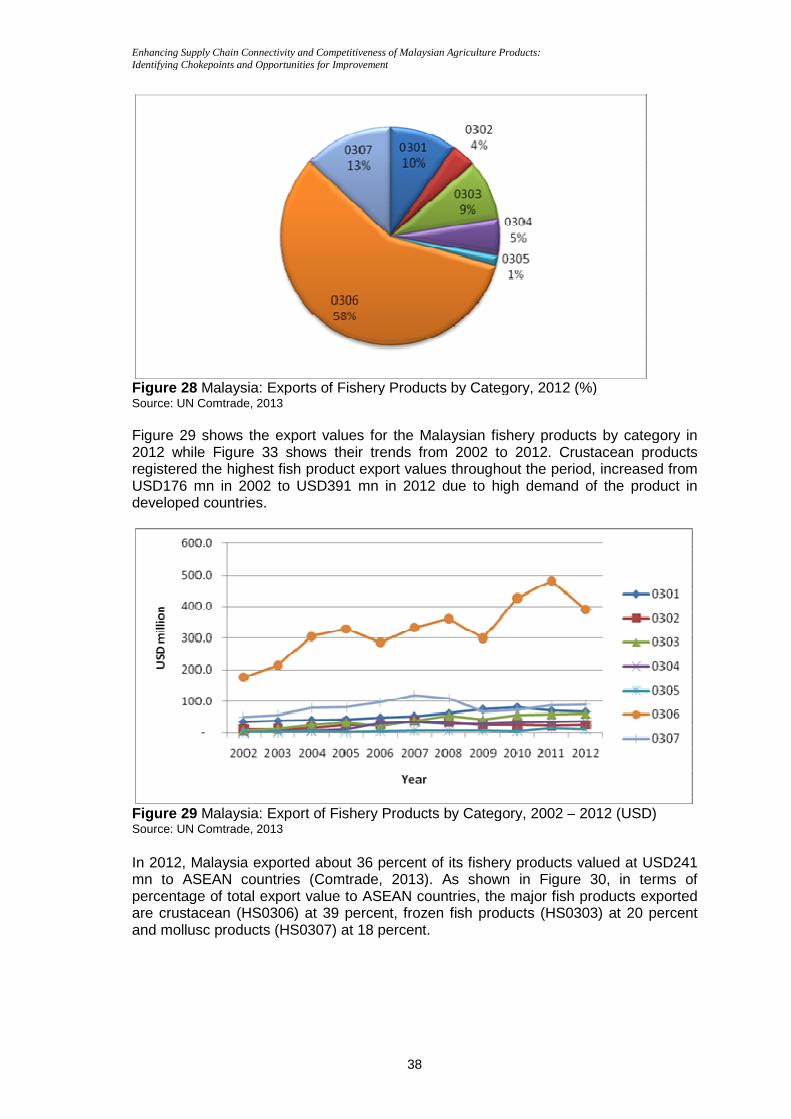

Figure 28 Malaysia: Exports of Fishery Products by Category, 2012 (%) ....................38

Figure 29 Malaysia: Export of Fishery Products by Category, 2002 – 2012 (USD) ......38

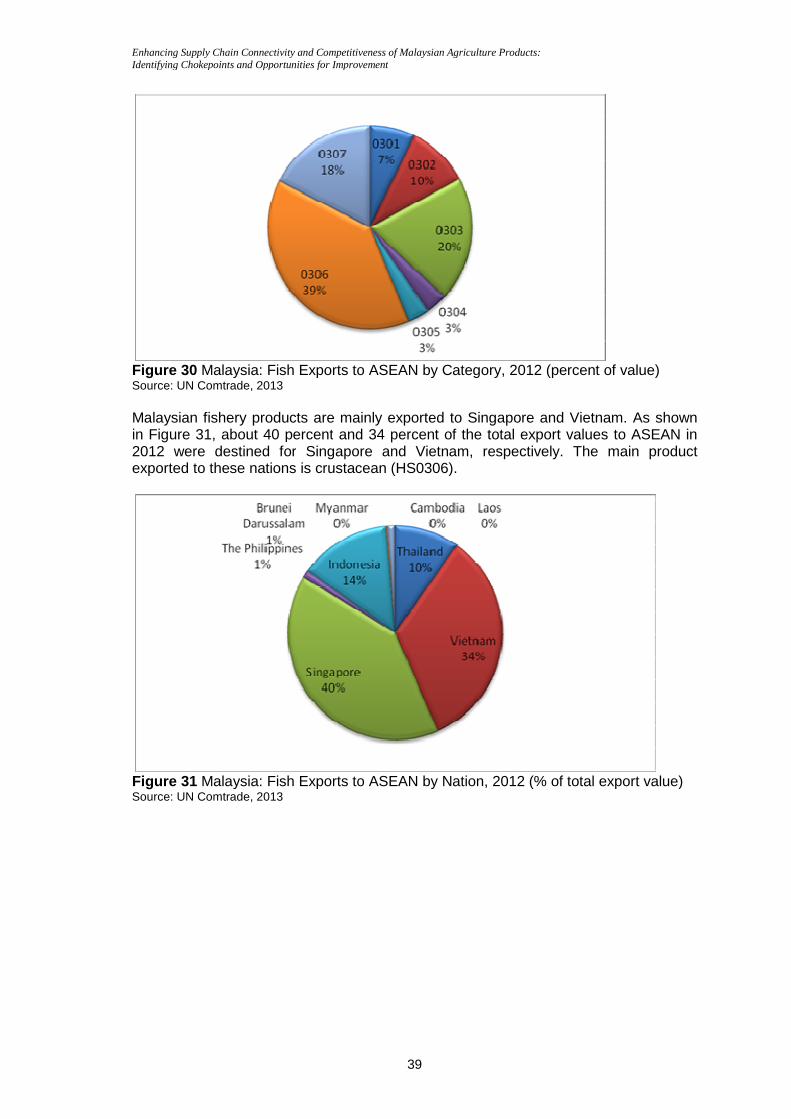

Figure 30 Malaysia: Fish Exports to ASEAN by Category, 2012 (percent of value) .....39

Figure 31 Malaysia: Fish Exports to ASEAN by Nation, 2012 (% of total export value) 39

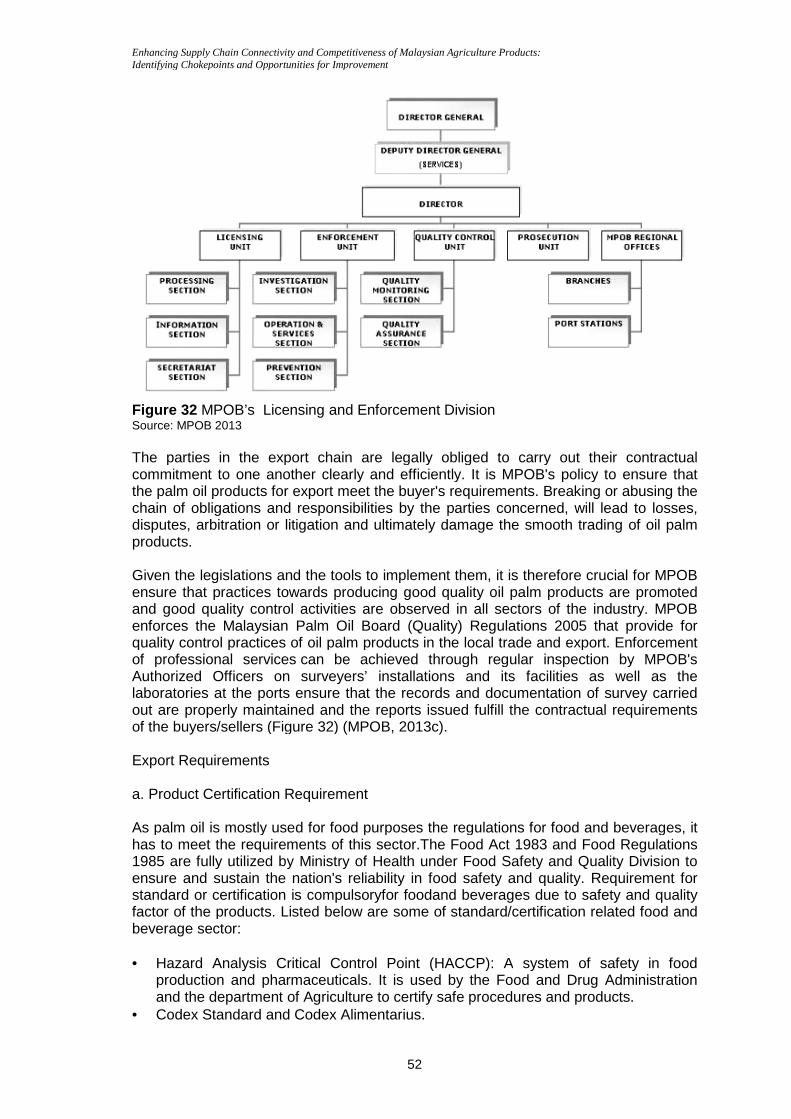

Figure 32 MPOB’s Licensing and Enforcement Division .............................................52

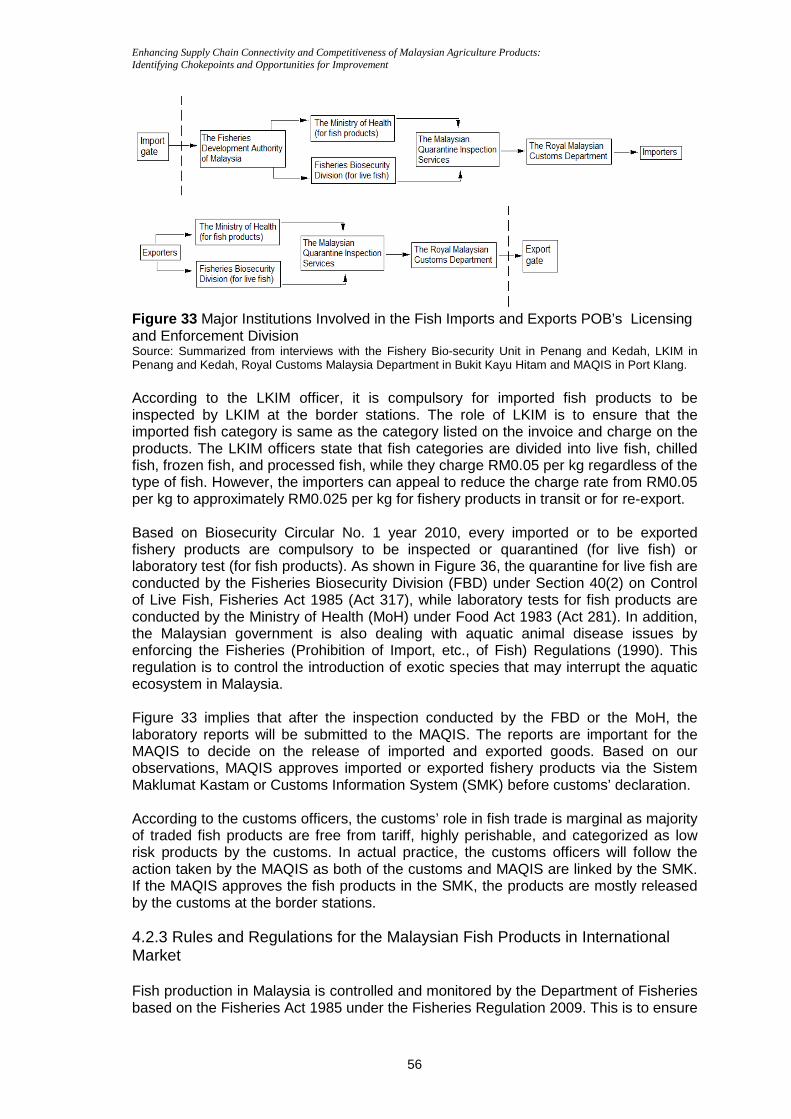

Figure 33 Major Institutions Involved in the Fish Imports and Exports POB’s Licensing and Enforcement Division............................................................................................56

Enhancing Supply Chain Connectivity and Competitiveness of Malaysian Agriculture Products: Identifying Chokepoints and Opportunities for Improvement

1

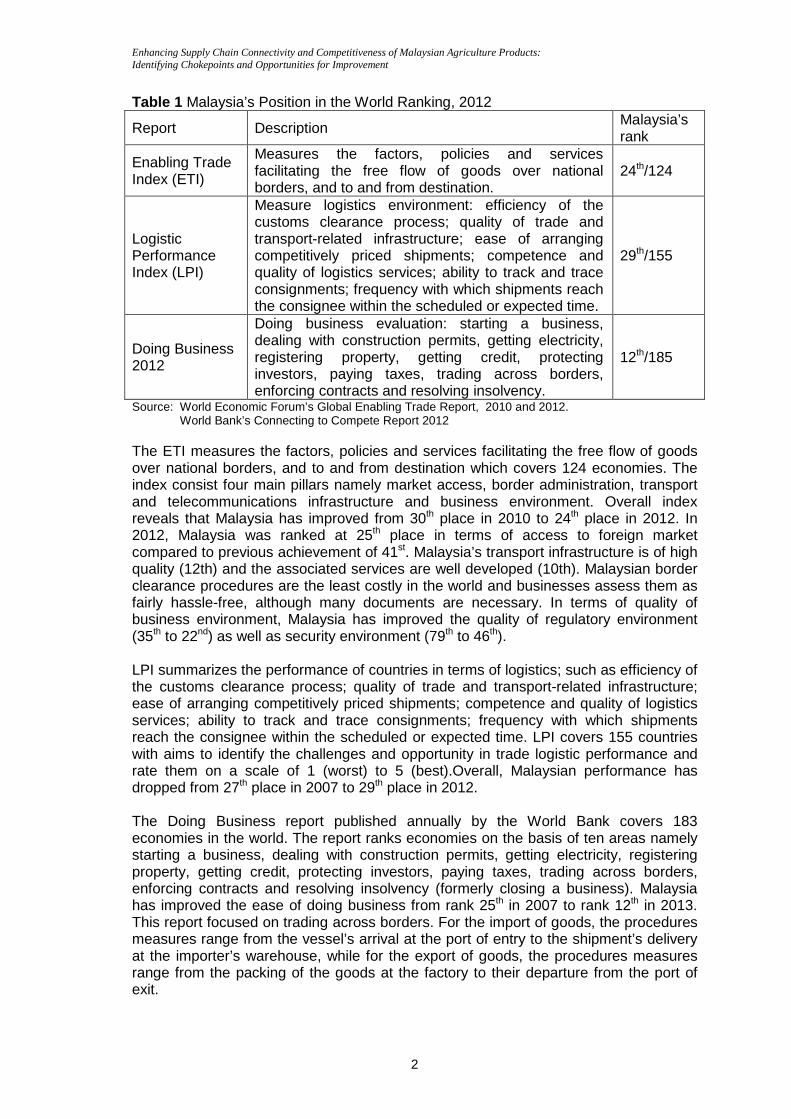

1. Introduction Supply chain evolves with changes in the trade landscape and environs. These changes include: globalization, technological advancement and emergence of new economic growth centres in Asia and other parts of the world. The ICT in particular revolutionize how trade and businesses are conducted across borders. For instance, the global supply network is characterized by speed delivery and definite delivery and high degree of custodial control throughout the supply chain. Under such a system, customs facilitation and logistics management are important processes in ensuring fast and reliable links to international markets and supply chains. One new dimension added to the framework of supply chain is the importance of connectivity which is defined as the “conduits” for flows of goods, services, capital, information and ideas around the world (PECC, 2009). These conduits provide the links between supply chain members, stakeholders and customers. Connectivity allows sharing of information between customers and suppliers, supply chain collaboration and time-based logistics solutions (Hoffmann, 2009). This in turn may lead to cost reductions and higher efficiency, i.e. savings in cycle times and reduction in ordering errors. Connectivity is a catalyst for trade and investment with enabler and multiplier effects for the wider socio-economy. However, as summarized by a study carried by USC (2011), the supply chain in ASEAN countries are plagued with “chokepoints”, inefficiencies and barriers which impose time delays, raise transaction costs, increase supply chain risk and uncertainty. The supply chain for food products in particular are at a higher risk due to its unique characteristics such as unstable or seasonal production, products are often bulky and perishable and require specialized equipments. In this regard, Asean Economic Community (AEC) Blueprint has identified the need for enhancing intra-and extra-ASEAN trade and long term competitiveness of ASEAN’s food, agriculture and forestry products/commodities. Identifying supply “chokepoints” is necessary as they are the pre-requisite inputs for the formulation of a more integrated, and hence more competitive ASEAN food trade. Staying competitive is neccesary for growth in a highly globalised world. “Competitiveness index” is the currency of trade as it provides the business climate of a country to investors. Malaysia performs fairly on a number of rating scales of supply chain and potential chokepoints as summarised by the World Economic Forum’s Global Enabling Trade Report-Enabling Trade Index (ETI) in 2012, World Bank’s Connecting to Compete Report 2012-Logistic Performance Index (LPI) and Doing Business 2012 (DB). Malaysia is the top 20% in ETI and LPI, and top 6% in DB (Table 1).

Enhancing Supply Chain Connectivity and Competitiveness of Malaysian Agriculture Products: Identifying Chokepoints and Opportunities for Improvement

2

Table 1 Malaysia’s Position in the World Ranking, 2012

Report Description Malaysia’s rank

Enabling Trade Index (ETI)

Measures the factors, policies and services facilitating the free flow of goods over national borders, and to and from destination.

24th/124

Logistic Performance Index (LPI)

Measure logistics environment: efficiency of the customs clearance process; quality of trade and transport-related infrastructure; ease of arranging competitively priced shipments; competence and quality of logistics services; ability to track and trace consignments; frequency with which shipments reach the consignee within the scheduled or expected time.

29th/155

Doing Business 2012

Doing business evaluation: starting a business, dealing with construction permits, getting electricity, registering property, getting credit, protecting investors, paying taxes, trading across borders, enforcing contracts and resolving insolvency.

12th/185

Source: World Economic Forum’s Global Enabling Trade Report, 2010 and 2012. World Bank’s Connecting to Compete Report 2012

The ETI measures the factors, policies and services facilitating the free flow of goods over national borders, and to and from destination which covers 124 economies. The index consist four main pillars namely market access, border administration, transport and telecommunications infrastructure and business environment. Overall index reveals that Malaysia has improved from 30th place in 2010 to 24th place in 2012. In 2012, Malaysia was ranked at 25th place in terms of access to foreign market compared to previous achievement of 41st. Malaysia’s transport infrastructure is of high quality (12th) and the associated services are well developed (10th). Malaysian border clearance procedures are the least costly in the world and businesses assess them as fairly hassle-free, although many documents are necessary. In terms of quality of business environment, Malaysia has improved the quality of regulatory environment (35th to 22nd) as well as security environment (79th to 46th). LPI summarizes the performance of countries in terms of logistics; such as efficiency of the customs clearance process; quality of trade and transport-related infrastructure; ease of arranging competitively priced shipments; competence and quality of logistics services; ability to track and trace consignments; frequency with which shipments reach the consignee within the scheduled or expected time. LPI covers 155 countries with aims to identify the challenges and opportunity in trade logistic performance and rate them on a scale of 1 (worst) to 5 (best).Overall, Malaysian performance has dropped from 27th place in 2007 to 29th place in 2012. The Doing Business report published annually by the World Bank covers 183 economies in the world. The report ranks economies on the basis of ten areas namely starting a business, dealing with construction permits, getting electricity, registering property, getting credit, protecting investors, paying taxes, trading across borders, enforcing contracts and resolving insolvency (formerly closing a business). Malaysia has improved the ease of doing business from rank 25th in 2007 to rank 12th in 2013. This report focused on trading across borders. For the import of goods, the procedures measures range from the vessel’s arrival at the port of entry to the shipment’s delivery at the importer’s warehouse, while for the export of goods, the procedures measures range from the packing of the goods at the factory to their departure from the port of exit.

Enhancing Supply Chain Connectivity and Competitiveness of Malaysian Agriculture Products: Identifying Chokepoints and Opportunities for Improvement

3

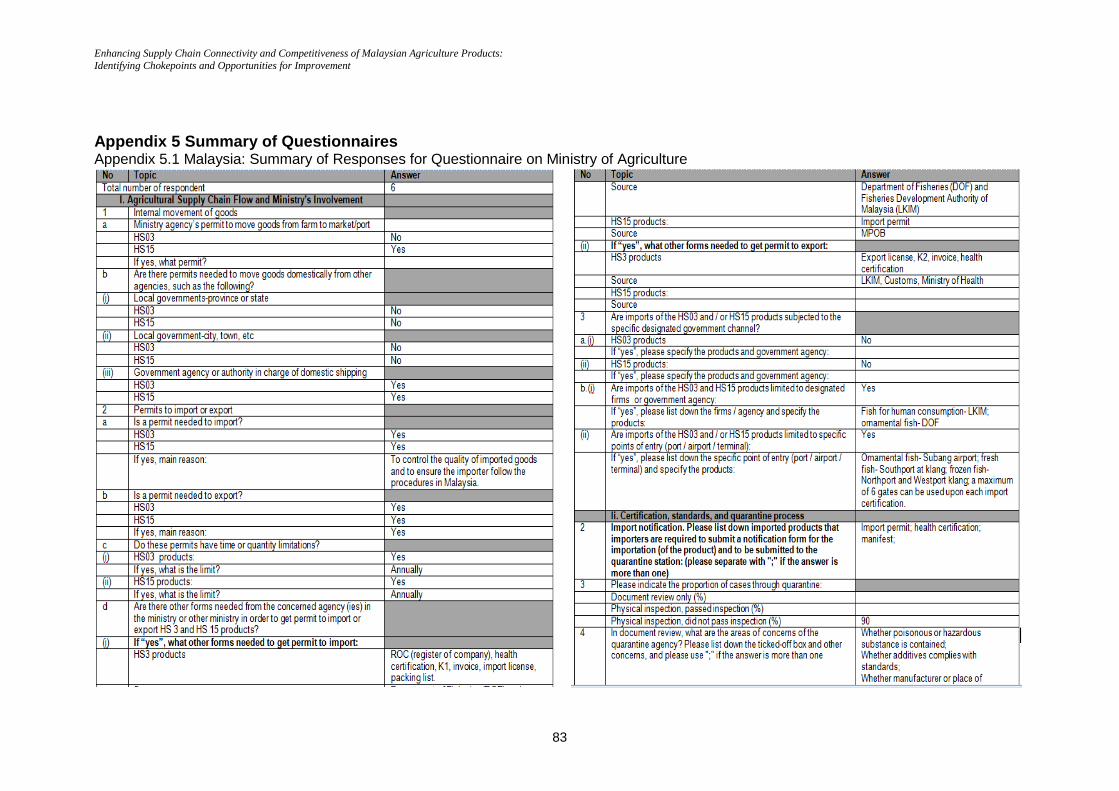

The above ratings cover mainly industrial products in Malaysia and serve as a benchmark for the country. Thus far, a similar ranking and rating on agricultural produce are limited. In view of the growing importance of agriculture and food commodities in the ASEAN trade, there is a need to examine the trade performance of this sector to gauge its competitiveness and efficiency. While “competitiveness” measurement involves a gamut of indicators, this report chooses to scrutinise the performance of the supply chain before further inference is made on the said concept. A good investigation of the supply chain is a broad measure to indicate competitiveness of the chosen sector. The two most important commodities traded within the ASEAN are palm oil and fish, which accounted for more than one fifth of intra-ASEAN agricultural trade (WITS database, 2011). Being agricultural products, these two commodities suffer a number of setbacks and experience “chokepoints” which impair their trade performance. Hence, this study attempts to examine the relative importance “chokepoints” in the supply chain of these two commodities in Malaysia. The study utilised both the primary and secondary data to examine the “chokepoints” in the supply chain system. The primary data is collected through a Key Informant Survey method using pre-designed questionnaires prepared by ERIA as shown on http://wbc.upm.edu.my/eria/ There are eight set of questionnaires (Q1-Q8) covering relevant ministry, custom and inspection at land border crossing and port, logistics provider, shipping services, road transport services,importers and exporters. An in-depth interview was carried out on relevant stakeholders which include government agencies (such as Malaysian Palm Oil Board (MPOB), Ministry of Agriculture and Agro-based Industries (MoA), Fisheries Development Authority of Malaysia (LKIM), Department of Fisheries Malaysia (DoF) and Malaysian Royal Customs Department), port authorities, transporters and traders. The survey was carried out during the months of February to May 2013. The study has adopted the mixed mode survey in that it involved a face-to-face interview with selected stakeholders as well as on-line survey and group discussion. An online questionnaire was also implemented to allow busy participants to fill up at their convenience. A total of 111 questionnaires have been distributed to various agencies and stakeholders. However, only 87 responded and out of this total only 52 questionnaires are useable for analysis because of some of the respondents come from the same department hence they provide more or less similar answers. A case study approach is used in analysing the data which are largely qualititative in nature and the sampling method is not probabilistic where meaningful statistical inference cannot be made. The study focuses on the findings that are considered insightful in contributing the chokepoints in the system1. The list and number of questionnaires analysed and face to face, group discussion and in-depth initerview carried out are presented in Appendix 1. This report presents the findings of Malaysian supply chain for two selected agriculture commodity groups namely animal/vegetable fats and oils (HS15) and fish and crustaceans molluscs, and other aquatic invertebrates (HS03). The reports provides the description of the two commodity and its supply chain processes, relative importance of chokepoints in the supply chain and a brief overview of policy, regulatory and institutional issues affecting major internal choke points and policy reccomendations. The report is organized as follows. Section 2 provides a brief institutional background and the economic roles of the two commodities. This is followed by a brief description 1 The rest of the data such as descriptive data and attitudinal scales are being used by ERIA for the preparation of the ASEAN report on a similar subject matter.

Enhancing Supply Chain Connectivity and Competitiveness of Malaysian Agriculture Products: Identifying Chokepoints and Opportunities for Improvement

4

of the products traded and their supply chain. Section 3 focuses on the chokepoints in the system and Section 4 provides the policy, regulatory and institutional issues. Section 5 concludes the study and provides some recommendations towards enhancing the supply chain and connectivity for both palm oil and fish commodities. List of samples, project activities, meetings and discussion, contacts, acts and regulations and summary of questionnaires are provided in the Appendices.

Enhancing Supply Chain Connectivity and Competitiveness of Malaysian Agriculture Products: Identifying Chokepoints and Opportunities for Improvement

5

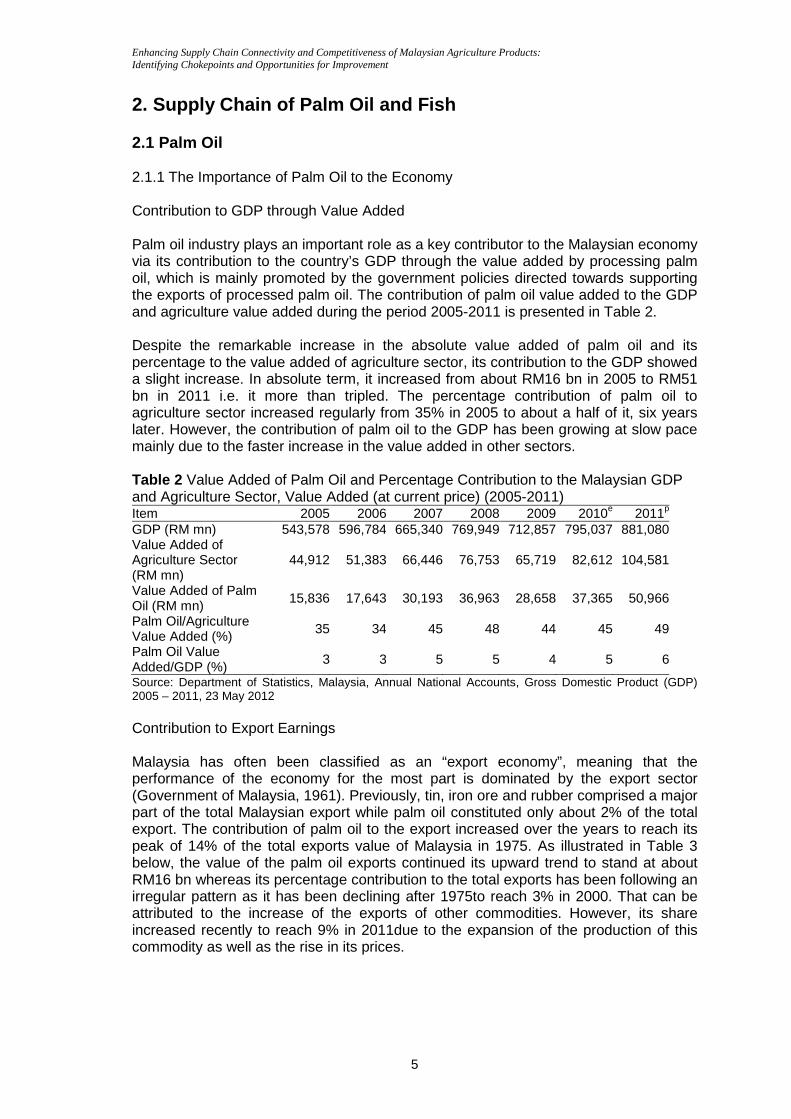

2. Supply Chain of Palm Oil and Fish 2.1 Palm Oil 2.1.1 The Importance of Palm Oil to the Economy Contribution to GDP through Value Added Palm oil industry plays an important role as a key contributor to the Malaysian economy via its contribution to the country’s GDP through the value added by processing palm oil, which is mainly promoted by the government policies directed towards supporting the exports of processed palm oil. The contribution of palm oil value added to the GDP and agriculture value added during the period 2005-2011 is presented in Table 2. Despite the remarkable increase in the absolute value added of palm oil and its percentage to the value added of agriculture sector, its contribution to the GDP showed a slight increase. In absolute term, it increased from about RM16 bn in 2005 to RM51 bn in 2011 i.e. it more than tripled. The percentage contribution of palm oil to agriculture sector increased regularly from 35% in 2005 to about a half of it, six years later. However, the contribution of palm oil to the GDP has been growing at slow pace mainly due to the faster increase in the value added in other sectors. Table 2 Value Added of Palm Oil and Percentage Contribution to the Malaysian GDP and Agriculture Sector, Value Added (at current price) (2005-2011) Item 2005 2006 2007 2008 2009 2010e 2011p

GDP (RM mn) 543,578 596,784 665,340 769,949 712,857 795,037 881,080Value Added of Agriculture Sector (RM mn)

44,912 51,383 66,446 76,753 65,719 82,612 104,581

Value Added of Palm Oil (RM mn)

15,836 17,643 30,193 36,963 28,658 37,365 50,966

Palm Oil/Agriculture Value Added (%) 35 34 45 48 44 45 49

Palm Oil Value Added/GDP (%)

3 3 5 5 4 5 6

Source: Department of Statistics, Malaysia, Annual National Accounts, Gross Domestic Product (GDP) 2005 – 2011, 23 May 2012 Contribution to Export Earnings Malaysia has often been classified as an “export economy”, meaning that the performance of the economy for the most part is dominated by the export sector (Government of Malaysia, 1961). Previously, tin, iron ore and rubber comprised a major part of the total Malaysian export while palm oil constituted only about 2% of the total export. The contribution of palm oil to the export increased over the years to reach its peak of 14% of the total exports value of Malaysia in 1975. As illustrated in Table 3 below, the value of the palm oil exports continued its upward trend to stand at about RM16 bn whereas its percentage contribution to the total exports has been following an irregular pattern as it has been declining after 1975to reach 3% in 2000. That can be attributed to the increase of the exports of other commodities. However, its share increased recently to reach 9% in 2011due to the expansion of the production of this commodity as well as the rise in its prices.

Enhancing Supply Chain Connectivity and Competitiveness of Malaysian Agriculture Products: Identifying Chokepoints and Opportunities for Improvement

6

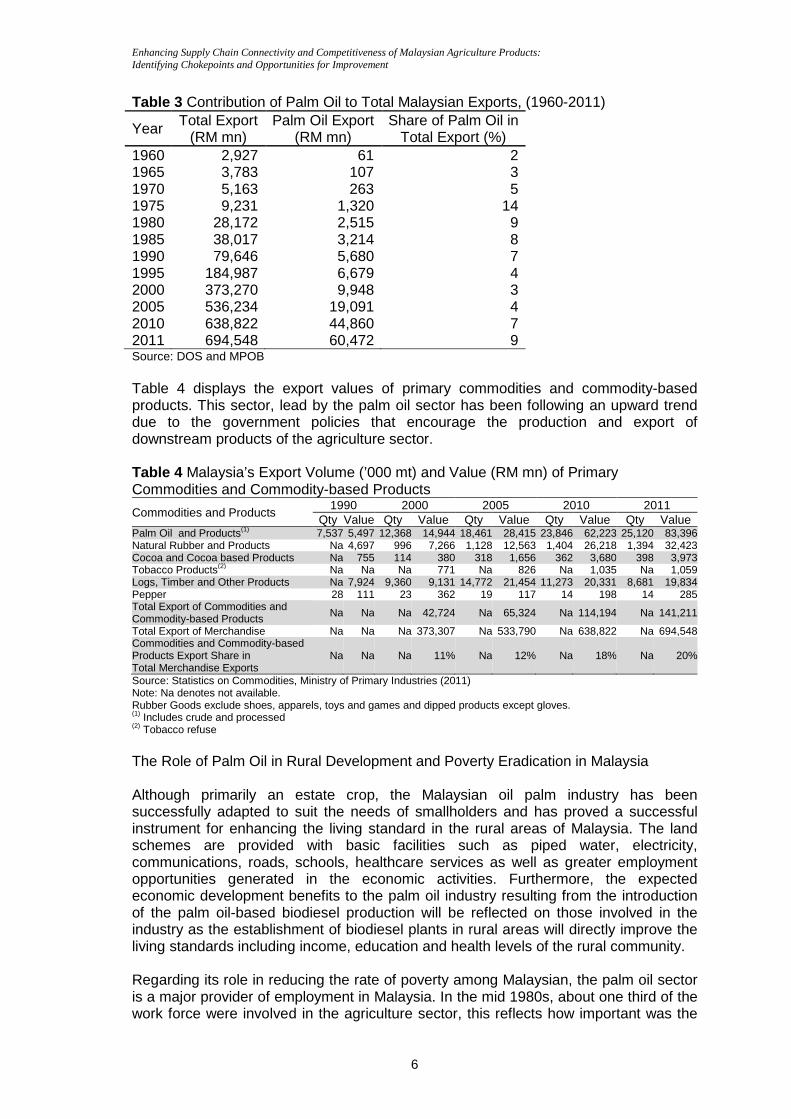

Table 3 Contribution of Palm Oil to Total Malaysian Exports, (1960-2011)

Year Total Export (RM mn)

Palm Oil Export (RM mn)

Share of Palm Oil in Total Export (%)

1960 2,927 61 2 1965 3,783 107 3 1970 5,163 263 5 1975 9,231 1,320 14 1980 28,172 2,515 9 1985 38,017 3,214 8 1990 79,646 5,680 7 1995 184,987 6,679 4 2000 373,270 9,948 3 2005 536,234 19,091 4 2010 638,822 44,860 7 2011 694,548 60,472 9 Source: DOS and MPOB Table 4 displays the export values of primary commodities and commodity-based products. This sector, lead by the palm oil sector has been following an upward trend due to the government policies that encourage the production and export of downstream products of the agriculture sector. Table 4 Malaysia’s Export Volume (’000 mt) and Value (RM mn) of Primary Commodities and Commodity-based Products

Commodities and Products 1990 2000 2005 2010 2011

Qty Value Qty Value Qty Value Qty Value Qty Value Palm Oil and Products(1) 7,537 5,497 12,368 14,944 18,461 28,415 23,846 62,223 25,120 83,396Natural Rubber and Products Na 4,697 996 7,266 1,128 12,563 1,404 26,218 1,394 32,423Cocoa and Cocoa based Products Na 755 114 380 318 1,656 362 3,680 398 3,973Tobacco Products(2) Na Na Na 771 Na 826 Na 1,035 Na 1,059Logs, Timber and Other Products Na 7,924 9,360 9,131 14,772 21,454 11,273 20,331 8,681 19,834Pepper 28 111 23 362 19 117 14 198 14 285Total Export of Commodities and Commodity-based Products Na Na Na 42,724 Na 65,324 Na 114,194 Na 141,211

Total Export of Merchandise Na Na Na 373,307 Na 533,790 Na 638,822 Na 694,548Commodities and Commodity-based Products Export Share in Total Merchandise Exports

Na Na Na 11% Na 12% Na 18% Na 20%

Source: Statistics on Commodities, Ministry of Primary Industries (2011) Note: Na denotes not available. Rubber Goods exclude shoes, apparels, toys and games and dipped products except gloves. (1) Includes crude and processed (2) Tobacco refuse

The Role of Palm Oil in Rural Development and Poverty Eradication in Malaysia Although primarily an estate crop, the Malaysian oil palm industry has been successfully adapted to suit the needs of smallholders and has proved a successful instrument for enhancing the living standard in the rural areas of Malaysia. The land schemes are provided with basic facilities such as piped water, electricity, communications, roads, schools, healthcare services as well as greater employment opportunities generated in the economic activities. Furthermore, the expected economic development benefits to the palm oil industry resulting from the introduction of the palm oil-based biodiesel production will be reflected on those involved in the industry as the establishment of biodiesel plants in rural areas will directly improve the living standards including income, education and health levels of the rural community. Regarding its role in reducing the rate of poverty among Malaysian, the palm oil sector is a major provider of employment in Malaysia. In the mid 1980s, about one third of the work force were involved in the agriculture sector, this reflects how important was the

Enhancing Supply Chain Connectivity and Competitiveness of Malaysian Agriculture Products: Identifying Chokepoints and Opportunities for Improvement

7

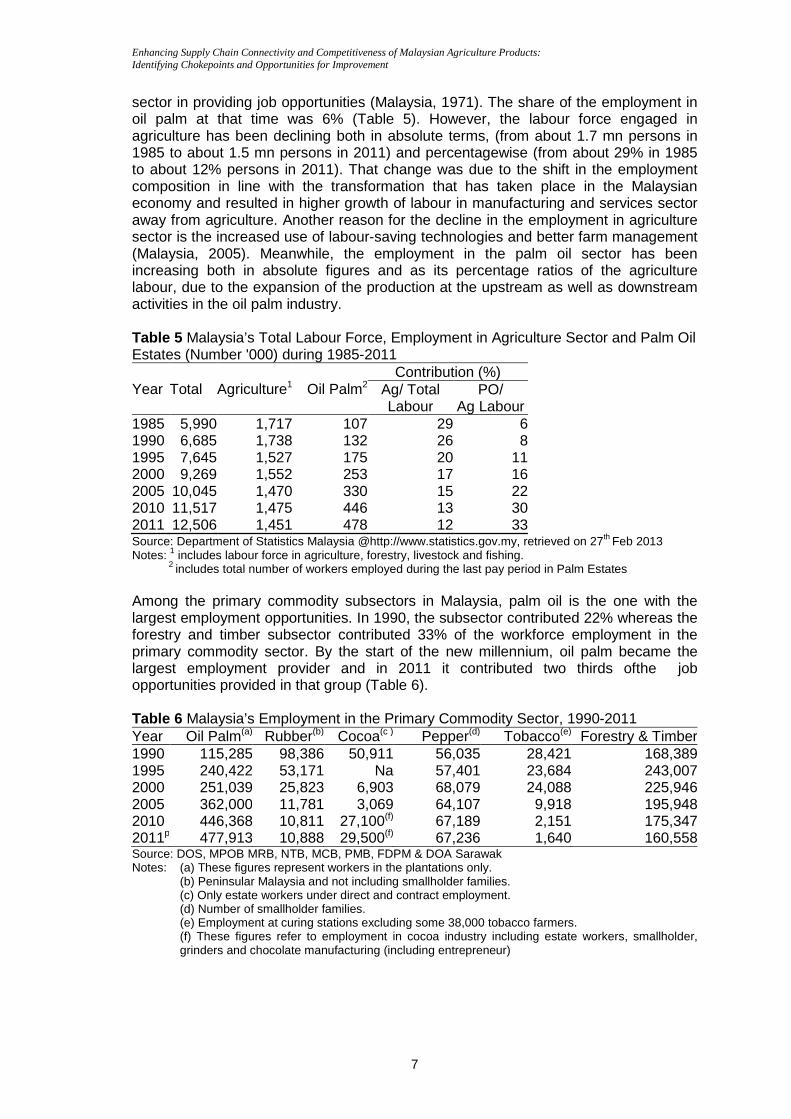

sector in providing job opportunities (Malaysia, 1971). The share of the employment in oil palm at that time was 6% (Table 5). However, the labour force engaged in agriculture has been declining both in absolute terms, (from about 1.7 mn persons in 1985 to about 1.5 mn persons in 2011) and percentagewise (from about 29% in 1985 to about 12% persons in 2011). That change was due to the shift in the employment composition in line with the transformation that has taken place in the Malaysian economy and resulted in higher growth of labour in manufacturing and services sector away from agriculture. Another reason for the decline in the employment in agriculture sector is the increased use of labour-saving technologies and better farm management (Malaysia, 2005). Meanwhile, the employment in the palm oil sector has been increasing both in absolute figures and as its percentage ratios of the agriculture labour, due to the expansion of the production at the upstream as well as downstream activities in the oil palm industry. Table 5 Malaysia’s Total Labour Force, Employment in Agriculture Sector and Palm Oil Estates (Number '000) during 1985-2011

Year Total Agriculture1 Oil Palm2 Contribution (%)

Ag/ Total Labour

PO/ Ag Labour

1985 5,990 1,717 107 29 61990 6,685 1,738 132 26 81995 7,645 1,527 175 20 112000 9,269 1,552 253 17 162005 10,045 1,470 330 15 222010 11,517 1,475 446 13 302011 12,506 1,451 478 12 33Source: Department of Statistics Malaysia @http://www.statistics.gov.my, retrieved on 27th Feb 2013 Notes: 1 includes labour force in agriculture, forestry, livestock and fishing. 2 includes total number of workers employed during the last pay period in Palm Estates Among the primary commodity subsectors in Malaysia, palm oil is the one with the largest employment opportunities. In 1990, the subsector contributed 22% whereas the forestry and timber subsector contributed 33% of the workforce employment in the primary commodity sector. By the start of the new millennium, oil palm became the largest employment provider and in 2011 it contributed two thirds ofthe job opportunities provided in that group (Table 6). Table 6 Malaysia’s Employment in the Primary Commodity Sector, 1990-2011 Year Oil Palm(a) Rubber(b) Cocoa(c ) Pepper(d) Tobacco(e) Forestry & Timber1990 115,285 98,386 50,911 56,035 28,421 168,3891995 240,422 53,171 Na 57,401 23,684 243,0072000 251,039 25,823 6,903 68,079 24,088 225,9462005 362,000 11,781 3,069 64,107 9,918 195,9482010 446,368 10,811 27,100(f) 67,189 2,151 175,3472011p 477,913 10,888 29,500(f) 67,236 1,640 160,558Source: DOS, MPOB MRB, NTB, MCB, PMB, FDPM & DOA Sarawak Notes: (a) These figures represent workers in the plantations only. (b) Peninsular Malaysia and not including smallholder families. (c) Only estate workers under direct and contract employment. (d) Number of smallholder families. (e) Employment at curing stations excluding some 38,000 tobacco farmers.

(f) These figures refer to employment in cocoa industry including estate workers, smallholder, grinders and chocolate manufacturing (including entrepreneur)

Enhancing Supply Chain Connectivity and Competitiveness of Malaysian Agriculture Products: Identifying Chokepoints and Opportunities for Improvement

8

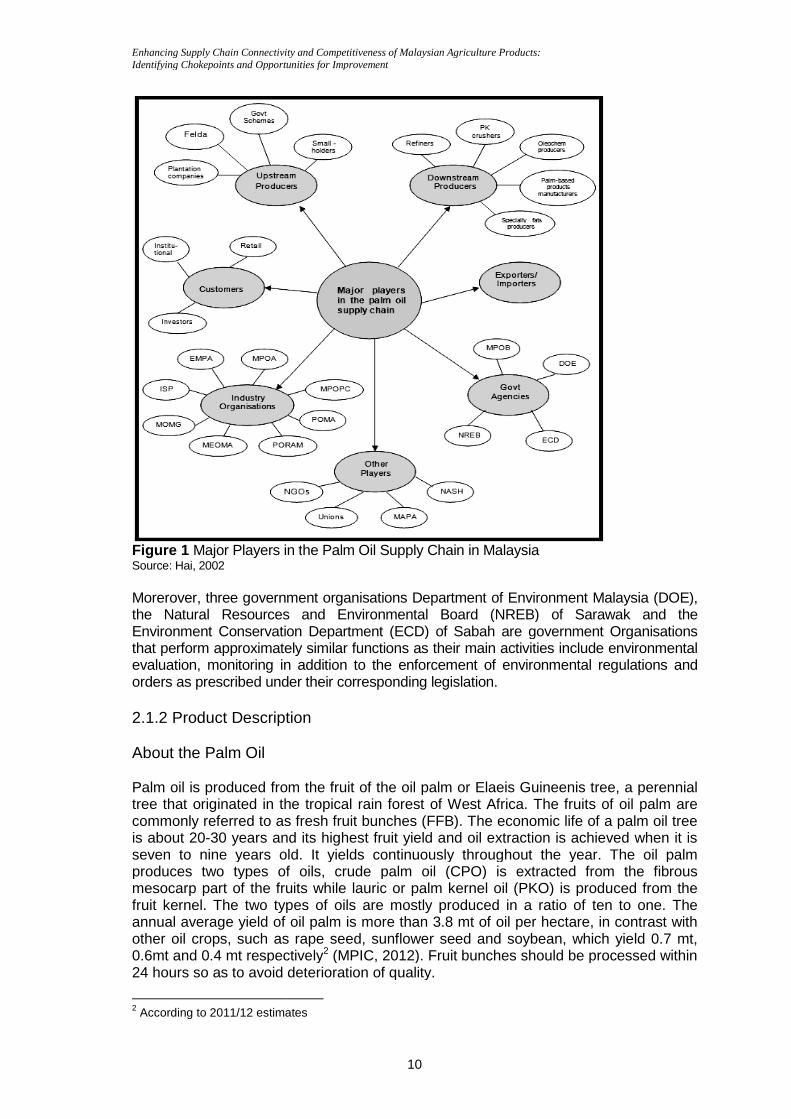

Major Players in the Industry The major players in the industry comprise upstream and downstream producers, exporters and importers, customers, Government agencies and non-governmental organisations (NGOs). The largest upstream player is the Federal Land Development Authority (FELDA). Plantation companies vary considerably in size, from a few hundred hectares to more than 100,000 hectares. The five largest companies in terms of planted area are Kumpulan Guthrie Berhad, Golden Hope Plantations Berhad, IOI Corporation Berhad and Sime Darby Berhad. Many current plantation companies have their beginnings in the colonial era at the turn of the 20th century when English and other European entrepreneurs transformed forest land into tea and coffee and rubber estates. Amongst the ‘old’ companies are Kumpulan Guthrie Berhad, Golden Hope Plantations Berhad, Sime Darby Berhad, Kuala Lumpur Kepong Berhad and United Plantations Berhad. Since the 1970s, several ‘home grown’ companies have entered the industry, the most notable example being IOI Corporation Berhad which started form zero base in 1983 to become one of the largest plantation companies today. The equity of plantation companies in the country is largely under Malaysian ownership, the largest investors being the national equity corporation, Permodalan Nasional Berhad (PNB) and the Employees Provident Fund (EPF). PNB has substantial holdings in seven major plantation companies while EPF which provide retirement benefits for its members has made substantial investments in more than 14 plantation companies listed on the Kuala Lumpur Stock Exchange. Only a few companies have substantial or controlling foreign shareholding, notable examples being United Plantations Berhad and Pamol Plantatins Sdn Bhd which is Unilever’s plantation interest in Malaysia. However, the latter had recently announced to dispose all its plantations in the Malaysia. In addition to producing crude palm oil, many companies are also engaged in downstream production activities along the supply chain, such as palm oil refining, production of edible oil and palm-based products and manufacture of basic oleochemicals. The larger companies have also expanded their downstream operations offshore by establishing palm oil refineries in consuming countries such as India, Bangladesh, Pakistan, China and Egypt. Recently, two plantation companies established their presence in edible oils in Europe; Golden Hope Plantations Berhad acquired Unlilever’s Unimills BV which is second largest processor of edible oils in Europe while IOI Corporation Berhad took control of Loders Croklaan BV, a global producer and supplier of specialty oils and fats. Moving in the opposite direction, several companies have ventured into establishment of oil palm plantations off-shore, particularly in Indonesia to take advantage of the availability of land and workers and lower cost of production. The biggest player in this context is Kumpulan Guthrie Berhad which acquired about 200,000 hectares in Minamas Plantations in 2001. The major players also include a number of industry organisations standing for the different interests of upstream and downstream producers of palm oil and palm-based products and their derivatives. The most important organisations are the Malaysian Palm Oil Association (MPOA), the Malaysian Palm Oil Board (MPOB) and the Malaysian Palm Oil Promotional Council (MPOPC). MPOA is the government supported organization that replaced three large plantation sector organisations, namely the Rubber Growers Association (RGA), the United Planting Association of Malaysia (UPAM) and the Malaysian Oil Palm Growers Council (MOPGC). Its mission is to guarantee the long term profitability and development of the Malaysian palm oil industry. It has been entrusted with the task of balancing the

Enhancing Supply Chain Connectivity and Competitiveness of Malaysian Agriculture Products: Identifying Chokepoints and Opportunities for Improvement

9

requirements and interests of the various sectors for synergy and development of the plantation industry as a whole. Its membership is open for any individual or company that owns or manages plantation in Malaysian with minimum 40 hectares or above (MPOA, 2013). The Malaysian Palm Oil Board (MPOB) is the main government agency entrusted with looking after the wellbeing of the overall performance the country's oil palm industry. Its main role is to promote and develop national objectives, policies and priorities for the interests of the Malaysian oil palm industry. The recent rapid expansion in the industry and changing global oils and fats market called for amendment in the regulations of MPOB to keep in pace with world market needs to controll the quality of palm oil products. Role and responsibilities of serving the country's palm oil industry. It has been established on 1st May 2000, to take over the functions of the former Palm Oil Research and Development Board (PORDB), Palm Oil Research Institute of Malaysia (PORIM) and the Palm Oil Registration and Licensing Authority (PORLA) (MPOB, 2004, 2013). It is financed mainly from cess imposed on the industry for palm oil and palm kernel oil produce. Besides, it obtains allocations from the government to support development projects and for approved research projects under the Intensification of Research in Priority Areas (IRPA) programme. The main functions of MPOB are: inter alia, to implement policies and development programmes, regulate, register, co-ordinate and promote all activities toward assuring the viability of the oil palm industry of Malaysia. Another function is to carry out and upgrade research and development activities and commercialise research result s as well as provide technical, advisory and consultancy services to the industry. It acts as a centre for the oil palm industry resource and information, including the publication and dissemination of information on oil palm as well as other oils and fats. The Malaysian Palm Oil Promotion Council (MPOPC), established by the industry in 1990 to undertake promotional programmes and to create market opportunities for Malaysian palm oil in the world market (Panapanaan et al., 2009). Its activities are focused on marketing communications, technical marketing and market promotion locally and in several edible oil consuming countries. MPOPC’s operations are supported by contributions from the industry, based on volume of palm oil production, to the Palm Oil Promotion Fund.

Enhancing Supply Chain Connectivity and Competitiveness of Malaysian Agriculture Products: Identifying Chokepoints and Opportunities for Improvement

Figure 1 Major Players in tSource: Hai, 2002 Morerover, three government organisations the Natural Resources and Environmental Board (NREB) of Sarawak and the Environment Conservation Department (ECD) of Sabahthat perform approximately similar functions as their main activities inevaluation, monitoring in orders as prescribed under their corresponding legislation. 2.1.2 Product Description About the Palm Oil Palm oil is produced from the fruit of the oil palm or tree that originated in the tropical rain forest of West Africa. The fruits of oil palm are commonly referred to as fresh fruit bunches (FFB). The economic life of a is about 20-30 years and its highest fruit yield and oil extraction is achieved when it is seven to nine years old. It yields continuously throughout the year. The oil palm produces two types of oils, crude palm oil (CPO) is extracted from thmesocarp part of the fruits while lauric or palm kernel oil (PKO) is produced from the fruit kernel. The two types of oils are mostly produced in a ratio of ten to one. The annual average yield of oil palm is more than 3.8 mt of oil per hectare, other oil crops, such as rape seed, sunflower seed and soybean, which yield 0.7 mt, 0.6mt and 0.4 mt respectively24 hours so as to avoid deterioration of quality.

2 According to 2011/12 estimates

Enhancing Supply Chain Connectivity and Competitiveness of Malaysian Agriculture Products: Identifying Chokepoints and Opportunities for Improvement

10

Players in the Palm Oil Supply Chain in Malaysia

government organisations Department of Environment Malaysia (DOE), the Natural Resources and Environmental Board (NREB) of Sarawak and the Environment Conservation Department (ECD) of Sabah are government Organisations that perform approximately similar functions as their main activities include environmental

in addition to the enforcement of environmental regulations and under their corresponding legislation.

Product Description

Palm oil is produced from the fruit of the oil palm or Elaeis Guineenistree that originated in the tropical rain forest of West Africa. The fruits of oil palm are commonly referred to as fresh fruit bunches (FFB). The economic life of a

30 years and its highest fruit yield and oil extraction is achieved when it is seven to nine years old. It yields continuously throughout the year. The oil palm produces two types of oils, crude palm oil (CPO) is extracted from thmesocarp part of the fruits while lauric or palm kernel oil (PKO) is produced from the fruit kernel. The two types of oils are mostly produced in a ratio of ten to one. The annual average yield of oil palm is more than 3.8 mt of oil per hectare, other oil crops, such as rape seed, sunflower seed and soybean, which yield 0.7 mt, 0.6mt and 0.4 mt respectively2 (MPIC, 2012). Fruit bunches should be processed within 24 hours so as to avoid deterioration of quality.

estimates

of Environment Malaysia (DOE), the Natural Resources and Environmental Board (NREB) of Sarawak and the

are government Organisations clude environmental

addition to the enforcement of environmental regulations and

Elaeis Guineenis tree, a perennial tree that originated in the tropical rain forest of West Africa. The fruits of oil palm are commonly referred to as fresh fruit bunches (FFB). The economic life of a palm oil tree

30 years and its highest fruit yield and oil extraction is achieved when it is seven to nine years old. It yields continuously throughout the year. The oil palm produces two types of oils, crude palm oil (CPO) is extracted from the fibrous mesocarp part of the fruits while lauric or palm kernel oil (PKO) is produced from the fruit kernel. The two types of oils are mostly produced in a ratio of ten to one. The annual average yield of oil palm is more than 3.8 mt of oil per hectare, in contrast with other oil crops, such as rape seed, sunflower seed and soybean, which yield 0.7 mt,

(MPIC, 2012). Fruit bunches should be processed within

Enhancing Supply Chain Connectivity and Competitiveness of Malaysian Agriculture Products: Identifying Chokepoints and Opportunities for Improvement

11

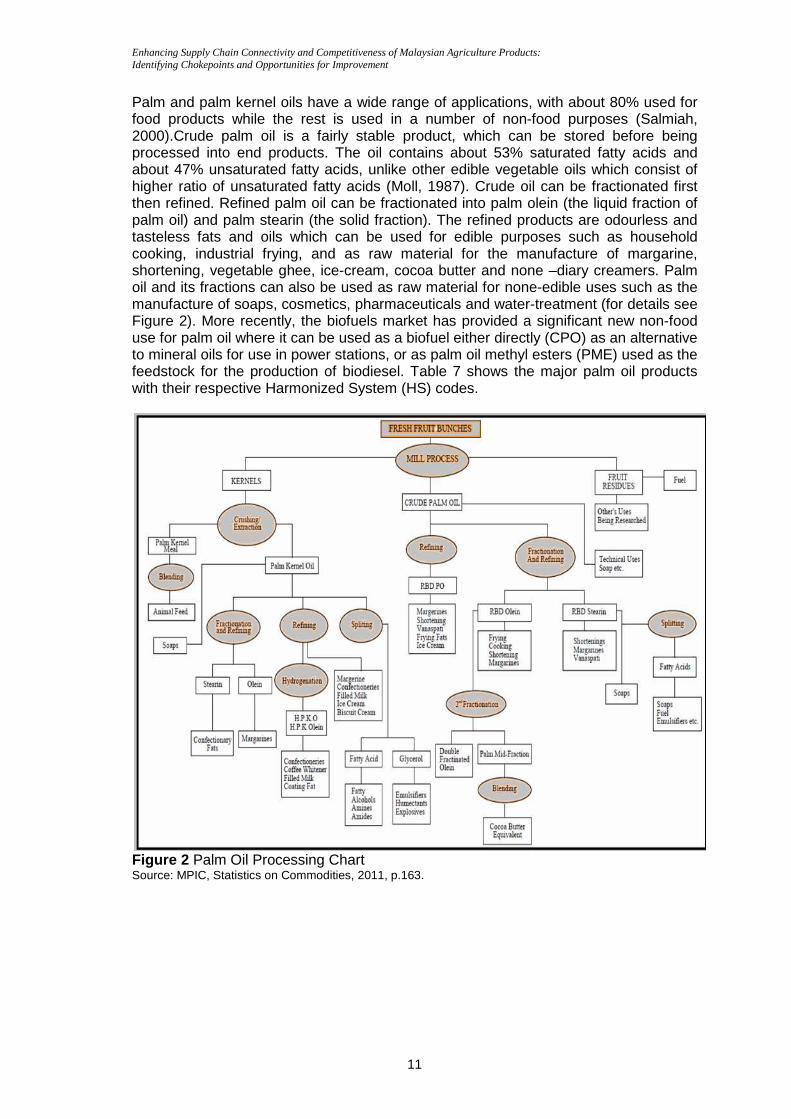

Palm and palm kernel oils have a wide range of applications, with about 80% used for food products while the rest is used in a number of non-food purposes (Salmiah, 2000).Crude palm oil is a fairly stable product, which can be stored before being processed into end products. The oil contains about 53% saturated fatty acids and about 47% unsaturated fatty acids, unlike other edible vegetable oils which consist of higher ratio of unsaturated fatty acids (Moll, 1987). Crude oil can be fractionated first then refined. Refined palm oil can be fractionated into palm olein (the liquid fraction of palm oil) and palm stearin (the solid fraction). The refined products are odourless and tasteless fats and oils which can be used for edible purposes such as household cooking, industrial frying, and as raw material for the manufacture of margarine, shortening, vegetable ghee, ice-cream, cocoa butter and none –diary creamers. Palm oil and its fractions can also be used as raw material for none-edible uses such as the manufacture of soaps, cosmetics, pharmaceuticals and water-treatment (for details see Figure 2). More recently, the biofuels market has provided a significant new non-food use for palm oil where it can be used as a biofuel either directly (CPO) as an alternative to mineral oils for use in power stations, or as palm oil methyl esters (PME) used as the feedstock for the production of biodiesel. Table 7 shows the major palm oil products with their respective Harmonized System (HS) codes.

Figure 2 Palm Oil Processing Chart Source: MPIC, Statistics on Commodities, 2011, p.163.

Enhancing Supply Chain Connectivity and Competitiveness of Malaysian Agriculture Products: Identifying Chokepoints and Opportunities for Improvement

12

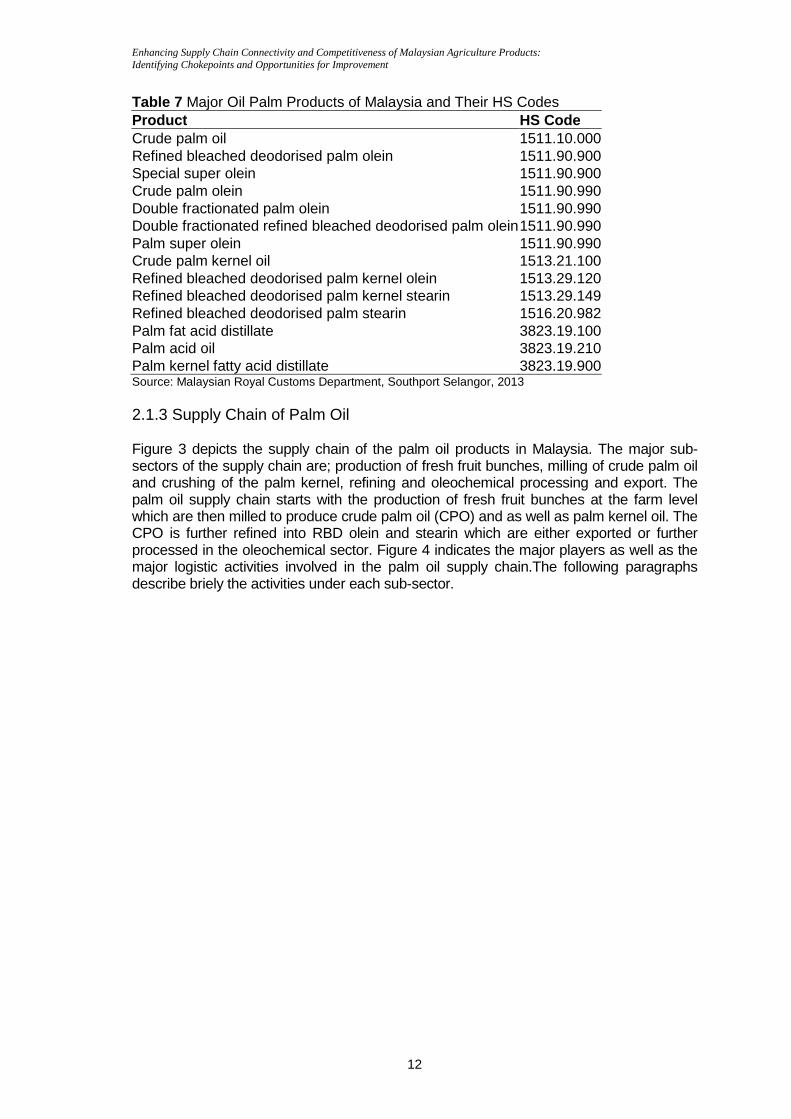

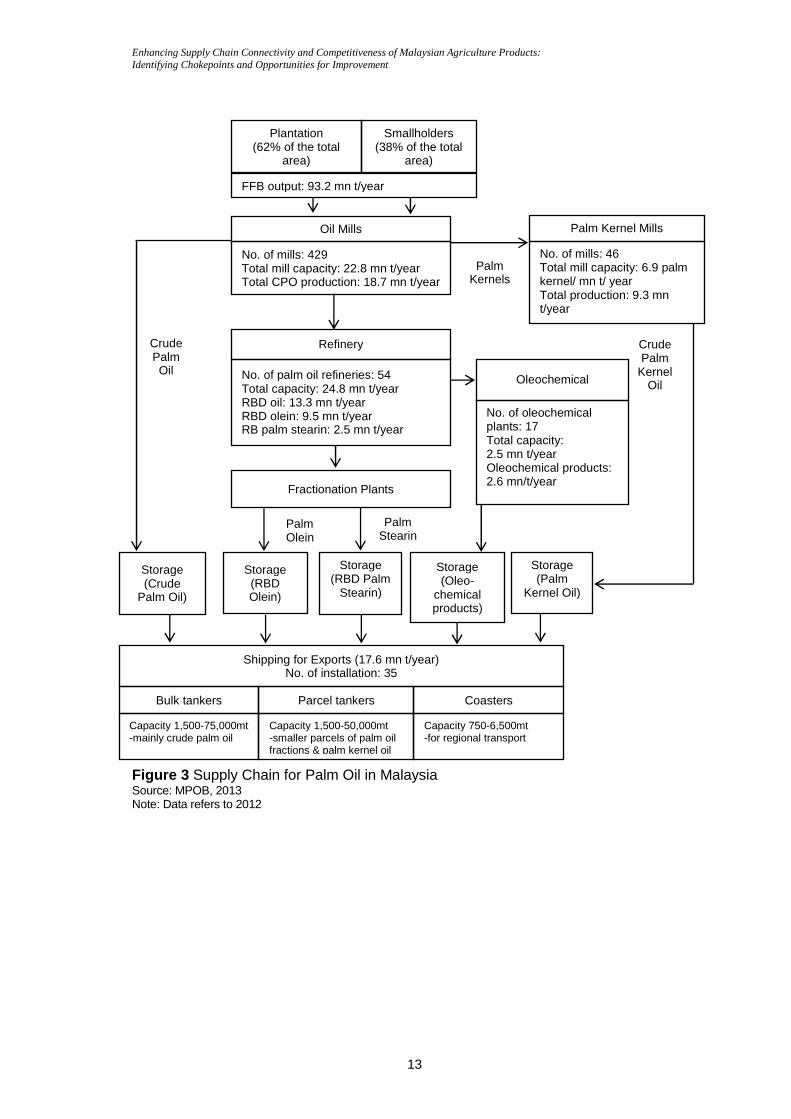

Table 7 Major Oil Palm Products of Malaysia and Their HS Codes Product HS Code Crude palm oil 1511.10.000 Refined bleached deodorised palm olein 1511.90.900 Special super olein 1511.90.900 Crude palm olein 1511.90.990 Double fractionated palm olein 1511.90.990 Double fractionated refined bleached deodorised palm olein 1511.90.990 Palm super olein 1511.90.990 Crude palm kernel oil 1513.21.100 Refined bleached deodorised palm kernel olein 1513.29.120 Refined bleached deodorised palm kernel stearin 1513.29.149 Refined bleached deodorised palm stearin 1516.20.982 Palm fat acid distillate 3823.19.100 Palm acid oil 3823.19.210 Palm kernel fatty acid distillate 3823.19.900 Source: Malaysian Royal Customs Department, Southport Selangor, 2013 2.1.3 Supply Chain of Palm Oil Figure 3 depicts the supply chain of the palm oil products in Malaysia. The major sub-sectors of the supply chain are; production of fresh fruit bunches, milling of crude palm oil and crushing of the palm kernel, refining and oleochemical processing and export. The palm oil supply chain starts with the production of fresh fruit bunches at the farm level which are then milled to produce crude palm oil (CPO) and as well as palm kernel oil. The CPO is further refined into RBD olein and stearin which are either exported or further processed in the oleochemical sector. Figure 4 indicates the major players as well as the major logistic activities involved in the palm oil supply chain.The following paragraphs describe briely the activities under each sub-sector.

Enhancing Supply Chain Connectivity and Competitiveness of Malaysian Agriculture Products: Identifying Chokepoints and Opportunities for Improvement

13

Figure 3 Supply Chain for Palm Oil in Malaysia Source: MPOB, 2013 Note: Data refers to 2012

Storage (Palm

Kernel Oil)

Storage (Oleo-

chemical products)

No. of oleochemical plants: 17 Total capacity: 2.5 mn t/year Oleochemical products: 2.6 mn/t/year

Refinery

Fractionation Plants

Storage (RBD Olein)

Storage (RBD Palm

Stearin)

Shipping for Exports (17.6 mn t/year) No. of installation: 35

Palm Kernels

No. of palm oil refineries: 54 Total capacity: 24.8 mn t/year RBD oil: 13.3 mn t/year RBD olein: 9.5 mn t/year RB palm stearin: 2.5 mn t/year

Palm Stearin

Palm Olein

Crude Palm

Kernel Oil Oleochemical

Storage (Crude

Palm Oil)

Bulk tankers Parcel tankers Coasters

Capacity 1,500-75,000mt -mainly crude palm oil

Capacity 1,500-50,000mt -smaller parcels of palm oil fractions & palm kernel oil

Capacity 750-6,500mt -for regional transport

Plantation (62% of the total

area)

Smallholders (38% of the total

area)

Oil Mills Palm Kernel Mills

No. of mills: 429 Total mill capacity: 22.8 mn t/year Total CPO production: 18.7 mn t/year

No. of mills: 46 Total mill capacity: 6.9 palm kernel/ mn t/ year Total production: 9.3 mn t/year

FFB output: 93.2 mn t/year

Crude Palm Oil

Enhancing Supply Chain Connectivity and Competitiveness of Malaysian Agriculture Products: Identifying Chokepoints and Opportunities for Improvement

14

Figure 4 Industry Players and Logistic Activities in the Supply Chain of Palm Oil in Malaysia Production of Fresh Fruit Bunches (FFB) The production of fruit bunches starts with the development of plantations for the production of (FFB). The development of new plantations would require the carrying out feasibility studies and an environment impact assessment (EIA) if the area to be developed is primary or secondary forest exceeding 500 hectares. An EIA is also required if the development involves changes in the types of agricultural use of land more than 500 hectares. The EIA study would help in identifying likely environmental and social effects and development of management plans to alleviate the unfavourable effects. The process for the approval is based on the approach adopted by the Natural Resources and Environment Board, Sarawak. As soon as the land is approved by the respective agencies for development to proceed nursery establishment commences, followed by site preparation which include land survey, clearing of existing vegetation, establishment of a road and field drainage system, soil conservation measures such as terracing, conservation bunds and silt pits and sowing of leguminous cover crops(Hai, 2002). A number of Good Agricultural Practices (GAPs) are adopted by the Malaysian oil palm industry. Zero burning had been introduced into the plantation and enforced since 1987 under the Environmental Quality Act (EQA) 1974 as part of the Oil Palm Good Agriculture Practice (OPGAP). Replanting, currently, includes chipping the old oil palm trunk and fronds and the residues are laid in the inter-rows as a biomass mulch to release nutrients for the newly replanted oil palm crop gradually. The OPGAP is excpected to pave way for sustainable production in the field. Similarly, oil palm GAP Integrated Pest Management (IPM) helps in reducing pesticide usage because the biological control through practices such as barn owl to control rat, and biopesticides like Metarhizzium fungi and virus to control Rhinocerous beetle grubs, Bt virus for control of bagworms, Trichoderma to control Ganoderma, etc, avoid use of chemicals. Furthermore, Codes of Practices (COPs) throughout the supply chain have been

Transportation

Forwarding Agents, Bulk Installation Operators, Surveyors and Chemists

Port/Installation

Transportation

Trade Producers, Processors,

Manufacturers

Refinery

Milling

Oleo-chemical Manufacturer

Importer

Exporter

Logistics Services Providers

Production

Enhancing Supply Chain Connectivity and Competitiveness of Malaysian Agriculture Products: Identifying Chokepoints and Opportunities for Improvement

15

launched by MPOB in August 2007. They include, inter alia, Good Practice for Nursery and Good Agricultural Practice for Oil Palm Estates & Smallholdings3 (MPOB, 2013d). The total area under palm oil was estimated at 5,076,929ha in 2012 in which the plantation sector accounted for 62% while the balance were the smallholders (MPOB, 2012). However, in terms of production, the share of the estates is relatively higher due to their higher productivity compared to smallholders. Palm Oil Milling Process (Production of CPO and PK) The palm oil milling process involves the physical extraction of palm products namely, crude palm oil and palm kernel from the FFB. After harvesting, it is important that the fresh fruit bunches (FFB) are processed as soon as possible to prevent a rapid rise in free fatty acids (FFA) which could adversely affect the quality of the crude palm oil (CPO). This immediate processing requires the mills to be located within the vicinity of the plantation area. Harvested FFB is loaded onto small 5-tonnes lorries to 25-tonnes open trailers to be transported to the mills. Some private mills do have their own tanker lorries, but the capacities of these lorries are rather small (Ibrahim 2008). After milling process the CPO then gets transported to the refineries for further processing and the PK to the crushers for the palm kernel oil to be extracted. In 2012, there were a total of 429 mills with a total capacity of 22.8 tonnes per year. This sub-sector produced about 18.7 mn tonnes of CPO in 2012. The total number of palm kernel mills stood at 46 with a total capacity of 6.9 mn tonnes per year. The total palm kernel product produced was estimated at 9.3 mn tonnes. Refining The purpose of the refining process is to produce an edible oil of uniform quality that meets industry’s standards and satisfies customer requirements. Specifically in respect of FFA, moisture and impurities, Iodine value, peroxide value, melting point, colour and flavour. Since processed palm oil is exported by the use of ship tankers, the refineries are usually located at the ports e.g. Cargill owns and operates three “state-of-the-art” refineries in Port Klang, Kuantan and West Port, and also a jointly owned refinery in Sarawak. Additionally they are building an additional oil refinery in the Port Klang Free Zone (Cargill, 2013). Other refiners include, inter alia, Kwantas Corp and Wilmar International. Wimar’s refinery is a joint venture with TSH Resources. These three refineries have a production capacity of 1.8 mn mt per annum. The refined oil must tasteless and have a plain flavour. This process removes free fatty acids, phosphatides, odouriferous matter, water as well as impurities such as dirt and traces of metals from the CPO by either physical or chemical refining to produce either refined, bleached and deodorised palm oil (RBDPO) or neutralised, bleached and deodorised palm oil (NBDPO). These are products subjected to fractionation to obtain the respective liquid olein fraction and the solid stearin fraction. Physical refining is the widespread method implemented by the refineries as it is simpler, less capital intensive, more efficient and produces a lower effluent load. Some companies e.g. Cargill beside owning a number of refineries, they are involved in manufacturing products ranging from palm oil-based bakery fats for use in baking and frying, value added bulk refined oils, packaged palm products as well as specialty fats

3 The other Codes of Practices are: Good Milling Practice for Palm Oil Mills; Good Crushing Practice for Palm Kernel Crushers; Good Refining Practice for Palm Oil Refineries; Good Practice for the Handling, Transport and Storage of Products from the Oil Palm and Good Practice for Bulking Installations.

Enhancing Supply Chain Connectivity and Competitiveness of Malaysian Agriculture Products: Identifying Chokepoints and Opportunities for Improvement

16

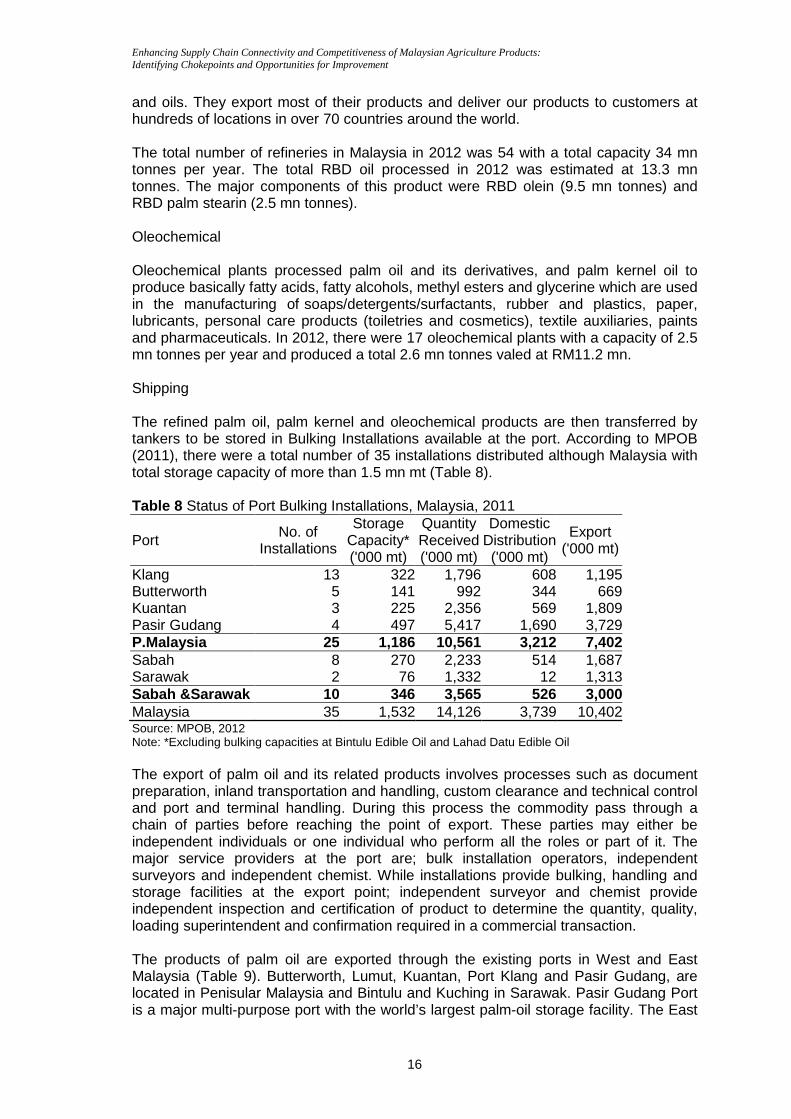

and oils. They export most of their products and deliver our products to customers at hundreds of locations in over 70 countries around the world. The total number of refineries in Malaysia in 2012 was 54 with a total capacity 34 mn tonnes per year. The total RBD oil processed in 2012 was estimated at 13.3 mn tonnes. The major components of this product were RBD olein (9.5 mn tonnes) and RBD palm stearin (2.5 mn tonnes). Oleochemical Oleochemical plants processed palm oil and its derivatives, and palm kernel oil to produce basically fatty acids, fatty alcohols, methyl esters and glycerine which are used in the manufacturing of soaps/detergents/surfactants, rubber and plastics, paper, lubricants, personal care products (toiletries and cosmetics), textile auxiliaries, paints and pharmaceuticals. In 2012, there were 17 oleochemical plants with a capacity of 2.5 mn tonnes per year and produced a total 2.6 mn tonnes valed at RM11.2 mn. Shipping The refined palm oil, palm kernel and oleochemical products are then transferred by tankers to be stored in Bulking Installations available at the port. According to MPOB (2011), there were a total number of 35 installations distributed although Malaysia with total storage capacity of more than 1.5 mn mt (Table 8). Table 8 Status of Port Bulking Installations, Malaysia, 2011

Port No. of Installations

Storage Capacity* ('000 mt)

Quantity Received ('000 mt)

Domestic Distribution ('000 mt)

Export ('000 mt)

Klang 13 322 1,796 608 1,195Butterworth 5 141 992 344 669Kuantan 3 225 2,356 569 1,809Pasir Gudang 4 497 5,417 1,690 3,729P.Malaysia 25 1,186 10,561 3,212 7,402Sabah 8 270 2,233 514 1,687Sarawak 2 76 1,332 12 1,313Sabah &Sarawak 10 346 3,565 526 3,000Malaysia 35 1,532 14,126 3,739 10,402Source: MPOB, 2012 Note: *Excluding bulking capacities at Bintulu Edible Oil and Lahad Datu Edible Oil The export of palm oil and its related products involves processes such as document preparation, inland transportation and handling, custom clearance and technical control and port and terminal handling. During this process the commodity pass through a chain of parties before reaching the point of export. These parties may either be independent individuals or one individual who perform all the roles or part of it. The major service providers at the port are; bulk installation operators, independent surveyors and independent chemist. While installations provide bulking, handling and storage facilities at the export point; independent surveyor and chemist provide independent inspection and certification of product to determine the quantity, quality, loading superintendent and confirmation required in a commercial transaction. The products of palm oil are exported through the existing ports in West and East Malaysia (Table 9). Butterworth, Lumut, Kuantan, Port Klang and Pasir Gudang, are located in Penisular Malaysia and Bintulu and Kuching in Sarawak. Pasir Gudang Port is a major multi-purpose port with the world’s largest palm-oil storage facility. The East

Enhancing Supply Chain Connectivity and Competitiveness of Malaysian Agriculture Products: Identifying Chokepoints and Opportunities for Improvement

17

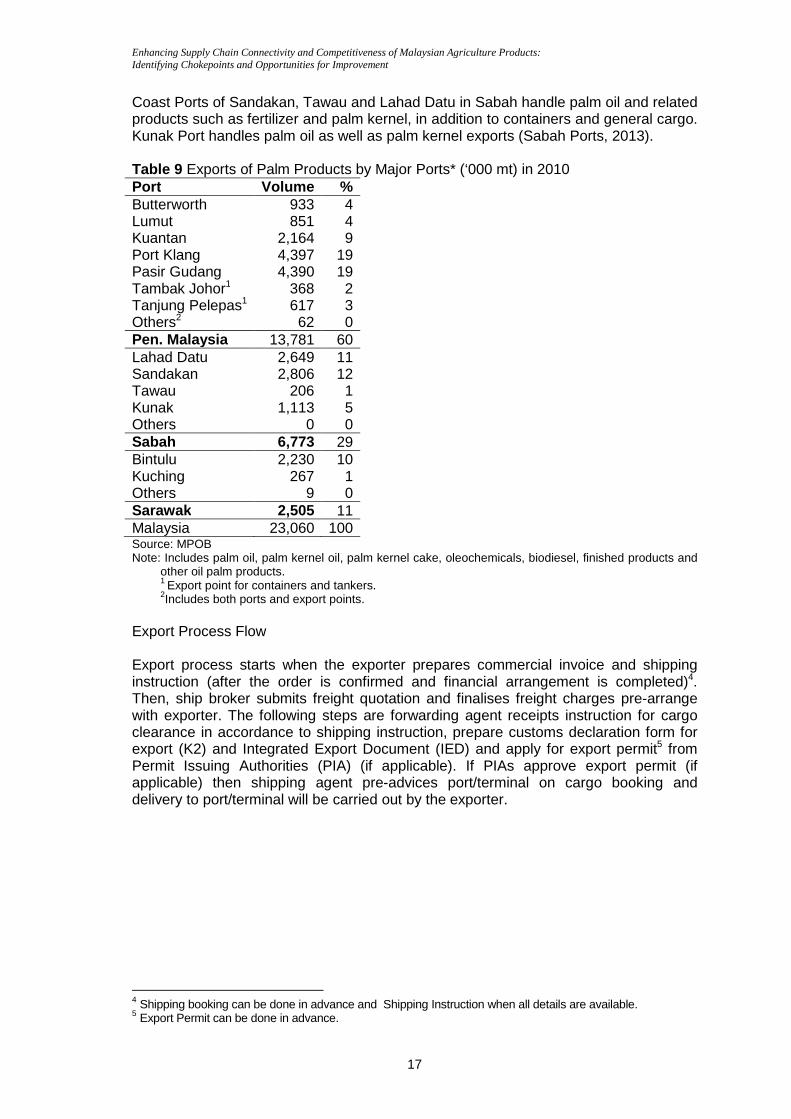

Coast Ports of Sandakan, Tawau and Lahad Datu in Sabah handle palm oil and related products such as fertilizer and palm kernel, in addition to containers and general cargo. Kunak Port handles palm oil as well as palm kernel exports (Sabah Ports, 2013). Table 9 Exports of Palm Products by Major Ports* (‘000 mt) in 2010 Port Volume % Butterworth 933 4 Lumut 851 4 Kuantan 2,164 9 Port Klang 4,397 19 Pasir Gudang 4,390 19 Tambak Johor1 368 2 Tanjung Pelepas1 617 3 Others2 62 0 Pen. Malaysia 13,781 60 Lahad Datu 2,649 11 Sandakan 2,806 12 Tawau 206 1 Kunak 1,113 5 Others 0 0 Sabah 6,773 29 Bintulu 2,230 10 Kuching 267 1 Others 9 0 Sarawak 2,505 11 Malaysia 23,060 100 Source: MPOB Note: Includes palm oil, palm kernel oil, palm kernel cake, oleochemicals, biodiesel, finished products and

other oil palm products. 1 Export point for containers and tankers. 2Includes both ports and export points.

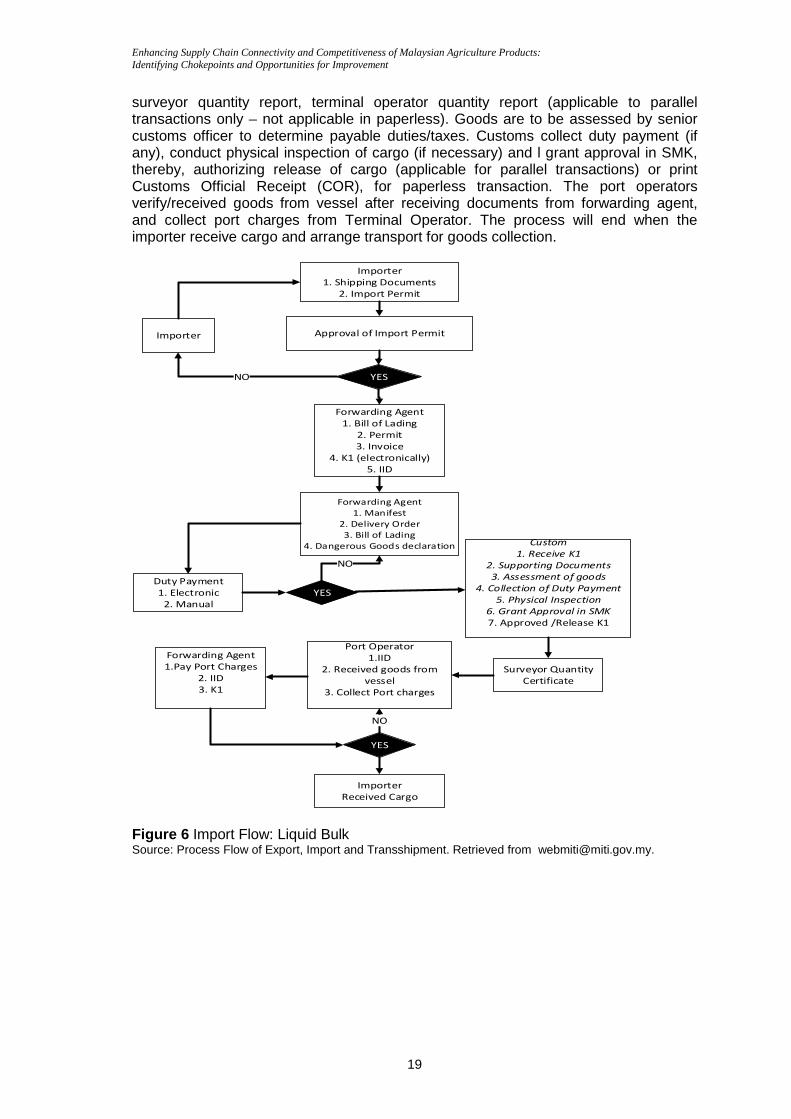

Export Process Flow Export process starts when the exporter prepares commercial invoice and shipping instruction (after the order is confirmed and financial arrangement is completed)4. Then, ship broker submits freight quotation and finalises freight charges pre-arrange with exporter. The following steps are forwarding agent receipts instruction for cargo clearance in accordance to shipping instruction, prepare customs declaration form for export (K2) and Integrated Export Document (IED) and apply for export permit5 from Permit Issuing Authorities (PIA) (if applicable). If PIAs approve export permit (if applicable) then shipping agent pre-advices port/terminal on cargo booking and delivery to port/terminal will be carried out by the exporter.

4 Shipping booking can be done in advance and Shipping Instruction when all details are available. 5 Export Permit can be done in advance.

Enhancing Supply Chain Connectivity and Competitiveness of Malaysian Agriculture Products: Identifying Chokepoints and Opportunities for Improvement

18

Export Flow: Liquid Bulk

Document

Preparation

Inland

Transportation

& Handling

Custom Clearance &

Tech Control

Port and

Terminal

Handling

Exporter

1. Invoice

2. Shipping Instruction

Forwarding Agent

Ship Broker

1. Letter of Offer

2. Contract of Freightment

Receive cargo instruction

1. K2

2. IED

3. Export Permit

Approved Export Permit by

PIA’s

YESNO

Note of Arrival

Deliver Cargo to Terminal

CUSTOMS

1. K2

2. Invoice

3. IED

4. Surveyor Quantity Report

YES Quantity Surveyor

Bill of Lading

E-Manifest

NO

Figure 5 Export Flow: Liquid Bulk Source: Process Flow of Export, Import and Transshipment. Retrieved from [email protected]. Import Flow The import flow is displayed on Figure 6. To start the import process, the importer prepares necessary documents, including shipping documents from banks (if applicable) and apply for import permit from PIAs (if applicable). When import permit is approved, importer instructs forwarding agent to clear cargo (together with supporting documents such as bill of lading, permit and invoice). The latter performs document preparation if instructed by the importer and submit K1, electronically (CUSDEC) through SMK-DNT interface, in addition to Integrated Import Document (IID). Forwarding agent applies Permit (if applicable). Shipping agent has to send manifest (Ocean Bill of Lading) to customs within 24 hours of arrival of vessel, in accordance with Section 52, Customs Act. Shipping agent has to release Delivery Order (DO) in return of Original Bill of Lading (BL) and submit DG Declaration (for dangerous goods if applicable). Forwarding Agent pays import duty on behalf of Importer. Customs computer system automatically processes and registers K1 and sends response back to forwarding agent with registration number. Customs receives Form K1 and supporting documents for customs clearance. These include basic supporting documents - Invoice and IID in addition to other supporting documents such as permit,

Enhancing Supply Chain Connectivity and Competitiveness of Malaysian Agriculture Products: Identifying Chokepoints and Opportunities for Improvement

19

surveyor quantity report, terminal operator quantity report (applicable to parallel transactions only – not applicable in paperless). Goods are to be assessed by senior customs officer to determine payable duties/taxes. Customs collect duty payment (if any), conduct physical inspection of cargo (if necessary) and l grant approval in SMK, thereby, authorizing release of cargo (applicable for parallel transactions) or print Customs Official Receipt (COR), for paperless transaction. The port operators verify/received goods from vessel after receiving documents from forwarding agent, and collect port charges from Terminal Operator. The process will end when the importer receive cargo and arrange transport for goods collection.

Importer

1. Shipping Documents

2. Import Permit

Approval of Import Permit

Forwarding Agent

1. Manifest

2. Delivery Order

3. Bill of Lading

4. Dangerous Goods declaration

YES

Duty Payment

1. Electronic

2. Manual

Custom

1. Receive K1

2. Supporting Documents

3. Assessment of goods

4. Collection of Duty Payment

5. Physical Inspection

6. Grant Approval in SMK

7. Approved /Release K1

Forwarding Agent

1.Pay Port Charges

2. IID

3. K1

YES

Importer

Received Cargo

Importer

YESNO

Forwarding Agent

1. Bill of Lading

2. Permit

3. Invoice

4. K1 (electronically)

5. IID

NO

Surveyor Quantity

Certificate

Port Operator

1.IID

2. Received goods from

vessel

3. Collect Port charges

NO