Embed Size (px)

Citation preview

Energy Outlook of Northeast Asiaand

Regional Energy Cooperation

June 9, 2006

Kensuke KanekiyoManaging Director

The Institute of Energy Economics, Japan

The Institute of Energy Economics, Japan 財団法人日本エネルギー経済研究所 Copyright IEEJ 2006

Seminar on EU Russia Energy RelationsAleksanteri Institute, University of Helsinki

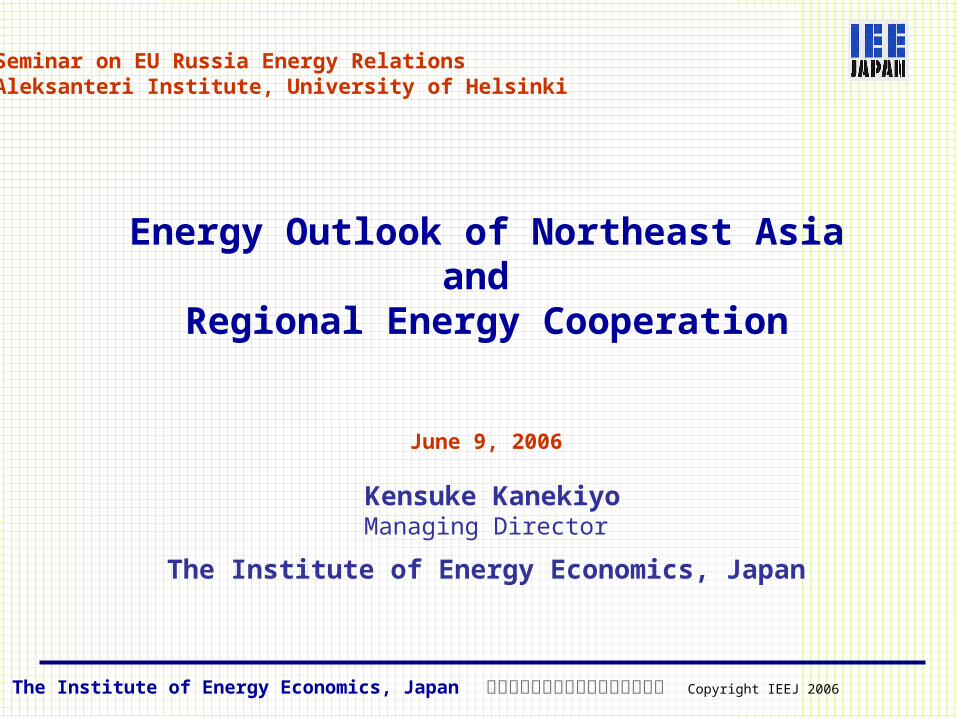

1.1 Oil Price Skyrocketing

1

1. Strong demand surge US plus Emerging economies(China, India, Brazil) 2. Shrinkage of surplus supply capacity in upstream,

downstream and US gas & power market. 3. Speculation by money funds.

The Institute of Energy Economics, Japan 財団法人日本能源経済研究所 Copyright IEEJ 2006

10

20

30

40

50

60

70

80

Sep-

01

Nov

-01

Jan-

02

Mar

-02

May

-02

Jul-

02

Sep-

02

Nov

-02

Jan-

03

Mar

-03

May

-03

Jul-

03

Sep-

03

Nov

-03

Jan-

04

Mar

-04

May

-04

Jul-

04

Sep-

04

Nov

-04

Jan-

05

Mar

-05

May

-05

Jul-

05

Sep-

05

Nov

-05

Jan-

06

Mar

-06

May

-06

General Strike in Venezuela

Iraqi War Terroist attack onSaudi oil sector

Hurricane "Ivan"

Deterioration of Iraqi sequrity

Yukos supply thretened

Nigerian tumult

Hurricane"Katorina"

$/Bbl

9-11 New YorkTerrorist Attack

Iranian CrisisWTI Futures at NYMEX

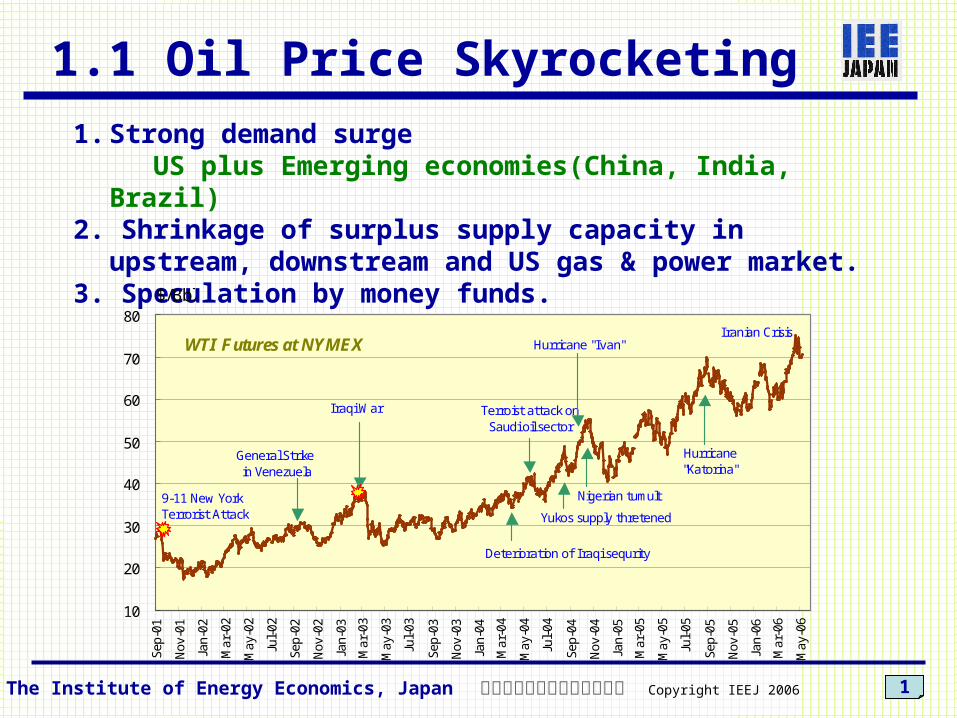

1.2 Energy Outlook of Asia1. Japan: Leveling off while fossil energy consumption

decreases.2. Developing Asia: More than double by 2030 as

China’s presence and import dependence greatly increase.

2The Institute of Energy Economics, Japan 財団法人日本能源経済研究所 Copyright IEEJ 2006

0

1000

2000

3000

4000

5000

6000

1971 1980 1990 2003 2010 2020 2030

Actual <= => Forecast

plus 3.1bill.toe1.1

1.5

0.40.10.0

Japan Korea China India Others

Bill.toe

Increase from 2003 to 2030

21%

13%

38%

8%20%

28%

13%

44%

6% 9%

Other Asia

India

China

KoreaJapan

April 2006, IEEJ

Million toe

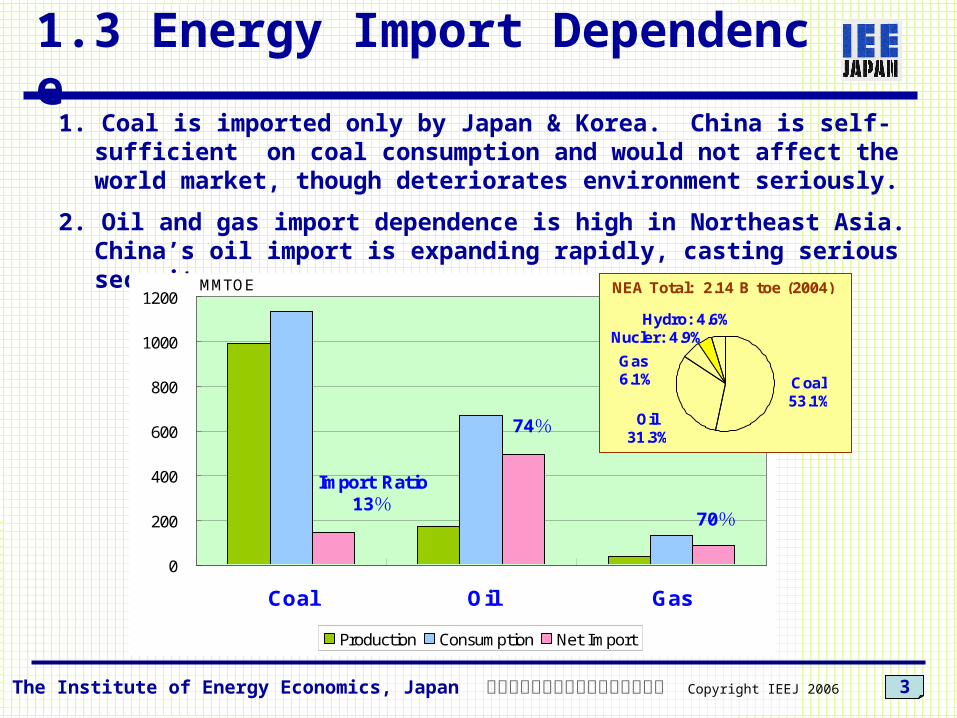

1.3 Energy Import Dependence1. Coal is imported only by Japan & Korea. China is self-

sufficient on coal consumption and would not affect the world market, though deteriorates environment seriously.

2. Oil and gas import dependence is high in Northeast Asia. China’s oil import is expanding rapidly, casting serious security concern.

3

0

200

400

600

800

1000

1200

Coal Oil Gas

Production Consumption Net Import

MMTOE

Import Ratio13%

74%

70%

NEA Total: 2.14 B toe (2004)

Coal53.1%

Oil31.3%

Gas6.1%

Hydro: 4.6%Nucler: 4.9%

The Institute of Energy Economics, Japan 財団法人日本エネルギー経済研究所 Copyright IEEJ 2006

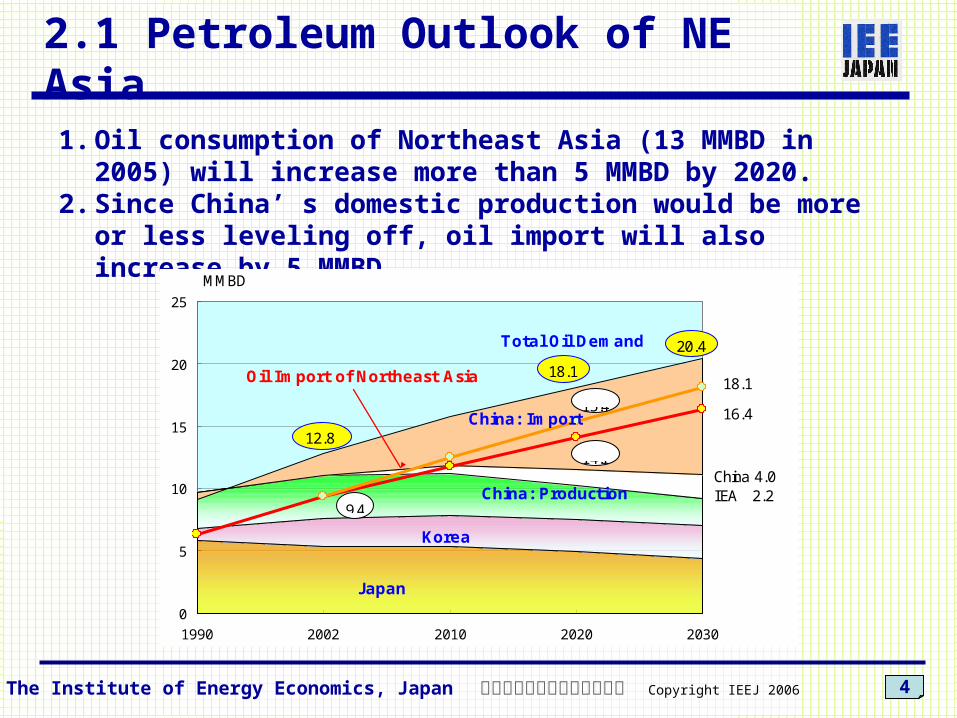

2.1 Petroleum Outlook of NE Asia1. Oil consumption of Northeast Asia (13 MMBD in

2005) will increase more than 5 MMBD by 2020.2. Since China’ s domestic production would be more or

less leveling off, oil import will also increase by 5 MMBD.

4The Institute of Energy Economics, Japan 財団法人日本能源経済研究所 Copyright IEEJ 2006

0

5

10

15

20

25

1990 2002 2010 2020 2030

14.1

15.4

Japan

Korea

China: Production

China: Import

Oil Import of Northeast Asia

MMBD

18.1

16.4

China 4.0IEA 2.2

9.4

12.8

18.1

20.4Total Oil Demand

0

50

100

150

200

250

300

2002 2003 2004 2002 2003 2004 2002 2003 2004

Japan Korea China

ME Ratio78.1%

ME Ratio45.4%

ME:74.1%SE Asia:8.9%

Others:17.0%

20048.9MMBD

Total Northeast Asia

Million KL

ME Ratio88.9%

2.2 Middle East Dependency of Oil

5

1. Northeast Asia depends on the Middle East 3/4 of oil Import

2. This causes vulnerability of supply and other issues such as the Asian Premium of the Middle East crude oils.

Source: National statistics

The Institute of Energy Economics, Japan 財団法人日本エネルギー経済研究所 Copyright IEEJ 2006

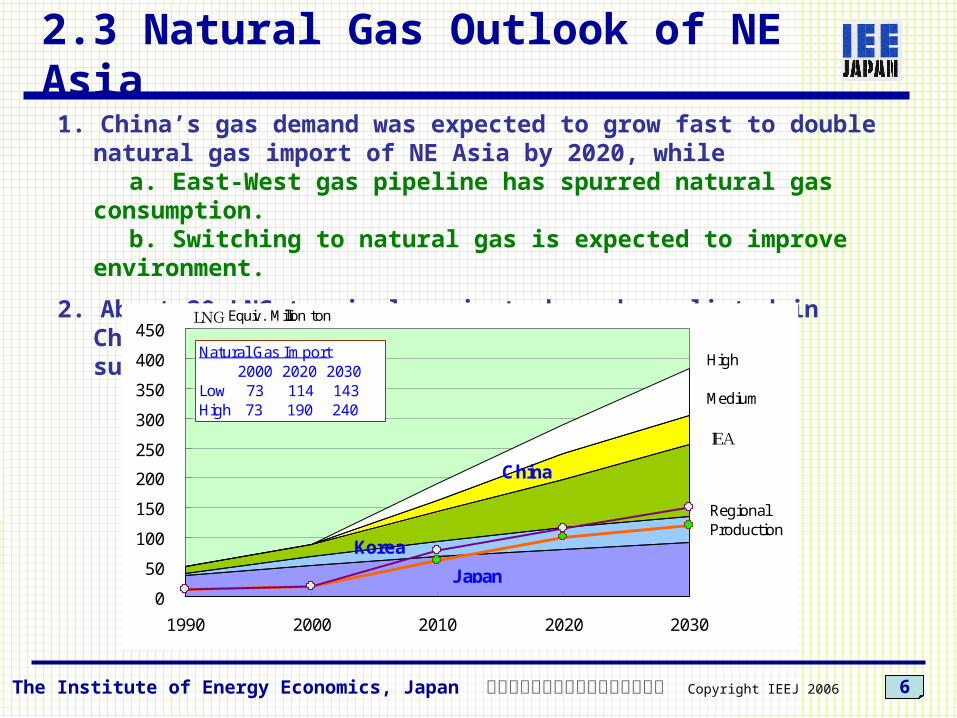

2.3 Natural Gas Outlook of NE Asia1. China’s gas demand was expected to grow fast to double

natural gas import of NE Asia by 2020, while a. East-West gas pipeline has spurred natural gas

consumption. b. Switching to natural gas is expected to improve

environment.

2. About 20 LNG terminal projects have been listed in China. However, skyrocketing gas price may cause substantial delay.

6

0

50

100

150

200

250

300

350

400

450

1990 2000 2010 2020 2030

High

Medium

IEA

RegionalProduction

LNG Equiv. Million ton

Natural Gas Import 2000 2020 2030Low 73 114 143High 73 190 240

J apan

Korea

China

The Institute of Energy Economics, Japan 財団法人日本エネルギー経済研究所 Copyright IEEJ 2006

3.1 Status of Energy Cooperation

1. Institutions discussing on energy cooperation APEC, ASEAN+3, SOM, Asia Pacific Partnership, etc

2. Active Projects only for Information Exchange 1) APERC (Energy Outlook and other research work) 2) JODI (Joint Oil Data Initiative) 3) RTEIS (Real-Time Emergency Information Sharing)

3. Candidate Energy Projects for Regional Cooperation 1) Joint Oil Stock Piling 2) Siberian Oil/Gas Pipelines 3) New Asian Oil Market 4) Rationalization of Energy Use / Energy Conservation 5) CDM/JI/ETS 6) Nuclear Power Development

No specific institution to talk on Northeast Asian Energy Cooperation, yet !!

7The Institute of Energy Economics, Japan 財団法人日本エネルギー経済研究所 Copyright IEEJ 2006

3.2 Russia and Northeast AsiaStranded oil & gas resources in eastern Russia will bean important answer to energy security of Northeast

Asia.

8

East Siberian Fields

West Siberian Fields

For EuropeOver 6000km

For Northeast Asia2000 - 3000km

Caspian oil fields(Major competitor for Russia)

2000km

3000km

4000km

6000km

The Institute of Energy Economics, Japan 財団法人日本エネルギー経済研究所 Copyright IEEJ 2006

3.3 Potential Energy Flow from Eastern Russia

9The Institute of Energy Economics, Japan 財団法人日本エネルギー経済研究所 Copyright IEEJ 2005

Phase-1:Taishet – Skovorodino Distance: 2400km Capacity: 0.6 MMBD Investment:$ 8 Billion Completion: End of 2008

Mohe

Branch Line ??

Phase-2: Skovorodino - Perevoznaya Distance: 2000km Capacity: 1.6MMBD (Whole line) Investments: $6 Billion Completion: 2012?

East Siberian Oil & Gas Fields(For Development)

Hydro Power

Offshore Sakhalin Fields(Under Development)

3.4 Petroleum Resources of Eastern Russia

Probable Possible Total

OilEast Siberia

Billion Barrels

6.1Billion Barrels

15.3Billion Barrels

21.4

Krasnoyarsk & Irkutsk 4.1 14.8 18.9

Sakha Republic 2.0 0.5 2.5

Sakhalin 4.3 5.6 9.9

Eastern Russia 10.4 20.9 31.3

Natural GasEast Siberia

Tcf106.2

Tcf91.6

Tcf197.8

Krasnoyarsk Krai 22.2 23.0 45.2

Irkutsk Oblast 41.0 31.0 72.0

Sakha Republic 42.9 37.6 80.5

Sakhalin 21.1 8.4 29.5

Eastern Russia 127.3 100.1 227.4

The Institute of Energy Economics, Japan 財団法人日本エネルギー経済研究所 Copyright IEEJ 2006

Source: IEEJ World Bank Report “Northeast Asia Natural Gas Trade”

10

Oil and gas reserves located in eastern Russia are yet to be developed except those in Sakhalin.

Siberian Trap

Siberian PlatformWest-Siberian Basin

West-Siberian Basin

Siberian Platform

Early Mesozoic

Present

Oil & Gas Fields

200 Ma – PresentMesozoic – Cenozoicclastics

250 Ma Triassic basaltic Lava

540 - 440 MaPaleozoic clasticsCarbonate, salt

640 – 540 MaVendian carbonate,Salt bedsUpper Proterozoic

1650 – 640 MaRephean carbonate, shaleProterozoic

2000 –1650 MaRephean basal sand,Eroded/weathered basement surface3000 – 2000 MaArchaen crystallineBasement rocks

Bazhenov Fm.

Siberian Trap

Siberian PlatformWest-Siberian Basin

West-Siberian Basin

Siberian Platform

Early Mesozoic

Present

Oil & Gas Fields

200 Ma – PresentMesozoic – Cenozoicclastics

250 Ma Triassic basaltic Lava

540 - 440 MaPaleozoic clasticsCarbonate, salt

640 – 540 MaVendian carbonate,Salt bedsUpper Proterozoic

1650 – 640 MaRephean carbonate, shaleProterozoic

2000 –1650 MaRephean basal sand,Eroded/weathered basement surface3000 – 2000 MaArchaen crystallineBasement rocks

Bazhenov Fm.

11

3.5 Geology of Siberia

Lava flew out

↑↑

↑↑

The Institute of Energy Economics, Japan 財団法人日本エネルギー経済研究所 Copyright IEEJ 2006

Geology of east Siberia is old, peculiar and difficult to interpret.

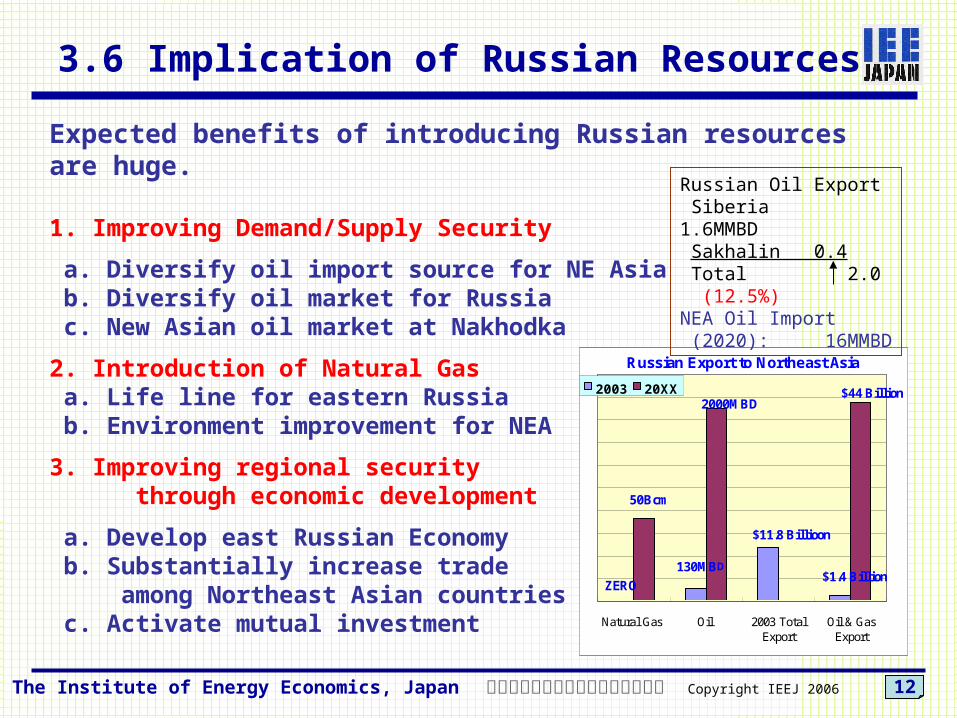

3.6 Implication of Russian Resources

Expected benefits of introducing Russian resources are huge.

1. Improving Demand/Supply Security

a. Diversify oil import source for NE Asia b. Diversify oil market for Russia c. New Asian oil market at Nakhodka

2. Introduction of Natural Gas a. Life line for eastern Russia b. Environment improvement for NEA

3. Improving regional security through economic development

a. Develop east Russian Economy b. Substantially increase trade among Northeast Asian countries c. Activate mutual investment Natural Gas Oil 2003 Total

ExportOil & Gas

Export

2003 20XX

ZERO

50Bcm

130MBD

2000MBD

$11.8 Billioon

$1.4 Billion

$44 Billion

Russian Export to Northeast Asia

Russian Oil Export Siberia 1.6MMBD Sakhalin 0.4 Total 2.0 (12.5%)NEA Oil Import (2020): 16MMBD

12The Institute of Energy Economics, Japan 財団法人日本エネルギー経済研究所 Copyright IEEJ 2006

4.1 Simple Principles to Apply

13The Institute of Energy Economics, Japan 財団法人日本エネルギー経済研究所 Copyright IEEJ 2005

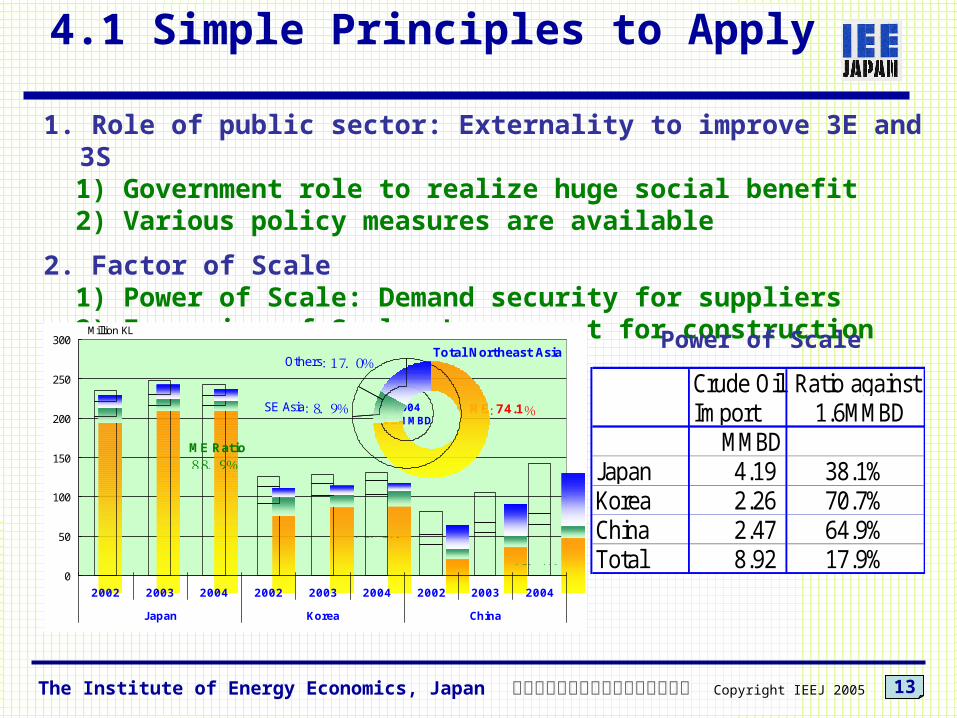

1. Role of public sector: Externality to improve 3E and 3S 1) Government role to realize huge social benefit 2) Various policy measures are available

2. Factor of Scale 1) Power of Scale: Demand security for suppliers 2) Economics of Scale: Lower cost for construction

Power of Scale

0

50

100

150

200

250

300

2002 2003 2004 2002 2003 2004 2002 2003 2004

Japan Korea China

ME Ratio78.1%

ME Ratio45.4%

ME:74.1%SE Asia:8.9%

Others:17.0%

20048.9MMBD

Total Northeast Asia

Million KL

ME Ratio88.9%

Crude Oil Ratio againstImport 1.6MMBD

MMBDJapan 4.19 38.1%Korea 2.26 70.7%China 2.47 64.9%Total 8.92 17.9%

4.2 Pipeline Economics

14The Institute of Energy Economics, Japan 財団法人日本エネルギー経済研究所 Copyright IEEJ 2005

1. Economics of Scale works greatly in long distance pipeline.

2. Pipeline tariff can be lowered by policy consideration, such as long term credit, lower tax, or subsidy.

0.00

2.00

4.00

6.00

8.00

10.00

12.00

0.8 1.2 1.6

Pipeline Capacity:MMBD

Pipeline Tariff: $/Bbl

Economics of Scale

0.0

2.0

4.0

6.0

8.0

10.0

12.0

10 15 20 25 30

$/Bbl

5.3

1.9

Project Period

Commercial Tariff(ROE=12%)

ROE=7%

Profit

Tax 35%

Interest

OPEX

CAPEX

TechnicalCost

Pipeline Economics

4.3 East-West Dialogue

15The Institute of Energy Economics, Japan 財団法人日本エネルギー経済研究所 Copyright IEEJ 2005

1. Supplier/Consumer Dialogue

x Energy development and transaction with Russia, CIS and Middle East countries x International cooperation and rational order in energy development x Technology development, energy transit issues, etc.

2. Consumer/Consumer Dialogue

x Energy conservation and rational use x Rational market design and government role x Technology development

3. Global Energy-Environment System: Post Kyoto Protocol

x Participation of every stakeholders Integration of KP(Top-down) and APP(Bottom-up) approaches x Harmonizing interests of developed and developing countries.

Thank You