Embed Size (px)

Citation preview

機密性○

Nov 4th, 2016

Ministry of Economy, Trade and Industry (METI), Japan

Enhancing Mekong-Japan

Economic Partnership

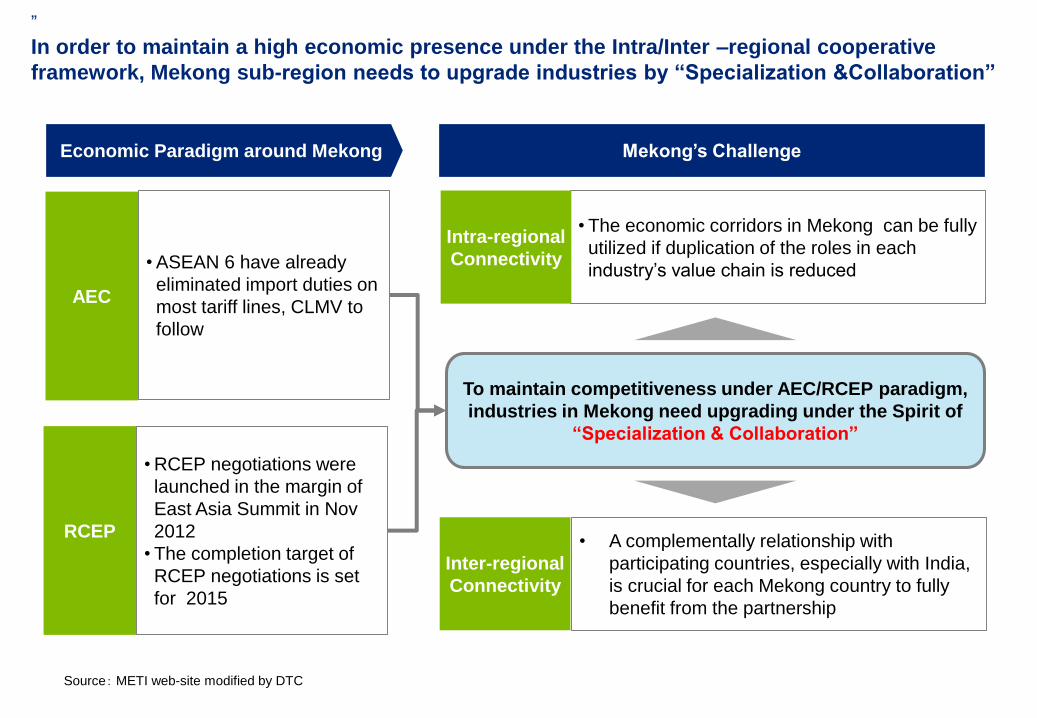

”

In order to maintain a high economic presence under the Intra/Inter –regional cooperative

framework, Mekong sub-region needs to upgrade industries by “Specialization &Collaboration”

• The economic corridors in Mekong can be fully

utilized if duplication of the roles in each

industry’s value chain is reduced

Intra-regional

Connectivity

AEC

RCEP

• ASEAN 6 have already

eliminated import duties on

most tariff lines, CLMV to

follow

• RCEP negotiations were

launched in the margin of

East Asia Summit in Nov

2012

• The completion target of

RCEP negotiations is set

for 2015

To maintain competitiveness under AEC/RCEP paradigm,

industries in Mekong need upgrading under the Spirit of

“Specialization & Collaboration”

• A complementally relationship with

participating countries, especially with India,

is crucial for each Mekong country to fully

benefit from the partnership

Inter-regional

Connectivity

Source: METI web-site modified by DTC

Economic Paradigm around Mekong Mekong’s Challenge

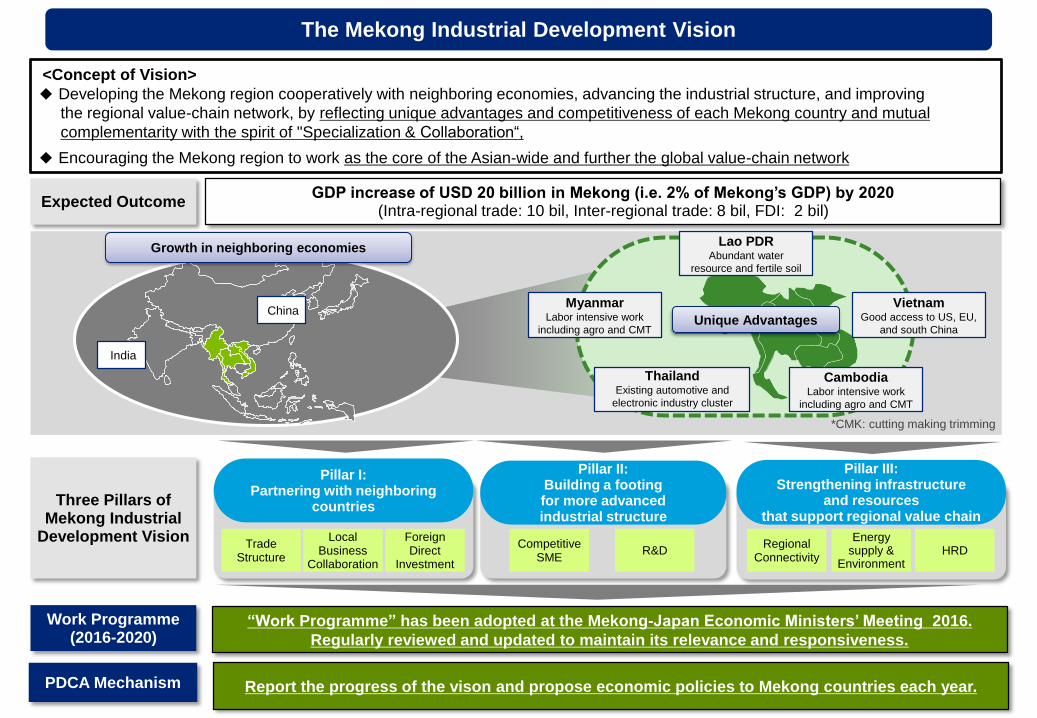

VietnamGood access to US, EU,

and south China

Lao PDRAbundant water

resource and fertile soil

CambodiaLabor intensive work

including agro and CMT

ThailandExisting automotive and

electronic industry cluster

MyanmarLabor intensive work

including agro and CMT

<Concept of Vision>

◆ Developing the Mekong region cooperatively with neighboring economies, advancing the industrial structure, and improving

the regional value-chain network, by reflecting unique advantages and competitiveness of each Mekong country and mutual

complementarity with the spirit of "Specialization & Collaboration“,

◆ Encouraging the Mekong region to work as the core of the Asian-wide and further the global value-chain network

Unique Advantages

Growth in neighboring economies

China

India

Pillar I: Partnering with neighboring

countries

Pillar II: Building a footing for more advanced industrial structure

Pillar III: Strengthening infrastructure

and resources that support regional value chain

TradeStructure

ForeignDirect

InvestmentHRD

LocalBusiness

CollaborationR&D

RegionalConnectivity

CompetitiveSME

Energysupply &

Environment

Expected OutcomeGDP increase of USD 20 billion in Mekong (i.e. 2% of Mekong’s GDP) by 2020

(Intra-regional trade: 10 bil, Inter-regional trade: 8 bil, FDI: 2 bil)

Three Pillars of Mekong Industrial

Development Vision

Work Programme(2016-2020)

*CMK: cutting making trimming

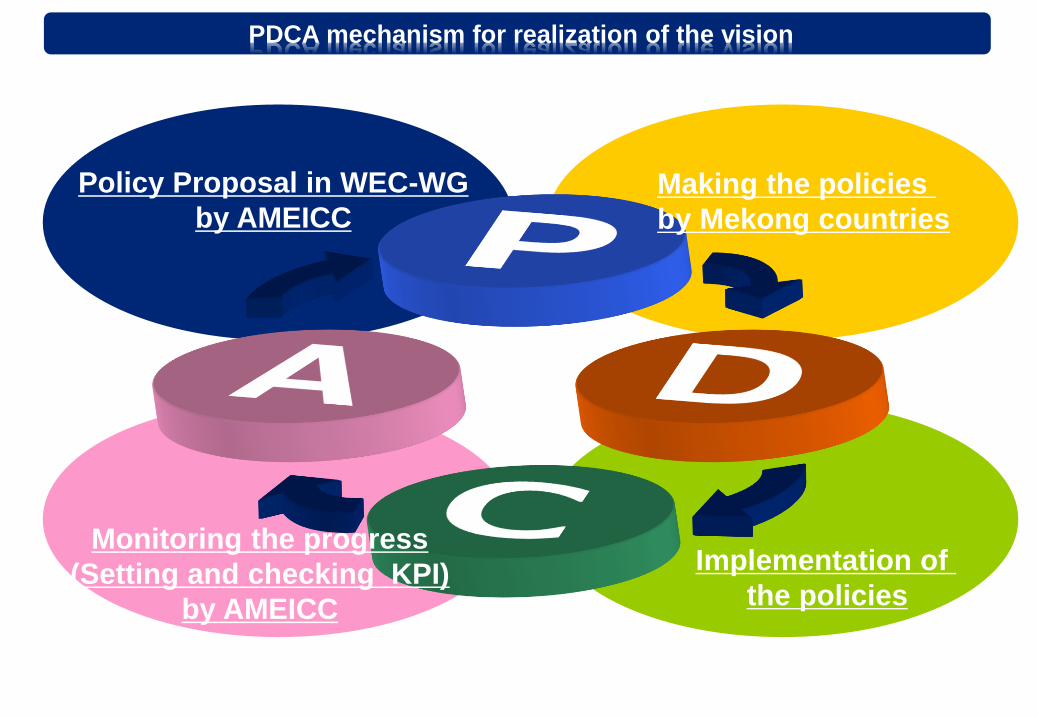

PDCA Mechanism Report the progress of the vison and propose economic policies to Mekong countries each year.

“Work Programme” has been adopted at the Mekong-Japan Economic Ministers’ Meeting 2016.

Regularly reviewed and updated to maintain its relevance and responsiveness.

The Mekong Industrial Development Vision

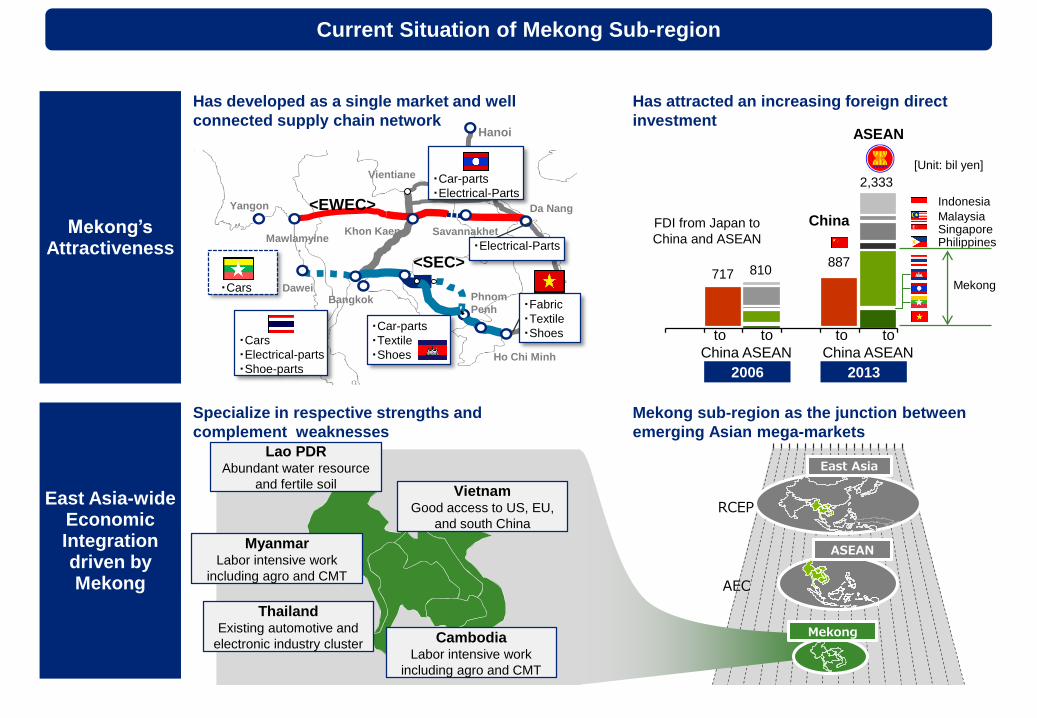

Mekong’sAttractiveness

887717 810

2,333

Bangkok Phnom

Penh

Dawei

Khon Kaen

Yangon

Mawlamyine

Hanoi

Vientiane

Da Nang<EWEC>

<SEC>

Savannakhet

Ho Chi Minh

・Car-parts

・Textile

・Shoes

・Fabric

・Textile

・Shoes

・Cars

・Cars

・Electrical-parts

・Shoe-parts

・Electrical-Parts

・Car-parts

・Electrical-Parts

to

China

to

ASEAN

20132006

Singapore

Indonesia

Malaysia

Philippines

China

ASEAN

Mekong

to

China

to

ASEAN

FDI from Japan to

China and ASEAN

East Asia-wideEconomicIntegrationdriven byMekong

VietnamGood access to US, EU,

and south China

Lao PDRAbundant water resource

and fertile soil

CambodiaLabor intensive work

including agro and CMT

ThailandExisting automotive and

electronic industry cluster

MyanmarLabor intensive work

including agro and CMT

ASEAN

RCEP

AEC

East Asia

Mekong

Specialize in respective strengths and

complement weaknesses

Mekong sub-region as the junction between

emerging Asian mega-markets

Has developed as a single market and well

connected supply chain network

Has attracted an increasing foreign direct

investment

Current Situation of Mekong Sub-region

[Unit: bil yen]

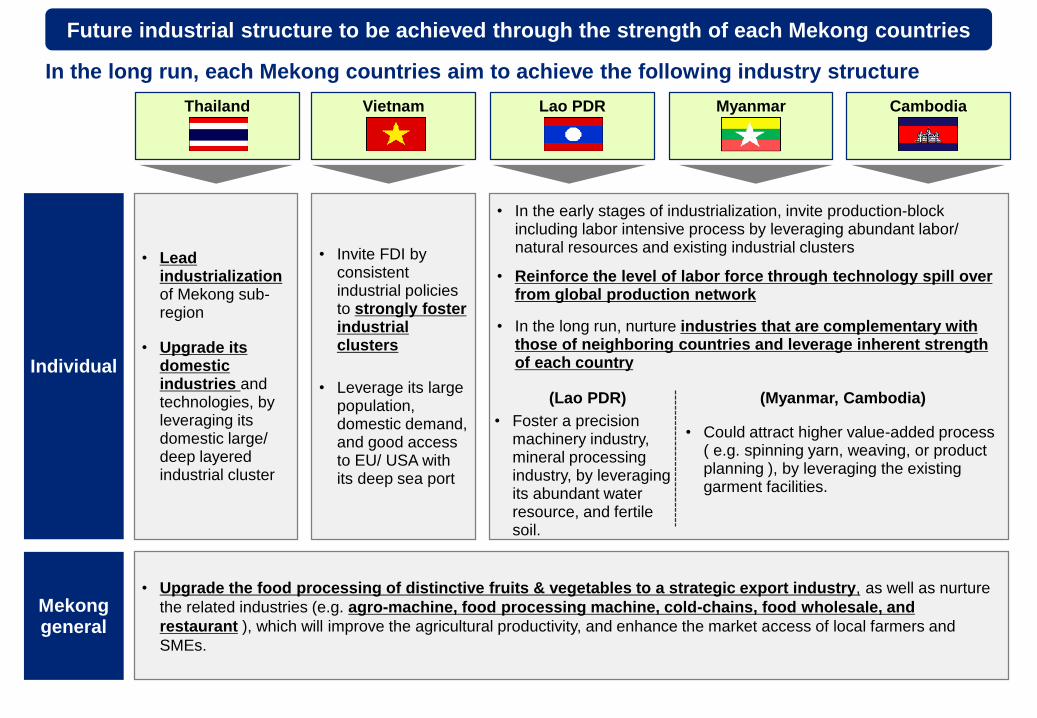

• Upgrade the food processing of distinctive fruits & vegetables to a strategic export industry, as well as nurture

the related industries (e.g. agro-machine, food processing machine, cold-chains, food wholesale, and

restaurant ), which will improve the agricultural productivity, and enhance the market access of local farmers and

SMEs.

Vietnam Lao PDR Myanmar CambodiaThailand

• Leadindustrializationof Mekong sub-region

• Upgrade itsdomesticindustries andtechnologies, byleveraging itsdomestic large/deep layeredindustrial cluster

• Invite FDI byconsistentindustrial policiesto strongly fosterindustrialclusters

• Leverage its largepopulation,domestic demand,and good accessto EU/ USA withits deep sea port

• In the early stages of industrialization, invite production-blockincluding labor intensive process by leveraging abundant labor/natural resources and existing industrial clusters

• Reinforce the level of labor force through technology spill overfrom global production network

• In the long run, nurture industries that are complementary withthose of neighboring countries and leverage inherent strengthof each country

Future industrial structure to be achieved through the strength of each Mekong countries

In the long run, each Mekong countries aim to achieve the following industry structure

(Lao PDR)

• Foster a precision machinery industry, mineral processing industry, by leveraging its abundant water resource, and fertile soil.

(Myanmar, Cambodia)

• Could attract higher value-added process ( e.g. spinning yarn, weaving, or product planning ), by leveraging the existing garment facilities.

Individual

Mekonggeneral

6

TradeStructure

ForeignDirect

Investment

LocalBusiness

Collaboration

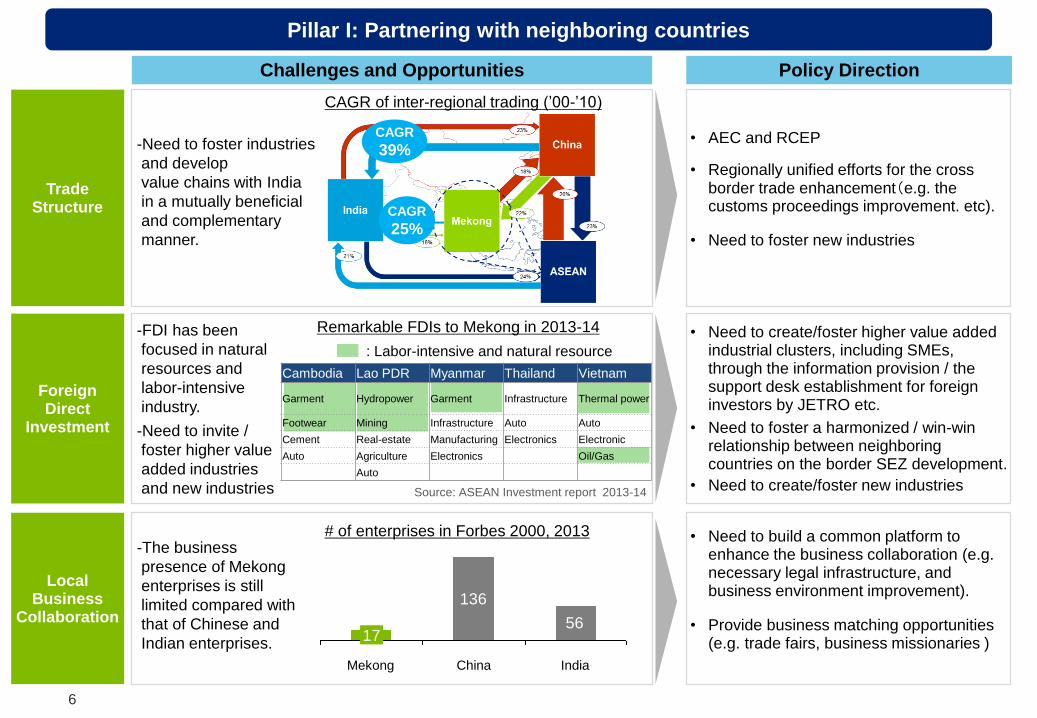

• AEC and RCEP

• Regionally unified efforts for the cross border trade enhancement(e.g. the customs proceedings improvement. etc).

• Need to foster new industries

• Need to create/foster higher value added industrial clusters, including SMEs, through the information provision / the support desk establishment for foreign investors by JETRO etc.

• Need to foster a harmonized / win-win relationship between neighboring countries on the border SEZ development.

• Need to create/foster new industries

• Need to build a common platform to enhance the business collaboration (e.g. necessary legal infrastructure, and business environment improvement).

• Provide business matching opportunities (e.g. trade fairs, business missionaries )

Pillar I: Partnering with neighboring countries

Policy DirectionChallenges and Opportunities

CAGR

39%

CAGR

25%

-Need to foster industries

and develop

value chains with India

in a mutually beneficial

and complementary

manner.

-FDI has been

focused in natural

resources and

labor-intensive

industry.

-Need to invite /

foster higher value

added industries

and new industries

-The business

presence of Mekong

enterprises is still

limited compared with

that of Chinese and

Indian enterprises.

136

56

IndiaMekong

17

China

# of enterprises in Forbes 2000, 2013

CAGR of inter-regional trading (’00-’10)

Remarkable FDIs to Mekong in 2013-14

: Labor-intensive and natural resource

Source: ASEAN Investment report 2013-14

Cambodia Lao PDR Myanmar Thailand Vietnam

Garment Hydropower Garment Infrastructure Thermal power

Footwear Mining Infrastructure Auto Auto

Cement Real-estate Manufacturing Electronics Electronic

Auto Agriculture Electronics Oil/Gas

Auto

7

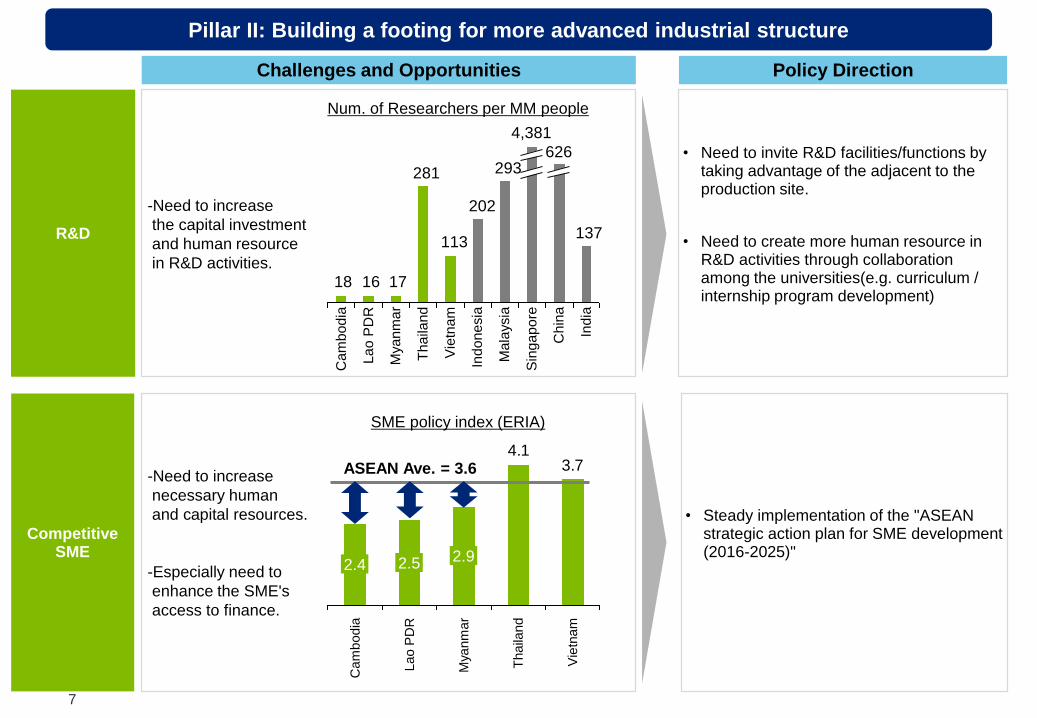

R&D

• Need to invite R&D facilities/functions by taking advantage of the adjacent to the production site.

• Need to create more human resource in R&D activities through collaboration among the universities(e.g. curriculum / internship program development)

CompetitiveSME

• Steady implementation of the "ASEAN strategic action plan for SME development (2016-2025)"

Pillar II: Building a footing for more advanced industrial structure

137

293

202

113

281

171618

4,381

626

Num. of Researchers per MM people

Ca

mb

od

ia

La

o P

DR

Myanm

ar

Th

aila

nd

Vie

tna

m

Ind

on

esia

Mala

ysia

Sin

ga

po

re

Ch

ina

Ind

ia

3.74.1

Cam

bodia

Thaila

nd

Vie

tnam

Lao P

DR

Mya

nm

ar

2.92.52.4

SME policy index (ERIA)

ASEAN Ave. = 3.6-Need to increase

necessary human

and capital resources.

-Especially need to

enhance the SME's

access to finance.

-Need to increase

the capital investment

and human resource

in R&D activities.

Policy DirectionChallenges and Opportunities

8

HRD

RegionalConnectivity

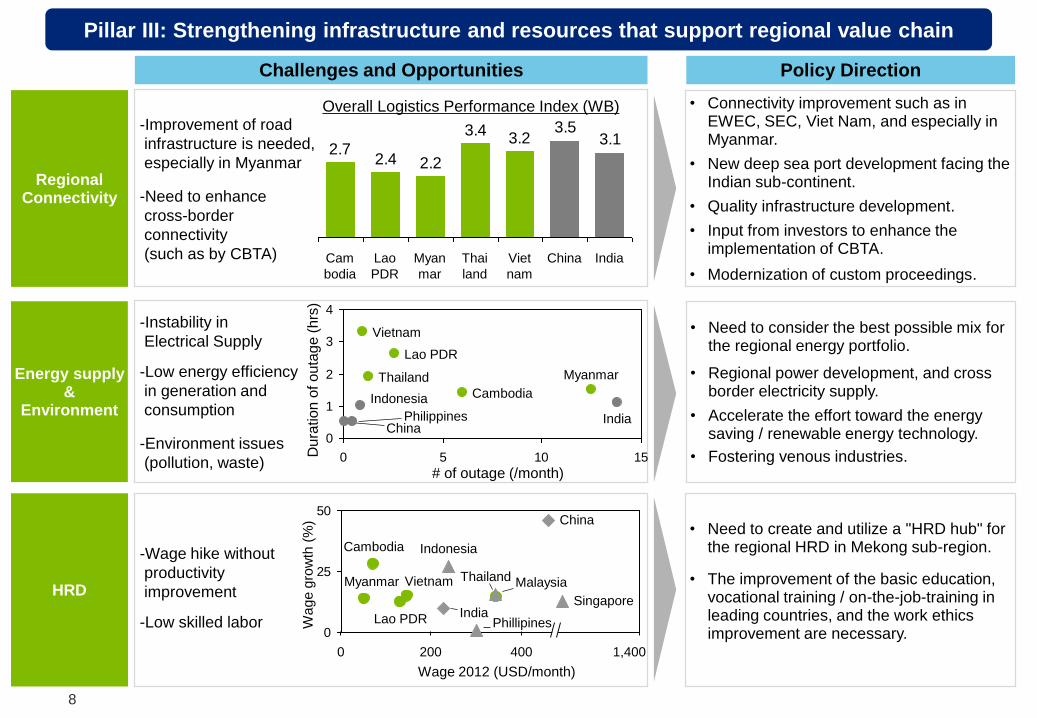

• Need to create and utilize a "HRD hub" for the regional HRD in Mekong sub-region.

• The improvement of the basic education, vocational training / on-the-job-training in leading countries, and the work ethics improvement are necessary.

• Connectivity improvement such as in EWEC, SEC, Viet Nam, and especially in Myanmar.

• New deep sea port development facing the Indian sub-continent.

• Quality infrastructure development.

• Input from investors to enhance the implementation of CBTA.

• Modernization of custom proceedings.

Energy supply&

Environment

• Need to consider the best possible mix for the regional energy portfolio.

• Regional power development, and cross border electricity supply.

• Accelerate the effort toward the energy saving / renewable energy technology.

• Fostering venous industries.

Pillar III: Strengthening infrastructure and resources that support regional value chain

0

25

50

1,4004002000

India

China

Phillipines

Indonesia

Malaysia

Singapore

Vietnam ThailandMyanmar

Lao PDR

Cambodia

Wa

ge

gro

wth

(%)

-Wage hike without

productivity

improvement

-Low skilled labor

-Instability in

Electrical Supply

-Low energy efficiency

in generation and

consumption

-Environment issues

(pollution, waste)

Wage 2012 (USD/month)

Policy DirectionChallenges and Opportunities

-Improvement of road

infrastructure is needed,

especially in Myanmar

-Need to enhance

cross-border

connectivity

(such as by CBTA)

Vietnam

Thailand

Philippines

Myanmar

Lao PDR

Indonesia

IndiaChina

Cambodia

# of outage (/month)

Du

ratio

nofo

uta

ge

(hrs

)

3.13.5

3.23.4

2.22.42.7

IndiaChinaViet

nam

Myan

mar

Lao

PDR

Cam

bodia

Thai

land

Overall Logistics Performance Index (WB)

0

1

2

3

4

0 5 10 15

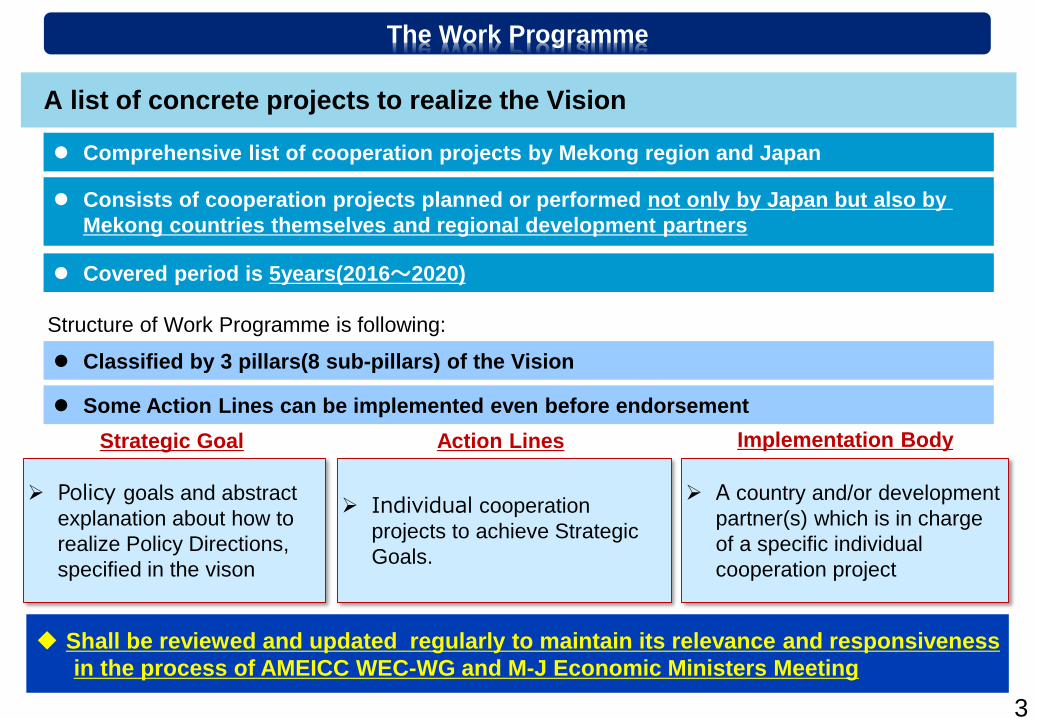

Covered period is 5years(2016~2020)

Comprehensive list of cooperation projects by Mekong region and Japan

A list of concrete projects to realize the Vision

Consists of cooperation projects planned or performed not only by Japan but also by

Mekong countries themselves and regional development partners

Individual cooperation

projects to achieve Strategic

Goals.

Strategic Goal Action Lines

Structure of Work Programme is following:

A country and/or development

partner(s) which is in charge

of a specific individual

cooperation project

Implementation Body

Policy goals and abstract

explanation about how to

realize Policy Directions,

specified in the vison

Shall be reviewed and updated regularly to maintain its relevance and responsiveness

in the process of AMEICC WEC-WG and M-J Economic Ministers Meeting

Some Action Lines can be implemented even before endorsement

Classified by 3 pillars(8 sub-pillars) of the Vision

The Work Programme

3

Policy Proposal in WEC-WG

by AMEICCMaking the policies

by Mekong countries

Monitoring the progress

(Setting and checking KPI)

by AMEICC

Implementation of

the policies

PDCA mechanism for realization of the vision

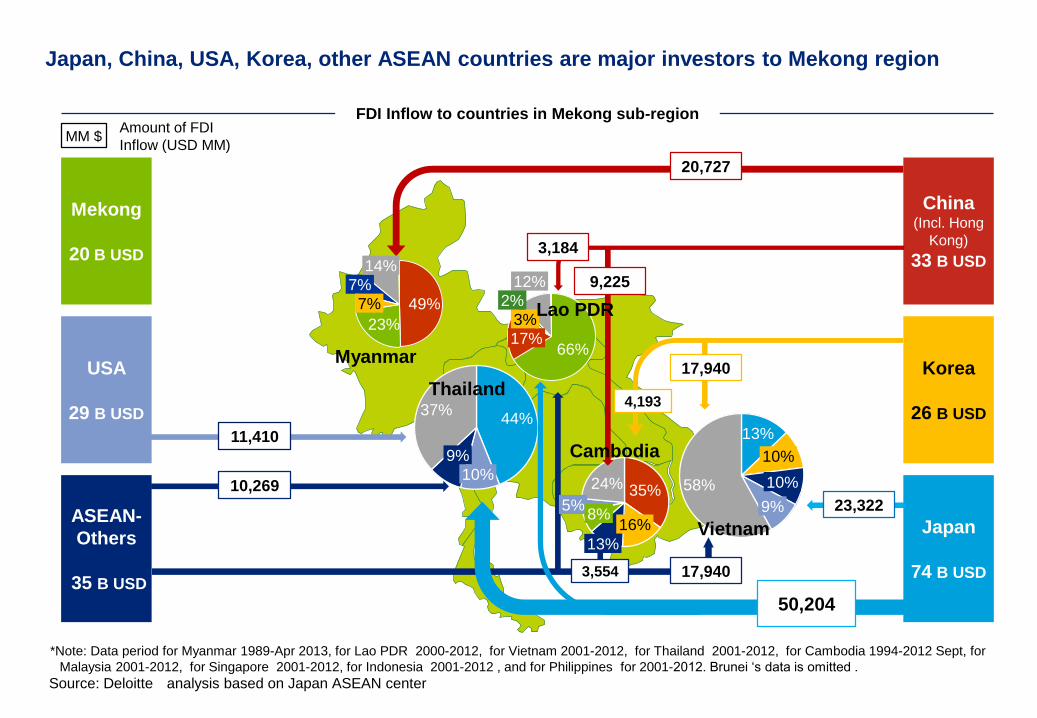

Japan, China, USA, Korea, other ASEAN countries are major investors to Mekong region

FDI Inflow to countries in Mekong sub-region

Source: Deloitte analysis based on Japan ASEAN center

*Note: Data period for Myanmar 1989-Apr 2013, for Lao PDR 2000-2012, for Vietnam 2001-2012, for Thailand 2001-2012, for Cambodia 1994-2012 Sept, for

Malaysia 2001-2012, for Singapore 2001-2012, for Indonesia 2001-2012 , and for Philippines for 2001-2012. Brunei ‘s data is omitted .

China(Incl. Hong

Kong)

33 B USD

Korea

26 B USD

USA

29 B USD

ASEAN-

Others

35 B USD

Japan

74 B USD

20,727

3,184

50,204

10,269

3,554 17,940

17,940

4,193

11,410

Mekong

20 B USD

MM $Amount of FDI

Inflow (USD MM)

23,322

9%

44%

10%

37%

10%

9%

58%

13%

10%

7%

49%7%

23%

14%

16%

13%

5%35%

8%

24%

9,225

17%

3%

12%

66%

2%

Myanmar

Thailand

Cambodia

Vietnam

Lao PDR

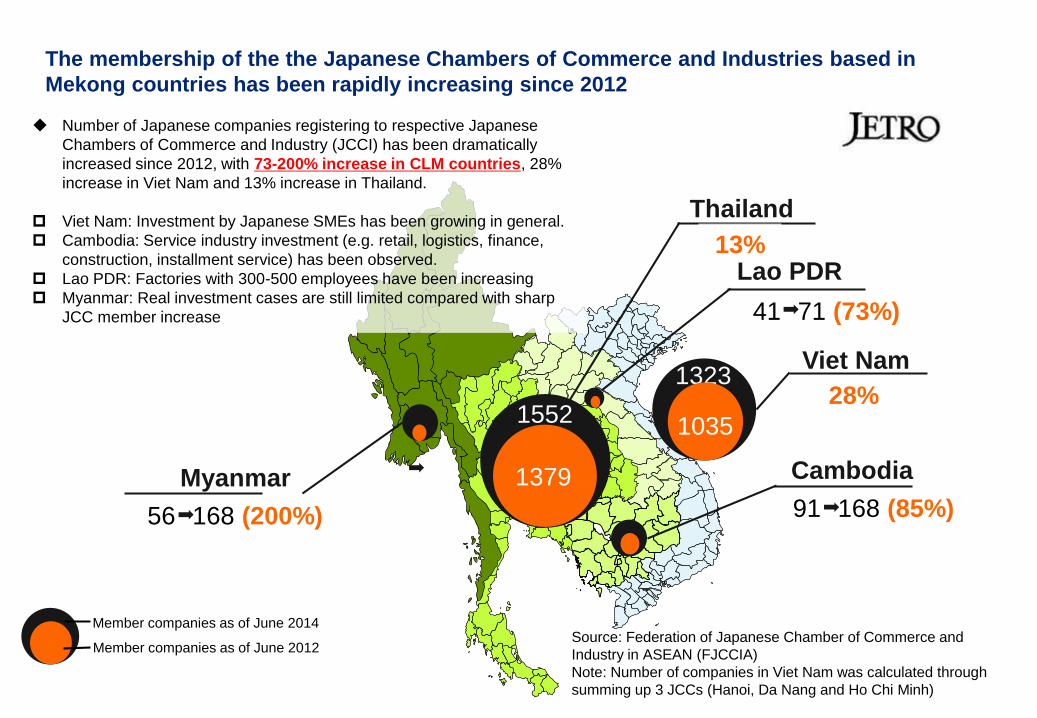

The membership of the the Japanese Chambers of Commerce and Industries based in

Mekong countries has been rapidly increasing since 2012

1552

1379

1323

1035

91 168 (85%)

41 71 (73%)

28%

Source: Federation of Japanese Chamber of Commerce and

Industry in ASEAN (FJCCIA)

Note: Number of companies in Viet Nam was calculated through

summing up 3 JCCs (Hanoi, Da Nang and Ho Chi Minh)

Member companies as of June 2014

Member companies as of June 2012

Number of Japanese companies registering to respective Japanese

Chambers of Commerce and Industry (JCCI) has been dramatically

increased since 2012, with 73-200% increase in CLM countries, 28%

increase in Viet Nam and 13% increase in Thailand.

Viet Nam: Investment by Japanese SMEs has been growing in general.

Cambodia: Service industry investment (e.g. retail, logistics, finance,

construction, installment service) has been observed.

Lao PDR: Factories with 300-500 employees have been increasing

Myanmar: Real investment cases are still limited compared with sharp

JCC member increase

Lao PDR

Viet Nam

Cambodia

Thailand

13%

56 168 (200%)

Myanmar

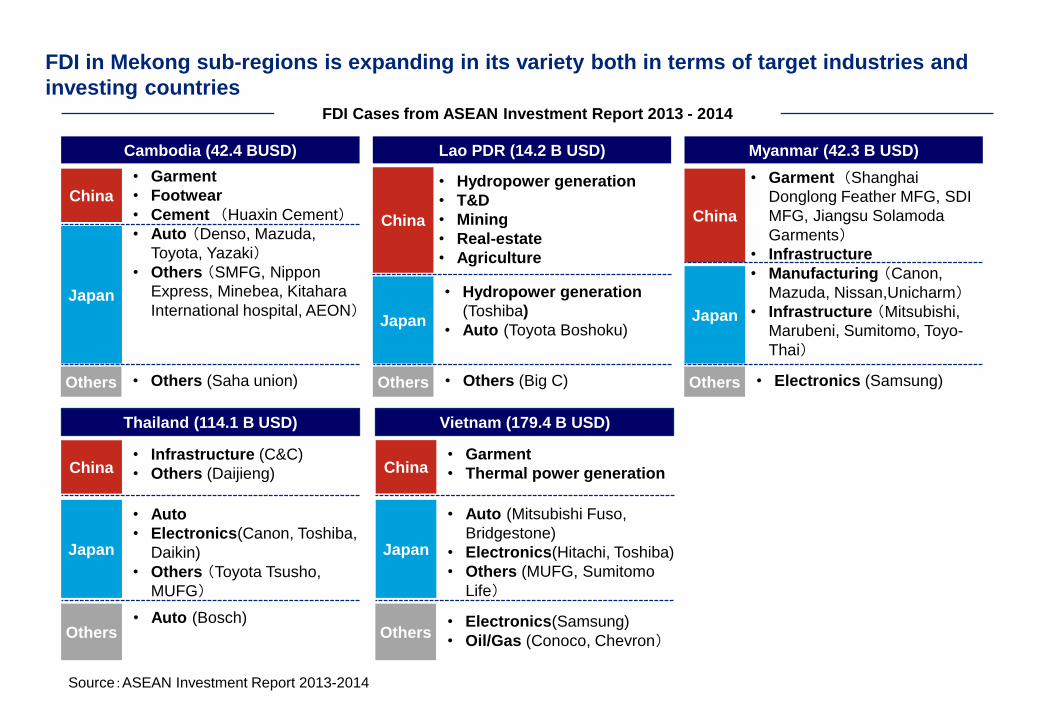

FDI in Mekong sub-regions is expanding in its variety both in terms of target industries and

investing countries

Source:ASEAN Investment Report 2013-2014

FDI Cases from ASEAN Investment Report 2013 - 2014

Lao PDR (14.2 B USD)

• Garment

• Footwear

• Cement (Huaxin Cement)• Auto (Denso, Mazuda,

Toyota, Yazaki)• Others (SMFG, Nippon

Express, Minebea, Kitahara

International hospital, AEON)

China

Japan

Vietnam (179.4 B USD)Thailand (114.1 B USD)

Cambodia (42.4 BUSD) Myanmar (42.3 B USD)

• Hydropower generation

• T&D

• Mining

• Real-estate

• Agriculture

China

Japan

China

Japan

• Garment (Shanghai

Donglong Feather MFG, SDI

MFG, Jiangsu Solamoda

Garments)• Infrastructure

• Manufacturing (Canon,

Mazuda, Nissan,Unicharm)• Infrastructure (Mitsubishi,

Marubeni, Sumitomo, Toyo-

Thai)

• Auto

• Electronics(Canon, Toshiba,

Daikin)

• Others (Toyota Tsusho,

MUFG)

China

Japan

Others

• Auto (Mitsubishi Fuso,

Bridgestone)

• Electronics(Hitachi, Toshiba)

• Others (MUFG, Sumitomo

Life)

China

Japan

• Hydropower generation

(Toshiba)

• Auto (Toyota Boshoku)

• Electronics(Samsung)

• Oil/Gas (Conoco, Chevron)

Others • Electronics (Samsung)

Others• Auto (Bosch)

Others • Others (Big C)

• Infrastructure (C&C)

• Others (Daijieng)

• Garment

• Thermal power generation

Others • Others (Saha union)