Embed Size (px)

Citation preview

"Financiamiento en Salud y Protección Financiera en

América Latina”

"Financiamiento en Salud y Protección Financiera en

América Latina”

Ciudad de México15 al 18 de octubre, 2007

Ciudad de México15 al 18 de octubre, 2007

Plan de trabajo:El caso de México

Felicia Marie KnaulRebeca Wong

Hector ArreolaOscar Mendez

Christian Norton

Plan de trabajo:El caso de México

Felicia Marie KnaulRebeca Wong

Hector ArreolaOscar Mendez

Christian Norton

Líneas de investigación sobre México en el proyecto IDRC

Aociación entre aseguramiento en salud y el Seguro Popular con el empobrecimiento por gastos en salud: Un modelo de pareo por puntaje de propensión

3. Análisis del sistema de salud y su financiamiento

a. general y comparativosb. especificos a México - 2

5. Entrenamineto y materiales de los cursos

4. Policy briefs

c. Documento sobre serie de tiempo y panel Mexicob. Ajuste temporal de los datos a través de un estudio tipo panel

a. El sistema de salud en México de donde viene y hacia donde va: Evolución de la cobertura de los diferentes subsistemas de salud; enfocado en la equidad de la ampliación de la cobertura y los retos a futuro (próximos pasos en la reforma)

a.i. Medición y actualización de los diferentes indicadores; serie de tiempo

2. Los determinantes del gastoscatastrófico y empobrecedor

d. Documento resumen general de determinantes

1. Avances en la medición de losindicadores principales

d. Documento general sobre metodología y medición

Líneas de Investigación

e. Documento general sobre niveles de gasto catastrófico y empobrecedor

a.ii. Implicaciones del gasto en salud sobre la brecha de pobreza

a. general y comparativos

b. Remesas y gasto en saludc. Políticas públicas para disminuir los gastos catastróficos y empobrecedores en salud

a. Envejecimiento y gasto en salud, proyeccion

a. Serie de tiempo, ENIGH 1992- 2006

Estudios específicos

Outline

1. Mexico: Complex, overlapping transitionsThe Health System: financing and reform

2. Trends in insurance coverage and challenges and next steps for reform3. Data and methods4 Results

Catastrophic and impoverishing health spendingTrends: 1992-2006Determinants: 1992-2005, 2006

Future research

New challenges are associated with the rapid advance of profound demographic and epidemiologic transition

Over 50 years, Mexico will complete an aging process that took two centuries in most European countries.

In 2050, one-in-four Mexicans will be 65 or over – a four-fold increase.

Costly, chronic, non-communicable illnesses now dominate the burden

of disease.

Costly, chronic, non-communicable illnesses now dominate the burden

of disease.

1955 2005

72%

22%

6%

73%

17%10%

Communicable

Chronic, Non-communicable

Injuries

Source: Sepúlveda et al. ,2006

Outline

1. Mexico: Complex, overlapping transitionsThe Health System: financing and reform

2. Trends in insurance coverage and challenges and next steps for reform3. Data and methods4 Results

Catastrophic and impoverishing health spendingTrends: 1992-2006Determinants: 1992-2005, 2006

Future research

Mexico Pre-Reform: Insurance Coverage was highly fragmented, inequitable and regressive

Source: Authors´ estimates using data from the 2000 Census; ENIGH, 2000; and Salud: México 2002, Ssa (2003).

Distribution of federal funds:-2.4 times more for the insured

Insurance coverage by quintile

50%

100%

I II IV V TOTALIIIUninsured Insured

55-60% uninsured

Reliance on OOP in Mexico is high at 50%+; especially given GDP

FranceGermany

PanamaUruguay

ItalyColombia SpainBolivia Costa RicaArgentinaVenezuelaPeru

Brazil Korea

ThailandMalaysiaParaguay

Ethiopia El Salvador

Congo ChinaVietnam

India

20

40

60

80

Chile

MexicoLAC

OECD

GDP per capita vs. OOP as a % of health system finance

GDP per capita

% O

OP

fin

ance

d

Source: Authors own estimations based on data from WHO 2006

=1.5 million families per trimester=~?? 4 million per year ??

Insured: 2.2%Uninsured: 9.6%

Poorest quintile: 19.6%

Quintiles 2-5: 3.1%

Catastrophe (30%) and Impoverishmentfrom health spending, 2000

Source: authors own estimations based on data from the ENIGH 2000

Catastrophic, 30%: 3.4%Impoverishment ($US1): 3.8%

Catastrophic and/or impoverishment: 6.3%

THE VISION BEHIND THE 2003 REFORM:ELIMINATE SEGMENTATION IN ACCESS TO HEALTH INSURANCE BY GENERATING A SYSTEM FOR SOCIAL PROTECTION IN HEALTH THAT INCLUDES POPULAR HEALTH INSURANCE FOR FAMILIES EXCLUDED FROM SOCIAL SECURITY

Social Security

Public and private, Formal sector workers

and their families: ~50% of population

Ministry of Health with residual

funding

Poor, informal sector, non-salaried,

rural areas: ~ 50% of population

1943

2001/3: Pilot of PHI2003: LawJan. 1, 2004: SSPH 2010: Universal coverage with Seguro Popular

System for Social

Protection in

Health

SeguroPopular

Frenk et al., 2004.

Increase in health spending in Mexico as a % of GDP

7.06.5

5.1

0

1

2

3

4

5

6

7

2000 2001 2002 2003 2004 2005 2006 2010

% G

DP

Fuente: Secretaría de Salud. Salud: México 2001-2005. México, D.F.: Secretaría de Salud, 2006.

Outline

1. Mexico: Complex, overlapping transitionsThe Health System: financing and reform

2. Trends in insurance coverage and challenges and next steps for reform3. Data and methods4 Results

Catastrophic and impoverishing health spendingTrends: 1992-2006Determinants: 1992-2005, 2006

Future research

Householdsaffiliated toSeguro Popular:% of families w/o social securityand millions offamilies

Increase in Seguro Popular coverage andexpansion of package of services

# of coveredservices

2006Pilot, 2003 2004

~100%

2007* - 20102005

104 113146

249

2003 20062004

262

20072005

Source: Comision Nacional de Protección Social en Salud, 2007; and UNSANUT, 2006.* Data until the first trimester of 2007.

3%9%

28%19%

29%

0.6 1.5

3.5

mill

ion

5.1

mill

ion

5.2

mill

ion

~18.

3 m

illio

nhh

~

Evolución de la Cobertura en el Aseguramiento por Institución

Fuente: INSP, Encuesta Nacional de Salud, 2000; Encuesta Nacional de Salud y Nutrición, 2006.

2000

32%60%

NO ASEGURADOS

IMSS2005-2006

28%53%

11%SEGURO

POPULAR

% of population without coverage

Censo 2000

Conteo 2005

Covered

Health insurance coverage increased between 2000-2005 in allregions and in almost all States, due, to a large extent, to theadvances of Seguro Popular

66-82% 49-65%29-49%

0

15

45

75

Sout

h

Nor

th

Sout

heas

t

Cen

ter

D.FCenso 2000

Conteo 2005

Nat

iona

l

Source: Aouthrs own estimations based on data from INEGI 2000, 2005

Insurance coverage by institution and level ofmarginalization, 2000 & 2005

SEG.POP OTHERS PEMEXISSSTE IMSS

0

20

40

60

2000 2005 2000 2005 2000 2005 2000 2005 2000 2005 2000 2005

Very high High Medium Low Very low Total

%

Source: Authors own estimations based on data from INEGI 2000, 2005

0

20

60

100

IMSS ISSSTE

SEG.POP PRIVADOS

78%87%

97% 100% 100%

% OF MUNICIPALITIES WITH AT LEAST ONE FAMILY W/ IMSS AND/OR SEGURO POPULAR

%

Municipalities with insured population, by level of´poverty´ and institution, 2005

Source: Authors own estimations based on data from INEGI 2005.

Very high High Medium Low Very low Total

92%

Challenges and next steps in the reform

• Coverage: rural areas, migrants (cross-border)

• Ageing, chronic illness: expanding coverage and package

• Affiliation: higher-income groups• At the system level:

– Prestación plural: reforms in IMSS– Payment and contracting mechanisms

Outline

1. Mexico: Complex, overlapping transitionsThe Health System: financing and reform

2. Trends in insurance coverage and challenges and next steps for reform3. Data and methods4 Results

Catastrophic and impoverishing health spendingTrends: 1992-2006Determinants: 1992-2005, 2006

Future research

Data: Data: National Household Income and National Household Income and Expenditure Surveys, 1992 to 2005Expenditure Surveys, 1992 to 2005

Households in the sampleYear

10,95210,95210,10810,10817,16717,167

22,59522,595

10,50310,50312,81512,81514,04214,042

199819982000200020022002

20042004

1994199419921992

19961996

20052005

Economic Crisis

Pilot of Popular Insurance (PHI)

New health insurance law goes into effect 23,17423,174

20062006 20,87520,875

Indicators:

1.Impoverishment (absolute) from healthspending:

cross the $US 1 poverty linelive below the poverty line and becomefurther impoverished

2.Catastrophic spending (relative):spend a high % of disposible income(20%, 30%, 40%; net of food)

WHO, 2000.3.Deepening of poverty: gaps

(Van Doorslaer, Wagstaff, ODonnell)

Methodology:1. DESCRIPTIVE AND TIME SERIES ANALYSIS:

(we are updating the series)Trends 1992-2006Poverty gaps: consecutive years, time periods

2. REGRESsION ANALYSIS, POOLED CROSS-SECTION: Dependent variables:

If hh spends 20, 30 or 40% (logit)If hh is impoverished (logit)Health spending as a % of disposable income (tobit)

Independent variables:• HH: family composition (elders & children), remittances• State: % coverage Seguro Popular

Controls: social security coverage (family and state), educacionand gender, family wealth, time and state dummies

Methodology:3.Propensity Score Matching and IV

-(Remittances: pooled time series)

-What is the ´impact´ of health insurancecoverage on catastrophic and impoverishinghealth spending

-SP can only be identified in 2006

Note: SP can only be identified in2006 (and 2004)

Outline

1. Mexico: Complex, overlapping transitionsThe Health System: financing and reform

2. Data and methods3. Results

Catastrophic and impoverishing health spendingTrends: 1992-2005Determinants: 1992-2005

Future research4. Trends in insurance coverage and challenges and next steps for reform

Impoverishment

0

5

10

15 Impoverishment and/or cat´c 20%

Cat´c 40%

Cat´c 30%

Cat´c 20%

1992 1994 1996 1998 2000 2002 20042005

2006

% o

fhou

seho

lds

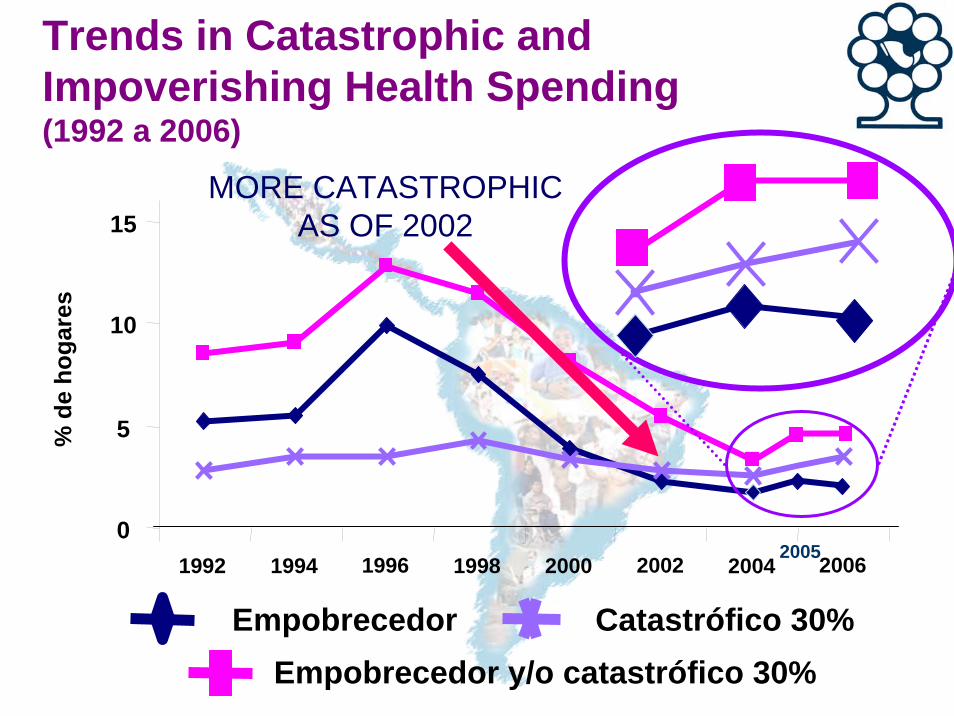

Trends in catastrophic and impoverishing health spending (1992-2006)

Fuente: Estimaciones propias basadas en información de la ENIGH 1992 a 2006

Trends in Catastrophic andImpoverishing Health Spending(1992 a 2006)

EmpobrecedorEmpobrecedor y/o catastrófico 30%

Catastrófico 30%

0

5

10

15

1992 1994 1996 1998 2000 2002 2004 2006

% d

e ho

gare

s

2005

MORE CATASTROPHICAS OF 2002

Catastrophic health expenditure in familieswith and without remittances, by quintile

With remittances Without remittances

Source: Authors own estimations based on data from the ENIGH 1992-2005

•5.6% of families receive income transfers;• these families account for about 9.7% of total

out-of-pocket health spending

Empobrecimiento absoluto

0

5

10

QUINTILE I QUINTILE V TOTAL QUINTILES II a V TOTAL0

5

10

QUINTILE I

Empobrecimiento relativo

Elderly >65 Children <5,elderly >65 Children > 5

Neither elderly nor children ALL

Catastrophic health expenditure by household composition, (1992-2005)

10

20

30Impoverishment

01992 1994 1996 1998 2000 2002 2004 2005

Catastrophic, 30%

0

5

10

15

1992 1994 1996 1998 2000 2002 2004 2005

Trends in Catastrophic and ImpoverishingHealth Spending by insurance status(1992 a 2006)

Catastrófico EmpobrecedorCatastrófico

y/o empobrecedor

Insured Seguro Popular anduninsurd

0

4

8

12

1992 1996 2000 2004 2006

0

4

8

12

1992 1996 2000 20042005

20062005

0%

2%

4%

6%

Catastrófico Empobrecedor Catastrófico y/oempobrecedor

Uninsured

Seguro PopularSocial Securityl

2006

Differences Post vs Pre1992……2005

Differences between years1992 - 19941994 - 19961996 - 19981998 - 20002000 - 20022002 – 20042004 – 20052000 - 20052002 - 2005

Differences between Periods(1998 - 2000) - (2000-2002)

(1998 - 2000) - (2002-2004)

(2000 - 2002) - (2002-2004)

(1992 - 1994) - (2002-2004)

(1992 - 1998) - (2002-2004)

(2000 - 2002) - (2002-2004)

(2000 - 2002) - (2004-2005)

Note: The values in bold represent significant differences with a 90% confidence level/1 Poverty line defined as one dollar (PPP) per day per capita

Poverty Gap before and after health expenditure (hasta 2005)/1

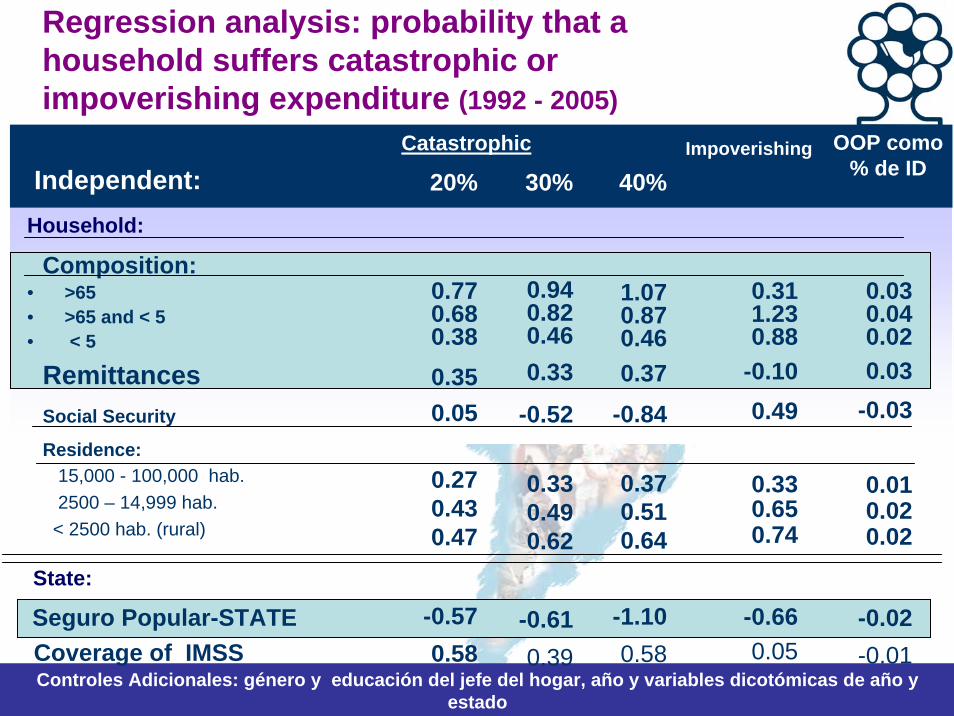

Regression analysis: probability that a household suffers catastrophic orimpoverishing expenditure (1992 - 2005)

Controles Adicionales: género y educación del jefe del hogar, año y variables dicotómicas de año y estado

OOP como % de ID

Impoverishing

20% 30% 40%Catastrophic

Independent:Household:

Composition:• >65• >65 and < 5 • < 5

RemittancesSocial Security

Residence:15,000 - 100,000 hab.2500 – 14,999 hab.

< 2500 hab. (rural)

State:

Seguro Popular-STATECoverage of IMSS

0.770.680.380.350.05

0.270.430.47

-0.570.58

0.940.820.460.33

-0.52

0.330.490.62

-0.610.39

1.070.870.460.37

-0.84

0.370.510.64

-1.100.58

0.311.230.88

-0.100.49

0.330.650.74

-0.660.05

0.030.040.020.03

-0.03

0.010.020.02

-0.02-0.01

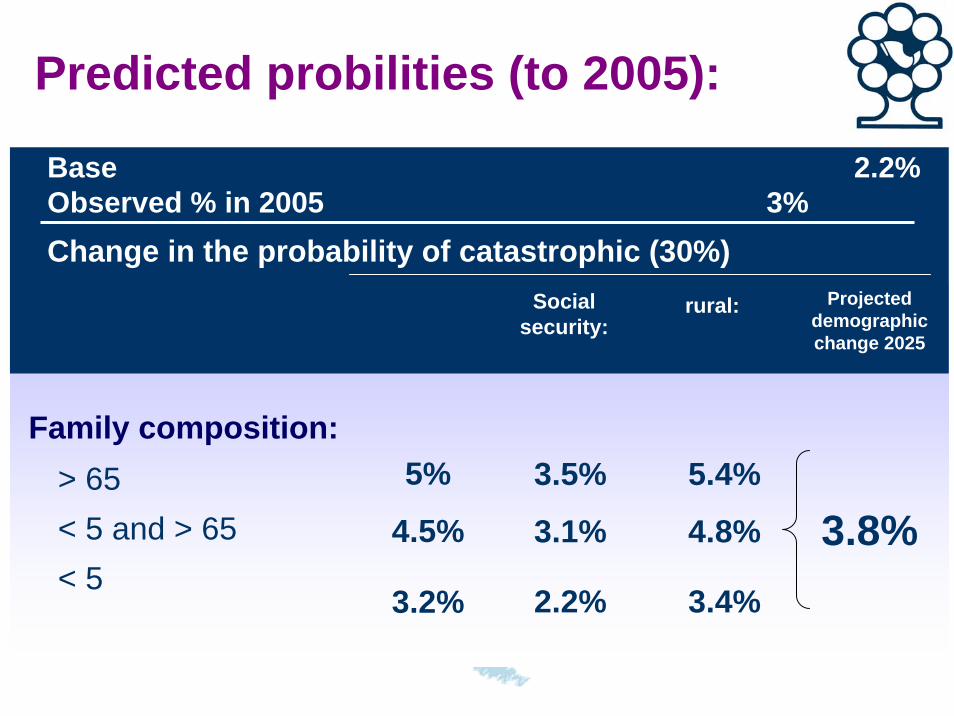

Predicted probilities (to 2005):

Social security:

rural:

Family composition:> 65 < 5 and > 65< 5

5%

4.5%

3.2%

3.5%

3.1%

2.2%

5.4%

4.8%

3.4%

Base 2.2% Observed % in 2005 3%Change in the probability of catastrophic (30%)

Projecteddemographicchange 2025

3.8%

Gasto catastrófico

Trends in ageing and catastrophicspending in Mexico (2002 a 2006)

2

3

% d

e ho

gare

s

4

2002 2004 2005 2006

Catastrophicwith without

ageing

2002 2006Annual

growth rate

TotalUninsuredw/ Seguro Popularw/ Seguridad Social

19%23%

12%

20%26%23%12%

8%9%

3%

% households with > 65

Resultados: Análisis sobre determinantescorriguiendo endogeneidad de Remesas

• Con variables instrumentales– Instrumento: Si hogar radica en un municipio expulsor– En los modelos logit de gasto catastrófico (20,30 y

40%, de gasto empobrecedor) y el tobit sobre contribución financiera del hogar los resultados son similares

• Variables estadísticamente significativas– Composición familiar (Viejos y niños) (+)– Remesas (+)– Familia cubierta por la seguridad social (-)– Lugar de residencia (Rural+)– Controles de estado (% de la seguridad social y avance en la

afiliación del SP) No significativas

Continuación

• Con PSM– Remesas es estadísticamente significativo en los

modelos logit de gasto catastrófico (20,30 y 40%), y el tobit sobre contribución financiera del hogar los resultados son similares.

– En el modelo de gasto empobrecedor es no significativa

– Variables estadísticamente significativas en los modelos

– Composición familiar (Viejos y niños) (+)– Remesas (+)– Familia cubierta por la seguridad social (-)– Lugar de residencia (Rural+)– Controles de estado (% de la seguridad social y avance en la

afiliación del SP) No significativas

Resultados: Análisis sobre sobre la asociación del incremento en la coberturadel SP sobre la protección financiera

Modelos con PSM• Estrategias:

1. Pareando libremente entre asegurados y no asegurados2. Pareando exclusivamente entre no asegurados3. Pareando haciendo control por tipo de hogar (Hogares que pueden

incluir miembros asegurados po la seguridad social y por el Seguro Popular)

• Resultados: – En los modelos 2 y 3 la prueba de diferencia de proporciones

de sufrir gastos catastróficos o empobrecedores son estadísticamente significativas a favor del grupo de tratamiento (cubiertos por el SP)

– Los modelos Logit de gastos catastróficos o empobrecedores en todos los casos no muestras un resultado estadísticamente significativo en estar asegurado por SP

– El modelo tobit sólo es estadísticamente significativo en la estrategia 2.

Continuación

• Otras variables significativas en el análisis

– Composición familiar (Viejos y niños) (+)– Remesas (+)– Familia cubierta por la seguridad social (-)– Lugar de residencia (Rural+)– Controles de estado (% de la seguridad social y avance

en la afiliación del SP) No significativas

"Financiamiento en Salud y Protección Financiera en

América Latina”

"Financiamiento en Salud y Protección Financiera en

América Latina”

Ciudad de México15 al 18 de octubre, 2007

Ciudad de México15 al 18 de octubre, 2007