Embed Size (px)

Citation preview

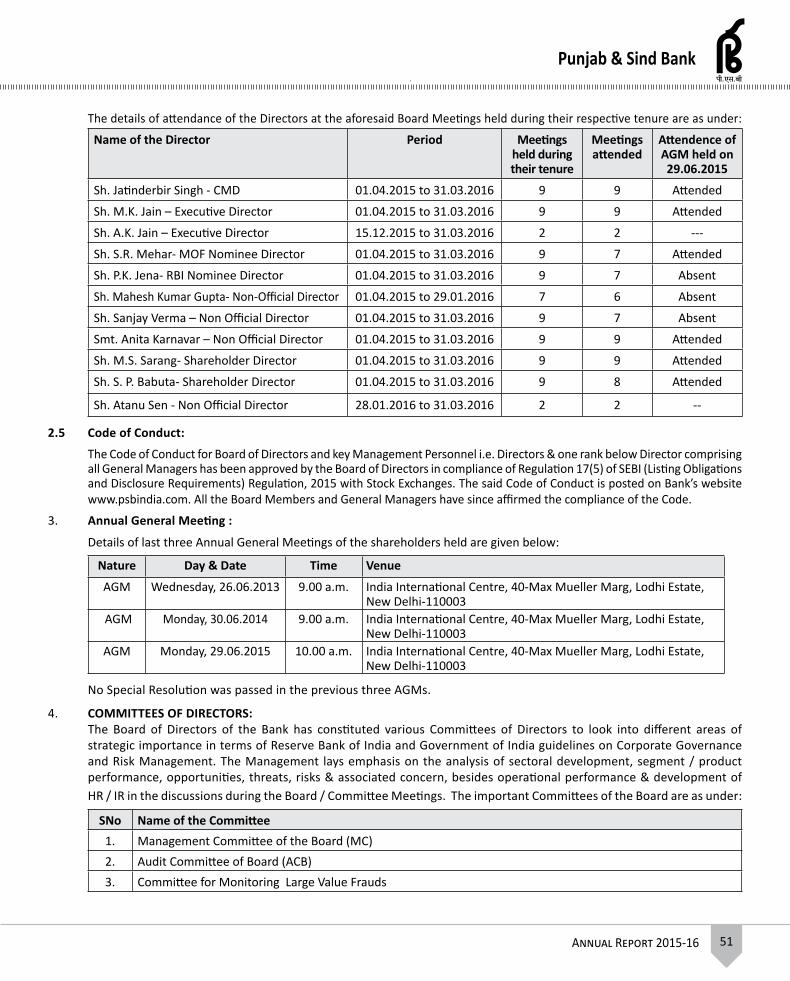

funs’kd eaMy / Board of Directors

dk;Zdkjh funs’kdJh eqds”k dqekj tSuExecutive Director

Sh. Mukesh Kumar Jain

dk;Zdkjh funs’kdJh vjfoUn dqekj tSu

Executive DirectorSh. Arvind Kumar Jain

Jh ,l-vkj- esgjSh. S.R. Mehar

Jh çnhIr- ds- tsukSh. Pradipta K. Jena

Jh lat; oekZSh. Sanjay Verma

v/;{k ,oa izca/k funs’kdJh tfrUnjchj flag] vkbZ-,-,l-

Chairman & Managing DirectorSh. Jatinderbir Singh, I.A.S.

Jhefr vuhrk d.kkZojSmt. Anita Karnavar

Jh ,e-,l- lkjaxSh. M.S. Sarang

Jh lq[ksu iky ccwrkSh. Sukhen Pal Babuta

Jh vruq lsuSh. Atanu Sen

Punjab & Sind Bank

Annual Report 2015-16 1

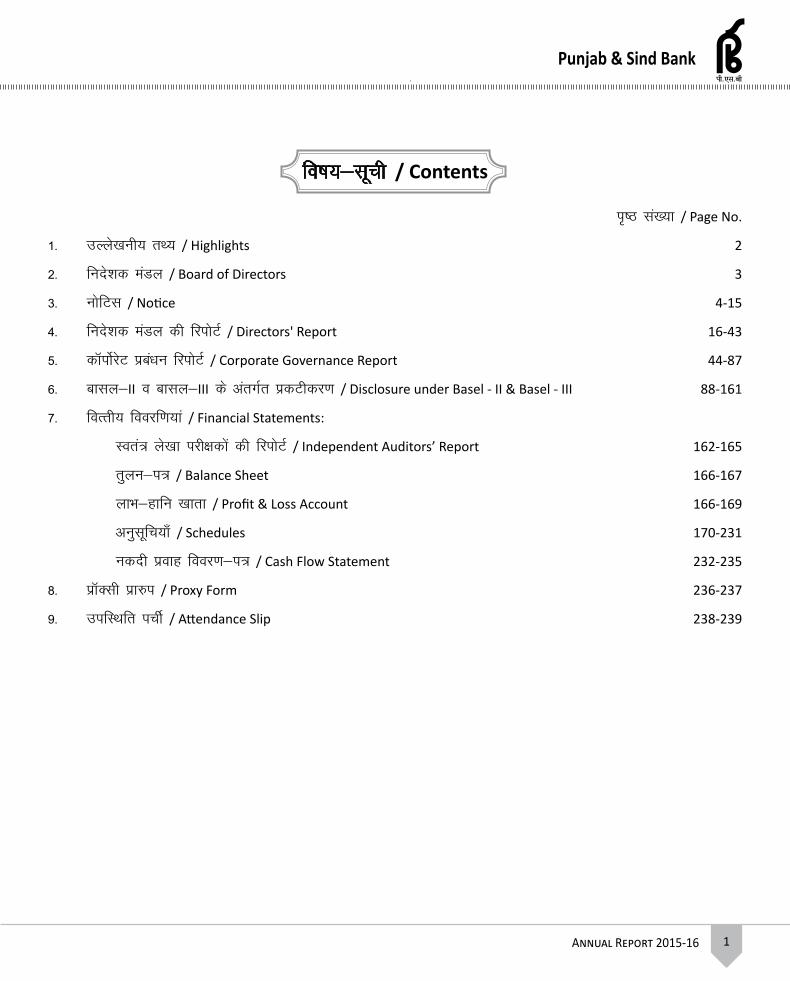

fo"k;&lwph / Contents

i`"B la[;k / Page No.

1- mYys[kuh; rF; / Highlights 2

2- funs”kd eaMy / Board of Directors 3

3- uksfVl / Notice 4-15

4- funs'kd eaMy dh fjiksVZ / Directors' Report 16-43

5- dkWiksZjsV izca/ku fjiksVZ / Corporate Governance Report 44-87

6- ckly&II o ckly&III ds varxZr izdVhdj.k / Disclosure under Basel - II & Basel - III 88-161

7- foRrh; foojf.k;ka / Financial Statements:

Lora= ys[kk ijh{kdksa dh fjiksVZ / Independent Auditors’ Report 162-165

rqyu&i= / Balance Sheet 166-167

ykHk&gkfu [kkrk / Profit & Loss Account 166-169

vuqlwfp;k¡ / Schedules 170-231

udnh izokg fooj.k&i= / Cash Flow Statement 232-235

8- izkWDlh izk#i / Proxy Form 236-237

9- mifLFkfr iphZ / Attendance Slip 238-239

iatkc ,.M fla/ cSad

okf"kZd fjiksVZ 2015-162

mYys[kuh; rF; / Highlights

#i, yk[kksa esa / Rupees. in lacs

fnukad 31-03-2016 dks / As on 31.03.20161- tek Deposits 91249962- ldy vfxze Gross Advances 65277223- izkFkfedrk {ks= vfxze Priority Sector Advances 24507974- ldy fuos'k Gross Investments 27693405- ifjpkyu ykHk Operating Profit 1269896- 'kq) ykHk Net Profit 335977- vkfLr;ksa ij izfrQy (%) Return on Assets (%) 0.34%8- “kq) ,u-ih-,- vuqikr (%) Net NPA Ratio (%) 4.62 % 9- iwaath i;kZIrrk vuqikr (%) (cklsy&II) Capital Adequacy Ratio (%) (Basel-II) 11.75%10- iwaath i;kZIrrk vuqikr (%) (cklsy&III) Capital Adequacy Ratio (%) (Basel-III) 10.91%

Punjab & Sind Bank

Annual Report 2015-16 3

cksMZ funs'kd / Board of Directors

v/;{k ,oa izca/k funs'kdJh tfrUnjchj flag] vkbZ-,-,l-

Chairman & Managing DirectorSh. Jatinderbir Singh, I.A.S.

dk;Zdkjh funs'kd dk;Zdkjh funs'kd Jh eqds'k dqekj tSu Jh vjfoUn dqekj tSuExecutive Director Executive DirectorSh. Mukesh Kumar Jain Sh. Arvind Kumar Jain

funs'kd @ Directors

Jh ,l-vkj- esgj Jh çnhIr ds- tsuk Jh lat; oekZ Jhefr vuhrk d.kkZojSh. S.R. Mehar Sh. Pradipta K. Jena Sh. Sanjay Verma Smt. Anita Karnavar

Jh ,e-,l- lkjax Jh lq[ksu iky ccwrk Jh vruq lsuSh. M.S. Sarang Sh. Sukhen Pal Babuta Sh. Atanu Sen

egkizca/kd / General Managers

Jh vkbZ-,l- HkkfV;k Jh ,e-th- JhokLro Jh nhid eSuh Jh th-,l- <Yy Sh. I.S. Bhatia Sh. M.G. Srivastava Sh. Deepak Maini Sh. G.S. Dhall

Jh Mh-Mh- 'kekZ Jh ohjsUnz xqIrk Jh ,l-lh- Dok=k Jh th-,l- ukjax¼izfrfu;qfDr ij½

Sh. D.D. Sharma Sh. Varinder Gupta Sh. S.C. Kwatra Sh. G.S. Narang (On Deputation)

Jh gjfoUnj flag Jh vkj- ds- caly Jh jfeUnjthr flag Jh th-,l- <haxjkSh. Harvinder Singh Sh. R.K.Bansal Sh. Raminderjit Singh Sh. G.S. Dhingra

ys[kk ijh{kd / Auditors

eSllZ frokjh ,.M ,lksf'k,Vl eSllZ f<+Yyksa ,.M ,lksf'k,VlM/s Tiwari & Associates M/s Dhillon & Associates

eSllZ /kou ,.M da- eSllZ nfoUnj iky flag ,.M da-M/S Dhawan & Co. M/S Davinder Pal Singh & Co.

iatkc ,.M fla/ cSad

okf"kZd fjiksVZ 2015-164

iatkc ,.M ÇLk/k cSad¼Òkjr Lkjdkj dk miØe½

Á/kku dk;kZy; % 21 &jktsUæ IysLk] ubZ fnYyh 110008www.psbindia.com

_______________________________________________________________________________________

uksfVl

,rn~ }kjk lwfpr fd;k tkrk gS fd iatkc ,.M Çlèk cSad ds 'ks;jèkkjdksa dh NBoÈ okÆ"kd lkekU; cSBd bafM;k baVjus'kuy lsUVj] 40 & eSDlewyj ekxZ] yksèkh ,LVsV] uà fnYyh &110003 esa eaxyokj] 28 twu 2016 dks çkr% 10-00 cts vk;ksftr dh tk,xhA blesa fuEufyf[kr dkjksckj lapkfyr gksaxs%

en la-1- cSad ds 31 ekpZ 2016 ds ys[kk ijhf{kr rqyu&i=] 31 ekpZ 2016 dk ykHk&gkfu ys[kk] ys[kksa esa lekfgr vofèk esa dk;Zfu"iknu

rFkk dk;Zdykiksa ij funs'kd eaMy dh fjiksVZ vkSj rqyu&i= ,oa ys[kksa ij ys[kk ijh{kdksa dh fjiksVZ ij fopkj&foe'kZ] vuqeksnu o Lohdkj djus gsrqA

2- foÙkh; o"kZ 2015&16 ds fy, 'ks;jksa ij ykHkka'k dk vuqeksnu o ?kks"k.kkA

;g Hkh lwfpr fd;k tkrk gS fd okÆ"kd lkekU; cSBd esa Ã&oksV@oksV nsus ds ik= 'ks;jèkkjdksa ds ukeksa dk irk yxkus ds fy, vafre frfFk¼dV v‚Q MsV½ 21-06-2016 fuèkkZfjr dh gSA ¼d½ okÆ"kd lkekU; cSBd ds flyflys esa 'ks;j&èkkjdksa ds jftLVj rFkk cSad dh 'ks;j varj.k cqd fnukad 22-06-2016 ls 28-06-2016 rd] ftlesa nksuks fnu lfEefyr gSa can jgsxh rFkk ¼[k½ NBoÈ okÆ"kd lkekU; cSBd esa ?kksf"kr vafre ykHkka'k] ;fn dksà gS rks çkIr djus okys 'ks;jèkkjdksa dh ik=rk dk fuèkkZj.k fd;k tk,xkA

funs'kd eaMy ds vkns'kkuqlkj

LFkku % ubZ fnYyh tfrUnjchj flag fnukad % 18 ebZ] 2016 v/;{k ,oa çca/k funs'kd

Punjab & Sind Bank

Annual Report 2015-16 5

Punjab & Sind Bank (A Government of India Undertaking)

Head Office : 21 – RAJENDRA PLACE, NEW DELHI -110008www.psbindia.com

_______________________________________________________________________________________

NOTICE

Notice is hereby given that the Sixth Annual General Meeting of Shareholders of Punjab & Sind Bank will be held on Tuesday, the 28th June, 2016 at 10.00 a.m. at India International Centre, 40-Max Mueller Marg, Lodi Estate, New Delhi-110003 to transact the following business:

Item No.

1. To discuss, approve and adopt the Financial Results viz. Audited Balance Sheet and Profit & Loss Accounts of the Bank for the year ended 31st March 2016, Report of the Board of Directors on the working and activities of the Bank for the period covered by the Accounts and Auditors' Report on the Balance Sheet and Accounts.

2. To approve and declare dividend on Equity Shares for the financial year 2015-16.

Notice is also given that the Bank has fixed 21.06.2016 as the ‘Cut-Off date’ to ascertain names of shareholders who shall be entitled to e-vote / vote at the Annual General Meeting and to receive dividend. Further, the Register of shareholders and the share transfer books of the Bank will remain closed from 22.06.2016 to 28.06.2016 (both days inclusive) in connection with (a) the Annual General Meeting and (b) to determine the entitlement of shareholders to receive dividend declared, if any, at the Sixth AGM.

By Order of the Board of Directors

Place : New Delhi Jatinderbir Singh Date : 18 May, 2016 Chairman & Managing Director

iatkc ,.M fla/ cSad

okf"kZd fjiksVZ 2015-166

fVIif.k;ka

1- ç‚Dlh dh fu;qfä

cSBd esa Hkkx ysus vkSj ernku ds fy, ik= 'ks;j&èkkjd vius LFkku ij cSBd esa Hkkx ysus ,oa er nsus ds fy, ç‚Dlh dh fu;qfä djus gsrq ik= gksxk@gksxh rFkk ç‚Dlh dks cSad dk 'ks;j?kkjd gksuk vfuok;Z ugÈ gSA

iatkc ,.M Çlèk cSad ¼'ks;j o cSBd½ fofu;e] 2008 ds çkoèkkuksa ds vuqlkj iatkc ,.M Çlèk cSad ds fdlh vfèkdkjh ;k deZpkjh dks ç‚Dlh fu;qä ugÈ fd;k tk ldrkA fofu;eksa ds fofu;e 70¼vi½ ds vuqlkj ç‚Dlh dks fn, x, fy[kr }kjk O;fäxr :i ls cSBd esa ernku dk vfèkdkj ugÈ gksxk ftlls fy[kr lacafèkr gSA

ç‚Dlh QkeZ ¼vuqyXud&,½ rHkh çHkkoh gksxk tc og iatkc ,.M Çlèk cSad] çèkku dk;kZy;] ys[kk ,oa ys[kk ijh{kk foHkkx] cSad ds 'ks;j d{k] 21&jktsUæ Iysl] uà fnYyh&110008 esa okÆ"kd lekU; cSBd dh frfFk ls de ls de pkj fnu igys vFkkZr~ fnukad 23-06-2016 ¼o`gLifrokj½ dks lk;a 5 cts vFkok cSad ds dk;Z&?kaVksa ds lekIr gksus ls iwoZ çkIr gks tk,xkA blds lkFk eq[rkjukek ;k vU; vfèkdkj i= ;fn dksà gS] tksfd gLrk{kfjr gS vFkok uksVjh ifCyd ;k eftLVªsV }kjk çekf.kr gS lR;&çfr ds :i esa çLrqr dh tk, c'kZrs ;g eq[krkjukek vFkok vfèkdkj i= iwoZ esa cSad ds ikl tek gS rFkk jftLVMZ gSA

2- vf/k—r çfrfuf/k dh fu;qfDr

iatkc ,.M Çlèk cSad ¼'ks;j o cSBd½ fofu;e] 2008 ds çkoèkkuksa ds vuqlkj iatkc ,.M Çlèk cSad ds fdlh vfèkdkjh ;k deZpkjh dks vfèk—r çfrfufèk ds :i esa fu;qä ugÈ fd;k tk ldrk gSA

dksà Hkh O;fä tks fdlh daiuh ;k fuxfer fudk; tksfd cSad dk 'ks;jèkkjd gS] ds fofèkor~ çfrfufèk ds :i esa cSBd esa Hkkx ysus vFkok oksV nsus ds fy, rc rd ik= ugÈ gksxk tc rd mls ,d ;Fkkfofèk vfèk—r çfrfufèk ds :i esa fu;qä djus lacaèkh ladYi dh ,d çfr ml cSBd ds vè;{k] ftlesa ;g ikfjr fd;k x;k Fkk] }kjk çekf.kr fd;k x;k gks] cSBd dh rkjh[k ls 4 fnu iwoZ vFkkZr~ 23-06-2016 ¼o`gLifrokj½ dks lk;a 5 cts ;k blls igys iatkc ,.M Çlèk cSad] çèkku dk;kZy;] ys[kk ,oa ys[kk ijh{kk foHkkx] cSad ds 'ks;j d{k] 21&jktsUæ Iysl] uà fnYyh&110008 esa çkIr gks tkuk pkfg,A

3- iathdj.k] mifLFkfr iphZ rFkk ços'k iphZ

'ks;jèkkjdksa dks cSBd esa Hkkx ysus dh lqfoèkk çnku djus gsrq fnukad 28-06-2016 dks çkr% 9-00 cts iathdj.k cSBd LFky ij vkjaHk gksxhA 'ks;jèkkjdksa dks iathdj.k vkSipkfjdrkvksa dks iw.kZ djus gsrq cSBd esa le; ls igys mifLFkr gksus dk vuqjksèk gSA

'ks;jèkkjdksa dh lqfoèkk gsrq bl uksfVl ds lkFk mifLFkfr ipÊ rFkk mifLFkfr ikl ¼vuqcaèk ^ch*½ esa layXu gSA 'ks;jèkkjdksa@ç‚Dlh èkkjdksa@vfèk—r çfrfufèk;ksa ls vuqjksèk gS fd mifLFkfr ipÊ Hkj dj] mlesa n'kkZ, x, LFkku ij vius gLrk{kj dj] bls cSBd LFky ij lkSi nsa blds i'pkr gh mUgsa ços'k ipÊ tkjh dh tk,A 'ks;jèkkjd ds ç‚Dlh@vfèk—r çfrfufèk tSlh Hkh fLFkfr gks ç‚Dlh@vfèk—r çfrfufèk mifLFkfr ipÊ ij ç‚Dlh ;k vfèk—r çfrfufèk tks Hkh fLFkfr gks vafdr djsxkA 'ks;jèkkjdksa@ç‚Dlh&èkkjdksa@çkfèk—r çfrfufèk;ksa dks lwfpr fd;k tkrk gS fd cSBd esa ços'k dk vfèkdkj lR;kiu@tkap] tSlk Hkh vko';d le>k tk,xk] ds i'pkr gksxk] vkSj mudks oSèk igpku tSls ernkrk igpku i=@fu;ksDrk igpku i=@iSu dkMZ@ikliksVZ@MªkbÇox ykblsal vkfn dks lkFk esa ykus dh lykg nh tkrh gSA ços'k ikl dks çLrqr djus ij pquko ds fy, eri= tkjh fd;k tk,xkA

4- 'ks;j varj.k ,tsUVksa ds lkFk i=&O;ogkj

'ks;jèkkjd] ftuds ikl 'ks;j HkkSfrd fLFkfr esa gSa] ls muds Ã&esy irs] Mkd irs] cSad fooj.k vkfn esa gq, ifjorZuksa] ;fn dksà gS rks] ÃysDVª‚fud eksM ls lHkh tkudkjh çkIr djus ds fy, mldh lwpuk cSd ds 'ks;j varj.k ,tsaV dks fuEu irs ij nh tk,%

fyad buVkbe bafM;k çk-fy- ;wfuV&iatkc ,.M fla/k cSad] 44] dEI;qfuVh lsUVj] nwljh eafty] ukjk;.kk vkS|ksfxd {ks=] Qst&I utnhd ih-oh-vkj- ukjk;.kk] ubZ fnYyh&110 028- Qksu 011 41410592] 41410593 bZ&esy% [email protected]

'ks;jèkkjd ftuds ikl 'ks;j vHkkSfrd :i esa gSa] ls vuqjksèk gS fd os vius bZ&esy irs] Mkd irs] cSad fooj.k esa ifjorZu@vn~;ru ;fn gks rks] vius fMi‚ft+V‚jh lgHkkxh dks lkjk laçs"k.k bySDVª‚fud ekè;e ls çkIr djus ds fy, lwfpr djsaA

Punjab & Sind Bank

Annual Report 2015-16 7

NOTES1. APPOINTMENT OF PROXY: A Shareholder entitled to attend and vote at the meeting is entitled to appoint a proxy to attend and vote instead of

himself/herself and such proxy need not be a shareholder of the Bank. No person shall be appointed as a proxy who is an officer or employee of Punjab & Sind Bank as per provisions of Punjab

& Sind Bank (Shares and Meetings) Regulations, 2008. As per the regulation 70 (vi) of Regulations, the grantor of an instrument of proxy shall not be entitled to vote in person at the meeting to which such instrument relates.

The Proxy Form (Annexure-‘A’) in order to be effective must be received at Punjab & Sind Bank, Head Office Accounts & Audit Department, Shares Cell, 21-Rajendra Place, New Delhi-110 008, at least four days before the date of the Annual General Meeting i.e. on or before the closing hours of the Bank at 5.00 p.m. on 23.06.2016 (Thursday) together with the Power of Attorney or other authority, if any, under which it is signed or a copy of that Power of Attorney or other authority certified as a true copy by a Notary Public or a Magistrate unless such Power of Attorney or other authority has been previously deposited and registered with the Bank.

2. APPOINTMENT OF AN AUTHORISED REPRESENTATIVE : No person shall be appointed as authorised representative who is an officer or employee of Punjab & Sind Bank as per

provisions of Punjab & Sind Bank (Shares and Meetings) Regulations, 2008. No person shall be entitled to attend or vote at the meeting as a duly authorized representative of a company or any other

Body Corporate which is a shareholder of the Bank, unless a copy of the Resolution appointing him/her as a duly authorized representative, certified to be true copy by the Chairman of the meeting at which it was passed, shall have been received at Punjab & Sind Bank, Head Office Accounts & Audit Department, Shares Cell, 21-Rajendra Place, New Delhi-110 008, at least four days before the date of the Annual General Meeting, i.e. on or before the closing hours of the Bank at 5.00 p.m. on 23.06.2016 (Thursday).

3. REGISTRATION, ATTENDENCE SLIP AND ENTRY SLIP: In order to facilitate the shareholders attending the meeting, Registration process will commence from 9.00 a.m. on

28.06.2016, at the venue. Shareholders are requested to be present for the meeting well in advance, to complete the Registration formalities.

For the convenience of the shareholders, attendance slip and entry pass is annexed (Annexure-‘B’) to this notice. Shareholders/Proxy Holders/Authorised Representatives are requested to fill in, affix their signatures at the space provided therein and surrender the same at the venue and thereafter entry slip shall be issued to them. Proxy/Authorised Representative of a shareholder should state on the attendance slip as ‘Proxy' or ‘Authorised Representative' as the case may be. Shareholders / Proxy holders / Authorised Representatives may note that the admission to the meeting will be subject to verification / checks, as may be deemed necessary and they are advised to carry valid proof of identity viz., Voters ID Card / Employer Identity Card / Pan Card / Passport / Driving license etc. Ballot paper for poll will be issued against surrendering of entry pass.

4. COMMUNICATION WITH THE SHARE TRANSFER AGENT: Shareholders holding shares in physical form are requested to intimate changes/update, if any, in their email address,

postal address, bank details etc. to Share Transfer Agent of the Bank at the following address to receive all communication through electronic mode:

Link Intime India Pvt Ltd. Unit: Punjab & Sind Bank 44, Community Centre, 2nd Floor, Naraina Industrial Area, Phase-I, Near PVR Naraina, NEW DELHI-110 028. Ph: 011 41410592, 41410593 email: [email protected] Shareholders holding shares in dematerialised form are requested to intimate changes/ update, if any, in their email address,

postal address, bank details etc. to their depository participants, to receive all communication through electronic mode.

iatkc ,.M fla/ cSad

okf"kZd fjiksVZ 2015-168

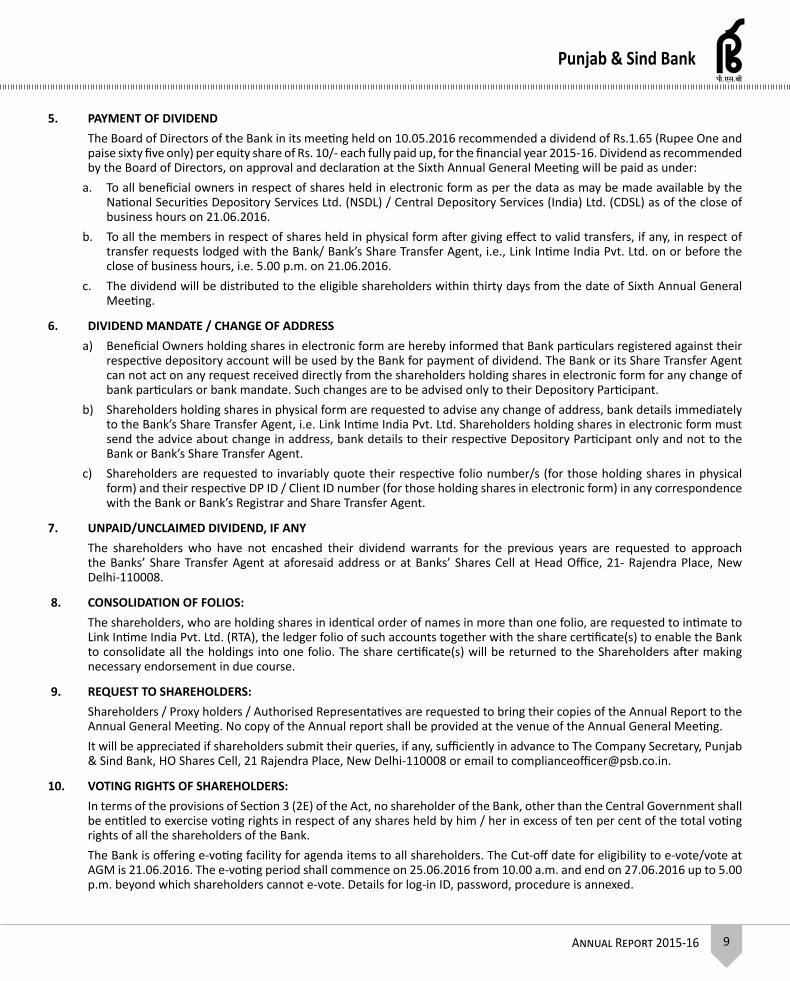

5- ykHkka'k dk Hkqxrku

cSad ds funs'kd e.My usa viuh fnukad 10-05-2016 dks vk;ksftr cSBd esa foÙkh; o"kZ 2015&16 ds fy, çR;sd 10@& #i, ds bfDoVh 'ks;j ds fy, vafre ykHkka'k 1-65 #i, ¼,d #i, vkSj iSalB iSls½ dh vuq'kalk dhA funs'kd e.My }kjk laLrqfr rFkk NBoÈ lkekU; cSBd ds vuqeksfnr ykHkka'k dk Hkqxrku fuEukuqlkj fd;k tk,xk%

d- fnukad 21-06-2016 dks dkjksckj le; dh lekfIr ij us'kuy flD;ksfjVht+ fMiksft+Vjh fyfeVsM¼,u,lMh,y½ vkSj lsUVªy fMiksftVjh lÆolst¼bafM;k½ fy-¼lhMh,l,y½ }kjk miyCèk djk, x, vkadM+ksa ds vuqlkj bysDVª‚fud #i esa èkkfjr 'ks;jksa ds lHkh ykHkkFkÊ Lokfe;ksa dksA

[k- fnukad 21-06-2016 ds dk;Zdky dh lekfIr vFkkZr~ 5-00 cts rd ;k mlls igys cSad@ cSad ds jftLVªkj vkSj 'ks;j gLrkarj.k ,tsaV vFkkZr~ Çyd buVkÃe bafM;k çk-fy- ds ikl ntZ 'ks;j gLrkarj.k vuqjksèk ds lacaèk esa oSèk gLrkarj.k çHkkoh djus ds i'pkr~ HkkSfrd :i esa èkkfjr 'ks;jksa ds lacaèk esa lHkh lnL;ksa dksA

x- NBoÈ okÆ"kd lkekU; cSBd dh frfFk ls 30 fnu ds vanj ik= 'ks;jèkkjdksa dks ykHkka'k forfjr fd;k tk,xkA

6- ykHkka'k vf/kns'k@Mkd irs esa ifjorZu

d- bySDVª‚fud :i esa j[ks x, ykHkkFkÊ 'ks;jèkkjdksa dks ,rn~ }kjk lwfpr fd;k tkrk gS fd muds lacafèkr fMiksftVjh [kkrs esa iath—r cSad fooj.kksa dks cSad }kjk ykHkka'k dk Hkqxrku djus ds fy, mi;ksx esa yk;k tk,xkA cSad vFkok bldk jftLVj ,oa 'ks;j gLrkarj.k ,tsaV] bySDVª‚fud :i esa 'ks;j j[kus okys lnL;ksa ls lhèks gh çkIr ,sls fdlh vuqjksèk ij dkjZokà ugÈ djsxk tks cSad fooj.kksa vFkok cSad vfèkns'k ls lacafèkr gksaxsA ,sls ifjorZuksa dh lwpuk dsoy muds fMi‚ftVjh lgHkkxh dks gh nh tkuh pkfg,A

[k- HkkSfrd :i ls 'ks;j j[kus okys lnL;ksa ls vuqjksèk gS fd ;fn muds irs rFkk cSad fooj.k esa dksà ifjorZu gks] rks bldh lwpuk rRdky cSad ds jftLVªkj vkSj 'ks;j gLrkarj.k ,tsaV vFkkZr Çyd buVkÃe bafM;k çk-fy- dks nsaA bySDVª‚fud :i esa 'ks;j j[kus okys lnL;ksa dks vius irs esa fdlh çdkj ds ifjorZu dh lwpuk vo'; gh vius lacafèkr lgHkkxh fMiksftVjh dks nsuh pkfg,A cSad vFkok cSad ds jftLVªkj ,o 'ks;j gLrkarj.k ,tsaV dks lwpuk nsus dh vko';drk ugÈ gSA

x- lnL;ksa ls vuqjksèk gS fd os cSad vFkok cSad ds jftLVªkj ,o 'ks;j gLrkarj.k ,tsaV ds lkFk fdlh Hkh çdkj ds i= O;ogkj esa vius lacafèkr Qksfy;ks uacj¼muds fy, ftuds ikl 'ks;j HkkSfrd :i esa gS½ vkSj viuk Mhih vkÃMh@xzkgd vkÃMh uacj ¼muds fy, ftuds ikl 'ks;j bySDVª‚fud :i esa gSa½ dk vo'; mYys[k djsaA

7- viznRr@nkok u fd, x, ykHkka'k] ;fn dksbZ gks

ftu 'ks;jèkkjdksa us vius fiNys ykHkka'k okjaVksa dk udnhdj.k ugÈ fy;k gS os cSad ds 'ks;j varj.k ,tsaV ls n'kkZ, x, irs ij ;k 21] jktsaæ Iysl] uà fnYyhs&110 008 esa cSad ds 'ks;j d{k ls laidZ djsaA

8- Qksfy;ksa dk lesdu

ftu 'ks;jèkkjdksa ds ikl ,d ls vfèkd [kkrksa esa vius le:i uke ls 'ks;j gSa] muls vuqjksèk gS fd os Çyd buVkÃe bafM;k çk-fy- ¼vkj-Vh-,-½ dks 'ks;j çek.k&i=ksa ds lkFk ,sls [kkrksa ds ystj Qksfy;ks ds lkFk lwfpr djsa rkfd cSad ,d [kkrs es lHkh èkkfjr 'ks;jksa dk lesdu djus esa l{ke gks ldsA i`"Bkadu lacaèkh vko';d dkjZokà djus ds ckn] lnL;ksa ds 'ks;j çek.k&i= ;Fkk le; ykSVk fn, tk,axsA

9- 'ks;j /kkjdksa ls vuqjks/k

'ks;jèkkjdksa@ç‚Dlh èkkjdksa@çkfèk—r çfrfufèk;ksa ls vuqjksèk gS fd os okÆ"kd lkekU; cSBd esa okÆ"kd fjiksVZ dh viuh çfr lkFk ysdj vk,A okÆ"kd lkekU; cSBd esa okÆ"kd fjiksVZ dh dksà çfr forfjr ugÈ dh tk,xhA

;g ç'kaluh; gksxk fd 'ks;jèkkjd vius ç'u] ;fn dksà gSa] le; ls i;kZIr igys daiuh lfpo] iatkc ,.M Çlèk cSad] ç-dk- 'ks;j d{k] 21] jktsaæ Iysl] uà fnYyh&110008 ds ikl çsf"kr djs ;k [email protected] ij esy djsA

10- 'ks;j /kkjdksa ds erkf/kdkj

vfèkfu;e dh èkkjk 3¼2ý esa fn, x, çkoèkkuksa dh 'krks± ds vuqlkj dsaUæ ljdkj ds vykok] cSad dk dksà Hkh 'ks;jèkkjd vius }kjk èkkjd 'ks;j] cSad ds lHkh 'ks;j èkkjdksa ds dqy erkfèkdkj dk 10 çfr'kr ls vfèkd 'ks;j j[krk gS rks og erkfèkdkj dk ik= ugÈ gksxkA

cSad lHkh 'ks;jèkkjdksa dks ,tsaMk enksa ds fy, Ã&oksÇVx dh lqfoèkk çnku dj jgk gSA ok-lk-cS- dh Ã&oksV] oksV dh ik=rk dh vafre fnukad¼dV v‚Q MsV½ 21-06-2016 gSA Ã&oksÇVx dh vofèk 25-06-2016 dks iwokZà 10-00 cts çkjaHk gksxh vkSj 27-06-2016 dks vijkà 5-00 cts rd gksxhA blds i'pkr Ã&oksV ugÈ dh tk ldsxhA y‚xbu vkÃMh] ikloMZ] i|fr vuqcaèk esa nh xà gSA

Punjab & Sind Bank

Annual Report 2015-16 9

5. PAYMENT OF DIVIDEND The Board of Directors of the Bank in its meeting held on 10.05.2016 recommended a dividend of Rs.1.65 (Rupee One and

paise sixty five only) per equity share of Rs. 10/- each fully paid up, for the financial year 2015-16. Dividend as recommended by the Board of Directors, on approval and declaration at the Sixth Annual General Meeting will be paid as under:

a. To all beneficial owners in respect of shares held in electronic form as per the data as may be made available by the National Securities Depository Services Ltd. (NSDL) / Central Depository Services (India) Ltd. (CDSL) as of the close of business hours on 21.06.2016.

b. To all the members in respect of shares held in physical form after giving effect to valid transfers, if any, in respect of transfer requests lodged with the Bank/ Bank’s Share Transfer Agent, i.e., Link Intime India Pvt. Ltd. on or before the close of business hours, i.e. 5.00 p.m. on 21.06.2016.

c. The dividend will be distributed to the eligible shareholders within thirty days from the date of Sixth Annual General Meeting.

6. DIVIDEND MANDATE / CHANGE OF ADDRESSa) Beneficial Owners holding shares in electronic form are hereby informed that Bank particulars registered against their

respective depository account will be used by the Bank for payment of dividend. The Bank or its Share Transfer Agent can not act on any request received directly from the shareholders holding shares in electronic form for any change of bank particulars or bank mandate. Such changes are to be advised only to their Depository Participant.

b) Shareholders holding shares in physical form are requested to advise any change of address, bank details immediately to the Bank’s Share Transfer Agent, i.e. Link Intime India Pvt. Ltd. Shareholders holding shares in electronic form must send the advice about change in address, bank details to their respective Depository Participant only and not to the Bank or Bank’s Share Transfer Agent.

c) Shareholders are requested to invariably quote their respective folio number/s (for those holding shares in physical form) and their respective DP ID / Client ID number (for those holding shares in electronic form) in any correspondence with the Bank or Bank’s Registrar and Share Transfer Agent.

7. UNPAID/UNCLAIMED DIVIDEND, IF ANY The shareholders who have not encashed their dividend warrants for the previous years are requested to approach

the Banks’ Share Transfer Agent at aforesaid address or at Banks’ Shares Cell at Head Office, 21- Rajendra Place, New Delhi-110008.

8. CONSOLIDATION OF FOLIOS: The shareholders, who are holding shares in identical order of names in more than one folio, are requested to intimate to

Link Intime India Pvt. Ltd. (RTA), the ledger folio of such accounts together with the share certificate(s) to enable the Bank to consolidate all the holdings into one folio. The share certificate(s) will be returned to the Shareholders after making necessary endorsement in due course.

9. REQUEST TO SHAREHOLDERS: Shareholders / Proxy holders / Authorised Representatives are requested to bring their copies of the Annual Report to the

Annual General Meeting. No copy of the Annual report shall be provided at the venue of the Annual General Meeting. It will be appreciated if shareholders submit their queries, if any, sufficiently in advance to The Company Secretary, Punjab

& Sind Bank, HO Shares Cell, 21 Rajendra Place, New Delhi-110008 or email to [email protected].

10. VOTING RIGHTS OF SHAREHOLDERS: In terms of the provisions of Section 3 (2E) of the Act, no shareholder of the Bank, other than the Central Government shall

be entitled to exercise voting rights in respect of any shares held by him / her in excess of ten per cent of the total voting rights of all the shareholders of the Bank.

The Bank is offering e-voting facility for agenda items to all shareholders. The Cut-off date for eligibility to e-vote/vote at AGM is 21.06.2016. The e-voting period shall commence on 25.06.2016 from 10.00 a.m. and end on 27.06.2016 up to 5.00 p.m. beyond which shareholders cannot e-vote. Details for log-in ID, password, procedure is annexed.

iatkc ,.M fla/ cSad

okf"kZd fjiksVZ 2015-1610

ftu 'ks;jèkkjdksa us Ã&oksV fd;k gS okÆ"kd lkekU; cSBd esa Hkkx ys ldrs gSa Çdrq ernku esa Hkkx ugÈ ys ldrsA ;fn mUgksaus ernku ds ekè;e ls er dk ç;ksx fd;k rks ml ij fopkj ugÈ fd;k tk,xkA

11- 'ks;j d{k

'ks;jèkkjdksa dks rhoz ,oa çHkkoh lsok çnku djus ds fy, cSad us çèkku dk;kZy; esa 'ks;j d{k dh LFkkiuk dh gSA 'ks;j/kkjd fuEu irs ij fdlh çdkj dh lgk;rk ds fy, laidZ dj ldrs gSa&

daiuh lfpo] iatkc ,.M fla/k cSad] ç/kku dk;kZy;] ys[kk ,oa ys[kk ijh{kk foHkkx ¼'ks;j d{k½ 21&jktsUæ Iysl] izFke ry] ubZ fnYyh&110008 VsfyQksu % 011&25782926] 25812922

bZ&esy : [email protected]

12- vU; tkudkjh

'ks;jèkkjd —i;k tku ysa fd lHkk esa fdlh Hkh çdkj dk migkj@migkj dwiu ugÈ fn;k tk,xkA

dM+h lqj{kk ds dkj.kksa ls gky ds Hkhrj czhQ dsl] [kk| inkFkZ rFkk futh oLrq,a ys tkuk euk gSA blfy, cSBd esa mifLFkr gksus okys lHkh O;fä vius lkeku dh lqj{kk dh O;oLFkk Lo;a djsaA

funs'kd eaMy ds vkns'kkuqlkj

LFkku % ubZ fnYyh tfrUnjchj flagfnukad % 18 ebZ] 2016 v/;{k ,oa Áca/k funs'kd

Punjab & Sind Bank

Annual Report 2015-16 11

The shareholders who have e-voted can participate in the AGM but cannot participate in poll. Incase they vote through poll, the same will not be considered.

11. SHARES CELL In order to facilitate quick and efficient service to the shareholders, the Bank has set up a Shares cell at its Head Office, New

Delhi, Shareholders may contact this Cell at the under mentioned address for any assistance : The Company Secretary, Punjab & Sind Bank, Head Office, Accounts & Audit Department (Shares Cell) 21 Rajendra Place, 1st floor, New Delhi-110008 Telephone: 011-25782926, 25812922 E-mail: [email protected].

12. OTHER INFORMATION Shareholders may kindly note that no gift/gift coupons will be distributed at the meeting. Due to strict security reasons, brief cases, eatables and other belongings are not allowed inside the hall. Persons attending

the meeting are, therefore, advised to make their own arrangements for the safe keeping of their articles.

By Order of the Board of Directors

Place : New Delhi Jatinderbir Singh Date : 18 May, 2016 Chairman & Managing Director

iatkc ,.M fla/ cSad

okf"kZd fjiksVZ 2015-1612

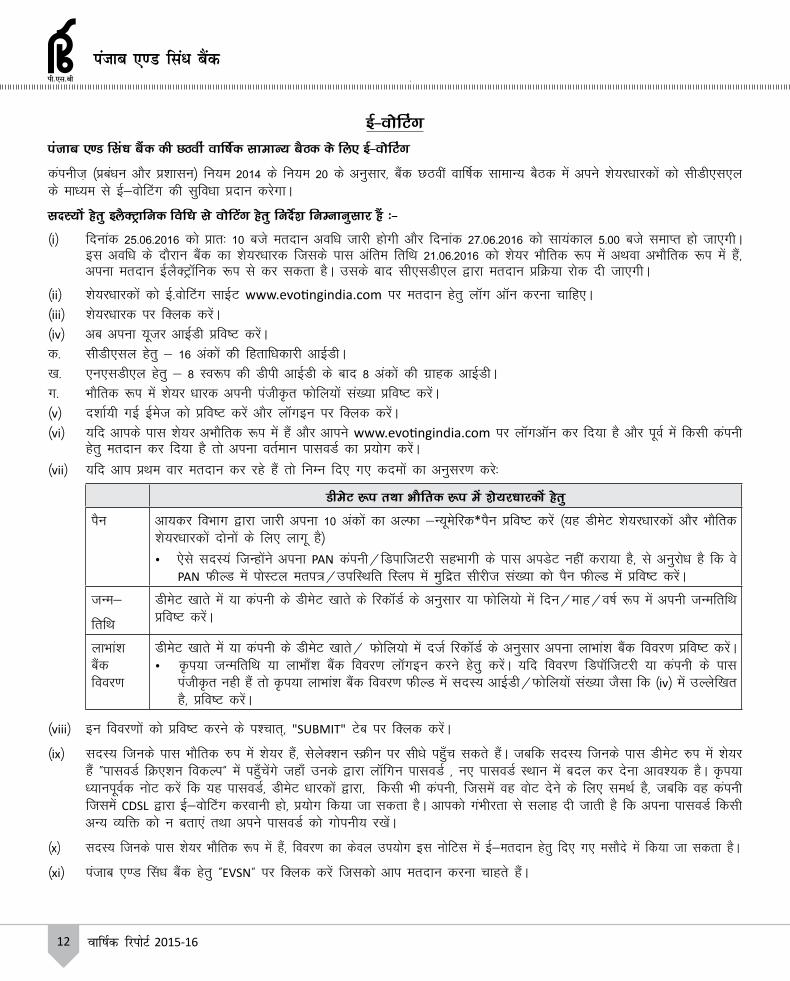

bZ&oksfVaxiatkc ,.M fla/k cSad dh NBoha okf"kZd lkekU; cSBd ds fy, bZ&oksfVax

daiuht+ ¼çcaèku vkSj ç'kklu½ fu;e 2014 ds fu;e 20 ds vuqlkj] cSad NBoÈ okÆ"kd lkekU; cSBd esa vius 'ks;jèkkjdksa dks lhMh,l,y ds ekè;e ls Ã&oksÇVx dh lqfoèkk çnku djsxkA

lnL;ksa gsrq bySDVªkfud fofèk ls oksÇVx gsrq funsZ'k fuEukuqlkj gSa %&

¼i½ fnukad 25-06-2016 dks çkr% 10 cts ernku vofèk tkjh gksxh vkSj fnukad 27-06-2016 dks lk;adky 5-00 cts lekIr gks tk,xhA bl vofèk ds nkSjku cSad dk 'ks;jèkkjd ftlds ikl vafre frfFk 21-06-2016 dks 'ks;j HkkSfrd :i esa vFkok vHkkSfrd :i esa gSa] viuk ernku ÃySDVª‚fud :i ls dj ldrk gSA mlds ckn lh,lMh,y }kjk ernku çfØ;k jksd nh tk,xhA

¼ii½ 'ks;jèkkjdksa dks Ã-oksÇVx lkÃV www.evotingindia.com ij ernku gsrq y‚x v‚u djuk pkfg,A¼iii½ 'ks;jèkkjd ij fDyd djsaA¼iv½ vc viuk ;wtj vkbZMh çfo"V djsaA d- lhMh,ly gsrq & 16 vadksa dh fgrkfèkdkjh vkÃMhA[k- ,u,lMh,y gsrq & 8 Lo:i dh Mhih vkÃMh ds ckn 8 vadksa dh xzkgd vkÃMhAx- HkkSfrd :i esa 'ks;j èkkjd viuh iath—r Qksfy;ksa la[;k çfo"V djsaA¼v½ n'kkZ;h xà Ãest dks çfo"V djsa vkSj y‚xbu ij fDyd djsaA¼vi½ ;fn vkids ikl 'ks;j vHkkSfrd :i esa gSa vkSj vkius www.evotingindia.com ij y‚xv‚u dj fn;k gS vkSj iwoZ esa fdlh daiuh

gsrq ernku dj fn;k gS rks viuk orZeku ikloMZ dk ç;ksx djsaA

¼vii½ ;fn vki çFke okj ernku dj jgs gSa rks fuEu fn, x, dneksa dk vuqlj.k djs%

MhesV :i rFkk HkkSfrd :i esa 'ks;j/kkjdksa gsrq

iSu vk;dj foHkkx }kjk tkjh viuk 10 vadksa dk vYQk &U;wesfjd*iSu çfo"V djsa ¼;g MhesV 'ks;jèkkjdksa vkSj HkkSfrd 'ks;jèkkjdksa nksuksa ds fy, ykxw gS½

Û ,sls lnL;a ftUgksaus viuk PAN daiuh@fMikftVjh lgHkkxh ds ikl viMsV ugÈ djk;k gS] ls vuqjksèk gS fd os PAN QhYM esa iksLVy eri=@mifLFkfr fLyi esa eqfnzr lhjht la[;k dks iSu QhYM esa çfo"V djsaA

tUe&

frfFk

MhesV [kkrs esa ;k daiuh ds MhesV [kkrs ds fjd‚MZ ds vuqlkj ;k Qksfy;ks esa fnu@ekg@o"kZ :i esa viuh tUefrfFk çfo"V djsaA

ykHkka'k cSad fooj.k

MhesV [kkrs esa ;k daiuh ds MhesV [kkrs@ Qksfy;ks esa ntZ fjd‚MZ ds vuqlkj viuk ykHkka'k cSad fooj.k çfo"V djsaAÛ —i;k tUefrfFk ;k ykHkk¡'k cSad fooj.k y‚xbu djus gsrq djsaA ;fn fooj.k fMi‚ftVjh ;k daiuh ds ikl

iath—r ugh gSa rks —i;k ykHkka'k cSad fooj.k QhYM esa lnL; vkÃMh@Qksfy;ksa la[;k tSlk fd ¼iv½ esa mYysf[kr gS] çfo"V djsaA

¼viii½ bu fooj.kksa dks çfo"V djus ds i'pkr~] "SUBMIT" Vsc ij fDyd djsaA

¼ix½ lnL; ftuds ikl HkkSfrd #i esa 'ks;j gSa] lsysD'ku LØhu ij lhèks igq¡p ldrs gSaA tcfd lnL; ftuds ikl MhesV #i esa 'ks;j gSa ÞikloMZ fØ,'ku fodYiß esa igq¡psaxs tgk¡ muds }kjk y‚fxu ikloMZ ] u, ikloMZ LFkku esa cny dj nsuk vko';d gSA —i;k è;kuiwoZd uksV djsa fd ;g ikloMZ] MhesV èkkjdksa }kjk] fdlh Hkh daiuh] ftlesa og oksV nsus ds fy, leFkZ gS] tcfd og daiuh ftlesa CDSL }kjk Ã&oksÇVx djokuh gks] ç;ksx fd;k tk ldrk gSA vkidks xaHkhjrk ls lykg nh tkrh gS fd viuk ikloMZ fdlh vU; O;fä dks u crk,a rFkk vius ikloMZ dks xksiuh; j[ksaA

¼x½ lnL; ftuds ikl 'ks;j HkkSfrd :i esa gSa] fooj.k dk dsoy mi;ksx bl uksfVl esa Ã&ernku gsrq fn, x, elkSns esa fd;k tk ldrk gSA

¼xi½ iatkc ,.M Çlèk cSad gsrq ÞEVSNß ij fDyd djsa ftldks vki ernku djuk pkgrs gSaA

Punjab & Sind Bank

Annual Report 2015-16 13

E-VotingE-Voting for the Sixth Annual General Meeting of Punjab & Sind Bank

In terms of Rule 20 of Companies (Management and Administration) Rules, 2014 as amended from time to time, Bank shall provide facility of e-Voting, through CDSL, to the shareholders for the Sixth AGM.

The instructions for shareholders voting electronically are as under:

(i) The voting period begins on 25.06.2016 at 10.00 a.m. and ends on 27.06.2016 at 5.00 p.m. During this period shareholders’ of the Bank, holding shares either in physical form or in dematerialized form, as on the cut-off date 21.06.2016, may cast their vote electronically. The e-voting module shall be disabled by CDSL for voting thereafter.

(ii) The shareholders should log on to the e-voting website www.evotingindia.com.

(iii) Click on Shareholders.

(iv) Now Enter your User ID

a. For CDSL: 16 digits beneficiary ID,

b. For NSDL: 8 Character DP ID followed by 8 Digits Client ID,

c. Members holding shares in Physical Form should enter Folio Number registered.

(v) Next enter the Image Verification as displayed and Click on Login.

(vi) If you are holding shares in demat form and had logged on to www.evotingindia.com and voted on an earlier voting of any company, then your existing password is to be used.

(vii) If you are a first time user follow the steps given below:

For Members holding shares in Demat Form and Physical FormPAN Enter your 10 digit alpha-numeric PAN issued by Income Tax Department (Applicable for both demat share-

holders as well as physical shareholders)

• Members who have not updated their PAN with the Company/Depository Participant are requested to use the sequence number which is printed on Postal Ballot/Attendance Slip indicated in the PAN field.

DOB Enter the Date of Birth as recorded in your demat account or in the company records for the said demat ac-count or folio in dd/mm/yyyy format.

Dividend Bank Details

Enter the Dividend Bank Details as recorded in your demat account or in the company records for the said demat account or folio.

• Please enter the DOB or Dividend Bank Details in order to login. If the details are not recorded with the depository or company please enter the member id / folio number in the Dividend Bank details field as mentioned in instruction (iv).

(viii) After entering these details appropriately, click on “SUBMIT” tab.

(ix) Members holding shares in physical form will then directly reach the Company selection screen. However, members holding shares in demat form will now reach ‘Password Creation’ menu wherein they are required to mandatorily enter their login password in the new password field. Kindly note that this password is to be also used by the demat holders for voting for resolutions of any other company on which they are eligible to vote, provided that company opts for e-voting through CDSL platform. It is strongly recommended not to share your password with any other person and take utmost care to keep your password confidential.

(x) For Members holding shares in physical form, the details can be used only for e-voting on the resolutions contained in this Notice.

(xi) Click on the EVSN for Punjab & Sind Bank on which you choose to vote.

iatkc ,.M fla/ cSad

okf"kZd fjiksVZ 2015-1614

¼xii½ oksÇVx i`"B ij vki fjtksY;w'ku fooj.k ds le{k gk¡@ugÈ dk fodYi] oksÇVx ds fy, ns[ksaxsA vko';d gk¡ vFkok ugÈ] fodYi dk pquko djsaA gk¡ dk fodYi] çLrko ds çfr vkidh lgefr lwfpr djrk gS rFkk ugÈ dk fodYi] çLrko ds çfr vkidh vlgefr lwfpr djrk gSA

¼xiii½ ;fn vki lHkh çLrkoksa dks ns[kuk pkgrs gSa rc ÞfjtksY;w'ku Qkby Çydß dks fDyd djsaA

¼xiv½ oksV djus ds çLrko dks pquus ds i'pkr SUBMIT ij fDyd djsaA ,d iqf"V c‚Dl ogk fn[ksxk] ;fn vki iqf"V djuk pkgrs gSa rks ÞOKß ij fDyd djsa vkSj ;fn viuk oksV cnyuk pkgrs gSa rks CANCEL ij fDyd djsa vkSj bl çdkj vki viuk oksV cny ldrs gSaA

¼xv½ ;fn vki çLrko ij ,d ckj viuk oksV dj nsrs gSa rc vkidks mls cnyus dh vuqefr ugÈ gksxhA

¼xvi½ vki vius }kjk fd, x, ernku dk ÇçV Hkh ernku i`"B ij ÞÇçV ysus gsrq ;gka fDyd djsaß ij fDyd dj ys ldrs gSaA

¼xvii½ ;fn MhesV [kkrkèkkjd viuk ifjoÆrr ikloMZ Hkwy x;k gS rc ;wtj vkÃMh vkSj Ãest lR;kiu dksM dks çfo"V djsa vkSj Hkwys gq, ikloMZ ij fDyd djsa rFkk ç.kkyh }kjk ekaxs x, fooj.k dks çfo"V djsaA

¼xviii½ voS;fDrd 'ks;jèkkjd rFkk vfHkj{kdksa gsrq uksV

Û voS;fDRkd 'ks;jèkkjd ¼tSls oS;fDrd ls vyx] Çgnw la;qä ifjokj] ,uvkjvkà vkfn½ vkSj vfHkj{kdksa dks www.evotingindia.com y‚xbu djuk gksxk vkSj d‚iksZjsV ds :i esa Lo;a dks iath—r djkuk gksxkA

Û iathdj.k dh LdSu d‚ih ftl ij laLFkk dh eksgj rFkk gLrk{kj gksus pkfg,] dks [email protected] ij Ã&esy dj nsuk pkfg,A

Û y‚xbu fooj.k çkIr gksus ds ckn admin y‚xbu vkSj ikloMZ dk mi;ksx dj vuqikyu ;wtj fØ,V dj ysuk pkfg,A vuqikyu ;wtj [kkrk¼vksa½ dks Çyd djus es leFkZ gksxk ftlds fy, oks ernku djuk pkgrs gSaA

Û lHkh [kkrksa dh lwph [email protected] dks esy dj nsuh pkfg, vkSj [kkrksa dh Loh—fr çkIr gksus ds ckn] oks ernku djus esa leFkZ gksaxsA

Û vfHkj{kd ds i{k esa muds }kjk tkjh i‚oj v‚Q vVkuÊ vkSj cksMZ ladYi dh LdSuM çfr] ;fn dksà gS] dks ihMh,Q çk:i esa ç.kkyh esa viyksM djuk pkfg, rkfd Nkuchu djus okyk mldks lR;kfir dj ldsA

¼xix½ O;fä;ksa ftUgksaus 'ks;j [kjhns gSa vkSj uksfVl dks çsf"kr djus ds ckn Hkh Ã&oksÇVx gsrq mijksä çfØ;k viuk ldrs gSaA

fVIi.kh% ;fn dksà lnL;a¼vksa½ vius oksV nksuksa vFkkZr HkkSfrd :i ;k Ã&oksÇVx ls ernku djrk gS rks Ã&oksÇVx ds ekè;e ls fd;k x;k ernku ekU; jgsxk rFkk HkkSfrd ernku dks vuns[kk dj fn;k tk,xkA ;|fi ftl 'ks;jèkkjd us us Ã&oksÇVx ds ekè;e ls viuk oksV fn;k gS og lkekU; cSBd esa lgHkkfxrk dj ldrk gS Çdrq iksy esa oksV ugÈ dj ldrkA

Jh nhid xqIrk] dk;Zjr daiuh lfpo¼lhoh ua- 4629½ dks bySDVª‚fud oksÇVx çfØ;k ds fy, vads{kd fu;qDr fd;k x;k gS] tks i{k ;k foi{k esa Mkys x, oksVksa dh fjiksVZ rS;kj djsaxs rFkk bls cSBd laiUu gksus ds rhu fnuksa ds Hkhrj vè;{k] okÆ"kd lkekU; cSBd dks lacafèkr fjiksVZ çLrqr djsaxs(

vè;{k }kjk ?kksf"kr ifj.kke ds lkFk vads{kd dh fjiksVZ dks cSad dh osclkbV rFkk lhMh,l,y dh osclkbV ij ifj.kke dh ?kks"k.kk ds rqjar ckn Mky fn;k tk,xk(

i;kZIr oksV dh çkfIr ij ladYi dks okÆ"kd lkekU; cSBd ds fnu ikfjr ekuk tk,xk(

cSBd dh lwpuk www.psbindia.com rFkk www.cdslindia.com ij Hkh çnÆ'kr gSA

;fn Ã&oksÇVx ds lanHkZ esa vkidk dksà ç'u vFkok ftKklk gS rks ckj&ckj iwNs tkus okys ç'u ¼ÞFAQsß½ ij tk,a rFkk lgk;rk vuqHkkx ds varxZr [email protected] ij Ã&oksÇVx esuqvy miyCèk gS ;k [email protected] dks Ã&esy djsa ;k Jh osuflly‚l QqjVsMks ¼Wenceslaus Furtado½] fMIVh çcaèkd] CDSL] 16oka ekyk] ih-ts- V‚oj] nyky LVªhV] QksVZ] eqEcÃ&400001] nwjHkk"k ua- 18002005533 ;k Jh Hkkjr Hkw"k.k] ,lksf'k,V mikè;{k] Çyd ÃuVkbe çk- bafM;k fyfeVsM] 44] dE;wfuVh lsaVj] f}rh; ry] ukjk;.kk vkS|ksfxd {ks=] Qst&1] uà fnYyh&28 nwjHkk"k ua- 011&41410592]41410593 ;k [email protected] dks Ã&esy djsaA

Punjab & Sind Bank

Annual Report 2015-16 15

(xii) On the voting page, you will see “RESOLUTION DESCRIPTION” and against the same the option “YES/NO” for voting. Select the option YES or NO as desired. The option YES implies that you assent to the Resolution and option NO implies that you dissent to the Resolution.

(xiii) Click on the “RESOLUTIONS FILE LINK” if you wish to view the entire Resolution details.

(xiv) After selecting the resolution you have decided to vote on, click on “SUBMIT”. A confirmation box will be displayed. If you wish to confirm your vote, click on “OK”, else to change your vote, click on “CANCEL” and accordingly modify your vote.

(xv) Once you “CONFIRM” your vote on the resolution, you will not be allowed to modify your vote.

(xvi) You can also take print out of the voting done by you by clicking on “Click here to print” option on the Voting page.

(xvii) If Demat account holder has forgotten the changed password then Enter the User ID and the image verification code and click on Forgot Password & enter the details as prompted by the system.

(xviii) Note for Non – Individual Shareholders and Custodians

• Non-Individual shareholders (i.e. other than Individuals, HUF, NRI etc.) and Custodian are required to log on to www.evotingindia.com and register themselves as Corporates.

• A scanned copy of the Registration Form bearing the stamp and sign of the entity should be emailed to [email protected].

• After receiving the login details a compliance user should be created using the admin login and password. The Compliance user would be able to link account(s) for which they wish to vote on.

• The list of accounts should be mailed to [email protected] and on approval of the accounts they would be able to cast their vote.

• A scanned copy of the Board Resolution and Power of Attorney (POA) which they have issued in favour of the Custodian, if any, should be uploaded in PDF format in the system for the scrutinizer to verify the same.

(xix) Person who have acquired shares and become members after despatch of notice may also use the above given procedure for remote e-voting.

Note: In case member(s) cast their vote both via Physical Ballot and e-voting, then voting done through e-voting shall prevail and voting done by Physical Ballot will be ignored. However, shareholder(s) who have casted their vote through e-voting can participate in General Meeting but cannot vote in poll.

Mr. Deepak Gupta, Practicing Company Secretary (CP No. 4629) has been appointed as the scrutinizer to the electronic voting process and for poll at the Annual General Meeting, who shall prepare and submit its report of the votes cast in favour or not in favour/ against, to the Chairman of the Annual General Meeting within 3 days of the conclusion of the meeting;

The results declared along with the scrutinizer’s report shall be placed on the website of the Bank and on the website of CDSL immediately after the result is declared by the Chairman;

Subject to receipt of the sufficient votes, the resolution(s) shall be deemed to be passed on the date of the Annual General Meeting;

Notice of the meeting is also displayed at www.psbindia.com and www.cdslindia.com.

In case you have any queries or issues regarding e-voting, you may refer the Frequently Asked Questions (“FAQs”) and e-voting manual available at www.evotingindia.com under help section or write an email to [email protected] or call Mr. Wenceslaus Furtado, Deputy Manager, CDSL, 16th floor, P.J Tower, Dalal Street, Fort, Mumbai-400001, Phone-18002005533 or Call Mr. Bharat Bhushan, Associate Vice President, Link Intime India Pvt. Ltd, 44-Community Centre, 2nd floor, Naraina Indl Area, Phase-I, New Delhi-28 Phone-41410592, 41410593 or write an email to [email protected].

iatkc ,.M fla/ cSad

okf"kZd fjiksVZ 2015-1616

funs'kd eaMy fjiksVZ 2015&16funs'kd eaMy fnukad 31 ekpZ] 2016 dks lekIr o"kZ dh okÆ"kd fjiksVZ] rqyu&i= rFkk ykHk&gkfu [kkrs dks g"kZ ds lkFk çLrqr djrk gSAçcaèku fopkj& foe'kZ ,oa fo'ys"k.k vkÆFkd ifj–';%,d o"kZ igys tc vkÆFkd losZ{k.k vkSj ctV çLrqr fd;k x;k Fkk] Hkkjrh; vFkZO;oLFkk o`gr vkÆFkd LFkkf;Ro dks cgky djus esa çkIr ykHkksa dks lesfdr djus esa lQy gqà gSA bl dfBu nkSj esa Hkkjr o`gr LFkkf;Ro dk vkJ; cuk gqvk gS ftlesa eqækLQhfr] jktdks"kh; ?kkVk vkSj pkyw [kkrk ?kkVk lHkh {kh.k gks x, gSaA gkykafd ?kVrh&c<rh xfr ls vkÆFkd o`f) cgky gksrs fn[kkà ns jgh gS] vkSj 2014&2015 ds 7-2% dh rqyuk esa vkÆFkd fodkl dh nj 7-6% gksus dh laHkkouk gSA fiNys o"kZ dh rqyuk esa —f"k {ks= esa csgrj ifj.kke dh laHkkouk gS vkSj 2015&2016 esa 1-7% dh o`f) fjd‚MZ dh tkus dh vk'kk gSA m|ksx us çkFkfed #i ls fofuekZ.k esa egRoiw.kZ fodkl çnÆ'kr fd;k gS vkSj o"kZ 2015&2016 esa vkÃvkÃih ds fy, var%o`f) dh Hkfo";ok.kh 4-3% dh xà gSA bl nkSjku lsok {ks= esa rsth ls foLrkj gks jgk gSaA o"kZ 2015&2016 ds fy, lhihvkà vkèkkfjr eqækLQhfr fu;a=.k ds lkFk 5-00% ds Hkhrj jgus dh Hkfo";ok.kh dh xà gS vkSj Fkksd ewY; lwpdkad ¼WPI½ vkèkkfjr eqækLQhfr uoacj 2014 ls udjkRed {ks= ¼&1-8%½ esa jgh gSA o"kZ 2014&2015 dh 4-2% dh thMhih dh rqyuk esa o"kZ 2015&2016 esa jktdks"kh; ?kkVk thMhih ds 4-00% rd fxjus dh laHkkouk gSA ewY; fLFkjrk esa Hkjkslk c<k gS ,oa lksuk vk;kr o`gÙk#i ls fLFkj gqvk gSA pkyw [kkrs ds ?kkVs esa deh vk;h gS vkSj fons'kh eqæk Hk.Mkj us yxHkx 350 fcfy;u ;w,l M‚yj ds vius loksZPp Lrj dks Nw fy;k gSA o"kZ 2014&2015 ds vçSy& fnlacj ds 21-9 fcfy;u M‚yj dh rqyuk esa ,QMhvkà varokZg o"kZ 2015&2016 esa mlh vofèk esa c<dj 27-7 fcfy;u M‚yj gks x;k gSA vkÃ,e,Q us gekjs ns'k dks lqLr oSfÜod vFkZO;oLFkk ds chp esa ,d ^czkÃV Li‚V* crk;k gSA nks o"kZ dh ekulwu esa 13% dh de ckfj'k gksus rFkk oSfÜod çfrdwy n'kk ds ckotwn] ;g lao`f) çkIr dh xà gSA ;|fi] Hkfo"; esa bl lao`f) ds lEeq[k dà pqukSfr;ka gSA oSfÜod eanh ds vkus okys tksf[ke vkSj leL;k,a] Hkfo"; esa oLrqvksa dh dherksa esa mrkj&p<+ko] fo'ks"kr;k rsy] lkrosa osru vk;ksx dk vfrfjä jktdks"kh; Hkkj ds vfrfjä fodflr ds lkFk&lkFk fodkl'khy ns'kksa dks vFkZO;oLFkk dh {kerk ds vuqlkj fQj ls dqy ekax ds lekuqikr fuos'k vkjaHk djuk gksxkA ;|fi] Hkkjr ljdkj] Hkkjrh; fjtoZ cSad vkSj vU; lacafèkr ,tsafl;ka bu leL;kvksa ds lekèkku gsrq leqfpr mik; dj jgs gSaA Hkkjr esa cSaÇdx {ks= ds lkFk&lkFk gekjk cSad Hkh mUufr dj jgk gSA ;|fi] gekjs lkeus dqN eq[; leL;k,a gSa vkSj vkfLr xq.koÙkk cSad ds lkeus ,d xEHkhj leL;k gSA tek ykxr esa deh vkSj vkfLr;ksa ij çfrQy esa lqèkkj] ,uvkÃ,e esa o`f) dh pqukSrh ds lkFk iwath i;kZIrrk] ykHkçnrk ncko esa gSA pqukSfr;ksa dk lkeuk djus gsrq fofHkUu Lrjksa ij dà rjg ds mik; fd, jgs gSaA

dk;Z&fu"iknu ifj.kkedqy O;kikjfnukad 31-03-2015 dks cSad ds #- 151511 djksM+ dh rqyuk esa o"kZ 31-03-2016 dh lekfIr ij cSad ds dqy O;kikj esa 3-31% dh o`f) ntZ dh xà tksfd #-156527 djksM+ jgkAykHkfoÙkh; o"kZ 2014&2015 ds nkSjku #- 121-35 djksM+ dh rqyuk esa cSad us o"kZ 2015&2016 ds nkSjku #- 335-97 djksM+ dk 'kq) ykHk ntZ fd;kA o"kZ 2014&15 ds 0-13% dh rqyuk esa vkfLr;ksa ij çfrQy 0-34% jgkA

31 ekpZ] 2016 d¨ LkekIr o"kZ ds ifj.kke a dh Áeq[k ckrsajkf”k yk[kksa esa

LkekIr o"kZ Áfr'kr esa ifjorZu31-03-2016 31-03-2015

C;kt dh vk; 874434 858855 1-81vU; vk; 47848 42875 11-60dqy vk; 922282 901730 2-28dqy O;; 795293 824185 &3-51ifjpkyu ykHk 126989 77545 63-76'kq) ykHk 33597 12135 176-86vkfLr;ksa ij çfrQy 0-34% 0-13%'kq) C;kt ekÆtu ¼,u-vkÃ-,e-½ 2-22% 1-80%ldy vutZd vkfLr;ka 6-48% 4-76%'kq) vutZd 4-62% 3-55%iwath i;kZIrrk vuqikr ¼cklsy II½ 11-75% 11-88%iwath i;kZIrrk vuqikr ¼cklsy III½ 10-91% 11-24%çfr 'ks;j vk; ¼#-½ 8-39 3-59

Punjab & Sind Bank

Annual Report 2015-16 17

DIRECTORS’ REPORT 2015-16The Board of Directors has pleasure in presenting the Annual Report of the Bank along with the Balance Sheet & Profit and Loss Account for the year ended 31st March, 2016.MANAGEMENT DISCUSSION AND ANALYSIS:ECONOMIC OUTLOOKSince the Economic Survey and Budget were presented a year ago, the Indian economy has continued to consolidate the gains achieved in restoring macroeconomic stability. Inflation, the fiscal deficit, and the current account deficit have all declined, rendering India a relative haven of macro stability in these turbulent times. Economic growth appears to be recovering, albeit at varying speeds across sectors and the growth of Economy expected having accelerated to 7.6% as against 7.2% in 2014-15. Agriculture is likely to perform better than last year and expected to record a growth of 1.7% in 2015-16. Industry has shown significant improvement primarily on account of acceleration in manufacturing and the median growth forecast for IIP has been put at 4.3% for 2015-16. Meanwhile, services continue to expand rapidly. The CPI based Inflation remains under control with a median forecast of 5.0% for 2015-16 and the Wholesale Price Index (WPI) based inflation has been put at (-1.8%), remaining in Negative territory since November 2014. The fiscal deficit has been expected to decline from 4.2% of GDP in 2014-15 to 4% of GDP in 2015-16. Confidence in price stability has improved, gold imports have largely stabilized. The current account deficit has declined and Foreign Exchange reserves touched highest ever level of about 350 billion US Dollars. FDI inflows have grown from 21.9 billion dollar in April-December 2014-15 to 27.7 billion dollar to the same period in 2015-16.

Our country has been held as a ‘bright spot’ amidst a slowing global economy by IMF. This growth has been achieved despite very unfavorable global conditions and two consecutive years shortfall in Monsoon by 13%. However, there are challenges before the growth in future. Risks of further global slowdown and turbulence, future movements in the commodity prices, especially oil, ability of developed as well as developing economies to once again initiate investments in aggregate demand besides the likely additional fiscal burden due to seventh pay commission. However, the Government, RBI and other concerned agencies are undertaking suitable measures for facing the same.

The Banking sector in India is growing, so is our Bank. However, there are some major issues before us. Assets quality remain a serious cause of concern for the Bank and Capital Adequacy, Profitability is under pressure along with greater challenge in increasing the NIM, decreasing the Cost of Deposit and improving the Return on Assets. Different measures at different levels are being taken up to face the challenges.

WORKING RESULTSTOTAL BUSINESSDuring the year ended 31.03.2016, total Business of the Bank recorded an increase of 3.31% at Rs.156527 crore as compared to Rs.151511 crore as on 31.03.2015.

PROFITThe Bank recorded a Net Profit of Rs.335.97 crore for the year 2015-16 as compared to that at Rs.121.35 crore during the FY 2014-15. The Return on Assets (ROA) stood at 0.34% as compared to that at 0.13% in the year 2014-15.

HIGHLIGHTS OF RESULTS FOR THE YEAR ENDED 31ST MARCH 2016 (Rs. in Lac)

Year Ended %age change31.03.2016 31.03.2015

Interest Income 874434 858855 1.81Other Income 47848 42875 11.60Total Income 922282 901730 2.28Total Expenditure 795293 824185 -3.51Operating profit 126989 77545 63.76Net Profit 33597 12135 176.86ROA 0.34% 0.13%Net Interest Margin (NIM) 2.22% 1.80%Gross NPA 6.48% 4.76%Net NPA 4.62% 3.55%Capital Adequacy Ratio (Basel II) 11.75% 11.88%Capital Adequacy Ratio (Basel III) 10.91% 11.24%EPS (Rs.) 8.39 3.59

iatkc ,.M fla/ cSad

okf"kZd fjiksVZ 2015-1618

iwath ,oa vkjf{kfr;k¡fnukad 31-03-2015 dks cSad dh fuoy ekfy;r #- 4811-56 djksM+ ls c<+ dj fnukad 31-03-2016 dks #-5068-08 djksM+ gks xÃA fnukad 31-03-2016 dks cSad dk iwath i;kZIrrk vuqikr ¼cklsy III½ 10-91% gS tksfd fuèkkZfjr U;wure iwath i;kZIrrk vuqikr 9-625% ds fo#) gSA

xSj&tekurh çfrns; ckaM% ¼Vh;j&II dh iwath gsrq xkS.k _.k½fnukad 31-03-2016 rd Vh;j II ckaM dk dqy cdk;k #- 1]325-00 djksM+ Fkk tksfd vifjorZuh; gSA

tek o`f)cSad dh dqy tek jkf'k;ksa esa 31 ekpZ] 2016 dks 5-23% dh o`f) gqÃ] ftlls #- 4535-24 djksM+ dh lao`f) ds lkFk ;g #- 91249-96 djksM+ gks xà tksfd fnukad 31-03-2015 dks #- 86714-72 djksM+ FkhA fnukad 31-03-2016 dks cSad dh vkSlr tek ykxr 7-47% jgh tksfd foxr o"kZ 8-21% FkhA

vfxze fnukad 31-03-2016 dks cSad ds dqy vfxze 0-74% dh o`f) ds lkFk #- 65277-22 djksM+ jgs tksfd fnukad 31-03-2015 dks #- 64796-42 djksM+ FksA fnukad 31-03-2016 ds vuqlkj vfxzeksa ij vkSlr çfrQy 10-70% jgk tksfd foxr o"kZ 11-12% FkkA

çkFkfedrk {ks= vfxzecSad jk"Vªh; çkFkfedrk ds varxZr fofHkUu y{;ksa dks fujarj egRo nsrk jgsxkA çkFkfedrk {ks= ds varxZr dqN eq[;&eq[; ckrsa fuEu çdkj gS%

fnukad 31-03-2015 dks çkFkfedrk {ks= vfxze #- 20234 djksM+ dh rqyuk esa o"kZ 31-03-2016 dh lekfIr ij #- 4274 djksM+ ¼21-12%½ dh o`f) ntZ djrs gq, #-24]508 djksM+ gks x,A

fnukad 31-03-2016 dks o"kZ nj o"kZ 2-31% o`f) ds lkFk çkFkfed {ks= vfxze ,,uchlh ds 34-55% ls c<dj 36-86% gks x;kA

fnukad 31-03-2015 dks cSad ds —f"k vfxze esa #- 9064 djksM+ dh rqyuk esa o"kZ 31-03-2016 dh lekfIr ij #- 2101 djksM+ ¼23-18%½ dh o`f) ntZ dh tks #-11165 djksM+ gks x,A

vkjchvkà ds fuèkkZfjr y{; 7-00% dh rqyuk esa cSad dk NksVs vkSj lhekar fdlkuksa dks vfxze #- 4663 djksM+ jgk tksfd dqy vfxze dk 7-01% gSA

foÙkh; o"kZ 2015&2016 esa o"kZ nj o"kZ ds 15-69% dh o`f) ds lkFk cSad dk —f"k {ks= esa _.k dk çokg #- 9056 djksM+ dh rqyuk esa #- 10012 djksM+ ¼110-56%½ jgkA

fnukad 31-03-2016 rd dslhlh lapkfyr dqy 1-91 yk[k [kkrs¼94-02%½ dh rqyuk esa] cSad us dslhlh ds 1-84 yk[k [kkrksa esa #is MsfcV dkMZ tkjh fd,A

fnukad 31-03-2016 rd cSad us iatkc esa Cy‚d Lrj ij 6 vU; ,Q,ylh [kksys ftlls ,Q,ylh dh dqy la[;k 12 gks xÃA

31-03-2015 o"kZ ds var esa xzkeh.k fodkl ea=ky; }kjk rhu esa ls nks vkj,lÃVhvkà tksfd eksxk vkSj QjhndksV esa gSa] dks loksZPp xzsM ^AA* fn;k x;k vkSj mUgsa xzkeh.k csjkstxkj ;qodksa ds çf'k{k.k nsus gsrq ljdkjh vuqnku çkIr djus ds fy, ik= cuk;k x;k gSA

çkFkfedrk {ks= ds fn'kkfunsZ'k ij Ã&cqd rS;kj dj bls cSad ds osclkbV ij viyksM dj fn;k x;k gSA

,e,là _.k ds çys[khdj.k ,oa leh{kk gsrq ,d foLr`r cqdysV rS;kj dj bls cSad ds osclkbV ij miyCèk fd;k x;k gSA

cSad us vYila[;d leqnk; dks _.k çnku djus gsrq fn, x, mi&y{; dks çkIr fd;k gSA

_.k fuxjkuhcSad us #- 50 yk[k ls vfèkd _.k ,Dlikstjksa okys mPp ewY; [kkrksa dh mfpr rFkk çHkko'kkyh fuxjkuh rFkk u;h pwd fxjkoV ij fu;a=.k j[kus ds fy, çèkku dk;kZy; Lrj ij fu;a=.k d{k dh LFkkiuk dhA fuxjkuh dks vkSj vfèkd et+cwr cukus ds fy,] vkapfyd dk;kZy; Lrj ij Hkh vyx ls fu;a=.k d{k cuk, x, tksfd #i, 5-00 yk[k ls #i, 50-00 yk[k rd ds lHkh ekud mèkkj [kkrksa dh fuxjkuh djsaxsA cSad@vkjchvkà ds fn'kkfunsZ'k ds vuqlkj ik= ekeyksa dk uohuhdj.k fd;k tk jgk gSA

mä ds lanHkZ esa cSad ds }kjk c<kok nsus ds fy, fofHkUu uhfr;ka cukà x;h gSa ftlds }kjk vU; ckrksa ds lkFk ncko esa vkà vkfLr;ksa ds iqutÊou ds fy, vFkZO;oLFkk esa foÙkh; ladV ls iwoZ gh fucVku rFkk mckjus ds fy, ra= dks fØ;k'khy djuk] Loh—r çLrko ds fy, Rofjr dne mBkuk rFkk _.knkrk ds fy, vPNh olwyh djuk] yphyh lajpuk ds }kjk iquÆoÙk lacaèkh funsZ'k nsuk] ,sls mèkkjdrkZ tks fd vlg;ksxh mèkkjdrkZ gSa] mudk oxÊdj.k djuk rFkk lwpuk nsuk vkfn gSA

Punjab & Sind Bank

Annual Report 2015-16 19

CAPITAL & RESERVEThe Net Worth of the Bank has improved from Rs.4811.56 crore as on 31.03.2015 to Rs.5068.08 crore as on 31.03.2016. The Capital Adequacy Ratio (Basel III) of the Bank is 10.91% as on 31.03.2016 against the minimum stipulated requirement of 9.625%.

UNSECURED REDEEMABLE BONDS: (Subordinated Debts for Tier –II Capital)Total outstanding of Tier II Bonds as on 31.03.2016 remains unchanged at Rs.1,325 crore.

DEPOSIT GROWTHThe total deposit of the Bank registered a growth of 5.23% with net accretion of Rs. 4535.24 crore to reach Rs. 91249.96 crore as on March 31, 2016 from Rs. 86714.72 crore as on March 31, 2015. The average cost of deposits of the bank stood at 7.47% as compared to 8.21% in previous year.

ADVANCESThe Bank’s Advances increased by 0.74% from Rs. 64796.42 crore as on 31.03.2015 to Rs. 65277.22 crore as on 31.03.2016. The average yield on advances stood at 10.70% as on 31.03.2016 compared to 11.12% during the last year.

PRIORITY SECTOR ADVANCESThe Bank continues to accord importance to various goals under national priority. Some of the highlights under Priority Sectors Advances are as under:

Total Priority Sector Advance increased to Rs. 24508 crore as on 31.03.2016 from Rs. 20234 crore as on 31.03.2015 registering a growth of Rs. 4274 crore (21.12%).

Total Priority Sector advance increased from 34.55% of ANBC to 36.86% of ANBC on Y-o-Y basis as on 31.03.2016, an increase of 2.31%.

Bank’s Agriculture advance increased by Rs. 2101 crore (23.18%) to Rs. 11165 crore as on 31.03.2016 from Rs. 9064 crore as on 31.03.2015.

Bank’s advance to Small & Marginal Farmers increased to Rs. 4663 crore which is 7.01% of total advance against the RBI stipulated target of 7.0%.

Bank’s flow of credit to agriculture for FY 2015-16 was to the tune of Rs. 10012 crore against the target of Rs. 9056 crore (110.56%) registering an Y-o-Y growth of 15.69%.

The Bank has issued RuPay Debit Cards in 1.84 lac KCC accounts against the total operative KCC accounts of 1.91 lac (94.02%) as on 31.03.2016.

The Bank has opened another 6 FLCs at block level in Punjab thus raising total number of FLCs to 12 as on 31.03.2016.

Two of three RSETI i.e. Moga and Faridkot were given highest grade ‘AA’ by Ministry of Rural Development for the year ended 31.03.2015 making them eligible for Govt grants for training of rural unemployed youth.

E-book on Priority Sector guidelines prepared and put on Bank’s website.

A comprehensive Booklet on documentation and appraisal of MSE loan prepared and put on Bank’s website.

The Bank has also achieved sub target for lending to Minority Community.

CREDIT MONITORING The Bank had setup a Control Room for proper and effective monitoring of large accounts and to check fresh slippages, with exposures above Rs. 50 lacs at HO level. To further strengthen the monitoring, separate Control Rooms have now been set up at Zonal Offices level to monitor all standard borrowal accounts from Rs.5.00 lac upto Rs. 50.00 lac. Restructuring of eligible cases are being undertaken as per Bank/RBI guidelines.In order to supplement the aforesaid, various policy related initiatives have also been taken by the Bank which inter-alia include implementation of Framework for Revitalizing Distressed Assets in the Economy for Early Recognition of Financial Distress, Prompt Steps for Resolution and Fair Recovery for lenders, guidelines on refinance by way of flexible structuring/take out financing, Classification and reporting of borrower as non-cooperative borrower etc.

iatkc ,.M fla/ cSad

okf"kZd fjiksVZ 2015-1620

çèkkuea=h tu&èku ;kstuk rFkk eqæk ;kstuk ds varxZr miyfCèk;ka Û cSad us 'kk[kkvksa ds ekè;e ls 12-76 yk[k [kkrs [kksys] 351 O;olkf;d çfrfufèk cuk, vkSj çfr [kkrs esa tek #- 3672 dh vkSlr ls

#- 468-43 djksM+ ds dklk@,QMh@vkjMh dh tek,a laxzfgr dhA Û O;olkf;d çfrfufèk;ksa us yxHkx #- 187 djksM+ dk O;olk; fd;k x;k ftlesa ,u-ih-,-@Vh-MCY;w-vks- ds 1659 [kkrksa esa #- 6-96

djksM+ dh dqy jkf'k dh olwyh lfEefyr gSA Û gekjs lHkh O;olkf;d çfrfufèk;ksa us rhu lkekftd lqj{kk ;kstukvksa ¼ih,etstschokÃ] ih,e,lchokà ,oa ,ihoký ds varxZr chek O;olk; ds fy,

rUe;rk ls dk;Z fd;k vkSj o"kZ 2015&16 ds nSjku 141101 i‚fylh dh rFkk ;g O;olk; ykus ij #- 10-94 yk[k deh'ku ds rkSj ij dek,A Û cSad us MhchVh@MhchVh,y ds varxZr 107 yk[k çfof"V;ka çkIr dh vkSj #- 407 djksM+ çkIr fd, tksfd dklk ds varxZr tek dk ,d Hkkx

gS vkSj oks Hkh fcuk fdlh çR;{k ç;kl dsA cSad us ekpZ 2016 rd MhchVh@MhchVh,y ds varxZr #- 27 yk[k dk jktLo vÆtr fd;kA Û foÙkh; o"kZ 2015&16 ds nkSjku cSad us eSllZ eSfVªDl çkslsÇlx gkml ds ekè;e ls 5-46 yk[k ukekadu djkus ij #- 32-80 yk[k fofoèk

vk; ds #i esa çkIr fd,A Û cSad us 183 ekbØks ,Vh,e ds fy, ;wvkÃMh,vkà ls vc rd vuqnku jkf'k ds #i esa #- 27-45 yk[k çkIr fd, vkSj 27 vfèkd e'khuksa

ds fy, 4-05 yk[k #i;s dh vuqnku jkf'k ekax Lo#i çfØ;kèkhu gSA ;wvkÃMh,vkà ls ihvks,l e'khuksa ds fy, bl rjg ds vuqnku jkf'k çkIr djus esa gekjk cSad dqN fxus&pqus lkoZtfud {ks= ds cSadksa esa 'kkfey gSA 351 O;olkf;d çfrfufèk;ksa esa ls 210 çfrfufèk;ksa tksfd 60% ls vfèkd gS] us yxHkx 2000 ls vfèkd dh ysu&nsuksa dks iw.kZ fd;k gSA

Û cSad us çR;sd frekgh esa Vsu LVkj ijQ‚Éex O;olkf;d çfrfufèk;ksa dks iqjL—r djus ds fy, #- 1100 dh iqjLdkj jkf'k vkSj ,d ç'kalk i= çnku djus dh çfØ;k vkjaHk dh gSA

Û gekjh efgyk O;olkf;d çfrfufèk;ksa ¼351 O;olkf;d çfrfufèk;ksa esa ls 57 efgyk O;olkf;d çfrfufèk gSa½ esa ls dqN us mR—"V dk;Z fd;k gSA Û ih,etsMhok, [kkrksa esa dqy thjks cSysal ds vkS|ksfxd vkSlr 27% dh rqyuk esa gekjk çfr'kr 0-35% ¼lHkh cSadksa esa fuEu½ gSA Û funs'kd] fe'ku dk;kZy;] Mh,Ql@,e-vks-,Q- us leLr cSadksa ds lh,eMh@lhÃvks ds lkFk ijLij laokn esa dgk fd iatkc ,.M Çlèk cSad us

ih,etsMhokà esa dqN mR—"V miyfC/k;kW çkIr dh gSaA rRi'pkr] lkIrkfgd@ikf{kd ohlh cSBdksa esa thjks cSysal [kkrksa dks de djus] O;olkf;d çfrfufèk;ksa }kjk fd, x, ysu&nsuksa vkSj vkÃvkÃch,Q }kjk O;olkf;d çfrfufèk;ksa dks çek.khdj.k ds lacaèk esa gekjs cSad dh dà ckj ç'kalk dh xÃA

Û gekjs vkjvkjch ds O;olkf;d çfrfufèk vkÃvkÃch,Q }kjk 100% çekf.kr gSa vkSj gekjs cSad ds 98% ¼lHkh cSadksa ls T;knk½ O;olkf;d çfrfufèk bf.M;u baLVhVîwV v‚Q cSaÇdx ,aM Qkbusal }kjk çekf.kr gSaA

Û Hkkjrh; cSad la?k us iatkc ,.M Çlèk cSad dks vkjvkjch O;olkf;d çfrfufèk;ksa ds 100% çek.khdj.k vkSj gekjs cSad ds 95% O;olkf;d çfrfufèk ds çek.khdj.k ds fy, cèkkÃ;ka nh vkSj nwljs cSadksa dks iatkc ,.M Çlèk cSad dk vuqlj.k djus dh lykg nhA

Û cSad us foÙkh; lekos'ku ds varxZr foÙkh; lk{kjrk gsrq vkoafVr xkaoksa esa 32600 xzkeh.k O;fä;ksa ds fy, vc rd 516 ls vfèkd dSEiksa dk vk;kstu fd;kA rRi'pkr foÙkh; lekos'ku ds varxZr vkoafVr xkaoksa dks lfEefyr djus ds fy, cSad us foÙkh; lk{kjrk dSEiksa ds }kjk foÙkh; lk{kjrk çnku djus gsrq vfHk;ku pyk;kA

Û cSad us ,Vh,e@ekbØks ,Vh,e ds vksVkses'ku }kjk ih,etsMhokà vksoj Mªk¶V dks lQyrkiwoZd fØ;kfUor fd;k gSA orZeku esa 'kk[kkvksa ds ekè;e ls 81524 vksoj Mªk¶Vksa dh laLoh—fr nh xà gSA

Û gekjs ekbØks ,Vh,e ,Ãih,l vkSj #is fiuiSM l{ke gSa tks xzkeh.k xzkgdksa dks muds ck;kseSfVªd ;k #is MsfcV dkMZ }kjk var% vkSj varj cSad ysu&nsuksa dks djus esa lgk;rk djrs gSaA

Û çèkkuea=h eqæk ;kstuk ds varxZr #- 570 djksM+ ds fuèkkZfjr y{; dh rqyuk esa cSad us #- 465-85 djksM+ dk _.k fn;k tksfd dsihvkà ds 75% ds y{; dh rqyuk esa 81-73% jgkA eqæk _.k ds f'k'kq laoxZ ds varxZr #- 60 djksM+ ds y{; dh rqyuk esa cSad us #- 95-93 djksM+ laforfjr djrs gq, y{; dks ikj dj fn;kA

[kqnjk _.kcSad us vkØedrk ls [kqnjk _.k esa lkgl fd;k gS vkSj [kqnjk _.k [kaM ds varxZr mRiknksa dh uhfr dks mnkj cuk;k gS rFkk ckt+kj esa mRiknksa dks çfrLièkÊ cukus ds fy, C;kt njksa dks vkSfpR;iw.kZ cuk;k gSA cSad us foÙkh; o"kZ 2015&16 ds nkSjku rhu uà uoksUes"kh ;kstukvksa dks vkjaHk fd;k gS vFkkZr ih,lch vkoklh; _.k V‚i&vi ;kstuk] ih,lch ^xzks ,.M Iks* vkoklh; _.k ;kstuk rFkk dkS'ky _.k ;kstukAblds vfrfjä] vkokl _.k] v‚Vks _.k rFkk miHkksäk _.k {ks= ds varxZr ÞQsfLVoy cksukUtk Ldheß dk 'kqHkkjaHk fd;k x;kA fnukad 31-03-2016 dks [kqnjk _.k dk cdk;k 6492 djksM+ gS vkSj ftlds dkj.k fiNys o"kZ dh rqyuk esa] bl o"kZ ds nkSjku [kqnjk _.k esa 24 çfr'kr dh o`f) ntZ dh xÃAfnukad 31-03-2016 dks [kqnjk _.k] ldy vfxzeksa dk 9-93 çfr'kr FkkA

Punjab & Sind Bank

Annual Report 2015-16 21

ACHIEVEMENTS UNDER PRADHAN MANTRI JAN DHAN YOJNA & MUDRA YOJNA• The Bank has opened 12.76 lac accounts through Branches and 351 BCs and mobilized CASA/FD/RD deposit of Rs.468.43 crore ,

with average deposit per account Rs.3672.

• Total Business generated by BCs is about Rs. 187 Crore, which include Recovery in 1659 NPA/TWO accounts amounting to Rs.6.96 crore.

• All our BCs worked whole heartedly to bring Insurance Business under three Social Security Schemes (PMJJBY, PMSBY & APY) and brought 1,41,101 policies during 2015-16 and also earned Rs.10.94 lac as commission for bringing this business.

• The Bank has received 107 lac entries under DBT/DBTL and amount received is Rs.407 crore, which forms part of CASA deposits and that too without any front end efforts. Bank has earned a revenue of Rs. 27 lacs up to March 2016 , under DBT/DBTL.

• During the financial year 2015-16, the Bank received sum of Rs.32.80 lacs as Miscellaneous income for 5.46 lac enrollments done through M/s Matrix Processing House.

• The Bank has so far received subsidy amount of Rs.27.45 lacs from UIDAI for 183 MicroATMs and subsidy claim for 27 more machines for Rs.4.05 lacs is under process with UIDAI. Our bank is one of few Public Sector Bank to receive such Subsidy from UIDAI for PoS machines. Out of 351 BC, 210 i.e. about 60% BCs have completed more than 2000 transactions.

• The Bank has introduced a system of awarding ten star performing BCs every quarter with cash rewards of Rs.1100/- and an appreciation letter.

• Some of our women BCs (out of total 351 BCs, 57 are women BCs) having outstanding performance.

• Total Zero Balance accounts in PMJDY are at 0.35% against industry average of 27% (lowest among all banks).

• Director, Mission office, DFS/MOF shared with all CMD/CEOs of bank, that PSB has achieved some remarkable milestones in PMJDY. Further our bank is appreciated many times during the weekly/fortnightly VC meetings for reducing zero balance accounts, BC transactions and Certification of BCs by IIBF.

• 100% BCs of our RRB are certified through IIBF and 98% BCs of our Bank are certified through Indian Institute of Banking & Finance (highest among all banks).

• The IBA has also congratulated Punjab & Sind Bank for achieving 100% certification of RRB BCs and 95% BCs certification of our Bank and exhorted other banks to emulate the achievements of the Punjab & Sind Bank.

• The Bank has so far organized more than 516 Camps for Financial Literacy in FI allotted villages covering 32600 rural persons. Further Bank has started campaign to cover all the FI allotted villages by imparting financial literacy through Financial Literacy Camps.

• The Bank has successfully implemented PMJDY OD through automation i.e. through ATMs/MicroATMs. At present 81524 ODs are sanctioned by the branches.

• Our MicroATMs are AEPS & RuPay PINPAD enabled, helping rural customers to do intra and inter Bank transactions using their biometrics or RuPay Debit cards.

• The Bank made advance to the tune of Rs. 465.85 crore against the target of Rs. 570 crore under Pradhan Mantri Mudra Yojana which is 81.73% against the KPI target of 75%. Bank made disbursement to the tune of Rs. 95.93 crore against the target of Rs. 60 crore under Shishu category of MUDRA loans, surpassing the given target.

RETAIL MARKETINGThe Bank aggressively ventured into Retail Lending and liberalized the policy for products under the Retail segment and rationalized the interest rates to make the products most competitive in the market. The Bank launched three new innovative schemes viz. PSB Housing Loan Top-up Scheme, PSB ‘Grow & Pay’ Housing Loan Scheme & Skill Loan Scheme during the FY 2015-16. Further, Festival Bonanza Scheme offering concessions under the Housing Loan, Auto Loan and Consumer Loan segments was launched. The Retail Lending outstanding as on 31.03.2016 is Rs 6492 crore and thereby, Retail Lending has registered a business growth of 24% over the previous year.

The percentage of Retail advances to gross advances was 9.93% as on 31.03.2016.

iatkc ,.M fla/ cSad

okf"kZd fjiksVZ 2015-1622

foi.ku ,oa chekcSad us Hkkjr ljdkj dh lksojsu xksYM ckUM ;kstuk esa Hkkx fy;kA cSad us J`a[kyk II esa vfHknku jkf'k ds vuq#i vfHknku çkIr djus okys vfHkdj.kksa esa NBk LFkku çkIr fd;k vkSj J`a[kyk III esa cSad us ik¡pok LFkku çkIr fd;kA cSad us cgqr cM+s cSadksa] lkoZtfud {ks= ds cSadksa ds lkFk&lkFk futh cSadksa dks ihNs NksM+rs gq, fof'k"V LFkku çkIr fd;k gSA

cSad us vkÃ-vkj-Mh-,-vkÃ- ds uohure fn'kk&funsZ'kksa ds vuqlkj d‚iksZjsV ,tsalh O;olk; ij uhfr cukà gSA

ubZ igy Û cSad us leLr dSisDl ,Vh,e esa ean –f"V okyksa ds fy, l‚Y;w'ku¼cksyus okys½ vkjEHk fd;kA Û cSad us y?kq Lrj dh Ãdkb;ksa ds fy, eqæk dkMZ vkjaHk fd;kAÛ cSad us #is MsfcV dkMZ ,oa ekLVj MsfcV dkMZ }kjk v‚uykbu [kjhnnkjh ds fy, Ã&d‚elZ dk lw=ikr fd;kA Û cSad us vkjchvkà ds fn'kkfunsZ'kksa ds vuqlkj lHkh çdkj ds #is vkSj ekLVj MsfcV dkMZ esa Ã,eoh fpi dkMZ tkjh djus dh 'kq#vkr dhA Û cSad us ,QMhvkj cdk;k] fuf"Ø;@vçHkkoh dklk@dsokÃlh lekiu vuqLekjd@_.k fd'rksa lacaèkh psrkouh@_.k C;kt nj esa

ifjorZu lwpuk gsrq ,l,e,l ,yVZ dh 'kq#vkr dhA Û cSad us Þthou çek.kß&isa'kuHkksxh }kjk ck;ksesfVªd lR;kiu] fjeksV IokbaV] ,oa fMftVy thou çek.k i= ftldk ,uvkÃlh ds dsUæh;

laxzg esa j[kj[kko fd;k tkrk gS] dks ykxw fd;k gSA Û cSad us 58 fof'k"V ,e,l,eà 'kk[kkvksa dks ukfer fd;k ftlls fof'k"V ,e,l,eà 'kk[kkvksa dh dqy la[;k 108 gks xà gSA Û cSad us ,e,là _.k ds çys[khdj.k ,oa leh{kk gsrq ,d foLr`r cqdysV rS;kj dh gS vkSj bls osclkbV ij miyCèk djk fn;k gSA Û —f"k e'khuhdj.k tSls VªSDVj@dackbZu gkosZLVj@i‚oj fVyj@jhij@Vª‚yh@iqjkus VªSDVjksa@vkStkjksa bR;kfn gsrq foÙk iks"k.k ds fy,

uà ;kstuk ykxw dhA Û fdlkuksa ds fy, nksifg;k@thi@dkj@fo'ks"k ;wfVfyVh fOgdy¼,l;woh½ ds foÙk iks"k.k gsrq uà ;kstuk ykxw dh xÃA Û cSad us Þeqæk ;kstuk ds varxZr Ã& fjD'kkß ds foÙk iks"k.k gsrq ,d uà ;kstuk dh 'kq#vkr dhA Û cSad us eqæk _.k vkSj dslhlh fyfeV ij C;kt njksa dks vkSfpR;iw.kZ cuk;k gS vkSj #-3-00 yk[k rd ds dslhlh ij çlaLdj.k 'kqYd

dks lekIr dj fn;k gSA Û 'kk[kk çcaèkdksa ¼Ldsy I,II vkSj III½ dh _.k çnku djus dh foosdkèkhu 'kfä;ksa dks i;kZIr #i ls c<k;k x;k gS rkfd 'kk[kk Lrj ij

vfèkdre la[;k esa _.k vkosnu dk fuLrkj.k fd;k tk ldsA Û cSad ds osclkbV www.psbindia.com ij ,Q,ylh@ vkjlsVh osc iksVZy dk yksdkiZ.k fd;k x;kA Û foÙkh; o"kZ 2015&2016 esa cSad us 32 'kk[kk,a [kksyh gSA Û cSad us foÙkh; o"kZ 2015&2016 dks Þdklk o"kZß ds #i esa euk;k vkSj fnukad 31-03-2015 ds tek jkf'k esa dklk dk çfr'kr 21-53%

dh rqyuk esa fnukad 31-03-2016 dks c<dj 22-72% gks x;k gSA

iqjLdkj ,oa miyfCèk;kaÛ ,lkspSe us cSad dks y?kq cSad dh Js.kh esa lkekftd cSaÇdx mR—"Vrk vokMZ] 2015 ¼xzkeh.k cSaÇdx½ ls lEekfur fd;kAÛ o"kZ 2015&16 ds nkSjku] cSad us y?kq cSadksa dh Js.kh ds varxZr ,u-,Q-,l- mRikn ds fy, Jh vkj- xkaèkh] mi jkT;iky] Hkkjrh; fjt+oZ

cSad ls jk"Vªh; Hkqxrku mR—"Vrk iqjLdkj] 2015 dk la;qä mi fotsrk dk iqjLdkj çkIr fd;kAÛ ljdkjh lksoju xksYM ckaM ;kstuk esa vfHknku dh 'krks± ds vuqlkj] gekjk cSad çFke 10 çkIrdrkZ ,tsafl;ksa esa 'kkfey gSAÛ xzkeh.k fodkl ea=ky; us o"kZ 2013&14 dh Js.kh II ds varxZr ÞAAß xzsM çkIr djus ij cSad çk;ksftr vkjlsVh] QjhndksV vkSj eksxk

dks mR—"Vrk vokMZ fn;kAÛ cSad dh Çgnh if=dk jktHkk"kk vadqj dks fnYyh cSad uxj jktHkk"kk lfefr }kjk çFke iqjLdkj ls lEekfur fd;k x;kA if=dk dks

o"kZ 2015 dk vkÃlhà vokMZ Hkh çkIr gqvkAÛ Çgnh esa vPNk dke djus ds fy, cSad dks fnYyh] iVuk] cSaxyw#] pSUuS] tksèkiqj] dksydkrk] fHkykà vkSj i.kth¼xksok½ esa lacafèkr uxj

jktHkk"kk dk;kZUo;u lfefr;ksa }kjk jktHkk"kk 'khYMsa çnku dh xb±AÛ cSad dh g‚dh Vhe us thrh%

d- vf[ky Hkkjrh; ,l- ,u- oksgjk xqjehr Çlg g‚dh çfr;ksfxrk [k- vf[ky Hkkjrh; usg# g‚dh çfr;ksfxrk

Punjab & Sind Bank

Annual Report 2015-16 23

MARKETING AND INSURANCEThe Bank participated in the Sovereign Gold bond Scheme of Government of India. Bank was on sixth position among the receiving agencies in terms of subscription amount in Trenche-II and in Trenche-III the Bank secured the fifth position. Bank had the distinction of stealing march over very big Banks, PSBs as well as private.

Bank formulated the policy on Corporate Agency Business as per the IRDAI’s latest guidelines.

NEW INITIATIVES• Bank has implemented solution for Visually Impaired (Talking facility) in all Capex ATMs. • Bank has Introduced Mudra Card for small scale units. • Bank has Implemented e-commerce in the Bank for online purchase through RUPAY Debit Card and Master Debit Card.• Bank has started issuing EMV Chip cards as per RBI guidelines in all variants of Rupay & Master Debit Cards. • Bank has started SMS alerts on Overdue FDR, Dormant / Inoperative CASA/KYC expiry reminder / Loan installment due alerts/

Loan ROI change Alerts.• Bank has implemented “Jeevan Praman” - biometric authentication by the pensioner, remote point and creation of digital life

certificate which is maintained in a central repository in NIC.• Bank designated 58 branches as Specialized MSME branches thus raising total specialized MSME branches to 108.• A comprehensive Booklet on documentation and appraisal of MSE loan prepared and put on Bank’s website.• New Scheme launched on financing of Farm Mechanization i.e. financing of Tractor/Combine Harvester/Power Tiller/Reaper/

Trolley/Old Tractors/implements etc.• New scheme on financing Two wheeler/Jeep/Car/Special Utility Vehicles (SUV) for Agriculturist introduced.• Bank launched a new scheme on “Financing of E-Rickshaw under MUDRA Scheme”• Bank rationalized rate of interest on MUDRA loans and KCC limits and waived processing fee on KCC upto Rs. 3.00 lac.• Discretionary lending powers of Branch Manager (Scale I, II and III) were increased substantially to facilitate disposal of

maximum number of loan applications at branch level itself. • FLC/RSETI Web Portal launched at Bank’s website www.psbindia.com• Bank has opened 32 new branches in FY 2015-16.• Bank celebrated the FY 2015-16 as “YEAR OF CASA” and CASA % to Deposits has increased from 21.53% as on 31.03.2015 to

22.72% as on 31.03.2016.

AWARDS & ACHIEVEMENTS• Social Banking Excellence Award -2015 was conferred on the Bank by ASSOCHAM under Small Bank Class & Rural Banking

category for providing Rural Banking services.• The Bank received Joint Runners up award in Small Banks category for NFS product from Sh. R Gandhi. Deputy Governor, RBI

at National Payment Excellence Awards 2015.• In Government’s Sovereign Gold Bond Scheme, Bank figured among top 10 receiving agencies in terms of subscription.• Ministry of Rural Development awarded Certificate of Excellence to Bank sponsored RSETI, Faridkot and Moga securing “AA”

grade under category II for the year 2013-14.• Bank’s Hindi Magazine ‘RAJBHASHA ANKUR’ was awarded 1st Prize by Delhi Bank Town Official Language Implementation

Committee. Magazine was also awarded ICE Award for the year 2015. • For Official Language Implementation, Bank was awarded Rajbhasha Shields in Delhi, Patna, Bengluru, Chennai, Jodhpur,

Kolkata, Bhilai and Panjim(Goa) by respective Town Official Language Implementation Committees.• The Bank’s Hockey Team won:

a. All India S.N. Vohra Gurmit Singh Hockey Tournamentb. All India Nehru Hockey Tournament

iatkc ,.M fla/ cSad

okf"kZd fjiksVZ 2015-1624

vkfLr xq.koÙkk

cSad us vutZd vkfLr;ksa ij fu;a=.k ds fy, vusd ç;kl fd, gSa rFkk fofèkd lkèkuksa ,oa ckrphr ij vkèkkfjr le>kSrksa lfgr olwyh ds lHkh miyCèk lkèkuksa dk ç;ksx fd;k gSA cSad us foÙkh; vkfLr;ksa dk çfrHkwfrdj.k vkSj iquxZBu rFkk çfrHkwfr fgr dk çorZu vfèkfu;e] 2002 ds çkoèkkuksa dk çHkkoh #i ls ç;ksx fd;kA cSad us bl foÙkh; o"kZ esa fofHkUu dsaæksa ij olwyh dSEiksa dk vk;kstu fd;kA o"kZ ds nkSjku cSad dh olwyh çcaèku ;kstuk ds vfrfjä xSj fu"ikfnr [kkrksa ds —f"k {ks= ds varxZr vutZd vkfLr;ksa ds fuiVku gsrq rFkk vlqjf{kr rduhdh cês&[kkrksa ds fuiVku gsrq nks vYikofèk ;kstukvksa dk fu#i.k fd;k x;kA lHkh 1366 ekeyksa dk #-39-28 djksM+ esa fuiVku gqvkA

o"kZ ds nkSjku xSj&fu"ikfnr [kkrksa esa cSad dh olwyh vPNh jghA olwyh ds fy, fd, x, vFkd rFkk dsfUær ç;klksa ds QyLo#i #-49-68 djksM+ dh rduhdh cêk [kkrksa esa olwyh lfgr dqy #- 945-90 djksM+ #-dh olwyh dh tk ldhA

cSad u, xSj fu"ikfnr [kkrksa esa c<+ksÙkjh dks jksdus esa lQy jgk gSA ifj.kkeLo#i dqy rFkk fuoy ,uih, fnukad 31-03-2015 ds #- 3082-19 djksM+ rFkk #- 2260-00 djksM dh vis{kk Øe'k% #- 4229-05 djksM+ rFkk #- 2949-47 djksM+ jgkA

31-03-2016 dks xSj&fu"ikfnr vkfLr;ksa dh ldy ,oa fuoy fLFkfr vFkkZr~ fiNys o"kZ dh rqyuk esa fuEukuqlkj gS &¼jkf'k djksM+ esa½

,uih, 31-03-2015 dh fLFkfr vuqLkkj 31-03-2016 dh fLFkfr vuqLkkj

ldy 3082-19 4-76% 4229-05 6-48%fuoy 2266-00 3-55% 2949-47 4-62%

fnukad 31-03-2016 dks cSad dk çkoèkku lqj{kk vuqikr ¼rduhdh cêk [kkrksa lfgr½ 48-26% jgkA

fuos'k çcaèku rFkk fons'kh fofue;

31-03-2016 dks cSad dh d‚jiksjsV {ks= dh vko';drk] tksf[ke laxzg ,oa fuos'k uhfr ds vuq#i fuos'k&lwph ljapuk lfgr cSad dk ldy fuos'k #-27693-40 djksM+ FkkA

ekpZ 2015 dks lekIr o"kZ esa ljdkjh çfrHkwfr;ksa rFkk xSj lkafofèkd pyfufèk vuqikr çfrHkwfr esa VªsÇMx xfrfofèk;ksa ls ykHk #- 133-60 ls c<dj lekIr o"kZ 31-03-2016 esa #- 140-10 djksM+ x;kA

o"kZ 2014&15 dh rqyuk esa fofue; ykHk #- 26-51 djksM+ ls c<+dj o"kZ 2015&16 esa c<+ dj #- 30-34 djksM+ gks x;kA bl çdkj] 14-45% dh o`f) ntZ dh xÃA

tksf[ke çca/ku

cSad us ;g lqfuf'pr djus ds fy, fd mlds tksf[ke] ifjHkkf"kr tksf[ke {kerk ds Hkhrj gSa vkSj mudh i;kZIrj #i ls fuxjkuh dh tkrh gS] ds fy, ,d lq–<+ ,dh—r tksf[ke çcaèku ç.kkyh dks dk;Z#i fn;k gSA cSad esa tksf[ke {kerk rFkk çHkkoh tksf[ke çcaèku dk;e djus dk laiw.kZ mÙkjnkf;Ro cSad ds funs'kd eaMy ,oa cSad ds 'kh"kZLFk çcaèku ij gSA cSad dh lesfdr tksf[ke çcaèku ç.kkyh] ç-dk- tksf[ke çcaèku foHkkx ¼vkj,eMh½ ds egkçcaèkd }kjk fuxjkuh dh tkrh gSA

fuEufyf[kr 'kh"kZLFkk lfefr;ksa ds ekè;e ls tksf[ke çcaèku fd;k tkrk gS%

1- tksf[ke çcaèku lfefr ¼vkj,elh½ ,d cksMZ Lrjh; milfefrA

2- _.k tksf[ke çcaèku lfefr ¼lhvkj,elh½

3- vkfLr ,oa ns;rk,a çcaèku lfefr ¼,,ylhvks½

4- lapkyxr tksf[ke çcaèku lfefr ¼vksvkj,elh½

5- cktkj tksf[ke çcaèku lfefr ¼,evkj,elh½

6- vkÃlh,,ih ds vuqlkj iwathxr ;kstuk lfefr

;s lfefr;ka tksf[ke çcaèku lfefr ¼vkj,elh½@funs'kd eaMy }kjk vuqeksfnr lE;d ekxZn'kÊ funsZ'kksa rFkk uhfr;ksa dh ifjfèk esa viuk dke djrh gSA

Punjab & Sind Bank

Annual Report 2015-16 25

ASSETS QUALITYThe Bank continued to make concerted efforts to contain NPAs and has used all available tools of recovery including negotiated settlements and legal means. The provisions of “The Securitization & Reconstruction of Financial Assets & Enforcement of Security Interest Act -2002” were used effectively. The Bank also organized Recovery Camps during the year at various centers. During the year, two short term schemes for settlement of NPAs were formulated under Agriculture Sector and unsecured T.W.O. accounts apart from Bank’s Recovery Management Policy. In all 1366 cases were settled at Rs. 39.28 crore.

The performance of the Bank under recovery of NPAs during the year continued to be good. The aggressive and focused efforts could result in the total recovery of over Rs. 945.90 crore including recovery of Rs. 49.68 crore in Technically Written Off Accounts.

Bank has been able to contain fresh slippage. As a result our gross NPAs and net NPAs as on 31.03.2016 have been contained at Rs. 4229.05 crore and Rs. 2949.47 crore respectively against Rs. 3082.19 Crore and Rs. 2266.00 Crore as on 31.03.2015.

The position of Gross and Net NPAs as on 31.03.2016 vis-à-vis previous year is as under: (Amount in Crore)

NPA As on 31.03.2015 As on 31.03.2016

Gross 3082.19 4.76 % 4229.05 6.48%

Net 2266.00 3.55 % 2949.47 4.62%

The Provision Coverage Ratio of the Bank (including T.W.O.A/Cs), as on 31.03.2016 stood at 48.26%.

INVESTMENT & FOREIGN EXCHANGEThe Bank’s total gross investment as on 31.03.2016 was Rs. 27693.40 crore, with a portfolio composition consistent with the corporate requirement, risk perception and investment policy of the Bank.

The profit on sale of securities for the year has increased from Rs. 133.60 crore for year ended March 2015 to Rs. 140.10 crore for the year ended 31.03.2016 on account of trading activities in G-sec and Non SLR securities.

The Exchange profit for the year has increased from Rs.26.51 crore in 2014-15 to Rs. 30.34 crore in 2015-16, registering a growth of 14.45%.

RISK MANAGEMENTThe Bank has put in place a robust and integrated Risk Management system to ensure that the risks assumed by it are within the defined risk appetites and are adequately monitored. The overall responsibility of setting the Bank’s risk appetite and effective risk management rests with the Board and apex level management of the Bank. The implementation of Integrated Risk Management System in the Bank is monitored by HO Risk Management Department (RMD) headed by General Manager.

Risk is managed through following Apex committees viz.

1. Risk Management Committee (RMC)- a board level subcommittee

2. Credit Risk Management Committee (CRMC)

3. Asset and Liabilities Management Committee (ALCO)

4. Operational Risk Management Committee (ORMC)

5. Market Risk Management Committee (MRMC)

6. Capital Planning Committee as per ICAAP

These committees work within the overall guidelines and policies approved by the Risk Management Committee (RMC) / Board.

iatkc ,.M fla/ cSad

okf"kZd fjiksVZ 2015-1626

uhfr&ra= cSad ds le{k tksf[keksa dk ekiu] çcaèku ,oa fu;a=.k djus ds fy, funs'kd eaMy }kjk vuqeksfnr uhfr;ka rFkk dk;Zfofèk;ka gSaA

cSad ds leLr çdkj ds tksf[keksa ds fo'ys~"k.k djus ds vkSj cSad ds lHkh tksf[keksa dks ,dh—r djus ds mís'; ls ,dh—r tksf[ke çcaèku uhfr rS;kj dh xà gSA vU; egRoiw.kZ tksf[ke uhfr;ksa esa vkfLr ns;rk çcaèku ¼,,y,e½ uhfr] _.k tksf[ke çcaèku uhfr] cktkj _.k çcaèku uhfr] ifjpkyuxr tksf[ke çcaèku ¼vksvkj,e½ uhfr] O;olk; fujarjrk ;kstuk ¼chlhih½ o vkink m)kj çcaèku ¼Mhvkj,e½ uhfr] LVªsl VsÇLVx uhfr] _.k tksf[ke de djus lacaèkh rduhdksa dh ç;ksx uhfr rFkk laikÆÜod çcaèku] vkarfjd iwath i;kZIrrk fuèkkZj.k çfØ;k ¼vkÃlh,,ih½A tksf[ke çcaèku lfefr@cksMZ ds }kjk okÆ"kd vkèkkj ij uhfr;ksa dh leh{kk dh tkrh gSA

cSad dk cklsy&II ds lkFk vuqikyuHkkjrh; fjt+oZ cSad ds fofu;ked fn'kk&funsZ'kksa ds vuqlkj cSad us 31-03-2009 dh çHkkoh frfFk ls u, iwath i;kZIrrk ÝseodZ dks viuk;k gSA cklsy&II ds vkèkkj ij cSad us iwath çHkkj dh lax.kuk ds fy, _.k tksf[ke gsrq ekud –f"Vdks.k] cktkj tksf[ke gsrq #ikarfjr vofèk –f"Vdks.k rFkk ifjpkyuxr tksf[ke gsrq ewy ladsrd –f"Vdks.k dks viuk;k gSA cSad us cklsy&III ds fn'kk&funsZ'kksa dks dk;kZfUor fd;k gS vkSj lhvkj,vkj dh lax.kuk 'kq# dh gS tks twu] 2013 ls çHkkoh gSA cSad ds funs'kd eaMy }kjk lhvkj,vkj dh frekgh vkèkkj ij leh{kk dh tkrh gSA cSad Hkkjrh; fjt+oZ cSad ds funsZ'kkuqlkj cklsy&II ds varxZr mUur –f"Vdks.k dh vksj vxzlj gksus ds fy, rS;kj gSA cklsy&II ds mUur –f"Vdks.k dh vksj vxzlj gksus rFkk cklsy&III ds fn'kk&funsZ'kksa ds dk;kZUo;u gsrq cSad esa foLr`r ladyu tksf[ke çcaèku m|e çfØ;k ¼ÃvkÃvkj,e,l½ dh LFkkiuk gsrq ,d ijke'kZnkrk dh fu;qfä dh xà gSA

vkbZ-lh-,-,-ih- uhfr cklsy&II o cklsy&III & LraHk 2& i;Zos{k.kh; leh{kk ,oa ewY;kadu çfØ;k ¼,lvkjÃih½ fo"k;d] Hkkjrh; fjt+oZ cSad ds fn'kk&funsZ'kksa ds vuqikyu esa ;g lqfuf'pr djus ds fy, fd iwath vko';drk dk ewY;kakdu] cSad ds vkdkj] tfVyrk dk Lrj] tksf[ke çksQkby rFkk lapkyu dh ifjfèk ds vuq#i gS] vkarfjd iwath i;kZIrrk ewY;kadu çfØ;k ¼vkÃlh,,ih½ uhfr rS;kj dh xà gSA fofHkUu vof'k"V tksf[keksa dk fuèkkZj.k fd;k tkrk gS rFkk tgk¡ visf{kr gks ogk¡ vfrfjDr iwath miyCèk djkà tkrh gSA orZeku rFkk vuqekfur foÙkh;&iwathxr fLFkfr ds fo'ys"k.k rFkk xqatkb'k ds vkèkkj ij cSad dh iwathxr i;kZIrrk dk fuèkkZj.k fd;k tkrk gSA

fofHkUu LVªsl ifjfLFkfr;ksa ls gksus okys laHkkfor çHkkoksa dk cSad dh ykHkçnrk dh {kerk ds lanHkZ esa vk?kkr lgu djus rFkk cSad dh iwath ij blds ijorÊ çHkko ds ewY;kadu ds fy, LVªsl VSLV vH;k~l Hkh fd;k tkrk gSA vkÃlh,,ih ifj.kke frekgh vkèkkj ij rS;kj fd;k tkrk gS rFkk tksf[ke çcèku lfefr ¼vkj,elh½ }kjk bldh leh{kk dh tkrh gSA