Embed Size (px)

Citation preview

GEORGIA BONDS

Daniel M. McRae, Partner Seyfarth Shaw LLP 1075 Peachtree Street, N.E. Suite 2500 Atlanta, GA 30309 404.888.1883 [email protected] [email protected] June 2014

17361176

©2014 Seyfarth Shaw LLP

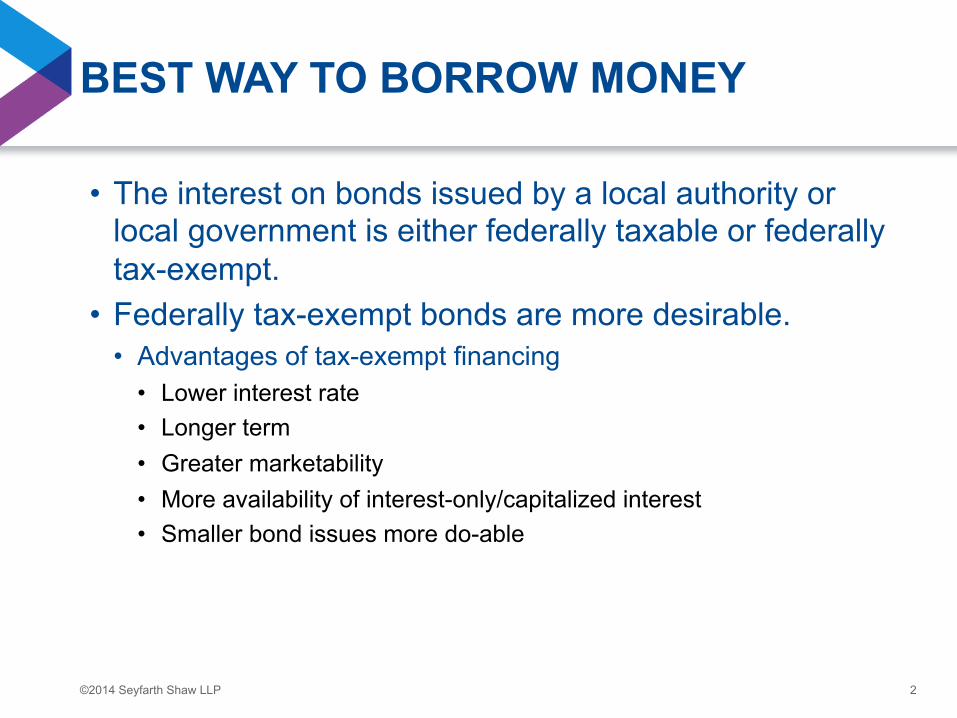

BEST WAY TO BORROW MONEY

• The interest on bonds issued by a local authority or local government is either federally taxable or federally tax-exempt.

• Federally tax-exempt bonds are more desirable. • Advantages of tax-exempt financing

• Lower interest rate • Longer term • Greater marketability • More availability of interest-only/capitalized interest • Smaller bond issues more do-able

2

©2014 Seyfarth Shaw LLP

BACKING THE BONDS

• LOCAL GOVERNMENT BONDS ARE OFTEN BACKED BY TAXING POWER • “GENERAL OBLIGATION” • REFERENDUM REQUIRED

• SOME LOCAL AUTHORITY BONDS ARE BACKED BY MILLAGE PLEDGE THROUGH INTERGOVERNMENTAL AGREEMENT (“IGA”) WITH LOCAL GOVERNMENT • CALLED “CONTRACT REVENUE BONDS” (FORMERLY

CALLED “BACK-DOOR G.O. BONDS”)

3

©2014 Seyfarth Shaw LLP

BACKING THE BONDS

• CONTRACT REVENUE BONDS • “LIMITED OBLIGATION” • NO REFERENDUM

• Example of Exception: If O.C.G.A. Sec. 36-75-11(c) applies (in practice, this applies only to DeKalb County).

4

©2014 Seyfarth Shaw LLP

NON-RECOURSE

• HOLDER OF REVENUE BONDS TYPICALLY HAS RECOURSE TO PLEDGED REVENUE OR OTHER BOND SECURITY, NOT TO CREDIT OF LOCAL AUTHORITY OR LOCAL GOVERNMENT

• ABILITY TO PLEDGE REVENUE DEPENDS ON LAWS GOVERNING THE ISSUER AND THE REVENUE

• DEVELOPMENT AUTHORITY PROJECT: REVENUE NORMALLY COMES FROM PROCEEDS OF LEASING OR SELLING THE PROJECT, OR, IF MANAGED, FROM PROJECT REVENUES • EXCEPTION – LOAN REPAYMENTS IN “DIRECT LOAN”

STRUCTURE

5

©2014 Seyfarth Shaw LLP

TAX-EXEMPT BONDS: REVENUE SOURCE MATTERS

• Interest on governmental purpose bonds will be tax-exempt unless certain tax rules are not satisfied. Interest on private activity bonds will not be tax-exempt unless an exemption applies and all applicable tax rules are satisfied.

• Bonds are governmental purpose bonds if they are not private activity bonds.

• Bonds are private activity bonds if they meet either: 1. the “private business tests” (both the 10% private business use

test and the 10% private payment or security test), or 2. the “private loan test”

• Governmental purpose bonds must flunk 1. one of the “private business tests”, and 2. the “private loan test”

6

©2014 Seyfarth Shaw LLP

“BQ” MEANS MORE MARKETABLE Taken from: Report of the Government Finance Officers’ Association of N.J. (April 2008)

• “BQ” stands for “bank qualified”. • Doesn’t imply that banks can’t buy other bonds. • The benefit of BQ debt for banks [and other financial

institutions] is the 80% interest expense deduction [they] may take when purchasing or carrying such BQ debt.

• BQ Requirements - • the tax-exempt obligations must be for a public purpose [i.e.,

governmental purpose or qualified 501(c)(3) bonds]; • the issuer must reasonably expect to issue less than $10 million

“public purpose” tax-exempt obligations during the calendar year, i.e., be a “qualified small issuer” (not the same as small issuer for arbitrage rebate purposes); and

• the tax-exempt obligations must be specifically designated as “qualified tax-exempt obligations” by the issuer.

7

©2014 Seyfarth Shaw LLP

DEVELOPMENT AUTHORITY BONDS: “SMALL ISSUE” MANUFACTURING BONDS

• Capital expenditure limit ($10 million tax-exempt bond proceeds + $10 million other) /$40 million national limit on tax-exempt bonds for the “Company”

• Spending requirements – • 95% or more of the proceeds must be used for a “manufacturing”

facility (only 5% may be “bad money”) • no more than 25% on land costs • at least 15% on rehabilitation expenditures, if acquiring an existing

building (and the equipment therein) • at least 70% on “core manufacturing” facilities (e.g., manufacturing

part of the building and new manufacturing equipment) • no more than 25% on “directly related and ancillary” facilities • up to 2% can be spent for issuance costs (this 2% is a part of the 5%

allowable “bad money”) 8

©2014 Seyfarth Shaw LLP

DEVELOPMENT AUTHORITY BONDS: “QUALIFIED 501(C)(3) BONDS”

• BONDS FOR ORGANIZATIONS THAT ARE TAX-EXEMPT 501(C)(3) ORGANIZATIONS UNDER THE INTERNAL REVENUE CODE WHICH ARE ISSUED FOR FACILITIES SUCH AS PRIVATE HIGH SCHOOLS AND COLLEGES AND MEDICAL FACILITIES.

• THESE ORGANIZATIONS ARE GENERALLY FAMILIAR WITH TAX-EXEMPT FINANCING (BECAUSE THEY TEND TO USE BOND FINANCING REPETITIVELY).

• NO “VOLUME CAP” FROM DCA NEEDED. • CAN “SELF-INDUCE” (BUT AUTHORITY HAS TO ISSUE

THE BONDS). • TEFRA APPROVAL FROM LOCAL GOVERNMENT

REQUIRED. • ISSUED BY DEVELOPMENT AUTHORITIES AND SOME

OTHER TYPES OF LOCAL AUTHORITIES; E.G., HOUSING AUTHORITIES.

9

©2014 Seyfarth Shaw LLP

“EXEMPT FACILITY” BONDS

• Exempt facility bonds can qualify for tax-exemption under federal law. • Not subject to capital expenditure limitation. Federal “volume cap” usually required. • Exempt facility bonds are for-

• airports • docks and wharves • mass commuting facilities • facilities for furnishing of water • sewage facilities • solid waste disposal facilities • qualified residential rental projects • facilities for the local furnishing of electric energy or gas • local district heating and cooling facilities • qualified hazardous waste facilities • high-speed intercity rail facilities • environmental enhancements of hydro-electric generating facilities • qualified public educational facilities • qualified green building and sustainable design projects • qualified highway or surface freight transfer facilities

• Local authority can issue if its state law powers permit. Some types issued by development authorities. Some types issued by Public Facilities Authorities or other specialized local authorities.

10

©2014 Seyfarth Shaw LLP

WHERE THE OPPORTUNITIES ARE

• RENEWABLE ENERGY • SENIOR LIVING • HIGHER ED • PRIVATE PLACEMENTS • DEVELOPMENT DISTRICTS • P3 STRUCTURES

11

©2014 Seyfarth Shaw LLP

RENEWABLE ENERGY- Bond Opportunities

• Solid waste disposal bonds • “Small issue” manufacturing bonds • Examples of projects:

• Biomass-to-electricity projects • pellet mills

• Typically issued by development authority

12

©2014 Seyfarth Shaw LLP

SENIOR LIVING- Bond Opportunities

• Affordable Housing: Sec. 142(d) Bonds • Example: Development Authority of Cobb County Revenue

Bonds (Provident Group - Creekside Properties LLC Project) Series 2014 in an aggregate principal amount not to exceed $14,500,000 (assisted living and memory care facility)

13

©2014 Seyfarth Shaw LLP

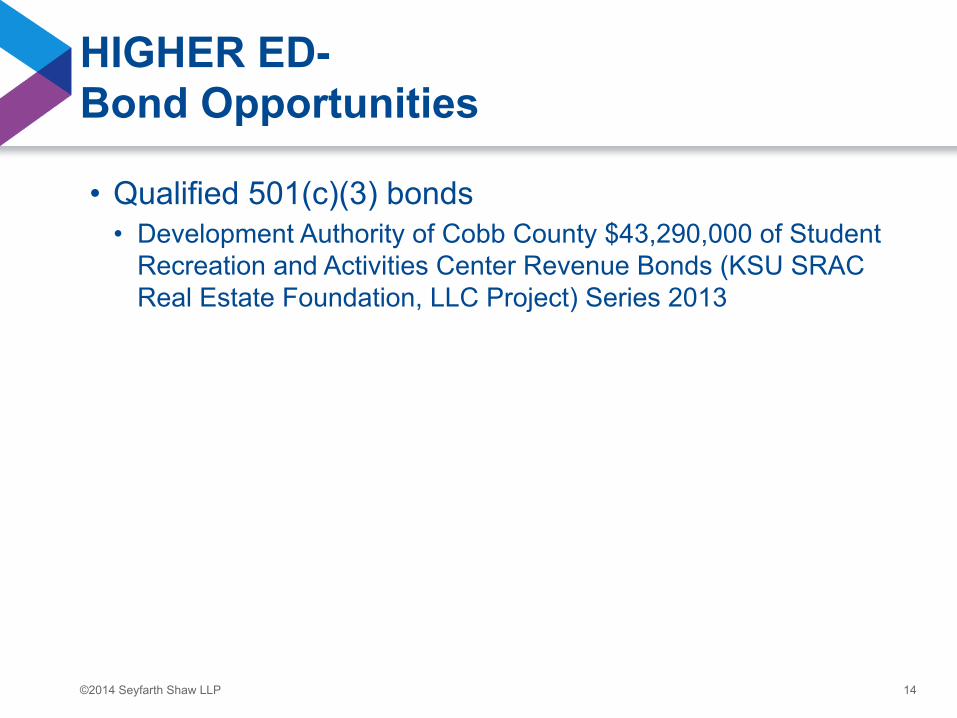

HIGHER ED- Bond Opportunities

• Qualified 501(c)(3) bonds • Development Authority of Cobb County $43,290,000 of Student

Recreation and Activities Center Revenue Bonds (KSU SRAC Real Estate Foundation, LLC Project) Series 2013

14

©2014 Seyfarth Shaw LLP

PRIVATE PLACEMENTS- Bond Opportunities

“Direct bank loans have become increasingly popular in the muni market since 2009 as an alternative to publicly offered bond issues. Bank loans can be structured with fixed or variable rates and do not need credit enhancement and have recently been replacing debt with expiring letters of credit. The term “bank loan” includes fixed-rate loans with defined maturities and loans or lines of credit that have variable interest rates and flexible payment provisions…” Government Finance Officers Association.

15

©2014 Seyfarth Shaw LLP

DEVELOPMENT DISTRICTS- Bond Opportunities

“When property taxes are “monetized”, TADs are just in the middle of the spectrum of choices. At one end of the extreme, potentially all of the property taxes can be monetized when PILOT Bonds (repayable out of payments in lieu of taxes) are used. TAD bonds are in the middle of the spectrum. This is because TAD bonds usually only monetize a “positive tax increment”, and only the positive tax increments of the property taxes of the jurisdictions that can, and do, participate. At the other extreme, when Community Improvement Districts are used, only the additional tax or assessment is used.” Dan McRae, “A Primer on PILOT Bonds,” at http://danmcrae.info/quicktakes

16

©2014 Seyfarth Shaw LLP

PILOT BONDS

• REVENUE TO REPAY THE BONDS COMES FROM PAYMENTS IN LIEU OF TAXES (PILOT payments) • to the extent normal taxes are not payable • In order to use PILOT payments, either the financing must not be

subject to the PILOT Restriction Act, or compliance with the Act is required. See O.C.G.A. Sec. 36- 80-16.1

• DON'T CONFUSE WITH "BONDS FOR TITLE" • Property taxes aren't monetized when a typical bond-financed

sale-leaseback structure is used for property tax savings ("abatement") purposes; i.e., "bonds for title"

17

©2014 Seyfarth Shaw LLP

P3- Bond Opportunities

OVERALL INVESTMENT ATLANTA BRAVES: $372 MILLION LOCAL CONTRIBUTION: $300 MILLION

$672 MILLION TOTAL

[PERCENTAGES BASED ON NET PRESENT VALUE] LOCAL ATLANTA BRAVES

COBB TRANSPORTATION CONTRIBUTION: $14 MILLION ATLANTA BRAVES UPFRONT CONTRIBUTIONS:* $280 MILLION

CUMBERLAND CID CONTRIBUTION: $10 MILLION

LOCAL ANNUAL CONTRIBUTIONS:* ATLANTA BRAVES ANNUAL CONTRIBUTIONS:*

EXISTING HOTEL/MOTEL TAX $940,000 RENT $3 MILLION

REALLOCATION OF EXISTING REVENUES** $8.67 MILLION NAMING RIGHTS REVENUE $1.5 MILLION

RENTAL CAR TAX $400,000 PARKING REVENUE $1.5 MILLION

CUMBERLAND DISTRICT TAX $5.15 MILLION ADVERTISING REVENUE $100,000

CUMBERLAND DISTRICT CIRCULATOR FEE $2.74 MILLION

**NO INCREASE IN PROPERTY TAXES TO COBB HOMEOWNERS: $17.9 MILLION PER YEAR

$6.1 MILLION PER YEAR

*ANNUAL CONTRIBUTIONS COVER PRINCIPAL AND INTEREST OF BOND ISSUANCE

ECONOMIC IMPACT • 5,227 construction jobs with $235,000,000 in construction earnings, $35,000,000 of which will be in earned in Cobb County. • 3,141 ongoing ballpark jobs, resulting in $35,800,000 in earnings, with 1,617 of those jobs in Cobb County, resulting in earnings of

$6,232,500 in Cobb County. • Visitor spending, resulting in 873 jobs which provide $25,000,000 in earnings, of which $8,906,754 will be earned in the county.

__________

These numbers do not include the anticipated tax revenues from the planned Braves-owned mixed-use development around the stadium.

18

©2014 Seyfarth Shaw LLP

CONCLUSION

• HOW TO FINANCE THE PROJECT? • INDUSTRIAL DEVELOPMENT REVENUE BONDS

USED TO BE THE ANSWER • NOW, THERE IS NO ONE ANSWER • BUT WHEN ONE DOOR CLOSES…

• OTHER DOORS OPEN • GOOD LUCK WITH ALL YOUR NEW BOND

OPPORTUNITIES!

19

©2014 Seyfarth Shaw LLP

REFERENCES

• THIS PRESENTATION AND OTHER REFERENCES CAN BE • DOWNLOADED AS FOLLOWS: • May 2013 – P3 – Public/Private Partnerships Done Right • May 2012- Renewable Energy- Start to Finish: Site Location, Development, Finance, Construction, and Commercial

Operations • May 2012- Opportunities in Bond Financing (Stern Brothers) • May 2012- Energy (Georgia Center of Innovation) • March 2012- "In-Sourcing Capital: EB-5 Loans and Equity; NMTC Tax Credit Equity; and Non-Recourse Project Finance

Bonds" • October 2011 - “Project Finance - No Banks, No Recourse, No Problem!” • August 2011 - "Green Energy/Green Dollars" • August 2011 - "Definition of Solid Waste Disposal Facilities for Tax-Exempt Bond Purposes" • January 2011 - “Bonds 101” • January 2011 - “Introduction to Tax-Exempt Bonds” • January 2011 - “Introduction to 'Taxable Floaters' ” • at http://danmcrae.info/whitepapers • May 2013 – Quick Takes: “Financing Updates and Save the Dates” • September 2011 - Quick Takes: "Section 1603 Grants" for Renewable Energy Projects: Take the Money and Run!” • August 2011 - Quick Takes: “New Regs, New Rush- Finance Your Renewable Energy and Solid Waste Disposal Projects

Now!” • June 2011 - Quick Takes: “Easy Equity- the NMTC and EB-5 programs” • January 2011 - Quick Takes: “After ARRA - What Bonds Can We Use Now to Finance Projects?” • at http://danmcrae.info/quicktakes

20

©2014 Seyfarth Shaw LLP

QUESTIONS?

Daniel M. McRae, Partner Seyfarth Shaw LLP

1075 Peachtree Street, N.E., Suite 2500 Atlanta, Georgia 30309

Telephone: 404.888.1883 [email protected]

http://danmcrae.info

21

©2014 Seyfarth Shaw LLP

MORE INFORMATION

This presentation is a quick-reference guide for company executives and managers, elected and appointed officials and their staffs, economic developers, participants in the real estate and financial industries, and their advisors. The information in this presentation is general in nature. Various points which could be important in a particular case have been condensed or omitted in the interest of readability. Specific professional advice should be obtained before this information is applied to any particular case. Any tax information or written tax advice contained herein is not intended to be and cannot be used by any taxpayer for the purpose of avoiding tax penalties that may be imposed on the taxpayer. (The foregoing legend has been affixed pursuant to U.S. Treasury Regulations governing tax practice.)

22