Embed Size (px)

Citation preview

II SimpósioInternacional PwCInovação em Gestão PúblicaAbril 2011

www.pwc.com/br

II Simpósio Internacional PwC - Inovação em Gestão Pública

Agenda

1. PwC

2. Global PPP context

3. What is PPP

4. Payment Mechanisms and Demand Risk

5. Alternative Financing Models

2

II Simpósio Internacional PwC - Inovação em Gestão Pública

PwC

3

II Simpósio Internacional PwC - Inovação em Gestão Pública

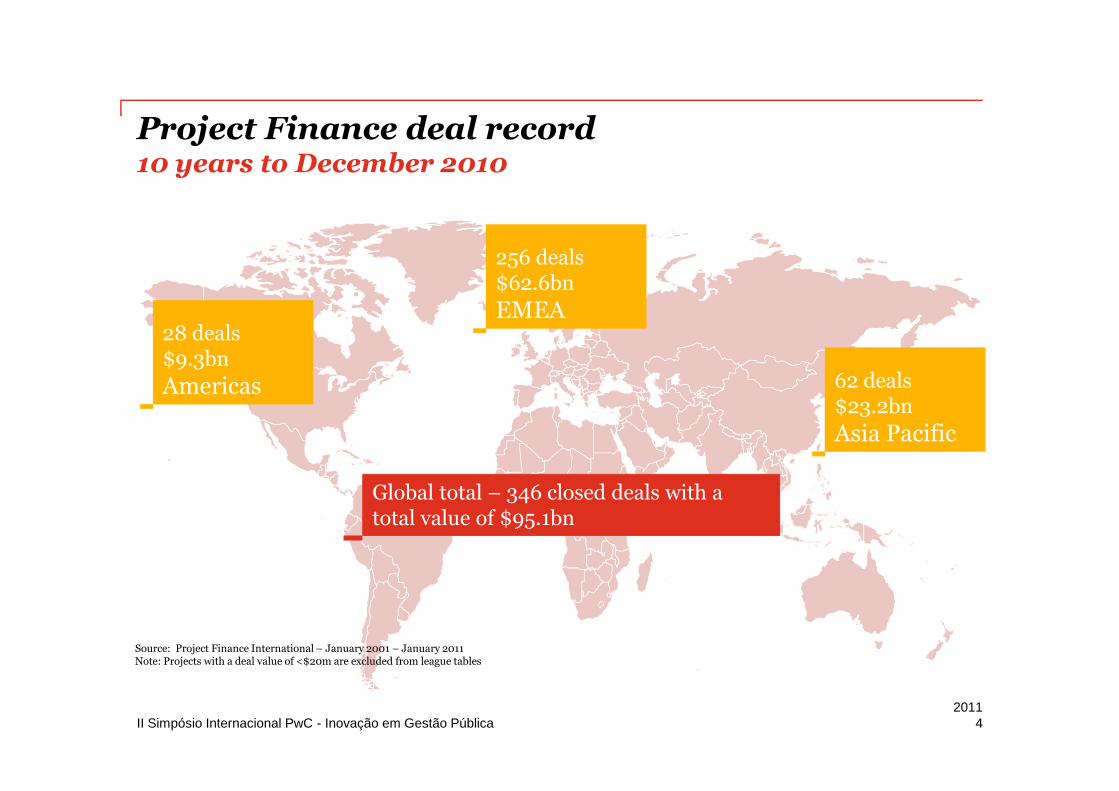

Project Finance deal record10 years to December 2010

42011

Source: Project Finance International – January 2001 – January 2011Note: Projects with a deal value of <$20m are excluded from league tables

256 deals$62.6bn

EMEA

62 deals$23.2bn

Asia Pacific

28 deals$9.3bn

Americas

Global total – 346 closed deals with atotal value of $95.1bn

II Simpósio Internacional PwC - Inovação em Gestão Pública

Latest league tablesProject Finance International – Global closed deals

52011

Global by number of closed deals for 2010

Source: Project Finance International, January 2011 Source: Project Finance International, January 2011

Global by value of closed deals for 2010

Rank Adviser No. ofdeals

Value(US$’m)

1 PwC 34 12,136

2 Ernst & Young 29 4,705

3 KPMG 27 9,934

4 RBC 16 12,033

5= Macquarie 15 11,682

5= Deloitte 15 4,958

7 Deutsche 11 2,305

8 HSBC 7 8,672

9 SBI Capital 4 4,043

10= Standard Chartered 3 8,764

10= Natixis 3 4,600

10= Investec 3 1,773

Rank Adviser Value(US$’m)

No. ofdeals

1 PwC 12,136 34

2 RBC 12,033 16

3 Macquarie 11,682 15

4 KPMG 9,934 27

5 Standard Chartered 8,764 3

6 HSBC 8,672 7

7 SG 8,600 2

8 Credit Agricole 8,500 1

9 Riyad 7,500 1

10 Deloitte 4,958 15

globally with 34 closed

deals for 2010

1stglobally by value

of closed deals for 2010Total deal value of

$12,136m

1st

II Simpósio Internacional PwC - Inovação em Gestão Pública

Global PPP Context

6

II Simpósio Internacional PwC - Inovação em Gestão Pública

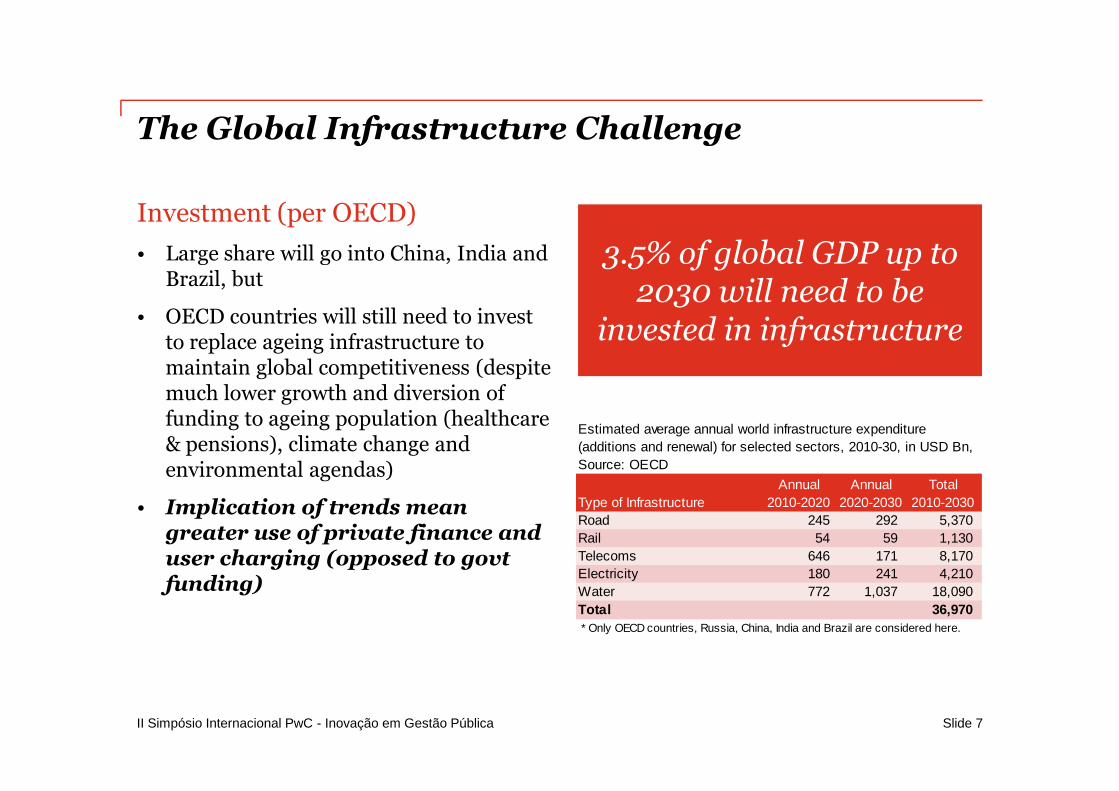

The Global Infrastructure Challenge

Investment (per OECD)

• Large share will go into China, India andBrazil, but

• OECD countries will still need to investto replace ageing infrastructure tomaintain global competitiveness (despitemuch lower growth and diversion offunding to ageing population (healthcare& pensions), climate change andenvironmental agendas)

• Implication of trends meangreater use of private finance anduser charging (opposed to govtfunding)

Slide 7

3.5% of global GDP up to2030 will need to be

invested in infrastructure

Annual Annual Total

Type of Infrastructure 2010-2020 2020-2030 2010-2030

Road 245 292 5,370

Rail 54 59 1,130

Telecoms 646 171 8,170

Electricity 180 241 4,210

Water 772 1,037 18,090

Total 36,970

* Only OECD countries, Russia, China, India and Brazil are considered here.

Estimated average annual world infrastructure expenditure

(additions and renewal) for selected sectors, 2010-30, in USD Bn,

Source: OECD

II Simpósio Internacional PwC - Inovação em Gestão Pública

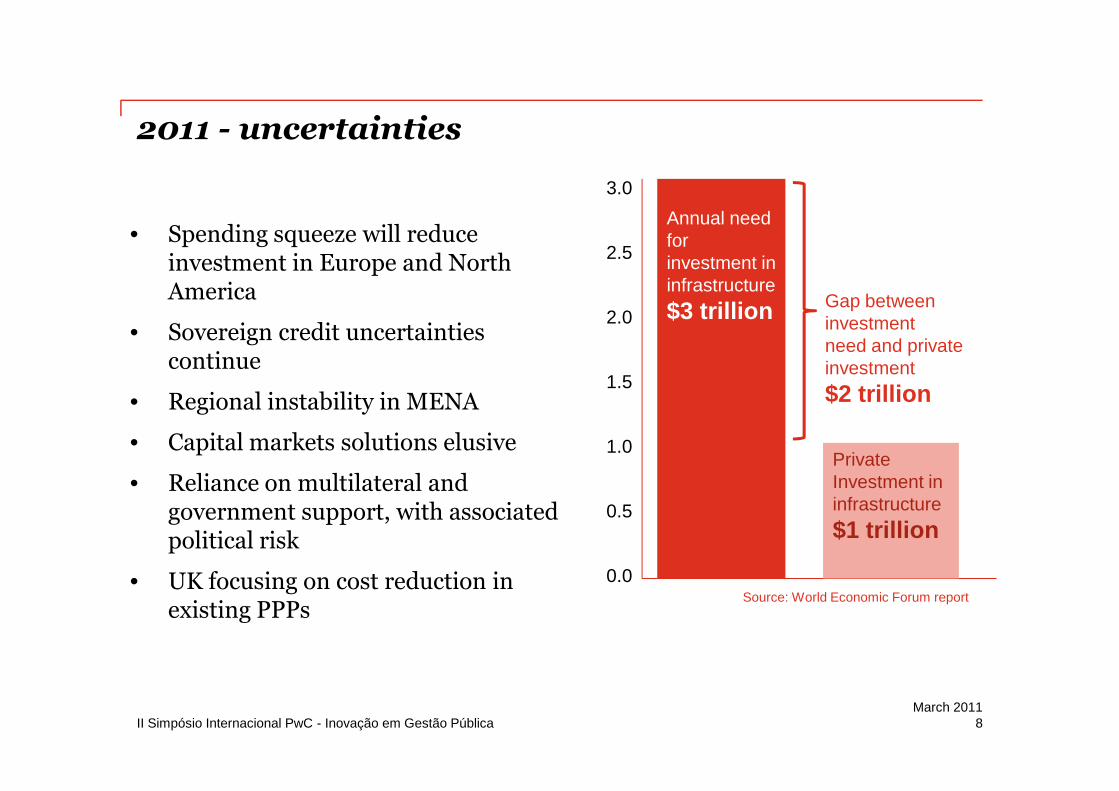

2011 - uncertainties

8March 2011

• Spending squeeze will reduceinvestment in Europe and NorthAmerica

• Sovereign credit uncertaintiescontinue

• Regional instability in MENA

• Capital markets solutions elusive

• Reliance on multilateral andgovernment support, with associatedpolitical risk

• UK focusing on cost reduction inexisting PPPs

3.0

2.5

2.0

1.5

1.0

0.5

0.0

Gap betweeninvestmentneed and privateinvestment

$2 trillion

PrivateInvestment ininfrastructure

$1 trillion

Annual needforinvestment ininfrastructure

$3 trillion

Source: World Economic Forum report

II Simpósio Internacional PwC - Inovação em Gestão Pública

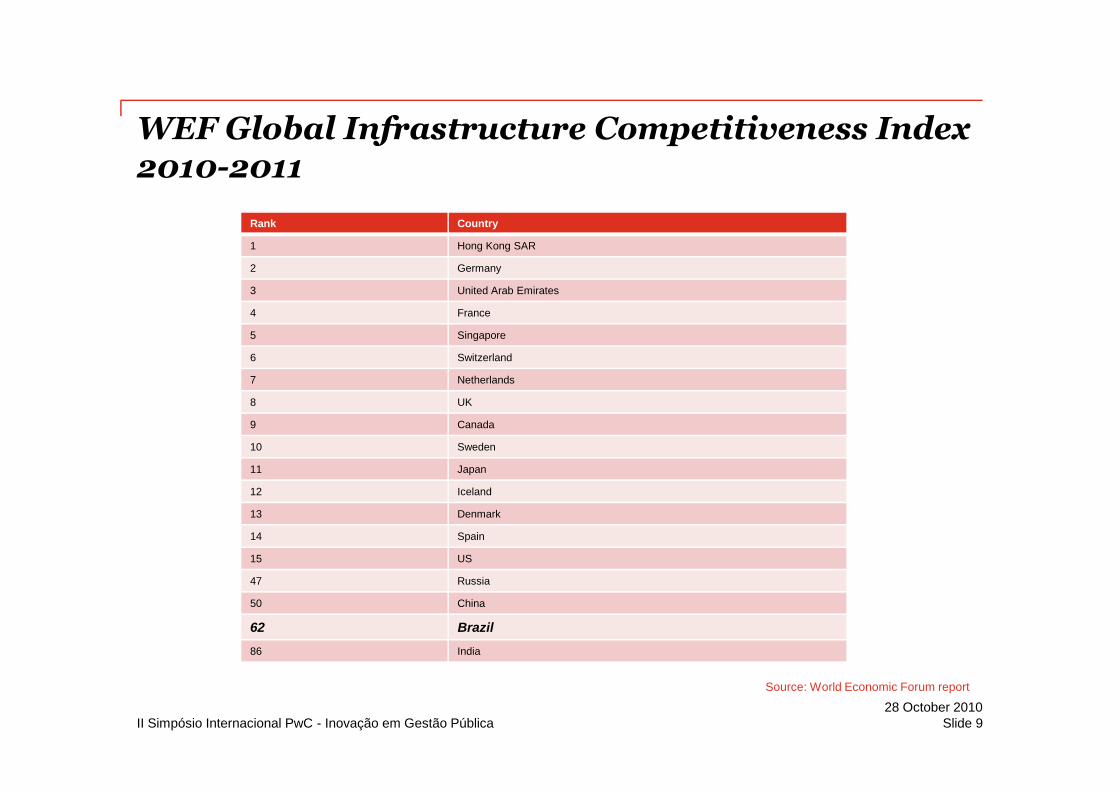

WEF Global Infrastructure Competitiveness Index2010-2011

Rank Country

1 Hong Kong SAR

2 Germany

3 United Arab Emirates

4 France

5 Singapore

6 Switzerland

7 Netherlands

8 UK

9 Canada

10 Sweden

11 Japan

12 Iceland

13 Denmark

14 Spain

15 US

47 Russia

50 China

62 Brazil

86 India

Slide 928 October 2010

Source: World Economic Forum report

II Simpósio Internacional PwC - Inovação em Gestão Pública

0

20

40

60

80

100

120

140%

of

GD

P

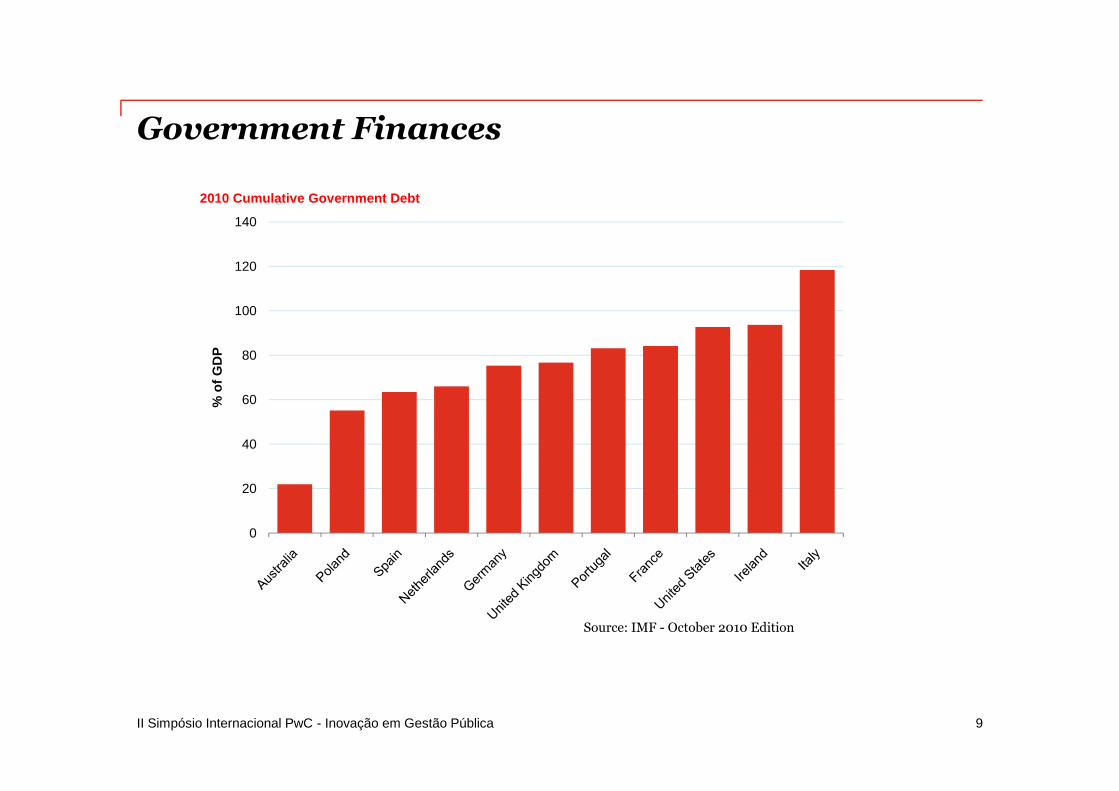

2010 Cumulative Government Debt

Government Finances

9

Source: IMF - October 2010 Edition

II Simpósio Internacional PwC - Inovação em Gestão Pública

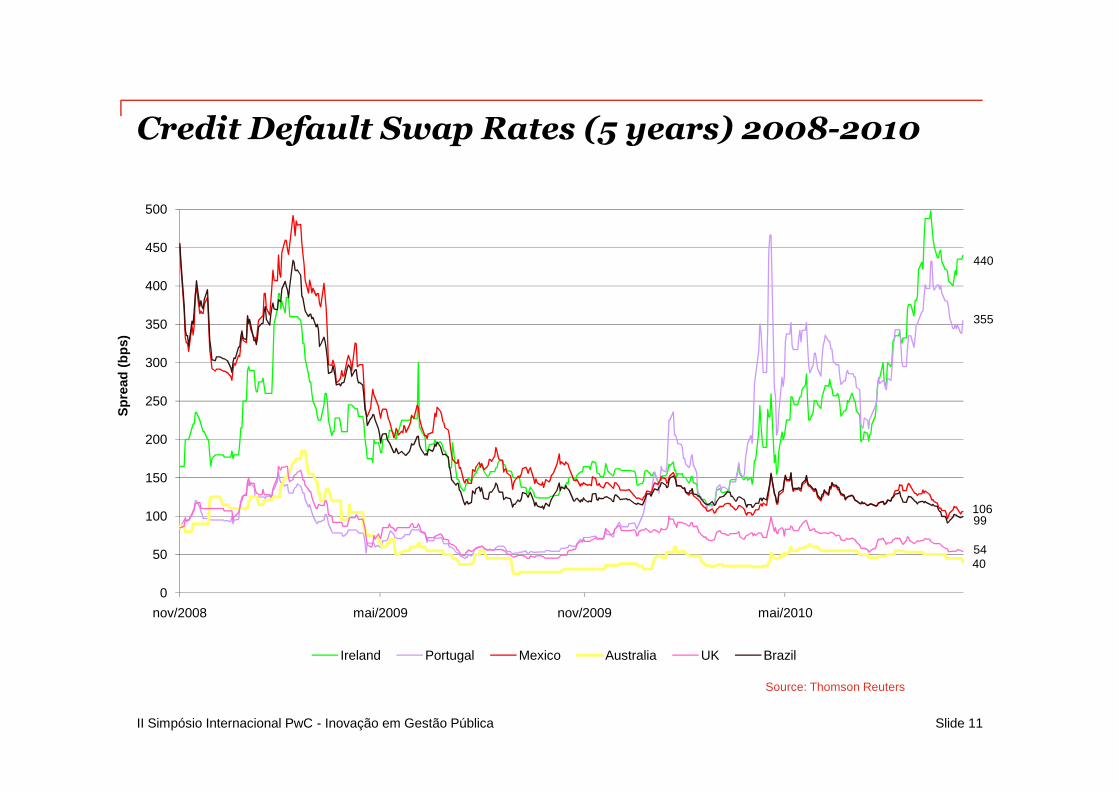

Credit Default Swap Rates (5 years) 2008-2010

Slide 11

Source: Thomson Reuters

0

50

100

150

200

250

300

350

400

450

500

nov/2008 mai/2009 nov/2009 mai/2010

Sp

read

(bp

s)

DateIreland Portugal Mexico Australia UK Brazil

99

440

106

355

5440

II Simpósio Internacional PwC - Inovação em Gestão Pública

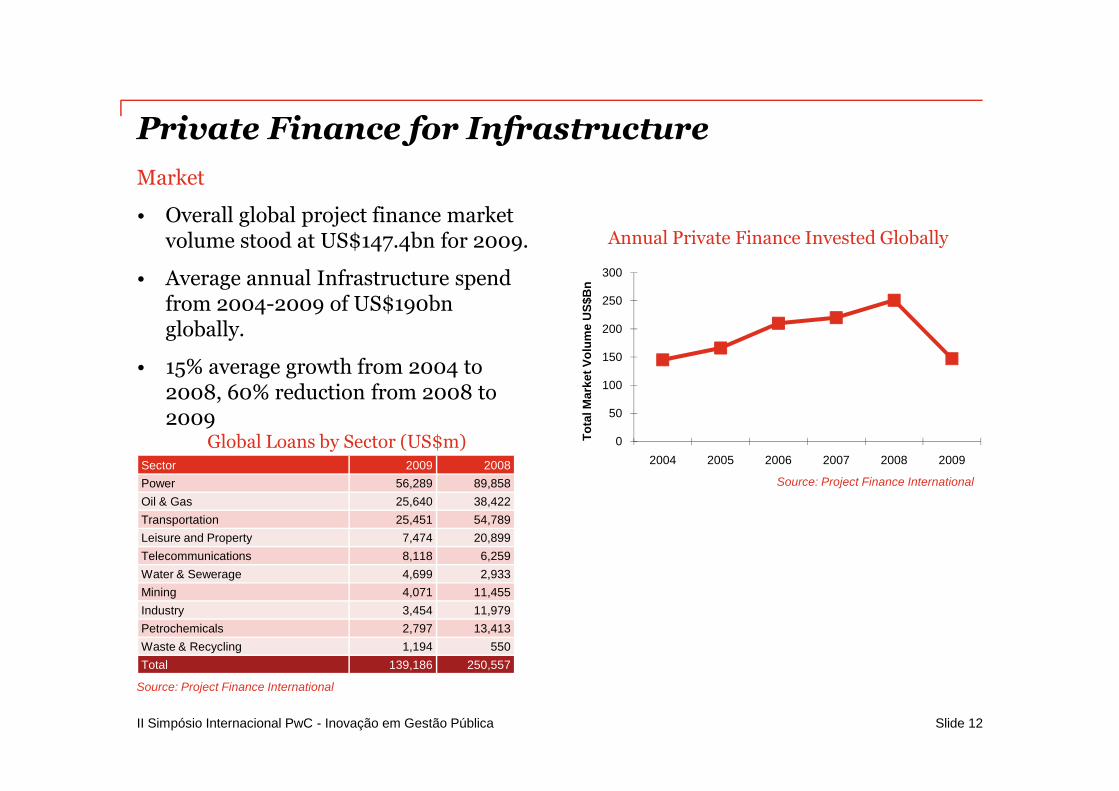

Private Finance for Infrastructure

Market

• Overall global project finance marketvolume stood at US$147.4bn for 2009.

• Average annual Infrastructure spendfrom 2004-2009 of US$190bnglobally.

• 15% average growth from 2004 to2008, 60% reduction from 2008 to2009

Slide 12

0

50

100

150

200

250

300

2004 2005 2006 2007 2008 2009

To

talM

ark

et

Vo

lum

eU

S$

Bn

Annual Private Finance Invested Globally

Sector 2009 2008

Power 56,289 89,858

Oil & Gas 25,640 38,422

Transportation 25,451 54,789

Leisure and Property 7,474 20,899

Telecommunications 8,118 6,259

Water & Sewerage 4,699 2,933

Mining 4,071 11,455

Industry 3,454 11,979

Petrochemicals 2,797 13,413

Waste & Recycling 1,194 550

Total 139,186 250,557

Global Loans by Sector (US$m)

Source: Project Finance International

Source: Project Finance International

II Simpósio Internacional PwC - Inovação em Gestão Pública

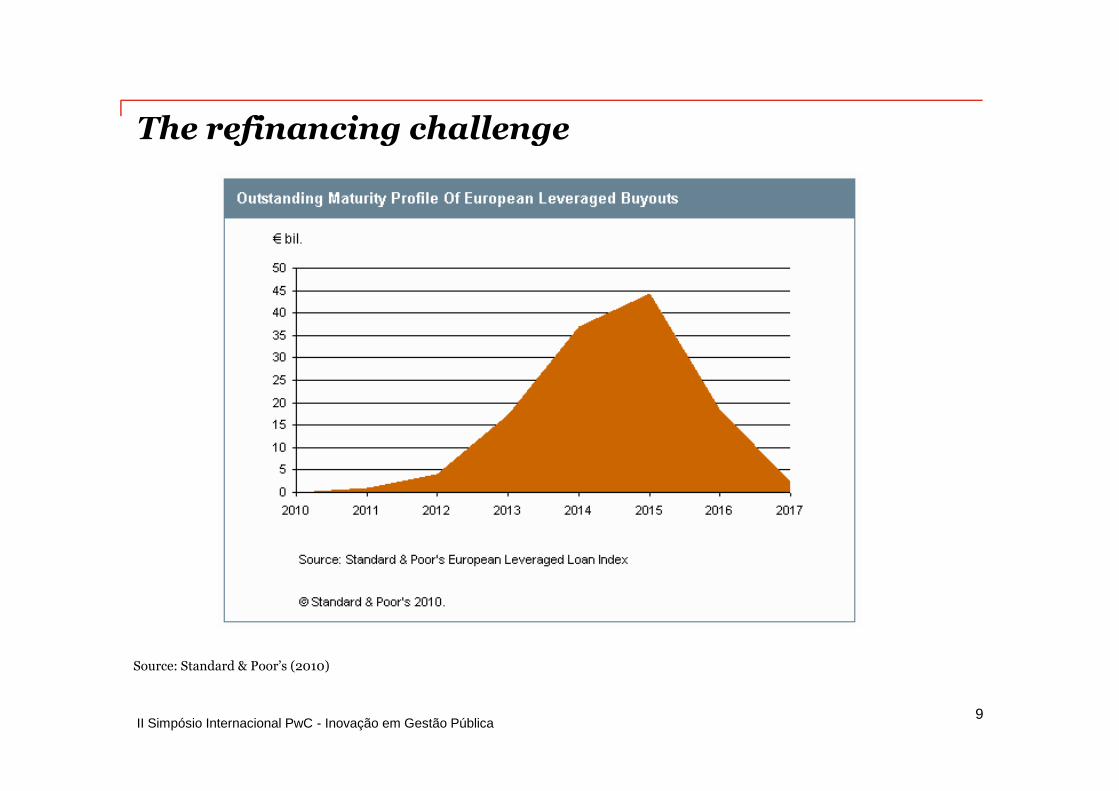

The refinancing challenge

9

Source: Standard & Poor’s (2010)

II Simpósio Internacional PwC - Inovação em Gestão Pública

UK PPP Context

14

II Simpósio Internacional PwC - Inovação em Gestão Pública

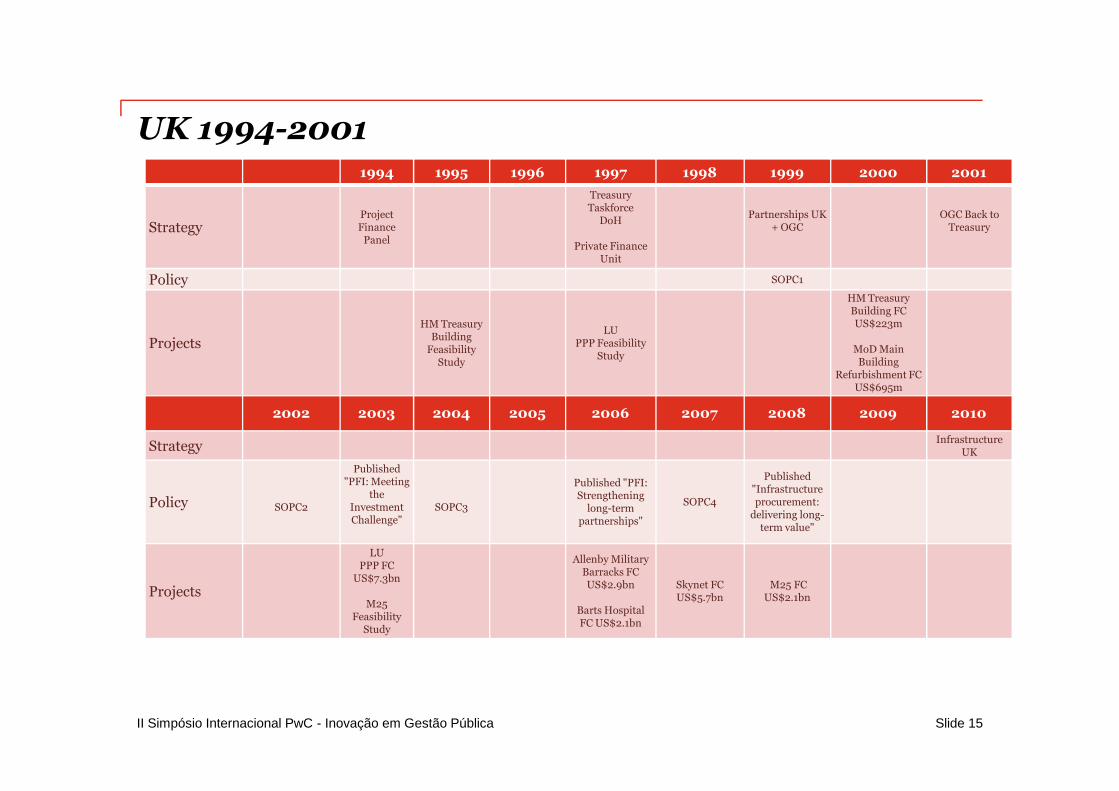

UK 1994-2001

Slide 15

1994 1995 1996 1997 1998 1999 2000 2001

StrategyProjectFinance

Panel

TreasuryTaskforce

DoH

Private FinanceUnit

Partnerships UK+ OGC

OGC Back toTreasury

Policy SOPC1

Projects

HM TreasuryBuilding

FeasibilityStudy

LUPPP Feasibility

Study

HM TreasuryBuilding FCUS$223m

MoD MainBuilding

Refurbishment FCUS$695m

2002 2003 2004 2005 2006 2007 2008 2009 2010

StrategyInfrastructure

UK

Policy SOPC2

Published"PFI: Meeting

theInvestmentChallenge"

SOPC3

Published "PFI:Strengthening

long-termpartnerships"

SOPC4

Published"Infrastructureprocurement:

delivering long-term value"

Projects

LUPPP FC

US$7.3bn

M25Feasibility

Study

Allenby MilitaryBarracks FCUS$2.9bn

Barts HospitalFC US$2.1bn

Skynet FCUS$5.7bn

M25 FCUS$2.1bn

II Simpósio Internacional PwC - Inovação em Gestão Pública

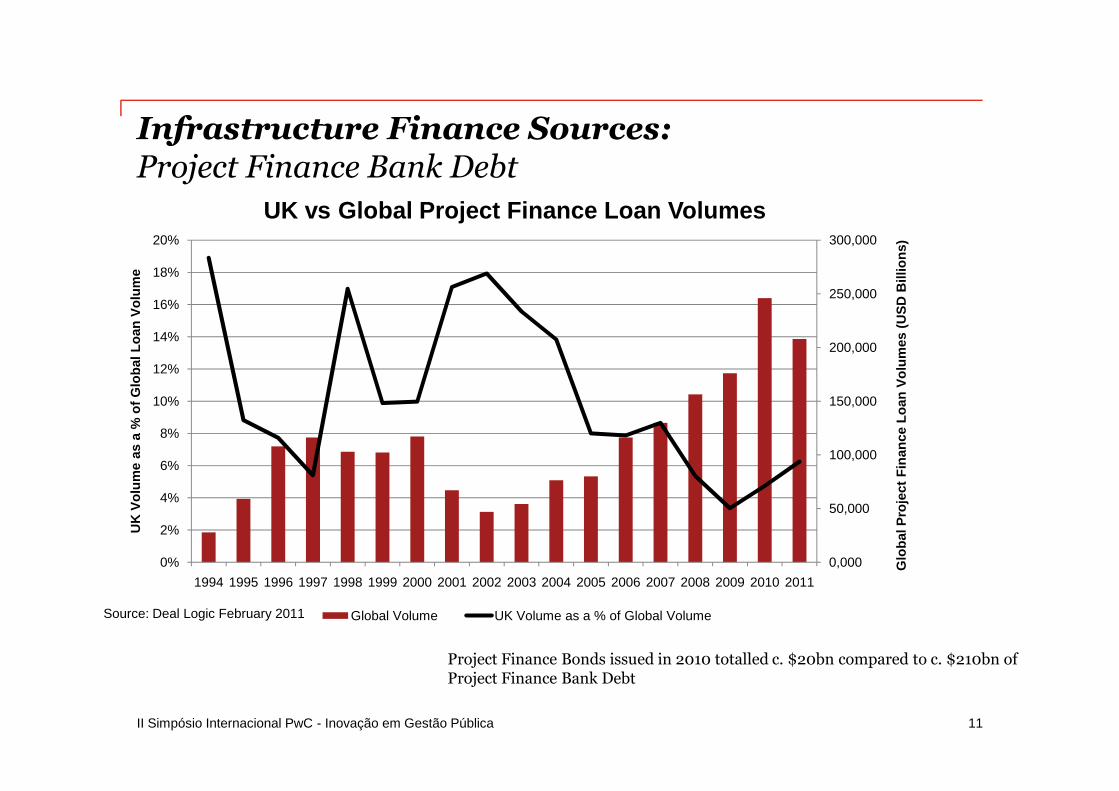

Infrastructure Finance Sources:Project Finance Bank Debt

11

Source: Deal Logic February 2011

0,000

50,000

100,000

150,000

200,000

250,000

300,000

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Glo

balP

roje

ct

Fin

an

ce

Lo

an

Vo

lum

es

(US

DB

illio

ns)

UK

Vo

lum

eas

a%

of

Glo

bal

Lo

an

Vo

lum

e

UK vs Global Project Finance Loan Volumes

Global Volume UK Volume as a % of Global Volume

Project Finance Bonds issued in 2010 totalled c. $20bn compared to c. $210bn ofProject Finance Bank Debt

II Simpósio Internacional PwC - Inovação em Gestão Pública

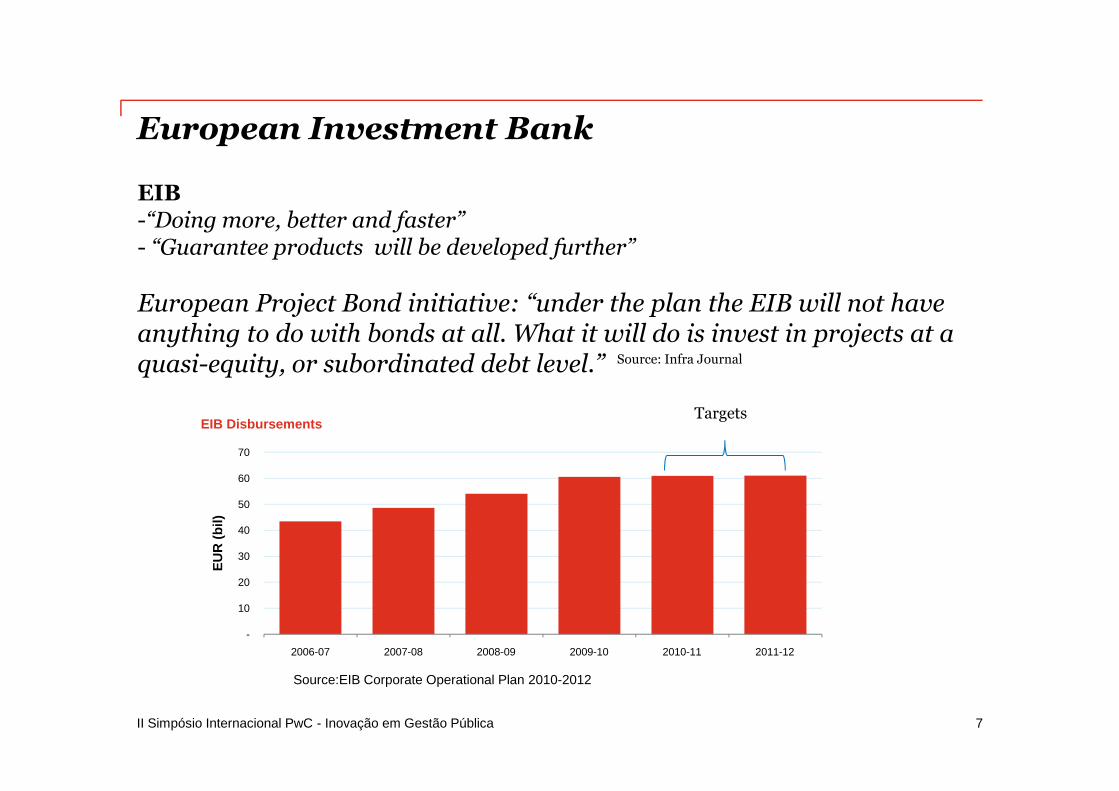

-

10

20

30

40

50

60

70

2006-07 2007-08 2008-09 2009-10 2010-11 2011-12

EU

R(b

il)

EIB Disbursements

European Investment Bank

7

EIB-“Doing more, better and faster”- “Guarantee products will be developed further”

European Project Bond initiative: “under the plan the EIB will not haveanything to do with bonds at all. What it will do is invest in projects at aquasi-equity, or subordinated debt level.”

Targets

Source: Infra Journal

Source:EIB Corporate Operational Plan 2010-2012

II Simpósio Internacional PwC - Inovação em Gestão Pública

What is PPP?

18

II Simpósio Internacional PwC - Inovação em Gestão Pública

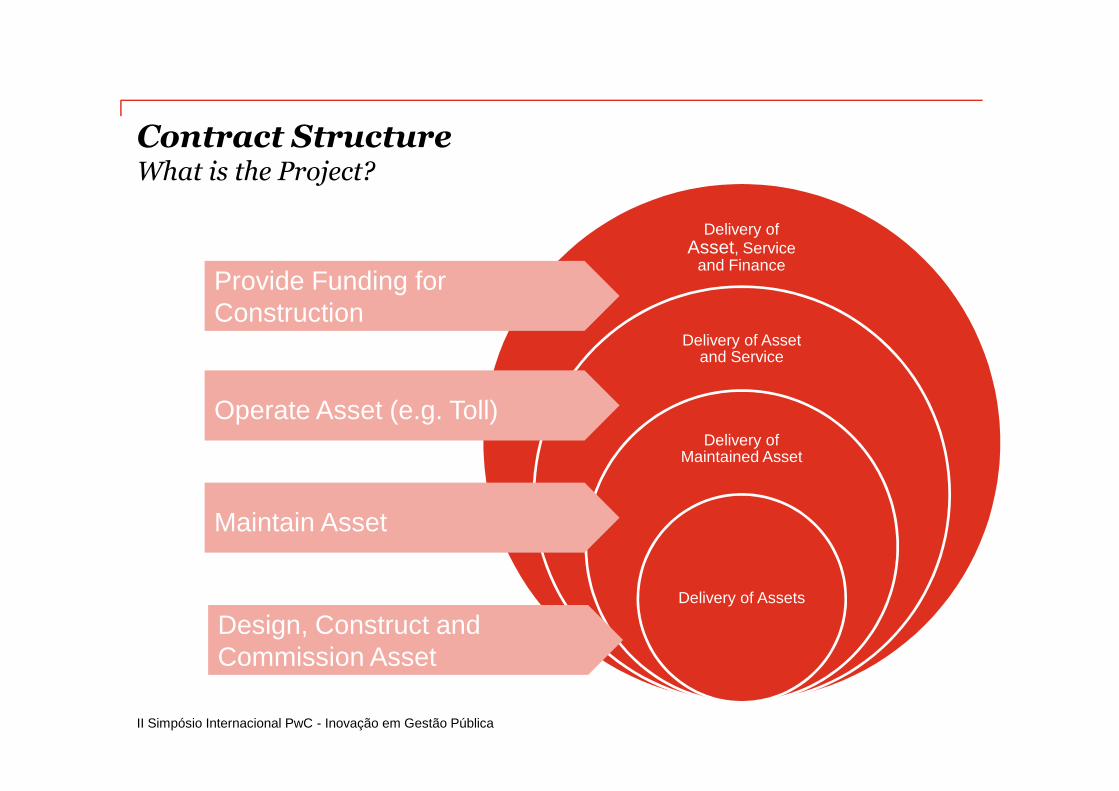

Contract StructureWhat is the Project?

Delivery ofAsset, Service

and Finance

Delivery of Assetand Service

Delivery ofMaintained Asset

Delivery of Assets

Provide Funding forConstruction

Operate Asset (e.g. Toll)

Maintain Asset

Design, Construct andCommission Asset

II Simpósio Internacional PwC - Inovação em Gestão Pública

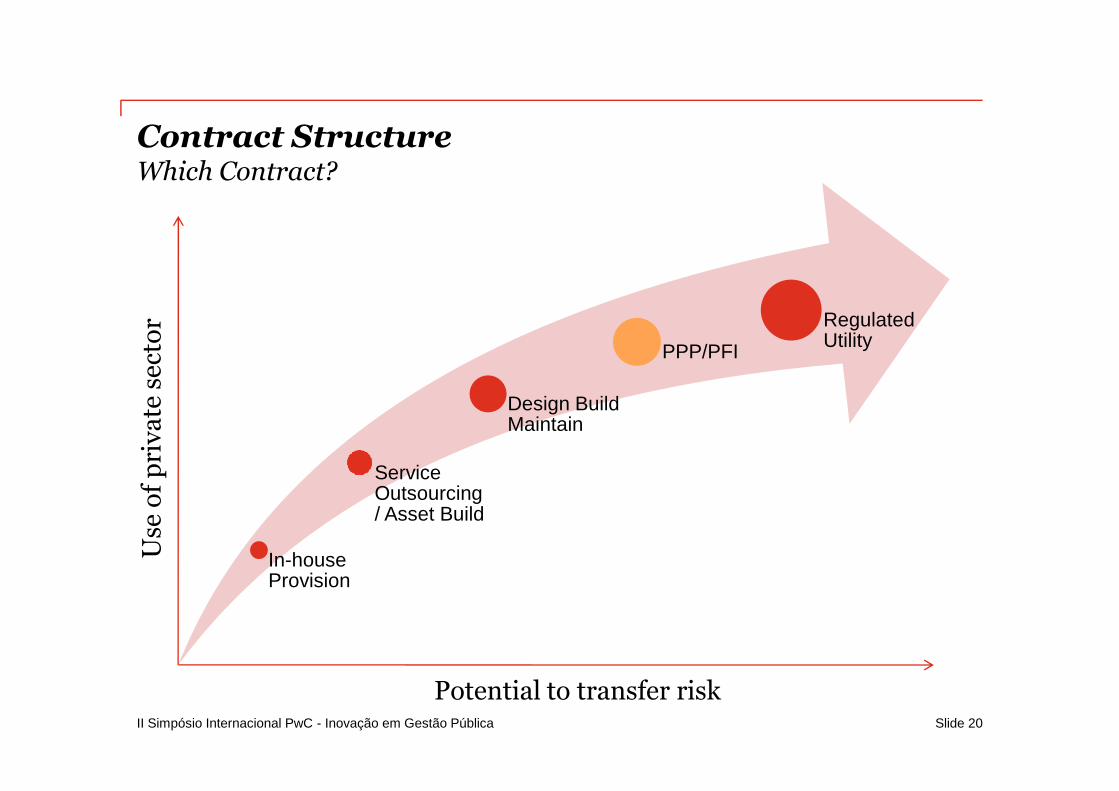

Contract StructureWhich Contract?

Slide 20

In-houseProvision

ServiceOutsourcing/ Asset Build

Design BuildMaintain

PPP/PFI

RegulatedUtility

Use

of

pri

vate

sect

or

Potential to transfer risk

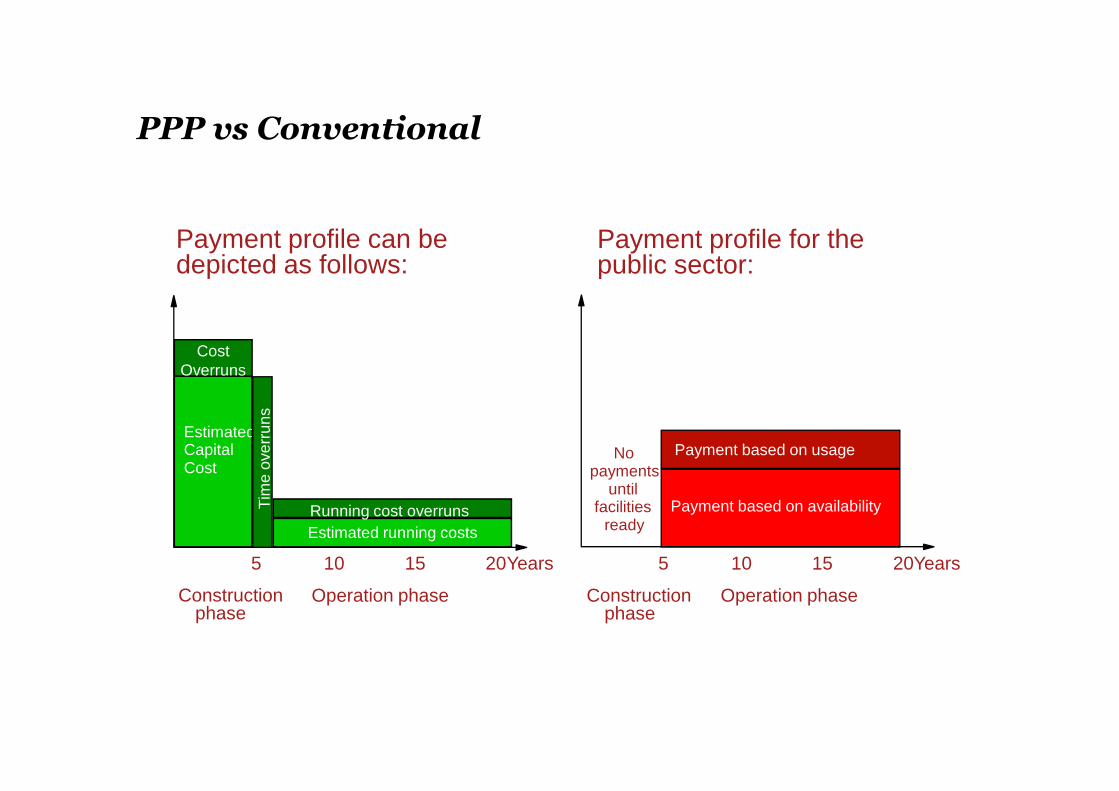

PPP vs Conventional

CostOverruns

Constructionphase

Operation phase

Running cost overruns

Payment based on usageNopayments

untilfacilities

readyPayment based on availability

5 10 15 20 5 10 15 20Years Years

Constructionphase

Operation phase

EstimatedCapitalCost

Estimated running costs

Payment profile can bedepicted as follows:

Payment profile for thepublic sector:

Tim

eo

verr

un

s

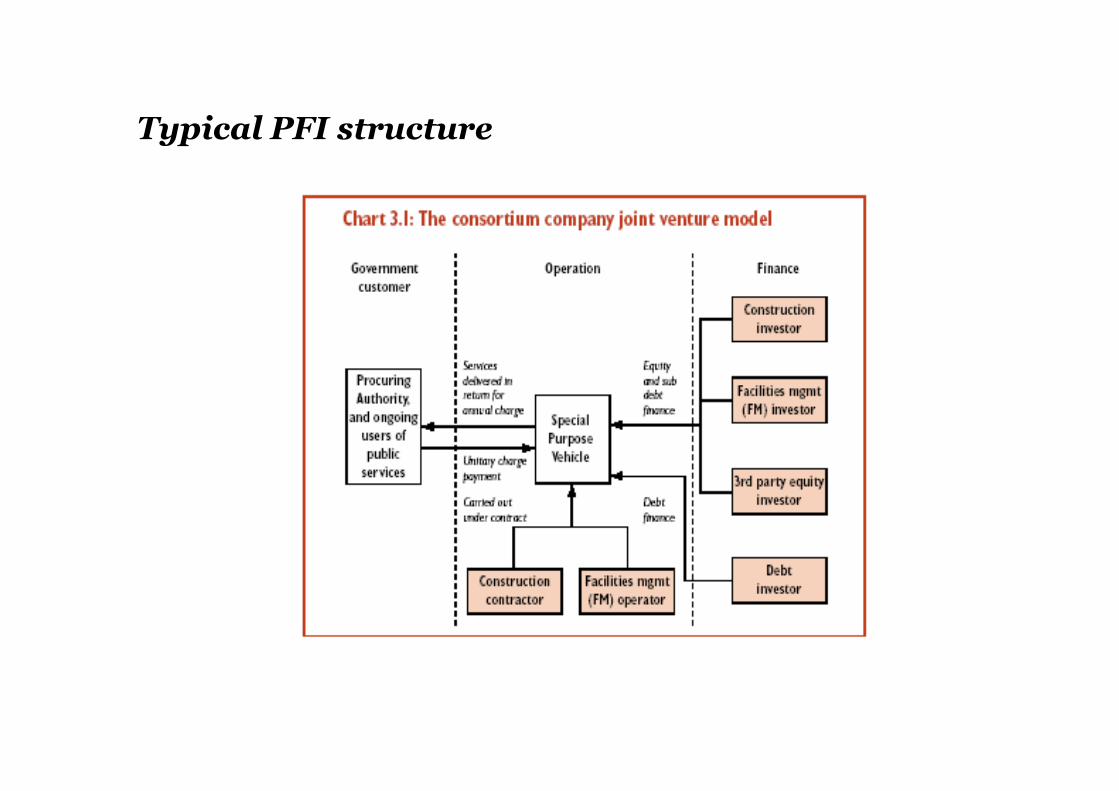

Typical PFI structure

II Simpósio Internacional PwC - Inovação em Gestão Pública

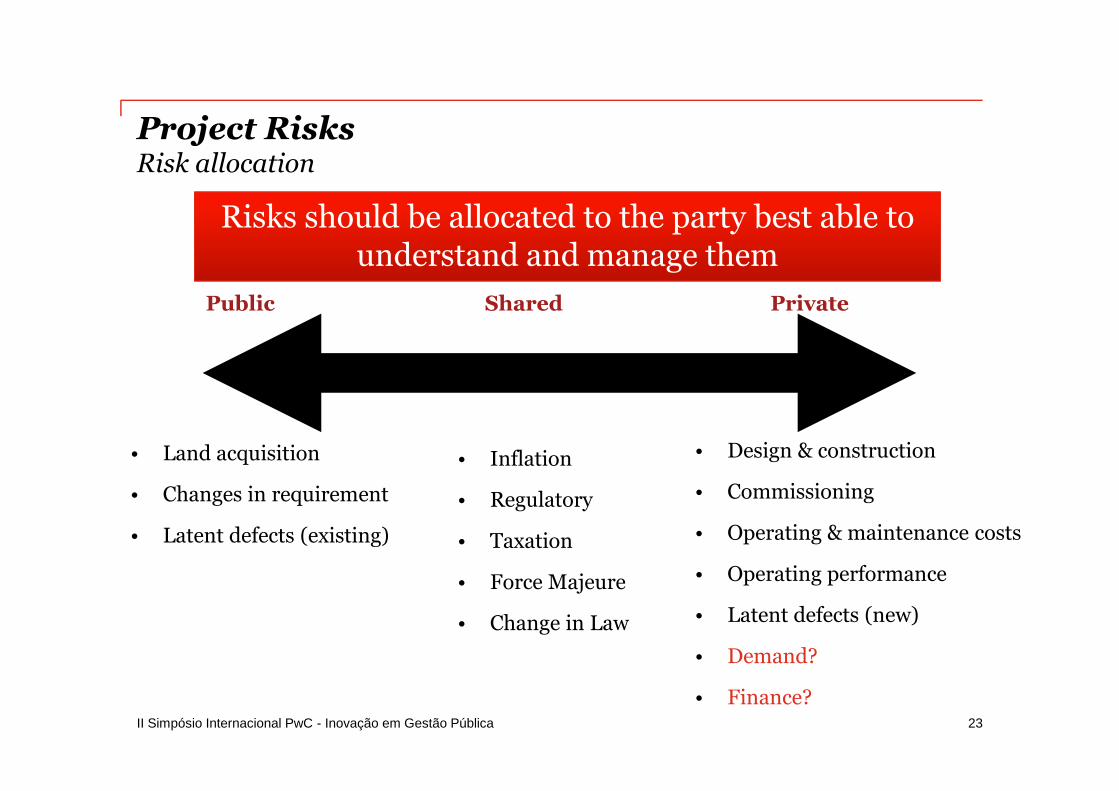

Project RisksRisk allocation

23

Public Shared Private

• Land acquisition

• Changes in requirement

• Latent defects (existing)

• Inflation

• Regulatory

• Taxation

• Force Majeure

• Change in Law

• Design & construction

• Commissioning

• Operating & maintenance costs

• Operating performance

• Latent defects (new)

• Demand?

• Finance?

Risks should be allocated to the party best able tounderstand and manage them

II Simpósio Internacional PwC - Inovação em Gestão Pública

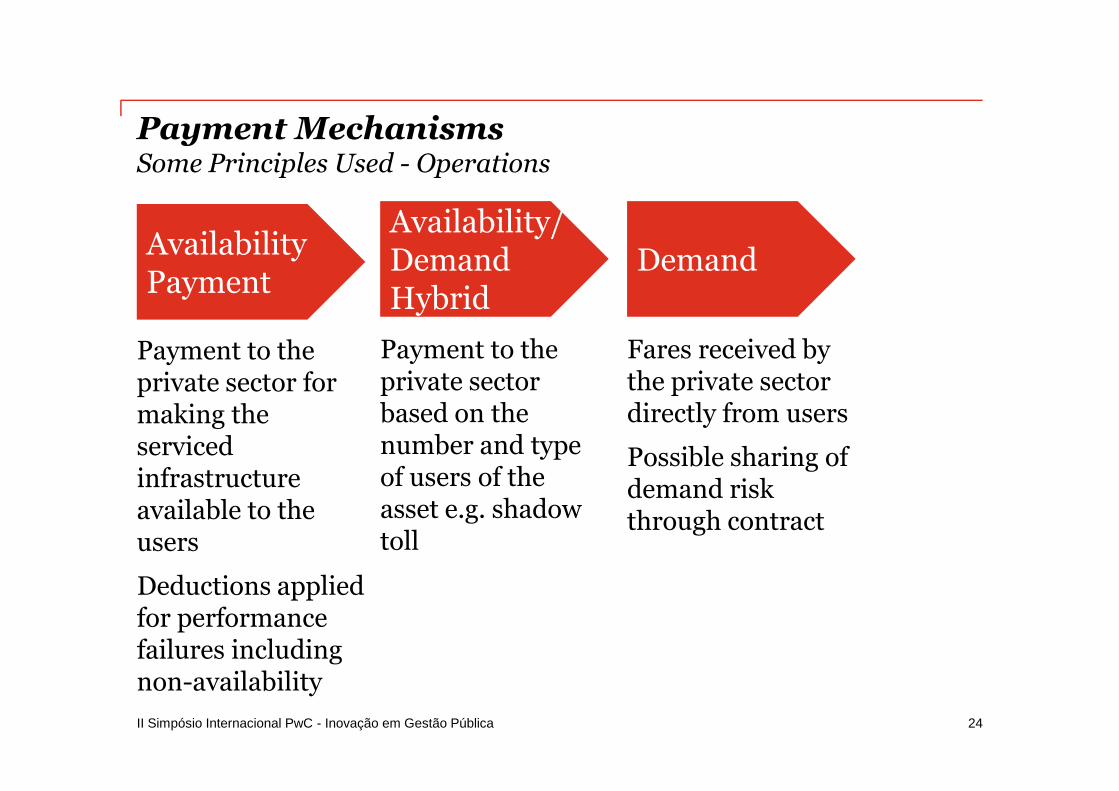

Payment MechanismsSome Principles Used - Operations

Payment to theprivate sector formaking theservicedinfrastructureavailable to theusers

Deductions appliedfor performancefailures includingnon-availability

24

AvailabilityPayment

Payment to theprivate sectorbased on thenumber and typeof users of theasset e.g. shadowtoll

Availability/DemandHybrid

Fares received bythe private sectordirectly from users

Possible sharing ofdemand riskthrough contract

Demand

II Simpósio Internacional PwC - Inovação em Gestão Pública

Demand RiskIn Passenger Rail Projects

Dec 2010

• Passenger revenues can seldom pay for the costs of a new passengerrail line whether metro/underground or tram/ over ground.

• New passenger transport projects normally require subsidies (eitherduring construction or operations).

• If demand risk is transferred to the private sector, concessionaireswill likely seek protection or compensation against changes incompeting modes of transport. eg bus services

II Simpósio Internacional PwC - Inovação em Gestão Pública

Demand RiskIn Passenger Rail Projects

Dec 2010

• Many examples of over-optimistic demand forecasts for passengerrail projects: Eurotunnel, Las Vegas monorail, Sydney airport link,Croydon Tramlink etc.

• (Well publicised financial failures of toll roads in Australia likeCross City tunnel, Lane Cove tunnel led to Availability paymentbased road project for Peninsula Link in Melbourne)

• This does not mean that passenger rail projects should not useprivate finance…

• But it is important to decide how much demand risk to transfer tothe private sector and how much to retain for the public sector.

II Simpósio Internacional PwC - Inovação em Gestão Pública

Why use PPP and private finance?

Dec 2010

• It enables risk transfer away from the taxpayer

• Whole life costs can be managed transparently

• Provides budgetary certainty

• Payments are related to outcomes

II Simpósio Internacional PwC - Inovação em Gestão Pública

Alternative Funding Models

28

II Simpósio Internacional PwC - Inovação em Gestão Pública

Alternative Financing Models

29March 2011

• Direct government lending (e.g. TIFU in UK)

• Direct government lending but guaranteed by private sector (e.g. CreditGuarantee Finance in UK)

• Indirect government lending: rise of state-owned infrastructure ordevelopment banks (e.g. EIB in Europe, Banobras in Mexico, DBSA inSouth Africa, BNDES in Brazil)

• Forfeiting/discounting (irrevocable payments by authorities e.g. 100% inGermany, 80% in France under Cession Dailly)

• Capital Grants (e.g. roads in Holland)

• Equity only models (no private debt e.g. St Johns Hospital in Vancouver)

• Construction Finance/DBF (e.g. Infrastructure Ontario)

• Tax-advantaged finance (e.g. munibond market in the USA)

This publication has been prepared for general guidance on matters of interest only, and doesnot constitute professional advice. You should not act upon the information contained in thispublication without obtaining specific professional advice. No representation or warranty(express or implied) is given as to the accuracy or completeness of the information containedin this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, itsmembers, employees and agents do not accept or assume any liability, responsibility or duty ofcare for any consequences of you or anyone else acting, or refraining to act, in reliance on theinformation contained in this publication or for any decision based on it.

© 2010 PricewaterhouseCoopers LLP. All rights reserved. In this document, “PwC” refers toPricewaterhouseCoopers LLP (a limited liability partnership in the United Kingdom) which is amember firm of PricewaterhouseCoopers International Limited, each member firm of which is aseparate legal entity.

![Calendario Fiscal PwC Costa Rica · conformada por siete firmas: PwC Panamá, PwC Costa Rica, PwC El Salvador, PwC Nicaragua, ... Ralph Waldo Emerson [Escritor y Poeta] 15; Mensuales-03:](https://img.pdfslide.tips/doc/110x75/5bb099af09d3f2830e8c5016/calendario-fiscal-pwc-costa-rica-conformada-por-siete-firmas-pwc-panama-pwc.jpg)