Embed Size (px)

Citation preview

International Accounting and Financial Reporting

Summer 2007

William F. O’Brien, MBA, CPA

Session XI-A

Control, Tax & Audit Issues

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-3

Control, Tax & Audit Issues

Strategic Planning Financial Measurement Financial Planning…don’t call it a “Budget” Transfer Pricing Performance Measurement

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-4

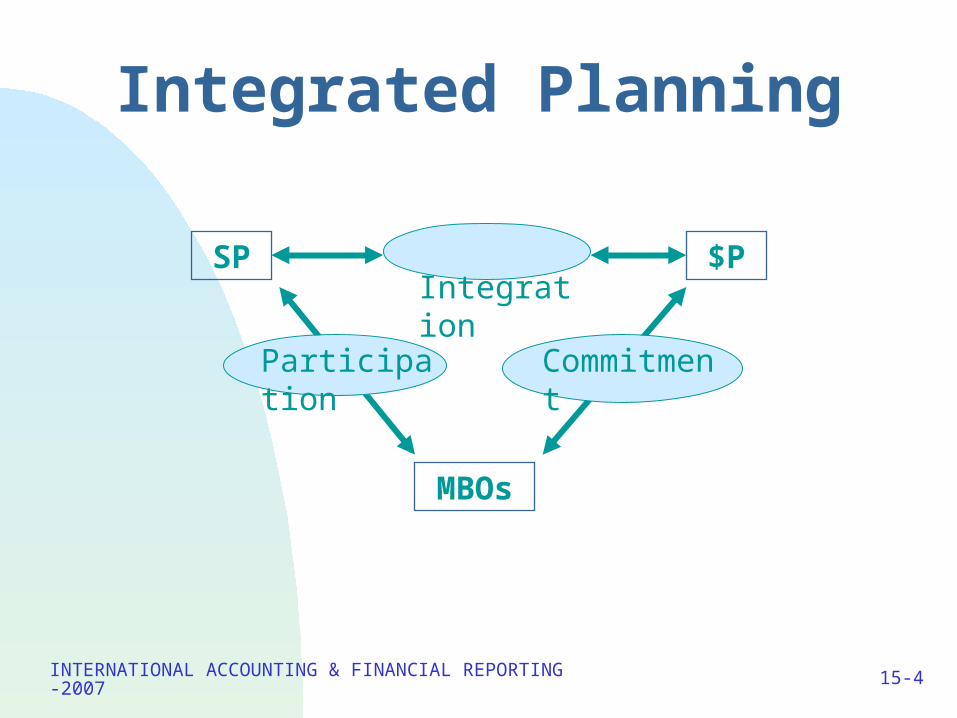

Integrated Planning

SP $P

MBOs

Integration

Participation Commitment

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-5

MNE Planning Stages

Strategic review

Annual operating plan Financial Non-financial

Integration & monitoring

Personal planning & rewards

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-6

Integrated Planning Benefits

Greater clarity & realism Performance stretch Increased motivation More timely intervention Clearer ownership

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-7

Financial Measurement

Varies by region US versus Japan

Numerous targets ROI Sales Quality Market share Income Variance minimization

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-8

Key Financial Planning Questions

Formal process? Who participates? Style of communication? Establishment of targets? International logistics? Time frame? Industry and geography volatility impact? Measurement of variances?

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-9

International Considerations

FX determination

FX impact on results

Resolution of FX fluctuation

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-10

Cross-National Examples

Mexico High participation among local senior managers High participation among local low level

managers Low participation among subsidiary managers

Asia-Pacific High participation

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-11

Cross-National Example…US and

Japan US —12 days longer US: focus on ROI; Japan: focus on sales US is more participative Both are bottoms up Japan: greater focus on action against

variances US: uses plan for evaluation, compensation

and incentives

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-12

Goals of Int’l Transfer Pricing

Strategic goal congruence Preservation of local management discretion Minimization of “built-in” conflicts

Taxes versus duties Local balance of payment status Inflation and politics

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-13

Transfer Pricing Issues

Government regulations and restrictions Tax statutes Tariff and duty rates Currency restrictions Inflation rates Local motivation

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-14

T/P Approaches

Market-based (recommended approach) Cost-based Negotiated rate Advanced pricing agreement General rule

Variable cost plus opportunity cost

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-15

Why Market-Based?

Legal Goal congruence Equity Simplicity

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-16

Taxation

Types Credits versus deductions Other issues Tax planning

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-17

Types of Taxes

Direct Income taxes

Double taxation impact due to dividends Indirect

Value-added taxes (VAT or TVA) See Exhibit 16.1 Paid at transfer point of goods or services Recovery of prior assessment

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-18

Tax Credits and Deductions

Two approaches to offset multinational taxation Credits usually result in more equitable impact See Exhibit 16.2 for an example

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-19

Other Tax Issues

Tax havens Attitudes and avoidance

U.S. foreign source income Sub-part F exception…taxed when earned

Transfer price issues Recall our discussion in Session XVI See pages 479-482 Note IRS Code Section 482

Incentives, rates and tax treaties

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-20

Tax Planning

Exports Withholding issues

Branches No income deferral; good for start-ups with

losses Subsidiaries

Normal sheltering of income until distributed Locations

Influenced by incentives, rates and treaties

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-21

Internal/Operational Auditing Objectives

S-C-O-R-E Safeguarding assets Compliance with laws and regulations Organization goal attainment Reliability of information Effectiveness and efficiency of operations

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-22

Current Governance Climate

Shift to Board focus from Senior Mgmt. focus Global perspective FCPA-Foreign Corrupt Practices Act (1977) COSO-Treadway Commission: Committee of

Sponsoring Organizations (1987) IIA, FEI, IMA, AICPA, AAA

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-23

Foreign Corrupt Practices Act

Passed in 1977 No bribery No influence peddling Facilitating payments are OK

Influences action that must be taken anyway

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-24

MNE Audit Challenges

FX

Language and culture

Legal considerations

Supply of audit professionals

Training

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-25

External Auditors

True and Fair View (TFV) EU base: 4th directive Subject to cultural interpretation

Presents Fairly More standardized meaning

Independent audit environment--varies widely Brazil, Germany, Japan, Netherlands & US

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-26

Other Audit Related Issues

Harmonization of GAAS Same fundamental arguments as GAAP Driven by globalization of capital markets

International Federation of Accountants-IFAC Worldwide equivalent of AICPA Practices, education, ethics Financial and managerial actg. concerns Also involves IT information Compliance is “encouraged”

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-27

International Audit Variances

Note the drive for harmonization on pages 436 - 450

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-28

Institute of Internal Auditors--IIA

Established 1941 Professional body for internal auditors Certification Literature Lobbying Training Code of ethics

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-29

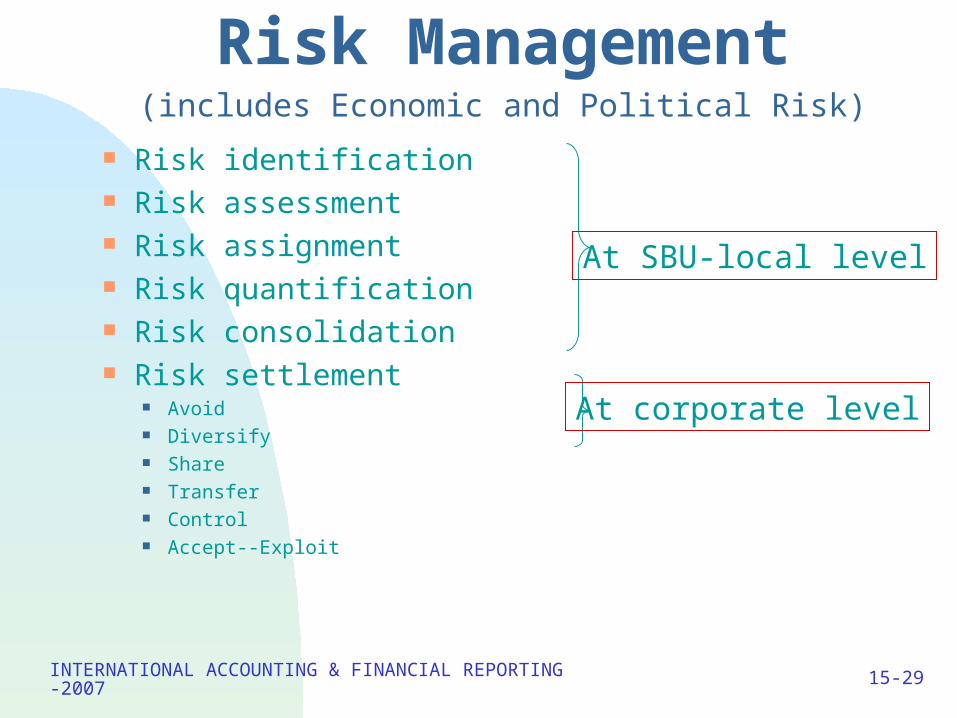

Risk Management(includes Economic and Political Risk)

Risk identification Risk assessment Risk assignment Risk quantification Risk consolidation Risk settlement

Avoid Diversify Share Transfer Control Accept--Exploit

At SBU-local level

At corporate level

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-30

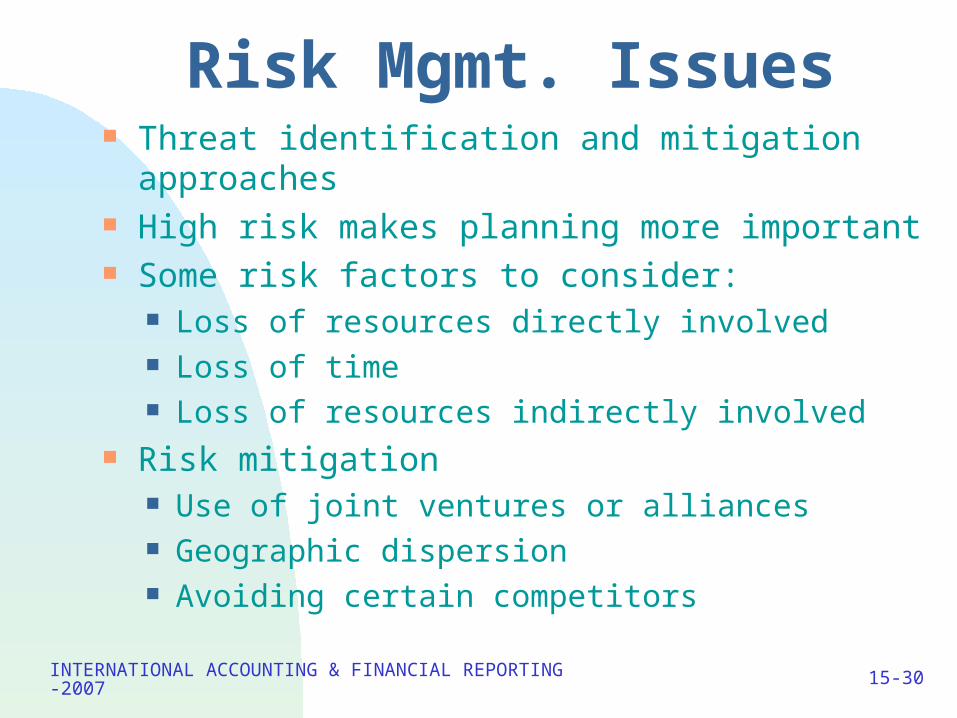

Risk Mgmt. Issues Threat identification and mitigation approaches High risk makes planning more important Some risk factors to consider:

Loss of resources directly involved Loss of time Loss of resources indirectly involved

Risk mitigation Use of joint ventures or alliances Geographic dispersion Avoiding certain competitors

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-31

Keep This Paradigm Shift in Mind

Moving from “Results of Operations”

To “ Operating information for Results”

Session XI-B

Course Wrap-Up

Major Themes

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2007

15-33

Major Themes

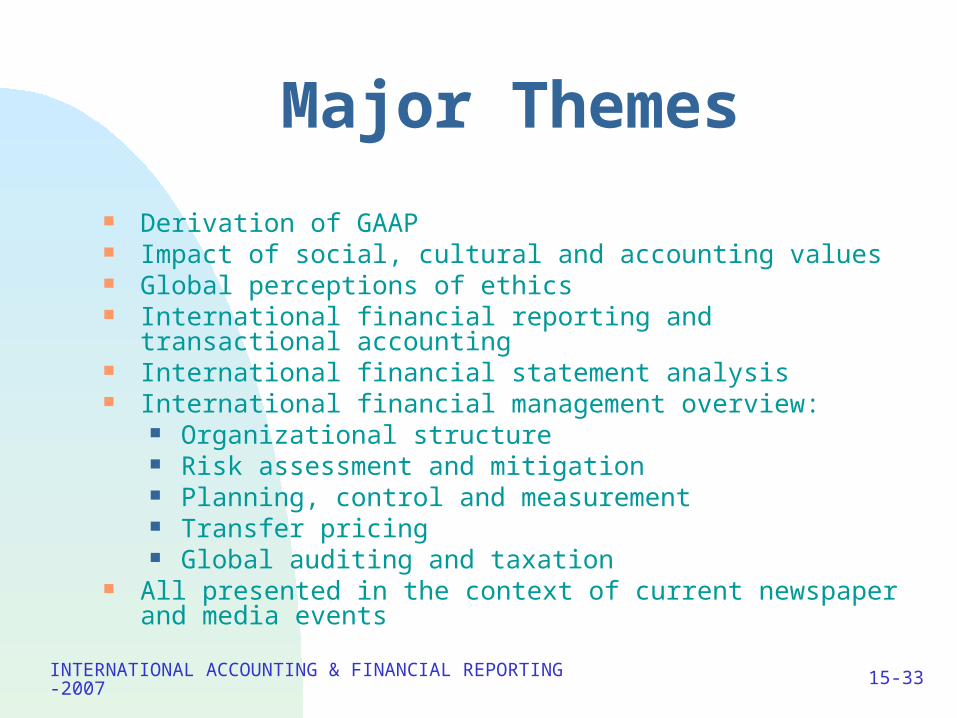

Derivation of GAAP Impact of social, cultural and accounting values Global perceptions of ethics International financial reporting and transactional accounting International financial statement analysis International financial management overview:

Organizational structure Risk assessment and mitigation Planning, control and measurement Transfer pricing Global auditing and taxation

All presented in the context of current newspaper and media events