Embed Size (px)

Citation preview

Private & Confidential

I Wanna Dance with Somebody

19th November 12

Market Study Hungary

- 1 -

Table of Contents

Demography

Willingness to pay, Music Market Opportunity

BtoC : Online Market opportunity

BtoB : Equipments: Is it a BtoB market ?

Usage

- 2 -

0.1 Country fact sheet

- 3 -

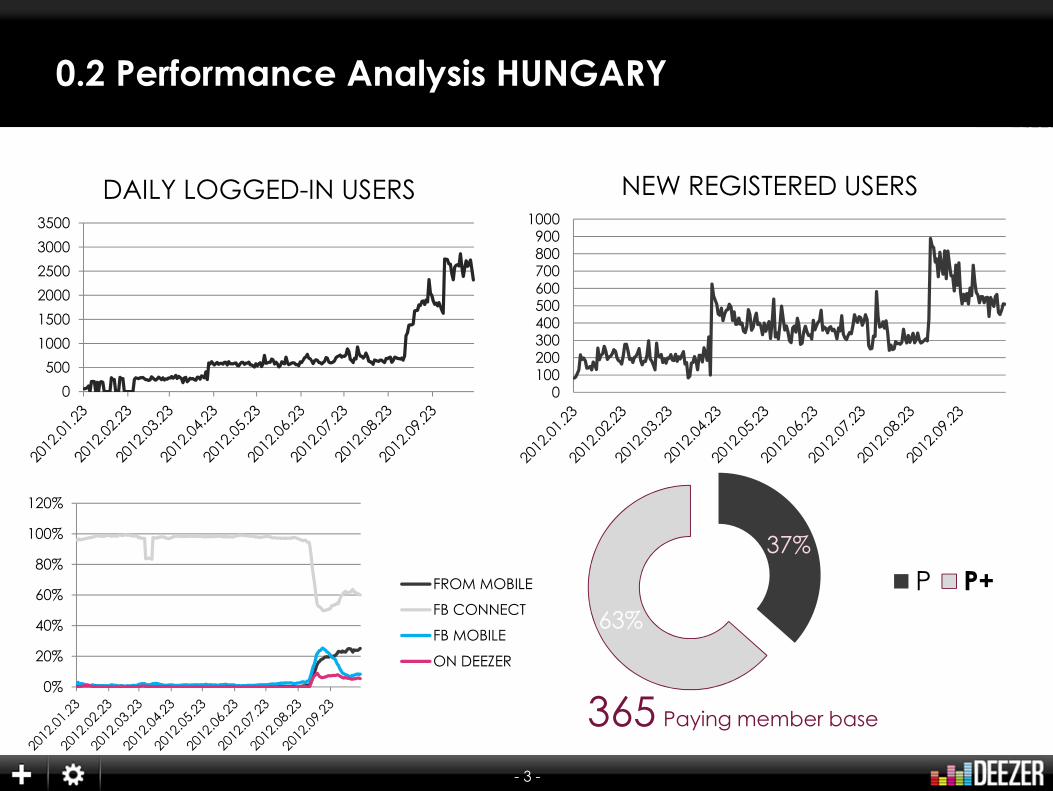

37%

63%

P P+

0100200300400500600700800900

1000

NEW REGISTERED USERS

0

500

1000

1500

2000

2500

3000

3500

DAILY LOGGED-IN USERS

0%

20%

40%

60%

80%

100%

120%

FROM MOBILE

FB CONNECT

FB MOBILE

ON DEEZER

365 Paying member base

0.2 Performance Analysis HUNGARY

- 4 -

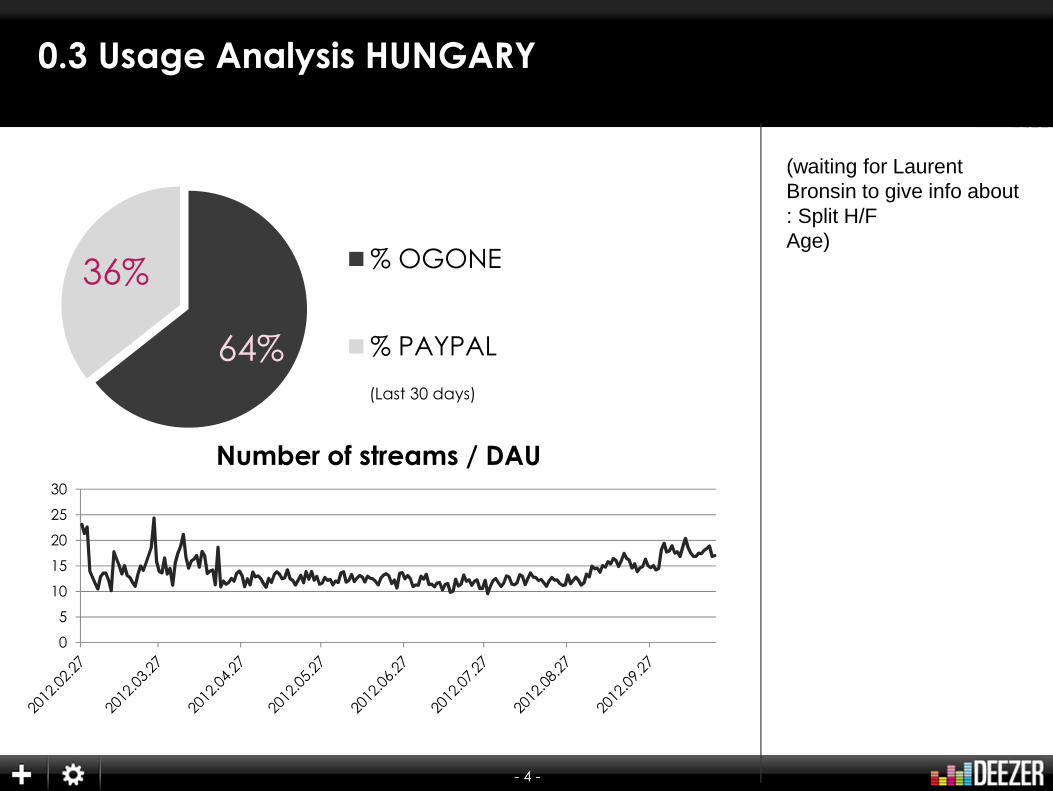

64%

36% % OGONE

% PAYPAL

0

5

10

15

20

25

30

Number of streams / DAU

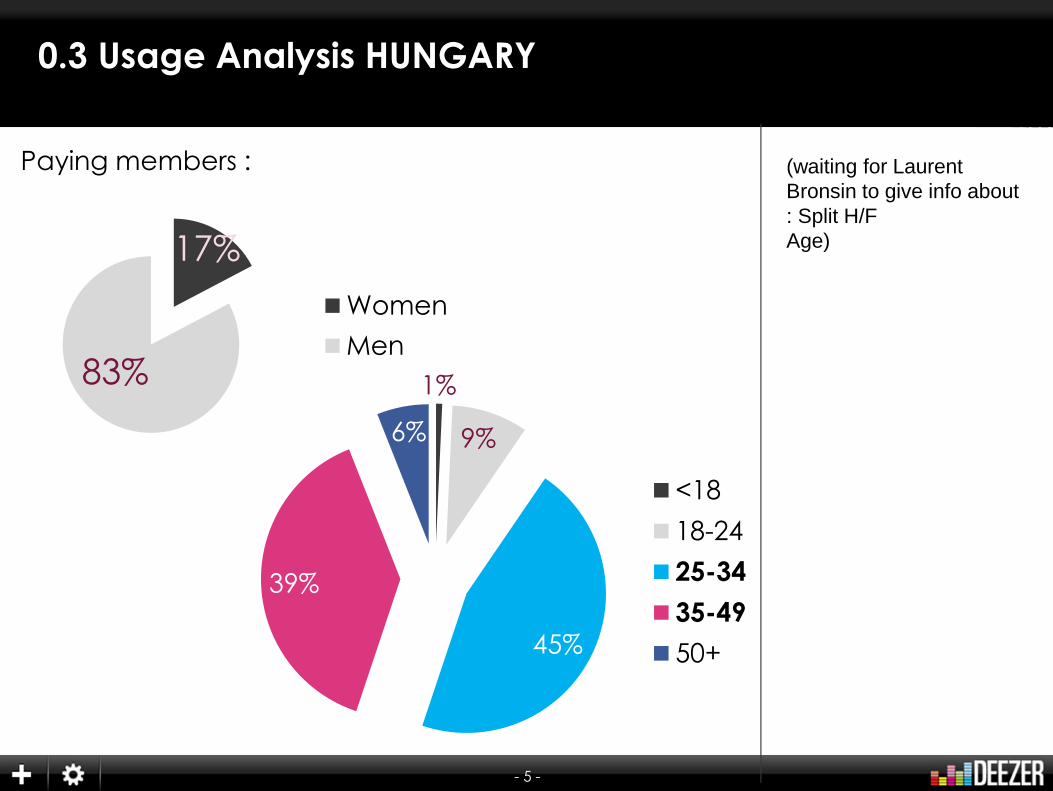

0.3 Usage Analysis HUNGARY

(waiting for Laurent Bronsin to give info about : Split H/FAge)

(Last 30 days)

- 5 -

0.3 Usage Analysis HUNGARY

(waiting for Laurent Bronsin to give info about : Split H/FAge)

Paying members :

1%

9%

45%

39%

6%

<18

18-24

25-34

35-49

50+

17%

83%

Women

Men

- 6 -

The Black Eyed Peas, Elephunk (2003), A&M/will.i.am/lnterscope

Let’s Get It StartedLet’s Get It StartedLet’s Get It StartedLet’s Get It StartedLet’s Get It Started

1. DEMOGRAPHYWhat are the demographic specificities of the

market ? Who should we target ?

- 7 -

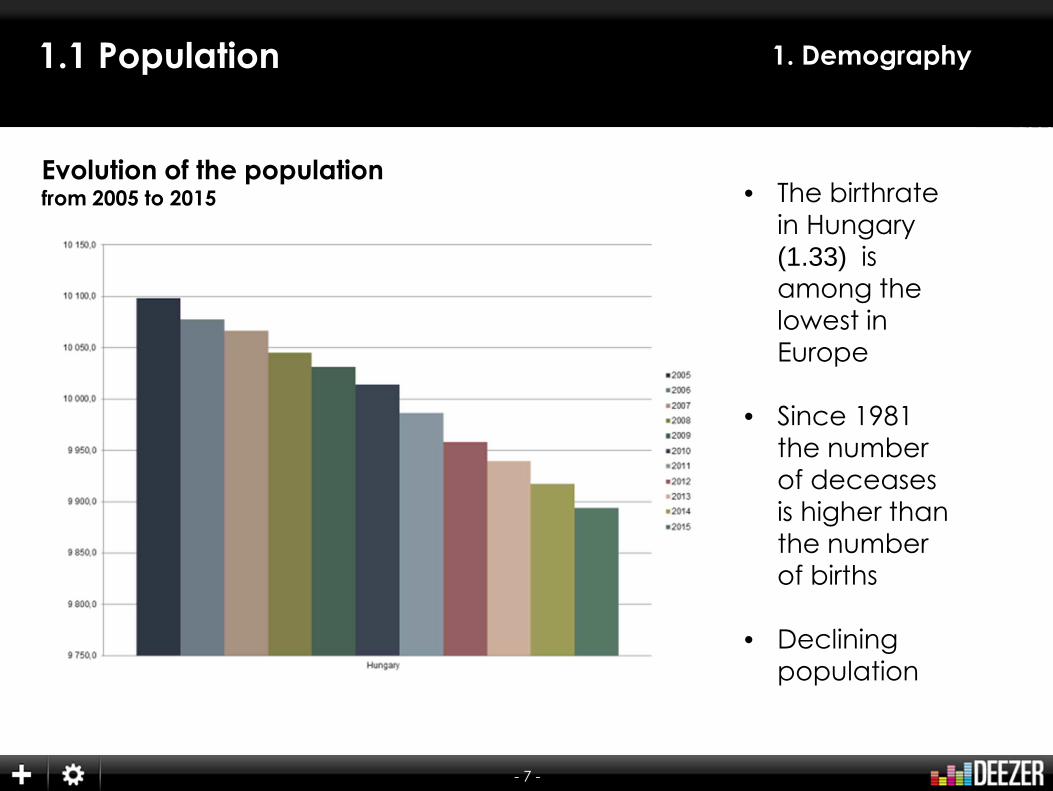

1. Demography1.1 Population

• The birthrate in Hungary (1.33) is among thelowest in Europe

• Since 1981the number of deceases is higher than the number of births

• Declining population

Evolution of the population from 2005 to 2015

- 8 -

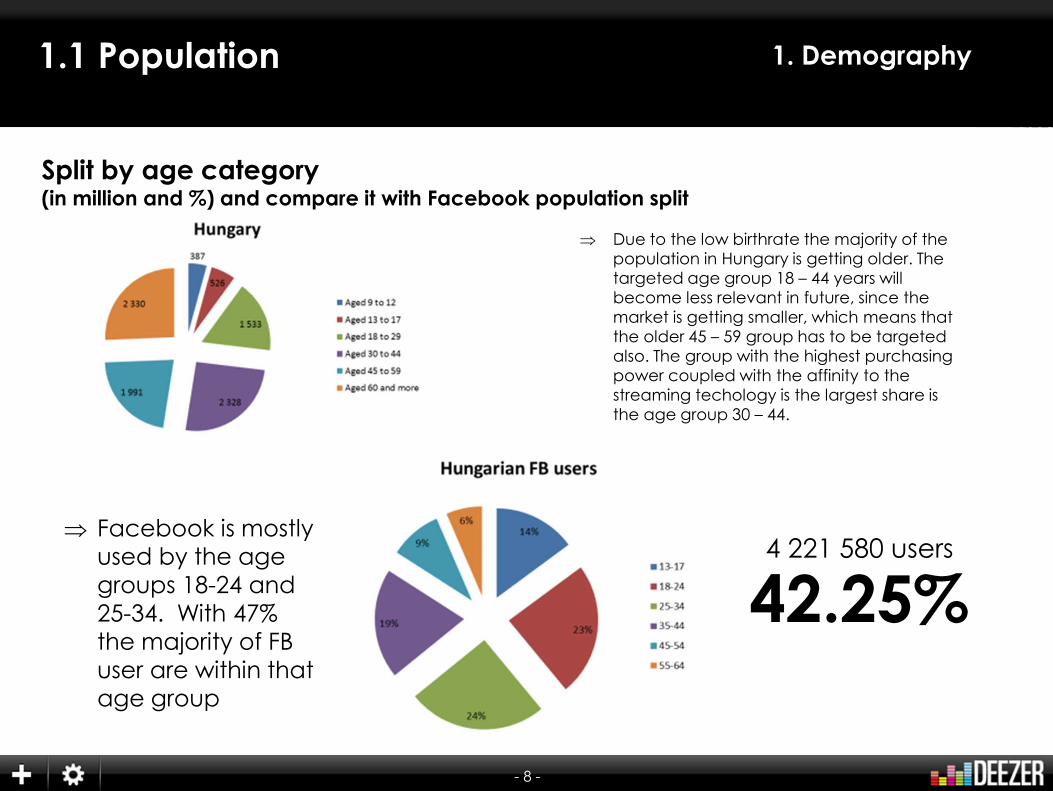

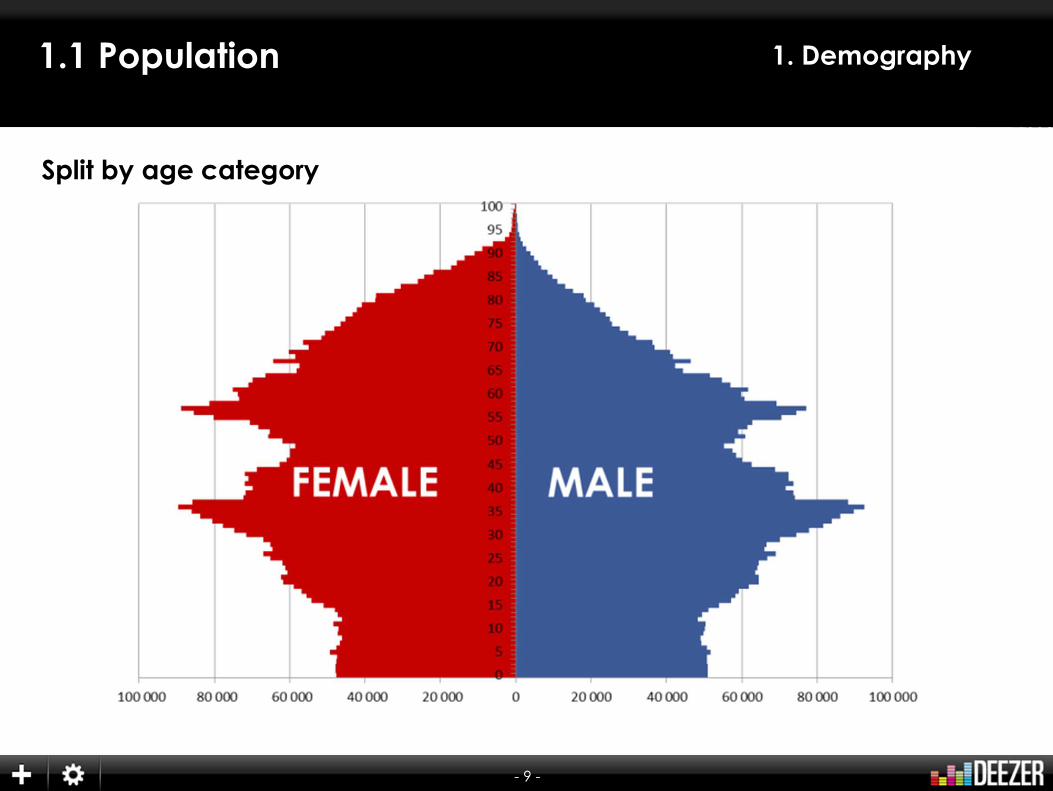

1. Demography1.1 Population

Split by age category(in million and %) and compare it with Facebook population split

⇒ Due to the low birthrate the majority of the population in Hungary is getting older. The targeted age group 18 – 44 years will become less relevant in future, since the market is getting smaller, which means that the older 45 – 59 group has to be targeted also. The group with the highest purchasing power coupled with the affinity to the streaming techology is the largest share is the age group 30 – 44.

⇒ Facebook is mostly used by the age groups 18-24 and 25-34. With 47% the majority of FB user are within that age group

4 221 580 users

42.25%

- 9 -

1. Demography1.1 Population

Split by age category

- 10 -

1. Demography1.1 Population

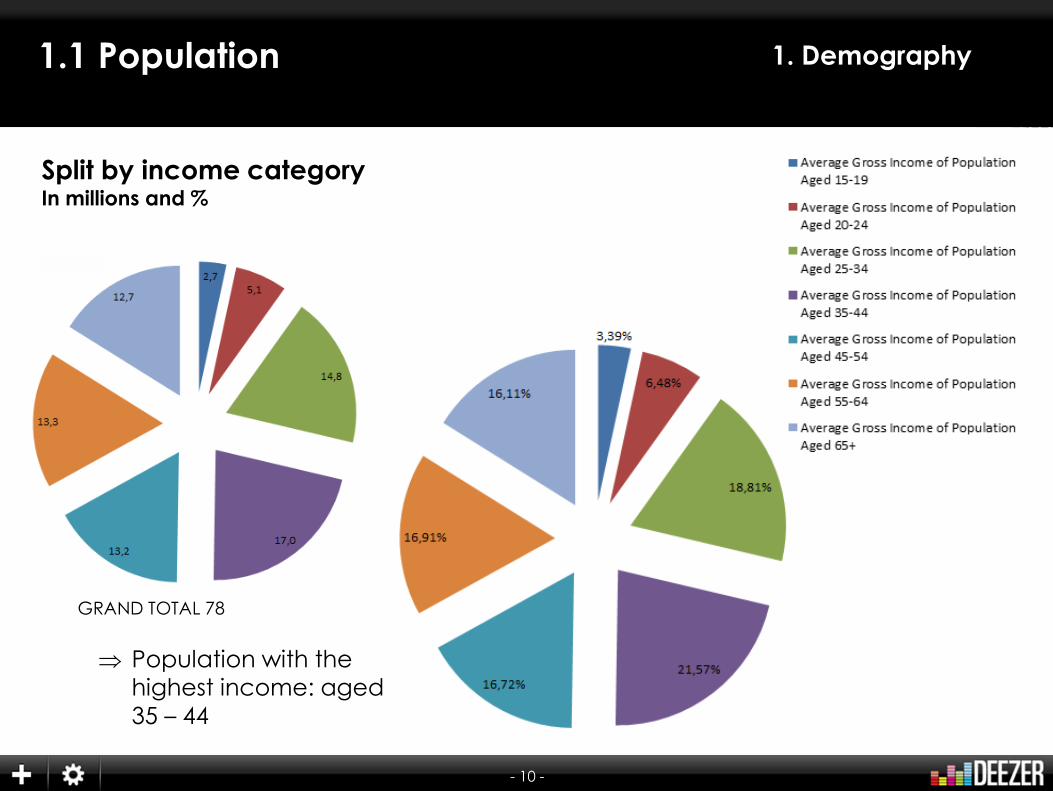

Split by income categoryIn millions and %

GRAND TOTAL 78

⇒ Population with the highest income: aged 35 – 44

- 11 -

1. Demography1.1 Population

CCL

• The population in Hungary is declining.

• Therefore the age group 45- 60 and more is constantly growing and potentially bigger market

• There is no view of having a higher birthrate of 1.33. The current economic situation not only causes a declining in births, but also a 10 thousands of people are expected to emigrate for longer time. 13.41% of the jobseekers would work outside Hungary.

• The new personal income tax has caused a higher polarization between the wealthy and the poorer deciles.

• => Percentage of age groups with highest music interest (age 16-19 and 20-29 slide 44) is declining

• => Population with the highest motivation to pay for music: 20-29 and 30-39 don’t necessarily have the highest salary

- 12 -

1. Demography1.2 Zoom on education

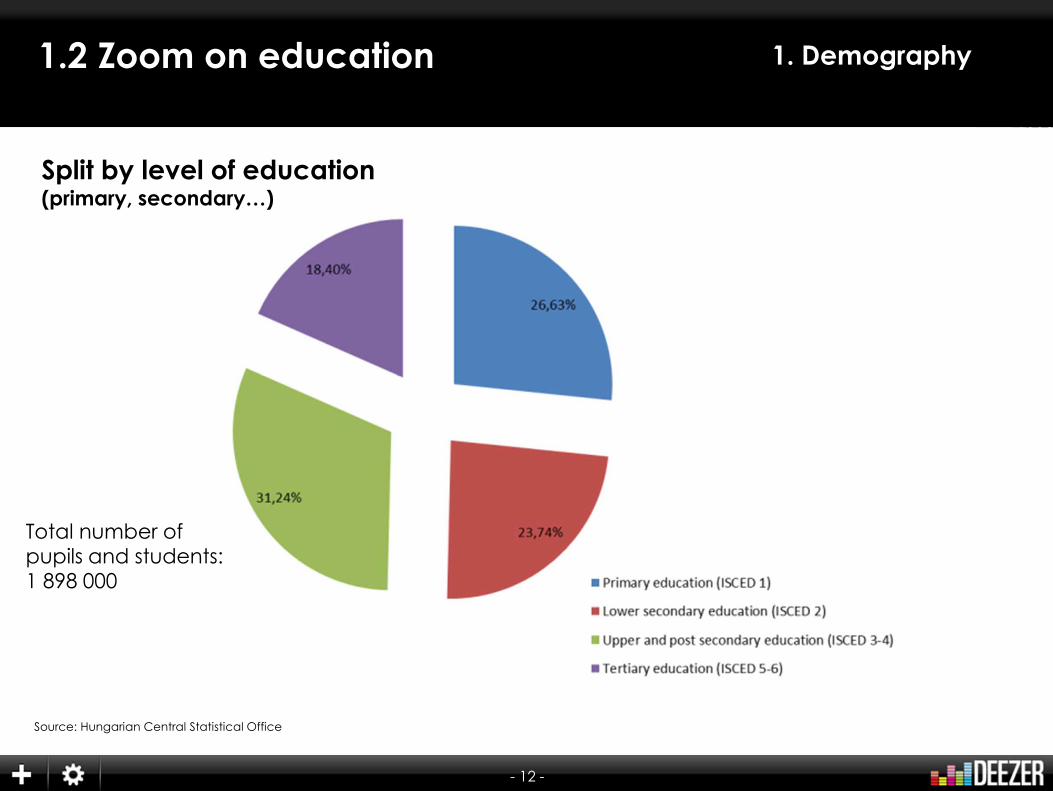

Split by level of education (primary, secondary…)

Total number of pupils and students: 1 898 000

Source: Hungarian Central Statistical Office

- 13 -

1. Demography1.2 Zoom on education

CCL

• To fight against the household deficit, the Hungarian state is drastically reducing the free places in the tertiary education system. Less and less people will be able to afford it.

• There is a big difference in the level of education

• Investment of education measured at the GDP is only 3.0% (vs. Iceland 7.9%, France 6.0%)1

- 14 -

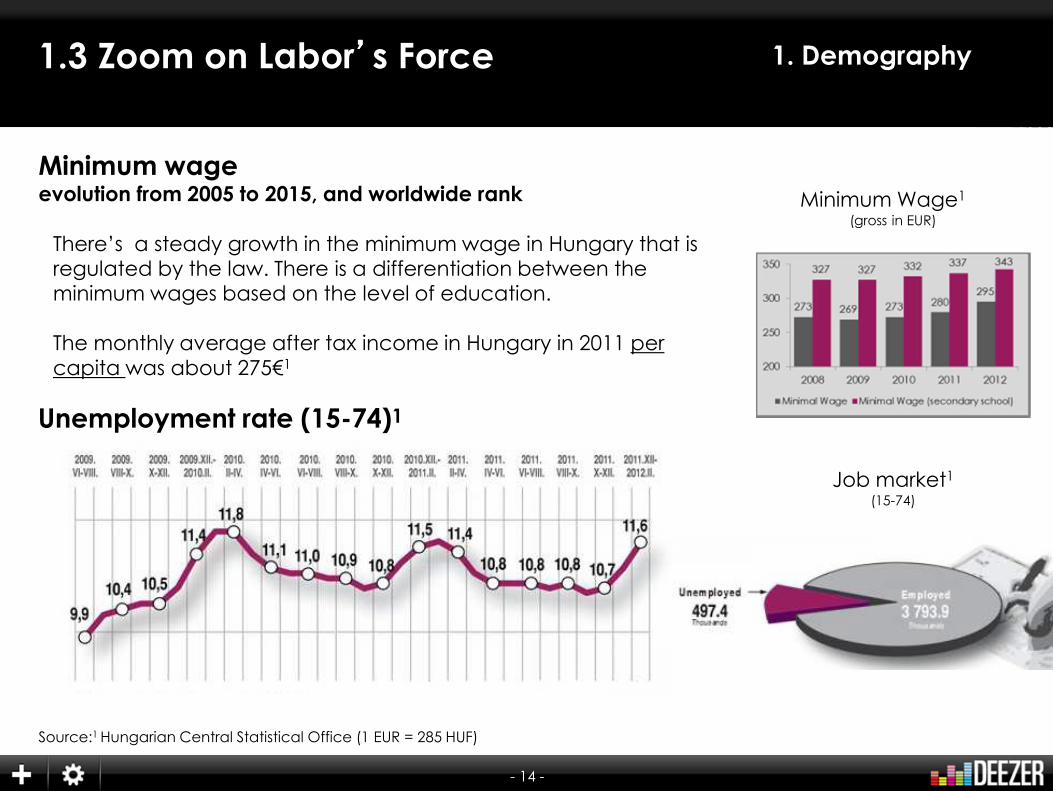

1. Demography1.3 Zoom on Labor’’’’s Force

Minimum wage evolution from 2005 to 2015, and worldwide rank

Unemployment rate (15-74)1

There’s a steady growth in the minimum wage in Hungary that is regulated by the law. There is a differentiation between the minimum wages based on the level of education.

The monthly average after tax income in Hungary in 2011 per capita was about 275€1

Minimum Wage1

(gross in EUR)

Source:1 Hungarian Central Statistical Office (1 EUR = 285 HUF)

Job market1

(15-74)

- 15 -

1. Demography1.3 Zoom on Labor’’’’s Force

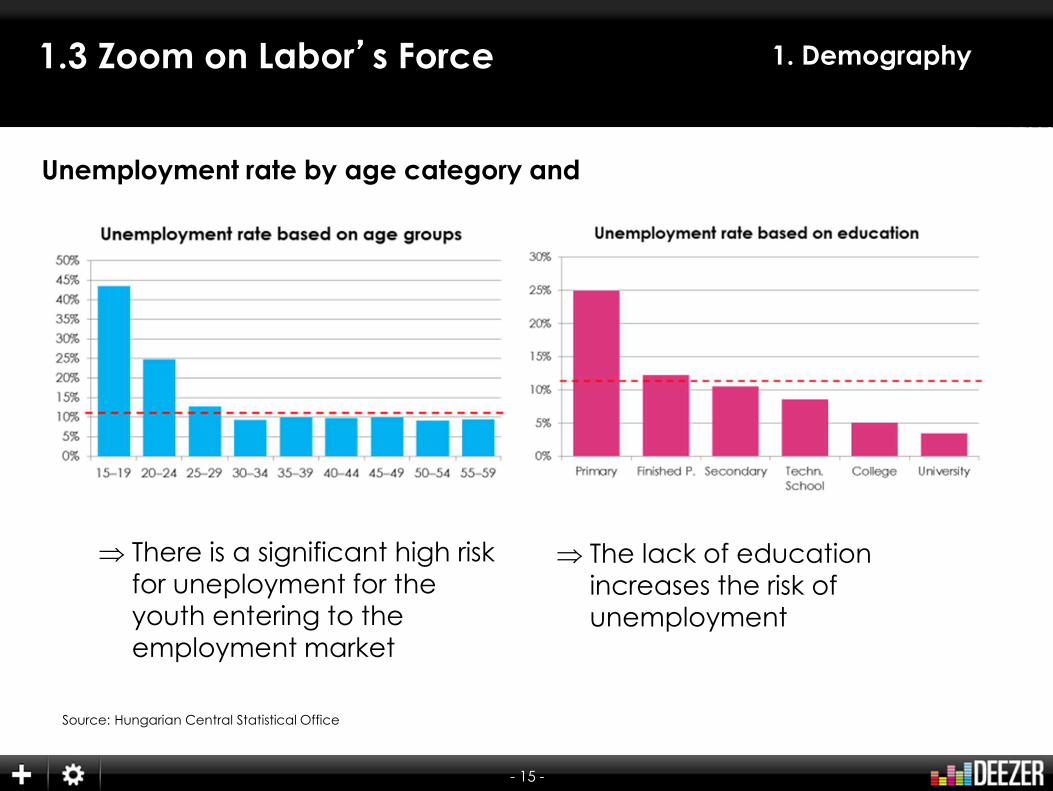

Unemployment rate by age category and

Source: Hungarian Central Statistical Office

⇒ There is a significant high risk for uneployment for the youth entering to the employment market

⇒ The lack of education increases the risk of unemployment

- 16 -

1. Demography1.3 Zoom on Labor’’’’s Force

CCL

• The Hungarian unemployment rate is increasing

• Hungary’s unemployment rate is about the average of Europe

• The gross minimum wage is almost identical with the net monthly average income per capita. This indicates a high level of tax avoidance (national „sport” of Hungarians) and a high level of underground economy.

• The level of education defines the salary to a high degree and also the chance for employment

- 17 -

1. Demography1.4 Willingness to pay

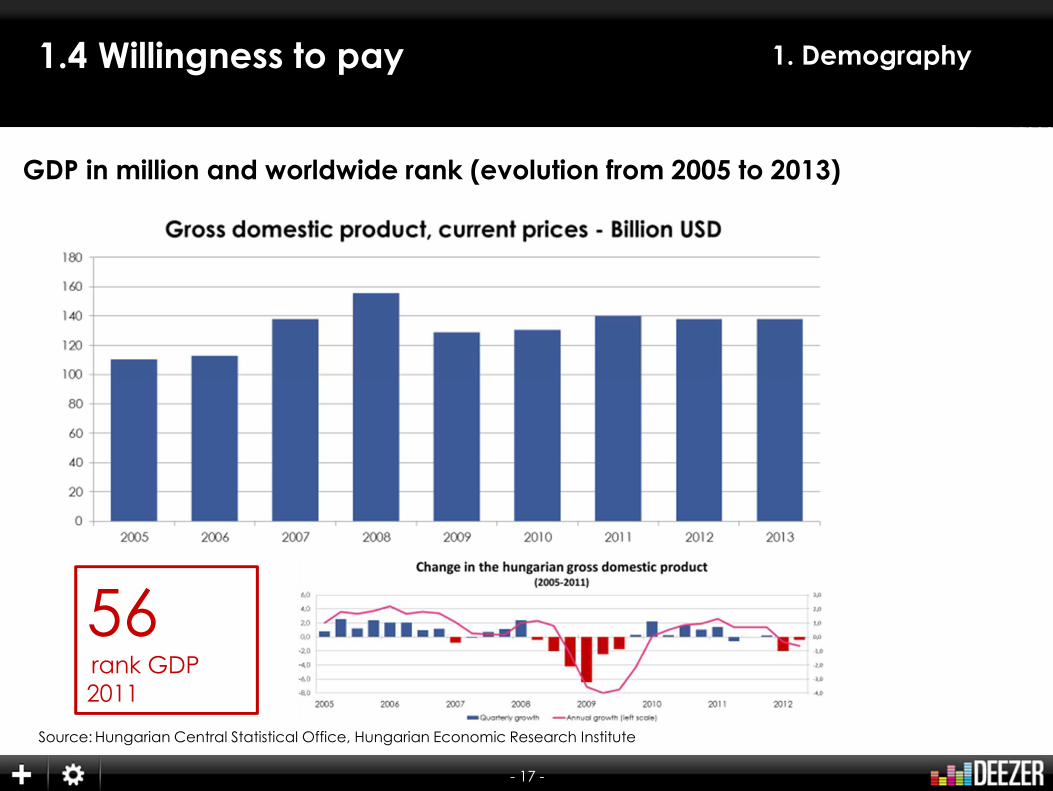

GDP in million and worldwide rank (evolution from 2005 to 2013)

56rank GDP 2011

Source: Hungarian Central Statistical Office, Hungarian Economic Research Institute

- 18 -

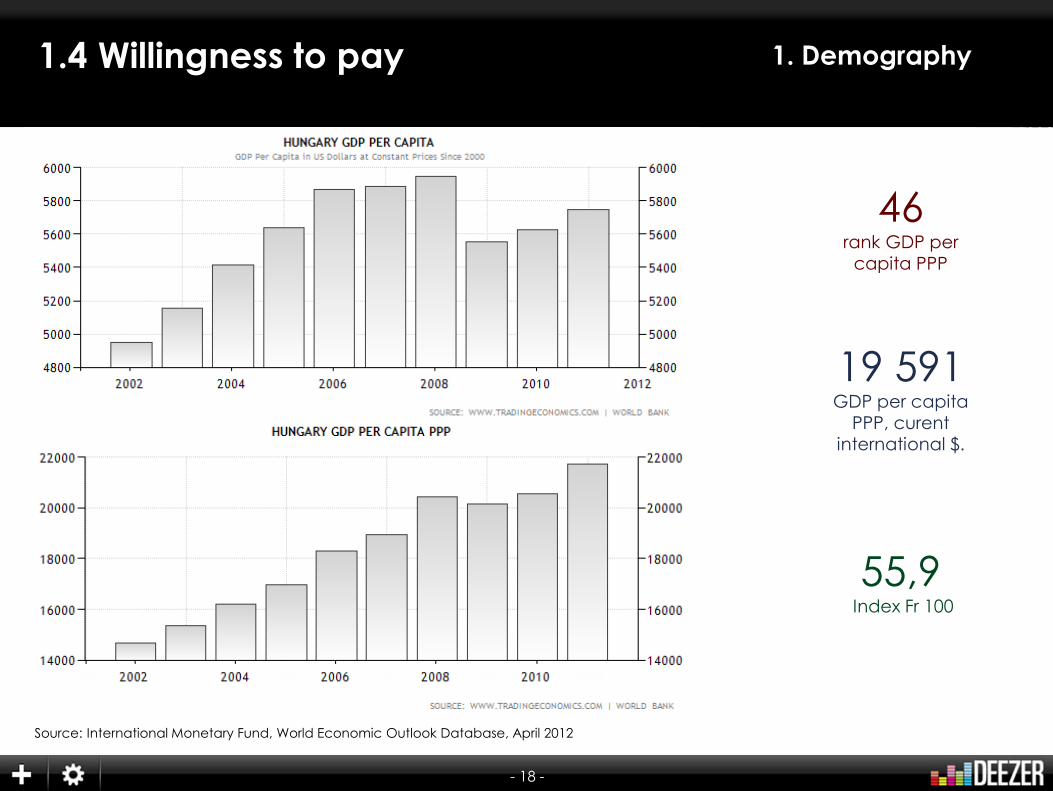

1. Demography1.4 Willingness to pay

46rank GDP per

capita PPP

19 591GDP per capita

PPP, curent international $.

55,9Index Fr 100

Source: International Monetary Fund, World Economic Outlook Database, April 2012

- 19 -

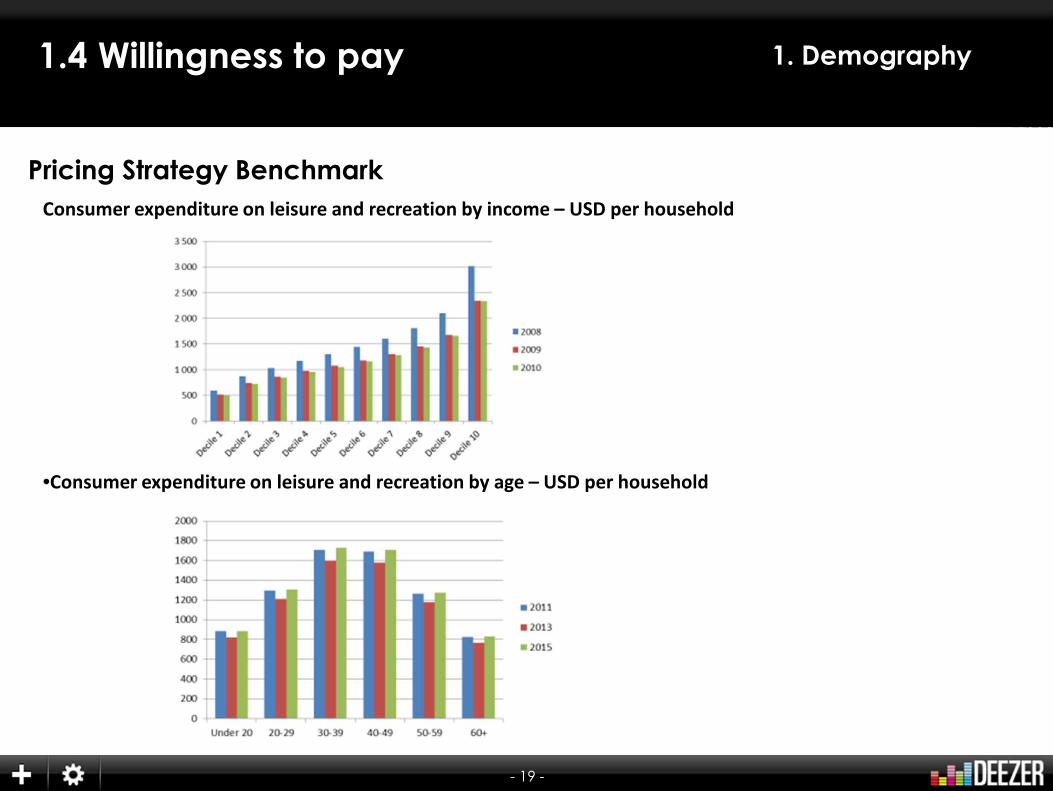

1. Demography1.4 Willingness to pay

Consumer expenditure on leisure and recreation by income – USD per household

•Consumer expenditure on leisure and recreation by age – USD per household

Pricing Strategy Benchmark

- 20 -

1. Demography1.4 Willingness to pay

Conclusion

• Consumer expenditures on leisure and recreation is the highest for the age groups 30–49

• However we recommend to target not only this group, but the younger, as they tend to have more interest in music and affinity to the internet.

• However in older age groups the probability of piracy decreases immensely, which gives a potentially higher purchasing group.

• Pricing will be essential because the general attitude towards the music on the internet is, that it is for free. This is independent from age groups.

- 21 -

The Black Eyed Peas, Elephunk (2003), A&M/will.i.am/lnterscope

Let’s Get It StartedLet’s Get It StartedLet’s Get It StartedLet’s Get It StartedLet’s Get It Started

2. MUSIC MARKET OPPORTUNITYWould they pay for streaming music?

- 22 -

2. Music Market

Opportunity

2.1 Local Music ecosystem :

Who should we partner with ?

2.1.1 PLAYERS

White FalconIndies

Aggregators

Ex-stateownedlabel

Big four major

Major labelsOnly Universal and Sony present actively, Warner representative office. Works as in other countries.

Indies/Content aggregatorsThe ex-stateowned monopoly Hungaroton owns a large quantity of the music of ’60-’80s. They have their own online shop. Very difficult to sign up. Other main indies are preparing their content for digital distribution via some of the 2 aggregators. WMMD is a Hungarian aggregator which not only aggregates but provides music service solutions to 3rd parties (Vodafone), the other is the Austrian Rebeat. Unfortunately there is not too much chance to have some organization managing all the small indies, which means they are lost for the digitized world. Some efforts are done by MAHASZ/ARTISJUS/EJI (IFPI and right societies) to have them collected.

- 23 -

2. Music Market

Opportunity

2.1 Local Music ecosystem :

Who should we partner with ?

2.1.1 PLAYERSCollecting societies

There are two collecting societies in Hungary.

Artisjus - Hungarian Bureau for the Protection of Authors’ RightsLegally approved by the ministry of culture - authors collecting society in Hungary. Earlier the monopolistic position of Artisjus made them quite difficult to negotiate with. Nowadays they became quite flexible.

EJI - Association of the Arts Unions Bureau for the Protection of Performers’ RightsIt is a very special society for the Hungarian music market, because there is a collection society for the performers too. They are legally approved by the ministry of culture too, and are officially forced to collect fees in the name of performers. The international labels do not recognize them, as they are at the standpoint that they are paying their performers directly. In the a-la-carte download business they had about this an agreement, however in the streaming business this has not been clarified yet. Apple is not paying them.They are also operating a music download store www.dalok.hu/www.songs.hu. Only niche content available where the performer and author is the same. I suggest to have a meeting with them, and somehow find a way to have a mutually satisfying agreement. I am also suggesting, that we could take their content to Deezer, as it is also Hungarian and in database, digitized and with metadata.

- 24 -

2. Music Market

Opportunity

2.1 Local Music ecosystem :

Who should we partner with ?

Source: WMMD

2.1.1 PLAYERS: Major Labels and Independent Labels: Digital Market

Share

Unfortunately no official market share figures available on the market. The following is an informal distribution by the largest Hungarian indie aggregator and B2B music service provider.

Informal rankingQ3/2012

1. Indies*2. Sony Music3. Warner Music4. Universal Music5. EMI6. Hungaroton*aggregated by WMMD

- 25 -

2. Music Market

Opportunity

2.1 Local Music ecosystem :

Who should we partner with ?

2.1.1 PLAYERSConclusion / To do

• With having agreements with all majors and the 2 music content aggregators active in Hungary: WMMD and Rebeat we have a good content coverage

• We have to convince Hungaroton to sign a deal with us, their content would be great fro addressing the 45-65 age group

• Small labels should be sent to one of the aggregators to get their content to Deezer

• We have to focus on the Hungarian content mainly, because with our international agreement, all international content is available . Sometimes content from local labels gets delayed to the aggregator.

- 26 -

2. Music Market

Opportunity

2.1 Local Music ecosystem :

Who should we partner with ?

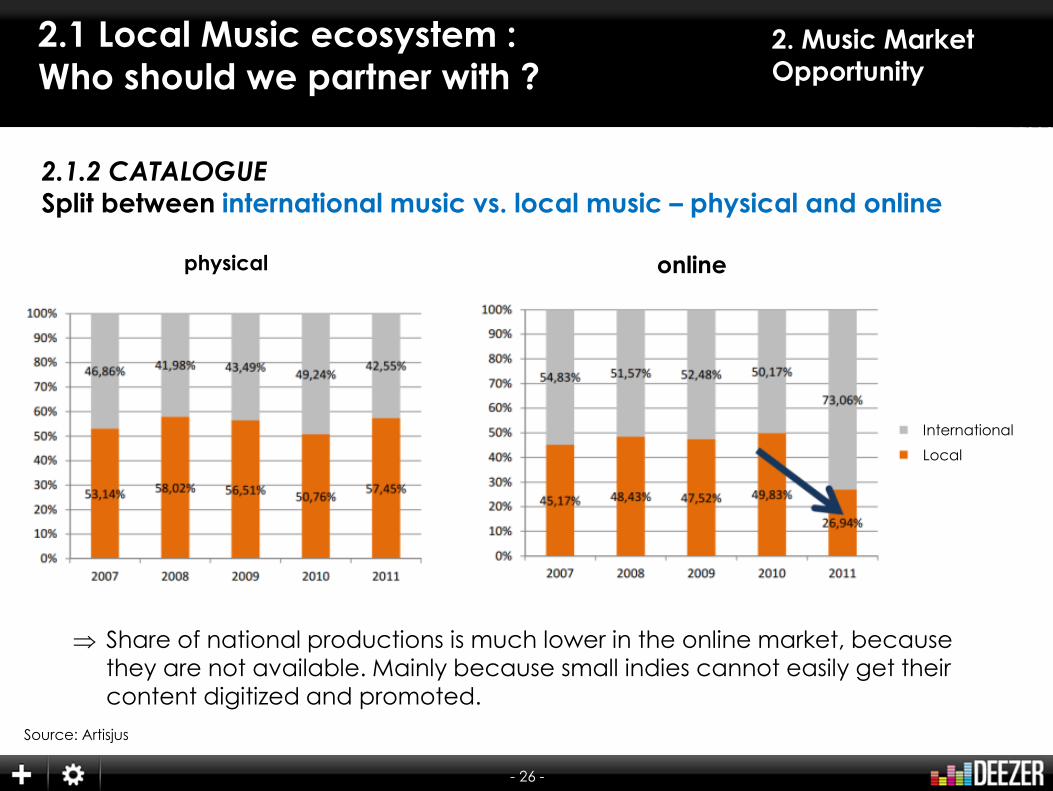

2.1.2 CATALOGUESplit between international music vs. local music – physical and online

Source: Artisjus

⇒ Share of national productions is much lower in the online market, because they are not available. Mainly because small indies cannot easily get their content digitized and promoted.

InternationalLocal

International

Local

physical online

- 27 -

2. Music Market

Opportunity

2.1 Local Music ecosystem :

Who should we partner with ?

2.1.2 CATALOGUE: Top national and international artists 2011

⇒ In the top list the local artists are overrepresented

⇒ Huge impact from the activity of commercial television⇒ X-factor⇒ The Voice

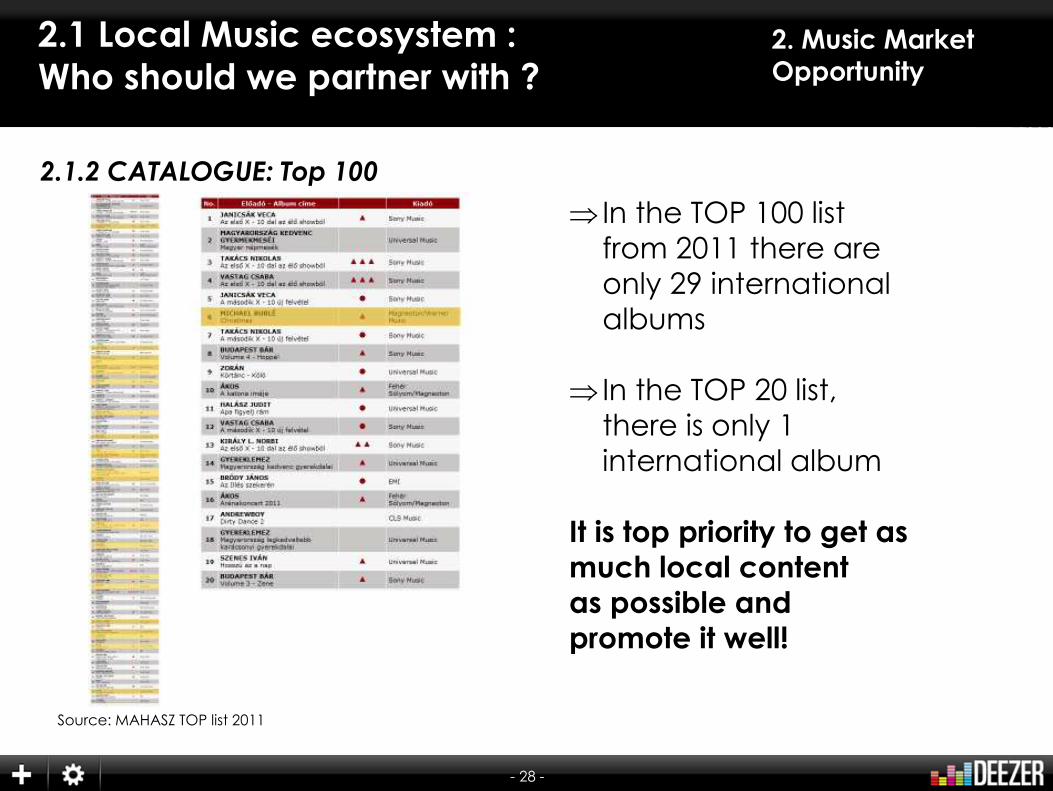

Source: MAHASZ TOP list 2011

- 28 -

2. Music Market

Opportunity

2.1 Local Music ecosystem :

Who should we partner with ?

2.1.2 CATALOGUE: Top 100

⇒ In the TOP 100 list from 2011 there are only 29 international albums

⇒ In the TOP 20 list, there is only 1 international album

It is top priority to get as

much local content

as possible and

promote it well!

Source: MAHASZ TOP list 2011

- 29 -

2. Music Market

Opportunity

2.1 Local Music ecosystem :

Who should we partner with ?

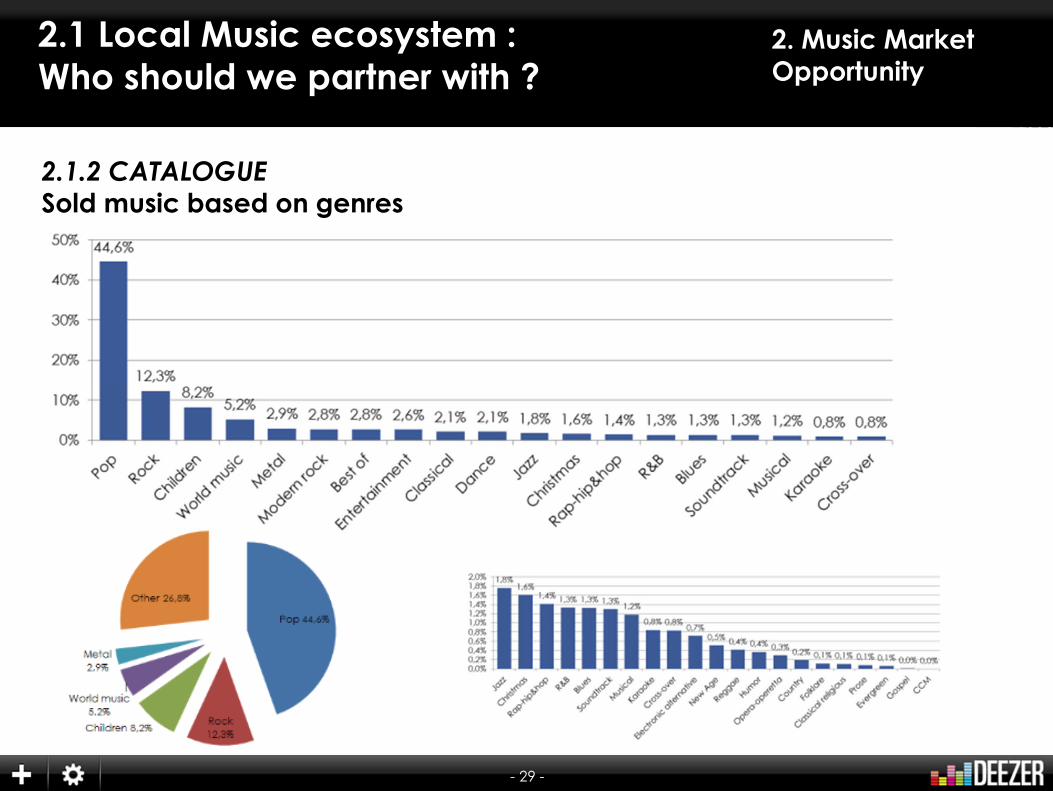

2.1.2 CATALOGUESold music based on genres

- 30 -

2. Music Market

Opportunity

2.1 Local Music ecosystem :

Who should we partner with ?

2.1.2 CATALOGUEConclusion

Deezer HU check of the Top 10 single charts and TOP 40 album charts:• Album charts: 85% available• Single charts: 100% available

Main catalog problem in Hungary:There are some national top artists with not complete repertoire

Examples: Tankcsapda, Copy Con, EDDA Művek, Havasi Balázs

- 31 -

2. Music Market

Opportunity

2.1 Local Music ecosystem :

Who should we partner with ?

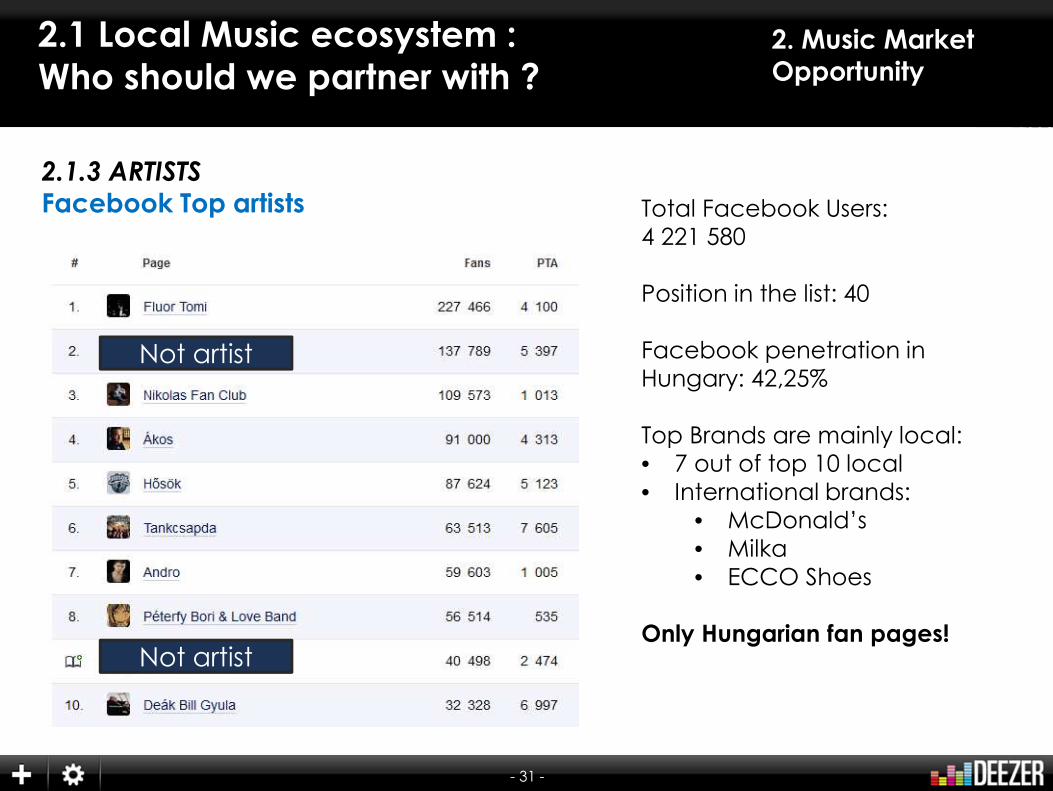

2.1.3 ARTISTSFacebook Top artists Total Facebook Users:

4 221 580

Position in the list: 40

Facebook penetration in Hungary: 42,25%

Top Brands are mainly local:• 7 out of top 10 local• International brands:

• McDonald’s • Milka• ECCO Shoes

Only Hungarian fan pages!

Not artist

Not artist

- 32 -

2. Music Market

Opportunity

2.1 Local Music ecosystem :

Who should we partner with ?

2.1.3 ARTISTSYoutube top artists : Top artists – most watched videos 2012

http://www.youtube.com/charts/videos_views/music?d=20121115

- 33 -

2. Music Market

Opportunity

2.1 Local Music ecosystem :

Who should we partner with ?

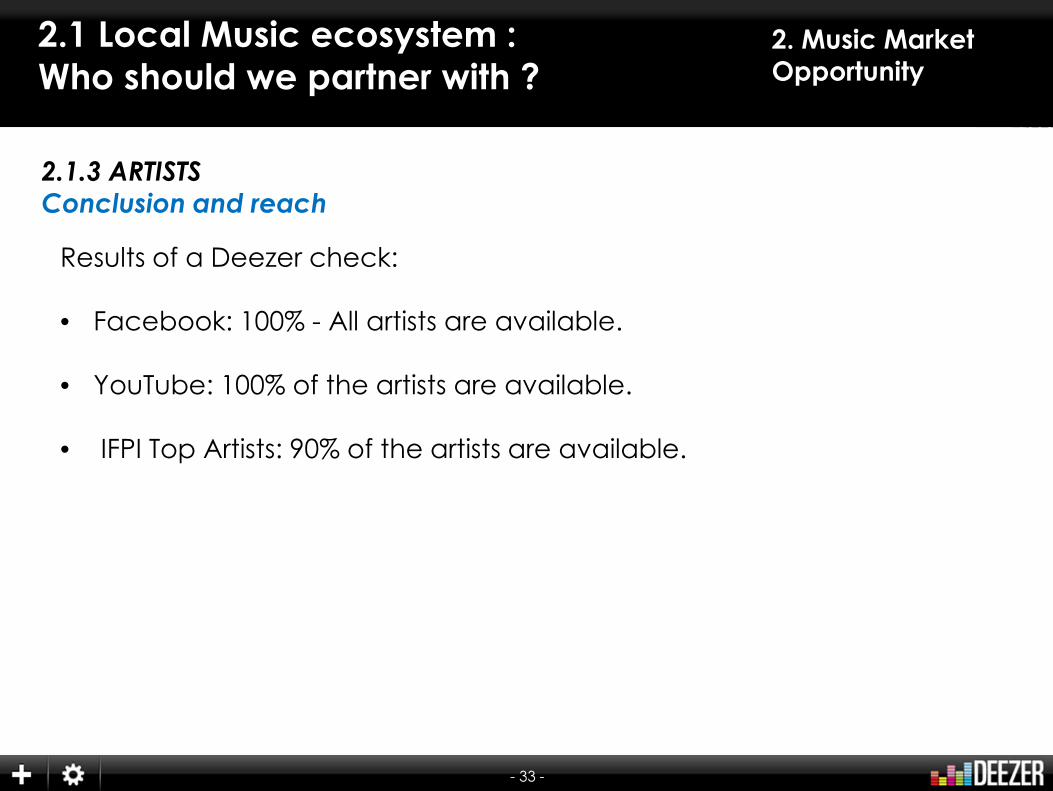

2.1.3 ARTISTS

Conclusion and reach

Results of a Deezer check:

• Facebook: 100% - All artists are available.

• YouTube: 100% of the artists are available.

• IFPI Top Artists: 90% of the artists are available.

- 34 -

2. Music Market

Opportunity

2.2 Market music size

How big is my cake ?

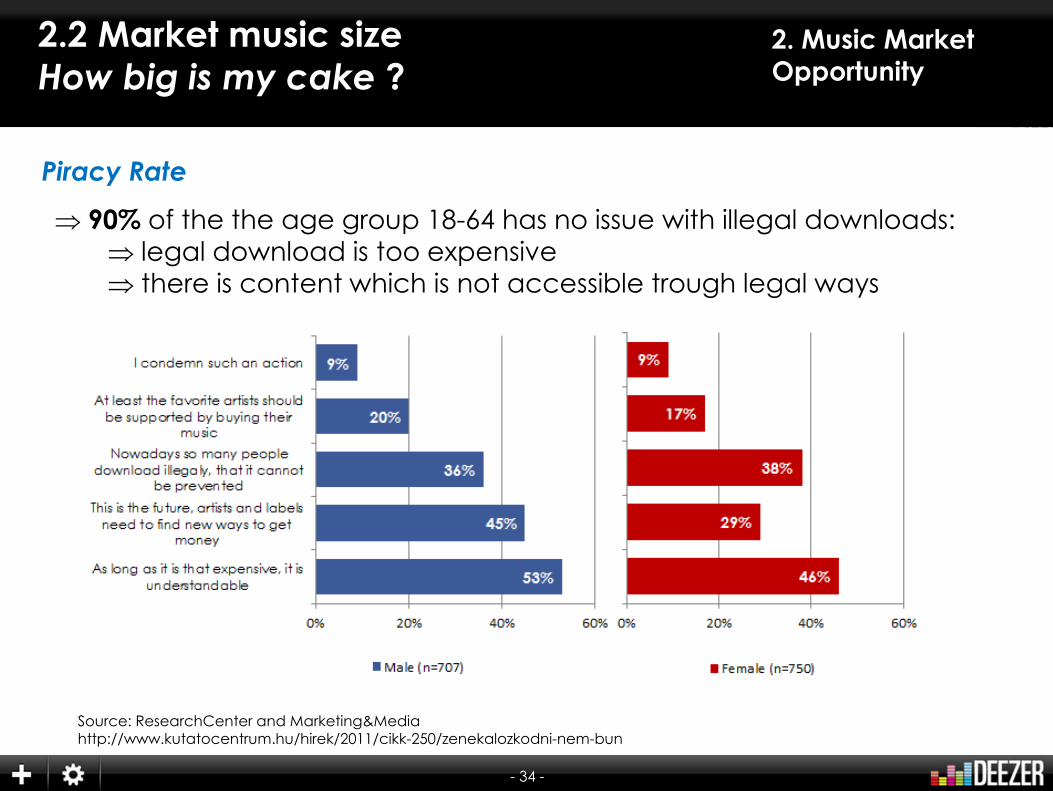

Piracy Rate

⇒ 90% of the the age group 18-64 has no issue with illegal downloads:⇒ legal download is too expensive⇒ there is content which is not accessible trough legal ways

Source: ResearchCenter and Marketing&Mediahttp://www.kutatocentrum.hu/hirek/2011/cikk-250/zenekalozkodni-nem-bun

- 35 -

2. Music Market

Opportunity

2.2 Market music size

How big is my cake ?

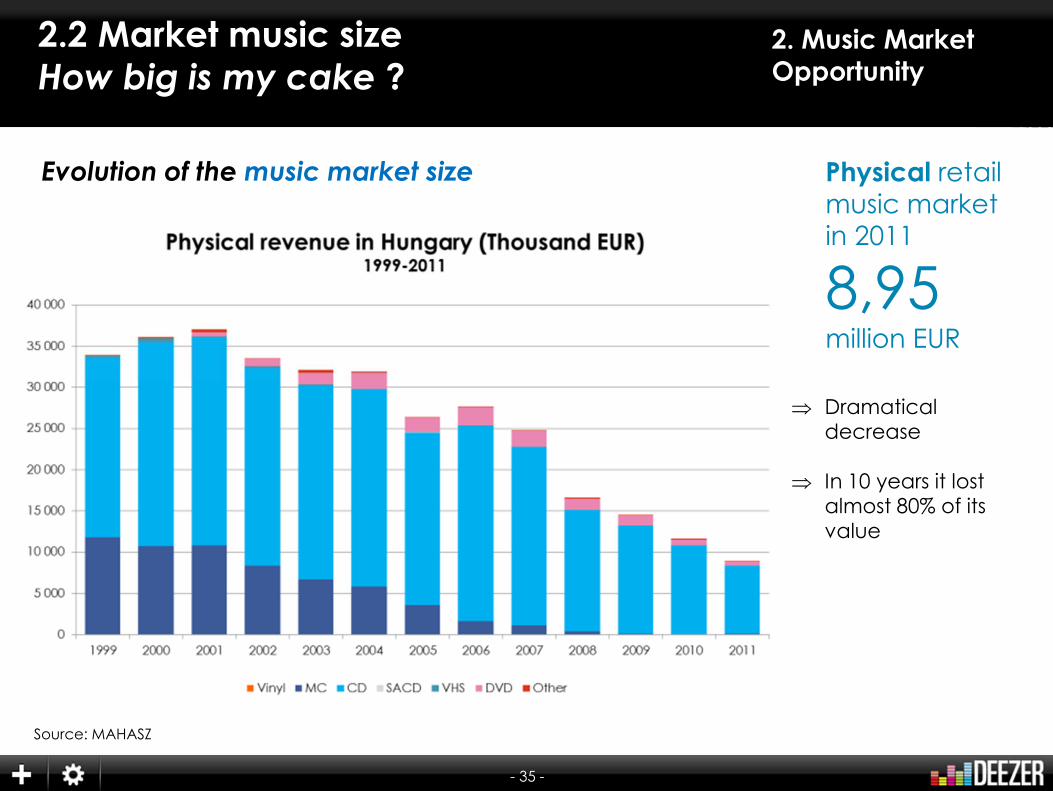

Evolution of the music market size

Source: MAHASZ

Physical retailmusic marketin 2011

8,95million EUR

⇒ Dramaticaldecrease

⇒ In 10 years it lost almost 80% of its value

- 36 -

2. Music Market

Opportunity

2.2 Market music size

How big is my cake ?

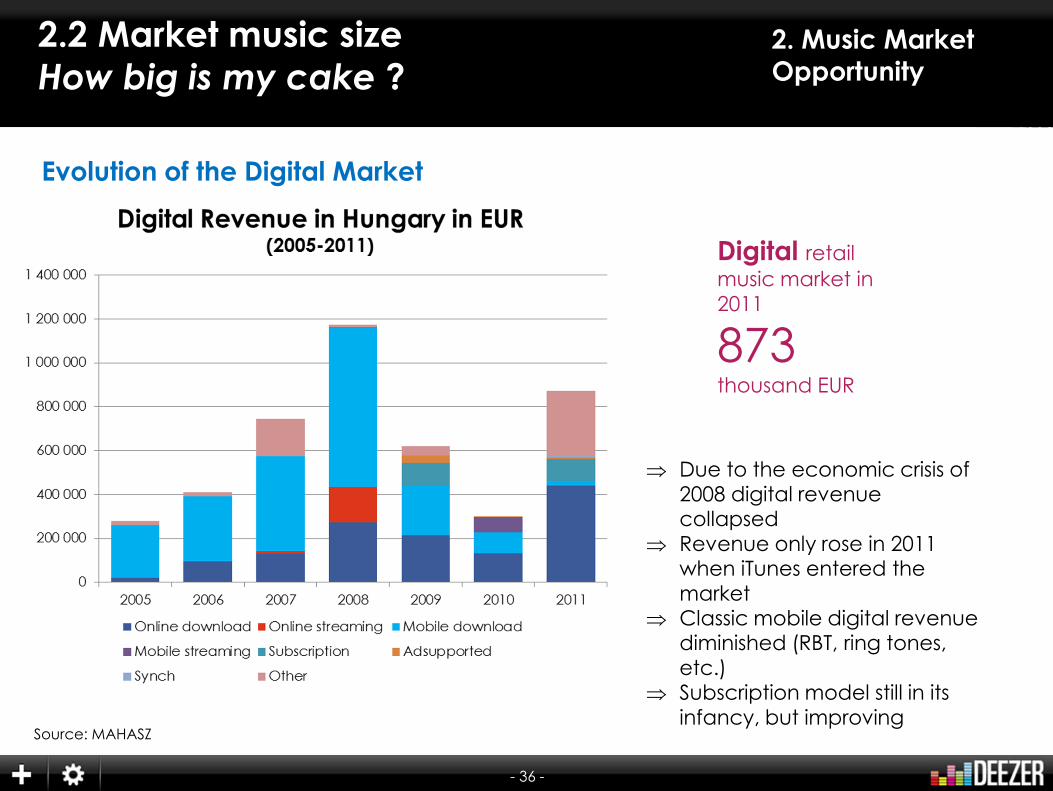

Evolution of the Digital Market

Source: MAHASZ

⇒ Due to the economic crisis of 2008 digital revenue collapsed

⇒ Revenue only rose in 2011 when iTunes entered the market

⇒ Classic mobile digital revenue diminished (RBT, ring tones, etc.)

⇒ Subscription model still in its infancy, but improving

Digital retail music market in 2011

873thousand EUR

- 37 -

2. Music Market

Opportunity

2.2 Market music size

How big is my cake ?

⇒ Digital cannot compansate the lost physical revenue

Digital is

10%of total market

- 38 -

2. Music Market

Opportunity

2.2 Market music size

How big is my cake ?

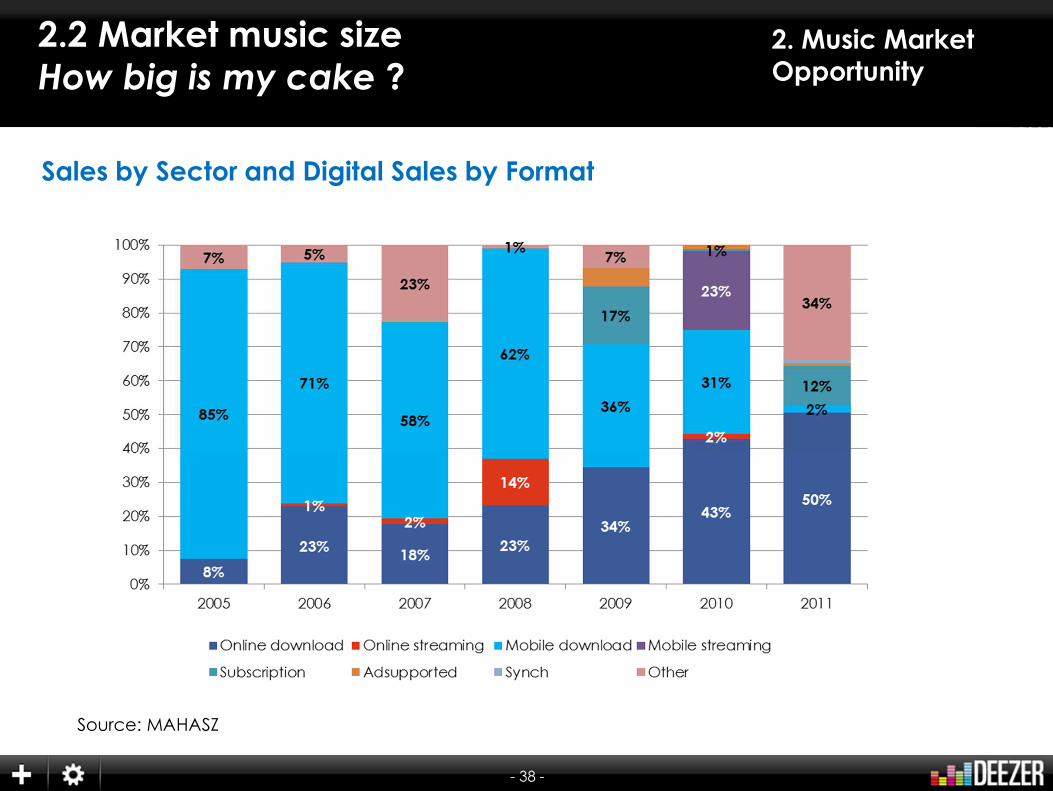

Sales by Sector and Digital Sales by Format

Source: MAHASZ

- 39 -

2. Music Market

Opportunity

2.2 Market music size

How big is my cake ?

Demographics about local music buyers: who are the early

adopters? What is my “current” potential market?

The first adopters will be people more open to the digital world and media. However people not older than 35 years, are already used to online music usage. The Youtube generation does not have to be taught about music streaming.For them it is more needed, to inform them about this service. In general the attitude towards the online music has to be changed. In the real life people still think that everything from the internet, especially music and video is for free. This has been supported by Youtube’s free model. This is why we do not only have to focus on the 20 million tracks accessible for reasonable price, but rather on the flexibility, accessibility and easiness. Not the content itself but how you get is the most important. All the content is accessible to this generation for free. We want to be the McDonald’s of streaming music.

As a second target group, the generation of the parents of the above mentioned early adopters. This is why is really important to get music in our repertoire. They will be taught by the younger generation how to use.We have to find „cool” and trustful artist(s) as a face of our service.

• We should sponsor highlife party pubs and their regular parties. The participants are mainly wealthy,

younger, opinions leaders.

• We should be present at the main festivals – Balaton Sound and Sziget Festival (at Sziget, more than a half of

the participants are from Western Europe)

• We should in our own campaigns be SIMPLE, EASY and COMFORTABLE – in the focus should be the message

that you get 1 month joy for less than a movie ticket

• We should work with the labels to get as much exclusive content from artist who are popular in the younger

age groups

• We also should have a secondary campaign for the elderly 40-60 age group, focused on their nostalgy

(Hungaroton is a must to sign up)

• Online sponsorship of music blogs, and Google Adwords advertising, even torrent sites as potential adspace

- 40 -

2. Music Market

Opportunity

2.2 Market music size

How big is my cake ?

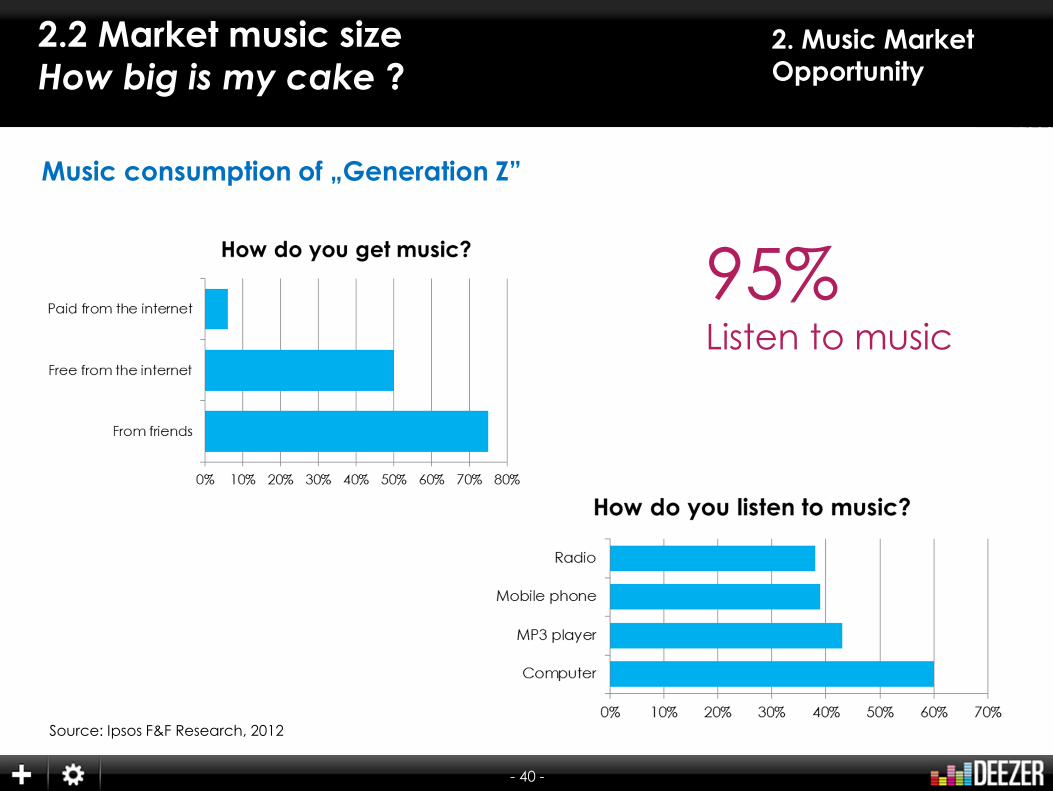

Music consumption of „Generation Z”

Source: Ipsos F&F Research, 2012

95%Listen to music

- 41 -

2. Music Market

Opportunity

2.2 Market music size

How big is my cake ?

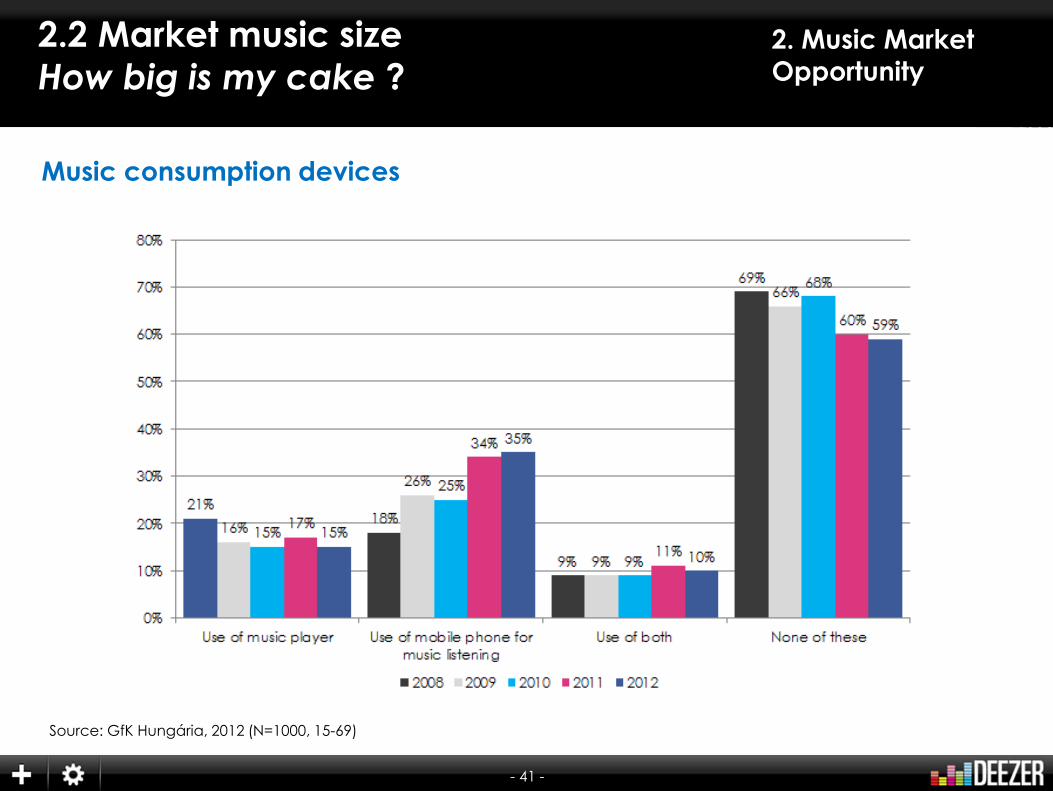

Music consumption devices

Source: GfK Hungária, 2012 (N=1000, 15-69)

- 42 -

2. Music Market

Opportunity

2.2 Market music size

How big is my cake ?

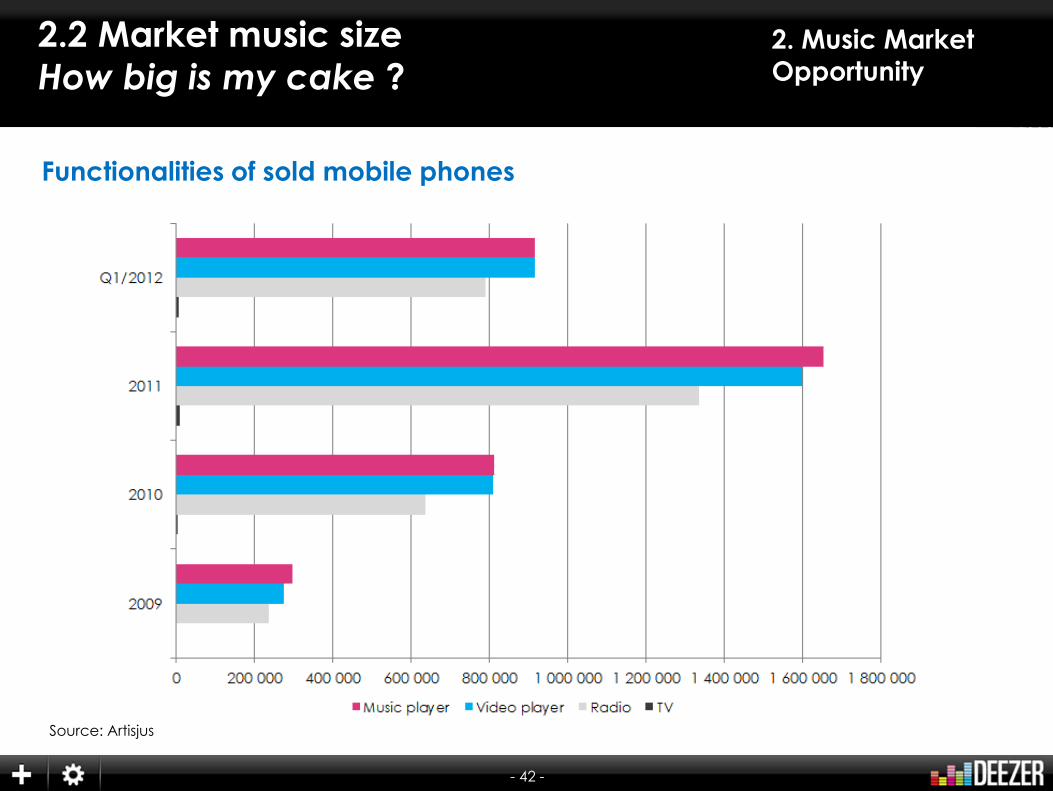

Functionalities of sold mobile phones

Source: Artisjus

- 43 -

2. Music Market

Opportunity

2.2 Market music size

How big is my cake ?

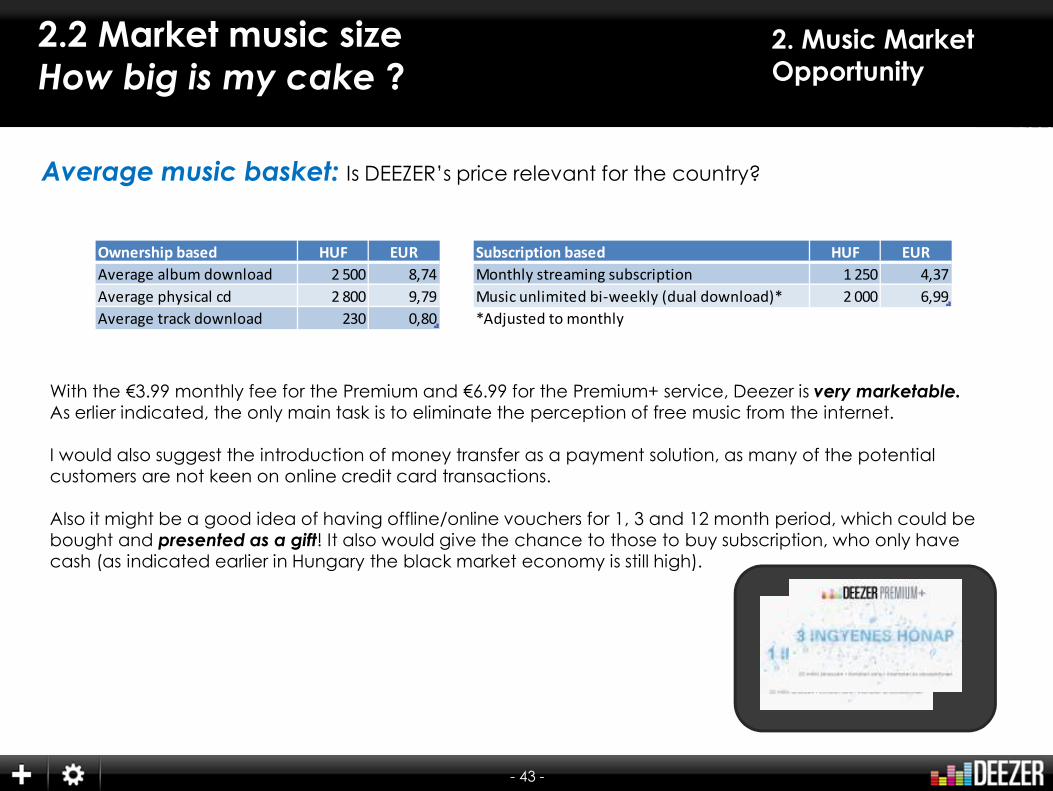

Average music basket: Is DEEZER’s price relevant for the country?

Ownership based HUF EUR

Average album download 2 500 8,74

Average physical cd 2 800 9,79

Average track download 230 0,80

Subscription based HUF EUR

Monthly streaming subscription 1 250 4,37

Music unlimited bi-weekly (dual download)* 2 000 6,99

*Adjusted to monthly

With the €3.99 monthly fee for the Premium and €6.99 for the Premium+ service, Deezer is very marketable.

As erlier indicated, the only main task is to eliminate the perception of free music from the internet.

I would also suggest the introduction of money transfer as a payment solution, as many of the potential customers are not keen on online credit card transactions.

Also it might be a good idea of having offline/online vouchers for 1, 3 and 12 month period, which could be bought and presented as a gift! It also would give the chance to those to buy subscription, who only have cash (as indicated earlier in Hungary the black market economy is still high).

- 44 -

2. Music Market

Opportunity

2.2 Market music size

How big is my cake ?

Worldwide rank of the music interest (dropbox >market intelligence > studies > Music. “Music related queries on adwords”

Specify rank and index62/76Worldwide Rank index

11,6/ index100(US)

Methodology : ranking on index 100 US, for % of search related to music per internet user.search related to music : mean between % of search of a basket of words proposed by adwords and % of search of the word « music » in local language

- 45 -

2. Music Market

Opportunity

2.2 Market music size

Who should we target?

Conclusions: Who should we target?

• Music is most important for the age groups 16-19 (85%) and 20-29 (79%)

• Most music buyers (54%) are among the 30-39 years old (26% for digital music)

⇒ Our main target groups should be 20-29 and 30-39 because they have the highest interest in digital music

⇒ As a second target group we should target the 40+ also, if the compelling content available (Hungaroton). They have the most money and are open to pay for

⇒ As an additional niche market the cildren music is also very popular (parents tend to buy and not to steal music for their children). In physical world it has an 8% share.

⇒ An attractive offer for pupils / students would help us to target younger age groups that have less access to money but highest interest in music (85%)

- 46 -

2. Music Market

Opportunity2.3 Local music usage

Particularities of the market

• The legal music market shrunk by 80% in the last 10 years. The physical market is still strong in Hungary and brings most of the revenue to the labels (85%), digital market is not fully fledged yet comparing to Western European Markets (however no clear metrics at the associations, which causes discrepancy in data)

• Most of the revenue on the digital market is brought by a la carte downloads.• Deezer together with Muzzia (locally financed, label supported streaming based on 24-7

Entertainment solution) are the only streaming services available in Hungary. Muzzia was targeting the mobile operators for cobranding, but failed. Without own technology, content, customers and well know brand they will fade out this year.

• Pure a la carte services have never made bigger successes in Hungary, Songo, T-Online Zeneáruház (later Z2) was closed or relaunched. Only iTunes can be considered as a small success.

• Payment methods, the most popular payment method is a bank transfer – PayPal and credit cards are still not accepted widely. For micro payments premium rate SMS is still used.

• Only a smaller part of local music from before the 90’s are not digitized, they are lost for the future. Rights and owners are not to be found. A concentrated local content from before the 90’s are at Hungaroton, the ex-stateowned national label. We need to have the on board as fast as we can. Elderly people can be addressed with that content, and the number of this generation is decreasing from day to day.

• The openness for innovation and new technologies in Hungary is average, depending on the technology (mobile phone, flat screen TV's were very fast, meanwhile credit card very slow).

• Key to success for customer proposition: good price and comfort

- 47 -

2.4 Conclusion2. Music Market

Opportunity

• Streaming services are still rather unknown in Hungary.

• There is still a lot of “educational” work to do: What is music streaming? What are the advantages etc.

• We have to be the McDonald’s of the music. Good price, easy, achievable, everywhere, you can afford it.

• We have to focus on the comfort of the service, NOT on the content itself. The content can be easily pirated. But with our service it can be always on you!

• Especially elderly people with less interest on computer, internet etc. have hardly been reached so far: You’ll find discussions only on streaming on tech blogs, computer journals, music magazines

=> Marketing should target elderly too.

• In Hungary the “switch” has not yet been made. People still prefer to “own”music by buying CDs, MP3s

⇒ Marketing should focus on the unlimited music experience

- 48 -

The Black Eyed Peas, Elephunk (2003), A&M/will.i.am/lnterscope

Let’s Get It StartedLet’s Get It StartedLet’s Get It StartedLet’s Get It StartedLet’s Get It Started

3. BtoC : ONLINE MARKET

OPPORTUNITY

- 49 -

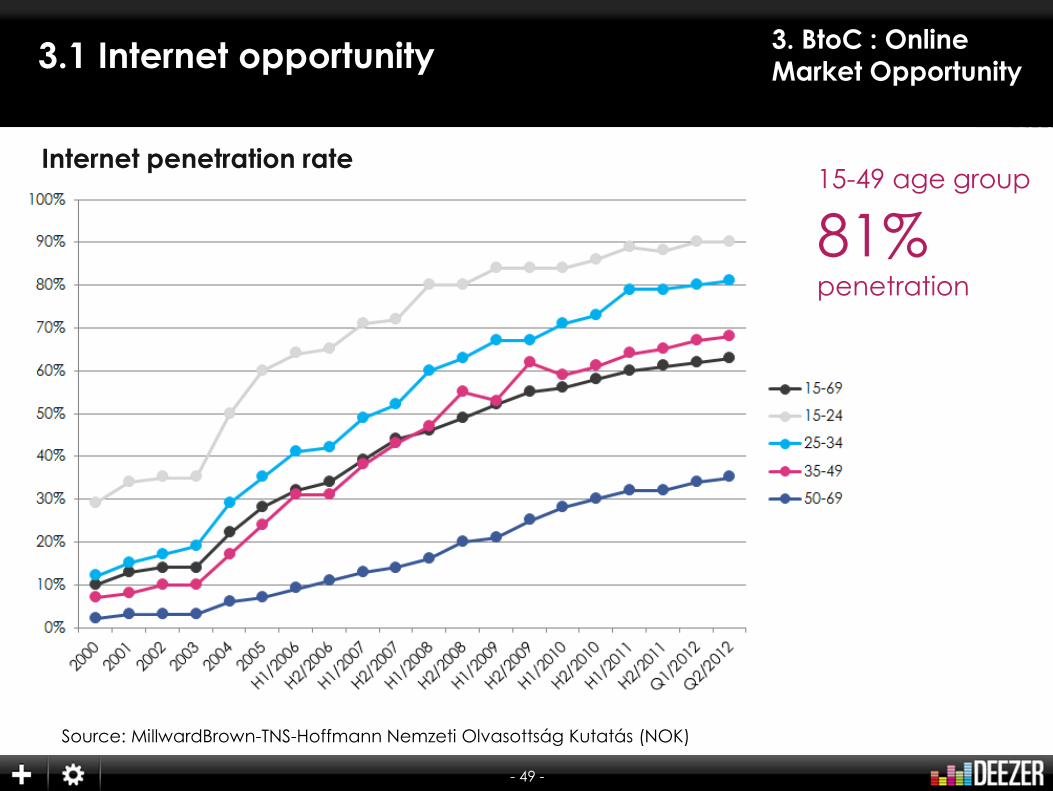

3. BtoC : Online

Market Opportunity3.1 Internet opportunity

Internet penetration rate

Source: MillwardBrown-TNS-Hoffmann Nemzeti Olvasottság Kutatás (NOK)

15-49 age group

81%penetration

- 50 -

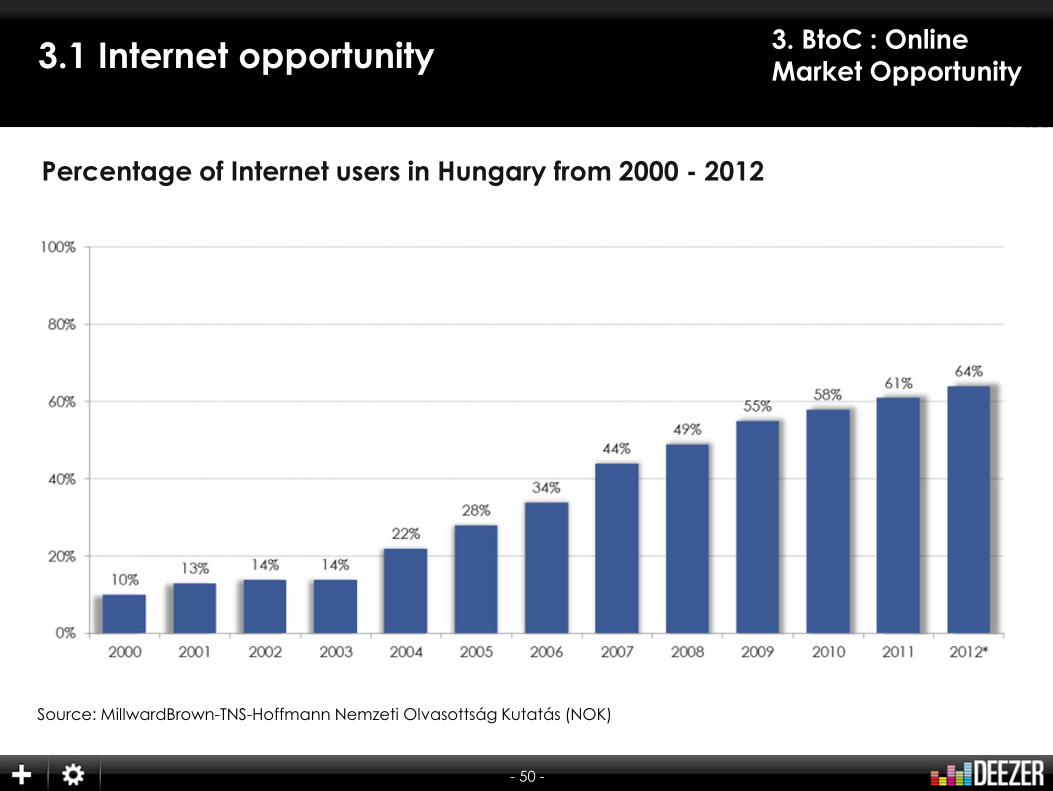

3. BtoC : Online

Market Opportunity3.1 Internet opportunity

Percentage of Internet users in Hungary from 2000 - 2012

Source: MillwardBrown-TNS-Hoffmann Nemzeti Olvasottság Kutatás (NOK)

- 51 -

3. BtoC : Online

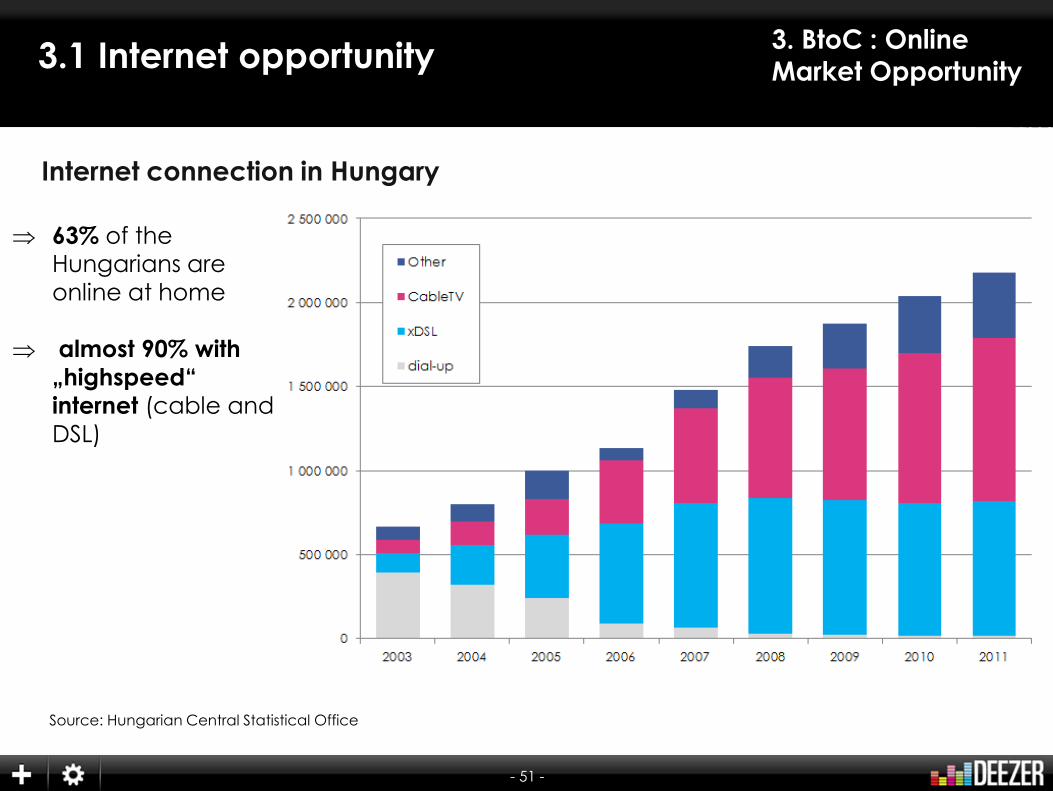

Market Opportunity3.1 Internet opportunity

Internet connection in Hungary

⇒ 63% of the Hungarians are online at home

⇒ almost 90% with

„highspeed“ internet (cable and DSL)

Source: Hungarian Central Statistical Office

- 52 -

3. BtoC : Online

Market Opportunity3.1 Internet opportunity

Households in Hungary

Source: Hungarian Central Statistical Office

- 53 -

3. BtoC : Online

Market Opportunity3.1 Internet opportunity

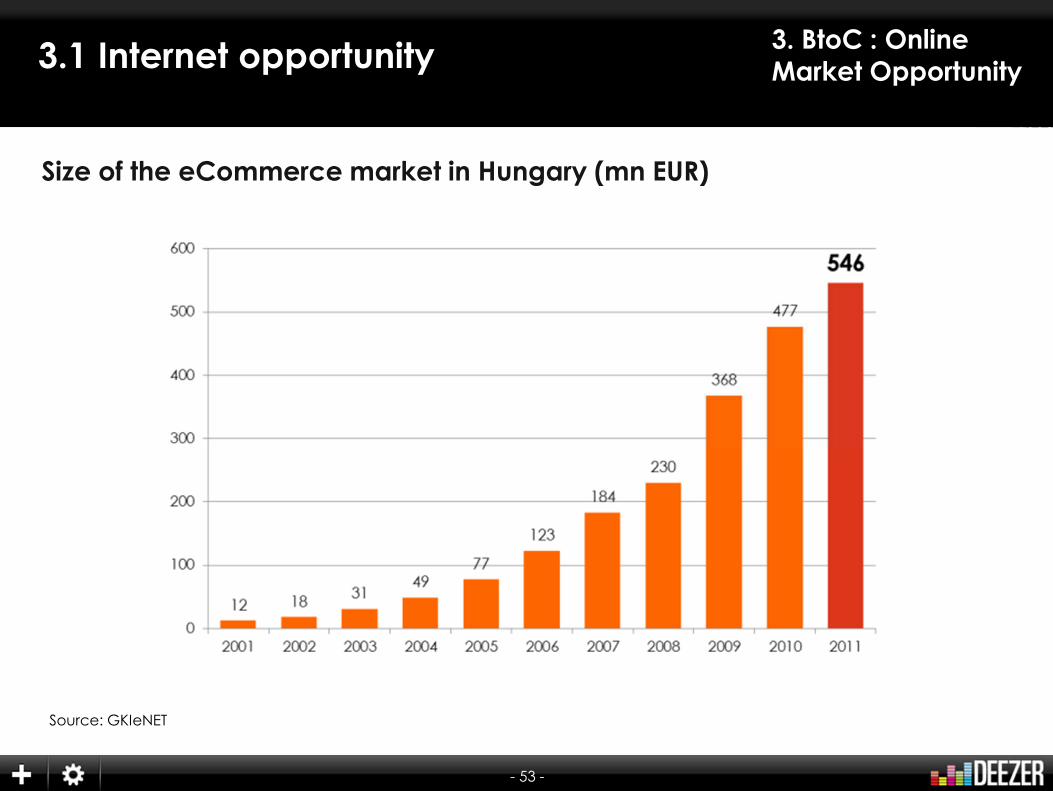

Size of the eCommerce market in Hungary (mn EUR)

Source: GKIeNET

- 54 -

3. BtoC : Online

Market Opportunity3.2 Ecommerce

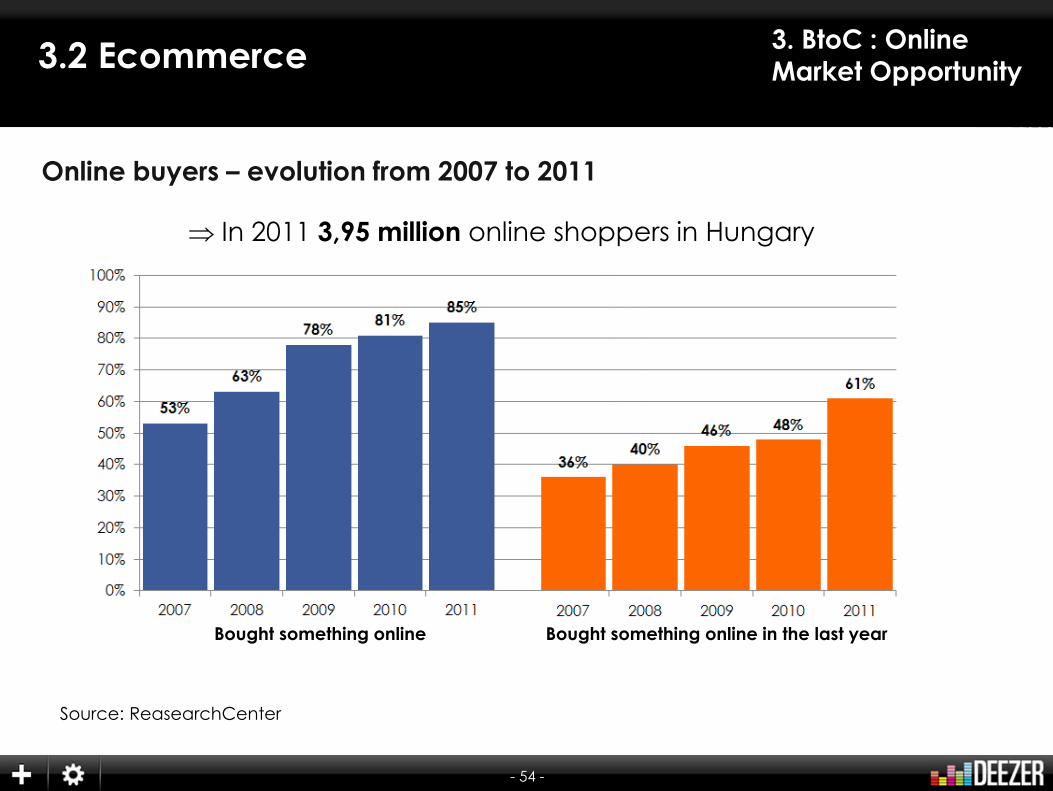

Online buyers – evolution from 2007 to 2011

⇒ In 2011 3,95 million online shoppers in Hungary

Source: ReasearchCenter

Bought something online Bought something online in the last year

- 55 -

3. BtoC : Online

Market Opportunity3.3 Conclusion

• Moderate Internet penetration rate in a moderately competitive market

• The mobile ad market is consistently growing, due to the fact that mobile business became more relevant

• E-commerce business is constantly growing. Most popular ecommerce product categories are clothing, books and electronics

• High concentration on very few players

• In Hungary security (date, payment etc.), is an important aspect: Many online shops are therefore working with labels (Trusted shops etc.)

• People don’t like to pay in advanced and with credit card, rather cash

• Client support is important for the Hungarian market

- 56 -

The Black Eyed Peas, Elephunk (2003), A&M/will.i.am/lnterscope

Let’s Get It StartedLet’s Get It StartedLet’s Get It StartedLet’s Get It StartedLet’s Get It Started

4. BtoB EquipmentsIs it a BtoB market ?

- 57 -

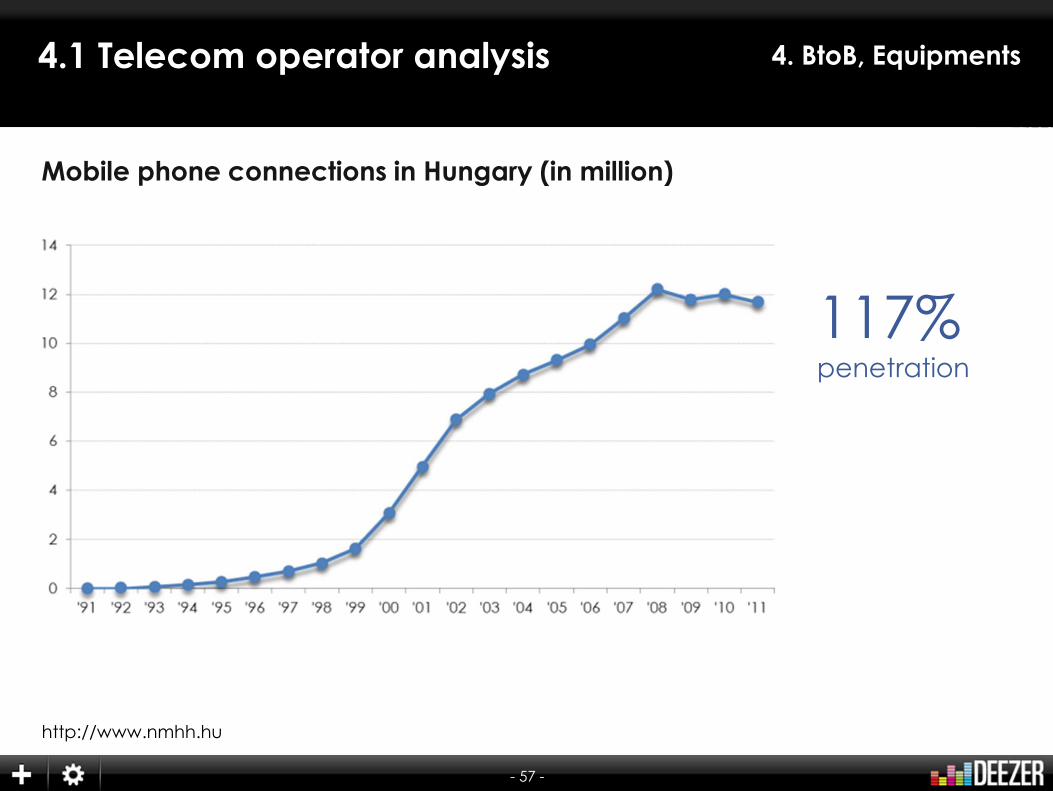

4. BtoB, Equipments4.1 Telecom operator analysis

Mobile phone connections in Hungary (in million)

http://www.nmhh.hu

117%penetration

- 58 -

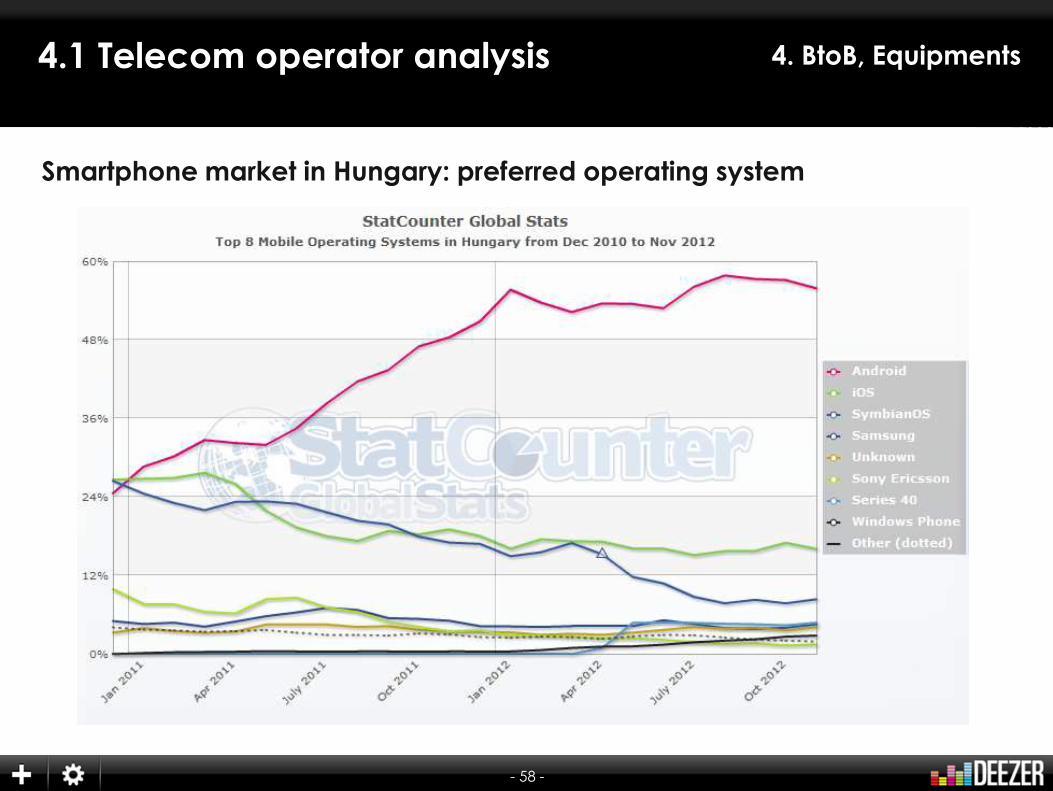

4. BtoB, Equipments4.1 Telecom operator analysis

Smartphone market in Hungary: preferred operating system

- 59 -

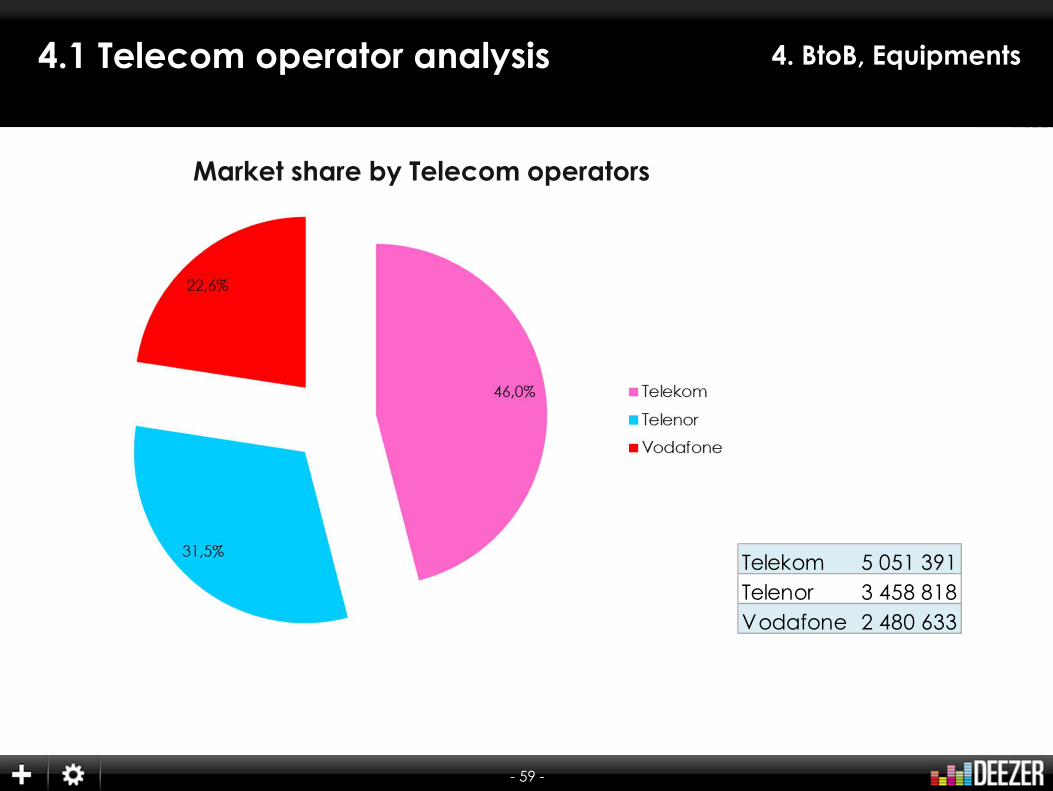

4. BtoB, Equipments4.1 Telecom operator analysis

Market share by Telecom operators

Telekom 5 051 391

Telenor 3 458 818

Vodafone 2 480 633

- 60 -

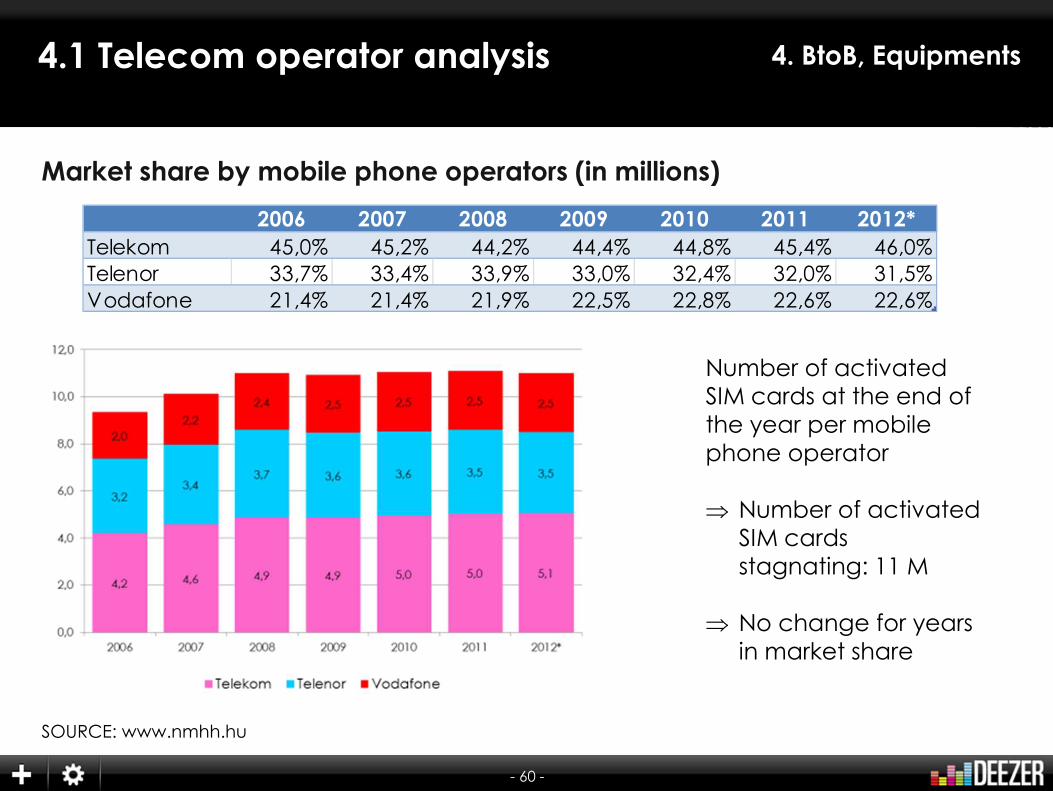

4. BtoB, Equipments4.1 Telecom operator analysis

Market share by mobile phone operators (in millions)

Number of activated SIM cards at the end of the year per mobile phone operator

⇒ Number of activated SIM cards stagnating: 11 M

⇒ No change for years in market share

SOURCE: www.nmhh.hu

2006 2007 2008 2009 2010 2011 2012*

Telekom 45,0% 45,2% 44,2% 44,4% 44,8% 45,4% 46,0%Telenor 33,7% 33,4% 33,9% 33,0% 32,4% 32,0% 31,5%Vodafone 21,4% 21,4% 21,9% 22,5% 22,8% 22,6% 22,6%

- 61 -

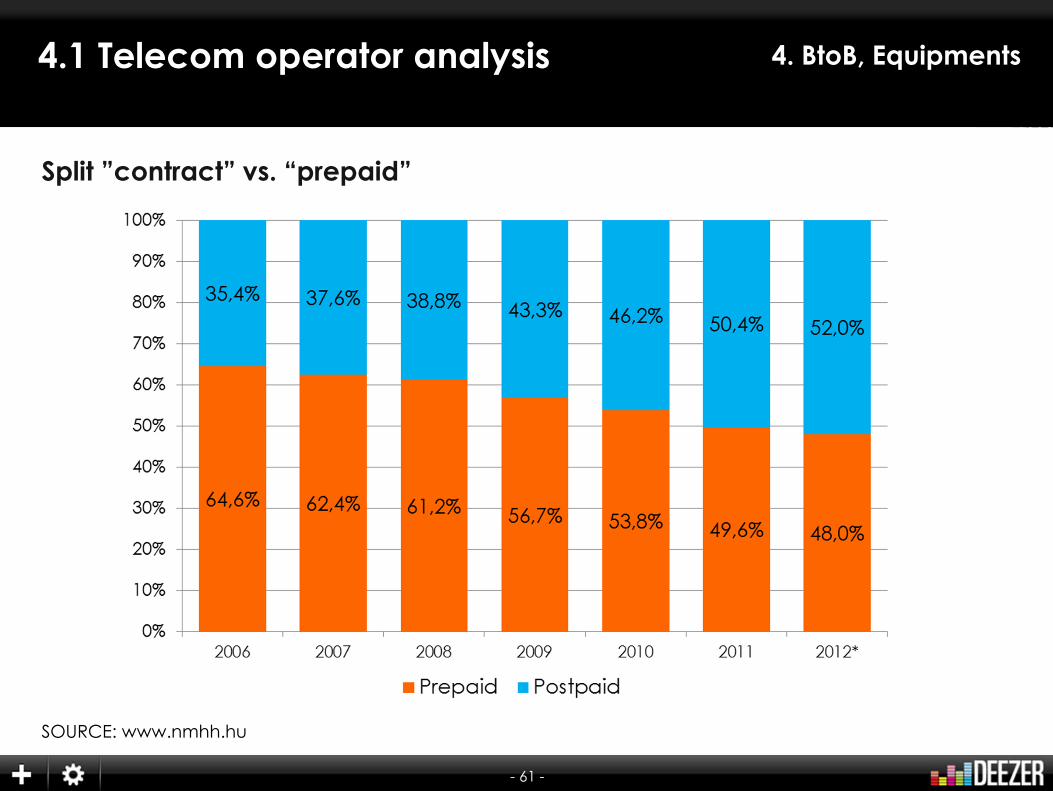

4. BtoB, Equipments4.1 Telecom operator analysis

Split ”contract” vs. “prepaid”

SOURCE: www.nmhh.hu

- 62 -

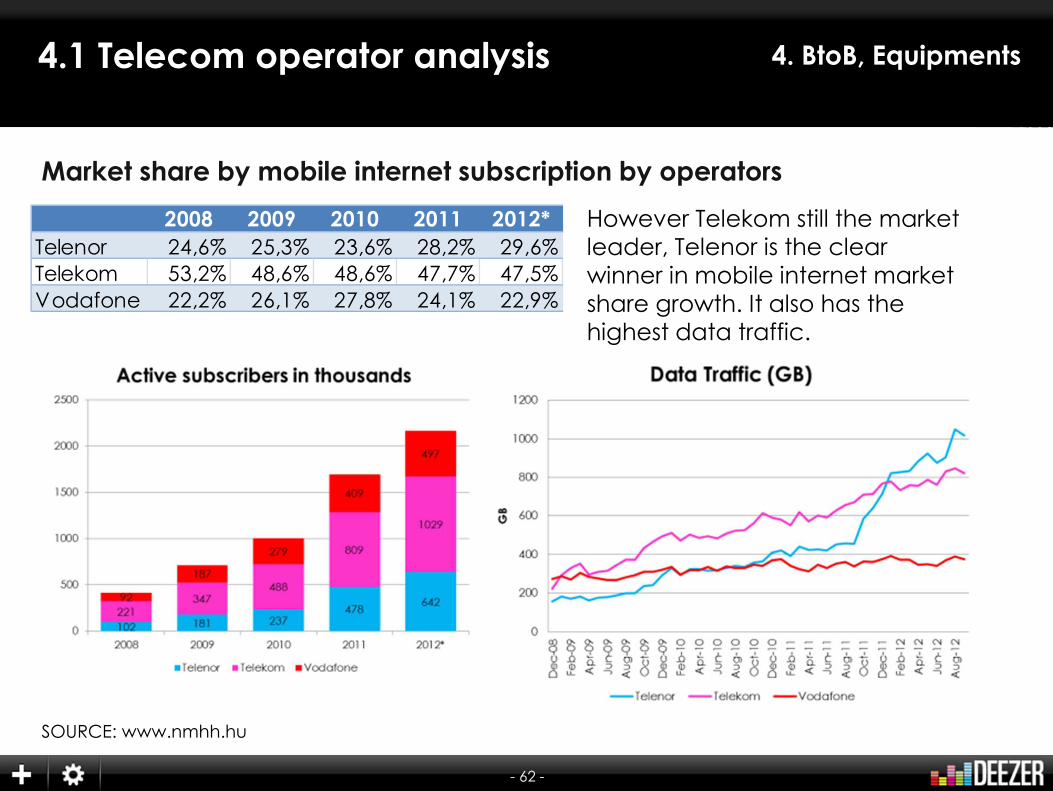

4. BtoB, Equipments4.1 Telecom operator analysis

Market share by mobile internet subscription by operators

SOURCE: www.nmhh.hu

2008 2009 2010 2011 2012*

Telenor 24,6% 25,3% 23,6% 28,2% 29,6%Telekom 53,2% 48,6% 48,6% 47,7% 47,5%Vodafone 22,2% 26,1% 27,8% 24,1% 22,9%

However Telekom still the market leader, Telenor is the clear winner in mobile internet market share growth. It also has the highest data traffic.

- 63 -

4. BtoB, Equipments4.2 Smartphones market vs. PC market

Smartphone users

SOURCE: Our Mobile Planet/Google, NMHH, NÉPSZABADSÁG

56%penetrationexpected in 2012

- 64 -

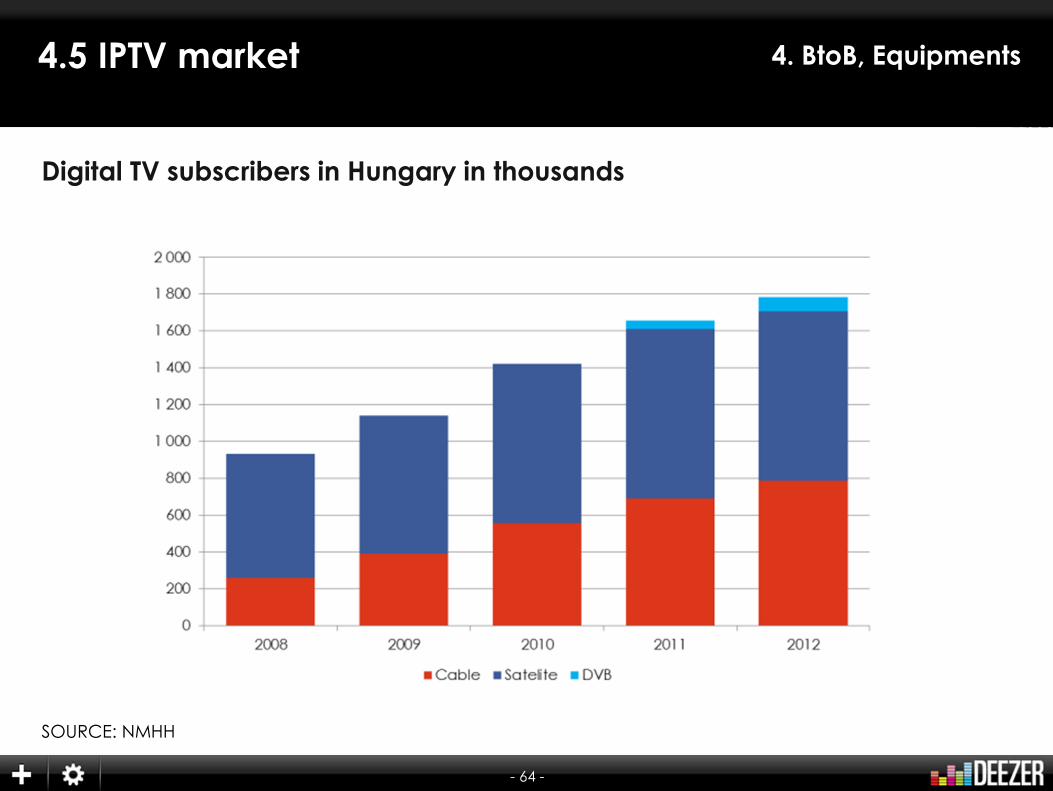

4. BtoB, Equipments4.5 IPTV market

Digital TV subscribers in Hungary in thousands

SOURCE: NMHH

- 65 -

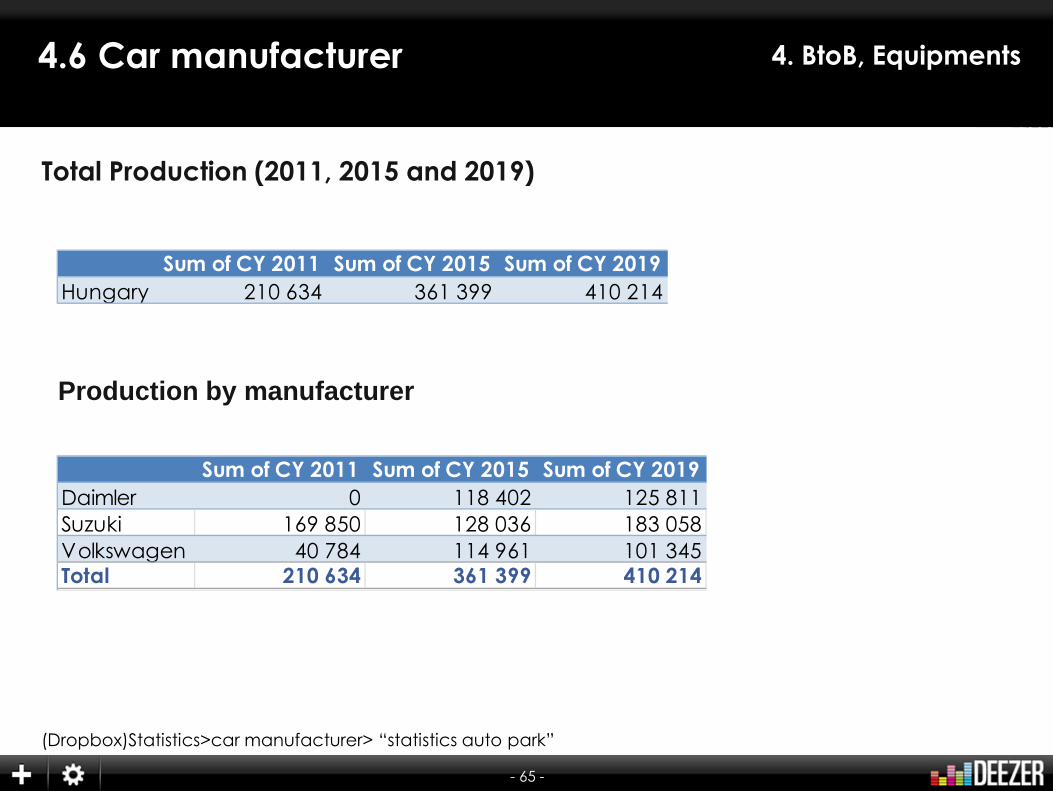

4. BtoB, Equipments4.6 Car manufacturer

Total Production (2011, 2015 and 2019)

(Dropbox)Statistics>car manufacturer> “statistics auto park”

Production by manufacturer

Sum of CY 2011 Sum of CY 2015 Sum of CY 2019

Hungary 210 634 361 399 410 214

Sum of CY 2011 Sum of CY 2015 Sum of CY 2019

Daimler 0 118 402 125 811Suzuki 169 850 128 036 183 058Volkswagen 40 784 114 961 101 345Total 210 634 361 399 410 214

- 66 -

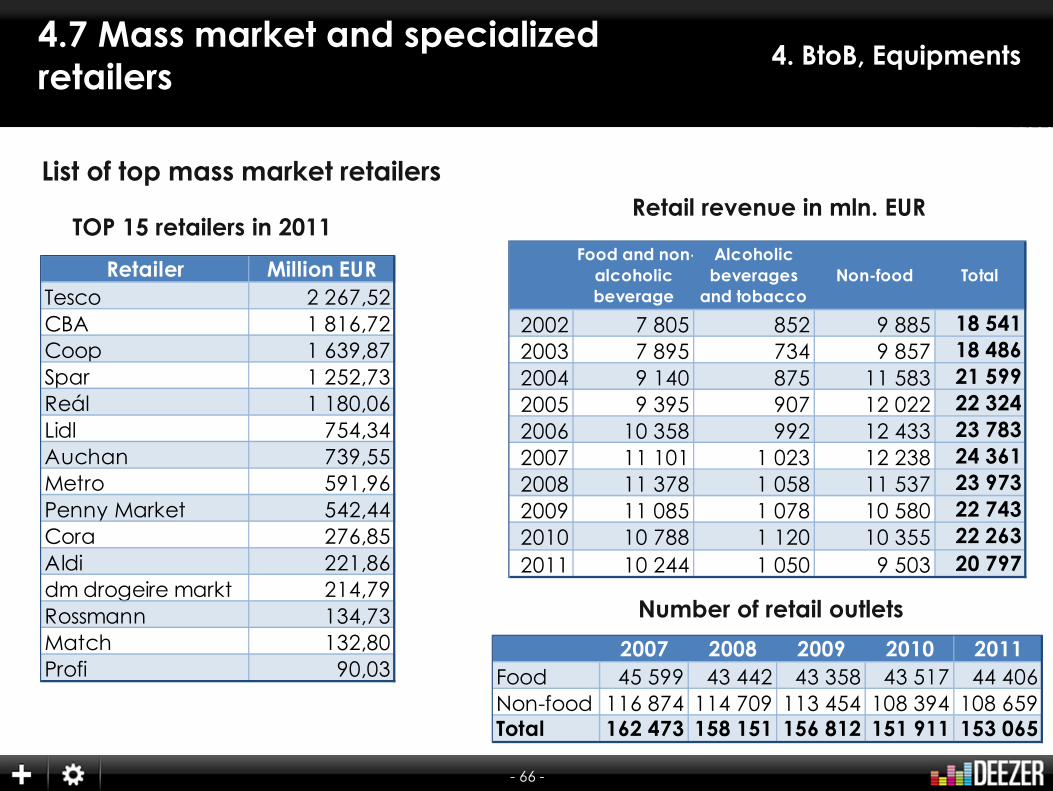

4. BtoB, Equipments4.7 Mass market and specialized

retailers

List of top mass market retailers

Retailer Million EUR

Tesco 2 267,52CBA 1 816,72Coop 1 639,87Spar 1 252,73Reál 1 180,06Lidl 754,34Auchan 739,55Metro 591,96Penny Market 542,44Cora 276,85Aldi 221,86dm drogeire markt 214,79Rossmann 134,73Match 132,80Profi 90,03

TOP 15 retailers in 2011

2007 2008 2009 2010 2011

Food 45 599 43 442 43 358 43 517 44 406Non-food 116 874 114 709 113 454 108 394 108 659Total 162 473 158 151 156 812 151 911 153 065

Number of retail outlets

Food and non-

alcoholic

beverage

Alcoholic

beverages

and tobacco

Non-food Total

2002 7 805 852 9 885 18 541

2003 7 895 734 9 857 18 486

2004 9 140 875 11 583 21 599

2005 9 395 907 12 022 22 324

2006 10 358 992 12 433 23 783

2007 11 101 1 023 12 238 24 361

2008 11 378 1 058 11 537 23 973

2009 11 085 1 078 10 580 22 743

2010 10 788 1 120 10 355 22 263

2011 10 244 1 050 9 503 20 797

Retail revenue in mln. EUR

- 67 -

4. BtoB, Equipments4.9 Conclusion

- 68 -

The Black Eyed Peas, Elephunk (2003), A&M/will.i.am/lnterscope

Let’s Get It StartedLet’s Get It StartedLet’s Get It StartedLet’s Get It StartedLet’s Get It Started

5. Usage

- 69 -

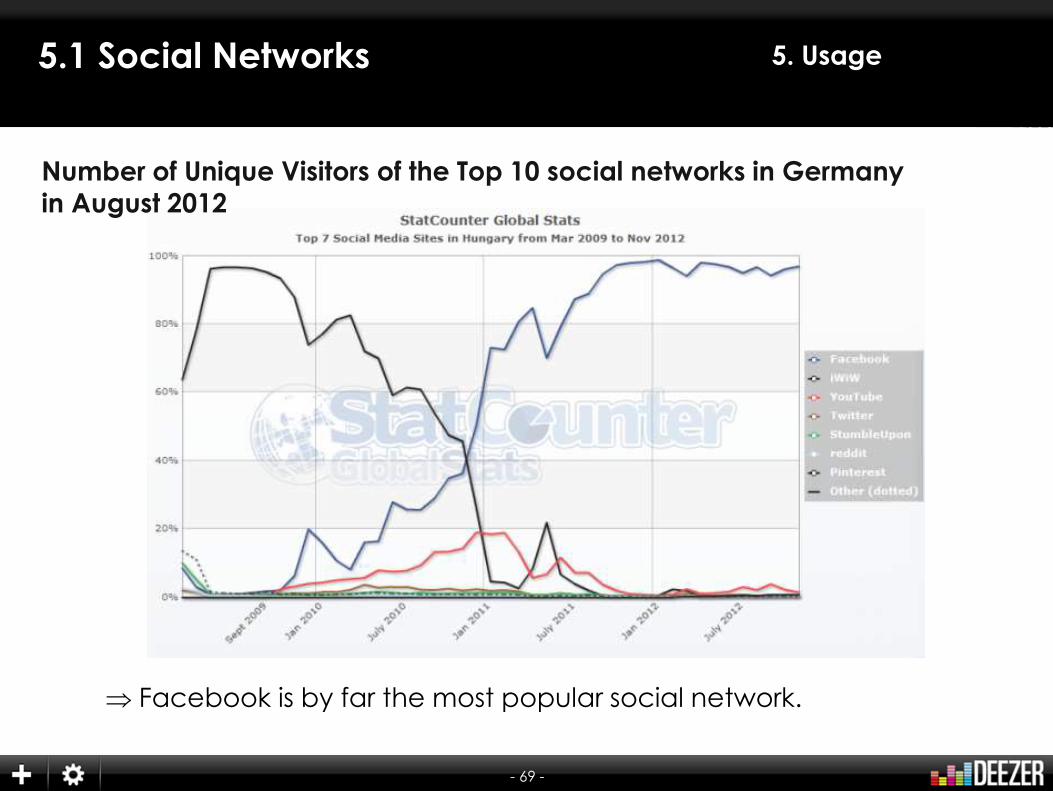

5. Usage5.1 Social Networks

Number of Unique Visitors of the Top 10 social networks in Germany

in August 2012

⇒ Facebook is by far the most popular social network.

- 70 -

5. Usage5.1 Social Networks

Your analysis and information + Extract of Social bakers profile

Total Facebook Users:4 222 660

Position in the list: 40

Facebook penetration in Hungary: 42,25%

Top Brands are mainly local:• 7 out of top 10 local• International brands:

• McDonald’s • Milka• ECCO Shoes

- 71 -

The Black Eyed Peas, Elephunk (2003), A&M/will.i.am/lnterscope

Let’s Get It StartedLet’s Get It StartedLet’s Get It StartedLet’s Get It StartedLet’s Get It Started

CONCLUSION

- 72 -

Conclusion

The population in Hungary is declining. The low birthrate of 1.33, the new wave of emigration due to economical reason are the main causes.

Since the population is shrinking and therefore our targeted group as well, we need to convert more people from physical market into the digital market. Besides focusing on the age group 20-39 we must focus on the younger age group 10-20 years old, since they have a high music interest. We need to find ways for this age group to access our service more easily in terms of pricing and payment. We have to target the elderly 45+ age group too, with content and artists, because this age group has dispensable income and were not targeted yet with digital music.

Our catalog contains all the major and most important independent labels. However most of the local content from the ’60s-’80s is missing. We need to convince Hungaroton, the label owning the rights, to get the streaming rights for this content, as the target audience will die out gradually. Streaming service, with its unlimited access to music in the first time in the life gives a good value for money proposition even for the customers, even in Hungary with a very high piracy rate. However there is a high need for education about the service. What is streaming, what are the advantages, how can I use it.

It is important for the Hungarian market to secure major label content, since they provide 90% of the digital content. The digital market is growing finally but is only 10% of the physical turnover. There’s a big potential on the digital market.

- 73 -

Conclusion

The mobile market is continually growing and represents a huge potential. Telenor our mobile partner in Hungary does a very good job to open our service to new target groups: young people that have the biggest interest in music but no access to our service due to the character of internet payment methods. However on mid- to long term we have to find a way to differentiate ourselves from Telenor as at the moment the general perception is that Deezer is only for Telenor customers. In general we need to be very thoughtful on planning our marketing campaign and message in a way, that we do not hurt our B2B partner.

We have to find other B2B partners, not only from telco, but also from financial or FMCG sector, let it be only for a campaign or for a longer cooperation.

We need to educate people and target groups about music streaming service in combination with Deezer. To market the brand Deezer alone is not converting people to our service. Our marketing message cannot communicate on the brand only but needs to have a clear and easily understandable message on what streaming services are and the advantages that they have.

We have to find a way for our B2C service to pay by money transfer and by cash (subscription cards or online terminals, as with mobile prepaid cards). Also very important to build an affiliate marketing service, such as Amazon provides. It is the cheapest way to get traffic to our site.

![[대학내일20대연구소]창업에대한대학생의생각을엿보다 20121122](https://img.pdfslide.tips/doc/110x75/55c31fcabb61eb17168b45d8/20-20121122.jpg)