Embed Size (px)

Citation preview

Morgan Stanley Convertible ConferenceSeptember 24, 2003

2

Forward Looking Information

Certain statements contained in this presentation are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are subject to the “safe harbor” created by those sections. Forward-looking statements include expressions of “belief,” “anticipation,” or “expectations” of management, statements as to industry trends or future results of operations of the Company, and other statements that are not historical fact. Forward-looking statements are based on certain assumptions by management and are subject to risks and uncertainties that could cause actual results to differ materially from those in the forward-looking statements. These risks and uncertainties include, but are not limited to: competitive pressures; factors that affect liquidity, delinquency rates, credit loss rates and charge-off rates; general economic conditions; consumer loan portfolio growth; changes in the cost and/or availability of funding due to changes in the deposit, credit or securitization markets, changes in the way in which the Company is perceived in such markets, and/or conditions relating to existing or future financing commitments; the effects of government policy and regulation, whether of general applicability or specific to the Company, including restrictions and/or limitations on the Company’s minimum capital requirements, deposit taking abilities, reserve methodologies, dividend policies and payments, growth, and/or underwriting criteria; year-end audit adjustments; changes in accounting rules, policies, practices and/or procedures; the success of product development efforts; legal and regulatory proceedings, including the impact of ongoing litigation; interest rates; acquisitions; one-time charges; extraordinary items; the ability to attract and retain key personnel and the impact of existing, modified or new strategic initiatives. These and other risks and uncertainties are described in detail in the Company’s Annual Report on Form 10-K and Annual Report to Stockholders for the fiscal year ended December 31, 2002 under the headings “Cautionary Statement Regard Forward-Looking Information”and “Risk Factors.” You are cautioned not to place undue reliance on any forward-looking statement, which speaks only as of the date thereof. The Company undertakes no obligation to update any forward-looking statements.

3

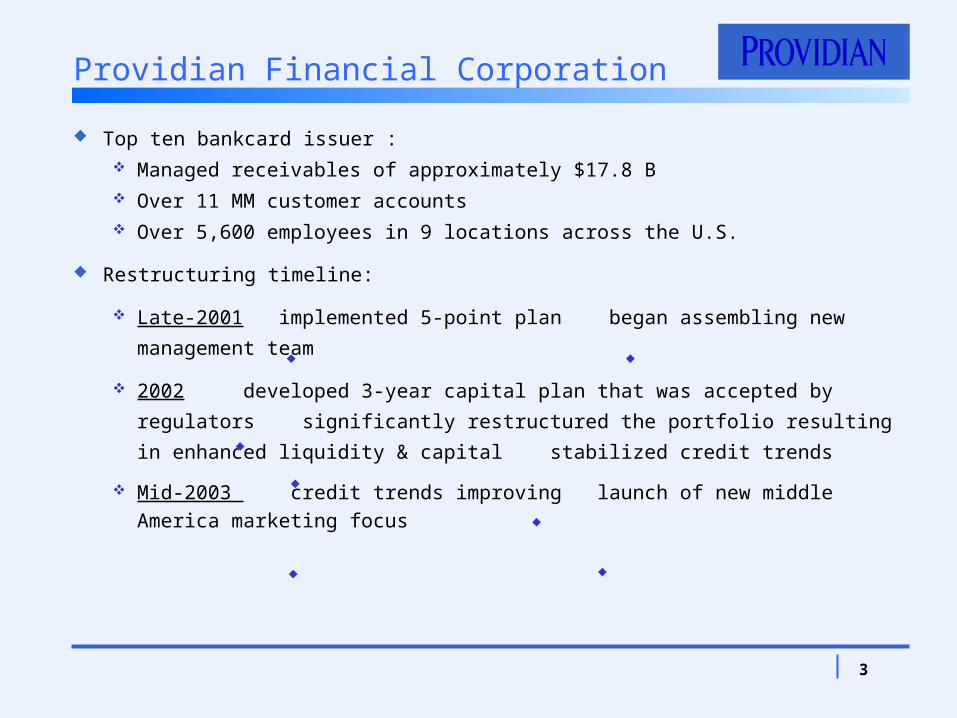

Top ten bankcard issuer : Managed receivables of approximately $17.8 B Over 11 MM customer accounts Over 5,600 employees in 9 locations across the U.S.

Restructuring timeline:

Late-2001 implemented 5-point plan began assembling new

management team

2002 developed 3-year capital plan that was accepted by regulators

significantly restructured the portfolio resulting in enhanced liquidity &

capital stabilized credit trends

Mid-2003 credit trends improving launch of new middle America marketing focus

Providian Financial Corporation

4

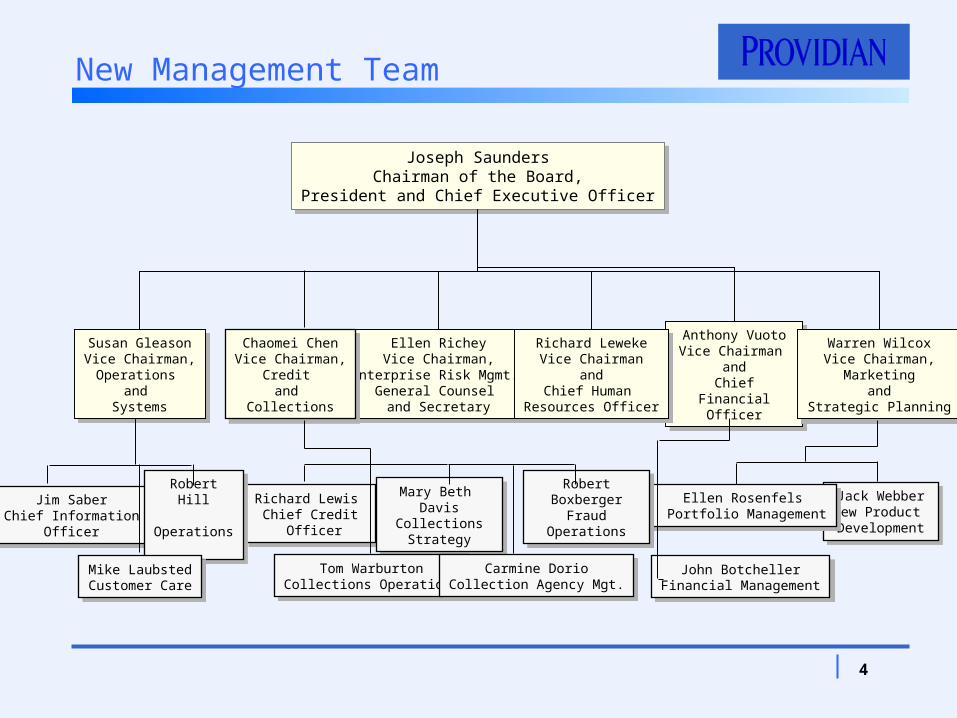

New Management Team

Joseph SaundersChairman of the Board,

President and Chief Executive Officer

Joseph SaundersChairman of the Board,

President and Chief Executive Officer

Susan GleasonVice Chairman,

Operations and

Systems

Susan GleasonVice Chairman,

Operations and

Systems

Ellen RicheyVice Chairman,

Enterprise Risk Mgmt.,General Counsel

and Secretary

Ellen RicheyVice Chairman,

Enterprise Risk Mgmt.,General Counsel

and Secretary

Anthony VuotoVice Chairman

andChief Financial

Officer

Anthony VuotoVice Chairman

andChief Financial

Officer

Warren WilcoxVice Chairman,

Marketingand

Strategic Planning

Warren WilcoxVice Chairman,

Marketingand

Strategic Planning

Richard LewekeVice Chairman

andChief Human

Resources Officer

Richard LewekeVice Chairman

andChief Human

Resources Officer

Chaomei ChenVice Chairman,

Credit and

Collections

Chaomei ChenVice Chairman,

Credit and

Collections

Jim Saber Chief Information

Officer

Jim Saber Chief Information

Officer

Richard Lewis Chief Credit

Officer

Richard Lewis Chief Credit

Officer

Jack WebberNew Product Development

Jack WebberNew Product Development

Ellen Rosenfels Portfolio Management

Ellen Rosenfels Portfolio Management

Robert Hill Operations

Robert Hill Operations

Mary Beth DavisCollections

Strategy

Mary Beth DavisCollections

Strategy

Tom WarburtonCollections Operations

Tom WarburtonCollections Operations

Robert BoxbergerFraud Operations

Robert BoxbergerFraud Operations

Carmine DorioCollection Agency Mgt.

Carmine DorioCollection Agency Mgt.

Mike LaubstedCustomer Care

Mike LaubstedCustomer Care

John BotchellerFinancial Management

John BotchellerFinancial Management

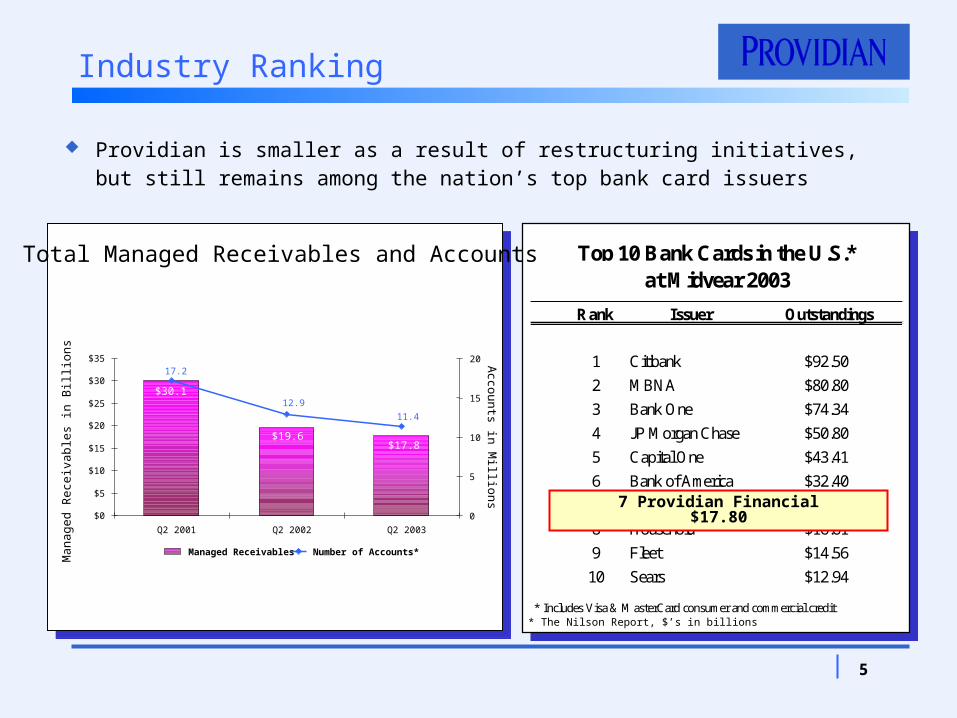

5

Rank Issuer Outstandings

1 Citibank $92.50

2 MBNA $80.80

3 Bank One $74.34

4 JP Morgan Chase $50.80

5 Capital One $43.41

6 Bank of America $32.40

7 Providian Financial $17.80

8 Household $16.61

9 Fleet $14.56

10 Sears $12.94

* Includes Visa & MasterCard consumer and commercial credit

Top 10 Bank Cards in the U.S.*at Midyear 2003

* The Nilson Report, $’s in billions

Industry Ranking

Providian is smaller as a result of restructuring initiatives, but still remains among the nation’s top bank card issuers

$30.1

$19.6$17.8

11.4

12.9

17.2

$0

$5

$10

$15

$20

$25

$30

$35

Q2 2001 Q2 2002 Q2 2003

0

5

10

15

20

Managed Receivables Number of Accounts*

Man

ag

ed

Rece

ivab

les

in B

illio

ns

Total Managed Receivables and Accounts

Acco

un

ts in M

illion

s

7 Providian Financial $17.80

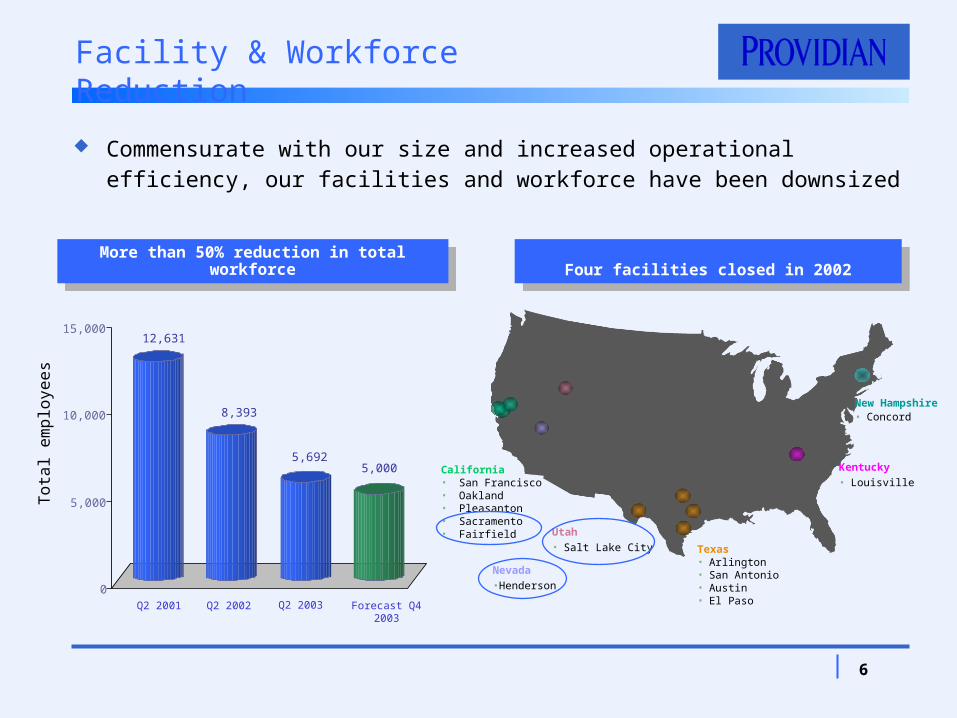

6

12,631

8,393

5,6925,000

0

5,000

10,000

15,000

To

tal e

mp

loye

es

Q2 2001 Q2 2002 Q2 2003 Forecast Q4 2003

More than 50% reduction in total workforce

More than 50% reduction in total workforce

Facility & Workforce Reduction

Commensurate with our size and increased operational efficiency, our facilities and workforce have been downsized

California• San Francisco• Oakland• Pleasanton• Sacramento• Fairfield

Kentucky• Louisville

New Hampshire• Concord

Four facilities closed in 2002Four facilities closed in 2002

Texas• Arlington • San Antonio • Austin • El Paso

Utah• Salt Lake City

Nevada•Henderson

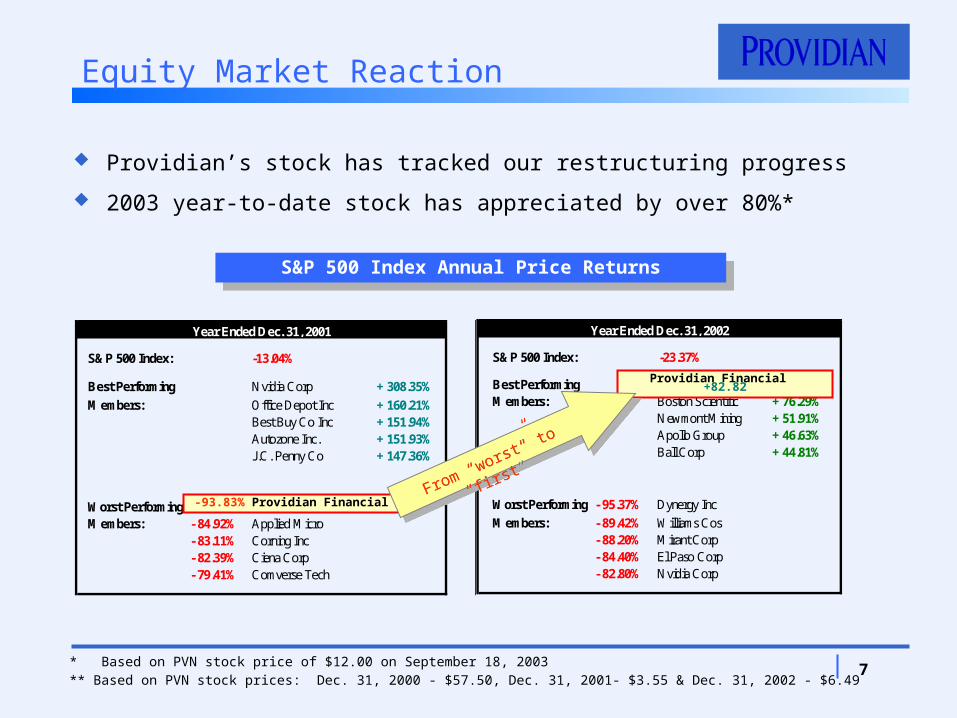

7

S&P 500 Index: -13.04%

Best Performing Nvidia Corp + 308.35%

Members: Office Depot Inc + 160.21%Best Buy Co Inc + 151.94%Autozone Inc. + 151.93%J.C. Penny Co + 147.36%

Worst Performing - 93.83% Providian FinancialMembers: - 84.92% Applied Micro

- 83.11% Corning Inc- 82.39% Ciena Corp- 79.41% Comverse Tech

Year Ended Dec. 31, 2001

S&P 500 Index: -23.37%

Best Performing Providian Financial + 82.82%Members: Boston Scientific + 76.29%

Newmont Mining + 51.91%Apollo Group + 46.63%Ball Corp + 44.81%

Worst Performing - 95.37% Dynergy Inc

Members: - 89.42% Williams Cos- 88.20% Mirant Corp- 84.40% El Paso Corp- 82.80% Nvidia Corp

Year Ended Dec. 31, 2002

Equity Market Reaction

Providian’s stock has tracked our restructuring progress

2003 year-to-date stock has appreciated by over 80%*

* Based on PVN stock price of $12.00 on September 18, 2003** Based on PVN stock prices: Dec. 31, 2000 - $57.50, Dec. 31, 2001- $3.55 & Dec. 31, 2002 - $6.49

S&P 500 Index Annual Price ReturnsS&P 500 Index Annual Price Returns

-93.83% Providian Financial

Providian Financial +82.82

From “worst” to “first

”

From “worst” to “first

”

8

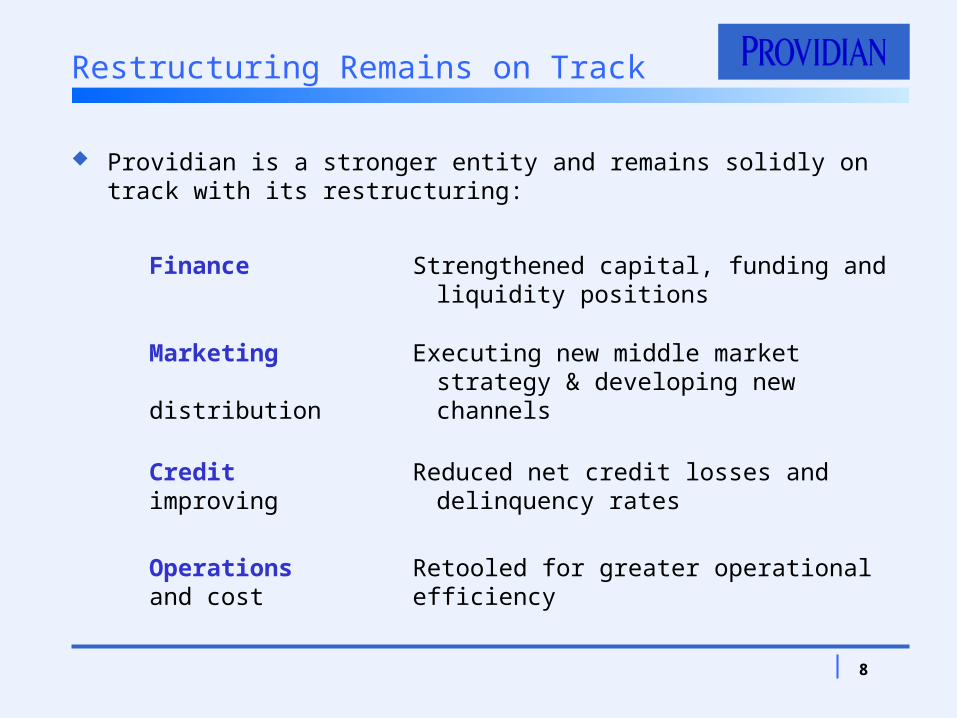

Restructuring Remains on Track

Providian is a stronger entity and remains solidly on track with its restructuring:

Finance Strengthened capital, funding and liquidity positions

Marketing Executing new middle market strategy & developing new distribution

channels

Credit Reduced net credit losses and improving delinquency rates

Operations Retooled for greater operational and cost efficiency

9

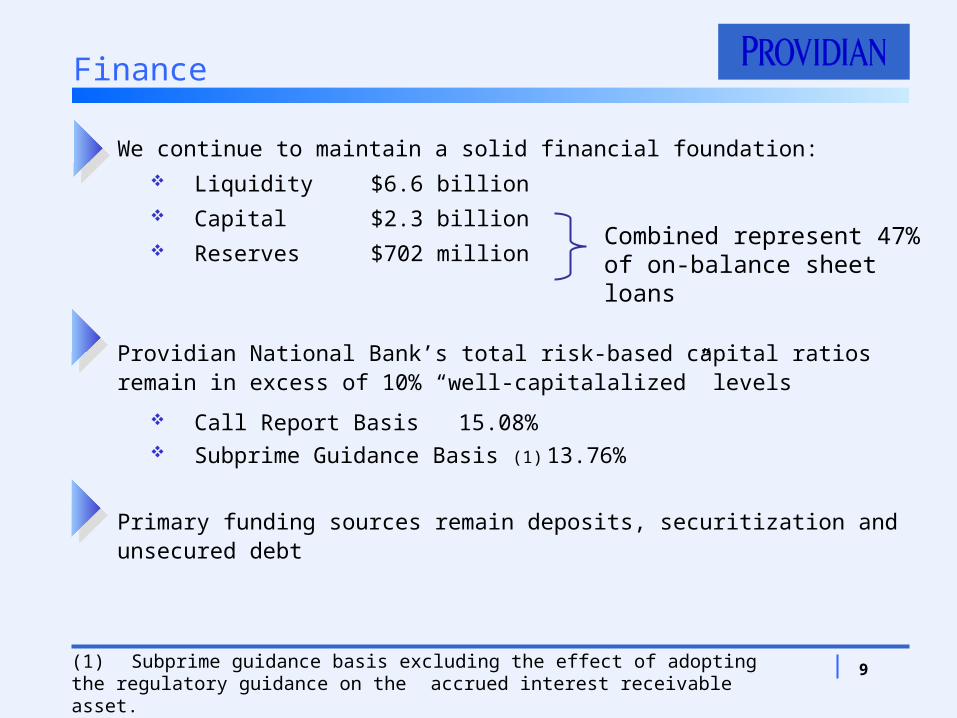

We continue to maintain a solid financial foundation: Liquidity $6.6 billion Capital $2.3 billion Reserves $702 million

Providian National Bank’s total risk-based capital ratios remain in excess of 10% “well-capitalalized” levels

Call Report Basis 15.08% Subprime Guidance Basis (1) 13.76%

Primary funding sources remain deposits, securitization and unsecured debt

Finance

Combined represent 47% of on-balance sheet loans

(1) Subprime guidance basis excluding the effect of adopting the regulatory guidance on the accrued interest receivable asset.

10

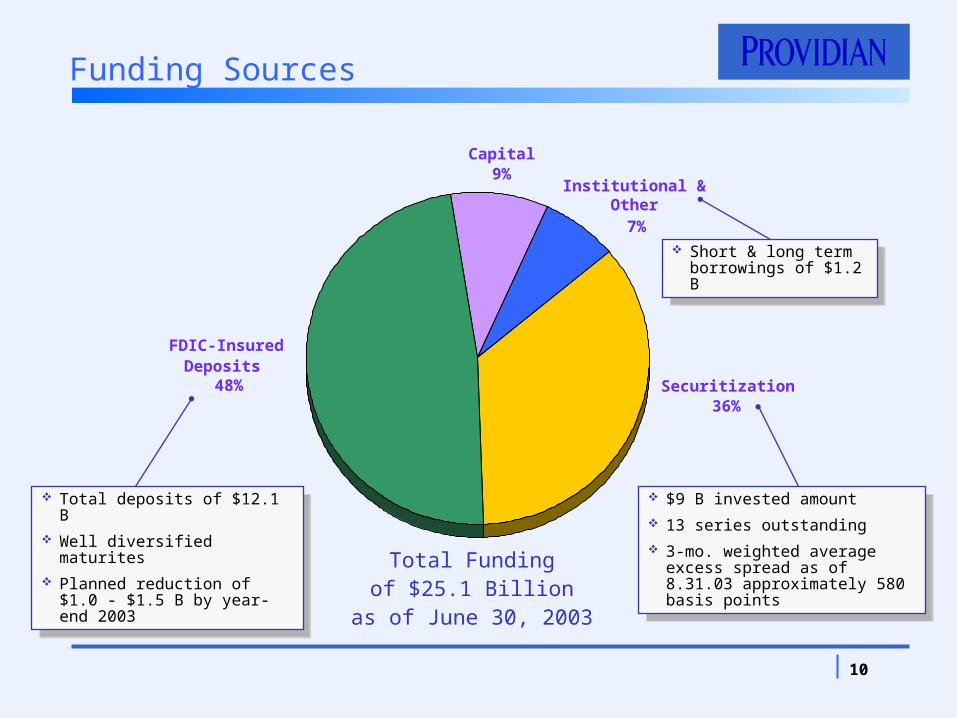

Total Fundingof $25.1 Billion

as of June 30, 2003

Funding Sources

Institutional & Other

7%

Securitization36%

Capital9%

FDIC-Insured Deposits

48%

Total deposits of $12.1 B Well diversified maturites Planned reduction of $1.0 -

$1.5 B by year-end 2003

Total deposits of $12.1 B Well diversified maturites Planned reduction of $1.0 -

$1.5 B by year-end 2003

$9 B invested amount 13 series outstanding 3-mo. weighted average

excess spread as of 8.31.03 approximately 580 basis points

$9 B invested amount 13 series outstanding 3-mo. weighted average

excess spread as of 8.31.03 approximately 580 basis points

Short & long term borrowings of $1.2 B

Short & long term borrowings of $1.2 B

11

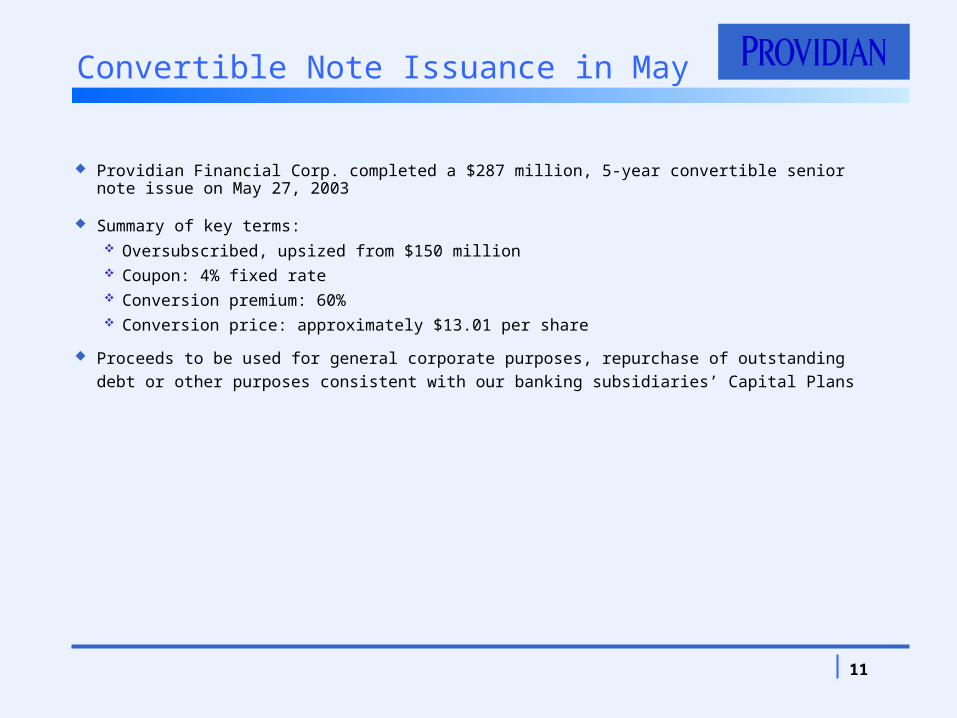

Convertible Note Issuance in May

Providian Financial Corp. completed a $287 million, 5-year convertible senior note issue on May 27, 2003

Summary of key terms: Oversubscribed, upsized from $150 million Coupon: 4% fixed rate Conversion premium: 60% Conversion price: approximately $13.01 per share

Proceeds to be used for general corporate purposes, repurchase of outstanding debt or other purposes consistent with our banking subsidiaries’ Capital Plans

12

Marketing Priorities

Pro-actively manage our existing portfolio to optimize performance

Maintain yields and reduce interest rate risk while improving credit quality of the portfolio

Pursue a new account acquisition strategy to recruit high quality, profitable prospects

Migrate acquisitions emphasis to Middle Market to capture greater profit potential and market opportunity

Develop new programs and channels to generate profitable growth consistent with our Middle America emphasis

Reposition the company by providing compelling new value propositions and customer experience

Leverage partner relationships

13

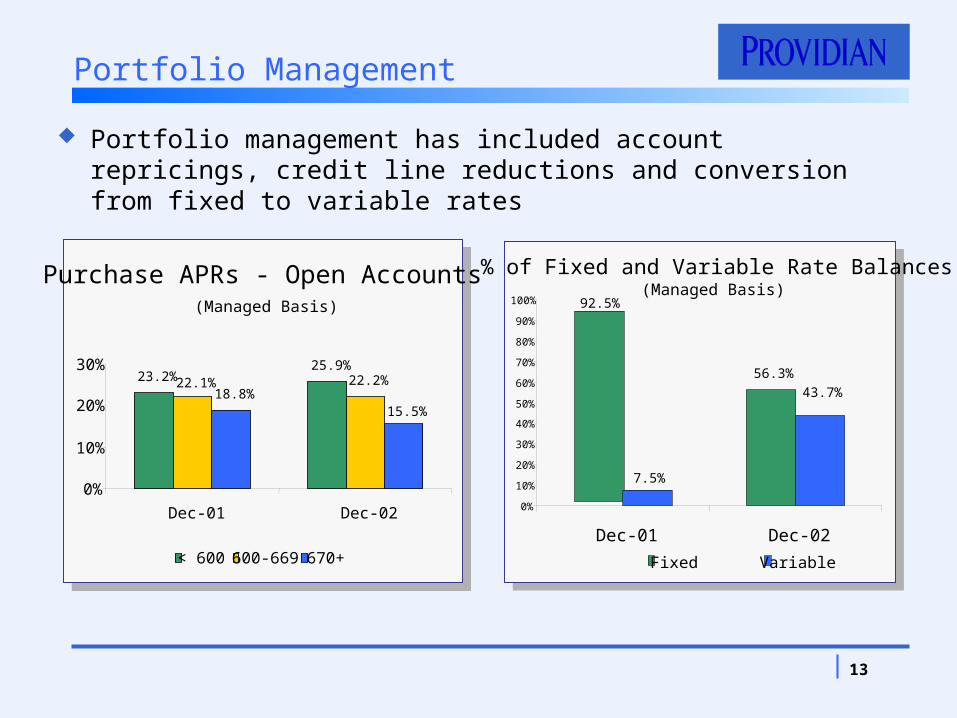

Portfolio Management

Portfolio management has included account repricings, credit line reductions and conversion from fixed to variable rates

% of Fixed and Variable Rate Balances

92.5%

56.3%

7.5%

43.7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Dec-01 Dec-02

Fixed Variable

Purchase APRs - Open Accounts

23.2%25.9%

22.2%18.8%

22.1%

15.5%

0%

10%

20%

30%

Dec-01 Dec-02

< 600 600-669 670+

(Managed Basis)(Managed Basis)

14

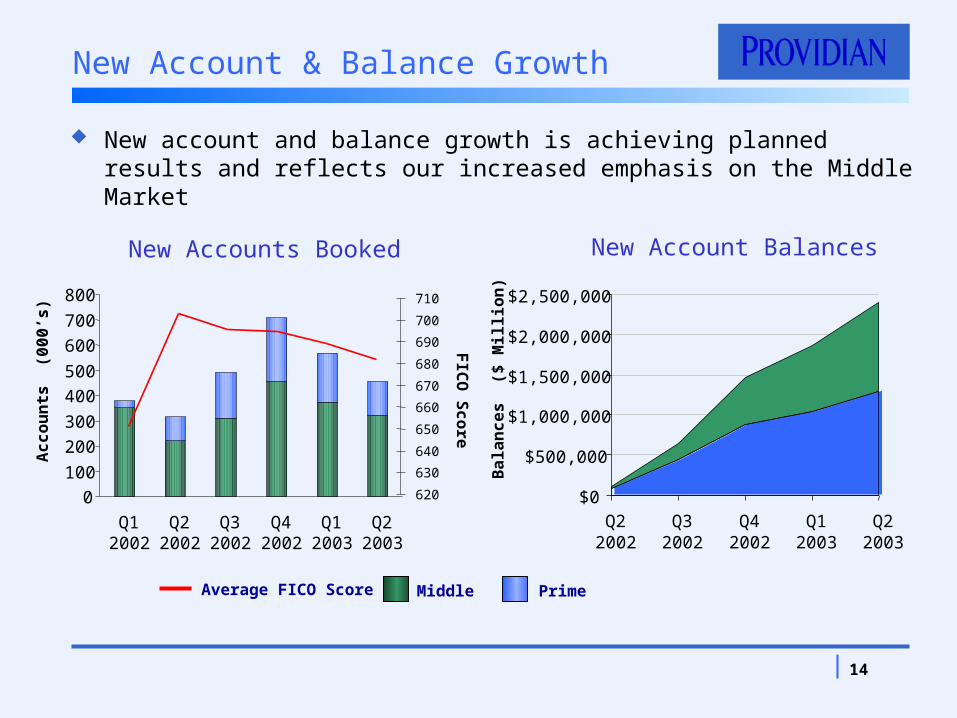

New Account & Balance Growth

New account and balance growth is achieving planned results and reflects our increased emphasis on the Middle Market

New Account Balances

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

Q22002

Q32002

Q42002

Q12003

Q22003

Ac

co

un

ts

(00

0’s

)

FIC

O S

co

re

New Accounts Booked

0100

200300

400500

600700

800

Q12002

Q22002

Q32002

Q42002

Q12003

Q22003

620

630

640

650

660

670

680

690

700

710

Ba

lan

ce

s

($ M

illi

on

)

PrimeMiddleAverage FICO Score

15

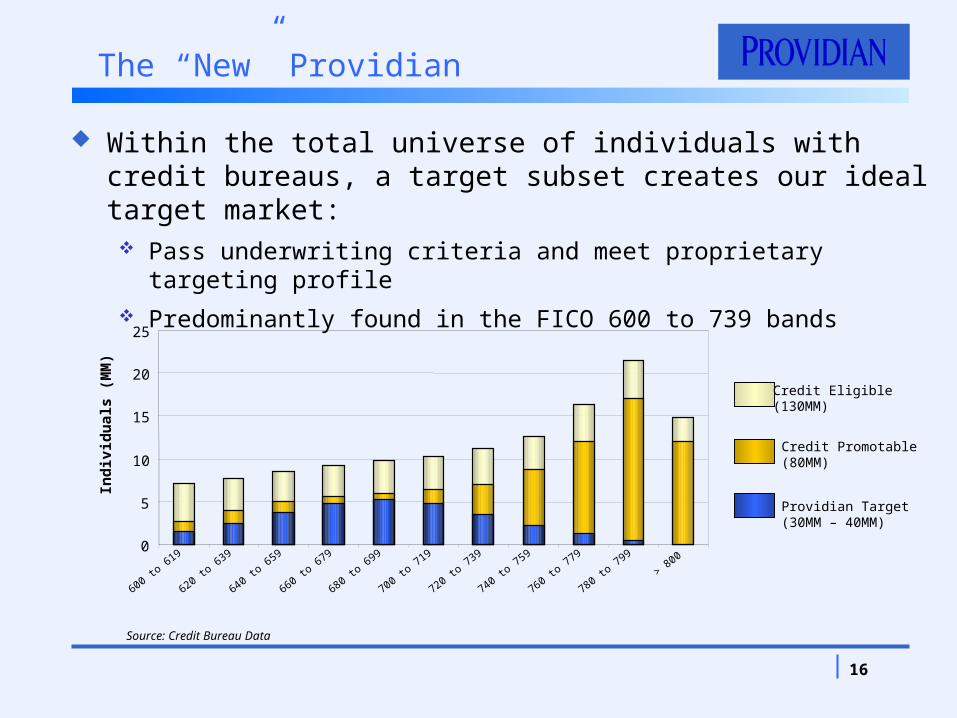

We have an opportunity to excel by focusing our company on serving “Middle Americans”

The “Middle America” market is attractive:

It’s large and targetable

It’s profitable

It’s receptive, less competitive and largely underserved

We have distinctive competencies and differentiated products and services which can be honed to enhance our competitive advantage

These competencies can be leveraged to differentiate Providian products and services, both under our own brand, and through relevant partner relationships

The “New” Providian

16

0

5

10

15

20

25

600 to 619

620 to 639

640 to 659

660 to 679

680 to 699

700 to 719

720 to 739

740 to 759

760 to 779

780 to 799

> 800

Ind

ivid

ual

s (M

M)

The “New” Providian

Within the total universe of individuals with credit bureaus, a target subset creates our ideal target market: Pass underwriting criteria and meet proprietary targeting profile Predominantly found in the FICO 600 to 739 bands

Source: Credit Bureau Data

Credit Eligible (130MM)

Credit Promotable(80MM)

Providian Target(30MM – 40MM)

17

$14

$21

$35

$45

$32

$24

$19

$0

$10

$20

$30

$40

$50

600-619 620-639 640-659 660-679 680-699 700-719 720-739

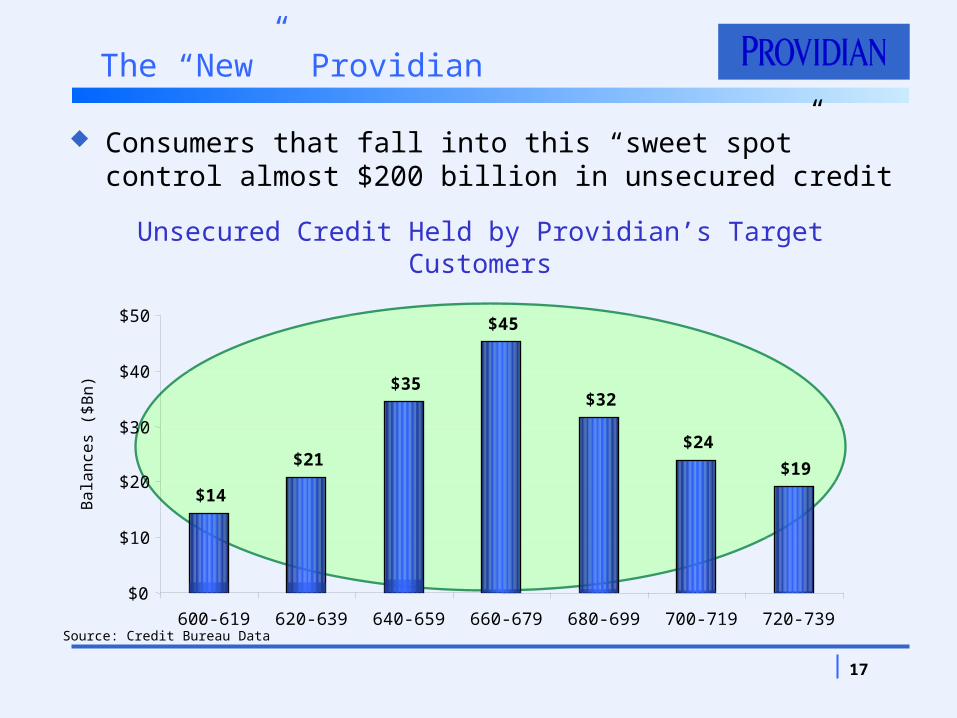

The “New” Providian

Unsecured Credit Held by Providian’s Target Customers

Consumers that fall into this “sweet spot” control almost $200 billion in unsecured credit

Source: Credit Bureau Data

Bal a

nce

s ($

Bn)

18

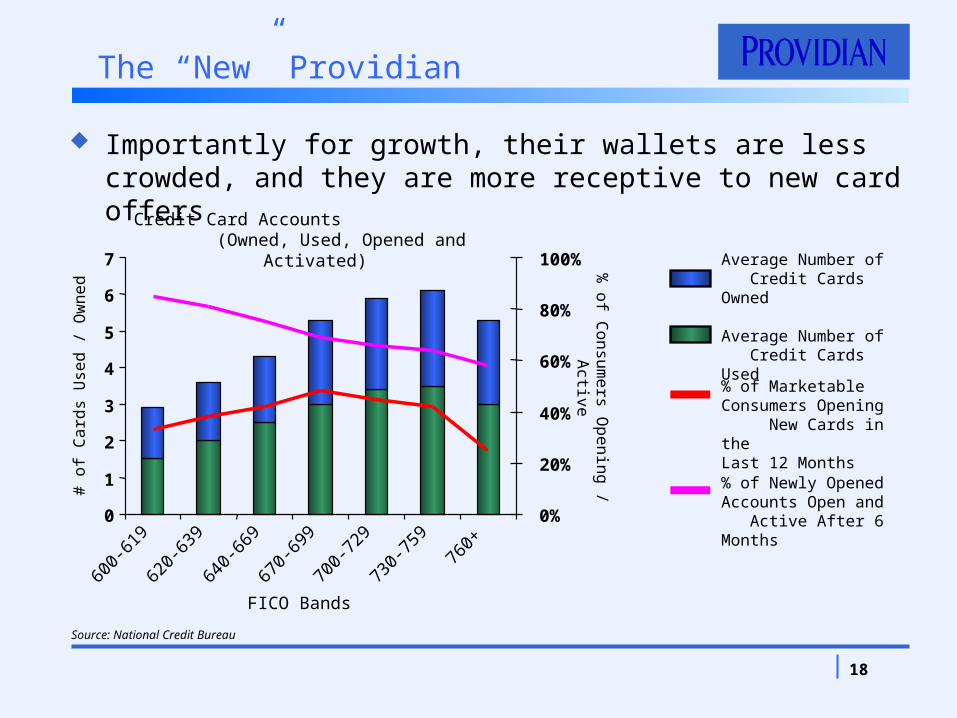

The “New” Providian

Importantly for growth, their wallets are less crowded, and they are more receptive to new card offers

0

1

2

3

4

5

6

7

600-

619

620-

639

640-

669

670-

699

700-

729

730-

759

760+

0%

20%

40%

60%

80%

100%Average Number of Credit Cards Owned

Average Number of Credit Cards Used

Source: National Credit Bureau

# o

f C

ard

s U

sed /

Ow

ned

% o

f Consu

mers O

penin

g / A

ctive

FICO Bands

Credit Card Accounts (Owned, Used, Opened and Activated)

% of Newly Opened Accounts Open and Active After 6 Months

% of Marketable Consumers Opening New Cards in the Last 12 Months

19

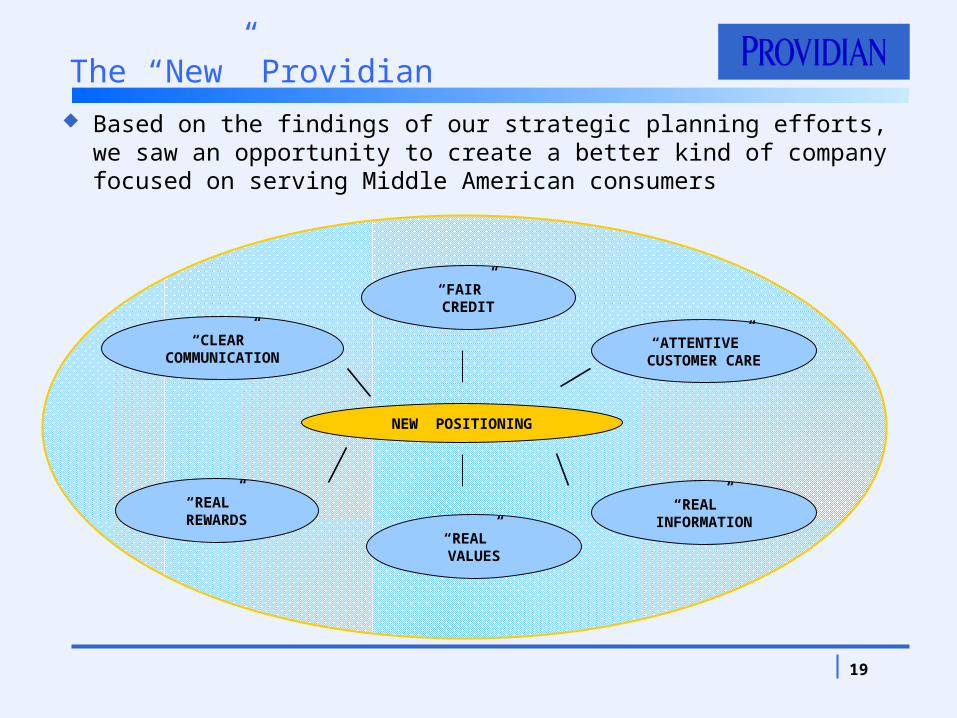

“REAL” VALUES

NEW POSITIONING

“REAL” INFORMATION

“ATTENTIVE” CUSTOMER

CARE

“REAL” REWARDS

“FAIR” CREDIT

“CLEAR”COMMUNICATION

Based on the findings of our strategic planning efforts, we saw an opportunity to create a better kind of company focused on serving Middle American consumers

The “New” Providian

20

Strategic Marketing Partnerships

Strategic marketing partnerships are expected to be a core component of our future marketing efforts

We are in latter stages of discussions with several entities on co-branded relationships:

Consistent with strategy Expected to begin producing accounts before year-

end

PayPal co-branded program is producing solid results

Working with partner to expand distribution

21

Credit & Collections

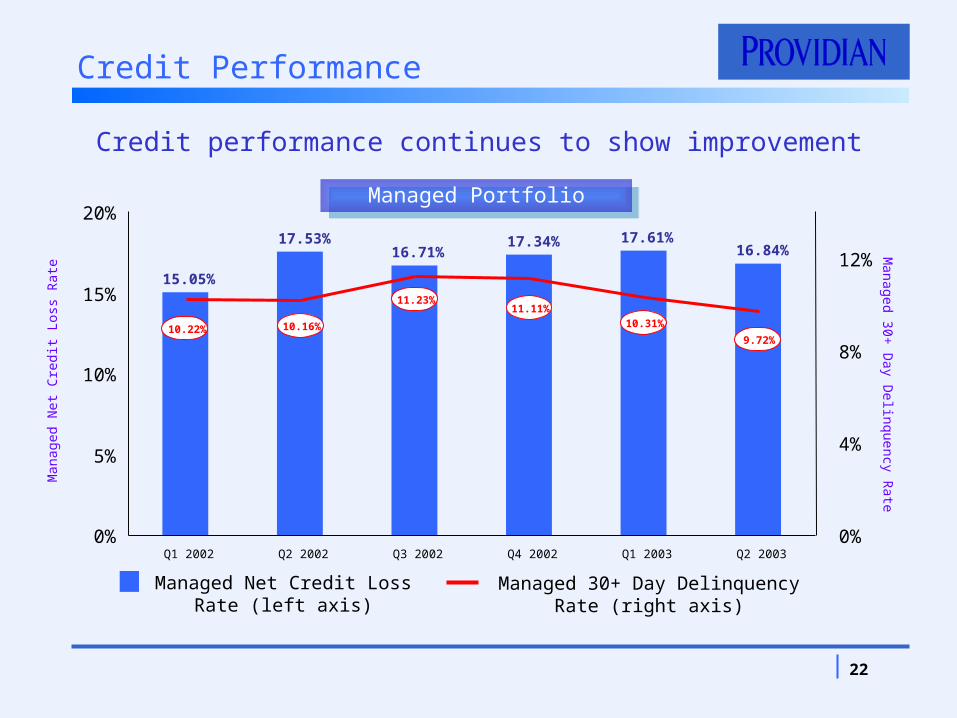

Credit performance continues to show improvement:

Managed net credit loss dollars continue to decline

Managed 30+ day delinquency rate in single digits

Managed net credit losses first half 2003 $1.59 B

Managed net credit loss guidance:

Full-year 2003 net credit losses $2.85 B

Third quarter 2003 $650 MM

22

Credit Performance

Managed 30+ Day Delinquency Rate (right axis)

Managed Net Credit Loss Rate (left axis)

Managed 30+

Day D

elinquency Rate

Man

aged

Net

Cre

dit L

oss

Rat

e 15.05%

17.53%16.71%

17.34% 17.61%16.84%

0%

5%

10%

15%

20%

Q1 2002 Q2 2002 Q3 2002 Q4 2002 Q1 2003 Q2 20030%

4%

8%

12%

10.22% 10.16%

11.23%11.11%

10.31%

9.72%

Credit performance continues to show improvement

Managed PortfolioManaged Portfolio

23

Annualized Dollar Chargeoff Rate

0%

5%

10%

15%

20%

25%

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

Account Age (in Months)

1998199920002001200201200202200203200204200205200206200207200208200209200210200211200212200301200302200303200304

Impact of Credit Initiatives

1998 - 2001 vintages

Early- 2002 vintages

Mid-2002 to early 2003 vintages

24

Operations & Enterprise Technology

Focus on quality performance and creating customer centric culture and processes

Develop flexible, robust platforms to support new opportunities Conversion to TS2 completed in August

Build a culture of continual improvement and cost reduction

Eliminate redundancies and outsource non-core activities to realize savings

Outsourced development activities to Accenture in August

25

Summary

Providian is a stronger entity and remains solidly on track with its restructuring:

Finance Strengthened capital, funding and liquidity positions

Marketing Executing new middle market strategy & developing new distribution

channels

Credit Reduced net credit losses and improving delinquency rates

Operations Retooled for greater operational and cost efficiency

Financial Addendum

28

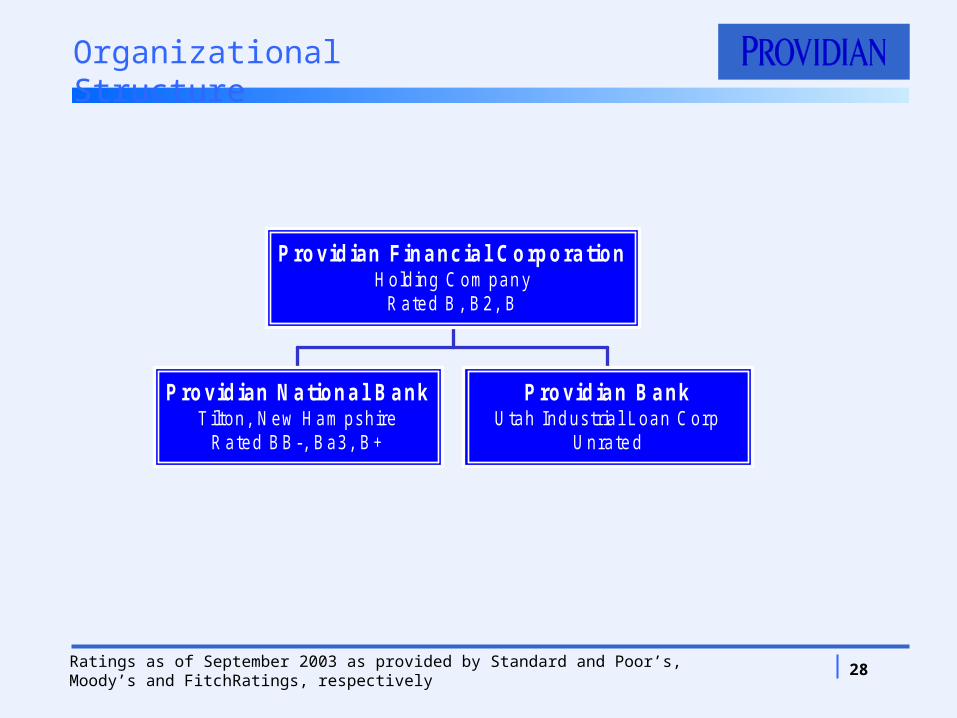

Organizational Structure

Providian National BankT ilton, New Ham pshire

Rated BB-, Ba3, B+

Providian BankUtah Ind ustrial L oan Corp

Unrate d

Providian Financial CorporationHolding C om pan y

Rated B , B2, B

Ratings as of September 2003 as provided by Standard and Poor’s, Moody’s and FitchRatings, respectively

29

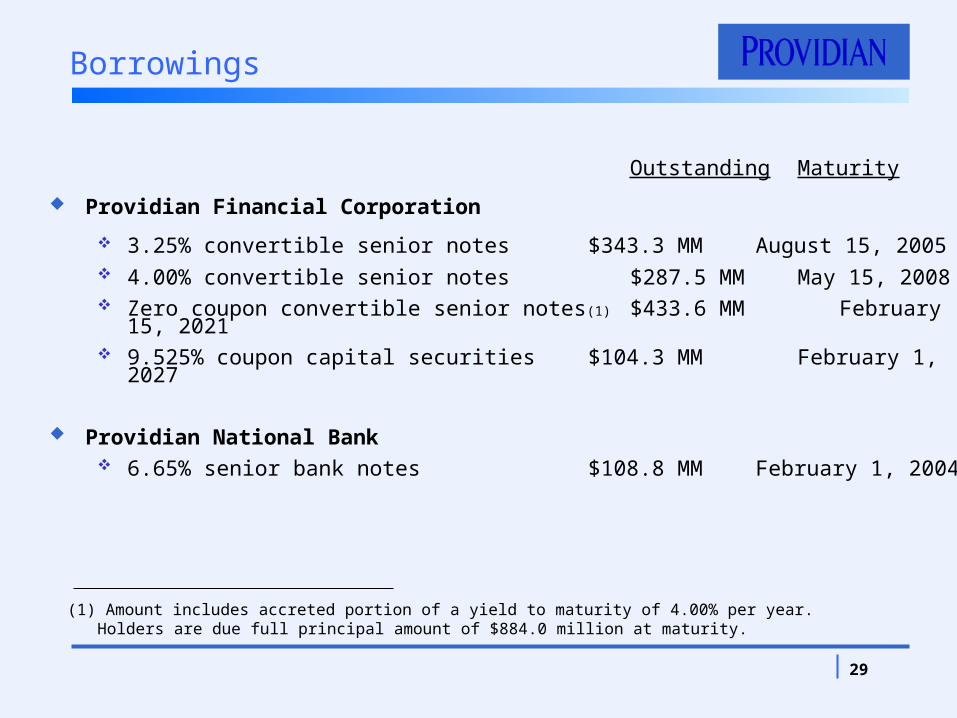

Borrowings

Outstanding Maturity

Providian Financial Corporation

3.25% convertible senior notes $343.3 MM August 15, 2005 4.00% convertible senior notes $287.5 MM May 15, 2008 Zero coupon convertible senior notes(1) $433.6 MM February 15, 2021 9.525% coupon capital securities $104.3 MM February 1, 2027

Providian National Bank 6.65% senior bank notes $108.8 MM February 1, 2004

(1) Amount includes accreted portion of a yield to maturity of 4.00% per year. Holders are due full principal amount of $884.0 million at maturity.

30

Non-GAAP Managed Financial Information

Loans that have been securitized and sold to third party investors are not considered to be our assets under GAAP and therefore are not shown on our balance sheet. However, the interests we retain in the securitized loan pools create financial exposure to the current and expected cash flows of the securitized loans. Although the loans sold are not on our balance sheet, their performance can affect some or all of our retained interests as well as our results of operations and our financial position. In addition, we continue to service these loans.

Because of this continued exposure and involvement, we use managed financial information to evaluate our historical performance, assess our current condition, and plan our future operations. We believe that managed financial information supplements our GAAP information and is helpful to the reader’s understanding of our consolidated financial condition and results of operations. “Reported” financial information refers to GAAP financial information. “Managed” financial information is derived by adjusting the reported financial information to add back securitized loan balances and the related finance charge and fee income, credit losses, and net interest costs.

The Company discloses certain projected financial measures relating to expected performance on a managed basis, such as net credit losses, net interest income margin and non-interest income margin. The Company develops such projections on a managed basis using managed financial information and does not in the normal course derive comparable GAAP projections. Developing such comparable GAAP projections would be unreasonably burdensome and in the opinion of management such comparable GAAP projections would not provide to the users of the financial information a significant benefit in understanding the Company’s expected future performance.

31

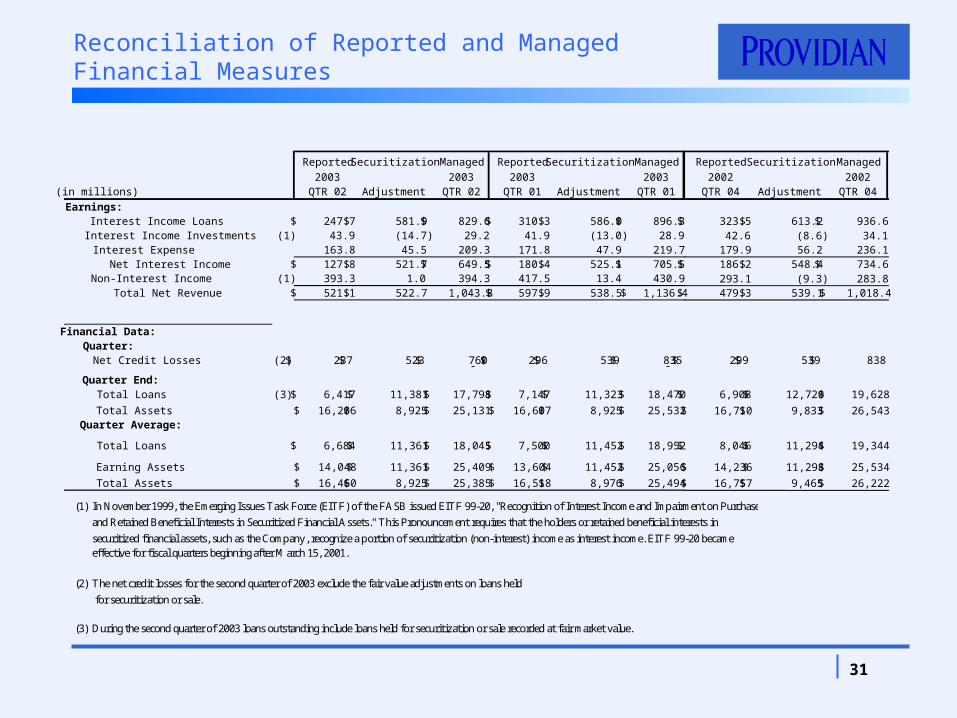

Reported Securitization Managed Reported Securitization Managed

2003 2003 2003 2003(in millions) QTR 02 Adjustment QTR 02 QTR 01 Adjustment QTR 01

Earnings:Interest Income Loans 247.7$ 581.9$ 829.6$ 310.3$ 586.0$ 896.3$ Interest Income Investments (1) 43.9 (14.7) 29.2 41.9 (13.0) 28.9 Interest Expense 163.8 45.5 209.3 171.8 47.9 219.7 Net Interest Income 127.8$ 521.7$ 649.5$ 180.4$ 525.1$ 705.5$ Non-Interest Income (1) 393.3 1.0 394.3 417.5 13.4 430.9 Total Net Revenue 521.1$ 522.7$ 1,043.8 597.9$ 538.5$ 1,136.4$

Financial Data:Quarter:

Net Credit Losses (2) 237$ 523$ 760$ 296$ 539$ 835$ - - Quarter End:

Total Loans (3) 6,417$ 11,381$ 17,798$ 7,147$ 11,323$ 18,470$

Total Assets 16,206$ 8,925$ 25,131$ 16,607$ 8,925$ 25,532$ Quarter Average:

Total Loans 6,684$ 11,361$ 18,045$ 7,500$ 11,452$ 18,952$

Earning Assets 14,048$ 11,361$ 25,409$ 13,604$ 11,452$ 25,056$

Total Assets 16,460$ 8,925$ 25,385$ 16,518$ 8,976$ 25,494$

Reported Securitization Managed

2002 2002QTR 04 Adjustment QTR 04

323.5$ 613.2$ 936.6$ 42.6 (8.6) 34.1

179.9 56.2 236.1 186.2$ 548.4$ 734.6$ 293.1 (9.3) 283.8 479.3$ 539.1$ 1,018.4$

299$ 539$ 838$

6,908$ 12,720$ 19,628$

16,710$ 9,833$ 26,543$

8,046$ 11,294$ 19,344$

14,236$ 11,298$ 25,534$

16,757$ 9,465$ 26,222$

Reconciliation of Reported and Managed Financial Measures

(1) In November 1999, the Emerging Issues Task Force (EITF) of the FASB issued EITF 99-20, "Recognition of Interest Income and Impairment on Purchased

and Retained Beneficial Interests in Securitized Financial Assets." This Pronouncement requires that the holders or retained beneficial interests in

securitized financial assets, such as the Company, recognize a portion of securitization (non-interest) income as interest income. EITF 99-20 becameeffective for fiscal quarters beginning after March 15, 2001.

(2) The net credit losses for the second quarter of 2003 exclude the fair value adjustments on loans held

for securitization or sale.

(3) During the second quarter of 2003 loans outstanding include loans held for securitization or sale recorded at fair market value.

32

Reported Securitization Managed Reported Securitization Managed2002 2002 2002 2002

QTR 03 Adjustment QTR 03 QTR 02 Adjustment QTR 02

328.2$ 656.2$ 984.4$ 350.5$ 654.5$ 1,005.0$ 60.3 (13.2) 47.1 53.9 (14.7) 39.2

189.0 62.7 251.7 196.0 65.0 261.0 199.5$ 580.3$ 779.8$ 208.4$ 574.8$ 783.2$ 465.1 (21.0) 444.1 509.9 22.7 532.6 664.6$ 559.3$ 1,223.9$ 718.3$ 597.5$ 1,315.8$

244$ 559$ 804$ 269$ 598$ 867$

8,198$ 11,255$ 19,453$ 7,513$ 12,126$ 19,639$

17,218$ 9,675$ 26,893$ 17,799$ 10,215$ 28,014$

7,305$ 11,932$ 19,237$ 7,578$ 12,195$ 19,773$

15,011$ 11,932$ 26,942$ 14,243$ 12,195$ 26,438$

17,384$ 10,127$ 27,511$ 18,319$ 10,257$ 28,576$

(in millions)Earnings:

Interest Income LoansInterest Income Investments (1)Interest Expense Net Interest IncomeNon-Interest Income (1) Total Net Revenue

Financial Data:Quarter:

Net Credit Losses (2)

Quarter End:Total Loans (3)

Total AssetsQuarter Average:

Total Loans

Earning Assets

Total Assets

(1) In November 1999, the Emerging Issues Task Force (EITF) of the FASB issued EITF 99-20, "Recognition of Interest Income and Impairment on Purchased

and Retained Beneficial Interests in Securitized Financial Assets." This Pronouncement requires that the holders or retained beneficial interests in

securitized financial assets, such as the Company, recognize a portion of securitization (non-interest) income as interest income. EITF 99-20 becameeffective for fiscal quarters beginning after March 15, 2001.

(2) The net credit losses for the second quarter of 2003 exclude the fair value adjustments on loans held

for securitization or sale.

(3) During the second quarter of 2003 loans outstanding include loans held for securitization or sale recorded at fair market value.

Reconciliation of Reported and Managed Financial Measures

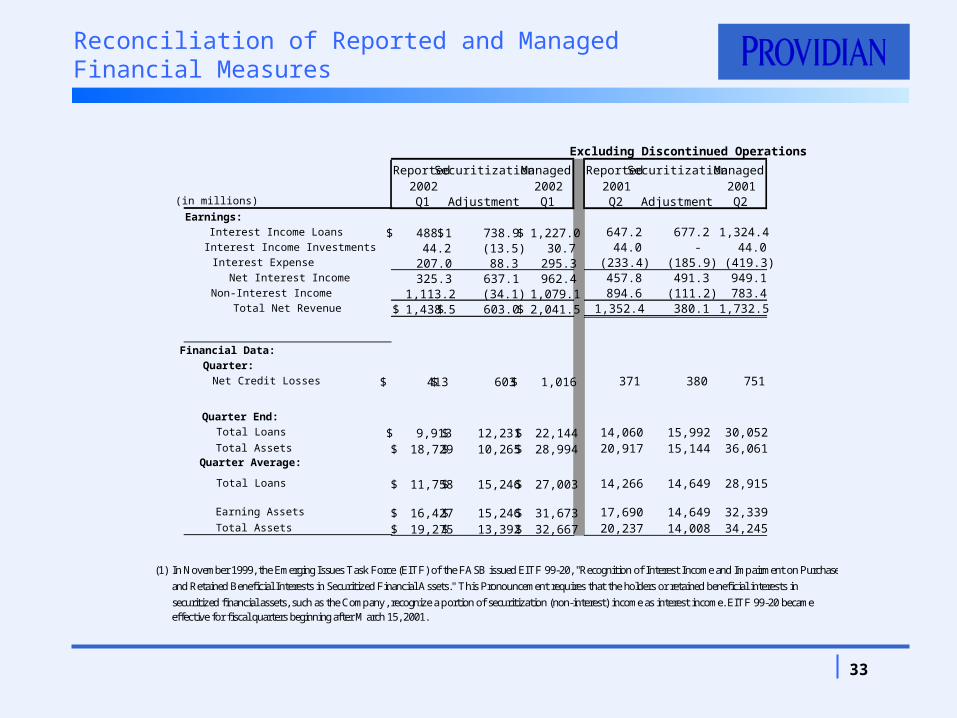

33

Reconciliation of Reported and Managed Financial Measures

(1) In November 1999, the Emerging Issues Task Force (EITF) of the FASB issued EITF 99-20, "Recognition of Interest Income and Impairment on Purchased

and Retained Beneficial Interests in Securitized Financial Assets." This Pronouncement requires that the holders or retained beneficial interests in

securitized financial assets, such as the Company, recognize a portion of securitization (non-interest) income as interest income. EITF 99-20 becameeffective for fiscal quarters beginning after March 15, 2001.

Excluding Discontinued Operations

Reported Securitization Managed Reported Securitization Managed2002 2002 2001 2001Q1 Adjustment Q1 Q2 Adjustment Q2

488.1$ 738.9$ 1,227.0$ 647.2 677.2 1,324.4 44.2 (13.5) 30.7 44.0 - 44.0

207.0 88.3 295.3 (233.4) (185.9) (419.3) 325.3 637.1 962.4 457.8 491.3 949.1

1,113.2 (34.1) 1,079.1 894.6 (111.2) 783.4 1,438.5$ 603.0$ 2,041.5$ 1,352.4 380.1 1,732.5

413$ 603$ 1,016$ 371 380 751

9,913$ 12,231$ 22,144$ 14,060 15,992 30,052

18,729$ 10,265$ 28,994$ 20,917 15,144 36,061

11,758$ 15,246$ 27,003$ 14,266 14,649 28,915

16,427$ 15,246$ 31,673$ 17,690 14,649 32,339

19,275$ 13,392$ 32,667$ 20,237 14,008 34,245

(in millions)

Earnings:

Interest Income Loans

Interest Income Investments

Interest Expense

Net Interest Income

Non-Interest Income

Total Net Revenue

Financial Data:

Quarter:

Net Credit Losses

Quarter End:

Total Loans

Total AssetsQuarter Average:

Total Loans

Earning Assets

Total Assets

34

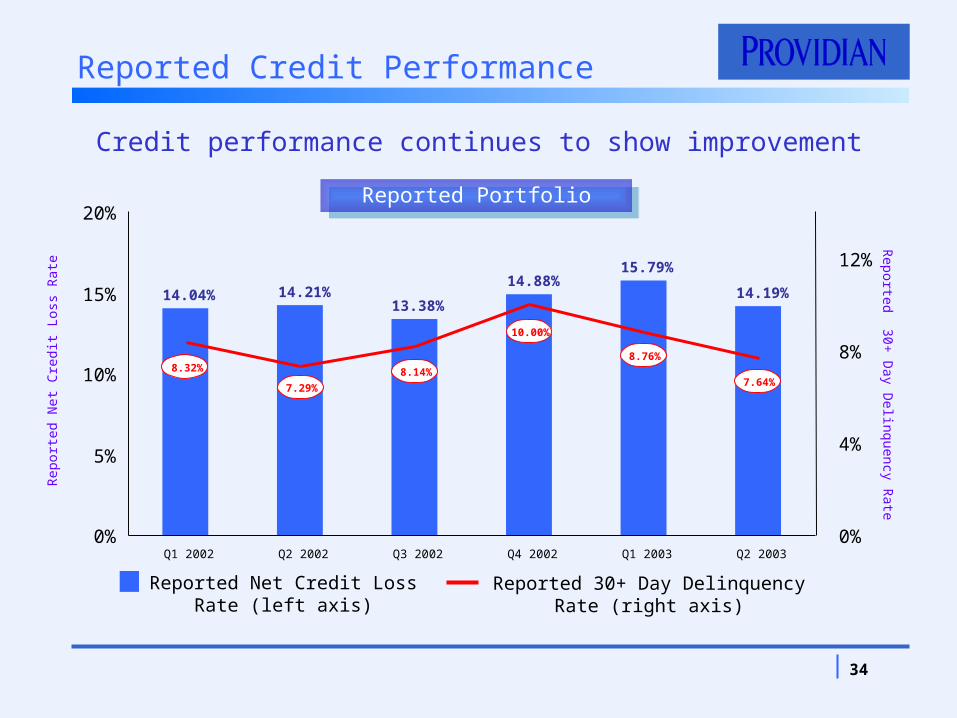

Reported Credit Performance

Reported 30+ Day Delinquency Rate (right axis)

Reported Net Credit Loss Rate (left axis)

Reported 30+

Day D

elinquency Rate

Rep

orte

d N

et C

redi

t Los

s R

ate

14.04% 14.21%13.38%

14.88%15.79%

14.19%

0%

5%

10%

15%

20%

Q1 2002 Q2 2002 Q3 2002 Q4 2002 Q1 2003 Q2 20030%

4%

8%

12%

8.32%

7.29%

8.14%

10.00%

8.76%

7.64%

Credit performance continues to show improvement

Reported PortfolioReported Portfolio