Embed Size (px)

Citation preview

ODIN Sverige C

Årskommentar december 2018

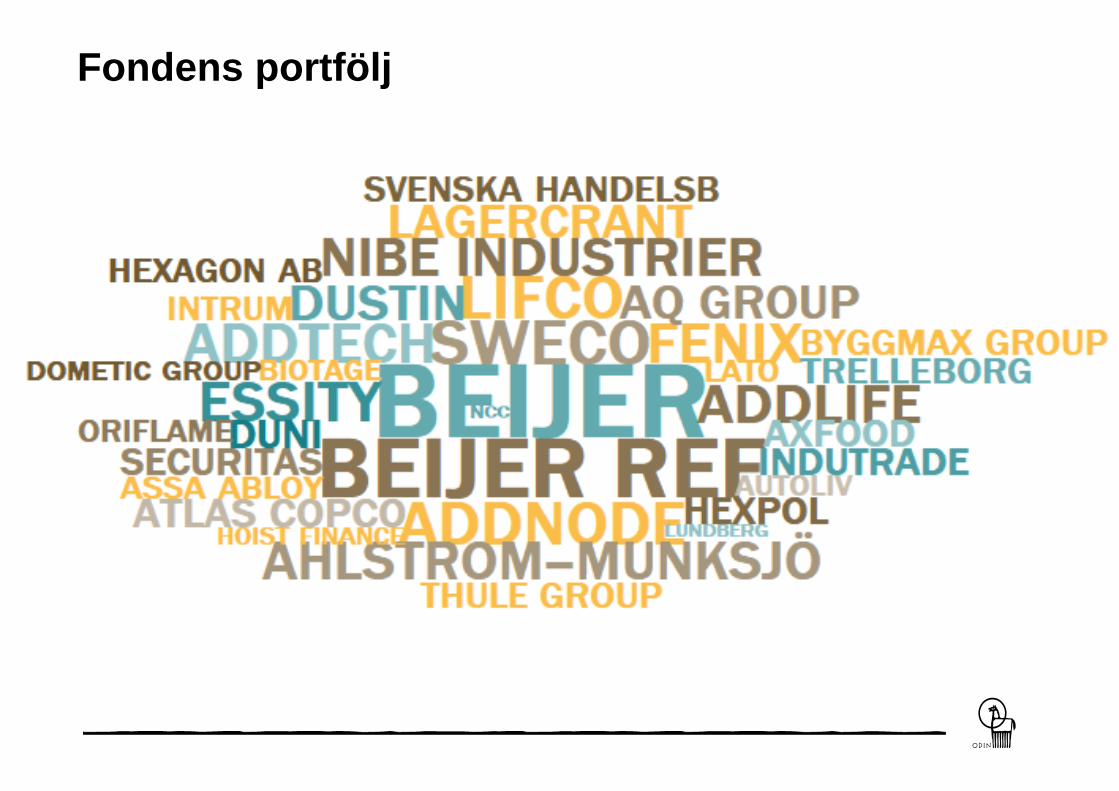

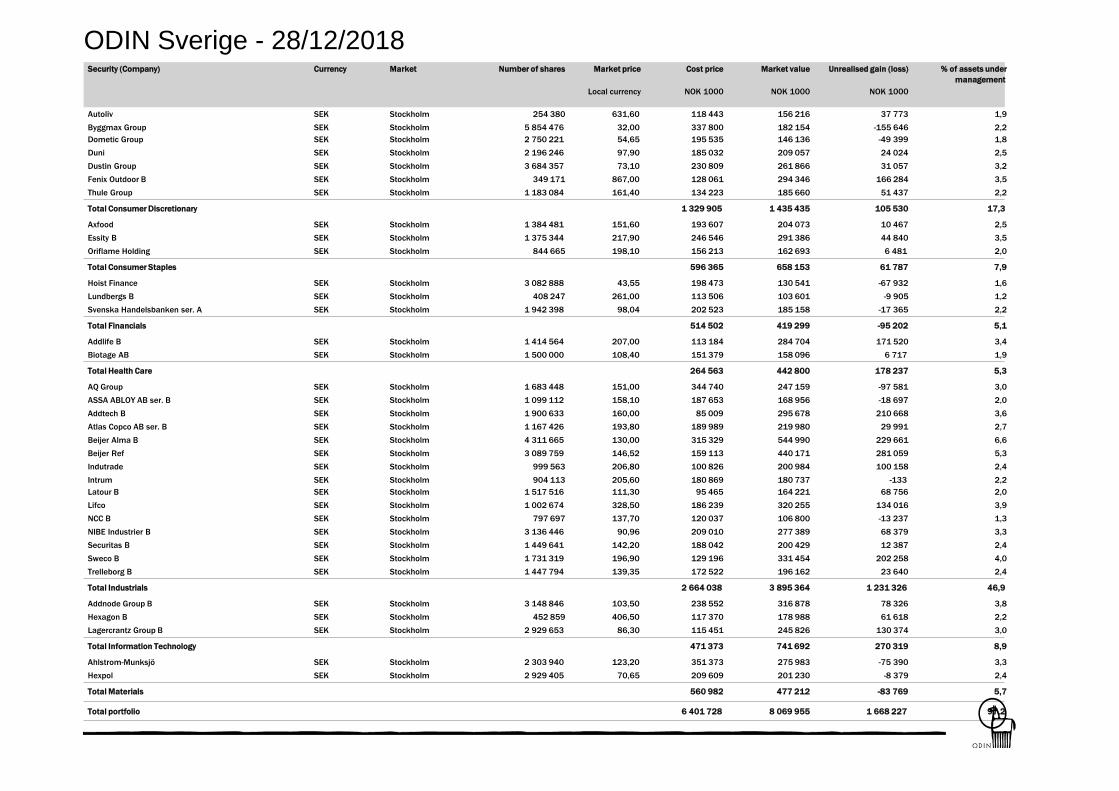

Fondens portfölj

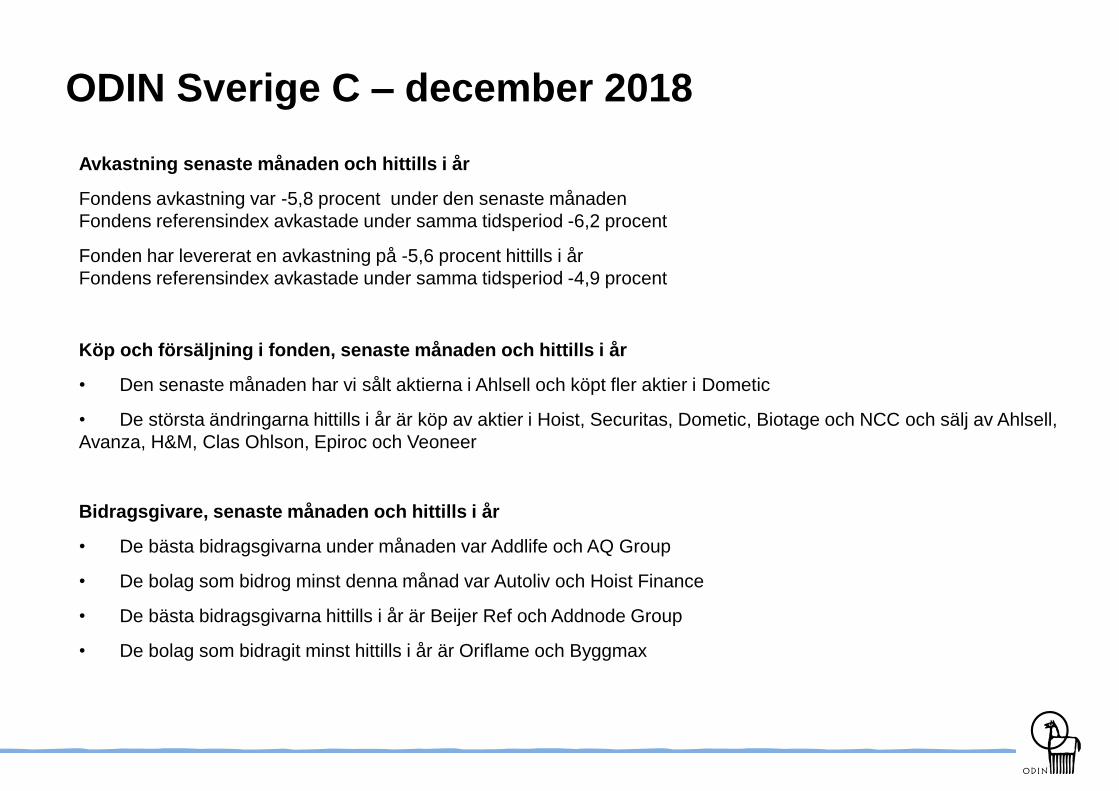

ODIN Sverige C – december 2018

Avkastning senaste månaden och hittills i år

Fondens avkastning var -5,8 procent under den senaste månaden

Fondens referensindex avkastade under samma tidsperiod -6,2 procent

Fonden har levererat en avkastning på -5,6 procent hittills i år

Fondens referensindex avkastade under samma tidsperiod -4,9 procent

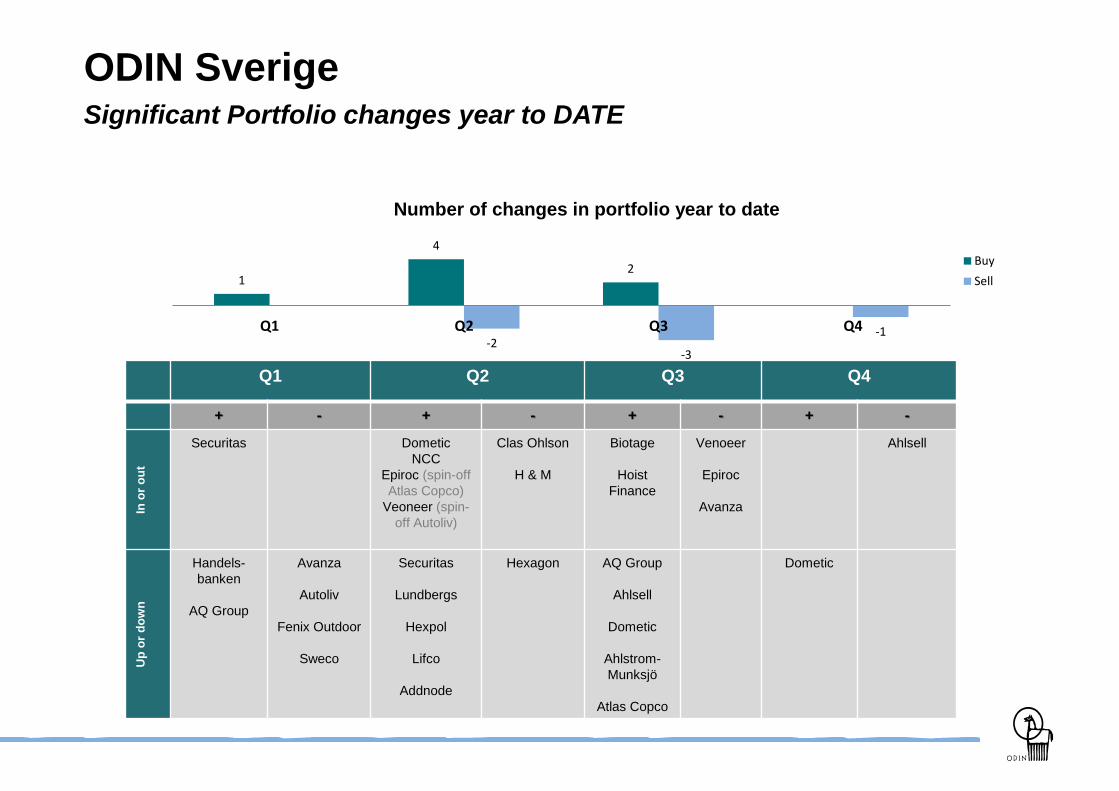

Köp och försäljning i fonden, senaste månaden och hittills i år

• Den senaste månaden har vi sålt aktierna i Ahlsell och köpt fler aktier i Dometic

• De största ändringarna hittills i år är köp av aktier i Hoist, Securitas, Dometic, Biotage och NCC och sälj av Ahlsell,

Avanza, H&M, Clas Ohlson, Epiroc och Veoneer

Bidragsgivare, senaste månaden och hittills i år

• De bästa bidragsgivarna under månaden var Addlife och AQ Group

• De bolag som bidrog minst denna månad var Autoliv och Hoist Finance

• De bästa bidragsgivarna hittills i år är Beijer Ref och Addnode Group

• De bolag som bidragit minst hittills i år är Oriflame och Byggmax

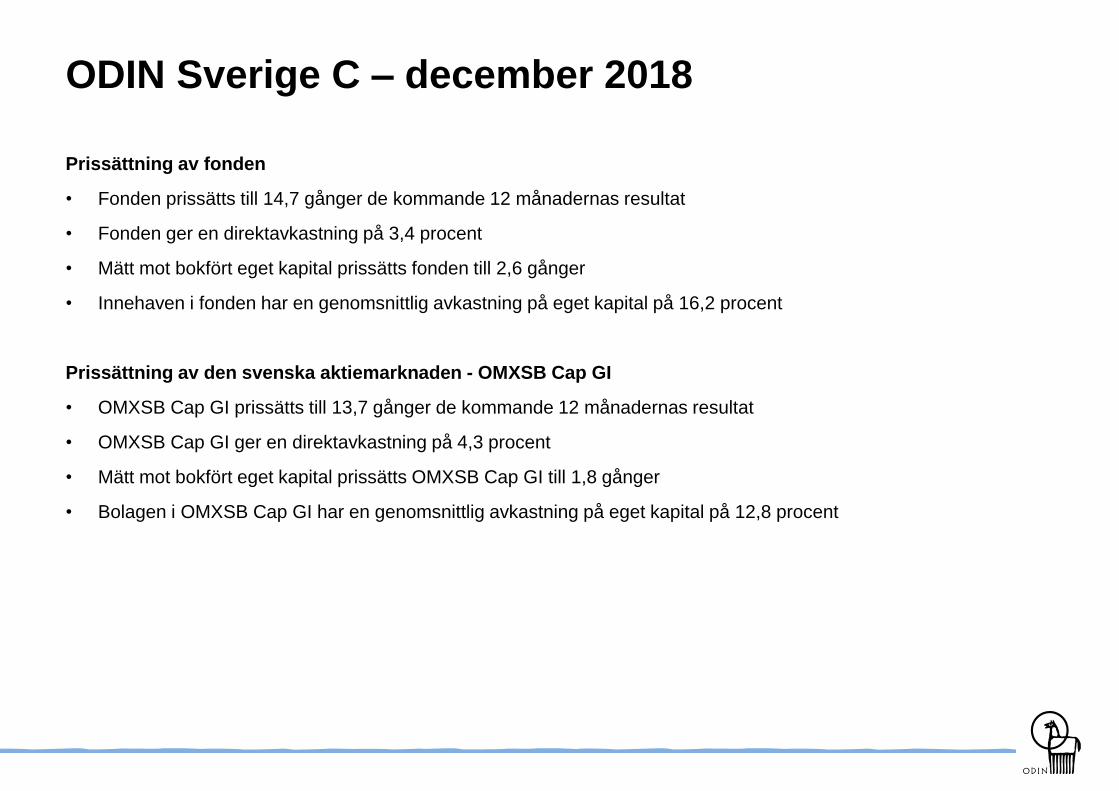

ODIN Sverige C – december 2018

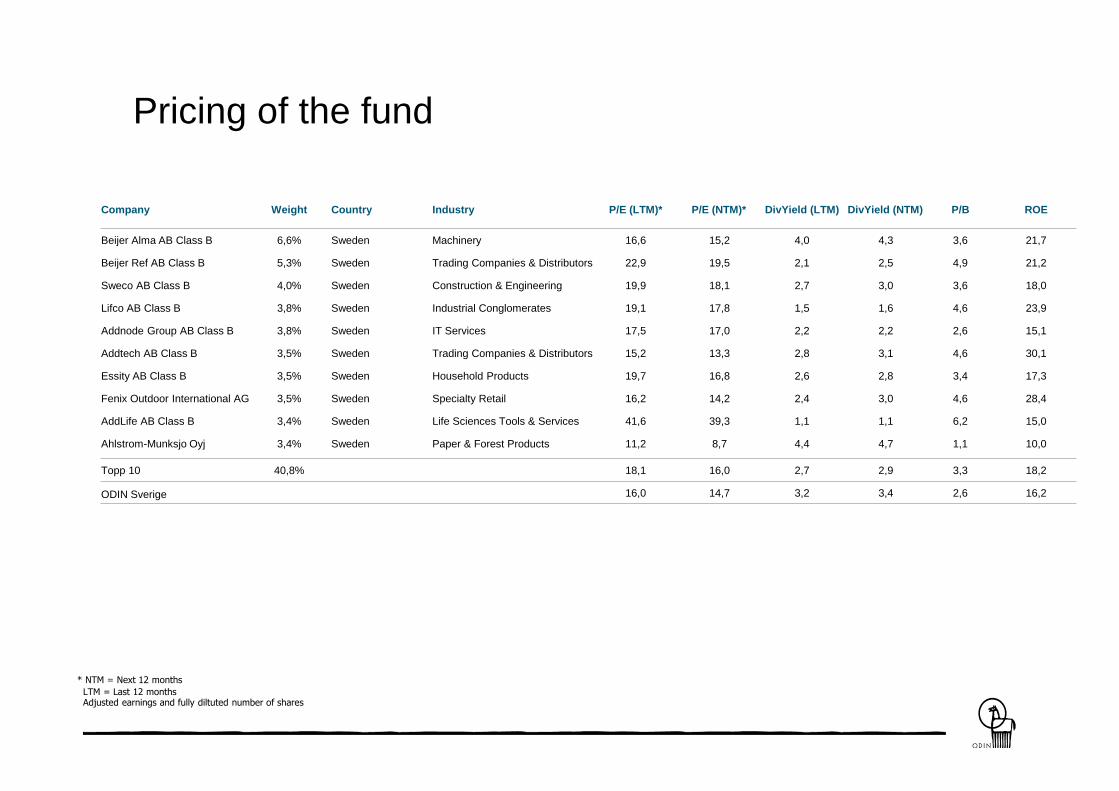

Prissättning av fonden

• Fonden prissätts till 14,7 gånger de kommande 12 månadernas resultat

• Fonden ger en direktavkastning på 3,4 procent

• Mätt mot bokfört eget kapital prissätts fonden till 2,6 gånger

• Innehaven i fonden har en genomsnittlig avkastning på eget kapital på 16,2 procent

Prissättning av den svenska aktiemarknaden - OMXSB Cap GI

• OMXSB Cap GI prissätts till 13,7 gånger de kommande 12 månadernas resultat

• OMXSB Cap GI ger en direktavkastning på 4,3 procent

• Mätt mot bokfört eget kapital prissätts OMXSB Cap GI till 1,8 gånger

• Bolagen i OMXSB Cap GI har en genomsnittlig avkastning på eget kapital på 12,8 procent

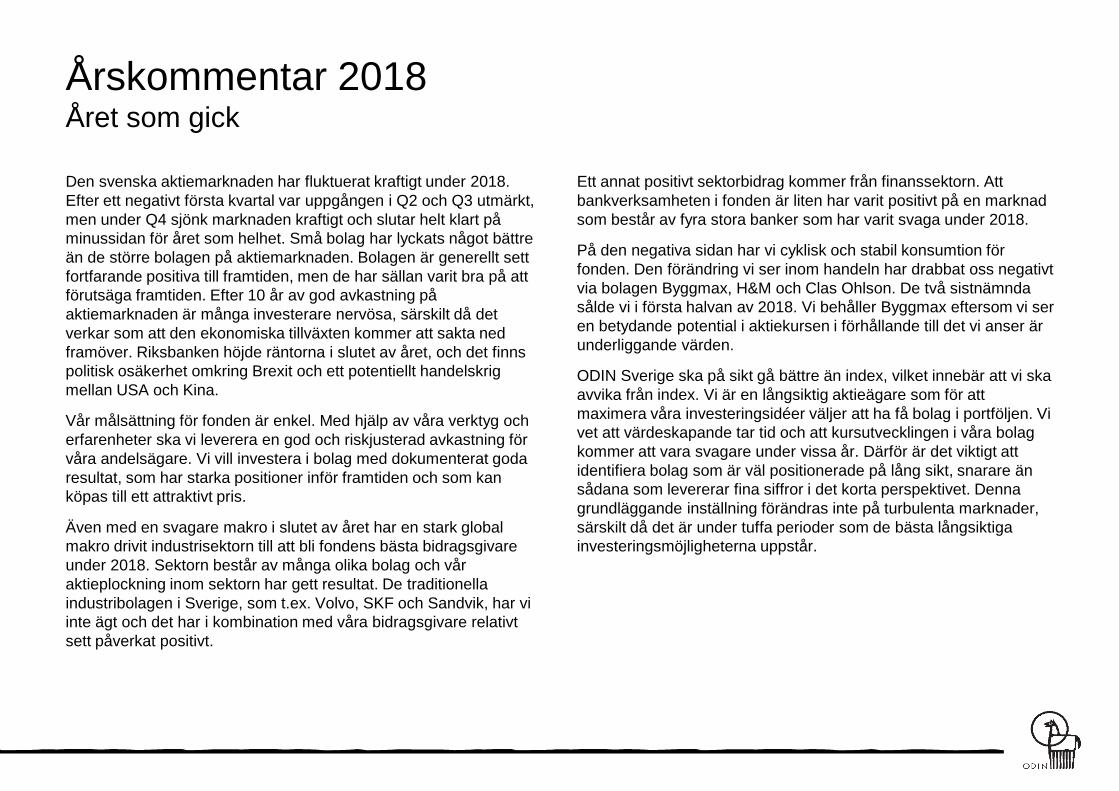

Årskommentar 2018Året som gick

Ett annat positivt sektorbidrag kommer från finanssektorn. Att

bankverksamheten i fonden är liten har varit positivt på en marknad

som består av fyra stora banker som har varit svaga under 2018.

På den negativa sidan har vi cyklisk och stabil konsumtion för

fonden. Den förändring vi ser inom handeln har drabbat oss negativt

via bolagen Byggmax, H&M och Clas Ohlson. De två sistnämnda

sålde vi i första halvan av 2018. Vi behåller Byggmax eftersom vi ser

en betydande potential i aktiekursen i förhållande till det vi anser är

underliggande värden.

ODIN Sverige ska på sikt gå bättre än index, vilket innebär att vi ska

avvika från index. Vi är en långsiktig aktieägare som för att

maximera våra investeringsidéer väljer att ha få bolag i portföljen. Vi

vet att värdeskapande tar tid och att kursutvecklingen i våra bolag

kommer att vara svagare under vissa år. Därför är det viktigt att

identifiera bolag som är väl positionerade på lång sikt, snarare än

sådana som levererar fina siffror i det korta perspektivet. Denna

grundläggande inställning förändras inte på turbulenta marknader,

särskilt då det är under tuffa perioder som de bästa långsiktiga

investeringsmöjligheterna uppstår.

Den svenska aktiemarknaden har fluktuerat kraftigt under 2018.

Efter ett negativt första kvartal var uppgången i Q2 och Q3 utmärkt,

men under Q4 sjönk marknaden kraftigt och slutar helt klart på

minussidan för året som helhet. Små bolag har lyckats något bättre

än de större bolagen på aktiemarknaden. Bolagen är generellt sett

fortfarande positiva till framtiden, men de har sällan varit bra på att

förutsäga framtiden. Efter 10 år av god avkastning på

aktiemarknaden är många investerare nervösa, särskilt då det

verkar som att den ekonomiska tillväxten kommer att sakta ned

framöver. Riksbanken höjde räntorna i slutet av året, och det finns

politisk osäkerhet omkring Brexit och ett potentiellt handelskrig

mellan USA och Kina.

Vår målsättning för fonden är enkel. Med hjälp av våra verktyg och

erfarenheter ska vi leverera en god och riskjusterad avkastning för

våra andelsägare. Vi vill investera i bolag med dokumenterat goda

resultat, som har starka positioner inför framtiden och som kan

köpas till ett attraktivt pris.

Även med en svagare makro i slutet av året har en stark global

makro drivit industrisektorn till att bli fondens bästa bidragsgivare

under 2018. Sektorn består av många olika bolag och vår

aktieplockning inom sektorn har gett resultat. De traditionella

industribolagen i Sverige, som t.ex. Volvo, SKF och Sandvik, har vi

inte ägt och det har i kombination med våra bidragsgivare relativt

sett påverkat positivt.

Årskommentar 2018 Fundamental utveckling

Det vi fokuserar på när vi utvärderar året som gått är den

fundamentala utvecklingen för de bolag som ingår i fonden. Bolagen

i ODIN Sverige förväntas kunna uppvisa en resultatökning på cirka

12 procent i SEK under 2018. Jämförelsevis förväntas vårt

referensindex (OMXSBENC) leverera en resultatökning på 8

procent.

Försäljningsökningen för bolagen i ODIN Sverige uppgår till drygt 6

procent. Beijer Ref, Dometic, Biotage och Addtech var bland de

bolag i Sverige-portföljen som hade högst försäljningstillväxt.

Den bästa resultatutvecklingen i fonden stod Addnode, Autoliv,

Beijer Ref och Lifco för, medan NCC*, Byggmax, Essity och

Ahlstrom-Munksjö gick sämst. Sex av våra 36 bolag uppvisade en

negativ resultatutveckling mellan 2017 och 2018.

Avkastningen på eget kapital beräknas till 16,5 procent för bolagen i

fonden. En direktavkastning på 3,2 procent från utdelningar är vi

nöjda med.

Om vi tittar på resultatprognosen för kommande år ligger den för

den svenska marknaden (SBXCAP) på 5 procent och for ODIN

Sverige på 13 procent.

* NCC endast ägd delar av året

Avkastningen på aktiemarknaden är svår att förutspå, åtminstone på

kort sikt. Det vi vet är att totalavkastningen på lång sikt består av

bolagets fundamentala utveckling (resultatökning + utdelning) och

prisförändring (multipelförändring).

I ODIN Sverige förväntas resultatökningen hamna på drygt 13

procent. En direktavkastning på omkring 3 procent pekar på en

möjlig totalavkastning på drygt 16 procent före eventuella

prisändringar på våra bolag i fonden.

Årskommentar 2018Förändringar i portföljen

sin vinst under de kommande åren genom organisk tillväxt och

förvärv. Dessutom tror vi att det finns utrymme för ytterligare

marginalförbättringar tack vare industrialiseringen av bolaget samt

kostnadssynergier från förvärvet av Seastar. Vi ser fram emot att

följa bolaget och menar att värdet ligger betydligt högre än dagens

kursnivå.

Vi köpte in oss i entreprenörsbolaget NCC, som utvecklades svagt

såväl verksamhets- som kursmässigt under 2017 och 2018. I maj

tillträdde den nya vd:n Tomas Carlsson. Han var tidigare vd för

konsultbolaget Sweco (2012-2018) där han lyckades mycket väl.

Dessförinnan arbetade han i över 20 år på NCC och har med andra

ord en mycket relevant bakgrund och kompetensbas. Vi tror att

Carlsson och resten av ledningen kommer att klara att vända den

svaga utvecklingen vi har sett på NCC och lyfta rörelsemarginalerna

mot forna höjder. Aktiemarknaden ser inte ut att väga ta in detta i

dagsläget. Vi anser därför att detta är en attraktiv investeringschans

för de som har tillräckligt med is i magen att behålla aktien under en

omställningsperiod.

Biotage är ett globalt bolag som utvecklar innovativa och effektiva

lösningar för separation inom organisk och analytisk kemi samt för

industriella tillämpningar. Vi gillar bolagets nuvarande

marknadsposition och ser stora tillväxtmöjligheter i nya segment och

branscher som miljö och livsmedelssäkerhet. Med en stark

topplinjetillväxt och marginalexpansion tror vi att beståndet har mer

att gå på i framtiden.

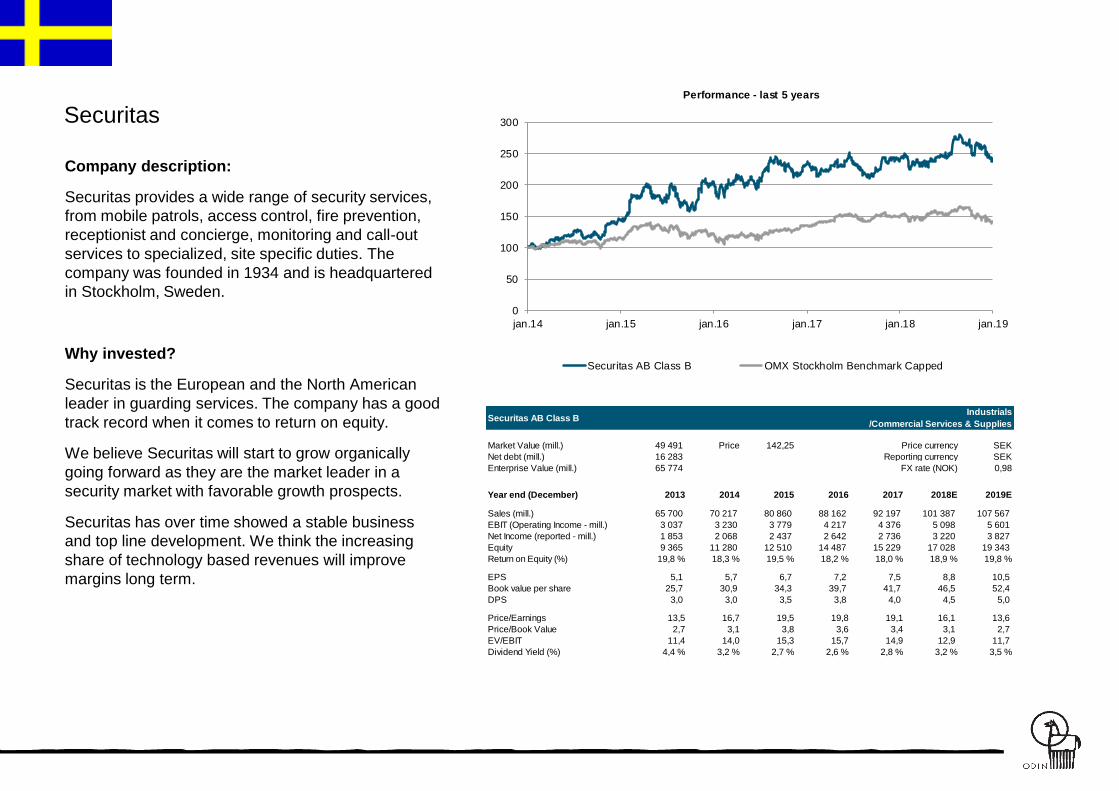

Under 2018 tog vi in fem nya bolag i portföljen. Vi köpte Securitas,

Dometic och NCC under första halvåret och två nya bolag under

andra halvåret – Biotage och Hoist Finance. Två av våra bolag har

under året knoppat av en del av sina respektive verksamheter. Här

valde vi att inte behålla de avknoppade bolagen Epiroc och

Veoneer. Utöver denna försäljning sålde vi ut oss ur Clas Ohlson

och H&M under årets första hälft. Under andra halvåret sålde vi oss

ut ur Avanza.

Vi lyfte in Securitas i ODIN Sverige i slutet av mars. Vi har följt

bolaget länge och betraktar aktiekursnivån kombinerat med

stabiliteten i verksamheten som attraktiv. ODIN Norden har länge

ägt aktier i Securitas. Genom ökat teknikinnehåll och försäljning av

säkerhetslösningar kommer bolaget att bli mer lönsamt framöver. I

kombination med en relativt stabil efterfrågan, långsiktigt behov av

ökad säkerhet och en attraktiv prislapp på aktien har vi valt att

bygga upp en position även för ODIN Sverige.

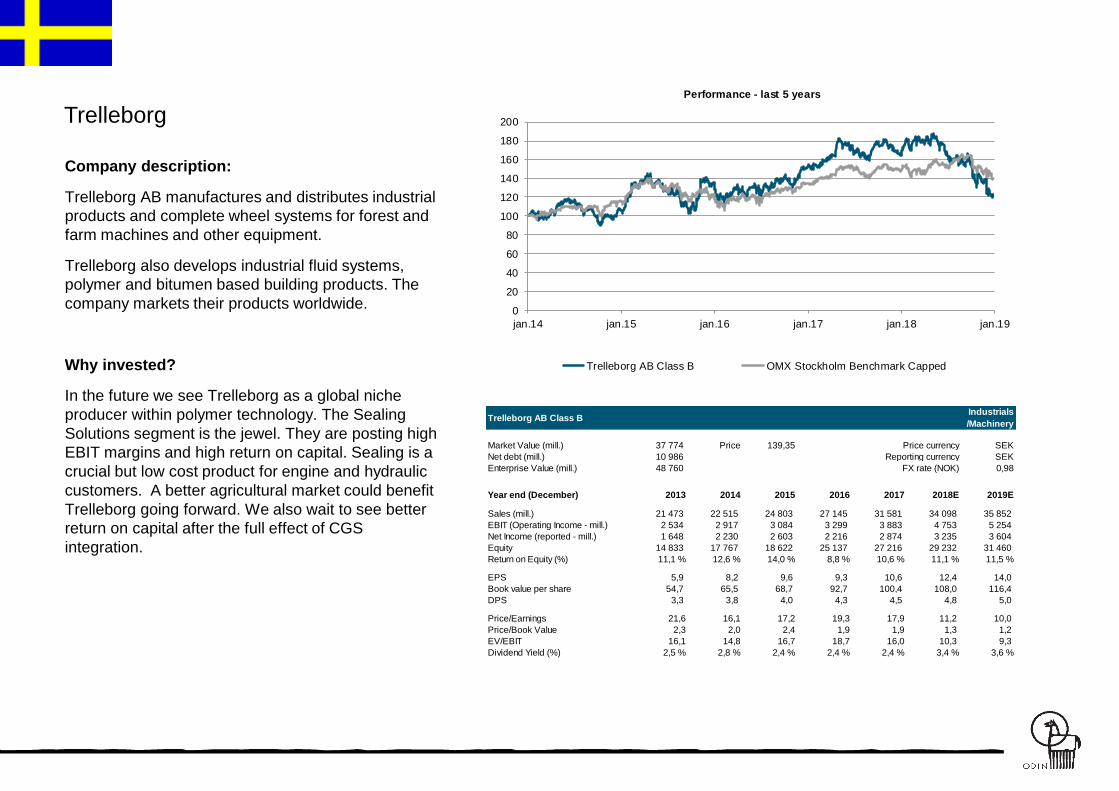

Svenska Dometic producerar bland annat klimatanläggningar,

kylsystem, sanitetssystem, belysning och andra komfortprodukter

för primärt husbilar, fritidsbåtar, kommersiella marina fartyg och

varubilar/lastbilar. De är globala marknadsledare som ligger på

första eller andra plats i 75 procent av sina verksamhetsområden

och tillverkar premiumprodukter. Detta förklarar bolagets höga

bruttomarginaler jämfört med konkurrenterna. I januari fick bolaget

en ny vd i Juan Vargues. Han imponerade på oss under tiden i Assa

Abloy (2006-2017) där han bidrog starkt till bolagets tillväxt genom

en rad förvärv. Dometic har en stark position på attraktiva

tillväxtmarknader och vi tror att bolaget kommer att fortsätta att öka

Årskommentar 2018Förändringar i portföljen

Ut ur portföljen 2018

Förutom två avknoppningar har vi sålt fyra bolag; HM, Clas Ohlson,

Avanza och Ahlsell.

H&M har varit en problematisk investering för oss under en längre

tid. Det har varit kärvt i detaljhandeln på senare år, även under

2018. Hela branschen förändras snabbt och det har skett mycket

snabbare och med mycket större kraft än vad både vi och de flesta

etablerade aktörer hade föreställt sig. Frågan är hur långt

utvecklingen kommer att gå. Kommer försäljningen via nätet att stå

för 20, 30 eller 70 procent av all handel inom fem år?

Vi sitter inte inne med svaret men att tillväxten i hög grad kommer

att ske på nätet råder det föga tvivel om. De aktörer som vi ska äga

framöver måste därför kunna hävda sig på nätet. Vi är som regel

inte den typen av investerare som säljer bolag så snart det blåser

upp. När vi väl har valt våra 25–35 kvalitetsbolag ökar vi normalt

innehavet i dem när aktiekurserna faller. I maj bestämde vi oss ändå

för att sälja av vårt innehav i bolaget och utnyttjade den tillfälliga

kursuppgång som kom efter huvudägarens aktieköp till att sälja. Det

var ett svårt beslut, mentalt sett, då vi gärna går mot strömmen när

kvalitetsbolag faller. Fokus i vår investeringsfilosofi ligger på historik,

framtid och pris, men i fallet med H&M var nog vårt misstag att vi

inte i tid insåg hur snabbt, och med vilken kraft, förutsättningarna i

detaljhandeln skulle komma att förändras.

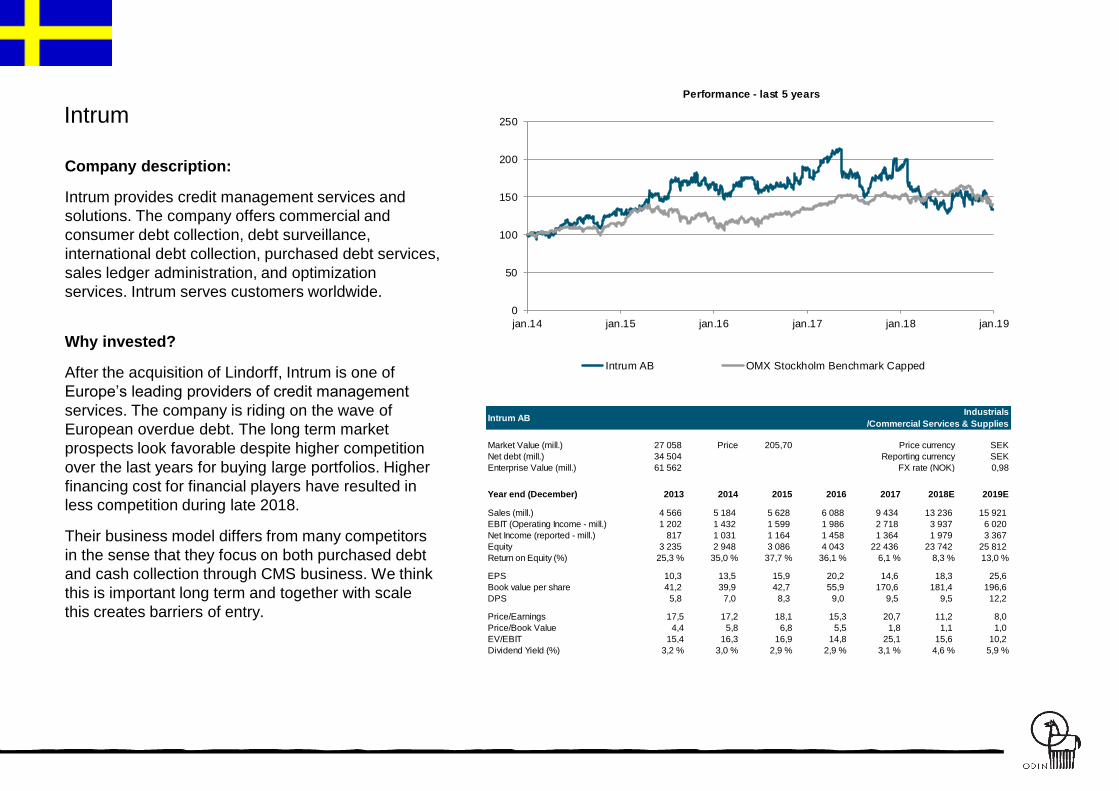

Hoist Finance är också en av våra nyare investeringar. Vi köpte i

september in oss i en emission i bolaget. Vi ser tydliga tecken på att

prispressen kring portföljköp är på väg att mattas av. Detta beror på

att finansieringskostnaderna har stigit och att de renodlade

finansiella aktörerna inte är lika aktiva. Hoist Finance är en aktör i

branschen med egen banklicens. Tack vare sin insättningsprodukt

har bolaget lägre finansieringskostnader. Detta betraktar vi som en

konkurrensfördel. Dessutom har den nye vd:n (tidigare vd på

Lindorff) satt ihop ett starkt team som ska bli effektivare på det

operativa planet.

ÅrskommentarFörändringar i portföljen

Avknoppningar

Precis före sommaren delade både Autoliv och Atlas Copco upp

sina respektive verksamheter i två börsnoterade bolag.

Autoliv lade ut den del av verksamheten som arbetar med aktiv

säkerhet i ett nytt bolag. Aktiv säkerhet är produkter som ska

förhindra en olycka, och bolaget fick namnet Veoneer. Den del av

verksamheten som arbetar med passiv säkerhet, dvs. utrustning

som ska minska konsekvenserna av en redan inträffad olycka, ligger

kvar i moderbolaget som behåller namnet Autoliv. Det slutade med

att vi sålde ut Veoneer ur fonden i augusti. Vad som händer på

marknaden kring aktiv säkerhet är mycket spännande. Den stora

osäkerheten är vilken position bolaget kommer att sluta med. Utan

en god historia, resultat och med brist på underlag för att utvärdera

framtiden, ansåg vi detta bortom vår investeringsfilosofi, med alltför

många osäkerhetsfaktorer. Vi behöll Autoliv.

Atlas Copco valde å sin sida att förlägga den del av verksamheten

som är exponerad mot gruvindustrin i bolaget Epiroc. Här slutade

det också med att vi sålde våra aktier i Epiroc för mer aktier i Atlas

Copco.

I slutet av året fick vi en god nyhet. CVC, som har varit långsiktig

ägare av Ahlsell och fortfarande ägde 25 procent av bolaget efter

börsnoteringen för två år sedan, valde att lägga bud på hela

bolaget. Priset var 33 procent högre än aktuell börskurs och 25

procent över IPO, justerat för erhållen utdelning. Ahlsell var därför

en bra investering för aktieägarna. För att kunna utnyttja andra

köpmöjligheter i korrigeringen valde vi att sälja våra aktier på

marknaden istället för att vänta på den färdiga uppgörelsen i slutet

av februari.

När det gäller beslutet om Clas Ohlson så har detta varit en

investering för oss i 2,5 år. Vi köpte in oss i bolaget när vi trodde att

man lärt sig av misstaget med expansionen i Storbritannien. Detta

var under den tid som bolaget leddes av vd Klas Balkow. De var då

ute på en expansionsresa med Tyskland som nästa anhalt. Med en

filosofi inriktad på historik, framtid och pris så anser vi att det största

felet med vår investering i Clas Ohlson är att bolaget säljer 3,5

procent av sina varor på nätet. Trots ny vd och ny strategi är vi inte

imponerade och det är en del av orsaken till att vi har valt att sälja

av denna position, som utgjorde 1,7 procent av fonden.

Avanza är ett välskött bolag med exponering mot sparande – ett

segment som upplever strukturell tillväxt. Avanza har en stark

nischposition och tack vare sin kapitallätta affärsmodell tror vi att

bolaget har en god position för framtiden. Stark aktiekursutveckling

och höga priser i kombination med att den underliggande

resultattillväxt har varit en besvikelse, har dock fått oss att sälja av

vårt innehav i bolaget. Även om vi gillar bolaget och kulturen finns

det en del orosmoln i och med att fondbranschen i allt högre grad

övergår till att sälja nettoklasser direkt till kunderna. Vi är osäkra på

vilken effekt detta kommer att få på Avanza.

Årskommentar 2018Vad gick bra?

Som nämnts har Avanza varit en bra investering för aktieägarna i ODIN

Sverige, men efter stark kursutveckling har vi sålt oss ut ur bolaget

under andra halvåret.

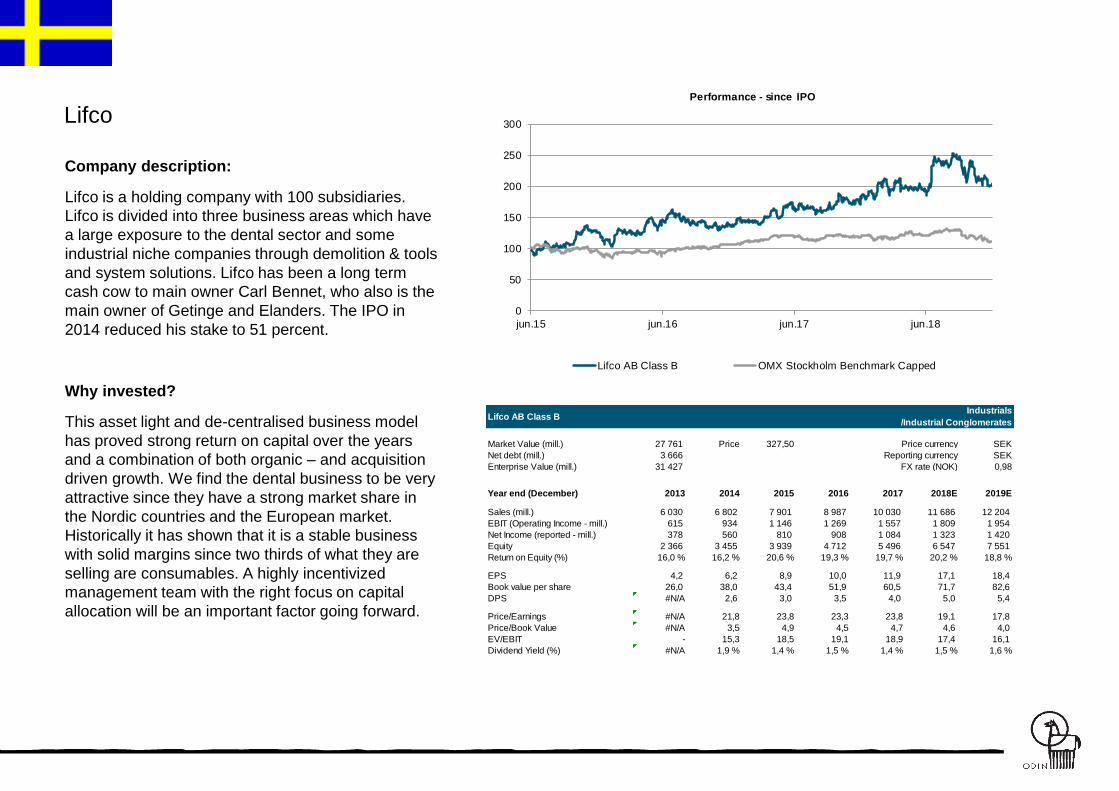

Förvärvsmaskinen Lifco fortsätter att leverera. Försäljningsintäkterna

och resultatet per aktie fortsätter att öka stadigt. Bolaget rapporterar i år

om goda utsikter i sina dotterbolag och växer stadigt genom nya,

stimulerande förvärv. Bolaget har också en stark balans med kapacitet

för ytterligare förvärv framöver.

2016 knoppades AddLife av från ett annat bolag i portföljen: Addtech.

Bolaget utvecklar och köper lönsamma och marknadsledande

nischbolag inom området medicinsk teknik. Merparten av kunderna

finns inom hälso- och sjukvården i Norden, men AddLife växer också

globalt. Med en förvärvsfokuserad och decentraliserad struktur

säkerställer de en stark entreprenörsanda i sina oberoende dotterbolag,

och det är en typ av bolagsstruktur och affärsmodell som vi i ODIN

uppskattar. 2018 har varit ett bra år för AddLife, med god

topplinjetillväxt och annonsering om nya förvärv. Allt tyder på att

AddLife kommer att fortsätta den starka utvecklingen under de

kommande åren. I november stöttade vi bolaget när de genomförde en

emission som finansierar ytterligare förvärv av en större verksamhet i

Österrike.

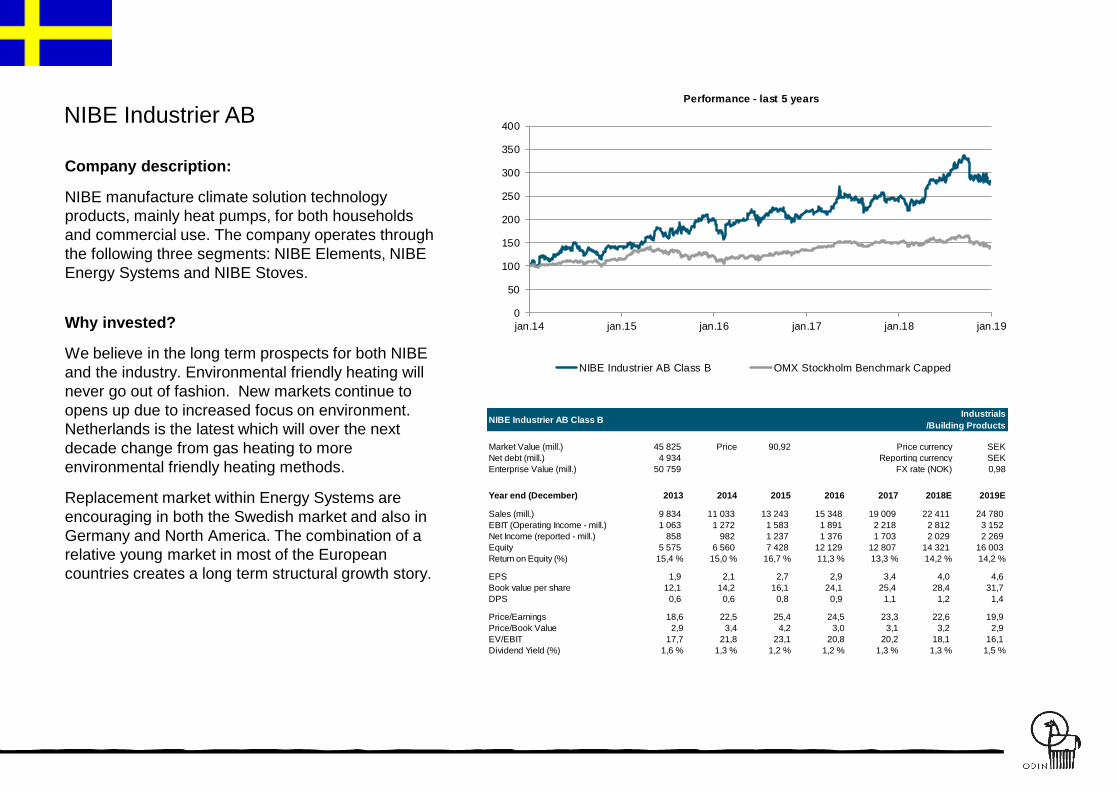

NIBE är ett annat svenskt bolag som har levererat mycket bra i år.

Bolaget erbjuder energibesparande lösningar för både hushåll och

industri, vilket bidrar till energieffektiva bostäder och byggnader. Nibe är

ett typiskt kvalitetsbolag som passar in i vår investeringsfilosofi. De har

en distinkt affärsidé och fokuserar på kvalitet och bra lösningar. De kan

hänvisa till en god historia och en stark bolagskultur. Vi tror fortfarande

att Nibe har många spännande år framför sig.

Efter ett turbulent aktieår är de positiva bidragsgivarna få, men det finns

några som har presterat mycket bra i 2018 trots fallande börser. Som

exempel kan Beijer Ref, Addnode, Avanza Bank, Lifco, AddLife och

NIBE nämnas.

Beijer Ref verkar på en stark marknad och fortsätter att rida på den

lagstadgade utfasningen av kylmedel i kylanläggningar. Detta beror på

att innan 2030 måste alla livsmedelsbutiker och restauranger ersätta sin

kylutrustning för att uppfylla nya EU-krav på utsläpp av farlig gas. I

Sverige har endast tio procent gjort denna investering hittills. Bolaget

driver sin verksamhet globalt och expanderar stadigt, senast med stora

förvärv i Australien och Asien. Ökade krav på miljövänliga lösningar och

en global exponering bidrar till att öka efterfrågan på Beijer Ref och

deras produkter under de kommande åren. Med gynnsamma

marknadsförutsättningar som bakgrund är bolagets starka resultat

under det senaste året inte någon överraskning.

Addnode är en ledande leverantör av programvara och andra IT-

tjänster som hjälper till med att digitalisera samhället. Deras

kärnverksamhet ligger inom design, konstruktion och produktdata. De är

också en ledande aktör inom dokument- och ledningssystem, där de

tillhandahåller tjänster och lösningar till den offentliga sektorn i Sverige

och Norge. Bolaget har vuxit med totalt 15 procent årligen sedan 2013,

både genom organisk tillväxt och förvärv av kompletterande

verksamheter. I år har de kvartalsvisa siffrorna varit bättre än väntat,

något som har premierats av marknaden med en stigande aktiekurs. Vi

tror att bolaget är väl positionerat för att fortsätta växa under många år

framöver och är positivt inställda till bolagets exponering och

positionering inom den starka digitaliseringstrenden inom både privat

och offentlig sektor. I somras genomförde Addnode en riktad

nyemission som kommer att bidra till att finansiera ytterligare tillväxt

genom förvärv, vilket vi är positiva till. Vi deltog därför i emissionen.

Årskommentar 2018 Vad gick mindre bra?

Förra året köpte vi in oss i Ahlstrom-Munksjö, en global ledare

inom fiberbaserade material. Bolaget har grundläggande

egenskaper som vi värdesätter, bland annat att man är

marknadsledande i nischer som skyddas av starka kundrelationer

via kontinuerlig produktutveckling. Högre priser för massa och

titandioxid har lett till ett fortsatt marginaltryck som har belastat

aktien under hela året. Vi ser tecken på att marginalpressen ger sig

nu, samtidigt som bolaget har meddelat att man vidtar åtgärder för

att vända de olönsamma delarna av verksamheten. Vi tror att

bolaget har kontroll över situationen och kommer att komma tillbaka

starkt, då också med hjälp av synergier från de två stora förvärven

av Expera (USA) och Caieiras (Brasilien) som slutfördes i oktober i

år.

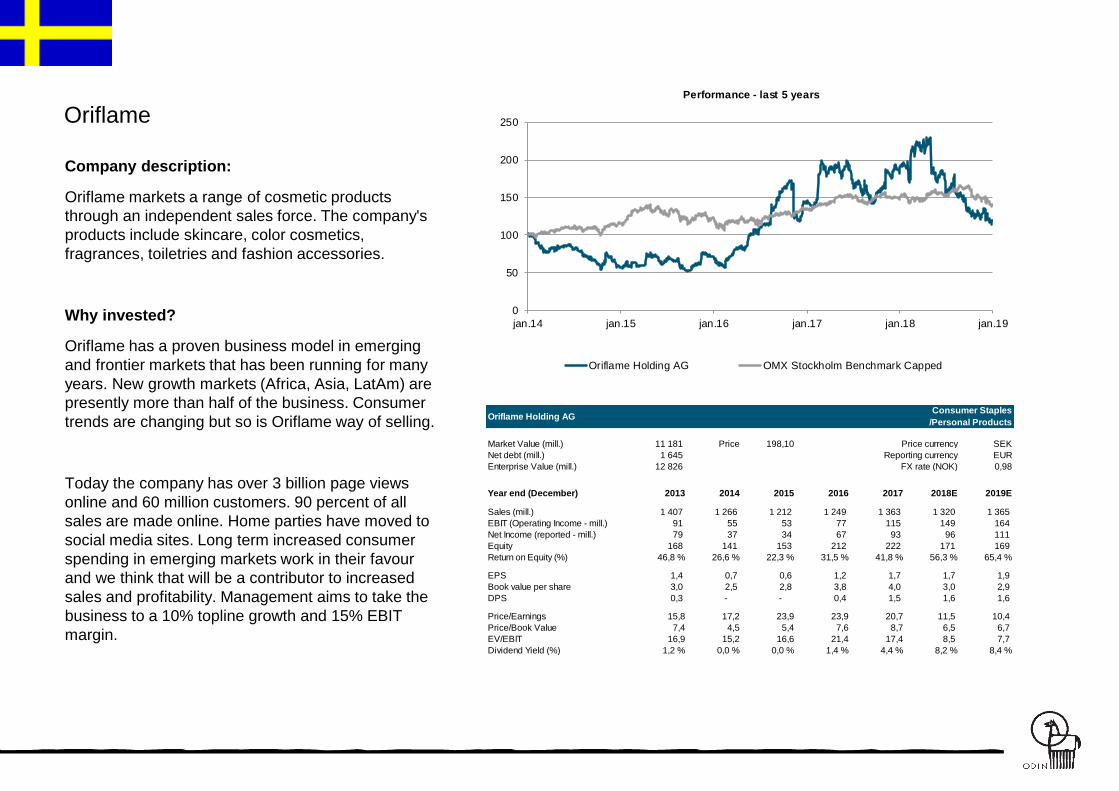

Efter en stark inledning på året har Oriflames aktiekurs varit under

stark press sedan i början av maj. Resultaten från första halvåret

var svagare än väntat och drevs av prishöjningar till kunderna, vilket

gav negativ effekt på efterfrågan. Vi tror att rädslan för att Oriflame

kommer att få se svag topplinjetillväxt och negativ

marginalutveckling under de kommande åren är överdriven. Vi tittar

nu på de låga förväntningar som ligger bakom dagens aktiekurs.

De svagaste bidragsgivarna i 2018 var Byggmax, AQ Group,

Ahlstrom-Munksjö och Oriflame.

Byggmax har en stark marknadsposition, men vinsten dämpas av

att Skånska Byggvaror genomgår en omstrukturering.

Vändningsarbetet har fortsatt under 2018, vilket har hållit tillbaka

gruppen något. Efter sommaren redovisade Byggmax både svagare

försäljning och marginaler på grund av den varma väderleken i

sommar och högre priser på virke. Det är positivt att

förändringsprocessen i Skånska Byggvaror ser ut att börja få effekt.

Bolagets utmaningar är redan inbakade i priset på aktien och vi är

övertygade om att ledningen kommer att få bolaget på banan igen.

2018 har varit ett utmanande år för AQ Group. Bolaget har

rapporterat om fortsatt stark organisk försäljningstillväxt, men tyvärr

har rörelsemarginalerna pressats på grund av svagare operationell

verksamhet i vissa dotterbolag samt högre råvarupriser. I egenskap

av långsiktiga investerare är vi dock naturligtvis beredda på att

resultaten svänger på kort- och medellång sikt. Vi anser att en hel

del av de utmaningar som bolaget tampas med är av övergående

art och känner oss trygga med att ledningen ska kunna vända den

negativa marginaltrenden.

Den globala konjunkturen är stark, men makroindikatorer har på

sistone pekat på en svagare utveckling. Norden, som är en

exportinriktad region, är emellertid sällan ensam om att uppleva

recession. Vi ser ingen stor risk för recession så länge räntor och

inflation håller sig på låga nivåer. Svagare makrostatistik och ökad

risk för negativa ekonomiska följder av ett uppseglande handelskrig

har emellertid ökat under det gångna halvåret.

Som vi ser det är de största riskerna knutna till ränteutvecklingen

och stimulanser från centralbanken. 10 år av sjunkande räntor har

fungerat som ett dopingpreparat på ekonomin. Mindre av den varan

utgör en uppenbar risk för tillväxten i världsekonomin. FED:s

trevande räntehöjningar hoppas vi ska verka "lärande" på resten av

världen. Snabba och tvära ändringar av detta mönster utgör en

uppenbar risk framöver.

Som vi har beskrivit tidigare har vi gjort ett antal förändringar i

portföljen under hela året för att förbättra den. ODIN Sverige

förväntas ge en direktavkastning på drygt tre procent i år. Fonden är

prissatt till 14,7 gånger årets resultat, vilket är marginellt högre än

referensindex. När det gäller de bokförda värdena är fondens

prissättning något högre. Detta beror på att fonden har högre

avkastning på sitt kapital.

Årskommentar ODIN SverigeUtsikter för 2019

Fonden består idag av 48 procent små bolag, 32 procent

medelstora bolag och 20 procent stora bolag. Börskorrigeringen har

gjort att några av våra större och medelstora bolag har gått över till

att bli små och medelstora bolag. Vårt minsta bolag i fonden är

Byggmax med ett marknadsvärde på cirka 2 miljarder SEK. Vi har

en all cap-fond som ska ta del av de möjligheter vi hittar där ute,

oavsett om det är små eller stora bolag.

Jämfört med den historiska prissättningen handlar marknaden nu

något över genomsnittet mellan 2007 och idag, något som inte

verkar avskräckande med tanke på rådande låga ränteläge. Som

sagt, vi rör oss mot slutet av en högkonjunktur. Som aktiv

aktieväljare kommer det alltid att finnas möjligheter att hitta bolag

som också kan utvecklas väl i en lågkonjunktur. Därför anser vi att

det blir allt viktigare att vara aktiv i tiden framöver. Det går alltid att

hitta bolag med god kapitalavkastning, lönsam tillväxt och attraktiv

prislapp.

Med förhoppning om ett gott investeringsår 2019!

Nyckeltal och nyheter från

portföljen

- presenterat på engelska

ODIN Sverige C Index

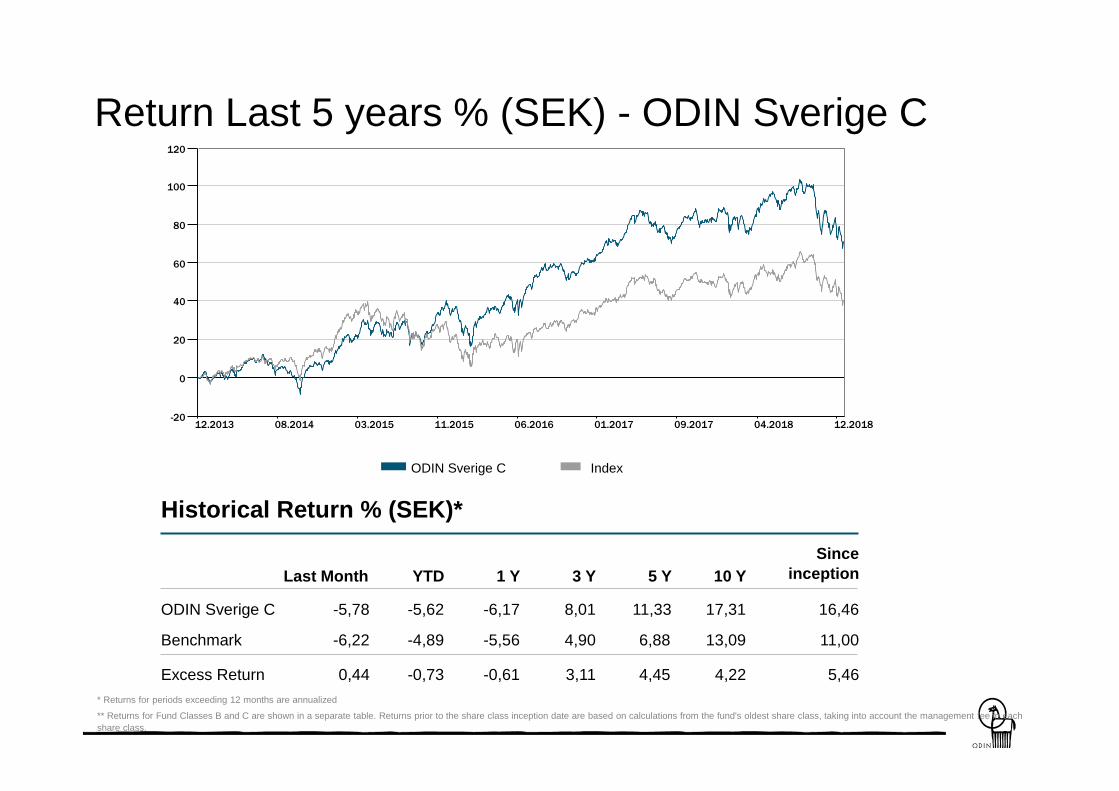

Return Last 5 years % (SEK) - ODIN Sverige C

Historical Return % (SEK)*

* Returns for periods exceeding 12 months are annualized

Last Month YTD 1 Y 3 Y 5 Y 10 Y

Since

inception

ODIN Sverige C

Benchmark

-5,78

-6,22

-5,62

-4,89

-6,17

-5,56

8,01

4,90

11,33

6,88

17,31

13,09

16,46

11,00

Excess Return 0,44 -0,73 -0,61 3,11 4,45 4,22 5,46

** Returns for Fund Classes B and C are shown in a separate table. Returns prior to the share class inception date are based on calculations from the fund's oldest share class, taking into account the management fee in each

share class.

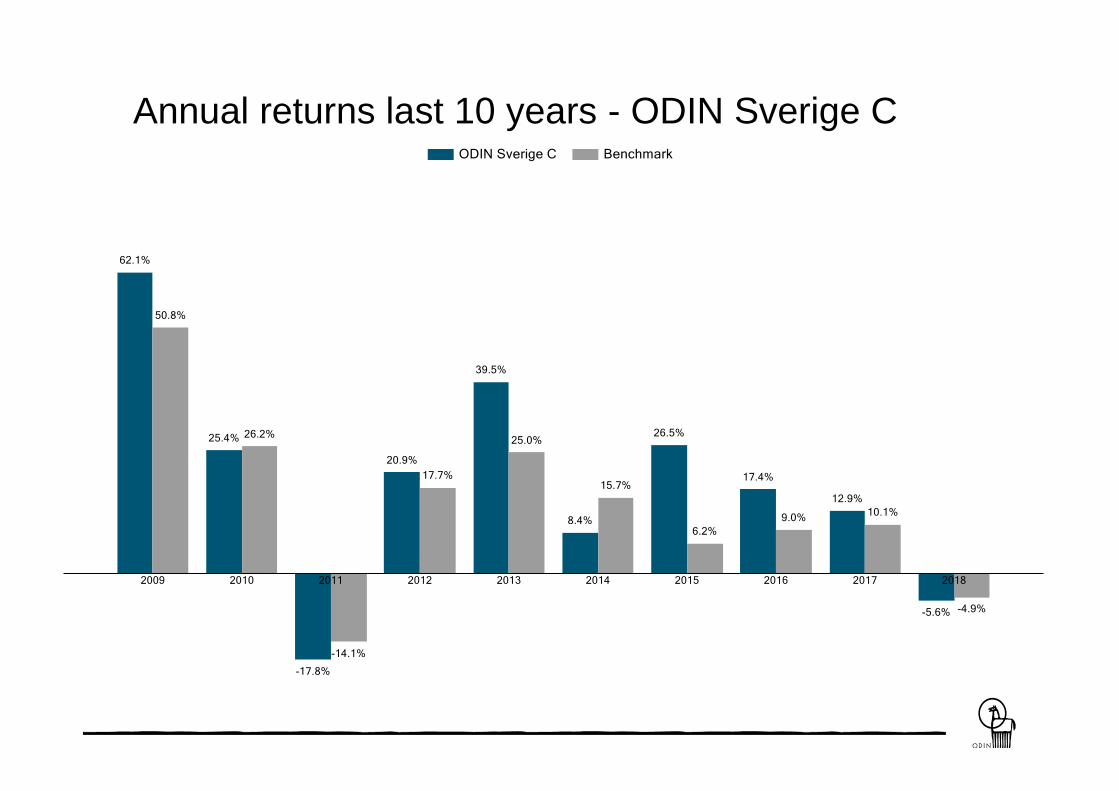

Annual returns last 10 years - ODIN Sverige C

ODIN SverigeSignificant Portfolio changes year to DATE

1

4

2

-2-3

-1Q1 Q2 Q3 Q4

Number of changes in portfolio year to date

Buy

Sell

Q1 Q2 Q3 Q4

+ - + - + - + -

In o

r o

ut

Securitas Dometic

NCC

Epiroc (spin-off

Atlas Copco)

Veoneer (spin-

off Autoliv)

Clas Ohlson

H & M

Biotage

Hoist

Finance

Venoeer

Epiroc

Avanza

Ahlsell

Up

or

do

wn

Handels-

banken

AQ Group

Avanza

Autoliv

Fenix Outdoor

Sweco

Securitas

Lundbergs

Hexpol

Lifco

Addnode

Hexagon AQ Group

Ahlsell

Dometic

Ahlstrom-

Munksjö

Atlas Copco

Dometic

Pricing of the fund

Company Weight Country Industry P/E (LTM)* P/E (NTM)* DivYield (LTM) DivYield (NTM) P/B ROE

Beijer Alma AB Class B 6,6% Sweden Machinery 16,6 15,2 4,0 4,3 3,6 21,7

Beijer Ref AB Class B 5,3% Sweden Trading Companies & Distributors 22,9 19,5 2,1 2,5 4,9 21,2

Sweco AB Class B 4,0% Sweden Construction & Engineering 19,9 18,1 2,7 3,0 3,6 18,0

Lifco AB Class B 3,8% Sweden Industrial Conglomerates 19,1 17,8 1,5 1,6 4,6 23,9

Addnode Group AB Class B 3,8% Sweden IT Services 17,5 17,0 2,2 2,2 2,6 15,1

Addtech AB Class B 3,5% Sweden Trading Companies & Distributors 15,2 13,3 2,8 3,1 4,6 30,1

Essity AB Class B 3,5% Sweden Household Products 19,7 16,8 2,6 2,8 3,4 17,3

Fenix Outdoor International AG 3,5% Sweden Specialty Retail 16,2 14,2 2,4 3,0 4,6 28,4

AddLife AB Class B 3,4% Sweden Life Sciences Tools & Services 41,6 39,3 1,1 1,1 6,2 15,0

Ahlstrom-Munksjo Oyj 3,4% Sweden Paper & Forest Products 11,2 8,7 4,4 4,7 1,1 10,0

Topp 10 40,8% 18,1 16,0 2,7 2,9 3,3 18,2

ODIN Sverige 16,0 14,7 3,2 3,4 2,6 16,2

* NTM = Next 12 months

LTM = Last 12 monthsAdjusted earnings and fully diltuted number of shares

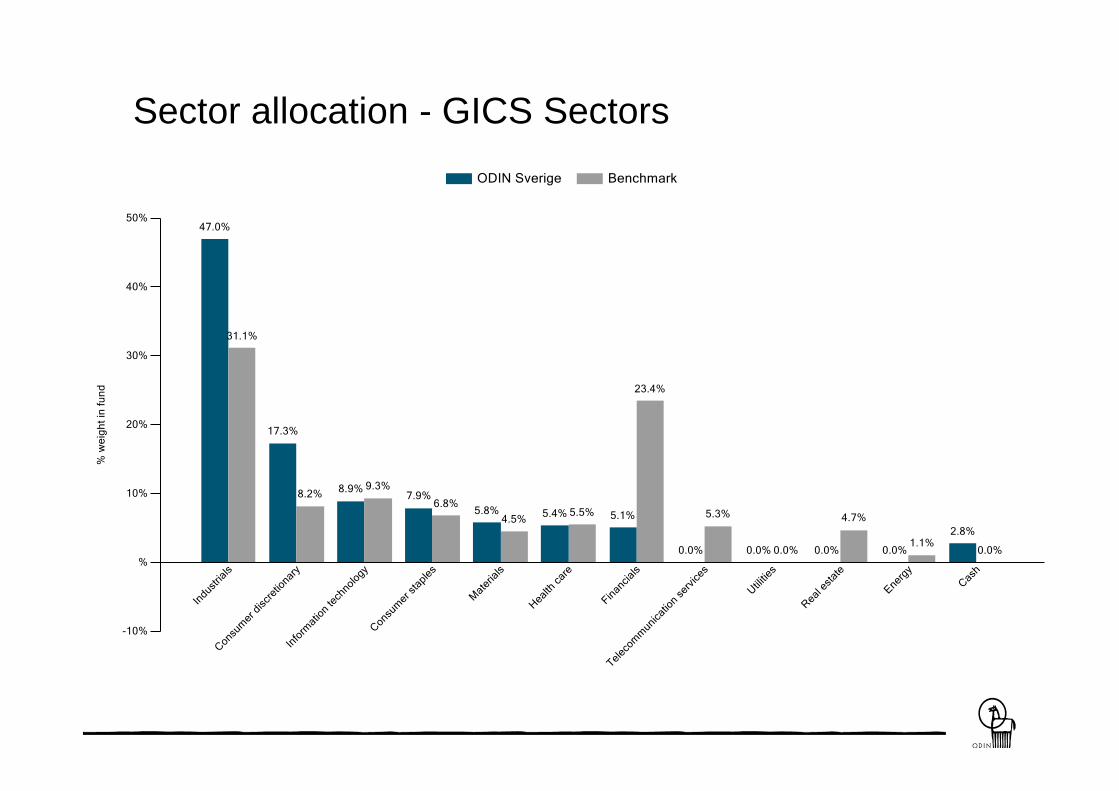

Sector allocation - GICS Sectors

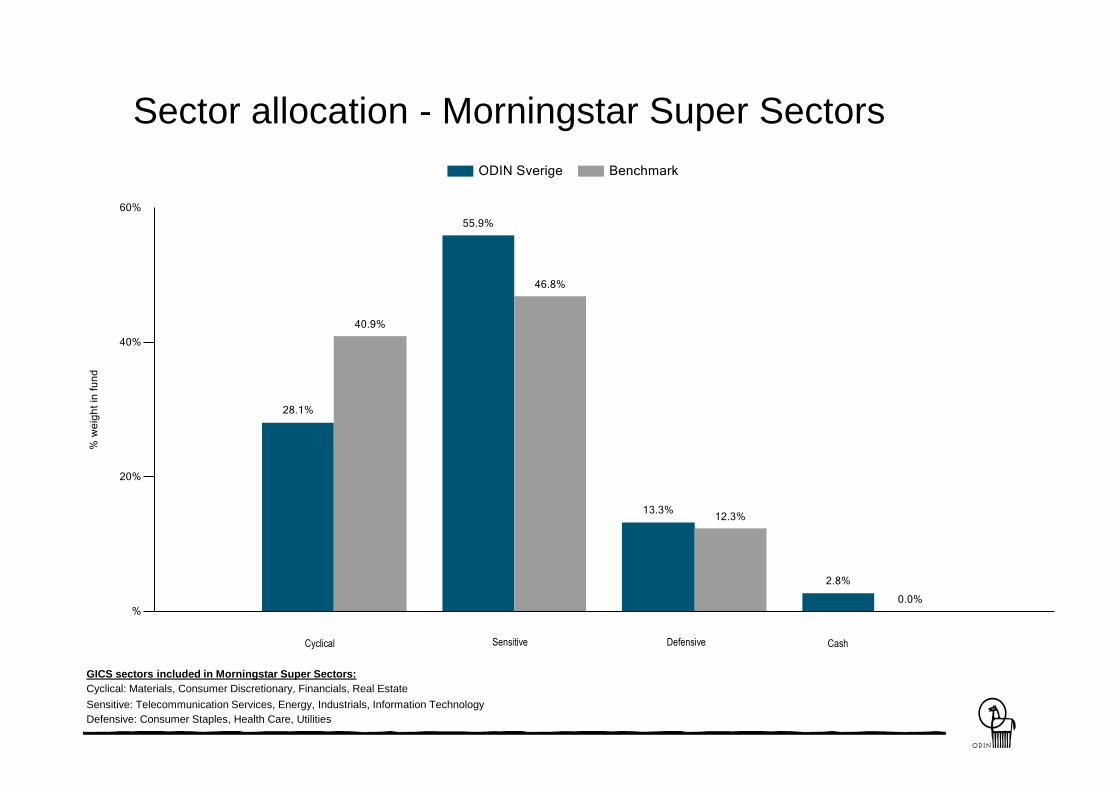

Sector allocation - Morningstar Super Sectors

GICS sectors included in Morningstar Super Sectors:

Cyclical: Materials, Consumer Discretionary, Financials, Real Estate

Sensitive: Telecommunication Services, Energy, Industrials, Information Technology

Defensive: Consumer Staples, Health Care, Utilities

Cyclical Sensitive Defensive Cash

Current holdings

*) Share price performance for equities included in the benchmark. Equities not included in the benchmark are calculated from portfolio figures.

(Sorted by weight in portfolio)

Share price performance*, year to date (SEK)

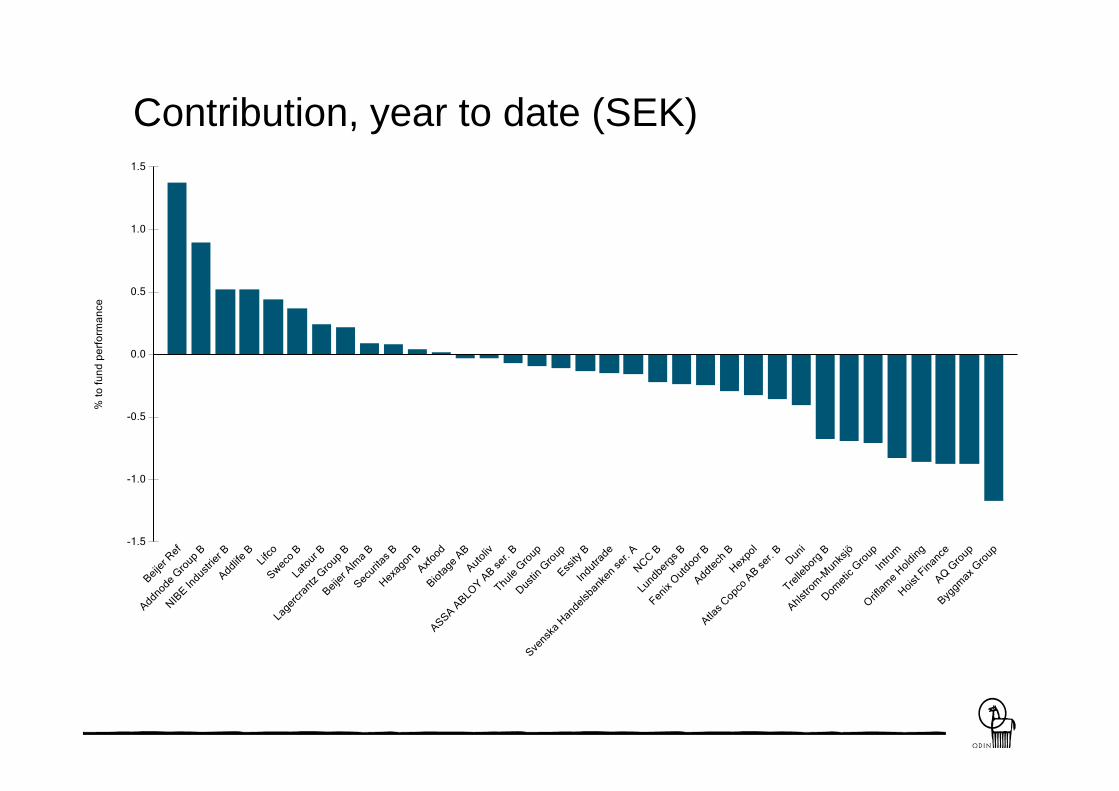

Contribution, year to date (SEK)

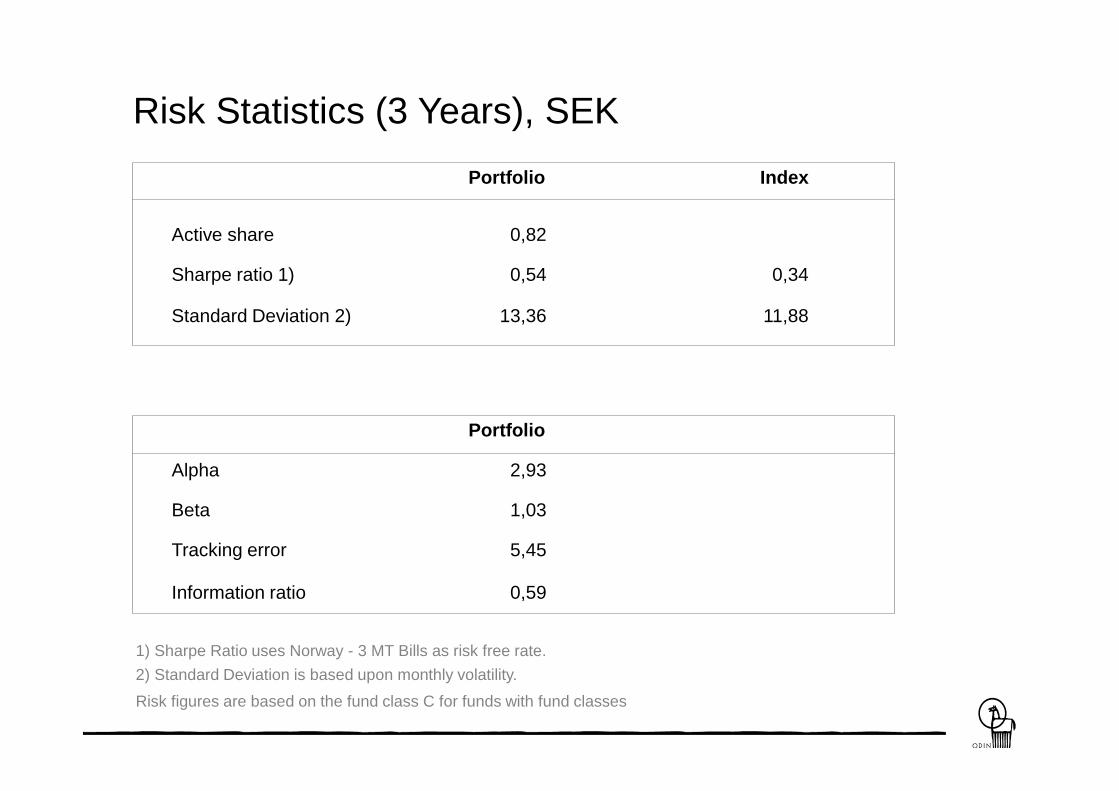

1) Sharpe Ratio uses Norway - 3 MT Bills as risk free rate.

2) Standard Deviation is based upon monthly volatility.

Risk Statistics (3 Years), SEK

Active share 0,82

Sharpe ratio 1) 0,54

Portfolio

Standard Deviation 2) 13,36

Index

0,34

11,88

Portfolio

Alpha 2,93

Beta 1,03

Tracking error 5,45

Information ratio 0,59

Risk figures are based on the fund class C for funds with fund classes

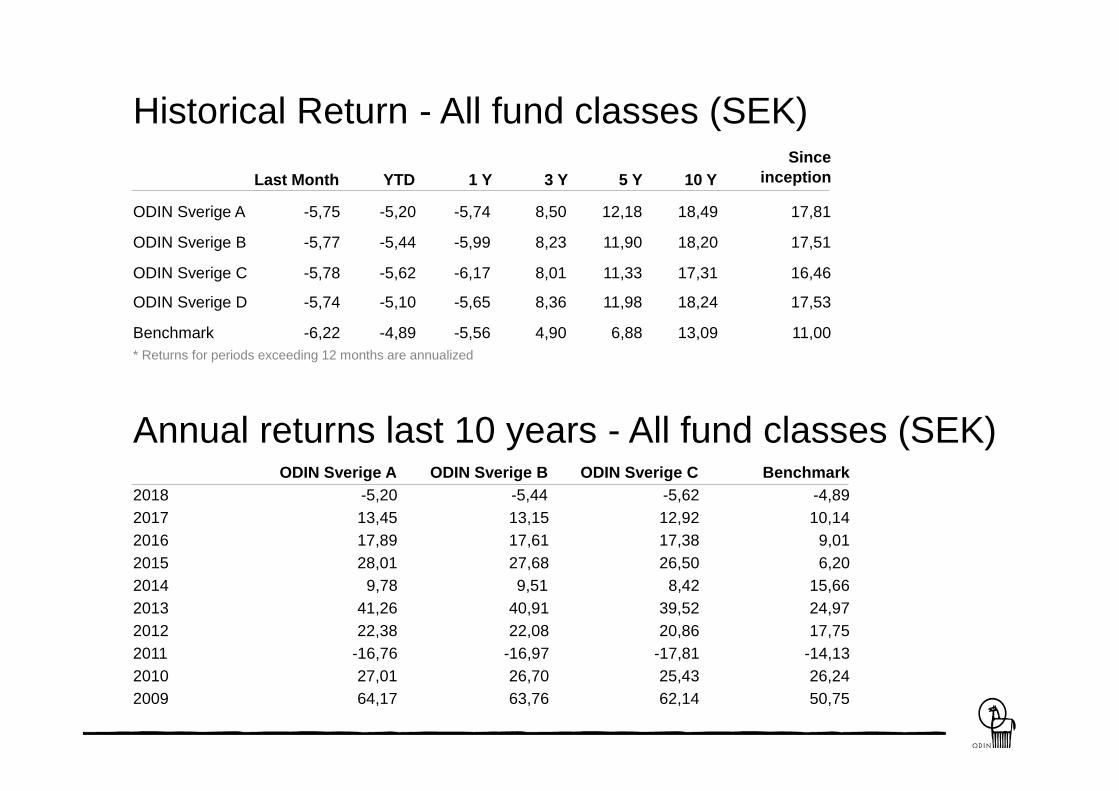

Historical Return - All fund classes (SEK)

Last Month YTD 1 Y 3 Y 5 Y 10 Y

Since

inception

ODIN Sverige A -5,75 -5,20 -5,74 8,50 12,18 18,49 17,81

ODIN Sverige B -5,77 -5,44 -5,99 8,23 11,90 18,20 17,51

ODIN Sverige C -5,78 -5,62 -6,17 8,01 11,33 17,31 16,46

ODIN Sverige D -5,74 -5,10 -5,65 8,36 11,98 18,24 17,53

Benchmark -6,22 -4,89 -5,56 4,90 6,88 13,09 11,00

* Returns for periods exceeding 12 months are annualized

Annual returns last 10 years - All fund classes (SEK)ODIN Sverige A

2018 -5,20

2017 13,45

2016 17,89

2015 28,01

2014 9,78

2013 41,26

2012 22,38

2011 -16,76

2010 27,01

2009 64,17

ODIN Sverige B

-5,44

13,15

17,61

27,68

9,51

40,91

22,08

-16,97

26,70

63,76

ODIN Sverige C

-5,62

12,92

17,38

26,50

8,42

39,52

20,86

-17,81

25,43

62,14

Benchmark

-4,89

10,14

9,01

6,20

15,66

24,97

17,75

-14,13

26,24

50,75

Macro and Market

Pricing - Swedish Equities (OMX Stockholm Benchmark Cap.)

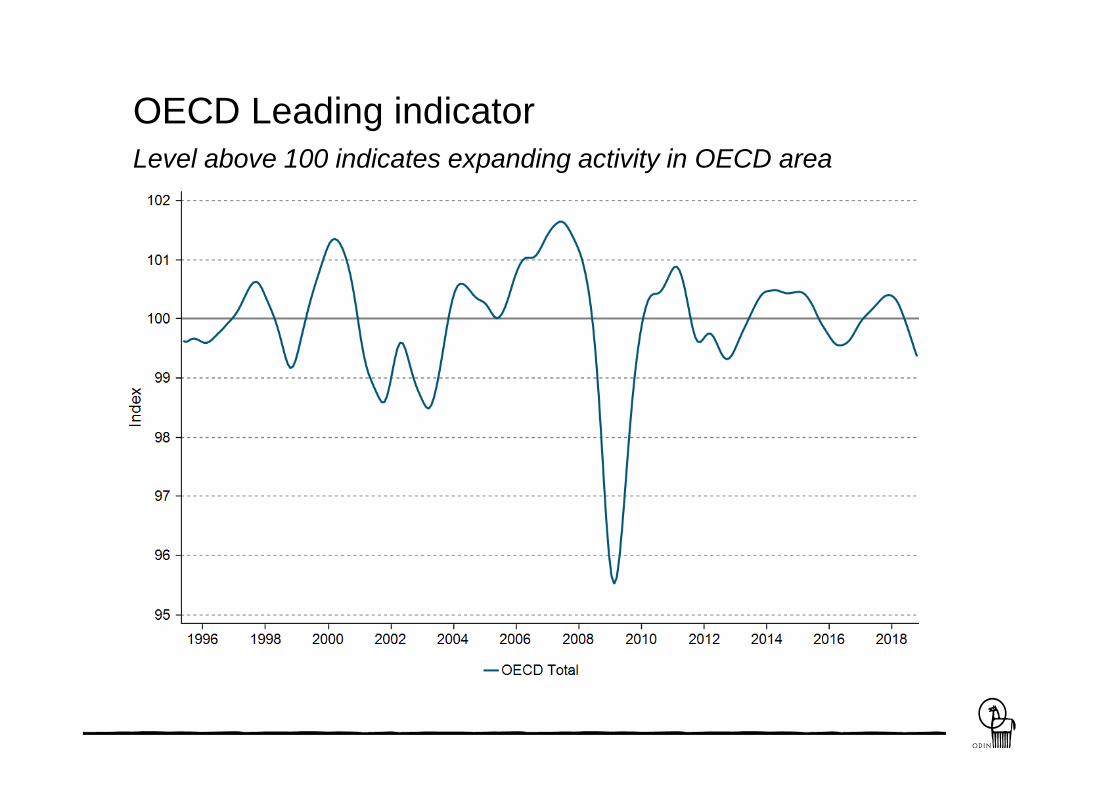

OECD Leading indicator

Level above 100 indicates expanding activity in OECD area

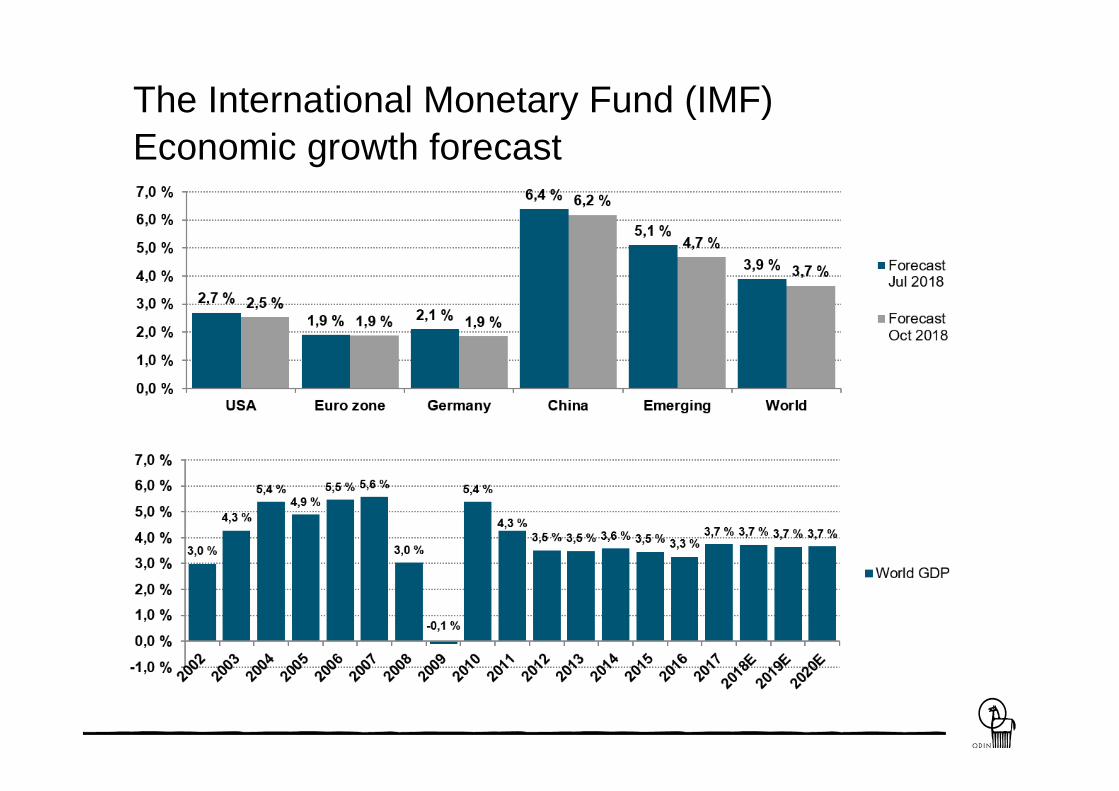

The International Monetary Fund (IMF)

Economic growth forecast

Investments

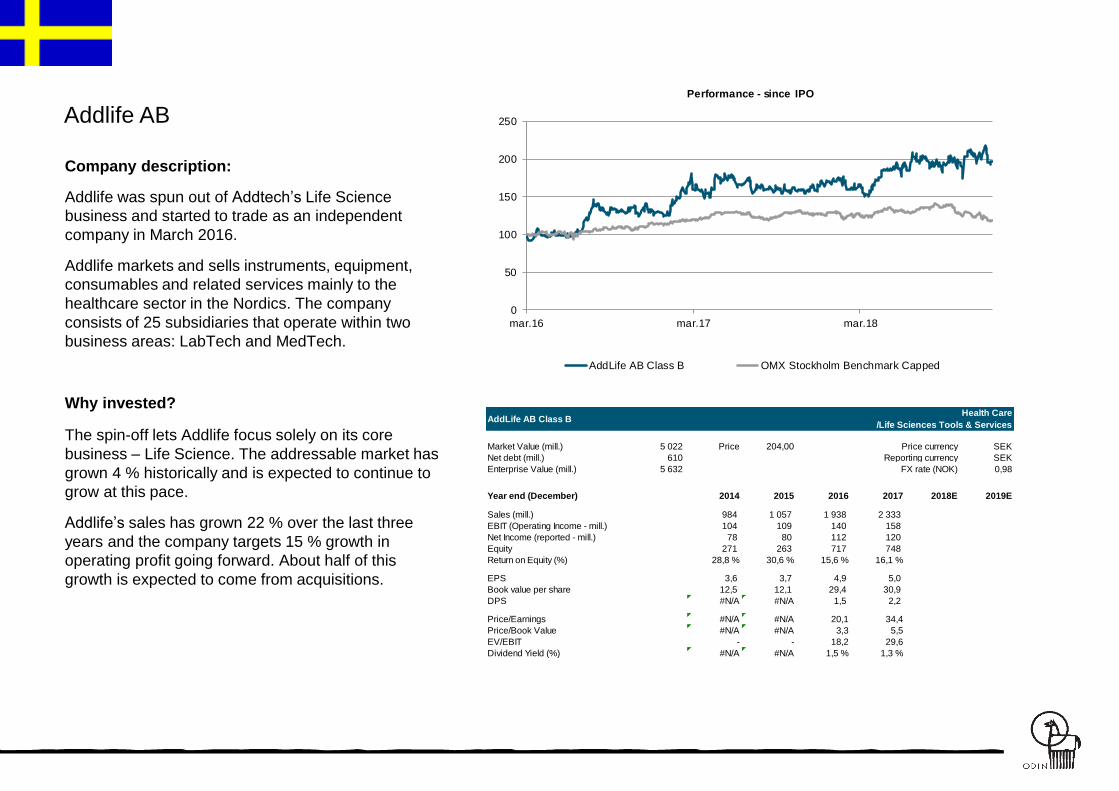

Addlife AB

Company description:

Addlife was spun out of Addtech’s Life Science

business and started to trade as an independent

company in March 2016.

Addlife markets and sells instruments, equipment,

consumables and related services mainly to the

healthcare sector in the Nordics. The company

consists of 25 subsidiaries that operate within two

business areas: LabTech and MedTech.

Why invested?

The spin-off lets Addlife focus solely on its core

business – Life Science. The addressable market has

grown 4 % historically and is expected to continue to

grow at this pace.

Addlife’s sales has grown 22 % over the last three

years and the company targets 15 % growth in

operating profit going forward. About half of this

growth is expected to come from acquisitions.

0

50

100

150

200

250

mar.16 mar.17 mar.18

Performance - since IPO

AddLife AB Class B OMX Stockholm Benchmark Capped

Market Value (mill.) 5 022 Price 204,00 SEK

Net debt (mill.) 610 SEK

Enterprise Value (mill.) 5 632 0,98

Year end (December) 2014 2015 2016 2017 2018E 2019E

Sales (mill.) 984 1 057 1 938 2 333

EBIT (Operating Income - mill.) 104 109 140 158

Net Income (reported - mill.) 78 80 112 120

Equity 271 263 717 748

Return on Equity (%) 28,8 % 30,6 % 15,6 % 16,1 %

EPS 3,6 3,7 4,9 5,0

Book value per share 12,5 12,1 29,4 30,9

DPS #N/A #N/A 1,5 2,2

Price/Earnings #N/A #N/A 20,1 34,4

Price/Book Value #N/A #N/A 3,3 5,5

EV/EBIT - - 18,2 29,6

Dividend Yield (%) #N/A #N/A 1,5 % 1,3 %

AddLife AB Class BHealth Care

/Life Sciences Tools & Services

Price currency

Reporting currency

FX rate (NOK)

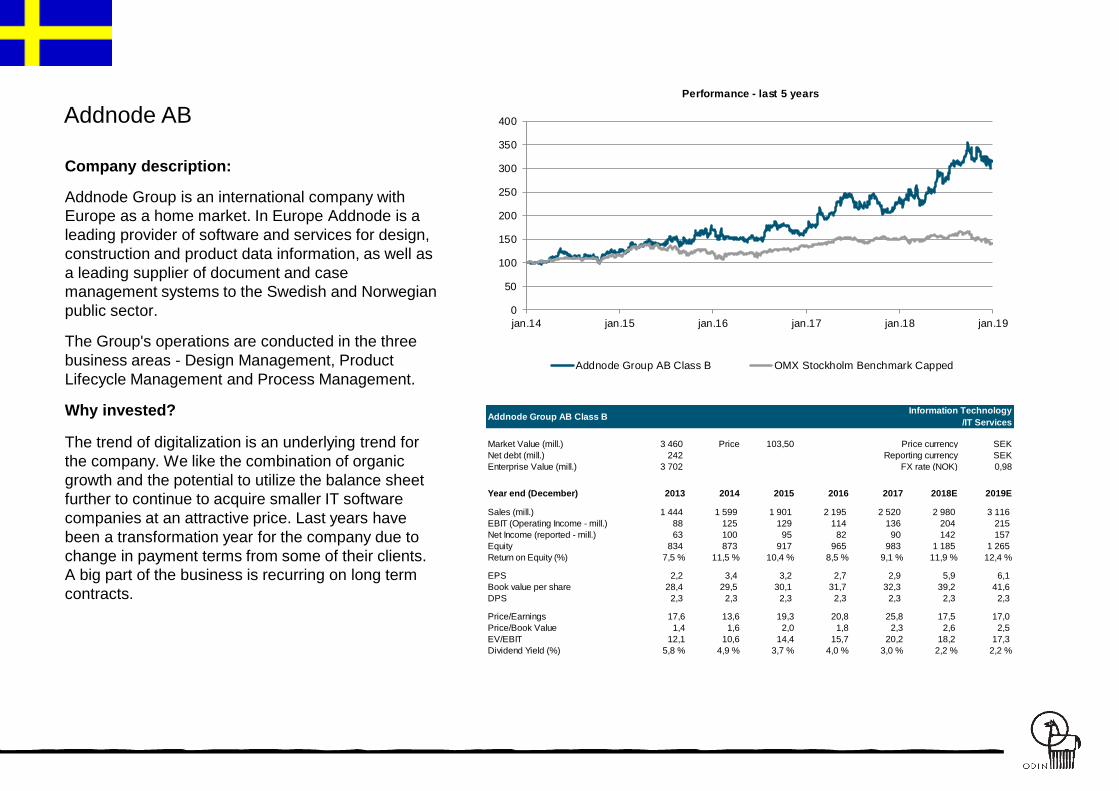

Addnode AB

Company description:

Addnode Group is an international company with

Europe as a home market. In Europe Addnode is a

leading provider of software and services for design,

construction and product data information, as well as

a leading supplier of document and case

management systems to the Swedish and Norwegian

public sector.

The Group's operations are conducted in the three

business areas - Design Management, Product

Lifecycle Management and Process Management.

Why invested?

The trend of digitalization is an underlying trend for

the company. We like the combination of organic

growth and the potential to utilize the balance sheet

further to continue to acquire smaller IT software

companies at an attractive price. Last years have

been a transformation year for the company due to

change in payment terms from some of their clients.

A big part of the business is recurring on long term

contracts.

Market Value (mill.) 3 460 Price 103,50 SEK

Net debt (mill.) 242 SEK

Enterprise Value (mill.) 3 702 0,98

Year end (December) 2013 2014 2015 2016 2017 2018E 2019E

Sales (mill.) 1 444 1 599 1 901 2 195 2 520 2 980 3 116

EBIT (Operating Income - mill.) 88 125 129 114 136 204 215

Net Income (reported - mill.) 63 100 95 82 90 142 157

Equity 834 873 917 965 983 1 185 1 265

Return on Equity (%) 7,5 % 11,5 % 10,4 % 8,5 % 9,1 % 11,9 % 12,4 %

EPS 2,2 3,4 3,2 2,7 2,9 5,9 6,1

Book value per share 28,4 29,5 30,1 31,7 32,3 39,2 41,6

DPS 2,3 2,3 2,3 2,3 2,3 2,3 2,3

Price/Earnings 17,6 13,6 19,3 20,8 25,8 17,5 17,0

Price/Book Value 1,4 1,6 2,0 1,8 2,3 2,6 2,5

EV/EBIT 12,1 10,6 14,4 15,7 20,2 18,2 17,3

Dividend Yield (%) 5,8 % 4,9 % 3,7 % 4,0 % 3,0 % 2,2 % 2,2 %

Addnode Group AB Class BInformation Technology

/IT Services

Price currency

Reporting currency

FX rate (NOK)

0

50

100

150

200

250

300

350

400

jan.14 jan.15 jan.16 jan.17 jan.18 jan.19

Performance - last 5 years

Addnode Group AB Class B OMX Stockholm Benchmark Capped

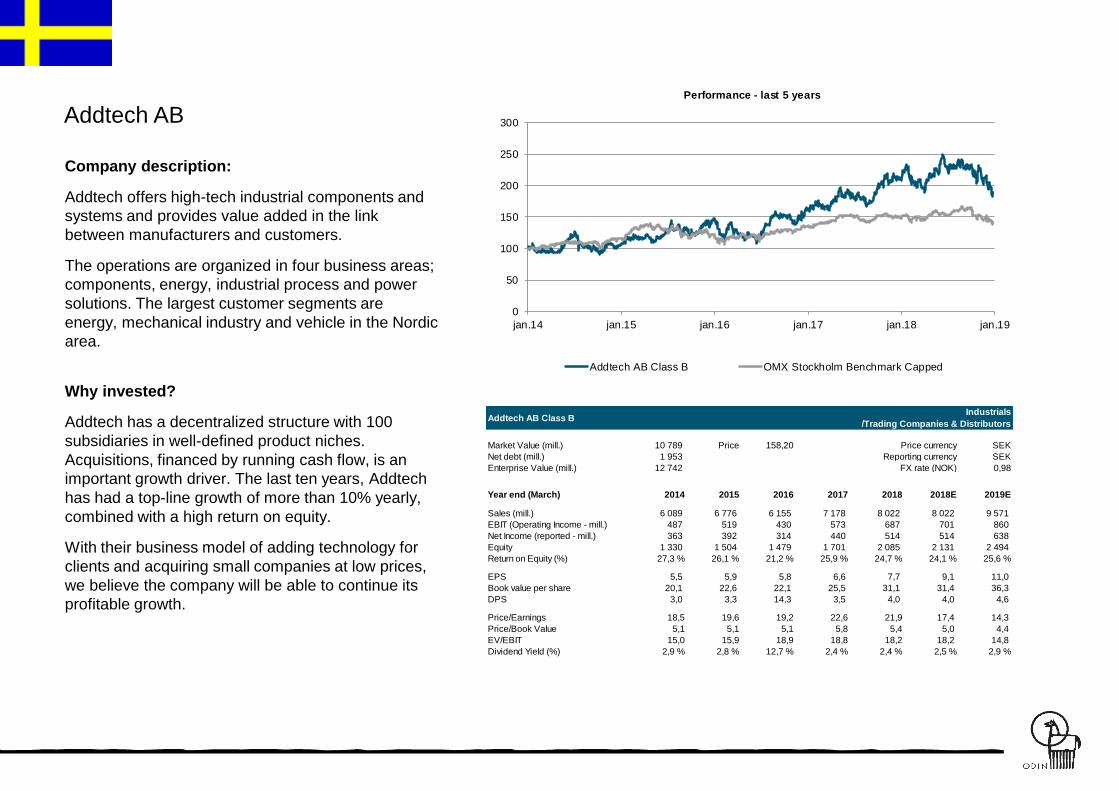

Addtech AB

Company description:

Addtech offers high-tech industrial components and

systems and provides value added in the link

between manufacturers and customers.

The operations are organized in four business areas;

components, energy, industrial process and power

solutions. The largest customer segments are

energy, mechanical industry and vehicle in the Nordic

area.

Why invested?

Addtech has a decentralized structure with 100

subsidiaries in well-defined product niches.

Acquisitions, financed by running cash flow, is an

important growth driver. The last ten years, Addtech

has had a top-line growth of more than 10% yearly,

combined with a high return on equity.

With their business model of adding technology for

clients and acquiring small companies at low prices,

we believe the company will be able to continue its

profitable growth.

Market Value (mill.) 10 789 Price 158,20 SEK

Net debt (mill.) 1 953 SEK

Enterprise Value (mill.) 12 742 0,98

Year end (March) 2014 2015 2016 2017 2018 2018E 2019E

Sales (mill.) 6 089 6 776 6 155 7 178 8 022 8 022 9 571

EBIT (Operating Income - mill.) 487 519 430 573 687 701 860

Net Income (reported - mill.) 363 392 314 440 514 514 638

Equity 1 330 1 504 1 479 1 701 2 085 2 131 2 494

Return on Equity (%) 27,3 % 26,1 % 21,2 % 25,9 % 24,7 % 24,1 % 25,6 %

EPS 5,5 5,9 5,8 6,6 7,7 9,1 11,0

Book value per share 20,1 22,6 22,1 25,5 31,1 31,4 36,3

DPS 3,0 3,3 14,3 3,5 4,0 4,0 4,6

Price/Earnings 18,5 19,6 19,2 22,6 21,9 17,4 14,3

Price/Book Value 5,1 5,1 5,1 5,8 5,4 5,0 4,4

EV/EBIT 15,0 15,9 18,9 18,8 18,2 18,2 14,8

Dividend Yield (%) 2,9 % 2,8 % 12,7 % 2,4 % 2,4 % 2,5 % 2,9 %

Addtech AB Class BIndustrials

/Trading Companies & Distributors

Price currency

Reporting currency

FX rate (NOK)

0

50

100

150

200

250

300

jan.14 jan.15 jan.16 jan.17 jan.18 jan.19

Performance - last 5 years

Addtech AB Class B OMX Stockholm Benchmark Capped

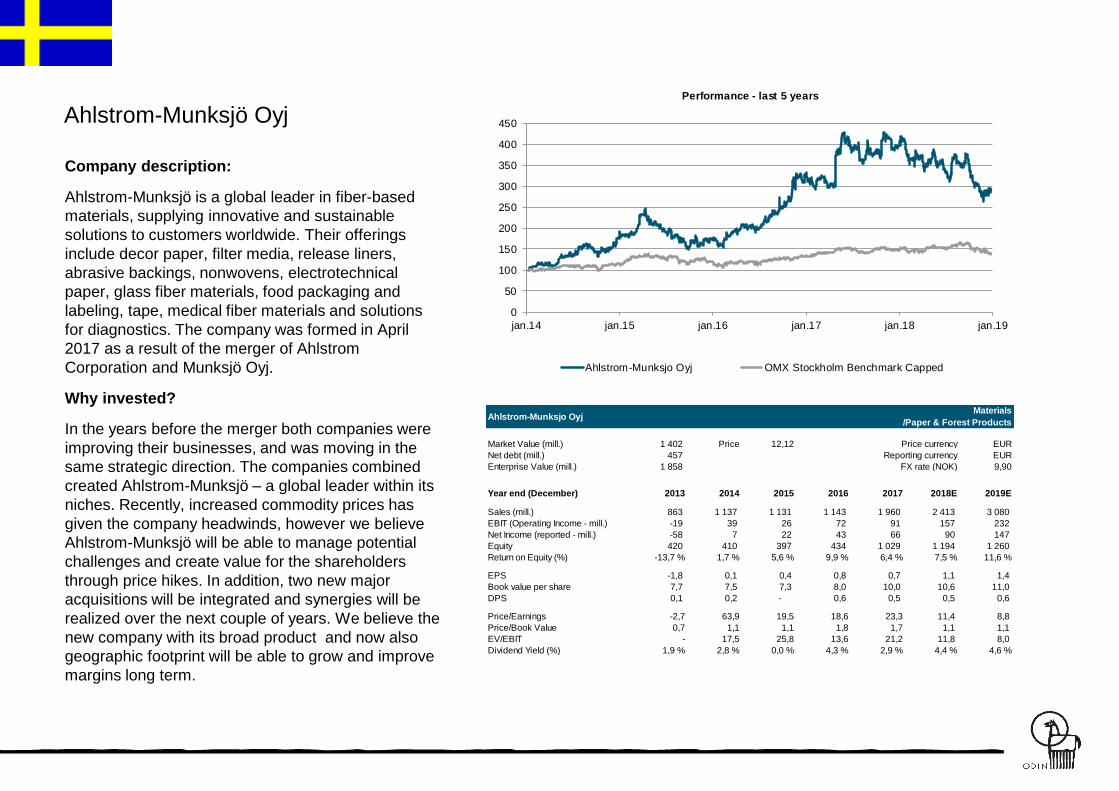

Ahlstrom-Munksjö Oyj

Company description:

Ahlstrom-Munksjö is a global leader in fiber-based

materials, supplying innovative and sustainable

solutions to customers worldwide. Their offerings

include decor paper, filter media, release liners,

abrasive backings, nonwovens, electrotechnical

paper, glass fiber materials, food packaging and

labeling, tape, medical fiber materials and solutions

for diagnostics. The company was formed in April

2017 as a result of the merger of Ahlstrom

Corporation and Munksjö Oyj.

Why invested?

In the years before the merger both companies were

improving their businesses, and was moving in the

same strategic direction. The companies combined

created Ahlstrom-Munksjö – a global leader within its

niches. Recently, increased commodity prices has

given the company headwinds, however we believe

Ahlstrom-Munksjö will be able to manage potential

challenges and create value for the shareholders

through price hikes. In addition, two new major

acquisitions will be integrated and synergies will be

realized over the next couple of years. We believe the

new company with its broad product and now also

geographic footprint will be able to grow and improve

margins long term.

Market Value (mill.) 1 402 Price 12,12 EUR

Net debt (mill.) 457 EUR

Enterprise Value (mill.) 1 858 9,90

Year end (December) 2013 2014 2015 2016 2017 2018E 2019E

Sales (mill.) 863 1 137 1 131 1 143 1 960 2 413 3 080

EBIT (Operating Income - mill.) -19 39 26 72 91 157 232

Net Income (reported - mill.) -58 7 22 43 66 90 147

Equity 420 410 397 434 1 029 1 194 1 260

Return on Equity (%) -13,7 % 1,7 % 5,6 % 9,9 % 6,4 % 7,5 % 11,6 %

EPS -1,8 0,1 0,4 0,8 0,7 1,1 1,4

Book value per share 7,7 7,5 7,3 8,0 10,0 10,6 11,0

DPS 0,1 0,2 - 0,6 0,5 0,5 0,6

Price/Earnings -2,7 63,9 19,5 18,6 23,3 11,4 8,8

Price/Book Value 0,7 1,1 1,1 1,8 1,7 1,1 1,1

EV/EBIT - 17,5 25,8 13,6 21,2 11,8 8,0

Dividend Yield (%) 1,9 % 2,8 % 0,0 % 4,3 % 2,9 % 4,4 % 4,6 %

Ahlstrom-Munksjo OyjMaterials

/Paper & Forest Products

Price currency

Reporting currency

FX rate (NOK)

0

50

100

150

200

250

300

350

400

450

jan.14 jan.15 jan.16 jan.17 jan.18 jan.19

Performance - last 5 years

Ahlstrom-Munksjo Oyj OMX Stockholm Benchmark Capped

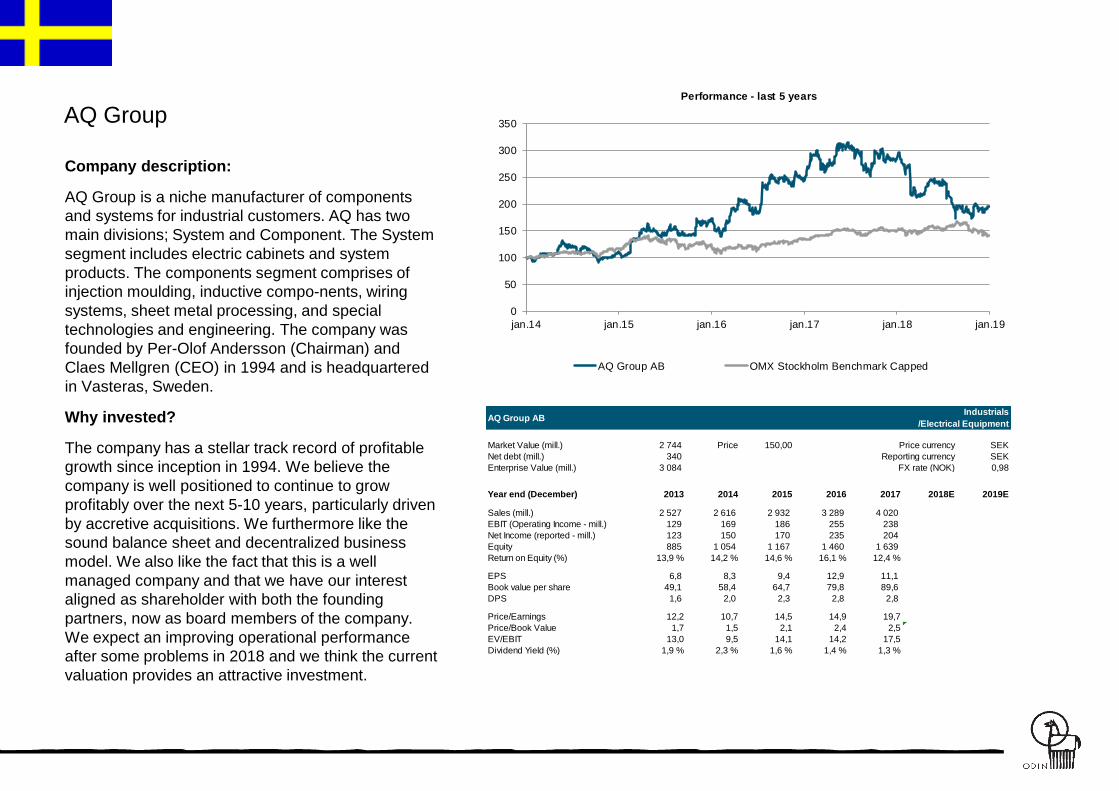

AQ Group

Company description:

AQ Group is a niche manufacturer of components

and systems for industrial customers. AQ has two

main divisions; System and Component. The System

segment includes electric cabinets and system

products. The components segment comprises of

injection moulding, inductive compo-nents, wiring

systems, sheet metal processing, and special

technologies and engineering. The company was

founded by Per-Olof Andersson (Chairman) and

Claes Mellgren (CEO) in 1994 and is headquartered

in Vasteras, Sweden.

Why invested?

The company has a stellar track record of profitable

growth since inception in 1994. We believe the

company is well positioned to continue to grow

profitably over the next 5-10 years, particularly driven

by accretive acquisitions. We furthermore like the

sound balance sheet and decentralized business

model. We also like the fact that this is a well

managed company and that we have our interest

aligned as shareholder with both the founding

partners, now as board members of the company.

We expect an improving operational performance

after some problems in 2018 and we think the current

valuation provides an attractive investment.

Market Value (mill.) 2 744 Price 150,00 SEK

Net debt (mill.) 340 SEK

Enterprise Value (mill.) 3 084 0,98

Year end (December) 2013 2014 2015 2016 2017 2018E 2019E

Sales (mill.) 2 527 2 616 2 932 3 289 4 020 - -

EBIT (Operating Income - mill.) 129 169 186 255 238 - -

Net Income (reported - mill.) 123 150 170 235 204 - -

Equity 885 1 054 1 167 1 460 1 639 - -

Return on Equity (%) 13,9 % 14,2 % 14,6 % 16,1 % 12,4 % #VALUE! #VALUE!

EPS 6,8 8,3 9,4 12,9 11,1 - -

Book value per share 49,1 58,4 64,7 79,8 89,6 - -

DPS 1,6 2,0 2,3 2,8 2,8 - -

Price/Earnings 12,2 10,7 14,5 14,9 19,7 #VALUE! #VALUE!

Price/Book Value 1,7 1,5 2,1 2,4 2,5 #VALUE! #VALUE!

EV/EBIT 13,0 9,5 14,1 14,2 17,5 #VALUE! #VALUE!

Dividend Yield (%) 1,9 % 2,3 % 1,6 % 1,4 % 1,3 % #VALUE! #VALUE!

AQ Group ABIndustrials

/Electrical Equipment

Price currency

Reporting currency

FX rate (NOK)

0

50

100

150

200

250

300

350

jan.14 jan.15 jan.16 jan.17 jan.18 jan.19

Performance - last 5 years

AQ Group AB OMX Stockholm Benchmark Capped

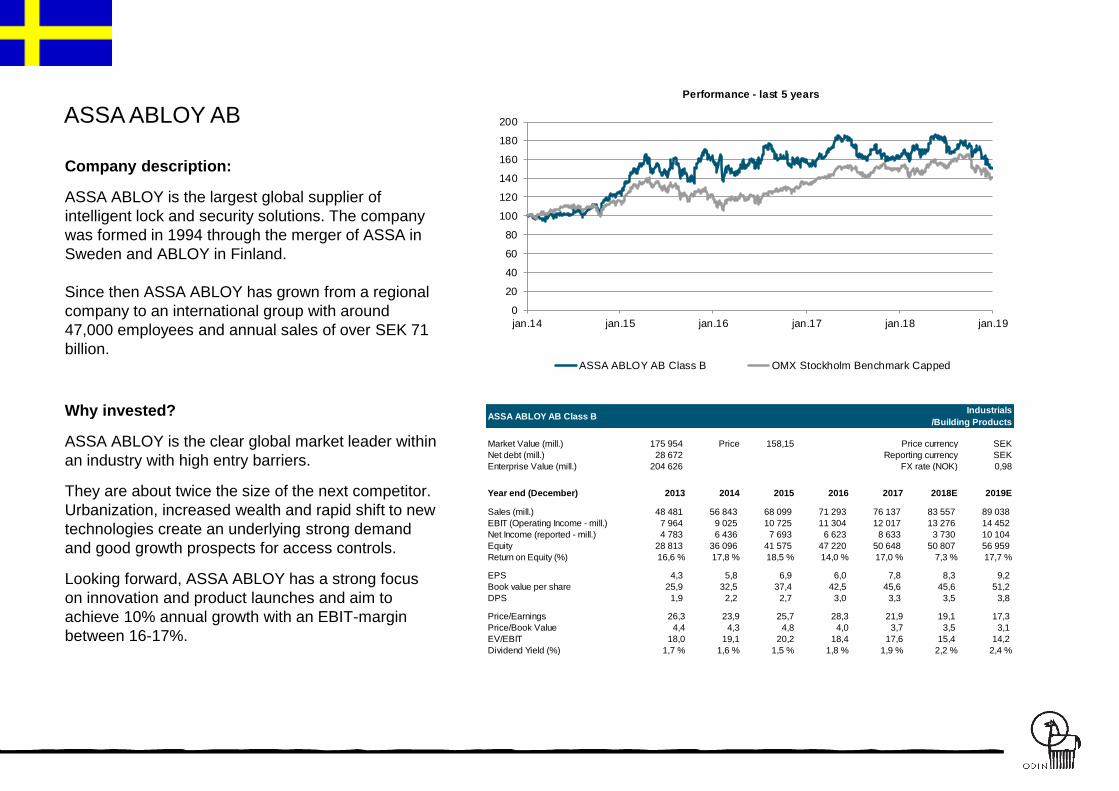

ASSA ABLOY AB

Company description:

ASSA ABLOY is the largest global supplier of

intelligent lock and security solutions. The company

was formed in 1994 through the merger of ASSA in

Sweden and ABLOY in Finland.

Since then ASSA ABLOY has grown from a regional

company to an international group with around

47,000 employees and annual sales of over SEK 71

billion.

Why invested?

ASSA ABLOY is the clear global market leader within

an industry with high entry barriers.

They are about twice the size of the next competitor.

Urbanization, increased wealth and rapid shift to new

technologies create an underlying strong demand

and good growth prospects for access controls.

Looking forward, ASSA ABLOY has a strong focus

on innovation and product launches and aim to

achieve 10% annual growth with an EBIT-margin

between 16-17%.

Market Value (mill.) 175 954 Price 158,15 SEK

Net debt (mill.) 28 672 SEK

Enterprise Value (mill.) 204 626 0,98

Year end (December) 2013 2014 2015 2016 2017 2018E 2019E

Sales (mill.) 48 481 56 843 68 099 71 293 76 137 83 557 89 038

EBIT (Operating Income - mill.) 7 964 9 025 10 725 11 304 12 017 13 276 14 452

Net Income (reported - mill.) 4 783 6 436 7 693 6 623 8 633 3 730 10 104

Equity 28 813 36 096 41 575 47 220 50 648 50 807 56 959

Return on Equity (%) 16,6 % 17,8 % 18,5 % 14,0 % 17,0 % 7,3 % 17,7 %

EPS 4,3 5,8 6,9 6,0 7,8 8,3 9,2

Book value per share 25,9 32,5 37,4 42,5 45,6 45,6 51,2

DPS 1,9 2,2 2,7 3,0 3,3 3,5 3,8

Price/Earnings 26,3 23,9 25,7 28,3 21,9 19,1 17,3

Price/Book Value 4,4 4,3 4,8 4,0 3,7 3,5 3,1

EV/EBIT 18,0 19,1 20,2 18,4 17,6 15,4 14,2

Dividend Yield (%) 1,7 % 1,6 % 1,5 % 1,8 % 1,9 % 2,2 % 2,4 %

ASSA ABLOY AB Class BIndustrials

/Building Products

Price currency

Reporting currency

FX rate (NOK)

0

20

40

60

80

100

120

140

160

180

200

jan.14 jan.15 jan.16 jan.17 jan.18 jan.19

Performance - last 5 years

ASSA ABLOY AB Class B OMX Stockholm Benchmark Capped

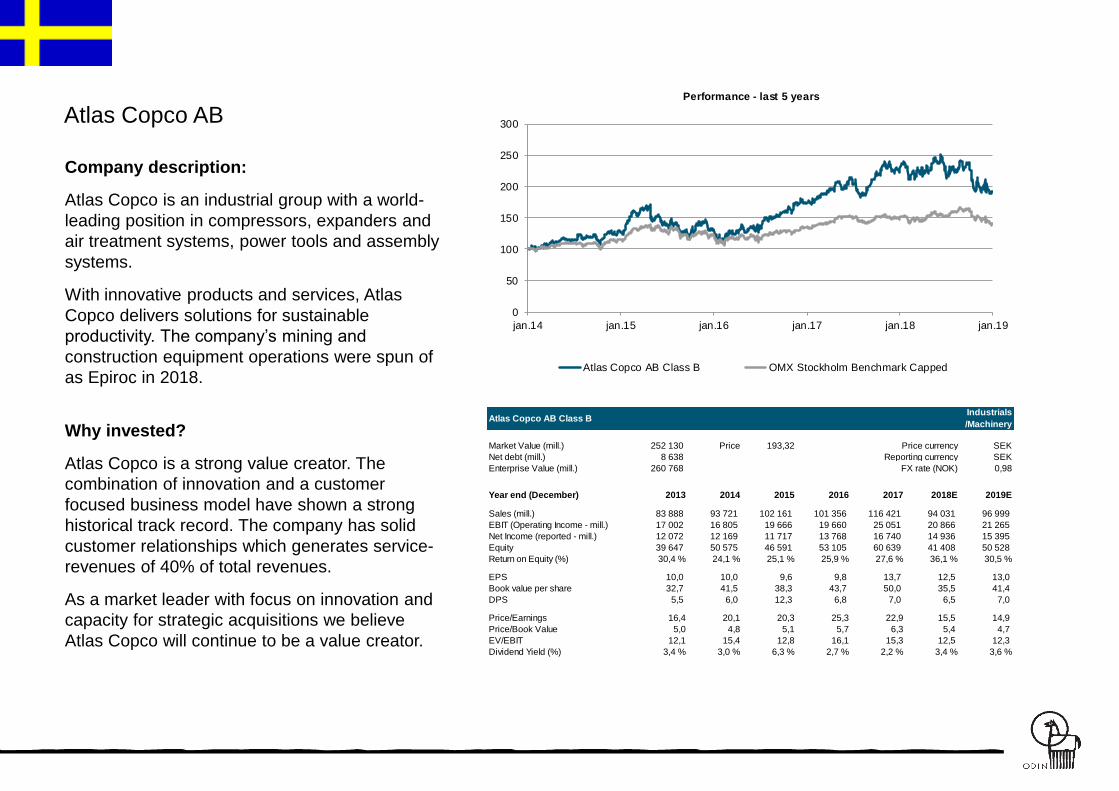

Atlas Copco AB

Company description:

Atlas Copco is an industrial group with a world-

leading position in compressors, expanders and

air treatment systems, power tools and assembly

systems.

With innovative products and services, Atlas

Copco delivers solutions for sustainable

productivity. The company’s mining and

construction equipment operations were spun of

as Epiroc in 2018.

Why invested?

Atlas Copco is a strong value creator. The

combination of innovation and a customer

focused business model have shown a strong

historical track record. The company has solid

customer relationships which generates service-

revenues of 40% of total revenues.

As a market leader with focus on innovation and

capacity for strategic acquisitions we believe

Atlas Copco will continue to be a value creator.

Market Value (mill.) 252 130 Price 193,32 SEK

Net debt (mill.) 8 638 SEK

Enterprise Value (mill.) 260 768 0,98

Year end (December) 2013 2014 2015 2016 2017 2018E 2019E

Sales (mill.) 83 888 93 721 102 161 101 356 116 421 94 031 96 999

EBIT (Operating Income - mill.) 17 002 16 805 19 666 19 660 25 051 20 866 21 265

Net Income (reported - mill.) 12 072 12 169 11 717 13 768 16 740 14 936 15 395

Equity 39 647 50 575 46 591 53 105 60 639 41 408 50 528

Return on Equity (%) 30,4 % 24,1 % 25,1 % 25,9 % 27,6 % 36,1 % 30,5 %

EPS 10,0 10,0 9,6 9,8 13,7 12,5 13,0

Book value per share 32,7 41,5 38,3 43,7 50,0 35,5 41,4

DPS 5,5 6,0 12,3 6,8 7,0 6,5 7,0

Price/Earnings 16,4 20,1 20,3 25,3 22,9 15,5 14,9

Price/Book Value 5,0 4,8 5,1 5,7 6,3 5,4 4,7

EV/EBIT 12,1 15,4 12,8 16,1 15,3 12,5 12,3

Dividend Yield (%) 3,4 % 3,0 % 6,3 % 2,7 % 2,2 % 3,4 % 3,6 %

Atlas Copco AB Class BIndustrials

/Machinery

Price currency

Reporting currency

FX rate (NOK)

0

50

100

150

200

250

300

jan.14 jan.15 jan.16 jan.17 jan.18 jan.19

Performance - last 5 years

Atlas Copco AB Class B OMX Stockholm Benchmark Capped

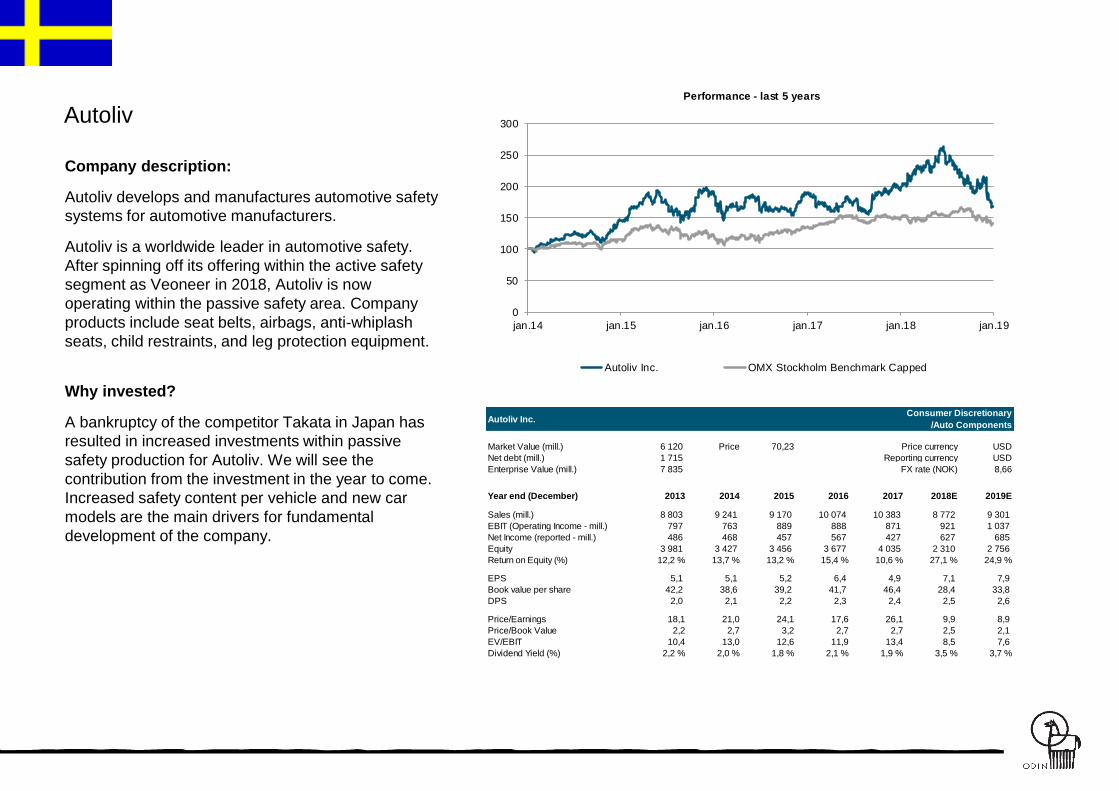

Autoliv

Company description:

Autoliv develops and manufactures automotive safety

systems for automotive manufacturers.

Autoliv is a worldwide leader in automotive safety.

After spinning off its offering within the active safety

segment as Veoneer in 2018, Autoliv is now

operating within the passive safety area. Company

products include seat belts, airbags, anti-whiplash

seats, child restraints, and leg protection equipment.

Why invested?

A bankruptcy of the competitor Takata in Japan has

resulted in increased investments within passive

safety production for Autoliv. We will see the

contribution from the investment in the year to come.

Increased safety content per vehicle and new car

models are the main drivers for fundamental

development of the company.

Market Value (mill.) 6 120 Price 70,23 USD

Net debt (mill.) 1 715 USD

Enterprise Value (mill.) 7 835 8,66

Year end (December) 2013 2014 2015 2016 2017 2018E 2019E

Sales (mill.) 8 803 9 241 9 170 10 074 10 383 8 772 9 301

EBIT (Operating Income - mill.) 797 763 889 888 871 921 1 037

Net Income (reported - mill.) 486 468 457 567 427 627 685

Equity 3 981 3 427 3 456 3 677 4 035 2 310 2 756

Return on Equity (%) 12,2 % 13,7 % 13,2 % 15,4 % 10,6 % 27,1 % 24,9 %

EPS 5,1 5,1 5,2 6,4 4,9 7,1 7,9

Book value per share 42,2 38,6 39,2 41,7 46,4 28,4 33,8

DPS 2,0 2,1 2,2 2,3 2,4 2,5 2,6

Price/Earnings 18,1 21,0 24,1 17,6 26,1 9,9 8,9

Price/Book Value 2,2 2,7 3,2 2,7 2,7 2,5 2,1

EV/EBIT 10,4 13,0 12,6 11,9 13,4 8,5 7,6

Dividend Yield (%) 2,2 % 2,0 % 1,8 % 2,1 % 1,9 % 3,5 % 3,7 %

Autoliv Inc.Consumer Discretionary

/Auto Components

Price currency

Reporting currency

FX rate (NOK)

0

50

100

150

200

250

300

jan.14 jan.15 jan.16 jan.17 jan.18 jan.19

Performance - last 5 years

Autoliv Inc. OMX Stockholm Benchmark Capped

Axfood

Company description:

Axfood is the second largest food retailer in Sweden

with brands such as Willys, Närlivs, Hemköp,

Snabbgross, Mat.se, Middagsfrid and Eurocash.

Axfood currently has a market share of approximately

21 percent.

Axfoods business model is built on a strong focus on

their customers and employees, in addition to

sustainability, efficiency and profitable growth.

Why invested?

Urbanization, digitalization and focus on sustainable

lifestyles are trends that affect the food retail trade.

We believe Axfood is up to the task, with a broad

selection of brands in different segments, including

private label (28%), omni-channel strategies and

focus on sustainability.

With decent growth and stable operating margins we

find the business appealing. We think the strong

fundamental story will continue despite higher

investments within digital offering going forward.

Market Value (mill.) 31 837 Price 151,70 SEK

Net debt (mill.) -557 SEK

Enterprise Value (mill.) 31 280 0,98

Year end (December) 2013 2014 2015 2016 2017 2018E 2019E

Sales (mill.) 37 522 38 484 41 247 43 355 45 968 47 979 49 639

EBIT (Operating Income - mill.) 972 1 118 1 410 1 486 1 429 2 025 2 048

Net Income (reported - mill.) 987 1 095 1 361 1 473 1 463 1 565 1 600

Equity 3 768 4 029 4 530 4 117 4 266 4 404 4 451

Return on Equity (%) 26,2 % 27,2 % 30,0 % 35,8 % 34,3 % 35,5 % 36,0 %

EPS 4,7 5,2 6,5 7,0 7,0 7,5 7,6

Book value per share 18,0 19,2 21,6 19,6 20,3 20,6 21,1

DPS 3,8 4,3 9,0 6,0 7,0 7,0 7,0

Price/Earnings 17,2 22,4 22,7 20,4 22,7 20,3 19,9

Price/Book Value 4,5 6,1 6,8 7,3 7,8 7,4 7,2

EV/EBIT 17,1 21,1 20,5 19,1 22,5 15,4 15,3

Dividend Yield (%) 4,6 % 3,6 % 6,1 % 4,2 % 4,4 % 4,6 % 4,6 %

Axfood ABConsumer Staples

/Food & Staples Retailing

Price currency

Reporting currency

FX rate (NOK)

0

50

100

150

200

250

300

350

jan.14 jan.15 jan.16 jan.17 jan.18 jan.19

Performance - last 5 years

Axfood AB OMX Stockholm Benchmark Capped

Beijer Alma AB

Company description:

Beijer Alma AB, through subsidiaries, develops,

manufactures, and markets industrial components.

The company makes specialty cables, chassis

springs, industrial springs and wire components,

valves, dampers, and ventilators, as well as precision

parts using the high speed machining and salt bath

dip brazing techniques.

Beijer Alma sells to telecommunications, electronic,

and high-tech companies.

Why invested?

The company has a strong track record of growth,

both organically and through acquisitions. With a

strong balance sheet and good cash generation

capacity in existing units, we expect acquisition

activity to step up. The first move into industrial

springs in the US could materialize in strong growth

prospects.

The company is very well managed with a strong

philosophy. We think the current valuation doesn’t

reflect the attractive niche markets they are serving

and the long term track record of the company.

Market Value (mill.) 7 834 Price 129,98 SEK

Net debt (mill.) 536 SEK

Enterprise Value (mill.) 8 370 0,98

Year end (December) 2013 2014 2015 2016 2017 2018E 2019E

Sales (mill.) 3 066 3 298 3 522 3 528 3 971 4 430 4 741

EBIT (Operating Income - mill.) 393 425 511 453 525 642 697

Net Income (reported - mill.) 289 319 354 328 388 473 517

Equity 1 611 1 745 1 835 1 902 1 991 2 178 2 351

Return on Equity (%) 17,9 % 18,3 % 19,3 % 17,2 % 19,5 % 21,7 % 22,0 %

EPS 4,8 5,3 5,9 5,4 6,4 7,8 8,6

Book value per share 26,7 29,0 30,5 31,6 33,0 36,1 39,0

DPS 4,0 4,3 4,8 4,8 4,8 5,3 5,6

Price/Earnings 18,5 17,2 18,7 21,4 20,3 16,6 15,2

Price/Book Value 3,3 3,2 3,6 3,7 4,0 3,6 3,3

EV/EBIT 13,8 13,4 13,8 16,2 15,8 13,0 12,0

Dividend Yield (%) 4,5 % 4,7 % 4,3 % 4,1 % 3,6 % 4,0 % 4,3 %

Beijer Alma AB Class BIndustrials

/Machinery

Price currency

Reporting currency

FX rate (NOK)

0

50

100

150

200

250

jan.14 jan.15 jan.16 jan.17 jan.18 jan.19

Performance - last 5 years

Beijer Alma AB Class B OMX Stockholm Benchmark Capped

Beijer Ref AB

Company description:

Beijer Ref is one of the largest refrigeration

wholesalers in the world and offers its customers

competitive solutions within refrigeration and air

conditioning, including refrigeration systems,

components for refrigeration systems, air conditioning

and heat pumps. The aftermarket accounts for 60-70

percent of sales. Europe make up 82 % of sales.

Why invested?

Beijer Ref is a well-run company with exposure to the

refrigeration business. The market is still fragmented

and Beijer Ref is one of only three global players,

which makes it possible to further consolidate the

market.

As older refrigeration systems are being phased out,

Beijer Ref will likely see increased demand. We

believe Beijer Ref is well positioned to continue to

grow through acquisitions as well as organic growth.

Market Value (mill.) 18 590 Price 145,88 SEK

Net debt (mill.) 2 909 SEK

Enterprise Value (mill.) 21 499 0,98

Year end (December) 2013 2014 2015 2016 2017 2018E 2019E

Sales (mill.) 6 595 7 189 8 361 9 045 9 830 13 033 14 597

EBIT (Operating Income - mill.) 398 462 550 577 716 1 141 1 340

Net Income (reported - mill.) 234 316 366 389 511 796 933

Equity 2 368 2 592 2 594 2 915 3 234 3 821 4 365

Return on Equity (%) 9,9 % 12,2 % 14,1 % 13,3 % 15,8 % 20,8 % 21,4 %

EPS 1,8 2,5 2,9 3,1 4,0 6,4 7,5

Book value per share 18,6 20,4 20,4 22,9 25,4 30,1 34,4

DPS 1,6 1,7 1,8 1,8 1,9 3,1 3,6

Price/Earnings 25,4 17,1 23,2 23,6 26,2 22,9 19,5

Price/Book Value 2,5 2,1 3,3 3,1 4,1 4,9 4,2

EV/EBIT 17,9 14,7 18,0 18,9 21,0 18,8 16,0

Dividend Yield (%) 3,4 % 3,9 % 2,6 % 2,5 % 1,8 % 2,1 % 2,5 %

Beijer Ref AB Class BIndustrials

/Trading Companies & Distributors

Price currency

Reporting currency

FX rate (NOK)

0

100

200

300

400

500

600

jan.14 jan.15 jan.16 jan.17 jan.18 jan.19

Performance - last 5 years

Beijer Ref AB Class B OMX Stockholm Benchmark Capped

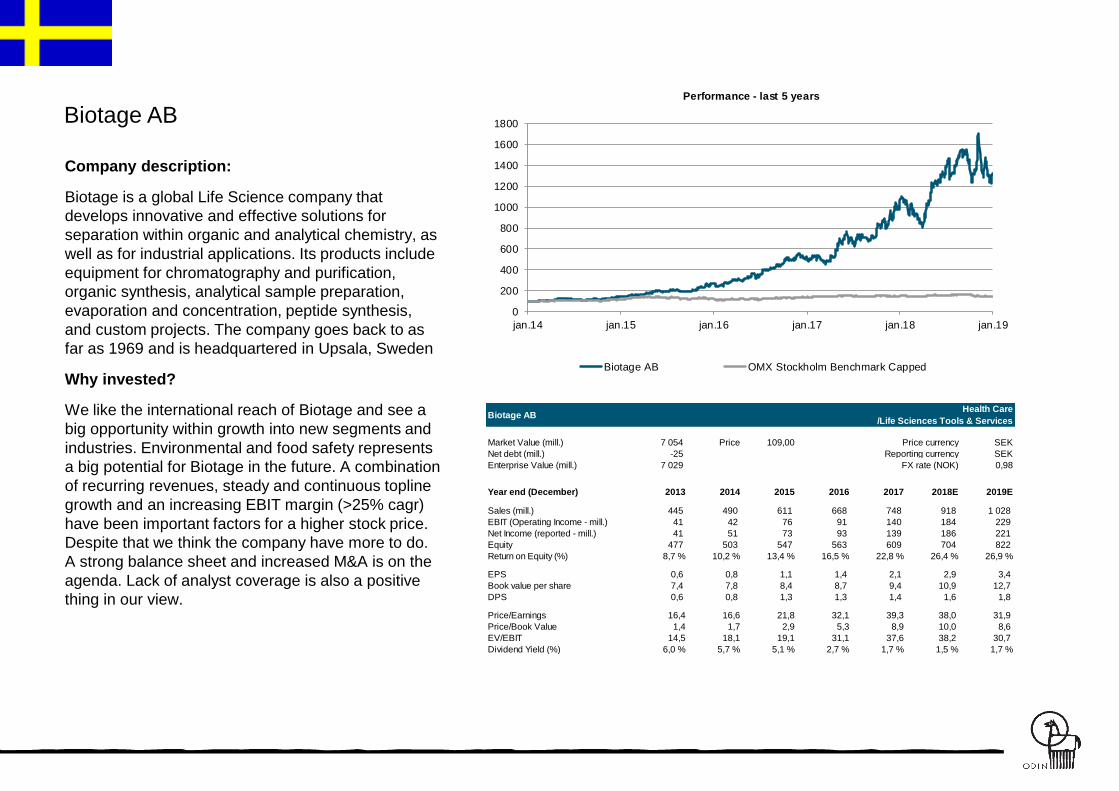

Biotage AB

Company description:

Biotage is a global Life Science company that

develops innovative and effective solutions for

separation within organic and analytical chemistry, as

well as for industrial applications. Its products include

equipment for chromatography and purification,

organic synthesis, analytical sample preparation,

evaporation and concentration, peptide synthesis,

and custom projects. The company goes back to as

far as 1969 and is headquartered in Upsala, Sweden

Why invested?

We like the international reach of Biotage and see a

big opportunity within growth into new segments and

industries. Environmental and food safety represents

a big potential for Biotage in the future. A combination

of recurring revenues, steady and continuous topline

growth and an increasing EBIT margin (>25% cagr)

have been important factors for a higher stock price.

Despite that we think the company have more to do.

A strong balance sheet and increased M&A is on the

agenda. Lack of analyst coverage is also a positive

thing in our view.

0

200

400

600

800

1000

1200

1400

1600

1800

jan.14 jan.15 jan.16 jan.17 jan.18 jan.19

Performance - last 5 years

Biotage AB OMX Stockholm Benchmark Capped

Market Value (mill.) 7 054 Price 109,00 SEK

Net debt (mill.) -25 SEK

Enterprise Value (mill.) 7 029 0,98

Year end (December) 2013 2014 2015 2016 2017 2018E 2019E

Sales (mill.) 445 490 611 668 748 918 1 028

EBIT (Operating Income - mill.) 41 42 76 91 140 184 229

Net Income (reported - mill.) 41 51 73 93 139 186 221

Equity 477 503 547 563 609 704 822

Return on Equity (%) 8,7 % 10,2 % 13,4 % 16,5 % 22,8 % 26,4 % 26,9 %

EPS 0,6 0,8 1,1 1,4 2,1 2,9 3,4

Book value per share 7,4 7,8 8,4 8,7 9,4 10,9 12,7

DPS 0,6 0,8 1,3 1,3 1,4 1,6 1,8

Price/Earnings 16,4 16,6 21,8 32,1 39,3 38,0 31,9

Price/Book Value 1,4 1,7 2,9 5,3 8,9 10,0 8,6

EV/EBIT 14,5 18,1 19,1 31,1 37,6 38,2 30,7

Dividend Yield (%) 6,0 % 5,7 % 5,1 % 2,7 % 1,7 % 1,5 % 1,7 %

Biotage ABHealth Care

/Life Sciences Tools & Services

Price currency

Reporting currency

FX rate (NOK)

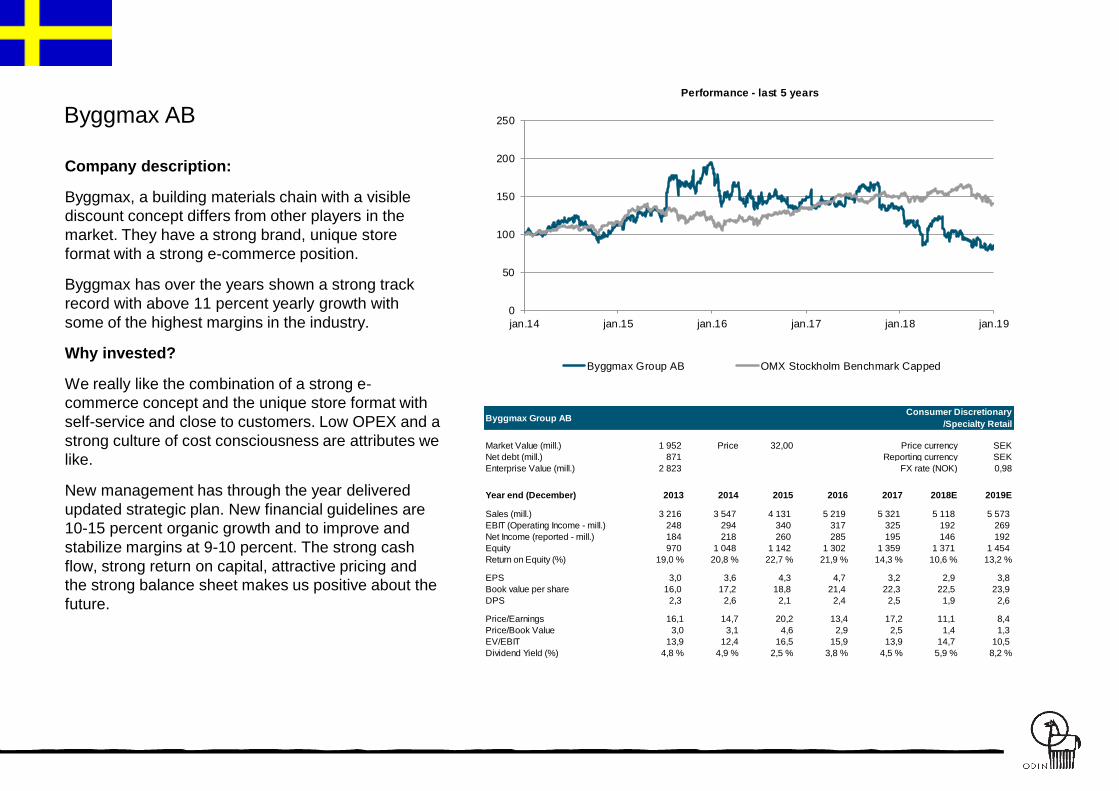

Byggmax AB

Company description:

Byggmax, a building materials chain with a visible

discount concept differs from other players in the

market. They have a strong brand, unique store

format with a strong e-commerce position.

Byggmax has over the years shown a strong track

record with above 11 percent yearly growth with

some of the highest margins in the industry.

Why invested?

We really like the combination of a strong e-

commerce concept and the unique store format with

self-service and close to customers. Low OPEX and a

strong culture of cost consciousness are attributes we

like.

New management has through the year delivered

updated strategic plan. New financial guidelines are

10-15 percent organic growth and to improve and

stabilize margins at 9-10 percent. The strong cash

flow, strong return on capital, attractive pricing and

the strong balance sheet makes us positive about the

future.

Market Value (mill.) 1 952 Price 32,00 SEK

Net debt (mill.) 871 SEK

Enterprise Value (mill.) 2 823 0,98

Year end (December) 2013 2014 2015 2016 2017 2018E 2019E

Sales (mill.) 3 216 3 547 4 131 5 219 5 321 5 118 5 573

EBIT (Operating Income - mill.) 248 294 340 317 325 192 269

Net Income (reported - mill.) 184 218 260 285 195 146 192

Equity 970 1 048 1 142 1 302 1 359 1 371 1 454

Return on Equity (%) 19,0 % 20,8 % 22,7 % 21,9 % 14,3 % 10,6 % 13,2 %

EPS 3,0 3,6 4,3 4,7 3,2 2,9 3,8

Book value per share 16,0 17,2 18,8 21,4 22,3 22,5 23,9

DPS 2,3 2,6 2,1 2,4 2,5 1,9 2,6

Price/Earnings 16,1 14,7 20,2 13,4 17,2 11,1 8,4

Price/Book Value 3,0 3,1 4,6 2,9 2,5 1,4 1,3

EV/EBIT 13,9 12,4 16,5 15,9 13,9 14,7 10,5

Dividend Yield (%) 4,8 % 4,9 % 2,5 % 3,8 % 4,5 % 5,9 % 8,2 %

Byggmax Group ABConsumer Discretionary

/Specialty Retail

Price currency

Reporting currency

FX rate (NOK)

0

50

100

150

200

250

jan.14 jan.15 jan.16 jan.17 jan.18 jan.19

Performance - last 5 years

Byggmax Group AB OMX Stockholm Benchmark Capped

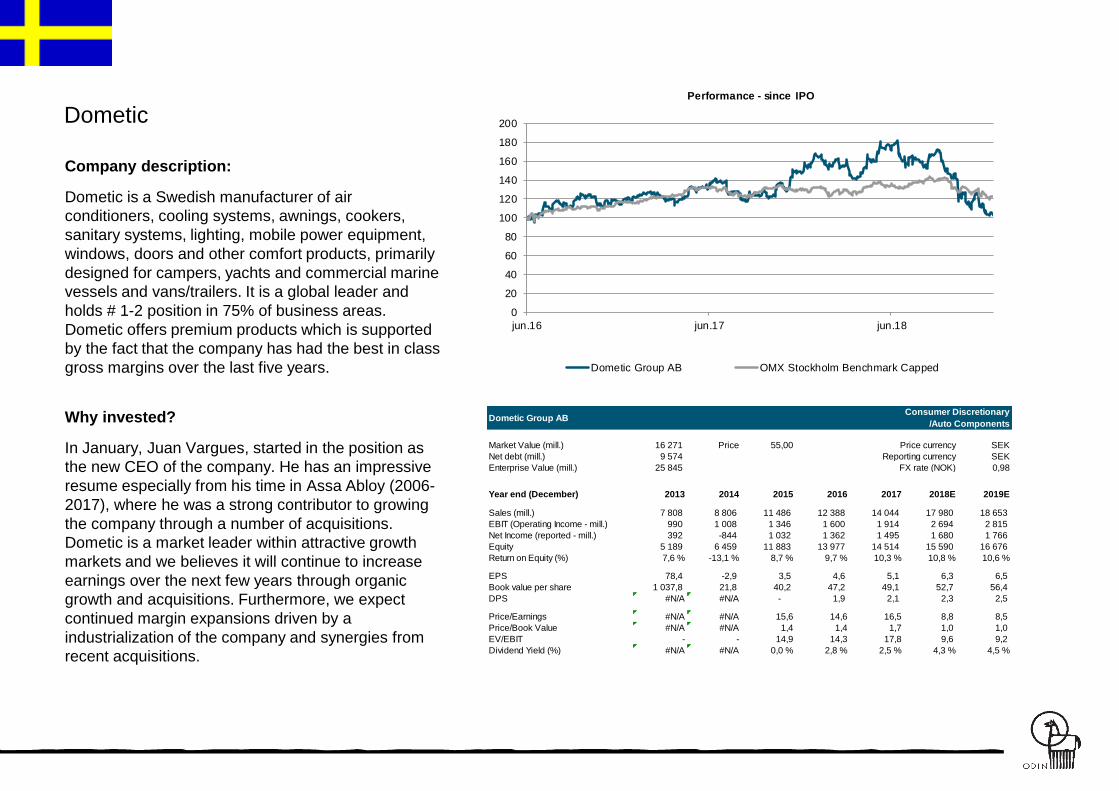

Dometic

Company description:

Dometic is a Swedish manufacturer of air

conditioners, cooling systems, awnings, cookers,

sanitary systems, lighting, mobile power equipment,

windows, doors and other comfort products, primarily

designed for campers, yachts and commercial marine

vessels and vans/trailers. It is a global leader and

holds # 1-2 position in 75% of business areas.

Dometic offers premium products which is supported

by the fact that the company has had the best in class

gross margins over the last five years.

Why invested?

In January, Juan Vargues, started in the position as

the new CEO of the company. He has an impressive

resume especially from his time in Assa Abloy (2006-

2017), where he was a strong contributor to growing

the company through a number of acquisitions.

Dometic is a market leader within attractive growth

markets and we believes it will continue to increase

earnings over the next few years through organic

growth and acquisitions. Furthermore, we expect

continued margin expansions driven by a

industrialization of the company and synergies from

recent acquisitions.

Market Value (mill.) 16 271 Price 55,00 SEK

Net debt (mill.) 9 574 SEK

Enterprise Value (mill.) 25 845 0,98

Year end (December) 2013 2014 2015 2016 2017 2018E 2019E

Sales (mill.) 7 808 8 806 11 486 12 388 14 044 17 980 18 653

EBIT (Operating Income - mill.) 990 1 008 1 346 1 600 1 914 2 694 2 815

Net Income (reported - mill.) 392 -844 1 032 1 362 1 495 1 680 1 766

Equity 5 189 6 459 11 883 13 977 14 514 15 590 16 676

Return on Equity (%) 7,6 % -13,1 % 8,7 % 9,7 % 10,3 % 10,8 % 10,6 %

EPS 78,4 -2,9 3,5 4,6 5,1 6,3 6,5

Book value per share 1 037,8 21,8 40,2 47,2 49,1 52,7 56,4

DPS #N/A #N/A - 1,9 2,1 2,3 2,5

Price/Earnings #N/A #N/A 15,6 14,6 16,5 8,8 8,5

Price/Book Value #N/A #N/A 1,4 1,4 1,7 1,0 1,0

EV/EBIT - - 14,9 14,3 17,8 9,6 9,2

Dividend Yield (%) #N/A #N/A 0,0 % 2,8 % 2,5 % 4,3 % 4,5 %

Dometic Group ABConsumer Discretionary

/Auto Components

Price currency

Reporting currency

FX rate (NOK)

0

20

40

60

80

100

120

140

160

180

200

jun.16 jun.17 jun.18

Performance - since IPO

Dometic Group AB OMX Stockholm Benchmark Capped

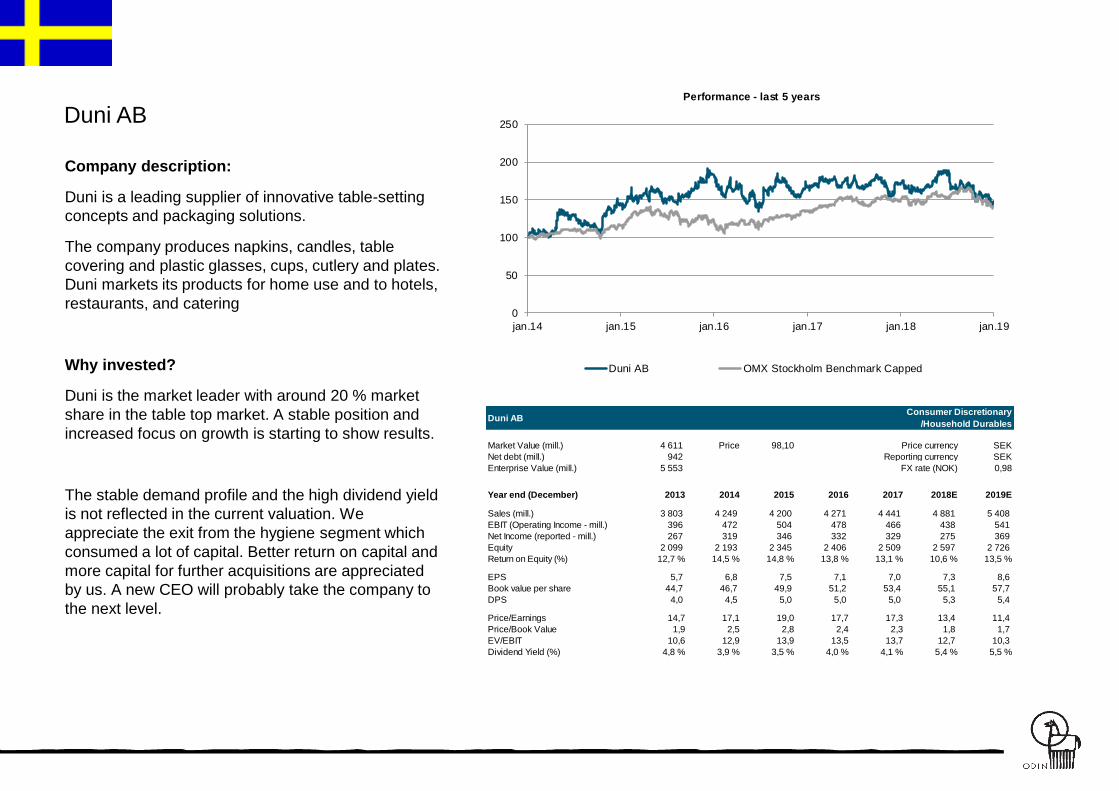

Duni AB

Company description:

Duni is a leading supplier of innovative table-setting

concepts and packaging solutions.

The company produces napkins, candles, table

covering and plastic glasses, cups, cutlery and plates.

Duni markets its products for home use and to hotels,

restaurants, and catering

Why invested?

Duni is the market leader with around 20 % market

share in the table top market. A stable position and

increased focus on growth is starting to show results.

The stable demand profile and the high dividend yield

is not reflected in the current valuation. We

appreciate the exit from the hygiene segment which

consumed a lot of capital. Better return on capital and

more capital for further acquisitions are appreciated

by us. A new CEO will probably take the company to

the next level.

Market Value (mill.) 4 611 Price 98,10 SEK

Net debt (mill.) 942 SEK

Enterprise Value (mill.) 5 553 0,98

Year end (December) 2013 2014 2015 2016 2017 2018E 2019E

Sales (mill.) 3 803 4 249 4 200 4 271 4 441 4 881 5 408

EBIT (Operating Income - mill.) 396 472 504 478 466 438 541

Net Income (reported - mill.) 267 319 346 332 329 275 369

Equity 2 099 2 193 2 345 2 406 2 509 2 597 2 726

Return on Equity (%) 12,7 % 14,5 % 14,8 % 13,8 % 13,1 % 10,6 % 13,5 %

EPS 5,7 6,8 7,5 7,1 7,0 7,3 8,6

Book value per share 44,7 46,7 49,9 51,2 53,4 55,1 57,7

DPS 4,0 4,5 5,0 5,0 5,0 5,3 5,4

Price/Earnings 14,7 17,1 19,0 17,7 17,3 13,4 11,4

Price/Book Value 1,9 2,5 2,8 2,4 2,3 1,8 1,7

EV/EBIT 10,6 12,9 13,9 13,5 13,7 12,7 10,3

Dividend Yield (%) 4,8 % 3,9 % 3,5 % 4,0 % 4,1 % 5,4 % 5,5 %

Duni ABConsumer Discretionary

/Household Durables

Price currency

Reporting currency

FX rate (NOK)

0

50

100

150

200

250

jan.14 jan.15 jan.16 jan.17 jan.18 jan.19

Performance - last 5 years

Duni AB OMX Stockholm Benchmark Capped

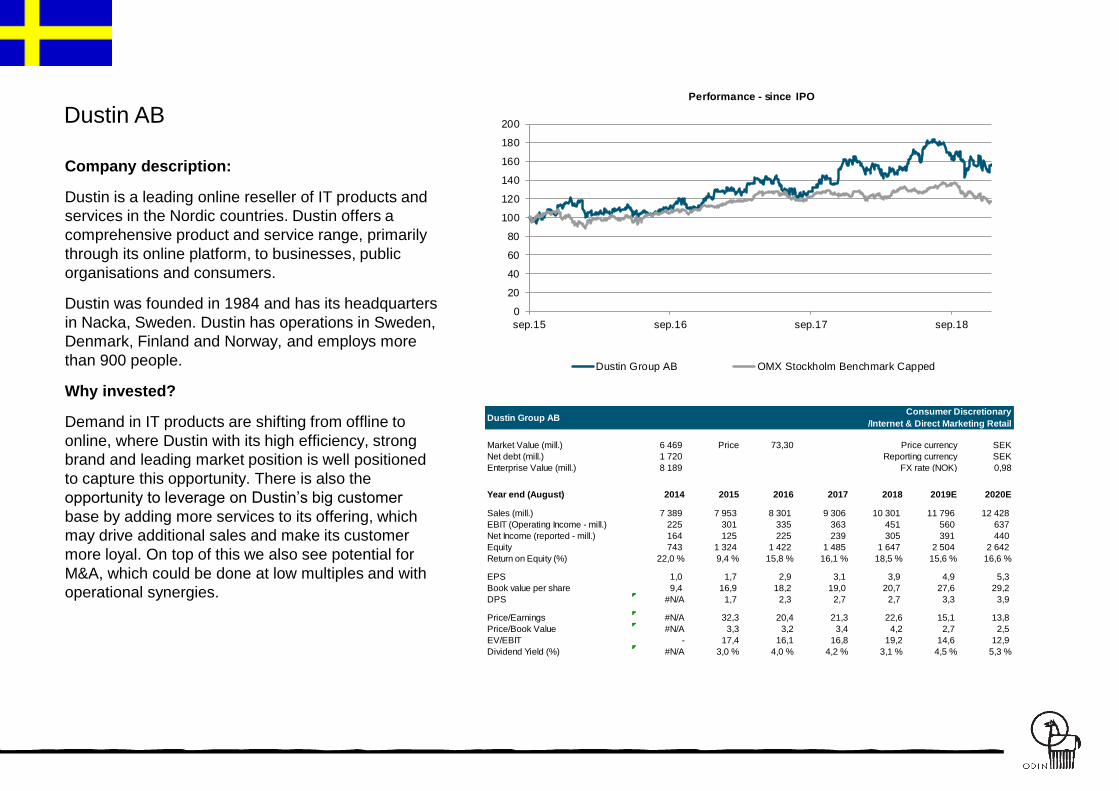

Dustin AB

Company description:

Dustin is a leading online reseller of IT products and

services in the Nordic countries. Dustin offers a

comprehensive product and service range, primarily

through its online platform, to businesses, public

organisations and consumers.

Dustin was founded in 1984 and has its headquarters

in Nacka, Sweden. Dustin has operations in Sweden,

Denmark, Finland and Norway, and employs more

than 900 people.

Why invested?

Demand in IT products are shifting from offline to

online, where Dustin with its high efficiency, strong

brand and leading market position is well positioned

to capture this opportunity. There is also the

opportunity to leverage on Dustin’s big customer

base by adding more services to its offering, which

may drive additional sales and make its customer

more loyal. On top of this we also see potential for

M&A, which could be done at low multiples and with

operational synergies.

Market Value (mill.) 6 469 Price 73,30 SEK

Net debt (mill.) 1 720 SEK

Enterprise Value (mill.) 8 189 0,98

Year end (August) 2014 2015 2016 2017 2018 2019E 2020E

Sales (mill.) 7 389 7 953 8 301 9 306 10 301 11 796 12 428

EBIT (Operating Income - mill.) 225 301 335 363 451 560 637

Net Income (reported - mill.) 164 125 225 239 305 391 440

Equity 743 1 324 1 422 1 485 1 647 2 504 2 642

Return on Equity (%) 22,0 % 9,4 % 15,8 % 16,1 % 18,5 % 15,6 % 16,6 %

EPS 1,0 1,7 2,9 3,1 3,9 4,9 5,3

Book value per share 9,4 16,9 18,2 19,0 20,7 27,6 29,2

DPS #N/A 1,7 2,3 2,7 2,7 3,3 3,9

Price/Earnings #N/A 32,3 20,4 21,3 22,6 15,1 13,8

Price/Book Value #N/A 3,3 3,2 3,4 4,2 2,7 2,5

EV/EBIT - 17,4 16,1 16,8 19,2 14,6 12,9

Dividend Yield (%) #N/A 3,0 % 4,0 % 4,2 % 3,1 % 4,5 % 5,3 %

Dustin Group ABConsumer Discretionary

/Internet & Direct Marketing Retail

Price currency

Reporting currency

FX rate (NOK)

0

20

40

60

80

100

120

140

160

180

200

sep.15 sep.16 sep.17 sep.18

Performance - since IPO

Dustin Group AB OMX Stockholm Benchmark Capped

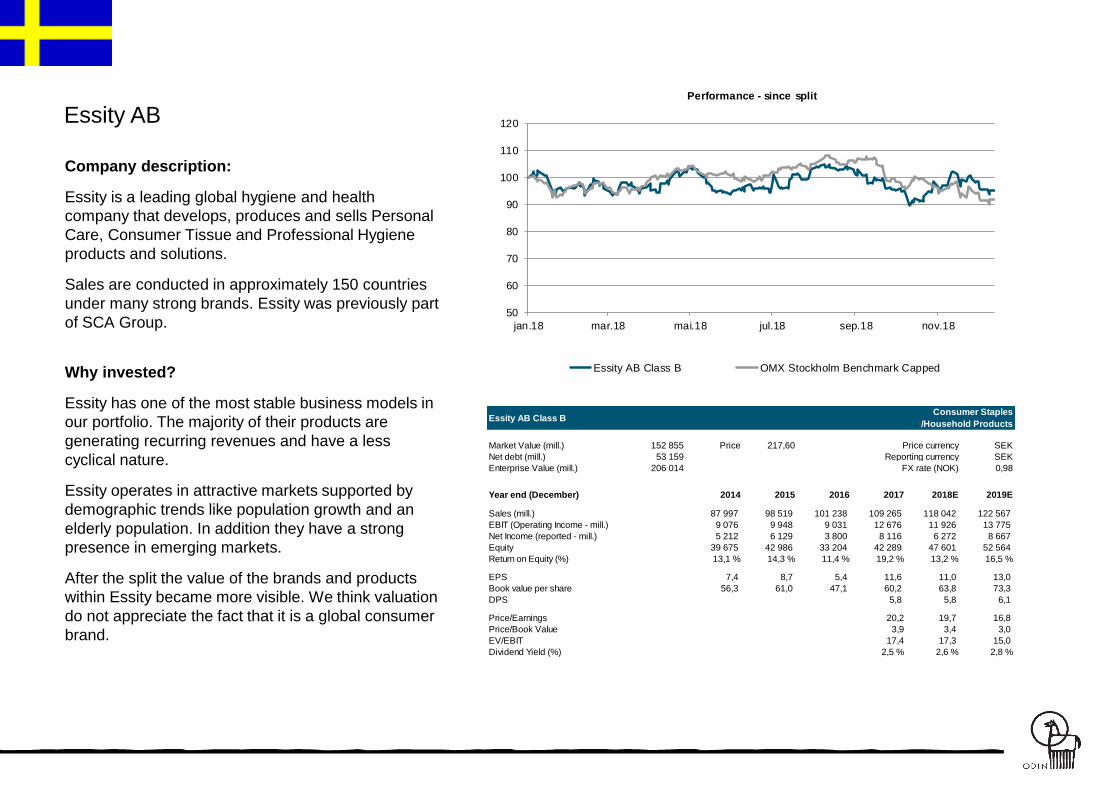

Essity AB

Company description:

Essity is a leading global hygiene and health

company that develops, produces and sells Personal

Care, Consumer Tissue and Professional Hygiene

products and solutions.

Sales are conducted in approximately 150 countries

under many strong brands. Essity was previously part

of SCA Group.

Why invested?

Essity has one of the most stable business models in

our portfolio. The majority of their products are

generating recurring revenues and have a less

cyclical nature.

Essity operates in attractive markets supported by

demographic trends like population growth and an

elderly population. In addition they have a strong

presence in emerging markets.

After the split the value of the brands and products

within Essity became more visible. We think valuation

do not appreciate the fact that it is a global consumer

brand.

Market Value (mill.) 152 855 Price 217,60 SEK

Net debt (mill.) 53 159 SEK

Enterprise Value (mill.) 206 014 0,98

Year end (December) #N/A 2014 2015 2016 2017 2018E 2019E

Sales (mill.) #VALUE! 87 997 98 519 101 238 109 265 118 042 122 567

EBIT (Operating Income - mill.) #VALUE! 9 076 9 948 9 031 12 676 11 926 13 775

Net Income (reported - mill.) #VALUE! 5 212 6 129 3 800 8 116 6 272 8 667

Equity #VALUE! 39 675 42 986 33 204 42 289 47 601 52 564

Return on Equity (%) #VALUE! 13,1 % 14,3 % 11,4 % 19,2 % 13,2 % 16,5 %

EPS #VALUE! 7,4 8,7 5,4 11,6 11,0 13,0

Book value per share #VALUE! 56,3 61,0 47,1 60,2 63,8 73,3

DPS #VALUE! #N/A #N/A #N/A 5,8 5,8 6,1

Price/Earnings #VALUE! #N/A #N/A #N/A 20,2 19,7 16,8

Price/Book Value #VALUE! #N/A #N/A #N/A 3,9 3,4 3,0

EV/EBIT #VALUE! - - - 17,4 17,3 15,0

Dividend Yield (%) #VALUE! #N/A #N/A #N/A 2,5 % 2,6 % 2,8 %

Essity AB Class BConsumer Staples

/Household Products

Price currency

Reporting currency

FX rate (NOK)

50

60

70

80

90

100

110

120

jan.18 mar.18 mai.18 jul.18 sep.18 nov.18

Performance - since split

Essity AB Class B OMX Stockholm Benchmark Capped

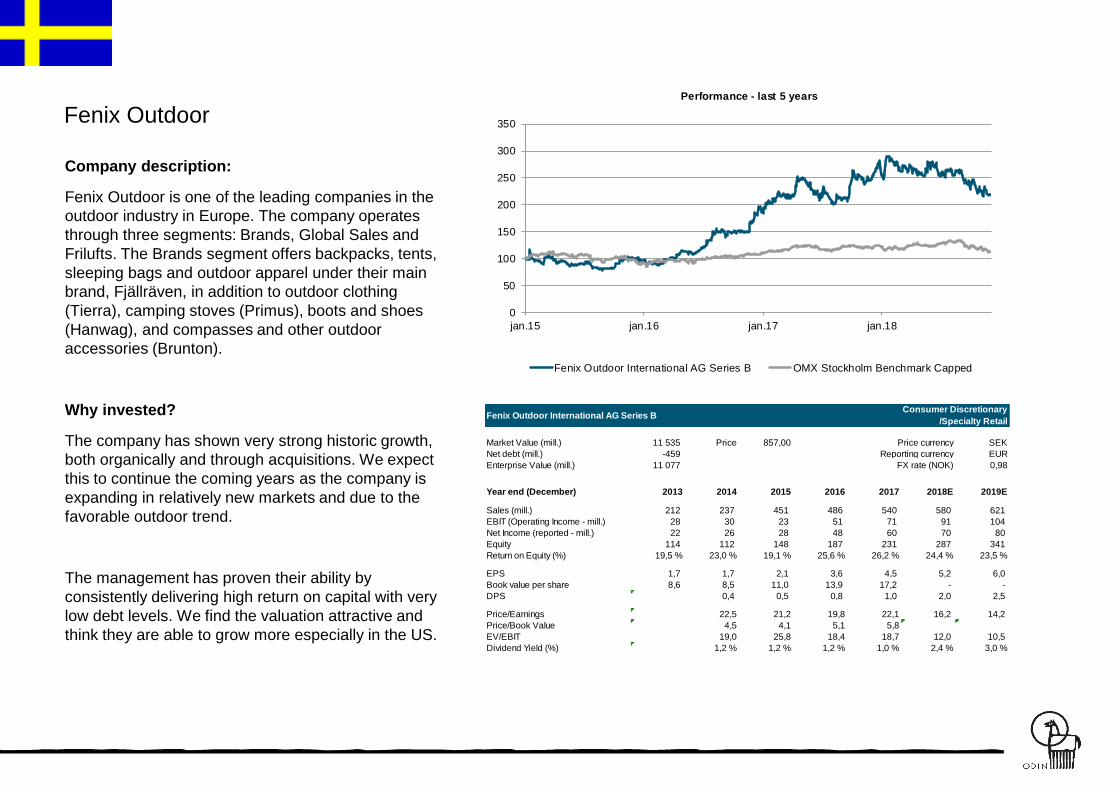

Fenix Outdoor

Company description:

Fenix Outdoor is one of the leading companies in the

outdoor industry in Europe. The company operates

through three segments: Brands, Global Sales and

Frilufts. The Brands segment offers backpacks, tents,

sleeping bags and outdoor apparel under their main

brand, Fjällräven, in addition to outdoor clothing

(Tierra), camping stoves (Primus), boots and shoes

(Hanwag), and compasses and other outdoor

accessories (Brunton).

Why invested?

The company has shown very strong historic growth,

both organically and through acquisitions. We expect

this to continue the coming years as the company is

expanding in relatively new markets and due to the

favorable outdoor trend.

The management has proven their ability by

consistently delivering high return on capital with very

low debt levels. We find the valuation attractive and

think they are able to grow more especially in the US.

Market Value (mill.) 11 535 Price 857,00 SEK

Net debt (mill.) -459 EUR

Enterprise Value (mill.) 11 077 0,98

Year end (December) 2013 2014 2015 2016 2017 2018E 2019E

Sales (mill.) 212 237 451 486 540 580 621

EBIT (Operating Income - mill.) 28 30 23 51 71 91 104

Net Income (reported - mill.) 22 26 28 48 60 70 80

Equity 114 112 148 187 231 287 341

Return on Equity (%) 19,5 % 23,0 % 19,1 % 25,6 % 26,2 % 24,4 % 23,5 %

EPS 1,7 1,7 2,1 3,6 4,5 5,2 6,0

Book value per share 8,6 8,5 11,0 13,9 17,2 - -

DPS #N/A 0,4 0,5 0,8 1,0 2,0 2,5

Price/Earnings #N/A 22,5 21,2 19,8 22,1 16,2 14,2

Price/Book Value #N/A 4,5 4,1 5,1 5,8 #VALUE! #VALUE!

EV/EBIT - 19,0 25,8 18,4 18,7 12,0 10,5

Dividend Yield (%) #N/A 1,2 % 1,2 % 1,2 % 1,0 % 2,4 % 3,0 %

Fenix Outdoor International AG Series BConsumer Discretionary

/Specialty Retail

Price currency

Reporting currency

FX rate (NOK)

0

50

100

150

200

250

300

350

jan.15 jan.16 jan.17 jan.18

Performance - last 5 years

Fenix Outdoor International AG Series B OMX Stockholm Benchmark Capped

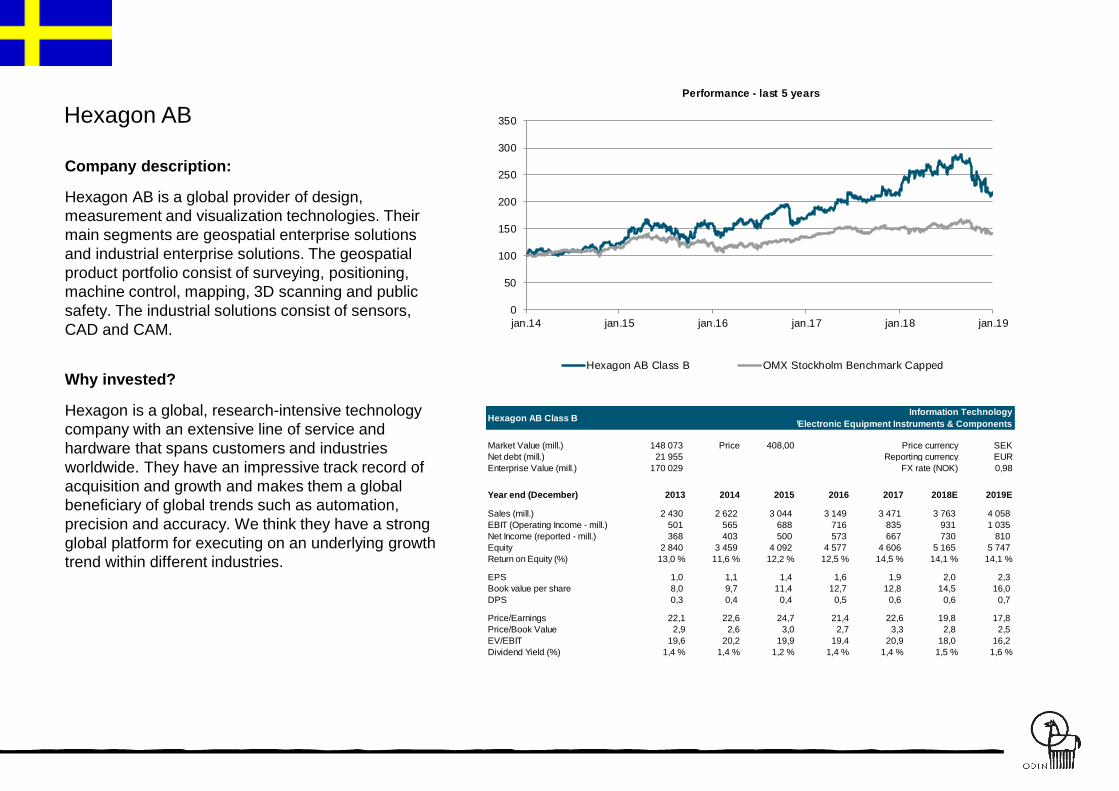

Hexagon AB

Company description:

Hexagon AB is a global provider of design,

measurement and visualization technologies. Their

main segments are geospatial enterprise solutions

and industrial enterprise solutions. The geospatial

product portfolio consist of surveying, positioning,

machine control, mapping, 3D scanning and public

safety. The industrial solutions consist of sensors,

CAD and CAM.

Why invested?

Hexagon is a global, research-intensive technology

company with an extensive line of service and

hardware that spans customers and industries

worldwide. They have an impressive track record of

acquisition and growth and makes them a global

beneficiary of global trends such as automation,

precision and accuracy. We think they have a strong

global platform for executing on an underlying growth

trend within different industries.

0

50

100

150

200

250

300

350

jan.14 jan.15 jan.16 jan.17 jan.18 jan.19

Performance - last 5 years

Hexagon AB Class B OMX Stockholm Benchmark Capped

Market Value (mill.) 148 073 Price 408,00 SEK

Net debt (mill.) 21 955 EUR

Enterprise Value (mill.) 170 029 0,98

Year end (December) 2013 2014 2015 2016 2017 2018E 2019E

Sales (mill.) 2 430 2 622 3 044 3 149 3 471 3 763 4 058

EBIT (Operating Income - mill.) 501 565 688 716 835 931 1 035

Net Income (reported - mill.) 368 403 500 573 667 730 810

Equity 2 840 3 459 4 092 4 577 4 606 5 165 5 747

Return on Equity (%) 13,0 % 11,6 % 12,2 % 12,5 % 14,5 % 14,1 % 14,1 %

EPS 1,0 1,1 1,4 1,6 1,9 2,0 2,3

Book value per share 8,0 9,7 11,4 12,7 12,8 14,5 16,0

DPS 0,3 0,4 0,4 0,5 0,6 0,6 0,7

Price/Earnings 22,1 22,6 24,7 21,4 22,6 19,8 17,8

Price/Book Value 2,9 2,6 3,0 2,7 3,3 2,8 2,5

EV/EBIT 19,6 20,2 19,9 19,4 20,9 18,0 16,2

Dividend Yield (%) 1,4 % 1,4 % 1,2 % 1,4 % 1,4 % 1,5 % 1,6 %

Hexagon AB Class BInformation Technology

/Electronic Equipment Instruments & Components

Price currency

Reporting currency

FX rate (NOK)

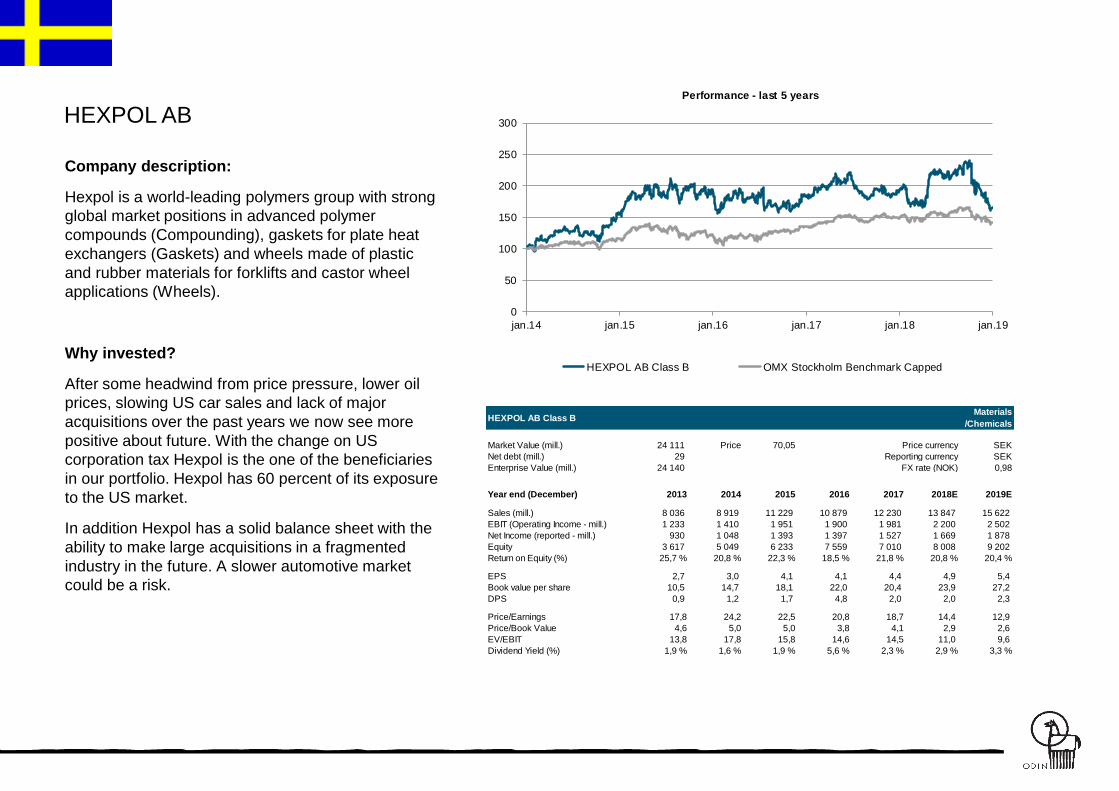

HEXPOL AB

Company description:

Hexpol is a world-leading polymers group with strong

global market positions in advanced polymer

compounds (Compounding), gaskets for plate heat

exchangers (Gaskets) and wheels made of plastic

and rubber materials for forklifts and castor wheel

applications (Wheels).

Why invested?

After some headwind from price pressure, lower oil

prices, slowing US car sales and lack of major

acquisitions over the past years we now see more

positive about future. With the change on US

corporation tax Hexpol is the one of the beneficiaries

in our portfolio. Hexpol has 60 percent of its exposure

to the US market.

In addition Hexpol has a solid balance sheet with the

ability to make large acquisitions in a fragmented

industry in the future. A slower automotive market

could be a risk.

Market Value (mill.) 24 111 Price 70,05 SEK

Net debt (mill.) 29 SEK

Enterprise Value (mill.) 24 140 0,98

Year end (December) 2013 2014 2015 2016 2017 2018E 2019E

Sales (mill.) 8 036 8 919 11 229 10 879 12 230 13 847 15 622

EBIT (Operating Income - mill.) 1 233 1 410 1 951 1 900 1 981 2 200 2 502

Net Income (reported - mill.) 930 1 048 1 393 1 397 1 527 1 669 1 878

Equity 3 617 5 049 6 233 7 559 7 010 8 008 9 202

Return on Equity (%) 25,7 % 20,8 % 22,3 % 18,5 % 21,8 % 20,8 % 20,4 %

EPS 2,7 3,0 4,1 4,1 4,4 4,9 5,4

Book value per share 10,5 14,7 18,1 22,0 20,4 23,9 27,2

DPS 0,9 1,2 1,7 4,8 2,0 2,0 2,3

Price/Earnings 17,8 24,2 22,5 20,8 18,7 14,4 12,9

Price/Book Value 4,6 5,0 5,0 3,8 4,1 2,9 2,6

EV/EBIT 13,8 17,8 15,8 14,6 14,5 11,0 9,6

Dividend Yield (%) 1,9 % 1,6 % 1,9 % 5,6 % 2,3 % 2,9 % 3,3 %

HEXPOL AB Class BMaterials

/Chemicals

Price currency

Reporting currency

FX rate (NOK)

0

50

100

150

200

250

300

jan.14 jan.15 jan.16 jan.17 jan.18 jan.19

Performance - last 5 years

HEXPOL AB Class B OMX Stockholm Benchmark Capped

Hoist Finance

Company description:

Hoist Finance (HOFI) is pan-European debt

purchaser focusing on unsecured and secured

consumer NPL market. The company has currently

operations in 11 European countries with and 1,335

FTEs at the end of 2017.

Why invested?

The company has a cost cutting program which

together with scale advantages will lower the C/I

significantly from ~80% to below 70%. We believe

management will be successful executing on its

current strategy which could potentially more than

double the value of the shareprice in the coming

years. A better more disciplined market behavior is

also positive for Hoist.

We consider its status as a Credit Market Company

to be a key competitive advantage, as certain claims

sold by banks are required to be handled by financial

institutions. It furthermore enables a higher leverage

at lower funding costs than peers. The flipside of it is

the regulation risk which we saw an example of in the

end of the year. Despite this we think they could

deliver on both cost and growth going forward.

0

20

40

60

80

100

120

140

160

180

jul.15 jul.16 jul.17 jul.18

Performance - last 5 years

Hoist Finance AB OMX Stockholm Benchmark Capped

Market Value (mill.) 3 853 Price 43,15 SEK

Net debt (mill.) 6 871 SEK

Enterprise Value (mill.) 10 724 0,98

2013 2014 2015 2016 2017

Year end (December) 2013 2014 2015 2016 2017 2018E 2019E

Total Income - 1 660 2 247 2 627 2 806 2 978 3 367

Net Interest Income - - 1 646 - - 2 470 3 045

Net Result 94 155 219 401 412 587 760

Equity 815 1 397 2 289 2 925 3 228 4 452 4 908

Return on Equity (%) 11,5 % 11,1 % 9,6 % 13,7 % 12,8 % 13,2 % 15,5 %

EPS 6,1 9,2 2,9 5,1 5,1 6,4 7,7

Book value per share 10,3 17,6 29,1 36,2 39,8 51,7 56,4

DPS #N/A #N/A 0,8 1,3 1,9 2,1 2,5

Price/Earnings #N/A #N/A 30,5 16,7 18,1 6,8 5,6

Price/Book Value 0,0 0,0 0,0 0,0 0,0 0,8 0,8

Dividend Yield (%) #N/A #N/A 0,8 % 1,5 % 2,1 % 4,8 % 5,8 %

Hoist Finance ABFinancials

/Consumer Finance

Price currency

Reporting currency

FX rate (NOK)

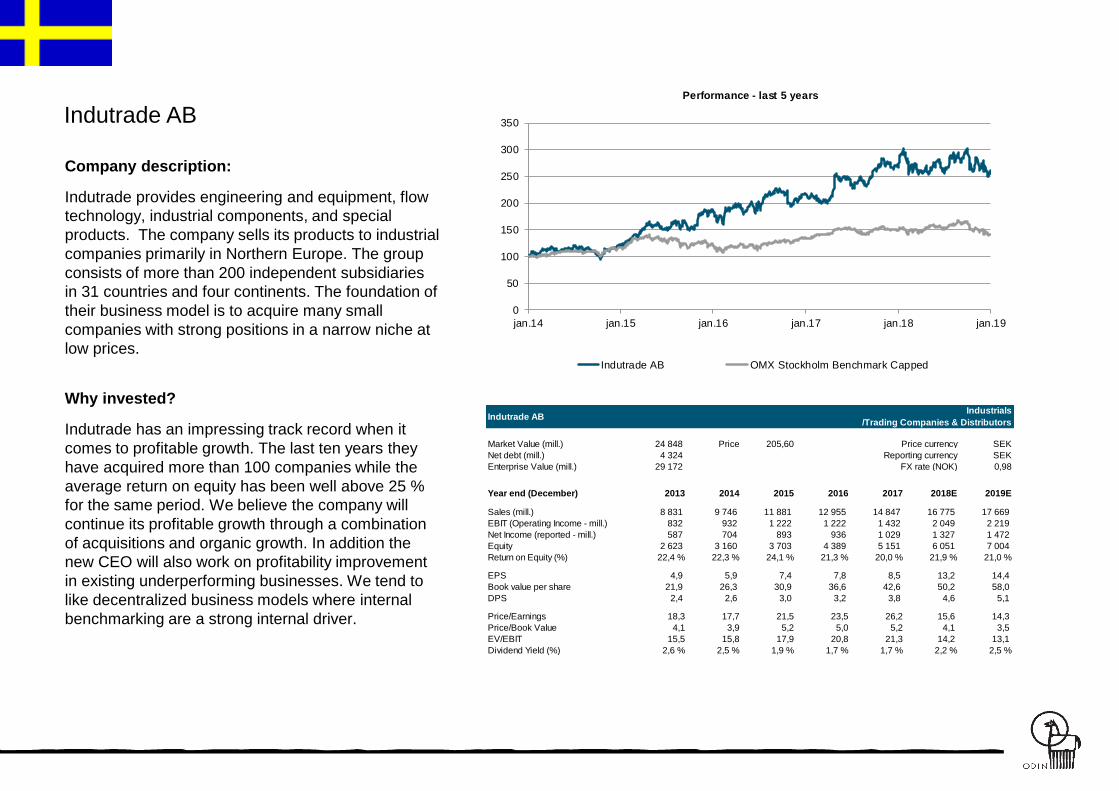

Indutrade AB

Company description:

Indutrade provides engineering and equipment, flow

technology, industrial components, and special

products. The company sells its products to industrial

companies primarily in Northern Europe. The group

consists of more than 200 independent subsidiaries

in 31 countries and four continents. The foundation of

their business model is to acquire many small

companies with strong positions in a narrow niche at

low prices.

Why invested?

Indutrade has an impressing track record when it

comes to profitable growth. The last ten years they

have acquired more than 100 companies while the

average return on equity has been well above 25 %

for the same period. We believe the company will

continue its profitable growth through a combination

of acquisitions and organic growth. In addition the

new CEO will also work on profitability improvement

in existing underperforming businesses. We tend to

like decentralized business models where internal

benchmarking are a strong internal driver.

Market Value (mill.) 24 848 Price 205,60 SEK

Net debt (mill.) 4 324 SEK

Enterprise Value (mill.) 29 172 0,98

Year end (December) 2013 2014 2015 2016 2017 2018E 2019E