Embed Size (px)

Citation preview

1

Lecture 1: Intro © Niels Peter Hahnemann 2011 1

• LECTURE ONE • 1) Purpose and scope of the lectures • 2) Reading list • 3) Intro to the main ideas of the lectures • 4) Plan and overview • 5) A crash course in the philosophy of

science for economists

Lectures in the history of economic thought

Lecture 1: Intro © Niels Peter Hahnemann 2011 2

• PURPOSE AND SCOPE • To familiarise students with the historical precursors of

contemporary economic theory • To give students a deeper understanding of theory’s

capability to unravel political and social problems • The lectures span the period from the foundation of

economics as a science by A. Smith to the first comprehensive macroeconomic theory by J. M. Keynes

• Economic theory: cumulation of ideas, so why not study the latest textbook only?

• Economic theory: a reflection of society and history, so why not study economic history only?

• Because there exists no model for a true consistent theory with which to assess theory =>

• Economics is about decisions that organise society in a certain manner ≡ no overall rational subject or guide

History of economic thought

Lecture 1: Intro © Niels Peter Hahnemann 2011 3

• In the footsteps of Enlightenment philosophy: using markets in a reasonable as opposed to traditional a priori given organisation of human interaction

• Necessitates construction of a theory that goes from description and intuition to science and rationality

• Goal 1: to explain modes of thought and reasoning by the great economists => to understand the enormous complexity of the subject matter of economics

• Goal 2: to see the mistakes or roads not taken by economists in the history of economic thought => to acknowledge the need for carefulness and caveats

• Curriculum: Mark Blaug (1997), Economic theory in retrospect; Adam Smith (1776), The wealth of nations; David Ricardo (1817), On the principles of political economy and taxation; Karl Marx (1867), Capital; John Maynard Keynes (1936), The general theory of employment, interest and money

History of economic thought

Lecture 1: Intro © Niels Peter Hahnemann 2011 4

• INTRO TO MAIN IDEAS • Economics: from technique to science • From instrument in the organisation of

society, to knowledge about the economic organisation of society

• From Quesnay + Smith, to Nash + Romer • Economics as technique => a reasonable

arrangement of social relations • From ”tradition, power, and feudalism”, to

”prices, profit, and capitalism”

History of economic thought

Lecture 1: Intro © Niels Peter Hahnemann 2011 5

• Economics as science => a reasonable arrangement of theory

• From description and intuition, to scientific interest i.e. an understanding of society’s economic organisation

• Aim of scientific economics: knowledge based on reason and argumentation, decision-making according to truth concept

• Terms of scientific economics: axioms, computability, proof of existence, determination of equilibrium

History of economic thought

Lecture 1: Intro © Niels Peter Hahnemann 2011 6

• Economics = practical ethics: decisions that organise society according to purpose

• Decision making: what is right, what is wrong => ethics, moral actions

• 1) Consequentialism, utilitarianism: only consequences count => economics

• 2) Deontology, categorical imperative: “duty is my command” => politics

• Economics: calculating the effects of actions, the good comes with some bad

• => ”Trade-off”: things seen in perspective

History of economic thought

2

Lecture 1: Intro © Niels Peter Hahnemann 2011 7

• Sketch of theory’s historical origins • Classical economists founded economics

as a science in mid-to-end 18th century • Contemporary historical events: American

independence, French revolution, Enlightenment philosophy, economic industrialisation

• Idea about rational organisation of society inspired by the world view of emerging (natural) science

• “Rational organisation” => calculation i.e. putting number (price) on decisions

History of economic thought

Lecture 1: Intro © Niels Peter Hahnemann 2011 8

• Difficult: 1) Limited market price formation in domestic (national) economy

• Short term market price determined only accidentally by supply and demand

• Long term price determined by supply side production costs only

• 2) But international price formation more market orientated:

• Demand mechanism effective in long run through “comparative advantage” =>

• 1)+2) = Very rudimentary equilibrium of trade determined far away from “home”

History of economic thought

Lecture 1: Intro © Niels Peter Hahnemann 2011 9

• Facts: full currency convertibility on world markets only, not domestically

• Domestic economy underdeveloped, few markets, many taxes and tolls =>

• No demand function in classics, comes 100 years later with the marginalists

• No aggregation, comes 150 years after with J. M. Keynes and national accounts

• 3) Aggregated price formation i.e. with prices and quantities = modern macro: international model turned national by quantity equation, money demand, etc.

History of economic thought

Lecture 1: Intro © Niels Peter Hahnemann 2011 10

• PLAN OF THE LECTURES • Lecture 1: Intro and ”crash course” • Lecture 2: Mercantilists and physiocrats (Blaug: chapter 1) • Lecture 3: Adam Smith and Wealth of Nations (Blaug: chapter 2, Smith:

volume 1, book 1, chapters 1-10 incl.) • Lecture 4: Thomas Malthus, population growth, returns (Blaug: chapter 3) • Lecture 5: David Ricardo and Principles (Blaug: chapter 4, Ricardo:

chapters I-VII incl. and XXX) • Lecture 6: Say’s law, classical monetary theory, and John Stuart Mill (Blaug:

chapters 5+6) • Lecture 7: Karl Marx and Das Kapital (Blaug: chapter 7, Marx: chapters in

English version 1+4+5+6+7+8+9) • Lecture 8: The marginalists (Blaug: chapter 8+9) • Lecture 9: Alfred Marshall (Blaug: chapter 15) • Lecture 10: General equilibrium and welfare: Walras and Pareto (Blaug:

chapter 13) • Lecture 11: Wicksell and the neoclassics (Blaug: chapter 15) • Lecture 12: John Maynard Keynes and General Theory (Blaug: chapter 16,

Keynes: chapters 1-13 incl. and 23-24) • Lecture 13: The aftermath. Foundations of modern economics

History of economic thought

Lecture 1: Intro © Niels Peter Hahnemann 2011 11

• CRASH COURSE IN THE PHILOSOPHY OF SCIENCE FOR ECONOMISTS

• Enlightenment and the scientific worldview • R. Descartes (1637): science

necessitates truth concept: • Doing the reasonable, arguing the right,

surmounting tradition-history-power • Can science be objective? Are there

special interests related to science? • Epistemology: theory about knowledge • Cannot do history of economic thought

without philosophy of science Lecture 1: Intro © Niels Peter Hahnemann 2011 12

Philosophy of science for economists

• Philosophy of science learns from science • Not a science, can never be a science • Phil. of sc. ≠ methodology where science

learns from philosophy • Phil. of sc. ≠ purely normative theory that

guides choices researchers need to take • Illuminates the reasoning and choices

made in any science • Illuminates battle between different

theories and shifts of focus in research • Reveals relation between science, history,

society and, thus, politics in theory

3

Lecture 1: Intro © Niels Peter Hahnemann 2011 13

Philosophy of science for economists

• Historically, 3 main schools or trends in the philosophy of science:

• 1) Inductivism, positivism • 2) Falsificationism, critical rationalism • 3) Methodological realism, pragmatism

2 world wars ”1968” “1789”

Inductivism

Falsificationism

Pragmatism

Where are we today?

“End of history”

Descartes, Hume Popper, Lakatos Foucault, Habermas

Timeline of methodological breakthroughs

Lecture 1: Intro © Niels Peter Hahnemann 2011 14

• Inductivism/positivism: build laws from observation

• Classical and modern economics: A. Smith pin factory example, standard procedure of econometrics today: we cannot reject (with a certain degree of confidence) = double negation, verification

• Rationalism/falsificationism: purely logical procedure => axiomatisation; “Bourbakism” as in neoclassical general equilibrium; heterodox economics

• Realism/pragmatism: economics as part of society, history and politics; K. Marx

Philosophy of science for economists

Lecture 1: Intro © Niels Peter Hahnemann 2011 15

• High point of philosophy of science in the 1970s, now more neglected (pragmatic)

• 3 schools only according to a very “broad brush”, in effect many overlaps and combinations between schools

• A more subdued issue today, but still relevant

• Most economists are (without knowing it) “spontaneous” inductivists + positivists

• 1) INDUCTIVISM and POSITIVISM • 1a) Inductivism: justification, verification

Philosophy of science for economists

Lecture 1: Intro © Niels Peter Hahnemann 2011 16

• Connection between science and the organisation of society from beginning of renaissance and the enlightenment project

• The scientific world view: Gallilei, Newton • Logic of discovery: how to find knowledge • General law on the basis of observations • Justificationism: prove validity of statement • Derived and non-derived statements: how

to justify the non-derived? • Verification = confirmation by evidence • Statements derived from experience =

unreflecting knowledge, a posteriori

Philosophy of science for economists

Lecture 1: Intro © Niels Peter Hahnemann 2011 17

• Inference from all events of a certain kind, to universal statements

• Data, or empirical evidence = statements of observation = singular statements

• Adjust observation for subjective content • Subjective = cannot be discussed • Objective = can be discussed • Generalisation based on assurances from:

1) many observations, 2) different obs. conditions, same result, 3) no single obs. contradicts general law

• Are observations theory-independent?

Philosophy of science for economists

Lecture 1: Intro © Niels Peter Hahnemann 2011 18

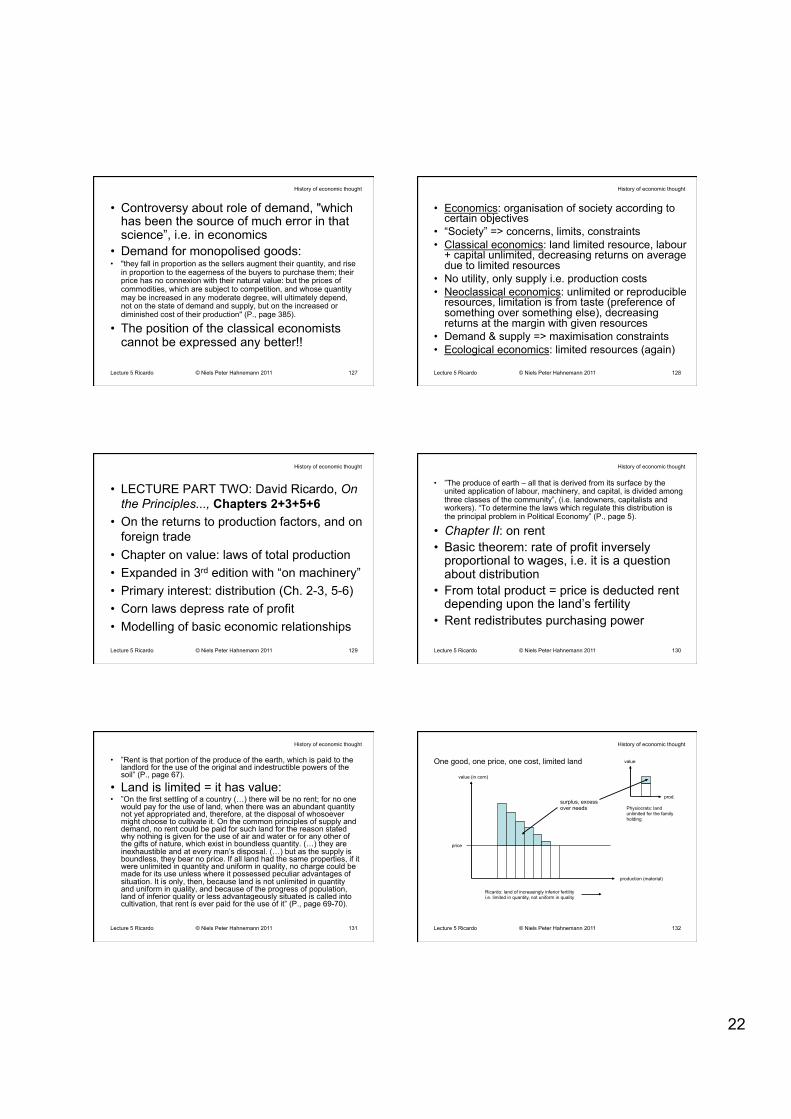

• Verification = modus ponens, i.e. THEOREM: if “A1 is B”, “A2 is B”, ..., “An is B” → then “all A are B” is true

• Conclusion, “all swans are white”, could be false even though the premise, “so far all observed swans are white”, is true => no logical contradiction between affirming premise and denying conclusion

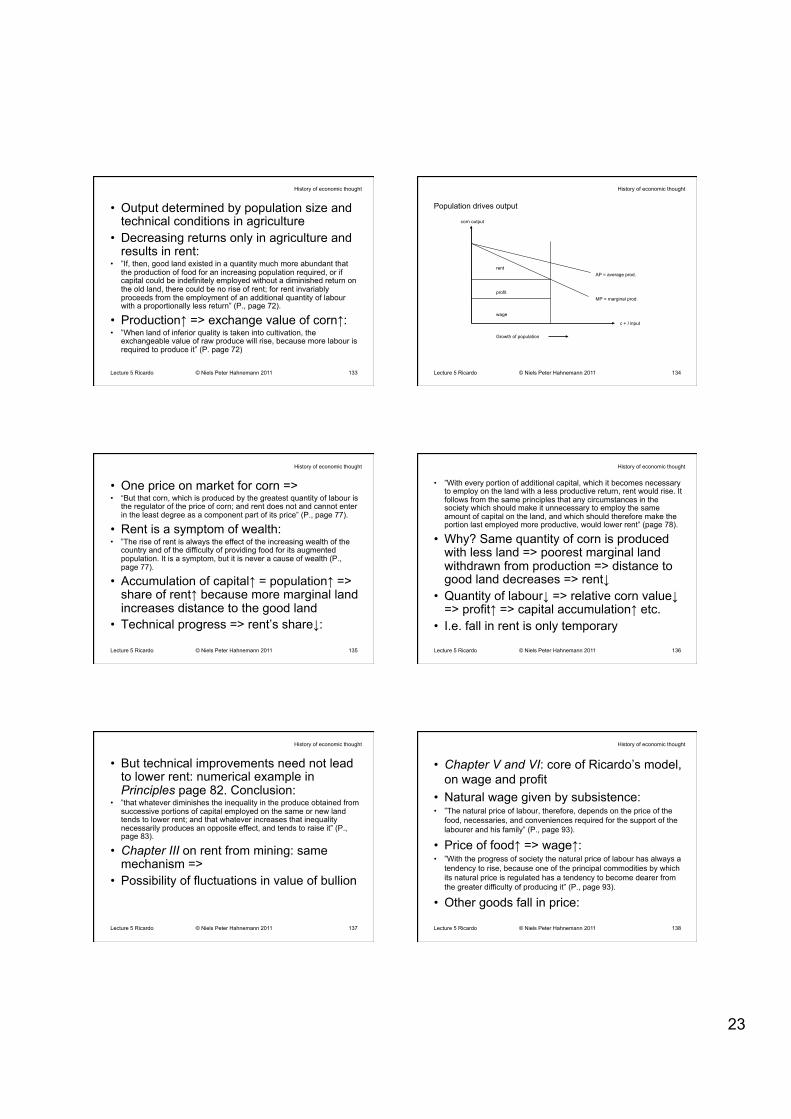

• Thus, modus ponens not logically binding • Verification ≈ jump from “particular” to “all”,

equivalent to bet based on assurances of non-arrival of a “black swan”

Philosophy of science for economists

4

Lecture 1: Intro © Niels Peter Hahnemann 2011 19

• Problem of induction: confirming induction with induction not logically tenable

• Furthermore: probability that a universal theory is true goes to zero with increasing number of observations

• D. Hume (1739): acknowledged problem of induction => scientific knowledge based on assurances, not logic ≡ inductivism

• 1b) Positivism (20th century): inductivism fortified with logical empiricism

• Testable observations: experiments, no metaphysics

Philosophy of science for economists

Lecture 1: Intro © Niels Peter Hahnemann 2011 20

• Science ≠ pseudo science • Verification: theory is positive about what

is, not normative about what ought to be • Synthetic statements only = empirical

generalisations i.e. modus ponens => still problem of induction

• Terms or concepts that cannot be verified (e.g. “atoms” or “utility”) are not allowed

• Operationalism: concepts = procedures for measurement, e.g. temperature = thermometer; pseudo science = no existing measurement procedures

Philosophy of science for economists

Lecture 1: Intro © Niels Peter Hahnemann 2011 21

• Descriptivism: science should describe rather than explain

• Reductionism: complexity reduced to more simple relations e.g. social relations to individual problems or even chemistry

• Immunisations such as (non-testable) ceteris paribus clauses not allowed; but is that possible?

• Covering law # 1: differentiation between explained (explicandum e.g. raindrops) and explaining (explicans i.e. the general law e.g. the depression to which explicandum is subjected)

Philosophy of science for economists

Lecture 1: Intro © Niels Peter Hahnemann 2011 22

• Important: explicandum and explicans must be independent, but can they really?

• The symmetry thesis: explanation and prediction have same logical structure

• Explanation = explicandum known, explicans unknown; prediction = explicans known, explicandum unknown

• M. Friedman (1953): moderate empiricism, positivism

• Increasingly good predictions => positive not normative science, realism of model less important (“as if”), only prediction counts (instrumentalism)

Philosophy of science for economists

Lecture 1: Intro © Niels Peter Hahnemann 2011 23

• 2) FALSIFICATIONISM and CRITICAL RATIONALISM

• 2a) Falsificationism (1940-50s): fallibilism is the opposite of justificationism (once confirmed, always confirmed) i.e. all theories are hypothetical and subject to eventual correction

• Logical impossibility of justifying a theory as true (Münchausen’s trilemma) => justificationism is self-contradictory

• Rationalism: knowledge is given a priori i.e. by reason (the human intellect)

Philosophy of science for economists

Lecture 1: Intro © Niels Peter Hahnemann 2011 24

• Verstand vs. Vernunft (Kant + Hegel) • Reasoning based on logical deductions =>

deductivism: the opposite of inductivism • Interest in logic of confirmation i.e. the

foundations of knowledge (as opposed to logic of discovery = how to get knowledge)

• K. Popper: the asymmetry thesis = modus ponens not valid, modus tollens valid

• Modus tollens i.e. THEOREM: if “An+1 is not B” → then “all A are B” is false

Philosophy of science for economists

5

Lecture 1: Intro © Niels Peter Hahnemann 2011 25

• Pure logic: observation of one black swan falsifies view that all swans are white

• Empirical tests + error correction => truth contents of theory gradually increase

• Science ≡ falsifiable => perpetual potential conflict with empirical data

• “Dogmatic falsificationism” = “Popper(0)”: we must reject all theories that cannot withstand falsification

• Ignores that falsification itself is fallible => impossible to show theory is absolutely false => risk of rejecting true, accepting false theory

Philosophy of science for economists

Lecture 1: Intro © Niels Peter Hahnemann 2011 26

• “Naive falsificationism” = “Popper(1)”: we need methodological rules for falsification

• Recognises that falsification does not imply that a theory is false with certainty =>

• Non-falsifiable ad hoc assumption support (e.g. ceteris paribus) necessary for any theory, but we must have rules for this

• Only reject theory, not data; testable ad hoc assumptions; ceteris paribus must not decrease theory’s falsifiability

• Pass falsification tests => “corroboration”↑

Philosophy of science for economists

Lecture 1: Intro © Niels Peter Hahnemann 2011 27

• Falsified theories i.e. false “explicans” must be rejected

• But: necessary to maintain some false assumptions (theories) even though we know they are false

• Because: we know something is wrong, but we do not know exactly where problem is (Duhem-Quine)

• E.g. the principle of rationality is obviously false (people do not always act rationally)

• If “rationality” is in explicans => no liberty, human behaviour fully determined

Philosophy of science for economists

Lecture 1: Intro © Niels Peter Hahnemann 2011 28

• Conclusion: “rationality” must be removed from explicans = covering law # 2

• Symmetry thesis only partly valid for social science and economics =>

• “Popper(2)”: theories must be maintained or rejected in their totality only =

• I. Lakatos: “sofisticated falsificationism”, new theory is better if more falsifiable => concept of “scientific progress”

• Exclude possible events (observations) = make better predictions

Philosophy of science for economists

Lecture 1: Intro © Niels Peter Hahnemann 2011 29

• 2b) Research programmes (1960s-70s) ≈ “Popper(2)” in a dynamical context

• Theories can only be assessed in their totality (weak version of Duhem-Quine)

• Hard core: never subject to falsification, modus tollens prohibited here (e.g. utility and profit maximisation)

• Protective belt: auxiliary hypotheses subject to falsification (e.g. decreasing returns, convexity)

• Heuristics: common rules, approaches (e.g. exogenous/endogenous)

Philosophy of science for economists

Lecture 1: Intro © Niels Peter Hahnemann 2011 30

• Progressive research programmes: increase in theory’s informative contents

• Theoretical progressivity: capacity to incorporate novel facts i.e. adapt to new information that was not predictable with existing theory

• Empirical progressivity: existing theory’s capacity to predict

• Progressivity => new hypotheses incorporated in protective belt

• Degenerating r.p. ≡ not progressive r.p.

Philosophy of science for economists

6

Lecture 1: Intro © Niels Peter Hahnemann 2011 31

• Lakatos: try to produce rational concept about progress in science and objectively distinguish between productive and non-productive research

• But: that decision is never final => • Impossible to rationally assess theories

(strong version of Duhem-Quine) • Empiricism and falsificationism unrealistic:

social, historical, psychological, political factors also important =>

Philosophy of science for economists

Lecture 1: Intro © Niels Peter Hahnemann 2011 32

• 2c) T. Kuhn: Scientific paradigms (1950s-60s) i.e. commonly accepted fundamentals of “normal” science, not necessarily fully rational

• Scientific revolutions rare • Different paradigms are not on speaking

terms (basis not fully rational), tend to battle, only one becomes predominant

• Research communication tends to stay within paradigm, conclusions of normal science known in advance

Philosophy of science for economists

Lecture 1: Intro © Niels Peter Hahnemann 2011 33

• Agreement within paradigm on the matrix of the scientific discipline i.e. on:

• Symbolic generalisations = what are the basic non-falsifiable theoretical laws

• Basic models for explanation of empirical phenomena

• Common values for what is good theory • Shared metaphysics (do’s and don’ts in

research) • Exemplars = implicit rules derived from

examples, e.g. apple falling from tree

Philosophy of science for economists

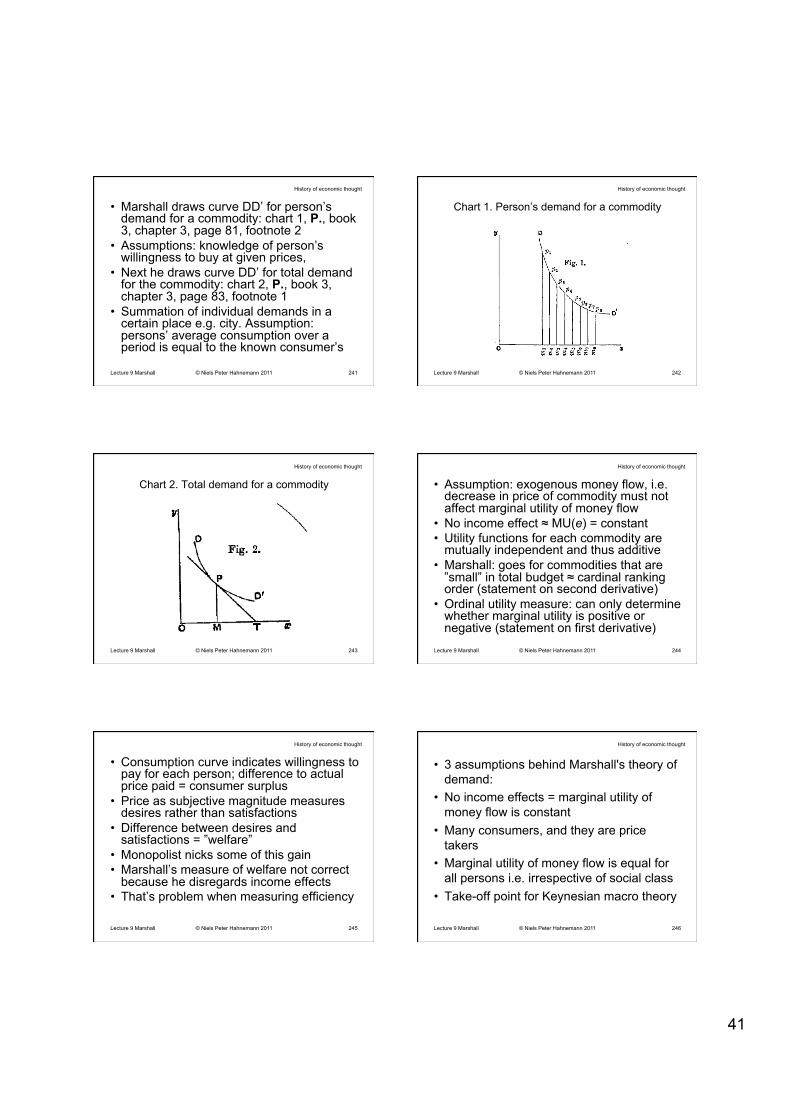

Lecture 1: Intro © Niels Peter Hahnemann 2011 34

• Anomalies that cannot be solved within existing paradigm

• Many anomalies => crisis for science => competing paradigms, incommensurability

• No rational test exists for deciding which paradigm is best + cannot be done independently of a paradigm =>

• Either: existing paradigm survives crisis, anomalies are reduced to puzzles

• Or: scientific revolution (paradigm shift) that explains anomalies

Philosophy of science for economists

Lecture 1: Intro © Niels Peter Hahnemann 2011 35

• New paradigm becomes predominant • No rational basis for the paradigm shift,

can also decrease knowledge as in politically or religiously motivated shifts

• Choice between theories not a purely logical internal matter

• Shifts => loss of problem solving capacity, different paradigms solve diff. problems

• Still: empirical success criteria for scientific progress, but more pragmatic, realistic

Philosophy of science for economists

Lecture 1: Intro © Niels Peter Hahnemann 2011 36

• 3) REALISM, PRAGMATISM (1980s) • Expands on Kuhn (as in 2c above) • Differentiate between good/bad science,

not between science/pseudo-science • Different theories do not have the same

structure of explanation • Covering law is a logical relation e.g. about

empirical regularities and covariation, does not reflect necessity

• Causality = mechanism that relates cause and effect

Philosophy of science for economists

7

Lecture 1: Intro © Niels Peter Hahnemann 2011 37

• Explanation = causal relation in reality, can only accept locality not action at a distance e.g. “gravity“ or “invisible hand”

• Locality = with space and time coordinates • But: we cannot do physics without

assumptions about gravity (Einstein did not succeed in explaining gravity); we cannot do economics without assumption about invisible hand such as diminishing returns (we have problems in explaining and predicting market equilibrium) =>

• Open system ontology: theory about being and reality (as opposed to epistemology)

Philosophy of science for economists

Lecture 1: Intro © Niels Peter Hahnemann 2011 38

• Reality exists independently of observation (not a logical relation i.e. ≠ covering law) => knowledge is necessarily imperfect = pragmatism

• Closure: theory must be as consistent and unequivocal as possible, necessary for understanding, but an economy is an open universe =>

• Knowledge is always part of a discourse (as in rhetoric) => pluralism

• Knowledge is about reality not about logic

Philosophy of science for economists

Lecture 1: Intro © Niels Peter Hahnemann 2011 39

• SUMMARY • 1) Positivism • Inductivism, logical empiricism, verification

or confirmation: modern philosophy of science

• Problem of induction ≈ circular reasoning => need for empirical success

• Justificationism, logic of scientific discovery knowledge is a posteriori (given through experience), modus ponens

• Covering law #1, symmetry thesis

Philosophy of science for economists

Lecture 1: Intro © Niels Peter Hahnemann 2011 40

• Moderate empiricism mrk.1: left hand side of hypothetico-deductive model

• Carnap, Hempel, Friedman • 2) Critical rationalism • Deductivism, falsificationism, fallibilism

(naive/dogmatic or sophisticated) • Knowledge is a priori (given through logic

and reason), modus tollens • Moderate empiricism mrk.2: right hand

side of hypothetico-deductive model

Philosophy of science for economists

Lecture 1: Intro © Niels Peter Hahnemann 2011 41

• Covering law # 2, asymmetry thesis • Logic of confirmation, “modernism” • Popper, Lakatos • 3) Methodological realism • Inductivism (again), discourse, rhetoric • Pragmatism (soft hypothetico-deductive

model + “revolution”), pluralism • Learning, knowledge as social activity • Logic of discovery, post-modernism • Kuhn, McCloskey (Foucault, Habermas)

Philosophy of science for economists

Lecture 2: Mercantilists © Niels Peter Hahnemann 2011 42

LECTURE 2: Mercantilists and Physiocrats

• Curriculum: Blaug, Chapter 1 • 1. Preconditions of classical economics: • Old Greek expression: ”eco" = house,

family, the household and its management • Before Adam Smith: theory develops not

only in England, but also on the Continent • Middle Ages → Renaissance →

Enlightenment: gradual development of markets

8

Lecture 2: Mercantilists © Niels Peter Hahnemann 2011 43

• Incipient reflections on the economic organisation of society

• Considerations regarding moral philosophy, the royal household, trade (the value of money)

• An instrumentalist, practical approach • Adam Smith distinguished between two

ancestors: the trading system (the mercantilists) and the agrarian system (the physiocrats)

History of economic thought

Lecture 2: Mercantilists © Niels Peter Hahnemann 2011 44

• 2. Mercantilists, balance of trade, and ”specie-flow”

• The ”trade balance” term dates back to Francis Bacon (1615), earlier in Italy

• Balance of payments ≈ balance of trade, ”balance of the realm”

• The only external mechanism to secure adaptation of price levels by means of flows in money and gold

• An abstract device with no physical existence

History of economic thought

Lecture 2: Mercantilists © Niels Peter Hahnemann 2011 45

• ”Balance of payments” only makes sense combined with other economic data => does a surplus imply wealth, or decline?

• Practical considerations rather than theory • Antonio Serra, Breve trattato delle cause…

(1613): the first to relate flows of gold and silver with the trade balance

• The balance takes care of itself, (change in) monetary matters are a consequence

History of economic thought

Lecture 2: Mercantilists © Niels Peter Hahnemann 2011 46

• Thomas Mun, England's Treasure by Foreign Trade (1664): surplus of exports = advantage of trade to a nation

• John Locke, Some Considerations of the Consequences (1692): money exists only by common consent, M↓=>IMP↓=>EXP↑, but no idea about automatic adjustment

• Exports = gain, imports = loss; gain of a nation = loss of another nation

• Zero sum game, economics externally given, ”just price”, moral system

History of economic thought

Lecture 2: Mercantilists © Niels Peter Hahnemann 2011 47

• Main points of mercantilist programme: • Gold etc. (“treasure”) is key to wealth • Money = specie = capital = wealth • Foreign trade must be regulated to secure

largest possible inflow of gold etc. • Protection of home industries supported by

imports of low-priced commodities • Duty on manufactured goods from abroad • Subsidies on exports • Population growth promoted + low wages

History of economic thought

Lecture 2: Mercantilists © Niels Peter Hahnemann 2011 48

• Realised that inflows of bullion lead to home price increases, and that a surplus of trade will be offset in the long term

• => Policies to maintain persistent trade surplus are self-defeating

• I. e. idea about existence of economic self regulation, the economy is considered as a coherent unity

• Automatic mechanisms at play by means of relative price levels in different countries

History of economic thought

9

Lecture 2: Mercantilists © Niels Peter Hahnemann 2011 49

• Josiah Child (1668): trade has its own ways, profit motive a regulatory principle

• Isaac Gervaise, The System or Theory of Trade of the World (1720): credit increase => C↑ => EXP↓ => IMP↑ => outflow of specie => binding credit constraint, i.e. an automatic mechanism

• David Hume, Of the Balance of Trade and Of Money (1752): clarified the mechanism by emphasising price adjustments

• No idea about international division of labour

History of economic thought

Lecture 2: Mercantilists © Niels Peter Hahnemann 2011 50

• 3. In defence of mercantilism • Smith and other classical economists were

strongly against the mercantilist view, Keynes in defence

• Economics subsumed to political purposes • Economics put in a national context:

protectionism => equilibrium (Keynes) • No idea about effective demand:

unemployment seen to be caused by adverse weather conditions in agriculture

• England needed gold in order to trade

History of economic thought

Lecture 2: Mercantilists © Niels Peter Hahnemann 2011 51

• 4. Quantity theory, inflation, interest rate • Monetary analysis: theory about the

economic process as expenditure streams • The economy as an aggregated whole • If we must aggregate then we need a

measure i.e. money • Metallism: purchasing power of money

originates with the purchasing power of the metal independently of its monetary role

• Cartalism: denial of metallism (fiat money)

History of economic thought

Lecture 2: Mercantilists © Niels Peter Hahnemann 2011 52

• Mercantilists demanded permanent inflow of specie: self-contradiction

• MV = PT: dilemma is ”solved” by assuming that M affects primarily T rather than P, i.e. ”money stimulates trade”

• The quantity equation linked quantity of money with quantity of goods => absolute magnitude of quantity of money not important for wealth of nations

• Hume: proportionality between M and P => money defined as unit of measurement and medium of exchange

History of economic thought

Lecture 2: Mercantilists © Niels Peter Hahnemann 2011 53

• John Law, Money and Trade Considered... (1705): money increases employment

• R. Cantillon, Essai sur la nature… (1755): entrepreneurs invest money, land owners consume money (Cantillon effect) => M↑ => P↑; power depends on the abundance of money => sell dear, buy cheap

• Ignores that decrease in price level abroad turns trade balance in their favour

• No idea about adjustment mechanism or equilibrium

History of economic thought

Lecture 2: Mercantilists © Niels Peter Hahnemann 2011 54

• Mercantilists: higher inflation from larger quantity of money is OK => focus on foreign trade, monetary analysis, glimpse of the overall (macro) perspective

• Smith + Ricardo: focus on savings and thrift, real analysis, no macro perspective

• Interest rate = price of borrowing money: M↑=>r↓ because more money makes it easier to borrow, i.e. a sign of wealth

• Cantillon effect: rudimentary idea about real interest rate

History of economic thought

10

Lecture 2: Mercantilists © Niels Peter Hahnemann 2011 55

• Nicholas Barbon, Discourse of Trade (1690): interest rate = return on “wrought or artifical stock” i.e. profits = rent i.e. ”rent of unwrought or natural stock” => money is but a veil, a value made by law

• Capital = principal of a loan = advance deposit: necessary condition for production

• Anne-Robert Jacques Turgot, Reflexions sur la formation… (1766): capital comes from saving and is ”immediately” turned into investment

History of economic thought

Lecture 2: Mercantilists © Niels Peter Hahnemann 2011 56

• 5. Physiocrates: the agrarian system • William Petty, A Treatise of Taxes and

Contributions (1662): “Political Arithmetick”: concept about government and national income, labour = father of wealth, land = mother of wealth

• Theory about the real economy, wealth = quantity of goods, theory about productive labour = agriculture, free trade

• French agriculture squeezed by higher taxes, physiocrates wanted to streamline

History of economic thought

Lecture 2: Mercantilists © Niels Peter Hahnemann 2011 57

• Francois Quesnay, Tableau economique des physiocrates (1758): income flows in an agrarian economy between sectors = social classes

• Stationary balance (equilibrium) from period to period, no explanation, only description

• Only land i.e. farmers produce value, capital = advance deposit, landlords receive rent, sterile class = manufacturing

• Everything bought is sold, everything sold is bought (≈ Say’s law)

History of economic thought

Lecture 2: Mercantilists © Niels Peter Hahnemann 2011 58

• Output = yearly harvest i.e. not value but ”stuff”; consumed in the following period, i.e. period = year: basic form of economics

• Quesnay’s economic principle: how to get largest possible ”jouissance” with less possible trouble of labour? A utilitarian maximisation problem

• Free competition; pursue of own interests; consumption, no saving

• Mutual dependency of social classes: prosperity for landlords => prosperity for all

History of economic thought

Lecture 2: Mercantilists © Niels Peter Hahnemann 2011 59

• The nation is an institution, the economy a ”machine” that is maintained by materials

• Only rent produces a net yield (and can therefore be taxed), while all other returns are offset by a cost entry in the accounts

• Production by ”stuff” calculated in amounts => use of arithmetic to balance revenue with expenditure

• Natural distribution of resources maintained in everybody’s interest, laws of nature are assumed to be known

History of economic thought

Lecture 2: Mercantilists © Niels Peter Hahnemann 2011 60

• Famous tableau page 58 in Quesnay:

History of economic thought

11

Lecture 2: Mercantilists © Niels Peter Hahnemann 2011 61

• Famous tableau page 58 in Quesnay:

• At start of period t landowners possess net national income from period t-1 (2 bn.). Everybody else stands ready to sell and produce

• Landowners use some to buy agricultural produce (1 bn.) and some to buy manufactures (1 bn.), the latter produced by the “sterile class”

• Farmers thereby receive a return from period t-1 (1 bn.), which they increase (redouble) in period t through their productive activities

• Some of the surplus goes to the landlords, who use it in period t+1, some of the surplus is consumed by farmers, and the last part goes to the sterile as payment for the manufactures that the farmers use

History of economic thought

Lecture 2: Mercantilists © Niels Peter Hahnemann 2011 62

• The “steriles” do not add value, only reproduce it. They spend some of the proceeds received from landlords on consumption of their own produce, and the rest on purchases from farmers, who then increase (redouble) these proceeds through their productive activities

• The same happens with the proceeds the sterile class receive from farmers. They receive a total of 2 bn. from farmers and landlords and spend 1. The rest, i.e. 1 bn., is saved for the next period

• Farmers steadily redouble the proceeds they receive from sales, and spend the proceeds on payments of rent to landlords and on purchases from the “steriles”. Farmers receive 3 bn. in toto of which 1 bn. is interest on their annual advance. The interest is spent on repair, maintenance, reserves, and depreciation. Farmers may spend 2 bn. on themselves and they then redouble this amount, i.e. net national income = 2 bn. payable as rent to landlords for spending in the next period

History of economic thought

Lecture 2: Mercantilists © Niels Peter Hahnemann 2011 63

• When the period terminates, the same amount is in the hands of the landlords as when the period started

• This is the first explicit conceptualisation of the nature of economic balance, a milestone in the history of economic thought!!

• But: why the particular terms of trade? • Important because terms of trade explains

population’s distribution on 3 social classes • Tableau describes a natural state, in which

the wealth of the kingdom is at its highest => all unnecessary expenditure of sterile class harmful luxury

History of economic thought

Lecture 2: Mercantilists © Niels Peter Hahnemann 2011 64

• 6. Scholastics, philosophers of natural law • Middle ages: natural law and philosophy • Scholastic economic ideas e.g. Thomas

Aquinas (13th century): utility is source of value; just price; money capital is sterile => economics is a legal-moral system determined by satisfaction of human needs

• Ferdinando Galiani, Della moneta (1751): ”value’s paradox” is caused by utility’s role in the pricing of a commodity, value depends on utility and scarcity

History of economic thought

Lecture 2: Mercantilists © Niels Peter Hahnemann 2011 65

• Beccaria, Elementi di economia pubblica (1769): theory of utilitarian, hedonistic egotism as driving principle of economic behaviour

• Mercantilists: focus on own interests and profit motive, not a legal-moral system

• Smith wanted to turn economics into an autonomous science => rejected explanations of value by utility i.e. by demand in relation to supply

• Demand reappears in explanations only 100-150 years later with the marginalists

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 66

Adam Smith and the Wealth of Nations

• Curriculum: Blaug, Chapter 2 + Wealth of Nations, Book One Chapter I-X (please also read the first 2½ pages of Chapter XI)

• 1. Smith as economist • His interest was in the long term forces that

govern an economy (“economic development”)

• Wealth = income produced over time, flow • Wealth’s basis: division of labour • Wealth’s main source: agriculture

History of economic thought

12

Lecture 3: Smith © Niels Peter Hahnemann 2011 67

• First treatise on economics based on abstract economic principles

• The price system is a mechanism that governs the actions of people (agents)

• Self-propelled, automatic, and human mechanics, neither selfish or benevolent

• How can human decision-making be self-governing? Against metaphysics

• Wrote Theory of Moral Sentiments (1759) on the moral basis of economics

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 68

• Morals/ethics based on reason • Competition is a process, division of labour

is a powerful engine for capital accumulation

• Which social institutions best propagate human self-sustaining mechanics?

• Not naive ”laissez-faire”: appropriate institutional and legal framework must be in place (political economy)

• Intuitive outline of an economy’s organisation, its first comprehensive account

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 69

• 2. Contents of the ”Wealth of Nations” • 1st edition published 1776 • Introduction: Against mercantilism: • "The annual labour of every nation is the fund which originally

supplies it with all the necessaries and conveniences of life, which it annually consumes, and which consists always either in the immediate produce of that labour, or in what is purchased with that produce from other nations" (WN I-III, page 104).

• Wealth of nations = production, which in particular depends on labour’s skills:

• "first, by the skill, dexterity, and judgement with which its labour is generally applied; and, secondly, by the proportion between the number of those who are employed in useful labour, and that of those who are not so employed" (WN I-III, page 104).

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 70

• Civilisation versus the savage state: • "Among civilised and thriving nations, on the contrary, though a great

number of people do not labour at all, many of whom consume the produce of ten times, frequently of a hundred times more labour than the greater part of those who work; yet the produce of the whole labour of the society is so great that all are often abundantly supplied, and a workman (…) may enjoy a greater share of the necessaries and conveniences of life than it is possible for any savage to acquire" (WH I-III, side 105).

• => Affordability of ”idlers” (the aristocracy), ordinary workmen also more wealthy

• Why? Skill and dexterity of labour • Chapter 1: Importance of division of labour

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 71

• Division of labour ≈ Smith’s only explanation for economic progress:

• (1) inside the factory: command, non-market, (2) outside and between factories: markets

• Smith primarily interested in (1) because he believes it explains value/price

• Economics: labour division network tied together by a price system

• Famous example: manufacturing of pins with considerable gain in productivity

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 72

• The pin factory example • “One man draws out the wire, another straights it, a third cuts it, a

fourth points it, a fifth grinds it at the top for receiving the head; • to make the head requires three distinct operations; to put it on is a

peculiar business, to whiten the pins is another; it is even a trade by itself to put them into the paper;

• and the important business of making a pin is, in this manner, divided into about eighteen distinct operations, which in some manufactories are all performed by distinct hands, though in others the same man will sometimes perform two or three of them.

• I have seen a small manufactory of this kind where ten men only were employed. (…) Those ten persons could make among them upwards of forty-eight thousand pins in a day.

• Each person, therefore, making a tenth part of forty-eight thousand pins might be considered as making four thousand eight hundred pins in a day.

• But if they had all wrought separately and independently (…) they could certainly not each of them have made twenty” (WN I-III, page 110).

History of economic thought

13

Lecture 3: Smith © Niels Peter Hahnemann 2011 73

• Chapter 2: More on the division of labour • Division is spontaneous and natural: • "This division of labour, from which so many advantages are derived,

is not originally the effect of any human wisdom, which foresees and intends that general opulence to which it gives occasion. It is the necessary, though very slow and gradual consequence of a certain propensity in human nature" (WN I-III, page 117).

• The propensity in humans ”to truck and barter” is:

• ”the necessary consequences of the faculties of reason and speech” (WN I-III, page 118).

• I.e. knowledge => expression => exchange: the basis of trade

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 74

• Trade is a rational exchange: • ”this is mine, that yours; I am willing to give this for that (…) Give me

that which I want, and you shall have this which you want” (WN I-III, page 118)

• Not the thing-in-itself, but one-thing-for- another, what does it take to get some:

• ”It is not from the benevolence of the butcher, the brewer, or the baker that we expect our dinner, but from their regard to their own interest” (WN I-III, page 119)

• Economic ”spacetime” emerges from division of labour => production ≠ consumption

• Exploitation of different natural talents

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 75

• Chapter 3: The extent of the market limits the division of labour

• ”As it is the power of exchanging that gives occasion to the division of labour, so the extent of this division must always be limited by the extent of that power, or, in other words, by the extent of the market. When the market is very small, no person can have any encourage- ment to dedicate himself entirely to one employment” (WN I-III, page 121).

• The market takes place in a space defined and bounded by the power of exchanging; this is not necessarily = marketplace; a necessary prerequisite is active use of ”reason and speech”

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 76

• Chapter 4: On money’s origin and use • Division of labour => barter/exchange: • ”When the division of labour has been once thoroughly established, it

is but a very small part of man’s wants which the produce of his own labour can supply. He supplies the far greater part of them by exchanging that surplus part of the produce of his own labour, which is over and above his consumption, for such parts of the produce of other men’s labour as he has occasion for” (WN I-III, page 126).

• Barter/exchange => money needed due to need for a commodity that:

• ”few people would be likely to refuse in exchange for the produce of their industry” (WN I-III, page 127).

• Under what conditions does the exchange of money for goods take place, at what rate?

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 77

• ”It is in this manner that money has become in all civilised nations the universal instrument of commerce, by the intervention of which goods of all kinds are bought and sold, or exchange for one another. What are the rules which men naturally observe in exchanging them either for money or for another, I shall now proceed to examine. These rules determine what may be called the relative or exchangeable value of goods” (WN I-III, page 131).

• It is by putting forward this problem, that Smith’s account becomes de facto a major oeuvre in the history of classical economic theory!!

• => Distinction between use value and exchange value, market price and natural price

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 78

• Chapter 5: The price of commodities. Important chapter!!

• What is the characteristic common to all commodities? They are produced by labour:

• "The value of any commodity, therefore, to the person who possesses it, and who means not to use or consume it himself, but to exchange it for other commodities, is equal to the quantity of labour which it enables him to purchase or command. Labour, therefore, is the real measure of the exchangeable value of all commodities" (WH I-III, page 133).

• ”Labour” term used in 3 different ways: as measure of value; as quantity with which a commodity will exchange = the quantity that it takes to produce it; as disutility that determines the real price of the commodity

History of economic thought

14

Lecture 3: Smith © Niels Peter Hahnemann 2011 79

• "The real price of everything (…) is the toil and trouble of acquiring it" (WN I-III, page 133).

• "Labour was the first price, the original purchase-money that was paid for all things. It was not by gold or by silver, but by labour that all the wealth was originally purchased; and its value (…) is precisely equal to the quantity of labour which it can enable them to purchase or command" (WN I-III, page 133).

• Labour ≈ provenance of the economy, its material basis ≠ labour value theory! Wealth is power = purchasing power:

• "Wealth, as Mr Hobbes says, is power. But the person who either acquires or succeeds to a great fortune, does not necessarily acquire or succeeds to any political power, either civil or military (…). The power which that possession immediately and directly conveys to him, is the power of purchasing" (WN I-III, page 134).

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 80

• Labour = ”toil and trouble” = ”time spent” + ”degree of hardship” (WN I-III, page 134)

• Labour is no exact measure, movements of the market achieve only a ”rough equality” (WN I-III, page 134)

• Quantity of money eventually estimates good’s exchange value (WN I-III, side 135)

• "At all times and places that is dear which it is difficult to come at, or which it costs much labour to acquire; and that cheap which is to be had easily, or with very little labour. Labour alone, therefore, never varying in its own value, is alone the ultimate and real standard (…). It is their real price; money is their nominal price only" (WN I-III, page 136).

• No concept about supply and demand

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 81

• Market price: short term • Equilibrium price: long term = costs of

production • “Market” and “equilibrium” are not linked

together due to the labour value theory • "But though equal quantities of labour are always of equal value to

the labourer, yet to the person who employs him they appear sometimes to be of greater and sometimes of smaller value. He purchases them sometimes with a greater and sometimes with a smaller quantity of goods (…). In reality, however, it is the goods which are cheap in the one case, and dear in the other" (WN I-III, page 136).

• Labour: value’s measure and determinator

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 82

• Real price = labour value: • "Its (i.e. labour’s) real price may be said to consist in the quantity of

the necessaries and conveniences of life which are given for it; its nominal price in the quantity of money" (WN I-III, page 136).

• Tautology: real price = value: • "The same real price is always of the same value; but on account of

the variations in the value of gold and silver, the same nominal price is sometimes of very different values" (WN I-III, page 134).

• I.e. mercantilists and quantity theory say: market price = supply + demand; but Smith says: real price = labour value:

• "Labour, therefore, it appears evidently, is the only universal, as well as the only accurate measure of value" (WN I-III, page 139-140).

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 83

• Chapter 6: Components of goods’ prices • Compares the primitive society, in which

products are not brought to the market: • "that early and rude state of society“, hvor "the whole produce of

labour belongs to the labourer" (WN I-III, page 150-51),

• - to the advanced society, in which: • "something must be given for the profits of the undertaker of the work

who hazards his stock in this adventure. The value which the workmen adds to the materials, therefore, resolves itself in this case into two parts, of which the one pays their wages, the other the profits of their employer upon the whole stock of materials and wages which he advanced" (WN I-III, page 151).

• => Price composed by wages and profits

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 84

• Products not brought to the market = the production function

• If total production belongs to the worker: value of the commodity = terms of trade = relative contents of labour:

• "If among a nation of hunters, for example, it usually costs twice the labour to kill a beaver which it does to kill a deer, one beaver should naturally exchange for or be worth two deer" (WN I-III, page 150).

• First use of algebra in economic theory? • Value = long term price determined by the

value of labour, not market price determined by supply and demand

History of economic thought

15

Lecture 3: Smith © Niels Peter Hahnemann 2011 85

• Advance of capital => profit is payable: • “Profits should bear a regular proportion to his capital. In the price of

commodities, therefore, the profits of stock constitute a component part altogether different from the wages of labour, and regulated by quite different principles. In this state of things, the whole produce of labour does not always belong to the labourer. He must in most cases share it with the owner of the stock which employs him" (WN I-III, page 152).

• If land is advanced (i.e. private property) => also rent is payable

• Real value of a commodity determined outside of the market, i.e. outside of the economy, by its cost of production, i.e. by value of labour:

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 86

• "The real value of all the different component parts of price, it must be observed, is measured by the quantity of labour which they can, each of them, purchase or command. Labour measures the value not only of that part of price which resolves itself into labour, but of that which resolves itself into rent, and of that which resolves itself into profit" (WN I-III, page 153).

• I.e. measure of (labour) = measure of (labour + rent + profits): the contradiction and inconsistency in Smith's theory, and the cause of countless theoretical disputes

• "Wages, profit, and rent, are the three original sources of all revenue as well as of all exchangeable value. All other revenue is ultimately derived from some one or other of these" (WN I-III, page 155).

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 87

• The annual labour product buys more (because it also contains profits + rent) than the labour product (??!!):

• "As in a civilized country there are but few commodities of which the exchangeable value arises from labour only, rent and profit contributing largely to that of the far greater part of them, so the annual produce of its labour will always be sufficient to purchase or command a much greater quantity of labour than what was employed in raising, preparing, and bringing that produce to market" (WN I-III, page 157).

• It does not add up • Max growth (determined by population) =>

full employment => zero profits and rent => production function has only labour input

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 88

• Chapter 7: Natural and market price • Natural price given by costs of production: • "When the price of any commodity is neither more nor less that what

is sufficient to pay the rent of the land, the wages of the labour, and the profits of the stock employed in raising, preparing, and bringing it to market, according to their natural rates, the commodity is then sold for what may be called its natural price. The commodity is then sold precisely for what it is worth, or for what it really costs" (WN I-III, page 158).

• Market price given by supply + demand: • "The market price of every particular commodity is regulated by the

proportion between the quantity which is actually brought to market, and the demand of those who are willing to pay the natural price of the commodity" (WN I-III, page 158).

• => Effective demand (= willingness to pay natural price) plays no role in the economy

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 89

• Supply ≠ effective demand => fluctuations in market price, but no explanation for ”≠”

• Competition = a process or mode of behaviour, not a state

• "The natural price, therefore, is, as it were, the central price to which the prices of all commodities are continually gravitating. (…) The whole quantity of industry annually employed in order to bring any commodity to market naturally suits itself in this manner to effectual demand. It naturally aims at bringing always that precise quantity thither which may be sufficient to supply, and no more than supply, that demand" (WN I-III, page 160-61).

• Natural price varies with price-components • "The natural price itself varies with the natural rate of each of its

component parts, of wages, profits, and rent" (WN I-III, page 166).

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 90

• Chapter 8: The return to labour • Subsistence wage determined by number

of persons in household: • ”A man must always live by his work, and his wages must at least be

sufficient to maintain him. They must even upon most occasions be more; otherwise it would be impossible for him to bring up a family” (WN I-III, page 170).

• National wealth↑ => capital↑ => wage advance (fund)↑ => wage↑:

• "It is not the actual greatness of national wealth, but its continual increase, which occasions a rise in the wages of labour" (WN I-III, page 172).

• => Real wage level higher in America than in England (WN I-III, page 172)?!

History of economic thought

16

Lecture 3: Smith © Niels Peter Hahnemann 2011 91

• Why? In a wealthy country wealth does not grow, but the population grows => no ”scarcity of hands”, but rather ”scarcity of employment”

• "Though the wealth of a country should be very great, yet if it has been long stationary, we must not expect to find the wages of labour very high in it. The funds destined for the payment of wages, the revenue and stock of its inhabitants, may be of the greatest extent; but if they have continued for several centuries of the same, or very nearly of the same extent, the number of labourers employed every year could easily supply, and even more than supply, the number wanted the following year. There could seldom be any scarcity of hands, nor could the masters be obliged to bid against one another in order to get them. The hands, on the contrary, would, in this case, naturally multiply beyond their employment. There would be a constant scarcity of employment…” (WN I-III, page 173-74).

• Too many ”hands” drive wages down

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 92

• Only the worst of poverty puts limit to the growth of the population, the more wealthy part of the population will still grow:

• ”But in civilised society it is only among the inferior ranks of people that the scantiness of subsistence can set limits to the further multiplication of the human species” (WN I-III, page 182).

• Chapter 9: On profits. Increase in ”stock” => reduction in profits due to increase in competition

• Profits will be lowest in the most wealthy country => tendency of rate of profit to fall

• Else: a primarily descriptive chapter

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 93

• Chapter 10: Wage and profit (descriptive) • Differences in wages according to labour’s

agreeableness or disagreeableness, difficulty, etc. (WN I-III, page 202-222)

• Differences in profits: corporations try to limit free competition (WN I-III, page 227) => unequal exchange between city and country (WN I-III, page 228-230)

• A highly regulated European economy • Point: market mechanism equalises

returns and wages – if allowed to operate

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 94

• Chapter 11: On rent (very long and descriptive, only page 247-249 of general interest)

• Rent for use of land is the highest price that the tenant can afford

• While wages and profits cause high commodity prices, high rent is a consequence of high commodity prices;

• Increase in economic welfare causes higher rent (but lower profits)

• Digression on the value of silver and the general development of prices

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 95

• Book Two: On the accumulation of capital, gross and net product, productive and unproductive labour, S ≡ I => money is only a means of exchange

• Book Three: On the development of agriculture in Europe

• Book Four: Mercantilism, Physiocrates, “political economy” (÷), “laissez faire” (+), free trade (+), the “invisible hand”

• Book Five: On public finances

History of economic thought

Lecture 3: Smith © Niels Peter Hahnemann 2011 96

• “Every individual is continually exerting himself to find out the most advantageous employment for whatever capital he can command. It is his own advantage, indeed, and not that of the society, which he has in view. But the study of his own advantage naturally, or rather necessarily, leads him to prefer that employment which is most advantageous to the society. (…) He generally, indeed, neither intends to promote the public interest, nor knows how much he is promoting it. By preferring the support of domestic to that of foreign industry, he intends only his own security; and by directing that industry in such a manner as its produce may be of the greatest value, he intends only his own gain, and he is in this, as in many other cases, led by an invisible hand to promote an end which was no part of his intention”, that is the common good: Adam Smith (1776), The Wealth of Nations, Books IV-V, pp. 30 and 32.

• Only place in Wealth of Nations where Smith used famous expression. Smith also used it in his earlier work: Theory of Moral Sentiments

History of economic thought

17

Lecture 4: Malthus © Niels Peter Hahnemann 2011 97

• LECTURE 4: Malthus, population, returns • Curriculum: Blaug Chapter 3 • ”Savage state”: consumption ≡ production • ”Civilised state”: division of labour, needs

satisfied via the market • => consumption ≠ production savings: • Consumption + savings = production =

consumption + investments • => Number and growth of population no

longer governed by production?

History of economic thought

Lecture 4: Malthus © Niels Peter Hahnemann 2011 98

• Overpopulation = underproduction: • Analytical problem for economic theory • Practical problem for society • Important issue for discussion over the 40

years between Smith and Ricardo • Link between S&R is: Thomas Robert

Malthus (1798), Essay on Population • Strong relation between growth of

population and food supply • Capacity to grow of human population

given by man’s reproductive instincts

History of economic thought

Lecture 4: Malthus © Niels Peter Hahnemann 2011 99

• Positive limits to population growth: food production, morals, ”vice”

• Negative limits to population growth: ”vice”, poverty

• Man’s biological capacity for reproduction (geometrical growth) > man’s physical capacity to increase the production of food (arithmetical growth)

• Dynamical argument that affects the poor only, who therefore must respect ”vice”

History of economic thought

Lecture 4: Malthus © Niels Peter Hahnemann 2011 100

• ”I think I may fairly make two postulata. First, that food is necessary to the existence of man. Second, that the passion between the sexes is necessary, and will remain nearly in its present state. These two laws, ever since we have had any knowledge of mankind, appear to have been fixed laws of our nature. (...) Assuming then my postulata as granted, I say that the power of population is indefinitely greater than the power in the earth to produce the subsistence for man” (EPP, page 12-13).

• ”This natural inequality of the two powers of population and of the production on the earth, and that great law of our nature which must constantly keep their effects equal, form the great difficulty that to me appears insurmountable in the way to the perfectibility of society” (EPP page 14).

• We will suppose the means of subsistence in any country just equal to the easy support of its inhabitants. The constant effort towards population, which is found to act even in the most vicious societies, increases the number of people before the means of subsistence are increased. The food therefore which before supported seven millions must now be divided among seven million and a half or eight millions. The poor consequently must live worse” (EPP page 19).

History of economic thought

Lecture 4: Malthus © Niels Peter Hahnemann 2011 101

• If no economic inequality, no need to respect ”vice”:

• ”We have seen the fatal effects that would result to a society if every man had a valid claim to an equal share of the produce of the earth. The members of a family which was grown too large for the original division of land appropriated to it could not then demand a part of the surplus produce of others, as a debt of justice. It has appeared that, from the inevitable laws of nature, some human beings must suffer from want. These are the unhappy persons who, in the great lottery of life, have drawn a blank” (EPP, page 85).

• Fear of starvation makes food constraint effective: empty non-falsifiable statement

• Builds on postulate about declining returns regardless of technical progress, from:

• Turgot (1765), Reflexions sur la formation et la distribution des richesses

History of economic thought

Lecture 4: Malthus © Niels Peter Hahnemann 2011 102

• Turgot: Increase in a factor of production + other factors remain constant => decline in rate of growth of total production

• Malthus: ”Where there are few people, and a great quantity of fertile land, the power the earth to afford a yearly increase of food may be compared to a great reservoir of water, supplied by a moderate stream. The faster population increases, the more help will be got to draw off the water, and consequently an increasing quantity will be taken every year. But the sooner, undoubtedly, will the reservoir be exhausted, and the streams only remain. When acre has been added to acre, till all the fertile land is occupied, the yearly increase of food will depend upon the amelioration of all the land already in possession; and even this moderate stream will be gradually diminishing. But population, could it be supplied with food, would go on with unexhausted vigour” (EPP page 48, footnote).

• Subsistence wage is function of ”habit & custom” => overpopulation is possible = food production too low, supply of land too low => return to production declines with increase in population

History of economic thought

18

Lecture 4: Malthus © Niels Peter Hahnemann 2011 103

• Price of corn a political issue (corn laws) • Thomas Robert Malthus (1815), Inquiry

into the Nature and Progress of Rent: high price on corn due to rent, not customs

• David Ricardo (1815), An Essay on the Influence of a Low Price of Corn: rent is payment to landowner that equilibrates (equalises) rates of profit on land of different fertility, rent is determined by price (as in Smith)

History of economic thought

Lecture 4: Malthus © Niels Peter Hahnemann 2011 104

• The emerging classical model: capital + labour cultivate land, output = corn (one good same price)

• Ongoing inputs of increasing, homogenous amounts of capital and labour in a fixed proportion, i.e. a two-factor model on land

• Two factors determine price: K,L • Third factor: J, determined by price • Price determines production’s return = rent • Costs differ (good or bad land) • Diminishing returns = rent declines

History of economic thought

Lecture 4: Malthus © Niels Peter Hahnemann 2011 105

• Rent is "unearned income" from the good land

• The land-resource is inexhaustible and non-reproducible: always in fixed supply and necessary as input (á la oil?)

• Rent = taxation object, e.g. Henry George (1879), Progress and Poverty

• Over-population ≈ under-consumption ≈ over-production => possibility of ”gluts” (too many goods): this is a dynamical argument in Malthus

History of economic thought

Lecture 5 Ricardo © Niels Peter Hahnemann 2011 106

• LECTURE 5: David Ricardo, On the Principles of Political Economy and Taxation (1st edition 1817, 3rd 1821)

• Curriculum: Blaug, Chapter 4, Principles, Chapter I-VII and XXX

• LECTURE PART ONE: CHAPTERS 1+4+30

• Probably one of the most difficult of the major works in the history of economics

• Leading idea: Growth ceases due to lack of natural resources (marginal land)

History of economic thought

Lecture 5 Ricardo © Niels Peter Hahnemann 2011 107

• Chapter I divided in 7 sections. 1st Section: value of commodity depends on quantity of labour required for its production

• Based on Smith, but also critique of Smith • "Possessing utility, commodities derive their exchangeable value

from two sources; from their scarcity, and from the quantity of labour required to obtain them" (Principles, page 12).

• Ricardo: ”utility” = Smith: ”use value” • Smith’s correct definition of value: • "If the quantity of labour realised in commodities regulate their

exchangeable value, every increase of the quantity of labour must augment the value of that commodity on which it is exercised, as every diminution must lower it" (P., page 13).

History of economic thought

Lecture 5 Ricardo © Niels Peter Hahnemann 2011 108

• Smith’s incorrect definition of value: wage fund determines relative price i.e. he

• "speaks of things being more or less valuable in proportion as they will exchange for more or less of this standard measure" (P, p. 14).

• Ricardo: value = embodied quantity of labour => terms of trade

• Smith: value = terms of trade i.e. regards • “the standard measure of value as not the quantity of labour

bestowed on the production of any object, but the quantity which it can command in the market" (P., page 14).

• Smith: labour determines exchange value • Ricardo: returns to labour and product of

labour not the same thing:

History of economic thought

19

Lecture 5 Ricardo © Niels Peter Hahnemann 2011 109

• "If the reward of the labourer were always in proportion to what he produced, the quantity of labour bestowed on a commodity, and the quantity of labour which that commodity would purchase, would be equal, and either might accurately measure the variations of other things; but they are not equal" (P., page 14).

• Smith: the produce of labour = the reward of the labourer (because value = exchange value) is sufficient to purchase a much greater quantity of labour

• Ricardo: they are not the same • "It is the comparative quantity of commodities which labour will

produce, that determines their present or past relative values, and not the comparative quantities of commodities, which are given to the labourer in exchange for his labour" (P., page 17).

History of economic thought

Lecture 5 Ricardo © Niels Peter Hahnemann 2011 110

• 2nd Section: different types of labour have different returns => different

• ”estimation of which different qualities of labour are held", (...which...), "when once formed, is liable to little variation". It is a matter of a "proper scale of value" (P., page 20-21).

• Does not change much over time • Variation = temporary fluctuation • => Rejects that fluctuations have any

impact on the commodities’ relative value • 3rd Section: labour bestowed (embodied) in

capital must also be included

History of economic thought

Lecture 5 Ricardo © Niels Peter Hahnemann 2011 111

• Share of capital small part of total value (P., page 23)

• Total labour = commodity’s production + supply to market (P., page 25)

• Value of capital = value of past labour embodied/put down/bestowed in capital

• Labour savings reduce relative value of commodities

• ”Quantity of labour bestowed" ≠ "reward of labour" =>

History of economic thought

Lecture 5 Ricardo © Niels Peter Hahnemann 2011 112

• "The proportion which might be paid for wages is of the outmost importance in the question of profits; for it must at once be seen, that profits would be high or low exactly in proportion as wages were low or high” (NOTE: because total labour value is unchanged); “but it could not in the least affect the relative value of fish and game as wages would be high or low at the same time in both occupation" (P., page 27)

• Equal wages in "fish" and "game". One wage: subsistence

• Ricardo thinks that the distribution between wages and profits can change

• Idea: distribution ≠ production ("proportion which might be paid"), i.e. value of labour is distributed between wages and profits

History of economic thought

Lecture 5 Ricardo © Niels Peter Hahnemann 2011 113

• "If with the same quantity of labour a less quantity of fish or a greater quantity of game were obtained, the value of fish would rise in comparison with that of game" (P., side 27). "No alteration in the wages of labour could produce any alteration in the relative value of these commodities; for suppose them” (NOTE: wages) “to rise, no greater quantity of labour would be required in any of these occupations, but it would be paid for at a higher price" (P., page 28).

• Reduced quantity of labour in the production of either "fish" or "game" by saving labour and investing capital => decreased labour value

• Change in wage does not change value of labour, only the distribution between wages and profits

History of economic thought

Lecture 5 Ricardo © Niels Peter Hahnemann 2011 114

• Sections 4 + 5: capital, labour, value • Complexities in the labour value theory: • "This difference in the degree of durability of fixed capital, and this

variety in the proportions in which the two sorts of capital may be combined, introduce another cause, besides the greater or less quantity of labour necessary to produce commodities, for the variations in their relative value – this cause is the rise or fall in the value of labour" (P., page 30).

• Another cause ≠ quantity of labour? • Difference in combination and durability of

capital => difference in labour saving => change in labour’s value even if quantity of labour is constant:

History of economic thought

20

Lecture 5 Ricardo © Niels Peter Hahnemann 2011 115

• "But although commodities produced under similar circumstances would not vary with respect to each other from any cause but an addition or diminution of the quantity of labour necessary to produce one or other of them, yet compared with others not produced with the same proportionate quantity of fixed capital they would vary from the other cause also which I have mentioned before, namely a rise in the value of labour, although neither more nor less labour were employed in the production of them" (P., page 32-33).

• Fixed capital = machinery, buildings; circulating capital = wages

• Labour value becomes dependent upon time to the market

• => More than one explanations for relative value?

• Value of labour ↑ ≡ profits ↓

History of economic thought

Lecture 5 Ricardo © Niels Peter Hahnemann 2011 116

• Change in relative value depends on share of fixed capital, but:

• ”There can be no rise in the value of labour without a fall of profits” (P., page 35)

• Total product will be of constant value for constant contribution of capital and labour

• Labour’s return ≠ labour’s exchange value • => Effect of wage↑ depends on fixed

capital: • ”The degree of alteration in the relative value of goods on account of

a rise or fall in the relative value of labour, would depend on the proportion which the fixed capital bore to the whole capital employed” (P., page 35).

History of economic thought

Lecture 5 Ricardo © Niels Peter Hahnemann 2011 117

• But this effect is small, says Ricardo => labour value theory only an approximation

• Difference between ”approximation” and ”actual” is due to time:

• ”The superior price of one commodity is owing to the greater length of time which must elapse before it can be brought to market (…) The difference in value arises in both cases from the profits being accumulated as capital, and is only a just compensation for the time that the profits are withheld” (P., page 37).

• The more fixed capital, the larger the fall in exchange value (P., page 38)

• Equivalent effect from difference in fixed capital’s ”durability”

History of economic thought

Lecture 5 Ricardo © Niels Peter Hahnemann 2011 118

• Ricardo wanted to: • 1) determine the average of relative value,

2) determine the distribution of value • Necessitated finding unit of measurement

for economy’s total returns, but value ends up being co-determined by distribution

• He ”solved" the problem by measuring only goods with the same capital-labour ratio

• Change in wage-profit relation will not change the average and, consequently, will not change total product value

History of economic thought

Lecture 5 Ricardo © Niels Peter Hahnemann 2011 119

• Wage increase => more machinery => equalisation of profit rates. Illustrated with numbers (P., page 40-41):

• If a manufacturer of machines increases his price (remember that wages are identical for all manufacturers), he will end up using "an unusual quantity of capital” in the production to get labour savings, and the price of his machines will fall ”till their price afforded only the common rate of profits”

History of economic thought

Lecture 5 Ricardo © Niels Peter Hahnemann 2011 120

• Wages↑ does not increase price of machines but increases amount of capital and decreases amount of labour:

• "With every difficulty of providing for the maintenance of men” (NOTE: because the population grows all the time), “labour necessarily rises” (NOTE: because more food is necessary), “and with every rise in the price of labour, new temptations are offered to the use of machinery" (P., footnote page 41).

• => Change in commodities’ relative value as a consequence of wage increase => equalisation of profit rates ≡ ”Ricardo effect”

• Increasingly over time, machines (“these mute agents”) substitute capital for labour

History of economic thought

21

Lecture 5 Ricardo © Niels Peter Hahnemann 2011 121

• Section 6: on the invariable standard of value (only in 3rd edition)

• Approximate labour value => does an invariable measure exist?

• "Of such a measure it is impossible to be possessed, because there is no such commodity which is not itself exposed to the same variations as the things, the value of which is to be ascertained" (P., page 43-44).

• Gold not a perfect measure either • Ricardo then assumes that gold is

produced with proportion of labour, fixed capital, etc. ≈ average of the economy:

History of economic thought

Lecture 5 Ricardo © Niels Peter Hahnemann 2011 122

• "May not gold be considered as a commodity produced with such proportions of the two kinds of capital as approach nearest to the average quantity employed in the production of most commodities?" (P., page 45).

• => Gold’s labour value will always only vary with quantity of labour => useable as measure

• Extra implicit assumption: corn is produced under same conditions as gold => corn/gold-standard => critique of Smith:

• "Smith (…) maintained that a rise in the price of labour would be uniformly followed by a rise in the price of all commodities. I hope that I have succeeded in showing (…) that only those commodities would rise which had less fixed capital employed upon them than the medium in which price was estimated" (P., page 46).

History of economic thought

Lecture 5 Ricardo © Niels Peter Hahnemann 2011 123

• Section 7: money is introduced • Money is neutral: Ricardo runs through the

argument • Fall in value of money => increase in

money wage + commodity prices => relative value unchanged: