Embed Size (px)

Citation preview

© Copyright 2015 RBN Energy

Report to NASEO:Propane Supply and Infrastructure Study

Based on a Report to PERC byRusty Braziel, Ron Gist

RBN Energy LLCJuly 14, 2015

Deck 1

2© Copyright 2015 RBN Energy

Propane Supply and Infrastructure Study

» Overview, Production

» NGL/Propane Infrastructure Developments

» U.S. Propane Market Analysis Supply/Demand Scenarios and Drivers Exports, Terminal Contracts, LPG Shipping,

International Markets Seasonal Model and Demand Sensitivities Price Outlook

» Conclusions and Recommendations

3© Copyright 2015 RBN Energy

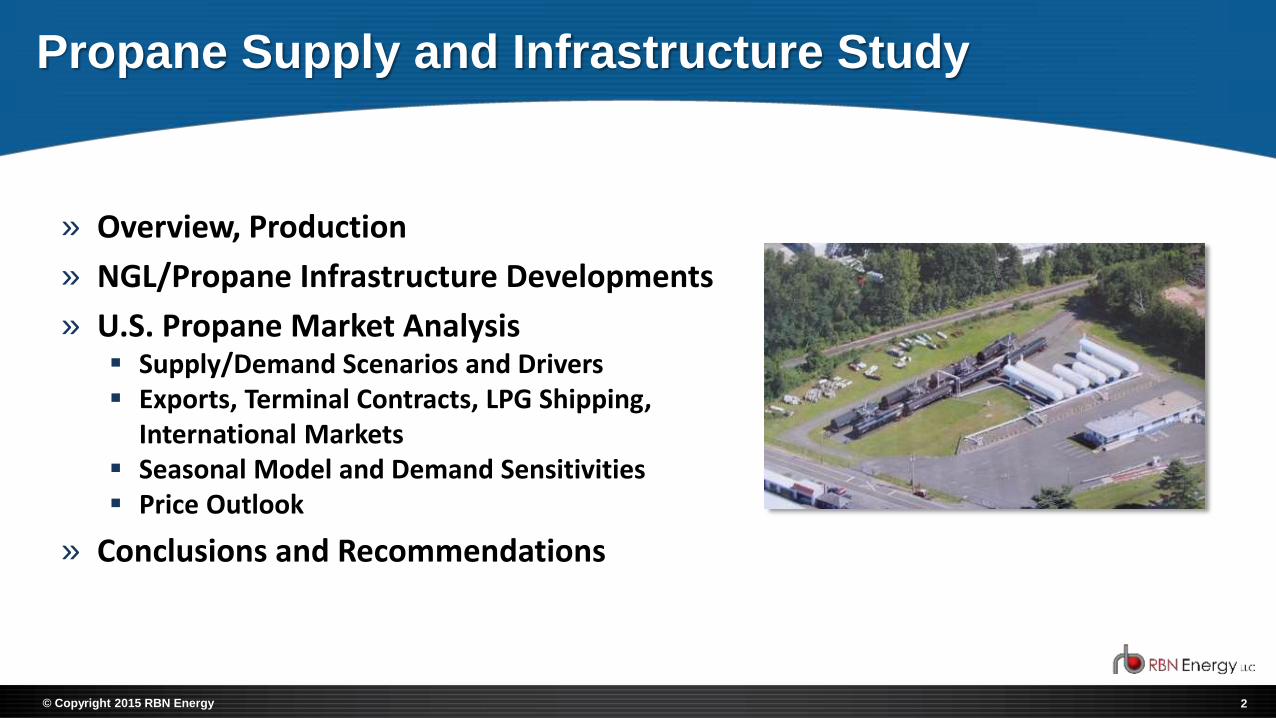

PADD Level Study

1

2

3

4

5

4© Copyright 2015 RBN Energy

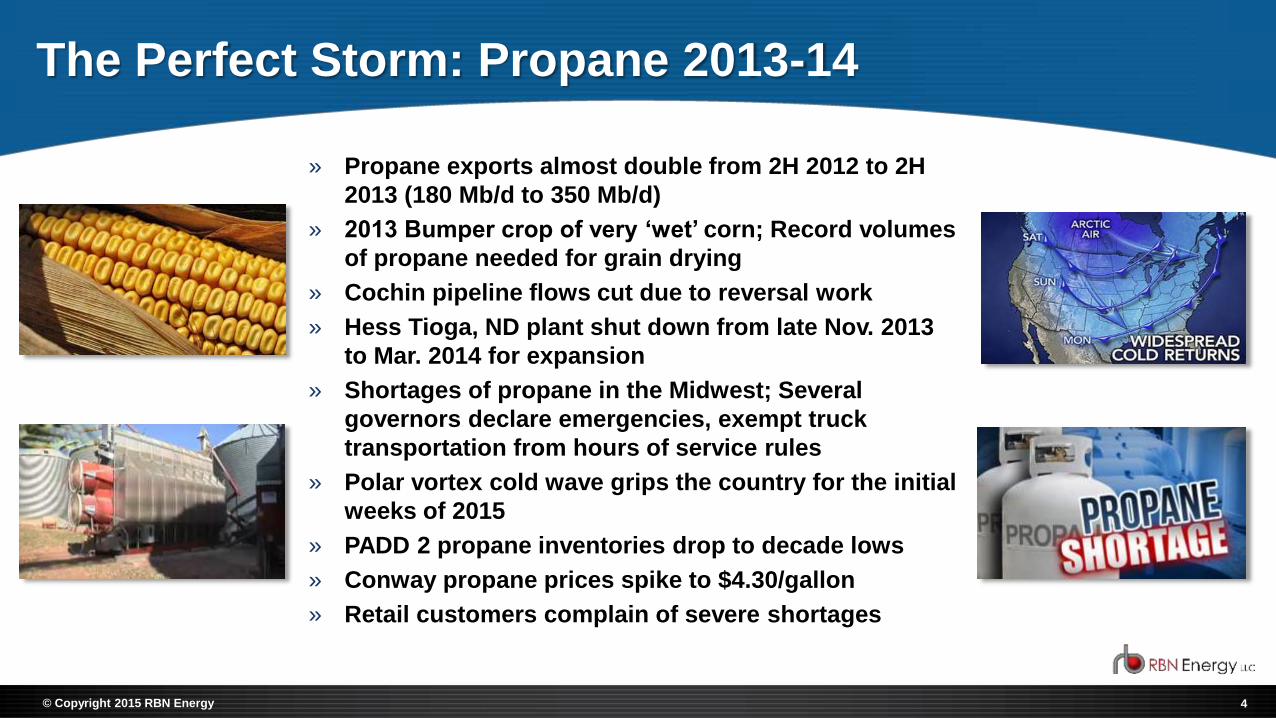

The Perfect Storm: Propane 2013-14

» Propane exports almost double from 2H 2012 to 2H

2013 (180 Mb/d to 350 Mb/d)

» 2013 Bumper crop of very ‘wet’ corn; Record volumes

of propane needed for grain drying

» Cochin pipeline flows cut due to reversal work

» Hess Tioga, ND plant shut down from late Nov. 2013

to Mar. 2014 for expansion

» Shortages of propane in the Midwest; Several

governors declare emergencies, exempt truck

transportation from hours of service rules

» Polar vortex cold wave grips the country for the initial

weeks of 2015

» PADD 2 propane inventories drop to decade lows

» Conway propane prices spike to $4.30/gallon

» Retail customers complain of severe shortages

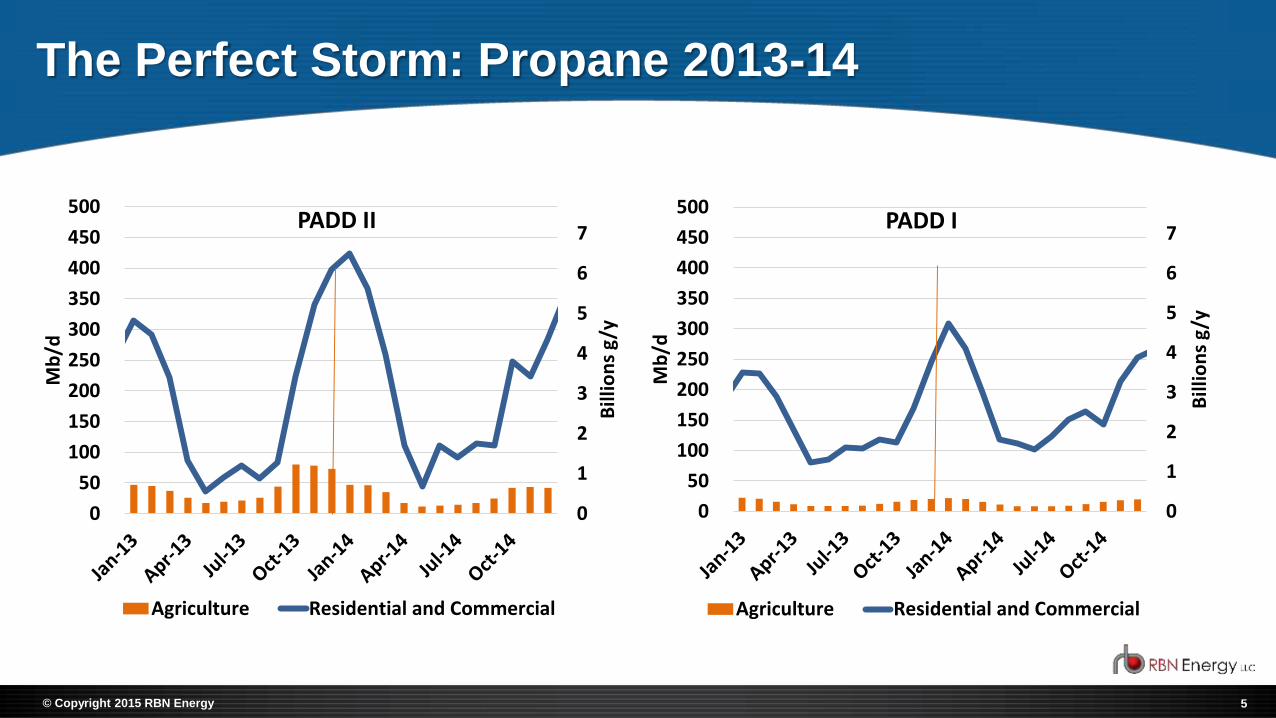

5© Copyright 2015 RBN Energy

The Perfect Storm: Propane 2013-14

0

1

2

3

4

5

6

7

0

50

100

150

200

250

300

350

400

450

500

Bill

ion

s g

/y

Mb

/d

PADD II

Agriculture Residential and Commercial

0

1

2

3

4

5

6

7

0

50

100

150

200

250

300

350

400

450

500

Bill

ion

s g

/y

Mb

/d

PADD I

Agriculture Residential and Commercial

6© Copyright 2015 RBN Energy

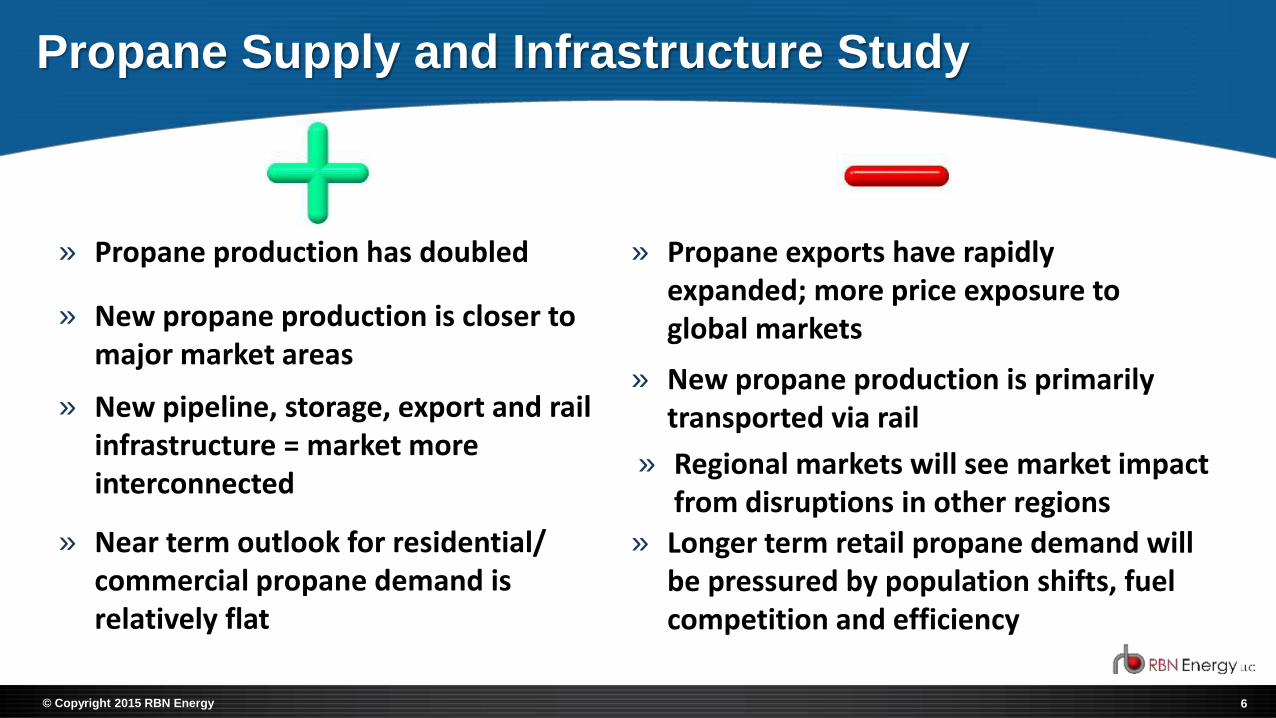

Propane Supply and Infrastructure Study

» Propane production has doubled » Propane exports have rapidly expanded; more price exposure to global markets» New propane production is closer to

major market areas» New propane production is primarily

transported via rail

» Near term outlook for residential/ commercial propane demand is relatively flat

» Longer term retail propane demand will be pressured by population shifts, fuel competition and efficiency

» New pipeline, storage, export and rail infrastructure = market more interconnected

» Regional markets will see market impact from disruptions in other regions

7© Copyright 2015 RBN Energy

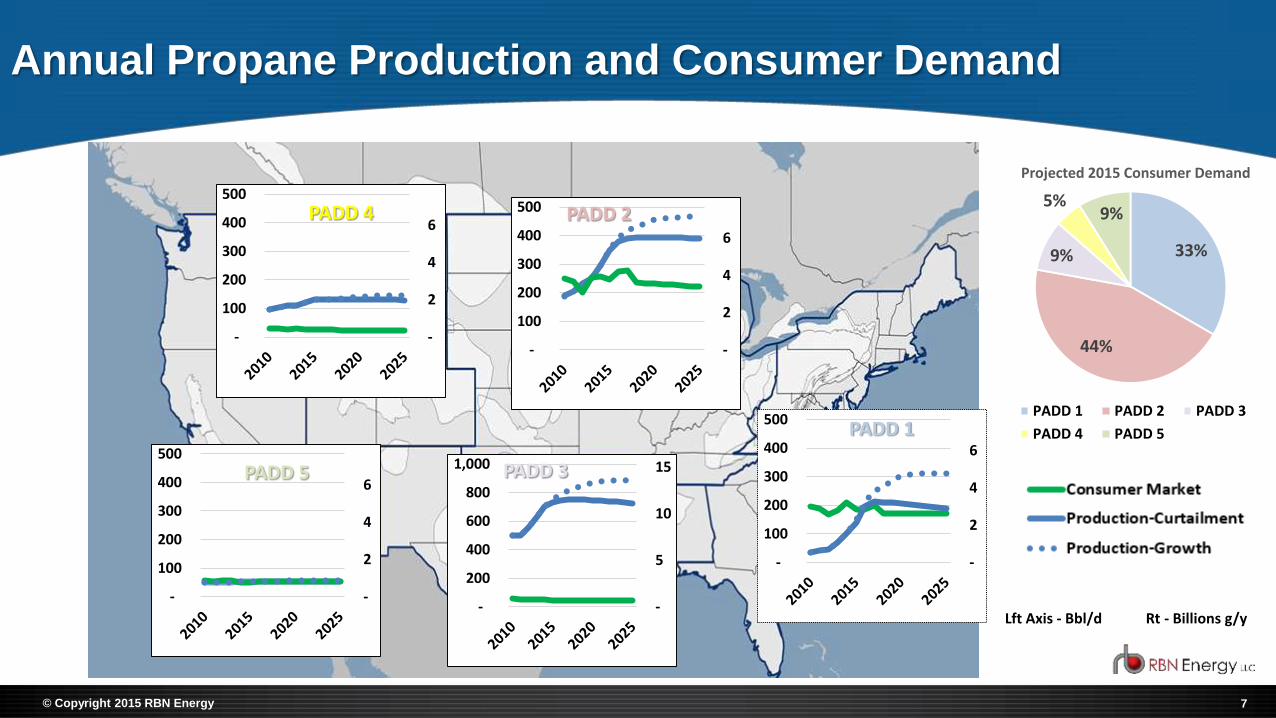

Annual Propane Production and Consumer Demand

-

2

4

6

-

100

200

300

400

500

MillionsPADD 1

33%

44%

9%

5%9%

Projected 2015 Consumer Demand

PADD 1 PADD 2 PADD 3

PADD 4 PADD 5

-

2

4

6

-

100

200

300

400

500

MillionsPADD 2

-

5

10

15

-

200

400

600

800

1,000

MillionsPADD 3

-

2

4

6

-

100

200

300

400

500

Millions

PADD 4

-

2

4

6

-

100

200

300

400

500

Millions

PADD 5

Lft Axis - Bbl/d Rt - Billions g/y

8© Copyright 2015 RBN Energy

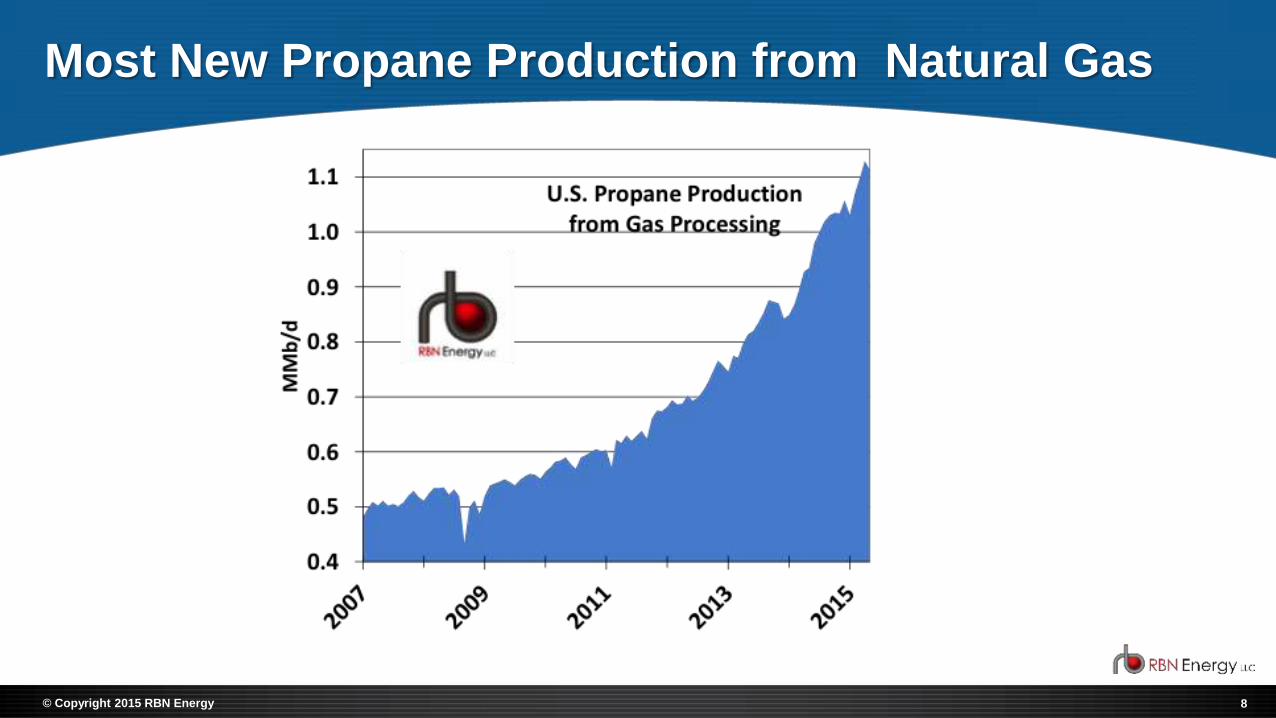

Most New Propane Production from Natural Gas

9© Copyright 2015 RBN Energy

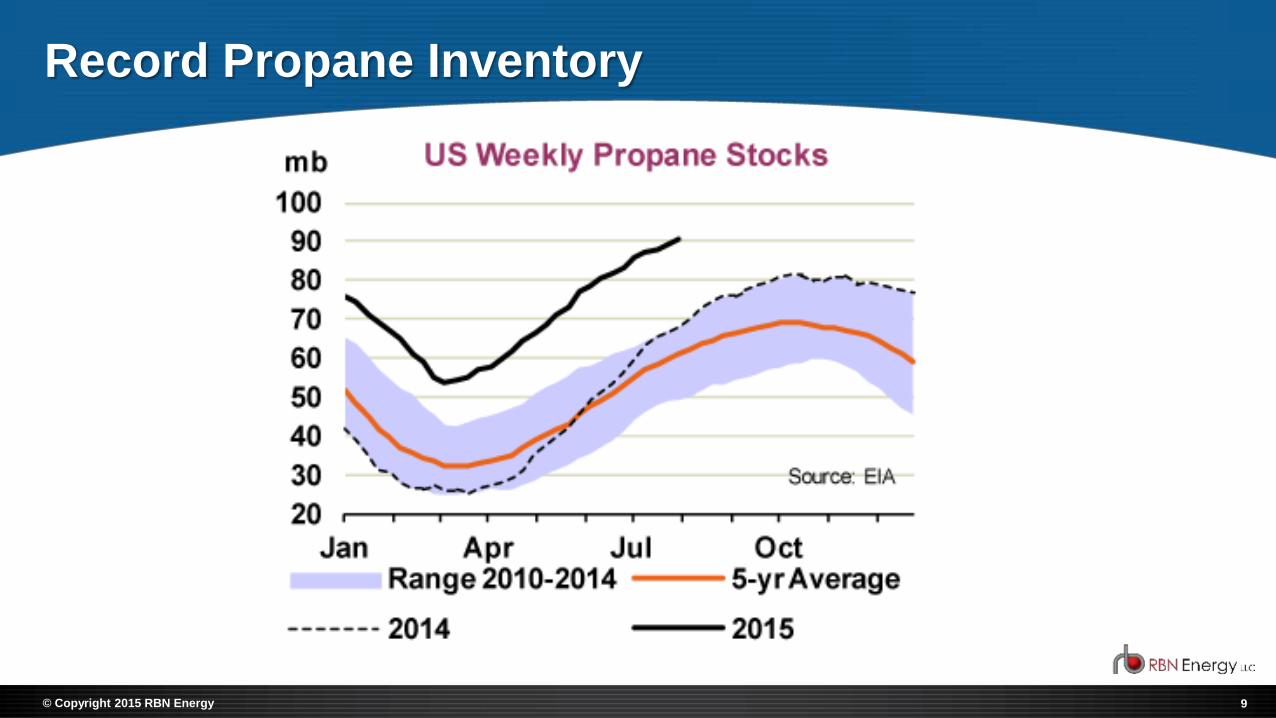

Record Propane Inventory

10© Copyright 2015 RBN Energy

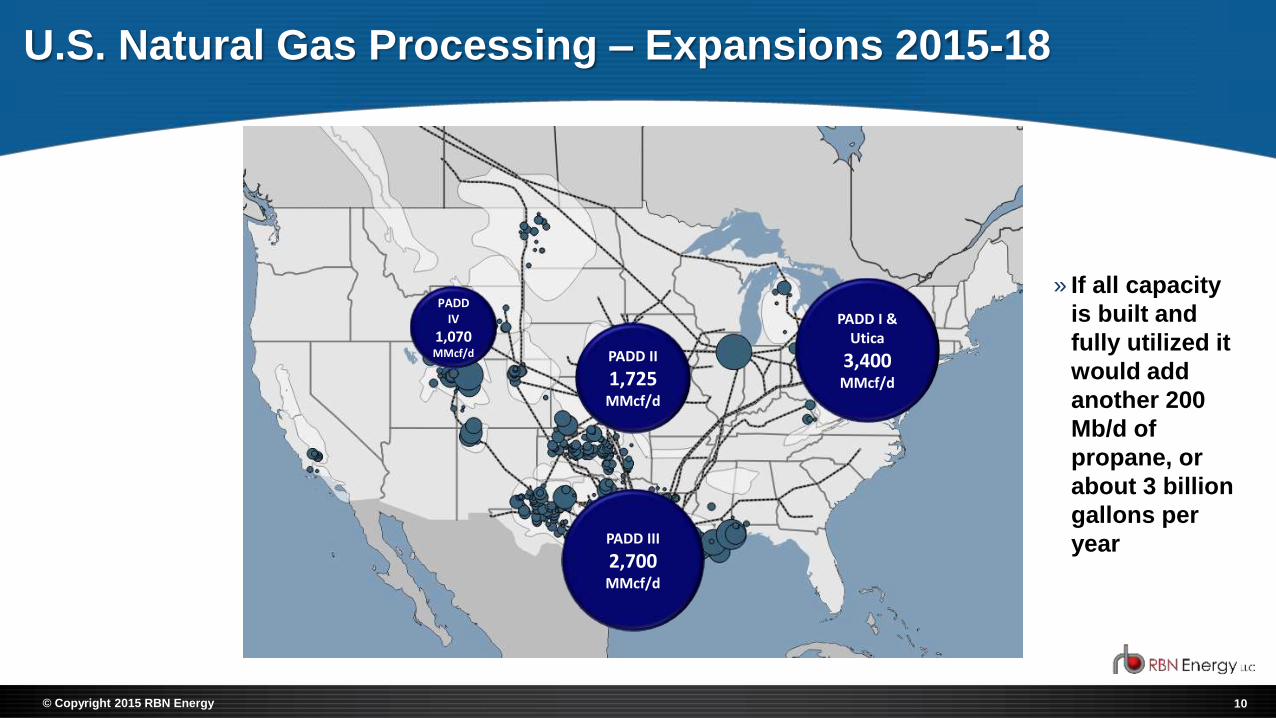

U.S. Natural Gas Processing – Expansions 2015-18

PADD I & Utica

3,400MMcf/d

PADD II

1,725MMcf/d

PADD IV

1,070MMcf/d

PADD III

2,700MMcf/d

» If all capacity

is built and

fully utilized it

would add

another 200

Mb/d of

propane, or

about 3 billion

gallons per

year

11© Copyright 2015 RBN Energy

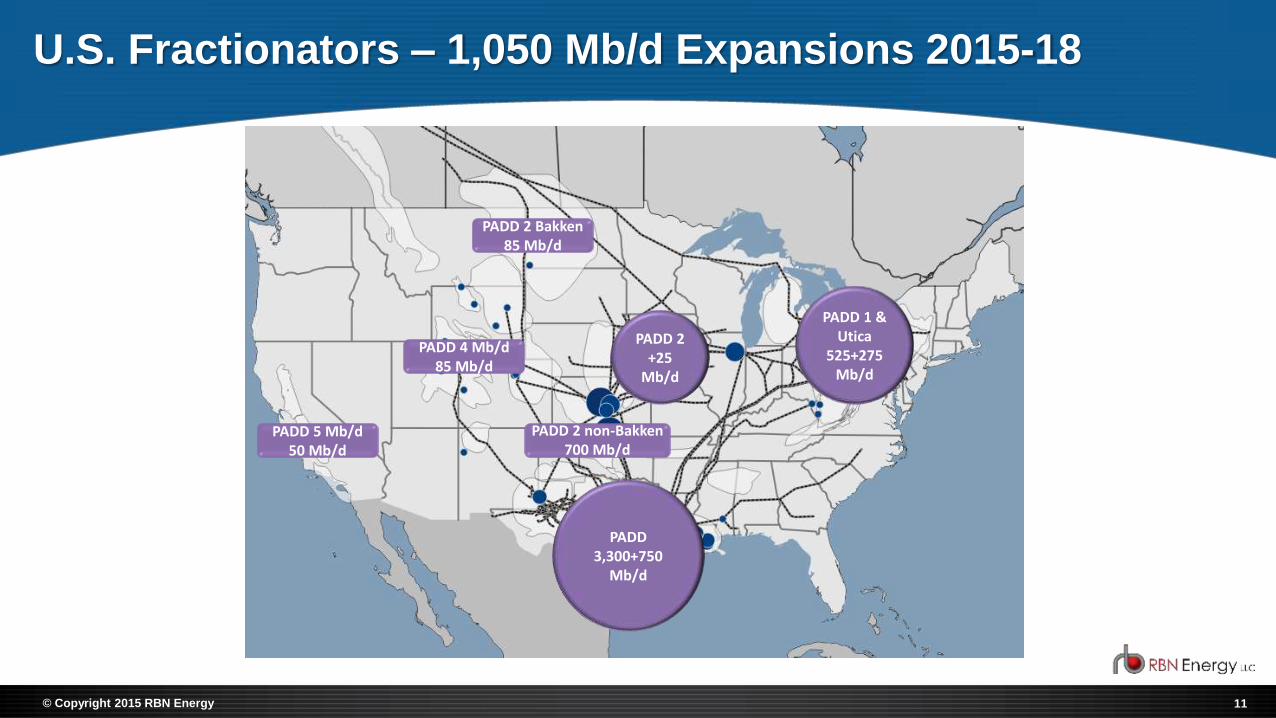

U.S. Fractionators – 1,050 Mb/d Expansions 2015-18

PADD 2 +25

Mb/d

PADD 3,300+750

Mb/d

PADD 1 & Utica

525+275Mb/d

PADD 2 Bakken 85 Mb/d

PADD 2 non-Bakken 700 Mb/d

PADD 4 Mb/d85 Mb/d

PADD 5 Mb/d50 Mb/d

12© Copyright 2015 RBN Energy

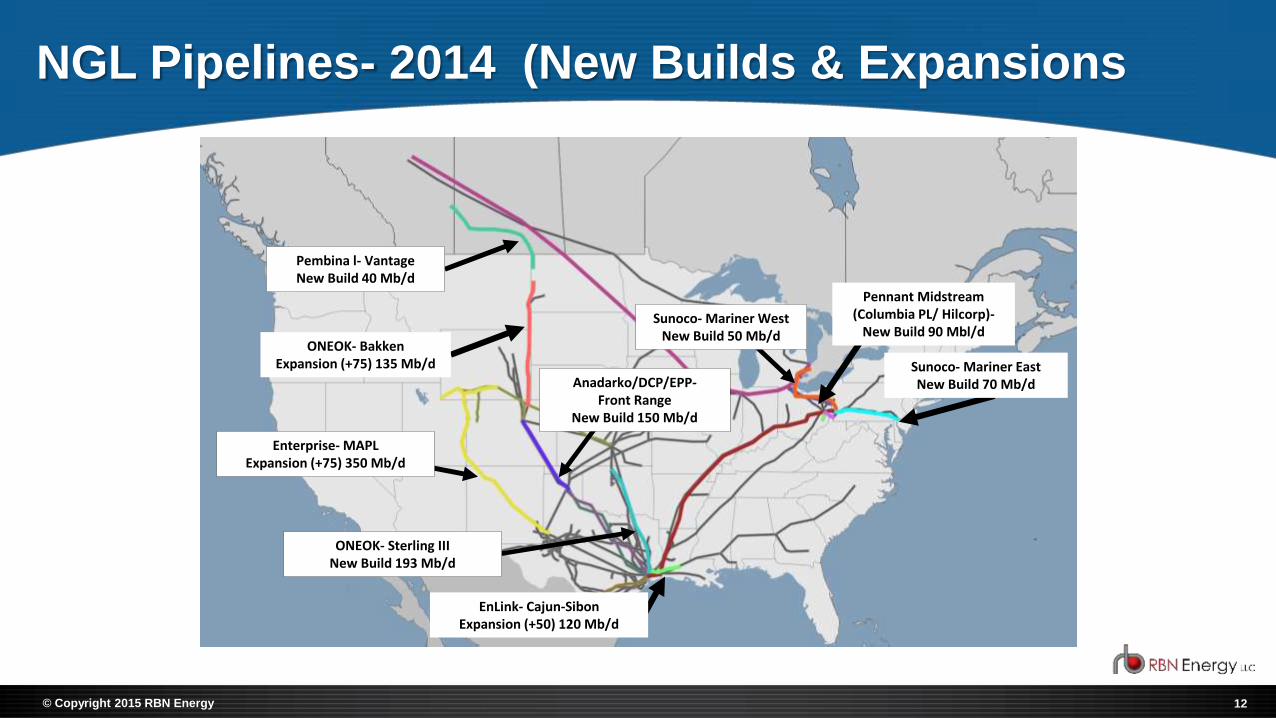

NGL Pipelines- 2014 (New Builds & Expansions

ONEOK- BakkenExpansion (+75) 135 Mb/d Sunoco- Mariner East

New Build 70 Mb/d

Pennant Midstream (Columbia PL/ Hilcorp)-

New Build 90 Mbl/d

EnLink- Cajun-SibonExpansion (+50) 120 Mb/d

Pembina l- VantageNew Build 40 Mb/d

Enterprise- MAPLExpansion (+75) 350 Mb/d

Anadarko/DCP/EPP-Front Range

New Build 150 Mb/d

ONEOK- Sterling IIINew Build 193 Mb/d

Sunoco- Mariner WestNew Build 50 Mb/d

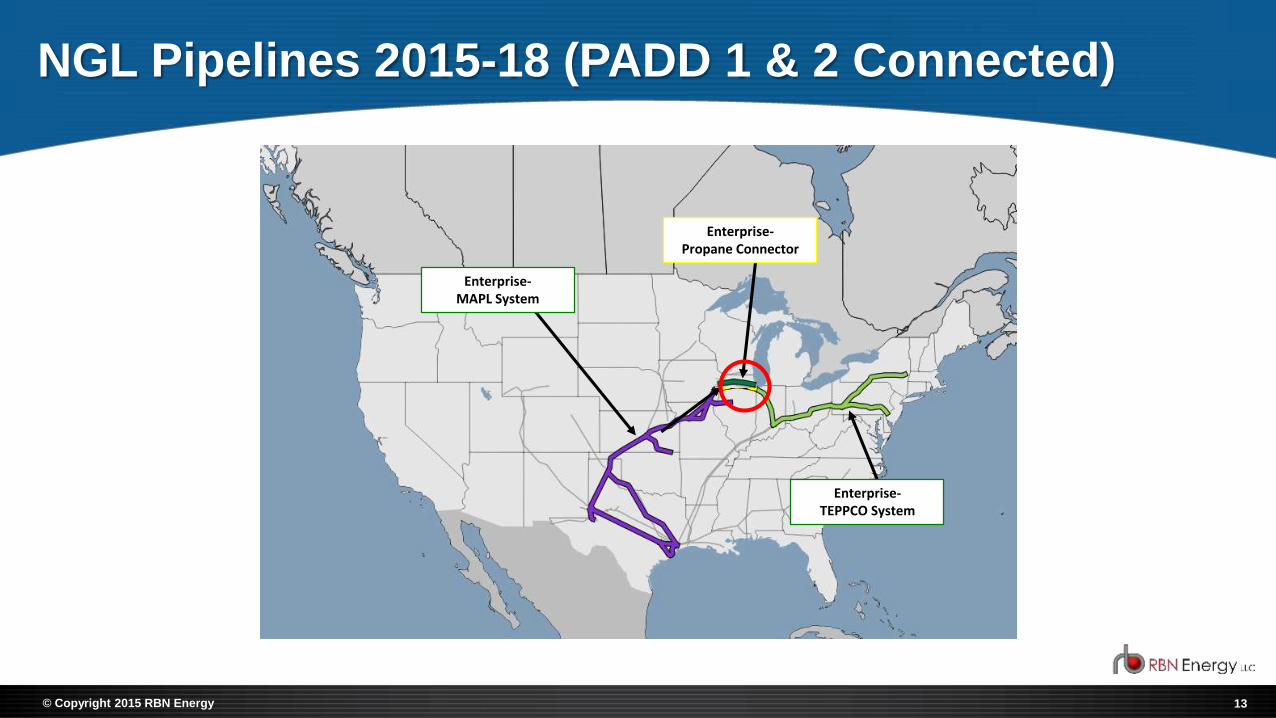

13© Copyright 2015 RBN Energy

Enterprise-MAPL System

Enterprise-TEPPCO System

Enterprise-Propane Connector

NGL Pipelines 2015-18 (PADD 1 & 2 Connected)

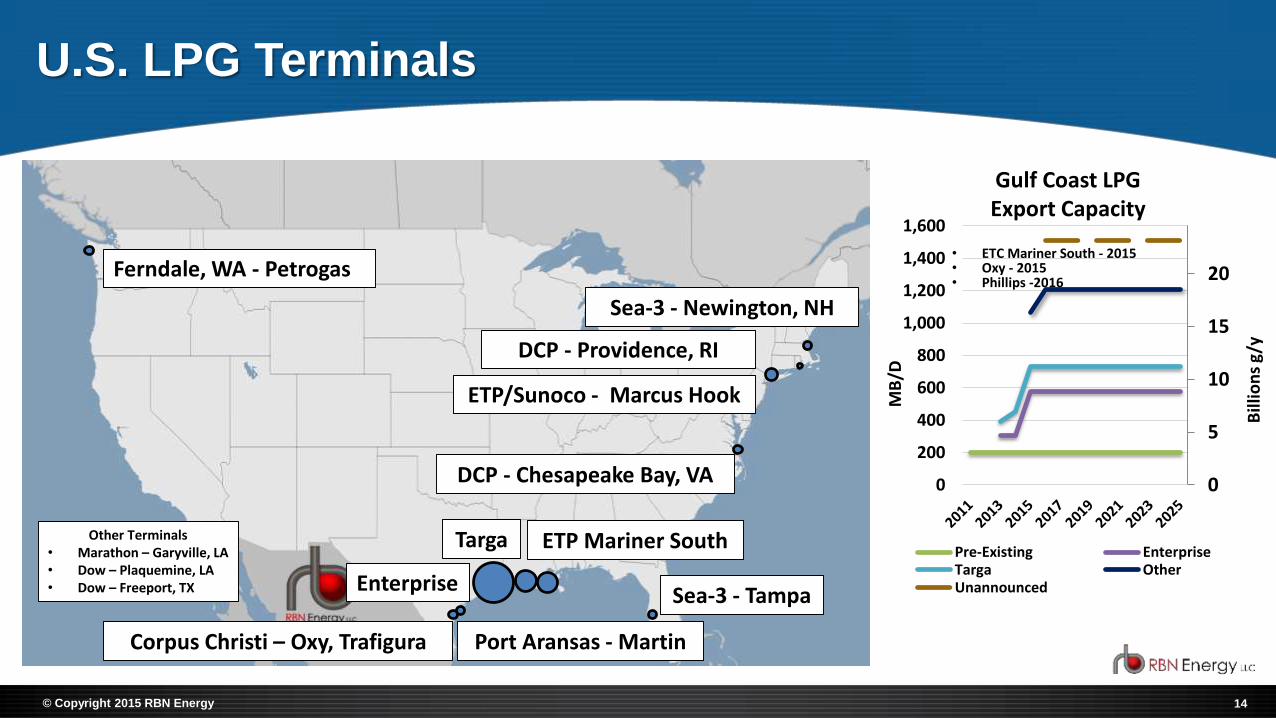

14© Copyright 2015 RBN Energy

U.S. LPG Terminals

Ferndale, WA - Petrogas

Enterprise

Corpus Christi – Oxy, Trafigura Port Aransas - Martin

Sea-3 - Newington, NH

DCP - Providence, RI

DCP - Chesapeake Bay, VA

ETP/Sunoco - Marcus Hook

Sea-3 - Tampa

Other Terminals• Marathon – Garyville, LA• Dow – Plaquemine, LA• Dow – Freeport, TX

Targa

0

5

10

15

20

0

200

400

600

800

1,000

1,200

1,400

1,600

Bill

ion

s g/

y

MB

/D

Pre-Existing EnterpriseTarga OtherUnannounced

Gulf Coast LPG Export Capacity

• ETC Mariner South - 2015• Oxy - 2015• Phillips -2016

ETP Mariner South

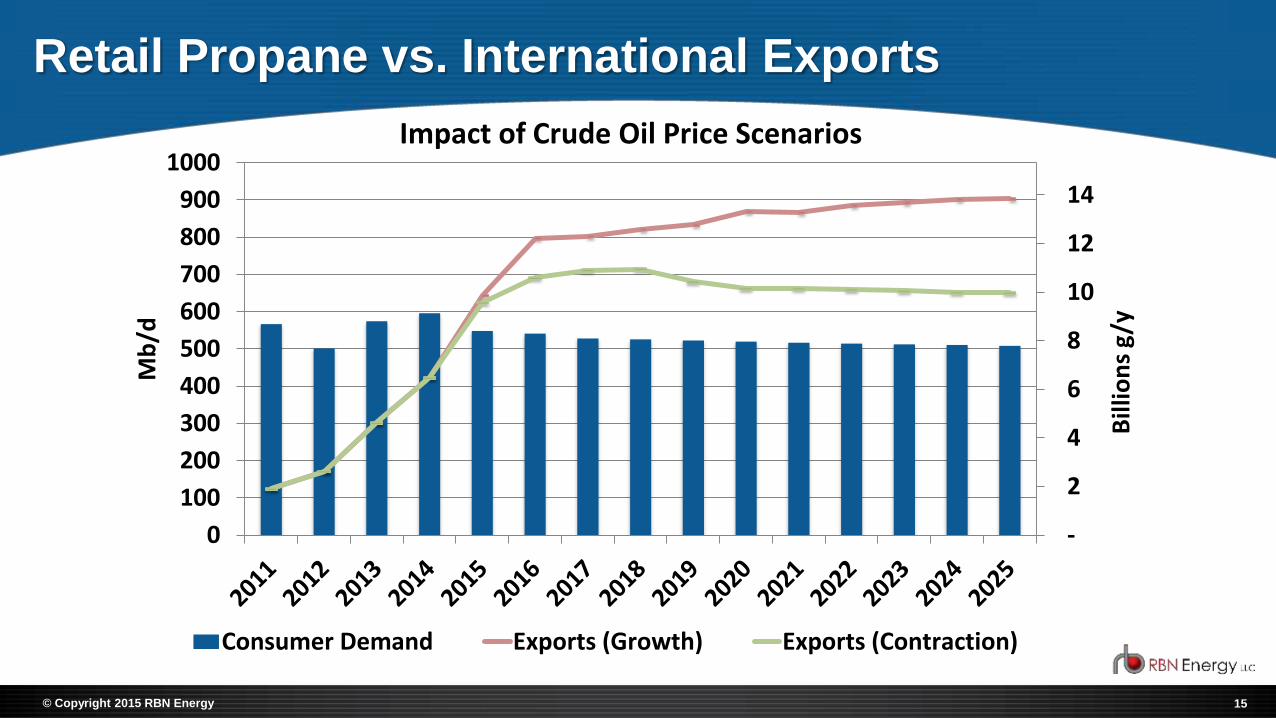

15© Copyright 2015 RBN Energy

Retail Propane vs. International Exports

-

2

4

6

8

10

12

14

0

100

200

300

400

500

600

700

800

900

1000

Bill

ion

s g

/y

Mb

/d

Consumer Demand Exports (Growth) Exports (Contraction)

Impact of Crude Oil Price Scenarios

16© Copyright 2015 RBN Energy

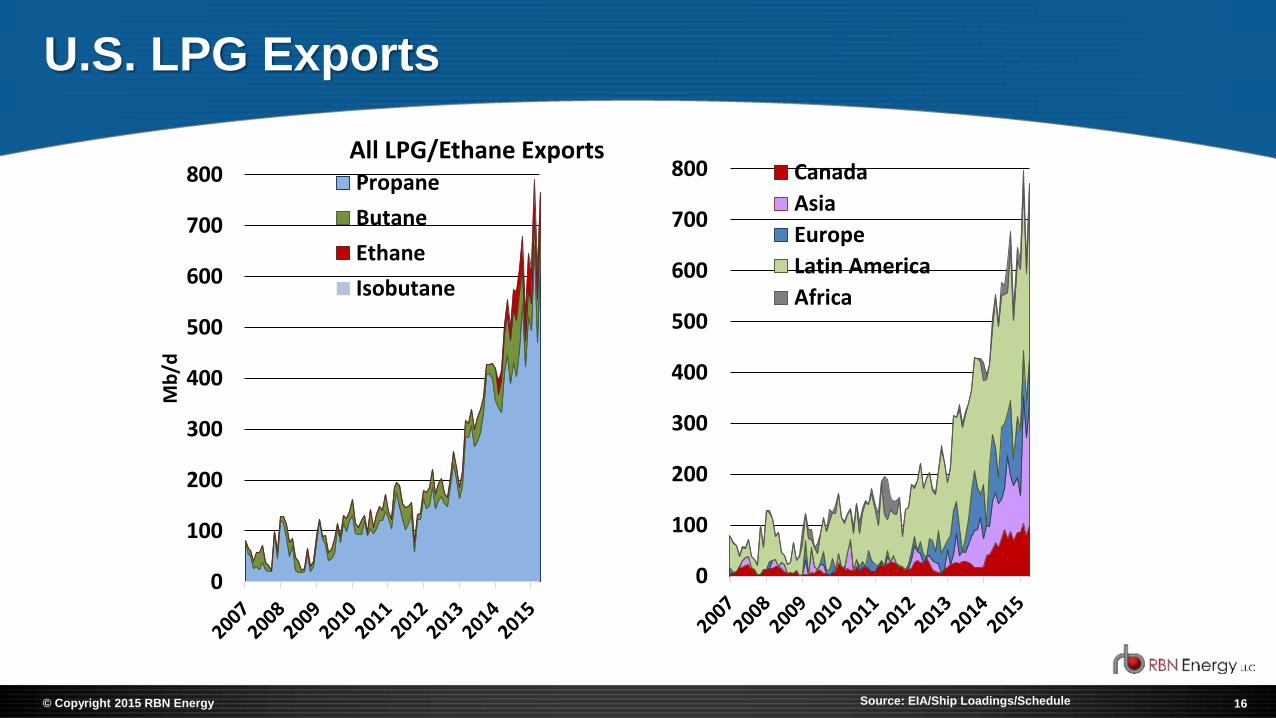

U.S. LPG Exports

0

100

200

300

400

500

600

700

800M

b/d

Propane

Butane

Ethane

Isobutane

0

100

200

300

400

500

600

700

800 Canada

Asia

Europe

Latin America

Africa

Source: EIA/Ship Loadings/Schedule

All LPG/Ethane Exports

17© Copyright 2015 RBN Energy

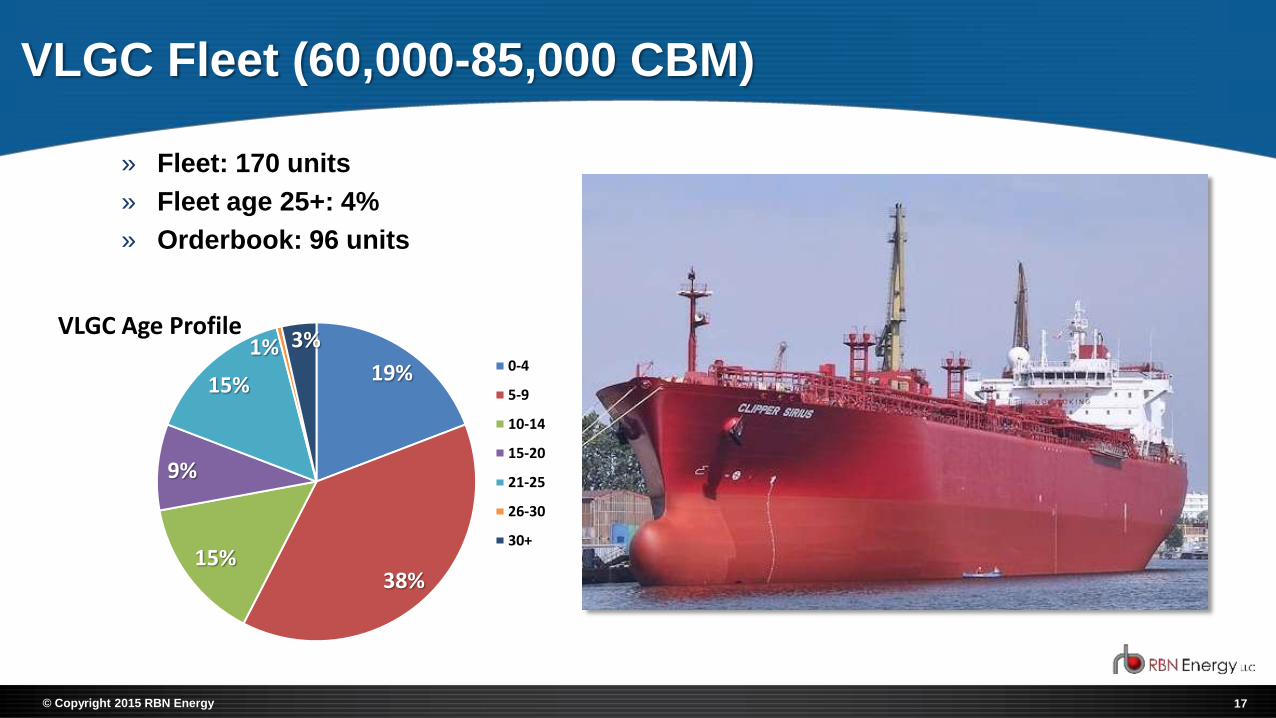

VLGC Fleet (60,000-85,000 CBM)

» Fleet: 170 units

» Fleet age 25+: 4%

» Orderbook: 96 units

19%

38%15%

9%

15%

1% 3%VLGC Age Profile

0-4

5-9

10-14

15-20

21-25

26-30

30+

18© Copyright 2015 RBN Energy

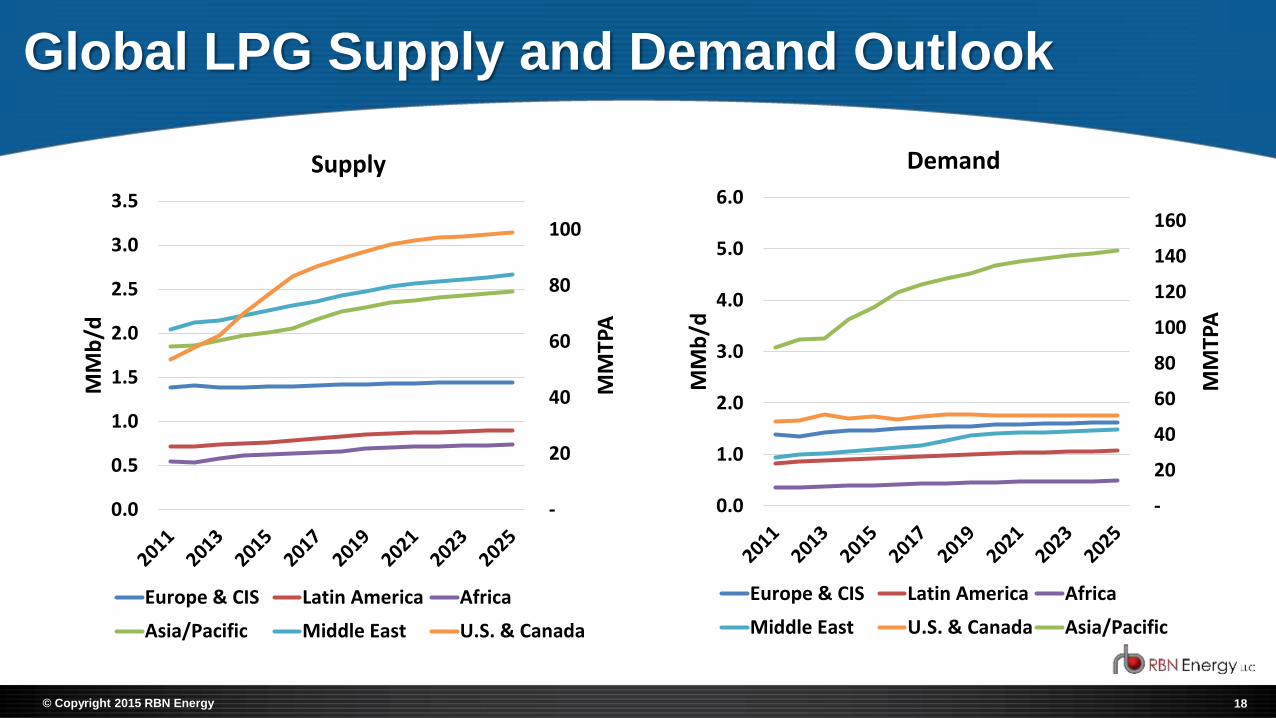

Global LPG Supply and Demand Outlook

-

20

40

60

80

100

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

MM

TPA

MM

b/d

Supply

Europe & CIS Latin America Africa

Asia/Pacific Middle East U.S. & Canada

-

20

40

60

80

100

120

140

160

0.0

1.0

2.0

3.0

4.0

5.0

6.0

MM

TPA

MM

b/d

Demand

Europe & CIS Latin America Africa

Middle East U.S. & Canada Asia/Pacific

19© Copyright 2015 RBN Energy

PADD 1

» Production growth adjacent to and within the Northeast demand

region will shift primary supply to local sources

» A higher proportion of supply will be delivered by rail

» Dixie and Teppco will continue to be important sources of

supply; Teppco volumes will be increasingly sourced from

Marcellus/Utica production

» Retailers should focus on local supplies for ratable volumes,

supplemented by seasonal purchases from pipeline, rail and

local storage

» The intermittent nature of rail deliveries will require more

planning/scheduling to avoid supply interruption

» Retailers can maximize rail flexibility through the use of trans-

flow units (mobile railcar to bobtail vehicles)

» It will be increasingly important for retailers to carefully monitor

export markets, export volumes and local production trends

20© Copyright 2015 RBN Energy

PADD 2

» Propane markets in the upper Midwest will

increasingly be supplied by Bakken and other PADD 2

production, much delivered by rail

» Retailers previously served by Cochin, or near new rail

terminals will need to plan for the more intermittent

nature of rail deliveries

» Retailers served from the MAPL and Oneok pipeline

systems can continue to rely on consistent deliveries

from those sources

» It will be increasingly important for retailers to

carefully monitor export markets, export volumes and

PADD 3 petrochemical demand

21© Copyright 2015 RBN Energy

PADD 3

» PADD 3 exports have become a huge gateway

to the global propane market

» Pricing in global markets will increasingly

impact pricing in U.S. markets, and vice versa

» Supplies to meet PADD 3 export commitments

will come from production within the PADD,

and significant receipts of PADD 2 and 4

volumes

» Additional base load demand will come from

new PDH units

» It will be increasingly important for retailers to

carefully monitor export markets, export

volumes and PADD 3 petrochemical demand

22© Copyright 2015 RBN Energy

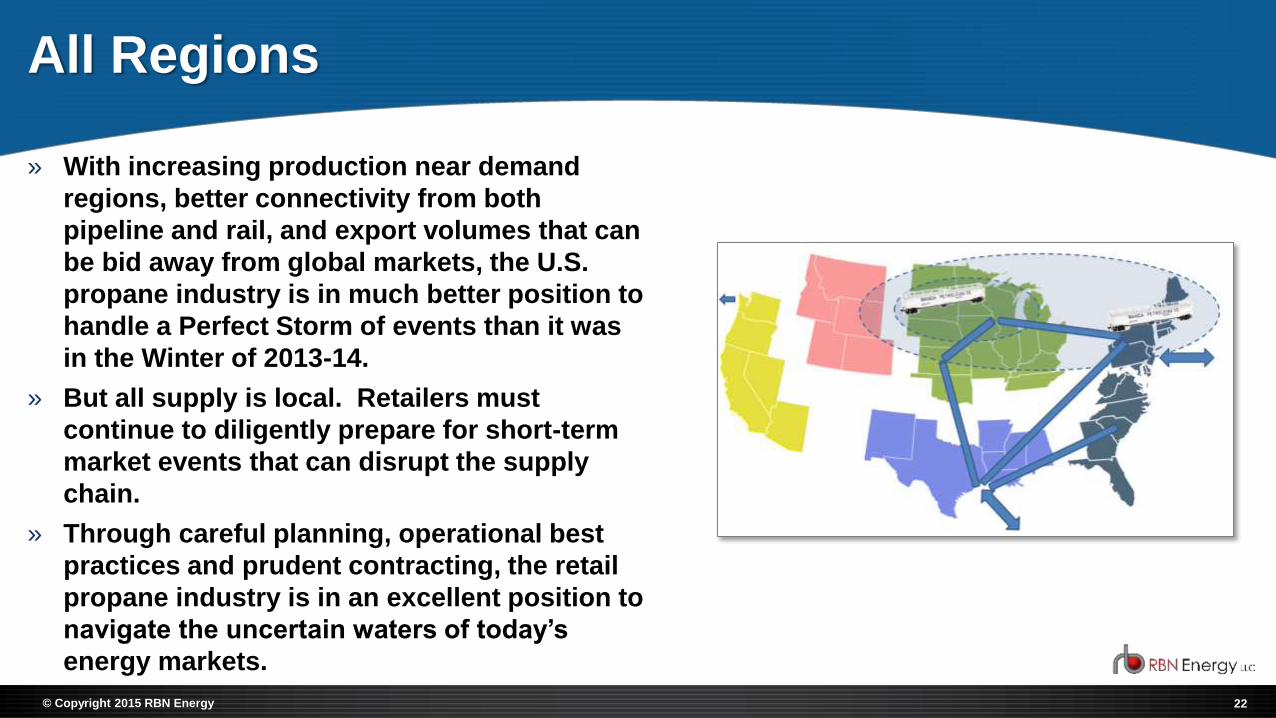

All Regions

» With increasing production near demand

regions, better connectivity from both

pipeline and rail, and export volumes that can

be bid away from global markets, the U.S.

propane industry is in much better position to

handle a Perfect Storm of events than it was

in the Winter of 2013-14.

» But all supply is local. Retailers must

continue to diligently prepare for short-term

market events that can disrupt the supply

chain.

» Through careful planning, operational best

practices and prudent contracting, the retail

propane industry is in an excellent position to

navigate the uncertain waters of today’s

energy markets.